Abstract

Although reacquiring customers can lead to beneficial outcomes, reacquisition processes are often unpleasant for employees, who may be required to admit and address failures. Because many organizational environments reward success and punish failure, companies need to understand how to create an organizational environment that stimulates customer reacquisitions. This study investigates the impact of failure-tolerant cultures and formal reacquisition policies on successful customer reacquisition management. Drawing on organizational design theory and psychological ownership theory, the authors find that failure-tolerant cultures have an inverted U-shaped effect on reacquisition performance because moderate failure tolerance increases reacquisition attempts while not inducing more failures or increasing their severity. Formal reacquisition policies, in contrast, have a positive linear relationship. Notably, formal reacquisition policies do not conflict with failure-tolerant cultures but enhance the beneficial effects of failure tolerance on reacquisition performance; formal reacquisition policies provide guidance for reacquisition attempts that failure-tolerant cultures inspire. Finally, results show that customer reacquisition performance is positively related to overall firm financial performance, a finding that emphasizes the managerial and organizational-level importance of reacquisition management.

Keywords

Understanding how companies can reacquire customers is important in both research and practice (e.g., Stauss and Friege 1999). Although companies likely benefit from winning back lost customers (e.g., Thomas, Blattberg, and Fox 2004), company cultures may present a hurdle to successful customer reacquisition management. More specifically, when attempting to reacquire customers, employees have to face and discuss unpleasant incidents, failures, or weaknesses. Organizational cultures often instill a tendency in employees to take failures “as indicators of poor performance, negligence, or as lack of competence” (Frese and Keith 2015, p. 665). Although companies have begun to acknowledge the value of failure (Farson and Keyes 2002), most organizations still interpret failure negatively (Khanna, Guler, and Nerkar 2016) by rewarding success and punishing failure (e.g., Cannon and Edmondson 2005). Thus, a reasonable assumption is that in a “competitive world of business, where a mistake can mean losing a bonus, a promotion, or even a job” (Farson and Keyes 2002, p. 65), employees are likely to refrain from addressing customer defection.

Successful customer reacquisition management may thus require companies to develop a failure-tolerant organizational culture that encourages a constructive treatment of failures (e.g., Danneels 2008). We argue that in failure-tolerant organizational cultures, employees might be willing to address failures by assuming “ownership” of the reacquisition process and going to great lengths to win customers back (e.g., Maxham and Netemeyer 2003; Schepers et al. 2012).

However, a failure-tolerant culture may also be counterproductive for customer reacquisitions in that employees might make decisions in other ongoing customer relationships with less due diligence (Danneels 2008). As a consequence, before defecting, customers may have encountered more frequent and more severe failures, substantially lowering the chance to win them back (e.g., Harmeling et al. 2015; Kumar, Bhagwat, and Zhang 2015). Thus, our first research question is, How does a failure-tolerant organizational culture affect reacquisition performance (i.e., the share of lost customers the organization reacquires)?

Importantly, while a tolerance for failure might benefit customer reacquisition management, companies face difficulty in managing or controlling which employee behaviors failure tolerance inspires (Maxham and Netemeyer 2003; Osterloh and Frey 2000). Unsurprisingly, companies have started to establish formal reacquisition policies (e.g., Reinartz, Krafft, and Hoyer 2004). Formal reacquisition policies are organizational specifications that guide employee behaviors during the reacquisition process (Stauss and Friege 1999). However, formal policies likely represent a different route to customer reacquisition. While failure tolerance may inspire employees to attempt reacquisition of their own accord, formal reacquisition policies prescribe and enforce employee reacquisition behaviors. Whether these two routes counterbalance or reinforce each other is unclear.

On the one hand, formal reacquisition policies may offset positive effects of failure tolerance by “crowding out” employees’ intrinsic motivation for reacquisition management (Hernandez 2012)—a phenomenon prior literature discusses as the corruption effect of extrinsic motivation (Deci 1975). On the other hand, formal reacquisition policies may have a “crowding-in” effect (Osterloh and Frey 2000), in that they may reinforce benefits of failure tolerance by providing helpful directives for employees (Locke and Latham 2002). Thus, our second research question is, How do formal reacquisition policies moderate the impact of failure-tolerant cultures on reacquisition performance?

Notably, customer reacquisition management creates costs—for example, directly in the form of monitoring costs or indirectly in the form of lost profits owing to price concessions—that need to be justified by revenue increases. Furthermore, reacquisition attempts may lower reference prices of not-defected customers (Kanuri and Andrews 2019; Mazumdar, Raj, and Sinha 2005) or provoke customers’ strategic defection behaviors (i.e., customers defect to get a better offer, such as a lower price from the same company; Thomas, Blattberg, and Fox 2004). Thus, our third research question asks, Is a company’s reacquisition performance relevant to its overall firm performance?

Our study responds to the Marketing Science Institute’s (2018) call to examine organizational issues in marketing and provides three focal contributions. As our first contribution, we introduce failure tolerance as an informal success factor for customer reacquisition management and demonstrate its inverted U-shaped impact on reacquisition performance. We find that reacquisition performance becomes three times larger, increasing from low to optimal levels of failure tolerance. However, failure tolerance can also elicit negative effects: moving from optimal to high levels of failure tolerance, reacquisition performance drops by 13%.

As our second contribution, we perform the first organization-level test of the proposition that formal reacquisition policies should favorably affect reacquisition performance (Stauss and Friege 1999). We analyze the interplay between formal and informal organizational elements (Hoetker and Mellewigt 2009) of customer reacquisition management: formal reacquisition policies enhance positive effects of failure tolerance. Our results indicate that in our sample, a company with an average level of failure tolerance increases reacquisition performance by more than 1.5 times when moving to a higher level of formal reacquisition policies. For those companies, the negative effects of failure tolerance set in later.

Our third contribution is the establishment of a positive effect of reacquisition performance on overall financial performance. Our results show that positive consequences (e.g., increased revenues) more than offset costs of customer reacquisition management, such as price concessions. Overall, our findings emphasize the managerial importance of customer reacquisition management.

Organizing for Customer Reacquisition Management

Organizational Perspective on Customer Reacquisition Management

Table 1 reviews the scarce literature on customer reacquisition management and reveals an important research void regarding the organizational level of customer reacquisition management (cf. Reinartz, Hoyer, and Krafft 2004). Prior research has focused on the customer (e.g., Homburg, Hoyer, and Stock 2007) and the customer relationship level (e.g., Kumar, Bhagwat, and Zhang 2015). Specifically, prior literature has explored how individual actions such as price concessions help win customers back but has not investigated the role of organizational elements, thereby implying that employees are willing to address defections. However, employees are likely to avoid addressing failures (Cannon and Edmondson 2005), and organizational cultures that display low levels of failure tolerance may nurture such a tendency in employees. Thus, understanding how organizational elements contribute to reacquisition performance is important (Hartline, Maxham, and McKee 2000).

Overview of Customer Reacquisition Literature and Positioning of Our Study.

a Qualitative study.

b Conceptual paper (no empirical analysis conducted).

Notes: ✓ = included in the study; (✓) = partially included in the study; — = not included in the study; N.A. = not applicable.

Our investigation draws on organizational design theory to study these elements. We introduce a failure-tolerant organizational culture as a focal informal organizational element and formal reacquisition policies as a focal formal organizational element for customer reacquisition management.

Organizational Design Theory and Customer Reacquisition Management

We couch our conceptual framework in organizational design theory, which identifies and emphasizes the importance of both informal and formal elements of organizations (e.g., Tushman and Nadler 1978). Informal organizational elements largely refer to social aspects within the organization and the resulting organizational norms, values, and beliefs (e.g., Gulati and Puranam 2009). Therefore, informal elements can be associated with organizational culture, which is “the pattern of shared values and beliefs that help individuals understand organizational functioning and thus provide them with the norms for behavior in the organization” (Deshpandé and Webster 1989, p. 4; Homburg and Pflesser 2000).

Failure-tolerant culture

We define a “failure-tolerant organizational culture” as organizational values, norms, and artifacts that imply that failures are constructively handled, openly addressed, and freely communicated; that the causes and underlying mechanisms of failures are analyzed for improvement; and that failures are even actively encouraged (e.g., Farson and Keyes 2002; Shepherd, Patzelt, and Wolfe 2011). Thus, a failure-tolerant organizational culture encompasses failure handling, failure communication, failure learning, and failure encouragement (e.g., Danneels 2008; Edmondson 1999; Van Dyck et al. 2005; Weinzimmer and Esken 2017).

We argue that a failure-tolerant organizational culture is essential for customer reacquisition management. Employees are likely to perceive customer defection as an undesirable or unpleasant occurrence equated with failure, regardless of the reason for defection. 1 Usually, employees do not freely and deliberately discuss their mistakes. They may fear blame from colleagues or punishment by superiors (Cannon and Edmondson 2005; Dahlin, Chuang, and Roulet 2018). As reluctance to address failures would be counterproductive for reacquisition management, it renders failure tolerance an important organizational quality.

Employees typically acquire a tolerance for failure outside the reacquisition context via organizational socialization—the process by which a person acquires knowledge necessary to assume an organizational role (Van Maanen and Schein 1979). Organizational socialization to failure tolerance might occur in several ways. First, symbolic acts may nurture a tolerance for failure (Homburg and Pflesser 2000). For instance, Procter & Gamble has reportedly humorously handed out a “heroic failure award” (Morgan 2015) that employees likely find indicative of a general failure-tolerant culture. Second, group observation may implicitly contribute to employees’ failure tolerance (Harmeling et al. 2017): employees may acquire a tolerance for failure through regular interactions with mentors or by observing coworkers’ behaviors (Lam, Kraus, and Ahearne 2010). Third, employees join companies with certain strengths and skills that the company values. After an employee is on board, socialization can also occur when employees discuss failures, thereby reinforcing an existing tolerance for failure as an important norm (Hartline, Maxham, and McKee 2000).

Once employees have internalized a failure-tolerant culture, they tend to view it as a “perfectly ‘natural’ response to the world of work” (Van Maanen and Schein 1979, p. 210). Thus, a reasonable expectation is that once employees have acquired a failure-tolerant mindset, it should guide them during customer reacquisition endeavors.

Formal reacquisition policies

“Formal reacquisition policies” refer to the extent to which companies establish and enforce strict formal rules and procedures that employees must follow when reacquiring customers. Classifying reacquisition policies as a formal element is in line with organizational design theory. Organizational design theory, for instance, lists specialization, formalization, and standardization as formal elements (Soda and Zaheer 2012). In addition, organizations expect formal elements to steer employees’ behavior toward support of high organizational performance (Reif, Monczka, and Newstrom 1973). The same applies for formal reacquisition policies, further supporting their classification as formal elements.

As the reacquisition process entails “the planning, realization, and control of all processes that the company puts in place to regain customers” (Stauss and Friege 1999, p. 348), formal reacquisition policies capture these three phases of the reacquisition process. Specifically, formal reacquisition policies comprise strict systematic and standardized processes for reacquisition analysis, reacquisition activities, and reacquisition monitoring (Stauss and Friege 1999).

Conceptual Framework and Predictions

To overview the logic, Figure 1 summarizes our predictions. We argue that a failure-tolerant organizational culture and formal reacquisition policies offer different routes to reacquisition performance (i.e., share of lost customers the organization reacquired). An internalized tolerance for failure will contribute to employees’ psychological ownership of the reacquisition process, leading employees to go to great lengths to win customers back (i.e., engage in extra-role behaviors). In contrast, formal reacquisition policies likely lead employees to perform formally defined customer reacquisition tasks in expected ways (i.e., employ in-role behaviors). As these divergent routes may create tensions, we explore the interaction between failure-tolerant cultures and formal reacquisition policies. 2

Conceptual framework.

The Impact of Failure-Tolerant Cultures on Customer Reacquisition Performance

We predict two countervailing effects of failure-tolerant cultures on reacquisition performance. We argue that reacquisition performance depends on employees’ willingness to address failures, but also on the experiences in the initial relationship. Failure tolerance impacts both factors, as we briefly summarize and explain in more detail in the sections that follow.

First, failure tolerance may increase the number of failures that are addressed given employees’ psychological ownership of the reacquisition process. Second, high levels of failure tolerance might, at the same time, lower the number of successful reacquisitions because more customers are likely to experience more problems due to failure frequency and severity. At low to moderate levels of failure tolerance, we expect that the benefits of the number of failures addressed will outweigh the costs of failure severity and frequency. However, as failure tolerance increases, the costs of failure severity and frequency may supersede the benefits of the number of failures addressed.

Benefits of number of failures addressed

As we have noted, failure-tolerant cultures may instill in employees a feeling of psychological ownership that makes them feel responsible for customer reacquisition. Psychological ownership is a cognitive–affective construct “in which individuals feel as though the target of ownership…is theirs” (Pierce, Kostova, and Dirks 2003, p. 86). Such targets of ownership can be activities such as the reacquisition process (Pierce, Kostova, and Dirks 2001; Schepers et al. 2012).

Employees are likely to assume ownership of the reacquisition process in failure-tolerant companies. Failure-tolerant cultures inspire employees to voice their ideas (Detert and Burris 2007) and discuss mistakes openly (Weinzimmer and Esken 2017) rather than provoking fear of being blamed for failures (e.g., customer defection; Shepherd, Patzelt, and Wolfe 2011). Consequently, employees are more disposed to invest their skills, ideas, and effort into customer reacquisition management. According to theory, such investments stimulate feelings of ownership (Pierce, Kostova, and Dirks 2001). In line with our rationale, research demonstrates that failure tolerance fosters employees’ feelings of responsibility for their own failures as well as those of their clients (Gronewold and Donle 2011).

We expect that feelings of ownership will increase the number of failures addressed by employees, meaning the number of attempts to engage in customer reacquisition. Theory predicts that once employees have assumed ownership of a target, they will be attentive to their “possessions” (Hernandez 2012), and research shows various positive outcomes of psychological ownership (e.g., Jussila et al. 2015). For instance, once employees assume psychological ownership, they engage in favorable extra-role behaviors (Schepers et al 2012). Thus, we predict that a sense of responsibility for the reacquisition process, which failure tolerance stimulates, spurs employees to work harder, be more creative, and act unconventionally in reacquiring customers. Thereby, they address more failures and increase reacquisition performance.

Costs of failure severity and frequency

However, we expect that high levels of failure tolerance can have a boomerang effect on customer reacquisition performance. High levels of failure tolerance are likely to increase the number of lost customers experiencing higher failure frequency and failure severity in their initial customer relationships. Failure frequency refers to the number of failures customers experience in relationships. Failure severity refers to the magnitude of loss that customers experience owing to failures. Such losses can be tangible (e.g., financial loss) or intangible (e.g., annoyance, anger) (Hess, Ganesan, and Klein 2003). Failure severity and frequency may increase because failure tolerance can introduce laxness in companies. Once employees have internalized a tolerance for failure, they may make decisions with less due diligence and effort and can even “hide” behind a failure-tolerant culture, provoking more and increasingly severe failures in customer relationships (Danneels 2008).

Failure frequency and severity likely lower reacquisition performance. Reacquisition performance depends substantially on the experiences customers had in the initial relationship; employees are less likely to successfully reacquire customers who experienced multiple and severe failures (Kumar, Bhagwat, and Zhang 2015). Research shows that even a few negative events in customer relationships can make customers reevaluate the complete relationship, potentially reinterpreting positive prior experiences as negative experiences (Harmeling et al. 2015). Thus, frequent and severe failures may cause “irrecoverable damage” (Harmeling and Palmatier 2015, p. 329) for reacquisition attempts, lowering reacquisition performance.

Importantly, failure tolerance may lead to an exponential increase in failure severity and frequency. In companies that are excessively failure-tolerant, coworkers are not likely to provide corrective measures when they note the occurrence of multiple and severe failures. Rather, as social learning theory predicts, dysfunctional effects of failure tolerance could spread rapidly in the organization as employees observe and imitate peers’ behaviors (Bandura 1977; Harmeling et al. 2017).

The combination of our predictions results in an inverted U-shaped relationship between failure tolerance and reacquisition performance. An inverted U-shaped relationship arises as the result of a linear positive benefit function and a convex cost function (for a detailed discussion of theorizing U-shaped effects, see Haans, Pieters, and He [2016], Gruner et al. [2019], and Lawrence et al. [2019]). The positive benefit function results from the linear relationship between psychological ownership and number of failures addressed. The convex curve stems from the exponential relationship between failure tolerance and failure severity and frequency (Figure 2, Panel A).

Illustration of the hypotheses on the inverted U-shaped effects.

Formal Reacquisition Policies and Reacquisition Performance

Formal reacquisition policies may be another route for companies to stimulate reacquisition performance. Formal elements such as monitoring or guidelines focus on task accomplishment by directing employees to engage in in-role behaviors (Niehoff and Moorman 1993). They prescribe employees’ behaviors, with the outcome that employees “do not feel that they can go beyond their well-defined areas of responsibility” (Podsakoff, MacKenzie, and Bommer 1996, p. 292). In line with this reasoning, formal elements lead to greater role clarity but lower engagement in extra-role behaviors (Podsakoff, MacKenzie, and Bommer 1996).

As a formal element, formal reacquisition policies constitute clear guidelines for reacquisition analysis, providing employees with a structured framework for identifying lost customers, pinpointing reasons for defection, and evaluating reacquisition potential (Stauss and Friege 1999). Formal reacquisition policies direct employees to engage in expected behaviors. They encourage in-role behaviors and increase the number of failures addressed. Similarly, formal guidelines for reacquisition monitoring help systematically detect shortcomings in reacquisition processes and promote organizational learning processes (March 1991). Overall, formal reacquisition policies encourage employees to make more reacquisition offers, increasing the firm’s reacquisition performance.

Failure-Tolerant Cultures and Formal Reacquisition Policies: Moderating Effect

Thus far, we have predicted the individual effects of failure-tolerant cultures and formal reacquisition policies. However, informal and formal organizational elements are likely to be present simultaneously in organizations and can create tensions (e.g., Schepers et al. 2012). In our sample, we observe a moderate correlation between failure-tolerant cultures and formal reacquisition policies (r = .34). Because the two elements represent different and potentially conflicting routes to reacquisition performance, their joint occurrence raises the question of how formal reacquisition policies moderate the effect of failure-tolerant cultures on reacquisition performance.

From a pragmatic perspective, following formal guidelines and providing reports likely ties up employees’ resources, lessening the potential for discretionary behaviors (Netemeyer, Maxham, and Pullig 2005). Hernandez (2012) even proposes (but does not test empirically) that formal elements could undermine feelings of ownership. Thus, with greater levels of formal reacquisition policies, an increase in failure tolerance may manifest in extra-role behaviors to a lesser extent (Homburg, Boehler, and Hohenberg 2019; Schepers et al. 2012).

However, in the context of customer reacquisition, we propose that formal reacquisition policies can enhance the positive effects of failure tolerance on reacquisition performance. Crowding theory suggests that formal reacquisition policies may beneficially affect outcomes of psychological ownership if employees perceive formal reacquisition policies as informative rather than controlling. In such a situation, a crowding-in effect sets in: formal management enhances intrinsic motivation for extra-role behaviors (Osterloh and Frey 2000).

This effect may apply in the context of customer reacquisitions, as employees assume ownership of the reacquisition process they strive to successfully reacquire customers. However, the unstructured context of customer reacquisitions may create ambiguity for employees as to which behaviors they should engage in. In line with goal-setting theory, formal reacquisition policies may serve a directive function, allowing employees to focus on goal-relevant activities (Locke and Latham 2002). Thus, instead of perceiving formal reacquisition policies as controlling, employees may consider them informative and respond positively (Osterloh and Frey 2000). Formal reacquisition policies provide clarity, work efficiency, and guidance when the unstructured context of customer reacquisition endeavors fails to do so (e.g., Podsakoff, MacKenzie, and Bommer 1996; Schepers et al. 2012).

Formal reacquisition policies thus enhance the linear positive relationship between failure tolerance and failures addressed. This enhancement shifts the turning point to the right, meaning that negative effects only set in at higher levels of failure tolerance. Notably, such a shift in the turning point does not require that formal reacquisition policies also moderate the relationships between failure tolerance and failure frequency and severity (Haans, Pieters, and He 2016).

3

Figure 2, Panel B, illustrates this prediction.

The Impact of Reacquisition Performance on Firm Performance

Several arguments suggest a positive relationship between reacquisition performance and firm performance. First, successful customer reacquisitions help maintain the customer base and thereby increase turnover and profits (Griffin and Lowenstein 2001). Second, as reacquired customers tend to show higher purchase volumes and loyalty than in the initial relationship, they are more profitable (e.g., Tokman, Davis, and Lemon 2007). Third, reacquiring customers is associated with solving problems of dissatisfied customers, who tend to vent their displeasure about unsolved problems. Customer reacquisition thus prevents negative word of mouth and enhances company reputation (Reichheld and Sasser 1990), exerting significant positive effects on company performance (Roberts and Dowling 2002). Fourth, companies that successfully reacquire customers can gain important insights into company weaknesses and eliminate them (Stauss and Friege 1999). Thus,

Methodology

Main Sample and Independent Financial Data

Because data on our focal construct (i.e., failure-tolerant culture) are generally not available from secondary data sources, we conducted a cross-sectional online survey to test our hypotheses (Rindfleisch et al. 2008). Survey research is often advantageous for investigating intraorganizational issues, because it allows for important insights that cannot be obtained from other data sources (Hulland, Baumgartner, and Smith 2018). However, as our model also includes the firm’s overall financial performance, we complement our survey data with financial indicators from an objective database.

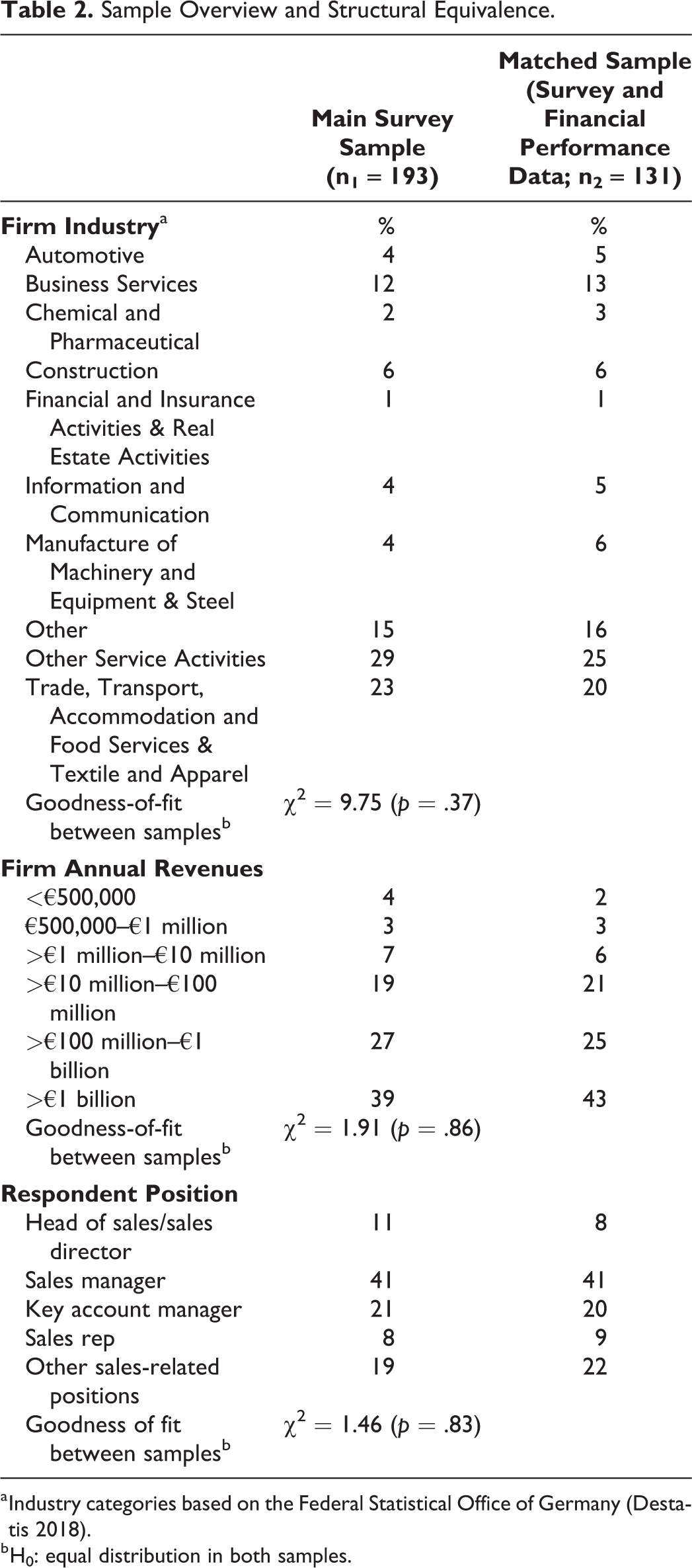

We identified potential respondents for our survey via the social business network XING, an established online career platform in Germany. We selected the contacts through filtering by position (we considered only sales positions) and work experience (we considered only respondents who had at least three years in their current position). We contacted 638 respondents via email, asking them to participate in our survey of approximately 20 minutes in length. As an incentive, we offered the choice between a €25 donation to a good cause or a €20 voucher from an online retailer. We collected 193 usable questionnaires. Our response rate of 30.25% compares favorably to the average business survey response rate of 21% (Dillmann 2007). We examined the representativeness of our sample by testing the industry distribution of the effective sample against the industry distribution of people employed in Germany (Destatis 2018). Because a chi-square goodness-of-fit test indicated no significant differences, the sample is unlikely to be biased (χ2 = 9.31, p = .50).

We tested H1–H3 with this survey sample. To test H4, we used the established financial database AMADEUS to match the respective financial performance data for each participant. However, owing to less-than-comprehensive public disclosure requirements, we could not obtain financial performance data for many family-, foundation-, or state-owned companies. Therefore, the sample to test H4 consists of 131 matched cases. In our analytical procedure, we accounted for a potential selection bias of this subsample. An overview of the sample characteristics appears in Table 2.

Sample Overview and Structural Equivalence.

a Industry categories based on the Federal Statistical Office of Germany (Destatis 2018).

b H0: equal distribution in both samples.

Measures

We followed standard psychometric scale development procedures, generating our measurements from a review of prior literature. All measurements and the respective items are provided in Table 3. We relied on multi-item scales unless constructs of interest are concrete enough for single-item measures. Because no widely accepted measure exists for failure tolerance, we developed a new measure along our conceptual definition. Specifically, we include failure handling, failure communication, failure learning, and failure encouragement (e.g., Danneels 2008; Edmondson 1999; Van Dyck et al. 2005; Weinzimmer and Esken 2017). Thereby, we created a new, comprehensive scale and measured a failure-tolerant culture as a second-order construct. We conceptualize formal reacquisition policies as a second-order construct. In the initial step, we identify three first-order constructs based on conceptual work (Stauss and Friege 1999)—reacquisition analysis, reacquisition activities, and reacquisition monitoring. These first-order constructs are measured reflectively and then come together to form the formative second-order construct of formal reacquisition policies (Jarvis, Mackenzie, and Podsakoff 2003).

Survey Construct Measurements.

a Standardized item loadings (ILs) represent the square root of indicator reliabilities (IRs) (Bagozzi and Yi 2012).

b A robustness check revealed that eliminating this item does not affect the regression estimations.

c Part of post hoc analysis to confirm the emergence of the inverted U-shaped effect (Figure 2, Panel A) but not part of the main model

Notes: Items are based on seven-point Likert scales (1 = “do not agree at all,” and 7 = “totally agree”) unless indicated otherwise. AVE = average variance extracted; CA = Cronbach’s alpha; CR = composite reliability; N.A. = not applicable as the construct is measured with a single item.

As all existing reacquisition performance measurements refer to the relationship level, we were unable to directly use any of these measurements. Instead, we asked respondents for the average percentage of lost customers their organization is able to reacquire, which yields a so-called quasiobjective measurement.

To measure a firm’s financial performance, we used data from the AMADEUS database. We chose earnings before interest and taxes (EBIT) margin as the dependent variable because it relates to the operating profit of a firm. When studying reacquisition on the organizational level, consideration of profitability rather than other indicators such as sales volume or growth is particularly important. Customer reacquisitions will naturally trigger sales number increases by raising the sales volumes of lost customers, but most reacquisitions are also associated with company costs such as costs of reacquisition policies, price discounts, or service upgrades (Stauss and Friege 1999).

In addition, we controlled for customer orientation, employee autonomy, competition, and market intensity. “Customer orientation” refers to a company’s understanding of its customers and its continuing endeavors to create superior value for them. “Employee autonomy” refers to employees’ degree of decision-making authority (Schepers et al. 2012). “Competition” is the extent of direct competition in the market, and “market intensity” is the intensity of competitive actions (e.g., advertising campaigns) in a given market. Table 4 shows the correlations of all measures.

Descriptive Statistics and Correlations.

*p < .05.

a Obtained from an independent financial database.

Measure Validity

Measurement assessment

We conducted one confirmatory factor analysis that contained all reflectively measured first-order constructs to assess their reliability and validity. We found acceptable model fit (χ2/d.f. = 1.83; comparative fit index = .94; root mean square error of approximation = .06; standardized root mean square residual = .04). Overall, the analysis had satisfactory results: composite reliability, average variance extracted, and Cronbach’s alpha exceeded the recommended threshold values for all constructs, and all indicator reliabilities surpassed a value of .40 except for one item from the formal reacquisition policies scale that had an indicator reliability of .33 (Table 3; Bagozzi and Yi 2012). We kept this item because one item’s deviation from the .40 threshold value is still acceptable and we favored conceptual concerns over maximizing internal consistency when selecting our indicators (e.g., Bagozzi and Yi 2012; Little, Lindenberger, and Nesselroade 1999). In addition, a robustness check in which we excluded this item revealed that our results remain stable. For the regression analysis, we used the mean scores for each of the constructs. However, factor scores led to similar results.

Key informant bias

We reduced key informant concerns by preselecting only participants that had at least three years’ experience in their position (e.g., Kumar, Stern, and Anderson 1993). In addition, key informant threats are low because most of our constructs relate to the current situation of the company and are concerned with information internal to the firm. Key informants tend to evaluate those constructs accurately (Homburg et al. 2012).

However, key informants are less likely to be highly accurate when assessing cultural factors such as failure tolerance (Homburg et al. 2012). Therefore, we also established key informant accuracy. For a subsample (n = 29 companies), we were able to triangulate our measures by acquiring at least one additional respondent per company. We calculated the average absolute deviation index from the mean (ADM) to evaluate interrater agreement. ADM values for our focal independent and dependent variables fell below suggested cut-off values (Burke and Dunlap 2002), further attenuating concerns regarding a key informant bias.

Common method variance

Concerns regarding common method variance (CMV) are low because we rely on different data sources to test H4 (Rindfleisch et al. 2008) and analytical and simulation studies suggest that CMV cannot create but can only deflate quadratic (H1) and interaction effects (H3) (e.g., Siemsen, Roth, and Oliveira 2010). In addition, we further reduce CMV by separating the items for our independent and dependent variables and by eliminating common scale properties. We measured most independent variables on seven-point Likert scales, whereas we assessed our central dependent variable (reacquisition performance) in percentages. Finally, evaluating reacquisition performance requires a rather low level of abstraction as it can be verified, which further reduces CMV (e.g., Podsakoff et al. 2003; Rindfleisch et al. 2008).

In addition, we applied Lindell and Whitney’s (2001) marker test, in which the smallest correlation of a variable that is theoretically unrelated to at least one of the constructs of the model (marker variable) is a valid indicator of CMV. With this marker variable, we built an adjusted correlation matrix and tested the new correlations for significance. Specifically, we conducted this test twice with two different marker variables: year of the company’s establishment and technical turbulence, which had correlations of .01 and .06 with reacquisition performance, respectively. For the first marker variable, all prior significant correlations remained at the 5% level, and for the second marker variable, only two correlations lost significance. Thus, CMV is unlikely to affect our results. In addition, Gaussian copula terms (discussed in the next section) further reduce CMV threats (Sande and Ghosh 2018).

Results

Estimation and Identification

To test our hypotheses (H1–H4), we estimated the following equations with the two dependent variables of (1) reacquisition performance and (2) EBIT margin. As EBIT margin is available for only a subset of the survey sample from Equation 1, we separately performed regression analysis on Equation 2 to avoid loss of statistical power.

where Reac_Perf is reacquisition performance; Fail_Tolerance (Fail_Tolerance2) is failure-tolerant culture (squared); Formal_RP is formal reacquisition policies, EBIT is EBIT margin; and Controls refers to a vector of control variables that comprises customer orientation, employee autonomy, competition, market intensity, revenue dummies, and industry dummies for company i; and ∊ and φ are the residual error terms. Equation 1 also contains copula terms for failure-tolerant cultures and formal reacquisition policies (specified next). Equation 2 includes an inverse Mills ratio (specified next) and copula terms for failure-tolerant cultures, formal reacquisition policies, and reacquisition performance.

We also checked for potential multicollinearity, included Gaussian copulas to account for omitted variables, and accounted for sampling-induced endogeneity. Overall, we have strong indications that these threats do not bias the results of our study.

Multicollinearity

Multicollinearity does not seem to threaten the results of our analyses. Calculated variance inflation factors and condition indices are smaller than 5 and 10, respectively, reducing potential concerns about multicollinearity.

Gaussian copulas

Omitted variables such as a company’s competitive strategy that may equally affect independent and dependent variables may introduce endogeneity. To model correlation between the error term and potentially endogenous regressors, Park and Gupta (2012) advise including Gaussian copulas (Ebbes, Papies, and Van Heerde 2017), an instrument-free method that is increasingly popular in marketing research (e.g., Datta, Foubert, and Van Heerde 2015). Because measurement error (e.g., in the form of CMV) is also a form of endogeneity, Gaussian copulas serve as an additional remedy to alleviate CMV (Sande and Ghosh 2018).

We include

Sampling-induced endogeneity

Our matching with archival performance data could have led to sampling-induced endogeneity. We address this possibility in two ways. First, we employed χ2 goodness-of-fit tests to compare our matched subsample (n2 = 131) with the initial survey sample (n1 = 193) in industry proportions, terms of revenues, and position of respondents. The comparison did not reveal any significant differences (all ps > .30; Table 2), indicating that availability bias does not threaten the results.

Second, we employed a Heckman selection model to account further for potential sampling-induced endogeneity (Heckman 1979). Specifically, we estimated Equation 3:

In Equation 3, we included the variables from Equation 2 (specified previously) and used the availability of financial performance data (Avail_FinData; 1: “financial performance data available”) as the dependent variable. For identification, the set of independent variables driving the availability of financial performance data (Equation 3) should contain at least one variable that provides an exclusion restriction. That is, this variable affects the availability of financial performance data but does not directly influence financial performance. We included the legal form of the company (Legal_Form). The selection model supports the strength of our exclusion variable (Table 6, Model 7: bLegal_Form = 2.81, p < .01), and we include the inverse Mills ratio in our financial performance model (Equation 2). Notably, legal form does not perfectly predict financial performance data availability. In contrast to U.S. regulations, German regulations can also require disclosures from non-publicly-listed companies. Some private companies deliberately disclose information, and missing values in databases can emerge for various reasons (Breuer, Hombach, and Müller 2017).

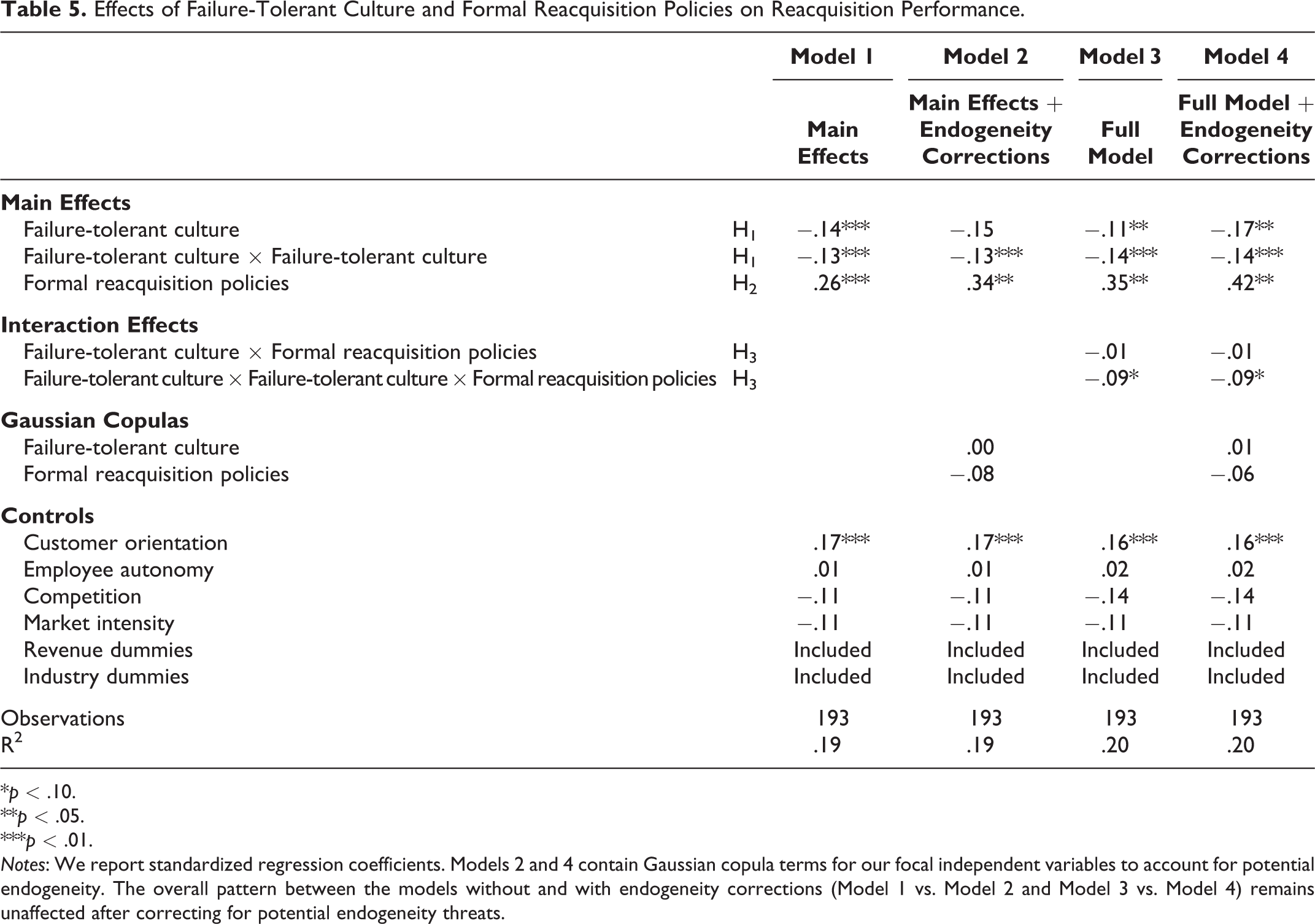

Effects of Failure-Tolerant Culture and Formal Reacquisition Policies on Reacquisition Performance.

*p < .10.

**p < .05.

***p < .01.

Notes: We report standardized regression coefficients. Models 2 and 4 contain Gaussian copula terms for our focal independent variables to account for potential endogeneity. The overall pattern between the models without and with endogeneity corrections (Model 1 vs. Model 2 and Model 3 vs. Model 4) remains unaffected after correcting for potential endogeneity threats.

Effect of Reacquisition Performance on Firm Financial Performance.

*p < .10.

**p < .05.

***p < .01.

Notes: We report standardized regression coefficients. Model 6 contains Gaussian copula terms for our focal independent variables to account for potential endogeneity. The overall pattern between Model 5 and Model 6 remains unaffected after correcting for potential endogeneity threats. For Model 7, we report the McFadden pseudo-R2 measure.

Hypothesis Testing

Failure-tolerant culture

Although reacquisition performance is measured in percent (0%–100%), we use ordinary least squares regressions to estimate Equation 1 to ease the interpretation of quadratic and interactive effects (Lambrecht and Tucker 2013; Sun, Zhang, and Zhu 2019). 4 In addition, we standardized our data before estimation. The results reveal strong support for our hypotheses. In Table 5, we report the results for H1–H3. We rely on the endogeneity-corrected models to test our hypotheses, employing Model 2 to test the main effects and Model 4 to test the interaction effects. With regard to H1—the inverted U-shaped effect—several aspects must be considered. First, the coefficient of the squared failure tolerance term is significantly negative (βFail_Tolerance2 = –.13; p < .01), which indicates the inverted U-shaped relationship. However, to validate that the inverted U-shaped effect actually exists within our data range, we tested the slope coefficients at the low end (XFail_Tolerance_low) and high end (XFail_Tolerance_high) of our data range (Haans, Pieters, and He 2016). We demonstrate a significantly positive slope at the low end of the data range (blow = βFail_Tolerance + βFail_Tolerance2 × XFail_Tolerance_low = 14.13, p < .05) and a significantly negative slope at high end of our data range (bhigh = βFail_Tolerance + βFail_Tolerance2 × XFail_Tolerance_high = –15.34, p < .01). Furthermore, the turning point of the curve lies within the data range (turning point = 4.03 [unstandardized] 5 ). Thus, the inverted U-shaped relationship is actually in our observed data range (Haans, Pieters, and He 2016). Appendix W1 illustrates this relationship.

Emergence of the inverted U-shape relationship

In an additional analysis (not reported here), we also tested the conceptual rationale underlying the inverted U-shaped relationship. In developing H1, we noted that the inverted U-shaped relationship results from the benefits of the number of failures addressed and the costs of failure severity and frequency (Figure 2, Panel A). We measured those constructs (Table 3). In line with our hypothesis development, we observe that failure tolerance positively relates to the number of failures addressed (βFail_Tolerance = .41, p < .01). We also observe that with increasing levels of failure tolerance, failure severity (βFail_Tolerance2 = .09; p < .05) and failure frequency (βFail_Tolerance2 = .09, p < .05) increase nonlinearly, resulting in a convex relationship as we predicted.

Formal reacquisition policies

Finally, we observe that formal reacquisition policies exert a positive influence on reacquisition performance (βFormal_RP = .34, p < .01). Thus, H2 is supported.

Moderating effect of formal reacquisition policies

To test the interaction effect between failure tolerance and formal reacquisition policies (Table 5, Model 4)—H3, regarding whether a turning point shift occurs in the inverted U-shaped effect of failure tolerance on reacquisition performance—simply checking significance levels of the interaction terms in the regression model is not possible (Haans, Pieters, and He 2016). Indeed, the interaction coefficients need not be significant. Instead, we need to perform two derivatives of Equation 1, which we then test for significance. First, we derive Equation 1 with regard to failure tolerance to determine the turning point, leading to Equation 4:

Second, because Equation 4 depends on the moderator formal reacquisition policies, we take its derivative to determine the direction of the turning point shift, resulting in Equation 5:

Because the denominator (Equation 5) can only be positive, the sign of the numerator indicates the direction in which the turning point shifts: a positive value of the numerator indicates a turning point shift to the right and a negative value a shift to the left. For our data, we observe a shift to the right (

On the basis of Equation 5, we further test whether this shift is significant. Specifically, we observe that Equation 5 is significantly different from zero at high (p < .05) and low values (p < .05) of the moderator, providing support for the proposed turning point shift to the right. This effect can also be illustrated by calculating the (unstandardized) turning point for a low level (turning pointFormal_RP_low = 3.76; p < .01) and a high level (turning pointFormal_RP_high = 4.18; p < .01; Δ(turning pointFormal_RP_high − turning pointFormal_RP_low) = .42; p < .01) of formal reacquisition policies. We illustrate this shift in Appendix W2 for high and low levels of formal reacquisition policies. Thus, higher levels of formal reacquisition policies allow higher levels of failure tolerance until the negative effects of failure tolerance set in.

Notably, in addition to our hypothesis, we observe a significant negative interaction between the quadratic term of failure tolerance and formal reacquisition policies (βFail_Tolerance2 × Formal_RP = −.09; p < .10). Thus, the inverted U-shaped relationship steepens with increasing levels of formal reacquisition policies. Importantly, the magnitude of the moderating effect is material: the curves appear relatively distant from each other in most of the data range. Appendix W2 demonstrates that the curves cross each other within our data range at low levels of failure tolerance whereas the upper intersection point does not lie in our observed data range, which suggests that formal reacquisition policies overall enhance the returns to failure-tolerant cultures.

More formally, we also compared the slope coefficients of failure tolerance at the lower and upper bound of our observed data range. At the lower bound, failure tolerance has stronger positive effects on reacquisition performance for high levels of formal reacquisition policies as compared with low levels (Δ(bFormal_RP_high − bFormal_RP_low) = 10.99; p < .10). However, we observe no difference at the upper bound (Δ(bFormal_RP_high − bFormal_RP_low) = −5.31; n.s.). These observations imply that formal reacquisition policies have a beneficial impact on the returns of failure tolerance for most of the observed data range. In addition, at the apex of the two curves (Appendix W2), the effect of failure tolerance on reacquisition performance is almost 1.5 times larger for companies with high than with low levels of formal reacquisition policies. Overall, our results suggest that while formal reacquisition policies cannot completely offset the negative effects of failure tolerance on reacquisition performance, they enhance the positive effects of failure tolerance.

Financial performance effects

Finally, analysis of the financial performance data (Table 6) shows that the positive relationship between reacquisition performance and financial performance is significant (Model 6: βReac_Perf = .40; p < .05). Therefore, H4 is supported.

Evaluating endogeneity

The endogeneity-corrected results in the reacquisition performance model (Table 5, Model 2 and Model 4) reveal no significant copula terms. Similarly, in the firm performance model (Table 6, Model 6) only the reacquisition performance copula term is significant (βReac_Perf_Copula = −.39; p < .05). However, in this case, endogeneity threats led only to a more conservative estimate. The estimate is even larger when accounting for endogeneity (Table 6, Model 5: βReac_Perf = .04; p < .01 vs. Model 6: βReac_Perf = .40; p < .05) while leading to the same substantive interpretation.

Post Hoc Analyses

Examining the subdimensions of failure-tolerant cultures

We further analyzed the interactions between failure tolerance and formal reacquisition policies by separately analyzing the theoretically developed dimensions of failure-tolerant cultures (failure handling, failure communication, failure learning, and failure encouragement). Appendix W3 provides the results of this post hoc study. Failure handling (Model 1: βHandling2 = −.12; p < .01), failure communication (Model 3: βComm2 = −.10; p < .01), and failure learning (Model 5: βLearning2 = −.08; p < .01) display inverted U-shaped relationships with reacquisition performance (Appendix W4). While formal reacquisition policies do not moderate the relationship of failure communication, they do affect failure handling and failure learning. Appendix W4 reveals that at low levels of formal reacquisition policies, the relationship between failure handling and reacquisition performance is rather negative; positive effects set in with higher levels of formal reacquisition policies. Specifically, at the apex of the curve, the net positive effect of failure handling on reacquisition performance is almost 1.50 times larger for companies with high versus low levels of formal reacquisition policies. The moderating effect of formal reacquisition policies becomes even more important for failure learning. While we observe an inverted U-shaped relationship between failure learning and reacquisition performance for high formal reacquisition policies, it becomes almost a null effect at low levels for formal reacquisition policies. Thus, failure learning requires formal reacquisition policies to be effective. Finally, without considering boundary conditions, failure encouragement relates linearly and negatively with reacquisition performance (Model 7: βEncourage = −.20; p < .01). However, as Appendix W4 reveals, the moderating effect of formal reacquisition policies is important: only with increasing levels of formal reacquisition policies does the effect assume an inverted U-shape, also exhibiting positive effects.

Test of competing model

We extended our hypothesized model by including failure tolerance as a driver of formal reacquisition policies. In a comparison of the model fit statistics of the hypothesized and the alternative model, the alternative model performs worse in terms of deviance (i.e., DevianceHypo_Model = 503.38 vs. DevianceAlt_Model = 995.09), Akaike information criterion (AIC) (i.e., AICHypo_Model = 515.38 vs. AICAlt_Model = 1,007.09), and Bayesian information criterion (BIC) (i.e., BICHypo_Model = 534.95 vs. BICAlt_Model = 1,026.66). In addition, failure tolerance (βFail_Tolerance = .16; n.s.) does not relate significantly with formal reacquisition policies. Therefore, this post hoc test delivers support for our hypothesized model (Table 5).

Exploring tensions between customer orientation and formal reacquisition policies

In our models, we also controlled for customer orientation, which represents another important informal element that is central to customer reacquisition management (Homburg, Hoyer, and Stock 2007). To check whether formal reacquisition policies also affect the relationship between customer orientation and reacquisition performance, we added the interaction of customer orientation and formal reacquisition policies and a copula term for customer orientation to our empirical model (Equation 1). We find a significant simple effect of customer orientation (β = .43; p < .01), but also find a significantly negative interaction effect with formal reacquisition policies (β = −.09; p < .01). Thus, formal reacquisition policies reduce the positive effect of customer orientation.

While formal reacquisition policies increase the positive effects of failure-tolerant cultures (Appendix W2), they weaken the positive effect of customer orientation on reacquisition performance. Thus, an important question is whether under some conditions formal reacquisition policies might be harmful. To gain such insights, we derived Equation 1 (including the added interaction between customer orientation and formal reacquisition policies) with regard to formal reacquisition policies (Equation 6):

We evaluated the impact of formal reacquisition policies on reacquisition performance for all possible combinations of a high versus low degree of customer orientation and failure tolerance. We observe that for high values of failure tolerance, formal reacquisition policies are always beneficial (low customer orientation: β = .46, p < .01; high customer orientation: β = .28, p < .05), suggesting their importance in failure-tolerant companies. In the situation of low failure tolerance, formal reacquisition policies are beneficial only when customer orientation is low (low customer orientation: β = .39, p < .01). However, their impact becomes insignificant when customer orientation is high (high customer orientation: β = .20, n.s.), but even in the latter situation formal reacquisition policies are not harmful for reacquisition performance.

Discussion

Two decades after Stauss and Friege’s (1999) seminal article, the field of customer reacquisition management arguably remains one of the least researched areas in customer relationship management. Prior empirical investigations of customer reacquisition management have occurred on only the customer or the customer relationship level and have implicitly assumed employees’ support during reacquisition attempts (e.g., Homburg, Hoyer, and Stock 2007). However, customer reacquisition activities can be uncomfortable, calling for employees to admit and discuss unpleasant incidents, failures, or weakness. Therefore, we took an organizational perspective (Moorman and Day 2016) and demonstrated that formal and informal organizational elements are highly relevant for reacquisition performance. We find that a failure-tolerant culture exhibits an inverted U-shaped relationship with reacquisition performance, whereas formal reacquisition policies exert a positive relationship with reacquisition performance. In addition, we observe that formal reacquisition policies enhance the link between failure tolerance and reacquisition performance. Finally, our organizational perspective allowed us to validly demonstrate the link between reacquisition performance and financial performance. Overall, our results reveal valuable insights and have important implications.

Implications for Research

The introduction of failure tolerance to the customer reacquisition literature has important implications. First, the inverted U-shaped relationship with reacquisition performance implies that failure tolerance affects reacquisition performance both positively and negatively. Regarding the positive effect of failure tolerance, a crucial avenue for future research is investigation of how companies can become more tolerant of failures. An understanding of how firms can increase their tolerance of failure is likely important for related research fields such as marketing agility (Kalaignanam, Kushwaha, and Tuli 2019), especially as the zero-defects mantra of total quality management, which may still dominate corporate philosophy, naturally conflicts with a culture that is open to failure. Future research should analyze, for instance, the effectiveness of various tactics (e.g., top management narratives that embrace failure and other cultural factors, Homburg and Pflesser 2000) to nurture a culture of failure tolerance. Regarding the negative effect of failure tolerance, our results offer a starting point for future marketing research to address the mechanisms underlying the harmful impact of failure tolerance throughout the organization.

Second, future investigators should link organization-level variables to individual reacquisition attempts. One direction would be to investigate how organization-level elements interact with a customer’s reason for defection. For instance, the effectiveness of formal reacquisition policies might depend on whether the company could control the reason for defection. Similarly, future research should explore whether the roles of informal and formal elements differ between complete and partial defections. Before defecting completely, some customers first defect only partially, by lowering their transaction volumes with the company (Coyles and Gokey 2002). In the case of partial defections, informal elements might be more pronounced, as they may cause employees to sense a threat of customer defection and initiate reacquisition processes earlier, increasing the probability of winning customers back (Thomas, Blattberg, and Fox 2004).

Third, prior research on psychological ownership has suggested that formal elements might be “not only unnecessary but also counterproductive” (Hernandez 2012, p. 173) once employees have acquired psychological ownership. Relatedly, general research on the interplay between formal and informal elements has suggested that informal aspects lead employees to ignore formal management (Grewal and Dharwadkar 2002). However, the results of our study reveal that these assumptions are too categorical. Specifically, in our context, formal reacquisition policies strengthen the positive effects of failure tolerance but weaken the positive effects of customer orientation on reacquisition performance (post hoc analysis). Thus, instead of investigating whether formal elements are counterproductive, future research should focus on when negative or positive interactive effects set in.

Relatedly, future research should examine both informal and formal aspects of customer acquisition and retention management. In this regard, the theory of psychological ownership represents a valuable starting point. For instance, drawing on this theory, marketing researchers could explore how and when informal and formal elements stimulate or reduce employees’ perceived psychological ownership of customers and explicitly study the outcomes of psychological ownership. While future research should investigate the impact of psychological ownership on in-role and extra-role behaviors, studies could also explore potential dysfunctional effects of psychological ownership. For instance, psychological ownership may result in a status quo bias (Jussila et al. 2015), leading employees to focus on current customers and eliciting resistance to customer acquisition.

Fourth, our results are the first to connect a firm’s reacquisition performance to its overall financial performance. How this positive financial impact originates is particularly interesting and should be explored in future studies. For instance, a positive relationship may occur because of the increased profitability of single-customer relationships (Kumar, Bhagwat, and Zhang 2015) but also because of reduced negative and increased positive word of mouth, resulting in gains through overall reputation (Reichheld and Sasser 1990). Understanding the origin of the performance-enhancing effect has importance for customer defection management, as it would foster development of different reacquisition strategies according to how the reacquisition of those customers may contribute to performance. For example, companies could differentiate between customers who should actually be won back (“profitability customers”) and others who should mainly be soothed, with reacquisition being subordinate (“reputation customers”).

Implications for Practitioners

Our study reveals that customer reacquisition management contributes significantly to firm performance. Therefore, the central managerial implication of our study is that managers should stimulate reacquisition activities.

Given this, managers must understand the crucial role of organizational elements for successful customer reacquisition management. In this regard, our study highlights the importance of a failure-tolerant culture. Because attempting to reacquire customers likely represents an unpleasant activity for employees, companies need to create a culture in which employees have the confidence to openly address failures. Once such a culture has been established, employees may go to greater lengths—even beyond their job duties—to win customers back.

However, the results of our study suggest that managers should also be aware of potential downsides of failure tolerance. An excessively failure-tolerant culture may suffer from a “too-much-of-a-good-thing” effect: tolerating failure is beneficial only to a certain point, beyond which a boomerang effect occurs and the negative impact outweighs the positive one. In this regard, our results reveal that failure tolerance is not a substitute for the management of reacquiring customers. Instead, management through formal reacquisition policies ensures that the boomerang effect of failure tolerance sets in only at higher levels of failure tolerance.

In this regard, for instance, our post hoc analysis reveals managerially important insights. While managers are often advised to encourage failures (e.g., Morgan 2015), we observe that failure encouragement has few positive effects unless it is accompanied by formal reacquisition policies.

Finally, our analyses reveal that formal reacquisition policies offer a powerful way to increase reacquisition performance, as the unmoderated regression coefficients (Table 5, Model 2) show a strong link between formal reacquisition policies and reacquisition performance (β = .34). In addition, our post hoc analysis reveals that positive returns of formal reacquisition policies are particularly pronounced for failure-tolerant companies. However, despite these positive effects of formal reacquisition policies, we observe that on average, companies have low levels of formal reacquisition policies (Table 4: mean value = 3.32). Consequently, our study implies that managers should increase their engagement through formal reacquisition policies.

Limitations and Avenues for Future Research

The conclusions reported here must be qualified with limitations. First, we rely on primary data. Despite our best efforts to safeguard against possible biases, such a design has limitations. Although we have addressed the issue of CMV in numerous ways, future research should employ an objective measure of company-level reacquisition performance derived from secondary data-based measurement. Second, future research might employ employee handbooks to offer more fine-grained insights into the design and effects of reacquisition policies. For instance, future investigators could examine different types of rules and how they affect the relationship between failure tolerance and reacquisition performance. Finally, our reliance on firm-level financial performance metrics is likely to have limitations. While such measures may be of interest to researchers and practitioners, they may be “causally-distant” (Katsikeas et al. 2016, p. 11) from the independent variables in our study. Therefore, we urge future researchers to explore potentially intervening performance variables.

Supplemental Material

Supplemental Material, jm.18.0016-File003 - Tolerating and Managing Failure: An Organizational Perspective on Customer Reacquisition Management

Supplemental Material, jm.18.0016-File003 for Tolerating and Managing Failure: An Organizational Perspective on Customer Reacquisition Management by Arnd Vomberg, Christian Homburg and Olivia Gwinner in Journal of Marketing

Footnotes

Acknowledgments

The authors owe special thanks to Dirk Totzek for extensive feedback and want to thank Martin Artz, Torsten Bornemann, Jenny van Doorn, Markus Glaser, Martin Klarmann, Peter Verhoef, and Simone Wies for their helpful comments on previous versions of this article. The article further benefited from a presentation at the 2018 European Marketing Academy Conference (EMAC) (Glasgow, UK) funded by the Julius-Paul-Stiegler-Memorial-Foundation and a presentation at the Annual Meeting of the Marketing Section within the VHB. Parts of the article were written while Arnd Vomberg was Assistant Professor at the University of Mannheim and Visiting Scholar at the Columbia Business School, Columbia University.

Associate Editor

Raj Venkatesan

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.