Abstract

Integrating housing tenure in Instrumental Motivation Theory predicts a tenure gap in electoral participation, as homeowners would be more motivated to vote compared with tenants. The empirical question is whether this effect is causal or rather due to selection into different housing tenures. This question is tackled using coarsened exact matching (CEM) on data for 19 countries, allowing us to better control for endogeneity. Even then, homeowners are found to vote more often than tenants. This association is stronger in countries characterized by a strong pro-homeownership ideology and/or where the financialization of housing markets turned houses into assets.

“Turning out to vote is the most common and important act citizens take in a democracy”.

Introduction: background and research questions

In many countries, the promotion of homeownership is a policy instrument aimed at achieving economic, social, and political goals (Bratt, 2012; Dietz and Haurin, 2003). Homeownership was traditionally used to stabilize the economy and promote growth. More recently, in some countries, it was believed to function as a private safety net through its association with wealth accumulation as part of a so-called ‘asset-based welfare’ strategy aimed at empowering low-income households (Sherraden and McBride, 2010). A social goal of homeownership policy is to rejuvenate deteriorated neighborhoods and quell social tensions. Homeownership is also supposed to encourage home maintenance and neighborhood involvement and improvement. With regard to the political consequences, it is argued that there is an association between housing tenure (homeownership, social, or private renting) and political behavior. Homeownership, by giving people a stake in society, would promote confidence in government and empower citizens, which, in turn, induces political participation and enhances democratic legitimacy (McCabe, 2013).

Recently, several studies addressed the impact of homeownership – or rather the potential to accumulate housing wealth under different housing regimes – on welfare attitudes. André and Dewilde (2016) found homeowners to be less supportive of government redistribution than tenants. They also found that for homeowners increased financialization of homeownership was associated with even lower support for redistribution. Ansell (2014) demonstrated that housing wealth seems to work as a self-supplied insurance against life-course risks, with owners experiencing house price appreciation becoming less supportive of government redistribution. He, furthermore, showed that right-wing parties respond to changes in voter preferences based on house price change by cutting down on redistributive spending during housing booms. While electoral outcomes and policy change are influenced by altered preferences of voters, these may also derive from changes in voter turnout. Such a tenure gap in electoral participation is particularly relevant when housing tenure is associated with political cleavages and divergent preferences between owners and tenants on social issues (see Barreto et al., 2007 for California).

Recent electoral participation research focused on explaining differences in turnout between social groups across countries, for example, the gender gap (Beauregard, 2014), the class gap (Anderson and Beramendi, 2012), the educational gap (Armingeon and Schädel, 2014), and the generational gap (Górecki, 2013). In this article, we research the potential difference in turnout between homeowners and tenants, that is, the tenure gap in electoral participation. 1 To this end, we integrate the ‘consequences’ of housing tenure into Instrumental Motivation Theory (Franklin, 2001). This theory predicts a higher turnout for those wishing to influence the course of public policy more because (1) they have more resources that enable them to vote, (2) they are more involved in politics, (3) they have a higher stake in the outcomes of an election and are mobilized as such, and (4) institutional arrangements render their vote more consequential, increasing the likelihood of policy change through electoral dynamics. In this article, we argue that housing tenure may influence instrumental motivation to vote in several different ways.

In general, a positive association between homeownership and voting in local and national elections is found for the United States, where part of this association is mediated by residential stability (how long one lives in and is invested in the house and the neighborhood) and financial investment considerations (DiPasquale and Glaeser, 1999; McCabe, 2013; Rossi and Weber, 1996). Engelhardt et al. (2010), however, found no effect for low-income homeowners. However, comparative research on the presumed political consequences of homeownership is scarce.

A major disadvantage of most studies relates to their weak designs, as it is difficult to disentangle causation from selection with cross-sectional observational data (Zavisca and Gerber, 2016). It is unclear whether the homeownership effect on political behavior is causal or (partly) due to selection bias (i.e. the endogeneity problem). The latter implies that higher electoral participation of homeowners versus tenants may simply arise from ‘common causes’ of both homeownership and voter turnout, such as more socio-economic resources and higher residential stability.

We improve upon earlier research in several ways. First, we incorporate homeownership as a potential determinant of voter turnout into Instrumental Motivation Theory. This means that we move beyond purely economic models of voting, since Instrumental Motivation Theory includes mobilization and institutions, besides resources. Second, we elaborate on previous US-focused research on electoral participation by including 18 European countries and the United States, using more recent data. This enables us to research contextual differences in the homeownership effect. Third, we take better account of methodological issues with regard to selection into homeownership (e.g. Engelhardt et al., 2010; Haurin et al., 2003). Social correlates of homeownership versus renting can largely be attributed to the fact that ‘different’ people select into homeownership. Mortgaged homeownership requires a stable income and employment position and is therefore more common among people in a better socio-economic position; these characteristics co-vary with electoral participation. Such observable socio-economic differences can be controlled for within a multivariate analysis framework. However, unobserved latent characteristics of people which determine their decision to become a homeowner (e.g. trust, lifestyle preferences, and psychological traits) may also influence their propensity to vote (e.g. Dietz and Haurin, 2003; Zavisca and Gerber, 2016). Although potential selection arising from such omitted variable bias is difficult to tackle with cross-sectional data, we improve upon earlier research by preprocessing the data using coarsened exact matching (CEM) (Ho et al., 2007; Iacus et al., 2012).

While we assume that the latent characteristics of individuals potentially increasing their likelihood of both homeownership and higher electoral participation are similar across countries, the institutional context (e.g. tax benefits, rent regulation, and social housing) renders it more likely for some individuals to accumulate savings and to enter homeownership than others. Who is selected into homeownership is thus conditional on these contextual arrangements and will differ between countries. Housing regimes – defined as the social, political, and economic organization of the provision, allocation, and consumption of housing (e.g. Kemeny, 1981) – influence the costs and benefits of housing tenures, as well as the average length of residence of owners versus tenants. We therefore take into account housing regimes, the likely selection of different ‘types’ of people into homeownership by these regimes, as well as their impact on residential stability of owners versus tenants and on the other mechanisms influencing people’s instrumental motivation to vote.

To summarize, our main research questions read as follows: do homeowners and tenants differ in their national electoral participation (i.e. tenure gap in turnout)? How does such a tenure gap vary by housing regime, and how can we explain such variation? We use data from the second wave of the European Social Survey (ESS) (Jowell and The Central Coordinating Team, 2005) and the 2004 General Social Survey (GSS) (Davis and Smith, 2004). The 2004 round of the ESS is the only one where housing tenure is recorded.

Why would homeowners have a higher likelihood to vote than tenants?

We start this section with a brief literature review on the assumed positive relationship between homeownership and turnout. Then, we integrate housing tenure as a potential determinant of voter turnout in Instrumental Motivation Theory.

The homeownership–voting relationship in earlier research

Political science studies addressing the relationship between homeownership and electoral participation distinguished between two explanations: residential mobility and economic interest (Johnston, 1987; Kelley et al., 1985; Squire et al., 1987; Studlar et al., 1990). Homeowners are more residentially stable, which provides the opportunity to build a larger social network. These extra ties are assumed to encourage electoral participation. Residential mobility in the United States furthermore implies electoral re-registration, which additionally leads to lower turnout. Squire et al. (1987), for instance, showed just-moved homeowners to have a lower likelihood to vote than residentially stable homeowners. Just-moved homeowners have a similar likelihood to vote than tenants with 7–9 years of residential stability. These findings indicate that homeownership as such and residential stability have separate, independent, effects on voting. In particular, homeowners are assumed to be more involved in their neighborhood because they want to safeguard emotional and financial investments in their property.

The positive association found between homeownership and voting in local and national elections in the United States was explained by both factors discussed above: residential stability and financial investment considerations (DiPasquale and Glaeser, 1999; McCabe, 2013; Rossi and Weber, 1996). Other studies used homeownership as a control variable and showed consistent positive effects on turnout (Geys, 2006; Highton and Wolfinger, 2001; Solt, 2010). More recently, McCabe (2013) found a positive effect of homeownership on local and national voting in the United States. There are hardly any comparative turnout studies taking homeownership into account. Glaeser and Sacerdote (2000) found no effect in Germany on local and national voting, while DiPasquale and Glaeser (1999) found a positive effect of homeownership on local voting in Germany, and both found an effect of homeownership on local and national voting in the United States. In the next section, we elaborate on arguments for a positive effect of homeownership on electoral participation by integrating them into Instrumental Motivation Theory.

Instrumental motivation theory

Most studies on voting focus on the (class-based) economic explanation of voting (Lewis-Beck and Stegmaier, 2007). British voter studies, however, show homeownership to cut across traditional class alignments (Dunleavy, 1979; Johnston, 1987). For instance, Dunleavy (1979) showed property ownership to be important for political alignment and related the decreased impact of occupational class on party choice to increased homeownership. We therefore incorporate homeownership into the broader theoretical framework of Instrumental Motivation Theory. This theory predicts a higher turnout for those groups that wish to influence the course of public policy more. Such instrumental motivation is promoted by resources, interest in politics, mobilization around specific interests, and institutional arrangements, for example, the extent to which votes translate into seats (Blais and Dobrzynska, 1998; Franklin, 2001, 2004).

First, individuals with more resources (knowledge, wealth, time, income, and education) are more likely to vote because they can more easily overcome the costs of voting (Verba and Nie, 1972). Homeowners by definition own housing wealth (and housing debt) in their primary residence, while tenants do not. On average, they also hold more financial resources, which made them able to enter homeownership in the first place (Di, 2005). These resources may thus be endogenous to the tenure-voting association. We expect differences in voter turnout between homeowners and tenants across countries to be explained at least partly by such socio-economic differences, that is, selection into different tenures.

A second theoretical mechanism explaining a potential tenure gap in voter turnout relates to interest-based mobilization of homeowners versus tenants. Although the presumed positive association between homeownership and political participation regularly resurfaces in research (e.g. Mau, 2015) and policy (e.g. Dutch Government, 2012), this relationship is not easily explained. The ‘stake in the system’ argument, for instance, implies that homeownership ties workers to the economic system and the local job market through mortgages (Castells, 1977; Engels, 1887 [1975]). These are assumed to encourage homeowners to vote for the powers-that-be in order to ensure stability and protect their housing investment. The interests of owners, however, often stand in opposition to the interests of tenants. Assuming that political parties will tailor their programs to different parts of the electorate, both owners and tenants can easily find a party that suits their needs and interests. 2 National debates on the ‘fairness’ of mortgage interest deduction (MID) or on the frustration of tenants who ‘miss out’ on the gains created through house price inflation (e.g. ‘generation rent’ in the United Kingdom) may thus mobilize both owners and tenants. The stake-in-the-system argument therefore potentially applies to party choice, but not to electoral turnout.

We can nevertheless formulate a number of arguments in favor of a positive homeownership effect on voter turnout. First, as also suggested by Mau (2015), political or economic interests around homeownership derive from its status as a special kind of resource/asset, related to

“the stability and concreteness of a home, the long-term nature of the investment, the expected asset appreciation and potential capital gain that could be achieved by selling, the emotional connection established while inhabiting it and the easy (and often tax-favored) transfer of a home to one’s children.” (Mau, 2015: 55)

It is no surprise that in economically precarious times where privatized assets (and debts) complement labor market incomes and social protection (see also Crouch, 2009), (mortgaged) homeowners are mobilized around policies that favor housing wealth accumulation. Although tenants also have housing-related interests, the latter revolve mainly around housing services (cost and quality) and do not represent a private asset, as is the case for homeowners. Second, as a ‘special’ kind of resource, homeownership positively impacts perceived social status and acts as a symbol of success and middle-class achievement. Owned houses are often larger, of better quality, and situated in better neighborhoods (Rohe and Stegman, 1994). Middle-class aspirations toward ‘increased prosperity, security and participation’ (Mau, 2015: xi) may encourage homeowners to vote through social pressure and social control (Feddersen, 2004). Third, individuals who are mobilized by political parties, unions, and other groups, or are more informed by the media and watch political news, are expected to have a higher propensity to vote (Rosenstone and Hansen, 1993; Verba et al., 1995). Such mobilization is easier through existing social networks, and homeowners are, on average, more residentially stable than tenants. Residential stability provides the opportunity to build social networks in the neighborhood (McCabe, 2013) and increases civic engagement, while residential mobility, according to Putnam’s (1995) re-potting hypothesis, decreases civic engagement. Using German panel data, Lancee and Radl (2014), for instance, found that becoming a homeowner incentivizes engagement in the local community as individuals start volunteering more. This homeownership effect may arise from a stakeholder effect partly related to the prospect of residential stability, from social expectations associated with the status of ‘being a homeowner’ or from increased mobilization through social networks.

Homeownership may thus reinforce the instrumental motivation to vote through various mechanisms. While some of these mechanisms are linked to residential stability, others are not. Therefore (and although previous research mainly looked at local voting), we argue that homeownership may also influence national voting. Policy outcomes at the national level are furthermore seen as important drivers of electoral participation (Franklin, 2001). Housing policy is mainly developed at the national level. For example, housing allowances, MID and property taxation are national regulations. Debates on the size of the social rental sector, right-to-buy schemes, and MID are covered by national media (André et al., in press). National parties profile themselves on their homeownership position. For example, in the United Kingdom, the Conservative Party presents itself as a homeowners’ party (Hamnett, 1999), and in the Netherlands housing became an important electoral issue for all political parties after the global financial crisis (GFC) (André et al., in press). Finally, politicians taking part in national elections are often chosen by a local electorate (Gallagher et al., 2006).

From the literature, we can now formulate the following micro-level hypotheses:

Hypothesis 1a. Homeowners have a higher propensity to vote in national elections than tenants because they have a higher instrumental motivation to do so. Such motivation is derived from their higher level of resources and from a number of mechanisms enhancing homeownership-related interests or the perceived social status of homeowners.

Hypothesis 1b. The higher propensity of homeowners to vote in national elections compared with tenants is partly explained by general differences in socio-economic characteristics that co-vary with homeownership (selection into homeownership), that is, age, education, income, political interest, and ideology, as well as by residential stability.

Housing regimes and the tenure gap in voter turnout

While homeownership became the majority tenure in most European countries, this happened in different time periods and for different reasons, which might further influence the tenure gap in voting. Tenure structures and housing outcomes result from ideologically driven power relations underlying qualitatively different institutional arrangements between states, markets, and families. In comparative research, the social production of housing is captured with the term ‘housing regimes’ (Dewilde, 2017; Kemeny, 2001, 2005; Matznetter and Mundt, 2012). We expect the instrumental motivation to vote derived from homeownership to influence the tenure gap in voting. Various factors play a role in this tenure gap, which are described below.

First, housing regimes ‘cause’ selection because they influence the costs and benefits of different tenures, rendering them more or less attainable and attractive for different groups of citizens. Governments can, for example, broaden or narrow the conditions of access to social housing or spend public resources on MID, the latter making homeownership more economically beneficial. Often governments promote homeownership at the expense of renting (Kemeny, 1981; Ronald, 2008). A second impact of housing regimes arises from tenure differences in residential stability. Homeowners are consistently found to be more residentially stable than tenants (i.e. McCabe, 2013). Reasons for such an effect are financial and emotional investment in the house and neighborhood, integration in the local job market, and higher costs associated with residential mobility. However, tenants may be more inclined to stay put when protected by stricter rental regulations (OECD, 2011). Tenure security, in combination with high-quality and affordable rental housing subject to some form of rent control, encourages tenants to be invested in their house and neighborhood, which, in turn increases the costs of residential mobility. We expect housing regimes, by causing systematic differences in residential stability between homeowners and tenants, to moderate the relationship between homeownership and voter turnout.

We distinguish between four regimes: market-based homeownership, family-based homeownership, the unitary rental market regime and post-socialist homeownership. For each regime, we lay out our expectations pertaining to the instrumental motivation to vote for owners and tenants, which is derived from (1) selection into homeownership, (2) tenure differences in residential stability, and (3) institutional and ideological arrangements around housing influencing social status and homeownership-related interests. We expect the tenure gap in voter turnout to be larger in regimes where (a) homeownership is the ideologically preferred tenure and thus more associated with perceived social status and moral expectations; (b) the tenure gap in residential stability is higher; (c) rental market regulation is less favorable for tenants; and (d) homeownership became more financialized (as investment motives influence the instrumental motivation to vote).

Housing markets became ‘financialized’ when deregulated mortgage securitization in the 1980s integrated local housing markets into global capital, although this is a geographically uneven process. Demand for mortgage lending and credit as well as rising house prices led to speculative bubbles in the United States, Ireland, Spain, Portugal, and the United Kingdom. In this process, households became more strongly exposed to house price booms and busts, with potentially not only higher rewards (capital gains) but also higher risks, such as indebtedness, interest rate fluctuations, capital losses, and unaffordability of homeownership for young people (Ronald and Dewilde, 2017).

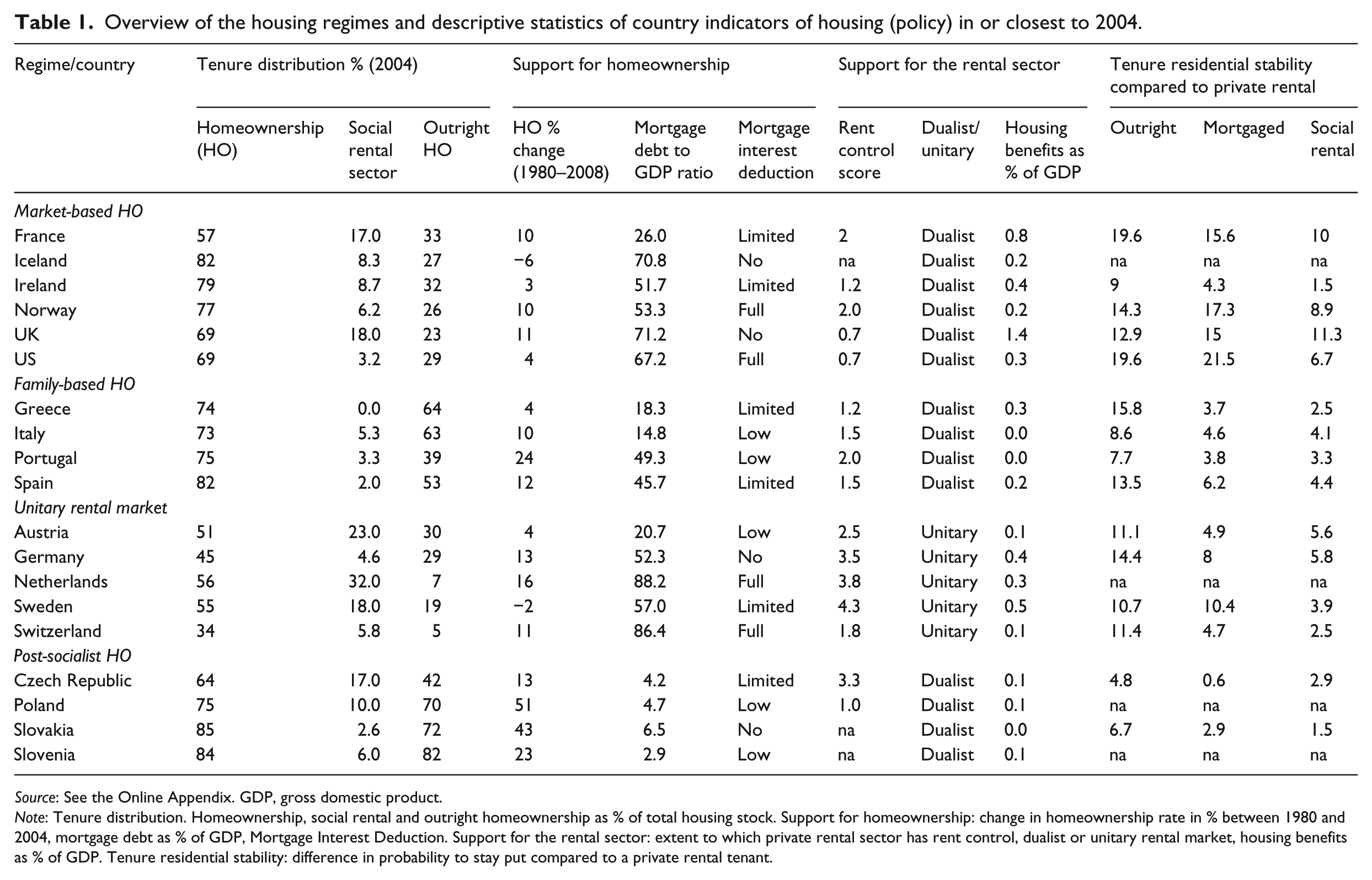

While the countries are classified into housing regimes based on characteristics discussed in the literature (Dewilde, 2017; Kemeny, 1981; Lowe, 2011), in Table 1 we also present some illustrative indicators taken from several macro-level sources. The data are from or closest to 2004, given that our survey data are from this year. The table shows, among others, indicators of residential stability of homeowners and social tenants (expressed as percentage difference compared to a private rental tenant), strictness of rental regulation in the private rental sector (in terms of the rent control score), and the extent of housing market financialization (mortgage debt to gross domestic product (GDP) ratio). The exact sources for Table 1 can be found in the Online Appendix (Table A1). A problem that always arises with regime classifications is that selected indicators do not capture the full picture; the indicators in Table 1 should thus be seen as a means to describe, rather than classify, countries.

Overview of the housing regimes and descriptive statistics of country indicators of housing (policy) in or closest to 2004.

Source: See the Online Appendix. GDP, gross domestic product.

Note: Tenure distribution. Homeownership, social rental and outright homeownership as % of total housing stock. Support for homeownership: change in homeownership rate in % between 1980 and 2004, mortgage debt as % of GDP, Mortgage Interest Deduction. Support for the rental sector: extent to which private rental sector has rent control, dualist or unitary rental market, housing benefits as % of GDP. Tenure residential stability: difference in probability to stay put compared to a private rental tenant.

The market-based homeownership regime

Countries that are historically characterized by an active pro-homeownership policy, reflecting an ideological preference for the provision of state-supported mortgaged-based homeownership (Ronald, 2008), are considered part of the market-based homeownership regime. Homeownership is seen as the ‘better’ and ‘natural’ tenure, conveying an ‘adult status’ (Colic-Peisker et al., 2015; Gurney, 1999). Homeownership may thus, more than in other regimes, add to perceived social status. Since housing is more likely perceived of as a tradable asset, housing wealth expectations or risks reinforce investment-related interests. Examples of homeownership policies, varying over time and across countries (Wind et al., 2016), are MID, right-to-buy of council housing, tax exemptions, and high loan-to-value ratios. These countries tend to have a dual rental market (Kemeny, 1995). The young and households with limited income are more often found in the (private) rental sector, which is lightly regulated. Social housing is shielded from the market, targeted at the poor and residual – and therefore more stigmatized (Kurz and Blossfeld, 2004). The social groups that are selected into homeownership are also those that are expected to vote more often in elections (higher incomes, higher education, and older age groups). We include France, Ireland, Iceland, Norway, the United Kingdom, and the United States in this regime. Table 1 illustrates some characteristics of the countries in each regime. For example, the difference in residential stability between homeowners and private tenants is largest in the market-based homeownership regime, and rent control in the private sector is limited. Except for France, countries in this regime have highly financialized mortgage markets (based on mortgage debt to GDP ratio).

The family-based homeownership regime

In the family-based homeownership regime, homeownership is outright and mainly acquired through self-provision by the extended family, pooling resources across generations to overcome credit constraints (Allen et al., 2004). Since housing is a family asset and housing markets are less financialized, housing is much less tradable and capital gains expectations will affect investment-related interests of homeowners less. Although the government hardly intervenes in the homeownership market, the housing trajectory is strongly focused on homeownership and is a prerequisite for family formation (Poggio, 2013). We therefore assume homeownership in this regime to be more strongly associated with social status. The social rental sector is shielded from the market, but small (dual rental market) and most low-income households live in family-owned housing (Allen et al., 2004). Compared to the market-based homeownership regime, we expect that the private rental sector mostly caters for young households that did not make the transition to homeownership yet and for poor households (who are less politically active than the young). We include Greece, Italy, Portugal, and Spain in this regime. Table 1 shows that the housing market in the family-based regime is less financialized (although housing market opportunities and risks may play a role in Spain and Portugal), rent control in the private rental sector is slightly stricter, and differences in residential stability between tenures are more moderate.

The unitary rental market regime

The unitary rental market regime is found in Austria, Germany, the Netherlands, Sweden, and Switzerland. A unitary rental market is characterized by relatively small differences between the social and private rental sectors (Hoekstra, 2009; Kemeny, 1995; Lowe, 2011). Historically, private landlords were allowed to enter a state-managed market in exchange for state subsidies. Rent control (as a proxy for strictness of rental regulation) is thus highest in this regime (see Table 1). The ensuing competition between public and private housing providers results in good-quality and affordable housing across rental tenures and income groups (Dewilde, 2017). In Germany, strong increases in the private rental stock since the 1990s arose from the privatization of public housing associated with the termination of subsidy arrangements. Both rental sectors, however, remain fairly strictly regulated. The level of social housing is thus only of secondary importance for the classification of Germany into the unitary rental regime.

In this regime, all tenures are more or less state-supported. Lower income groups have access to better-quality rental housing, while the middle-income groups can choose between homeownership and renting. Higher income groups are generally in homeownership. We expect the perceived social status effect to be smaller in this regime, although selection bias is more likely. As the social rental sector is not marginalized, residential stability is higher compared to homeowners (OECD, 2011). Homeowners are more residentially stable than private tenants (see Table 1) at rates comparable to the family-based homeownership regime. In recent decades, housing markets became strongly financialized in a subgroup of countries, that is, the Netherlands and Switzerland. Homeownership-related economic interests thus provide a possible instrumental motivation to vote.

The post-socialist homeownership regime

Homeownership is extremely high and mostly non-mortgaged in the post-socialist regime, comparable to the family-based regime. This is the outcome of privatization, that is, the sale of state-owned rental housing to tenants for below-market prices and the restitution of property to pre-communist owners. Houses are, however, often unfit and in bad condition while shared by generations (Lux et al., 2013; Mandic and Clapham, 1996). This means that the benefits normally associated with homeownership compared to renting are less evident. The lack of development in housing finance following privatization of state-provided housing furthermore implies that investment-related considerations do not play a role. The Czech Republic, Poland, Slovenia, and Slovakia belong to this regime. Differences in residential stability between owners and private tenants are lowest in this regime, as evident from Table 1. Renting is a transitional tenure consisting of residualized social housing and illegal private renting (Lux et al., 2016).

We formulate the following hypotheses:

Hypothesis 2a. A larger tenure gap in voter turnout in the market-based homeownership regime is likely to arise from several different sources: selection bias, tenure differences in residential stability, perceived social status of homeownership, and (mobilization around) homeownership-related interests in a financialized housing market.

Hypothesis 2b. Compared with the market-based homeownership regime, the tenure gap in voter turnout is smaller in the family-based homeownership regime (less likely selection bias and less mobilization around housing-related interests) and in the unitary rental market regime (less tenure differences in residential stability) – although some of these differences are partially controlled for in the micro-models.

Hypothesis 2c. The tenure gap in voter turnout in the post-socialist homeownership regime will be non-significant, as potential selection bias is minimal and all tenures have high residential stability. Housing tenure is far less associated with the mechanisms predicting a positive remaining homeownership effect derived from the instrumental motivation to vote, that is, perceived social status and homeownership-related economic interests.

Data and methods

We use data for 18 European countries from the 2004 ESS (Jowell and The Central Coordinating Team, 2005) and the 2004 GSS for the United States (Davis and Smith, 2004). We are limited to 2004, as this is the only round of the ESS which contains high-quality data on both tenure and political behavior for all European countries. This may be a distinctive year since it is in the middle of the housing boom. However, following the economic and housing crisis of 2007–2008, governments did not fundamentally change their policies toward homeownership; they rather protected housing markets and (mortgaged) homeowners. Unfortunately, there are no comparative datasets in which information on housing tenure, political participation, and residential stability are included at the same time. We therefore combine data from different sources and approximate length of residence.

Variables

We coded whether people voted in the last national election (1) or not (0) and excluded those not eligible to vote. We coded whether any member of the household owned the dwelling (yes (1)/no (0)), excluding young adults and students living at home. We unfortunately have no information on the type of rental housing (public/private/rent-free).

Control variables

Control variables are included in order to minimize the possibility that ‘common causes’ of both homeownership and voting are confounding a potential tenure effect on voter turnout. To control for individual-level differences in political resources and engagement with politics, control variables often used in research on electoral participation (Beauregard, 2014; Franklin, 2004) are included. Age is calculated from the year of birth and centered. Gender is recoded into female (1). Education is measured as (1) primary education and not-completed secondary education; (2) secondary education completed; (3) post-secondary/tertiary, bachelor, master completed; and (4) education missing. Income is measured as the country-specific relative household income percentile. Marital status is measured with four dummies as ‘married or living together’, ‘single’, ‘divorced’, and ‘widowed’. Urban/rural living is measured as ‘big city’, ‘suburbs’, ‘small city’, and ‘rural area’. Occupational status is operationalized by means of the International Socio-Economic Index of Occupational Status (ISEI), indicating the cultural and economic resources typical for different occupations (Ganzeboom and Treiman, 2014). For those who did not have a valid score, because they were housewives, long-term unemployed, or did not answer the question, the mean score was imputed and a dummy variable flags this imputation. Internal political efficacy is measured as low (1)/middle (2)/high (3) based on the average on the items ‘politics is too complicated to understand’ and ‘making my mind up on political issues is hard’ for ESS countries and with the question ‘most people in America are better informed about politics than I am’ for the United States. Political ideology is measured as left/democrat (1) versus middle/independent (2) versus right/republican (3), using the left–right self-placement scale of ESS and the ‘feel closer to party’ variable from GSS. Political interest is measured as interested (1) versus not interested (0). Political trust is operationalized as the mean score on the partisan trust items in the survey, because only trust in partisan institutions would enhance voter turnout (Rothstein and Stolle, 2008). 3

Length of residence

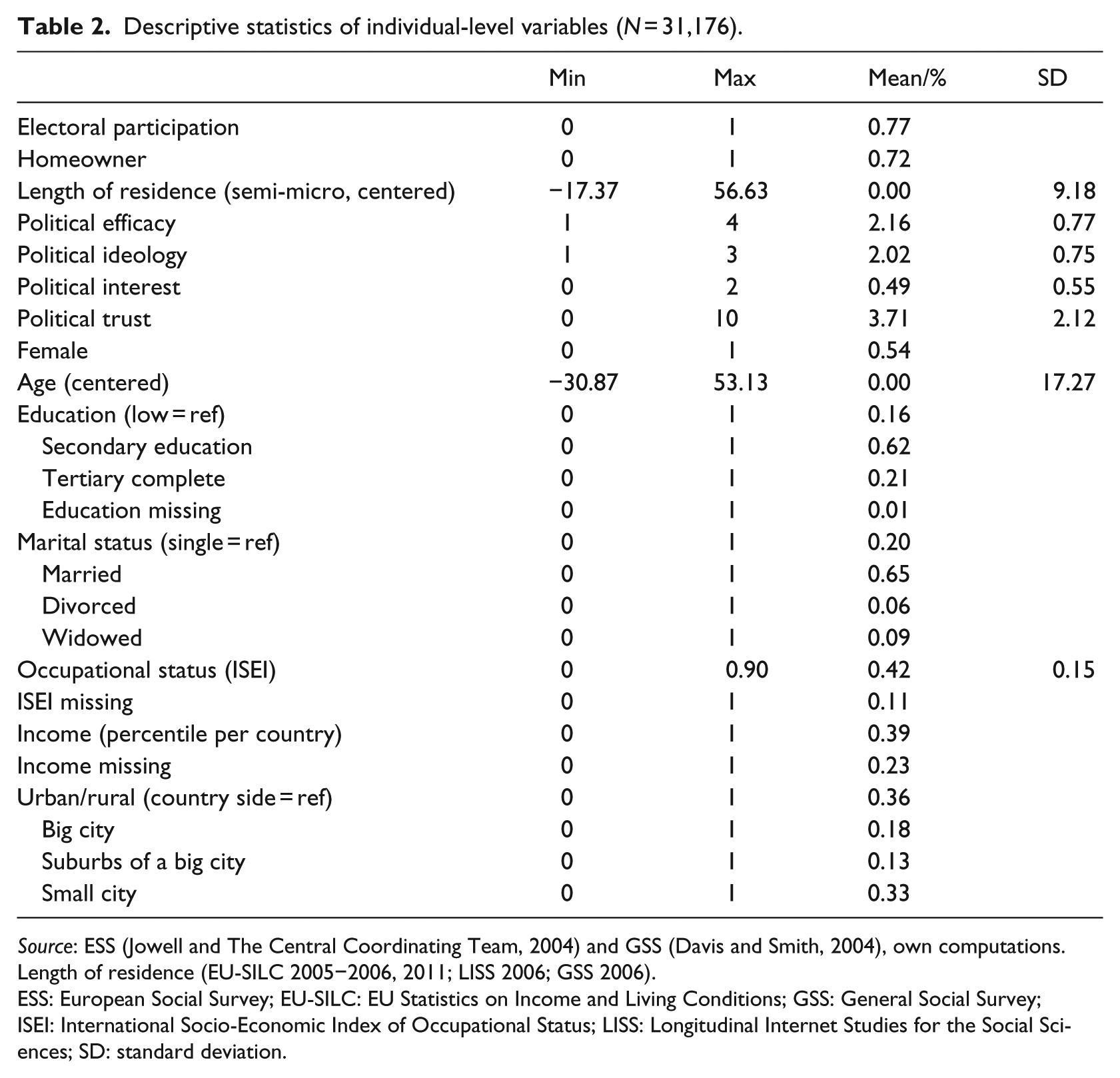

Length of residence refers to the number of years a respondent lived in the current house based on the date of purchase or of the first lease. Unfortunately, this information was not available in the 2004 waves of ESS and GSS. Therefore, we used other data sources and imputed a proxy for length of residence. Length of residence was calculated from European Union Statistics on Income and Living Conditions (EU SILC, 2005) for all countries, except Norway (EU-SILC 2006) and Switzerland (EU-SILC 2011). 4 We made the sample selection comparable to ESS and GSS, randomly selected one person per household, and measured the length of residence based on the date of purchase or of installment of the rental contract. We calculated the average length of residence for groups of respondents based on age (18−35, 36−50, 51−65, 65+), gender, married or not, education (low, middle, and high), and tenure (homeowner and tenant). We calculated the length of residence for the United States with the 2002 GSS and for the Netherlands with the 2006 wave of the LISS panel. 5 Since older people are more likely to have lived longer in their house, there is a high correlation between length of residence and age (r = 0.70). 6 We matched respondents (see the next section) on both variables. This also implies that we cannot test specific hypotheses on the length of residence effect. We do, however, control for length of residence in the best possible way, given the data at hand. Descriptive statistics of all variables used in the analyses can be found in Table 2.

Descriptive statistics of individual-level variables (N = 31,176).

Source: ESS (Jowell and The Central Coordinating Team, 2004) and GSS (Davis and Smith, 2004), own computations. Length of residence (EU-SILC 2005−2006, 2011; LISS 2006; GSS 2006).

ESS: European Social Survey; EU-SILC: EU Statistics on Income and Living Conditions; GSS: General Social Survey; ISEI: International Socio-Economic Index of Occupational Status; LISS: Longitudinal Internet Studies for the Social Sciences; SD: standard deviation.

Analytical strategy

Earlier studies on the relationship between homeownership and electoral participation used multivariate (and sometimes multilevel) logistic regression analysis with various approaches to the endogeneity problem (i.e. selection bias). In observational data, the treatment assignment (in our case homeownership) is not controlled by the investigator; this compromises causal inference. Put differently, selection into homeownership makes it difficult to assess whether a positive association between homeownership and turnout is explained by instrumental motivations to vote or by characteristics of people that make them more likely to both vote and be a homeowner. McCabe (2013) used placebo measures to control for selection into homeownership, while others used instrumental variable modeling (Aaronson, 2000; DiPasquale and Glaeser, 1999). We tackled this issue in two ways. First, as discussed above and based on the political science and housing literature, we selected appropriate control variables that potentially confound the voting–tenure relationship. Second, for a better and stricter test, we preprocessed our data by means of CEM (Blackwell et al., 2009).

CEM is a straightforward way to improve causal inference from survey data through matching. Matching is a non-parametric data preprocessing approach to control for the confounding influence of pretreatment variables and to reduce statistical bias and model dependence (Ho et al., 2007). As the matching procedure balances out owners and tenants in terms of their observed covariates, this method mainly does a better job of controlling for observables. However, to the extent that the observed variables are correlated with unobservable characteristics associated with tenure outcomes, the likelihood that the latter are balanced out is higher as well (Iacus et al., 2012). In particular, we argue that by matching on political trust – a variable which is arguably correlated with a number of unobservable traits, for example, general social trust – we are able to better control for factors endogenous to the tenure–voting association and are therefore also better equipped to evaluate a potential tenure effect on voting.

Traditionally, exact matching (one-to-one) would be used and yield a limited number of matches by pairing treated units to control units with the same values on covariates. Including continuous variables would almost automatically imply no matches. CEM provides a solution to this problem by temporarily coarsening (categorizing) continuous variables into meaningful groups, which makes the likelihood of a match higher and prunes less cases. By subsequently including the original uncoarsened variables in the models and performing statistical estimations, we end up with a better balanced dataset without losing too many observations. Concretely, we categorized all independent variables (including imputed length of residence and political characteristics) 7 and matched, per country, each tenant with these specific characteristics to a homeowner with the same characteristics. Applying CEM reduced the global imbalance of our dataset from 1.0 (total imbalance) to 0 (complete balance), which means that we have complete balance on the (coarsened) covariates (for more information on CEM, see Iacus et al., 2012). The number of respondents decreased from 31,097 to 12,323. We reran the models on all data with the preprocessed data and also included the original uncoarsened variables that we matched on because these have more variation than the dummies used in the matching process (Blackwell et al., 2009).

The matching procedure also provides a solution for the high correlation between age and length of residence (r = 0.77). This correlation is high by default. Since we have no direct measurement of length of residence and imputed a proxy from other data sources (based on age, education, gender, tenure, and marital status), these were all correlated. Since all of these variables were used in the CEM, we are able to bypass this multicollinearity problem. This, however, also implies that we cannot attach any meaning, except for ‘controlled for’, to our length of residence measure.

Normally, when analyzing multiple countries, multilevel analysis is applied to account for the clustering of individuals in countries. However, because our intra-class correlation is low (0.08), we use linear regression analysis with the clustered standard errors option in STATA. We also provide the results of identical models controlling for country fixed effects in the Online Appendix (results are robust). 8

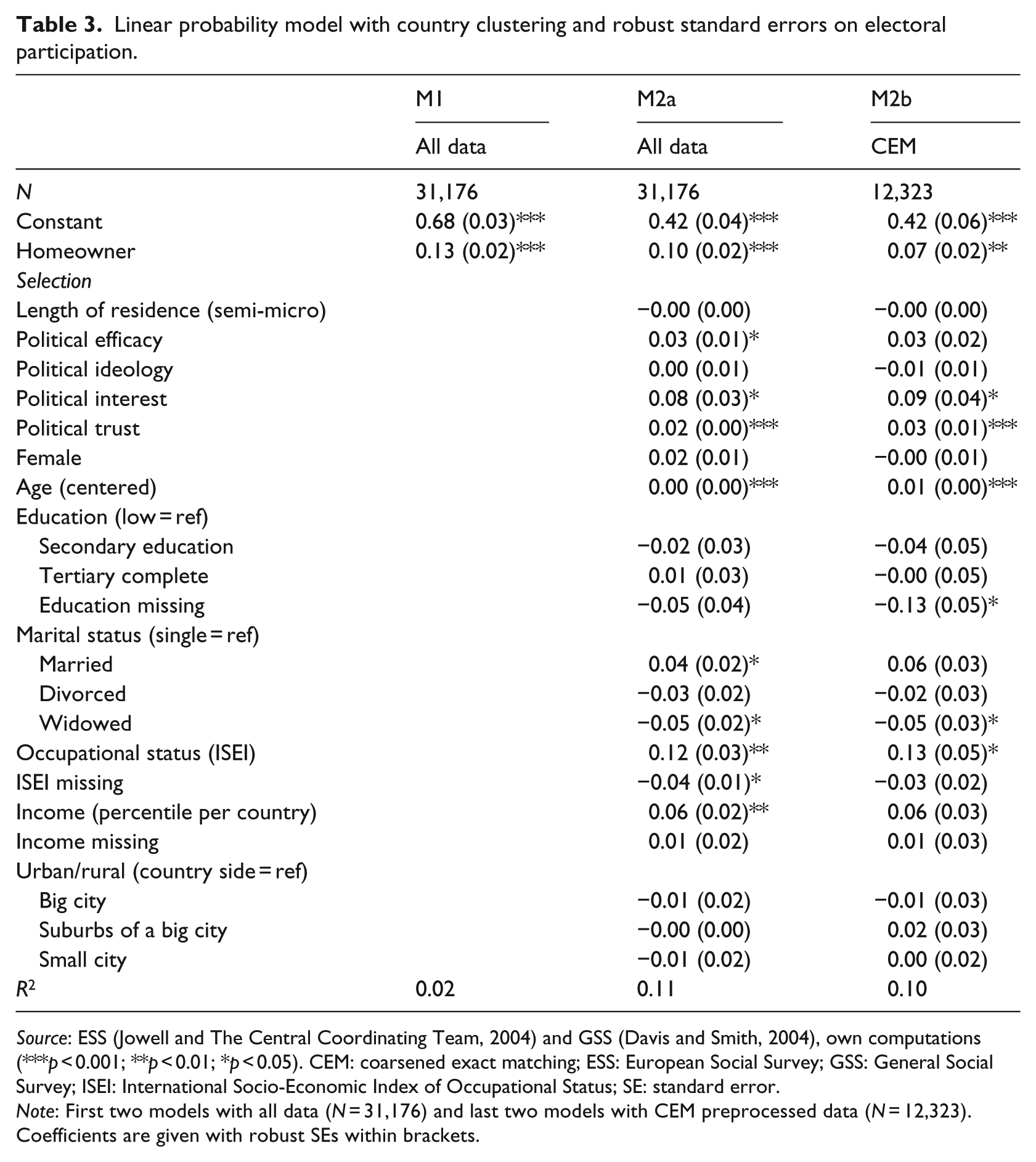

Mood (2010) showed that odds ratios cannot be interpreted as effect measures because they also reflect the unobserved heterogeneity in the model, which can differ between models or groups. To test mediation and interaction models, it is better to use linear probability models (LPMs), which yield unbiased and consistent estimates of a variable’s average effect on the chance that the event occurs. This means that we will run linear regression models although having a binary dependent variable. The b-coefficients in LPM can be read as average marginal effects on the likelihood of voting (Matter and Stutzer, 2014). We present the individual-level models in Table 3 and the country-level models in Table 4.

Linear probability model with country clustering and robust standard errors on electoral participation.

Source: ESS (Jowell and The Central Coordinating Team, 2004) and GSS (Davis and Smith, 2004), own computations (***p < 0.001; **p < 0.01; *p < 0.05). CEM: coarsened exact matching; ESS: European Social Survey; GSS: General Social Survey; ISEI: International Socio-Economic Index of Occupational Status; SE: standard error.

Note: First two models with all data (N = 31,176) and last two models with CEM preprocessed data (N = 12,323). Coefficients are given with robust SEs within brackets.

Linear probability model with country clustering and robust standard errors on electoral participation.

Source: ESS (Jowell and The Central Coordinating Team, 2004) and GSS (Davis and Smith, 2004), own computations (***p < 0.001, **p < 0.01, *p < 0.05). CEM: coarsened exact matching; ESS: European Social Survey; GSS: General Social Survey; HO: homeownership; ISEI: International Socio-Economic Index of occupational status; SE: standard error.

Note: First two models with all data (N = 31,176) and last two models with CEM preprocessed data (N = 12,323). Coefficients are given with robust SEs between brackets.

Results

Our general micro-level hypothesis (Hypothesis 1a) predicted homeowners to have a higher propensity to vote in national elections compared with tenants because of their higher instrumental motivation derived from more ‘enabling’ resources and from a number of social mechanisms which enhance perceived social status and homeownership-related considerations. Table 3 shows the individual-level results of the LPMs with country-clustered standard errors. Model 1 (uncontrolled estimates) confirms our hypothesis as homeowners are 13 percentage points more likely to vote in national elections than tenants. We assumed this association to be (partly) explained by general differences in socio-economic characteristics that co-vary with homeownership (‘selection into homeownership’), as well as by residential stability differences between owners and tenants. Therefore, we control for these characteristics in Model 2a. The estimate for ‘homeownership’ becomes smaller (10 percentage points) but remains significant. Since we control for, among others, age, income, and education, we can safely set aside the argument that resources alone are responsible for the association between tenure and voter turnout. In Model 2b, we use our preprocessed dataset, which has a better balance of homeowners and tenants and potentially provides more certainty as to whether the ‘treatment’ effect of homeownership is ‘real’, rather than arising from pretreatment confounders which remained unmeasured, such as, for example, trust, lifestyle preferences, and personality traits. Model 2b is thus the strictest test possible with the data at hand. We find that the ‘homeowner’ estimate is reduced from 13 to 7 percentage points between Models 1 and 2b, which is a significant reduction (χ2 = 10.90, p = 0.004). Homeowners are still 7 percentage points more likely to vote in national elections than tenants. These findings are in line with H1b, as at least part of the effect arises from the ‘consequences of being a homeowner’, for example, through perceived social status or homeownership-related (investment) considerations.

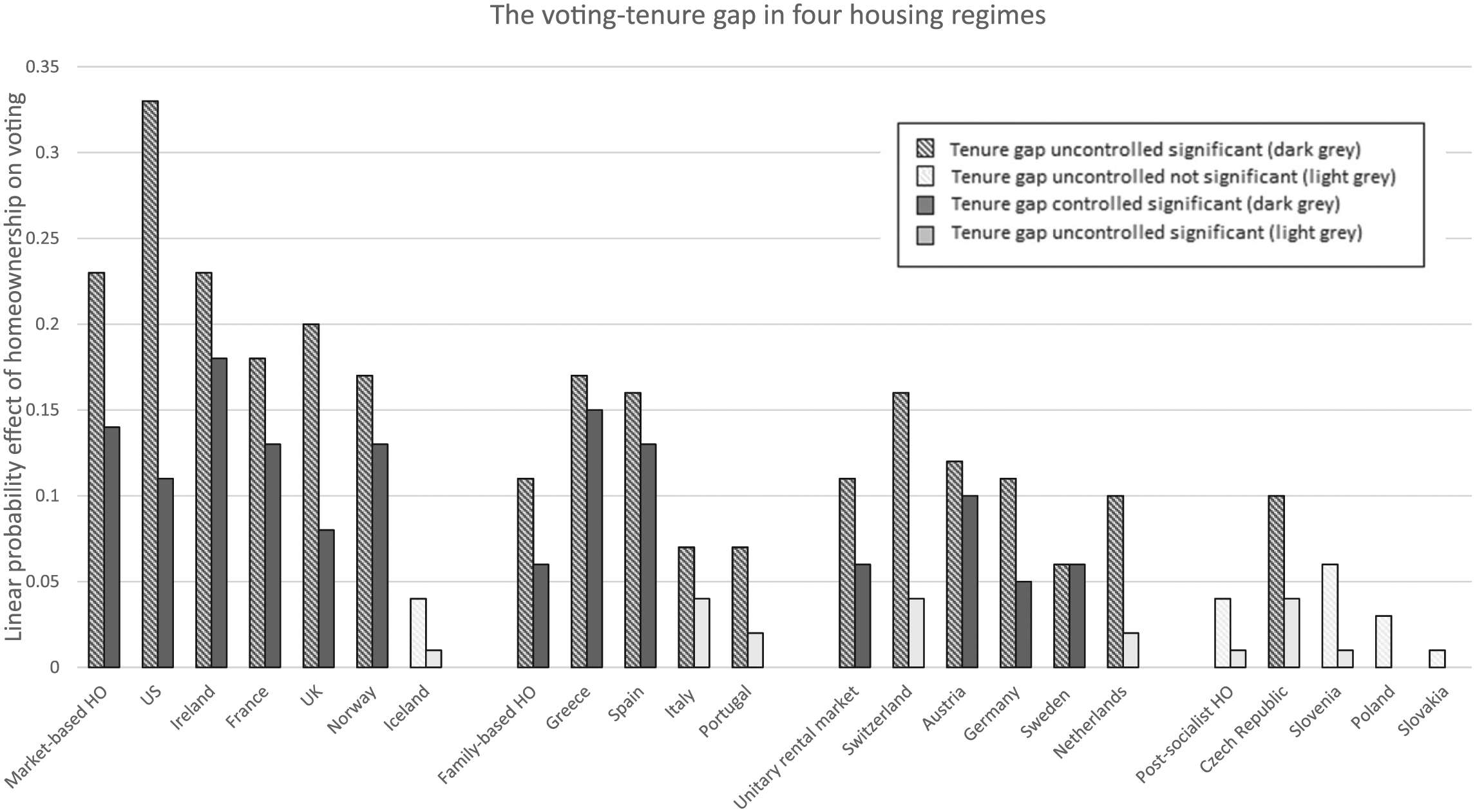

Hypothesis 2 predicted the tenure gap in voter turnout to be largest in the market-based homeownership regime, followed by the family-based homeownership regime and unitary rental market regime (the latter regimes having more or less comparable tenure gaps). We expected a non-significant tenure gap in the post-socialist homeownership regime. Figure 1 shows the estimate for the effect of ‘homeownership’ on voter turnout for each regime and country separately (before matching). The first bar is the uncontrolled estimate and the second bar is the ‘controlled’ estimate, including a control for our proxy of length of residence. When the tenure gap is statistically significant, the bar is dark gray; when it is not significant the bar is light gray. 9 For example, in the United Kingdom the controlled probability of a homeowner to vote in national elections is 8 percentage points higher than for a tenant, and this difference is significant. We indeed find the tenure gap in voting to be largest in the market-based homeownership regime (in line with Hypothesis 2a), while the gap is smaller in – but does not differ between – the family-based homeownership regime and the unitary rental market regime (in line with Hypotheses 2b). In line with Hypothesis 2c, the homeownership estimate is no longer significant for the post-socialist homeownership regime when controlling for measured socio-economic resources and for our proxy for residential stability.

The tenure gap in voting in four housing regimes.

In the market-based homeownership regime, we find large and significant estimates for ‘being a homeowner’ for all countries, except Iceland. In the family-based homeownership regime, estimates are only significant for Spain and Greece. A possible explanation is that house prices increased more in Spain and Greece between 2001 and 2004 than in Italy and Portugal (European Mortgage Federation (EMF), 2009), making investment-related considerations a possible driver of electoral participation for homeowners. The differences between the controlled and uncontrolled tenure gaps in Greece and Spain are rather small, indicating that resource-based selection into homeownership matters less. In the unitary rental market regime, estimates are, on average, half of those for the market-based homeownership regime.

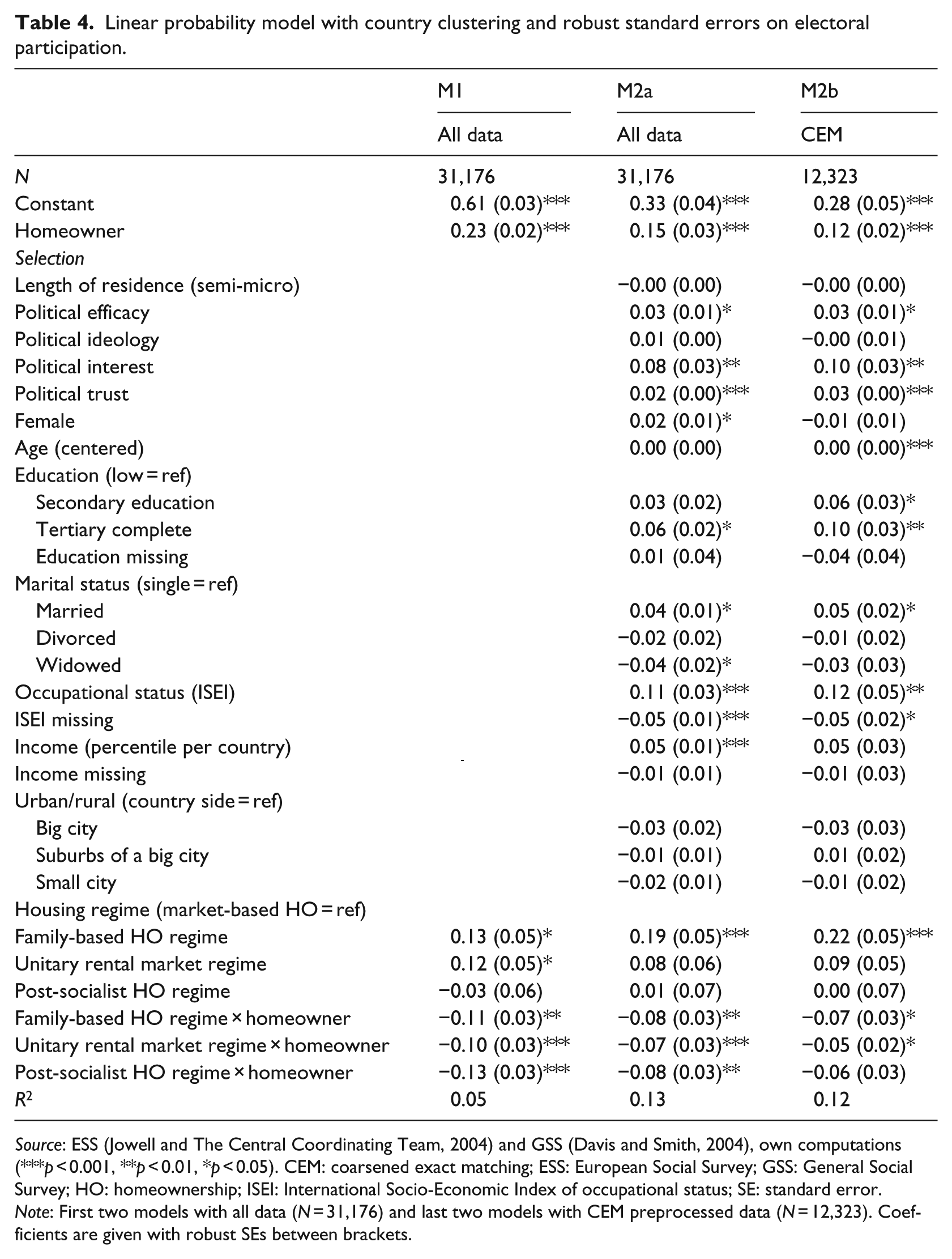

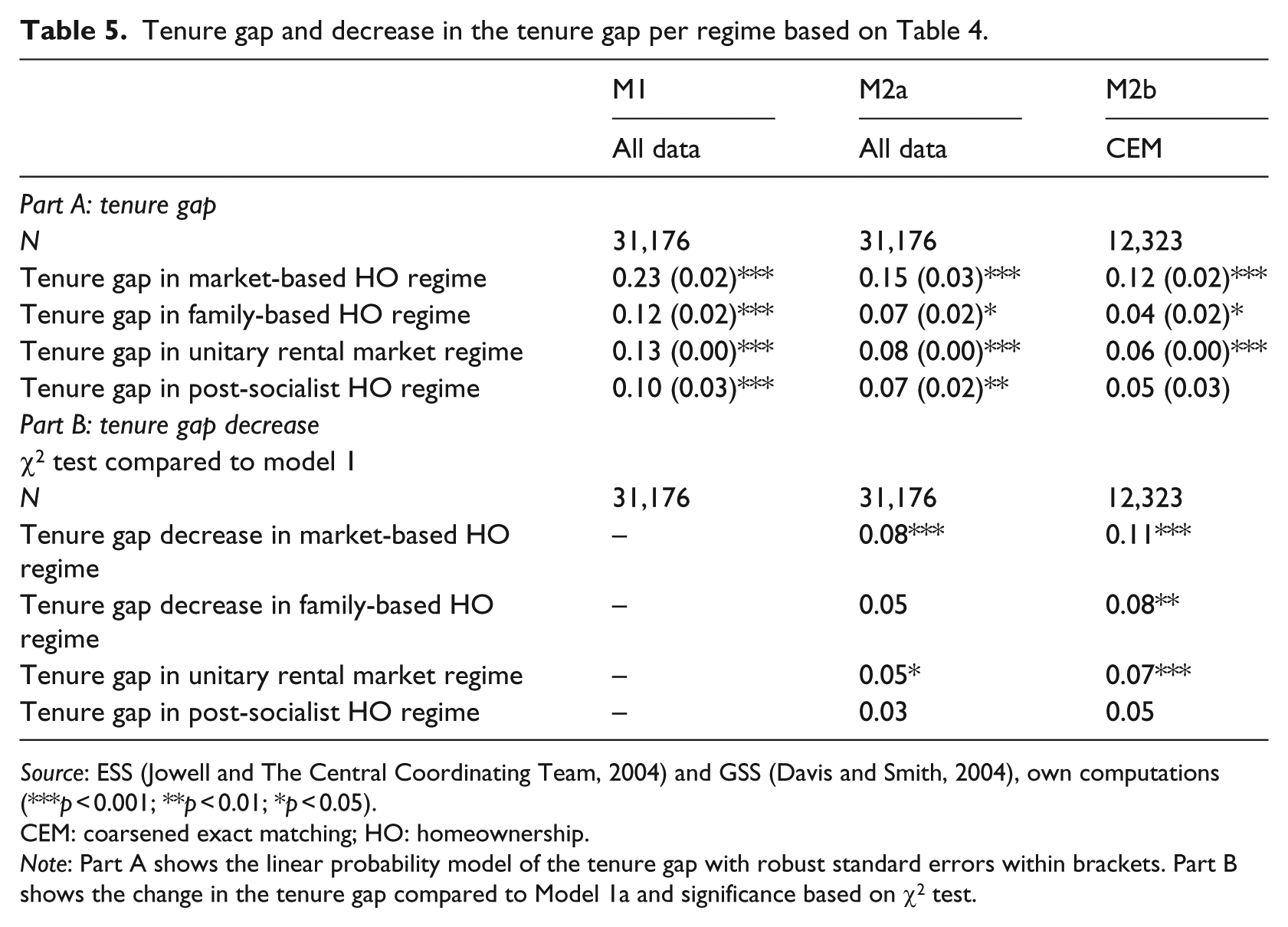

Additional information on Hypotheses 2a–c is provided in Tables 4 and 5. Table 4 shows results from LPMs with country-clustered standard errors. The tenure gap in voting for each regime can be calculated from the interaction estimate for the regime and the main effect of ‘homeownership’ (which refers to the tenure gap in the market-based homeownership regime). These tenure gaps are presented separately in Table 5. Model 1 presents the uncontrolled tenure gap in each regime, Model 2a shows the tenure gap controlled for measured socio-economic differences, length of residence, and political variables, and Model 2b shows the controlled tenure gap using CEM, with controls for the coarsened variables. In part A of Table 5, the tenure gap (i.e. the ‘homeownership’ effect) is shown, as well as an indication of its level of statistical significance. In part B, the decrease in the tenure gap compared to Model 1 is shown, alongside an indication of the level of statistical significance of this decrease, based on a χ2 test.

Tenure gap and decrease in the tenure gap per regime based on Table 4.

Source: ESS (Jowell and The Central Coordinating Team, 2004) and GSS (Davis and Smith, 2004), own computations (***p < 0.001; **p < 0.01; *p < 0.05).

CEM: coarsened exact matching; HO: homeownership.

Note: Part A shows the linear probability model of the tenure gap with robust standard errors within brackets. Part B shows the change in the tenure gap compared to Model 1a and significance based on χ2 test.

Table 5 shows the extent to which the tenure gap for each regime is reduced after including control variables (M2a). The tenure gap is reduced further when in Model 2b we control, as far as possible with cross-sectional data (through matching), for selection bias not captured by observed differences in socio-economic resources. The absolute decreases in the market-based homeownership regime (11 percentage points), the family-based homeownership regime (8 percentage points), and the unitary rental market regime (7 percentage points) are larger than in the post-socialist homeownership regime (5 percentage points), where less selection was expected. The ‘remaining’ effect is, as hypothesized, largest in the market-based homeownership regime, followed by the unitary rental market regime and the family-based homeownership regime (which do not significantly differ from each other), while it is no longer significant in the post-socialist homeownership regime. These findings are in line with Hypotheses 2a–c. 10

When controlling for differences in socio-economic resources as well as tenure-differences in residential stability and likely selection, differences between housing regimes diminish considerably. However, the tenure gap in voter turnout – be it of a smaller size – still remains significant in all regimes, except the post-socialist homeownership regime. Other explanations are thus needed in order to explain the higher turnout of homeowners versus tenants. Put differently, we cannot rule out that homeowners are encouraged to vote through instrumental motivations related to perceived social status or homeownership-related (investment) considerations. This is supported by our finding that the tenure gap is highest in countries characterized by a strong pro-homeownership ideology and/or where the financialization of housing markets turned owned homes into assets.

Conclusion and discussion

While policymakers and politicians in Europe and the United States justify pro-homeownership policies by referring to its presumed economic, social, and political benefits, we researched whether such a tenure effect can be established with regard to electoral participation for 19 countries. Expansion of homeownership was promoted to include and empower low-income households, although the (financial) limitations of these strategies became painfully clear after the GFC (Schwartz, 2012). Nevertheless, as housing and housing wealth are central to the welfare provision of households and to the overall political economy, and will remain so in the foreseeable future, it is relevant to research whether the presumed positive effect of homeownership on political participation is causal or rather due to selection into different housing tenures.

We integrated housing tenure in Instrumental Motivation Theory and expected a higher turnout of homeowners versus tenants based on perceived social status and economic considerations. In order to tackle – to the best of our abilities – issues with regard to selection bias, potential effects arising from tenure differences in residential stability, and general data limitations, a variety of methodological tools were used, such as matching (CEM) and the use of an imputed measure for residential stability. The latter means that we have to be cautious with our measure of residential stability. We furthermore ‘approximated’ different explanations for the tenure gap in voting by exploiting cross-country differences in contextual arrangements.

We indeed found a tenure gap in national election participation, and the positive estimate of ‘homeownership’ on voting varied in a systematic way across countries and housing regimes. At the micro-level, we found the tenure gap to be partly explained by differences in socio-economic resources (although a significant effect remained), tenure differences in residential stability, and ‘additional’ selection bias potentially captured through matching. At the macro-level, we showed the tenure effect to be largest in the market-based homeownership regime and smaller in the family-based homeownership regime and the unitary rental market regime. In the post-socialist homeownership regime, homeowners are no more likely to vote than tenants after controlling for likely confounders. We therefore cannot rule out that homeowners are encouraged to vote through instrumental motivations related to perceived social status or homeownership-related (investment) considerations. This is supported by our finding that the tenure gap is highest in countries characterized by a strong pro-homeownership ideology, and/or where the financialization of housing markets turned owned homes into assets. A limitation of this study is that with the data at hand, we cannot distinguish between these different motives. This should be addressed in future data collection and research projects.

Part of the difference in the tenure gap in voting between countries might be attributed to registration differences, which may somehow co-vary with housing regimes. When tenants move more often than homeowners, this may compromise electoral registration, which would in turn lower electoral participation (Kemp and Kofner, 2010). Although this is a possibility, we still find similar estimates in the country fixed-effects models, 11 in which all unobserved heterogeneity between countries is controlled for, for example, aspects of the electoral system (Franklin, 2004).

Future research should address two other limitations of our study: causality and a measure for residential stability. Although we controlled for the possibility that people who are more likely to vote are also more likely to buy a house in the strictest way possible with the cross-sectional data at hand, we cannot be sure that we captured all possible confounders. If there are ‘omitted variables’ that confound the association between housing tenure and voting but are not related to the ones we included, CEM will not be a fix to the causality issue. Furthermore, we only approximated residential stability at the micro-level and can therefore not explicitly test for this mechanism. Future research would thus be advised to use panel data (and therefore probably focus on one or several countries) to overcome these limitations.

Since we only researched voter turnout, we cannot comment on the association between homeownership and other forms of political participation. Although voting is the key political act in all countries under study, other indicators (e.g. membership of political parties) vary more strongly or have different meanings across countries. It would be interesting to replicate this research with more recent data, as the GFC has placed housing at the core of economic and public policy debates (André et al., in press), and recent housing market dynamics and trends affect outcomes for and interests of homeowners and tenants in several different ways.

Finally, the hypothesized (positive) homeownership effect on voting in national elections is present, but part of this effect is caused by selection into homeownership. There is no significant tenure gap in the post-socialist countries, as well as in five other countries. Better measurements potentially would allow for a ‘complete’ explanation of the tenure gap in more countries. Finally, housing regime differences in the tenure gap point at motivations related to both perceived social status and self-interested investment-related concerns around homeownership as an asset and welfare resource. Policy-makers should therefore be more cautious when promoting homeownership based on the argument that it turns people into ‘better citizens’ (DiPasquale and Glaeser, 1999). Homeownership may affect one’s interests, but it does not change one’s character.

Footnotes

Appendix 1

Description of macro-indicators in Table 1.

| Indicator | Description and source |

|---|---|

| Homeownership percentage | Homeownership as a percentage of the total housing stock are data from or closest to 2004 and are taken from Housing Statistics in the EU report from 2005−2006. Data are from 2004 except for Czech Republic (2000) and Portugal (2000). Data on Iceland and Norway are from the Hypostat 2005 (EMF, 2005) report. Data on Switzerland are from Bourassa & Hoesli (2006), Swiss Finance Institute Research Paper Series No. 07-04 |

| Social rental percentage | The social housing percentage of stock data are from the CECODHAS 2012 Housing Europe Review (HFN, 2014; Pittini & Laino 2011). Where data were missing, we used data of Eurostat. |

| Outright homeownership percentage | Data are from the European Quality of Life Survey (EQLS), for Turkey data are from EURLIFE, for Switzerland data are from EUROSTAT (see social housing), and for Iceland data are from a newspaper clipping (Iceland outright homeowenrship rate (n.d.). Outright homeownership for the United States is from Zillow Real Estate Research US outright homeownership rate (n.d.) |

| Homeownership percentage change 1980−2008 | Homeownership data from 1980 are taken from the same data sources as homeownership rates and from ‘housing indicators time-series’ for Norway, Iceland, and the United States |

| Mortgage debt to GDP ratio | Data are from the European Mortgage Federation (EMF 2005, 2009), Hypostat report 2008. Data are on 2004 except for Switzerland Hypostat 2004 report. |

| GDP | GDP per capita in US dollars divided by 1000. Data are from the World bank: http://databank.worldbank.org/data/reports.aspx?source=2&series=NY.GDP.PCAP.CD&;country=# |

| Mortgage Interest Deduction | Mortgage interest deduction (yes/no) is primarily taken from the IMF working paper Wp/08/211 House Price Developments in Europe: A comparison (Hilbers et al, 2008). Furthermore, Luxembourg has MID (Donner, 2000). Czech Republic has MID (Jahoda and Godarová, 2014) Hungary has MID (Donner, 2006) Poland has MID (Donner, 2006) Slovenia has MID (3%; Donner, 2006) also housing finance network.org Slovakia has no MID (Donner, 2006) United States has MID (housing-finance-network.org) ‘This unlimited, untargeted mortgage interest tax deduction causes costs of over 3 per cent of the total budget’. Iceland has no MID http://www.imf.org/External/Pubs/FT/SCR/2010/cr10213.pdf and Mortgage Credit Markets in Iceland and other European countries. |

| Rent control score | Rent control data are on the private rental sector from 2009, based on Organisation for Economic Co-operation and Development (OECD) Housing and the Economy file (OECD_47431120.xls), Figure 19. |

| Dualist/unitary | According to Kemeny (1995): Sweden, the Netherlands, Germany, and Switzerland are unitary rental systems. The United Kingdom is a dualist rental system. Hoekstra (2009) also classifies Austria and Denmark as unitary and Belgium and Ireland as dualist. Kemeny (1995) states that Anglo-Saxon countries (like the UK, New Zealand, and Australia) are dualist and therefore we also classify the United States as dualist. If we look at the macro-indicators for the countries that have already been categorized, we see, like Hoekstra (2009), that in dualist countries homeownership rates are high and social rental rates are low. The other countries in our sample are categorized as dualist, except for France, because of the relatively large social rental sector. Other data to inform our choice were from Donner (2000, 2006). |

| Housing benefits as percentage of GDP | Data are from the Public Expenditures Database of the OECD (Housing/Housing Assistance as percentage of GDP). For Slovenia, we use the number from Donner (Donner, 2006: 214). |

| Tenure residential stability | Compared to the private rental sector. Data are from OECD Housing and the Economy file (OECD_47431120.xls), Figure 8. |

GDP: gross domestic product; IMF: International Monetary Fund; MID: mortgage interest deduction.

Acknowledgements

The authors thank participants of the Housing Market Dynamics workshop of ENHR for their useful feedback on an earlier version.

Funding

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.