Abstract

This article investigates “growth departments,” an increasingly popular governance structure in modern organizations. Using a multimethod approach, the authors examine the purpose, responsibilities, and effectiveness of these departments. In Studies 1a and 1b, the authors analyze job ads to understand the growth department. Study 2 expands this understanding via interviews with chief growth officers. Findings show that the growth department is a cross-functional unit distinct from marketing and sales departments, designed to unify and orchestrate growth throughout the organization. Studies 3 and 4 assess their impact on firm outcomes, drawing from boundary spanning and organizational ambidexterity theories. In startups, hiring a growth leader results in better advancement through funding rounds, a key proxy of startup growth, than hiring a marketing or sales leader (Study 3). In public firms, a powerful growth department improves performance metrics including Tobin's Q, cash flow, and return on assets (Study 4). The authors also identify contingency factors influencing the growth department's effectiveness, including the growth leader's past sales or marketing experience and the firm's strategic emphasis on exploration versus exploitation. Together, the findings advance theory and practice by clarifying what growth departments are, how they operate, and under what conditions they enhance firm performance.

Keywords

Growth is the top priority for most organizations. It is often expressed as the most pressing problem for senior executives, a decisive indicator of value to investors, and an important predictor of firm performance (Atsmon and Smit 2015; Homburg, Theel, and Hohenberg 2020; Jaworski and Lurie 2020). Decorated leaders in most industries happen to be the ones who garnered their reputation by driving successful growth (Gulati 2004; Marsh 2015), while firms with lackluster growth are destined to perish (Atsmon and Smit 2015). Despite its importance, growth is a challenging endeavor due to fierce competition in most industries, lack of a systematic approach to growth, and implementation roadblocks, which leave many firms falling behind their growth targets (Jaworski and Lurie 2020). Marketing scholars have expressed growth as a research priority and called for studies that document the role of marketing in driving growth (Moorman and Day 2016), but response to such calls remains largely lacking. To compound matters, according to an IBM report (2018), most marketing and sales leaders struggle to demonstrate whether and how their activities contribute to growth.

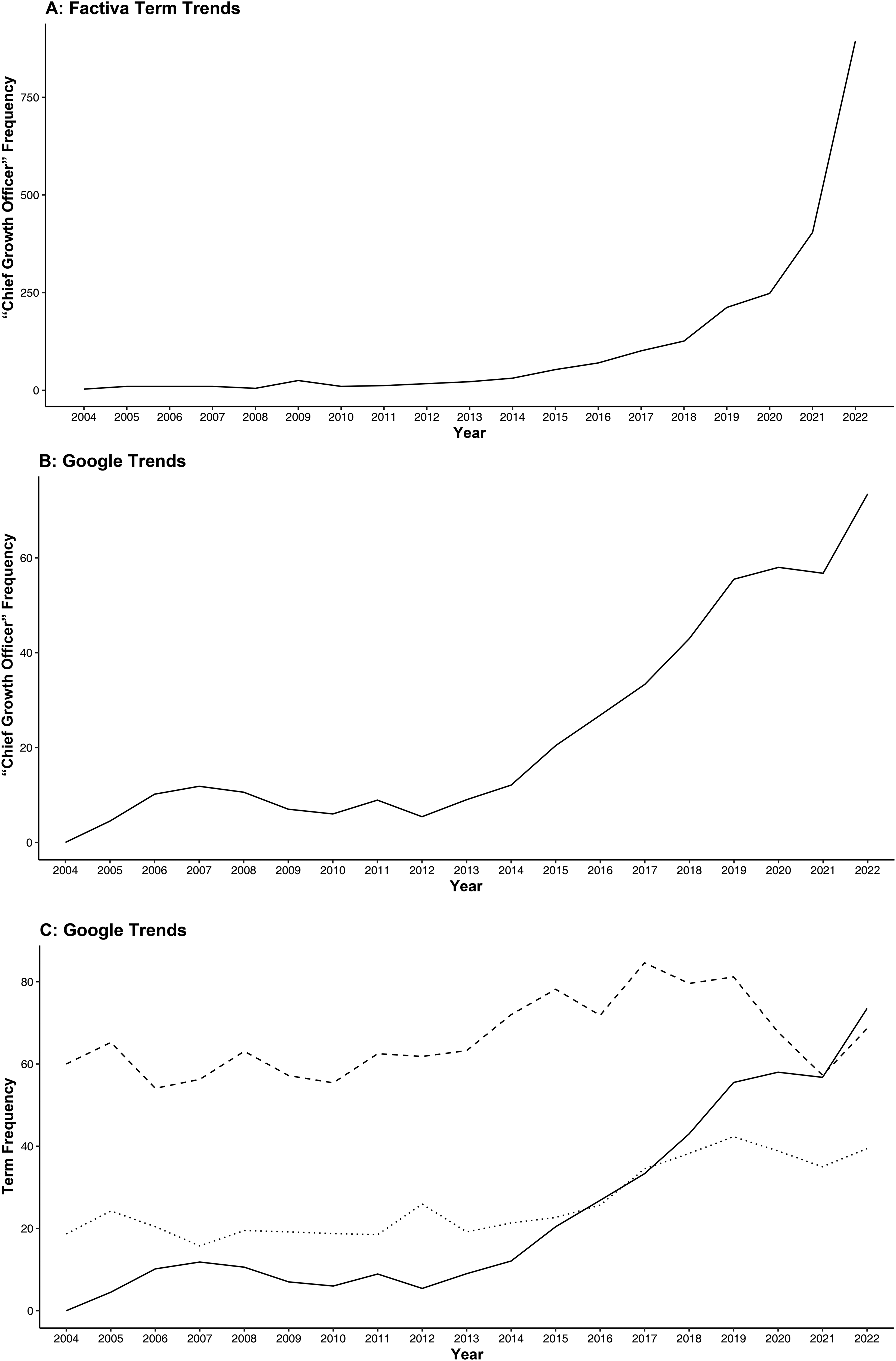

While growth has arguably been one of the main concerns of business leaders for many decades, a novel trend to address this challenge has emerged across numerous industries and is gaining increasing popularity: a whole new department solely focused on growth (Hall 2019; O’Neill 2021). The growth department includes job titles that run the gamut of the corporate ladder, ranging from growth specialists, growth analysts, and growth hackers to head of growth, vice president (VP) of growth, and chief growth officer (CGO) (Bussgang and Benbarak 2016; Holiday 2014). A cursory search of Google Trends or Factiva attests to the mounting popularity of these positions in recent years (Figure 1). According to an industry survey, 14% of firms in the United States have CGOs, 29% have a VP, director, or head of growth, and 41% have a growth manager (Singular 2019).

Rising Popularity of the Term “Chief Growth Officer.”

Despite the growing interest, academic research on the topic is lagging, and only anecdotal evidence across practitioner-oriented journals or blogs sheds some light on what growth positions may entail. However, even this evidence is speculative and fails to create a comprehensive picture of the growth department. For instance, while some practitioners posit that the growth department is a hybrid of sales and marketing with a cross-functional role across product, sales, and marketing departments (Hall 2019), others maintain that it is a replacement or extension of marketing (O’Neill 2021), and some throw operations in the mix with marketing and sales (Andrews 2015) or call a host of digital marketing strategies “growth hacking” (Holiday 2014). Moreover, many leaders report difficulties in deciding whether creating a growth department would be beneficial for their firm, whom to hire for this department, and how to align it with and distinguish it from related functions, such as marketing or sales (Hall 2019).

In this article, we address this knowledge gap by answering the following questions: RQ1, the nature of the growth department: What does it do and what tasks and responsibilities does it undertake? and RQ2, the impact of the growth department: How effective is the growth department in improving firm performance and what factors moderate this impact?

We investigate these questions using an exploratory, “empirics-first” approach (Golder et al. 2023). In Studies 1a, 1b, and 2, we investigate the nature of the growth department using insights from text mining of 523 growth job ads at various levels of the corporate ladder (Study 1a), comparison of C-level growth job ads with C-level marketing and sales job ads (Study 1b), and interviews with CGOs (Study 2). Our results indicate that the growth department is a horizontal unit, distinct from both marketing and sales departments, created to unify growth initiatives across the organization. Initial insights from text mining of job ads (Study 1a) reveal themes such as data-driven decision-making, cross-functional strategizing, optimizing marketing channels, and sales and customer relationship management, while comparison of C-suite job ads across functions (Study 1b) corroborates the distinctiveness of growth from sales and marketing.

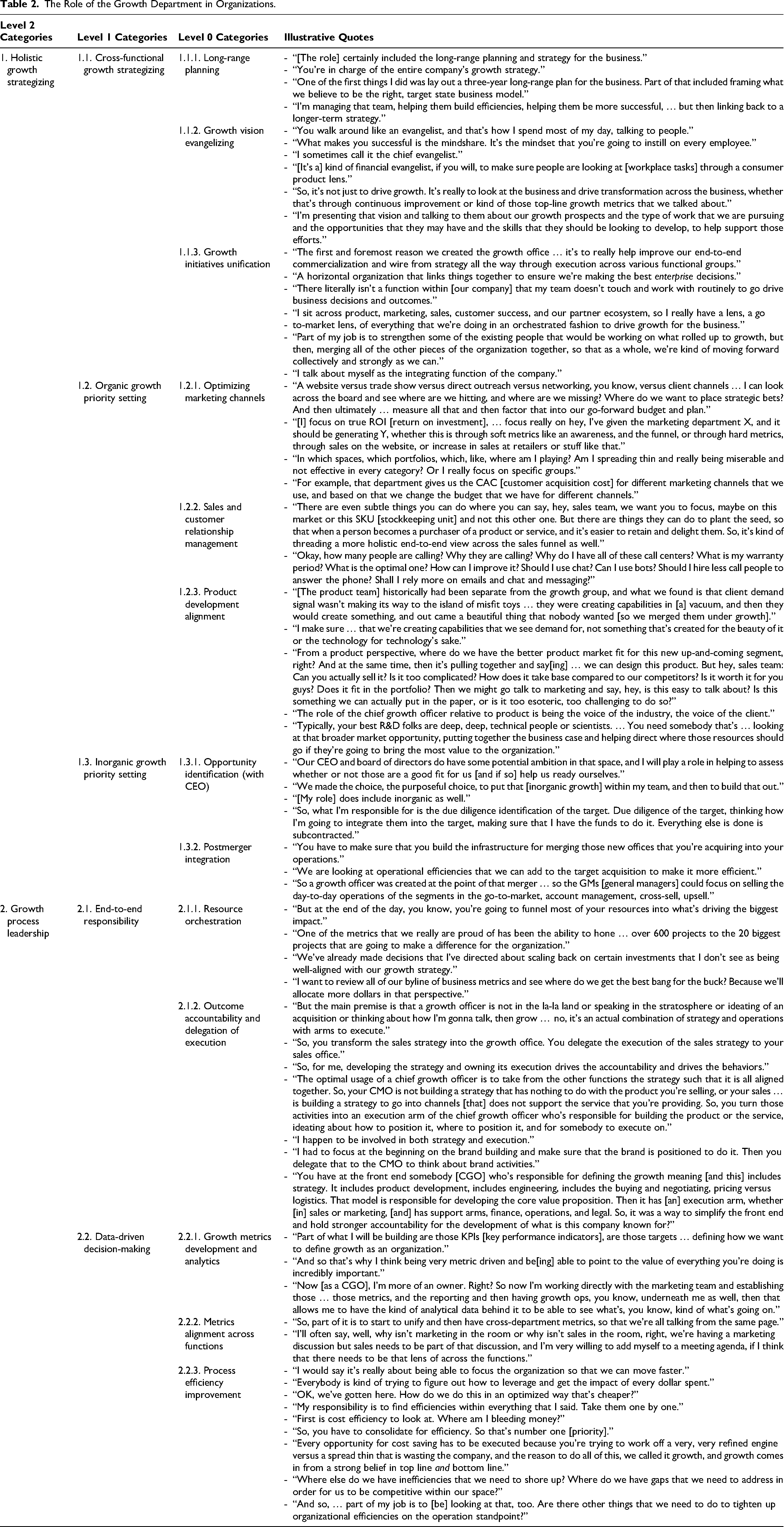

In-depth interviews with 20 CGOs (Study 2) reveal that the growth department is cross-functional in nature, created to own and lead organization-wide growth. It does so by holistic growth strategizing and growth process leadership. Holistic growth strategizing involves (1) cross-functional growth strategizing through activities such as long-range growth planning, evangelizing the growth vision throughout the organization, and unification of growth initiatives across various functions, (2) organic growth priority setting through working closely with marketing to optimize marketing channels, working closely with sales and customer relationship management, and aligning product development efforts, and (3) inorganic growth priority setting through partnering with the CEO on opportunity identification and postmerger integration of the acquired businesses. The growth department does not stop at strategizing and leads growth implementation by (1) assuming end-to-end responsibility via orchestrating resources around high-impact initiatives, outcome accountability, and delegation of execution to relevant departments, and (2) engaging in data-driven decision-making through developing growth metrics, aligning metrics across functions, and having a strong emphasis on improving process efficiency.

Insights from interviews and job ads are closely connected to ideas laid out by two organization theories, the boundary spanning theory and the organizational ambidexterity theory, which we draw from to hypothesize on the impact of the growth department. Our findings from the first three studies reveal that growth departments combine two important mechanisms that have a crucial impact on firm performance: coordination (boundary spanning theory) and balance (ambidexterity theory). The growth department's cross-functional approach to growth spans functional boundaries and improves coordination across silos, while its holistic approach integrates and balances competing demands of exploration (innovation and expansion) and exploitation (efficiency and betterment of existing processes).

In the next two studies, we explore the impact that growth departments have on firm outcomes, in both startups (Study 3) and public firms (Study 4). In Study 3, we find that startups that hire a growth leader obtain significantly more funding rounds than those that hire a marketing or a sales leader in the same year. In Study 4, we turn to public firms and find that growth departments contribute to higher firm value, measured by Tobin's Q, and lead to improved return on assets (ROA) and cash flow. Furthermore, we find that firms with a cost-leadership strategy benefit more from growth departments, while the impact of the growth department is hampered in innovation-intensive firms. These findings highlight that improving exploration efforts in firms that have already mastered exploitation may be easier than vice versa, particularly through the growth department's disciplined approach to innovation. In contrast, improving exploitation in innovation-intensive firms, which often focus extensive resources on research and development (R&D) and have a higher tolerance for uncertain results, is at odds with the growth department's focus on coordination of efforts across departments and allocating resources to the most proven initiatives.

Our primary contribution is substantive in nature: the detailed investigation of the growth department, an emerging, yet unexplored phenomenon. Through extensive analyses, we document its purpose, responsibilities across organizational levels, employee backgrounds, and distinction from marketing and sales. Our study offers a comprehensive synthesis of what a growth department is and its key functions, providing valuable insights for practitioners seeking governance structures for their growth activities. Additionally, we highlight the benefits of growth departments for startups and public firms, exploring factors that influence their effectiveness. These findings guide firms in determining when a growth department is beneficial, how to design it, and how to identify the ideal candidate profiles to maximize outcomes.

Moreover, we contribute to (1) the marketing strategy literature, which identifies growth as a research priority but lacks a comprehensive study on the topic, (2) research on how firms achieve superior results (e.g., market orientation, marketing doctrine, marketing excellence) by introducing a novel approach grounded in a clear organizational structure, (3) boundary spanning and organizational ambidexterity theories by integrating the two and highlighting nuances in their application for firms emphasizing exploration or exploitation, and (4) the literature on marketing department power, which often aggregates various departments and relies on upper echelons theory, by emphasizing the need to study individual departments, their relationships with other functions, and their responsibilities across all organizational levels.

Theoretical Background

Despite the importance of growth for firm performance and survival, the question of how organizations internally structure and coordinate efforts to achieve growth has received meager attention. Frameworks like the Ansoff Matrix have traditionally provided a foundation for understanding growth strategies (Carman and Langeard 1980; Kotler and Keller 2014). Economists have also explored growth through game-theoretic or empirical models, examining issues such as the probability distribution of corporate growth rates or the impact of strategies such as innovation on growth (Bottazzi and Secchi 2006; Demirgüç-Kunt and Maksimovic 1998). However, research on organizational structures that support growth remains limited, with existing studies examining the effects of factors such as centralization or mechanistic versus organic structures on growth (Fombrun and Wally 1989; Raisch 2008). Consequently, scant research addresses critical questions such as how diverse growth initiatives are integrated across the organization or which departments are responsible for driving these efforts.

Growth and the Role of the Marketing Department in Organizations

Marketing scholars have emphasized the importance of studying growth and the role of the marketing department in driving it, identifying this as a critical research priority (Moorman and Day 2016). Despite such calls, there is little research on how firms approach growth or how marketing contributes to it. Industry reports further highlight a disconnect, showing that marketing departments are often uninvolved in setting growth strategies and struggle to demonstrate how their activities contribute to growth (IBM 2018; Whitler 2016).

These reports are notable since the multidimensional nature of growth, spanning product development, promotion channels, sales, customer success, and more, makes marketing a natural candidate for leading (at least organic) growth initiatives, given its ascribed oversight of the four Ps (i.e., product, price, promotion, and place; Kotler and Keller 2014). However, scholars have recently noted that although marketing roles and activities remain central in firms, many of them are not always housed within the marketing department (McAlister et al. 2023). For example, in many industries, products are managed by a separate department and often represented in the C-suite by the chief product officer (Sheanoy 2023). Similarly, pricing may fall under finance, operations, analytics, or a dedicated pricing team (Homburg, Jensen, and Hahn 2012). Even within promotion, sales is typically a distinct function (Biemans, Malshe, and Johnson 2022). 1

Despite such heterogeneity, marketing scholars have often lumped together these departments and functions under the label “marketing department,” clouding the distinction between marketing-related activities and marketing departments and leaving out important questions about how these departments work with each other and how firms in practice synergize and coordinate efforts across these departments. For instance, researchers studying the influence of the marketing department’s power on firm outcomes have often included sales, product, or even growth departments in the calculation of marketing department power, limiting our understanding of how these departments interact and contribute to shared organizational goals (Nath and Mahajan 2008; Varma, Bommaraju, and Singh 2023). Moreover, this literature often focuses on upper echelons theory and the strategic role of chief marketing officers (CMOs), which offers limited insight into what a given department does at all levels of the organizational hierarchy. This leaves open important questions around the ownership and coordination of growth-related initiatives.

The literature on the sales–marketing interface has addressed some of these coordination challenges, especially those stemming from misaligned goals, communication gaps, and trust issues between sales and marketing (Homburg and Jensen 2007). Studies have explored different structural configurations of this interface and their impact on firm outcomes (Biemans, Malshe, and Johnson 2022; Homburg and Jensen 2007). Scholars have also examined marketing's interactions with other departments, including finance, logistics, engineering, human resources, and purchasing, highlighting the importance of alignment between marketing and these functions (for a comprehensive review, see Hughes, Le Bon, and Malshe [2012]). However, this body of work has overlooked the broader fragmentation of marketing activities across multiple departments and the resulting challenges in coordinating these dispersed functions (Biemans, Malshe, and Johnson 2022).

Overall, addressing the question of who owns growth and how disparate functions are coordinated remains critical to advancing our understanding of organizational growth. Beyond improving individual interdepartmental relationships, such as between sales and marketing, scholars need to explore the broader fragmentation of growth-related initiatives across various organizational silos and ways to improve their collective contribution to shared growth goals.

Boundary Spanning Theory and Organizational Ambidexterity Theory

In studying how firms organize internally to achieve superior performance, two management theories, the boundary spanning theory and the organizational ambidexterity theory, stand out. These two theories provide the most relevant foundations for understanding the insights from Studies 1a, 1b, and 2, which explore the nature of the growth department, and we subsequently draw from them to hypothesize on the impact of the growth department.

Boundary spanning theory

Boundary spanning refers to the ability of individuals and teams to cross organizational boundaries and collaborate across functional, departmental, or knowledge-based divisions (Ancona 1990; Marrone 2010; Schotter et al. 2017). 2 Research shows that firms excelling at bridging silos and fostering interdepartmental collaboration can leverage this capability as a competitive advantage, achieving collective success beyond the immediate goals of individual departments (Levina and Vaast 2005; Marrone 2010). Given that growth requires coordination across multiple departments and is a multidimensional goal that goes beyond individual unit goals, this theory provides a germane foundation for our research. One notable study shows that the effectiveness of boundary spanning is associated with the emergence of “a new joint field” that unites all fields in their pursuit of a common organizational interest (Levina and Vaast 2005). Actors within this new field use organizational resources along with the influence that comes with the boundary-spanning role to help move the organization toward the broader goal (Levina and Vaast 2005). Although these researchers derive their implications from case studies, the concept of a new joint field is very close to the growth department as a cross-functional entity created to unify growth initiatives across the firm. Our multimethod investigation adds to this literature, which is predominantly conceptual or case-based (Schotter et al. 2017), and we combine this stream with the organizational ambidexterity research to generate novel nuances in achieving growth.

Organizational ambidexterity theory

A central tension in an enterprise's progress is managing the internal balance between exploration and exploitation (O’Reilly and Tushman 2013). Exploration involves innovation, risk-taking, and pursuing new opportunities, while exploitation focuses on efficiency, refinement, and optimizing existing processes (Campbell, Short, and Graffin 2025). These two are inherently incongruent: Exploration is inefficient and risky due to the uncertainty of developing untested products or entering unproven markets, whereas exploitation prioritizes efficiency, often at the expense of innovation (O’Reilly and Tushman 2013). Organizational ambidexterity, or the ability to balance these competing demands by creating structures and management systems that internally support and balance the pursuit of both innovation and efficiency, is crucial for firm survival (Smith and Lewis 2011).

Firms may achieve ambidexterity through sequential adjustments (sequential ambidexterity) or by having individuals alternate between exploration and exploitation within the same unit (contextual ambidexterity). However, structural ambidexterity, where separate subunits are dedicated to each activity, is often viewed as the most practical approach (O’Reilly and Tushman 2013). Case studies, such as those on IBM, show that for structural ambidexterity to succeed, firms require a common strategic vision and targeted integration via linking mechanisms between subunits (O’Reilly, Harreld, and Tushman 2009). Moreover, ambidexterity can potentially contribute to growth, given its balanced attention to both innovation and efficiency (Raisch 2008). While ambidexterity has demonstrated clear benefits, the literature often lacks specific guidance on how firms can implement it effectively. We address this gap by introducing the growth department as a governance mechanism for achieving structural ambidexterity and use this theory to guide our selection of moderators.

Overview of Studies

Table 1 summarizes our studies. We begin by exploring the role of the growth department by analyzing growth job ads (Studies 1a and 1b) and interviews with CGOs (Study 2). We focus on startups in Study 3, comparing the impact of growth leaders with the impact of sales and marketing leaders on obtaining funding. In Study 4, we examine the impact of growth departments on public firms and the moderating roles of firm strategies.

Overview of Studies.

Studies 1a and 1b: The Nature of the Growth Department: Initial Insights from Job Ads

Study 1a: Responsibilities and Qualifications

To gain initial insights on what growth positions entail, we collected growth position job ads from two leading professional networking and career development platforms. Data were collected daily for a week, from June 10 to June 17, 2020. To compile the sample, we included all job ads that had the word “growth” in the job titles and were posted on these platforms, resulting in an initial sample 827 job ads. After eliminating job ads that included the word “growth” but were unrelated to our research questions, such as obvious marketing or sales positions (e.g., growth marketer) or a job with a “high-growth opportunity,” we obtained our effective sample of 523 job ads, representing a diverse set of industries. We employed topic modeling to examine the content of the job ads, following a four-step process (Ningrum, Pansombut, and Ueranantasun 2020). Specifically, we extracted from each ad the job content (i.e., responsibilities and qualifications) and divided it into two corpora before applying the meaning extraction method (Chung and Pennebaker 2008). Details on data processing and the analysis are presented in Web Appendix A.

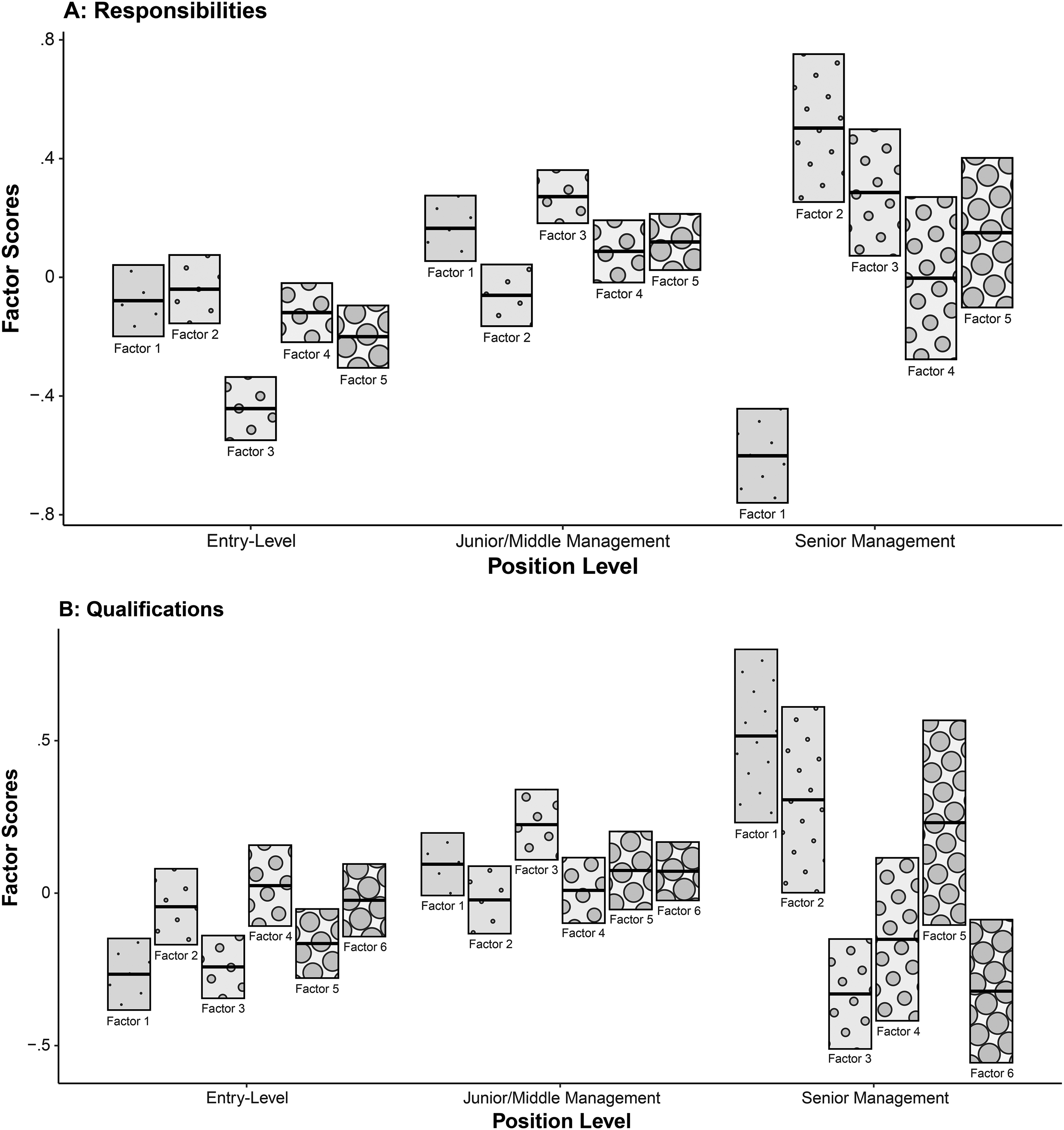

In the job responsibility corpus, through a scree plot of eigenvalues, we extracted five factors, adequately distinct as indicated by minimal cross-loadings, retaining factor loadings of ±.35 or higher (Markowitz 2022). Factor 1, which we named “Data-Driven Decision-Making,” contained keywords like “data,” “research,” “engineer,” “metrics,” “insight,” and “test”; Factor 2, “Business Leadership,” included keywords such as “plan,” “leadership,” and “position”; Factor 3, “Cross-Functional Strategizing,” included keywords such as “strategy,” “cross-functional,” “execute,” and “initiative”; Factor 4, “Optimizing Marketing Channels,” encompassed keywords such as “channel,” “optimize,” “analytical,” and “marketing”; and Factor 5, “Sales and Customer Relationship Management,” contained keywords such as “sale,” “customer,” and “relationship.”

Overall, the growth department seems to be tasked with leading the organization-wide growth effort (Factor 2), which requires developing and executing cross-functional strategies for growth initiatives (Factor 3), using research and data to work with product teams and user experience designers on identifying offerings that are more aligned with customer growth goals (Factor 1), working with the marketing team on reevaluating and optimizing marketing and customer acquisition efforts across various channels (Factor 4), and working with sales to ensure that customer strategies are in line with growth goals (Factor 5). Thus, the growth department is created to (1) lead the organization's growth by (2) using data to (3) formulate growth strategies and (4) work cross-functionally to ensure that these strategies are executed across marketing, sales, product, and other departments.

In addition to the analysis of the job responsibilities, we also analyzed the qualifications corpus of job ads to understand preferred qualities that the candidates bring to the table to be considered a good fit for a growth position (detailed results are in Web Appendix A). Besides common themes such as degree or track record, we identified a sales leadership requirement (Factor 1), a marketing experience requirement (Factor 3), and analytical abilities (Factor 6). To expand on these insights, we explored how the different factors identified in the job requirements and qualifications vary in importance across different organizational levels. To do so, we first allocated each position to one of the three categories: (1) entry-level (e.g., growth analyst, growth specialist; 200 responsibilities, 184 qualifications), (2) junior or middle management (e.g., head, manager, director of growth; 274 responsibilities, 266 qualifications), and (3) senior management (e.g., VP, senior and executive VP, president, CGO; 49 responsibilities, 46 qualifications). Next, we grouped job ads by position level and calculated the mean factor score per level to see how factors vary by position level. The results are displayed in Figure 2.

The Relative Importance of Different Factors Across Position Levels for Responsibilities and Qualifications.

Several insights arise from Figure 2. For instance, growth leaders seem to be the users of the analytics reports and research carried out by their mid- or junior-level growth employees, since the words associated with the analytics element of the growth job (Factor 1) in the responsibilities section of job ads have a significantly higher occurrence at junior or mid-level growth positions than at the leadership level (Level 3). Moreover, cross-functional strategizing is more relevant at mid- to higher-level positions. The marketing- and sales-related factors (Factors 4 and 5) seem to be roughly equivalent, with marketing having a slightly higher presence at the junior level and sales being slightly higher in importance at the senior level. Among qualifications, past sales leadership experience is more emphasized at the leadership level, while past marketing experience is slightly more valued for mid-level positions.

Study 1b: Is Growth a New Name for Marketing or Sales Positions?

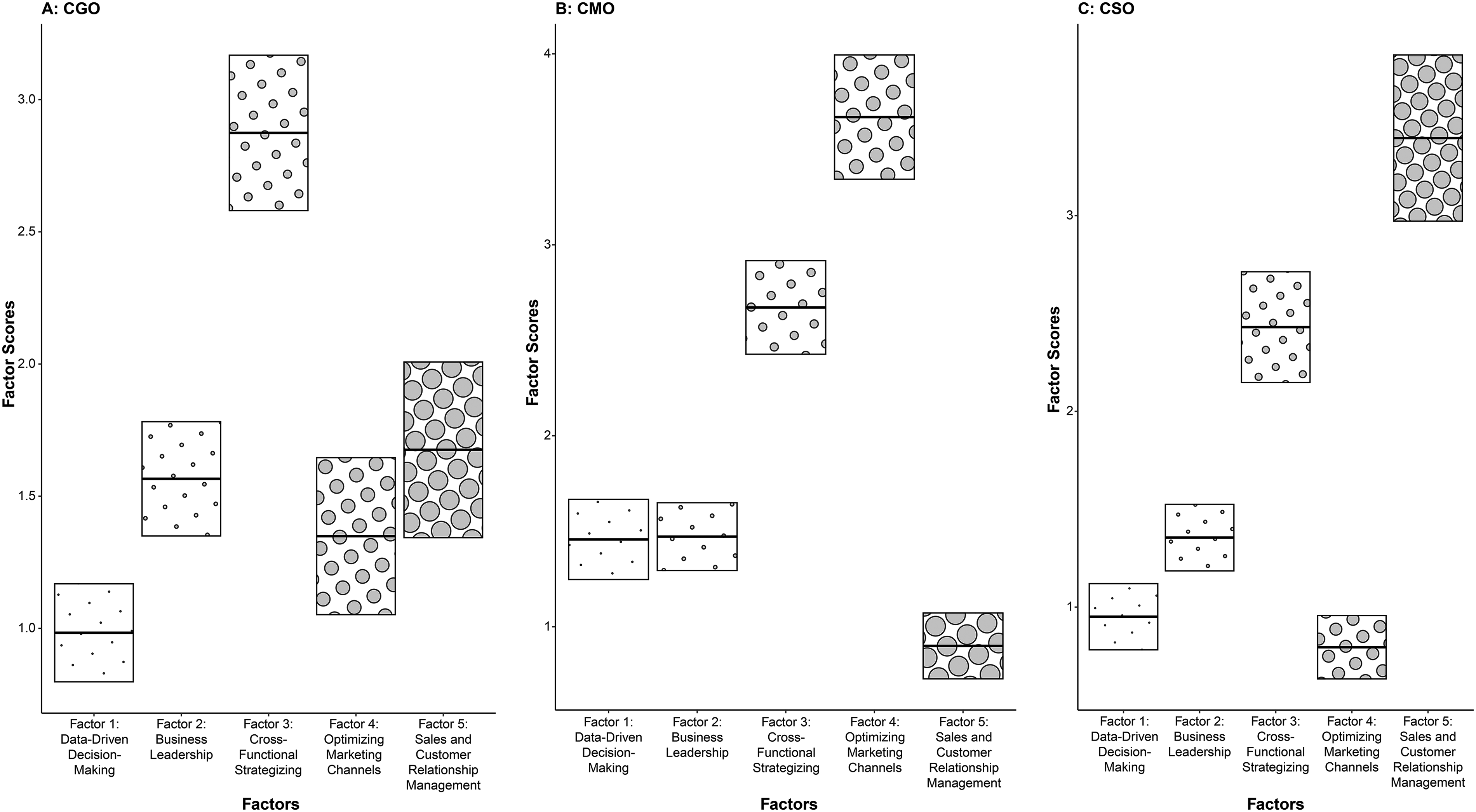

In this study, we examine whether the growth department differs from marketing and sales. To compare, we focused on the highest-level positions across these functions: CGOs, CMOs, and chief sales officers (CSOs). We used all 16 CGO job ads from Study 1a, collected 84 additional CGO ads, and added 100 new CMO and 100 new CSO ads for a total of 300 job ads (100 per category). Data were collected roughly within a ten-day window, with collection periods varying slightly by category, depending on posting volume. Our sample includes all available postings during that period from a broad range of sectors including services, industrial goods, consumer goods, and retail, with a roughly equivalent distribution across the categories. From the job ads’ responsibility sections, we created the Study 1b corpus. Using the five factors from Study 1a, we developed dictionaries based on words with loadings above ±.35 and applied them to the Study 1b datasets using the LIWC (Linguistic Inquiry and Word Count) program (Tausczik and Pennebaker 2010). The results, plotted in Figure 3, show how each position emphasizes each factor differently. Expectedly, the marketing factor (Factor 4) dominated CMO ads, and the sales factor (Factor 5) dominated CSO ads. For CGOs, cross-functional strategizing (Factor 3) was the top-ranked factor, confirming that the growth department operates independently from and cross-functionally with both sales and marketing. Marketing- and sales-related factors were close for CGOs, with sales slightly higher, aligning with the preceding findings that sales is slightly more emphasized at the leadership level.

Analysis of CGO, CMO, and CSO Job Ads Based on Dictionary Derived from Study 1a.

Study 2: The Nature of the Growth Department: Deeper Insights from Interviews

In this study, we aimed to hear directly from growth practitioners to better understand the rationale behind the creation of the role and what it entails. We focused on CGOs, since as the top growth executives they would offer valuable insights into the function of growth departments within organizations. We analyzed ten publicly available YouTube interviews and supplemented them with ten semistructured interviews we conducted with CGOs. For the YouTube interviews, we selected those that either focused specifically on the CGO role or included detailed discussions about its responsibilities. The links to these interviews are provided in Web Appendix B. For the self-conducted interviews, we continued interviewing CGOs until no new insights emerged, reaching theoretical saturation (Strauss and Corbin 1990). Following qualitative research guidelines (Strauss and Corbin 1990), two authors iteratively applied open coding to develop first-order concepts, axial coding to identify second-order themes, and selective coding to aggregate themes into final theoretical dimensions. Table 2 presents the resulting Level 2, Level 1, and Level 0 codes, with selected excerpts illustrating the growth department's role, centered around two main (Level 2) dimensions: holistic growth strategizing and growth process leadership. Before describing these dimensions in detail, we first explain what the interviews revealed about the motivations for creating this department and how it differs from and relates to sales and marketing.

The Role of the Growth Department in Organizations.

The Purpose Behind Creating the Department

A synthesis of interviewee insights suggests that growth departments are primarily established to unify strategy and execution across both organic and inorganic growth initiatives. The need emerges from the recognition that growth in modern businesses is multidimensional, requiring a coordinated approach across various functions, ensuring that efforts in marketing, sales, customer success, innovation, and the like are not siloed but are part of a comprehensive strategy to drive sustainable growth. As one interviewee mentioned, “[The growth department] is a response to the prevalent issue of silos in organizations. It's about integrating various functions for cohesive growth strategies.” In the words of another CGO, “It's about creating and making sense of clear shared growth plans for the entire organization.”

Relationship with Sales and Marketing

All interviewees asserted that the growth department is cross-functional and distinct from marketing and sales departments, existing in addition to and working closely with these and many other departments. They indicated that the growth department directly reports to the CEO and is responsible for “all things growth,” ensuring that sales and marketing as well as other areas such as mergers and acquisitions (M&As), product development, or customer success are aligned with each other and with the overall growth strategy. When asked about the differences between them and a CMO or CSO and their relationship with these departments, respondents noted that (1) their role is broader, unifying all growth initiatives, both organic and inorganic (e.g., M&As), across various departments, (2) marketing and sales departments are typically preoccupied by more immediate targets (e.g., trade shows, campaign launches, quarterly or annual sales targets) and more operational, whereas the growth department has a more strategic and longer-term perspective, (3) marketing, sales, and similar departments across many organizations limit themselves to responsibilities indicated by their title (i.e., marketing-specific or sales-specific tasks), whereas the growth department is cross-functional, responsible for all growth-related initiatives across the firm, and (4) beyond organic growth, the growth department also manages inorganic growth (i.e., M&As) in close collaboration with the CEO and the board—areas traditionally outside the scope of marketing or sales.

The Role of the Growth Department: (1) Holistic Growth Strategizing

Insights from the interviews indicated that the first major role of the growth department is developing a holistic growth strategy for the organization. This overall theme emerged from combining three lower-level concepts: cross-functional growth strategizing, organic growth priority setting, and inorganic growth priority setting.

Cross-functional growth strategizing

Growth departments are pivotal in developing long-range planning and strategies for business growth. They are tasked with envisioning and framing the target state of the business, often extending over multiyear horizons. A core responsibility includes evangelizing growth visions across the organization. As “chief evangelists,” they promote a mindset focused on transformation and growth, ensuring all departments align with the company's growth objectives. Another essential aspect is unifying growth initiatives by integrating various functional groups, from product and marketing to sales and customer success, ensuring cohesive efforts and enterprise-wide decision-making. In the words of one CGO, the most important reason for creating the growth department was to improve “end-to-end commercialization and wire from strategy all the way through execution across various functional groups.” Another way to describe the growth department, according to a CGO, is “a horizontal organization that links things together to ensure we’re making the best enterprise decisions.” Another CGO expressed that “there literally isn’t a function within [the company] that my team doesn’t touch and work with routinely to go drive business decisions and outcomes,” while another CGO described her role as “the integrating function of the company.”

Organic growth priority setting

A big part of growth departments’ focus is improving organic growth, which is done by working closely with the revenue-generating functions of marketing, sales and customer success, and product on setting and revising strategies and priorities. In particular, they work on optimizing marketing channels through tailoring strategies based on metrics like customer acquisition cost and return on investment, and they guide marketing in focusing resources effectively and strategically. A CGO described this process as follows: “A website versus trade show versus direct outreach versus networking versus client channels … I can look across the board and see where are we hitting, and where are we missing? Where do we want to place strategic bets? And then ultimately … measure all that and then factor that into our go-forward budget and plan.” They also work closely with sales on customer and sales operations strategies, ensuring streamlined end-to-end processes in customer interactions. Additionally, the growth department aligns product development efforts with market demands and client needs, bridging the gap between R&D and sales to ensure the development of relevant and sellable products. In the words of one CGO, “The role of the chief growth officer relative to product is being the voice of the industry, the voice of the client.” Another CGO explained the decision to merge the product team under the growth department so that the product team would become fully aligned with the growth department and report to the CGO, because “client demand signal wasn’t making its way to the island of misfit toys … they were creating capabilities in [a] vacuum, and then they would create something, and out came a beautiful thing that nobody wanted.”

Inorganic growth priority setting

CGOs identify and capitalize on inorganic growth opportunities by collaborating with CEOs and boards to assess acquisitions and similar expansion strategies. Their role includes conducting due diligence, preparing integration strategies, and ensuring that the newly acquired entities align with the organization's goals. After a merger, the growth department focuses on operational efficiencies and integration, ensuring seamless incorporation into existing systems and maximizing value from acquisitions.

The Role of the Growth Department: (2) Growth Process Leadership

We classified the second part of growth department's responsibilities as “growth process leadership,” which emerged from merging two lower-level concepts: end-to-end responsibility and data-driven decision-making.

End-to-end responsibility

Many interviewees indicated that a major difference between the growth department and many traditional strategy-making offices (e.g., office of the chief strategy officer) is that growth departments are created to connect strategy making with execution; thus, they are mainly a cross-functional office working closely with all relevant departments such as marketing and sales on the execution side of growth strategies. In doing so, they orchestrate resources across the organization to ensure efficient allocation and alignment with impactful growth initiatives. In the words of one CGO, “One of the metrics that we really are proud of has been the ability to hone … over 600 projects to the 20 biggest projects that are going to make a difference for the organization.” Another mentioned: “I want to review all of our byline of business metrics and see where do we get the best bang for the buck? Because we’ll allocate more dollars in that perspective.” They combine strategy with operational execution, holding accountability for growth outcomes while delegating execution tasks to the relevant departments. This role requires the growth department to unify strategies across departments, ensuring cohesive efforts in product development, engineering, and sales, while maintaining a strong focus on accountability and operational alignment.

Data-driven decision-making

Growth departments develop growth metrics and analytical tools to guide the organization's growth trajectory. They define key performance indicators and targets that reflect the company's growth objectives. A significant part of this role is to align metrics across functions, fostering unified goals and cross-department collaboration. Moreover, many CGOs indicated that efficiency is at the center of their priorities. Growth departments drive process efficiency improvements by identifying cost-saving opportunities, addressing inefficiencies, and optimizing organizational operations to support top-line as well as bottom-line growth. In the words of one CGO, “Every opportunity for cost saving has to be executed because you’re trying to work off a very refined engine versus a spread thin that is wasting the company, and the reason to do all of this, we called it growth, and growth comes in from a strong belief in top line and bottom line.” Another CGO put it this way: “It's really about being able to focus the organization so that we can move faster.” Another CGO mentioned that his main focus is “how to leverage and get the impact of every dollar spent,” while another expressed that “my role in aligning and optimizing these resources plays a significant part in maintaining our financial health.”

In summary, the growth department serves as the linchpin of organizational growth strategies, combining visionary planning, cross-functional integration, and a relentless focus on both organic and inorganic opportunities. By leveraging data-driven insights and streamlining processes, they focus on sustainable and impactful growth across the enterprise.

The Impact of the Growth Department

Building on our findings so far and drawing from the boundary spanning and the organizational ambidexterity theories, we next hypothesize on the impact of the growth department. The boundary spanning theory aligns very well with our interviews, where respondents emphasized the growth department's cross-functional role in overcoming organizational silos and disconnects. Growth departments, as boundary-spanning entities, bridge gaps between siloed departments, enhancing organizational performance through holistic growth strategizing and growth process leadership. By addressing disconnects such as strategy–execution misalignment and departmental silos, they align efforts across teams and unify growth initiatives.

Being designated as a horizontal organization tasked with aligning all growth-related functions toward the common organizational goal of growth gives the growth department agency and influence in doing so, which is manifested in the way they instill the growth vision in their colleagues (Table 2, Point 1.1.2 [growth vision evangelizing]), unify growth initiatives throughout the organization (Table 2, Point 1.1.3 [growth initiatives unification]), and help create unified metrics across functions (Table 2, Point 2.2.2 [metrics alignment across functions]). Such agency and influence that follows the growth department's designation as a boundary-spanning entity is reminiscent of Levina and Vaast's (2005) concept of a new joint field, although in their conceptualization, they allow the boundary spanners in the new field to hold positions in other functions as well.

Moreover, in our interviews we detected a heavy emphasis on aligning new product development efforts (Table 2, Point 1.2.3 [product development alignment]) as well as a focus on optimizing and orchestrating efforts and resources toward improving efficiency (Table 2, Point 2.1.1 [resource orchestration], Point 2.2.3 [process efficiency improvement], or Point 1.2.1 [optimizing marketing channels]). Such efforts toward balancing innovation with efficiency are very much in line with the organizational ambidexterity theory and are central to organizational success (O’Reilly and Tushman 2013).

The interplay between boundary spanning and organizational ambidexterity provides a cohesive framework for understanding how influential growth departments drive organizational effectiveness. Scholars have previously theorized that structural ambidexterity, the most practical form of ambidexterity, whereby exploration and exploitation are simultaneously pursued through separate subunits devoted to each pursuit, would probably need linking mechanisms and a common vision between units to be successful (O’Reilly and Tushman 2013). With this line of reasoning, a boundary-spanning unit is uniquely positioned to enable structural ambidexterity, by integrating exploratory and exploitative activities across siloed structures, facilitating collaboration and alignment in fragmented organizational contexts. In turn, ambidextrous organizations create environments that amplify the impact of boundary-spanning roles by fostering adaptability and operational efficiency (Rapp et al. 2017). Influential growth departments exemplify this dynamic, acting as boundary-spanning entities that align innovation-focused strategies with operational realities. This dual role enhances their ability to balance exploration and exploitation, driving firm performance through strategic coordination and resource optimization. Therefore, we hypothesize:

Drawing from the organizational ambidexterity literature, we focus on two firm-level contingency factors: innovation intensity and cost leadership, which reflect the extent to which an organization concentrates its focus and resources on either exploration or exploitation (O’Reilly and Tushman 2013). Innovation-intensive firms dedicate exceptional attention to new product development and R&D, while cost leaders are masters of efficiency (Modi and Mishra 2011; Nath and Bharadwaj 2020). If the growth department's mission is to balance exploration and exploitation through boundary-spanning agency over growth, then a strong growth department may enhance the performance of firms leaning toward either side of the innovation–efficiency spectrum by enabling them to capture the benefits of both worlds.

Cost leaders are already highly efficient, but their emphasis on refining existing processes often dampens their willingness to embrace the unknown and its concomitant risks (O’Reilly and Tushman 2013). The growth department helps unlock innovation and market expansion by virtue of its institutional role in driving firm growth, enabling the firm to pursue various avenues including innovation and market entry. However, the growth department approaches these goals by optimizing marketing channels, directing resources to the highest-return initiatives, aligning product development with validated customer needs, and ensuring an overall focus on efficiency (Table 2). This disciplined approach to growth likely enhances cost leaders’ strengths while enabling expansion that aligns with their operational excellence.

Conversely, innovation-intensive firms often tolerate failure, which can result in a high number of unsuccessful products and wasted resources (O’Reilly and Tushman 2013). As noted by our interviewees, the growth department curbs the creation of “misfit toys” or “beautiful [products] that nobody want[s]” by working closely with the product team to ensure that customer needs and demand signals are clearly communicated. It also collaborates with data scientists, A/B testers, and user experience designers to ensure innovation efforts are data-supported and market-ready. However, innovation-dominant firms tend to prioritize novel, high-risk ideas over cost-effectiveness, potentially conflicting with the growth department's aim to balance innovation and efficiency. As a result, powerful growth departments may face heightened resistance from R&D and product teams when redirecting overly risky initiatives, increasing coordination burdens and diminishing the growth department's effectiveness.

Study 3: The Impact of Growth Departments in Startups

In Study 3 we focus on startup firms to examine the role of growth leaders in organizations. We decided to include startups in our exploration of growth positions mainly for two reasons. First, startups are fully focused on growth as their main outcome of interest, since only the ones that sufficiently grow can achieve either of the two coveted destinies of startups: being acquired or going public (Zider 1998). Second, by definition, startups have more room to grow than firms that have already fulfilled their growth potential, which allows us to better detect and capture the impact of growth leaders.

Study Context

In this study we investigate the relative impact of hiring a growth leader, compared with hiring a marketing or sales leader, on the success of a startup in obtaining more rounds of funding. 3 In this sense, among the studies in this article, this study is the only one in which we directly compare the impact of growth leaders with that of sales or marketing leaders. To this end, we collected data on startups that hired either a sales leader, a marketing leader, or a growth leader in 2017 and followed their metrics until 2019, the end of the observation period. We use the number of funding rounds obtained by the firm during the tenure of the hired individual as the dependent variable, controlling for a range of other variables during that time period that could impact funding.

In the startup world, advancing through various funding rounds is often synonymous with scaling the business to the next level (Zider 1998). Startups typically seek successive funding rounds to fuel expansion, both in operational capacity and market reach (Eldar and Grennan 2024; Gompers et al. 2020). In Web Appendix C, we give a detailed explanation of various stages of funding and what each round means for startups that successfully complete it. With each additional funding round, the valuation of the company generally increases, implying growth in its perceived potential and actual business metrics (Gompers et al. 2020). For instance, firms that secure Series A funding are generally valued at up to $15 million, those that successfully complete Series B funding enjoy valuations between $30 to $60 million, and Series C firms are valued at around $100 million (Reiff, Mansa, and Eichler 2023). These rounds not only denote increasing firm valuation but also highlight the evolution and maturation of the startup. Inherent in each funding round is a milestone or set of achievements that the startup aims for, and securing that funding implies confidence from investors in the startup's ability to reach those milestones. Therefore, the number of funding rounds is a germane proxy for the pace and the stage of growth a startup is experiencing and is the main metric used for measuring startup growth in the literature (Eldar and Grennan 2024; Gompers et al. 2020; Zider 1998). Prior marketing research has also used the number of funding rounds as the primary indicator of startup performance (Homburg et al. 2014).

Data Collection and Variables

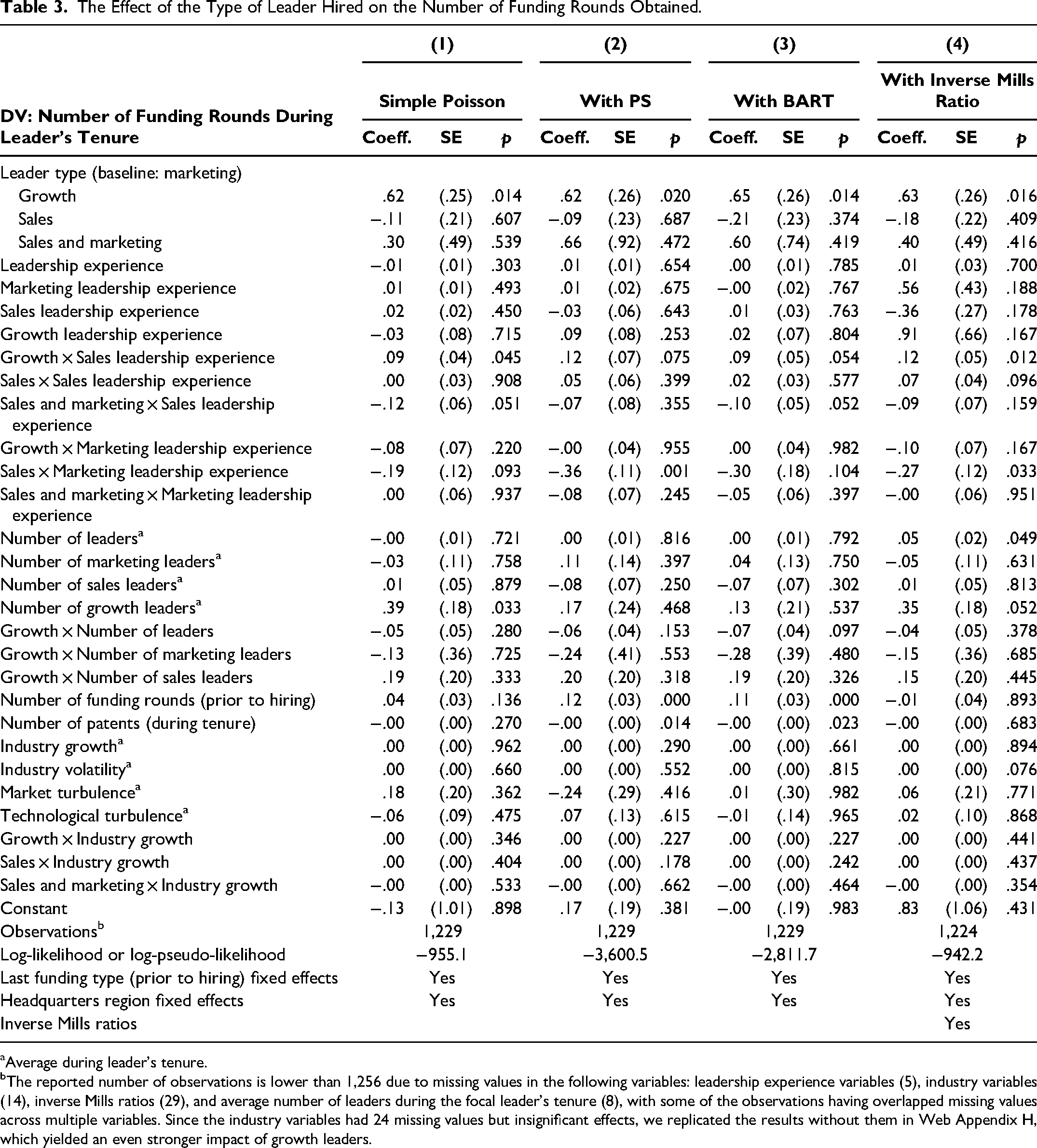

We collected our main data from Crunchbase, a company that tracks startups and has been used in prior research on startups by various scholars (e.g., Homburg et al. 2014; Winkler, Rieger, and Engelen 2020). In particular, we used the subscription-based service of Crunchbase, Crunchbase Pro, which allows users to create filters on its platform and extract data built by those filters. Data collection was completed for the most part in June 2019, but we had to go back to the platform in 2020 to build filters specifically for funding rounds, which enabled us to separate funding before and after the recruitment of the leaders. Therefore, all the data were downloaded from the platform in 2019 and 2020. We created separate filters for growth, sales, and marketing. For each category, we used the “People” filters on the platform, finding people with primary job title of growth, sales, or marketing who had joined their company in 2017. Web Appendix D shows a sample set of filters used to extract growth leaders. From there, we took several additional steps to validate and clean the data and prepare it for analysis. For brevity, these steps are in Web Appendix E. The final sample has 1,256 observations, including 116 growth leaders, 698 marketing leaders, 355 sales leaders, and 87 leaders with a marketing-and-sales joint title. While Study 3 captures the presence of growth (vs. sales or marketing) leaders, it offers first insights into H1, as top management team (TMT) presence in startups typically signals a meaningful level of influence and power.

Our dependent variable is the number of funding rounds that the startups received after hiring the leader in 2017 and during their tenure. 4 We picked this timeline because in our subsequent validation research on LinkedIn, we realized that some of the leaders had left their companies earlier than 2019, even though the filters we had created in 2019 captured “current job” titles. Therefore, rather than capturing the full timeline from hiring date to the study cutoff date in June 2019, we counted the number of funding rounds a firm obtained during the leader's tenure up until their departure or the study cutoff date (whichever came first) to avoid accounting for funding that may have been awarded after the leader's departure. The leaders’ tenure durations (i.e., from their recruitment date in 2017 till their departure date or the study cutoff date) were not significantly different across the four leadership categories (growth: M = 1.83 years, SD = .59; marketing: M = 1.80 years, SD = .73; sales: M = 1.85 years, SD = .75; marketing and sales: M = 1.70 years, SD = .63). We also collected additional variables, particularly two versions of certain variables, one to be used in the selection correction models (using the leaders’ exact start date with the company) and one version to be used in the main model. Details of these steps, additional sources of data, and the final breakdown of the variables along with the descriptive statistics are also in Web Appendix E.

Selection Correction

Given the observational nature of this study, we account for potential selection issues, unobserved heterogeneity, or endogeneity related to leader, firm, or industry characteristics that might correlate with additional funding during the leader's tenure and bias our results. For instance, if growth leaders had significantly richer leadership experience than marketing or sales leaders, better firm performance could be attributed to preexisting heterogeneity in leadership know-how rather than differences in functional approaches to growth. However, in our data, growth leaders had significantly lower leadership experience than other categories (see Web Appendix F), countering this scenario. Regarding firm-related confounders, startups hiring growth leaders were not at significantly different growth stages (e.g., number of previous funding rounds) compared with those hiring marketing or sales leaders. Additionally, we controlled for the category of the last funding round (e.g., “seed,” “Series B”), directly controlling for a startup's growth stage at the time of hiring. Similarly, startups hiring growth leaders were not in higher-growth industries at the time of hiring or during the leader's tenure, as no significant industry growth differences existed across categories (see Web Appendix F).

We employed three methods to address selection issues formally. Because our treatment variable has four levels (leadership categories), standard propensity score matching or selection models for binary treatments were unsuitable (Guo and Fraser 2015). Thus, we used generalized propensity score weighting (PS), a doubly robust method for multivalued treatments (Li and Li 2019). Additionally, we applied Bayesian additive regression trees (BART; Spertus and Normand 2018), a machine learning method enabling robust causal inference for multivalued treatments. Finally, we used a variation of Heckman-type selection models with a multinomial specification of the selection equation (Bourguignon, Fournier, and Gurgand 2007), as applied in recent marketing studies (Atefi et al. 2020). To ensure similarity across leadership categories, variables included in the selection equation were chosen based on their potential influence on treatment assignment (type of leader hired), the outcome variable (funding rounds obtained), or relevant background characteristics (Guo and Fraser 2015). For the PS and BART models, calculated weights were used in the main regression model. The Heckman-type selection model generated three inverse Mills ratios, which were added as controls in the main model. More details on these methodologies are in Web Appendix G.

Model Specification and Results

Due to the count nature of the dependent variable, we specified the following Poisson regression, where

The Effect of the Type of Leader Hired on the Number of Funding Rounds Obtained.

aAverage during leader's tenure.

bThe reported number of observations is lower than 1,256 due to missing values in the following variables: leadership experience variables (5), industry variables (14), inverse Mills ratios (29), and average number of leaders during the focal leader's tenure (8), with some of the observations having overlapped missing values across multiple variables. Since the industry variables had 24 missing values but insignificant effects, we replicated the results without them in Web Appendix H, which yielded an even stronger impact of growth leaders.

As Table 3 illustrates, we found that startups that hired a growth leader in 2017 obtained significantly more funding rounds compared with those that hired a marketing leader (baseline), while the impact of hiring a sales leader or a joint sales-and-marketing leader was not significantly different from hiring a marketing leader. These results are in line with H1 as they demonstrate the superiority of hiring a growth leader relative to the other three categories and provide first evidence for the effectiveness of an influential growth department. Besides the significance of the effect of the growth leader, we obtained a surprisingly large effect size (higher than .6 and in some robustness checks in Web Appendix H higher than .7). The large effect does not seem to be driven by any major outliers in the growth condition, since the highest number of funding rounds obtained by a company that hired a growth leader was four (M =. 96, SD = 1.11), while the maximum number of funding rounds for firms that hired a marketing or sales leader was five (M = .47, SD = .83) and seven (M = .42, SD = .87) respectively. Other sizable and significant coefficients existed among the fixed effects of the last funding type obtained by the firm before hiring the leader. For instance, in Model 1, firms whose last funding type before hiring the leader was seed (Coeff. = .72, SE = .15, p = .000), Series A (Coeff. = .53, SE = .19, p = .004), Series B (Coeff. = .61, SE = .20, p = .002), Series C (Coeff. = .90, SE = .24, p = .000), Series D (Coeff. = .72, SE = .33, p = .031), or Series E (Coeff. = 1.17, SE = .35, p = .001) were substantially more successful in obtaining additional funding rounds, while firms that either were too early (e.g., last funding type was preseed), were too late (e.g., Series F, Series G, and so on as last funding type), or had obtained other types of funding prior to hiring the leader (e.g., private equity, corporate round, equity crowdfunding, debt financing, secondary market) did not experience significant success in securing additional funding.

We also found that growth leaders with higher prior sales leadership experience were more successful in positively impacting the growth of the startup, but we did not find prior marketing leadership experience to be consequential for growth leaders. This finding echoes findings from Study 1a, in which the impact of the sales factor was slightly more pronounced at the leadership level for both job responsibilities and qualifications. Sales leaders often have a good understanding of the entire sales funnel, customers’ major pain points, and the profit ramifications of cultivating existing or new client relationships (Cron et al. 2014). Perhaps this perspective helps them when they take a growth position, enabling them to better articulate and implement an action plan for growth. In contrast, past sales leadership experience may be less critical when it comes to lower-level or more marketing-related or analytics-driven growth outcomes such as website visits or app downloads, which may rely more on the other elements of a growth position.

We did not find an interaction between growth and the number of marketing or sales leaders. The interaction between industry growth and the effect of the growth leader was not significant either, implying that, at least in the startup scene, the impact of a growth leader is neither amplified nor attenuated in high-growth industries. In Web Appendix I, we rule out an alternative explanation (signaling account) for our finding that a growth leader significantly contributes to obtaining more funding rounds.

Study 4: The Impact of Growth Departments in Public Firms

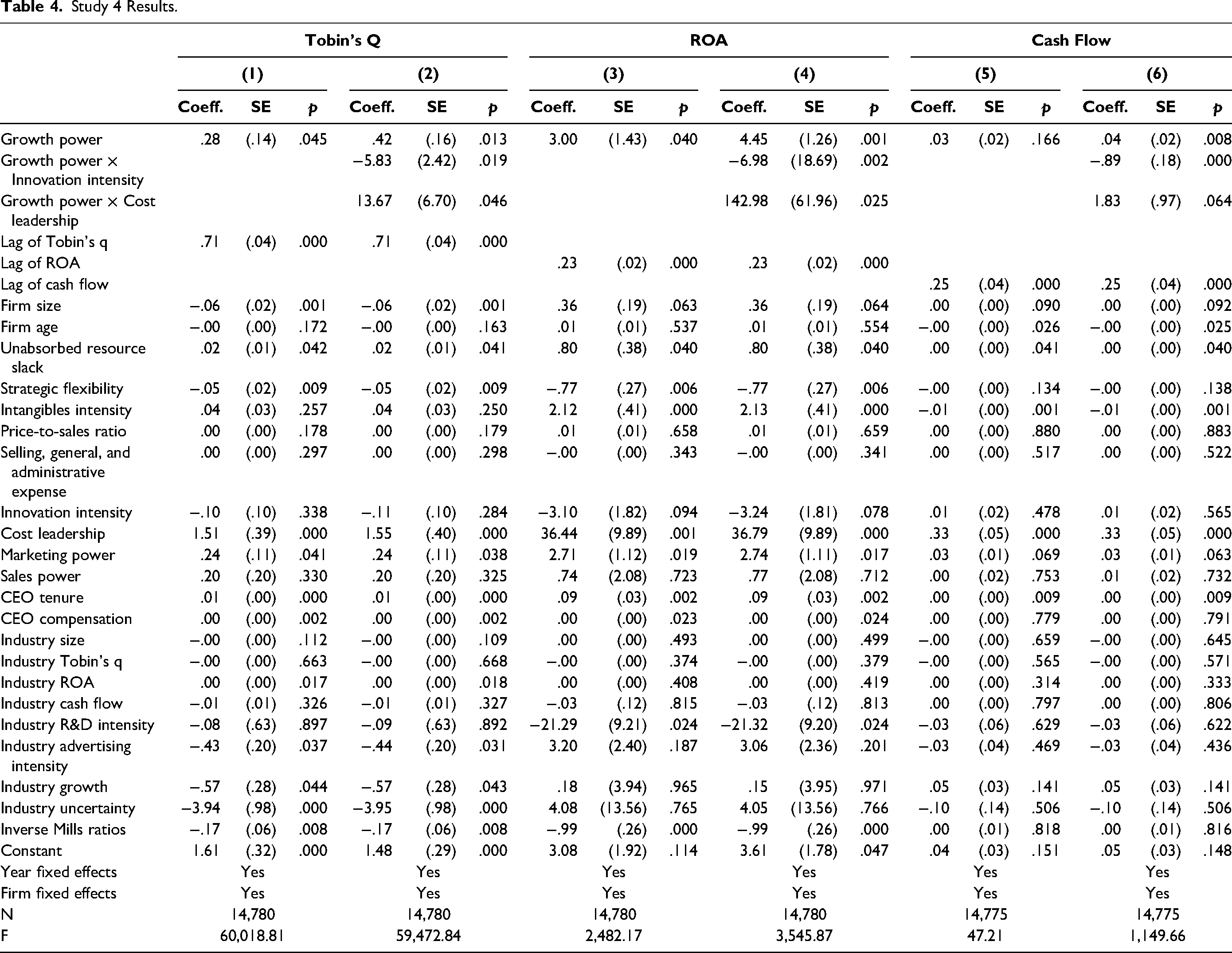

In this study, we shift our focus to studying the role of growth departments in publicly traded firms in the United States, particularly analyzing the role of the growth department’s power, defined as its ability to influence other people and departments within the firm (Feng, Morgan, and Rego 2015). This study provides a more direct test of H1, as we can more precisely measure growth department power, and better enables us to test our moderating hypotheses, H2a and H2b.

We focused on three performance metrics to explore the impact of a centralized growth department. First, we used Tobin's Q, a widely applied measure of firm performance (Edeling, Srinivasan, and Hanssens 2021). Additionally, we used two metrics that directly reflect growth department effectiveness: cash flow and ROA. These proxies capture key dimensions of financial performance and operational efficiency (Kang, Germann, and Grewal 2016; Morgan and Rego 2009). Cash flow measures liquidity and a firm's capacity to generate funds from operations, critical for reinvesting in initiatives like product development, market expansion, and acquisitions (Morgan and Rego 2009). It provides a tangible measure of financial growth (Srivastava, Shervani, and Fahey 1998). ROA evaluates how effectively a company uses assets to generate profits, serving as an indicator of efficiency and profitability (Kang, Germann, and Grewal 2016). High ROA demonstrates efficient resource utilization, a hallmark of sustainable growth (Morgan, Vorhies, and Mason 2009). Together, these metrics provide a holistic view of corporate growth: Tobin's Q offers a forward-looking, long-term, market-based perspective; cash flow highlights the financial foundation for expansion; and ROA emphasizes operational success and the translation of investments into earnings (Germann, Ebbes, and Grewal 2015; Miller 2004). Combining these metrics captures a firm's growth trajectory, including market valuation, financial stability, and operational effectiveness (Kang, Germann, and Grewal 2016; Morgan and Rego 2009).

Data and Variables

We collected data from multiple secondary sources to address our research questions using a large sample of firms over an extended period. Financial data for publicly traded U.S. firms was obtained from the Compustat database. Following prior research (e.g., Nath and Bharadwaj 2020; Nath and Mahajan 2008), we restricted the sample to firms with sales of at least $250 million at the midpoint of the observation period to increase the likelihood of identifying dedicated executives. TMT measures, including growth, were sourced from the Execucomp database, complemented by Securities and Exchange Commission 10-K filings to identify growth executives. After first-differencing the model and addressing missing data across control variables, our final dataset included 1,271 firms spanning 59 two-digit SIC (Standard Industrial Classification) codes, with 14,780 firm-year observations and an average of 11.6 years of data per firm from 2005 to 2020.

Growth executives were identified using the Execucomp database by searching for the keyword “growth” and manually reviewing titles to exclude those unrelated to dedicated growth positions (e.g., “chief executive of technology growth”). Since some firms may have multiple growth executives, it was crucial to capture their significance within the TMT. Using the method by Feng, Morgan, and Rego (2015), we measured the number of growth officers, their compensation, the scope of their position, and their rank within the TMT. These factors were combined through principal component factor analysis, yielding a highly correlated set (r = .83–.97) that loaded onto a single factor, explaining 93% of the variance. The resulting score was rescaled to range from 0 to 1, indicating growth power for each firm-year.

To measure cost leadership, we adopted Modi and Mishra's (2011) approach, calculating the log-transformed ratio of sales to the cost of goods sold for each firm, with higher values indicating a stronger cost focus. This ratio was normalized by industry averages and ranges to account for cross-industry differences. For innovation intensity, we used the log-transformed ratio of R&D expenditures to sales (Nath and Mahajan 2008), similarly normalized by industry averages and ranges, excluding the focal firm.

Our dependent variables included Tobin's Q, calculated using Chung and Pruitt's (1994) method as the ratio of a firm's market value plus the liquidating value of the firm's outstanding preferred stock and the firm's short-term liabilities to its total assets, offering a forward-looking, goal-agnostic assessment of firm performance. We also used ROA to evaluate operational efficiency and profitability, examining whether growth strategies enhance profitability or strain asset utilization. Finally, we assessed cash flow as the ratio of net cash flow to total assets, providing a tangible measure of liquidity and operational efficiency (Morgan and Rego 2009).

To control for determinants of firm performance, we included variables categorized into firm, TMT, and industry (market) characteristics, along with firm and year fixed effects. Detailed description of additional control variables is in Web Appendix J. Descriptive statistics and the correlation matrix can be found in Web Appendix K.

Identification Strategy and Modeling Approach

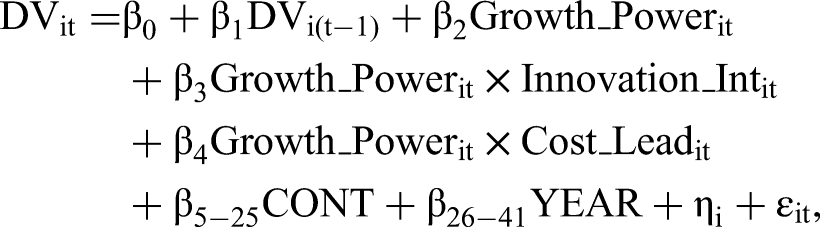

We took several steps to address endogeneity and unobserved heterogeneity. First, our choice of modeling directly addresses several identification concerns. In particular, to obviate omitted variable bias and reduce serial correlation, we introduced the lag of the dependent variable in our model (Germann, Ebbes, and Grewal 2015; Wooldridge, Wadud, and Lye 2016), which gives rise to a dynamic panel estimation (i.e., system generalized method of moments) that has been commonly used in the marketing strategy literature (Feng, Morgan, and Rego 2015; Janani et al. 2022). This approach is suitable for situations in which past realizations of the dependent variable may affect its current state, the covariates may not be strictly exogenous (i.e., covariates may be correlated with the past or current realizations of the error term), arbitrarily distributed fixed individual effects are present, and heteroskedasticity and autocorrelation within individuals are suspected (Roodman 2009). System generalized method of moments takes the level and the first-differenced equations as a system of equations, where the lagged differences of a potentially endogenous variable are used as instruments for it in the level equation, and its past values are used as instruments for the first-differenced equation (Arellano and Bond 1991; Roodman 2009). We used the following model specifications:

Second, we employed a two-stage Heckman method as an additional step to further address potential identification issues with the treatment variable (Wooldridge, Wadud, and Lye 2016). In the first stage, we utilized a probit estimation to ascertain the likelihood of a firm having a growth executive using all the control variables 5 in our main model as well as two instrumental variables: lag of sales growth and the proportion of firms that have growth officers to all firms operating in the same two-digit SIC category, excluding the focal firm. The peer-based instrument is expected to be positively correlated with the probability that a firm has a growth executive (relevance). The exogeneity argument is that the mere presence of other firms in an industry with growth officers should not have a direct effect on a particular firm's performance, once we control for a host of firm and industry characteristics that arise from competing in that industry. The correlation between our instrument and performance outcomes of firms that did not have a growth department was also insignificant, corroborating that the peer-based instrument did not have spillover effects impacting the industry and contaminating the causal impact on a focal firm's outcomes. We report the first-stage estimates in Web Appendix L. We added the estimated inverse Mills ratio from this stage to the main model as a control. The Breusch–Pagan/Cook–Weisberg test confirms the presence of heteroskedasticity in the data (p < .001), and therefore we utilized the sandwich estimator of variance (i.e., White–Huber standard errors) to correct the standard errors in all of the models.

Third, we used two copula-based methods, one based on a two-stage copula endogeneity correction (Yang, Qian, and Xie 2025) and one based on a nonparametric control function (Breitung, Mayer, and Wied 2024). The details on these steps are in Web Appendix M.

In summary, we controlled for unobserved time-invariant firm heterogeneity, time fixed effects, carryover effects of a firm's prior status, and other factors that can affect firm performance to reduce omitted variable bias as much as possible. In addition, we directly accounted for potential endogeneity of growth power by using a two-stage Heckman model and two copula-based methods reported in Web Appendix M. We allowed for heteroskedasticity at the industry level and utilized the robust estimator of variance to produce valid standard errors. Besides all these steps, we replicated our results after performing additional endogeneity analyses by including more lagged values as additional moment conditions, using a Rubin causal framework and a matched sample, changing lag structures in the model, performing outlier sensitivity analysis, and ruling out unobserved intentions of the board as a potential confounder. 6

Results

Table 4 demonstrates our results, with main-effects-only models reported first, followed by models with interactions. 7 The AR(II) test indicates that the second-order lags are not correlated with the error term (p > .53) and hence can be used as instrumental variables. However, to avoid overidentification and biases associated with having too many instruments, we limited the number of instrumental variables to only the second-order through fifth-order lags in the estimation (Roodman 2009). The results from the difference-in-Hansen test of endogeneity reveal that the instruments are exogenous (p ≈ .99). Overall, we find that growth power in firms’ TMT enhances firm performance, providing support for H1.

Study 4 Results.

Turning to the moderation effects in Models 2, 4, and 6 in Table 4, we find support for the positive interaction between growth power and cost leadership (H2a) and the negative interaction between growth power and innovation intensity (H2b). A culture focused on long-term, uncertain gains with high tolerance for failure tends to be inefficient. In innovation-centric environments, product and R&D teams often hold greater institutional power than they do in less innovation-intensive firms. Adding a powerful growth department aimed at reducing waste and aligning product development can create frictions between these influential parties. In our interviews, we discerned that in many cases, growth departments held significant oversight of product teams, often requiring the product organization to merge under the growth department and report to the CGO to align with the growth vision. These findings underscore the challenges of achieving ambidexterity in firms heavily skewed toward exploration. From a different angle, adding exploration efforts to highly efficient firms may be less challenging, as it does not require major changes to the exploitation side. This is particularly true when ambidexterity is overseen by an entity like the growth department, which ensures that innovation aligns with efficiency and resource optimization. However, incorporating exploitation into highly innovative firms often demands significant organizational changes, including reassessment of product development, customer alignment, and elimination of wasteful initiatives. The literature on ambidexterity has largely overlooked this nuance: Improving exploration in exploitation-focused firms may be easier than improving exploitation in exploration-focused firms. Interaction plots are provided in Web Appendix N.

General Discussion

Our multimethod investigation provides the first comprehensive examination of the growth department's nature (RQ1) and impact (RQ2). Studies 1a, 1b, and 2 identify growth departments as units prioritizing (1) holistic growth strategizing and (2) comprehensive growth process leadership. These studies also clarify how growth departments operate and differ from other units like marketing and sales. Studies 3 and 4 assess their impact, showing that startups with growth leaders secured more funding rounds than those with sales or marketing leaders (Study 3). In public firms, growth departments significantly enhanced Tobin's Q, ROA, and cash flow (Study 4). Additionally, growth departments proved more effective for cost leaders but less so in innovation-intensive environments.

Contributions to Academia and Practice

Our article advances academic knowledge in several ways. First, we provide the first examination of an emerging governance approach for coordinating firms’ activities in driving growth: the growth department. The results of our studies emphasize this contribution.

Second, we contribute to a stream of marketing strategy research that explores how organizations achieve superior marketplace performance. This literature draws from organizational learning theory to document approaches such as increasing responsiveness to market needs through the generation and dissemination of market intelligence (i.e., market orientation; Kohli and Jaworski 1990); benchmarking marketing competence against top firms (i.e., benchmarking marketing capabilities; Vorhies and Morgan 2005); executing priorities tied to the marketing ecosystem, end-user focus, and agility (i.e., marketing excellence; Homburg, Theel, and Hohenberg 2020; Moorman and Day 2016); and establishing high-level principles and guidelines (i.e., marketing doctrine; Challagalla, Murtha, and Jaworski 2014). One criticism of this literature is that practitioners often find these concepts difficult to implement due to structures and workflows that do not support them (Homburg, Theel, and Hohenberg 2020). We broaden this literature by documenting the growth department, which offers a clear governance structure for growth and consolidates growth ownership, and by defining its role and interactions with other departments. Third, we show that growth departments manage both organic and inorganic growth, extending textbook marketing frameworks that primarily focus on organic growth. Fourth, we contribute to cross-functional collaboration research by showing that growth departments align growth activities across functions without overhauling formal reporting lines, instead using unified metrics, vision evangelizing, and resource orchestration to offer an agile governance mechanism. While prior research has highlighted the benefits of better marketing–sales alignment, growth departments take this further by focusing specifically on growth and mobilizing all related departments toward both organic and inorganic growth outcomes.

Fifth, we integrate boundary spanning and ambidexterity theories, revealing how exploration versus exploitation priorities influence boundary spanners’ effectiveness. Boundary-spanning coordination is more impactful in exploitation-focused firms (e.g., cost leadership emphasis) but less effective in exploration-focused firms (e.g., high innovation intensity). Our findings illustrate how growth departments, with their disciplined innovation, can improve exploration in exploitation-heavy firms more easily than adding exploitation to exploration-heavy firms, which requires process changes that may face resistance from entrenched teams.

Our final theoretical contribution pertains to the literature on the role and impact of marketing departments in organizations. This literature often aggregates various departments under the marketing label, overlooking key distinctions between functions. Moreover, it focuses heavily on C-suite influence, neglecting the tasks, relationships, and responsibilities of individual departments across organizational levels. We emphasize the importance of studying departments individually to understand their unique contributions to firm strategy.

Managerially, our article offers several important insights. First, we are the first to demonstrate the benefits of a consolidated approach to growth via a dedicated department responsible for driving initiatives across organizational silos. With many industries adopting growth departments, our work is the first to show the effectiveness of this structure for firms considering it. However, simply creating a growth department based on its effectiveness is insufficient without clear guidance on what it does; how it differs from traditional functions like sales, marketing, and product; how it interacts with those functions; and what its core responsibilities are. Our Study 2 documents these elements in detail. Further, our findings help clarify when a growth department is likely to be effective. While our studies show a consistently positive average effect on performance, the effect is stronger in firms focused on cost leadership and weaker in those with high innovation intensity. We recommend that cost-focused firms consider adopting a growth department to better align growth efforts, while innovation-intensive firms may not benefit unless they are comfortable with the department's focus on investing only in data-backed initiatives and divesting from unproven innovation. Our results also offer guidance on designing and developing a growth department. Managers can use our framework—including Level 2, Level 1, and Level 0 categories—as a blueprint to define work streams, assign responsibilities, set goals, and track progress. For instance, the “growth vision evangelizing” category can be broken into stages: (1) defining a communication process, (2) measuring efforts, and (3) tailoring messaging to stakeholders. Scorecards can monitor execution and outcomes in each area.

Finally, our research informs talent selection and development for growth roles. While prior experience in marketing, sales, or analytics is helpful, it is not sufficient for senior roles. Successful candidates need cross-functional leadership and strategic abilities, including expertise in areas like postmerger integration. We recommend prioritizing candidates with broader (possibly nonlinear) career paths and offering training that goes beyond functional skills. Programs should include modules on cross-functional strategy, end-to-end process ownership, and leading initiatives across silos.

Limitations and Future Research