Abstract

In a critical review of seven prominent flagship reports from five international organisations – the International Labour Organization (ILO), Organisation for Economic Co-operation and Development (OECD), United Nations Industrial Development Organization (UNIDO), United Nations Development Programme (UNDP) and World Bank – this article explores how the policy narratives set out during 2019 and early 2020 have characterised the major future of work challenges associated with new technologies and inequality. It identifies some similarities in viewpoints, including about the unevenness of job changes caused by new technologies and about the declining labour income share, a key measure of inequality. However, there are major points of differentiation. The ILO, OECD and UNDP express serious concerns about the interaction between new technologies and growing inequalities, on the one hand, and a rise in precarious work, concentration of corporate power and erosion of labour bargaining power on the other. Also, UNIDO emphasises the inequalities in technological capacities between developed and developing countries, which make it difficult for markets to distribute the gains from growth evenly. While the World Bank makes some concessions, it remains less open to real-world heterodox evidence about how labour markets function in society. The World Bank aside, there is a growing consensus that labour institutions around the world need to be reinvigorated in order to respond to the challenges facing the future of work.

Keywords

Introduction

There are good reasons for industrial relations specialists (academics and practitioners) to pay close attention to the policy narratives of the major international organisations, especially the various United Nations (UN) agencies, the Organisation for Economic Co-operation and Development (OECD) and the World Bank. The first is that many of the potentially transformative ‘future of work’ challenges confronting contemporary labour markets require international cooperation, and it is within the multilateral system where the possibilities of an overarching policy framework are most visibly negotiated and articulated. Examples of challenges that are unlikely to be solved by a nation state acting alone include establishing international labour standards, moving to sustainable development, protecting workers in global value chains, migration, regulating digital labour platforms, and corporate taxation. Critical and constructive analysis of the international policy narrative in these areas therefore supports a potentially more effective and legitimate policy response.

A second reason is that the multilateral system is riddled with conflicts and disagreements about the nature of the policy approach required and thus deserves close scrutiny to shed light on problems of empirical evidence, theoretical assumptions or misunderstandings of literature so that policy recommendations are as robust as might be expected. International organisations routinely draw on the latest academic research, and yet in the field of employment there is far greater reliance on macro- and labour economics literature than industrial relations (or development studies, feminist economics or sociology of work) despite the strong interest in policy analysis of these other fields. The OECD has considerably widened its reach recently (including an entire chapter on collective bargaining in its Employment Outlook 2019 report) and the International Labour Organization (ILO) promises to launch a new flagship report on industrial relations in 2021. Nevertheless, far greater interaction with the industrial relations community is needed in order to improve the way ‘future of work’ issues are interpreted.

A third reason is simply that the policy narratives of international organisations are very influential, particularly among governments and civil society organisations, despite the often virulent opposition from right-wing populist governments and certain corporate lobby groups. Major employment-related themes and policy recommendations are routinely picked up by national governments, re-designed and implemented for the local context. This means that attention to the underlying analysis is useful.

This article presents a critical review of a sample of seven flagship reports published in 2019 or early 2020 by five international organisations: the ILO, the OECD, the United Nations Development Programme (UNDP), the United Nations Industrial Development Organization (UNIDO) and the World Bank (Box 1). In order to narrow the range of analysis, the article asks two specific questions related to debates on the ‘future of work’: What are the major insights concerning the impact of new technologies on work and employment? What are the causes and consequences of high-income inequality with regard to employment issues? The first two sections explore each question in turn. In both cases, the analysis includes an appraisal of the role of labour institutions in the recommended international policy response. The article concludes by emphasising some of the notable differences among international organisations and identifying areas of research needed to answer questions about the future of work. Seven flagship reports selected for review.

New technologies: Job losses, inequalities and precarious work

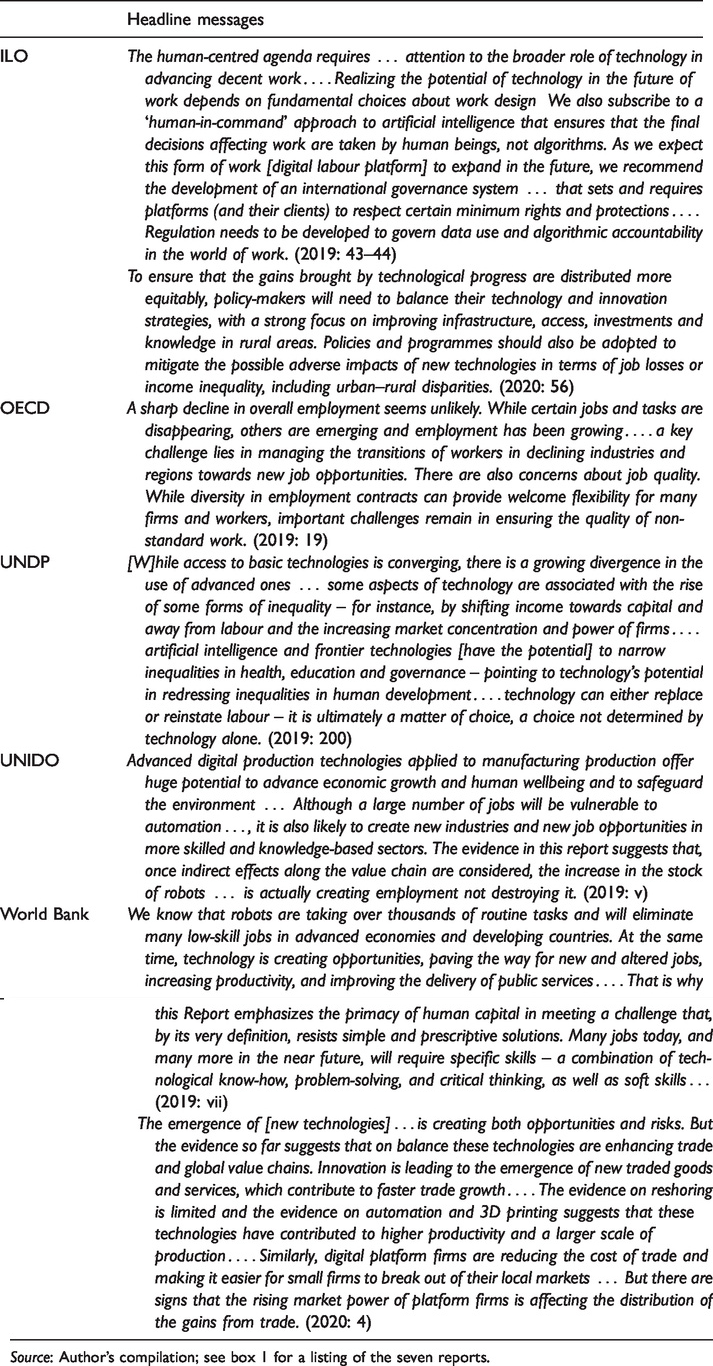

The flagship reports of the international organisations selected for review each chose not to exploit the headline forecasts about possible job losses resulting from new technologies. Instead, they emphasised the array of positive countervailing effects, as well as the contingencies of technological design and implementation. The common identified employment risks concerned various dimensions of inequalities, especially regarding patterns of segmentation across developed and developing countries, industries and workforce groups (including by skill and by gender). Only the ILO OECD and UNDP reports investigated the problematic consequences for the standard employment relationship and in particular the association between new technologies (especially digital) and precarious work. These reports call for a revitalisation of labour institutions to sustain and extend employment protections. Table 1 presents extracts of the relevant headline messages from all seven reports.

Headline messages regarding impacts of new technologies: Selected flagship reports.

Source: Author’s compilation; see box 1 for a listing of the seven reports.

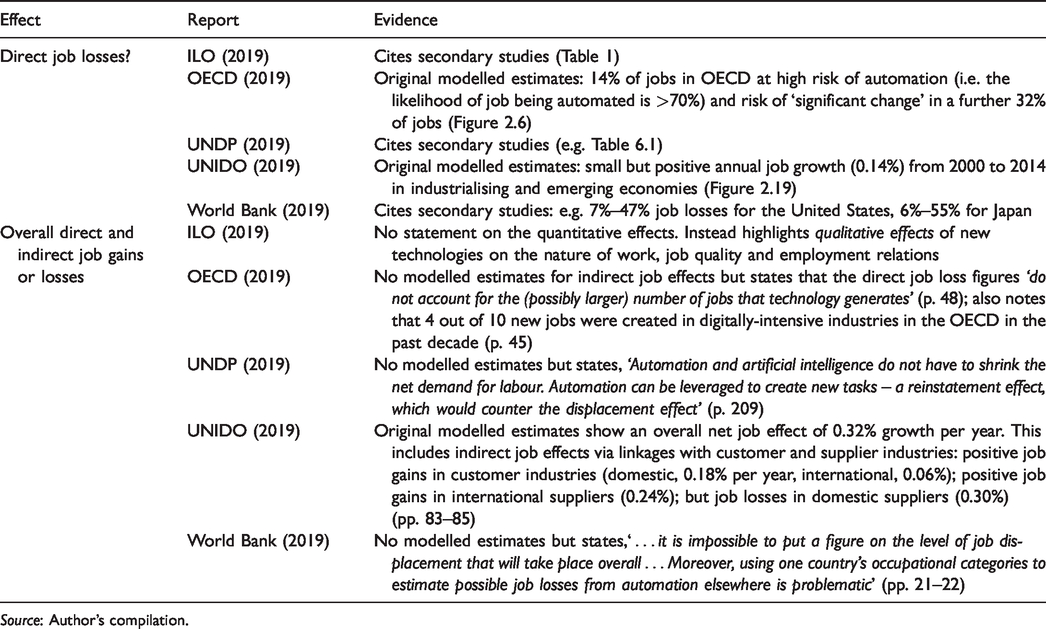

Job losses

Despite several high-profile studies that argued massive job losses would result from new technologies (Brynjolfsson and McAfee, 2012; McKinsey, 2017), in their 2019 flagship reports the OECD, World Bank and United Nations agencies each adopted a cautiously optimistic stance. In large part, this reflects the analytical rebuttal by the economists David Autor and Daron Acemoglu to the rather alarmist perspective (Acemoglu and Restrepo, 2018, 2019; Autor, 2015; Autor and Salamons, 2018). Drawing on historical evidence and the results of technical modelling, their work has been very influential in showing that the quantitative labour displacement effects of automation and artificial intelligence

1

are likely to be accompanied by several important countervailing effects. These can be summarised as:

a productivity effect (which reduces prices, raises demand for goods and services and thus increases demand for labour, including in customer and supplier industries and to perform non-automated tasks); a capital accumulation effect (triggered by new investments that increase the demand for labour); a deepening of automation effect (that improves the productivity of tasks that have already been automated); and a growth of jobs effect to complete new tasks (in areas where humans have an advantage over machines).

This alternative more holistic economics perspective tends to emphasise the interconnections between high-tech and low-tech sectors of the economy, the positive and negative aggregate multiplier effects of new technologies on prices and productivity, and the way in which technologies substitute for labour at the level of work tasks rather than entire occupational groups.

The flagship reports all support this nuanced economics perspective (see Table 2). For example, while the OECD presents its own modelled estimates that around one in seven jobs (14%) are at high risk of automation, it argues that this risk is offset at the aggregate level by possibly larger job-creation effects as evidenced by the pattern of rising employment rates in the last three decades among developed and emerging economies (except the United States and Brazil) (2019: 44–49). UNIDO finds that the ‘direct effect’ of increased use of robots was in fact positive globally for the period 2000–2014 and was further reinforced by the ‘indirect effects’ of increased employment in customer and supplier industries (UNIDO, 2019: 83–84). Figure 1 presents UNIDO’s estimates of the gains and losses for industrialised and emerging economies; while the total job effect is positive (around 0.3% per year), there is a large (unexplained) indirect job loss in domestic supplier industries, especially in emerging economies.

Summary of evidence of job losses from new technologies: Selected flagship reports.

Source: Author’s compilation.

Modelled estimates of direct and indirect employment gains and losses (percent per year) due to robots, 2000–2014.

The World Bank’s flagship report is also critical of studies that only focus on the direct job losses and points out that the differential country absorption rates of new technologies mean that job losses vary significantly depending on the context (2019: 22). The ILO and UNDP reports cite the results of secondary studies and argue for closer attention to how new technologies can advance ‘decent work’ and ‘the quality of work’, respectively, since we cannot predict with any certainty the net change in jobs (ILO, 2019: 43; UNDP, 2019: 209; see below).

Inequalities and new technologies

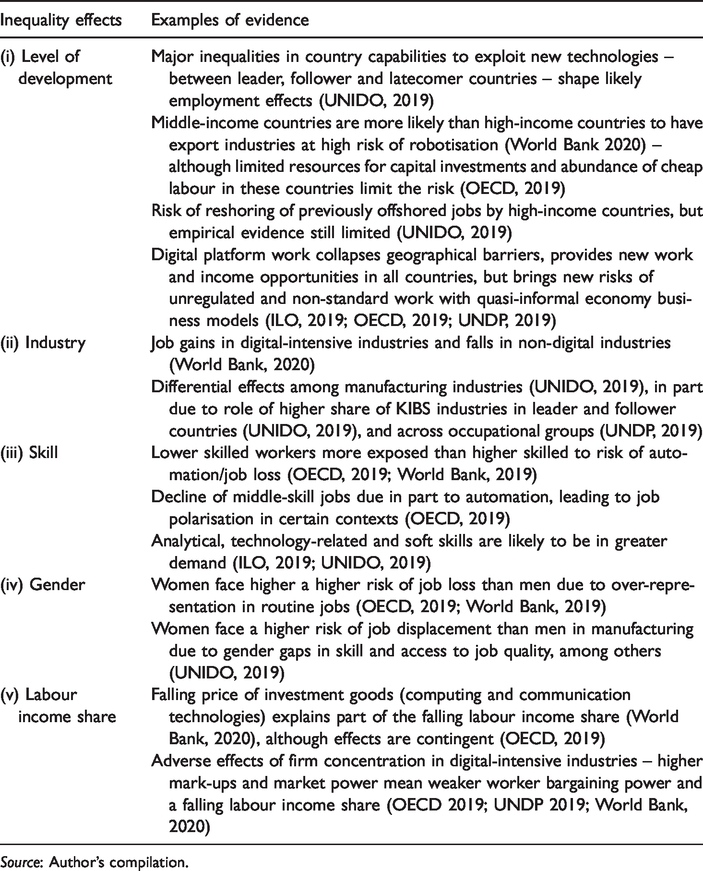

In their flagship reports, these international organisations thus consistently direct policy-makers’ attention away from large-scale aggregate job losses resulting from automation and advanced digital production technologies. Instead, albeit with varied emphasis, each report draws attention to the uneven and contingent impact of new technologies on employment by country, industry and workforce group (Table 3).

Summary of the potential inequality effects of new technologies on employment: Selected flagship reports.

Source: Author’s compilation.

The unevenness of country differences in the scale of job impacts is especially highlighted in the UNIDO, World Bank and OECD reports, as part of a broader effort to understand the shifting international division of labour. By far the richest analytical account is presented in the UNIDO (2019) report, reflecting its deeper intellectual association with the literature on innovation, firm capabilities and uneven development. Inter-country inequalities primarily reflect differences in technological development. The world is characterised by highly unequal divisions between leader, follower and latecomer countries concerning the production and use of new technologies, 2 rooted in differences in capabilities and endowments, as well as infrastructural and institutional conditions. While latecomers may be able to leapfrog into new technologies, minimum levels of technological and production capabilities are nevertheless still required (UNIDO, 2019: 49–60). This sets the context for the likely unequal international effects of positive and negative employment effects of new technologies.

While all countries may benefit from the countervailing positive employment effects identified above, some will be more exposed to the adverse risks of robotisation than others and therefore more likely to suffer net job losses. This is particularly the case for middle-income countries with a high share of exports in industries characterised as having tasks that are replaceable by robots (World Bank, 2020: 147–153). However, as the OECD points out, many middle-income countries will not be making the predicted cost-saving technology investments in the short term – both because the vast majority of businesses are small or medium-sized and lack the resources for such investments and because of an abundance of cheap and low-skilled labour among expanding youth populations in many developing countries (OECD, 2019: 48–50).

In addition to the direct job displacement caused by robots in these industries, there may in the future be reshoring of jobs from low- and middle-income countries to high-income countries if tasks previously performed by inexpensive workers in emerging economies can be carried out by inexpensive robots in high-income countries (Rodrik, 2018). Labour-cost savings from adopting advanced industrial robots, estimated at 33% in Korea and 25% in Japan, suggest such reshoring disruptions could be significant. Again, however, the empirical evidence presented in some of the flagship reports suggests such fears are not yet warranted. For example, a survey of manufacturing firms in Europe found that of those firms that had reshored some activities it was a concern for flexibility and quality rather than labour-cost savings that was more likely to have motivated the decision (UNIDO, 2019: Figure 3.13). This may be related to a perception that labour-cost savings from offshoring still exceed the potential savings from automation and reshoring.

Inequalities in the international division of labour are further impacted by the way digital platform work is collapsing geographical barriers, especially those barriers that had restricted access of workers in developing countries to new sources of income and types of paid work (Rani and Grimshaw, 2019). The World Development Report places special emphasis on this point. It notes that Bangladesh now contributes an estimated 15% of the global online labour pool via its 650,000 online freelance workers (World Bank, 2019: 25). In tracing the impact of digital labour platforms on global inequalities, we face a similar set of context-contingent issues addressed in research on global value chains (GVCs) (e.g. Reinecke and Posthuma, 2019). While the new work opportunities provided on a digital platform (or by a GVC supplier firm) may in many countries be more attractive than the next best domestic alternative, they are unlikely to offer anything like the standard of remuneration paid in the home country of the business client – although country context (institutions, gender relations, legal compliance and trade unions) matter very much (Barrientos, 2019). Moreover, because the next best alternative in the developing country may involve poor working conditions and informal economic status, there is no guarantee that new forms of digitally enabled work lift workers out of poverty and insecurity, as a recent ILO report demonstrates (Berg et al., 2018).

A further distributive effect concerns the way new technologies can shift employment and wage prospects by industry within countries. The World Bank observes that growth of e-commerce through digital platforms may have delivered welfare gains by reducing prices and making more consumer goods accessible to a greater share of the world’s population, but it is displacing a growing share of workers from the traditional bricks and mortar retail stores (World Bank, 2020). In the United States, the growth of e-commerce as a share of total retail sales is associated not only with a drop in traditional retail employment, but also with a relative decline in wages and job stability in those retail stores neighbouring the mammoth Amazon fulfilment centres compared to other retail stores (Chava et al., 2018). While the World Bank over-emphasises welfare gains for the consumer, especially in its headline observations, it does acknowledge that, ‘Consumption gains … come at the expense of labor market adjustments’ (2020: 145).

Considering the effects of new technologies by skill and gender of workers, there is clear evidence that existing inequalities are being exacerbated. The OECD and the World Bank note that lower skilled workers are more at risk of automation than higher skilled workers and that women are over-represented in jobs involving routine tasks (Nedelkoska and Quintini, 2018, cited in OECD, 2019: 48; World Bank, 2019: 153). Valuable detail is presented in the UNIDO report, which devotes an explicit section (of around six pages) to investigating the gendered nature of new technologies on manufacturing employment in developing and emerging economies. It raises four key issues: 3 on average the risk of job displacement is higher for women in manufacturing than for men; women’s risk is higher than for men at all levels of skill (measured by level of education); men are far more likely to have developed ‘skills of the future’ than women, which are valuable for working with new technologies; and women’s access to high-quality jobs in manufacturing is constrained by employer stereotypes and patriarchal cultural norms (UNIDO, 2019: 76–81). These issues have parallels with work in the services sectors. More nuanced research identifies shifting gender inequalities resulting from trends towards flexible work locations, greater diversity of working hours, uncertain prospects for relational skills and uneven entitlements to employment and social protection (Howcroft and Rubery, 2019; Piasna and Drahokoupil 2017).

A further gender inequality issue not addressed in the flagship reports is that adjustments in the retail workforce caused by the growth of e-commerce are more likely to impact women than men, given women’s over-representation in retail. Findings from the industrial relations and feminist economics literatures are instructive. Research on the restructuring practices of managers in supermarket chains demonstrates that the combination of feminisation, low union membership, low pay and part-time employment status make retail workers especially vulnerable to cost-cutting adjustments and, even where unions are present, to concessionary spirals that allow terms and conditions to deteriorate over time (Beynon et al., 2002; Kainer, 1998). Further displacement and recalibration of retail jobs is likely with the growing share of e-commerce, and further research is needed to identify the gender and industrial relations dynamics in developed and developing countries.

With respect to changing employment dynamics in industry, the UNIDO report similarly calls for more gender-sensitive research: ‘Filling this information gap is crucial for developing a policy agenda to increase women’s equitable participation in the industrial workforce and in the development of technologies, which is fundamental to promoting inclusive and sustainable industrial development’ (2019: 76).

A final, major inequality effect of new technologies, addressed in all flagship reports selected here, concerns the labour income share. All international organisations appear to be concerned that technological progress, accompanied by a fall in the price of capital goods, may be a reason for the falling labour income share. Drawing on EU data, the World Development Report observes that the decline is highest in industries with higher robot density (World Bank, 2020: Figure 6.8). More generally, all reports follow the insights of Autor et al. (2017) and warn of the adverse effects of firm concentration in digital-intensive sectors, of oversized mark-ups or rents and of the emergence of superstar firms. The problem is that the labour share in digital-intensive sectors is already, on average, lower than in non-digital sectors and in addition is declining. The next main section elaborates on this issue.

Precarious work

In their 2019 flagship reports the ILO, OECD and UNDP share a common focus on the potentially adverse effects of new technologies, especially digital platform technologies, on the quality of work. This marks a welcome contrast with the conventional economics approaches that focus solely on the long-term beneficial capacities of technologies a) to raise productivity, earnings and work standards and b) to reduce workers’ exposure to hazards, especially in the agriculture, construction and mining industries. While recognising the long-term positive potential of current technological transformations, the ILO, OECD and UNDP emphasise three specific downside risks.

First, in direct contrast to economic theories of the upwards skill-bias of technical change, these international organisations now stress that automation and digitalisation can in fact reduce the richness of work content, leading to deskilling and a worsening of worker satisfaction (ILO, 2019: 43; UNDP, 2019: 213; OECD, 2019: 54). For example, the distribution of digital work to a globally dispersed online workforce involves the algorithmic unbundling of jobs into ‘micro tasks’, which significantly reduces the skill (and value) required for the overall job. The empirical evidence collected by the ILO, drawing on original international surveys of ‘microtask workers’, demonstrates that despite the high education of most online platform workers

4

the work tends to be (in the words of workers) ‘repetitive’, ‘boring’ and ‘mindnumbing’ (Berg et al., 2018: 84–85). This has wider implications for economic development, as the ILO report’s authors describe: The risk is that crowdwork, particularly microtask work, has the potential of deskilling work and also displacing or replacing some forms of skilled labour with unskilled labour, as jobs tend to be broken down into smaller tasks. Moreover, for developing countries (but true as well for industrialized countries), the public investments in education, particularly in science, technology, engineering and mathematics (STEM) undertaken to promote innovations and country-specific leadership in IT, risk being wasted or under-utilized. (Berg et al., 2018: 89)

Closely related to digital deskilling is the business practice of ‘management by algorithm’, a second downside risk. Research evidence demonstrates that the new models of digital management are associated with both intensive digital surveillance, which reduces worker control and autonomy, and illegal bias against certain workforce groups in recruitment, selection and job allocation decisions (Kellogg et al., 2020; Lambrecht and Tucker, 2019). As well as new challenges for employees, digital platform workers with uncertain legal status are also at risk of customer discrimination. There is increased potential for explicit or implicit customer discrimination against workers with the growing use of photographs and other personal data used to screen workers who provide domestic, transport and delivery services (Kotkin, 2019). The OECD is alert to current business surveillance practices 5 and alerts policy-makers to the risk that they ‘may have negative impacts on their (workers’) job quality and well-being’ (2019: 55; see also UNDP, 2019: box 6.3). In warning against digitised use of sensors, wearables and online monitoring, as well as potentially biased algorithmic job matching, the ILO goes further and calls for workers to have the right to access surveillance data ownership and for new governance rules for ‘algorithmic accountability’ (ILO, 2019: 44).

A third and major driver of more precarious work concerns the way that digital platforms have expanded the number of workers in the grey area of statutory rights between employee and self-employed, leading to proven legal cases of false self-employment. Despite the business rhetoric espoused by the digital platform companies, many of the jobs they offer do not provide the worker the required set of freedoms that would align with the legal status of self-employment. Depending on the legal context, these may include the freedom to set the level of earnings per gig, choice of hours of work, choice of work clothing, ability to contract with more than one business client, information about customers and ownership over data related to the transaction and business delivered (De Stefano and Aloisi, 2020). Overall, the increasing imbalance of market power means that precarious work is increasingly associated with advanced digital technologies. As the UNDP report puts it, ‘While crowdwork is a product of technological advances, it also represents a return to the past casual labour in industrialized economies, and in developing economies it adds to the casual labour force’ (2019: 208).

What role for labour institutions?

On the surface, each of the seven reports seem to follow the same policy narrative regarding the challenges posed by new technologies for decent work. For example, there is a common theme that digital platform technologies have evolved a pattern of working that conflicts with the standard open-ended formal contract, which has traditionally provided worker rights, trade union representation and social protection. However, there is no agreement on what ought to be done regarding reforms of labour and social policy institutions. This disagreement reflects in part the specific mandate and focus of these organisations, but also their openness to heterodox research outside of traditional macro and labour economics.

In its introduction, the 2019 World Development Report states, ‘Creating formal jobs is the first-best policy, consistent with the International Labour Organization’s decent work agenda, to seize the benefits of technological change’ (World Bank, 2019: 4). However, the report subsequently questions the relevance of existing labour laws in developed and developing countries, given what it perceives as the inevitable blurring of the formal and informal work boundaries spurred on by digital technologies (World Bank, 2019: 26–27). Drawing on recent World Bank technical papers and others (especially Bartelsman et al., 2016; Packard and Montenegro, 2017), the report brings back the argument from the 1980s that labour regulations reduce the speed of labour market adjustment and therefore slow down the capacity of an economy to benefit from new technologies and to increase productivity: … while regulations address labor market imperfections, they often reduce dynamism in the economy by affecting labor market flows and increasing the length of time spent in both employment and unemployment. When regulations are too strict and exclude many workers, … firms find it difficult to adjust the composition of their workforces. The ability to adjust is an important condition for adopting new technologies and increasing productivity. (World Bank, 2019: 116) The human-centred agenda requires equally urgent attention to the broader role of technology in advancing decent work . … Governments and workers’ and employers’ organisations need to invest in incubating, testing and disseminating digital technologies in support of decent work. (ILO, 2019: 43–44) Governments should ensure that all workers in the labour market have access to an adequate set of rights and protections, regardless of their employment status or contract type, and guarantee a level playing field among firms by preventing some from gaining a competitive advantage by avoiding their obligations and responsibilities. (OECD, 2019: 157) Realizing technology’s potential in the future of work depends on fundamental choices about work design, including detailed job-crafting discussions between workers and management. (UNDP, 2019: 211)

For the ILO, a reinvigoration of labour institutions extends to the international arena. Its Global Commission report calls for development financing to support strategic technology investments and an international governance system for digital labour platforms that obliges platforms and their business clients to respect minimum rights and protections (ILO, 2019: 44).

Income inequality and economic power

A very significant feature of the narrative about international economic policy and the future of work during 2019 was its general acknowledgement, as well as often detailed analysis, about the effects of income inequality – in particular the role of economic power in aggravating and reinforcing inequality and its adverse employment effects. This does not imply of course that we have arrived at a consensus among the World Bank, OECD and United Nations about the scale of the problem, its causes and what ought to be done. But it does mark a significant shift in narrative, especially at the World Bank, where notions of inequalities and economic power have not tended to figure prominently.

The declining labour income share as a key measure of inequality

Thanks to improvements in the collection of international data, high-profile economic analyses (especially Autor et al., 2017; Karabarbounis and Neiman, 2014) and its adoption as an indicator for one of the UN Sustainable Development Goals, 6 a measure of labour’s share of income is now routinely integrated into reviews of the international economy and appears as a key indicator of income inequality. This is certainly true of the seven reports reviewed here. Labour’s share of income is defined as the proportion of a country’s GDP that accrues to workers in the form of compensation, as opposed to capital income (profits and physical capital). Attention is likely to intensify in coming years thanks to further efforts by the ILO to improve labour income data – both by improving methodological techniques to incorporate estimates of self-employed workers’ earnings (who account for almost half the world’s workforce) and by expanding the sample of countries (Gomis, 2019).

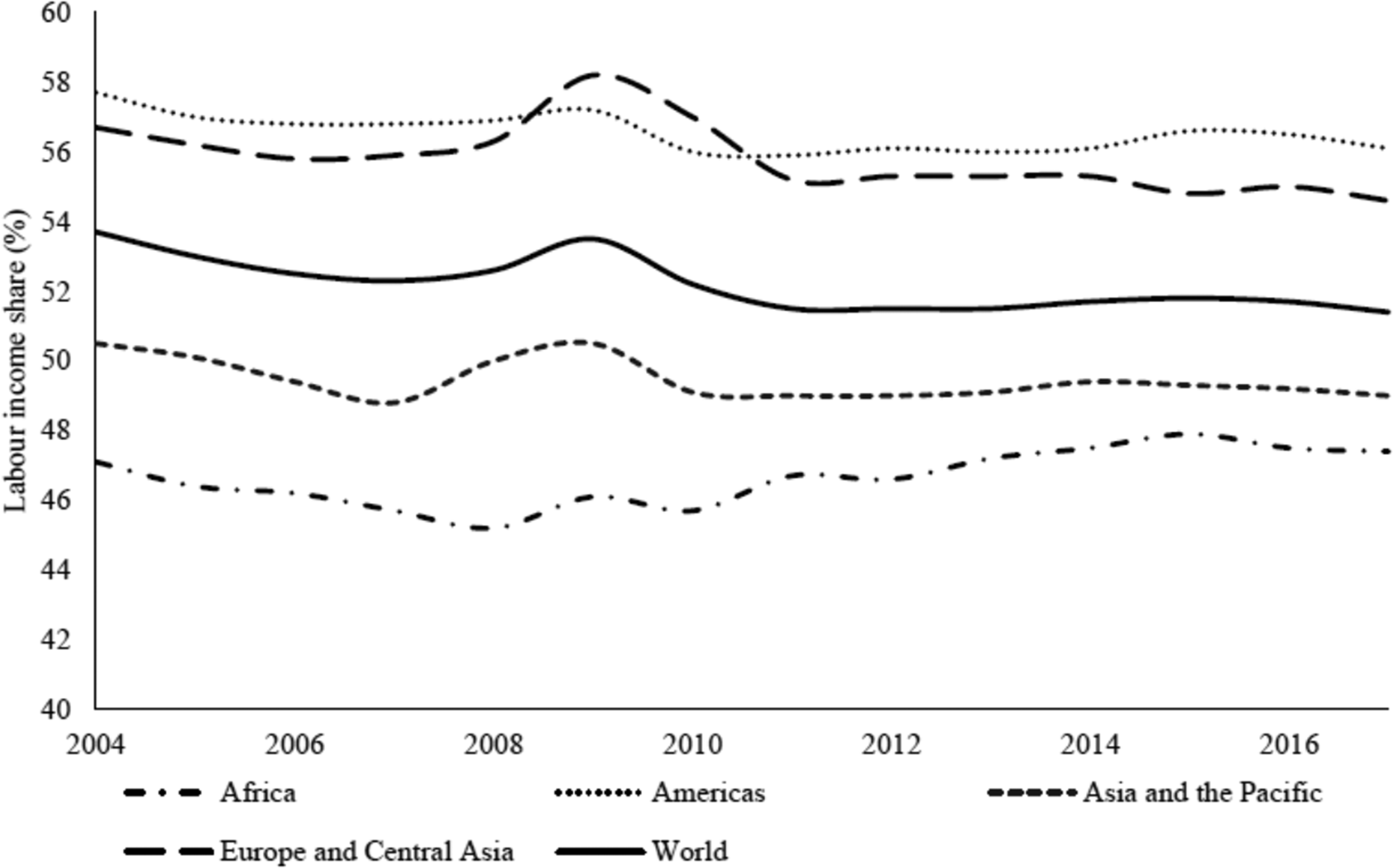

Analysis of labour income share data reveals three interesting features about income inequality. The first, and most widely cited, is that the labour share of income at the global level has declined significantly. The ILO data reproduced in Figure 2 suggest a drop of around two percentage points since 2004. This is corroborated by alternative estimations using different datasets: for example, the OECD reports a fall of 3.5 percentage points over the last two decades in 24 OECD countries (OECD, 2019); and longer trend international data suggest that the contemporary downward trend began in 1980, marked by a five percentage point fall during 1980–2012 (Karabarbounis and Neiman, 2014).

Global and regional labour income shares, 2004–2017.

The second feature is that the trend is not uniform around the world. In fact, a handful of high-income countries account for the bulk of the global decline in labour income share. This includes the United States, which experienced a fall of three percentage points during 2004–2017, along with Germany, the UK, Italy and Spain (Gomis, 2019: 25–26). More diverse patterns are apparent among low- and middle-income countries. For example, Brazil experienced a significant rise in labour income share during 2004–2017 (56 to 60%, among the highest rises), while Mexico fell from 39 to 35% (ILO data 7 ).

The third feature is the considerable disparity in absolute levels of labour income shares by region. There is some convergence over the 2004–2017 period shown in Figure 2, but the gap remains wide between the average labour income shares in Africa (around 47%) and the Americas region (56%). Workers in Africa are thus doubly penalised, suffering lower earnings as a function of both the level of development and a worse bargain with capital in distributing the shares of national income. Moreover, the gaps are even wider at the sub-region and country levels given the close positive association between a country’s income level and labour income share.

While the aggregate labour share of income is referenced in all seven reports, there is less systematic attention to the distribution of labour income, whether at global, regional or national level; it is only referenced in the ILO, OECD and UNDP reports. According to ILO data for 2017, the top decile of workers in the world earned almost half of total labour income (48%), while the bottom decile earned just 0.1% (ILO, 2020: Figure 3.5). In general, the poorer the region the greater the inequality in labour income distribution: in Africa, the richest half enjoy 28 times the share of total labour income as the poorest half, while in Europe and Central Asia the ratio is four times (ILO, 2020).Similarly, the UNDP observes that more unequal distributions of labour income are strongly associated with low levels of productivity. It argues that because the direction of causation is not clear, policies to raise productivity must be ‘consistent with a framework of inclusive income expansion’ (UNDP, 2019: 233).

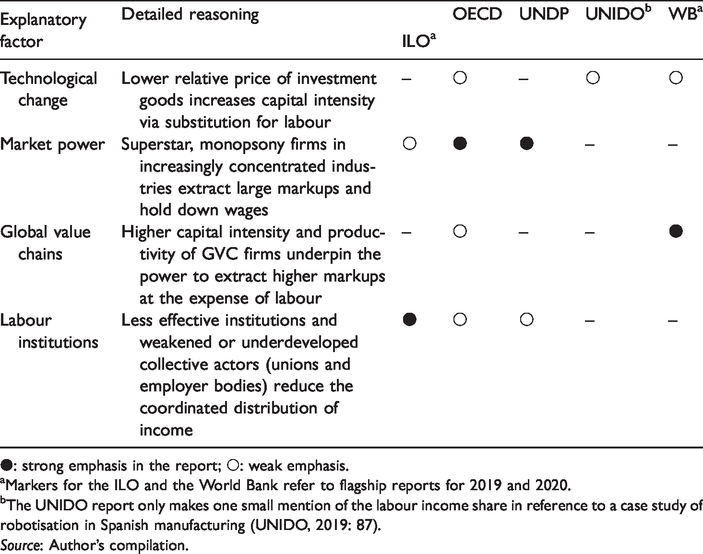

Technological change and the declining labour income share

The flagship reports advance various explanations for the declining labour income share (Table 4). A first explanation emphasises the role of technological change. The argument is that new ‘capital-augmenting’ technologies have tended to lower the price of investment goods (especially computing and communication technologies) compared to the price of labour and consumer goods, thereby increasing overall capital intensity and lowering the labour income share via labour-capital substitution effects. The widely referenced study by Karabarbounis and Neiman (2014) shows that there was an inflection point in the early 1980s beyond which the relative price of investment goods exhibits a steep downward trend all around the world (op. cit.: Figure 7). Their application of a macroeconomic model to the data finds a statistically significant association between labour income share and the relative price of investment goods (with a coefficient of 0.28), averaged out across 50 or so countries. 8 Controlling for changes in skill composition, their model further suggests that the falling price of investment goods can explain around half the total global decline of labour income share (op. cit.).

Explanatory factors associated with the declining labour income share: Selected flagship reports.

●: strong emphasis in the report; ○: weak emphasis.

aMarkers for the ILO and the World Bank refer to flagship reports for 2019 and 2020.

bThe UNIDO report only makes one small mention of the labour income share in reference to a case study of robotisation in Spanish manufacturing (UNIDO, 2019: 87).

Source: Author’s compilation.

This general result is repeated in the OECD (2019: 67) and World Bank (2020: 149) reports. While a seemingly robust result from state-of-the-art economic modelling, it nevertheless feels like an analytical short-cut. This is largely because of a reliance on relative prices as the key action variable and the assumed exogeneity of the change in technology. There are three substantive problems. The first is the failure to consider interaction, or feedback effects, between the model of economic growth associated with the new technology and the level of inequality as characterised by the labour income share. Early work by Dani Rodrik, picked up by many scholars since, demonstrated a negative association between inequality and economic growth (Alesina and Rodrik, 1994; Van der Weide and Milanovic, 2018).

A second problem is that in reality actors make investment decisions in a given institutional context, and it is this context that shapes the long-term distributional impact of capital-labour substitution practices. Diverse production systems (or varieties of capitalism) favour low or high inequality for a given technology, via a complex array of high or low financialised investment systems, strong versus weak institutionalised bodies of countervailing power (such as trade unions and employer bodies), skill-inducing or skill-degrading labour market rules and regulated versus deregulated product markets (Berg, 2015; Grimshaw et al., 2017; Roberts and Kwon, 2017). Relative prices open up the opportunities for hiring capital versus labour, but the distributional and growth impacts are contingent. The OECD report is certainly open to such an approach: … the cross-country evidence on rising inequality also shows that there is nothing inevitable about its rise. Policies and institutions matter and can play an important role in mitigating the impact of new technologies … on inequality (OECD, 2019: 71).

Market power and the declining labour income share

A second related explanation, especially emphasised in the OECD and World Bank narratives, is the growing concentration of market power among firms that has skewed the distribution of capital and labour in countries by increasing the profit rate or mark-up. The argument set out mainly in economics studies is that within many sectors of the economy an elite of ‘superstar firms’ and individuals have taken advantage of conditions that generate ‘winner takes most’ outcomes. Firms have rapidly scaled up by exploiting falling information and communications technology (ICT) and transport costs, easier access to consumer data and reduced tariffs, while a small class of high-income individuals have captured an increasing share of a country’s wealth (Allen, 2017; Autor et al., 2017; Brown and Lauder, 2012; Piketty and Zucman, 2014).

The underlying empirical analysis certainly confirms an increase in industry concentration in the United States and Europe. In an OECD working paper, Bajgar et al. (2019) find an increase in the market share of the top decile of firms in both manufacturing and services, as well as an increase when limited to the top eight firms. 9

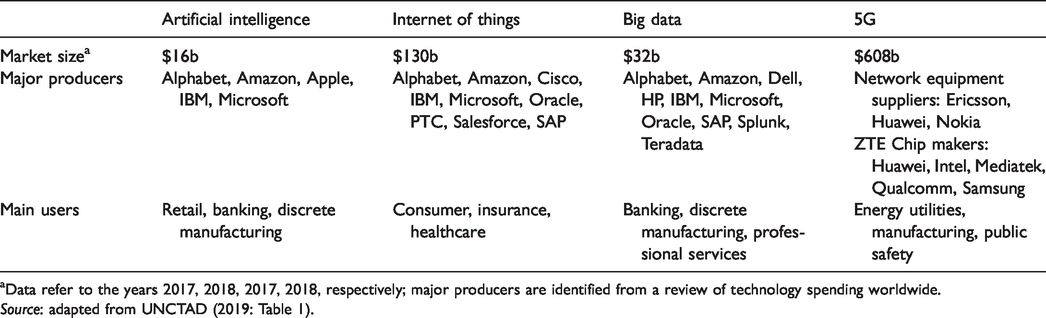

However, firm power is exercised both within an industry and, perhaps more importantly, on the basis of prowess in a given technology at an international level, which extends a company’s reach. For each of the ‘frontier technologies’ (artificial intelligence, internet of things, big data and 5G), a few large companies dominate through providing all-in-one platforms (hardware, software, servers, cloud platforms, etc.) to clients across all industries. The effect is to crowd out development of technologies by potential competitors (UNCTAD, 2020). Table 5 presents the estimated size of each frontier technology market and lists the major players.

Market size, major producers and clients of frontier technologies.

aData refer to the years 2017, 2018, 2017, 2018, respectively; major producers are identified from a review of technology spending worldwide.

Source: adapted from UNCTAD (2019: Table 1).

The dominance of an industry and/or technology by so-called superstar firms has increased concerns about the problematic consequences of labour market monopsony power for delivering fair rewards to workers (OECD, 2019: 68; UNDP, 2019: 208; World Bank, 2020: 223). This is a situation where a company can exert power by holding wages low because of the relative absence of job alternatives, influenced also by the degree of limited information about alternative jobs and/or workers’ mobility constraints (Manning, 2003). Therefore, the growing industry concentration and associated monopsony power exercised by employers contribute, at an aggregate level, both to a bifurcation between productivity growth and real wage gains and to a declining labour income share.

The World Bank and OECD are essentially making a ‘market failure’ argument, as if a perfectly competitive labour market devoid of labour institutions would establish a level playing field for workers to negotiate fair wages. Nevertheless, both organisations instrumentalise the evidence of monopsony power in labour markets to justify a strengthening of labour institutions to bolster workers’ wage bargaining power. While not listed among its headline policy recommendations, the World Bank report does align with the ILO and OECD in calling for collective bargaining and a transparent minimum wage policy implemented via tripartite social dialogue to protect workers’ earnings (World Bank, 2020: 195, 199). The World Bank also calls for investment in public transport and travel subsidies (e.g. to export processing zones) so as to improve workers’ mobility and employment possibilities, thereby potentially reducing the degree of monopsony power.

Global value chain power imbalances and income inequality

A further explanation of growing inequality concerns the way that GVCs reflect and reinforce global power inequalities among firms across different industries, particularly between developed and developing countries. The World Bank argues that GVCs, on average, deliver more productive jobs through scale effects that increase productivity and output (World Bank, 2020). The problem is that with a higher profit rate for firms, ‘GVCs also generate a force that results in a lower share of an economy’s income being paid to labor’ (op. cit.: 86). Its statistical analysis suggests the rise in GVC integration of firms around the world accounts for around one-quarter of the global decline in labour income share (op. cit.: Figure 3.17b). However, the chain of argument between increased productivity for GVC firms and a higher mark-up or profit for capital, as opposed to higher compensation for labour (or lower prices for consumers), is ambiguous. The 2020 report offers two possible reasons: first, increased concentration of market power among GVC superstar buyer firms (see above) reduces the likelihood of cost reductions being passed on to consumers, presumably due to restricted consumer choice; and second, GVC firms must cover the fixed costs of more complex global sourcing (op. cit.).

What is not fully incorporated into the World Bank's frame of analysis is the relationship between market power (meaning stronger GVC capital compared to non-GVC capital) and employer power (meaning stronger capital compared to labour). Furthermore, the World Bank’s own data analysis suggests that the general picture of higher mark-ups, higher productivity and falling labour income share is in fact a story about developed countries. Albeit without referencing any of the wider literature that already documents the unequal distribution of mark-ups in GVCs (e.g. Barrientos et al., 2011; Heintz, 2005; Kaplinsky, 2000), the World Bank report shows that buyer firms in developed countries have experienced fast growth in mark-ups since the late 1990s. By contrast, suppliers in developing countries have registered falling mark-ups, or mark-ups that are lower than non-GVC firms; empirical evidence is reported for Ethiopia, Poland, India and South Africa, among other countries, although China is referenced as a key exception to this pattern (World Bank, 2020: 84–86). This is a remarkable admission. As the World Bank puts it: ‘The risk that firms from developing countries experience limited profits after becoming suppliers for global firms mirrors the rise in profits in developed countries’ (2020: 86). The squeeze on suppliers in developing countries is especially significant since it signals increased stress on workers. In a further surprising admission, albeit restricted to the case of Bangladesh, the World Bank acknowledges that GVC suppliers exploit leverage over their workforces.

Moreover, because GVCs can emerge as enclaves or dominant sectors in developing country economies, there is a risk that employers take advantage of monopsony and political power in labor bargaining. For example, in Bangladesh garment factory owners have managed, despite repeated large-scale protests, to avoid any real term increase in garment factory wages. Depressed wages can be particularly problematic for low-income workers in developing countries where GVC integration is associated with rapid urbanization and where housing and transport costs are rising far more quickly than overall inflation rates (World Bank 2020: 199).

As such, the GVC contribution to the falling labour income share is in fact a narrative about global inequality among GVCs wherein higher mark-ups in (mostly) developed country GVC firms have both reduced labour’s share of income worldwide and reduced the share of capital among GVC firms located in developing countries. This more nuanced set of results may go some way to explaining the heterogeneous pattern of change in labour income share reported above. Capital has gained at the expense of labour in developed countries, but also, thanks to GVC power inequalities, at the expense of both capital and labour in developing countries. This points to a possible resurgence of patterns of global unequal exchange.

Finally, as with all statistical indicators that focus attention on a single percentage share figure, care is needed to disentangle what is happening to actual levels of labour income and capital income. In developing countries, less income may be accruing to both capital and labour, so whether or not the labour income share is rising or falling is really a secondary consideration.

The effect of labour institutions on income inequality

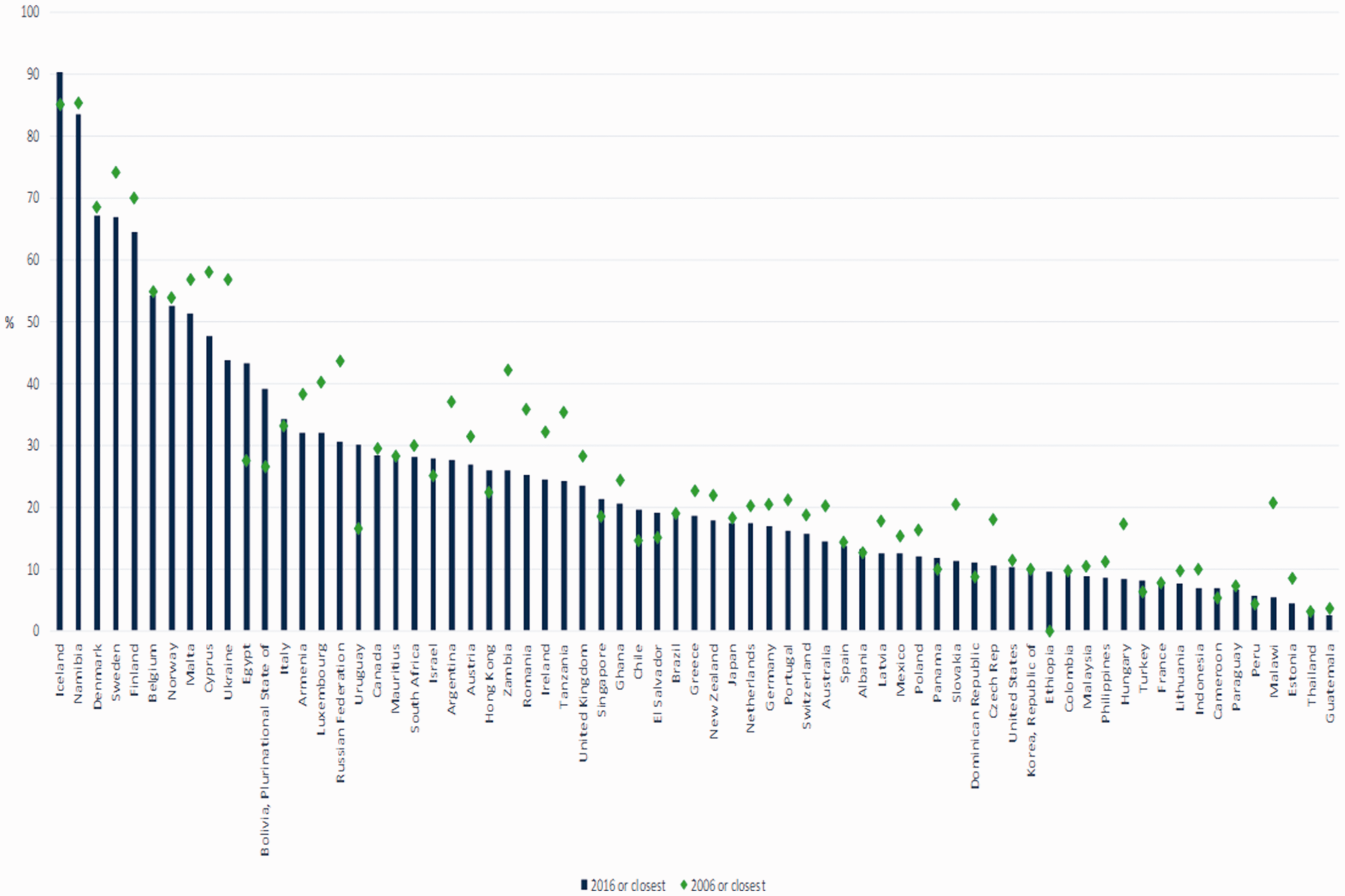

The weakening countervailing power of labour institutions is noted with more or less emphasis in four of the seven reports (not in UNIDO, 2019; World Bank, 2019, 2020) and explicitly tied to evidence of high-income inequality and declining labour income share. Three key features are highlighted with respect to income inequality. The first is the decline in the strength of trade unions. ILO data for a sample of 69 countries shows that between 2006 and 2016, 41 countries experienced a decline of more than one percentage point and just 16 a rise by more than one point. There is no obvious pattern by high or low union density or high or low country income. Countries with high declines include Zambia, Malawi and Russia, while those experiencing large increases in union membership include Egypt, Uruguay and Bolivia (Figure 3). In a context of increasingly concentrated corporate power (above), as well as financialisation (Kus, 2012), the decline in power of workers’ organisations is argued to have failed to combat rising inequality within countries (ILO, 2019: 41; OECD, 2019: 66–67; UNDP, 2019: 234).

Change in trade union density, 2006--2016.

The second feature is the limited success of workers’ organisations in expanding membership to workers in non-standard employment and, especially, to informal workers. The fragmentation of services and goods production, associated with domestic and global supply chains, has further complicated boundaries between standard and non-standard, formal and informal work and made the organising job of unions more difficult. The OECD (2019) devotes most of its very welcome chapter on collective bargaining to this issue, drawing especially on European research to highlight obstacles and opportunities, including strategies to reduce use of non-standard and informal workers, to establish a bridge to standard contracts, or to extend protections to workers outside the standard employment relationship (e.g. Benassi and Dorigatti, 2015). The ILO (2019) warns of the major challenges confronting unions in organising workers outside standard employment contracts and traditional workplaces. More inclusive union organising strategies would contribute to formalisation of work (ILO, 2019: 42). This would extend employment and social rights to more workers and in turn amplify their voice to bargain for a higher claim to income, improving the aggregate labour income share. The World Bank (2020: 88–90) does briefly acknowledge that ‘GVC participation can increase casual employment’ and lists examples of displacement of farmers, poor worker conditions and violations of core labour standards. However, it does not identify the potential role of trade unions, instead calling for private firms and international policy action to play a role.

The third feature concerns the ineffectiveness of wage-setting institutions (collective bargaining and minimum wages) to shore up the labour income share and reduce inequality. There is strong empirical evidence to suggest that minimum wages and collective bargaining coverage combine to lower wage inequality (Grimshaw et al., 2014; Hayter, 2015), although the evidence tends to focus on the impact of wage institutions on the lower half of the distribution. The UNDP report goes further and shows for the first time the power of minimum wages to reduce the extreme inequality of labour income; it shows a strong positive association between the value of a country’s minimum wage and the share of labour income earned by the richest 10% (2019: Figure 7.4).

The World Bank stands in stark opposition to this position. It still assumes, despite longstanding intellectual arguments by Nobel-prize winning economists and developing country evidence to the contrary (Ghosh, 2016; Solow, 1990), including World Bank papers (Bhorat et al., 2017), that labour institutions distort an assumed natural state of labour market functioning. It argues that minimum wages (and other labour regulations) ‘ensure that informality is appealing for all but the most productive workers before the economy grows’ (World Bank, 2019: 31). This is one part of the World Bank’s (2019) broader strategic policy position to call governments to shift from ‘regulation-based redistribution’ to ‘direct social welfare support’. In other words, it seeks to shift responsibility and financial contributions from private business to the government. The UNDP report presents an articulate response. It argues that minimum wages can be effective in a context of informality precisely because the informal sector is not perfectly competitive. Rather it is characterised by a major imbalance of employer--worker power, lack of information and incomplete contracts (associated with a risk of wage theft, for example) (see also Basu et al., 2015). Therefore, in the same way that wage-setting institutions correct an imbalance of power in formal labour markets, all the more reason for them to play an effective role in informal labour markets and thereby extend the zone of formal work and contribute to a fairer distribution of income (UNDP, 2019: 235–236).

Conclusion

In a critical review of seven prominent flagship reports from five of the leading international organisations – the ILO, OECD, UNIDO, UNDP and World Bank – this article has explored how the policy narratives set out during 2019 and early 2020 have characterised the major future of work challenges associated with new technologies and inequality. In many areas, it identifies a perhaps surprising consensus of viewpoints. For example, all five international organisations embrace the relatively nuanced economics account of job change caused by new technologies, which identifies direct and indirect countervailing effects via numerous ripple effects throughout the economy. This stands in stark contrast to some of the highly cited academic and management consultancy reports of recent years which insist on massive job displacement by robots and artificial intelligence. There is also a concerted effort by all five organisations to highlight the global unevenness of employment effects caused by new technologies, whether by level of development, industry, skill or gender. Furthermore, and perhaps most surprising, all five organisations acknowledge that the global labour income share is declining and that this is a fundamental concern for economic governance. These common viewpoints mean that all five organisations can share platforms and possibly join up on research programmes on broad questions of new technologies, inequalities and the future of work.

For an industrial relations audience, however, this article has illuminated key points of differentiation, which may be said to reflect the overarching ethos and mission of each international organisation, as well as its openness to heterodox thinking about how labour markets function in contemporary society. This can be illustrated in the approach to evidence of a declining labour income share. In its headline narrative, the World Bank draws a strong association with the increase in productivity in digital-intensive sectors, falling price of capital investment and higher profits or mark-ups. The falling labour income share is presented as an unfortunate consequence of a more dynamic economy. The problem is that this ignores the potentially destabilising interaction between rising inequality and economic growth. Furthermore, it assumes the uneven distributional impact of new technologies is a given rather than shaped, for example, by labour institutions, and it sidesteps the considerable (and diverging) global inequalities in trends in both capital and labour income levels. In its 2020 flagship report, the World Bank does in fact present evidence of poor working conditions and falling business mark-ups in global value chain suppliers in developing countries (World Bank, 2020: 86), but this does not feed into the central narrative.

By contrast, the ILO, OECD and UNDP express serious concerns about the relationship between new technologies and growing inequalities on the one hand and a growth in precarious work, growing corporate power in key industries and erosion of labour bargaining power on the other. The UNIDO flagship report is especially powerful in its emphasis on major structural inequalities between countries by level of development and technological capacities. These organisations therefore provide a more grounded analysis of, and recommendations for, the kinds of reinvigorated labour institutions required to confront and shape the challenges facing the future of work, from pursuing more inclusive union-organising strategies to extending rules governing the standard employment relationship in order to embrace non-standard and informal work arrangements. The ILO's (2019) Global Commission report is especially powerful in calling for new institutions at the international level, including measures of the distributional dimensions of economic growth and governance systems to regulate digital labour platforms and their client businesses.

Many areas highlighted in this article point to knowledge gaps and avenues for further research. First, while there is much industrial relations research on the exploitative character of certain forms of digital platform work, there is a need to understand the potential for advanced digital technologies to advance an agenda of decent work, attentive to differences by country level of development, gender and skill: What institutional conditions can best advance a ‘human-in-command’ approach to applying such technologies? What is the relationship between a country’s positioning in leading or following developments in digital technologies (including within global value chains) and its capacity to leverage benefits for its workforce? Are trade unions sufficiently resourced to navigate (and negotiate) this fast changing dynamic between new technologies and decent work? A second research agenda could explore the new ILO data on labour income share to interrogate the relationship between labour income distribution and (a) patterns of productivity by industry and country (particularly in light of the finding that labour income inequality is strongly associated with low productivity – UNDP, 2019: 233) and (b) different industrial relations systems so as to test the thesis that stronger, more inclusive systems are associated with greater equality.

Footnotes

Acknowledgements

Thanks very much to the editor and reviewers, as well as Uma Rani (ILO) and Jill Rubery (University of Manchester), for very helpful comments on an earlier draft.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship and/or publication of this article.