Abstract

We examine how the authority of investors to speak about climate change with corporations is established. Leveraging the ‘communication as constitutive of organisations’ (CCO) perspective, we analyse who speaks on behalf of whom (or what) in shareholder engagement on corporate carbon emissions. Based on access to private dialogues between an engager acting on behalf of a pool of investors with 20 utility corporations, we identify how three authoritative personae—that of diplomat, advocate, and coach—convey climate change concerns. We find that the mirroring of these authoritative personae by corporations may lead to deliberation, evasion, or rejection of the suggested courses of action. We theorise how relational authority is communicatively constituted in shareholder engagement through a process of mirroring and switching between authoritative personae. Our framework contributes to the study of CCO and relational authority by highlighting how meta-figures are used by external actors in an attempt to author appropriate corporate actions. We discuss the implications of our framework for the role of shareholder engagement in current attempts at greening financial capitalism.

Keywords

Climate change communication is often characterised by polarised public discussions (Bowden et al., 2021; Porter et al., 2018), and the recent debate about the role of financial actors in addressing environmental, social, and governance (ESG) issues has not escaped this polarisation (Economist, 2022, The Economist, 23 July 2022, Three letters that won’t save the world, p.9). On the one hand, it has been argued that financial markets are part of the systemic structures that contribute to climate change by encouraging corporations to focus on short-term shareholder value (de Bakker et al., 2020; Schneider, 2020). Practices such as shareholder engagement, which entails the communication of investor concerns about ESG issues in private interactions with corporate managers, are therefore viewed with scepticism. These practices are typically described as maintaining financial capitalism’s status quo (Rhodes and Fleming, 2020), especially as some of the actors involved—such as iconic pension funds BlackRock or Vanguard—also contribute to financing the fossil energy industry (Buller, 2022). On the other hand, a growing number of governments (PRI, 2022) and institutional investors believe financial actors play an important role in the transition of capitalism towards sustainability (European Commission, 2018). From this perspective, shareholder engagement is seen as a promising approach for redirecting corporate attention towards climate change issues (Ferraro and Beunza, 2018; Krueger et al., 2020). Such practices have been encouraged through regulation in several countries (e.g. France, the United Kingdom) and at the European level in recent years (European Commission, 2018).

Beneath these contrasting views on shareholder engagement lies a broader question about the authority of financial actors to speak about and act on climate change concerns within the constraints of financial capitalism (Beccarini et al., 2023; Rhodes and Fleming, 2020). We investigate this question by asking whether and how investors gain the authority to speak about climate change in the context of shareholder engagement. We argue that shareholder engagement constitutes and builds on the relational authority (Huising, 2015) of investors, as their formal authority to influence corporate practices is contested (Fama and Jensen, 1983; Hendry et al., 2006). In such contexts, authority needs to be established through the building of relationships and interactions (Bourgoin et al., 2020; Mukherjee and Thomas, 2023), which becomes even more crucial when engagement is outsourced to specialised intermediary organisations, as is often the case in shareholder engagement (Cundill et al., 2018). We thus explore the process by which shareholders and their intermediaries constitute their authority to speak about climate change in shareholder engagement.

Even though ‘communicative action’ (Habermas, 1987) has been found to be key to the effectiveness of shareholder engagement (Ferraro and Beunza, 2018), the ways in which the constitutive character of communication in this setting impacts on authority relations (Kuhn, 2008) have remained relatively underexplored. 1 We employ the ‘communication as constitutive of organisation’ (CCO) perspective to highlight how communication in shareholder engagement is constituted by mediated chains of actors speaking for or on behalf of—that is, ventriloquising (Cooren, 2012)—different matters of concern. The metaphor of ventriloquism signifies the idea that all parties in an interaction constantly animate, or are animated by, different figures to make their case (Cooren and Sandler, 2014). Owing to the constant oscillation between being the ventriloquist and the dummy figure (Schoeneborn and Vásquez, 2017), anyone or anything can be positioned to speak. CCO’s broader, relational view of agency in communication (Cooren et al., 2015) allows us to analyse the constitution of relational authority in interaction by unpacking how the figures that convey matters of concern regarding climate change come to prescribe or ‘author’ a specific course of action (Porter et al., 2018; Vásquez et al., 2018).

Based on a case study of shareholder engagement undertaken by a specialised intermediary organisation, working on behalf of institutional investors, we examine how figures are animated to convey matters of concern regarding carbon emission reductions to utility companies. We show that these figures and their associated vents and material attributes constitute a repertoire of authoritative personae, including those of a diplomat, advocate, and coach. Furthermore, the mirroring of these personae in the communication process leads to deliberation, rejection, or evasion of the suggested course of action to be taken to reduce corporate carbon emissions. We theorise that the communication that underlies shareholder engagement is constitutive of relational authority through a process of mirroring and switching between authoritative personae.

Our study offers a threefold contribution to organisational theory. First, we advance organisational studies of shareholder engagement and activism (Ferraro and Beunza, 2018; Goronova and Ryan, 2014) by highlighting how the authority of intermediaries in shareholder engagement is relationally constituted through communication. In so doing, we draw attention to both the potential and the limitations of shareholder engagement in embedding ESG within the financial marketplace. Second, we contribute to the CCO perspective (Cooren, 2012, 2020) by examining how distinct authoritative personae are constituted communicatively through ventriloquising. We conceptualise ‘meta-figures’ as a collection of figures and associated attributes that together animate overarching matters of concern, and delineate how the concept can be used to investigate interorganisational communication in the contexts of sustainability, financial markets, and the dynamics of authoring the organisation (Benoit-Barné and Fox, 2022; Kuhn, 2008; Taylor and van Every, 2014). Third and finally, our study extends concepts of relational authority (Bencherki et al., 2021; Bourgoin et al., 2020) by showing how switching and mirroring of authoritative personae can enable or constrain the process by which matters of concern become matters of authority. As a whole, our findings show the value of CCO concepts (Schoeneborn et al., 2019) to understanding whether and how ESG concerns can be embedded in financial markets.

Communication as constitutive of shareholder engagement

Shareholder engagement is generally conceived as a specific form of shareholder activism whereby shareholders try to engage in direct dialogue with corporate representatives on ESG issues (Ferraro and Beunza, 2018: 1190). 2 Although there is a long history of activism by fringe shareholders on social issues, particularly in the US (Vogel, 1978), shareholder engagement on climate change concerns has recently gained currency among mainstream institutional investors (e.g. BlackRock, 2018). In the wake of the 2008 financial crisis and the global climate crisis, regulators have called for more ‘active ownership’ by which shareholders intentionally seek to influence corporate policies and practices (Dimson et al., 2015, 2021; Goronova and Ryan, 2014). This active role is frequently theorised by building on Hirschman’s (1970) ‘exit, voice or loyalty’ framework: when confronted with questionable corporate behaviour, ‘investors have a limited range of actions open to them’ (McNulty and Nordberg, 2016: 351). Essentially, they can exit by selling shares, or choose to exercise voice, that is, seek to influence corporate practices through private dialogue or public activism (Goronova and Ryan, 2014).

Shareholder engagement usually involves dialogue and private interactions with company managers through letters, conference calls, or face-to-face meetings, which makes it distinct but complementary to other, more public practices of shareholder activism, such as voting or filing a resolution at an annual general meeting (AGM). Given the time- and resource-intensive nature of engagement, many investors outsource the dialogue to intermediary organisations that collectively represent their interests, such as the Principles for Responsible Investment (PRI) (e.g. Dimson et al., 2021; Slager et al., 2023) and the Interfaith Centre for Corporate Responsibility (ICCR) (e.g. Ferraro and Beunza, 2018; Rehbein et al., 2013), or to specialised service providers, which undertake dialogue on their behalf (Dimson et al., 2015). A fully fledged ‘industry’ of engagement services has thus emerged (O’Sullivan and Gond, 2016).

Research that has examined the effectiveness of shareholder engagement has focused on financial outcomes as well as corporate performance in managing ESG issues. Based on proprietary datasets, these studies have clarified the conditions under which engagement is associated with improvements in corporate ESG performance (Barko et al., 2022; Dimson et al., 2015, 2021; Semenova and Hassel, 2019; Slager et al., 2023). Somewhat surprisingly, given recognition of the communicative character of engagement as captured by the phenomenon of exercising voice, actual communication between shareholders and corporate managers has received scant scrutiny in these studies. A notable exception is the work by Beccarini et al., 2023 and Ferraro and Beunza, 2018. Building on Habermas’s (1987) theory of communicative action, or action determined ‘on the basis of common situation definitions’ (p. 285), these studies recognise the value of focusing on the communicative dimension of shareholder engagement. We extend their approach by examining the constitutive character of the communicative process by which opposing principles, norms, values, policies, and other nonhuman entities express themselves to come to define the situation (Cooren, 2020: 177), as we still have limited insight into the process by which the agreed courses of action on ESG issues are ‘authored’ (Porter et al., 2018) or ‘talked into being’ (Cooren, 2020) in engagement.

The process of authoring legitimate action on climate change is especially poignant given the fragmented and contested nature of authority in regulating social and environmental challenges (Beccarini et al., 2023), which is reflected in the debate about ESG and the appropriate role of financial markets in transitioning capitalism towards sustainability (Rhodes and Fleming, 2020; Schneider, 2020; Slawinski et al., 2017). Within the sphere of corporate governance, questions about the authority of shareholders also continue to be raised (Fama and Jensen, 1983; Hendry et al., 2006). In many corporate governance systems, shareholders’ monitoring role does not automatically translate into a formal duty for the corporation to listen to shareholder concerns raised outside of the AGM. Investor Relation departments have been established in many corporations since the 1990s to manage communication and information disclosure between corporate boards, analysts, and the financial market (Rao and Sivakumar, 1999), but these departments have traditionally not been focused on ESG issues.

In the absence of an accepted authoritative voice, investors and their intermediaries need to establish relational authority to speak about climate change concerns. Research on relational authority shows that in the absence of traditional sources of authority, such as hierarchy or professional status, authority resides in networks of relationships (Bourgoin et al., 2020; Taylor and van Every, 2014) that may be built through managing emotions (Mukherjee and Thomas, 2023) or performing menial tasks (Huising, 2015). In the relational view, authority is conceived of as a process of interactions that shape a situation in such a way that it orients collective action (Bourgoin et al., 2020). We argue that in the context of shareholder engagement, shareholders—and their intermediaries—need to constitute their relational authority regarding ESG concerns in and through the communication process of shareholder engagement. To unpack this idea, we turn to the communication perspective that regards communication as constitutive of organisation.

Establishing authority in shareholder engagement through communication

The CCO perspective is grounded in the ontological notion that communication serves to establish, compose, design, and sustain organisations (Ashcraft et al., 2009; Cooren et al., 2011: 1150). As an approach, CCO studies the co-constructed nature of communicational events (Cooren et al., 2011; Schoeneborn et al., 2019). Communication is more than a form of action (Austin, 1975; Searle, 1969): it ‘allows organisations to exist and do things’ as ‘it is constitutive of their mode of existence and action’ (Cooren, 2020: 177). The Montréal School of the CCO perspective uses the metaphor of ‘ventriloquism’ to draw attention to the ways in which (non)human actants can make other beings say or do things, similar to a ventriloquist and their dummy (Cooren, 2012). Ventriloquism also notes the sociomateriality in communication, as it is not just the human actant who engages in dialogue but also the figures on behalf of which they claim to speak (Cooren, 2020: 183). These figures can be other-than-human objects (e.g. principles, policies, nature) that materialise through ventriloquism (Cooren, 2020).

The CCO perspective has previously been applied to study the communicative practices through which ‘social actors explore, construct, negotiate, and modify what it means to be a socially responsible organisation’ (Christensen and Cheney, 2011: 491). Cooren (2020) argues that both corporate representatives and external stakeholders can ventriloquise corporate responsibilities. Various groups of stakeholders may speak on behalf of other (human) beings by acting as a ventriloquist making a puppet or ‘figure’ speak. By mobilising figures in communication, the agency of the speaker becomes decentred (Cooren, 2004), as it is the figures that dictate something to the stakeholders involved in the communication, in a way that a ‘no smoking’ sign can be invoked to forbid smoking. Ventriloquial analysis pays close attention to the way stakeholders may be positioned or position themselves as the intermediaries through which other figures speak (Cooren, 2012), which makes it well suited to study shareholder engagement, in which many actors may be positioned or position themselves to dictate action related to environmental and social concerns.

The decentred, relational view of communication underlying CCO and ventriloquism also has implications for the study of authority. Drawing on the common root for ‘authority’ and ‘authoring’, the communicative constitution of authority involves negotiating competing claims regarding the positive outcomes of proposed actions (Porter et al., 2018). In this process, the ability to invoke figures considered relevant by others is an important source of authority (Christensen and Christensen, 2022). In the absence of formal authority, relational authority is performed when a ‘matter of concern’—a figure that expresses what drives someone to ventriloquise a position, action, or objective—is transformed into a ‘matter of authority’, that is, a matter that can legitimise a specific course of action to the detriment of others (Bourgoin et al., 2020; Vásquez et al., 2018: 419). Such transformation requires matters of concern to be voiced in communication or written text and subsequently to become recognised as legitimately dictating a particular course of action (Vásquez et al., 2018).

In other words, there are things that matter to people, which are animated in communication, thereby being made present (Benoit-Barné and Fox, 2022). These matters, once expressed, can attain a ‘life of their own’ (Bencherki et al., 2021: 612), dictating relatively independently from the speaker what needs to be done. Using a ventriloquism perspective can enrich the study of relational authority by unpacking how various figures are mobilised to mediate matters of concern, either individually (e.g. a particular regulation) or collectively (e.g. the natural environment or financial markets), attaining relative autonomy to author a specific course of action. Therefore, we ask the following question: How is relational authority constituted in shareholder engagement on climate change concerns?

Methods and data

To address this question, we examine communication in a three-year engagement project carried out by a European engagement consultant (hereafter ‘the engager’) on behalf of five European institutional investors and one country-wide association for responsible investment. At the time of data collection, the organisation for which the engager worked represented clients totalling €1500b in assets under management. The engagement targeted 20 corporations in the utility sector, which were selected based on their portfolio share and greenhouse gas (GHG) emission levels, in particular their level of carbon emissions from energy generation. The corporations were located in Europe, North America, and Asia. The engagement project, which was carried out from September 2015 to June 2018, posed four demands, namely, that the corporation would: (a) commit to reducing its own GHG emissions; (b) compile and externally verify GHG emission inventories; (c) set GHG reduction targets and adopt relevant action plans; and (d) document and quantify climate change risks and have an appropriate mitigation strategy. These demands formed the basis for key performance indicators that the corporations were regularly assessed on by an external rating organisation. The engager had not previously been in contact with corporate representatives, and this shareholder engagement project therefore provides an ideal opportunity for studying the constitution of relational authority.

The engager initiated the interaction by sending a standardised letter to the head of the investor relations department at each of the 20 corporations. In it, the engager informed the corporation about the project and extended an invitation to participate in a first conference call. The letter also included a report that benchmarked the 20 corporations on carbon reduction plans and practices. Every six months, a new report with an updated benchmark was sent to all the companies, whether they chose to join the dialogue or not, together with a new invitation to discuss climate change issues with the engager. The engager managed to establish a dialogue with 13 corporations (65% of the target group, a percentage that is similar to other studies of shareholder engagement, e.g. Dimson et al., 2015).

As part of a wider research project, we were granted access to all the documents and communications logged by the engager. The data comprise the email exchanges and notes from conference calls, and biannual reports in which the progress of the engagement is described. To contextualise the data, we conducted several follow-up interviews with the engager. We also conducted interviews with a selection of investors and corporate representatives. Table A (online Appendix) describes our data sources further.

We followed the recommendations on ventriloquial analysis to move from the raw data in a stepwise manner (Nathues and van Vuuren, 2022; Nathues et al., 2021). Initially, we focused on identifying the commonly invoked figures (who or what is being made to do or say something) and vents (who or what makes someone or something do or say something) (Nathues et al., 2021: 1461–1462), paying attention to both explicit and implicit invocations. This step involved numerous discussions amongst the authors related to the interpretation of sections of raw data to identify frequently invoked figures, such as ‘institutional investors’ and ‘government regulation’. We also discussed the way in which these animated, or were animated, to ‘defend or evaluate a position, account for or disalign from an action, or justify or oppose an objective’ (Cooren et al., 2015: 369), that is, the main matters of concern that seemed to prompt the invocation.

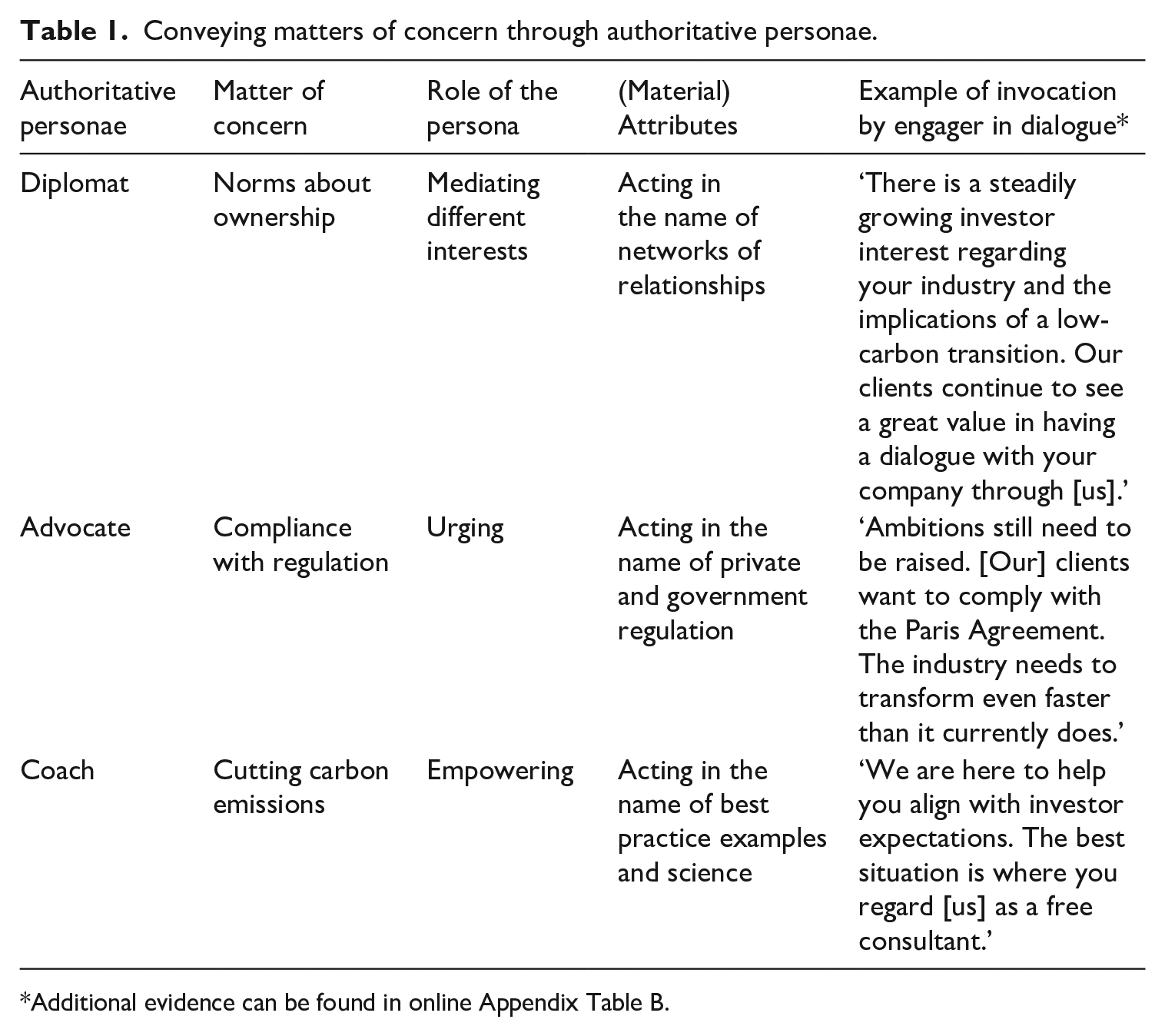

In the next step, we started clustering seemingly related figures and matters of concern while also paying attention to attributes (e.g. reports and standards) that these coincided with. In this clustering exercise, we paid particular attention to the way the most frequently invoked matters of concern prescribed specific courses of action, first within and then across multiple instances of communication. Owing to the longitudinal and scripted nature of the communication in our study, we were able to cluster repeated invocations of matters of concern into three authoritative personae—that of diplomat, advocate, and coach. Akin to the staging of characters in a play, each of these personae draws on different material attributes to play a distinct role in communication. Each authoritative persona is animated by, or animates, a distinct matter of concern, which prescribes a specific course of action. The diplomat is animated by norms of ownership, which compel him or her to request energy corporations to provide accountability to investors, drawing on networks of relationships to enable the opening of a dialogue. The advocate urges corporations to comply with the spirit of climate change regulation, ventriloquising institutional investors as concerned about alignment between corporate actions and ambitions in international agreements. Finally, the coach is animated by the desire to help corporations cut carbon emissions by drawing on his or her own expertise and best practices based on climate science. These personae are summarised in Table 1, and further evidence is presented in Table B of the online Appendix.

Conveying matters of concern through authoritative personae.

Additional evidence can be found in online Appendix Table B.

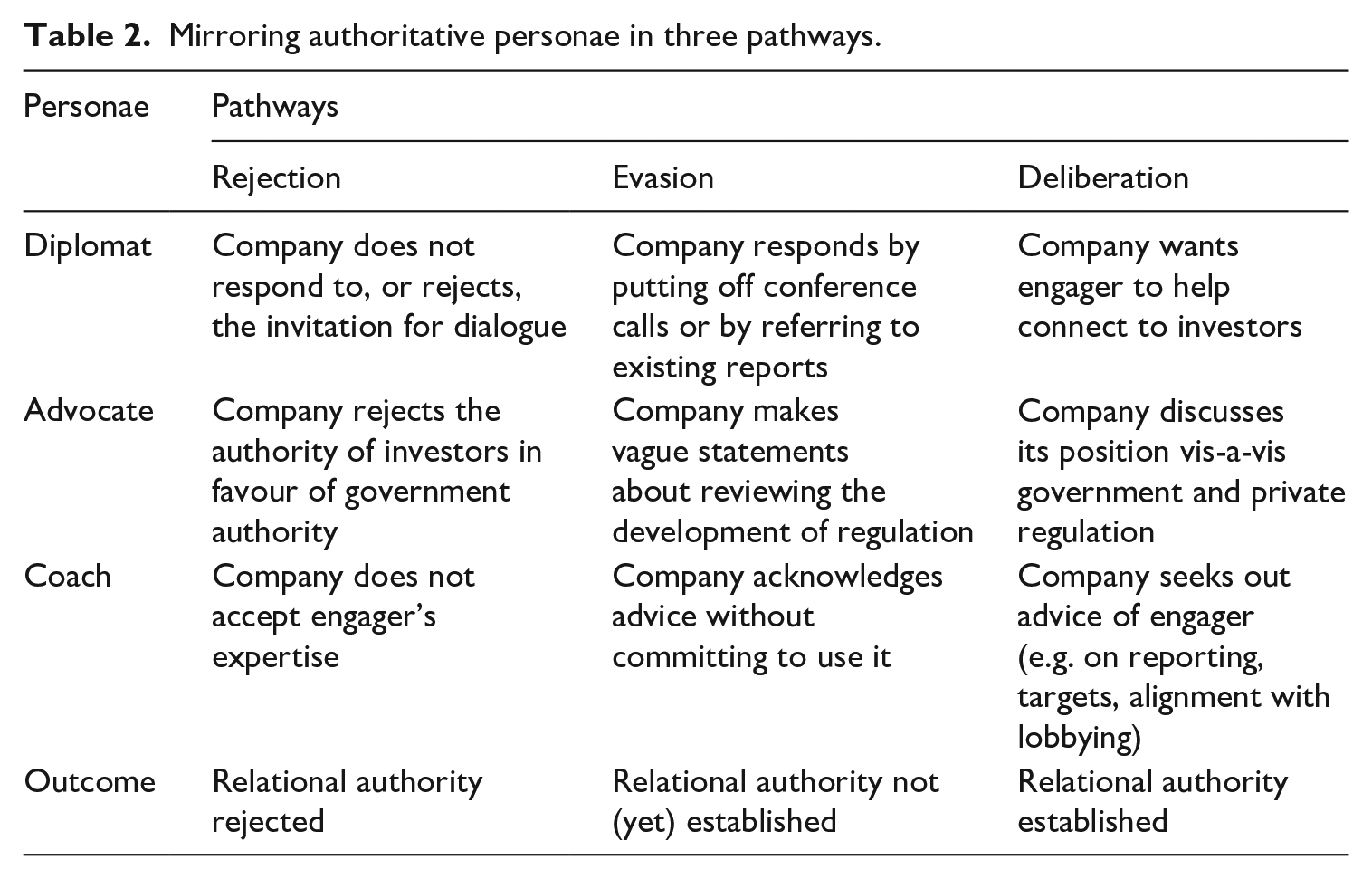

In the third step of our analysis, we turned our attention to the dynamics of interaction that occurred when an authoritative persona was ‘speaking’. To do so, we first traced the general pattern of invocation and response to the three authoritative personae within each case of dialogue, paying attention to both the frequency of invocation and types of responses. We also gave attention to the development of dialogue over time within each case, noting, for instance, patterns of repetition of requests, the introduction of a new request, or the uptake of an offer for advice. Through tracing chains of authorship and relations (Nathues and van Vuuren, 2022), we noticed two frequently occurring dynamics: that of mirroring, where the invocation of an authoritative personae was mimicked by copying its tone or echoing the matter of concern, and switching, where another authoritative persona was introduced in the response or follow up to the interaction.

Then, moving back and forth between the data and theory on relational authority (Bourgoin et al., 2020; Vásquez et al., 2018), we categorised interaction patterns across cases into three response pathways based on their degree of (explicit or implicit) acceptance of the matter of concern animating the authoritative persona and the movement (or lack thereof) that the response allowed towards a specific course of action, or matter of authority. Table 2 summarises the pathways that correspond to mirroring the three authoritative personae. We most frequently noted mirroring in company responses; and switching in engager communication. We summarise the patterns arising from the within-case coding in Table C in the online Appendix, which forms the basis of our theorising of mirroring and switching dynamics, as depicted in Figure 1 in the discussion section.

Mirroring authoritative personae in three pathways.

Switching and mirroring pathways.

In a final step, as recommended by Nathues et al. (2021), we returned to the data to select vignettes that were illustrative of our key insights. Based on our coding of the dialogue with each company (Table C online Appendix), we selected vignettes that clearly showed the invocation of the authoritative personae and supplemented these with additional data segments to show the various response pathways. The vignettes are therefore not presented in chronological order but were selected based on their illustrative power.

Constituting relational authority through three authoritative personae

In what follows, we present three authoritative personae that convey matters of concern regarding climate change in the dialogue between the engager and corporations: that of a diplomat, advocate, and coach. We outline the core matter of concern that the authoritative persona seeks to convey, the role the persona takes in the dialogue and the attributes that are at play. Furthermore, we show how different responses to authoritative personae (fail to) enable the communicative constitution of relational authority.

Diplomat

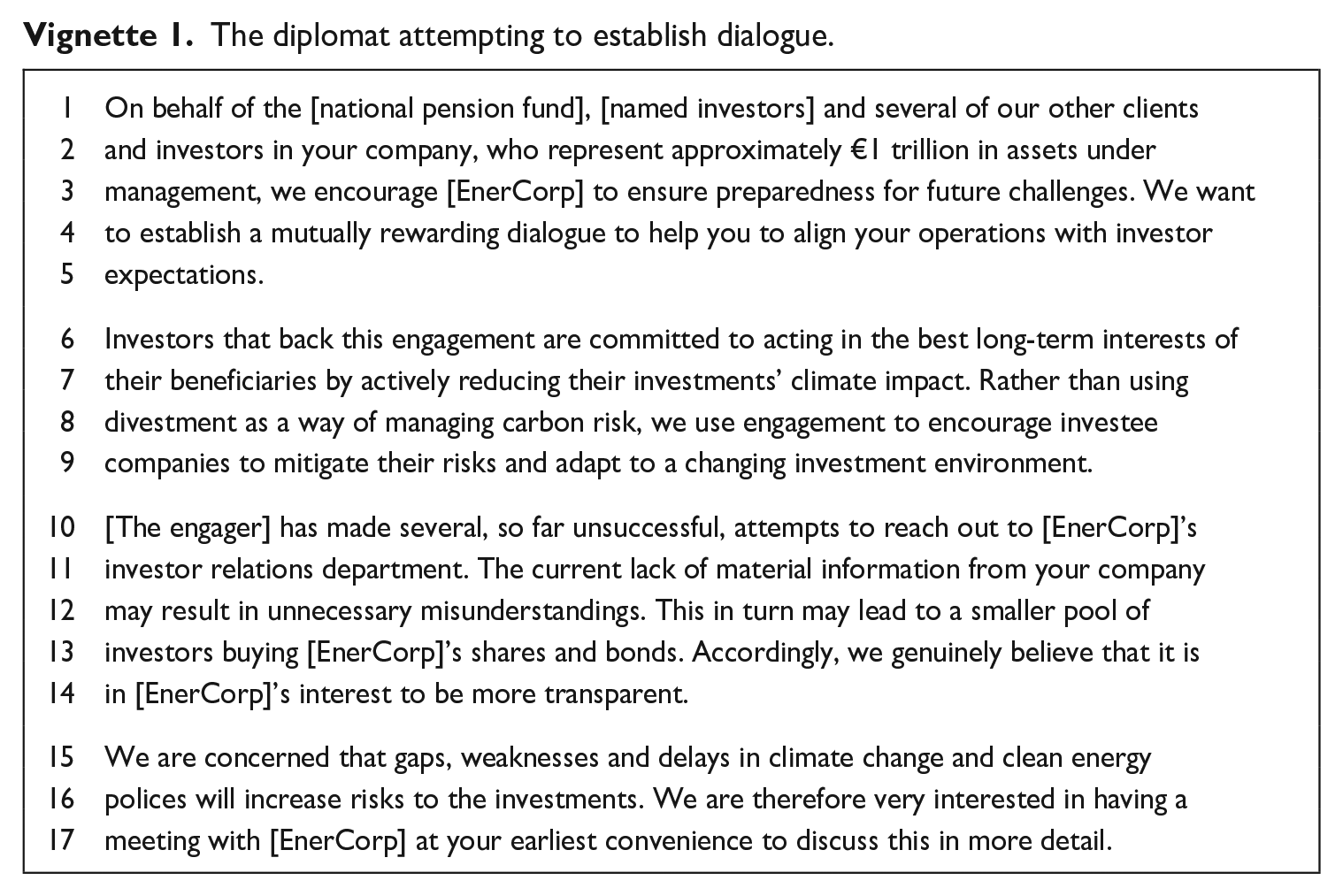

To convince the corporation that the engager has the authority to speak on behalf of a group of shareholders and to start the dialogue, the engager first tries to convey norms of ownership through the authoritative persona of the diplomat. In most instances, the engager is unknown to the corporate representatives. Furthermore, although in Anglo-Saxon contexts corporate representatives may be accustomed to shareholder questions regarding environmental concerns, owing to a long history of social shareholder activism (Goronova and Ryan, 2014; Vogel, 1978), in other countries this is not always customary. Vignette 1 shows a letter written to the chairman of the board of a corporation that did not respond to several requests for information.

The diplomat attempting to establish dialogue.

The diplomat is animated by norms of ownership: the idea that publicly owned corporations are accountable to their owners (i.e., shareholders) and need to ‘align’ their operations ‘with investor expectations’ (Lines 4–5). Positioning itself as representing large institutional investors (Lines 1–3), the diplomat ventriloquises them as having two options: reduce the carbon footprint of their investment funds by selling their shares in the corporation (Lines 7–8; 12–13) or expect large emitters, such as energy corporations, to reduce their carbon emissions. To lend authority to this message, the diplomat draws on the role of institutional investors as capital providers in the financial marketplace, referring to the size of their investments in the market (Lines 2–3) and the risk that investors face when corporations do not reduce emissions (Lines 15–16).

The appropriate response to the norms of ownership invoked by the diplomat is for companies to provide ‘material information’ (Lines 11–12). In the financial marketplace, ‘material information’ is generally understood as information that would probably have an impact on the price of a security or if reasonable investors would want to know the information before making an investment decision (CFA, 2014). The diplomat draws on norms of ownership to argue that information about corporate carbon emissions is material to investors. The diplomat is driven by a genuine belief (Line 13) that corporations that do not provide transparency on their operations breach the norms of ownership, which ‘may result in unnecessary misunderstandings’ (Lines 11–12).

The network of relationships that the diplomat draws on to establish authority extends beyond investors to their beneficiaries. The investors that the engager represents are ventriloquised as being concerned about ‘the long-term interests of their beneficiaries’ (Lines 6–7). The diplomat uses the interests of pension holders as beneficiaries to establish authority to speak on behalf of institutional investors. Implicitly, the invocation of the beneficiaries is also a means to point to the social benefits of a broader range of actors indirectly affected by corporate carbon emissions. The appropriate course of action for corporations is therefore to speak to the engager, who mediates the concerns of investors and their beneficiaries.

Despite the apparent breaching of norms of ownership when corporations do not respond to the requests for dialogue, the diplomat remains polite in character, drawing on the existing hierarchy of relationships in corporate governance, starting with the Investor Relations (IR) department: We try to be formal, do it ‘the right way.’ Because if you don’t get a good response from IR and you contact the ESG manager, it can backfire quite badly if IR feels circumvented. We represent investors, and our interface is through the IR. (Interview 2, Engager)

Writing to the chairman of the board presents a way of escalating the matter of concern further up the hierarchical chain of command within the corporation. In doing so, the diplomat also mediates different communication channels by offering the opportunity to use alternative communication modes, such as exchanging information by email rather than setting up ‘live’ conference calls in English or arranging a professional translator. In some instances, this literally means using ‘diplomatic channels’ to create first contact with the corporation. For example, in the case of a corporation that was contacted multiple times, the engager stated, ‘If there is still no response, which happens quite a lot, then you have to get creative’ (Interview 2, Engager): Yes, so I was ‘what can I do?’ So, I contacted the embassy and there was a really helpful woman there, being responsible for exports and so on, and they meet with companies regularly including this company, so she sent a formal letter [asking them to speak with us] – and that worked for a while, they actually responded, quite surprisingly. (Interview 2, Engager)

In addition to the nonresponse, which implies a rejection of norms of ownership, as evidenced in the vignette by the repeated but unsuccessful attempts to reach out (Lines 10–11), we find two further pathways of responding to the request for dialogue voiced by the diplomat in the name of investors. The first we label evasion. In this pathway, the polite tone of the diplomat is mirrored by corporate representatives, but it is used to avoid moving the matter of concern that animates the diplomat into a matter of authority. The polite language of the diplomat and the accompanying respect for functional hierarchy may mean that specific requests for action—to arrange a conference call or meeting to discuss carbon emission reduction strategies—receive noncommittal answers. For example, company representatives may simply respond by providing a link to their existing, publicly available environmental reporting, or promising to investigate the possibility of holding a conference call, without confirming a date: Thank you for your note, [first name lead contact engager]. I will check with my colleagues and coordinate some dates that we are available to have a phone dialogue with you. We appreciate the opportunity. In the meantime, I would like to forward some information that you might find helpful in advance of the call. . . . If you haven’t had a chance to do so, we encourage you to take a look at our corporate sustainability report. [weblinks attached]. (Email from the Investor Relations department of EnerCorp 2 in response to letter to chairman, March 2017)

Such an evasive response helps to constitute the diplomat, which is mirrored in tone and message (e.g. ‘We appreciate the opportunity’). The norms of ownership are not openly breached. At the same time, evasion means putting off the proposed action; in the example above, the representative never replied to the engager to set up a phone call. The evasion of the diplomat’s requests shows that relational authority may not (yet) be established.

It is only in the deliberation response pathway that we can see some evidence of relational authority being established. Deliberation occurs when the central matter of concern of the authoritative persona seems to be shared by the corporation, which provides the opportunity for further discussion on the appropriate course of action to be taken. When responding to the diplomat persona, corporate representatives may, for example, agree to discuss carbon emission reduction strategies during a conference call or meeting. At that moment, they confirm the position of the diplomat as conveying the expectations of investors. After repeated interactions, this position may also become proactively animated by company representatives, for example, when they ask the engager to facilitate meetings with other investors ‘to learn more about investor expectations from the company’ (EnerCorp 12, Conference call notes). More frequently, however, the diplomat’s role is limited to establishing the initial dialogue, after which the engager switches to one of the other authoritative personae.

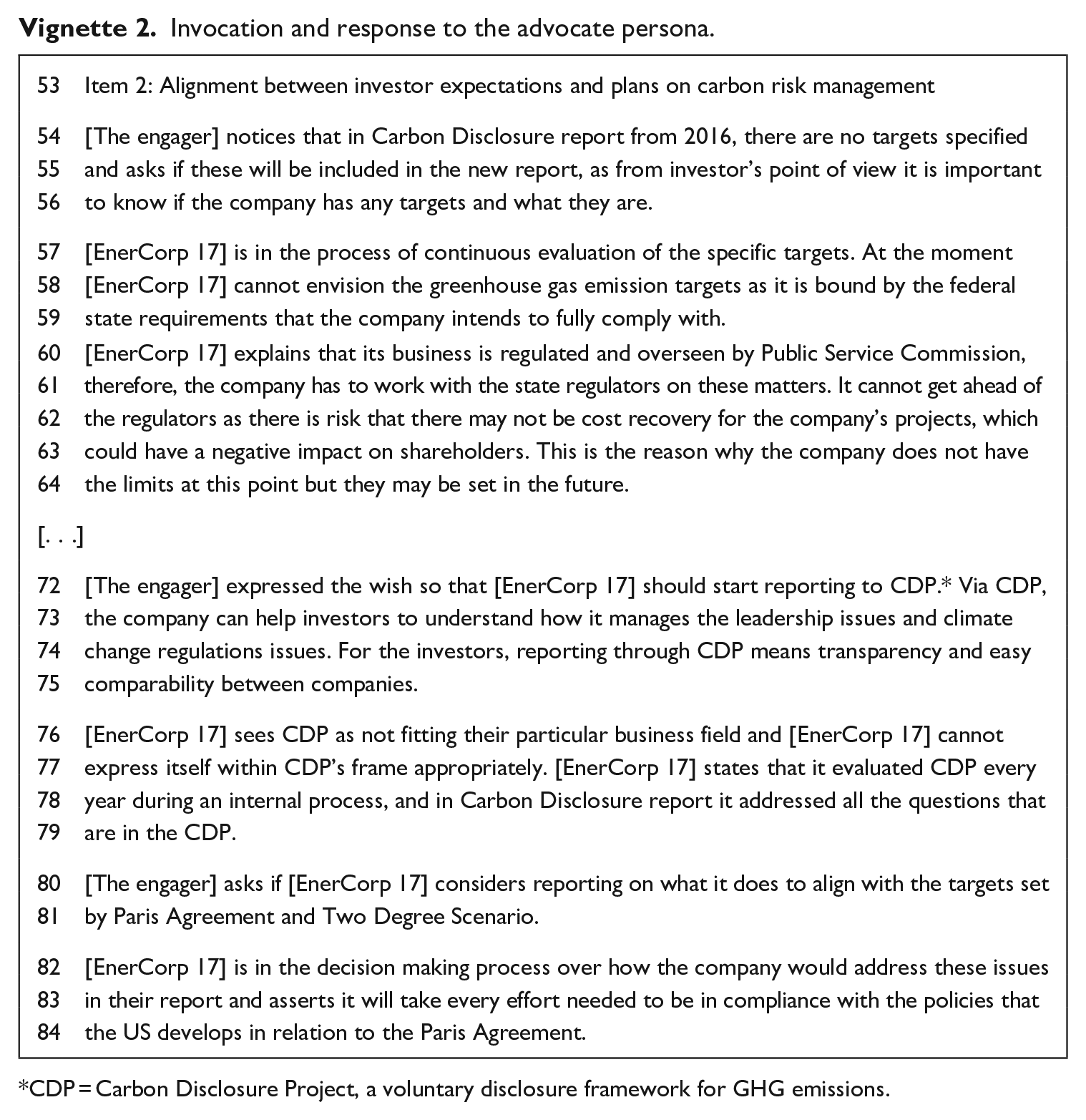

Advocate

The advocate persona is often invoked once corporate representatives have reacted to the engager’s request for dialogue and have provided information on their current practices regarding carbon emissions. Vignette 2 presents notes from a conference call written up by the engager and verified by EnerCorp 17, which takes place after the engager has escalated its request to speak to corporate representatives to the chairman of the board.

Invocation and response to the advocate persona.

CDP = Carbon Disclosure Project, a voluntary disclosure framework for GHG emissions.

The advocate is animated by the need for compliance with global climate regulations and has a more forceful character than that of the diplomat. When invoked by the engager, the advocate is urging corporations to accelerate their reduction of carbon emissions to live up to the ‘spirit’ of international agreements and standards, in particular the Paris Agreement ambition of limiting global warming to well below 2 degrees Celsius (Lines 80–81). Often, this means acknowledging the progress made by corporations while pushing for further actions: [We would say:] ‘These clients have said [that] the Paris Agreement is good and [they] want it implemented. These are the consequences for the power sector. We see that you are not going in that direction.’ [. . .] And then they come back and say ‘but look at us now, now we will invest 200% more in renewables. Are we not good?’ ‘Yes, it’s much better than before, but remember that our basic premise is the Paris agreement and the two-degree goal. Are you on your way there? Even with 200% more renewables it is still not . . .’ and then we will have to explain. (Interview 4, Engager)

Given the absence of mandatory standards on carbon emission disclosures, the advocate frequently draws on existing voluntary sustainability standards, such as the Carbon Disclosure Project (CDP), to encourage corporations to design and communicate about carbon emission policies (Line 72). The advocate persona animates its matter of concern by explicitly invoking institutional investors as wanting more consistency between disclosed company practices and the aim of global agreements for carbon reduction (Lines 72–75). This also entails calling for consistency between disclosure and practice by, for example, checking whether the corporation is a member of associations known for supporting lobbying efforts that seek to undermine climate change regulations, an issue that is particularly relevant for US corporations (see Table B online Appendix).

The advocate persona seeks to establish relational authority based on the authority of international agreements and voluntary private standards, ventriloquising institutional investors as being concerned about compliance with these regulations. In this vignette, there is little evidence of relational authority being established, as the response to the invocation of the advocate by company representatives is mixed. Initially, the discussion centres on the need for setting carbon reduction targets. Notably, in response to the question of whether the corporation intends to set and publicly disclose such targets, the energy corporation repeatedly invokes the figure of federal government regulation (e.g. Lines 58–59; 60–61), but this is invoked to reject the authority of the advocate persona, as getting ‘ahead of the regulators’ can have ‘a negative impact on shareholders’ (Lines 62–63). Here, a similar matter of concern (compliance with regulation) is used to reject the suggested course of action, as the corporation ‘cannot envision’ setting carbon emission targets (Lines 57–59). Subsequently, the suggested use of CDP disclosure standards to provide clarity on the corporation’s alignment with regulation (Lines 74–75) is rejected, as EnerCorp 17 cannot ‘express itself within CDP’s frame appropriately’ (Lines 76–77). In these instances, the representatives of the corporation seemingly mirror the matter of concern—compliance—but reject the suggested course of action, or matter of authority.

When the advocate pushes for clearer reporting regarding alignment with the Paris Agreement, the representatives of the corporation evade by mirroring the need for compliance with regulation by invoking US policies (Lines 83–84), while making no clear commitment to provide further reporting on this issue (Lines 82–83). In the evasion response to the advocate, there is no explicit rejection of the matter of concern but neither is there an explicit acceptance of the matter of authority, showing that relational authority is not (yet) established. A similar evasion can be seen in other cases of dialogue. For example, when the advocate is pushing corporations to align short-term investment plans into new energy generation with longer-term carbon reduction targets, EnerCorp 19 responds with a similar evasion technique:

How far head into the future does your current CAPEX plan extend? Q3: When do you expect carbon reduction targets and yet unplanned non-nuclear/non-fossil CAPEX to be approved by [EnerCorp 19]’s management? What is the time horizon for implementing the targets once they are in place? Answer: We have not made a concrete decision on the above matters yet. (Email from EnerCorp 19 in response to written questions from Engager, July 2016)

Although less frequently found in our data, the third response pathway of deliberation consists of discussing corporate compliance with the ‘spirit’ of government regulation and private standards or initiatives in the context of climate change. For the advocate personae this includes insisting on transparency regarding trade association memberships, implicitly urging corporations to avoid trade associations that promote agendas which are ‘unhelpful’ to climate change (Engager correspondence with EnerCorp 8). In several meetings EnerCorp 8 representatives discuss how they deal with trade associations in the US regulatory context that does not favour stringent climate regulations, but where transparency on trade association membership is expected. By discussing how to best comply with these expectations, the relational authority of the advocate is established. However, given the voluntary nature of private regulation such as CDP, we do not often find a deliberation response to the advocate persona. Instead, the engager may decide to switch to another authoritative persona animated by another matter of concern, such as that of the coach.

Coach

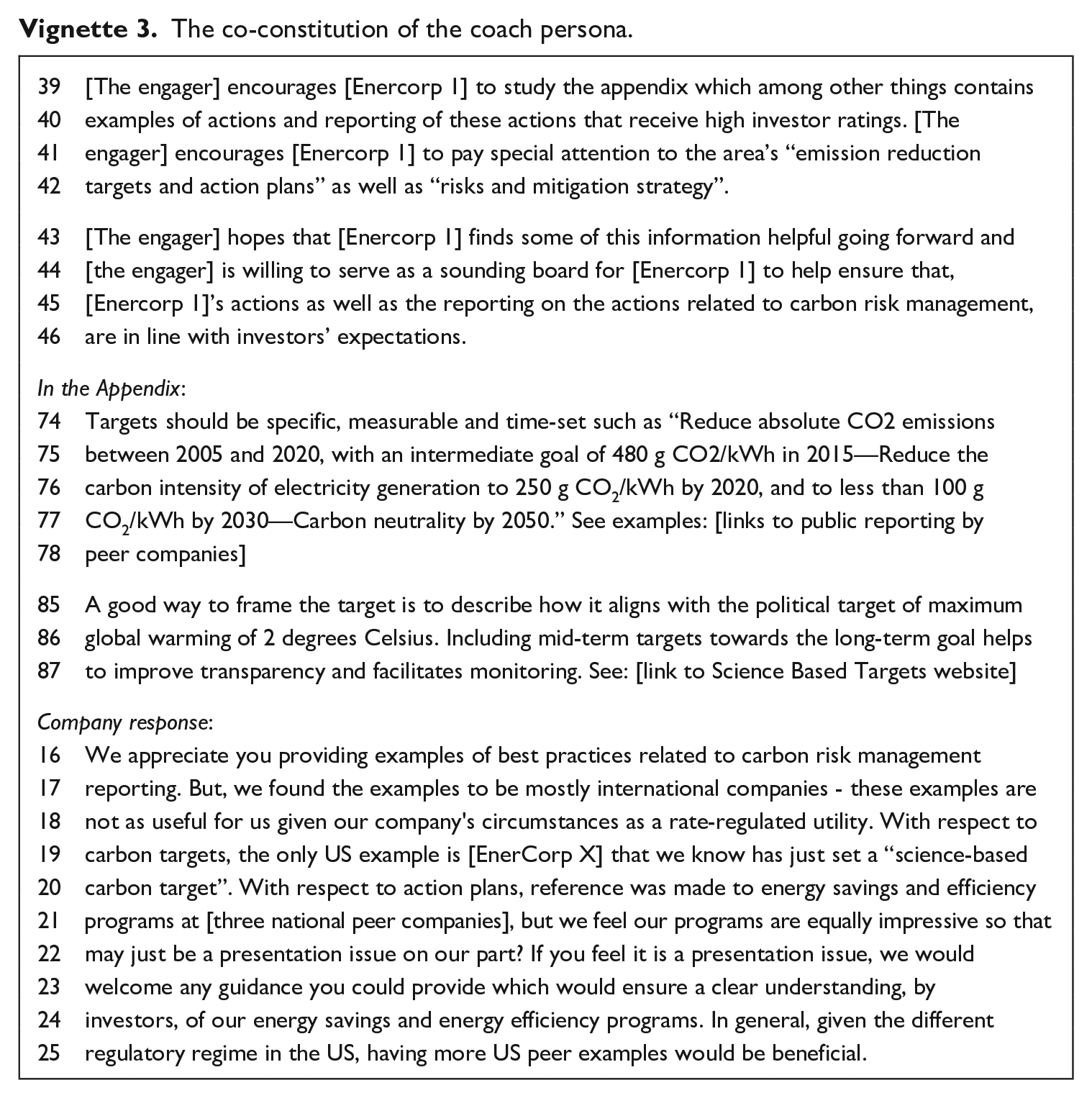

The third and last authoritative persona that the engager invokes is that of the coach. This persona is found in cases of repeated dialogues between the engager and corporate representatives. Vignette 3 is an excerpt of the dialogue with EnerCorp 1, which starts with notes from a conference call and the subsequent email response to the call.

The co-constitution of the coach persona.

The coach is animated by the desire to help corporations reduce carbon emissions. This matter of concern is presented not only to help ensure companies meet investors’ expectations of carbon emission reductions (Line 46), but also to help companies become more attractive for investors by invoking ‘higher investor ratings’ (Line 40) that could result from listening to advice provided by the coach. The tone of the coach is empowering; for example, the coach ‘encourages’ (Lines 39, 41) EnerCorp 1 to study the advice. The coach expresses willingness to ‘serve as a sounding board’ (Line 44) by offering practical and sometimes tactical tips to corporate actors: [Our approach is] ‘Okay, we will take you by the hand and show you where to go, and you will continue to get it here, but there is actually something that your investors would appreciate if you did, and they still want to be your investors. So, this is what you can quite concretely do.’ (Interview 3, Engager)

In providing guidance, the coach draws on examples of peer company practices, industry reports and other sources of information. These attributes are invoked as specific suggestions that will help improve company practices, for example, in Lines 75–77, where the coach spells out how carbon reduction targets should be formulated and provides references to the reporting of carbon reduction targets by a number of energy companies.

Reference is also made to science-based targets (Line 87). Science-based targets ‘show companies how much and how quickly businesses need to reduce their greenhouse gas emissions to prevent the worst impacts of climate change’ (SBTI, n.d.) by linking corporate emission reduction targets to long-term carbon reduction scenarios developed by climate scientists under the auspices of the Intergovernmental Panel on Climate Change (IPCC). 3 By setting science-based targets, corporations can ensure that their carbon reduction goals are aligned with the Paris Agreement and that their targets are ‘specific, measurable and time-set’ (Line 74). In invoking these recommendations, the coach also invokes the figure of science as a basis for his or her expertise. The coach uses expertise to build the relational authority needed to move the matter of concern it is animated by to a matter of authority. The coach’s expertise comes from the knowledge obtained through communicating with several of the largest companies in the industry and through being aware of the current recommended practices and guidelines, including those backed up by science.

In this vignette, the response to the coach is mixed: initially, the representative of the energy corporation is rejecting the expertise of the coach by questioning the relevance of the examples provided. In its response to the coach, the representative invokes the figure of federal government regulations (Lines 18; Lines 24–25) to argue that the guidance provided is not relevant for corporations that fall under US federal government rules and can therefore not be used as a basis to agree to further action. In doing so, she implicitly argues that the expertise of the coach is not relevant, and that the engager has not judged the corporation’s situation correctly. At the same time, the representative is asking advice on the best way to present the company’s current practices related to energy saving and energy efficiency to investors (Lines 21–24). In the request for advice, the representative of EnerCorp 1 is nevertheless limiting the relevance of the expertise of the coach to presentation issues only, being quite convinced that the substantive content of its programmes is ‘equally impressive’ (Line 21) to that of peer corporations referenced by the coach.

In the evasion response pathway, guidance offered by the coach is generally ignored. For example, the reports in which corporations are benchmarked against their peers, that are sent out by the engager every six months, provide an opportunity for the engager to switch to the coach persona: Attached you will find the second biannual report on [our engagement]. A segment is devoted to how we assess your company in terms of carbon risk management. [. . .] By engaging with your company and 19 other power companies we are able to report on emerging trends and we hope that you are interested in learning more on best practices within the industry. (Correspondence to all corporations, December 2016)

In response to these reports, corporate representatives may acknowledge the encouraging role of the coach persona, for example by extending thanks for the information, without committing to taking up the offer of guidance by the coach. For example, in several cases (see EnerCorp 3, 9, 10 in Table C in the online Appendix), corporate representatives decline the invitation extended by the coach to provide feedback and comments on their assessment. This shows that the engager has not yet established enough relational authority; although its expertise is not rejected, it is largely ignored.

In a deliberation response pathway to the coach persona, we see some evidence that relational authority has been established. Some corporate representatives ask for feedback on draft policy or disclosure documents to ‘road test’ whether the engager thinks these drafts will be acceptable to institutional investors. When representatives of energy corporations proactively reach out to the coach by asking for advice, they acknowledge the coach’s expertise. In doing so, they co-constitute the authority of the engager as a coach that can help them present their practices to investors. In responding to these requests, the coach in turn asks these corporate reports to be written so that they speak to investors: The target audience for the report in my view should be institutional investors. [. . .] If you take into account the potential societal costs (including equity destruction) from a business-as-usual scenario that is included in the two-degree narrative, institutional investors would not live up to their fiduciary duty by leaving this unaddressed. So, you have now returned the ball into the lap of the institutional investors who called for the report. And you have perhaps also woken up some of the investors who have not yet reflected on the matter. (Email from Engager to EnerCorp 8 in response to a request for feedback on a corporate environmental report)

Here, the coach sees the request for advice as an opportunity not only to provide feedback on appropriate ways to present information to investors but also to encourage corporate representatives to use their public reporting to ‘wake up’ investors and remind them of their duty to ensure the well-being of their beneficiaries (referred to as fiduciary duty). In doing so, the coach is asking the corporation to speak to investors about the matter of concern that is animating this persona, that is, reduction of carbon emissions. The coach is trying to animate the corporation as speaking to investors who are not yet addressing the costs of climate inaction by following the ‘business-as-usual’ scenario. As a result of this invocation, the mediation between investors and energy corporations as undertaken by the engager serves to co-constitute not only the appropriate course of action for corporations, but also for investors, as responsible investors who should be supportive of corporate programmes for carbon emissions reduction.

In sum, our analysis shows that the three authoritative personae are animated by distinct matters of concern and that each persona has a different role to play in the dialogue, drawing on or speaking in the name of different attributes to ventriloquise the concerns of institutional investors regarding carbon risk. Furthermore, we show that corporations mirror these authoritative personae, leading to three pathways, as summarised in Table 2. Corporate representatives may (implicitly or explicitly) reject the basis of authority that the persona draws on in communication, and by extension, reject the relational authority that the engager is trying to establish. They may also evade the invocation of the authoritative personae by mirroring the animated matter of concern yet not committing to move into the suggested course of action. Last, an acceptance of matters of concern provides evidence of the establishment of relational authority and may lead to deliberation on the exact course of action to be taken.

Discussion and conclusion

We started our study by asking how relational authority is constituted in shareholder engagement on climate change concerns. In the following section, we integrate our findings into a framework that addresses this question. We then outline the contributions of the framework to the literature and delineate some of its limitations and practical implications.

Constructing relational authority in shareholder engagement: A ventriloquial framework

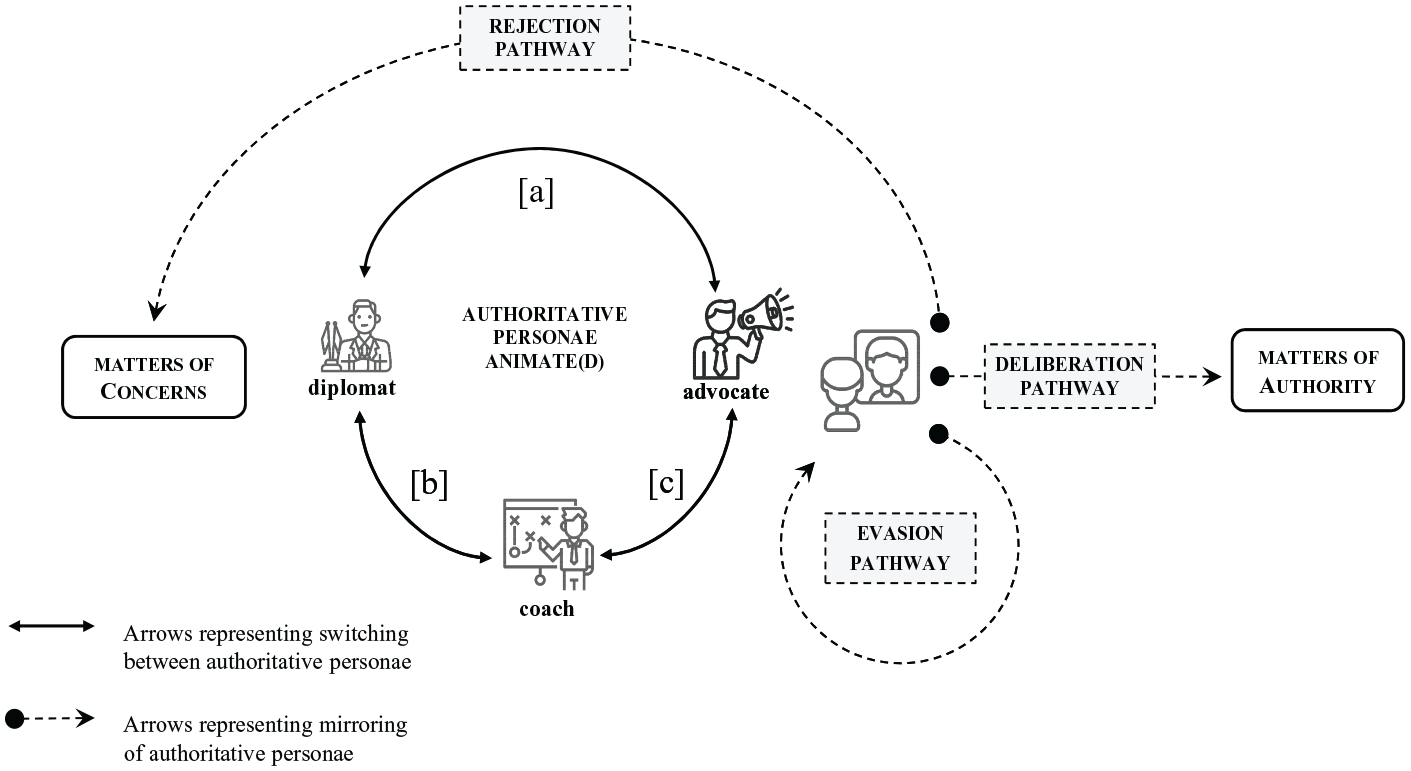

Our findings show how an intermediary ventriloquises the concerns of investors regarding carbon emissions through authoritative personae. Akin to characters in a play, these authoritative personae are driven by specific matters of concern, have individual characters, and invoke distinct attributes to make their case. As they are formed in a process of dialogue, personae may take on a life of their own, depending also on the reaction of the responding party. The constant oscillation between the ventriloquist and the personae used to convey matters of concern creates a dynamic process in which both can be seen as attempting to author what becomes the agreed course of action, the matter of authority. Figure 1 displays these dynamics, which derive from the switching from one persona to another and from the mirroring of authoritative personae in authoring matters of concern into matters of authority. Our framework is grounded in the dynamics of interactions within each case (Table C in the online Appendix summarises this analysis).

Switching between authoritative personae may occur between conversations as an implicit progression of the dialogue, much like a new character may enter the stage in Act 2 of a play. Although either party may switch to another authoritative persona at any time during the conversation, in our data the dominant pattern that emerges is that the engager will switch from the diplomat persona, used to open up the channel of communication, to the advocate or coach persona, to deliberate on substantive points of action (see also Table C, online Appendix). Switching by the engager also depends on the response of the corporation. A switch from the diplomat to the advocate may be triggered by a perceived lack of progress of the corporation (arrow [a] in Figure 1), whereas a switch to the coach may be triggered by an explicit request for guidance uttered by corporate representatives (arrow [b]). Frequently, switching takes place during a single conversation and may then constitute a deliberate attempt to evoke a different response. For example, when the advocate is urging compliance with specific standards, but it becomes clear that the corporation has little knowledge of these, the engager may switch to the coach to provide guidance (arrow [c]). In doing so, the engager also switches position in the chain of mediation: whereas the diplomat seeks to convey investor concerns regarding accountability to corporations, the coach is placed ‘on the side of the company’, seeking to help corporations convey matters of concern to investors.

The mirroring of authoritative personae in communication constitutes the relational authority needed to move matters of concern to matters of authority. Research shows that mimicry of body movements in an interaction are innately human and serve to foster rapport between interacting parties (Chartrand and van Baaren, 2009). Repetition of key words by the responding party in a verbal conversation may likewise foster positive feelings (van Baaren et al., 2003). In our setting, we see a frequent pattern of mirroring the matter of concern raised by the authoritative persona in the response of the corporation. 4 For example, when a corporation responds to the engager in the dialogue by asking for advice, it implicitly accepts the invocation of the coach persona by the engager, who subsequently can use this to legitimise a specific course of action, such as setting specific emission reduction targets (see Table C in the online Appendix). Our concept of mirroring reflects the idea that the responding party needs to ‘play along’ to establish the personae (Porter et al., 2018) and, in doing so, enables or constrains the constitution of relational authority. Specifically, mirroring of the matter of concern invoked by the authoritative persona may allow a movement towards the matter of authority as shown in the deliberation pathway in Figure 1.

Mirroring opens up the possibility of moving matters of concern to matters of authority, but notably, it can also constrain relational authority through two alternative pathways: evasion and rejection. In the evasion pathway, the matter of concern that animates the authoritative persona is mirrored, but no movement towards the matter of authority is made. For example, the formal tone and respect for hierarchy that is characteristic of the diplomat persona provides scope for evasive language from the responding corporation. This indicates that the prevailing norms of interaction between shareholders and companies, which require a polite conversation, may at the same time hinder the movement of matters of concern to matters of authority, as deeper deliberation is not established. As depicted in Figure 1, this in turn may lead the engager to switch to another authoritative persona invoking a different matter of concern (see online Table C).

In the rejection pathway, the invocation of a figure by an authoritative persona is mirrored by the responding party by copying that same figure yet rejecting its authority. In our setting, this frequently occurs when the advocate persona builds on the authority of government to argue for compliance with the spirit of international regulation aimed at reducing carbon emissions. In response, some companies invoke the same figure to argue that they are bound by national or state regulations that prevent them from setting more ambitious targets for carbon emission reductions through the use of renewable energy sources. In these instances, even though the authoritative persona is mirrored, the engager fails in authorising the legitimate course of action, and communication remains focused on determining agreement on matters of concern (see online Table C).

Although our analysis accounts for the role of communicative dynamics in explaining dominant response pathways, prior studies of engagement on environmental issues suggest that boundary conditions such as financial capacity (Slager et al., 2023) and pre-existing commitment to the reduction of GHG emissions (Durand et al., 2019), or the perceived salience of demands in the eyes of senior management (Bundy et al., 2013), may influence the chosen pathway. For example, a company that is already committed to GHG reductions may recognise the value of deliberation and sharing expertise more readily. Other conditions in the institutional environment may influence the dominant response pathway in more complex ways. For example, strong norms of shareholder ownership may make evasion less likely in Anglo-Saxon contexts, whilst different norms regarding the role of government in enforcing sustainability (Matten and Moon, 2008) may influence the likelihood of the rejection of the engager’s authority. Future studies could adopt configurational approaches (Furnari et al., 2021) to unpack how such boundary conditions interact with the communicative dynamics we identified.

Evaluating (and reconsidering) the potential of shareholder engagement

Our first contribution is to the body of research dedicated to shareholder engagement (Ferraro and Beunza, 2018; Goronova and Ryan, 2014). Most studies on the use of ‘voice’ by investors have studied its effectiveness in improving financial or ESG performance (e.g. Dimson et al., 2015, 2021) without studying the communication process underlying shareholder engagement in detail. In contrast to these studies, as well as studies grounded in Habermasian notions of communication (Ferraro and Beunza, 2018), we show that the establishment of relational authority to speak for, or on behalf of, investors is an important precursor to reaching common ground and moving towards a process of deliberation (Beccarini et al., 2023; Ferraro and Beunza, 2018). In addition, we focus on shareholder engagement undertaken by an intermediary—a context that naturally involves actors who speak on behalf of the organisations they represent. Institutional investors make frequent use of intermediaries in shareholder engagement, and our study provides further insight into the process by which relational authority is established in such a mediated context.

Moving beyond shareholder engagement as a subset of ESG practices to the broader debate about the value of sustainable finance, our framework has implications for a critical evaluation of ESG-focused communicative practices in the financial marketplace. Some argue that any attempt from financial markets under the ESG label, including addressing climate change, is ‘doomed to fail’ (Rhodes and Fleming, 2020) because financial actors are embedded in systems that prevent them from actually addressing such issues. Such views are predicated upon a classical take on communication as unilateral manipulation (Schneider, 2020; Slawinski et al., 2017), which overlooks the constitutive and relational character of communication. Our results confirm insights from previous research that shareholder engagement on ESG issues is notoriously difficult and often results in a lack of corporate change (Dimson et al., 2015, 2021). We find that corporations have multiple communicative opportunities to evade or reject suggested actions, or fail to respond.

However, by building on alternative assumptions from the CCO perspective regarding the constitutive nature of communication, we suggest that investors and their market intermediaries could still play a role in encouraging corporate discourse and actions on ESG concerns. The effectiveness of such communicative processes, however, depends strongly on their capacity to manage the communicative dynamics by invoking authoritative personae, mirroring and switching between them at the right time. This provides scope to develop and harness the competencies of engagers to manage these communicative mechanisms, to develop shareholder engagement as a lever in pushing corporations towards sustainability. This lever could be studied in combination with other engagement levers to clarify the conditions under which ESG engagement can be effective (Slager et al., 2023).

Overall, our study points to the communicatively constituted nature of investor capitalism (Useem, 1996) and revitalises the idea of using investor activism as a potential lever for corporate radical change (Alinsky, 1971). Future studies could further investigate how the communicative capacity of financial intermediaries is constituted and enhanced into ‘critical capacity’ (Boltanski and Thévenot, 1999) and used to nudge the integration of ESG issues into corporate practices and trigger endogenous systemic change.

Authoritative personae as meta-figures in CCO

Our analysis also contributes to CCO research by inducing the concept of authoritative persona. Similar to characters in a play, the authoritative personae we find in our context are motivated by different principles and values, such as respecting ownership norms in interorganisational communication, compliance with the ‘spirit’ of international regulatory frameworks regarding climate change and enhancing corporate understanding of carbon reduction practices. The scripted and repeated nature of the dialogue we study in the context of shareholder engagement enables us to trace clusters of these matters of concern that are animated by, or animate, different vents. Authoritative personae can therefore be seen as ‘meta-figures’: a collection of figures and associated attributes that are repeatedly invoked to animate matters of concern. In doing so, authoritative personae enable the presentification (Benoit-Barne and Cooren, 2009) of distinct sources of authority in interaction. In other words, authoritative personae make present the central matter of concern that grounds them, in an attempt to define the ‘right’ kind of organisational practices. Like moving from observing a single act to a full play, the concept of authoritative personae allows us to trace the invocation of singular figures into fully rounded personae that become ‘full-fledged participants’ (Cooren et al., 2013: 264) in communication.

The concept of authoritative personae can be used to bridge micro-interactional analysis, which forms the core strength of CCO, with communicative approaches that have paid greater attention to the narratives (Czarniawska, 1997) that exist at a more macro level, particularly in relation to sustainability and climate change (Wright et al., 2012). For example, in our study, we see that the engager tries to position the ‘two-degree narrative’ as the overarching matter of authority that should inform the actions of responsible investors and corporations. The two-degree narrative, which refers to the target to limit the rise in global temperature to (well below) 2 degrees, originated in 1970s climate modelling (Randalls, 2010) and was enshrined in the Paris Agreement in 2015. As a narrative, it draws on several sources of authority, including science and global regulation, to set a broadly defined goal.

As the effects of global climate change become more apparent and frequent, as seen in extreme weather events worldwide, climate change narratives are likely to become more frequently ventriloquised in organisational communication. Our framework provides a way to study how such narratives may be drawn upon to author what constitutes a responsible investor or corporation. The concept of authoritative personae enables a ventriloquial analysis that pays specific attention to the distinct sources of authority that are made present to guide the interaction (Benoit-Barné and Fox, 2022; Taylor and van Every, 2014). Such an analysis highlights, for example, that the presencing of some sources of authority may be more successful in authoring change outcomes than others (Porter et al., 2018).

Constituting relational authority communicatively

Our third and final contribution is to the study of relational authority, which builds on the CCO perspective to argue that authority is not granted to a person through hierarchy or professional expertise but communicated into being (Taylor and van Every, 2014). Whereas previous studies have focused on the work practices of individuals as they try to build relational authority (Huising, 2015; Mukherjee and Thomas, 2023), our study examines the communicative constitution of relational authority by examining how matters of concern move towards matters of authority (Vásquez et al., 2018) in communication between external actors and corporate representatives. We find that mirroring can seemingly accept the matter of concern made present by the invocation of an authoritative persona, yet still be used to reject the associated matter of authority. Equally, the switching of authoritative personae shows relational authority not only has to result from purposive action (Bourgoin et al., 2020) but can also result from trying, sometimes succeeding and other times failing, to ‘strike the right tone’ in interaction.

Our framework can be used to evaluate the attempts of external actors to co-author what an organisation is or should do. Specifically, we can trace the extent to which the dynamic invocation of authoritative personae resonates with the corporation’s authoritative text, which represents what the corporation stands for (Kuhn, 2008). Such resonance may lead to deliberation of matters of authority and a process of co-authoring specific actions, whereas conflicting invocations may induce a dynamic cycle of switching and mirroring. As such, our framework also speaks to the dual notion of authority as emergent as well as enduring (Benoit-Barné and Fox, 2022): emergent in a single communicative act, but enduring in its consistent use across multiple organisational communication settings.

The communicative dynamics we observe in our setting are played out through multiple ‘links’ in the long chain of actors involved in the field of sustainable finance. Our insights may form a basis for studying the relational authority of other actors, such as security analysts (Leins, 2020) and investment managers (Arjaliès and Bansal, 2018), in sustainable finance. For instance, institutional investors frequently invoke their fiduciary duty to represent beneficiaries’ interests (i.e., pension holders) to argue for or against sustainable finance strategies such as divestment from fossil fuel companies (Ayling and Gunningham, 2017), a context ripe for analysis of the communicative constitution of relational authority. More broadly, various groups of actors working together on the grand challenges facing society, including climate change (George et al., 2016), mainly rely on relational authority to coordinate their efforts. Further attention to mirroring and switching may provide a better understanding of how communication constitutes this interorganisational space and its dominant modes of governance (Aragon-Correa et al., 2020) and authority (Porter et al., 2018).

Limitations and perspectives for future research

Our unique access to the dialogue between one engager and multiple corporations provided us with an ideal case through which to capture the communicative constitution of relational authority, but also presents limitations. A first limitation relates to our reliance on pre-existing rather than in vivo data sources. Even though we clarified in follow-up interviews with the engager that our confidential dataset reflected actual practices, direct observation of engagement discussions could help deepen the analysis of the role played by the three personae as well as the dynamics of switching and mirroring. Future studies could rely on our framework (Figure 1) as a starting point to explore how other engagers, operating as market intermediaries or for their own account (e.g. asset managers), build their authority dynamically by ventriloquising.

Furthermore, our research design, which focuses on the dialogue between the engager and corporate representatives, does not capture the internal dialogue between corporate representatives. Building on the Actor-Network Theory assumptions that inform CCO research (Gond et al., 2016), future work could adopt research designs that enable more symmetry in the perspectives of the various actors involved in communicative processes.

A third limitation relates to the location of our focal intermediary in the financial markets of the EU, where shareholder engagement is relatively salient. Our case confirms the insight that engagers may struggle to elicit responses from corporate managers operating in other, and culturally more distant, varieties of capitalism (Dimson et al., 2021; Slager et al., 2023). Future studies could focus on these cultural and institutional dimensions when investigating the communicative constitution of authority through shareholder engagement.

Practical implications

The ventriloqual framework moves beyond reiterating the value of communication for effective shareholder engagement (Gond et al., 2018) by making explicit the communication processes that form the bedrock of day-to-day engagement practices. Our framework can be used to explicitly analyse when and why one of the three response pathways identified occurs in specific processes of engagement. Although practitioners may do this intuitively in the practice of shareholder engagement, our framework provides a tool to analyse more systematically which figures help them gain authority. It invites engagement practitioners and shareholder activists to pay more explicit attention to the intended and unintended consequences of ventriloquising figures such as global agreements, and to reflect critically about the political legitimacy of their own position regarding financial risk or broader societal concerns. It also implies practitioners should give more attention to the building of relational authority in and through engagement, depending on their location in the ESG chain of investment. Our findings show that the constitution of relational authority is difficult, owing in part to the mediated nature of shareholder engagement. This implies that investors should reflect on the outsourcing of engagement to intermediaries, and what that says (literally) about their genuine interest in ESG.

By clarifying the communicatively constituted nature of investor capitalism, this study also suggests that policymakers and activists should not assume that ESG-related communicative practices are always forms of greenwashing. Rather, our results suggest that we should enhance the communicative and critical competencies of actors using these practices so that they can deliver their transformative potential on the corporate side. Within the shortening window for climate action, harnessing financial capitalism's communicative channels remains a useful, although not the only, lever to focus corporate attention on this grand challenge.

Supplemental Material

sj-pdf-1-hum-10.1177_00187267231174700 – Supplemental material for Mirroring and switching authoritative personae: A ventriloquial analysis of shareholder engagement on carbon emissions

Supplemental material, sj-pdf-1-hum-10.1177_00187267231174700 for Mirroring and switching authoritative personae: A ventriloquial analysis of shareholder engagement on carbon emissions by Rieneke Slager, Jean-Pascal Gond and Emma Sjöström in Human Relations

Footnotes

Acknowledgements

The authors thank all interview participants for taking the time to share their insights. In particular, we would like to thank the engager for providing access to the data in the context of this project. We thank our editor and our team of reviewers for their editorial guidance and excellent comments on our article. A previous version of this manuscript was presented at the Principles for Responsible Investment (PRI) Academic Conference 2019; we thank discussants Fabrizio Ferraro and Tom Barron for their valuable insights. We have further greatly benefited from discussions with participants at the following events: ETHOS seminar at Bayes Business School, February 2022 and European Group for Organization Studies (EGOS) in July 2022. We take full responsibility for any errors in this study.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article. This research has received funding from Sweden’s Innovation Agency, and Mistra, The Swedish Foundation for Strategic Environmental Research.

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.