Abstract

The paper focusses on one of the aspects of the Covid-19 induced economic crisis in India .i.e., the consumption demand for non-essential commodities which is an important component of the overall aggregate demand. As the number of Covid-19 positive cases are swelling up and lockdown is being phased out, this study, based on the primary survey of 900 plus individuals across various states, age, income and occupation groups in urban areas, has attempted to ascertain the consumer sentiment so as to predict the changes in private consumer spending during the current financial year on various items once the lockdown is completely lifted. These items include those that were ‘planned’ for during the year (for instance, electronics, real estate, automobiles, domestic travel) as well as ‘discretionary’ spending on retail and e-commerce, wellness and hospitality services. The survey responses have been used to determine the timeframe of recovery for each sector through econometric analysis of the deferment in the expenditures for each sector.

Introduction

The novel COVID-19 has resulted in substantial and palpable damages across the globe in a short span of the past few months. India has been particularly susceptible to the effects of the pandemic, owing to the high population coupled with high density. The nationwide lockdown called by the State had been lauded as an effective pre-emptive measure, seeing as one that led to plateauing the curve, with experts indicating a slower rise in the number of cases when compared to most other economies, particularly those in the West. Notwithstanding, there are signs of a greater threat to economic stability in the short, medium and long-term. The disruptions in the supply chain and a reduction in consumption demand have the potential to spin the crisis to unprecedented levels, with even the possibility of a complete breakdown of the economy (Ghosh, 2020). This article focuses on one of the aspects of the ensuing crisis, that is, the consumption demand for non-essential commodities which is an important component of the overall aggregate demand of the economy.

This is particularly relevant because laggard GDP growth in India over the past few quarters has been attributed largely to low private consumption, which contributes approximately 60 per cent to the GDP. Given the trudge of a run-up over the past fiscal year, the lockdown and the anticipated economic crisis are collectively expected to exacerbate the decline throughout this fiscal. In fact, in its Monetary Policy Report (April,2020), the Reserve Bank of India expressed concern over a potential repeated ‘severe demand shock’ for the economy, which can further translate into even lower growth in the country’s GDP. Moreover, Moody’s slashed India’s GDP growth forecast to zero for the current fiscal year. This outlook is a reflection of the increasing risks to economic growth and warrants a dire need for recovery measures.

Given this increasingly abysmal scenario as the number of COVID-19 positive cases are swelling up and lockdown is being phased out, this study, based on the primary survey of 900 plus individuals across various age, income and occupation groups in urban areas, attempts to ascertain the consumer sentiment so as to predict the changes in private consumer spending during the current financial year on various items once the lockdown is lifted. These items include consumer spending that was ‘planned’ for during the year (e.g., electronics, real estate, automobiles, domestic travel) as well as ‘discretionary’ spending on retail, e-commerce and other services. The study also aims to identify the time of recovery in each sector by analysing the deferment in demand for all the respective sectors.

The paper is divided into five sections. Section II details the survey and the questionnaire, followed by Section III which elaborated the methodology and model fitting for this study. Further, the results of the study for different categories of consumer demand are presented in Section IV.

Data and Survey

The data for the study has been obtained through a primary survey during the peak of the COVID-19-induced lockdown (first and second week of May 2020). The sample constitutes of 967 participants from the urban areas of 26 States and Union territories. Around 78.2 per cent of the total participants reside in Delhi NCR, Rajasthan, Maharashtra and Haryana 1 while other states 2 contribute about 21.8 per cent of the total respondents. Due to the limitations of online reach during the lockdown, data from other states could not be collected as extensively.

As regard the demographic composition of the sample, 40.4 per cent of the respondents were females. Moreover, 55.6 per cent were in a ‘relatively young’ age group of 18–35 while the remaining were in 36 years and above (‘relatively older’) group. The survey also collected responses across diverse occupational groups including Private sector employees, Business owners/self-employed, government employees and others. 3 Furthermore, the survey covered individuals with different economic status. 23.8 per cent of the respondents had a monthly income of less than Rs. 30,000, 22.1 per cent with income between Rs. 30,000 and 60,000 and 22.3 per cent belonged to the income group of Rs. 60,000–1,00,000. On the other hand, very high-income individuals (with a monthly income of more than 2 lakhs) constituted only 12.3 per cent of the sample. Thus, the survey largely constitutes of the middle-class in urban India.

Through the questionnaire, information was collected on how the respondents will alter their consumption demand for non-essentials during the current financial year once the lockdown restrictions are removed. The survey included questions regarding demand during the year for five items that were planned for by a respondent at the beginning of the calendar year—consumer electronics, 4 real estate, gold, automobiles and domestic tourism. These are referred to as the ‘planned demand’ for the purpose of the study. Additionally, ‘discretionary demand’ like shopping other than essential items, beauty services, occasional outings 5 and ordering-in food were also included. The questionnaire also gathered information on the relative choice between e-commerce versus retail sector as regards these ‘discretionary demand’ for the remainder of the year once the lockdown restrictions are completely lifted. In addition, responses were also collected about whether COVID-19 positive cases were present in the locality of an individual (indicative of the risk of contagion) and if the household constituted of dependents (above 60 and below 10 years of age) who could be at a higher risk of contracting the disease.

Model Fitting

Given the differing nature of the expenditures, ‘planned’ and ‘discretionary’ items have been analysed separately. Both descriptive and econometric analysis has been undertaken in an attempt to determine the likelihood of individuals to continue demand per usual, defer or altogether cancel it. The timeframe of assessment has been taken starting from whenever the lockdown is completely phased out in individual states.

For planned demand, two types of models have been applied. Firstly, binary logistic regression analysis (I) was used to determine if there are any significant differences across each item’s demand (hence, the corresponding sector demand), gender (female or male), occupation (private or government), age group (‘relatively young’ and ‘relatively old’) and income on the dichotomous response variable (deferment by less than 6 months from the lockdown being lifted/deferment by more than 6 months). Separate regressions are run for each sector offering a comparison with other sectors taken together. Dummies were used for the independent variables—occupation, sex and age group, presence of COVID-19 positive cases in the vicinity (yes or no) and that of dependents in the household.

Secondly, in an attempt to assess a detailed timeframe of demand recovery across different sectors, a more granular-dependent response variable, with not only multiple but also ordinal categories, was used. These categories are—no change in demand, deferred by 1–3 months, deferred by 3–6 months, deferred by more than 6 months from when the lockdown is completely lifted and Cancelled demand for the current year. Consequently, ordinal regression method 6 (proportional odds model) was applied using the previously used independent variables. The parallel regression assumption holds in the model as indicated by the likelihood ratio tests of cumulative link models (CLM). The p-value, thus, obtained was >0.05 indicating that the null cannot be rejected 7 and there is no evidence of non-parallel slopes. To facilitate across sector comparisons, dummies have been created pertaining to each sector in this regression model (II) with base category electronics (discussed in the next section). The other independent variables as in model (I) were used.

As regards the discretionary demand for retail and e-commerce, only ordinal regression (CLM) was applied (model III) wherein the response variable was ordered with the values—use immediately after lockdown, deferred by 1–3 months, deferred by 3–6 months, deferred by 6–9 months and deferred by more than 9 months post lockdown.

The likelihood function of the cumulative link model (proportional odds model) used for regression II and III along with the interpretations of the MLE estimates are discussed in the appendix.

Consumer Sentiment for the Current Financial Year 2020 Post the Lockdown: An Enquiry

Planned Demand

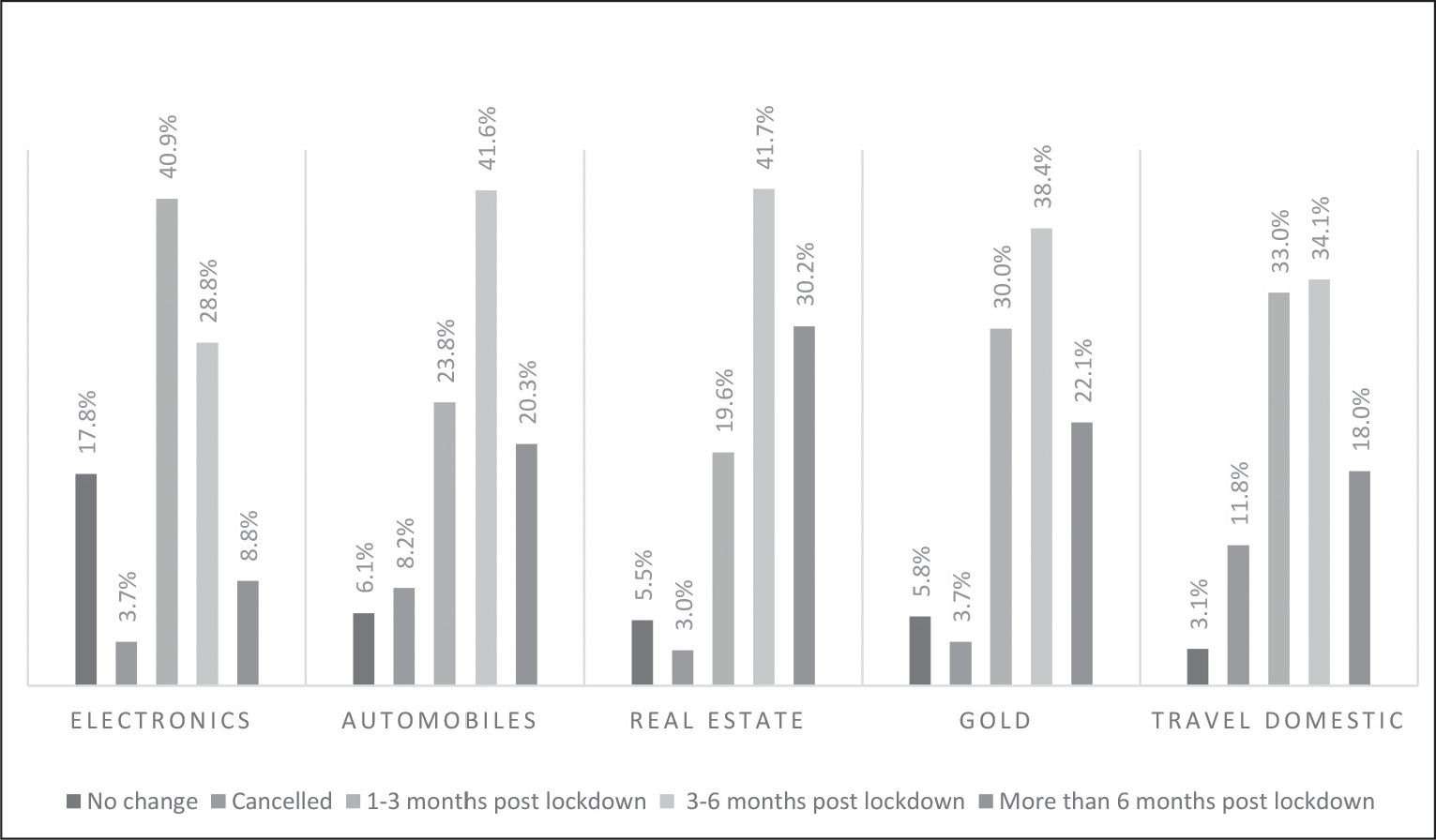

The proportion of total respondents who had planned purchases under this category for the year was highest for domestic tourism (59%) followed closely by electronics (45%). However, for automobiles, gold and real estate, the share was less than 24 per cent. This is in lines with an already low private consumption demand for these sectors in India, particularly since the last financial year. However, as a consequence of the lockdown, there are significant changes in the private demand as indicated by the responses of the participants. The sector-wise results have been presented in Figure 1.

It is observed that the lowest cancellations 8 have been for electronics and gold to the tune of only 3.7 per cent of those who had planned for such purchases. On the other hand, automobiles (8.2%) and domestic tourism (11.8%) have witnessed the highest cancellations. Furthermore, Electronics also had the largest share of respondents have not altered their planned consumption demand despite the COVID-19 scare (17.8%). The said share is quite low for the other sectors—domestic tourism (3.1%), real estate (5.5%), gold (5.8%) and automobiles (6.1%). Notwithstanding, the overall deferment ratio 9 is quite high (>75%) for all items, though it varies across sectors. There are also significant differences in the timeframe of deferment across these five sectors.

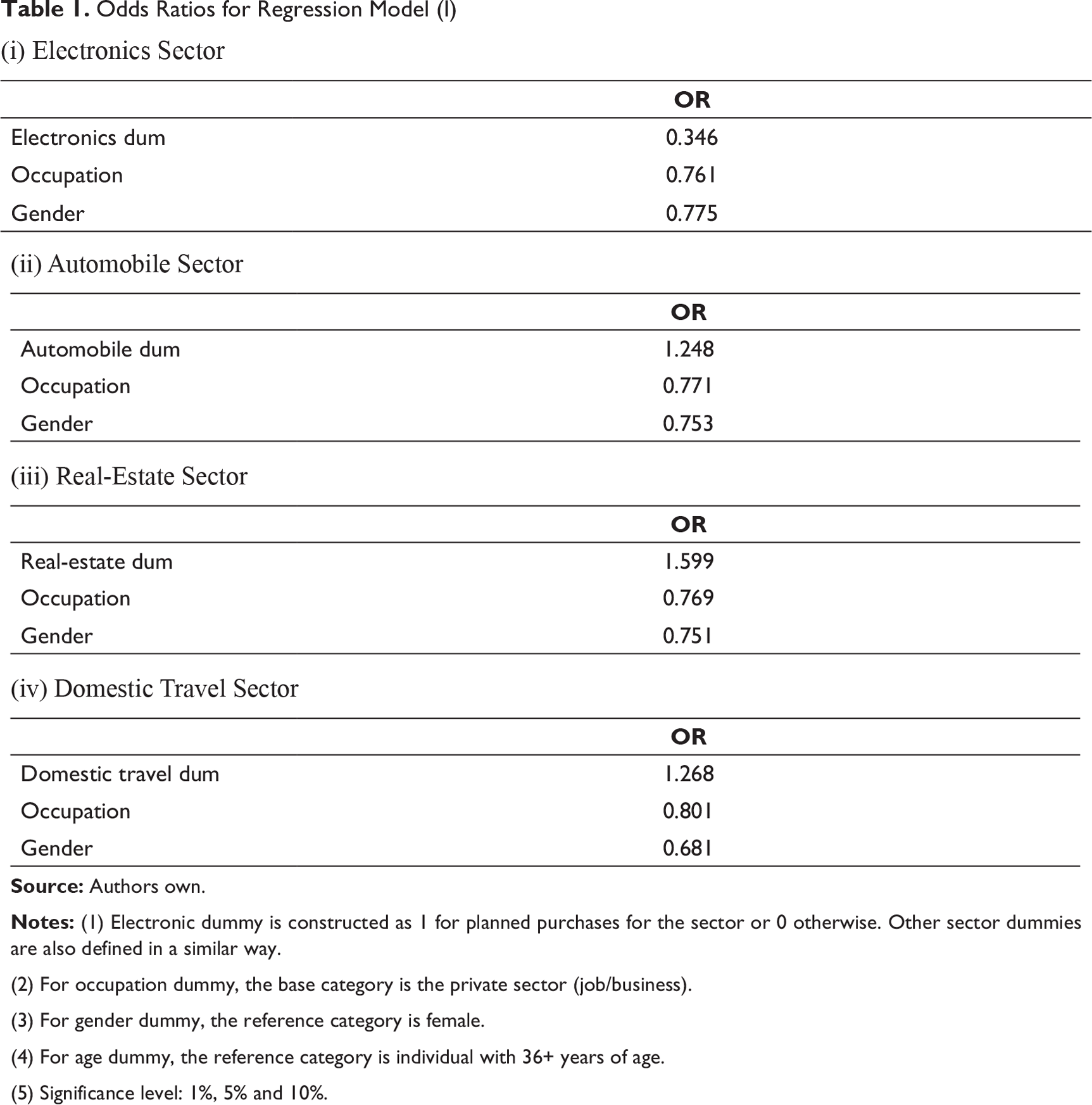

Odds Ratios for Regression Model (I)

(2) For occupation dummy, the base category is the private sector (job/business).

(3) For gender dummy, the reference category is female.

(4) For age dummy, the reference category is individual with 36+ years of age.

(5) Significance level: 1%, 5% and 10%.

For the electronics sector, the odds ratio of 0.346 signify that those who planned to buy electronics in the year 2020 are less likely to defer the consumption demand by more than 6 months versus less than six months relative to other sectors. For automobiles, real estate and domestic travel, the odds ratio being greater than 1 indicates a higher probability of deferment of ‘more than 6 months’ compared to ‘less than 6 months’ when compared to the other items. The Gold dummy was found insignificant.

Furthermore, to assess the impact of the economic slow-down (and the consequent financial/job uncertainty) on people’s buying behaviour, the occupation dummy was used. Gender, age groups and income were also considered. While the occupation and the gender dummy were significant, the age and income dummies were insignificant for all sectors. For the respondents employed in the government sector, the odds of deferring by more than 6 months versus deferring by less than 6 months are lesser than of those employed in the private sector for all the regressions. A similar observation is made for female participants in the survey. Regardless of the sector, the odds ratio so obtained demonstrates a risk-averse behaviour of the females. A lower odds ratio implies that the males are less likely to defer the planned consumption demand by more than 6 months versus less than 6 months, when compared to females, for all the items considered.

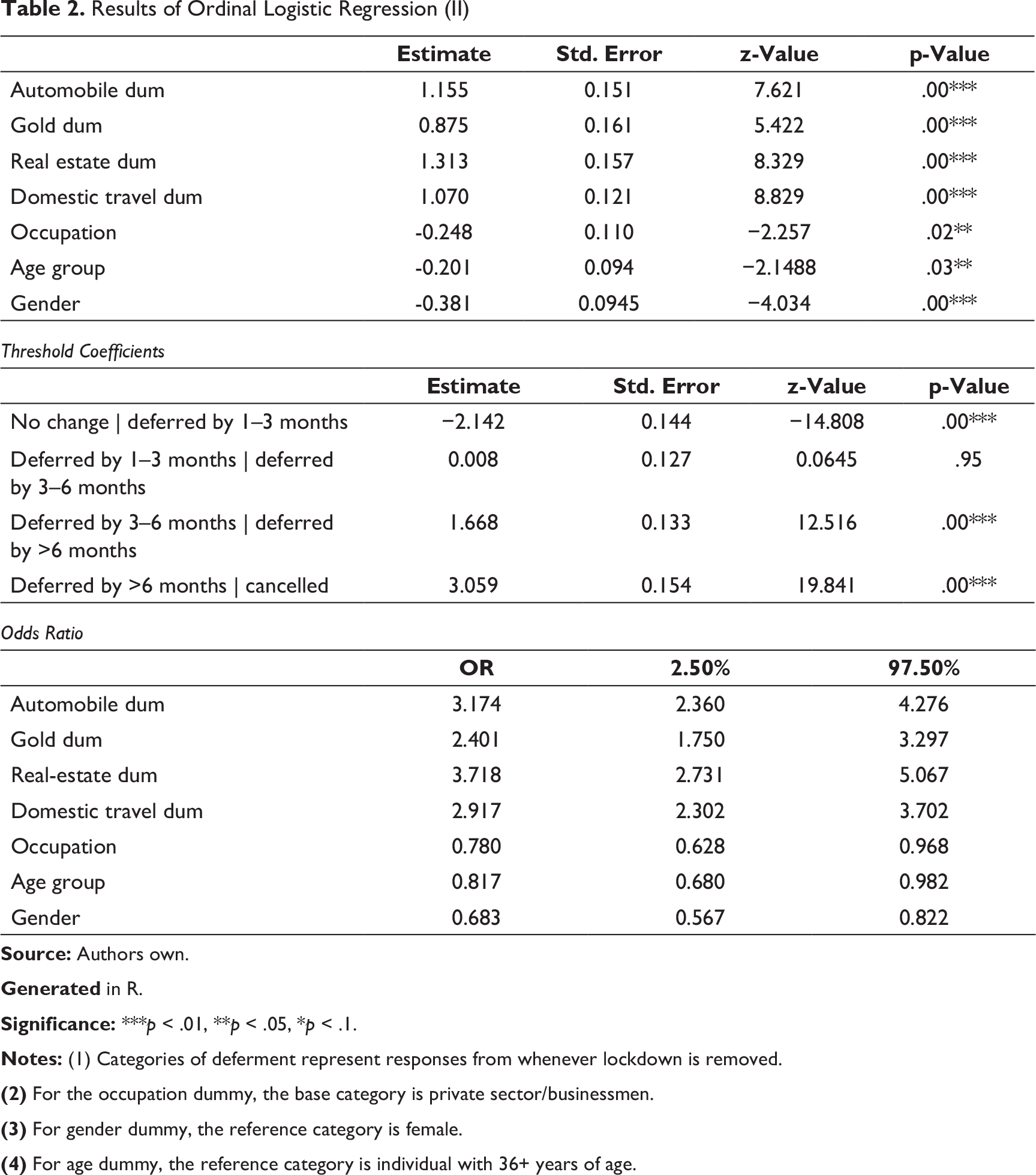

Results of Ordinal Logistic Regression (II)

Generated in R.

Significance: ***p < .01, **p < .05, *p < .1.

(2) For the occupation dummy, the base category is private sector/businessmen.

(3) For gender dummy, the reference category is female.

(4) For age dummy, the reference category is individual with 36+ years of age.

The positive sign of the regression coefficient for automobile, gold, real estate and domestic travel sector dummies indicate that an individual who had planned to purchase these items at the beginning of the year is more likely to be in the higher categories of deferment when compared to the electronics sector. Using the odds ratio, it is evident that the odds for automobiles sector of ‘cancelled’ versus ‘deferred by >6 months’, ‘deferred by 3–6 months’, ‘deferred by 1–3 months’ and ‘no change’ combined are 3.17 times that of electronics. A similar trend is observed for gold (2.4 times), real estate (3.72 times) and domestic travel (2.92 times) relative to electronics.

Thus, it can be inferred that the respondents are more likely to cancel their planned demand on all sectors relative to electronics. The likelihood of ‘cancelled’ versus ‘deferred by >6 months’, ‘deferred by 3–6 months’, ‘deferred by 1–3 months’ and ‘no change’ combined is the highest for real estate followed by automobiles. This suggests that while the novel COVID-19 has adversely affected the private consumption demand for all the sectors, private consumption of electronics is expected to fall the least for urban areas during the financial year while domestic tourism, automobiles and real estate, the most. While their deferment period is also more than 6 months, their fall in demand during the financial year relative to their planned demand will be much higher.

This can be could be attributed to three factors. Firstly, for the past decade or so, there has been high penetration of consumer electronics, particularly in urban areas, making them near-essentials (phones, tablets, laptops, etc.). Secondly, e-commerce offers an already accessible easy substitute for retail outlets thereby reducing the overall impact of contagion risk on these purchases. Thirdly, relative to the other sectors, the size of expenditure under this head is much smaller. Hence, while there will be a severe immediate impact on the private demand of electronics, it can pick-up to a certain extent within 6 months of the lifting of the lockdown. This sector can then head for a speedy recovery at least in the urban areas so long as there are limited supply-side disruptions.

Furthermore, the odds ratio for the occupation dummy is 0.78 implying that the government sector employees are less likely than the ‘others’ to ‘Cancelled’ versus ‘deferred by >6 months’, ‘deferred by 3–6 months’, ‘deferred by 1–3 months’ and ‘no change’ combined for all items and individual Income level were insignificant variables. Consequently, the exogenous factor of COVID-19 and the consequent impact on the state of the economy (and job stability) is an important factor in explaining the change of expected consumption behaviours.

Moreover, results similar to previous regression (I) regarding gender were obtained. On the contrary, the Age dummy was now significant; the odds being 0.82. It can be inferred that respondents in a younger age-group (18–35 years) are less likely to cancel their planned demand versus the other categories combined, relative to the respondents of 36+ years. A general risk-averse behaviour accompanying ageing could explain the result.

Interactive terms of sector dummies with age, gender and occupation were found insignificant. Thus, differences across sector-wise buying decisions due to age, occupation or sex cannot be anticipated in the dataset. In addition, the presence of COVID-19 cases in the vicinity or that of the dependents in the household was also found to be insignificant with respect to the deferment decision for planned expenditure items.

Discretionary Demand

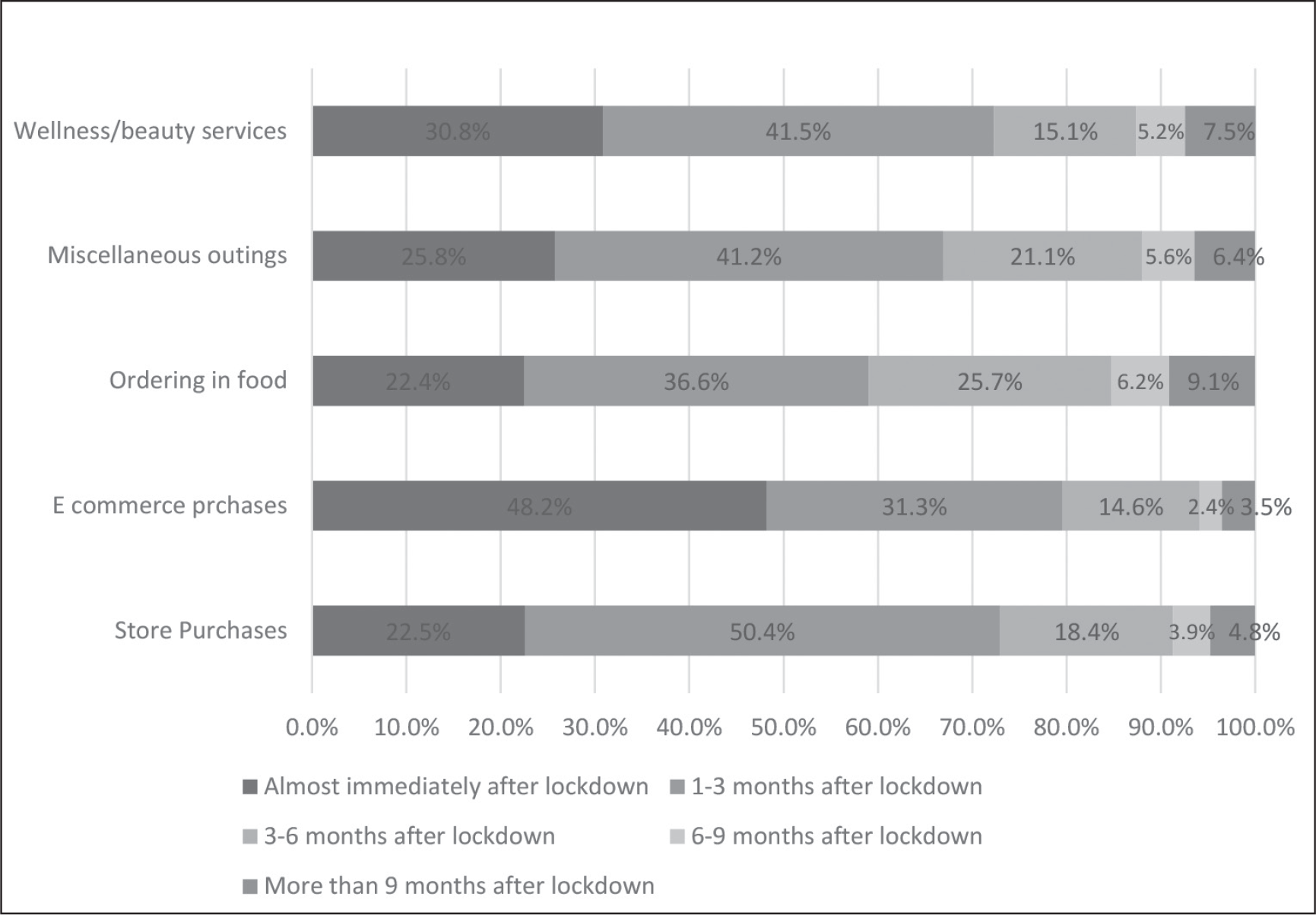

The responses in the survey conducted also aspire to capture the effect the present situation may have on the private consumption of discretionary goods and services. In the wake of the COVID-19 virus scare as well as the lockdown put in place as a preventive measure for the same, the citizens face a changed scenario and the analysis of responses so given, hopes to examine this change through the consumption pattern (Figure 2).

The results reveal that amid the corona scare, people have deferred the consumption of goods classified as discretionary by a few months for most of the goods and services, other than those offered by the e-commerce sector which includes the giants like Amazon and Flipkart and other mushrooming startups. A detailed discussion for both e-commerce and retail has been explained later.

The analysis reveals that the circumstances are not so encouraging for the sectors in consideration. Most of the respondents seem hesitant in resuming consumption demand immediately after the lockdown ends. Regarding the food, beverage and the entertainment industry which can be gauged by the decisions regarding ‘going out’, it is observed that the respondents are willing to defer their expenditure. As less as one-fourth of the total respondents (25.7%) are willing to take chances and resume spending on restaurants, movie theatres and other recreational activities immediately once the lockdown ends. Others, however, are prepared to wait for additional three months after these places are opened up (41.16%). Interestingly, a less percentage of participants came across as highly risk-averse and delayed the resumption by 6–9 months or more of incurring expenditure on stores (8.69%) and going out (11.99%) entailing that a large share of the respondents will possibly resume spending and aid revive the retail sector and the food, beverage and the entertainment sector within 9 months of the lifting of lockdown, subject to the COVID-19 cases not increasing steeply.

The lockdown restrictions have been more stringent in public places to avert the risk of increasing the virus spread and thus the aforementioned sectors seem to be facing distress. These public places also include salons, barber shops, spas and other such services on which the government guidelines have been particularly strict regarding their remaining closed till the present conditions are brought back under control. Coherent to the directions issued, most respondents (41.47%) are hesitant and are willing to wait up to three months of the end of the lockdown before resuming these services, as analysed through the responses received. Although surprisingly, 30.82 per cent of the respondents would not hesitate to start spending on these services immediately when they open up whereas, only 7.45 per cent highly risk-averse people are planning to put off the utilisation of these services for more than nine months.

Furthermore, the most unexpected observation which was observed through the examination of the survey was the decisions regarding ordering in of food, which is carried out by service providers for food delivery like Zomato, Swiggy, etc. This sector seems to have taken the greatest hit and do not seem to be recovering soon. Triggered primarily due to the threat of the virus spread and presumably the COVID-19 infected food delivery boys in news, a majority of respondents (77.56%) do not wish to start ordering food immediately after the lockdown ends. 36.61 per cent of the respondents are willing to wait at least a period of up to three months and 25.65 per cent up to 6 months of the end of the restrictions before beginning ordering in food again. This sector shows the most sluggish-paced signs of revival. Once at least 6 months have passed after the end of restrictions and circumstances seem to be getting restored, only then does this sector shows signs of improvement.

The results are uniform across age, income and occupation groups. The present reason for the delay is apprehended to be the scare of the COVID-19 contagion and would improve eventually with the medical treatment or/and a vaccine for COVID-19 being introduced.

All the above-stated sectors have endured strains in demand of their services in the present circumstances which appears to continue further for a few more months even after the restrictions are lifted but the demand seemingly will bounce back within 9 months to a year of the ending of the restrictions put up by the government contingent on the fact that the economic situation at the macro level does not deteriorate and the virus spread does not shoot up. Although, this can have a cascading effect if the macroeconomic conditions in the country do not improve amid the twin problems of supply chain disruptions and a decreased demand. The revival which can take place within nine months will then be further advanced, hampering the economy in turn by a circular effect and the economy would be at the risk of getting tangled into this vicious circle of lower demand and lower incomes.

e-commerce and Retail

Allying with the other sectors, though both the e-commerce and retail sector will be put up against the fence due to a reduction in consumer demand, e-commerce sector appears to be bouncing back the earliest, as evident in the responses received. As shown in Figure 2, most of the respondents (48.19%) plan to resume shopping through e-commerce immediately as the lockdown ends. e-commerce offers the facility to stay at home and thus seems to be the safer choice for the respondents. Majority of the participants were eager to resume availing the e-commerce services within three months after the restrictions are lifted completely (79.52%). Comparatively, the survey reveals that more than half of the respondents (50.36%) do not plan to resume shopping from stores before 1–3 months have passed after the lifting of the lockdown restrictions.

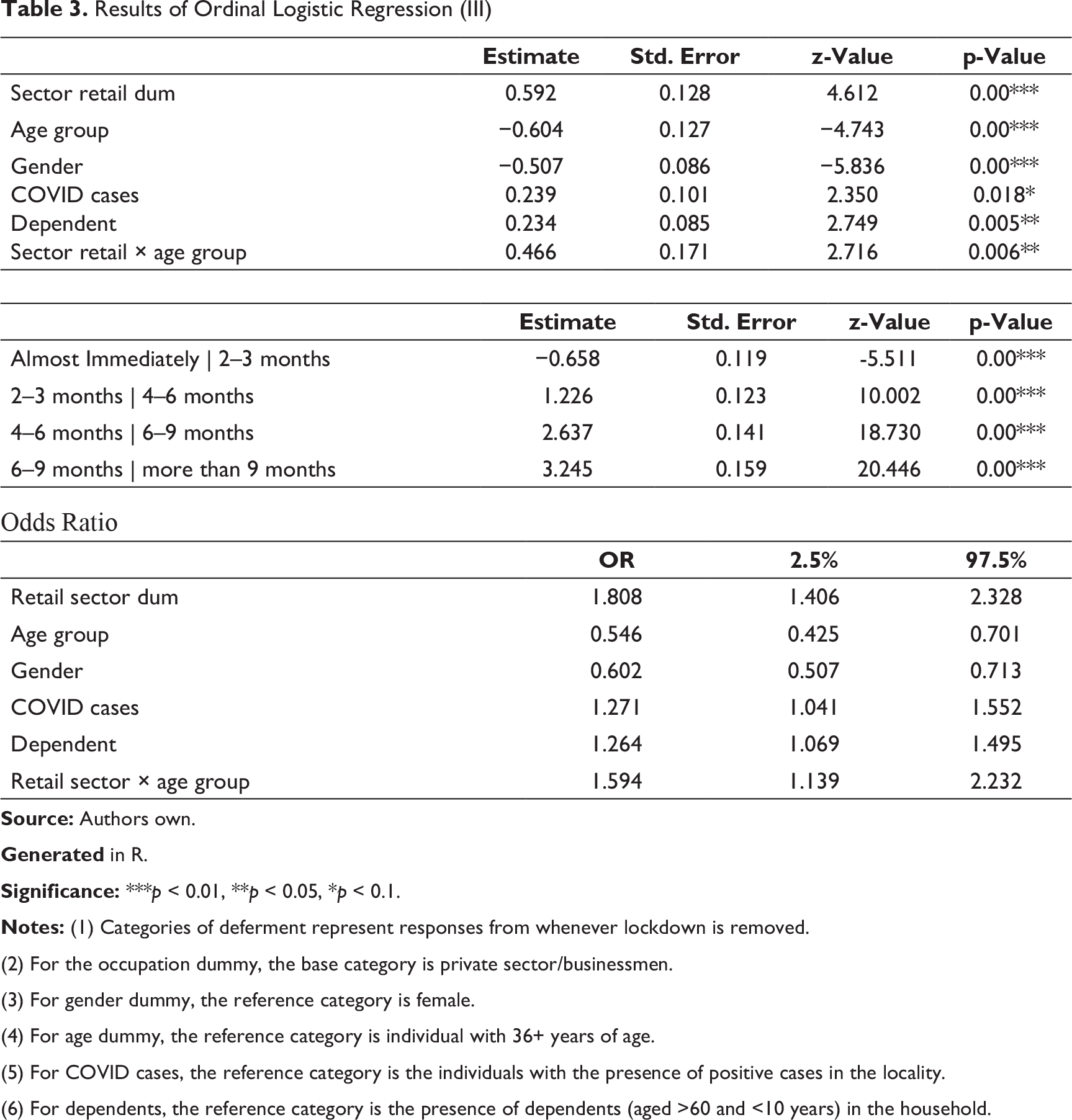

Results of Ordinal Logistic Regression (III)

Generated in R.

Significance: ***p < 0.01, **p < 0.05, *p < 0.1.

(2) For the occupation dummy, the base category is private sector/businessmen.

(3) For gender dummy, the reference category is female.

(4) For age dummy, the reference category is individual with 36+ years of age.

(5) For COVID cases, the reference category is the individuals with the presence of positive cases in the locality.

(6) For dependents, the reference category is the presence of dependents (aged >60 and <10 years) in the household.

The results of the cumulative link model have been shown in Table 3 along with the regression coefficients as well as the odds ratios so calculated. All the considered variables were found significant. The odds ratio of the explanatory variables along with the 95 per cent confidence interval has been shown in Table 2. The fit of the model was determined using the Lipsitz test and no lack of fit was found (p-value > 0.05).

The coefficients for the age and gender dummies are negative indicating that males (relative to females), as well as the respondents who are relatively young (compared to age group 36+ years), are less likely to be in higher categories of deferment. When expressed through the odds ratios, the odds of males deferring their consumption demand for retail or e-commerce by more than 9 months versus other categories combined is 0.6 times that of females. This indicates that females are more risk-averse to COVID-19 in this analysis even if lockdown is removed. Additionally, the odds ratio for the age dummy is 0.54 implying that the respondents in a younger age-group (18–35 years) are less likely to defer their demand versus the other categories combined, relative to the respondents of 36+ years.

It is observed that the odds of deferring by more than 9 months versus deferring by 1–3 months, 3–6 months, 6–9 months and ‘almost immediately’ combined are 1.88 times more likely for retail than that of e-commerce. This implies that the demand for e-commerce services, although has reduced under the present circumstances, yet the sector offers a greater opportunity of improvement owing primarily to the ease it provides for the people in the comfort and safety of their homes.

The regression coefficients so obtained for the variables COVID cases and Dependent are positive signifying that the individuals with the presence of positive COVID cases in the locality as well as the individuals with the presence of dependents (members <10 and >60 years of age) in the household are more likely to be in the higher categories of deferment as compared to their counterparts. In terms of odds ratios, such individuals are 1.2 times more likely to defer by 9 months versus other categories than individuals with no COVID cases in their locality or dependents in the households. The presence of COVID cases and dependents put the individuals in a more vulnerable situation and as a risk-averse decision, he/she is more likely to defer consumption to avoid contact and thus probable infection.

Occupation dummy was found to be insignificant and thus no inference can be made. Interactive dummies were also taken in account and regressions were thus run. There was, also, significant interaction found between age group and sector in this segment. The coefficient is positive, and the odds ratio is 1.594, implying that the individuals belonging to the relatively younger group are more likely to defer retail sector consumption as compared to e-commerce. This can be attributed to the younger population being more at ease with technology and electronic gadgets as compared to the relatively older population.

As lockdown restrictions have begun to be lifted in a phased manner across the states, it is imperative for the State to recognize not only an anticipated demand shock but also the various sector-wise nuances of the consumer spending on non-essential items, notwithstanding the supply side difficulties. In this regard, the present study has attempted to provide a small-scale assessment of the consumer sentiment in the post-lockdown scenario in the urban areas to provide some useful insights for policymakers.

The survey, expectantly, revealed that consumer demand is expected to decline significantly for both discretionary items as well as planned items during this financial year. What is pertinent, in this regard, is that despite lockdown easing, consumer expectations have been altered in a manner that demand for all sectors considered in the study (albeit at varying degrees) is expected to be low even after the economy is allowed to operate per usual.

Within planned expenditures, while the demand for electronics is observed to recover largely within 1–3 months post lockdown, for others like real estate, automobiles and domestic tourism, it can only recover after 6 months of the lockdown being lifted. As found by the ordinal regression analysis, the respondents are more likely to cancel their planned demand for all these sectors and on gold relative to electronics. This could largely be attributed to increased penetration of consumer electronics in India as well as a lower size of the expenditure itself vis-à-vis other expenditures. Furthermore, when comparing across various categories of discretionary expenditure, the e-commerce sector is most likely to recover from the repercussions of the ongoing pandemic and its restrictions. It can, thus, be argued that a push to e-commerce in the form of allowing delivery services, encouragement to existing retail stores to permit delivery sales online can have the twin benefit of having a feedback effect on the demand and of providing a means of income to the vulnerable ‘gig economy workers’. Together, consumption demand with assurances of safe delivery can push the demand for these products almost immediately.

For the other sectors, however, the primary concern for postponement of purchases has been financial insecurities particularly among the private sector employees and business owners/self-employed anticipating a general collapse of the economy. As shown in the analysis through ordinal regression, the occupation dummies are significant implying that the respondents working in the government service are the least likely to be affected as income security may play a significant role for the same. The absolute decline in the consumption demand of government employees for the year is also much lower than that of Private sector employees or Business-owners/self-employed individuals. Thus, financial or job insecurity forms an important reason for the deferment and cancellation of planned expenditure.

Other factors like distance to the nearest health centre, availability of COVID insurance cover or cashless Mediclaim, access to ICT services and other institutional factors like governance and regulatory quality can also have a worsened impact on the individual expenditure decisions but they could not be incorporated owing to the limitations of our survey. It is essential to emphasize here that the survey has explicitly focused on the urban middle class which constitutes a larger share in the overall demand for the sectors considered. However, once the migrant workers (who have now been forced to return to their respective states) and the rural population is accounted for, the overall fall in consumption will be significantly higher for most of these sectors. For individuals belonging to lower-income quintiles and informal occupations, the impact may be even higher. In brief, it could be summarised and reaffirmed that owing to the onslaught of the pandemic the consumption demand has overall dwindled and the year 2020 is annus horribilis for the economy.

Footnotes

Declaration of Conflicting Interests

Funding

The authors no financial support for the research, authorship and/or publication of this article.

Notes

Appendix

The cumulative link model with a logit link is widely known as the proportional odds model. A cumulative link model with a logit link is a regression model (Christensen, 2015) for cumulative logits:

logit(γij) = θj −

The logit function is defined as logit(π) = log[π/(1 − π)] and cumulative logits are defined as

logit(γij) = logit(P(Yi ≤ j)) = log(P(Yi ≤ j)/(1 − P(Yi ≤ j)), j = 1, …, J − 1

where cumulative probabilities are

γij = P(Yi ≤ j) = πi1 + … + π

ij

; such that P(Yi ≤ j) = P(Y ≤ j|

F is the inverse of link function, γij is the linear predictor and

−∞ ≡ θ0 ≤ θ1 ≤ …≤ θJ−1 ≤ θJ ≡ ∞