Abstract

Millions of eligible lower-income people do not apply for government benefits. Increasing interest in applying for these benefits is a crucial concern for marketers and policymakers, as the underutilization of benefits limits their effectiveness. This research proposes that expenditure reframes, descriptions translating monetary amounts into expense categories, can increase interest in government benefits. Expenditure reframes enhance a benefit's psychological value, helping consumers better understand its impact on their financial lives. Evidence from a large-scale preregistered field experiment (N = 14,267) aimed at encouraging lower-income individuals to claim a tax credit demonstrates that expenditure reframe messages increased interest, increasing visits to the claiming website. A second preregistered large-scale field experiment among Medicaid recipients (N = 71,939) identifies a boundary condition for the effect of expenditure reframes on interest. A third preregistered large-scale field experiment replicates the efficacy of expenditure reframes (N = 36,081) and highlights how the expense type featured in the reframe moderates these effects. Results from three preregistered online experiments support these findings and further elucidate the impact of expenditure reframes on psychological value. This work underscores how marketers, practitioners, and policymakers shape perceptions of government benefits and illustrates key considerations for designing effective outreach campaigns targeting lower-income households.

Keywords

Millions of eligible lower-income people in the United States do not apply for government benefits. Increasing interest in applying for these benefits is a crucial concern for many marketers and policymakers, as their underutilization poses considerable societal and economic challenges (Currie 2006; De Schutter 2022; Dubois and Ludwinek 2015). Failure to take up government benefits can decrease the financial, physical, and mental well-being of those in need (Evans and Garthwaite 2014; Hoynes, Miller, and Simon 2015; Marr et al. 2015; Nichols and Rothstein 2015). More broadly, underutilization exacerbates poverty rates, widens income inequality (De Schutter 2022; Marr et al. 2015; Sidek 2021), and hampers economic growth by curtailing consumer spending in local economies (Avalos and Alley 2010; Interlante 2022). For example, researchers estimate that $1.1 billion in unclaimed Earned Income Tax Credit (EITC) payments in 2007 cost California $1.2 billion in economic activity and 7,500 jobs (Avalos and Alley 2010).

Despite the clear advantages, underutilization of government benefits is a global and persistent problem (De Schutter 2022). In the United States, roughly 20% of eligible individuals do not claim the EITC, an unrestricted cash transfer comprising the largest poverty alleviation program in the country (U.S. Treasury Inspector General for Tax Administration 2018). Similarly, an estimated 49% of eligible lower-income women and children do not receive food assistance through the Special Supplemental Nutrition Program for Women, Infants, and Children (WIC) (U.S. Department of Agriculture 2023). This problem is not confined to the United States; underutilization of government benefits is also widespread across the European Union, where benefit programs with utilization rates below 60% are common (De Schutter 2022; Dubois and Ludwinek 2015; Van Oorschot 1991). For example, an estimated 72% of eligible lower-income individuals in the Czech Republic and 79% in Slovakia do not claim their “material need benefits,” forgoing assistance for basic needs (Dubois and Ludwinek 2015).

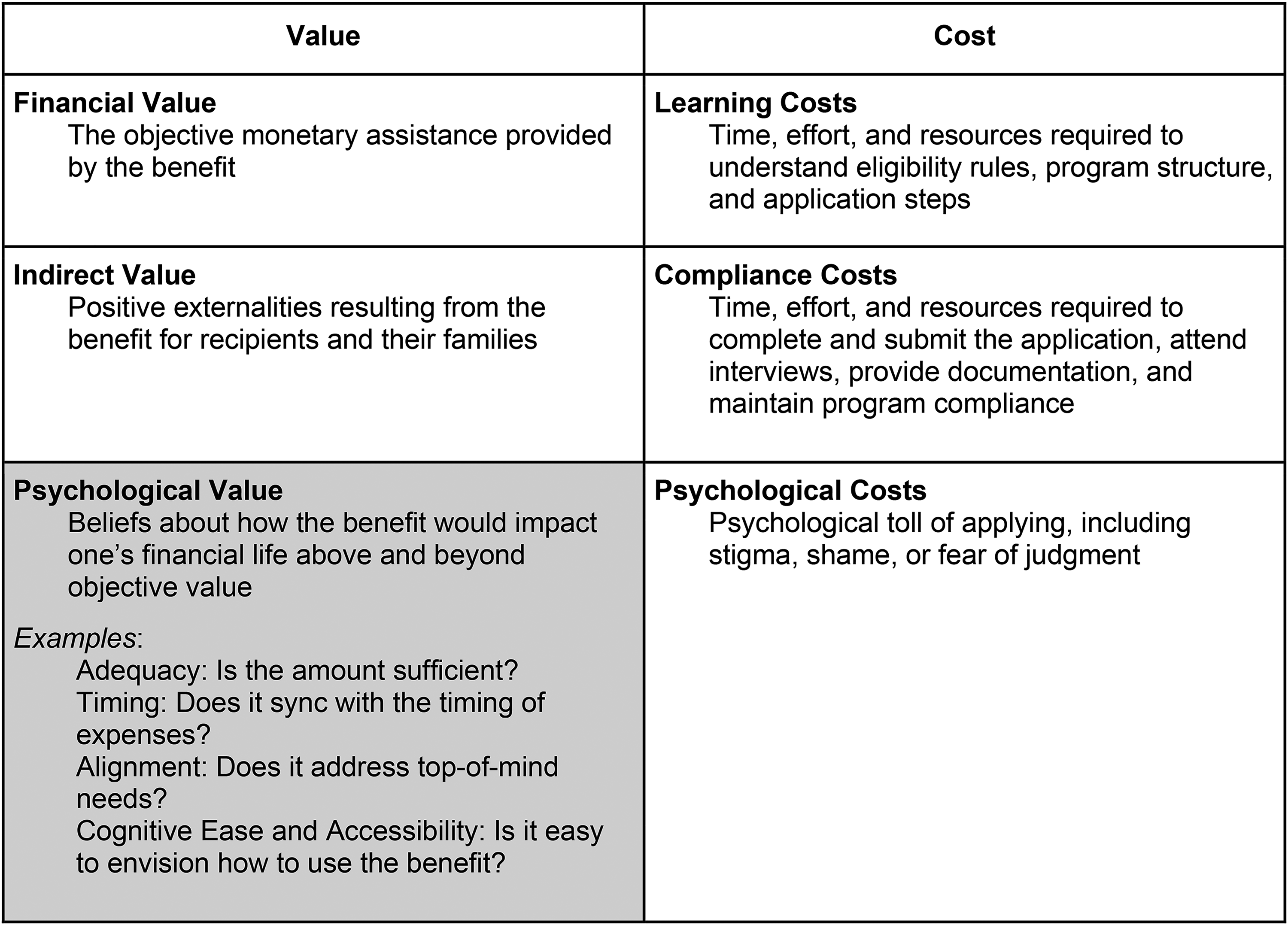

Once individuals become aware of a public assistance program, their interest in applying is shaped by the costs of obtaining the benefit relative to the value 1 of receiving it (Currie 2006; Moffitt 1983; Moynihan, Herd, and Harvey 2015). Prior research has conceptualized the costs of obtaining benefits across three primary categories: learning costs (e.g., the effort required to understand the benefit), compliance costs (e.g., the effort involved in applying for the benefit), and psychological costs (e.g., the stigma associated with applying for or receiving benefits) (Moynihan, Herd, and Harvey 2015).

We extend this cost framework and propose a complementary framework for organizing the value of government benefits into three components: financial value, indirect value, and psychological value. Financial value refers to the objective monetary assistance provided by the benefit (e.g., receiving $2,400). Indirect value captures the broader positive externalities of receiving the benefit for individuals and their families (e.g., the benefits’ positive influence on improved health or children's educational outcomes). Finally, psychological value reflects consumers’ beliefs about how the benefit would impact their financial lives (see Figure 1). Although indirect and psychological value may stem from financial value, the three are conceptually and functionally distinct. 2 We focus on psychological value because it is central to shaping benefit perceptions and is the form of value marketers are best positioned to influence.

The Expanded Value–Cost Framework for Government Benefits.

Sample Text Messages Used in Experiment 1.

Psychological value is not merely a reflection of financial value. A benefit with lower financial value can generate greater psychological value than one with higher financial value if it enables recipients to better understand its impact on their financial lives. For example, a $200 grocery benefit might carry greater psychological value than a $400 housing benefit if it covers a discrete and top-of-mind expense, such as a week's worth of groceries, and is easier for recipients to understand, visualize, and incorporate into their mental accounting of household finances. Psychological value incorporates several factors beyond financial value, including perceived adequacy (e.g., does it feel sufficient to make a meaningful difference?), timing (e.g., does it sync with the timing of my expenses or budget?), alignment (e.g., does it address salient financial concerns?), and cognitive ease and accessibility (e.g., does it simplify mental accounting? is it easy to envision how to use it?). Together, these factors underscore that even modest benefit amounts may yield substantial psychological value when communicated in ways that resonate with recipients’ lived experiences.

The need to focus on increasing the value of government benefits is particularly important given that $100 in benefits is psychologically distinct from $100 in earned income (Moffitt 1983). This discrepancy arises in part because government benefits carry unique costs that are not present with earned income, such as stigma and feelings of dependency (Moffitt 1983). Indeed, for many individuals, the value of receiving benefits does not outweigh the costs.

In examining this value–cost trade-off, one straightforward way to improve benefit uptake is simply to increase the financial value of the benefit. Unsurprisingly, people are more likely to take advantage of larger rather than smaller incentives (e.g., Dahan and Nisan 2010). Alternatively, policymakers can focus on reducing the costs associated with applying for and receiving government assistance. Accordingly, some research has focused on lowering learning and psychological costs by increasing awareness, clarifying eligibility requirements, or addressing stigma (Bhargava and Manoli 2015; De La Rosa et al. 2021; Lain and Julia 2024; Linos et al. 2022), while other work has targeted compliance costs by reducing friction and sludge in the application process, such as by making it less time-consuming, effortful, or financially burdensome (Bettinger et al. 2012; Guyton et al. 2016; Zhao, Datta, and Soman 2023). However, these seemingly straightforward approaches are often difficult to implement due to financial, political, or procedural constraints.

Considerably less research has focused on understanding how to increase the benefit's psychological value, a critical factor in driving application interest. In the current work, we address this research gap by introducing expenditure reframes, descriptions that translate a benefit's monetary amount into expense categories, as a communication strategy that marketers and policymakers could use to increase the benefit's psychological value and consequently, application interest.

Expenditure Reframes

Given the challenges of increasing benefit amounts or simplifying application processes, practitioners and policymakers have turned to marketing interventions. For example, the United Nations has encouraged member states to address benefit underutilization by developing campaigns to raise awareness and interest in government programs (De Schutter 2022). Many messages emphasize the financial value of the benefit. To increase interest in claiming the EITC, for instance, the U.S. Internal Revenue Service highlights the average credit amount: “eligible workers received an average EITC amount of $2,541” (U.S. Internal Revenue Service 2024c).

However, such messaging may fall short because it overlooks the psychological value of the benefit. Simply stating the amount does not help recipients understand how the benefit would affect their financial lives. Without additional messaging conveying psychological value, the benefit may feel abstract, disconnected, and difficult to evaluate, even though $2,541 is more than two months of pretax income for someone earning minimum wage.

Rather than promoting a tax credit as a lump sum of “$2,541,” we propose that practitioners could more effectively promote the credit using an expenditure reframe such as describing it as “enough to cover 12 weeks of groceries.” Expenditure reframes translate monetary amounts into expenditures that directly address consumers’ financial needs, helping them visualize how a benefit could tangibly support their lives. We hypothesize that expenditure reframes can increase a benefit's psychological value, and, thus, application interest. We suspect that this effect is likely multiply determined as expenditure reframes simplify mental accounting through several routes, including shaping adequacy perceptions, facilitating mental allocations, and enhancing cognitive ease and accessibility.

Consumers do not evaluate monetary amounts purely in objective terms. Instead, the psychological value of a given amount can vary widely depending on context, a foundational finding from the mental accounting literature (Heath, Chatterjee, and France 1995; Soman 2004; Thaler 1999; Tversky and Kahneman 1981; Zhang and Sussman 2017). Mental accounting is the “set of cognitive operations used by individuals and households to organize, evaluate, and keep track of their financial activities” (Thaler 1999). Consumers use mental accounting to simplify their complex financial lives. One consequence of mental accounting is that the perceived adequacy of an amount is often determined not in absolute terms, but relative to the size of the mental account considered. For example, marketers can influence whether a purchase is perceived as more or less expensive by encouraging consumers to consider it in relation to a larger or smaller account (e.g., the amount of money in their retirement savings vs. the amount of money in their wallet; Morewedge, Holtzman, and Epley 2007). Similarly, a $100 benefit is likely to have a higher psychological value when it fully covers a $100 expense than when it makes a small dent in a $10,000 expense (Kahneman and Tversky 1979).

Expenditure reframes can also simplify mental accounting by facilitating consumers’ mental allocations. By framing the benefit in terms of specific expenses, expenditure reframes help consumers allocate the funds to a new or existing mental account even in the absence of a broader budget plan. Prior mental accounting research posits that categorizing money according to expense types can make it easier for consumers to evaluate its practical value (e.g., Thaler 1999; Zhang and Sussman 2017). Expenditure reframes can also make the benefit feel more concrete by helping consumers visualize how to use the benefit. This can be beneficial given the documented positive effects of concreteness on memory, learning, and behavior (Hamilton and Rajaram 2001; Wattenmaker and Shoben 1987). Thus, expenditure reframes can help consumers better assess how the benefit supports their financial priorities by reducing the cognitive effort required to interpret the benefit, increasing its accessibility, and facilitating its integration into financial decision-making.

In line with aiding financial organization, expenditure reframes may also reduce the cognitive burden associated with managing complex financial lives. Lower-income consumers often face irregular income, fluctuating expenses, and limited slack, conditions that heighten cognitive demands (Mullainathan and Shafir 2013). By linking a monetary benefit to a concrete and familiar expense category (e.g., “enough to cover one week of groceries”), expenditure reframes can simplify decision-making and reduce the mental effort required to determine how the benefit might be used. This may also create perceived slack, both financial and psychological, by signaling that one essential category is already taken care of. Greater perceived slack can help consumers redirect their attention toward other pressing needs, thereby facilitating more effective budgeting and reducing the mental strain of managing a tight budget.

Another way to influence the psychological value of a financial incentive is by using temporal framing. For example, presenting a benefit as “$300 per month” versus “$3,600 per year” can shift how people perceive its size or adequacy, though these effects appear to depend on the amount considered (De La Rosa and Tully 2022; Goldstein, Hershfield, and Benartzi 2016; Gourville 1998). Temporal reframing may also enhance cognitive ease and accessibility, and thus increase the psychological value of a benefit, when it aligns with consumers’ mental accounting periods. For instance, De La Rosa et al. (2022) found that framing a tax credit as $300 per month (vs. $3,600 per year) increased consumers’ interest in the credit. The authors suggest that these temporal reframe effects are driven by the match between the reframe and consumers’ budgeting periods, and speculate that this match may help make the financial incentive seem more concrete and less abstract. An implicit assumption of that work is that three conditions must be met for such an intervention to be effective: (1) the consumer budgets, (2) the consumer has a salient budgeting period, and (3) the researcher can identify and target consumers based on their budget.

Although many consumers budget, not all do. Roughly one-third of U.S. consumers do not currently budget (Zhang et al. 2022), with nonbudgeters more likely to be lower-income and, by extension, more likely to qualify for government benefits. Furthermore, even among those who do budget, there is vast heterogeneity in how consumers do so, with consumers often relying on multiple budgeting strategies and budgeting periods simultaneously (Cheema and Soman 2006; Heath and Soll 1996; Zhang et al. 2022). For example, Heath and Soll (1996) found that participants frequently had different budgeting periods for different expenses, such as weekly budgets for food and monthly budgets for clothing. This diversity in budgeting highlights the complexity of using temporal reframes as a broad strategy and suggests they may need to be tailored to various financial routines and constraints, which can be difficult to implement in certain contexts.

Even though not all consumers budget, virtually all incur expenses, which can provide another meaningful context for framing financial incentives. While temporal reframes can help align benefits with budgeting practices, expenditure reframes can provide a more universally relatable context for some populations. People may care deeply about their expenses without maintaining a formal budget for various reasons, including a lack of time, ability, or willingness to engage in the tracking and monitoring that budgeting requires. Indeed, people are likely to be aware of their expenditures (when and where they spend their money) even in the absence of a structured budgeting plan. As such, expenditure reframes may offer a more reliable bridge between the benefit and the financial realities consumers navigate in their everyday lives.

The effect of expenditure reframes on psychological value is likely to be moderated by the context in which they are deployed. Practitioners can use various tactics to enhance the psychological value of a financial incentive including using temporal reframes and, as we propose, expenditure reframes. While not anticipated in our original theorizing, our findings reveal that combining multiple reframes may not produce additive gains and may instead yield diminishing marginal returns. Although each reframe can increase psychological value on its own, the impact of each successive reframe appears to diminish. This pattern may occur for several reasons, including the possibility that multiple reframes could be perceived as redundant or even overwhelming if they increase cognitive load or reduce clarity.

Furthermore, while virtually all consumers incur expenses, not all expenses carry equal weight in consumers’ minds. Expenses vary across several dimensions that influence their salience and alignment with consumers’ financial concerns, including relevance, regularity, and the degree of attention they require. Due to individual lifestyles and circumstances, not all expenses are equally relevant; some may incur childcare costs, for instance, while others may not. The regularity and predictability of an expense also contribute to its prominence in consumers’ active decision-making and financial planning. Irregular and atypical expenses are more prone to being misremembered, underestimated, or overlooked in budgeting (Howard et al. 2022; Sussman and Alter 2012). Finally, expenses requiring frequent monitoring and decision-making are more likely to be top-of-mind, while “set and forget” expenses, such as automatic payments, are typically less salient. When expenditure reframes align with consumers’ salient expenses, they may increase the benefit's psychological value.

Given these factors, we propose that food expenditures represent a uniquely prominent expense category for most consumers. Food is a universal necessity, a frequent and recurring expenditure, and a category that requires daily decision-making and planning. In a nationally representative study, when asked to report their budget categories, consumers listed food more than any other category, including housing (Zhang et al. 2022). It is also the category where consumers most frequently report overspending (Marder 2023; O’Brien 2019; Slickdeals 2019). Based on these insights, we expect that expenditure reframes focused on food expenses may be particularly effective.

Overview of Experiments

We tested these propositions across six experiments, including three large-scale field experiments among lower-income populations. We first examined the effect of adding expenditure reframes to marketing messages targeting lower-income individuals likely eligible for the EITC (Experiment 1; N = 14,267). Expenditure reframes increased interest in claiming the EITC, as measured by consumers’ actual behavior: specifically, whether they visited an EITC-claiming website and initiated the claiming process. An online experiment with lower- to moderate-income participants supports these findings, demonstrating that expenditure reframes enhance the psychological value of a proposed benefit (Experiment 2; N = 293).

We then assessed the effectiveness of expenditure reframes in a restricted cash transfer context among lower-income parents in Louisiana eligible for food assistance through WIC (Experiment 3; N = 71,939). We tested the efficacy of including expenditure reframes in marketing messages on people's propensity to call their local WIC office and ultimately enroll in the program. This experiment revealed an unexpected but important boundary condition for the effectiveness of expenditure reframes. Adding expenditure reframes to a temporally reframed amount did not increase interest in claiming WIC benefits. A follow-up online experiment with lower- to moderate-income people supports this conclusion by exploring the psychological value of the benefit as a function of expenditure and temporal reframes (Experiment 4; N = 1,197).

We further investigated the efficacy of expenditure reframes in driving interest in claiming government benefits while also exploring how the type of expense considered in the reframe moderates these effects (Experiments 5; N = 36,081). This large-scale field experiment replicated the main effect of the expenditure reframe used in Experiment 1 and highlighted the moderating role of expense type. Finally, another online experiment with lower- to moderate-income individuals complements these findings by showing that the type of expense mentioned in the reframe is an important moderator of psychological value (Experiment 6; N = 599).

The results from all experiments are summarized in Figures 3–8. We preregistered our hypotheses, study designs, and planned analyses for all experiments. We report all measures and did not exclude any participants from our analyses unless specified in the preregistration. All anonymized data, preregistrations, online experiment materials, and analysis scripts are publicly available on ResearchBox (https://researchbox.org/3689). Due to the sensitive nature of the field experiment data and in accordance with agreements with our field partners, individual-level covariates cannot be made publicly available.

Expenditure Reframes Boost Visits and “Get Started” Clicks on the EITC-Claiming Website (Experiment 1).

Expenditure Reframes Increase Psychological Value (Experiment 2).

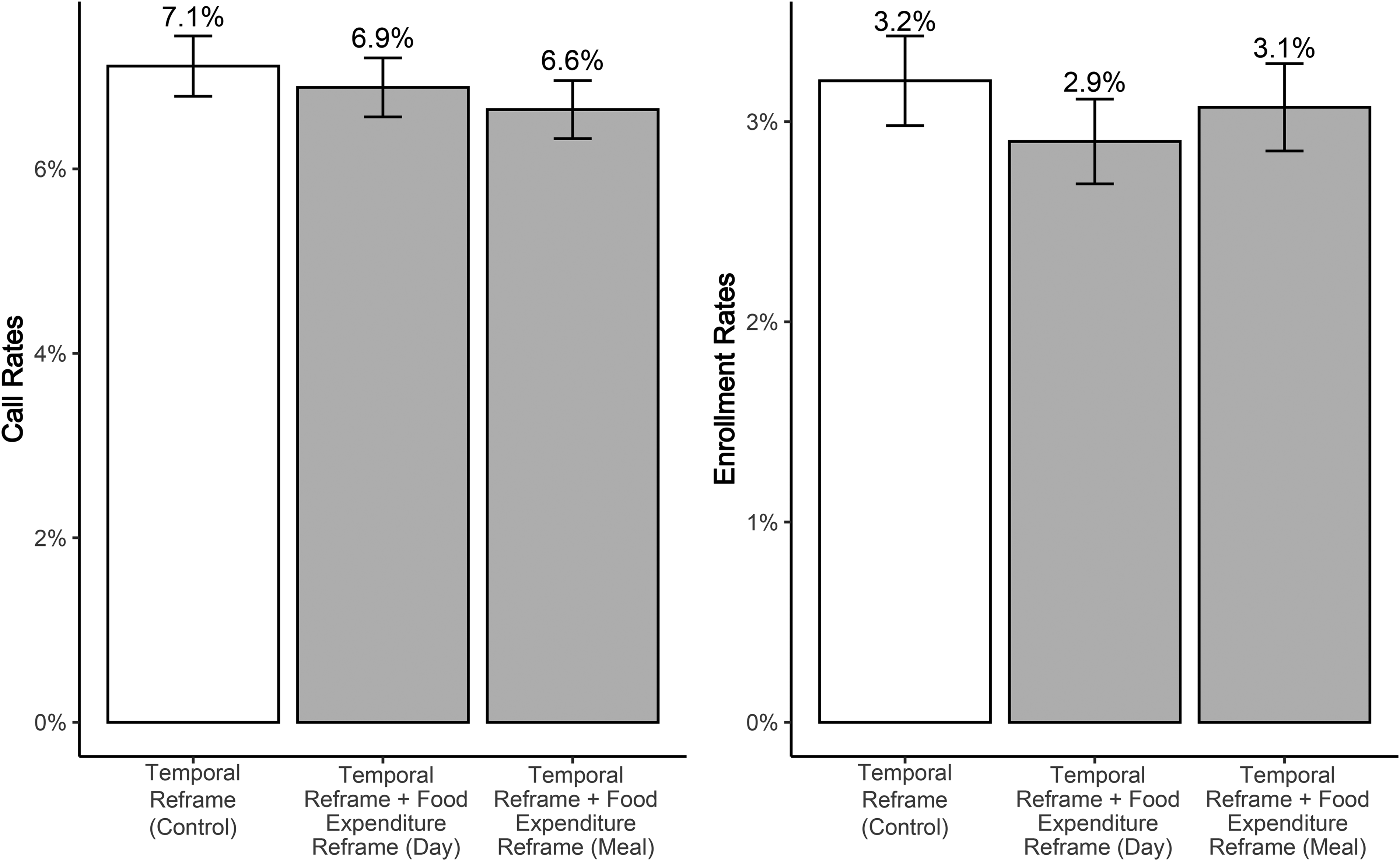

Combining Expenditure and Temporal Reframes Does Not Increase Call Rates or Final WIC Enrollment (Experiment 3).

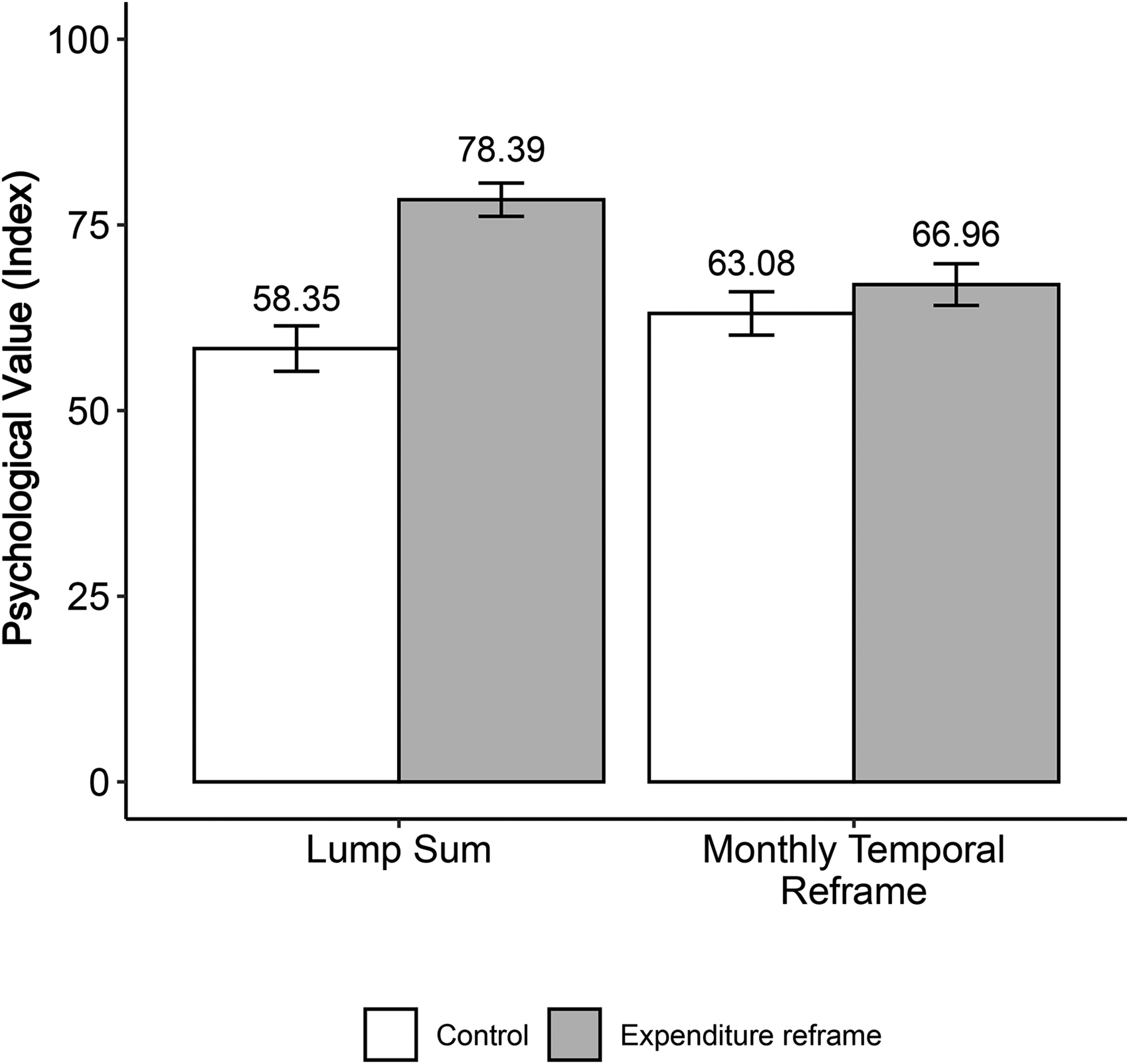

Temporal Reframes Moderate the Effect of Expenditure Reframes on Psychological Value (Experiment 4).

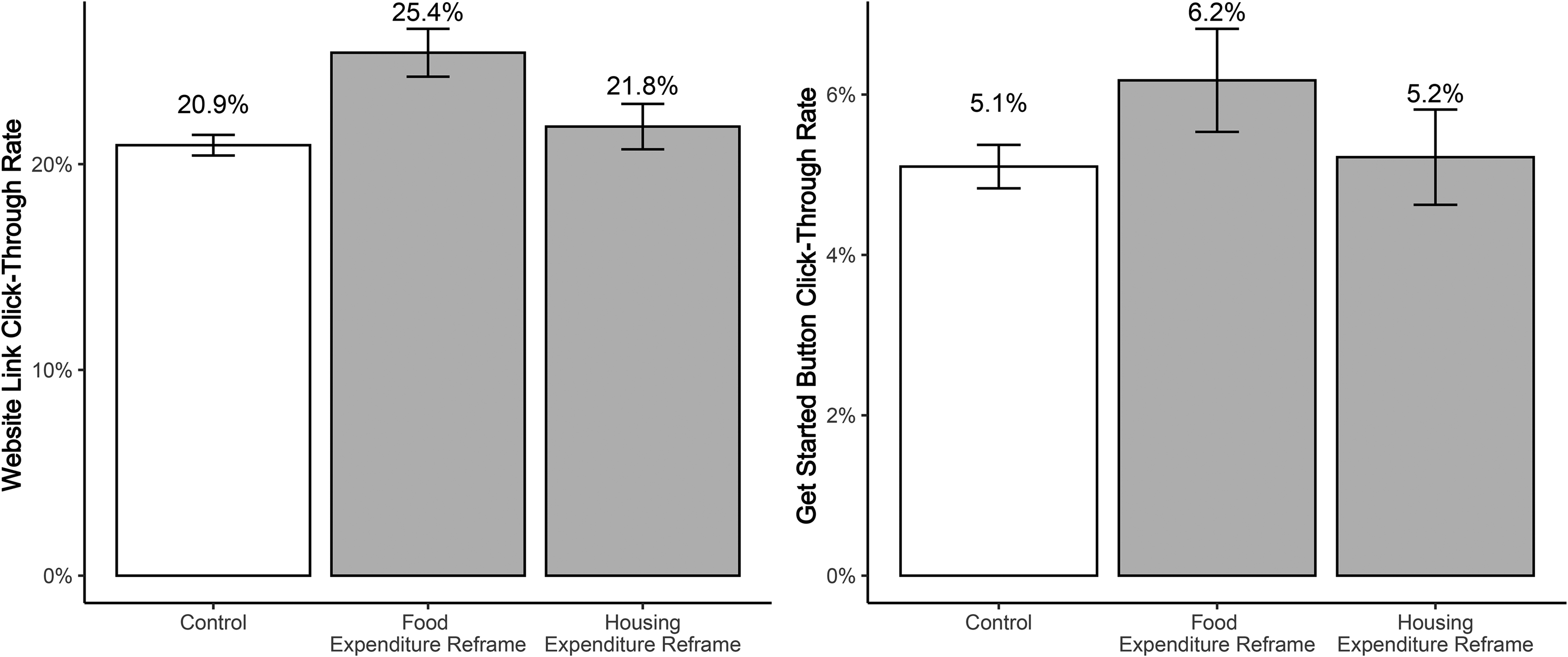

Moderating the Effect of Expenditure Reframes on Visits and “Get Started” Clicks on the EITC-Claiming Website (Experiment 5).

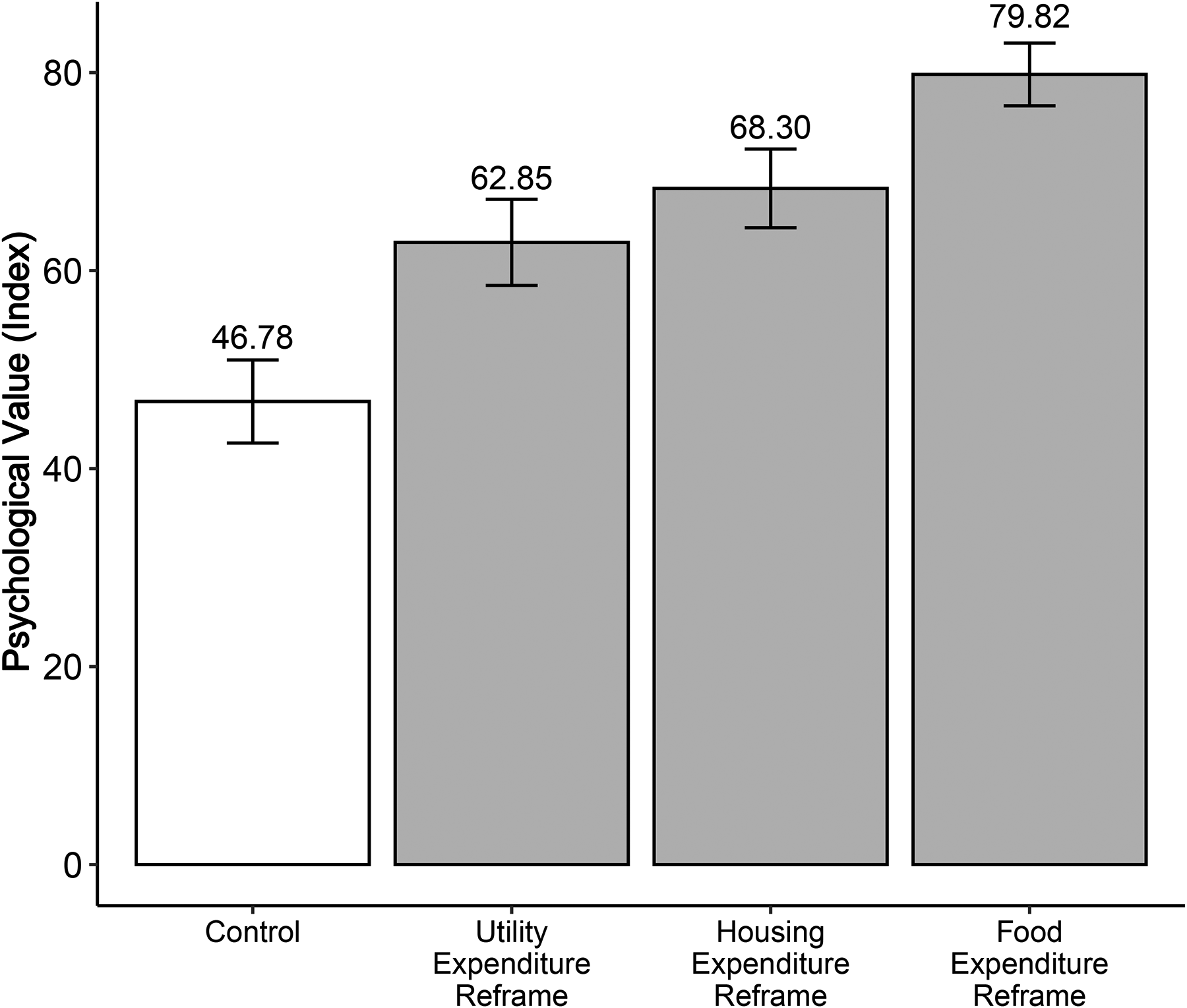

Expense Type Moderates the Effect of Expenditure Reframes on Psychological Value (Experiment 6).

Experiment 1: Adding Expenditure Reframes Increases Interest in Claiming the EITC

This study aims to test in the field whether adding expenditure reframes to marketing messages about a government benefit can increase consumers’ interest in claiming it. To do this, we partnered with a nonprofit organization (NPO). The NPO conducted a large-scale experiment messaging lower-income people likely eligible for the EITC. Across two outcome variables, we measured consumers’ interest by observing their actual online behavior: (1) whether they clicked the link in the text message and visited the EITC-claiming website, and (2) whether they clicked the “Get Started” button on the homepage of the website to start the claiming process.

This experiment was part of a larger investigation by the NPO and 17 research teams (De La Rosa et al. 2024) in which participants received a control message or one of three treatment messages, one of which was an expenditure reframe message. The current investigation exclusively focuses on the comparison between the expenditure reframe message and the control.

Empirical Context and Method

The EITC is one of the largest federal tax credit programs in the United States, aimed at supporting working people with low to moderate income, especially those with children. Established to reduce poverty and incentivize employment, the EITC functions as a refundable tax credit, so if the credit exceeds the taxes owed, the recipient obtains the difference as an unrestricted cash payment. Thirty states, including California, have their own EITC programs to supplement the federal EITC. Twenty-three million workers and their families benefited from the EITC in 2023, receiving an average credit of $2,541 (U.S. Internal Revenue Service 2024d).

Eligibility for the EITC is based on income, household size, and filing status. The credit is structured progressively, increasing with earned income up to a maximum threshold, remaining constant at that level, and then phasing out as income rises further, effectively targeting lower earners. For instance, in tax year 2022, a married couple with three or more children could qualify for the EITC with a maximum income of $59,187, with the highest credit amount set at $6,935 (U.S. Internal Revenue Service 2024b).

The EITC is not automatically applied; eligible workers must actively claim it when filing taxes. This requirement presents a significant barrier, particularly for lower-income households not required to file taxes. For example, an individual with two children earning $20,000 a year (more than the annual income of a full-time U.S. minimum wage worker) is not obligated to file taxes (U.S. Internal Revenue Service 2024a). However, if they do not file, they forgo a potential EITC of $6,604. Due to these and other barriers, approximately 20% of eligible lower-income workers do not claim the EITC, collectively forfeiting an estimated $7.3 billion every year (U.S. Treasury Inspector General for Tax Administration 2018). Recognizing that those who would benefit most from the EITC are among the least likely to claim it, the NPO launched a targeted marketing campaign aimed at individuals with lower incomes who may not have filed taxes. The campaign encouraged these individuals to visit a free tax-filing and EITC-claiming website.

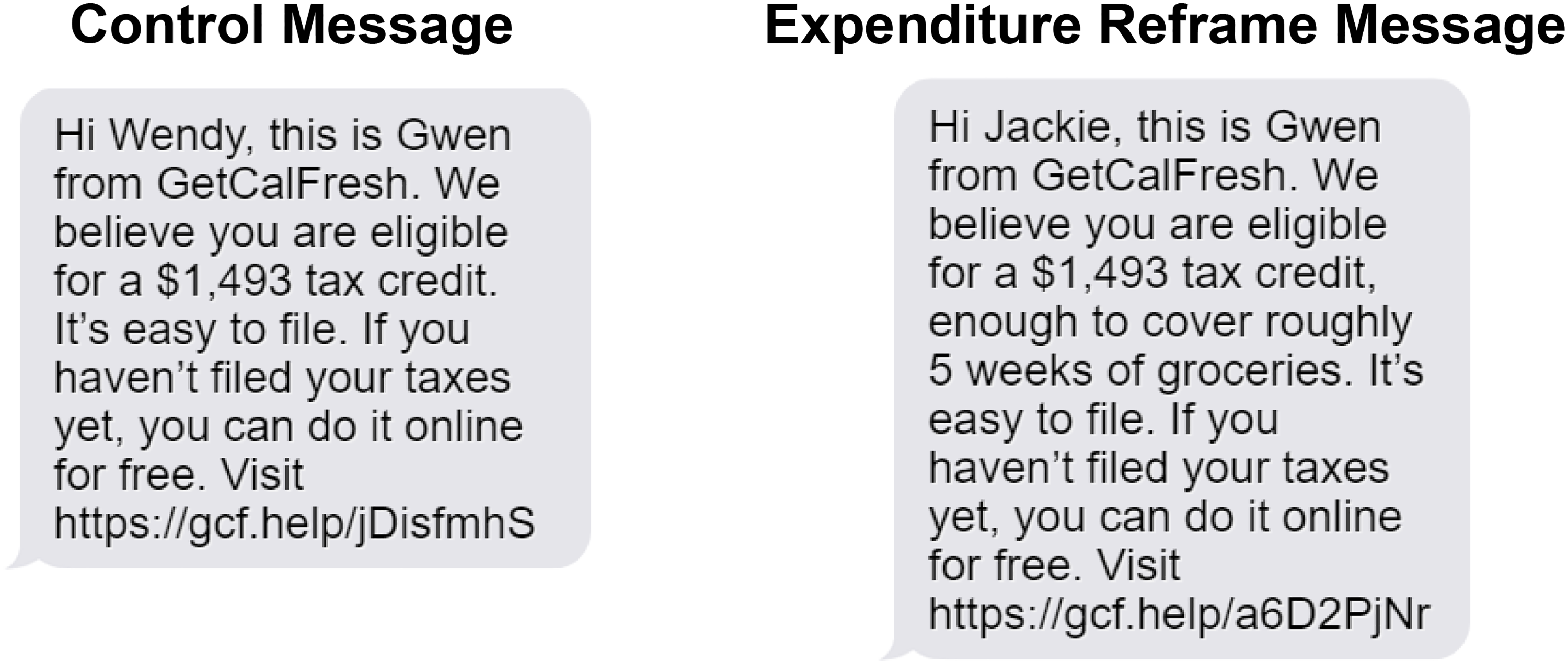

The NPO sent text messages to 30,000 lower-income Californians who had previously applied for CalFresh, California's food assistance program, through the GetCalFresh.org portal and were likely eligible for at least $250 in combined state and federal EITC. Recipients were sent a personalized text message from the NPO, including their name, expected EITC benefit amount, and a link to the EITC-claiming website. EITC amounts were calculated using the California Franchise Tax Board Earned Income Tax Calculator, based on individuals’ household income and composition reported in their prior GetCalFresh application. For this calculation, we assumed all message recipients had a social security number or a tax identification number, no investment income, had lived in California for more than six months, and could not be claimed as a dependent on someone else's tax return (California Franchise Tax Board n.d.).

Participants received a control message or one of three treatment messages, including an expenditure reframe message. In this work, we focus exclusively on the comparison between the control and the expenditure reframe messages (N = 15,000). This study was preregistered on AsPredicted.org (https://aspredicted.org/KJ8_ZN2).

The control message, which the NPO refined over years of testing, read: “Hi [First Name], this is Gwen from GetCalFresh. We believe you are eligible for a [Amount] tax credit. It's easy to file. If you haven’t filed your taxes yet, you can do it online for free. Visit [Website].” The expenditure reframe message added eight words: “Hi [First Name], this is Gwen from GetCalFresh. We believe you are eligible for a [Amount] tax credit, enough to cover roughly [X] weeks of groceries. It's easy to file …” (see Figure 2 and Web Appendix for more details on the expenditure reframing methodology and conversions used across experiments).

We measured participants’ interest in claiming the EITC in two ways. First, we measured whether they clicked on the link provided and visited the EITC-claiming website. Second, we measured a more downstream signal: whether they clicked on the “Get Started” button on the website's homepage. The only way participants could start the claiming process on the website was by clicking on the “Get Started” button.

Results

Sample and balance checks

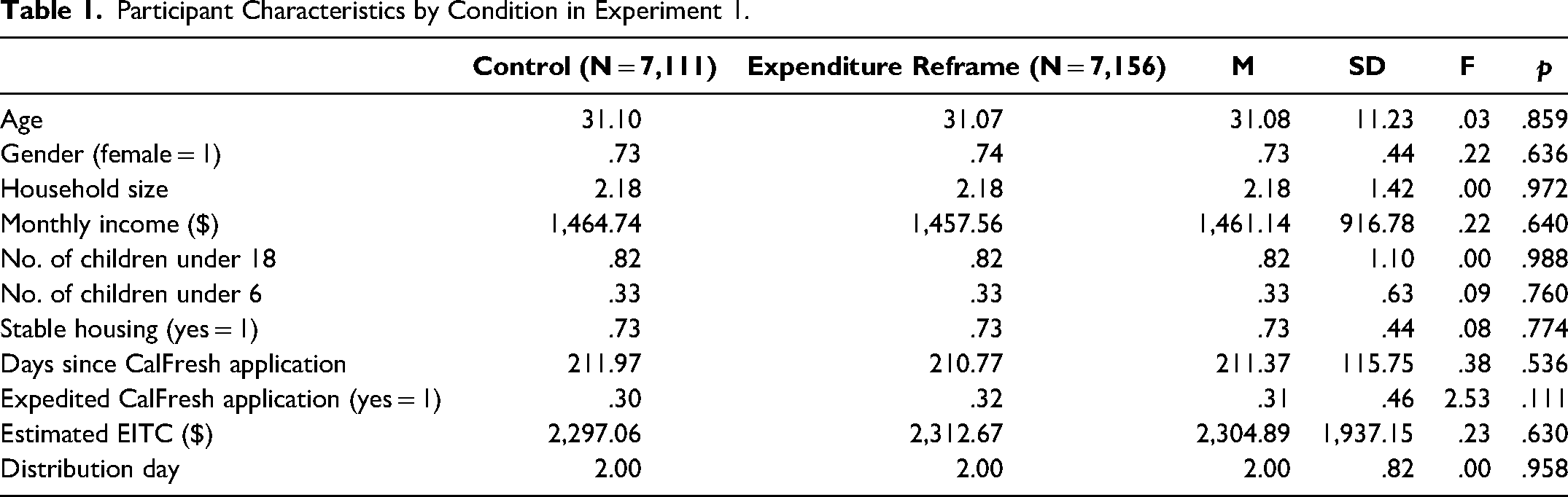

Due to undelivered text messages and disconnected phone numbers, 14,267 individuals (95.11% of those messaged) successfully received either the control or expenditure reframe message. The conditions were properly balanced across the observable person-level covariates: age, gender, household size, monthly income, number of children under 18, number of children under 6, stable housing, number of days since their CalFresh application, whether their CalFresh application was expedited (a measure of extreme need), and the estimated EITC amount (see Table 1).

Participant Characteristics by Condition in Experiment 1.

The message recipients were primarily young, lower-income women with an average monthly income of $1,461 and an estimated EITC of $2,305. This estimated EITC amount was substantial for this population; for more than 67% of the sample, their estimated EITC was more than their reported monthly income.

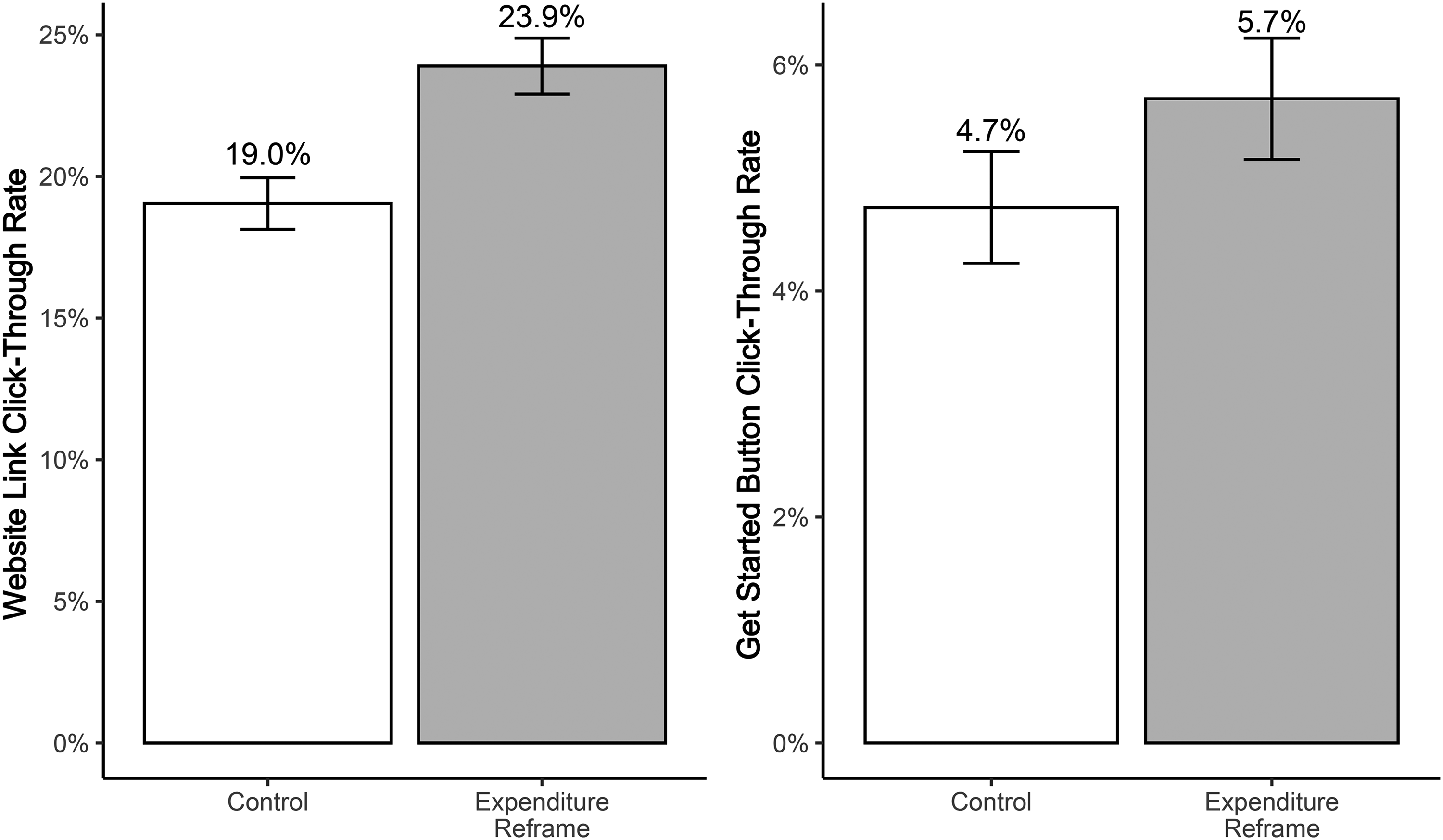

EITC interest

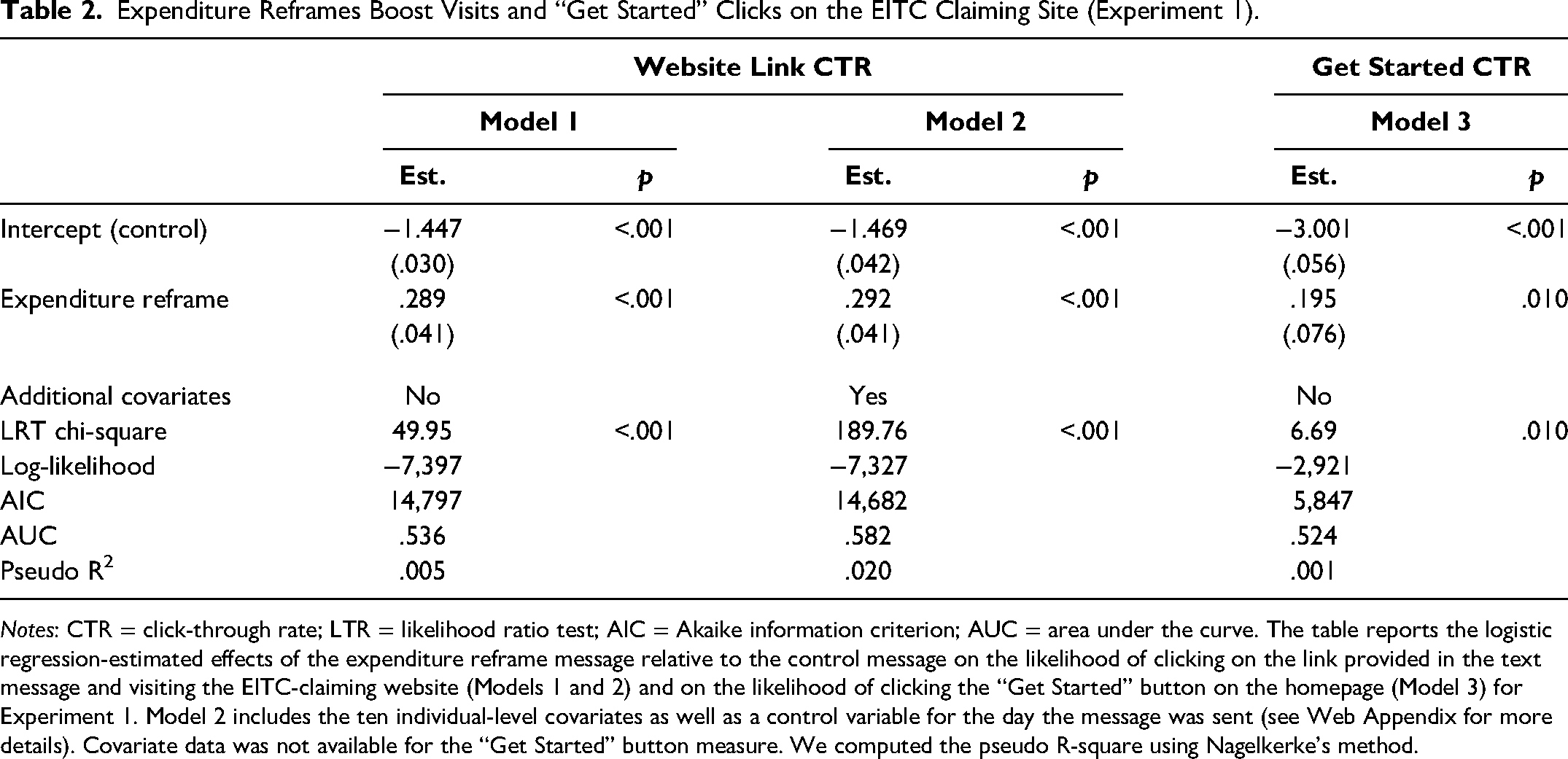

As expected, the expenditure reframe condition increased participants’ interest in claiming the EITC. Compared with the control message, the expenditure reframe message increased the percentage of participants who visited the EITC-claiming website from 19.0% to 23.9% (b = .29, SE = .04, z = 7.05, p < .001, Cohen's h = .12; see Figure 3). The expenditure reframe message also significantly increased the percentage of participants who began the claiming process from 4.7% to 5.7%, as measured by the percentage of message recipients who clicked on the “Get Started” button on the homepage (b = .20, SE = .08, z = 2.58, p = .010, Cohen's h = .04). These findings are robust to the exclusion or inclusion of covariates (see Table 2 and Web Appendix for more details).

Expenditure Reframes Boost Visits and “Get Started” Clicks on the EITC Claiming Site (Experiment 1).

Notes: CTR = click-through rate; LTR = likelihood ratio test; AIC = Akaike information criterion; AUC = area under the curve. The table reports the logistic regression-estimated effects of the expenditure reframe message relative to the control message on the likelihood of clicking on the link provided in the text message and visiting the EITC-claiming website (Models 1 and 2) and on the likelihood of clicking the “Get Started” button on the homepage (Model 3) for Experiment 1. Model 2 includes the ten individual-level covariates as well as a control variable for the day the message was sent (see Web Appendix for more details). Covariate data was not available for the “Get Started” button measure. We computed the pseudo R-square using Nagelkerke's method.

Heterogeneity analysis

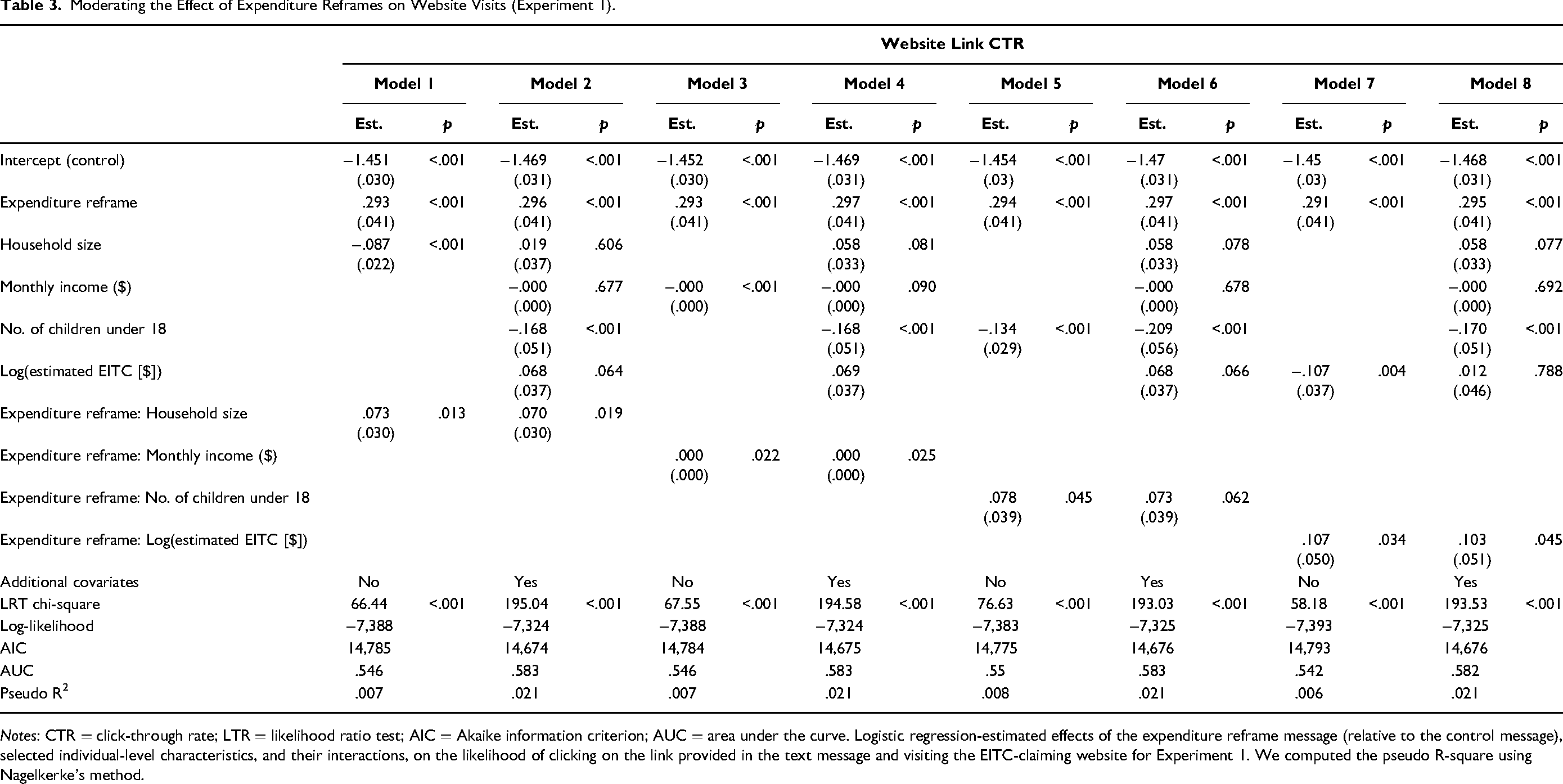

As an exploratory analysis, we examined whether any of the individual-level covariates moderated the effect of expenditure reframes. Expenditure reframe messages were more effective among individuals with larger households, more children, greater monthly incomes, and greater EITC estimates (log-transformed due to skewness) (see Table 3). By design, up to a certain level, individuals with larger households, more children, and greater incomes receive a larger EITC payment. Correspondingly, these variables are highly correlated with one another (see Web Appendix). An exploratory principal component analysis confirmed that a factor that mostly related to consumers’ household size, number of children, income, and EITC estimates moderated the effect of expenditure reframes on click-through rates (b = .06, SE = .02, z = 2.61, p = .009; see Web Appendix). No other individual-level covariate or principal factor significantly moderated the effect of expenditure reframe on EITC interest.

Moderating the Effect of Expenditure Reframes on Website Visits (Experiment 1).

Notes: CTR = click-through rate; LTR = likelihood ratio test; AIC = Akaike information criterion; AUC = area under the curve. Logistic regression-estimated effects of the expenditure reframe message (relative to the control message), selected individual-level characteristics, and their interactions, on the likelihood of clicking on the link provided in the text message and visiting the EITC-claiming website for Experiment 1. We computed the pseudo R-square using Nagelkerke's method.

Discussion

This experiment highlights the effectiveness of expenditure reframes in increasing interest in claiming government benefits, demonstrated within a meaningful, real-world context among lower-income individuals likely eligible for the benefit. By adding only eight words to the marketing message, interest in claiming the EITC among lower-income individuals rose by 4.9 absolute percentage points, reflecting a 25% relative increase above the control. These effects seemed to be strongest for those with the combination of factors that lead to larger EITC benefits (e.g., larger households, greater incomes).

Experiment 2: Expenditure Reframes Increase the Benefit's Psychological Value

We propose that expenditure reframes enhance the psychological value of the benefit. To test this proposition directly, we conducted Experiment 2 in a controlled online setting among lower- to moderate-income individuals.

Method

We recruited 302 participants from Prolific Academic, using Prolific filters to target individuals with annual household incomes below the U.S. median of $80,000 (U.S. Census Bureau 2024). This study was preregistered on AsPredicted.org (https://aspredicted.org/ht8k-gwj6.pdf).

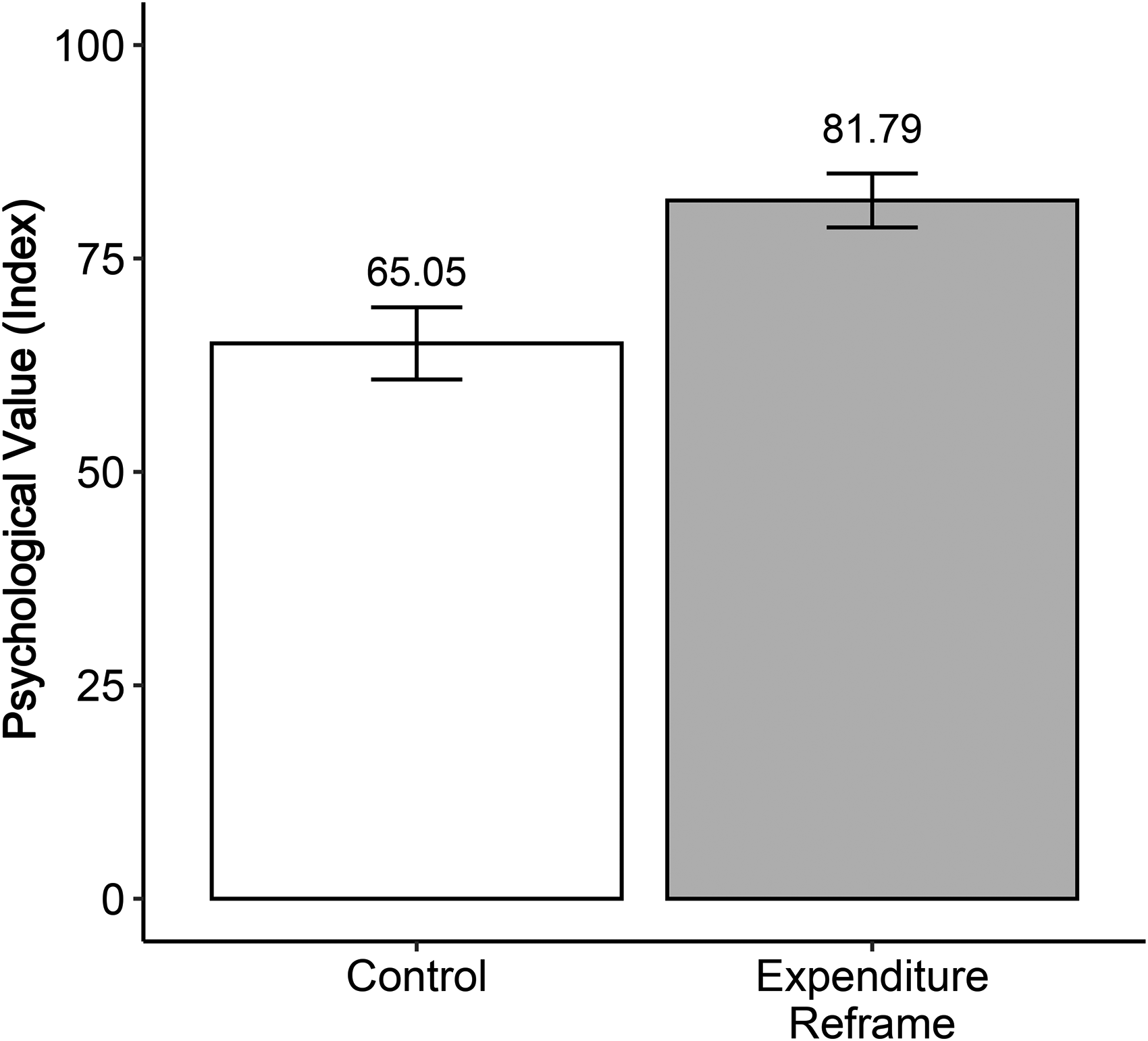

Participants were randomly assigned to one of two conditions in this between-subject experiment: a control condition or an expenditure reframe condition. All participants read the following prompt: “A nonprofit you have worked with in the past recommends a government benefit program to you that helps people cover their food costs. They describe the program as follows…” In the control condition, the benefit was described as “People can receive $2,400.” In the expenditure reframe condition, the benefit was described as “People can receive $2,400, which can roughly cover 12 weeks of groceries for an average family.”

Participants then rated their level of agreement with six statements regarding the psychological value of the benefit on a 101-point scale (0 = “strongly disagree,” and 100 = “strongly agree”) presented in a random order. Specifically, “To what extent do you agree or disagree with the following statements…” (1) “Based on the way this benefit is described, this benefit would have a meaningful impact on my financial life,” (2) “Based on the way this benefit is described, this benefit would be very useful to me,” (3) “This description helps me picture how to use the benefit,” (4) “This description helps me understand in a very real way how useful the benefit could be,” (5) “This description helps me understand how the benefit could help with one's budget,” and (6) “This description helps me consider the value that the benefit would provide over time.”

Finally, participants reported their demographic information, including age, gender, ethnicity, education, and household income.

Results

As preregistered, we excluded responses from participants who (1) failed an initial attention check question before starting the study (e.g., “How many legs does a typical fish have?”), (2) circumvented our duplicate response prevention measures and participated in the survey more than once, or (3) did not complete the study. We used the same exclusion criteria across all online experiments.

A total of 296 participants were included in the final sample (48.99% female, 47.97% male, 2.36% other, .68% preferred not to answer; Mage = 37.98 years, SD = 12.23). Our income targeting was largely effective, with over 91% of the sample reporting annual household incomes below $80,000.

We analyzed how the expenditure reframe condition influenced psychological value by combining the six items into an index (α = .92; all items loaded onto one factor in an exploratory factor analysis). As expected, relative to the control, expenditure reframes increased the benefit's psychological value (Mcontrol = 65.05, SD = 25.78 vs. Mreframe = 81.79, SD = 19.95, d = .73; b = 16.74, SE = 2.67, t(294) = 6.27, p < .001; see Figure 4). These effects were robust. Expenditure reframes increased psychological value even when we excluded the 8.8% of participants with reported household incomes above the U.S. median (b = 16.54, SE = 2.82, t(268) = 5.86, p < .001, d = .71), focused on lower-income participants with reported annual household incomes of less than $40,000 (b = 18.02, SE = 3.61, t(141) = 5.00, p < .001, d = .84), or analyzed each measure individually (all ts > 2.42, all ps < .016, all ds > .28; see Web Appendix for more details).

Discussion

The results of Experiment 2 provide evidence that expenditure reframes enhance the psychological value of a benefit. In a controlled online setting, lower- to moderate-income participants exposed to expenditure reframes viewed the benefit as significantly more valuable compared with those in the control condition. Together with the findings from Experiment 1, these results underscore the importance of expenditure reframes as an effective tool in government benefit communications, suggesting that such reframes can play a key role in increasing program interest among target populations.

Experiment 3: Adding Expenditure Reframes to a Temporally Reframed Benefit Does Not Increase Interest in WIC

Thus far, we have demonstrated that expenditure reframes can increase consumers’ interest in claiming a government benefit. In this experiment, we examined whether adding expenditure reframes could enhance marketing messages that already utilized temporal reframes. To do so, we partnered with Louisiana's Bureau of Nutrition Services (BONS) and Benefits Data Trust (BDT), an organization that worked to connect people with government benefits, to conduct a large-scale experiment messaging lower-income people eligible for WIC. Participants received a control message that used a monthly temporal reframe (as is the standard distribution frequency for WIC benefits) or one of two intervention messages that added an expenditure reframe to the control message. We assessed consumers’ interest in the benefit through their actual behavior: (1) whether they called the number provided in the text message, which connected them to their nearest WIC office, and (2) whether they enrolled in the WIC program. Thus, this new field context allowed us to test the effect of expenditure reframes in the presence of another reframe description.

Empirical Context and Method

WIC is a federally funded program established in 1974 to “safeguard the health of low-income women, infants, and children up to age five who are at nutritional risk” (U.S. Department of Agriculture 2024c). WIC provides recipients with food assistance, nutrition education and counseling, and referrals to other health, welfare, and social services. In 2023, WIC served approximately 6.6 million participants each month, supporting 39% of all infants in the United States (U.S. Department of Agriculture 2024d).

WIC food benefits are restricted cash transfers that can only be used to purchase specific foods, such as formula, milk, eggs, and cereal. For example, the maximum monthly WIC allowance for a one-year-old includes a 64-ounce jar of juice, a 12-quart carton of milk, 36 ounces of cereal, one dozen eggs, $26 in fruits and vegetables, 24 ounces of whole wheat bread, 6 ounces of canned fish, and one pound of legumes (U.S. Department of Agriculture 2024b). Other food items cannot be purchased with WIC funds. The benefits are distributed through a special Electronic Benefit Transfer (EBT) card, which can only be used at certain retailers.

Receiving WIC has been associated with a wide range of positive outcomes, including lower rates of premature births, fewer infant deaths, reduced health care costs, and improved child development outcomes (U.S. Department of Agriculture 2024a). However, like the EITC, WIC benefits are not automatically applied; individuals must apply for WIC and be assessed by a health care professional for nutritional risk. Unlike other programs, WIC applications cannot be completed online. Applicants must schedule and attend an in-person appointment at a WIC clinic, a barrier that likely contributes to the fact that roughly 49% of eligible individuals do not receive WIC benefits (U.S. Department of Agriculture 2023).

To help address this gap, BDT conducted a targeted marketing campaign, messaging 93,345 lower-income Louisiana parents with children under five enrolled in Medicaid who were likely eligible for WIC and connecting them to their local WIC office. These Medicaid enrollees met the income criteria for WIC benefits, making them a prime audience for outreach. We preregistered this study on AsPredicted.org (https://aspredicted.org/3QT_P2J).

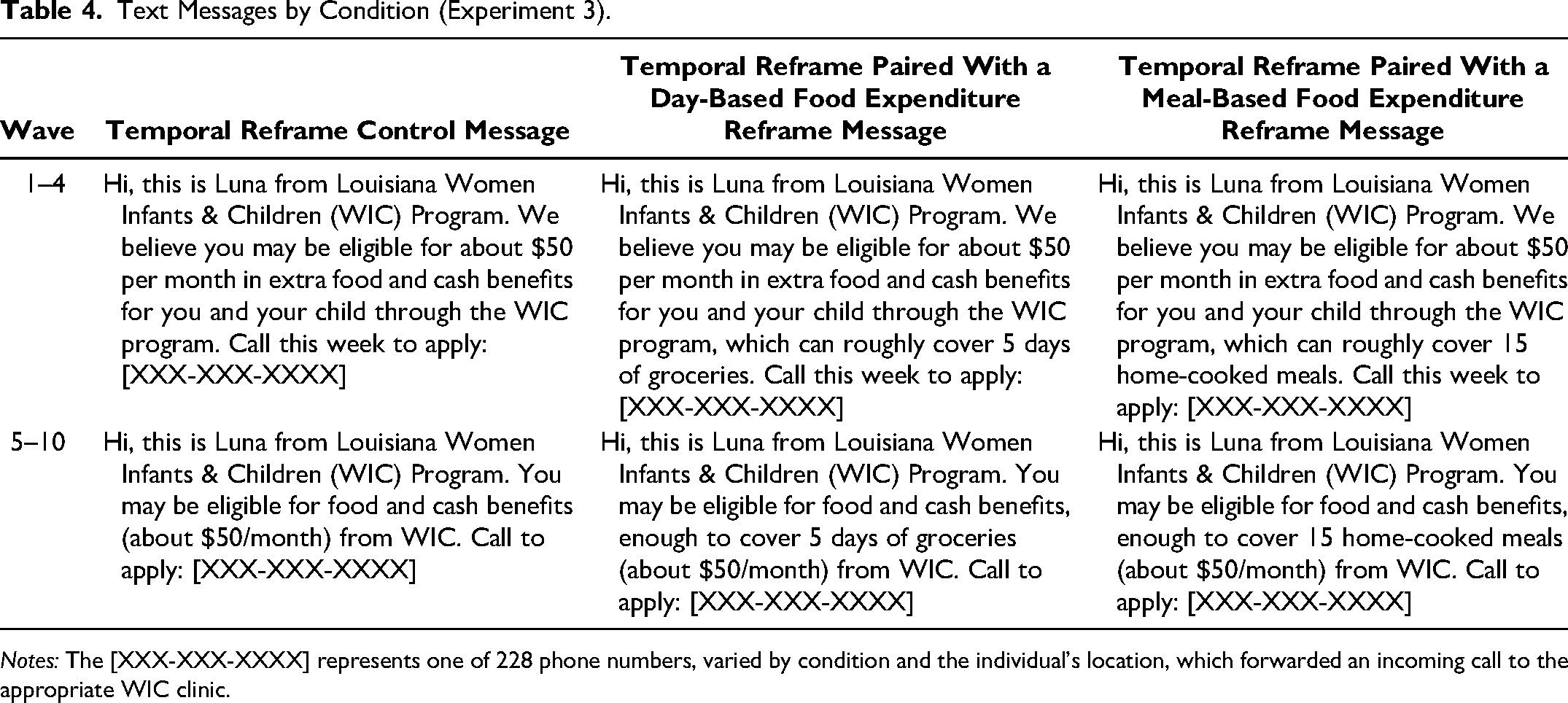

Parents were randomly assigned to one of three message conditions: a temporal reframe control message, a temporal reframe paired with a day-based food expenditure reframe message, or a temporal reframe paired with a meal-based food expenditure reframe message (see Table 4). The control message informed recipients that they were likely eligible for approximately $50 in monthly benefits through WIC and encouraged them to call their local WIC clinic. The two treatment messages added a food expenditure reframe: the day-based reframe described the benefit as covering “5 days of groceries” and the meal-based reframe described it as covering “15 home-cooked meals.”

Text Messages by Condition (Experiment 3).

Notes: The [XXX-XXX-XXXX] represents one of 228 phone numbers, varied by condition and the individual's location, which forwarded an incoming call to the appropriate WIC clinic.

This messaging campaign was spread across ten waves to avoid overwhelming the WIC clinics with a large influx of calls at one time. Waves were balanced across the available covariates (see Web Appendix). Every Monday morning for ten weeks, an initial text message was sent to a new segment of the sample. Those who had not yet called their WIC clinic received up to two reminder texts over the next two weeks, also sent on Monday (see Web Appendix for reminder message details). As indicated in Table 4, the messages were shortened across all conditions for waves 5–10 to reduce “spam” filtering by recipients’ phone carriers.

Each message contained one of 228 phone numbers, which varied by condition and by each of the 76 local WIC clinics that participated in the study, as determined by BONS. Calls were automatically directed to the appropriate clinic, enabling BDT to track call rates by clinic and condition as a direct result of our messaging campaign.

Our first outcome variable was the percentage of message recipients who used the phone number included in the text message to call their local WIC clinic; this is a direct measure of participants’ interest in claiming the WIC benefit. Our second outcome variable was the percentage of message recipients who ultimately enrolled in WIC.

Results

Sample and balance checks

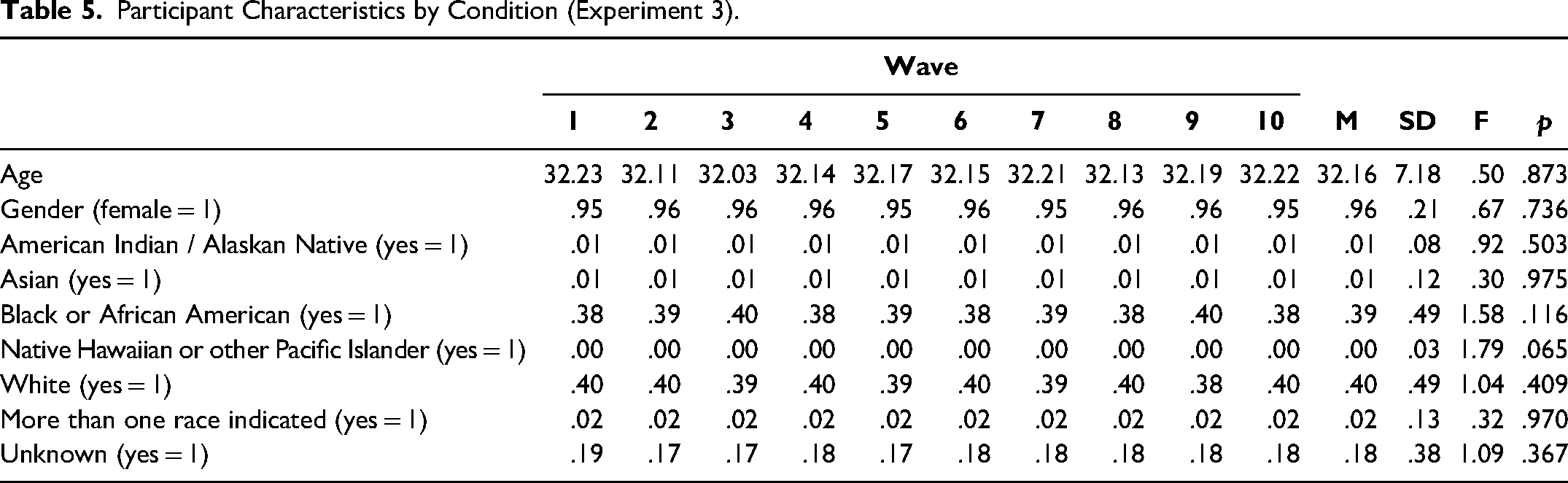

Due to undelivered text messages and disconnected phone numbers, 71,939 individuals (77.07% of those messaged) successfully received at least one message. Conditions were properly balanced across the available covariates (see Table 5).

Participant Characteristics by Condition (Experiment 3).

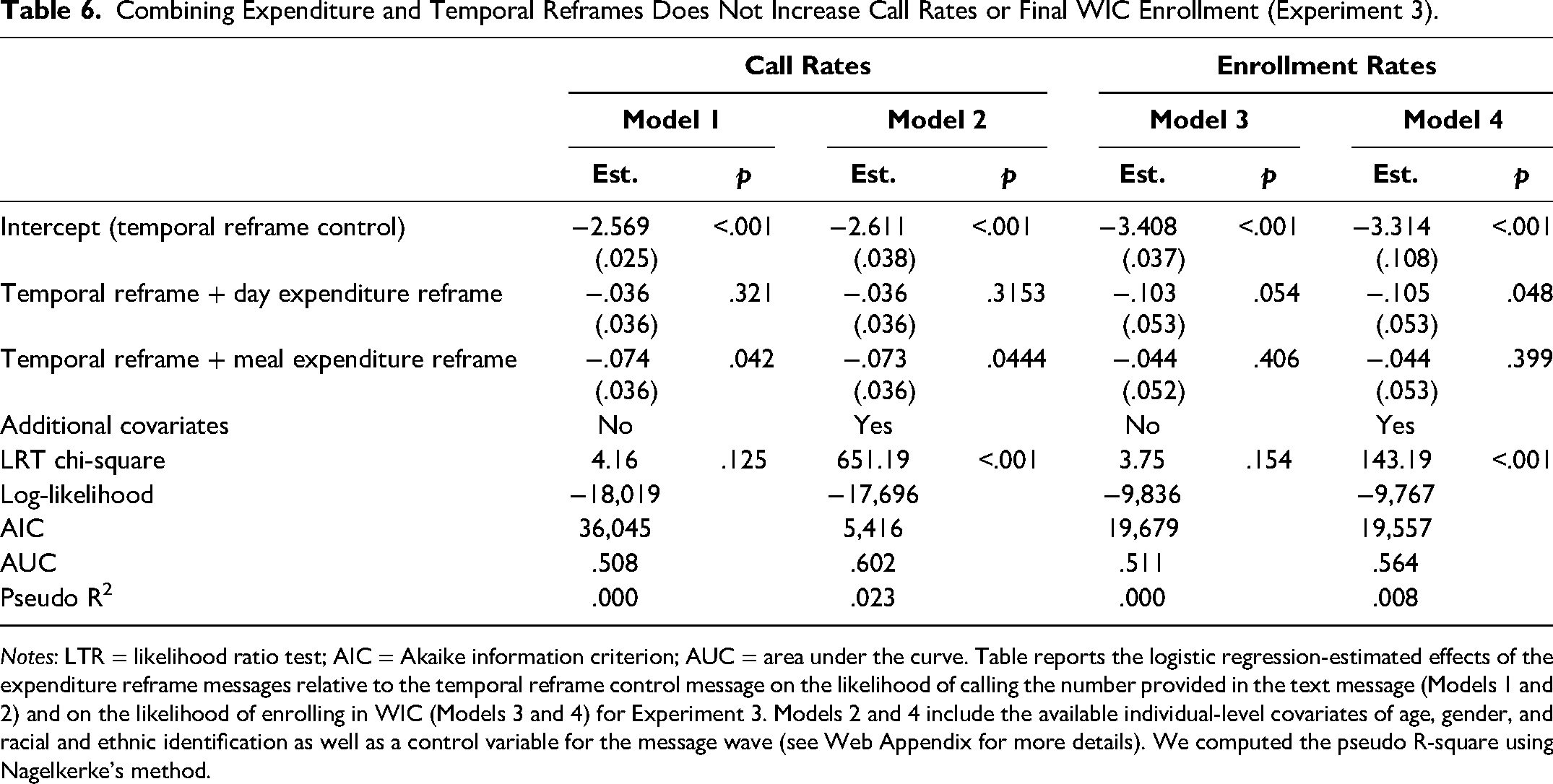

WIC interest

In contrast to our preregistered hypothesis, neither expenditure reframe condition increased call rates relative to the temporal reframe control condition (control = 7.11% vs. day-based expenditure reframe = 6.88% vs. meal-based expenditure reframe = 6.64%; χ2(2) = 4.15, p = .125). Similarly, there was no effect of condition on final WIC benefit enrollment among message recipients (control = 3.20% vs. day-based expenditure reframe = 2.90% vs. meal-based expenditure reframe = 3.07%; χ2(2) = 3.74, p = .154). See Figure 5 and Table 6.

Combining Expenditure and Temporal Reframes Does Not Increase Call Rates or Final WIC Enrollment (Experiment 3).

Notes: LTR = likelihood ratio test; AIC = Akaike information criterion; AUC = area under the curve. Table reports the logistic regression-estimated effects of the expenditure reframe messages relative to the temporal reframe control message on the likelihood of calling the number provided in the text message (Models 1 and 2) and on the likelihood of enrolling in WIC (Models 3 and 4) for Experiment 3. Models 2 and 4 include the available individual-level covariates of age, gender, and racial and ethnic identification as well as a control variable for the message wave (see Web Appendix for more details). We computed the pseudo R-square using Nagelkerke's method.

Discussion

These results ran counter to our preregistered hypotheses. We had initially expected that, as in Experiment 1, adding an expenditure reframe (either in terms of days of groceries or meals) would outperform the control message and increase individuals’ interest in claiming the benefit. Instead, these results demonstrate an important boundary condition to the efficacy of expenditure reframes and suggest that adding expenditure reframes to a temporally reframed amount may not be helpful and may even yield unfavorable outcomes. For example, we speculate that the combination of the reframes might have come across as overwhelming.

Of course, many other factors besides the presence of temporal reframes differentiate Experiment 3 from Experiment 1, where we found expenditure reframes to be effective in the field. These include the benefit examined (EITC vs. WIC), the outcome measures tracked (website visits vs. call rates), the benefit recipients themselves (prior food assistance applicants in California vs. Medicaid recipients in Louisiana), and the units used in the reframe (weeks of groceries vs. days or meals). Therefore, we further explore the proposed moderation via the presence (vs. absence) of temporal reframes in more detail in our next controlled online experiment.

Experiment 4: Monthly Temporal Reframes as a Boundary Condition

To help understand the findings from Experiment 3, we propose that the effects of expenditure reframes are attenuated when combined with temporal reframes in benefit descriptions (although again this may be one of many reasons for the observed effects in Experiment 3). Experiment 4 directly investigates our proposed explanation by examining whether expenditure reframes provide additional psychological value when a benefit is already presented with a monthly temporal reframe, such as “$50 per month,” versus an equivalent lump sum payment, such as “$600.” De La Rosa et al. (2022) showed that monthly temporal reframes can increase interest in government benefits as they match many people's budgeting periods. While not explicitly proposed by the authors, monthly temporal reframes may independently enhance the psychological value of the benefit, potentially diminishing the impact of an additional expenditure reframe.

This experiment explores the possibility that when a benefit's monetary value is already reframed in terms of its monthly temporal impact, expenditure reframes may not further increase psychological value. That is, if a monthly temporal reframe such as “$50 a month” already enhances the psychological value of the benefit, introducing an expenditure reframe may yield diminishing returns. Thus, we predict that expenditure reframes will have a weaker effect on increasing psychological value when combined with a monthly temporal reframe, positioning the latter as a potential boundary condition to the effectiveness of expenditure reframes.

Method

We recruited 1,204 participants from Prolific Academic, using the same Prolific filters as in Experiment 2 to target individuals with annual household incomes below the U.S. median of $80,000 (U.S. Census Bureau 2024). This study was preregistered on AsPredicted.org (https://aspredicted.org/qxyn-jrkv.pdf).

Participants were randomized into one of four conditions in this 2 (control vs. expenditure reframe) × 2 (lump sum vs. monthly reframe) between-subject experiment. All participants read the same prompt as in Experiment 2: “A nonprofit you have worked with in the past recommends a government benefit program to you that helps people cover their food costs. They describe the program as follows…” Participants then read one of four variations describing the benefit amount, depending on their assigned condition:

Control, lump sum: “People can receive $600.” Expenditure reframe, lump sum: “People can receive $600, which can roughly cover 24 days of groceries for an average family.” Control, monthly reframe: “People can receive $50 a month for a year.” Expenditure reframe, monthly reframe: “People can receive $50 a month for a year, which can roughly cover 2 days of groceries per month for an average family.”

Participants then rated their level of agreement with the same six psychological value items as in Experiment 2 (e.g., “this benefit would have a meaningful impact on my financial life”). Finally, participants reported their demographic information, including age, gender, ethnicity, education, and household income.

Results

As preregistered, we followed the same exclusion criteria as in Experiment 2. A total of 1,197 participants were included in the final sample (48.87% female, 49.04% male, 1.75% other, .33% preferred not to answer; Mage = 39.43 years, SD = 13.56). Our income targeting seemed effective, with over 90% of the sample reporting annual household incomes below $80,000.

We analyzed how the expenditure and temporal reframe conditions influenced consumers’ six-item psychological value index (α = .91; all items loaded onto one factor in an exploratory factor analysis). The results revealed significant main effects of the expenditure reframe (b = 5.98, SE = .71, t(1,193) = 8.46, p < .001) and the monthly reframe (b = −1.67, SE = .71, t(1,193) = −2.37, p = .018). Importantly, as expected, these results were qualified by a significant interaction between the two factors (b = −4.04, SE = .71, t(1,193) = −5.71, p < .001, Cohen's f2 = .03). Specifically, when the benefit was described as a lump sum of $600, expenditure reframes increased psychological value (Mcontrol = 58.35, SD = 27.09 vs. Mreframe = 78.39, SD = 19.84, d = .84; b = 20.05, SE = 2.00, t(1,193) = 10.05, p < .001, see Figure 6). However, this effect was attenuated when the benefit was described not as a lump sum but as a recurring $50/month benefit (Mcontrol = 63.08, SD = 25.68 vs. Mreframe = 66.96, SD = 24.69, d = .15; b = 3.89, SE = 2.01, t(1,193) = 1.94, p = .053). This interaction is robust and present even when we excluded the 9.5% of participants with reported household incomes above the U.S. median (b = −3.75, SE = .74, t(1,079) = −5.04, p < .001, Cohen's f2 = .02) or focus on lower-income participants with household incomes of less than $40,000 (b = −2.00, SE = 1.05, t(516) = −1.90, p = .058, Cohen's f2 = .01), and when we analyzed each measure individually (all ts < −4.03, all ps < .001, all Cohen's f2 > .01; see Web Appendix for more details).

Discussion

These results provide evidence that the effects of expenditure reframes are moderated by whether the amount itself has already been reframed into recurring temporal units (vs. a lump sum). Of course, while the null effects in our large-scale field experiment may be multiply determined, this online experiment helps illuminate at least one possible explanation as to why expenditure reframes did not seem to drive interest in that context.

Importantly, these effects cannot be explained by the possibility that $50/month is perceived as less than $600. In contrast, we provide a conceptual replication of De La Rosa et al. (2022) demonstrating the usefulness of monthly temporal reframes, as they significantly increased psychological value (b = 4.73, SE = 2.00, t(1,193) = 2.37, p = .018). While temporal reframes are helpful, interestingly, adding an expenditure reframe to a standard benefit description of $600 seems to be more beneficial, increasing psychological value by more than four times compared with the temporal reframe.

Experiment 5: Moderating the Effect of Expenditure Reframes in Increasing Interest in the EITC via Expense Type

Not all expenses hold equal weight in consumers’ minds. An expense's relevance, regularity, predictability, and required monitoring and decision-making may each play a role in how salient an expense is in consumers’ minds. We believe food is a unique expenditure that is high on all of these factors. It is arguably one of the few expenses that is relevant to almost all consumers, requiring daily decision-making and planning. As a result, it is likely to take up a substantial share of cognitive efforts dedicated to expenses for many consumers, irrespective of whether it also takes up the largest share of their wallet. For example, in a nationally representative survey, over 60% of respondents listed “food” or “groceries” as one of their top five budget categories, while just 37% listed “housing,” “house,” “mortgage,” or “rent” as one of their budget categories (Zhang et al. 2022).

A preregistered pilot study with 250 lower- to moderate-income individuals provided further evidence that spending on food is more salient and top-of-mind to consumers than their spending on housing, transportation, personal insurance and retirement, or health care (the top five spending categories according to the U.S. Bureau of Labor Statistics 2024). Specifically, participants reported spending more time thinking about food expenses, having food spending more top-of-mind, thinking about it more frequently, and devoting more mental effort to planning and tracking their food spending compared with these other categories (all ts > 7.14, all ps < .001, all ds > .45; see Web Appendix for more details). Because of the prominence food expenditures hold in consumers’ minds, we hypothesize that expenditure reframes focused on food should be particularly effective. We test this proposition more directly in Experiment 5 by manipulating the type of expense referenced in the expenditure reframe.

To do so, we again partnered with the NPO from Experiment 1 to market the EITC to lower-income people likely eligible for the tax credit. As in Experiment 1, this experiment was part of a larger investigation by the NPO and 17 research teams (De La Rosa et al. 2024). Participants received a control message or one of 22 treatment messages. For the purposes of this investigation, we focus on comparing the effect of the two expenditure reframe messages to the control message. The first expenditure reframe message was exactly the same as in Experiment 1, focusing on food expenditures, while the second expenditure reframe message focused on housing expenditures. In addition to the aforementioned reasons, we suspect that food expenses might be particularly salient relative to housing costs for this population, as our sample was composed of those who had recently applied for food assistance.

Method

The NPO sent text messages to 150,000 lower-income Californians who had previously applied for food assistance through the GetCalFresh service and were likely eligible for the EITC. EITC eligibility was estimated using the same criteria as in Experiment 1.

In this work, we focus on the comparisons between three message conditions: the control condition, the food expenditure reframe condition, and the housing expenditure reframe condition (N = 37,600). This study was preregistered on AsPredicted.org (https://aspredicted.org/3XS_QRS; https://aspredicted.org/VVL_GP8).

The control and food expenditure messages were identical to those used in Experiment 1, while the housing expenditure reframe message differed slightly and read: “Hi [First Name], this is Gwen from GetCalFresh. We believe you are eligible for a [Amount] tax credit, enough to cover roughly [X] months of rent in California.”

As in Experiment 1, we examine participants’ EITC-claiming intentions as measured across two outcome variables of actual online behavior: (1) whether they clicked on the website link included in the text message to visit the EITC-claiming website and (2) whether they clicked the “Get Started” button on the homepage of the website to start the claiming process.

Results

Sample and balance checks

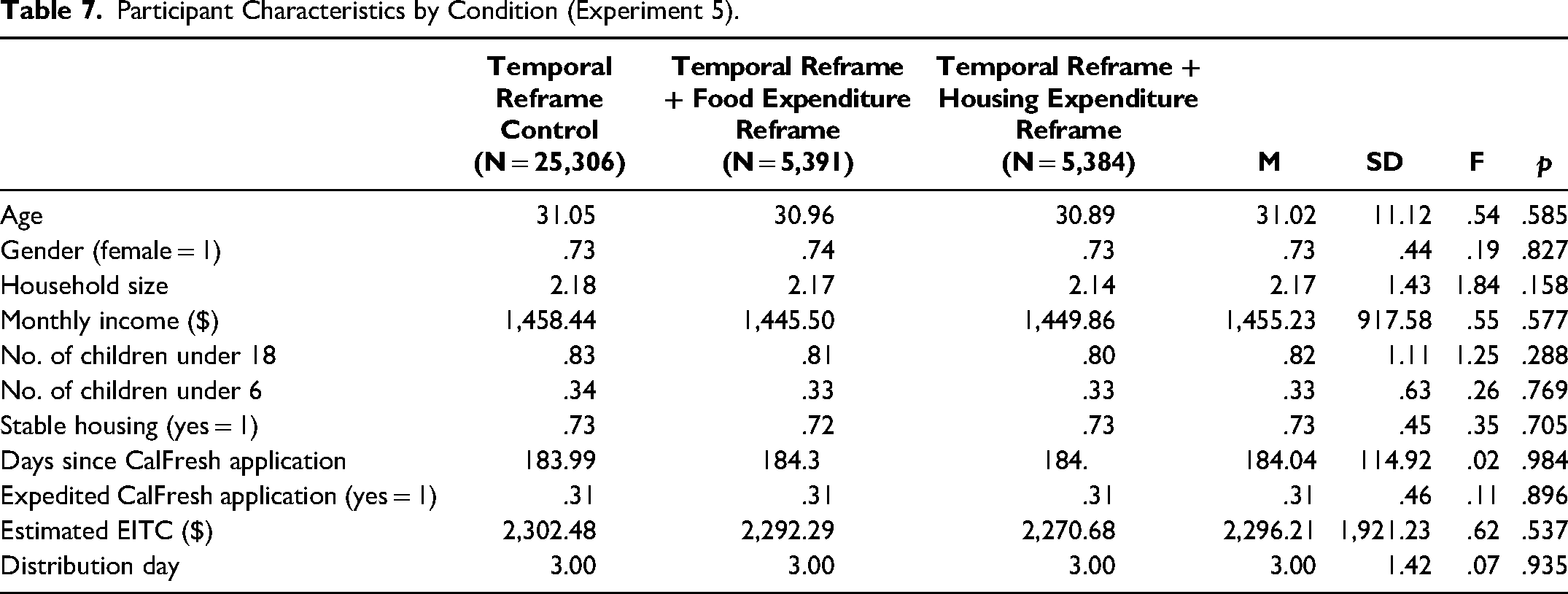

Due to undelivered text messages and disconnected phone numbers, 36,081 individuals (95.96% of those messaged) successfully received one of the three messages of interest. The conditions were properly balanced across the observable covariates (see Table 7).

Participant Characteristics by Condition (Experiment 5).

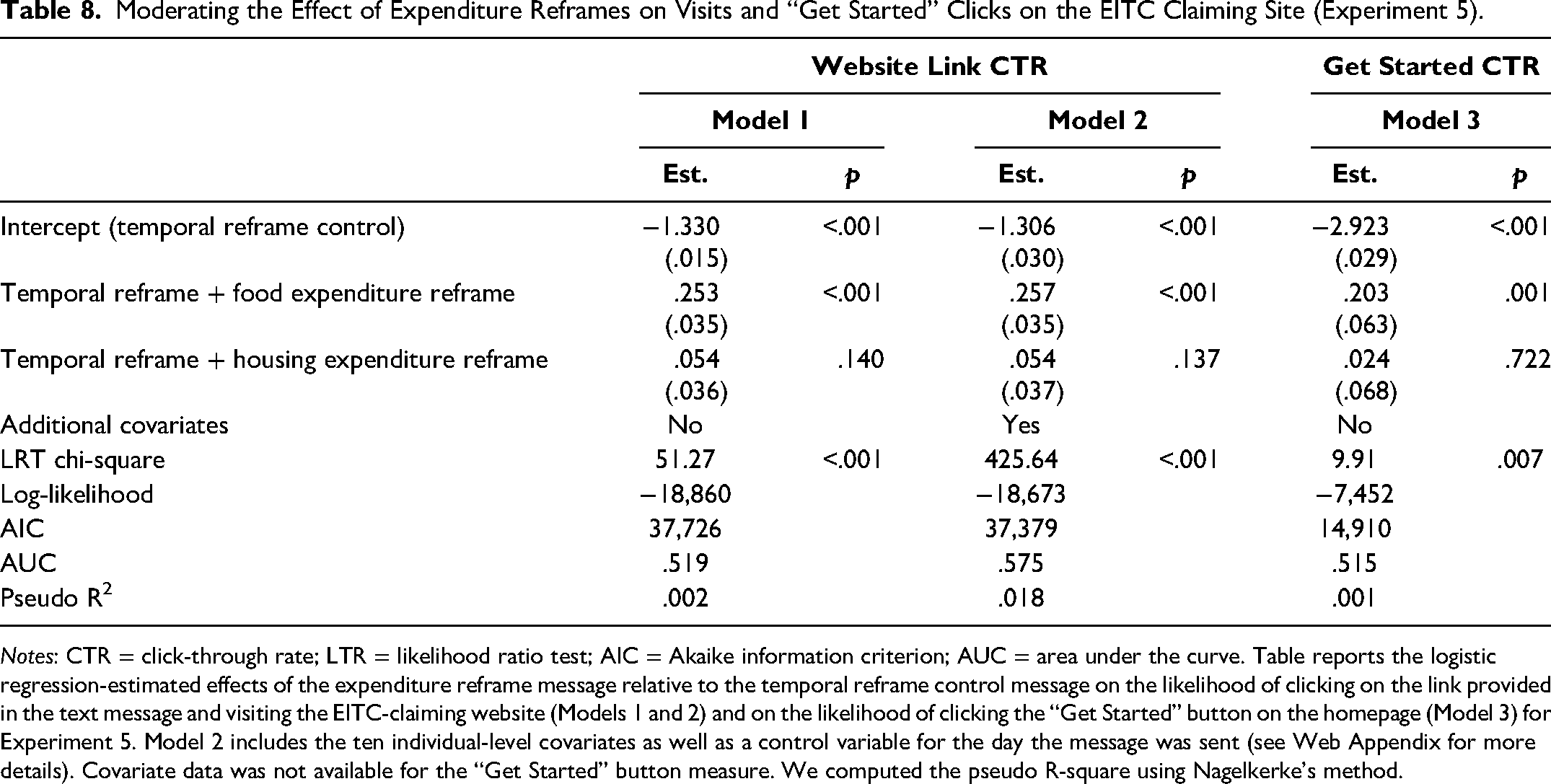

EITC interest

As in Experiment 1, the food expenditure reframe message increased the percentage of participants clicking the provided link and visiting the EITC-claiming website relative to the control message from 20.9% to 25.4% (b = .25, SE = .03, z = 7.25, p < .001, Cohen's h = .11; see Figure 7 and Table 8). The food expenditure reframe message also outperformed the housing expenditure reframe message (25.4% vs. 21.8%, b = .20, SE = .05, z = 4.38, p < .001, Cohen's h = .08). Relative to the control, the housing expenditure reframe message increased the percentage of participants visiting the website, though it was not statistically significant (21.8% vs. 20.9%, b = .05, SE = .04, z = 1.48, p = .140, Cohen's h = .02).

Moderating the Effect of Expenditure Reframes on Visits and “Get Started” Clicks on the EITC Claiming Site (Experiment 5).

Notes: CTR = click-through rate; LTR = likelihood ratio test; AIC = Akaike information criterion; AUC = area under the curve. Table reports the logistic regression-estimated effects of the expenditure reframe message relative to the temporal reframe control message on the likelihood of clicking on the link provided in the text message and visiting the EITC-claiming website (Models 1 and 2) and on the likelihood of clicking the “Get Started” button on the homepage (Model 3) for Experiment 5. Model 2 includes the ten individual-level covariates as well as a control variable for the day the message was sent (see Web Appendix for more details). Covariate data was not available for the “Get Started” button measure. We computed the pseudo R-square using Nagelkerke's method.

The food expenditure reframe message also increased the percentage of participants clicking the “Get Started” button and starting the filing process relative to the control message and the housing expenditure reframe message (vs. control: 6.2% vs 5.1%, b = .20, SE = .06, z = 3.20, p = .001, Cohen's h = .05; vs. housing: 6.2% vs 5.2%, b = .18, SE = .08, z = 2.14, p = .032, Cohen's h = .04).

Discussion

These findings replicated the efficacy of a food expenditure reframe from Experiment 1 in the field among a different group of lower-income people, again measuring their actual online behavior in pursuing the EITC. Moreover, these findings demonstrate that the expense type used within the reframe plays a crucial role in the effect. Food expenditures hold particular prominence for most consumers, and they can serve as an especially effective expense category to leverage within expenditure reframes to boost the psychological value of the government benefit being described. We test this directly in Experiment 6.

Experiment 6: Moderating the Effect of Expenditure Reframes on Psychological Value via Expense Type

Experiment 5 provided initial evidence in a consequential setting that the type of expense featured in expenditure reframes can moderate its effectiveness. However, these results could potentially be explained by alternative accounts. For example, one potential alternative explanation could be the variation in personalization; the food expenditure messages were based on individuals’ household size, while the housing expenditure messages were based on the average cost of a two-bedroom apartment in California. Second, we also varied the units used in the messages; the food expenditure reframe was presented in weeks, whereas the rent expenditure reframe was presented in months. We opted for this design because these units match how many consumers naturally think about those expenses. Indeed, a pretest found that 51% of participants budgeted food on a weekly basis, and 68% budgeted rent on a monthly basis. Because expenditure reframes likely increase psychological value for many reasons, including their ability to simplify mental accounting, we felt it was most prudent to use units with which consumers are familiar (and thus can easily connect to their existing mental accounts).

To disentangle the demonstrated impact of expense type from these possible confounds, we conducted a controlled online experiment with lower- to moderate-income individuals. In this setting, we tested the moderating effect of different expense types on the influence of expenditure reframes on psychological value while keeping the units and personalization level consistent across the expenditure reframe descriptions.

Method

We recruited 599 participants from Prolific Academic, using Prolific filters to target individuals with annual household incomes below the U.S. median of $80,000 (U.S. Census Bureau 2024). This study was preregistered on AsPredicted.org (https://aspredicted.org/c9x6-md4s.pdf).

In this between-subjects experiment, participants were randomly assigned to one of four conditions: a control condition or one of three expenditure reframe conditions, each targeting a specific type of expense (food, housing, or utilities). All participants read: “A nonprofit you have worked with in the past recommends a government benefit program to you that helps people cover their costs. They describe the program as follows…” In the control condition, the benefit was simply described as “People can receive $600.” In the food, housing, or utility expenditure reframe conditions, the benefit was described as “People can receive $600, which can roughly cover [24 days of groceries / 8 days of rent / 147 days of cable] for an average family.”

Participants then rated their level of agreement with the same six psychological value items as in Experiments 2 and 4. Finally, participants reported their demographic information, including age, gender, ethnicity, education, and household income.

Results

As preregistered, we followed the same exclusion criteria as in Experiment 2. A total of 599 participants were included in the final sample (71.95% female, 26.54% male, 1.17% other, .33% preferred not to answer; Mage = 40.51 years, SD = 13.66). Our income targeting was largely effective, with over 92% of the sample reporting annual household incomes below $80,000.

We analyzed how the expenditure reframe conditions influenced the benefit's psychological value by combining the six psychological value questions into one index (α = .92; all items loaded onto one factor in an exploratory factor analysis). As expected, compared with the control (Mcontrol = 46.78, SD = 26.30), all of the expenditure reframe conditions significantly increased the psychological value (vs. Mfood reframe = 79.82, SD = 19.90, d = 1.41, b = 33.04, SE = 2.84, t(595) = 11.65, p < .001; vs. Mhousing reframe = 68.30, SD = 24.68, d = .84, b = 21.52, SE = 2.85, t(595) = 7.55, p < .001; vs. Mutility reframe = 62.85, SD = 27.10, d = .60, b = 16.07, SE = 2.85, t(595) = 5.65, p < .001; see Figure 8). Importantly, the food expenditure reframe outperformed all the other expenditure reframe conditions (all ts > 3.92, all ps < .001, all ds > .51). Once again, these effects were robust: the food expenditure reframe outperformed all other conditions even when we excluded the 7.3% of participants with reported household incomes above the U.S. median (all ts > 2.95, all ps < .001, all ds > .51), or when we focus on lower-income participants with reported annual household incomes of less than $40,000 (all ts > 2.32, all ps < .022, all ds > .44). See Web Appendix for additional analyses.

Discussion

The results of Experiment 6 demonstrate that the expense type used can moderate the effects of expenditure reframes on consumers’ psychological value of a benefit. In particular, this experiment, coupled with our pilot study and Experiment 5, provides evidence for the unique role food expenditures hold in consumers’ minds. Notably, these results help rule out multiple alternative explanations for why food expenditure reframes outperformed housing expenditure reframes in Experiment 5. In particular, all three expenditure reframe conditions in this experiment used the same level of personalization and the same units (days of expenses covered). Additionally, that food expenditure reframes increased value perceptions over utility expenditure reframes despite the latter involving larger numeric values (“8 days of groceries” vs. “147 days of cable”) suggests that numeric differences were unlikely to lead to the effects observed in Experiment 5.

General Discussion

Across six preregistered experiments, we investigated the effectiveness of expenditure reframes in driving consumers’ interest in claiming government benefits. First, we demonstrated the usefulness of expenditure reframes in a consequential large-scale field context, as well as in an online experiment, finding that it can help increase both consumers’ psychological value and their benefit-seeking behavior. Second, we uncovered important boundary conditions for these effects, both in online experiments and in the field. Specifically, we demonstrated the limited ability of expenditure reframes to increase psychological value when paired with other tactics that were also intended to boost psychological value (i.e., temporal reframes). We further showed that food expenses may be a particularly effective expense for expenditure reframes, given how salient they are for many consumers.

Additionally, we contribute to the benefits literature by expanding the value–cost framework, identifying and clearly organizing the different types of value consumers may derive from receiving government benefits, including the financial value, the indirect value, and the psychological value. We also highlight several factors that shape psychological value, such as adequacy perceptions and cognitive ease. We hope this updated framework is useful for future researchers and engenders more research on drivers of psychological value as well as a deeper investigation into indirect value.

More broadly, our work adds to the existing literature on consumers’ subjective valuations of monetary amounts. Much research has investigated the malleability of such perceptions, finding that consumers value monetary amounts differently based on provided reference prices (Morewedge, Holtzman, and Epley 2007; Tversky and Kahneman 1981), temporal brackets (Goldstein, Hershfield, and Benartzi 2016; Ülkümen, Thomas, and Morwitz 2008), and numeric formatting (e.g., percentiles; Heath, Chatterjee, and France 1995). We contribute to this literature by establishing expenditure reframes as monetary descriptions that can increase psychological value and drive action. The importance of this contribution is underscored by our examination of the effectiveness of expenditure reframes in communicating benefits to relevant populations, both in the field and in controlled online settings.

Implications for Marketers and Policymakers

This article has several notable implications for marketers and policymakers. The most direct implication is that practitioners and researchers can employ expenditure reframes to help increase interest in claiming government benefits. This is not a trivial pursuit. Ensuring that eligible lower-income people access government benefits like the EITC and WIC is one of the main levers governments have to reduce poverty. Furthermore, this work clarifies the contexts in which expenditure reframes might be most helpful and provides a framework that future practitioners can use to assess other marketing tactics aimed at increasing value perceptions.

Beyond government benefits, this work suggests that expenditure reframes might be a valuable tool for marketers who aim to increase interest in a particular income stream. For example, companies seeking to recruit new employees might benefit from adding expenditure reframes to the annual salary estimates in their job postings. This may be especially important in tight labor markets where unemployment is at historic lows, as companies must market themselves effectively to vie for talent. Given differences in the target population and dollar amounts being considered, additional research is needed to determine how best to implement the reframe in this context.

Furthermore, managers might consider using expenditure reframes in other contexts where communicating value is necessary. Expenditure reframes may be used not just for describing potential gains, but also for describing potential savings. For example, marketers may use expenditure reframes to increase the psychological value of sales, rebates, points, or coupons to increase consumer interest in their products.

Limitations and Future Directions

Practitioners can employ various tools to help drive interest when communicating dollar values of benefits, income, or savings. This research provides initial evidence that, at least in the context we examine, expenditure reframes can be more effective in increasing psychological value than temporal reframes. We show that expenditure reframes increase benefit interest in the field, which we posit is a logical consequence of an increase in psychological value. However, our experiments do not capture this process directly through mediation. Future research could better document the proposed psychological mechanism.

Much of this research focused on using expenditure reframes to increase interest in government benefits. We measure interest in several ways, including real behavioral metrics such as click-through rates and calls to begin the application process. These are critical top-of-funnel metrics; if people do not start the process, they cannot complete it. However, while necessary, interest alone is not sufficient. Thus, our findings complement other efforts to increase benefit uptake (e.g., simplifying the application process; Bhargava and Manoli 2015). As in Experiment 3, we encourage future researchers to investigate how expenditure reframes influence downstream outcomes, including final benefit enrollment. Furthermore, future research could explore the potential additive effects of combining expenditure reframes with other application interventions.

Understanding potential moderators will be instrumental in providing a fuller understanding of why these reframes influence consumers’ psychological value of a benefit. For example, our theory suggests that the ease with which consumers can understand and mentally allocate the expenditure reframe to their own financial needs is a likely moderator; reframes which are harder to understand (e.g., “this benefit roughly covers 13.44 days of groceries”) are unlikely to increase interest. Moreover, as prior research demonstrates (e.g., Goldstein, Hershfield, and Benartzi 2016) and as shown by the heterogeneity analysis from Experiment 1, the effectiveness of temporal and expenditure reframes may vary based on the amount involved.

Additionally, as discussed, we suspect that the effects of expenditure reframes may stem from their ability to make financial incentives more concrete and aid in mental accounting. Yet other accounts may also play a role; for instance, consumers might underestimate the value of a benefit described as a lump sum because of scope insensitivity, or the inability to conceptualize large numbers (Hsee and Rottenstreich 2004; Kahneman and Knetsch 1992). We encourage researchers to further investigate and differentiate between these and other potential mechanisms.

In addition, the current work points to the relevance of specific expenses for consumers. Future research might explore the characteristics that lead a particular expense to be more or less salient in consumers’ minds. We have argued that food expenditures are unique given that they are an essential expense that requires frequent, active decision-making and planning for lower-income consumers. Of course, other factors concerning an expense, such as its volatility, the level of autonomy consumers feel over it, its overall amount, or even its desirability or temptation could all play a role in how salient the expense is to consumers. Such an investigation could help researchers understand heterogeneity across different types of expenses and lead to new expense taxonomies.

The interventions in the current article increased interest in claiming government benefits using a single expense reframe for all participants within a condition. Future researchers could focus on individual-level heterogeneity in consumers’ expense salience and create tailored and targeted interventions. For example, while we have identified consumers who are focused on food expenses (i.e., those who have recently applied for food assistance) some consumers might be more focused on other expenses like housing or transportation. It will be important to understand and parse the antecedents of expense salience, as we suspect that it can predict a host of consumer behaviors, including consumers’ mental well-being.

We investigated the effectiveness of food expenditure reframes primarily by operationalizing them in terms of common temporal units (e.g., the number of weeks or days of expenses the benefit can cover). We used this approach because of its natural fit with how consumers think about their food expenses, yet it also introduces a temporal component. Thus, it is possible that expenditure reframes are less effective in the presence of temporal reframes, as demonstrated in Experiments 3 and 4, in part because of this redundancy (although this would not explain the lack of an effect for the meal-based food expenditure reframe in Experiment 3). Future work could explore the impact of expenditure reframes by testing new framing units. An open question remains as to whether reframing a benefit in terms of the number of grocery bags or fast-food meals affects psychological value of and interest in the benefit, and how these effects might persist alongside temporal reframing.

Furthermore, we encourage future investigations focusing on different income streams, including other government benefits. For example, benefits like the Low Income Home Energy Assistance Program focus on reducing consumers’ heating bills and do not involve a direct cash transfer. It is unclear how expenditure reframes for these sorts of savings or cost reductions (vs. income) might influence benefit interest. Outside of government benefits, marketers could explore how using expenditure reframes for various other employee benefits or income streams, like social security benefits, might influence consumer attitudes and behavior.

We hope that this work empowers policymakers and engenders new research shaping our understanding of how consumers evaluate available resources and make income-seeking decisions.

Supplemental Material

sj-pdf-1-jmx-10.1177_00222429251356992 - Supplemental material for Using Expenditure Reframes to Increase Interest in Claiming Government Benefits

Supplemental material, sj-pdf-1-jmx-10.1177_00222429251356992 for Using Expenditure Reframes to Increase Interest in Claiming Government Benefits by Wendy De La Rosa, Jackie Silverman, Abigail B. Sussman, Gwen Rino, Vince Dorie, Maximilian Hell, Eric Giannella and Lisa Dillman in Journal of Marketing

Footnotes

Acknowledgments

The authors thank Caiti Roth-Eisenberg, Julia Kosov, Gabrielle FilipCrawford, Annelise Rolander, our nonprofit partner, Benefits Data Trust, and Louisiana’s Bureau of Nutrition Services teams, without whom this work could not have been made possible. Thank you to Yujin Yang and Jieyi Chen for their outstanding research assistance and to Christophe Van den Bulte, Ron Berman, and Christopher Bechler for their helpful comments.

Author Note

W.D.L.R and A.B.S designed the expenditure reframe messages in Experiments 1 and 5; G.R., V.D., M.H., and E.G. implemented the experiments and collected the data. W.D.L.R. analyzed the data. W.D.L.R., J.S., and A.B.S. designed and conducted Experiments 2, 4, and 6. W.D.L.R. analyzed the data. W.D.L.R, J.S., and A.B.S. designed Experiment 3. L.D. implemented and collected the data. W.D.L.R. and J.S. analyzed the data. W.D.L.R. and J.S. drafted the manuscript, W.D.L.R., J.S., and A.B.S. revised it.

Coeditor

Vanitha Swaminathan

Associate Editor

Claudia Townsend

Ethical Considerations and Consent to Participate

Before this project commenced, the field experiments were reviewed by the institutional review board (IRB) of the University of Pennsylvania. This IRB determined that these experiments were exempt from the regulations at 45 CFR 46. The online experiments were approved by the IRB of the University of Pennsylvania, and all subjects provided informed consent. No identifying information about experiment participants was ever shared with the researchers.

Declaration of Conflicting Interests

The author(s) declared the following potential conflicts of interest with respect to the research, authorship, and/or publication of this article: Wendy De La Rosa served on the board of the nonprofit organization that conducted Experiments 1 and 5. She did not receive any monetary compensation for her service. Gwen Rino, Vince Dorie, Maximilian Hell, and Eric Giannella were employed by the nonprofit when Experiments 1 and 5 were conducted. Lisa Dillman was employed by Benefits Data Trust when Experiment 3 was conducted.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Wharton Behavioral Lab and the Wharton Dean’s Research Fund at the University of Pennsylvania, as well as the Beatrice Foods Co. Faculty Research Fund at the University of Chicago Booth School of Business.

Data Availability Statement

All anonymized data, preregistrations, online experiment materials, and analysis scripts are publicly available on ResearchBox (https://researchbox.org/3689). Due to the sensitive nature of the field experiment data and in accordance with agreements with our field partners, individual-level covariates cannot be made publicly available.