Abstract

The COVID-19 pandemic spurred an economic downturn that may have eroded population mental health, especially for renters and homeowners who experienced financial hardship and were at risk of housing loss. Using household-level data from the Census Bureau's Household Pulse Survey (n = 805,223; August 2020–August 2021) and state-level data on eviction/foreclosure bans, we estimated linear probability models with two-way fixed effects to (1) examine links between COVID-related financial hardship and anxiety/depression and (2) assess whether state eviction/foreclosure bans buffered the detrimental mental health impacts of financial hardship. Findings show that individuals who reported difficulty paying for household expenses and keeping up with rent or mortgage had increased anxiety and depression risks but that state eviction/foreclosure bans weakened these associations. Our findings underscore the importance of state policies in protecting mental health and suggest that heterogeneity in state responses may have contributed to mental health inequities during the pandemic.

The economic tsunami that followed the onset of the COVID-19 pandemic left very few American households untouched. As unemployment soared to 15% and work hours and wages fell (Bureau of Labor Statistics, U.S. Department of Labor 2020), many found themselves unable to pay bills, provide food for their families, or cover other basic expenses. The economic crunch faced by millions of Americans was particularly evident in levels of housing insecurity, which left millions of renters and homeowners struggling to remain in their homes. By September 2020, roughly one in six renter households was behind on rent and at threat of eviction (Llobrera et al. 2020). Similarly, mortgage delinquency rates in early 2020 reached their highest point since 2010 (DeSanctis 2020). By fall 2021, an estimated 7.5 million homeowners faced foreclosure because they were unable to keep up with mortgage payments (Center on Budget and Policy Priorities 2022).

The economic hardships that accompanied the COVID-19 pandemic, including the rising threat of housing loss, likely had detrimental effects on mental health. Financial hardships, such as having difficulty paying for household expenses or experiencing the threat of housing loss, have clear, negative effects on health, particularly mental health (Donnelly and Farina 2021; Fowler et al. 2015; Hoke and Boen 2021; Houle 2014; Kim 2021). Experiencing financial hardship can increase stress and worry and reduce spending on health-related goods and services in ways that negatively affect well-being (Boen and Yang 2016). It is also likely, however, that state policy responses to the pandemic may have played an important role in shaping individual- and population-level health. In particular, state-level policies that reduced evictions and foreclosures may have buffered the detrimental mental health impacts of financial hardship during the COVID-19 pandemic.

In response to the looming housing crisis, Congress enacted a federal eviction ban in March 2020 that ended in July 2020, and the U.S. Centers for Disease Control and Prevention (CDC) later enacted a national eviction moratorium in September 2020. Struggling homeowners were also protected by a federally backed mortgage forbearance allowance (i.e., an option to suspend mortgage payments, ultimately for 18 months) and a moratorium that prevented lenders from initiating foreclosure proceedings for homeowners struggling financially as a result of the pandemic (U.S. Government Accountability Office 2021). Still, these federal policies had limitations and did not protect all renters and homeowners at risk of eviction or foreclosure.

Importantly, these federal policies were layered on top of a patchwork of housing policies that a majority of states introduced between 2020 and 2021. As a result, individuals and families were subject to a range of housing security policies that varied both across both time and place. Recent research documents that these policies were beneficial for population health, in part because their implementation decreased state-level COVID-19 incidence and mortality rates, particularly for the most economically vulnerable households (Leifheit, Linton, et al. 2021; Nande et al. 2021; Sandoval-Olascoaga, Venkataramani, and Arcaya 2021).

Whether eviction and foreclosure bans protected mental health is less clear. Given documented links between housing loss and mental health (Burgard, Seefeldt, and Zelner 2012; Cagney et al. 2014; Desmond and Kimbro 2015; Fowler et al. 2015; Hoke and Boen 2021; Houle 2014), we hypothesize that the benefits of state-level eviction and foreclosure moratoria extend beyond COVID-19 infection and prevalence to mental health. By lowering eviction and foreclosure risks for households experiencing financial hardship, these bans may have reduced stress for cost-burdened, economically vulnerable households in ways that affected—and in some cases, protected—mental health. The bans may have been especially important for those experiencing financial hardship insofar as those who report difficulty in meeting usual expenses or keeping up with rent or mortgage payments may have been at heightened risk of eviction or foreclosure and—by consequence—poor mental health. To date, studies provide preliminary support for this notion, with recent research indicating that eviction bans may have reduced mental health risks for renters (Ali and Wehby 2022), generally, and low-income renters (Leifheit, Pollack, et al. 2021), in particular.

In this study, we propose that the pandemic may have negatively affected mental health in part by increasing financial hardship and risks of housing loss and that state-level eviction/foreclosure bans may have moderated this association. We use data from the Census Bureau's Household Pulse Survey (CHHPS) merged to state-level data on the timing eviction bans from the COVID-19 U.S. state policy database (Raifman 2020) to assess whether financial hardship predicted anxiety and depression risks and then consider whether state-level eviction/foreclosure bans potentially alleviated the negative mental health effects of financial hardship. Our large, nationally representative sample includes more than 800,000 individuals under the age of 65, observed between August 2020 and August 2021, a larger sample and later period than most previous work on this topic (e.g., Ali and Wehby 2022; An, Gabriel, and Tzur-Ilan 2021; Donnelly and Farina 2021; Leifheit, Pollack, et al. 2021). We focus our analyses on measures indicating anxiety and depression risks, critical outcomes given the large increase in mental health risks experienced during the pandemic (Vindegaard and Benros 2020).

Our study makes several contributions. First, in contrast to previous research focusing on renters (e.g., Ali and Wehby 2022; An et al. 2021; Leifheit, Pollack, et al. 2021), we study both renters and homeowners. As described, many state eviction bans protected homeowners from foreclosure (National Consumer Law Center 2022; Raifman 2020; Silcox 2020; The White House 2021). For this reason, we include both renters and homeowners in our investigation. Second, our models include both state and week fixed effects. State fixed effects account for time-invariant state-level sources of unobserved heterogeneity, and week fixed effects control for underlying national time trends, including federal policies. This estimation strategy is more than a simple analytic tweak on several previous studies. Rather, this approach provides a rigorous test of how financial hardships resulting from the pandemic were associated with anxiety and depression while better accounting for sources of between-state heterogeneity and period shocks. Third, in order to more fully capture the financial devastation of the pandemic for American households, we use a broad definition of financial hardship that includes both difficulty paying rent or mortgages and meeting usual household expenses. Finally, while much previous work on the impacts of state policies on health during the pandemic has focused on COVID-19 infection and mortality (e.g., Leifheit, Linton, et al. 2021; Nande et al. 2021; Sandoval-Olascoaga et al. 2021), we provide evidence of the role of state eviction policies in mitigating the pandemic’s indirect harms on population health. Our results offer new insights into how the historic economic downturn spurred by the pandemic shaped mental health while also highlighting the critical role of state policies in protecting the well-being of financially vulnerable households.

Background

COVID-19 Financial Hardship and Population Mental Health

In addition to the devastating toll that the COVID-19 pandemic had on physical health and longevity, the pandemic-related economic downturn also likely had effects on population mental health. A large body of research from across disciplines links negative financial shocks, such as job and income losses, to increased mental health risks (Brand, Levy, and Gallo 2008; Donnelly and Farina 2021; Gallo et al. 2000; Kuhn, Lalive, and Zweimüller 2009; Noelke and Beckfield 2014; Pool et al. 2017). This association reflects, in large part, increases in stress and worry that accompany the uncertainty of such financial shocks (Boen and Yang 2016).

One factor that was likely to worsen mental health during the pandemic was the rising threat of housing loss. The massive job losses and wage cuts that followed the onset of the pandemic made meeting housing expenses especially difficult for many American households. In the early months of the pandemic, U.S. workers lost roughly 22 million jobs, with unemployment hitting a record high 14.7% in April 2020 (Bureau of Labor Statistics, U.S. Department of Labor 2020). Just over half of these losses were recovered by October 2020, but the recovery was uneven (Bureau of Labor Statistics, U.S. Department of Labor 2020). Even among workers who did not lose their jobs, an estimated 60% experienced a wage cut or freeze between March and June 2020 (Cajner et al. 2020). Job and income losses were especially concentrated among workers in lower wage occupations, who were disproportionately Black and Hispanic (Amburgey and Birinci 2020; Cajner et al. 2020). These economic losses exacerbated an already widespread housing affordability crisis in the United States. Prior to the pandemic, millions of American households forcibly lost their homes each year, and a striking number of households experienced extreme housing cost burden (Desmond 2015). With the onset of the pandemic, the number of households at risk of losing their homes increased nearly exponentially (Llobrera et al. 2020).

A growing body of research documents the health-harming effects of forced housing loss (Desmond and Kimbro 2015; Fowler et al. 2015; Hoke and Boen 2021), including detrimental mental health impacts of housing loss following foreclosure (Cagney et al. 2014; Houle 2014; Houle and Light 2014). Forced housing loss exposes individuals to a host of health risks, including heightened levels of psychosocial stress (Hoke and Boen 2021). Eviction has been linked to disrupted health care access and use (Schwartz et al. 2022) and increased risks of unhealthy and substandard housing conditions, including overcrowding and physical risks, such as lead and asbestos exposure (Desmond 2012). Together, these negative outcomes resulting from being forcibly removed from one’s home can adversely impact mental health. Even the mere threat of eviction or foreclosure can increase stress and worry in ways that affect mental health (Desmond 2016). To the extent that low-income and Black and Hispanic people experienced especially high levels of housing instability and insecurity both before and during the pandemic (Benfer et al. 2021; Hepburn, Louis, and Desmond 2020), they may have also seen the greatest reductions in mental health as a result of the COVID economic downturn.

A Patchwork of Policies: State Eviction and Foreclosure Bans

In recognition of the rising threat of housing loss and the adverse consequences of eviction and foreclosure during the pandemic, both the federal government and states enacted legislation to reduce viral transmission and, simultaneously, curtail forced housing loss. At the federal level, Congress enacted the Coronavirus Aid, Relief, and Economic Security Act in late March 2020, which included a 120-day eviction moratorium that was in effect until July 25, 2020. In September 2020, the CDC enacted a moratorium on evictions; this was later deemed unconstitutional by the U.S. Supreme Court. Later, the American Rescue Plan of 2021 included a number of provisions aimed at preventing housing loss among both renters and homeowners, including emergency rental assistance, homeowner assistance funds, mortgage forbearance, moratoria on foreclosure, and other relief measures aimed to help low-income homeowners. Importantly, these federal policies did not protect all renters and homeowners. For example, the CDC moratorium did not block all stages of the eviction process and allowed landlords to initiate eviction proceedings, which could still create pressures for tenants to leave their homes and have long-term detrimental effects on households’ financial records.

Given the limitations of these federal policies and actions, a majority of states and the District of Columbia also implemented their own eviction and foreclosure bans beginning in March 2020. Notably, state-level bans on eviction and foreclosure did not necessarily mirror state-level prepandemic risk of housing loss. For example, in the years leading up to the pandemic, state eviction rates ranged from less than 1% (e.g., Idaho and New Jersey) to closer to 10% (e.g., South Carolina; Desmond et al. 2018). During the pandemic, however, Idaho and South Carolina both enacted very brief bans (lasting only between March and May 2020), whereas New Jersey’s ban, also enacted in March 2020, was in place through the beginning of 2022 (Raifman 2020).

Evidence suggests that these bans were effective in blunting the worst of COVID-19’s direct toll on morbidity and mortality. Research exploiting the time-varying nature of the implementation and repeals of state-level eviction/foreclosure bans documents that these bans significantly reduced state-level COVID-19 incidence and mortality rates (Leifheit, Linton, et al. 2021; Nande et al. 2021; Sandoval-Olascoaga et al. 2021). Importantly, the impact of state-level eviction/foreclosure bans on COVID-19 infection risks were particularly pronounced for lower socioeconomic status (SES) individuals (Sandoval-Olascoaga et al. 2021). Consistent with other work showing that state policies are particularly important for protecting health among the most socioeconomically vulnerable (Donnelly and Farina 2021; Montez et al. 2019, 2020), findings from these studies indicate that these bans may be most protective for those at greatest risks of both eviction and infection. In addition, a handful of studies have assessed the effect of eviction bans on mental health. For example, Ali and Wehby (2022) and Leifheit, Pollack, et al. (2021) found that eviction moratoriums were associated with reduced risks of mental distress among renters. Analyses by An et al. (2021) showed that eviction moratoria reduced evictions, redirected scarce financial resources to health-related consumption needs (including food), and reduced mental stress, especially for Black households.

Hypotheses

We build on and extend research in this area by assessing two hypotheses. First, we examine how financial difficulties reported by renters and homeowners during the pandemic were associated with mental health risks. Drawing on work showing that financial difficulties and losses have negative consequences for health (Boen and Yang 2016; Brand et al. 2008; Donnelly and Farina 2021; Gallo et al. 2000; Kim 2021; Kuhn et al. 2009; Noelke and Beckfield 2014; Pool et al. 2017), we hypothesize that individuals who report difficulty paying for household expenses and keeping up with rent or mortgage payments during the pandemic will have worse mental health than individuals not reporting these financial difficulties. That is:

Hypothesis 1: Renter and homeowner households reporting difficulty paying rent or mortgage and other household expenses have higher levels of anxiety and depression than households not reporting these financial difficulties.

We test Hypothesis 1 primarily to confirm prior research findings on the mental health impacts of financial hardship—in this case, under pandemic conditions—and to allow us to test our second hypothesis: that living in a state with an active eviction/foreclosure ban moderates the association between household financial difficulties and mental health risks. Although the mental health consequences of financial difficulties during the pandemic were likely widespread, state bans on evictions/foreclosures may have lessened the mental health consequences of financial hardship by reducing the risks of housing loss. A growing body of research shows how state policy contexts shape health in part by strengthening or weakening the associations between individual- and household-level socioeconomic factors and health (Donnelly and Farina 2021; Montez et al. 2019). State-level eviction and foreclosure bans protected financially vulnerable households from housing loss, potentially reducing eviction- or foreclosure-related stress and allowing these households to redirect consumption to health-related needs. Thus, we hypothesize that the associations between financial difficulties and mental health will be weaker when states have active eviction/foreclosure bans than when they do not have active bans. That is:

Hypothesis 2: State-level eviction bans moderate the associations between financial difficulties and mental health, with the association being weaker for renter and homeowner households living in states with active eviction/foreclosure moratoria.

Data and Methods

Data and Sample

Data for this study came from two sources. First, our household-level data came from the Census Bureau's Household Pulse Survey (CHHPS), a repeated cross-sectional national household survey originally administered by the Census and five other federal agencies (the Pulse is currently fielded by a large group of federal agencies). The survey was designed to gather information on the pandemic’s effects on well-being. Data collection began in April 2020 and is ongoing at the time of writing, and surveys were administered on either a weekly or biweekly basis. Our analyses included data from 22 separate waves, starting in mid-August 2020 (CHHPS Week 13) and ending in early August 2021 (CHHPS Week 34). We began our analysis in August 2020 because the CHHPS questions about difficulty paying for household expenses were not asked until CHHPS Week 13. The CHHPS sample is nationally representative and includes detailed household-level data on economic hardship, health, and sociodemographic characteristics. The survey had sufficient sample size to allow us to compare patterns and model outcomes within and across states. The CHHPS is also unique in that it allows for examining how patterns of economic hardship and health have evolved across the course of the pandemic.

Second, we used state-level policy data from the COVID-19 U.S. state policy database (Raifman 2020), which included time-varying, state-level information on the implementation and repeal of state eviction moratoria. Although labeled “eviction” bans in the data, many of these policies also protected homeowners from forced housing loss. The CHHPS data include state identifiers, allowing us to link household-level survey data from CHHPS to state-level eviction moratoria data to conduct our analyses.

We restricted our CHHPS sample to individuals under 65 years old, and we included both renters (22% of the full CHHPS sample) and homeowners who had mortgages or loans on their homes (43% of the full CHHPS sample). We did not include in our analytic sample homeowners who owned their homes outright without mortgages or loans (14% of the full sample) because these households presumably would not be responsive to eviction bans. As we describe later, however, we ran supplementary falsification tests with this group of homeowners. We also excluded individuals who reported occupying a home without paying rent (1% of the full sample) and individuals who did not report their housing status (20% of the full sample). Missing data on the other covariates was minimal (<1% missing on all other variables). Compared to those included in our analytic sample, respondents who did not report their housing status had slightly lower mental health risks; were more likely to be Black, Hispanic, or Asian; were more likely to have a high school degree or lower; and were more likely to be married or never married. A majority of respondents participated in only one weekly survey, but some participants participated in two or three surveys. For respondents with repeated observations, we used only their first observation. Our main analytic sample included 805,223 individuals observed in survey Weeks 13 to 34 of the CHHPS. Sample sizes varied by outcome and key exposure.

Measures

We modeled two mental health outcomes from the CHHPS that indicate anxiety and depression risks. First, we used the validated two-item Generalized Anxiety Disorder scale (GAD-2). The GAD-2 asked how often, over the past seven days, respondents had uncontrollable levels of worrying or felt nervous or on edge. Second, as a measure of depressive risk, we used the validated two-item Patient Health Questionnaire (PHQ), which asked respondents how often, over the past seven days, they have had little interest in doing things or were feeling depressed or hopeless. For each question, responses ranged from 0 (not at all) to 3 (every day). We summed scores across the two items in each scale. We classified respondents who scored a 3 or higher on the GAD-2 or the PHQ as having probable anxiety and depression, respectively. For both measures of mental health, a score of 3 or higher has been shown to indicate high probabilities of these disorders (Staples et al. 2019). Importantly, these measures have been used effectively in previous studies of population mental health (e.g., Donnelly and Farina 2021; Kim 2021). Supplementary analyses using count versions of the outcomes and negative binomial models produced substantively similar results to those included here.

We used three measures of household-level financial hardship from the CHHPS: difficulty paying expenses, not caught up on rent payments, and not caught up on mortgage payments. 1 To assess whether households were having difficulty paying expenses, all respondents (e.g., both renters and homeowners) were asked, “In the last 7 days, how difficult has it been for your household to pay for usual household expenses, including but not limited to food, rent or mortgage, car payments, medical expenses, students loans, and so on?” Possible responses included “not at all difficult,” “a little difficult,” “somewhat difficult,” and “very difficult.” We coded households that responded somewhat or very difficult as having difficulty paying expenses (1 = has difficulty). To determine whether households were behind on rent or mortgage, renters were asked, “Is this household currently caught up on rent payments?,” and homeowners who reported having mortgages or loans were asked, “Is this household currently caught up on mortgage payments?” We coded respondents who answered “no” as being not caught up on rent/mortgage (1 = not caught up). We included these measures of household financial hardship in our analyses because households who report having difficulty paying usual household expenses and/or are not caught up on rent or mortgage payments may be at particularly high risk of eviction/foreclosure and therefore especially vulnerable to state-level eviction/foreclosure moratoria.

Information about whether and when states had active eviction/foreclosure moratoria in place comes from the COVID-19 U.S. state policy database (Raifman 2020). Importantly, many state eviction/foreclosure moratoria aimed to prevent housing loss for both renters and homeowners. Our measure of state-level eviction/foreclosure moratorium was time-varying and was coded as 1 if the state had an active policy in place and 0 if it had no active policy in place.

We included several control variables in our models, based on prior literature suggesting that these factors may be correlated with both economic hardship and mental health, including sex, race-ethnicity, educational attainment, marital status, and household structure (Baker et al. 2022; Clarke et al. 2011; McLanahan and Percheski 2008; Simon 2014; Williams 2018; Williams et al. 2010). We acknowledge that while these measures were included as individual-level variables in our analyses, in many ways, these measures proxied structural and institutional conditions and arrangements that pattern both financial and mental health risks. We measured sex with a dummy variable (1 = female) to control for well-documented sex differences in mental health. We measured respondents’ race-ethnicity with a series of dummy variables coded as non-Hispanic White, non-Hispanic Black, Hispanic, non-Hispanic Asian, and non-Hispanic other race-ethnicity. We adjusted for race-ethnicity to control for patterns of financial hardship and mental health that may be affected by racism, discrimination, and other race-related processes and stressors that could affect our estimation. We ran supplementary models stratified by race-ethnicity to ensure that the results were largely consistent across groups, and indeed they were. To adjust for potential sources of individual- and household-level confounding, we also adjusted for educational attainment (using a series of dummy variables indicating high school or less, some college, and bachelor’s degree or higher) and marital status (using a series of dummy variables indicating currently, previously, and never married). We also included several other measures of household structure, including whether the household has children (1 = yes), the number of children in the household, and the total number of individuals in the household. All models included survey year-week and state fixed effects.

Methods

We first present descriptive statistics for the full sample and stratified by homeownership (renters vs. homeowners). We also show descriptive information about the timing of state eviction policies.

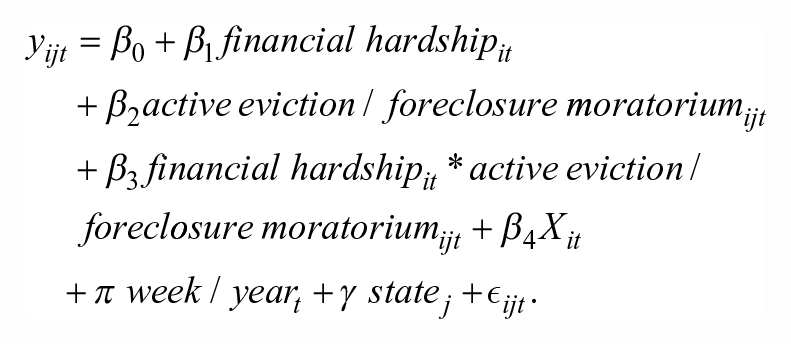

To examine associations among household financial hardship, state eviction/foreclosure bans, and mental health, we estimated linear probability models for each outcome separately with week-year and state fixed effects. We stratified our models by homeownership status (renters vs. homeowners). We used linear regression instead of logistic regression, given evidence that linear models produce less biased estimates than logistic regression models when fixed effects are included in models of binary outcomes (Gomila 2021). Model 1 estimated the associations between the measures of financial hardship and the outcomes, adjusting for all covariates except for whether the state had an active eviction/foreclosure ban. Model 2 was the fully adjusted model that took the following generic form:

In the aforementioned equation, we modeled mental health outcomes y of individual i in state j at time t as a function of the two household financial hardship measures (separately; β1), whether the individual is living in a state that has an active eviction/foreclosure moratorium at the time of the survey (β2), and the covariates (β4). In these models, we allowed the association between the household financial hardship measures and mental health to vary according to whether the respondent’s state has an active eviction/foreclosure moratorium at the time of the survey (β3). Importantly, all models included both week-year (π) and state (γ) fixed effects. Week-year fixed effects absorbed national time trends (e.g., federal policy changes), and state fixed effects accounted for time-invariant confounders at the state level (e.g., stable levels of state racial composition or state policy liberalism that would be relatively invariant in the relatively short time period included in our analyses). Conceptually, by including both time and state fixed effects, our models compared the mental health risks of individuals living in the same state over time. Variation in survey dates and in the timing of state eviction/foreclosure bans produced substantial variation in exposure to these bans over the period of observation.

We weighted all descriptive statistics and multivariable models to account for survey design effects, and we clustered all standard errors in regression models by state.

Results

Descriptive Statistics and Time Trends

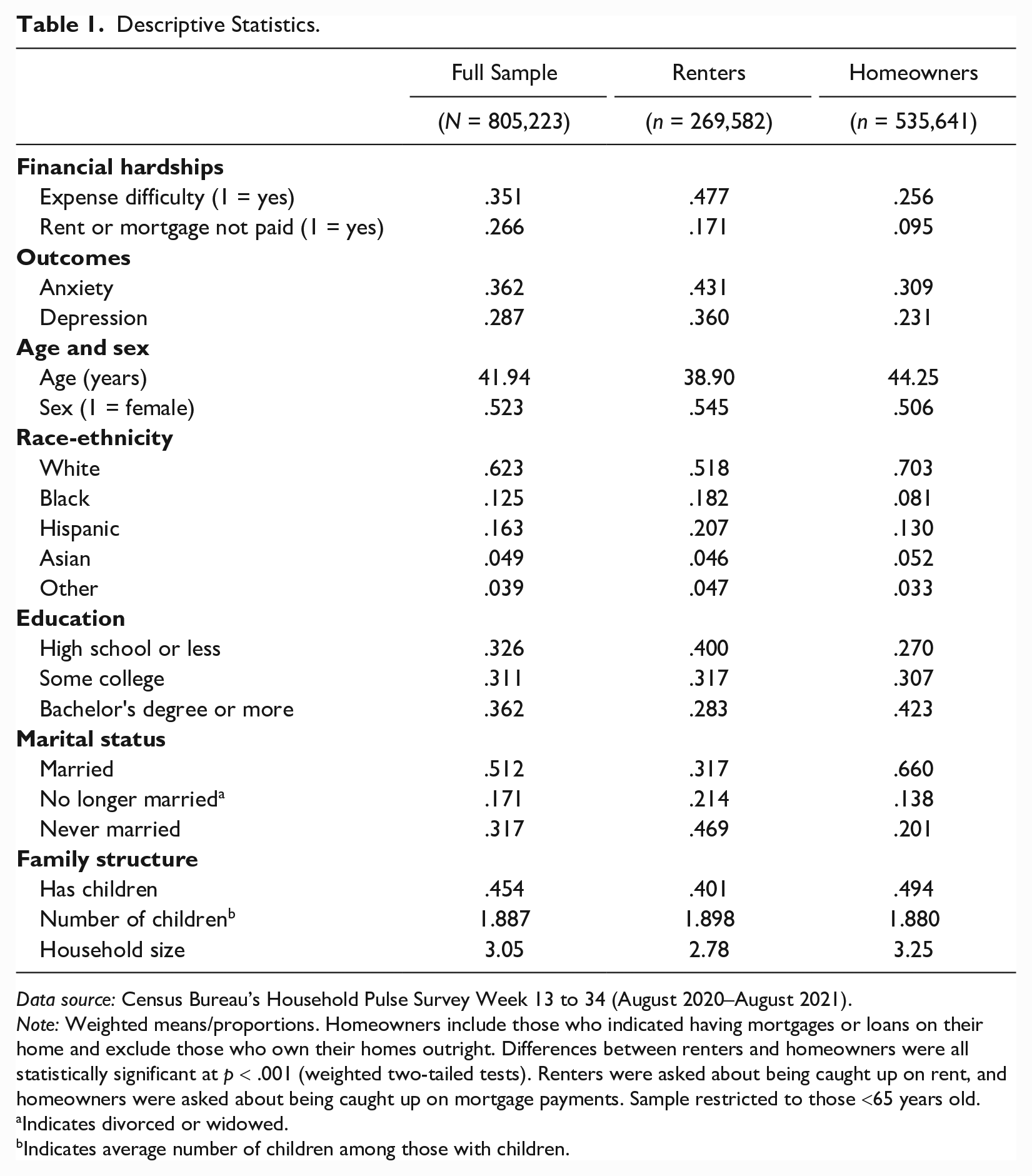

Table 1 includes weighted descriptive statistics for the full sample and separately for renters and homeowners. More than 1 in 3 households (35.1%) reported difficulty paying for usual household expenses during the August 2020 to August 2021 period, with striking disparities between renters and homeowners. Nearly one-half (47.7%) of renter households reported having difficulty paying for usual household expenses, which is roughly double the proportion of homeowners reporting expense difficulties (25.6%). Nearly 2 in 10 (17.1%) renter households reported not being caught up on rent, and about 1 in 10 (9.5%) homeowner households reported being behind on mortgage payments.

Descriptive Statistics.

Data source: Census Bureau’s Household Pulse Survey Week 13 to 34 (August 2020–August 2021).

Note: Weighted means/proportions. Homeowners include those who indicated having mortgages or loans on their home and exclude those who own their homes outright. Differences between renters and homeowners were all statistically significant at p < .001 (weighted two-tailed tests). Renters were asked about being caught up on rent, and homeowners were asked about being caught up on mortgage payments. Sample restricted to those <65 years old.

Indicates divorced or widowed.

Indicates average number of children among those with children.

Descriptive statistics in Table 1 also reveal high levels of probable anxiety and depression, with 36.2% of individuals having probable anxiety and 28.7% having probable depression. We find especially high rates of probable anxiety and depression among renters compared to homeowners (p < .001 for differences). Compared to homeowners, renters are more likely to be Black, Hispanic, or other race; have lower levels of education; and be no longer married or never married (p < .001).

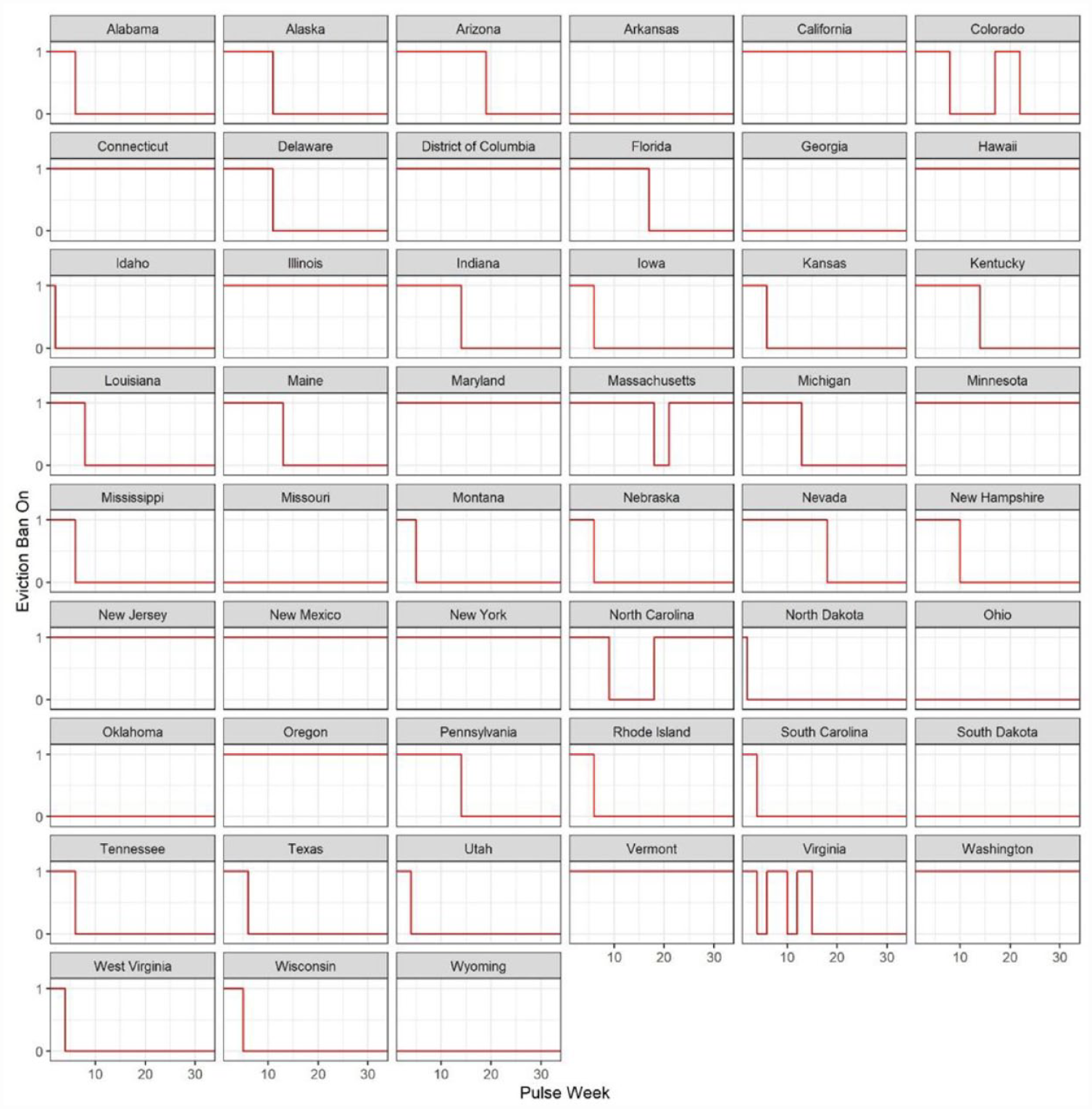

Figure 1 shows time trends in the state-level eviction/foreclosure bans, providing the timing of these bans for each state and the District of Columbia separately. A handful of states never implemented bans (e.g., Arkansas, Georgia, Missouri, Ohio, Oklahoma, South Dakota, Wyoming), while others had active bans over the entire period (e.g., California, District of Columbia, Hawaii, Illinois, Minnesota, New Jersey, New Mexico, New York, Oregon, Vermont, Washington). Importantly, Figure 1 illustrates that there was substantial heterogeneity in eviction/foreclosure bans across states and over time.

State Eviction/Foreclosure Ban Policy Timeline by State and U.S. Census Bureau’s Household Pulse Survey (CHHPS) Wave

Linear Probability Models

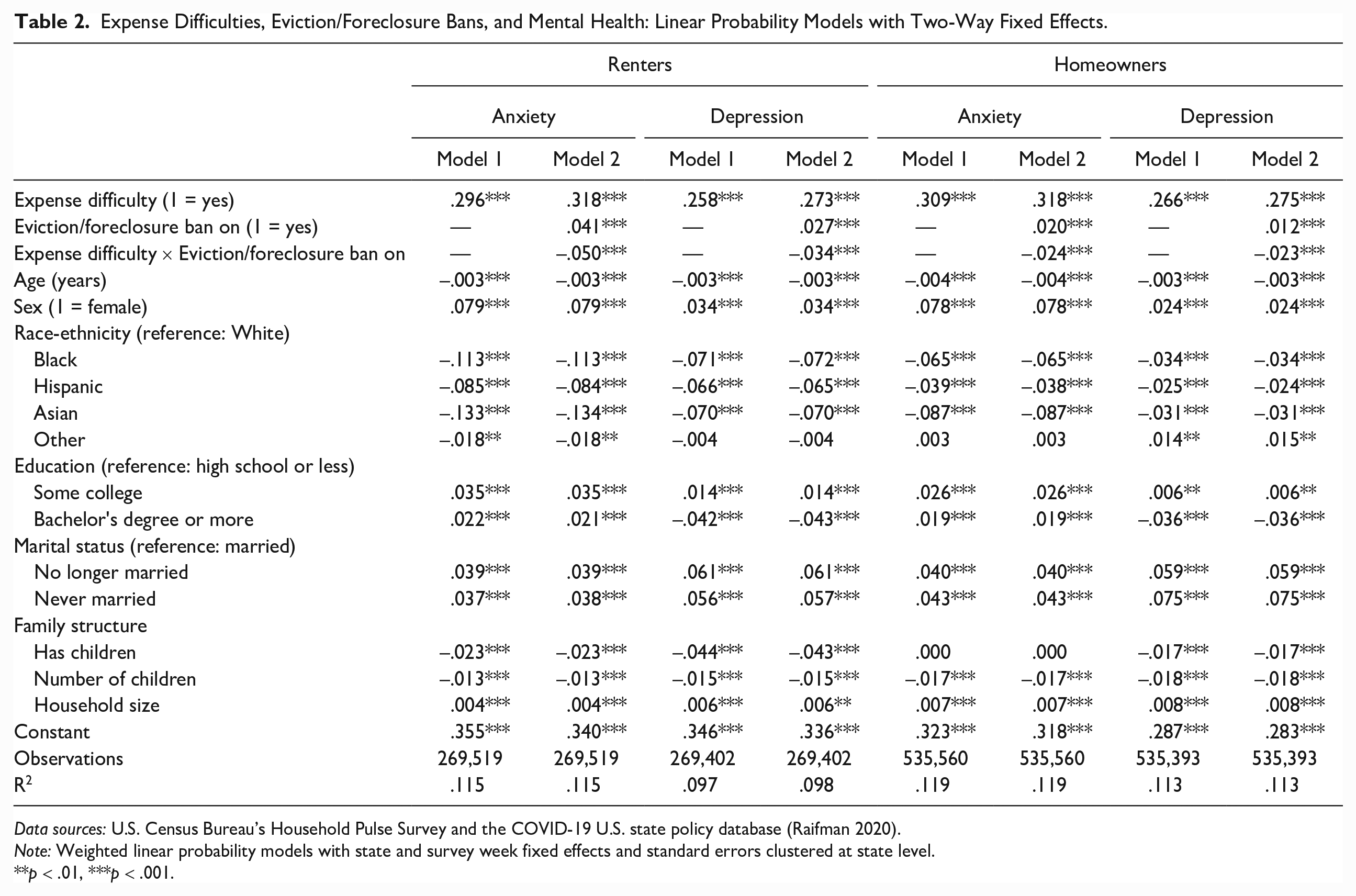

Table 2 shows results of linear probability models of probable anxiety and depression as a function of expense difficulty and state eviction/foreclosure bans. We report separate models for renters and homeowners. Results from Model 1 indicate strong support for our first hypothesis: Individuals reporting difficulty paying for usual expenses have higher levels of anxiety and depression than individuals not reporting such difficulties. Model 1 shows that among renters, reporting expense difficulties is associated with a 29.6 percentage point increase in the probability of anxiety (p < .001) and a 25.8 percentage point increase in probability of depression (p < .001). We find similar associations for homeowners, for whom reporting expense difficulties is associated with a 30.9 percentage point increase in the probability of anxiety (p < .001) and a 26.6 percentage point increase in probability of depression (p < .001).

Expense Difficulties, Eviction/Foreclosure Bans, and Mental Health: Linear Probability Models with Two-Way Fixed Effects.

Data sources: U.S. Census Bureau’s Household Pulse Survey and the COVID-19 U.S. state policy database (Raifman 2020).

Note: Weighted linear probability models with state and survey week fixed effects and standard errors clustered at state level.

p < .01, ***p < .001.

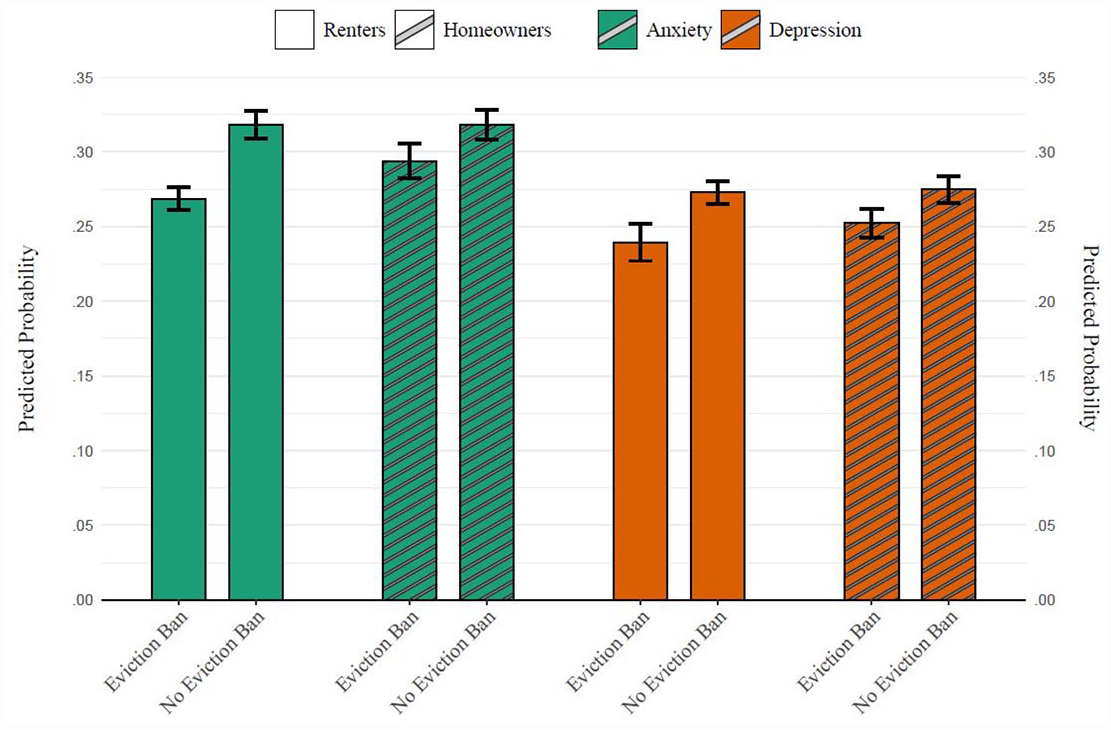

Findings in Model 2 of Table 2 also provide support for our second hypothesis: Living in a state with an active eviction/foreclosure ban weakens the associations between expense difficulties and anxiety and depression. The parameter estimate for the interaction term between expense difficulty and eviction/foreclosure ban is strong and negative, suggesting that active bans partially buffer the negative mental health consequences of reporting difficulty paying for household expenses. For example, results in Model 2 of Table 2 indicate that for renters living in states without active eviction/foreclosure bans, reporting expense difficulty is associated with increased risk of anxiety (expense difficulty: β = .318, p < .001) but that increased risk of anxiety is smaller for individuals in states with an active ban (Expense Difficulty × Eviction/Foreclosure Ban on: β = –.050, p < .001). Figure 2 illustrates this finding by displaying the results from Model 2 in Table 2 as predicted probabilities. Figure 2 highlights differences across models and shows that the average marginal effect of reporting expense difficulty on probable anxiety and depression varies by state policy context. Although both renters and homeowners reporting expense difficulties are protected by state eviction/foreclosure bans, the reduction in the mental health consequences of experiencing expense difficulties offered by state eviction/foreclosure bans is generally slightly larger for renters compared to homeowners.

Average Marginal Effect of Expense Difficulty on Anxiety and Depression among Renters and Homeowners by State Eviction/Foreclosure Ban Status

Behind on Rent or Mortgage

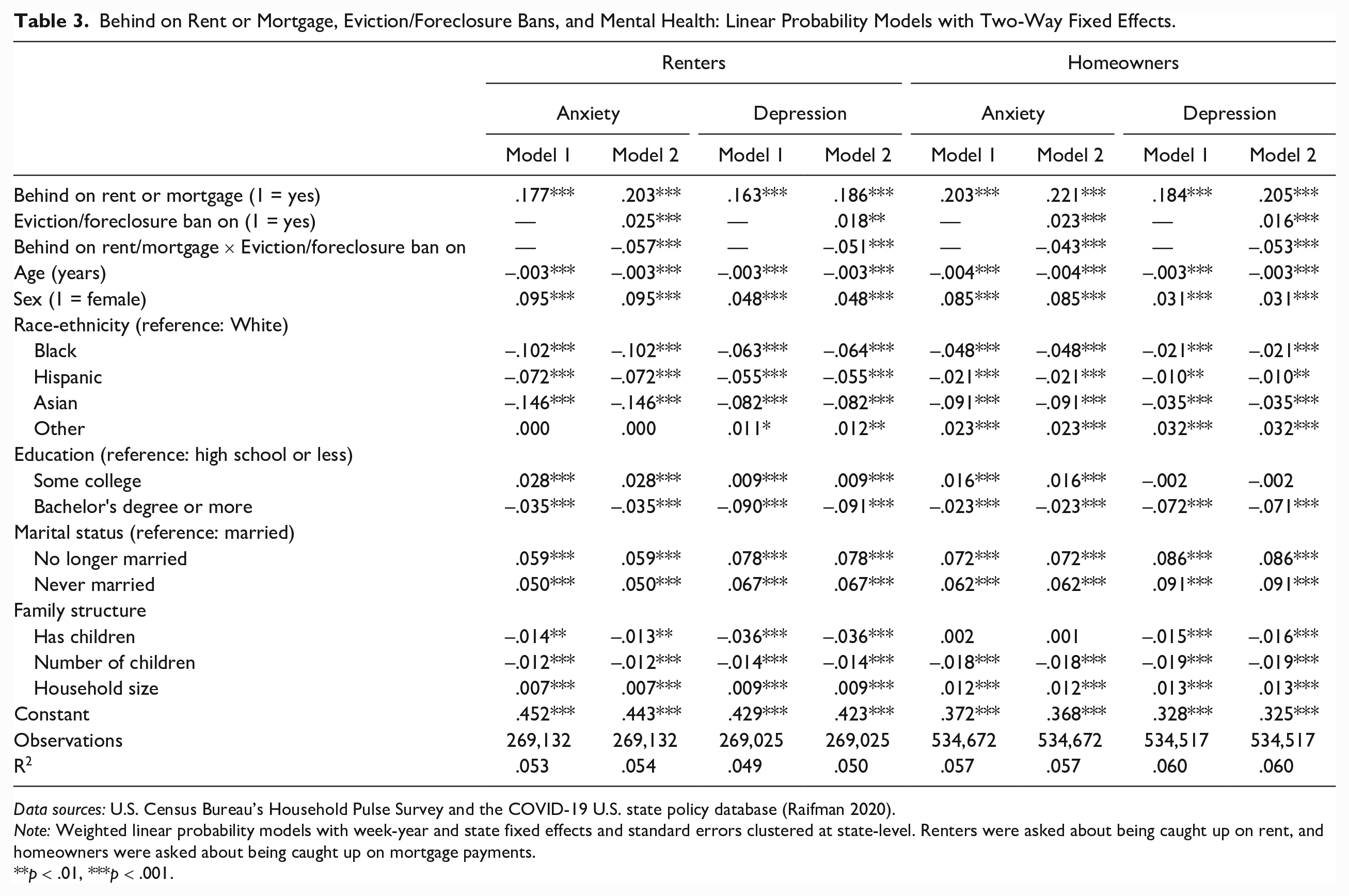

Table 3 shows results of linear probability models of probable anxiety and depression as a function of being behind on rent or mortgage and state eviction/foreclosure bans. Results show that renters who report being behind on rent have higher risks of anxiety and depression than individuals who are caught up on rent. In Model 1 of Table 3, being behind on rent is associated with a 17.7 percentage point increase in anxiety risk (p < .001) and 16.3 percentage point increase in depressive risk (p < .001). Similarly, being behind on mortgage is associated with a 20.3 percentage point increase in anxiety risk (p < .001) and an 18.4 percentage point increase in depressive risk (p < .001). These results provide strong support for Hypothesis 1: Individuals who are behind on rent or mortgage have higher risks of anxiety and depression than individuals who are caught up on their housing payments.

Behind on Rent or Mortgage, Eviction/Foreclosure Bans, and Mental Health: Linear Probability Models with Two-Way Fixed Effects.

Data sources: U.S. Census Bureau’s Household Pulse Survey and the COVID-19 U.S. state policy database (Raifman 2020).

Note: Weighted linear probability models with week-year and state fixed effects and standard errors clustered at state-level. Renters were asked about being caught up on rent, and homeowners were asked about being caught up on mortgage payments.

p < .01, ***p < .001.

Results in Model 2 of Table 3 also provide support for Hypothesis 2: Living in a state with an active eviction/foreclosure weakens the associations between being behind on rent/mortgage and mental health. The parameter estimates for the interaction term Behind on Rent or Mortgage × Eviction/Foreclosure Ban on are strong and negative in both the anxiety and depression models to a similar extent across both renters and homeowners. For example, in Model 2, we find that being behind on rent is associated with increased risk of anxiety among renters living in states without active bans (behind on rent: β = .203, p < .001) but that increased risk of anxiety associated with being behind on rent is smaller for renters living in states with an active ban (Behind on Rent × Eviction/Foreclosure Ban on: β = –.057, p < .001). Similarly, being behind on mortgage payments is associated with an increased risk of anxiety for homeowners in states without active bans (behind on mortgage: β = .221, p < .001), but again, that increased risk of anxiety associated with being behind on mortgage payments is smaller for individuals living in states with active bans (Behind on Mortgage × Eviction/Foreclosure Ban on: β = −.043, p < .001).

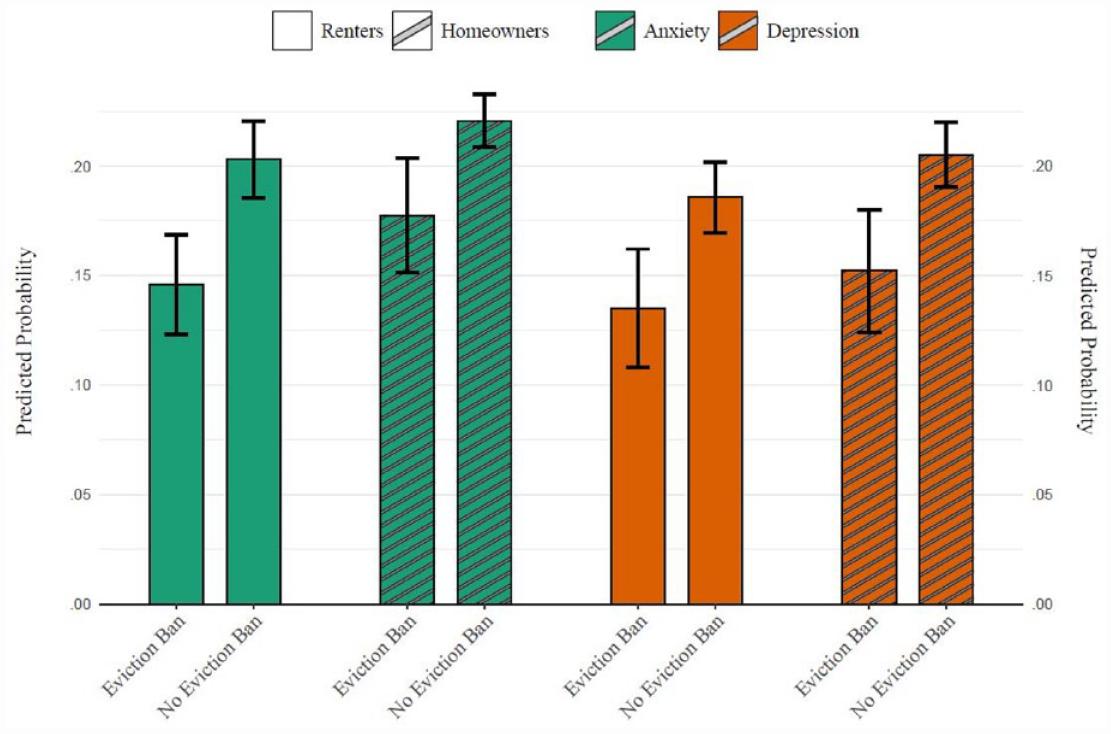

Figure 3 illustrates the main findings from Model 2 of Table 3 using predicted probabilities. Figure 3 shows that being behind on rent or mortgage is associated with increased anxiety and depression risk, but consistent with our hypotheses, the average marginal effect of being behind on payments on the outcomes varies by state eviction/foreclosure ban status.

Average Marginal Effect of Not Being Caught Up on Rent or Mortgage on Anxiety and Depression among Renters and Homeowners by State Eviction/Foreclosure Ban Status

Racial-Ethnic and Educational Differences

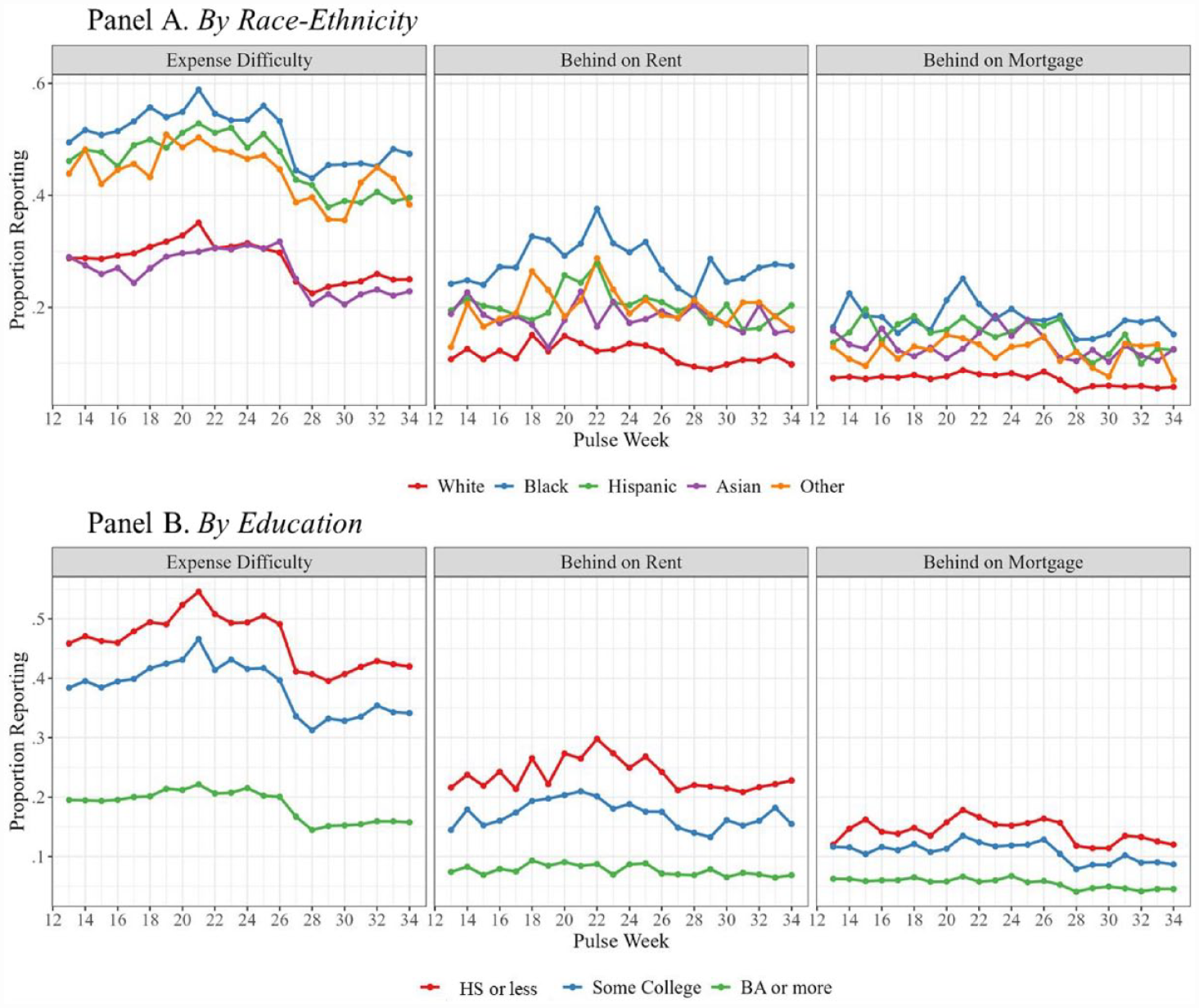

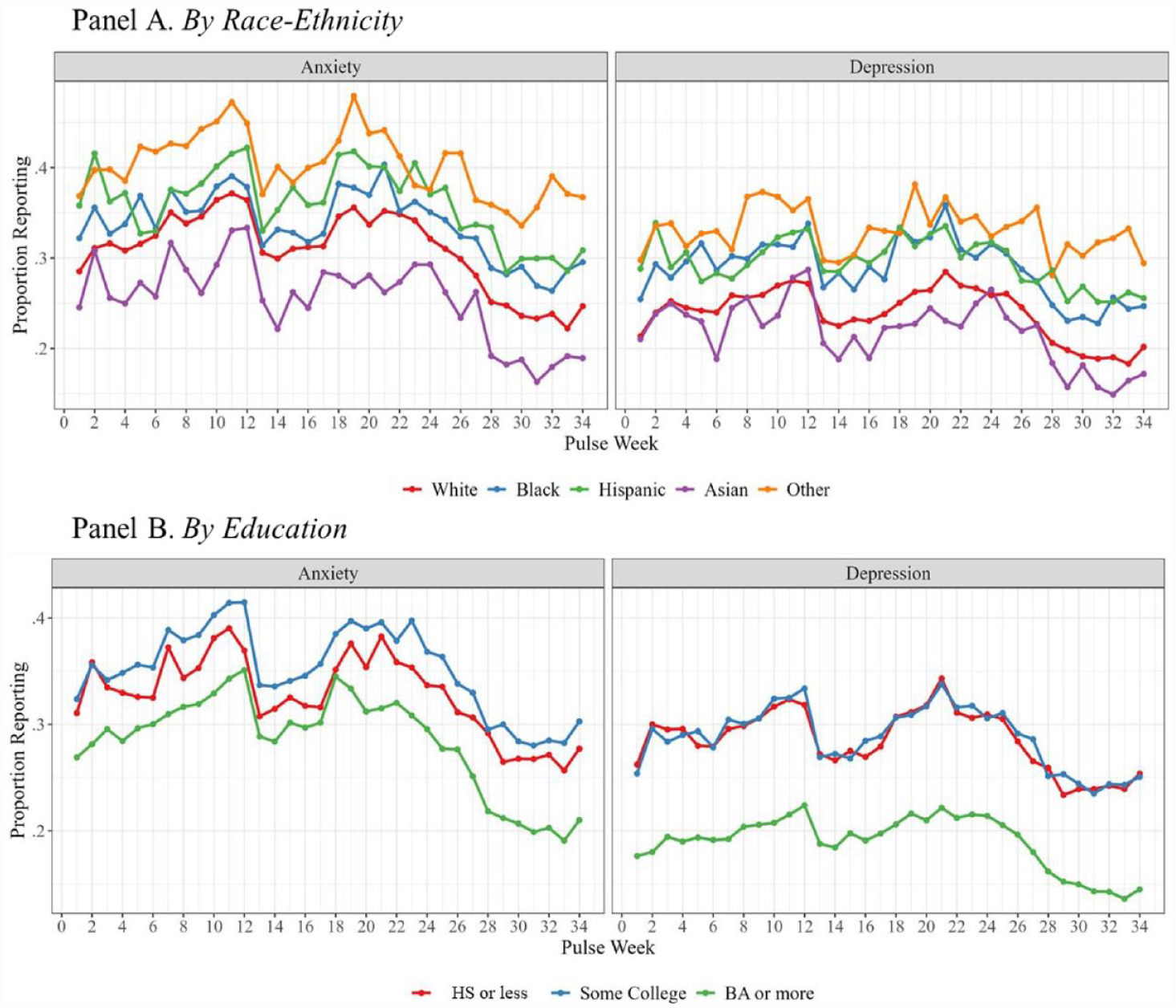

As noted previously, the pandemic may have contributed to racialized and socioeconomic inequalities in mental health given that the pandemic’s economic effects were disproportionately borne by Black and Hispanic individuals and those with lower levels of education. To investigate these potential patterns, we began by plotting the over-time differences in our three financial hardship measures (expense difficulty, behind on rent, and behind on mortgage) by race-ethnicity and education (Figure 4). We also plotted the over-time differences in our outcomes (probable anxiety and depression) by race-ethnicity and education (Figure 5).

Time Trends in Financial Hardship by Race-Ethnicity and Education

Time Trends in Anxiety and Depression by Race-Ethnicity and Education

Figure 4 confirms that three measures of financial hardship are unequally patterned by race-ethnicity and education. Among the racial-ethnic groups included, White and Asian individuals had the lowest levels of expense difficulty, and White respondents were least likely to be behind on rent or mortgage (see Panel A). In general, Black individuals experienced the highest levels of financial hardship. There is also an educational gradient across the three financial hardship (see Panel B): All three measures were inversely correlated with educational attainment. Despite some variation in the prevalence of financial hardship across the study period, the racial-ethnic and educational gradients across the three measures are largely persistent over time. Figure 5 shows corresponding variation in our mental health outcomes over the period. In Panel A, Asian and White individuals had the lowest mental health risks, while Black, Hispanic, and other race individuals had comparatively higher risks. There is also an educational gradient in mental health, with individuals with a college degree or higher having the lowest risks of anxiety and depression.

In other analyses (not shown here), we ran models stratified by race-ethnicity and education to assess for differential associations between the measures of financial hardship and the mental health outcomes and to assess whether the moderating role of state-level eviction/foreclosure bans varied across these groups. We found no evidence of differential associations. Taken together, then, our descriptive and multivariable analyses by race-ethnicity and education showed that racially minoritized and less educated individuals had higher levels of financial hardship during the pandemic, but we found no evidence of heterogeneous associations between the financial hardship measures and the mental health outcomes by race-ethnicity or education.

Supplementary Models and Robustness Checks

In other supplementary analyses, we ran logistic regression models and multilevel mixed effects models with random intercepts for states; results were substantively similar to the fixed effects linear probability models presented here. We also ran falsification tests that included replicating our multivariable models with the sample of homeowners who owned their homes without a mortgage or other debt (see Appendix A in the online version of the article). In times of economic hardship, homeowners who do not have debt on their homes are unlikely to experience the same stress associated with the threat of housing loss as their counterparts who have mortgages; as a result, the reported anxiety/depression of homeowners who do not have mortgages should not respond as much to eviction/foreclosure bans compared to homeowners with mortgages. Our falsification tests show that, indeed, homeowners without mortgages do not respond to eviction/foreclosure bans in the same way other homeowners do. Homeowners who do not have a mortgage and report difficulty paying expenses do report significantly higher levels of both anxiety and depression. However, the moderating or buffering role of eviction/foreclosure bans (indicated by the estimate for Expense Difficulty × Eviction/Foreclosure Ban on) is either insignificant (for depression) or only modestly significant (for anxiety) for these homeowner households.

Discussion

The COVID-19 pandemic spurred an economic downturn that increased levels of financial hardship and put millions of Americans at risk of housing loss. In this study, we investigated the population-level mental health toll of experiencing financial hardship during the pandemic, and we also assessed whether state-level eviction/foreclosure bans mitigated the mental health consequences of financial hardship. Findings from this study inform theoretical understanding of both the role of the macro-level economic conditions in shaping mental health and the potential public policy interventions aimed at preventing housing loss for improving population well-being.

Our results support two broad conclusions. First, we found that experiencing financial difficulties during the pandemic was associated with increased risks of anxiety and depression. Among both renters and homeowners, those who reported difficulty keeping up with usual household expenses experienced substantial increases in anxiety and depression. Similarly, those who reported being behind on rent or mortgage payments were at elevated risk of poor mental health. These findings are consistent with a large body of research showing that financial hardship is detrimental to health (Brand et al. 2008; Gallo et al. 2000; Kuhn et al. 2009; Noelke and Beckfield 2014; Pool et al. 2017), including recent research on pandemic-related economic hardships and health (Donnelly and Farina 2021; Kim 2021). Financial hardships can increase stress and worry and affect household consumption in ways that erode health in both the short and long terms (Boen and Yang 2016). COVID-19 is widely recognized as a direct threat to population health, but our results suggest that the pandemic also indirectly shaped mental health in part through its effects on the financial stability and security of American households. In this way, the economic downturn spurred by the pandemic had widespread effects on health in ways that extended the pandemic’s harms beyond the direct health risks by the coronavirus. Importantly, financial hardship during the pandemic was concentrated among low-wage workers and Black and Hispanic households (An et al. 2021; Cajner et al. 2020). As we showed in Figure 4, White individuals and those with higher levels of education were least likely to report difficulties paying for household expenses or keeping up with rent or mortgage payments. In these ways, our results are consistent with the notion that racism and other structural inequalities shaped financial hardships during the pandemic. In supplementary analyses, we found no consistent evidence that the associations between the measures of financial hardship and mental health varied by race-ethnicity or socioeconomic status, but to the extent that exposure to financial hardships was highest among financially disadvantaged and racially minoritized households, the pandemic may have contributed to inequities in mental health risks.

Second, our findings showed that state eviction/foreclosure bans partially buffered individuals from the negative mental health consequences of financial difficulties during the pandemic. As we highlighted in Figures 3 and 4, experiencing financial difficulties during the pandemic was associated with increased anxiety and depression risks; however, the associations were dampened for individuals living in states with active eviction/foreclosure bans. Previous research showed that eviction bans met their original goal of reducing COVID-19 risks (Leifheit, Linton, et al. 2021; Nande et al. 2021; Sandoval-Olascoaga et al. 2021); our study adds to a growing body of work showing that these bans also have mental health benefits (An et al. 2021; Leifheit, Pollack, et al. 2021). Importantly, we extend previous work on the links between eviction bans and mental health by showing that state eviction/foreclosure bans especially buffered both renters and homeowners with mortgages from the negative mental health consequences of financial hardship during the pandemic. Our inclusion of time and state fixed effects bolsters our confidence in this conclusion by offering a rigorous test of these links. Importantly, our findings also show that the mental health benefits of these state policies were not limited to renters but also included financially vulnerable homeowners, who have largely been excluded from previous studies on the health impacts of eviction bans. As shown in Tables 2 and 3, among renters experiencing financial hardships, we found that living in a state with an active eviction/foreclosure ban reduced the probabilities of anxiety and depression by between 2.7% and 5.7%; among homeowners, the estimated reductions in anxiety and depression ranged from 2.3% to 5.3%.

We proposed that financial hardships—including having a hard time paying for household expenses and being behind on rent or mortgage—are stressful for individuals, in large part because these financial hardships increase risks of housing loss. To the extent that state eviction/foreclosure bans protected financially vulnerable households from housing loss, these policies helped to buffer individuals from the many stressors associated with the threat of eviction or foreclosure. We see these reductions as important, albeit modest in size. There are likely several reasons for this. For one, these state policies were heterogeneous in nature. Most states only halted parts of the eviction process, with few states freezing evictions completely. Furthermore, most state eviction/foreclosure bans restricted eviction or foreclosure protections to certain subsets of renters or homeowners or certain types of cases, meaning that not everyone was protected against housing loss. In this sense, our results may be conservative because not everyone included in our “treatment” sample was protected by these bans. Second, housing loss was just one of the many stressors likely experienced by households facing financial hardship. These households also had to worry about paying for food, child care, medical care, utilities, and other expenses and costs. Eviction and foreclosure bans may have provided some relief for these vulnerable households, in the sense that the bans may have reduced worries related to housing loss, but the policies did not shield households from all of the stress and worry of financial hardship.

This study is not without limitations. As described, in supplementary analyses, we assessed for potential heterogenous associations by race-ethnicity and education but found no consistent evidence of differential associations. Still, low-income and racially minorized households experienced the highest prepandemic rates of eviction (Desmond 2012; Hall, Crowder, and Spring 2015; Rugh 2015), and these groups were also hardest hit by the economic downturn and eviction crisis spurred by the pandemic (Amburgey and Birinci 2020; Hepburn et al. 2020). This suggests that the worsening of the eviction crisis during the COVID-19 pandemic likely exacerbated already striking and persistent inequities in health by SES and race-ethnicity. We strongly encourage future research to address this important gap in scientific knowledge.

Our data imposed other limitations. As noted previously, roughly 20% of the full CHHPS sample was missing data on housing status and were not included in models. Relative to our analytical sample, those who were missing data on housing status were more socioeconomically disadvantaged. Given results found here, we speculate that their omission from our analytic sample may result in producing lower bound estimates, although we are unable to test this empirically. Additionally, our individual-level data are cross-sectional, so our results may be subject to concerns about unmeasured confounding. We adjusted for potential sources of measured individual confounding and included in our models both time and state fixed effects, which reduce concerns about unobserved heterogeneity over time and across states. Furthermore, because of data limitations, we cannot identify homeowners who are landlords, who may be less sensitive to the impact of the bans. Because relatively few (about 7%) of homeowners are landlords (Desilver 2021), however, we do not think our inability to identify them as a separate group unduly biases our results. Another data limitation is that we are unable to assess how differential durations of financial hardship shape mental health risks and/or vulnerability to state eviction/foreclosure bans. Understanding the time people spent in financial hardships—whether operationalized as spells of hardship or persistence in the state of heighted financial risk—is critical to understanding mental health risks and the efficacy of state efforts to redress these risks. Unfortunately, it is not possible to explore this important issue with extant data. As more data on the COVID-19 pandemic and related policy interventions become available, research might usefully fill this gap.

Taken together, results from this study add to the growing body of research documenting the critical role of state policy contexts in patterning population health (Montez 2020; Montez and Farina 2020), including mental health during the pandemic (Donnelly and Farina 2021; Leifheit, Pollack, et al. 2021). Our study’s focus on state eviction and foreclosure bans is, in some ways, narrow, in the sense that it focuses on one particular type of housing policy—one of many state-level policies aimed at protecting the financial well-being and security of households during the pandemic. Still, our analyses reveal that this one policy lever was an important one, given that state efforts to reduce evictions and foreclosures had detectable impacts on mental health.

Our results are also consistent with studies showing that state policies play an especially important role in shaping health risks among structurally marginalized groups (Montez et al. 2019), including those most vulnerable to economic downturns. To the extent that political power has devolved to the states over the past several decades, states have seized considerable authority in crafting and enacting policies governing population health and well-being (Montez 2020). Our results add to the growing body of literature showing that inequalities in state-level policies can contribute to geographic inequities in health, including mental health. In this way, our study identifies public policies—and the macro- and meso-level social, economic, and political forces that shape them—as critical determinants of health inequality. As the parallel COVID-19 pandemic and housing affordability crisis continue, our study points to the continued importance of protecting individuals from housing loss as a means for promoting public health and health equity.

Supplemental Material

sj-docx-1-hsb-10.1177_00221465231175939 – Supplemental material for The Buffering Effect of State Eviction and Foreclosure Policies for Mental Health during the COVID-19 Pandemic in the United States

Supplemental material, sj-docx-1-hsb-10.1177_00221465231175939 for The Buffering Effect of State Eviction and Foreclosure Policies for Mental Health during the COVID-19 Pandemic in the United States by Courtney E. Boen, Lisa A. Keister, Christina Gibson-Davis and Anneliese Luck in Journal of Health and Social Behavior

Footnotes

Acknowledgements

We thank the anonymous reviewers for their helpful comments and suggestions. An earlier version of this article was presented at the 2022 Population Association of America Annual Meeting. We thank Richard Patti for assistance with creating some of the data visualizations for this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Courtney E. Boen is grateful to the Population Studies Center at the University of Pennsylvania (National Institutes of Health’s Eunice Kennedy Shriver National Institute of Child Health and Human Development, NIH Grant No. R24 HD044964) and the Axilrod Faculty Fellowship program at the University of Pennsylvania for general support. Lisa A. Keister and Christina Gibson-Davis acknowledge funding support from the National Institutes of Health’s Eunice Kennedy Shriver National Institute of Child Health and Human Development, NIH Grant No. R21-HD107249. Anneliese Luck received support from the Population Research Training Grant (NIH T32 HD007242) awarded to the Population Studies Center at the University of Pennsylvania by the Eunice Kennedy Shriver National Institute of Child Health and Human Development.

Supplemental Material

Appendix A is available in the online version of the article.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.