Abstract

Background:

Since October 2019, Lebanon has been facing a severe and multifaceted economic crisis, considered one of the three most severe crises globally since the mid-1980s. Generally, economic crises and recessions are known to impact psychological well-being and mental health significantly.

Aim:

Considering this unique social context, the objective of this cross-sectional study was to investigate the association between financial well-being, anxiety, and depression among Lebanese adults during times of crisis.

Method:

This study included 225 Lebanese adults who completed an online questionnaire assessing sociodemographic data, financial well-being, anxiety, and depression.

Results:

Statistical analysis showed strong correlations between financial well-being and anxiety, as well as depression. This study shows an association between increasing levels of financial well-being and decreasing levels of anxiety and depression among Lebanese adults in times of crisis. Moreover, the study found negative correlations between age and anxiety, as well as age and depression. It also found that education level correlated with anxiety.

Conclusion:

The study offers insights into mental health in Lebanese society during times of crisis and recession, especially among relatively younger adults.

Introduction

Economic crises and recessions are known to impact psychological well-being and mental health significantly. During periods of economic downturn, individuals often experience increased mental health concerns, including stress, anxiety, and depression due to financial insecurity, job loss, and uncertainty about the future (Frasquilho et al., 2015).

Since October 2019, Lebanon has been facing a severe and multifaceted economic crisis caused by an accumulation of dramatic occurrences over the years that have aggravated the already fragile economic and financial sectors (Arezki et al., 2018). Lebanon has experienced clashes, various armed conflicts, and problems with the mismanagement of essential resources (González et al., 2016). Additionally, the spread of the COVID-19 pandemic in Lebanon led to a reduction in the production activities of companies (Kikstra, 2021) and the bankruptcy of others, which, in turn, led to a challenge in providing job opportunities and led to the unemployment of many (Gourinchas, 2020; Pilloni et al., 2022). Then, the port explosion in the Lebanese capital, Beirut, occurred in the summer of 2020 and was considered one of the most powerful explosions worldwide (Hernandez et al., 2020). This blast led to material damage of approximately 10 to 15 billion US dollars (Lakes, 2020) and led to the closure of numerous companies and the unemployment of many (Kebede et al., 2021), and left a deep collective trauma among Lebanese citizens (Akoury et al., 2025; Mzawak et al., 2025).

By the end of this crisis, the Lebanese Lira ultimately lost around 98% of its value (International Monetary Fund, 2023). Three million of the Lebanese population (78%) were estimated to be in poverty (UNICEF, 2021), and the yearly inflation rate reached a record high of 253.55% by June 2023 (Choueiri et al., 2023). The value of people’s incomes and savings has eroded rapidly, rendering it increasingly difficult for individuals and families to cover basic expenses.

Generally, the issue of mental health in Lebanon is underestimated. Mental disorders are prevalent in this population, especially following the accumulation of conflicts faced, making the Lebanese more vulnerable to mental disturbances (Khansa et al., 2020). Additionally, an economic crisis of this severity will undoubtedly have an impact on the mental health of the Lebanese population (Karam et al., 2022; Salameh et al., 2020). However, before the emergence of this crisis, around a third of Lebanese adults were in mental distress (Obeid et al., 2020). The World Health Organization estimates that 22% of Lebanese individuals suffer from a mental disorder and have been exposed to local conflicts in the previous 10 years, of which 11% of this estimate suffer from depression (Naal et al., 2021).

A psychological variable often examined during economic crises and recessions is financial well-being (Viseu et al., 2015), which refers to the individual’s subjective perception of their ability to maintain their desired levels of living conditions and financial security, both in the present and future (Brüggen et al., 2017). This concept encompasses an individual’s control over their finances, their ability to fulfill financial obligations, their resilience to financial challenges, and their freedom to make choices that enhance their quality of life (Prawitz et al., 2006).

Worldwide, following periods of crisis similar to the one experienced in Lebanon, numerous studies have reported a decline in financial well-being after such periods (Greenglass et al., 2013; Viseu et al., 2015; Wilkinson, 2016). Subsequently, some studies have shown an association between the latter and higher rates of depression and anxiety in different populations. (Frasquilho et al., 2015; Hassan et al., 2021; Richardson et al., 2018; Viseu et al., 2018). For instance, Greek data from before and after the 2008–2009 recession indicated a significant increase in depression rates (Economou et al., 2013; Madianos et al., 2010). In Spain, the risk of depression during the recession was nearly three times higher than in normal circumstances, alongside a rise in anxiety disorders (Gili et al., 2012). However, this is not unanimous, as research by Mamun et al. (2020) shows the absence of an association between financial well-being and anxiety among graduated and job-seeking women. It indicates a weak association between financial well-being and depression in this population.

Based on this research landscape, the objective of this study was to evaluate the associations between these three constructs of financial well-being, anxiety, and depression in the Lebanese context, which is currently facing an unprecedented multifaceted economic crisis. More specifically, this study will be guided by the following two hypotheses:

Hypothesis 1: Lebanese adults with a low level of financial well-being present a high level of anxiety compared to those with an average level of financial well-being and those with a high level of financial well-being.

Hypothesis 2: Lebanese adults with a low level of financial well-being have a high level of depression compared to those with an average level of financial well-being and those with a high level of financial well-being.

Materials and methods

Sample

Based on the G*Power software, the minimum necessary sample size for this study was 144, taking into account a 5% risk of alpha error, at 95% power and based on a financial well-being average of 13.96 ± 3.44 among non-depressed participants compared to 10.02 ± 3.50 among those who were depressed (Mamun et al., 2020).

The total sample included 312 participants; however, the final number of included subjects was 225, aged between 20 and 62 years, following the exclusion of non-Lebanese participants, participants aged less than 20 years, and participants not living in Lebanon, as well as those who take antidepressants and anxiolytics.

Procedures

This cross-sectional study was conducted between November 2022 and March 2023. Participants were recruited through convenience sampling. An online link was sent to the students of the Holy Spirit University of Kaslik (USEK), Lebanon, through the Student Affairs Office, and it was shared on the social media pages of the researchers. The recipients of the link were informed about the study’s objectives and their anonymity and then invited to send this same link to their circles. No financial compensation was offered for their participation.

Instruments

The data was collected through a questionnaire composed of two parts. The first collected sociodemographic data, including age, sex, area of residence, marital status, and educational and socioeconomic level, among other variables. The socioeconomic level was obtained through the household overcrowding index. The second part comprised the standardized scales concerning financial well-being, anxiety, and depression to measure the study variables.

Incharge Financial Distress/Financial Well-Being Scale (IFDFW Scale)

The IFDFW Scale (Prawitz et al., 2006) is a psychometric instrument that assesses through self-reporting the level of stress and budgetary well-being emanating from the personal financial situation. It consists of 8 items and uses a 10-point Likert scale where, for example, the first and last items rate 1 – ‘overwhelming stress’ and 10 – ‘no pressure at all’. The final score is obtained by adding the scores collected by each item, then dividing it by 8 (Prawitz et al., 2006). The latter is interpreted along a continuum where a higher score shows overwhelming financial distress and a low level of financial well-being, and a lower score shows no financial distress and a higher level of financial well-being (Prawitz et al., 2006). An Arabic version of this scale was recently validated for the Lebanese population (Nasr et al., 2024).

Lebanese Anxiety Scale (LAS-10)

LAS-10 is an anxiety screening scale that was specifically developed for the Lebanese population. It consists of 10 items in total. The first 7 items use a 4-point Likert scale (1 – ‘almost never’; 4 – ‘almost always’), and the last 3 items use a 5-point Likert scale (0 – ‘there is no’; 4 – ‘very strong’). The scores obtained by each item are added to provide a final score, allowing the interpretation of the level of anxiety, which worsens with the increase in the final score (Hallit et al., 2020).

Patient Health Questionnaire Depression Scale (PHQ-9)

PHQ-9 is a brief module extracted from the Patient Health Questionnaire (PHQ) based on the diagnostic criteria for depression according to the DSM IV and allows the screening of depression symptoms and their severity by a simple self-test (Kroenke et al., 2001; Kroenke & Spitzer, 2002). This scale includes 9 items using a 4-point Likert scale (0 – ‘not at all’; 3 – ‘almost every day’ and a final item with answers ranging from ‘not difficult at all’ to ‘extremely difficult.’ Following the addition of the scores of the first 9 items, the final score obtained can then vary between 0 and 27, showing the degree of severity of the depressive symptoms (Kroenke et al., 2001). As a standard, and according to a validation study conducted in Lebanon, it categorizes depression severity as: 0 to 4 (none), 5 to 9 (mild), 10 to 14 (moderate), 15 to 19 (moderately severe), and 20 to 27 (severe) (Dagher et al., 2023; Kroenke et al., 2001). The PHQ-9 scale was translated and validated to suit the Lebanese population (Dagher et al., 2023; Sawaya et al., 2016).

Data analysis

Data analysis was conducted using the 23rd version of Statistical Package for Social Sciences (SPSS) software. The normality of the distribution of depression and anxiety scores was confirmed by a calculation of skewness and kurtosis, with skewness and kurtosis values between −1 and +1 being considered acceptable to prove a normal univariate distribution (Hair et al., 2017).

Pearson correlations were investigated between the variables. Partial correlations were evaluated between depression and anxiety scores and each variable while controlling for others. Additionally, partial correlations were chosen as regression models for multiple purposes. First, Pearson and partial correlation can be compared relatively easily since both align between −1 and +1. Second, regression coefficients and partial correlations both generate the exact inferential results because they have equal p-values. Third, there was no reason to include more covariates in the present study.

In psychological statistical analysis, correlations of 0.1, 0.2, and 0.3 are usually considered to equate to small, medium, and large effect sizes, respectively (Funder & Ozer, 2020). Significance is considered with a p-value less than .05.

Results

Descriptive results

A total of 225 Lebanese adults were included in this study, with an average age of 29.37 ± 11.39 years, and 59.1% were female participants. The entirety of the participants’ characteristics can be found in Table 1.

Sociodemographic characteristics and other characteristics of participants.

The Financial Well-Being (FWB) scores ranged from 0 to 72 (M = 37.74, SD = 18.73). Anxiety (LAS) scores ranged from 0 to 37 (M = 19.98, SD = 8.86). Patient Health Questionnaire (PHQ) scores ranged from 0 to 27 (M = 9.98, SD = 6.27).

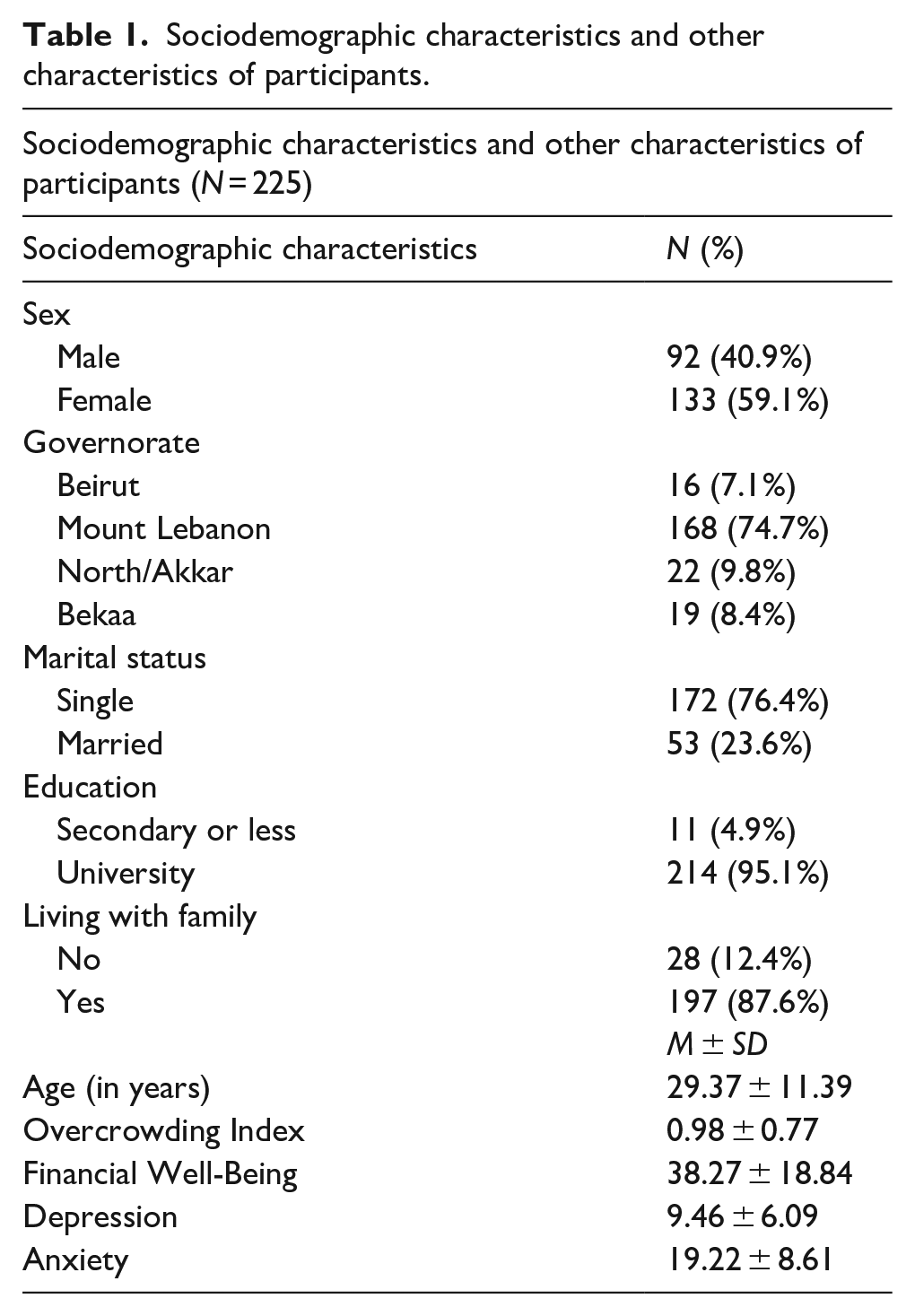

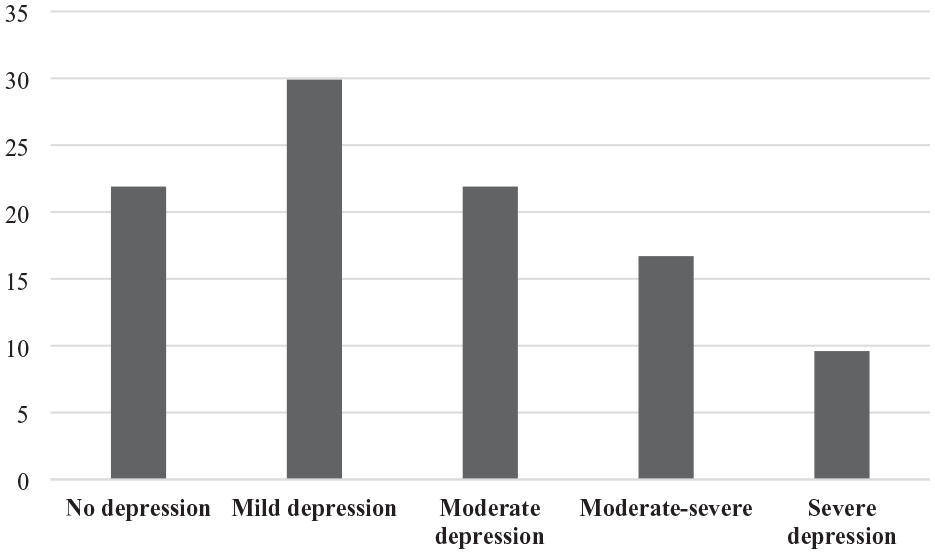

In the study sample, 21.9% of participants did not present signs of depression, 29.9% mild depression, 21.9% moderate depression, 16.7% moderate-severe depression, and 9.6% severe depression (Figure 1). Similarly, 75.3% of participants had clinically significant anxiety according to the LAS scale (Figure 2).

Distribution of depression severity levels based on PHQ-9 scores.

Anxiety prevalence based on the LAS.

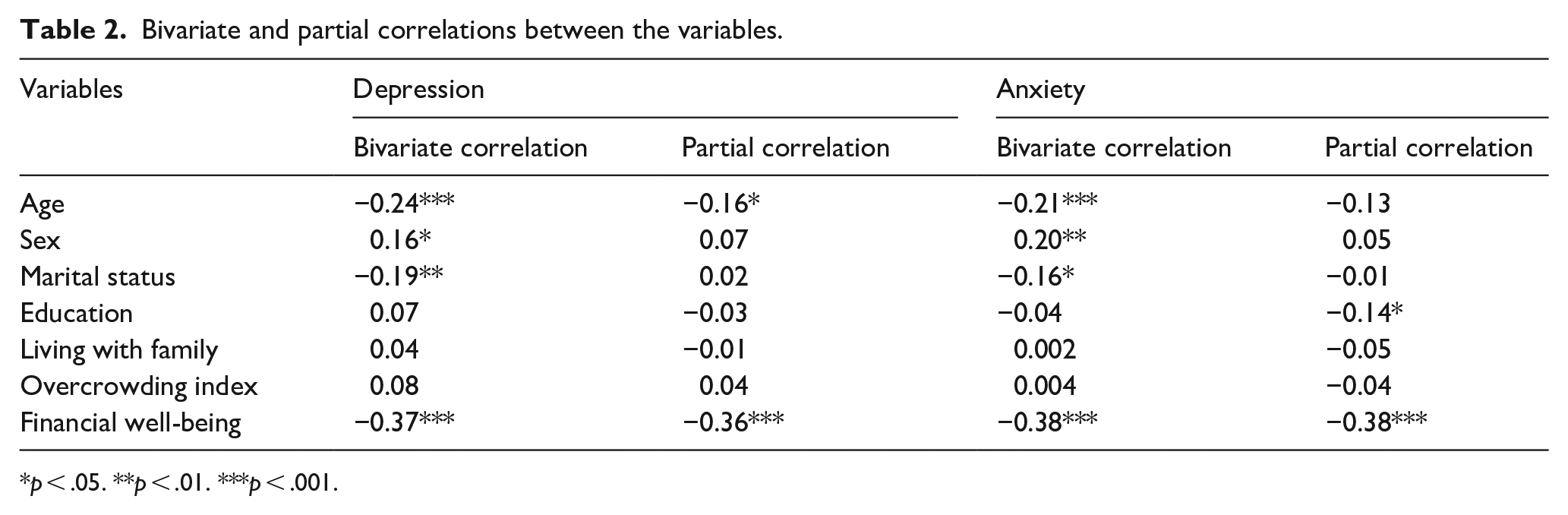

Bivariate associations

The results of the bivariate analysis showed that being relatively older (r = −0.24), being married (r = −0.19), and having greater financial well-being (r = −0.37) were significantly associated with lower depression scores, while women (r = 0.16) had significantly higher depression scores than men (Table 2).

Bivariate and partial correlations between the variables.

p < .05. **p < .01. ***p < .001.

The results of the bivariate analysis showed that relatively older age (r = −0.21), being married (r = −0.16), and having greater financial well-being (r = −0.38) were significantly associated with lower anxiety scores (Table 2).

However, the results of the multivariate analysis (partial correlation) showed that relatively older age (r = −0.16) and having higher financial well-being (r = −0.36) were significantly associated with lower scores of depression (Table 2).

However, the results of the multivariate analysis (partial correlations) showed that having university-level education, compared to secondary school or less (r = −0.14), and having higher financial satisfaction (r = −0.38) were significantly associated with lower anxiety scores (Table 2). A description of the principal findings is provided in Table 2.

Comparison analysis

An independent samples t-test was conducted to compare Financial Well-Being (FWB), anxiety (LAS), and Patient Health Questionnaire (PHQ) scores between two genders. The t-test results revealed a significant difference in FWB scores between groups, t = 2.162, p = .032, with a mean difference of 5.17 (95% CI [0.46, 9.87]). Similarly, LAS scores showed a significant difference, t = −2.990, p = .003, with a mean difference of −3.35 (95% CI [−5.56, −1.14]), indicating that males reported lower loneliness. PHQ scores approached significance, t = −1.990, p = .048, with a mean difference of −1.59 (95% CI [−3.17, −0.02]), suggesting a marginally lower depression score in the male group. These findings suggest significant group differences in financial well-being and anxiety, with a weaker effect observed for depression levels.

An independent samples t-test was conducted to examine differences in Financial Well-Being (FWB), Anxiety (LAS), and Patient Health Questionnaire (PHQ) scores between married and non-married individuals. The t-test results for FWB revealed no significant difference between groups, t = −1.005, p = .316, with a mean difference of −2.84 (95% CI [−8.40, 2.72]). However, LAS scores showed a significant difference, t = 2.754, p = .006, with a mean difference of 3.63 (95% CI [1.03, 6.22]), suggesting that non married experienced higher anxiety. Similarly, PHQ scores were significantly different, t = 3.119, p = .002, with a mean difference of 2.90 (95% CI [1.07, 4.73]), indicating higher depression levels in non married group. These findings suggest that while financial well-being did not differ between groups, there were significant differences in anxiety and depression levels.

An independent samples t-test was conducted to compare the scores of FWB, LAS, and PHQ between individuals who live with their families and those who do not. The t-test revealed no significant difference, t = −0.484, p = .629, with a mean difference of -0.82 (95% CI: −4.18 to 2.53). For PHQ, equal variances were assumed (F = 0.121, p = .728), and the t-test showed no significant difference between groups, t = -0.650, p = .517, with a mean difference of −0.78 (95% CI: −3.15 to 1.59). These results indicate that none of the variables showed statistically significant differences between the groups.

Regression analysis

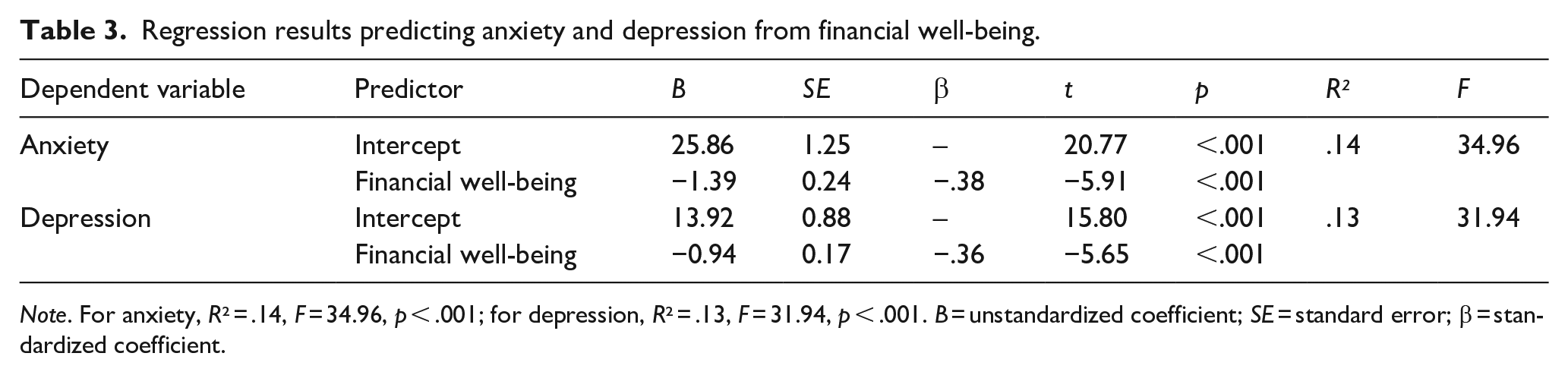

A regression analysis was conducted to predict anxiety and depression based on financial well-being. Both were statistically significant, with p < .001, indicating that financial well-being significantly predicts anxiety and depression. The detailed regression results are presented in Table 3.

Regression results predicting anxiety and depression from financial well-being.

Note. For anxiety, R² = .14, F = 34.96, p < .001; for depression, R² = .13, F = 31.94, p < .001. B = unstandardized coefficient; SE = standard error; β = standardized coefficient.

Discussion

The results of this study indicate that the level of financial well-being in this Lebanese population is associated with the levels of anxiety and depression experienced during the current crisis. This study included 225 Lebanese adult participants with an average age of 29.37 (±11.39), of whom 133 were women (59.1%). Most of the participants in the sample resided in Mount Lebanon (74.7%), while 9.8%, 8.4%, and 7.1% are the respective percentages of residents of the North/Akkar, Bekaa, and Beirut governorates. The reason for the high proportion of participants from Mount Lebanon is that the recruitment using the snowball technique started at a university located in Mount Lebanon.

Due to convenience sampling, some demographic skewness should be noted in the sample for accurate interpretation of results. It consisted of a majority of single individuals, with most living with parents or family. This high proportion of singles reflects cultural norms where adults typically remain in the family home until marriage (Kaddoura & Sarouphim, 2019), but it may not fully represent Lebanon’s broader marital status distribution across all age groups. The high proportion of university-educated participants is consistent with educational trends among Lebanese adults who seek high levels of education and have high levels of literacy (European Training Foundation, 2018). Despite this, the findings may be more generalizable to educated populations, while further research is needed to understand patterns among less educated individuals.

The descriptive statistics revealed alarming rates of psychological distress among participants, with only 21.9% showing no signs of depression, while 78.1% presented at least mild depressive symptoms. Similarly, 75.3% of participants exhibited clinically significant anxiety. These findings align with a recent prevalence study in Lebanon, which reported that 47.8% of their sample screened positive for probable depression and 45.3% for probable anxiety (Karam et al., 2025). These results suggest that the socioeconomic crisis in Lebanon has had significant adverse impacts on mental health outcomes among the population (Al-Khalil et al., 2025).

Concerning the principal aims of the study, the first hypothesis was validated through multivariate analysis, where the various levels of financial well-being were strongly and negatively correlated with the levels of anxiety felt by Lebanese adults. Furthermore, the results of the partial correlations in this study reveal that having a university education level is an additional factor of financial well-being, which is negatively associated with these levels of anxiety in Lebanese adults. The confirmation of this hypothesis is consistent with previous research (Baroud et al., 2022; Ozyuksel, 2022; Richardson et al., 2018; Viseu et al., 2015; Wilkinson, 2016) that found this negative association between financial well-being and anxiety in different populations. Moreover, an increase in anxiety symptoms has already been shown during periods of economic recession and this is due to economic instability (Catalano, 1991; Catalano et al., 2011). In other words, economic recessions and economic stressors present during these periods, including financial well-being, offer significant impacts on mental health and predict anxiety (Jesus et al., 2016; Leal et al., 2014).

In addition, the results obtained by Ozyuksel (2022) support the results of the second multivariate analysis of this study in which a bachelor’s education level was associated with higher levels of financial well-being than those with education levels of lower degree and subsequently reduced anxiety levels. This may be explained by the fact that a low educational level usually restricts an individual’s occupational options to various forms of manual work, as opposed to a higher educational level that widens the work options for people, leading to a feeling of relative financial safety (Bjelland et al., 2008). However, due to the small number of individuals with a secondary education level, this association should be interpreted with caution.

The multivariate analysis of the results of this study showed no importance regarding the variable of the sex of the participants with respect to an association between financial well-being and anxiety. This reveals a contradiction regarding the results obtained in another research (Mamun et al., 2020) showing a negative relationship between financial well-being and anxiety in men while an absence of association between these variables in women. This lack of difference between the sexes can be explained by the fact that Lebanese women are increasingly focusing on their education and careers (Riachi, 2021), which may lead to more financial security and, in turn, lower anxiety.

Second, a multivariate analysis allowed the confirmation of the second hypothesis, highlighting a significant association and a strongly negative correlation between the levels of financial well-being and depression felt towards Lebanese adults. The affirmation of our second hypothesis is consistent with results obtained by various studies on the same subject (Baroud et al., 2022; Mamun et al., 2020; Richardson et al., 2018; Viseu et al., 2015; Wilkinson, 2016). Our hypothesis and findings align with data from the systematic literature review by Hassan et al. (2021), which found that financial well-being is significantly linked to mental health and particularly to depression, especially during periods of recession where an economic slowdown and financial difficulties.

Furthermore, the multivariate analysis of our study highlights that age is, in addition to financial well-being, a factor negatively correlated with levels of depression in our sample. Our finding contradicts a previous study by Bierman (2014), which found that the subjective aspect of financial well-being decreases with increasing age factor. Contrastingly, other research supports the hypothesis of our study, including a study suggesting that adults aged over 65 experienced less financial constraints, in other words, better financial well-being, compared to younger adults (Morin & Taylor, 2009). Likewise, the results of Wilkinson’s (2016) study support this latter hypothesis: the levels of the subjective side of financial well-being and the averages of depression within an elderly population improved after the Great Recession despite the decrease in financial resources during this period. This finding is in line with the proposition of Francoeur (2002), who noted that adults develop better adaptation responses to economic stress with age, which explains our findings.

Strengths and limitations

Similar to all research, our study has strengths and weaknesses. On the one hand, its uniqueness adds insights to the literature, as it was conducted in the Lebanese context. On the other hand, this cross-sectional study only reflects the state of the population examined during a specific period of time, which limits the evaluation of the causal relation between these studied variables over different time frames. The conclusions obtained by this study should not be used in future studies to support a causal relation between these variables since the information obtained by this study was provided by a cross-sectional study. The obtained data are described in a very specific time and therefore subsequently cannot be affected by changes over time which can compromise the evolutions of the information in the long term, which can also not take into consideration any temporal changes in the individuals participating in this study.

Additionally, the collected data was not entirely randomized since the snowball technique was followed. A potential misrepresentation could occur due to the lack of random sampling, which is one of the weaknesses of this sampling technique since it limits the generalizability of the results: the recruited individuals may present similar traits, which will expose a bias in the representation of the entire population.

Moreover, gathering data on occupational status would have been relevant to this study and would have enriched the findings.

Finally, the sampling process gathered a sample of 225 participants, which is statistically representative at the country level but not at the governorate level. This sampling bias is attributed to the concentration of responses in the Mount Lebanon governorate. Furthermore, the demographic characteristics of the sample may limit the possibility of generalizing the results to different samples since a high percentage of the recruited individuals reside in Mount Lebanon. Similarly, the sample showed demographic skewness toward younger and educated individuals, which should be noted for transparency in result interpretation. Given the average age of participants, findings appear most generalizable to adults under 40, while results for relatively older adults should be interpreted with caution.

Clinical implications

Treatment for the categories with high-risk, including individuals with low income or in debt, individuals already experiencing financial difficulties or mental health disorders, and people with low education levels, is crucial, especially given the high prevalence of mental illness indicated in our study, as well as others. Cognitive-behavioral therapies are an example of potentially effective interventions because they address serious concerns and cognitive patterns related to finance and support and can protect individuals’ mental health against the effects of destructive thought patterns (Richardson et al., 2018).

Also, previous research has highlighted the crucial role of coping strategies in mitigating the effects of poor financial well-being on mental health, particularly anxiety and depression (Jesus et al., 2016; Ozyuksel, 2022). Thus, interventions to promote such strategies can help people become more resilient to financial challenges, thereby reducing their psychological vulnerability.

Conclusion

The objective of this study was to investigate the association between financial well-being, anxiety, and depression among Lebanese adults in a period of severe economic crisis. Mental health disorders are underestimated in developing countries like Lebanon despite the combination of all the factors faced by our population, which make them more vulnerable to mental disorders.

In this study, the association between financial well-being, anxiety, and depression among Lebanese adults has been examined, and the results show that during this period of economic and financial recession in Lebanon, high levels of financial well-being are strongly associated with low levels of anxiety and depression among Lebanese adults. Additionally, these data reveal that low levels of financial well-being are strongly linked to high levels of anxiety and depression in this Lebanese population. These results also demonstrate the potential benefits of having an advanced level of education and a high level of financial well-being since they are associated with lower levels of anxiety.

Lastly, future research is needed to examine this correlation in a longitudinal study to explore the causal relationships between mental health and financial well-being during periods of crisis. Future research should also explore the relationship between the variables on older adults, as our findings have limited generalizability to this population.

Footnotes

Funding

The authors received no financial support for the research. The APC was covered by the Higher Center for Research (HCR) at the Holy Spirit University of Kaslik (USEK).

Ethical approval

This study obtained ethical approval from the Ethics and Research Committee of the Hôpital Psychiatrique de la Croix (HPC 033/2022) before the start of this study.

Availability of data and materials

The data that support the findings of this study are available from the corresponding author but restrictions apply to the availability of these data, which were used under license for the current study, and so are not publicly available. Data are however available from the authors upon reasonable request and with permission of the ethics committee.