Abstract

In board governance literature and practice, the presence of outside directors is presumed to have a beneficial effect on board effectiveness and firm performance. This study challenges this prevailing view by exploring the boundary conditions and intermediate mechanism preventing the potential benefits of outside directors. Our results reveal that reality is more complex than previously assumed. Using unique data from a sample of 561 Belgian small and medium-sized enterprises, we find that the presence of outside directors has a neutral or even negative effect under certain boundary conditions on board service engagement in the small and medium-sized enterprises context. Family ownership control and infrequent board meetings are two important contingencies that reduce management’s propensity to disclose firm-specific information to the board in the presence of outside directors. The disclosure of such information, in turn, serves as a critical mechanism to offset firm-specific information asymmetry, associated with better board service engagement and (indirectly) enhanced firm performance. Based on our study, we articulate new theoretical insights for understanding board governance in small and medium-sized enterprises, which integrate existing board governance theories with the dominant coalition context, serving as a springboard for future board governance research.

Keywords

Introduction

Small and medium-sized enterprises (SMEs) are widely recognized as key to the competitiveness of many of the world’s top economies, including those in the European Union (EU) (Skuras et al., 2008). 1 However, we know much less about board governance in SMEs than in publicly-held firms, making them a particularly important target for research (Kumar and Zattoni, 2019). Furthermore, while studies on the board’s monitoring role dominate much of the board governance literature, other researchers (Daily et al., 2003; Forbes and Milliken, 1999; Lorsch and MacIver, 1989; Westphal, 1999) highlight the importance of the board’s service role, that is, the advice and counsel the board provides to the firm. In the SME context, empirical research indicates that a board’s service role may be more important than monitoring to create firm value and enhance performance (Judge and Zeithaml, 1992; Lohe and Calabrò, 2017; Stiles, 2001; Zattoni et al., 2015). As our research context consists of a population of family and nonfamily-controlled SMEs, we focus on board service engagement, namely the extent to which the board advises and counsels the CEO and other top managers in strategy formulation and other high-level matters.

Our core research question ‘Are outside directors in the SME board beneficial (or not)?’ centers on the impact that the presence of outside directors may have on board service engagement. The prevailing view in board governance literature and practice is that the presence of outside directors is beneficial to board and firm performance. Such advocacy is grounded in agency theory arguments contending that independent or outside directors can better protect owner interests, countering the possible self-interests of management (Eisenhardt, 1989; Fama and Jensen, 1983; Rindova, 1999). According to both resource dependence theory (RDT) and the resource-based view (RBV), outside directors enhance a board’s service role by bringing new knowledge and an independent and objective view to the board (Bammens et al., 2011; Barney, 1991; Hillman and Dalziel, 2003). Moreover, the inclusion of outside directors is a board composition variable that is widely recommended in governance codes for both listed and unlisted firms, 2 and strongly advocated by many business consultants and board governance experts worldwide (Collard, 2013; Evans and Kipp, 2014; PwC, 2016). Taken together, this has led to the prevailing assumption that the presence of outside directors is beneficial to board effectiveness and firm performance.

However, prior governance research in the SME context has overlooked the underlying mechanisms accounting for the effect of the presence of outside directors and its boundary conditions. In search of a better understanding of such effect, tracing back to at least Pettigrew (1992), many scholars have argued for the need to identify board process variables that may mediate the relationship between board composition so-called ‘input’ variables and board and firm output variables (e.g. Bammens et al., 2011; Boivie et al., 2016; Charas and Perelli, 2013; Corley, 2005; Cornforth, 2001; Desender et al., 2013; Forbes and Milliken, 1999; Francoeur et al., 2018; Huse, 2005; Kumar and Zattoni, 2019; Pettigrew, 1992; Roberts et al., 2005; Van Ees et al., 2009; Zattoni et al., 2015; Zona and Zattoni, 2007). Such approaches have been variously called board dynamics (Forbes and Milliken, 1999), board information processing (Boivie et al., 2016), and cognitive approaches (Rindova, 1999). As an extension of these approaches, which primarily consider intra-board group processes, our study focuses on firm-specific information disclosure from management to the board, henceforth referred to as information disclosure, an ‘inter-board process’ mechanism. We examine whether the presence of outside directors indirectly enhances (or hampers) the board’s service engagement by way of information disclosure in board-management relations, and to what boundary conditions this may apply.

Information disclosure is central to understanding board governance due to its potential to offset information asymmetry among board members, and especially between executive and outside (i.e. nonexecutive) directors (Forbes and Milliken, 1999; Nowak and McCabe, 2003; Roberts et al., 2005) 3 . In a variety of contexts (including top management teams), information asymmetry has been found to negatively affect team decision-making effectiveness (Edmondson et al., 2003). Information asymmetry is especially problematic when external or outside board members depend on management to keep them informed (Boivie et al., 2016). We presume that information disclosure is an important behavioral process mechanism to offset firm-specific information asymmetry, especially when outside directors are included in the board.

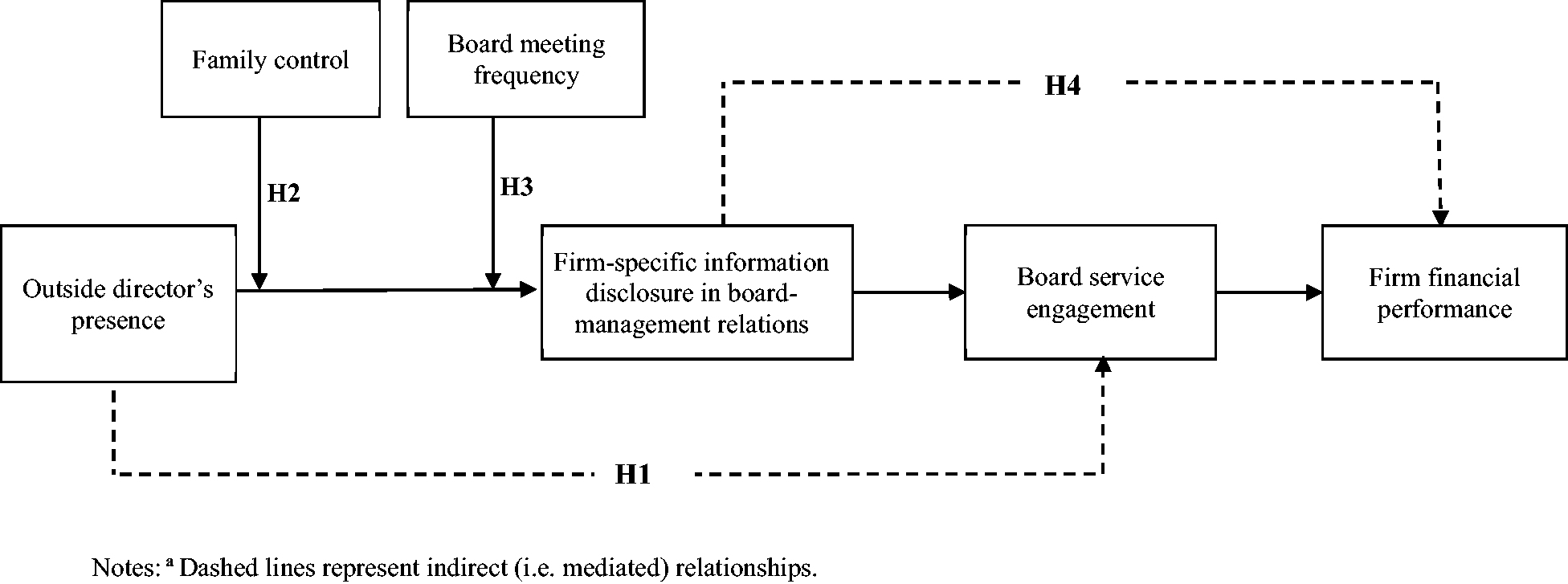

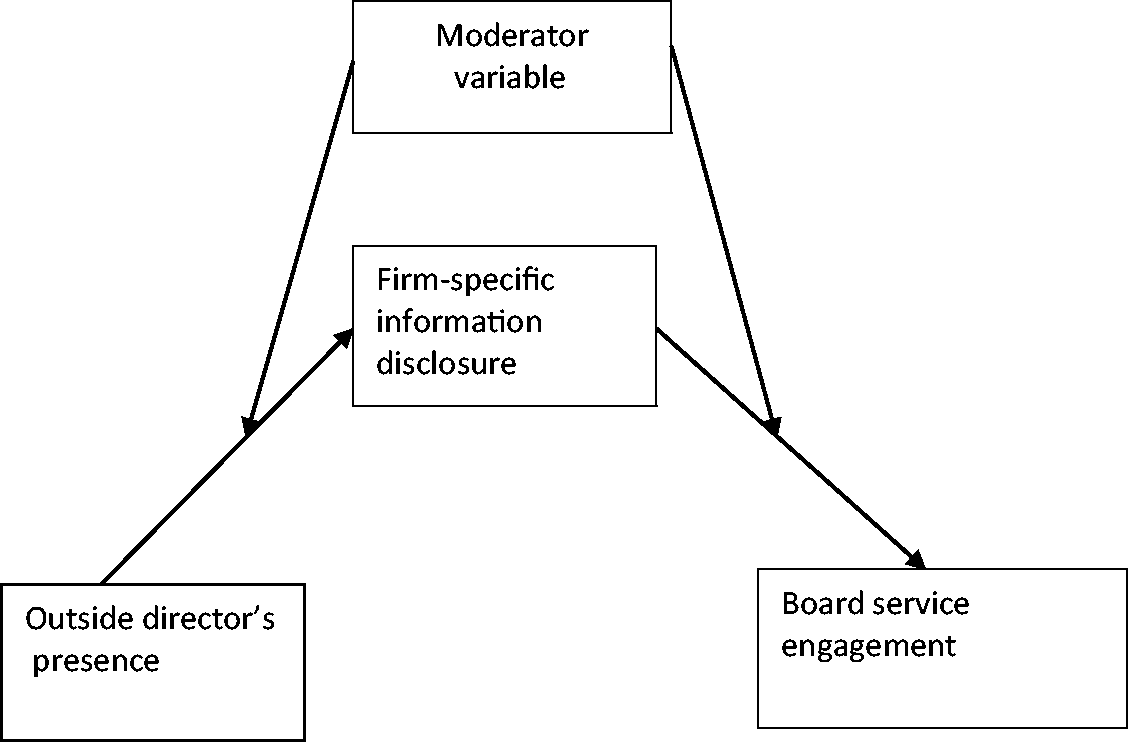

Figure 1 shows the overall theoretical model investigated in this research. The model departs from prevailing board process-based models by identifying information disclosure as a key mediating variable in the relationship between the presence of outside directors and board service engagement. It also proposes two boundary conditions or moderators for this mediating effect (i.e. a moderated mediation effect), representing common variations in the SME context, namely ownership (family vs. nonfamily) control and board meeting frequency. We interpret these variables as possible proxies for respectively the type of dominant coalition in the firm, that is, the group with the greatest influence or discretion over the firm’s goals and mission (Cyert and March, 1992; De Massis et al., 2008), and the dominant coalition’s willingness to make the board an active participant in firm decision-making (Pearce and Zahra, 1992). To further validate the role of information disclosure in board-management relations as a behavioral process mechanism, we test whether it is indirectly associated with (lagged) firm financial performance (mediated by board service engagement).

Theoretical model.a

To theorize and validate this new perspective, we tested our hypotheses combining two sources of data: questionnaire responses from 561 firms derived from a population of Belgian privately-held SMEs, and Bel-first, a Belgian source of longitudinal financial performance and board size data.

Theoretical background and hypotheses

Offsetting information asymmetry in the presence of outside directors

Board process-based approaches typically view the board’s core task as problem solving, and information acquisition as critical to effective decision-making (Boivie et al., 2016; Forbes and Milliken, 1999; Hinsz et al., 1997; Milliken and Vollrath, 1991; Rindova, 1999; Van Ees et al., 2009). However, while on the one hand, outside board members are thought to enhance the firm’s ability to make strategic decisions by providing an independent and objective view, this goal is difficult to realize in practice due to several individual, group, and firm barriers that hinder the board’s ability to obtain, process, and share firm-specific information (Boivie et al., 2016). One such barrier is CEO power and the related willingness of the CEO to share information with the board (Boivie et al., 2016). Paradoxically, while the board is officially responsible for overseeing the management’s activities, especially in the SME context, the board depends on the CEO to disclose information to oversee firm activities (Aguilera, 2005; Boivie et al., 2016; Demb and Neubauer, 1992). This paradox is accentuated when the board includes outsiders who, at the outset, typically have far less firm-specific information than management and less time to obtain access to such information (Roberts et al., 2005).

The problem of information disclosure is not limited to SMEs. In a survey of directors in listed firms, more than half the respondents ranked the risk of information non-disclosure as important (MacDougall et al., 2016). Nonetheless, listed firm directors may turn to alternative sources for firm-specific information, including financial analysts, the media, and investor reports (Healy and Palepu, 2001; Joh and Jung, 2018). However, given the lack of publicly available information on most SMEs, outside directors in such firms depend almost solely on management’s willingness to share firm-specific information, making information disclosure by the CEO to (outside) board members in such firms even more important to reduce information asymmetry. Thus, in the SME context, the CEO is an essential communication link between outside directors and the rest of the firm (Barratt and Korac‐Kakabadse, 2002).

Information disclosure as a mediator between outside directors’ presence and board service engagement in SMEs

Our first hypothesis posits that the presence of outside directors indirectly enhances board service engagement by encouraging information disclosure by the CEO to the board. Outside directors are often seen as a counterweight to internal management, compelling the latter to greater transparency on behalf of constituent stakeholders (e.g. minority shareholders), whether themselves or those they represent (Eisenhardt, 1989; Stiles and Taylor, 2001). Furthermore, according to the board dynamics perspective, the presence of outside directors may also stimulate greater board activity, as they might see the board’s tasks as separate from, and complementary to, the management’s tasks, enhancing effort norms that result in higher board service engagement (Forbes and Milliken, 1999; Mace, 1986; Zattoni et al., 2015; Zona and Zattoni, 2007). In addition, especially in a regime where the appointment of outside directors is voluntary, RDT suggests that their inclusion in the board may signal the firm’s need and willingness to accept different skills and knowledge from outside the organization (Hillman and Dalziel, 2003; Pearce and Zahra, 1992; Pfeffer and Salancik, 1978). Under such conditions, one might expect management to disclose information to enhance (outside) directors’ awareness and comprehension of firm-specific issues (Judge and Dobbins, 1995), and in turn, their ability to make informed decisions. The presence of outside directors may also stimulate inside directors to show that they have their house in order, thus putting more effort into board activities, which might include addressing the information needs of the board (Forbes and Milliken, 1999). Based on the literature, we could thus expect that the presence of outside directors is associated with greater information disclosure to enhance their decision-making.

In turn, offsetting information asymmetry through firm-specific information disclosure is key to ensuring that the potential of outside directors can be realized regarding board service engagement. Without sufficient disclosure of firm-specific information, the board may overlook plausible options, fail to examine the full consequences of each alternative, or underestimate risks, all of which may affect the quality of decision effectiveness and the ability to carry out its service role (Edmondson et al., 2003; Erakovic and Overall, 2010). The resulting information asymmetry thus hampers the board’s ability to fulfill its service role.

The need for firm-specific-information disclosure as a prerequisite of board service engagement has been partially addressed in past qualitative research. For example, Stiles (2001: 639) quotes the chairman of a board of directors, ‘There is a rule, which our board adheres to: there should be no surprises at the board meeting. The directors should be familiar with what comes before them and they should not be asked to decide upon a large issue without having knowledge of it well beforehand’. Roberts et al. (2005: S14) note that, ‘Without appropriate information, it is impossible for non-executives to develop a confidence that management are focused on the most appropriate indicators of business conduct and performance’. These quotes underscore the importance of information disclosure to enhance the board’s service role. Accordingly, we posit that the presence of outside directors can indirectly enhance board service engagement through firm-specific information disclosure by management to the board:

Moderated mediation relationships between outside directors’ presence and board service engagement

Prior board governance research, drawing on the RDT literature, tends to view the inclusion of outside directors in a positive light as a means of obtaining resources from the external environment, thereby protecting the firm from environmental diversity and gaining competitive advantage (Hillman and Dalziel, 2003; Pearce and Zahra, 1992; Pfeffer and Salancik, 1978). However, any stakeholder that holds resources vital to the firm’s operations also holds power over the company (Boxall and Purcell, 2016; Schuler and Jackson, 2007), a point that Pfeffer and Salancik (1978) recognized but was often overlooked in later interpretations of their work, especially in the board context (Garg and Eisenhardt, 2017). Garg and Eisenhardt (2017) address this gap, noting that while sharing information with outside directors can enhance the board’s ability to assist the organization in problem solving, it can also potentially shift the balance of power toward the board and away from the firm’s inside members (Garg and Eisenhardt, 2017; Wry et al., 2013). We consider this trade-off between external resource acquisition and the potential loss of power of the dominant coalition in developing hypotheses H2 and H3.

Family control as moderator

As a first variant of H1, we explore family control as a possible moderator. H2 posits a moderated mediation relationship such that family control negatively moderates the relationship between the presence of outside directors and the mediator, namely information disclosure. In family-controlled firms, the owning-family likely serves as the dominant coalition, especially when the family is the largest shareholder (De Massis et al., 2008). The family business literature argues that in family-controlled firms, family-centered noneconomic goals, including family dynasty continuity and retaining family control, often drive decision-making, taking precedence over business-centered economic goals (Debicki et al., 2016; De Massis et al., 2020; Ducassy and Prevot, 2010; Gomez-Mejia et al., 2011; Schmid et al., 2015). To retain family control, family owners often guard their privacy and are more cautious in choosing with whom they share confidential information (Lester and Cannella, 2006). For this reason, owning families may be reluctant to lose discretion to outsiders on the board, or to the board as a whole (Bammens et al., 2011). Retaining family control may therefore trigger greater secrecy and lack of transparency with outside board members (Chrisman et al., 2012; Kotlar and De Massis, 2013; Kotlar et al., 2018). Thus, to maintain control when outsiders are present, family-controlled firms may withhold firm-specific information to avoid being challenged (Gomez-Mejia et al., 2011). Furthermore, family members often prefer managing their conflicts outside of board meetings to avoid the potential embarrassment of exposing nonfamily (outside) directors to conflicts within the family (Bettinelli, 2011). In summary, all else being equal, to retain power, family-controlled firms may rely less on the board (vs. the family) as an active participant in the firm’s decisions. In family-controlled firms, the trade-off between ‘resource acquisition vs. power’ hence turns in favor of the dominant coalition holding power within the family.

A second rationale for H2 links the concepts of trust, family in-group, and open communication. In family-controlled firms, kinship, shared history, and repeated social interactions among relatives are bonding mechanisms that build mutual trust (Steier, 2001; Sundaramurthy, 2008) and create an in-group culture (Uhlaner et al., 2007). Despite the benefits of diversity that outside members may bring to the board, they are not part of the family in-group (Foddy et al., 2009). As such, their greater social distance from the family may generate distrust (Forbes and Milliken, 1999; Minichilli et al., 2010; Stolle et al., 2008). Given that trust is a prerequisite for more open communication (Forbes and Milliken, 1999; Roberts et al., 2005; Zahra and Filatotchev, 2004), CEOs in family-controlled firms, either as a family CEO belonging to the dominant coalition or as a nonfamily CEO abiding by the controlling-family’s preferences, may thus be more reluctant to disclose firm-specific information to the board in the presence of outside directors than CEOs in nonfamily-controlled firms.

Conversely, consistent with the above rationale, when all board members are insiders, family control would have a less negative effect on information disclosure, since the insiders are most likely to be family members or managers, and already know sensitive issues. Accordingly:

Board meeting frequency as moderator

We also explore board meeting frequency as a possible moderator of the relationship proposed in H1. We assume that in the SME context, the dominant coalition of the firm (usually including its CEO), using its discretion, designs the type of board it wishes to have, within the bounds of government regulations. The board dynamics literature distinguishes between minimalist and maximalist boards, the former severely limiting the board’s engagement in, and influence on, the affairs of the firm (Roberts et al., 2005). In a minimalist board, outside directors are appointed chiefly to respond to pressures from external stakeholders (e.g. a minority investor or bank), or alternatively to enhance the SME’s legitimacy to outside stakeholders (Fiegener, 2005; Johannisson and Huse, 2000; Kammerlander et al., 2015). As such, in a minimalist board, the trade-off between ‘resource acquisition vs. power’ turns in favor of the dominant coalition holding power.

By contrast, boards meeting more frequently may reflect the desire of the dominant coalition to build a ‘maximalist’ board, that is, one that can assist the firm in making more effective strategic decisions (Roberts et al., 2005). Based on Allport’s (1954) contact hypothesis, board meeting frequency may also provide greater opportunities for outside directors to interact and communicate with internal directors and managers, building the trust required as a prerequisite of information disclosure (Adams and Ferreira, 2008; Bettinelli, 2011; Boivie et al., 2016; Pugliese and Wenstøp, 2007; Zattoni et al., 2015).

But when all board members are insiders, the frequency of meetings may have less impact on information disclosure, since inside members are likely to have much more access to firm-specific information outside of board meetings as part of their daily activities. Thus, we would expect board meeting frequency to be less important for all-insider boards. Accordingly:

Board service engagement as a mediator between information disclosure and firm financial performance

Finally, we posit a mediating effect of board service engagement on the relationship between information disclosure and firm financial performance. First, overlapping with the rationale in H1, we expect a positive direct relationship between information disclosure and board service engagement, consistent with the underlying view of the board as an information processing (Boivie et al., 2016) and strategic decision-making group (Forbes and Milliken, 1999). In fact, while board members come to the board with their own function-specific knowledge and skills, especially in SMEs, they depend on management to obtain firm-specific information vital for effective problem solving (Van Ees et al., 2009).

Second, we expect a positive relationship between board service engagement and financial performance. Prior research has acknowledged the importance of well-functioning boards in SMEs, since good governance practices may improve the firm’s value and avoid exit or failure (Bammens, et al., 2008; Fiegener et al., 2000; Johannisson and Huse, 2000). Entrepreneurs and managers in SMEs may especially benefit from board support to develop more effective strategies (Forbes and Milliken, 1999; Zattoni et al., 2015) due to limitations often found among SME top management teams (TMTs). These might include the TMT’s smaller size (Feltham et al., 2005; Forbes and Milliken, 1999; Voordeckers et al., 2007), lack of general business knowledge, and limited external work experience (Vandenbroucke et al., 2016). Consistent with this argument, several studies find empirical support for the positive relationship between board service engagement and a firm’s financial performance (Judge and Zeithaml, 1992; Lohe and Calabrò, 2017; Stiles, 2001; Zattoni et al., 2015).

Given the positive direct effect of information disclosure on board service engagement, and a positive relationship between board service engagement and a firm’s financial performance, we expect an indirect positive effect of information disclosure on firm performance through board service engagement. Accordingly:

Research method

Data

This research is based on a sample of 561 Belgian private SMEs (both family- and nonfamily-controlled) designated as naamloze vennootschap (NV), a type of limited liability legal form similar to the US ‘C’ corporation, which requires a board of directors, but with legal flexibility on how it is constituted. In the period of our study (2011–2014), all Belgian NVs had one-tier boards, meaning that executive and non-executive (i.e. outside) directors serve together on the same board. Moreover, in Belgium, the firm’s owners can decide whether to appoint outside directors, whether to combine or split the positions of board Chair and CEO (i.e. CEO duality vs. CEO/Chair separation), and how frequently the board should meet beyond the minimum-required annual meeting. Regarding information disclosure, management is only obliged to share its annual financial statements with its board, which must be board-approved. Disclosure of other information or more frequent sharing of interim financial information is optional.

To define the population of firms for the study, we initially drew on the total population of privately-held Belgian NVs in 2010 with between 11 and 250 employees, the latter being the upper limit in the European Commission’s definition of SMEs. As to the lower limit, similarly to Gabrielsson (2007), we included firms with at least 11 employees, since very small (micro) firms are more likely to have ‘pro forma’ or rubber-stamp boards. We excluded financial services firms (SIC 60–67) and firms in public administration (SIC 91–99), as these are subject to different governance regulations. Finally, we excluded firms controlled by another corporation. A population of 5059 firms remained after applying the size and industry criteria to the total population of privately-held Belgian NVs.

We collected data from two sources: (1) a questionnaire distributed by post and via a web survey in 2011, and (2) Bel-First (Bureau Marcel van Dijk), a secondary database providing information on firms in Belgium and Luxembourg, which allowed for the lagged measurement of firm financial performance in 2013 and 2014, and prior financial performance (2009–2011). We designed the questionnaire according to the recommendations of Dillman (2000), including pretesting the items with scholars and practitioners to improve content validity.

In line with previous studies examining board service engagement (e.g. Pugliese et al., 2014; Van den Heuvel et al., 2006), we targeted firm CEOs as key informants, since they are knowledgeable about the issues investigated in our study. 4 We sent the questionnaire to all 5059 SMEs. The initial questionnaire survey and two follow-ups yielded 613 responses for a response rate of 12%. This response rate is in line with other Belgian survey-based studies on SME board governance and family firms (e.g. Bammens et al., 2008; Huybrechts et al., 2013).

We verified the suitability of the responses first by comparing responding and nonresponding firms from the population (n = 5,059) using archival data. Results of a two-sample t-test indicated that the two groups differed neither in total assets (t = 1.13, ns) nor return on assets (t = –1.21, ns). Second, we compared respondents from different survey waves using the Wilcoxon-Mann-Whitney and chi-square tests on the variables in the analyses. The results revealed no significant differences for the majority of variables.

In the next step, we removed firms with large amounts of missing data, resulting in 561 SMEs in the full sample. Of these, 393 stated that the largest shareholder was a family, also indicating that two or more shareholders had family ties. The remaining 168 firms identified their largest shareholder as an individual (i.e. a single shareholder without shareholding relatives), a private equity investor (i.e. a company whose main objective is to provide capital), or a financial institution (i.e. a bank or insurance company).

Variable measurement

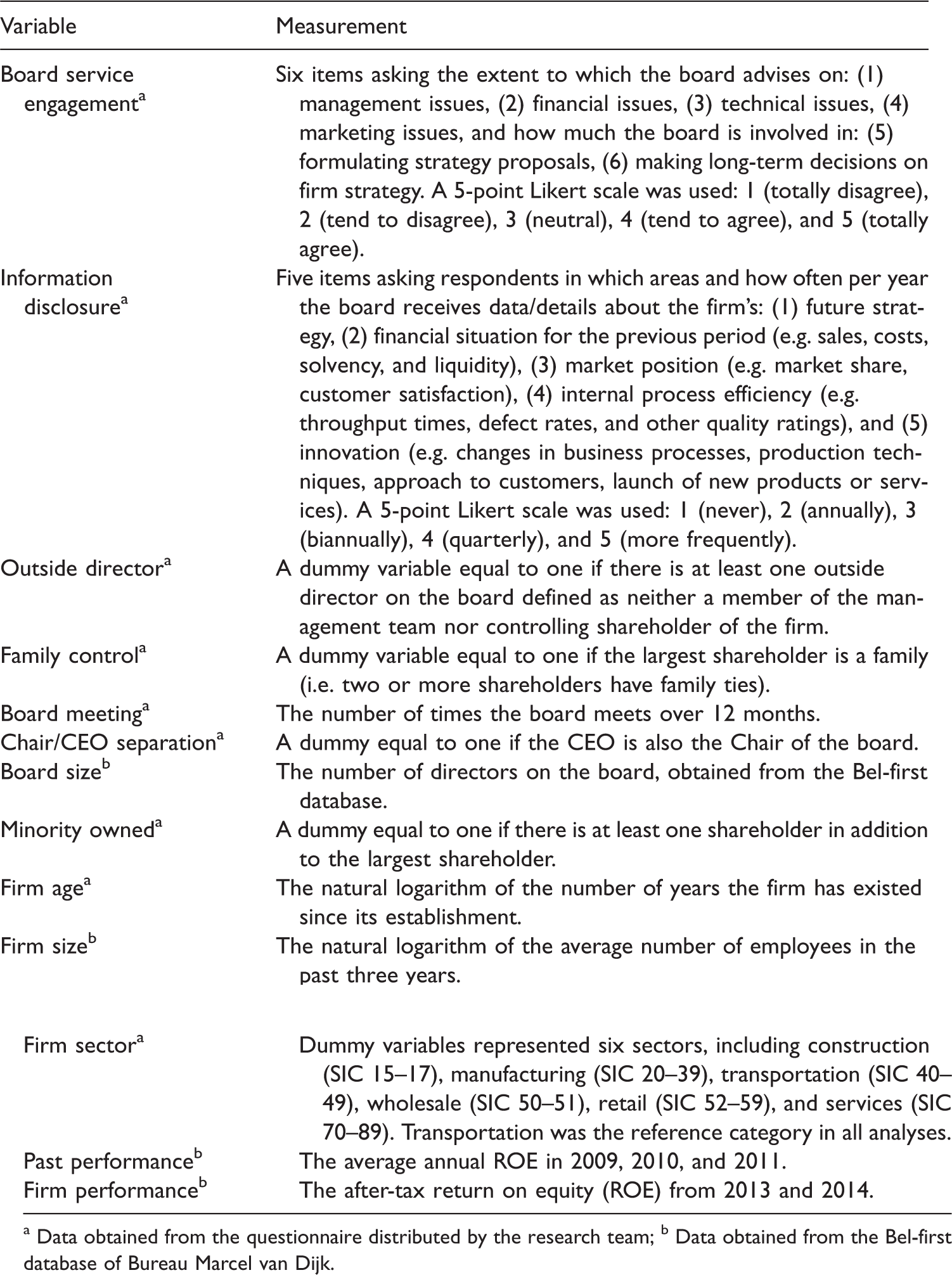

A brief description and the source of each variable follow in this section, with detailed descriptions in the Appendix. Unless otherwise stated, data were gathered from the questionnaire.

Dependent variables

Board service engagement is based on a scale developed by Zattoni et al. (2015) 5 comprised of a mean of six items measuring the extent to which the board advises and/or is involved in a range of matters including: (1) management issues, (2) financial issues, (3) technical issues, (4) marketing issues, (5) formulating strategy proposals, and (6) making long-term decisions on firm strategy. Data for the variable firm financial performance, measured as after-tax return on equity (ROE) from 2013 and 2014, was obtained from the Bel-first database. We chose ROE, as it measures a firm’s overall profitability in the operating, investment, and financing activities on which boards advise management.

Independent and mediating variables

Similarly to Khanna et al. (2013), we measured the variable presence of an outside director (henceforth outside director) with a dummy variable equal to one if there was at least one outside director on the board. Consistent with the definitions in Belgium’s Code Buysse and Brunninge et al. (2007), we defined outside directors as those who are neither members of the management team nor controlling shareholders. Information disclosure is a scale based on the mean of five items adapted from research in the TMT context (Henri, 2006; Hoque et al., 2001). The measurement captures the scope of disclosure of firm-specific information by the management to the board, and includes: (1) future strategy of the firm, (2) financial situation of the firm (revenues, costs, profit, leverage, liquidity), (3) market position of the firm (market share, customer satisfaction), (4) efficiency of the firm’s internal processes (defect rates, response times), and (5) innovation and renewal within the firm (time to market, new products and services). For each type of information, respondents were asked to indicate the frequency with which their board received such information on a scale ranging from zero to four (0 = never, 4 = more frequently than once a quarter).

Moderating variables

Family control is a dummy variable equal to one if the largest shareholder is a family, defined as two or more shareholders having family ties. This measure is similar to that of Deephouse and Jaskiewicz (2013), and Peng and Yiang (2010). Board meeting frequency was posed as an open question where respondents were asked to report the exact number of times the board meets over 12 months. 6

Control variables

Based on previous studies on board task roles, we controlled for other board and firm characteristics including Chair/CEO separation, board size, minority ownership, firm age, firm size, past performance, and industry dummies. Chair/CEO separation is a dummy equal to one if the board Chair is not the CEO, as used in previous studies (e.g. DeMaere et al., 2014). Prior research shows that the separation of Chair and CEO positions is associated with greater board service engagement in SMEs (Gabrielsson, 2007; Knockaert et al., 2015). Board size, obtained from the Bel-first database, is the number of directors on the board. On the one hand, larger boards usually consist of directors with diverse educational and industrial backgrounds and skills, and multiple perspectives that improve board service engagement (Zahra and Pearce, 1989). On the other hand, larger boards face greater communication and coordination difficulties, are less cohesive, and thus less effective in performing board tasks (Eisenberg et al., 1998; Boivie et al., 2016). Minority owned is a dummy equal to one if there is at least one (nonfamily) minority shareholder. When minority shareholders are present, SMEs often appoint outsiders to the board primarily to satisfy these shareholders and obtain legitimacy rather than contribute to its service role (Fiegener et al., 2000). Firm age is the natural logarithm of the number of years the firm has existed since its establishment. Firm size, also obtained from the Bel-first database, is measured by the natural logarithm of the average number of employees in the past three years. Larger and older firms face a greater variety and complexity of issues, and as a result, CEOs rely more on their board of directors for advice in decision-making processes (Bettinelli, 2011). Past performance is measured by the average annual ROE in 2009, 2010, and 2011, obtained from the Bel-first database. Poor past performance may stimulate greater board service engagement (Reid and Turbide, 2012). We included the following five industry dummies to control for board and firm performance differences: construction (SIC 15–17), manufacturing (SIC 20–39), wholesale (SIC 50–51), retail (SIC 52–59), and services (SIC 70–89), using transportation (SIC 40–49) as the reference category. 7

Method of analysis and scale construction

Following Podsakoff et al.’s (2003) suggestion, we aimed to limit common method bias both ex-ante and ex-post. Ex-ante, at the questionnaire design stage, we selected factual measures for key variables, such as information disclosure (scope measured by type of information and frequency vs. quality). To test for common method variance ex-post, we used confirmatory factor analysis with the AMOS software to test for convergent and discriminant validity. To check for multicollinearity among the indicators, we also calculated the variance inflation factor (VIF) score based on output from an ordinary least squares multiple regression analysis with firm financial performance as the dependent variable.

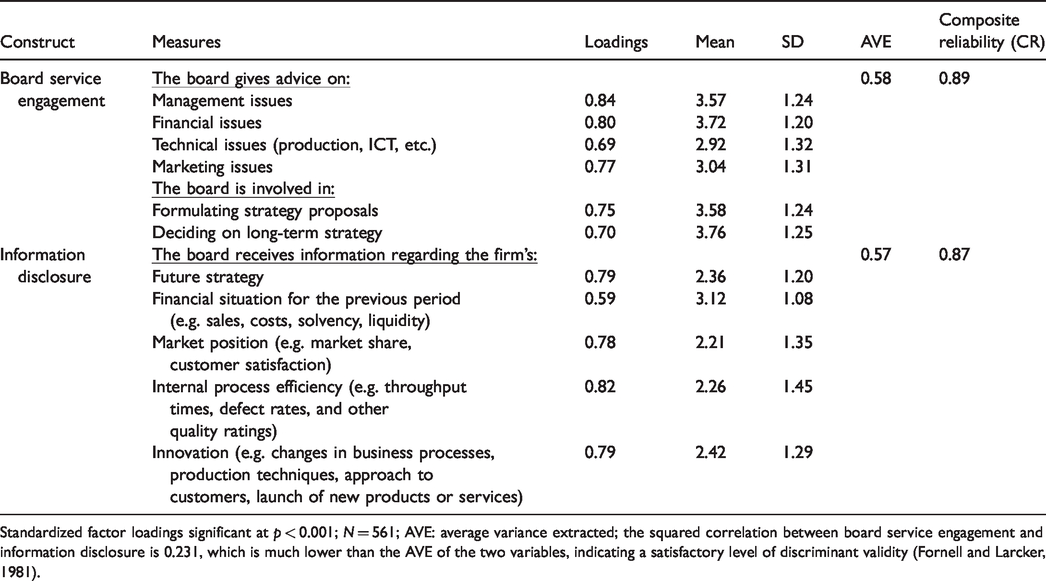

Table 1 presents the results of the confirmatory factor analysis of the latent variables using AMOS. The overall fit indices for our measurement model are χ2 = 105.68, df = 39, p < 0.001 (CMIN/degrees of freedom (df) = 2.71), RMSEA = 0.055, CFI = 0.981, NFI = 0.97, indicating that the measurement model fits the data well (Brown, 2006). As Table 1 shows, the factor loadings range from 0.59 to 0.84, above the 0.55 cut-off for a ‘good’ loading (Tabachnick and Fidell, 2007). The average variance extracted (AVE) for each latent variable is above 0.50, indicating adequate convergent validity (Fornell and Larcker, 1981). Both AVE values for our latent constructs are higher than the squared inter-construct correlation (r2 = 0.28), indicating a satisfactory level of discriminant validity (Fornell and Larcker, 1981). Finally, the composite reliability (CR) scores are well above the recommended cut-off of 0.70, indicating a satisfactory level of reliability (Hair et al., 2006). In summary, the measurement model results provide support for the validity and reliability of our latent constructs. Table 1 also shows the mean value of each item measuring the latent constructs. Referring to the Likert scale for information disclosure, boards in our sample on average receive financial information biannually (mean = 3.11) and other information almost annually (mean range: 2.15 to 2.40).

Confirmatory factor analysis and measurement validity.

Standardized factor loadings significant at p < 0.001; N = 561; AVE: average variance extracted; the squared correlation between board service engagement and information disclosure is 0.231, which is much lower than the AVE of the two variables, indicating a satisfactory level of discriminant validity (Fornell and Larcker, 1981).

To test our four hypotheses, we used different models from Hayes’ (2017) conditional process analysis (PROCESS). This approach enabled us to estimate the direct and indirect effects in single and multiple mediator models, and allowed for non-normality assumptions (Hayes, 2017; Preacher et al., 2007). To test the significance of all effects, we followed Hayes’ (2017) guidelines to generate 95% confidence intervals using the bias-corrected bootstrapping procedure with 5000 bootstrap samples. A confidence interval not intersecting zero would thus show a significant statistical effect at the p < 0.05 level. To test for moderated mediation effects, we first inspected the hypothesized interaction term in the multiple regression model, then the significance of each conditional indirect effect, and finally, the significance of the index of the moderated mediation index (Hayes, 2015; Preacher et al., 2007), reporting each result in the text and tables. 8 PROCESS was also used for robustness checks and additional post-hoc analyses.

In testing the first three hypotheses, we were more interested in the simultaneous association between information disclosure and the presence of outside directors (i.e. rather than their temporal order), especially given different boundary conditions. Our results indicate that the dominant coalition’s characteristics and attitude act as significant contingent variables influencing the relationships among the firm-level governance variables. We thus do not imply causal inferences for these hypotheses, especially between the presence of outside directors and firm-specific information disclosure (H1, H2, and H3). As a first robustness check of the moderated mediation effects, we also checked for moderation of the relationship between information disclosure and board service engagement.

Since we do imply a temporal order amongst the three variables in H4, we took certain steps to support this premise. First, we used longitudinal data to measure firm financial performance, introducing a time-lag of two years between the dependent variable and the other two variables. Second, as a robustness check, we reversed the order of the independent and mediating variables in predicting firm performance, as recommended by Hayes (2017) and Shrum et al. (2011). Finally, as Hayes and Rockwood (2020) and Wunsch et al. (2010) recommend, we considered the logic behind the proposed temporal order for H4 (discussed in the summary of results).

Results

Descriptive statistics

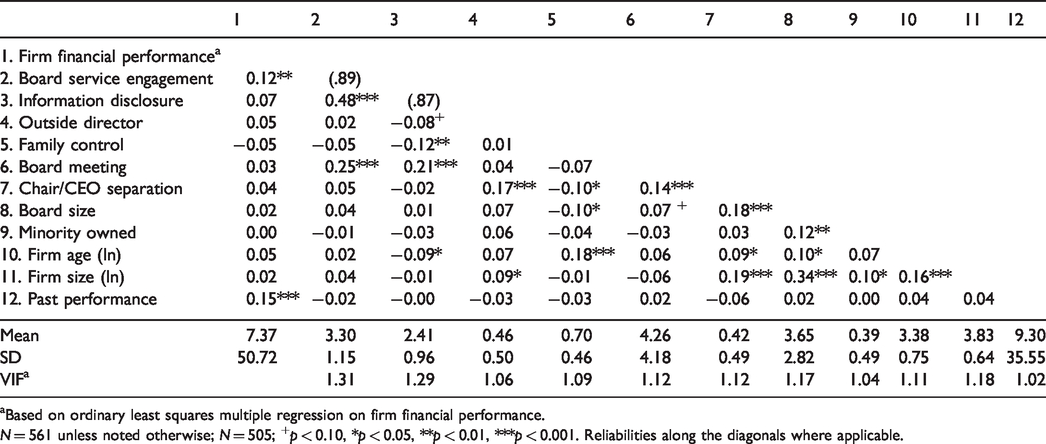

Table 2 presents the Pearson-product moment correlation, mean, and standard deviation for all variables. It also presents VIF scores generated from an ordinary least squares (OLS) regression analysis using firm financial performance as the dependent variable. The VIF scores of all variables are well below 2, indicating that multicollinearity is not likely to be a problem.

Summary statistics, variance inflation factor (VIF) scores, and Pearson-product moment correlation coefficients.

aBased on ordinary least squares multiple regression on firm financial performance.

N = 561 unless noted otherwise; N = 505; +p < 0.10, *p < 0.05, **p < 0.01, ***p < 0.001. Reliabilities along the diagonals where applicable.

Regarding the descriptive statistics of the sample, approximately 46% of firms have at least one outside director. Firms reported holding board meetings on average four times per year. Further, 43% of firms separate the Chair and CEO positions, and the average board comprises four members. On average, firms have 58 employees and are 46 years old. The correlation analysis shows that information disclosure and board meeting frequency are positively correlated with board service engagement (r = 0.48, p < 0.001; r = 0.25, p < 0.001, respectively). Board meeting frequency is positively associated with information disclosure (r = 0.21, p < 0.001). However, a small correlation coefficient size indicates rather low variance overlap (about 4%) between the two variables. Also verified by separate t-tests, the correlation coefficients show that CEOs in family-controlled firms disclose less firm-specific information, family-controlled firms are less likely to separate the Chair and CEO positions, have a smaller board, and are older than nonfamily-controlled firms.

Tests of the hypotheses

H1: Mediation effect of information disclosure in the relationship between outside director and board service engagement H2: Mediation effect of information disclosure (H1) moderated by family control

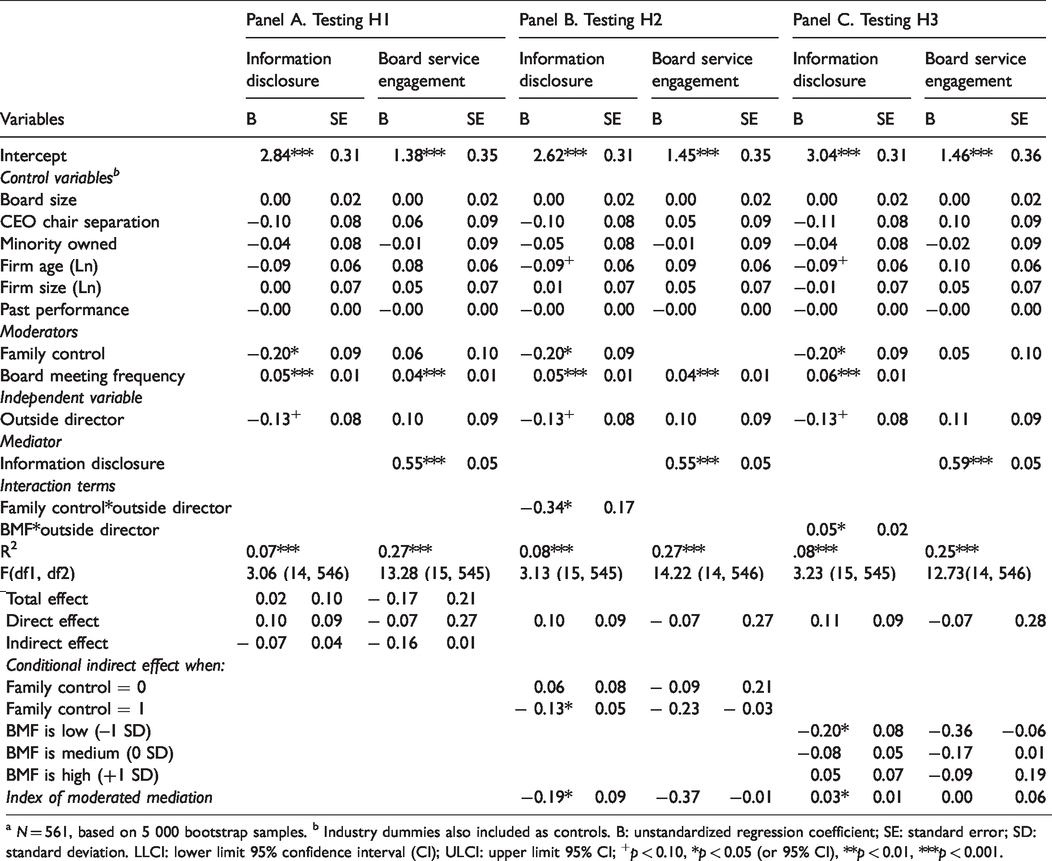

Prediction of board service engagement by outside directors’ presence (outside director).a

a N = 561, based on 5 000 bootstrap samples. b Industry dummies also included as controls. B: unstandardized regression coefficient; SE: standard error; SD: standard deviation. LLCI: lower limit 95% confidence interval (CI); ULCI: upper limit 95% CI; +p < 0.10, *p < 0.05 (or 95% CI), **p < 0.01, ***p < 0.001.

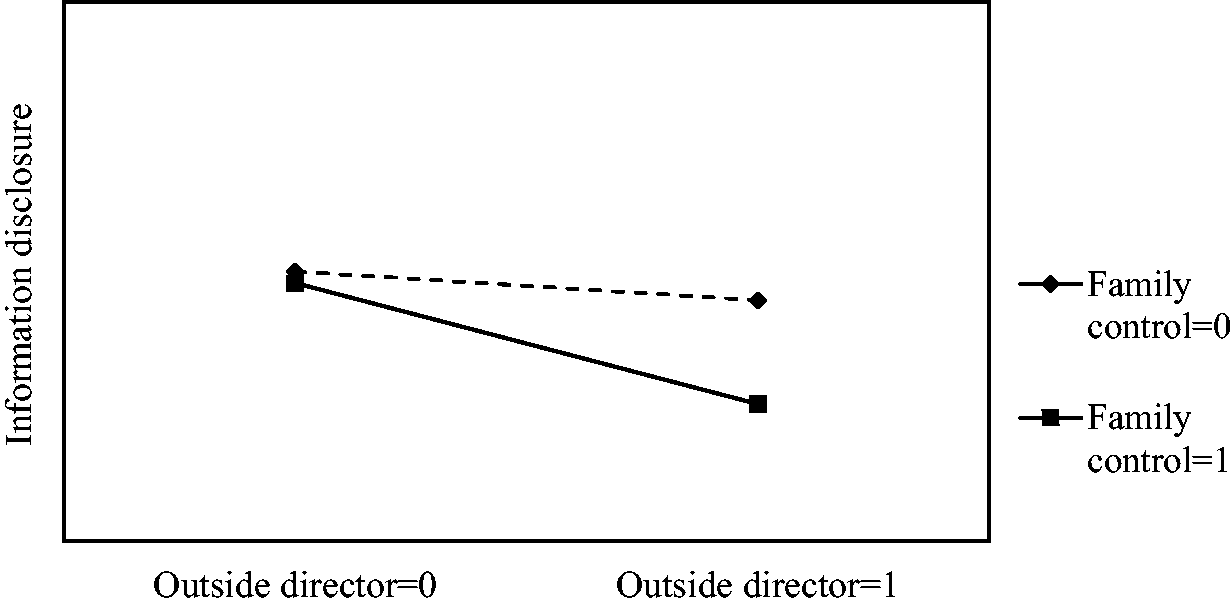

To test the moderated mediation proposed in H2, we first tested the significance of the interaction between outside director and family control in predicting information disclosure. Table 3, Panel B reports this interaction term as statistically significant (B = –0.34, p < 0.05). As shown in Table 3, Panel B, the conditional indirect effect of outside director on board service engagement is statistically significant (p < 0.05) and negative for family-controlled firms (B = –0.13, 95% CI of –0.23 and –0.03), but not significant for nonfamily-controlled firms (B = 0.06, 95% CI of –0.09 and 0.21). We also find that the index of moderated mediation is significant (p < 0.05) and negative (B = –0.19; 95% CI of –0.37 and –0.01). Thus, H2 is strongly supported. This is graphically illustrated in Figure 2. H3: Mediation effect of information disclosure (H1) moderated by board meeting frequency

Plotting the moderating effect of family control on the relationship between outside director and information disclosure (H3).

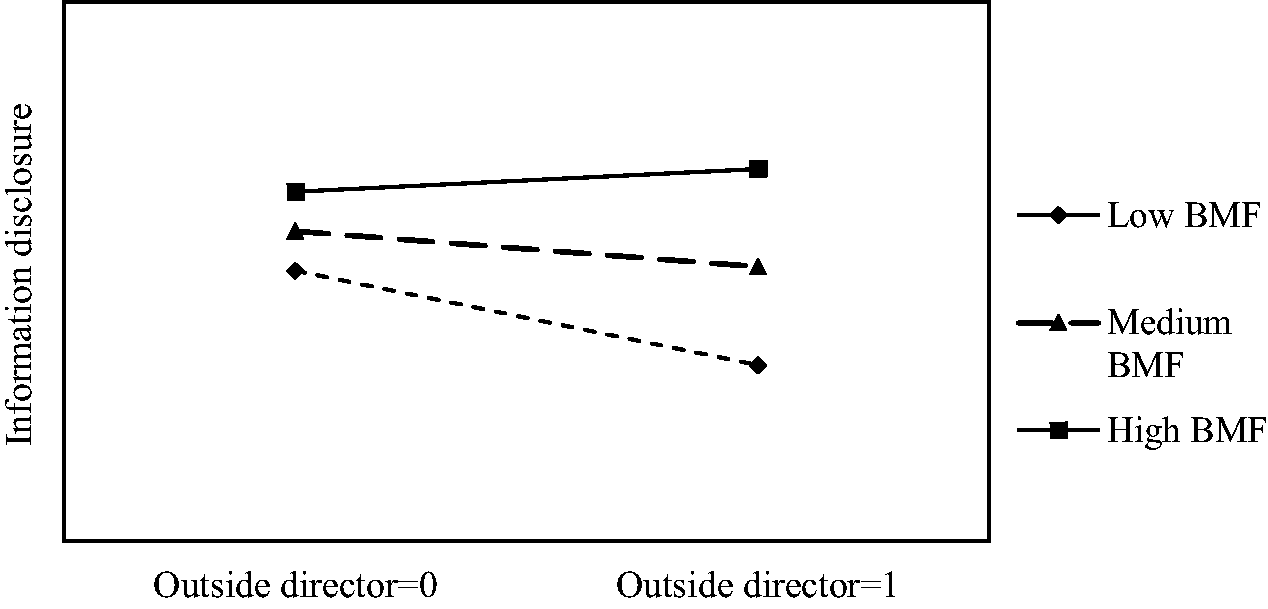

To test the moderated mediation proposed in H3 (Table 3, Panel C), we used the same three tests as for H2. The interaction term of outside director and board meeting frequency predicting information disclosure is statistically significant (B = 0.05, p < 0.05). We find a significant negative conditional indirect effect of outside director on board service engagement for firms with one standard deviation (SD) below the mean (–1 SD or less than one meeting per year) (B = –0.20, 95% CI of –0.36 and –0.06), but not for a medium (0 SD or about four meetings per year), (B = –0.08, 95% CI of –0.17 and 0.01) or high level of board meeting frequency (+1 SD or about eight meetings per year) (B = 0.05, 95% CI of –0.09 and 0.19). As also reported in Table 3, Panel C, the index of moderated mediation is significant (p < 0.05) and positive (B = 0.03, 95% CI of 0.00 and 0.06) (Preacher et al., 2007). These results support H3 and are graphically represented in Figure 3. H4: Mediation effect of board service engagement in the relationship between information disclosure and firm financial performance

Plotting the moderating effect of board meeting frequency on the relationship between outside director and information disclosure (H4).

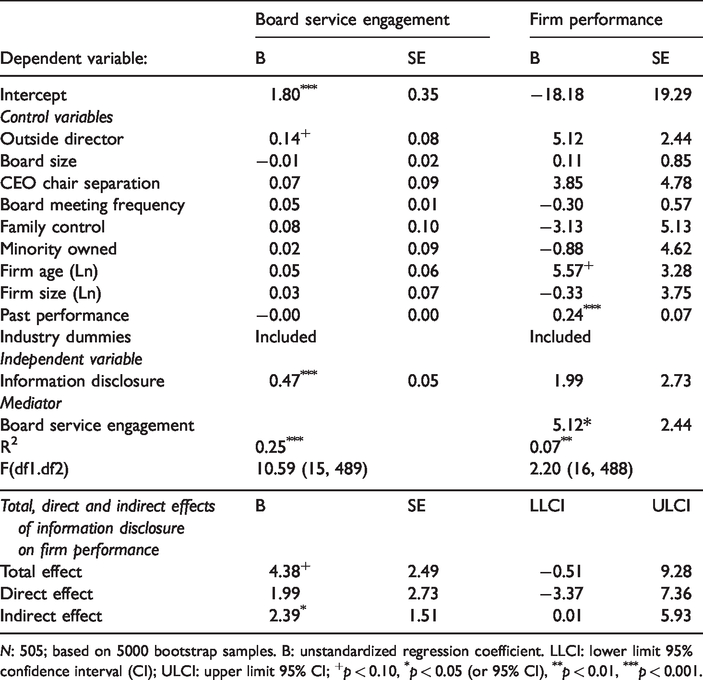

In H4, we stated that board service engagement mediates the effect of information disclosure on firm financial performance. As shown in Table 4, the bootstrapped results confirm the predicted indirect effect (B = 2.39; 95% CI = 0.01 and 5.93), thus supporting H4.

Prediction of firm performance by information disclosure (H4).

N: 505; based on 5000 bootstrap samples. B: unstandardized regression coefficient. LLCI: lower limit 95% confidence interval (CI); ULCI: upper limit 95% CI; +p < 0.10, *p < 0.05 (or 95% CI), **p < 0.01, ***p < 0.001.

Robustness checks

As a first robustness check, especially for the posited non-moderated effect of information disclosure on board service engagement, we tested a two-pronged moderation model, including the originally predicted moderating effect for both H2 and H3, adding a second moderating effect on the relationship between information disclosure and board service engagement (Figure 4 below and Table S.1, Panels A and B in the Supplementary Document). 9 The results of the originally predicted moderating effects for both H2 and H3 remain the same. For H2, the second family control moderating effect on the relationship between information disclosure and board service engagement is not significant, consistent with the simple mediation predicted in H4. The second interaction term for board meeting frequency and information disclosure is negative, since the coefficients and slopes for all three conditions are positive and significant, suggesting a substitution effect between information disclosure and board meeting frequency. Supporting this interpretation, a plot of the findings shows that for firms with high information disclosure, the values of board service engagement for the three board meeting frequency conditions converge to the same value (Figure S.1 in the Supplementary Document).

Testing a two-pronged moderated mediation model as a robustness check for H2 and H3.

As an additional robustness check for H4, to strengthen support for the presumed temporal order (i.e. from information disclosure to board service engagement to firm financial performance), we swapped the order of the first two variables in predicting firm financial performance (Table S.2 in the Supplementary Document). We find a significant direct and nonsignificant indirect effect of board service engagement on firm financial performance, and a significant indirect but nonsignificant direct effect of information disclosure on firm financial performance, consistent with the mediation hypothesis stated in H4.

Other post-hoc analyses

To gain a better understanding of our data, we re-tested H1–H4, replacing the information disclosure scale with each of the five individual information disclosure items (Tables S.3–S.6 in the supplemental material). As described in more detail in the supplement, while the results for individual information disclosure items vary slightly for H1–H3, all five information disclosure items have a significant positive direct effect on board service engagement (p < 0.05), and a positive significant indirect effect on firm financial performance (Table S.6), providing strong additional support for H4.

As an extension of our model, we also examined the relationship between outside director and firm financial performance, including information disclosure and board service engagement as mediators (Table S.7. in the supplemental material). Using the bootstrapping method, none of the tested effects of outside director on firm financial performance fell within a 95% confidence interval, suggesting that we cannot confirm either a positive or negative indirect effect of outside directors on firm financial performance.

Summary of results

To summarize our findings, while our results do not support the simple mediation effect of information disclosure (H1), they do support the proposed moderated mediation effects for H2 and H3. We identify boundary conditions for which the presence of outside directors has a negative effect on board service engagement, but none for a positive effect. Regarding H4, both our initial analyses and robustness check support the proposition that board service engagement mediates the relationship between information disclosure and firm financial performance but not the reverse (i.e. that information disclosure would mediate the relationship between board service engagement and firm performance).

While these findings support the temporal order proposed in H4, Hayes and Rockwood (2020) note that causal inference is hard to prove through statistical methods alone, whether or not data are longitudinal, and depends on the logic of the argument. 10 Thus, worth considering for our dataset is the logic of the proposed ordering of variables, especially for H4. Our measures imply a certain temporal ordering, since information disclosure refers to the frequency of disclosure to board members over the past year, whereas board service engagement refers to the extent of current or ongoing activities. Furthermore, information disclosure is a process, whereas board service engagement is an outcome. It also seems less logical (albeit not impossible) that greater board service engagement stimulates or causes (especially an unwilling) CEO to release more firm-specific information. Based on the initial analysis for H4 and the second robustness check, our results clearly contradict such possibility. In sum, the logical ordering of these variables, the way they were measured, and our statistical findings all support the proposed temporal direction implied in H4.

Discussion

In this section, we summarize our study’s theoretical contributions, present a framework for future research on board governance in the SME context, suggest how our findings contribute to management practice, and finally, point out limitations and directions for future research.

Theoretical contributions

Here, we will indicate how our research advances board governance theory in the SME context. First, we challenge the dominant board governance theoretical perspectives, especially agency theory, RBV, and more simplified and widely adapted versions of RDT arguing that the presence of outside directors benefits the firm. Agency theory argues that independent or outside directors can better protect owner interests, countering the possible self-interests of management (Eisenhardt, 1989; Fama and Jensen, 1983; Rindova, 1999). More specific to board service engagement, RDT and RBV are often used to argue that outside directors enhance a board’s service role by bringing new knowledge and an independent and objective view to the board (Bammens et al., 2011; Bankewitz, 2018; Barney, 1991; Hillman and Dalziel, 2003), yet our overall results run counter to such predictions. We find, instead, an overall lack of effect of outside directors on board service engagement, and for certain boundary conditions (family control and low board meeting frequency), we observe that the presence of outside directors has an indirect negative effect via reduced information disclosure.

Compared to those that existing board governance theory predicts, our results are more consistent with the ‘trade-off’ arguments between external resource acquisition and power preservation in the earliest formulations of RDT (Pfeffer and Salancik, 1978) and in Garg and Eisenhardt (2017), shedding further light on such trade-off by considering the dominant coalition. For some SMEs, especially those that are family-controlled, or with a ‘minimalist’ board, information disclosure appears to be viewed as a double-edged sword. Despite its possible benefits for enhancing the board’s effectiveness in decision-making, such firms resist the use of the board, given the potential loss of power for the CEO and the dominant coalition. Family control and lower board meeting frequency may thus reflect the dominant coalition’s choice to retain power versus expanding its (externally acquired) resources. This logic thus helps explain why in certain SME contexts, the presence of outside directors is associated with less information disclosure. The dominant coalition in certain firms would prefer to retain power over the benefits of improving firm performance derived from a more effectively functioning board. This finding, especially for the dominant coalition of family-controlled firms, follows and extends the application of the RDT perspective, underscoring the need to consider power besides external resource acquisition.

However, our results also highlight that choosing power over the benefits of resource acquisition resulting from withholding firm-specific information comes at an additional cost that can negatively affect firm performance. Thus, a second core contribution of our research is identifying information disclosure by the CEO to the board as an essential behavioral process mechanism, offsetting information asymmetry between the board and management, thus assuring board service engagement and firm performance.

While agency theory, board dynamics (Forbes and Milliken, 1999), and board information processing models (Boivie et al., 2016; Edmondson et al., 2003) acknowledge negative effects of information asymmetry between the management and the board, they differ from our study’s findings in important ways. First, agency theory nearly always takes a structural approach, presuming that information asymmetry arises from including outsiders on the board, a position not supported by the present research. Second, while Forbes and Milliken’s (1999) strategic decision-making model, and subsequent board dynamics research, includes firm-specific information as an input to board functioning, the process mechanism by which such information is shared, especially with less informed outside directors, has been largely neglected (e.g. Bezemer et al., 2014; 2018; Forbes and Milliken, 1999; Francoeur et al., 2018; Minichilli et al., 2009; Neill and Dulewicz, 2010; Pugliese et al., 2015; Zattoni et al., 2015; Zona and Zattoni, 2007). Third, while the board information processing perspective acknowledges the importance of information-sharing by the CEO to reduce information asymmetry and enhance board monitoring, such perspective largely overlooks its relevance in the SME context and for board service engagement (Boivie et al., 2016).

Our findings suggest that the reduction of information asymmetry is not only central to improved board governance, but is more likely achieved via a behavioral process mechanism (e.g. information disclosure) than board composition (e.g. presence of outside directors), underscoring the need to take an integrated board dynamics and board information processing approach to explain board behavior and firm performance (e.g., Arzubiaga et al., 2018).

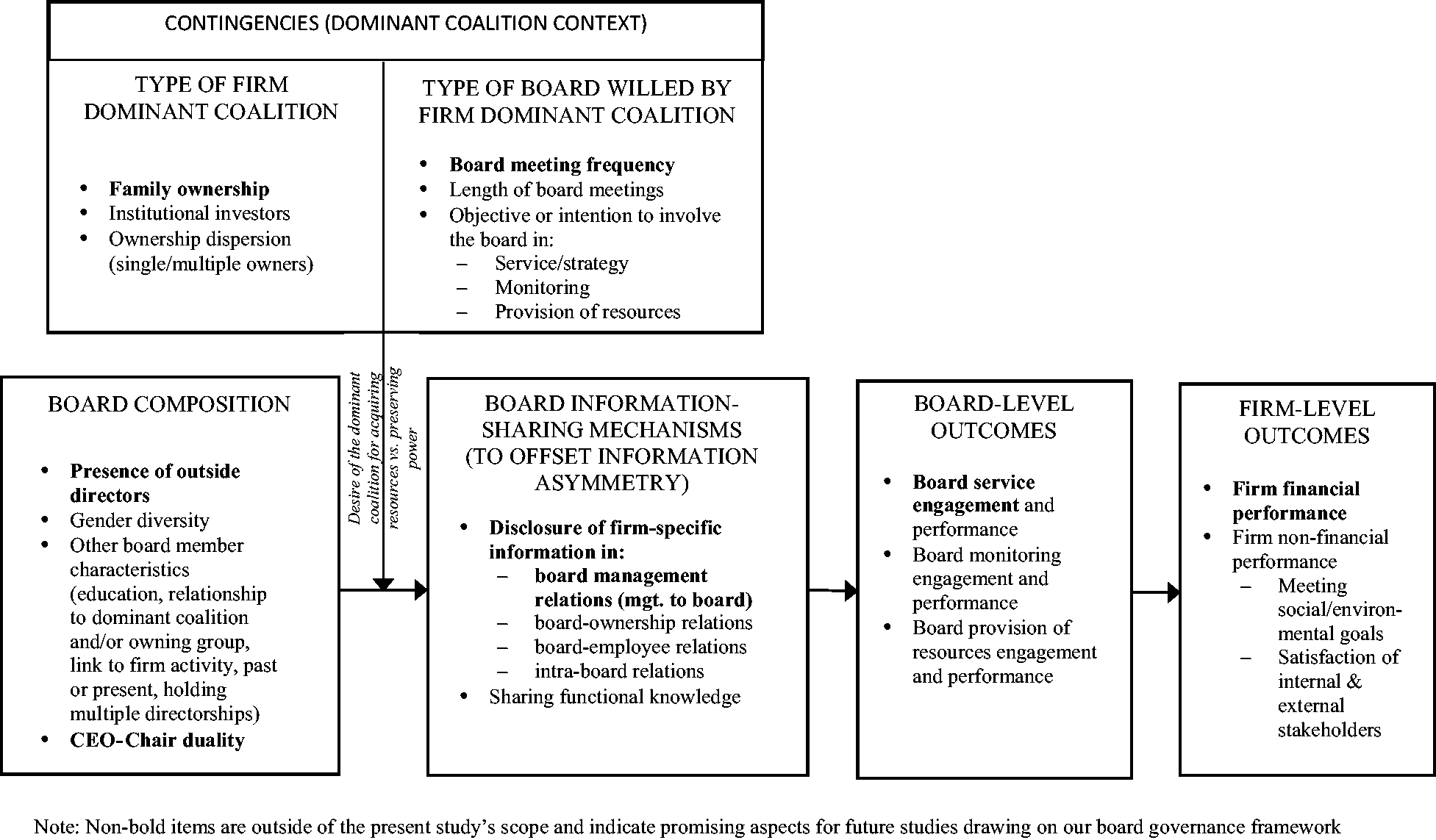

A board governance framework in the SME context

We now present an integrated framework of board governance in the SME context based on the theoretical implications in the preceding section and illustrated in Figure 5.

Board governance framework in the SME context: Board information-sharing mechanisms, contingencies, and their effects on board- and firm-level outcomes.

Theoretical abstraction from our study’s findings forms the basis of our framework. Central to this framework are two key aspects identified in the prior section, namely the type of firm dominant coalition and the type of board willed by such dominant coalition, which determine how the dominant coalition manages the trade-off between acquiring resources and preserving internal power. In Figure 5, we have marked in bold the variables measured in our study. Then, by abstracting away from our findings, we have identified additional variables that represent promising research directions. As such, the proposed framework serves as a springboard for future board governance research, specifying key elements and relationships that offer an established, coherent explanation of the board governance phenomenon under investigation in the SME context.

We begin with firm-specific information disclosure from management to the board as a central behavioral process mechanism (precisely, board information-sharing). This variable is central to offsetting information asymmetry and enhancing the overall level of firm-specific information and functional knowledge available to the board. While our research has primarily focused on information disclosure from management to the board, future studies could also investigate whether other types of inter-group information exchange (e.g. disclosure from the board to management, from employees to the board, from outside or external sources to the board) or intra-board information exchange, might also offset information asymmetry between board members and management.

Also essential to the proposed framework in the SME context are the contingencies defining the dominant coalition context. In our study, we explored family control and board meeting frequency. Our framework suggests extending these two boundary conditions by considering: (i) the type of dominant coalition through a broader examination of its attributes in addition to family control, such as the presence of institutional investors (e.g. private equity, venture capital, banks, government, etc.) and ownership dispersion (e.g. single vs. multiple, concentrated vs. fragmented ownership); and (ii) the type of board willed by the dominant coalition through the examination of further board attributes besides board meeting frequency, such as the length of board meetings and core objectives (i.e. service/strategy, monitoring, resource provision). These aspects of the dominant coalition determine the trade-off between the desire to retain power versus the benefits of acquiring resources through a more active board for decision-making.

Our emerging framework also suggests that researchers consider board composition more broadly than in the current study, encouraging scholars to take into account further elements that characterize board composition, such as gender diversity, CEO-Chair duality, and board member characteristics in terms of education, relation to the dominant coalition and/or the owning group. Regarding board-level outcomes, our framework suggests that researchers consider other outcomes, such as board monitoring engagement and resource provision (beyond advice and counsel). Finally, it advises expanding firm-level outcomes to consider nonfinancial performance depending on the achievement of social/environmental goals and the satisfaction of various internal and external stakeholders, including employees, customers, and members of the community, and the realization of social and environmental goals.

Contributions to practice

Our research cautions against the wide-spread advice to place an outsider on the SME board. In an inappropriate context, pressing an SME’s CEO or top management team to include outside directors (either through regulation or a consultant’s well-intended advice), may restrict the flow of firm-specific information from management to the board, and thus curtail the board’s decision-making ability to serve the firm. We have identified two boundary conditions (family-controlled firms and board meeting infrequency) where the CEO or top management team may first require coaching not only on why an active board can be valuable for enhancing firm performance (even if it results in losing power or autonomy), but also why sharing firm-specific information with such outsiders can maximize benefits.

Limitations and directions for future research

This study is subject to several limitations that open avenues for future research not mentioned in the framework. First, we must be cautious about drawing causal inferences from our data due to its correlational nature and the limited use of longitudinal data (except for firm financial performance). However, our findings fit a logic that supports the temporal ordering we proposed for H4. Second, our questionnaire data are subject to the usual limitations of surveys, which rely on the perceptions and self-reports of individuals, albeit key informants. Third, regarding our measure of firm-specific information disclosure, while covering frequency and scope, we do not measure the quality or timeliness of information provided, nor how it is used. Future studies might go beyond disclosure frequency and scope by considering the quality, timeliness, and format of information, and how such aspects may influence how information is shared in board-management relations.

Another limitation of our study is the focus on the one-tier corporate board structure. We cannot assume that our findings generalize to other types of boards. However, interviews conducted in a comparison study of one-tier and two-tier boards in Dutch SMEs suggest similarities, especially regarding the problem of information asymmetry between management and nonexecutive directors (De Moor, 2014). One inside director in a Dutch retail SME noted that, ‘supervisory board members receive substantially less information than management. Yet that is not necessarily a consequence of the two-tier structure. Even in a one-tier structure, management will always be more involved and receive more information’ (De Moor, 2014: 32).

Another limitation is that while we use the concepts of power and trust in our rationale and interpretation of results, we do not measure power or trust directly. We welcome future qualitative and quantitative investigations that capture the management’s perceived trust of the board, and whether the CEO’s level of trust in board members, and/or her/his concern for autonomy or power, are associated with her/his willingness to disclose firm-specific information to the board. Future research could also examine alternative explanations for limiting firm-specific information disclosure in the SME context, such as lack of time or awareness of the CEO that outside members need more detailed information to assist with strategic decision-making.

Future research could also examine whether excessive trust between the CEO and the board, shown to lead to board passivity (Cornforth, 2001; Reid and Turbide, 2012), has relevance in the SME context. Finally, future research might test our hypotheses beyond the privately-held SME context to consider how the information-sharing mechanisms might affect governance in listed firms and cooperative organizations, including board-staff relationships.

Conclusion

In assuming that the presence of outside directors can enhance board service engagement and firm performance, prior research has provided an incomplete account of board governance. In the context of Belgian SMEs organized as naamloze vennootschap corporations, we integrate several of the prevailing board governance theories and perspectives with the notion of a dominant coalition to challenge this assumption, and reveal that the disclosure of firm-specific information from management to the board is a missing mechanism to address the information asymmetry issue, and thereby the effects of outside directors’ presence. We identify boundary conditions for which the presence of outside directors has a negative effect on board service engagement, mediated by firm-specific information disclosure from management to the board, but none for a positive effect. When SMEs are controlled by families or when their boards meet infrequently, the presence of outside directors is associated with reduced information disclosure, and indirectly, less board service engagement. We interpret these results further in the context of RDT, suggesting that dominant coalitions vary in how they make a trade-off between acquiring external resources from outside board members versus retaining power. Nevertheless, regardless of such trade-offs, information disclosure is unconditionally and positively associated with board service engagement and (indirectly) with a lagged measure of firm financial performance. This finding suggests that management should offset the potentially negative consequences of information asymmetry by disclosing more firm-specific information to its board of directors, even at the risk of the dominant coalition losing power. The benefit of a more engaged board would appear to outweigh the risks of power loss, at least with respect to firm performance. Building on these findings, we have presented a more extended framework for the study of board governance that will hopefully serve as a springboard for future board governance research in the SME context.

Appendix 1. Description of variables

a Data obtained from the questionnaire distributed by the research team; b Data obtained from the Bel-first database of Bureau Marcel van Dijk.

Supplemental Material

sj-pdf-1-hum-10.1177_0018726720932985 - Supplemental material for Are outside directors on the small and medium-sized enterprise board always beneficial? Disclosure of firm-specific information in board-management relations as the missing mechanism

Supplemental material, sj-pdf-1-hum-10.1177_0018726720932985 for Are outside directors on the small and medium-sized enterprise board always beneficial? Disclosure of firm-specific information in board-management relations as the missing mechanism by Lorraine Uhlaner, Alfredo de Massis, Ann Jorissen and Yan Du in Human Relations

Footnotes

Acknowledgments

We are indebted to our associate editor, Professor Aichia Chang, and to the three anonymous reviewers for their constructive feedback. Moreover, this article has benefited from feedback provided by numerous colleagues to presentations of the article at the 14th European Academy of Management (EURAM) conference in Valencia, the 38th European Accounting Association (EAA) Annual Congress in Glasgow, the 10th Workshop on Corporate Governance in Brussels, the 13th workshop on Family Firm Management Research in Bilbao, the 2018 Research Day in Accounting at KULeuven, a research workshop at Ghent University and the International Family Enterprise Research Academy (IFERA) 2018 conference in Zwolle. Finally, a preliminary version of this article received the ‘Best Paper in Practice’ award sponsored by the Dutch Family Business Network at the 2018 IFERA (International Family Enterprise Research Academy) conference held in Zwolle, the Netherland.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We gratefully acknowledge financial support for this project from the Flemish Agency for Innovation by Science and Technology (IWT) in the framework of the project ‘Effective Governance in private enterprises’ [grant number SBO 90061, 2009–2013].

Supplemental material

Supplemental material for this article is available online.

Notes

![]() . [Email:

. [Email:

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.