Abstract

In this article, we analyse how the crisis that emerged in Europe, specifically in Russia and Ukraine, has severely affected European Bull Market. Because of the political unpredictability and the fallout from the most recent sanctions placed on Russia, the financial markets in Europe have often responded negatively to the current geopolitical crisis. The contribution of the Europe Market is the focus of this article, and it does so by analysing several aspects of their behaviour. At the same time, this article contributes to an investigation into the consequences that the proclamation of war against Ukraine had on the stock markets of European countries, global economy and European economy specifically. In addition, the unfavourable reactions shown in stock prices lasted into the post-event period of time. There is a large range of variance in the degree to which stock values are affected by this crisis across sectors, nations, and the size of the firm. This variance may be seen in a wide range of possible outcomes. In addition to its empirical investigation, the research delves into topics pertaining to the marketing modulation as a future scope.

Introduction

The announcement of war against Ukraine affected the entire world, and at the same time, impacted the global business. Along with this, the event significantly influenced the stock market worldwide. The announcement influenced various sectors while drawing down a few. Additionally, affecting the stock market a few sectors were still stable compared with drawing down sectors.

The recent conflict between Russia and Ukraine worsened when Russia recognised the two regions of Ukraine, Donetsk and Luhansk, as independent isolated states. Then, the Russians mobilised their army to maintain peace in that region. This action by Russia exacerbated the conflict between the two countries. The leaders of the world have described the event as the beginning of a war. This led superpowers like the US, UK, and EU Nations to embargo Russia economically. The European Union (EU) was Russia’s most promising business and trade partner in 2020. Russia had an overall business of 37.3% across the globe (EC, 2022). The EU imported crude oil at a rate of 27%, solid fuel at a rate of 46.7%, and natural gas at a rate of 41.1% from Russia (Eurostat, 2022). Due to the interconnected economic structure of Russia with European countries by having global trade of various commodities, geopolitical conflict and restrictions are likely to affect world markets, as well as the Russian economy.

As a result, we feel obligated to investigate how traders in European financial markets respond to this tragic situation. According to previous research that investigated the connection between political unpredictability and the performance of financial markets, both market returns and the risk appetite of financial resources are greatly impacted by investors’ aversion to political instability (Jones & Banning, 2008). Berkman et al. (2011) use international political crises of varying severity to prove the importance of politics. They demonstrate that political crises are a significant explanatory factor for both average and extreme returns on stock markets worldwide. Similarly, Lehkonen and Heimonen (2015) argued that political risk is inversely related to stock performance. The authors backed up their conclusions with data from developing countries. Dimic et al. (2016) have concluded in their work that the profits made from currency carry trades are influenced by the level of political risk involved.

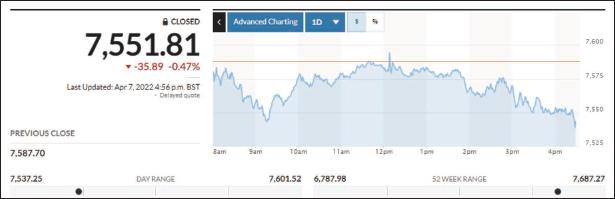

According to Smales (2017), there is a strong correlation between political uncertainty (such as the Brexit vote) and market turbulence. This conclusion was reached as a result of research on previous significant political risk incidents. Findings on the financial costs of diplomatic unrest between Taiwan and China demonstrate that political uncertainty is strongly correlated with an adverse effect from a stock return perspective (He et al., 2017). This investigation was released in 2017; additionally, they found a link between current stock return declines and predictions of future stress which was very substantial. According to Buigut and Kapar (2020) findings, the economic sanctions placed on Qatar stemmed from a significant increase in the stock market volatility seen in Qatar. In addition, Buigut and Kapar (2020) provided evidence for the Qatar sanction, which had a significant influence on the stocks that make up the Gulf Cooperation Council; however, the authors note that the impacts of the blockade were not uniform across industries or nations. This article focuses on the value of the stock market affected due to the war declaration against Ukraine. FTSE 100 index helps to understand the stock value that Europe is dealing with; on the other hand, the previously closed stock value of Europe was 7,587.70 as compared to the day range was also changed by showing the changes in numeric values from 7,537.25 to 7,601.52 (Figure 1). At the same time, the 52-week range change shows 6,787.98 to 6,787.98, respectively (MarketWatch, 2022).

This article highlights the war announcement effect on the stock market in terms of ‘cumulative average abnormal return (CAAR)’. The article also aims to evaluate the downfall sectors by comparing them with other sectors that were little more stable once the war against Ukraine was announced. Lastly, the effects are found by assuming the cumulative abnormal returns (CARs) value and return on assets (ROA) value in the article, respectively.

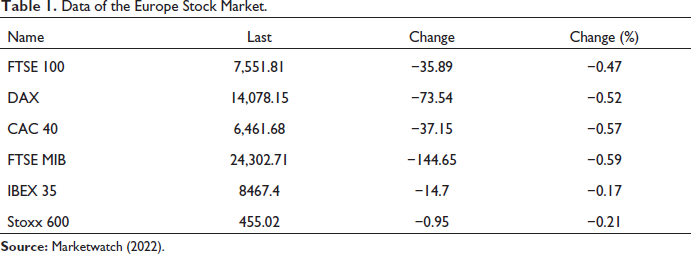

The behaviour of the Europe stock market was affected due to the announcement of war against Ukraine. At the same time, the stock market ripples affect the spooking investor and woes. According to Gordon and Recio (2022), the war between Ukraine and Russia shows some external effects, such as increasing the price of oil and reducing the stock price. At the same time, the approval of war against Ukraine has affected the behaviour of the stock market toward Ukraine investors. On the other hand, an effect on crude oil prices is considered a short-term impact. War affected the stock market of Europe and the UK, which are examined below. The changes occur in the stock price due to this crisis (Table 1).

Data of the Europe Stock Market.

Data of the Europe Stock Market.

The Ukraine conflict contributed to the increment in short-term market volatility. The stock market has constantly fluctuated due to the war between Russia and Ukraine. The FTSE 100’s last stock market rate was taken into account and which stood at 7,551.81, and it has changed by –35.89, the change in percentage was –0.47% due to the war crisis. Dax’s stock rate before the declaration of war was 14,078.15 and changed by –0.52% to –73.54 (Marketwatch, 2022). It may contribute to the almost deadline of the market. The Ukraine war also had an impact on the market of the CAC 40, and indices reduced the rate by –0.59% from its last value of 6,461.68 to –37.15 (Marketwatch, 2022).

The market index of Europe Data is FTSE 100 which helps to show

Here, R is shown as the rate of return of the sectors dealing with the stock market of Europe. The market of the index is termed as day t. At the same time, this helps to understand the CAAR of Europe stock value.

On the other hand, Rit is termed as the rate of return from the market value of the stock while the estimates of ARit and day t by Rit and ARit. At the same time, the abnormal return (AR) of firm R on day t is

The valuation of CAR is conducted on the market value of the stock as per today’s value

The above model (Equations [1–4]) will help us determine the position and impact on the Europe Data market.

Critical Analysis of the Behaviour of the Europe Stock Market After the Announcement of War Against Ukraine

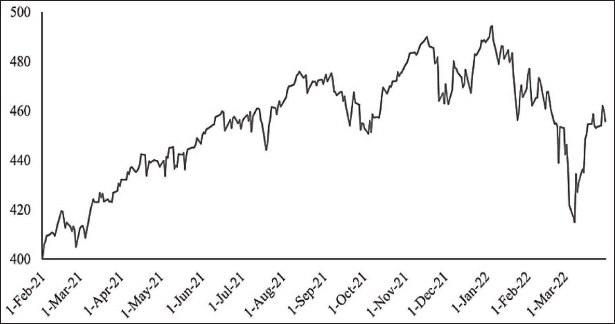

The study helps to understand the structure of the stock market after Russia declared war. behavioural changes in the Europe Data Market (Figure 2) were affecting the entire stock market worldwide. In this case, we are analysing the data from the stock market, focusing on the Europe data of the stock market (Marketwatch, 2022).

Trend in STOXX EUROPE 600 Index.

Trend in STOXX EUROPE 600 Index.

Impact of Announcement of War Against Ukraine on the Stock Market

Russia and Ukraine have a substantial impact on the global commodity and stock markets, and their conflict has affected them. An increment in crude oil prices crossed $100 per barrel now a day; it shows that it will become more expensive in the future (Boungou & Yatié, 2022). Furthermore, commodities such as oil and raw material coal directly affect the profitability of the corporate sector for going ahead. The cycle of interest rates is also rising at a very high speed, including the threat of inflation and the valuation of the stock market at a stiff premium (Ali et al., 2022). The trailing PE of FTSE 100 becomes 22 times earned, as well as at its highest record from the last year. It may still be above the benchmark of Kospi (11.5 times), Bovespa (7.1 times), Shanghai Composite Index (14.8 times), and so on (The Hindu Business Line, 2022). The announcement of the war’s negative impact on the London Stock Exchange (LSE) had major losses even from the beginning of the global pandemic in March 2020. European bouncers have recorded high falls in the interest rates affected by the fight in Ukraine across the continent. The FTSE 100 index has finished the 251 points, down by 6,998, which May 3.5% drop. The French and German stock market rate has continuously fallen by more than 4% (The Hindu Business Line, 2022).

Dax in Frankfurt indices of the German Stock Exchange had reached its lowest level. The Italian stocks turned 6.2% to the bare minimum level throughout the year. The chief market analyst estimated that the FTSE 100 faced shocker changes at its largest decline since the war (The Guardian, 2022). Investors in stock markets were piled up to invest their currency like the yen and dollar or gold and government bonds after the war announcement (Canuto, 2022). The Moscow stock exchange was almost reached at the point of its deadline. Moreover, the rouble had fallen to record lows amid the wider range of Russia (Yang et al., 2021).

Critical Evaluation of the Downfall Sectors by Comparing with Other Sectors That Are a Little More Stable Once the War Against Ukraine Was Announced

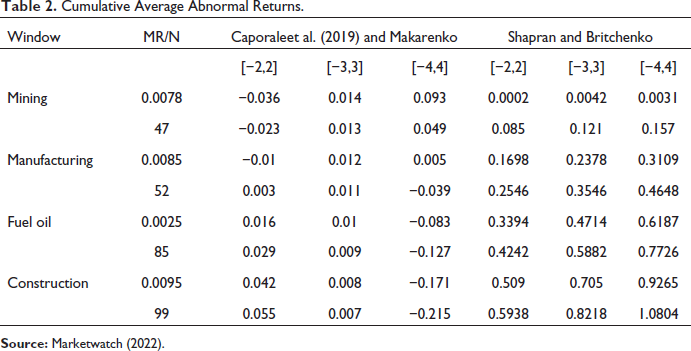

As given in Tables 2 and 3 above, helps us to understand the short-term reactions calculated CAAR’s sectors on taking the aspects on the Europe data market. At the same time, the above table helps to understand that some sectors were drawing down only by announcing war against Ukraine. The sector of mining was negatively impacted as the labour working in the mining industry refused to overcome the work scenario. The value of the downfall sector is 0.0025 compared to that of the stable value of 0.0042, respectively (Ikani, 2019). At the same time, the value of fuel oil has increased, which greatly impacts the European stock value. On the other hand, the Central Bank was going through the policy under the section that deals with the Russian Federation’s experience after the announcement of war, that value is 0.0078 and its overcoming chance value is –0.036, respectively (Shapran & Britchenko, 2022).

Cumulative Average Abnormal Returns.

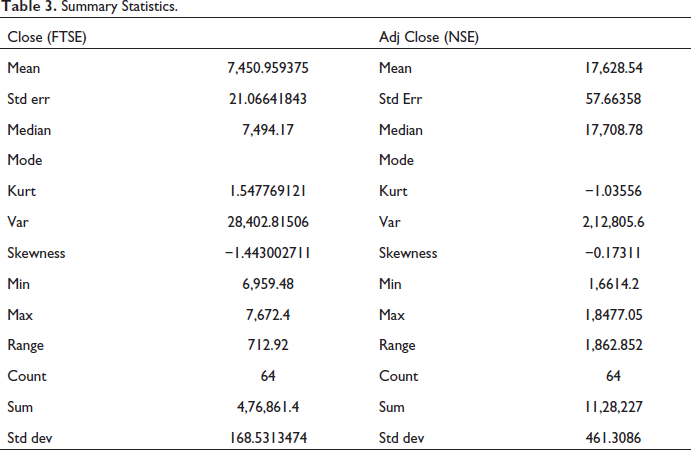

Summary Statistics.

The FTSE MIB has 24,302.71 at its past or before war desertion rate, which was reduced by –144.65 by –0.57%, as shown in the above data sheet (Marketwatch, 2022). The conflict affected the IBEX 35, which became –14.70 from the last rate of 8,467.40. Due to the conflict, Stoxx 600’s stock market rate has become –0.95 by its last rate value of 455.02, and the percentage has reduced by –0.21% (Marketwatch, 2022). This type of inflation and the changes in the value of the interest rate of the stock market before the announcement of the Ukraine war may contribute to the market’s volatility.

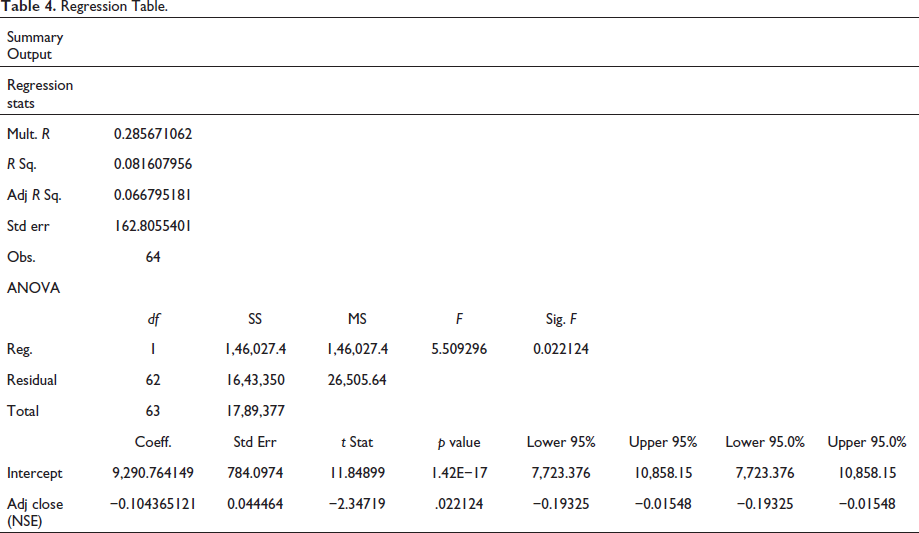

Therefore, the correlation helps to show the relation between the factors that are dealing by both the downfall sectors and little stable sectors after the announcement of war against Ukraine (Tables 4, 5 and 6).

Regression Table.

Correlation Table of High and Low NSE Market Value.

Correlation Table of Adjusted Close and Volume of NIFTY Market Value.

The NIFTY 50 helps to understand the condition of stock of shares after the announcement of war against Ukraine, where the mining sector has been down by reducing the share value to –1.89% per day (Yahoo, 2022). Compared to that, the construction sectors were improving stability by focusing more on and increasing the share price by 0.53% per day (Yahoo, 2022). Therefore, the implication of the high variations for determining the factors affecting the share value helps to understand the main reason for down falling sectors and stable sectors, respectively.

The Economic Impact on Global Economy

Europe’s economies are the most susceptible to disruptions because, According to institutional forecasts, a deflation of at least 1.5 percentage points is anticipated for the year 2022, with a potential reduction of 1% in GDP growth (EU, 2022). The automobile, transportation, and chemical sectors are among those that are most vulnerable to long-term inflation brought on by costly commodities. This increases the possibility of both public unrest and deflation of the economy. Some of the factors that will have a significant impact on the economic effects and the potential The economic impact of the suspension of Russian energy on Europe is expected to be significant, with potential consequences such as resource reallocation, fuel source switching, demand reduction, and source substitution. It is anticipated that the majority of the natural gas reserves held by Russia in Europe will not be able to be replicated, and it is anticipated that the existing prices will have a significant impact on inflation. With the exception of Russia and Ukraine, all countries’ growth forecasts have been revised downward as a result of war-related spillovers, a slowdown in growth in the euro area, and rundowns in resource, marketing, and monetary markets. Because Russia makes purchases in a great number of Asian nations, the amount of money that it sends to some Middle Asian nations, such as the Kyrgyz Republic and Tajikistan, is equivalent to 30% of their GDP. The Food and Agriculture Organisation of the UN (2022) reports that Middle Asia and the South Caucasus are accountable for the importation of nearly 75% of the wheat in the region, whereas Russia and Ukraine import roughly 40% (FAO, 2022).

Emerging economies in Europe and Central Asia are also being thrown into disarray as a direct result of the conflict. The lingering impact of the pandemic has led to a precarious economic situation in this region, with the potential for a slowdown in the coming year. According to Weizhen Tan’s projections for 2022, The European continent’s reliance on Russia for its oil and natural gas supply poses a challenge in achieving its consumption targets for these resources. The Eurozone’s reliance on trade exhibits a decline in overall terms, while Germany, Italy, and a significant number of Central and Eastern European nations continue to rely on Russia’s supply of natural gas. Between June 2021 and the onset of 2022, there has been a significant decrease in the importation of Russian gas to the EU, resulting in a reduction of its share from 40% to a range of 20–30%. ‘(McWilliams et al., 2022)’. Prior to the escalation of the crisis with Ukraine, the EU experienced a surge in the costs of petroleum, crude oil, and coal. The aforementioned phenomenon can be attributed to the relaxation of COVID-19 restrictions, the strengthening of the US dollar, and the reluctance of OPEC to increase production. The citation provided is attributed to Bachmann et al. (2022). With the abundance of varied sources in the worldwide market, it is possible to ascertain a feasible substitute for the importation of oil from Russia through the process of supplier substitution. The timing of targeted policy measures will determine the total costs; thus, the action should be assumed regardless of whether or not there is an embargo in order to prevent higher losses over the years 2022 and 2023. The utilisation of Russian imports in various sectors such as industry, households, trade and commerce, power provider organisations, and transportation, has been identified as a significant contributor to energy consumption (Bachmann et al., 2022). The utilisation of lignite, hard coal, and nuclear energy has the potential to decrease the reliance on natural gas for electricity generation. The adoption of alternative input applications for energy generation in industrial power plants may yield cost savings by reducing imports and substituting energy sources. This, in turn, could potentially alleviate the financial burden on the European economy (Mahler, 2007).

The Economic Impact of the Russia–Ukraine Crisis on Europe and UK

This article examines the economic impact of the ongoing conflict between Russia and Ukraine on Europe. Similar to the situation in the United Kingdom and other countries globally, analysts predict that EU nations will encounter elevated levels of inflation and supply chain disruptions in 2022 due to the direct impact of Russia’s incursion into Ukraine. The ‘majority of public debate on the crisis has portrayed European governments as divided, weak, and absent (Krastev & Leonard, 2022), As per the 2022 report by the European Council on Foreign Relations’, it has been suggested that a potential Russian aggression towards Ukraine could have a profound impact on the European perception of their security. According to Thomas and Strupczewski (2022), prominent financial authorities in the EU have suggested that the ongoing conflict between Russia and Ukraine will have a negative impact on the EU’s economic growth, resulting in higher energy prices and decreased business confidence. Nonetheless, these authorities have asserted that the EU is adequately prepared to manage these challenges. Bhattarai et al. (2022) have found that Russia holds the position of being the foremost exporter of both natural gas and oil globally, and that it is also the primary exporter of these commodities to Europe. Saudi Arabia’s decision to withhold additional oil supply as a supplement to Russia’s exports in the event of a decrease could have a substantial global impact on the price of the commodity (Lanktree, 2022). The authors posit that in spite of the high cost to Russia, a significant energy supplier to the EU, it is plausible that Russia may retaliate against EU sanctions by imposing limitations on the supply of oil, gas, and coal to the EU. The outcome of such a scenario would be elevated pricing for said commodities, heightened levels of uncertainty, and a reduction in consumption. According to Thomas and Strupczewski (2022), ‘persistent uncertainty will most likely act as a drag on consumption and investment, which will, in turn, impede growth’. The recent invasion of Ukraine by Russia has resulted in a significant increase in the price of natural gas in Europe, which has risen by approximately 20% since the beginning of 2022. This has led to a surge in inflation and inflated utility bills, with the current cost of natural gas in Europe being almost six times higher than its initial value (Wiseman, 2022). As per Wiseman’s 2022 study, it has been observed that European nations procure around 25% of their oil and 40% of their natural gas from Russia. The following is a statement issued by the President of the European Central Bank, Christine Lagarde:

What we know is that the two main channels through which the economy of the euro area will be affected will be through energy, prices, and confidence or the uncertainty channel; not so much through trade, which is limited between Russia and the euro area.

As per the European Commission’s projection, there is a possibility of a decline in the economic growth trajectory of all EU member states utilising the euro currency, which could potentially reach 4.0% by the conclusion of 2022. The current projection is lower than the anticipated 4.3% forecasted in November 2021, and its reliability is further compromised due to the recent aggression by Russia towards Ukraine (Thomas & Strupczewski, 2022). According to the same source, the chief economist of Berenberg Bank stated that ‘the drag from higher prices and the negative confidence effect may lower real GDP growth in the eurozone from 4.3% to 3.7% for 2022’ (Wiseman, 2022). Despite Russia’s significant role as a gas exporter to several European countries, the UK is not among them. Nevertheless, the sharp increase in oil prices on the global market has had a comparable impact on the United Kingdom, causing considerable apprehension. The aforementioned scenario bears resemblance to the circumstances observed in the United States. Similar to many other Western countries, the United Kingdom has been grappling with a persistent and escalating inflationary trend, characterised by a notable and swift surge in prices over the past three decades. As per the United Kingdom Parliament of 2022, a number of experts have expressed apprehension regarding the ongoing aggression of Russia towards Ukraine, which may result in a surge of inflationary pressure in the forthcoming months. As a result of this new development, the Bank of England might decide to investigate the possibility of increasing interest rates as a means of bringing the rate of inflation back down to its target range (House of Commons of the United Kingdom, 2022). Because Russia and Ukraine are both significant producers of a wide variety of agricultural products, such as wheat, and because an increase in inflation may place additional strain on the financial resources of households as well as businesses in the United Kingdom, there is a great deal of concern regarding the rise in the cost of food. This is due to the fact that Russia and Ukraine are both significant producers of a wide variety of agricultural products, such as wheat (United Kingdom Parliament, 2022). According to Martin Young, an analyst working for the financial group Investec, the amount of money spent on fuel by households each year might exceed £3,000 (Jones, 2022). According to Nick Allen, the Chief Executive Officer of British Meat Processors, two-thirds of the ammonium nitrate fertilisers that are used by farmers around the world come from Russia (Lanktree, 2022). Fertiliser is one of Russia’s top export commodities, and despite the fact that the United Kingdom produces 90% of its wheat, farmers may have to pay extra for it because it is one of Russia’s most competitive exports (Jones, 2022).

This research explores the responses of the European financial market to Russia amid the announcement of war with Ukraine. We predicted a negative response from the European capital market, which has a unified conglomerate with Russia’s economy, due to increased political instability, geographical closeness, and the possible repercussions of any negative measures being enforced on Russia. Wars and military confrontations significantly limit the trade among adversaries through the use of embargoes or the patriotism of customers; nevertheless, following the cessation of immediate military threats and there is no tension forecast for the future, the trade will steadily resume (European Commission, 2022). The struggle between Russia and Ukraine in 2022 can be summed up by what Antony Blinken, the Secretary of State of the United States of America, had to say about it: ‘it’s greater than a conflict between two countries. It is more extensive than both Russia and NATO together’. According to the United States Department of State (2022), ‘It is a crisis with global consequences, and it requires the attention and action of global stakeholders’. Previous research has demonstrated that armed conflicts and wars have a significant impact, both locally and on the economy of the entire world (Hang et al., 2021; Jola-Sanchez & Serpa, 2021).

In addition to the direct costs, which are typically quantified in terms of the loss of human lives and other resources, there are additional costs associated with the destruction of property as well as the disruption of international trade (Glick & Talyor, 2010). According to our investigation’s findings, most investors are taking the situation in Russia and Ukraine meticulously. The consequences of this geo-political situation are already being felt in many regions of the globe. If this battle continues for a long period of time, it might have extremely negative repercussions globally. As a result, world leaders must act in dialogue to safeguard their individual countries’ financial stability. The adoption of governmental actions such as fiscal and monetary policies, as well as other applicable measures, may boost investor confidence. Europe’s short-term priorities should include lowering its dependency on crude oil and gas supplies over Russia and developing alternative resources for long-term sustainability. Meanwhile, European officials should investigate ways to reduce their dependency on Russia. The present political instability in Russia and Ukraine has underlined the need to emphasise the growth of renewable energy sources.

According to Hang et al. (2021), wars and other forms of armed conflict have negative repercussions not just for the states that are actively involved in the conflict, but also for other nations that are indirectly affected by it. Hence, it can be concluded that the behaviour of the European stock market was affecting the entire stock market after the announcement of war against Ukraine. At the same time, European bouncers have recorded high falls in the interest rates affected by the fight in Ukraine across the continent. Additionally, the announcement of war against Ukraine has become the main reason for the rising price of fuel oil in the market. Therefore, the article also includes the data and the methodology on the stock prices that are affected due to the war announcement by showing Empirical Results, respectively. We were unable to include the larger data set in order to examine the accuracy of the model, which we have decided to leave for the scope of future study.