Abstract

This article studies the role of the General Agreement on Trade in Services and the Reference Paper (RP) on telecommunications for the digital transformation of services trade, motivated by the special role assigned to telecommunications as the underlying transport means of all services. Using structural gravity applying recommended best practice (Poisson pseudo–maximum likelihood, three-way fixed effects and internal trade), it finds out that having scheduled the RP is associated with a boost in services trade and a shift over time towards digitally deliverable services. However, it does not find evidence that the RP and underlying domestic regulation have shifted trade from commercial presence towards cross-border trade.

Introduction

The General Agreement on Trade in Services (GATS) is one of the four pillars of the World Trade Organization (WTO), established in 1995. Although services have always been traded, they were considered non-tradable both by policy makers and by scholars at the time. The GATS was thus a novelty in international trade governance. 1 True, services do not cross borders in the same manner as goods, so the GATS required conceptual work on the definition of services trade, conventions on how to measure it and not least how to schedule commitments to liberalise services trade (Adlung & Mattoo, 2007; Deardorff, 2001; Francois & Hoekman, 2010; Marchetti & Mavroidis, 2011; Staiger & Sykes, 2021). The result was a legal definition of services trade at odds with the statistical definition, which to this day has made empirical services trade research a challenge.

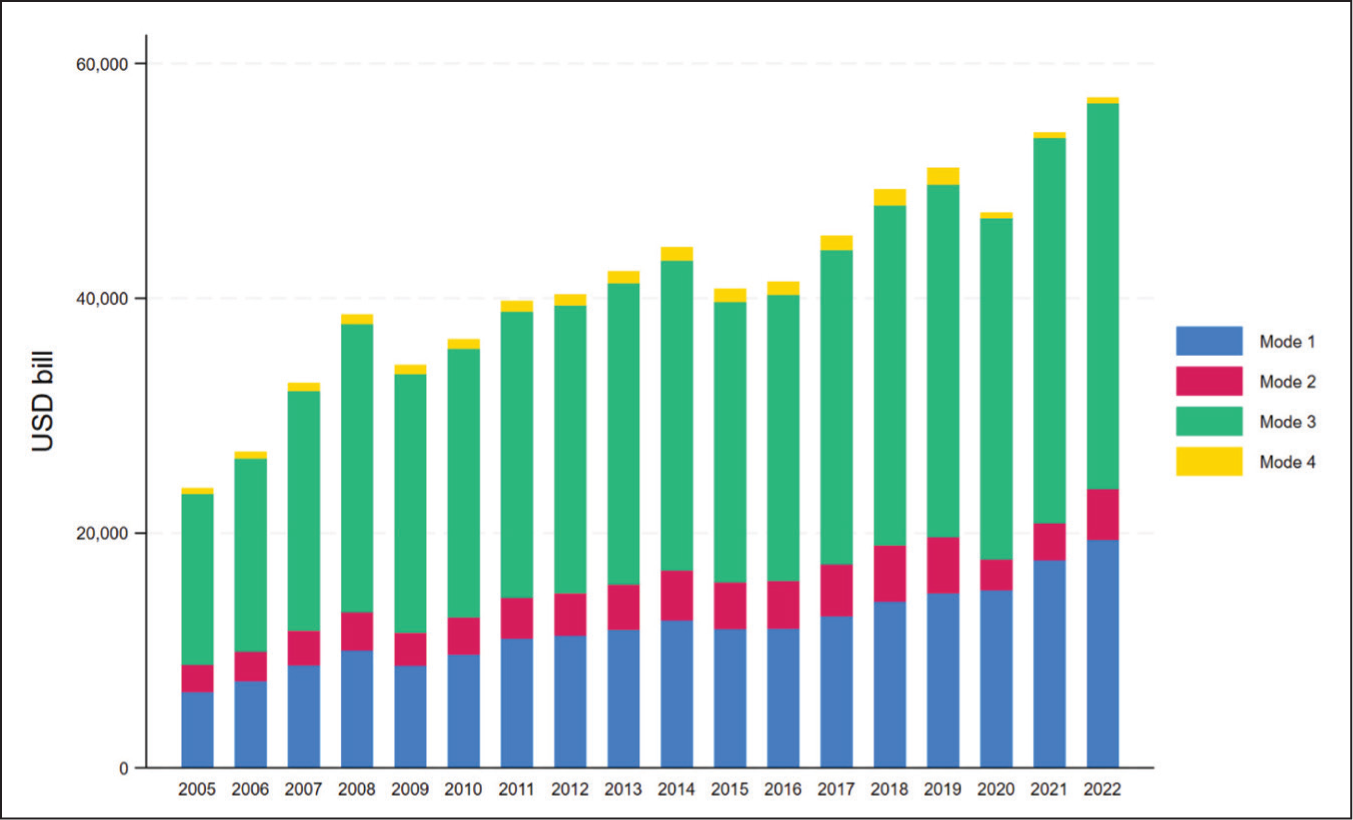

The GATS breaks services trade into four modes: cross-border trade (Mode 1), consumption abroad (Mode 2), commercial presence (Mode 3) and movement of natural persons (Mode 4), while trade in the balance of payment is defined as a transaction between a resident and a non-resident, and does not cover Mode 3. As we shall see, Mode 3 is by far the most important mode of supply, while Mode 4 accounts for a tiny share of total services trade (Figure 1).

At its inception, the GATS was considered a framework to be developed through subsequent negotiations. They started in earnest as part of the single undertaking under the Doha round. Covering broad areas, such as the movement of factors of production across borders combined with lack of jurisprudence, brought the negotiations into unchartered territory. Several modalities, including plurilateral request-offer negotiations, model schedules (for maritime transport and telecommunications) and understanding on commitments (in financial services), were tried out. However, the chairman of the Services Council reported that no substantive progress had been made by 2005 (Adlung, 2006; Adlung & Roy, 2005; WTO, 2005).

A coalition of the willing started plurilateral negotiations on the Trade in Services Agreement (TISA) outside the WTO in 2013. The intention was to finalise the agreement and then bring it into the WTO rule book during the Doha round negotiations (Gootiiz, 2009; Marchetti & Roy, 2014; Sauvé, 2014). The initiative came to nothing, while the Doha round fizzled out. 2

Meanwhile, 217 3 Regional Trade Agreements notified to the WTO include services. Although most of them go beyond GATS in terms of the breadth and depth of commitments, so-called GATS + (Der Marel & Miroudot, 2014; Roy et al., 2007), few go beyond binding existing applied policies (Fiorini & Hoekman, 2018). 4 Thus, neither the GATS nor RTAs have substantially liberalised trade in services. As documented by the OECD (2024), unilateral services trade liberalisation has also been feeble over the past decade.

The joint initiatives (JIs) on electronic commerce and services domestic regulation have recently brought new life into the WTO services agenda. Both are plurilateral agreements envisaged to become part of the WTO rule book. Against the backdrop of the digital transformation of services and bearing in mind that trade barriers in services are largely behind the border, these two agreements complement each other and could potentially reinvigorate services trade. Domestic regulation and digital services trade governance are also important elements in a new generation of economic partnership agreements such as the Australia–India Comprehensive Economic Co-operation Agreement (Mitchell & Mishra, 2023) or digital economy partnership agreements where Singapore has played a leading role (Allen & Liao, 2025).

This article focuses on the interplay between information and communication technology (ICT) and WTO rules as a driver of services trade. The digital transformation of services has reduced cross-border trade costs substantially, brought new services into international markets and opened opportunities for small and medium-sized enterprises to engage in international trade. As we shall see, the digital transformation has seen a faster growth of trade in services that can be traded over electronic networks, so-called digitally deliverable services (DDS), than services trade in general. Estimates also suggest that the share of cross-border trade in total services trade as defined by the GATS has increased gradually over the past 20 years. Nevertheless, it appears that the potential for cross-border services trade growth is far from fully exploited.

The special role of telecommunications as the underlying transport means for other services as well as a service in its own right was recognised already in the GATS agreement—before the commercial internet had taken hold. The Annex on Telecommunications includes obligations to ensure access to and use of telecommunications networks for transport of any services. It applies to all WTO members whether they have made commitments in telecommunications or not. In addition, a Reference Paper (RP) imposes disciplines on domestic regulation in the telecommunications sector. Indeed, the RP was the first and hitherto only effort to bring legally binding competition policy provisions into the WTO (Blouin, 2000). The JI on e-commerce aims for modernising trade rules related to ICT, including a revised RP. 5

Unlike the Annex, the RP is binding only for WTO members that have included it in their GATS schedules. It entails obligations to establish an independent telecommunications regulator responsible for monitoring the market and impose access and interconnection obligations on local suppliers with significant market power. In the pre-internet era, this was essential for telecoms entrants, whether local or foreign, to establish in the market and build a customer base (Cave, 2006).

The RP addressed the fact that market access and national treatment in the telecoms sector would be illusory in the presence of a local incumbent with significant market power. Scheduling the RP in the GATS sent a strong signal of commitment to an open and competitive telecoms market over the long term, regardless of shifting governments. Nordås and Rouzet (2017) provide evidence of a robust relationship between domestic regulation in telecommunications and the cost effectiveness and density of the telecoms network and, thus, its role as the underlying transport means for all services sectors.

While the RP has remained the same since its introduction in the late 1990s, the telecommunications and ICT sector at large has been transformed tremendously and the best-practice regulation with it (Cave & Shortall, 2025; ITU & World Bank, 2020). The ITU Regulatory Tracker provides a benchmark for measuring such best-practice regulation and is a rich source of information on applied pro-competitive policies over time. It includes four pillars of measures: regulatory authority, which records the independence and functioning of the regulator: regulatory mandate, which spells out the scope of the regulators; regulatory regime, which informs about the measures that the regulators impose on the market; and finally, competition framework, which informs about the strength of competition in the ICT markets.

Using structural gravity, this article estimates the impact of the RP as well as applied pro-competitive regulation in telecoms and ICT more broadly on total services trade and trade in DDS by mode of supply. It finds a sound relationship between the RP and services trade. Surprisingly, the impact is much stronger for affiliate sales than for cross-border trade and does not seem to have made a discernible impact on the shift towards Mode 1.

The rest of the article is organised as follows: The second section describes the digital transformation of services trade using WTO statistics. The impact of the RP and applied pro-competitive domestic regulation is analysed empirically in the next sections. The structural gravity model, presented in the third section, constitutes the analytical framework. The data used are described in the fourth section, while the fifth section presents the results. The sixth section draws policy implications and concludes.

Cross-border Trade and the Digital Transformation of Services

As services become increasingly digitalised, one would expect an increase in the relative importance of cross-border trade (Mode 1). To some extent, this is borne out in the data. According to estimated data from the WTO, the share of Mode 1 in total services trade increased from 27% to 34% from 2005 to 2022 (Figure 1).

One would also expect that connectivity is positively associated with the transition to Mode 1. However, surprisingly, a simple correlation analysis did not support this prediction. Thus, the share of Mode 1 in total exports or imports is unrelated to or even negatively related to connectivity. 6 Whether this is due to poorly estimated trade data by mode of supply or regulatory barriers to cross-border trade in digital services will be discussed in the next sections.

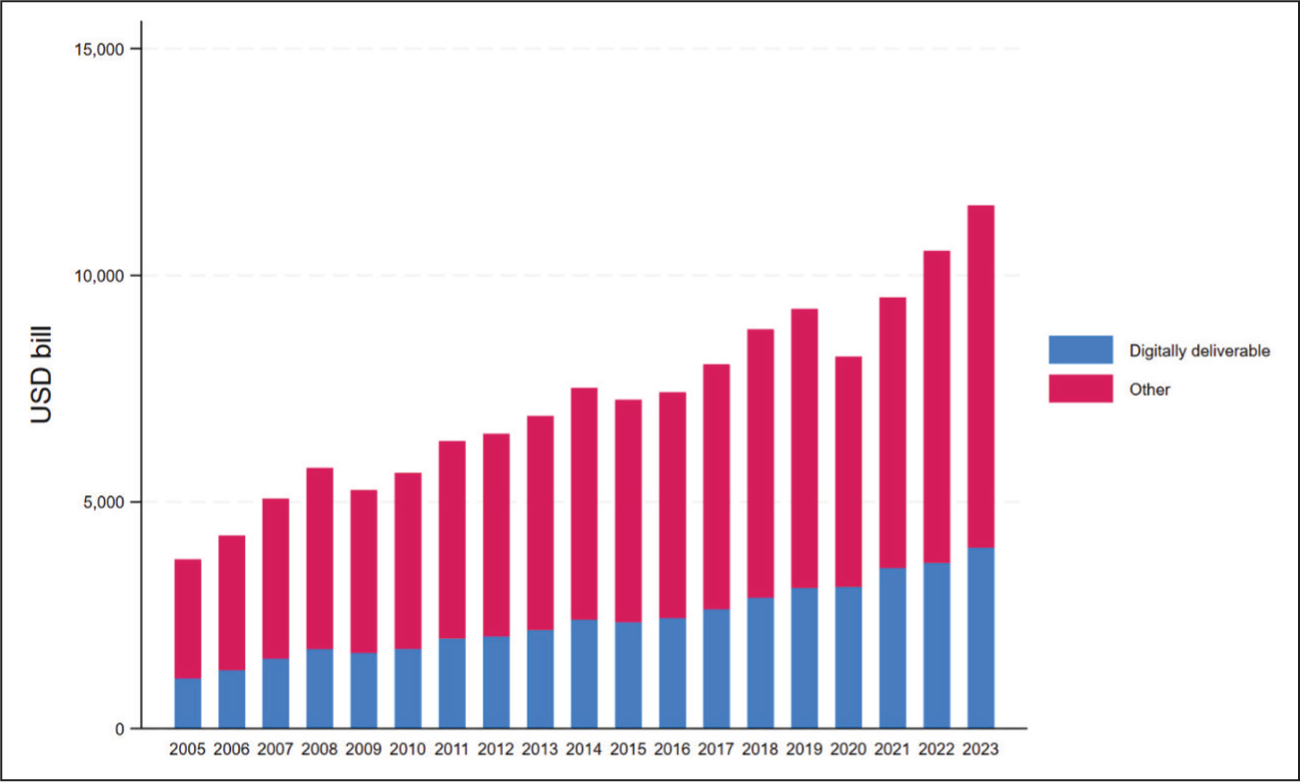

A different way of looking at digital services trade is to identify the services that are digitally deliverable and trace out trade patterns on that basis. While total services trade has experienced setbacks over the period recorded, notably during the COVID-19 pandemic, exports of DDS have expanded steadily and seen a rising share of total global services trade (Figure 2).

DDS are not necessarily digitally delivered. There is no official statistics on digital delivery, but estimates from the WTO suggest that digitally delivered services had increased about fivefold in nominal terms between 2005 and 2023. However, at close to 4.4 trillion dollars in 2023, this estimate exceeded the total value of DDS from BaTiS, as reported in Figure 2. Obviously, these figures cannot both be true. Either the digital delivery figure is overestimated, or digitally deliverable is too narrowly defined.

The Model and Empirical Strategy

This section spells out the empirical strategy for further analysis of the determinants of trade flows by mode. The workhorse model for analysing the relationship between trade costs and bilateral trade flows is the gravity model. Structural gravity consists of three equations in three unknowns and is thus a fully specified model (Yotov, 2024).

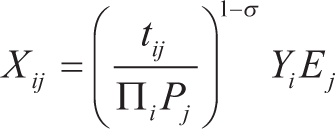

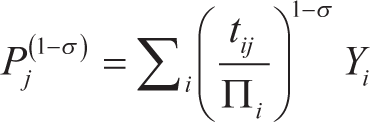

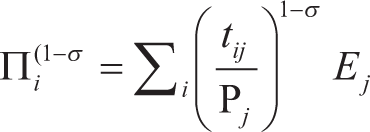

where Xij represents exports from country i to country j, or sales in country j of affiliates originating in country i. Bilateral trade or investment costs are captured by tij, while Yi and Ej denote output in the exporting country and expenditure in the importing country, respectively. Π i and Pj are price indices, which are weighted constant elasticity of substitution aggregates of the bilateral trade costs with all other trading partners. They are referred to as the outward and inward multilateral resistance, respectively. These are important transmitters of relative trade costs throughout the global trading network and capture the fact that changes in bilateral trade costs between two trading partners have repercussions for the entire network, although the impact gets smaller the further away from the initial shock one gets. The Armington elasticity of substitution between services from different origins is denoted as σ.

The regression equation reads:

The variables are indexed i, j, s and t for exporter, importer, sector and year, respectively. The explanatory variables are: FTA is a dummy that takes the value 1 if the country pair is the member of the same free trade area and 0 otherwise; RP is a dummy that takes the value 1 if a country has committed the RP, and lnYRP is log of 1 plus the number of years for which the RP has been in place. 7 The next four variables are exporter-time, importer-time, country pair and sector dummies, while εij, t is an error term. The variable of interest, the RP, is country specific and can therefore not be identified when applying the full set of fixed effects. This problem is solved by including domestic trade, that is, Xij when i = j (Heid et al., 2021; Yotov, 2022), and multiplying the country-specific variable with a dummy (brdr) that takes the value 0 if i = j and 1 otherwise. The equation is estimated using the Poisson pseudo–maximum likelihood (PPML) estimator. 8

Data

Robust gravity regressions require information on bilateral trade flows, including internal trade. The International Trade and Production Database for Estimation (ITIP-E), published on the USICT website, satisfies this requirement and is the preferred data source in recent empirical trade literature (Larch et al., 2025). Data on foreign affiliate sales as well as the number of foreign affiliates by origin, destination and sector are taken from the Multinational Revenue, Employment and Investment Database (MREID) (Ahmad et al., 2025).

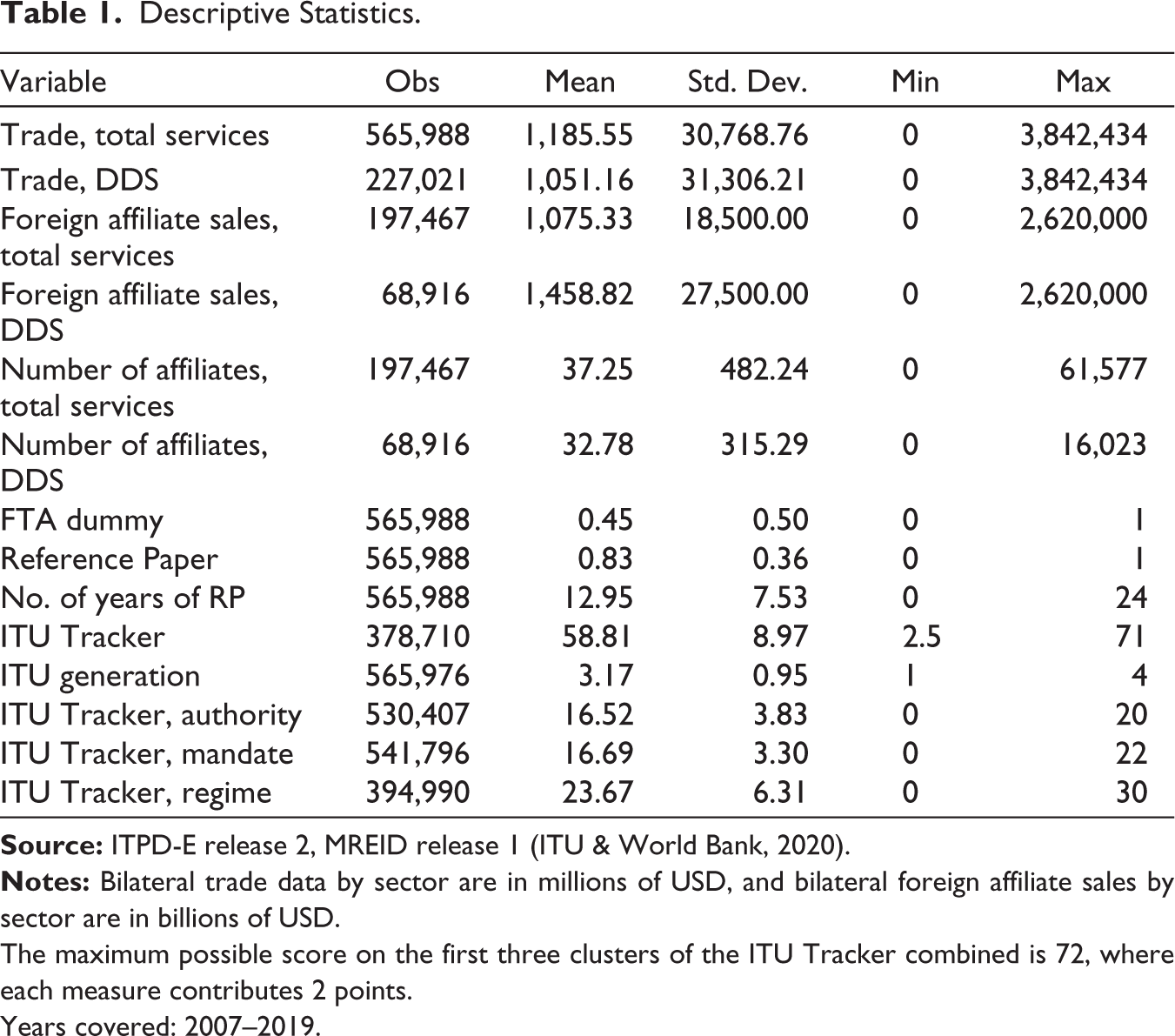

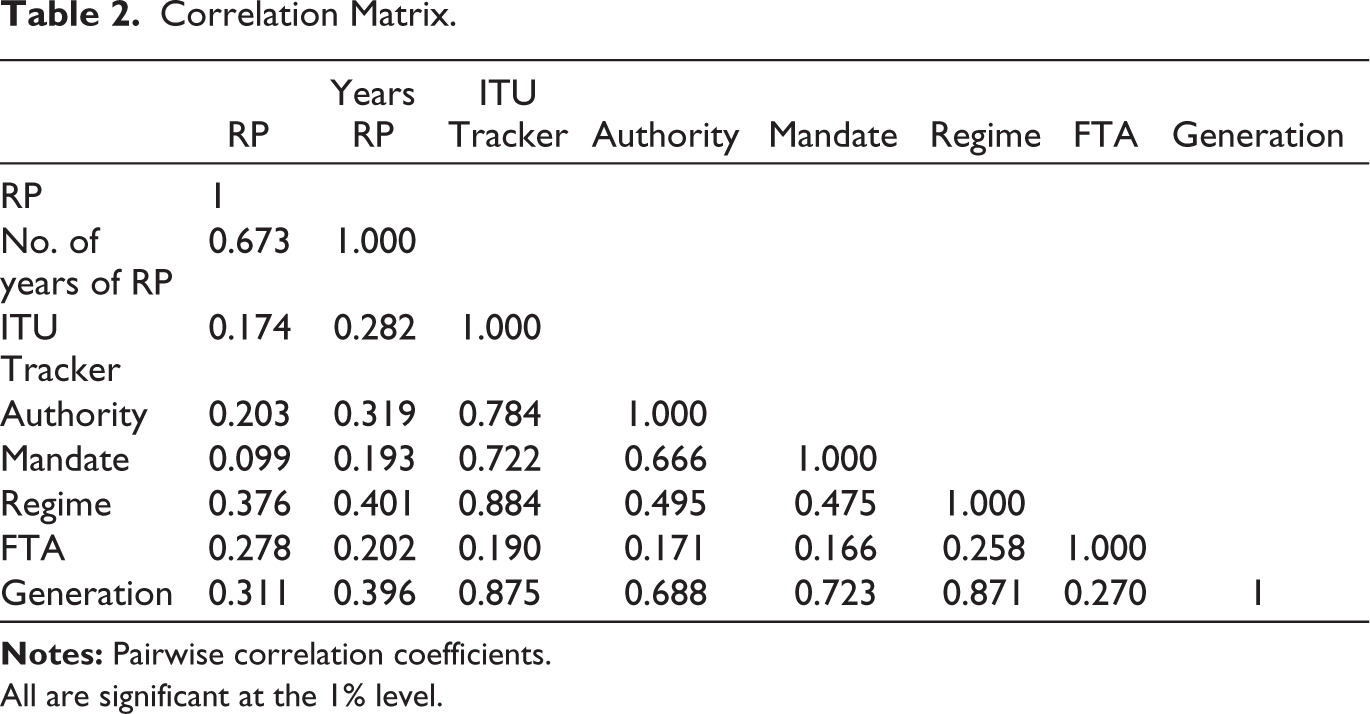

In addition to the RP and the time it has been in place, extracted from the WTO ITIP database, measures of applied pro-competitive policies as captured by the ITU’s Regulatory Tracker are included. The tracker contains information on 50 policy measures organised into four clusters as described above. While the first three clusters capture policy inputs, the fourth focuses on outcomes related to the status of competition in each market segment. Due to endogeneity concerns, the fourth pillar is excluded from the gravity regressions. Based on the Regulatory Tracker, the ITU has also constructed four generations of ICT regulation (command and control, early open markets, enabling investment and access, and integrated regulation). Descriptive statistics are presented in Table 1, while Table 2 depicts the correlation matrix for the explanatory variables.

Descriptive Statistics.

The maximum possible score on the first three clusters of the ITU Tracker combined is 72, where each measure contributes 2 points.

Years covered: 2007–2019.

Correlation Matrix.

All are significant at the 1% level.

We note that more than 80% of the observations score 1 on the RP dummy. There is, however, more variation across time. The average number of years of adoption in 2019, the end of the period, was 19, while the maximum was 24 at that point.

Results

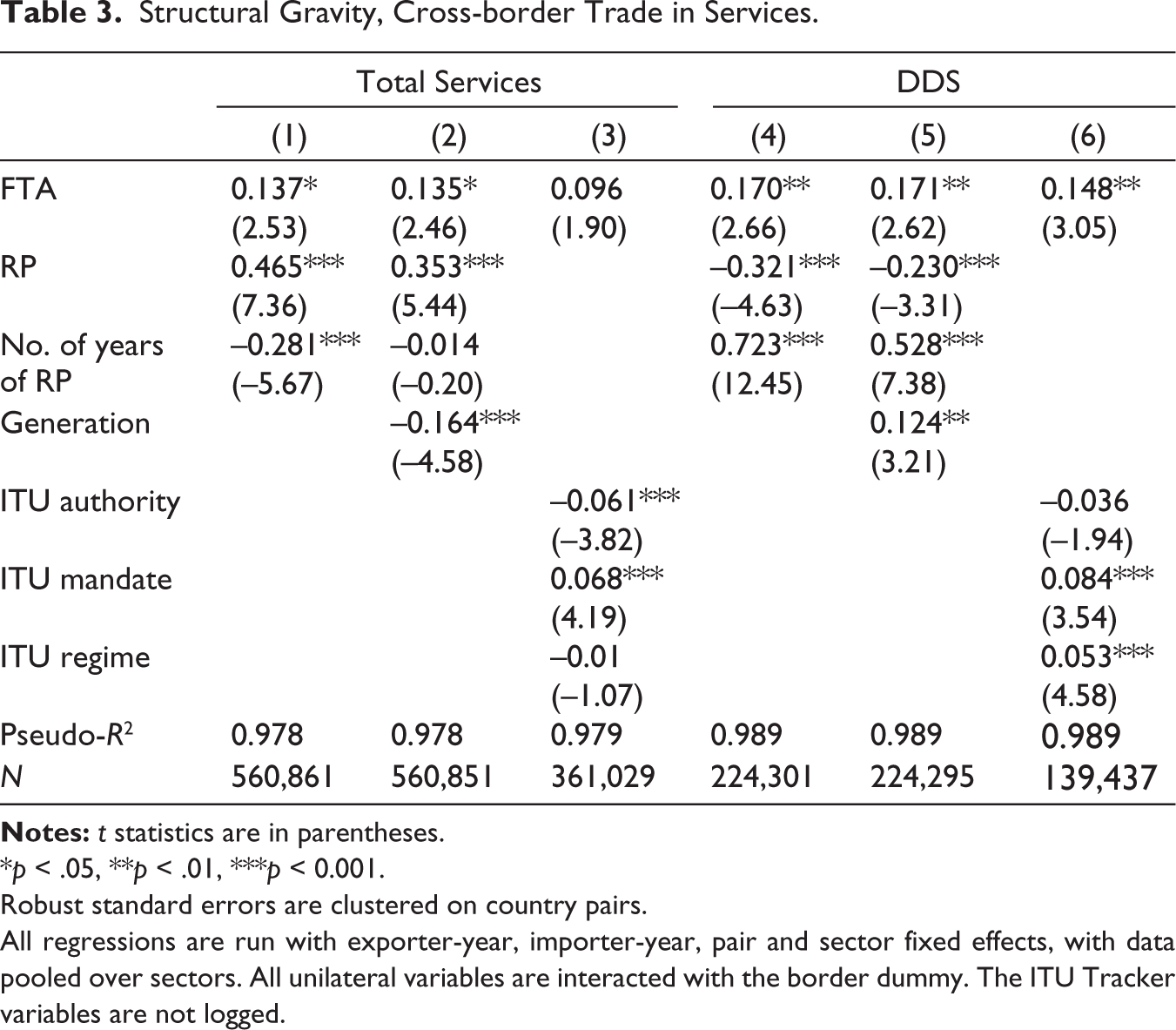

This article first explores the relationship between committing the RP in the GATS and trade in total services, followed by the analysis of applied pro-competitive regulation as captured by the ITU Tracker. With the proliferation of the internet, high-speed broadband and over-the-top and virtual networks, one would expect that the relationship between the RP and services trade weakens over time, while the opposite may apply to the Regulatory Tracker.

The results are presented in Table 3 for total services (Columns 1–3) and DDS (Columns 4–6). Starting with total services, the prediction that the RP is positively associated with trade and the impact diminishes over time is borne out in the analysis. Column 1 indicates that the total services trade is on average about 60% higher when the RP is committed, while the effect drops off by about 3% for every 10% extension of the time the RP has been in force. Translated into years, the coefficient suggests that the impact drops by about 14% after 1 year, 2.8% in the 10th year and 1.8% in the 15th year. 9 Column 2 introduces the generations of ICT regulations, while Column 3 introduces the ITU Tracker by clusters to study applied regulation more granularly.

Structural Gravity, Cross-border Trade in Services.

*p < .05, **p < .01, ***p < 0.001.

Robust standard errors are clustered on country pairs.

All regressions are run with exporter-year, importer-year, pair and sector fixed effects, with data pooled over sectors. All unilateral variables are interacted with the border dummy. The ITU Tracker variables are not logged.

The introduction of the ITU generations does not affect the coefficient on the RP much, but it does render the number of years it has been in place insignificant. This is no surprise since the generations evolve with technology over time and correlates significantly with the years of RP (Table 2). It is, however, surprising that the coefficient is negative and significant. A possible explanation is that graduating to a higher regulatory generation attracts more services affiliates at the expense of trade, which, as we shall see, is weakly supported by the regression presented in Table 4.

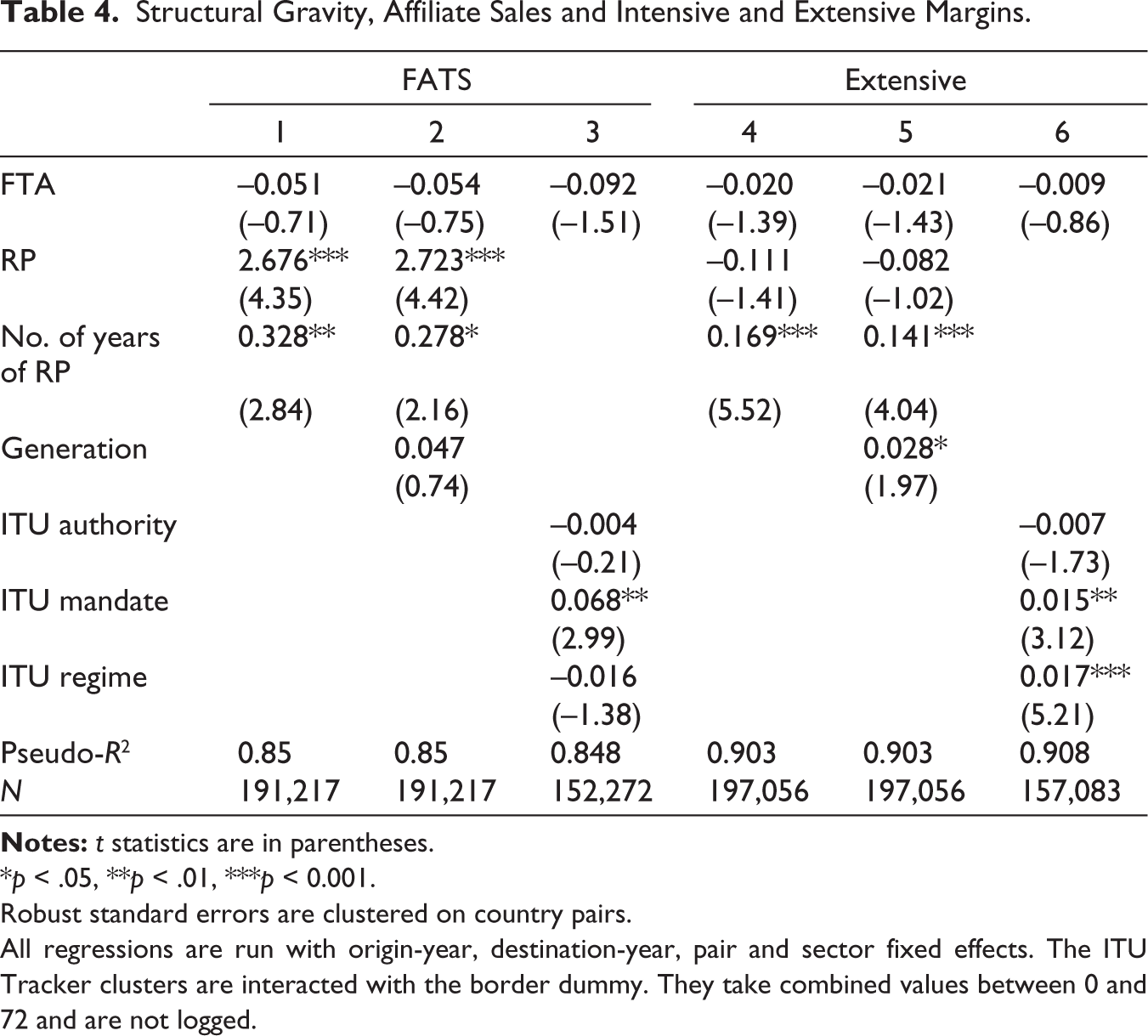

Structural Gravity, Affiliate Sales and Intensive and Extensive Margins.

*p < .05, **p < .01, ***p < 0.001.

Robust standard errors are clustered on country pairs.

All regressions are run with origin-year, destination-year, pair and sector fixed effects. The ITU Tracker clusters are interacted with the border dummy. They take combined values between 0 and 72 and are not logged.

Regulatory authority and regulatory mandate cancel each other out. Recall that all country-specific measures capture the impact of foreign trade and affiliate sales relative to local sales. A reasonable interpretation is thus that a strong and autonomous regulatory authority with stakeholder engagement benefits local firms more than foreign ones, while a broad mandate may be relatively more beneficial for foreign suppliers. The mandate includes, for instance, interconnection obligations and conditions for interconnection, a requirement found in the RP as well.

Turning to DDS (Columns 4–6), they are more sensitive to telecom commitments and ICT regulation than services in general as one would expect. Interestingly, the trade impact of the RP strengthens over time for DDS. The coefficient suggests that the RP is associated with as much as 36% higher DDS trade after 1 year, 7% in the 10th year and 5% in the 15th year.

The ITU Tracker is not included in the same regressions as the RP and the number of years in place because they capture substantially the same policy stance. Each measure in the tracker contributes 2 points to the overall score. The marginal impact on DDS trade of one additional measure is about 17% if in the mandate cluster and 11% if in the regime cluster, while regulatory authority is insignificant. 10

The results for Mode 3, both the extensive and the intensive margins, that is, changes in the number of affiliates and changes in the sales of existing affiliates, are depicted in Table 4. It turns out that DDS is not significantly different from services in general, so only total services are included. The results suggest that the largest effect took place at the intensive margin. Thus, affiliate sales are strongly associated with the RP and the effect has increased over time. Having committed the RP has also attracted new affiliates over time, albeit at a slower pace. Using the post-estimation margins function in Stata reveals that the predicted number of affiliates for the average country pair is 33 in the year the RP was introduced, increasing to 45 after 5 years, 50 after 10 years and 53 after 15 years. 11

When we replace the RP with actual pro-competitive regulation, the effect is limited to the regulatory mandate at the intensive margin, while regime is also significant at the extensive margin. Using the post-estimation function to predict the number of affiliates at different scores on the tracker reveals that the predicted number of affiliates at the mean score of mandate is 47, rising to 51 at the max score. Similarly, for scores under the regime cluster, the predicted number of affiliates at the mean is 52, rising to 59 at the maximum score. The regressions in Mode 3, in other words, suggest that committing to the RP is associated with policies that keep operational costs for foreign affiliates down, expanding the sales of existing affiliates. Attracting new firms, however, relies more on current pro-competitive regulation. Such policies affect establishment costs and hence the extensive margin of Mode 3. 12

We finally note that the FTA dummy is not significant in the Mode 3 regressions. The literature on the relationship between FTAs and FDI is mixed. While a robust positive relationship is found between deep FTAs and FDI stocks (e.g., Kox & Rojas-Romagosa, 2020), others find a negative relationship on North–North investment flows and a positive relationship on North–South flows (e.g., Chala & Lee, 2015). It is beyond the scope of this article to go further into this question, but we note that an insignificant coefficient is not unprecedented in the literature.

A key question throughout this article is to what extent the RP and the applied domestic regulation as captured in the ITU Regulatory Tracker contribute to shifting services trade towards Mode 1. The results from studying cross-border trade and commercial presence separately are mixed. It appears, perhaps surprisingly, that the RP is more important for commercial presence, particularly at the intensive margin, than for cross-border trade.

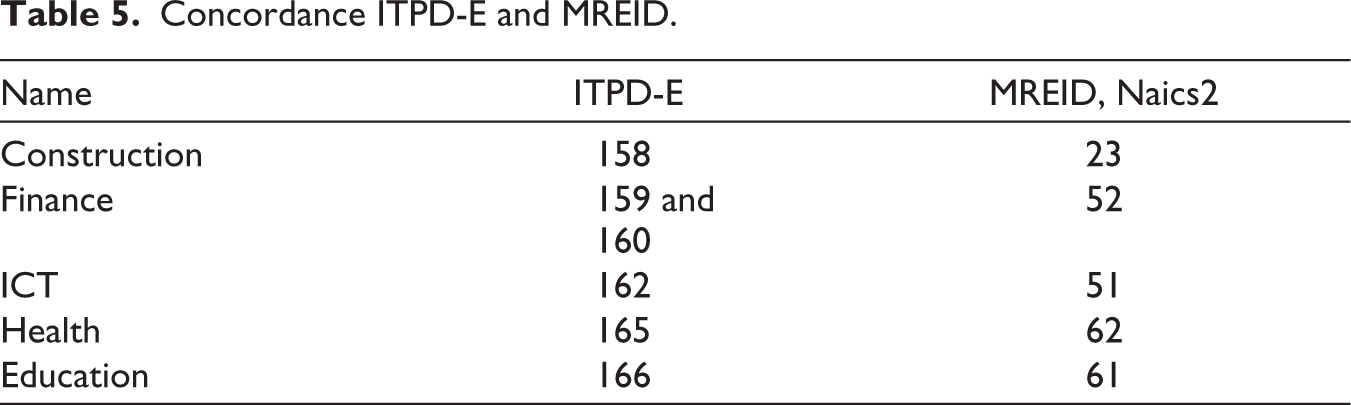

To shed further light on this question, simultaneous equations on cross-border trade and affiliate sales for total services and for DDS are explored. To do this, it is necessary to match the services classification in the ITPD-E to the sector classification in the MREID. Table 5 presents the correspondence applied. It was not possible to match other business services, the largest services category at the two-digit level, which limits the generality of the results from the regressions.

The regression equations are as follows:

Concordance ITPD-E and MREID.

The corresponding equation for affiliate sales has Fats as the dependent variable and trade on the right-hand side; otherwise, it has the same variables. lndist signifies the distance between countries i and j, contig and commlang are dummy variables which take the value 1 if a country pair shares a common land border or a common language and 0 otherwise.

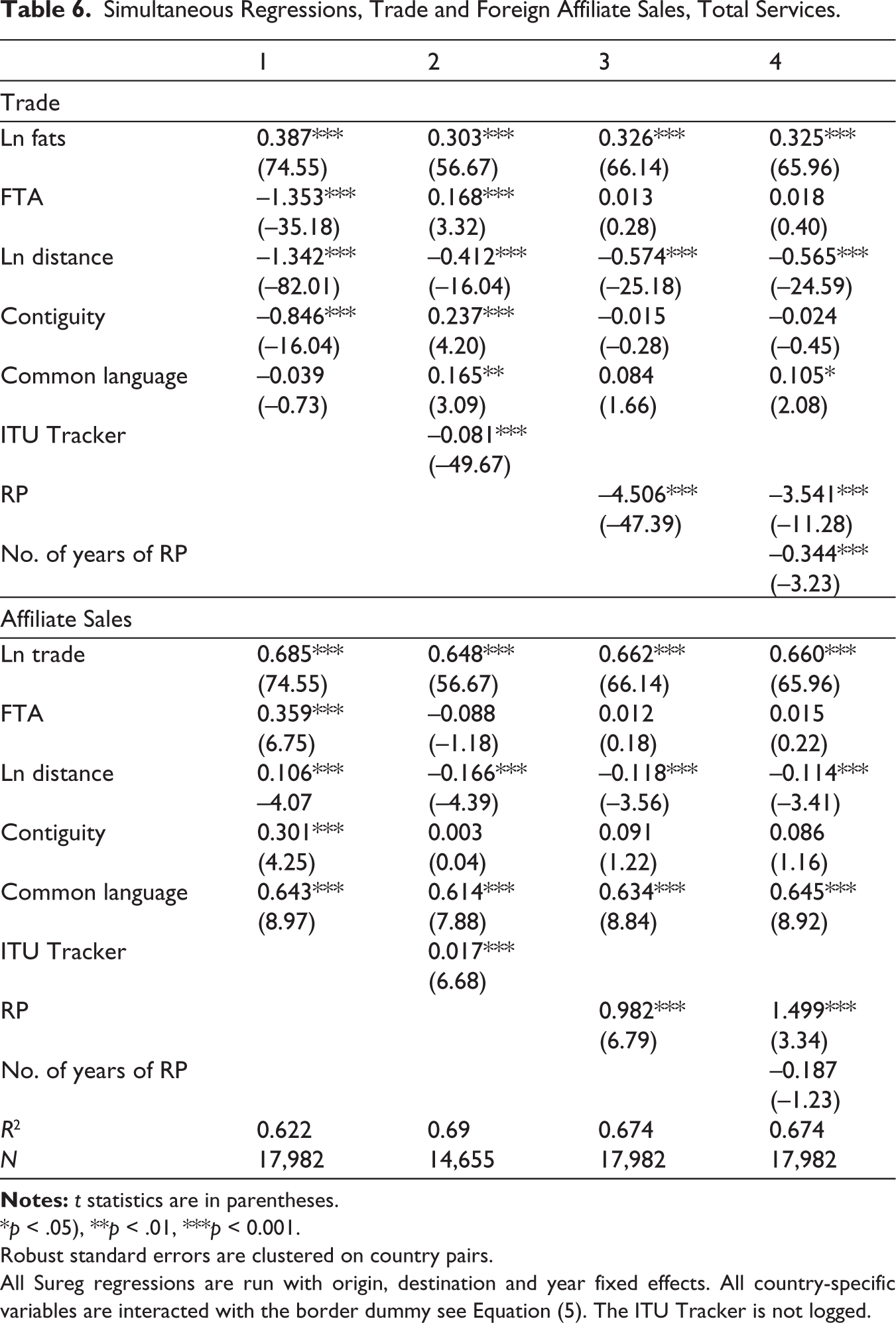

Due to the limited coverage when combining IPD-E, MREID and the ITU Tracker, the number of observations is much smaller than in the other regressions. Results should therefore be interpreted with caution. The simultaneous regressions, however, suggest that Modes 1 and 3 are highly complementary. Thus, a 10% increase in affiliate sales is associated with a 3% increase in trade, while a 10% increase in trade is associated with about 6.5% higher affiliate sales, all else being equal (Table 6). This aligns with previous studies reporting strong complementarities between the modes of supply in services (e.g., Khachaturian & Oliver, 2023). The results also support the above findings that the RP as well as applied domestic regulation in the ICT sector favour FDI over cross-border trade.

Simultaneous Regressions, Trade and Foreign Affiliate Sales, Total Services.

*p < .05), **p < .01, ***p < 0.001.

Robust standard errors are clustered on country pairs.

All Sureg regressions are run with origin, destination and year fixed effects. All country-specific variables are interacted with the border dummy see Equation (5). The ITU Tracker is not logged.

Concluding Remarks

This article has studied the interplay between technology and WTO rules in driving services trade, against the backdrop of the digital transformation of services. Focusing on domestic and multilateral governance of the telecoms and broader ICT sector, it finds that having committed the RP on telecommunications in the early days of the ICT revolution is strongly associated with subsequent services trade in all sectors, and the effect is, somewhat surprisingly, the strongest for Mode 3.

A possible explanation is that making a legally binding commitment to establish an independent regulator tasked with pro-competitive regulation in telecommunications sends a strong signal to markets. Thus, the RP may have been a catalyst for good domestic regulation in telecommunications and the ICT sector at large. Indeed, although only indicative, the article finds a strong correlation between the number of years since the RP was committed and the score on the ITU Regulatory Tracker. As a host of studies and business surveys show, access to high-quality telecommunications and electronic networks is one of the key factors driving investment decisions in any sector, particularly in low and middle-income countries (Mensah & Traore, 2024).

Second, although the quality-adjusted transmission costs of digital products over the internet have come down substantially over time, policy-induced trade costs facing DDS render seamless global digital markets elusive. Thus, commercial presence requirements are quite common in a host of business services and local licenses are often required. Furthermore, among the requirements to obtain a license are typically qualifications obtained locally, experience from local practice and compliance with local standards. 13 Together with other features of services, notably their credence product characteristics, this may render FDI the lowest-cost entry mode in foreign markets (Nordås et al., 2023).

The JIs on e-commerce and services domestic regulation address head-on the regulatory issues that may prevent cross-border trade in DDS from reaching its full potential. Lessons from the RP in the GATS suggest that these two agreements, if widely implemented, could substantially boost services trade through all modes of supply. The sharp rise in services trade after the accelerated digitisation of services during COVID-19 (Figures 1 and 2) illustrates the point.

To conclude, when introduced in 1995, the GATS was considered a framework for further negotiations. Such negotiations did not materialise, leaving the agreement incomplete and increasingly outdated with the rise of the (increasingly artificial intelligence enabled) platform economy. Such technology is blurring the boundaries between sectors, occupations, modes of supply and even the location of production and consumption. To match the realities of current services markets, the GATS needs an architecture less anchored in sector and mode classifications, drawing lessons from recent FTAs and economic partnership agreements.

Footnotes

Acknowledgements

The author would like to thank the editor and two anonymous referees for insightful and useful comments and suggestions.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.