Abstract

The impact of tariff barriers affecting participation in global value chain (GVC) trade has received attention in recent literature. However, the empirical evidence in the context of mega-regional trade agreements, such as the Regional Comprehensive Economic Partnership (RCEP), from which India opted out recently, remains non-existent. Our study contributes to the empirical literature by undertaking an economy-wide modelling exercise, augmenting it to the automobile sector trade in GVC goods in the Indian context. We conduct two policy simulations with an aim to analyse how India’s auto-industry and auto-parts trade, involving forward and backward linkages in GVCs, have been affected by its decision to opt out of RCEP compared to a hypothetical scenario of not doing so. Our results suggest that a potential RCEP membership would have created net trade in both the finished automobile and intermediate auto-parts sectors, although imports would exceed exports. Further, we infer that both backward linkages and forward linkages in this industry will be adversely affected by opting out of RCEP, as there is export diversion in the auto-parts sectors globally, with India facing terms of trade losses due to higher import prices. This informs policymakers that developing domestic resilience and improving productivity are critical for India to improve its long-run export competitiveness while contemplating future trade agreements, including those with RCEP members.

Introduction

The impact of tariff barriers affecting participation in global value chain (GVC)-based trade has been analysed in recent literature, such as Antràs (2020). Simola (2021) notes in the post-COVID context that protectionist pressures have indeed slowed down the growth of GVC-led trade, with even a small tariff having a cascading effect for countries that involve more backward participation or foreign value added (FVA) in gross exports.

Empirical evidence of the above phenomenon in the context of membership in mega-regional trade agreements has been largely non-existent. These include the case of the Regional Comprehensive Economic Partnership (RCEP), from which India opted out in 2019 and which came into force in 2022. Gilbert et al. (2018), Narayanan and Sharma (2016) and Lee and Itakura (2018) have utilised computable general equilibrium (CGE) simulations that examine the impact of mega-regional trade agreements, including RCEP, but not in the GVC context of sub-sectoral tariffs or not just the final goods but also their parts and components.

India’s trade linkages with RCEP members have been an important part of its Act East Policy over the years. As of 2016, India exported goods worth a total of $46 billion to RCEP member countries, constituting a share of 17.6% of its total merchandise exports (United Nations, 2018). Apart from China, Singapore and Vietnam were the other RCEP members among India’s top 10 export destinations during this period. 1 These countries, along with Malaysia, constituted more than half of India’s total exports to RCEP members during the same period.

In contrast, India imported goods worth $130 billion from RCEP members, constituting a share of 36% of India’s total merchandise imports during 2016. China, India’s largest source of RCEP merchandise imports, accounted for $60 billion, or nearly half of the total, followed by the Republic of Korea and Indonesia. 2 India, experiencing a significant trade deficit concerning RCEP members, was therefore likely to be extremely cautious against committing to substantial tariff liberalisation under a formal RCEP trade agreement. The caution is based on the premise that cheaper imports through RCEP will be bad for India’s domestic import-competing producers and generate job losses. However, from the Indian exporters’ perspective, being a part of this agreement would also be providing an opportunity for them to plug into trade involving GVC goods.

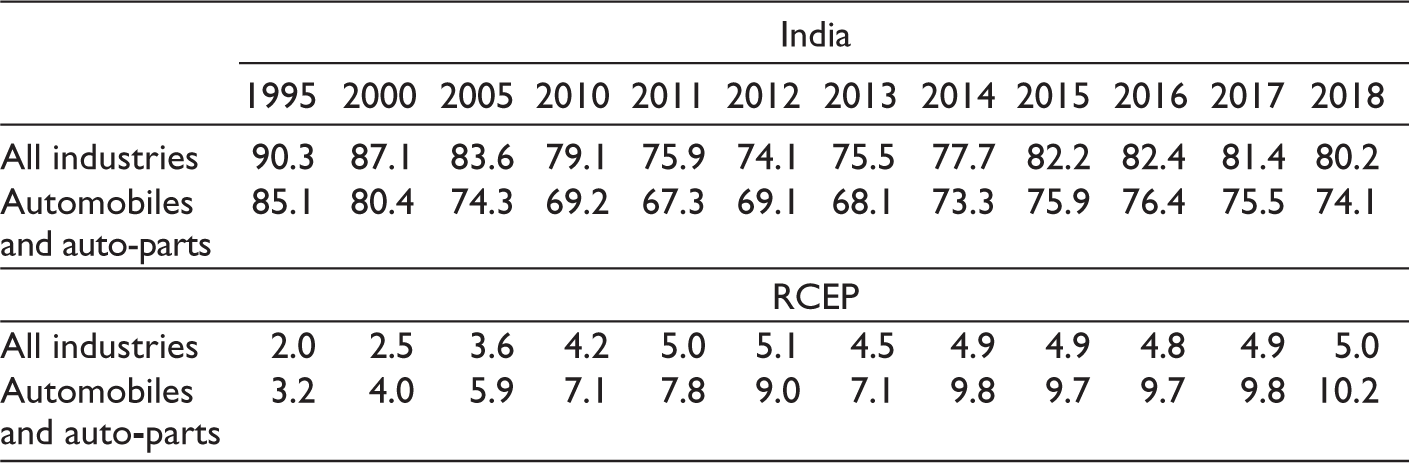

Two facts demonstrate the evidence of India’s increasing involvement in GVC-related trade over the period 1995–2018. First, its share in domestic value-added in its gross exports of all industries has declined from 90% to 80%, while that in its exports of automobiles and auto-parts has fallen more sharply from 85% to 74% over the same period. Second, the share of other RCEP members, most notably China, in India’s value added in its gross exports of all industries more than doubled during the same period, and more than tripled in the case of the automobiles and auto-parts industries only (Table 1). A comparison of recent data over the period 2007–2017, based on UNESCAP (2021), reveals that India’s overall participation in GVCs declined by 2% in terms of its backward linkages and 3% based on its forward linkages, which could be due to existing trade barriers to GVC participation observed by Antràs (2020).

Share of Origin of Value Added in India’s Gross Exports (%).

Based on 2017 data released recently by UNESCAP (2021)’s Regional Value-Added analyser, China, Japan and Australia were among the top five RCEP members contributing to 1.8% of India’s foreign value added (worth $7.2 billion) in its gross exports (backward linkages), while Singapore and China constituted the same, respectively, in terms of forward linkages (wherein 3.6% of India’s gross exports were used in further export production of these countries, contributing to $12.47 billion in their gross exports. Out of nearly $65 billion in gross exports of motor vehicles from India, $10.1 billion (15.5%) was utilised by its trading partners in their exports globally, demonstrating evidence of forward linkages in GVCs. Japan (2.3%), Korea (1%), Indonesia (0.89%), China (0.8%) and Australia (0.6%) were the top four RCEP members in this context. These trading partners contributed a lot more to India’s backward linkages (28%) in the same sector during this period. This suggests that tariff barriers from the Indian perspective, as per Antràs (2020) and Simola (2021), would be detrimental to its GVC participation in the motor vehicle sector.

Removal of trade barriers and costs as per Kowalski et al. (2015) and Antràs (2020) should facilitate the creation of both forward and backward linkages in this industry, thereby boosting India’s exports and domestic production capacity in this sector, which is what we want to check quantitatively through our economy wide modelling framework.

We contribute to the empirical literature by undertaking an economy-wide modelling of policy simulations that utilises 2015 3 baseline data in an updated Global Trade Analysis Project (GTAP) 9 database, augmenting it to study the automobile sector of trade in GVC goods in the Indian context. Our modelling approach first employs the Splitcom tool (Horridge, 2008) to separate the automobile sector from the auto-components sector, using the data on production and trade of these commodities from the United Nations (2018). The standard GTAP model can be utilised to simulate the effect of trade liberalisation in the entire automobile sector only, but not on auto-parts, which are intermediate inputs into the final product. Our augmented model allows us to analyse this. After that, we update the whole dataset to the year 2015, using the data from the World Bank. 4 Our study therefore follows an approach like Dixon et al. (2020) and Aguiar et al. (2021), who more recently also attempted to disaggregate automobile sector in a CGE model, by extending it to GTAP Motor Vehicles (GTAP-MVH), but in the context of North American Free Trade Agreement (NAFTA), and not Asia, including India.

We then conduct two policy simulations. The first scenario, therefore, involves a tariff liberalisation scenario within RCEP members without including India, which represents the current status quo. The second scenario takes a retrospective stance, that is, the scenario of India being in RCEP, assuming it had agreed to eliminate or reduce its tariff barriers for other member countries in this agreement. The key issue that we analyse here is how India’s auto-industry and auto-parts trade (that involves forward and backward linkages in global GVCs, not just in Asia) would get affected by India’s decision to opt out of RCEP compared to not doing so. We specifically analyse the impact on output, prices, trade patterns and overall welfare in the automobile and auto-parts industries, considering tariff liberalization (with and without India).

While we acknowledge that RCEP chapters also focus on trade facilitation and reduction of trade costs that go beyond tariffs, we restrict our analysis to tariff reduction. This is because tariffs have been the most critical and challenging part of negotiating this agreement from India’s perspective, and ultimately the prime reason for its decision to opt out of this agreement in November 2019.

We organise the remainder of this article as follows. The second section reviews the existing literature on trade in GVC goods involving India, including a data overview. The third section analyses the modelling framework and methodology. The fourth section discusses the policy scenarios and simulation rationale. The fifth section explains the results, informing policymakers on the implications of entering mega-regional RTAs for India in the longer term and concluding the article.

Literature Review

Three trade policy channels can facilitate forward and backward linkages in trade in GVC goods involving RTAs. These are: (a) lower or no import tariffs, both at home and in export markets; (b) investment agreements that enhance Foreign Direct Investment (FDI) openness; (c) improved trade facilitation focusing on logistics performance, intellectual property protection and standards, improving institutional quality trade-related infrastructure (Kowalski et al., 2015). Recent literature on GVC trade by Antràs (2020) and Simola (2021) suggests that tariff barriers form an important part of trade costs, and greater barriers could affect GVC participation, especially where FVA is involved. These barriers, from the perspective of downstream trading partners, could also impact production costs upstream and adversely impact forward linkages in trade involving multiple cross-border value chains.

The benefits of participation in (GVCs) have been widely recognised, particularly for developing countries, as it allows countries to benefit from its comparative advantage in creating specialised items or parts and components of final products, generating additional jobs and spillover to local firms through access to technical know-how and contributions to global exports (Nag, 2011).

The theoretical and empirical literature focuses on improving the measurement of value-added trade data, including indicators of participation of countries in GVC-related trade (Johnson & Noguera, 2012; Koopman et al., 2010). OECD-WTO (2022), through its TiVA database, provides an internationally comparable dataset on trade in GVC goods involving 63 economies in 34 industrial sectors. The integration of such data with the global economic model is still evolving in the literature, and there are data limitations in the RCEP context.

Therefore, in the Indian context, empirical work on trade in GVC goods has primarily been from the perspective of intra-industry trade and international production fragmentation involving vertically specialised trade. 5 They have concluded that international production fragmentation in India has been primarily concentrated thus far at the lower end of the value chain. Studies involving vertically specialised trade in Indian manufacturing, including Srivastava and Sen (2015) and Tewari et al. (2015), suggest that the automobile industry has been one of the few sectors in India that demonstrates the emergence of production fragmentation.

While there are many CGE studies analysing effects on non-members in a mega-regional trade agreement, Narayanan and Sharma (2016) relates to impact on India, but in the context of the now-defunct Trans-Pacific Partnership (TPP) agreement. Gilbert et al. (2018), in a comprehensive survey of CGE studies utilising GTAP, based on 2011 as a baseline year, estimated that India would experience a welfare gain to the tune of 0.38% if they joined RCEP in a scenario of tariff liberalisation. They argue that even though the results of these models are dependent on a set of assumptions, these are by and large consistent, and their findings are reasonably robust. Lee and Itakura (2018) considered a scenario of tariff liberalisation in all commodities, except rice, over the period of 2017–2025 using a dynamic version of the GTAP model. They projected that India stands to achieve a welfare gain in the case of joining the RCEP by 0.5%–1.3% in comparison to their baseline projections. None of these studies, however, explicitly focused on the impact of tariff liberalisation, separating automobile and auto-parts industries in the context of an Regional Trade Agreement (RTA).

Modelling Framework and Methodology

The GTAP Model

The CGE analysis and the policy simulation scenarios are hence explicitly focused on the auto-parts industry in India. We utilise the standard GTAP model 6 described in Hertel (1997) with an updated GTAP 9 database for 2015 for this analysis. GTAP 9 Data Base incorporates 2004, 2007 and 2011 reference years for 140 regions and 57 GTAP sectors. This is a static model. Data from the World Bank dataset for 2015 was used for the update of the existing GTAP 9 database. The GTAPadjust tool was used to update the dataset on GDP, consumption, investment, government expenditure, exports and imports for all countries while keeping the balance intact. To keep a zero global trade balance, which does not necessarily happen in any real dataset due to errors, we let the rest of the world’s (ROW) trade adjust to preserve the balance. We employed production data for all countries from the United Nations Industrial Development Organization (UNIDO) industrial statistics. Trade and tariff data are from the ITC MacMAP database. For specific countries like India, China, the USA, Canada, Mexico, Japan and Germany, input–output tables provided details on intermediate consumption and final demand. For other countries, we assume an average structure in terms of value shares and not absolute values, for developing and developed countries separately.

Our study involved a 58 sector 7 and 23 region aggregation of the original GTAP 9 database, with skilled and unskilled labour further disaggregated into five more factor endowments. We left the sectors disaggregated in our database to capture the output impact on all sectors of the economy because of joining RCEP compared to opting out of it, although our prime focus remains on the automobile industry and parts sector only. The regional aggregation of 23 regions consists of India, 14 RCEP members 8 and its other major trading partners. These include Bangladesh, Sri Lanka, Latin America, NAFTA members, Chile and Peru, EU-25, ROW, as well as other less developed countries (LDCs), for whom India already has eliminated tariffs on auto-parts, as a regional grouping. 9 We separate the motor vehicles sector (corresponding to mvh code in GTAP) into finished automobiles (from now on referred to as MotorVeh) and automobile parts (after this referred to as MotorVehParts or auto-parts) in our model, respectively, and disaggregate all the other sectors. 10

We use the Splitcom tool to split the automobile sector into automobiles and auto-parts, preserving the balance and other elements of the data and model unaffected, following Narayanan and Khorana’s (2014) approach to sectoral disaggregation in a CGE model. 11 In the case of the Indian auto industry, ours is the first attempt to employ this tool in this context and constitutes one of the methodological contributions of our article.

Finally, the standard GTAP closure is updated as follows: First, we fix trade balances for all regions except EU-25, NAFTA and Japan. Second, we consider the assumptions of unemployment for all disaggregated categories of skilled and unskilled labour in all countries modelled. The altered closure ensures that our simulations reflect a more realistic scenario of the labour and trade balances in our model. 12

When tariffs or import taxes are changed in a GTAP model, the relationship that links their effects in terms of trade creation (expansion effect) and trade diversion (substitution effect) can be stated through equation (1)

where qxs (i, r, s) and pms (i, r, s) are percentage changes in quantities and prices of bilateral imports of commodity ‘i’ from region r to region s and qim (i, s) and pim (i, s) are percentage changes in total quantities and prices of aggregate imports of commodity ‘i’ by region s, respectively. ESUBM (i) refers to the (Armington) elasticity of substitution among imports from different sources for commodity ‘i’.

The first term, qim (i, s) in (1), captures the extent of trade created overall due to tariff reduction, while the second term captures the substitution between different sources of imports due to the price differential between the exporter and the importer.

As discussed in an earlier version of this study by Narayanan et al. (2019), in the GTAP model, changes in bilateral import prices are driven by changes in tariffs and costs, insurance and freight (CIF) prices of imports from the source country. Equation (2) shows this relationship, wherein tms (i, r, s) and pcif (i, r, s) are percentage changes in tariffs and CIF prices of bilateral imports of commodity ‘i’ from region ‘r’ to region ‘s’:

The results for exports and imports are therefore interpreted in terms of these price linkages in (1) and (2).

In the GVC context, we are further interested in analysing the changes in domestic and FVA in total gross exports, as well as the price linkages therein. The domestic value-added changes are provided by the changes in the variable qfd in the model for both automobiles and auto-parts pre- and post-simulation, which denotes the quantity of domestic tradable i demanded by sector j firm in region r. To estimate the value changes as a proportion of gross exports, we estimate the value changes in this variable as a share of output changes, and then apply these proportions to the gross exports changes (qxw) in the model. For FVA, we follow the same procedure but use the GTAP variable qfm, that denotes the quantity of imported tradable i demanded by sector j firm in region r.

The price changes in the GVC due to being a part of RCEP or opting out of it are analysed by comparing the changes across the key price variables in the model (pxw and pim) that denote export prices (constituting domestic prices) and import prices, respectively. These are analysed specifically for the automobile GVC only.

Choosing the Tariff Shocks

In modelling our choice of tariff shocks, we compare most-favoured-nation (MFN) and preferential tariff rates under recent regional Free Trade Agreements (FTAs) for India and four other developing country RCEP members in automobile parts whose MFN tariffs were also non-zero. Such comparison ensures that our choice of tariff shocks is consistent with what is already agreed at the Harmonised System (HS) product classification in other FTAs involving RCEP members.

Appendix 1 presents this data for India, Indonesia, Malaysia, Thailand and Vietnam. 13 We note at the outset that India has agreed to reduce or eliminate tariffs in auto-parts only for eight HS six-digit codes in the ASEAN-India FTA (AIFTA). However, they have been higher than non-MFN preferential rates accorded to India by ASEAN members, for example, Thailand under the same FTA, in one product category, HS870840 (Gearboxes and parts), and lower in another, such as HS870870 (Wheels and their parts). 14

Seven of the RCEP members, that is, Australia, Brunei Darussalam, New Zealand, Japan, Malaysia, Singapore and Vietnam, have already agreed to eventually eliminate tariffs under the CPTPP agreement. Vietnam agreed to a 0.5%–2.5% annual phased tariff cut in this agreement, entirely removing tariffs to zero in the thirteenth year of its enforcement.

The base simulation, therefore, assumes that tariffs on imports of all commodities, including automobiles and auto-parts, have been substantially reduced among RCEP member partners that currently do not include India. We compare this with a hypothetical scenario of India signing on to this agreement.

Policy Scenarios and Simulation Design

Tariff Liberalisation in RCEP Without India (RCEP-14: Scenario 1)

This scenario simulates an RCEP-14 RTA that substantially eliminates tariffs on imports of all tradable commodities within RCEP members except India upon entry into force. One reason why the model may not solve for complete tariff elimination is that it represents several small countries (and hence small bilateral trade flows). So, we chose an 80% tariff reduction for all countries except Cambodia for whom the reduction is 40%. This allows the model to converge, although this scenario can be inconsistent with Article XXIV of the WTO. We feel this is realistic, given a range of sensitive sectors across the board in the RCEP agreement for India, automobiles and auto-parts being one of them. As this is the current status quo scenario for India, we are interested in analysing the counter-factual scenario, that is, would the economic impact have been different if India had signed onto it?

Tariff Liberalisation in RCEP Including India (RCEP-15: Scenario 2)

This repeats the policy simulations under scenario 1, now analysing RCEP-15 that could have included India. This allows us to directly compare how output and trade volumes changed as India decided to opt out. As it is a static model updated for a pre-pandemic scenario, it does not consider any future interactive effects of the COVID-19 pandemic induced shock on any of the original RCEP members.

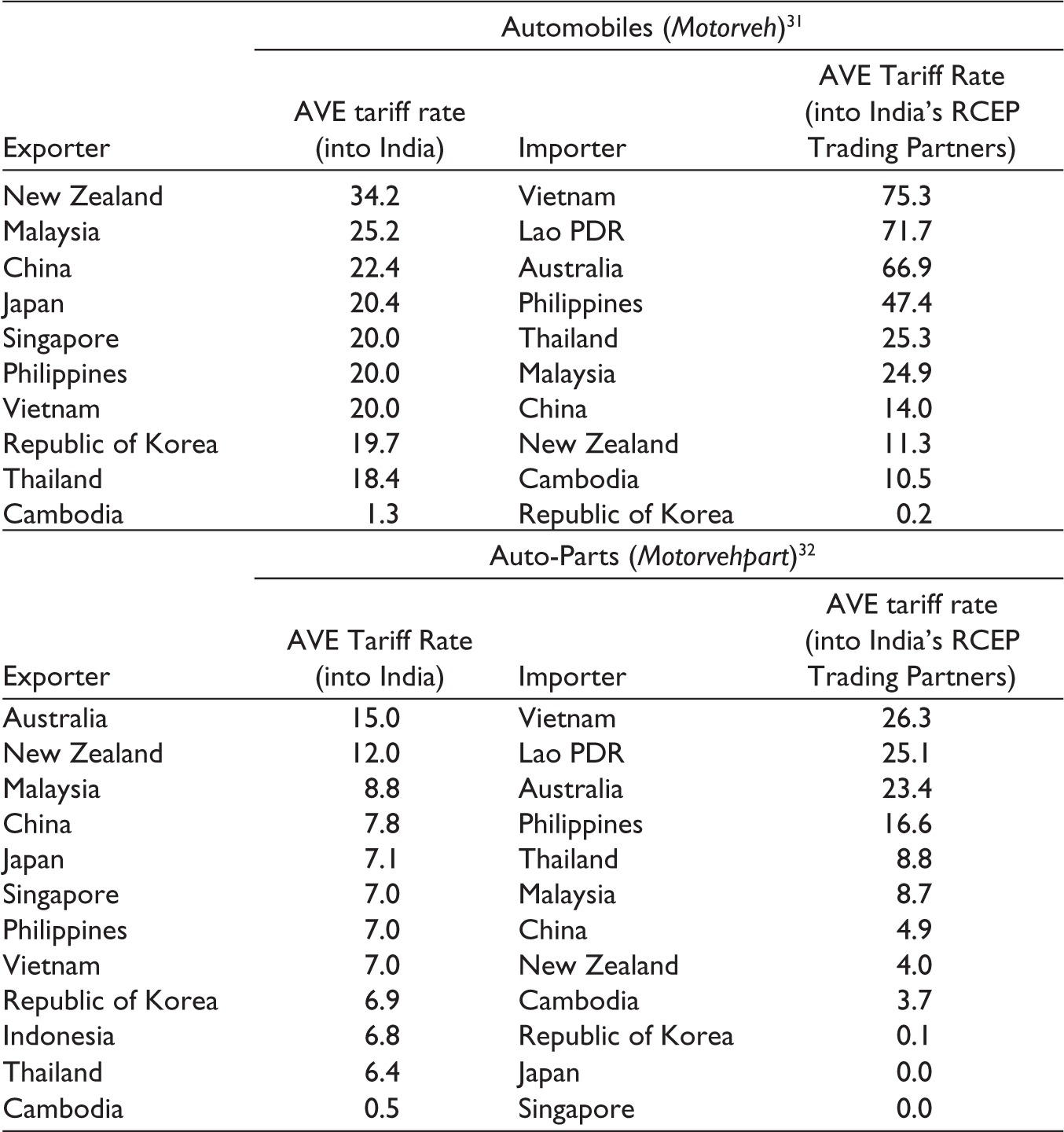

The initial ad-valorem equivalent (AVE) tariff at the final goods sector, that is, automobiles (Motorveh), and the disaggregated intermediate goods sector, auto-parts (Motorvehpart), for India’s exports to and imports from RCEP members constructed from the updated GTAP database of 2015, based on the Splitcom tool, are both presented in Table 2. Macmap HS-6 tariff classifications are the source of GTAP tariff data, and they are calculated on a bilateral import-weighted basis. It converts all non-ad-valorem specific tariffs into their ad-valorem percentage equivalent, first taking a trade-weighted average duty of each subsector for each trading partner and then averaging it over all trading partners, following Plummer et al. (2011). Hence, even if applied MFN or AVE tariffs are high, a negligible or low volume of bilateral imports of automobiles or auto-parts will translate to a very low tariff incidence on an import-weighted basis. 15 India’s current import tariff barriers are higher in automobile and auto-parts sectors for imports from six RCEP members. These are China, Japan, Malaysia, Korea, New Zealand and Singapore.

Baseline Ad-Valorem Equivalent (AVE) Tariffs of RCEP Members vis-à-vis India in Automobiles and Auto-Parts (%). 30

We expect that if these AVE tariffs go to zero for RCEP-14 members, 16 assuming no changes in productivity growth as of 2015, India would likely witness a decline in imports of automobiles and auto-parts from these countries. Domestic production will substitute for imports, thereby protecting Indian automakers and parts manufacturers, but adversely affecting the backward linkages in this sector’s GVC. Export reduction from opting out of RCEP can have negative ramifications for India’s forward linkages in this GVC of this industry, potentially reducing the former’s use of India’s export production for final demand globally beyond RCEP members.

Results

For each simulation scenario, we analyse the microeconomic impact in terms of percentage changes in output, exports and imports in automobile and auto-parts sectors. Macroeconomic impacts are analysed through welfare changes (in terms of equivalent variation [EV] as measured by GTAP). This is the amount of money consumers in each of the analysed regions would pay instead of responding to changes in prices and quantities due to the simulation scenarios. The sources of these welfare changes, including those in terms of trade, are further analysed.

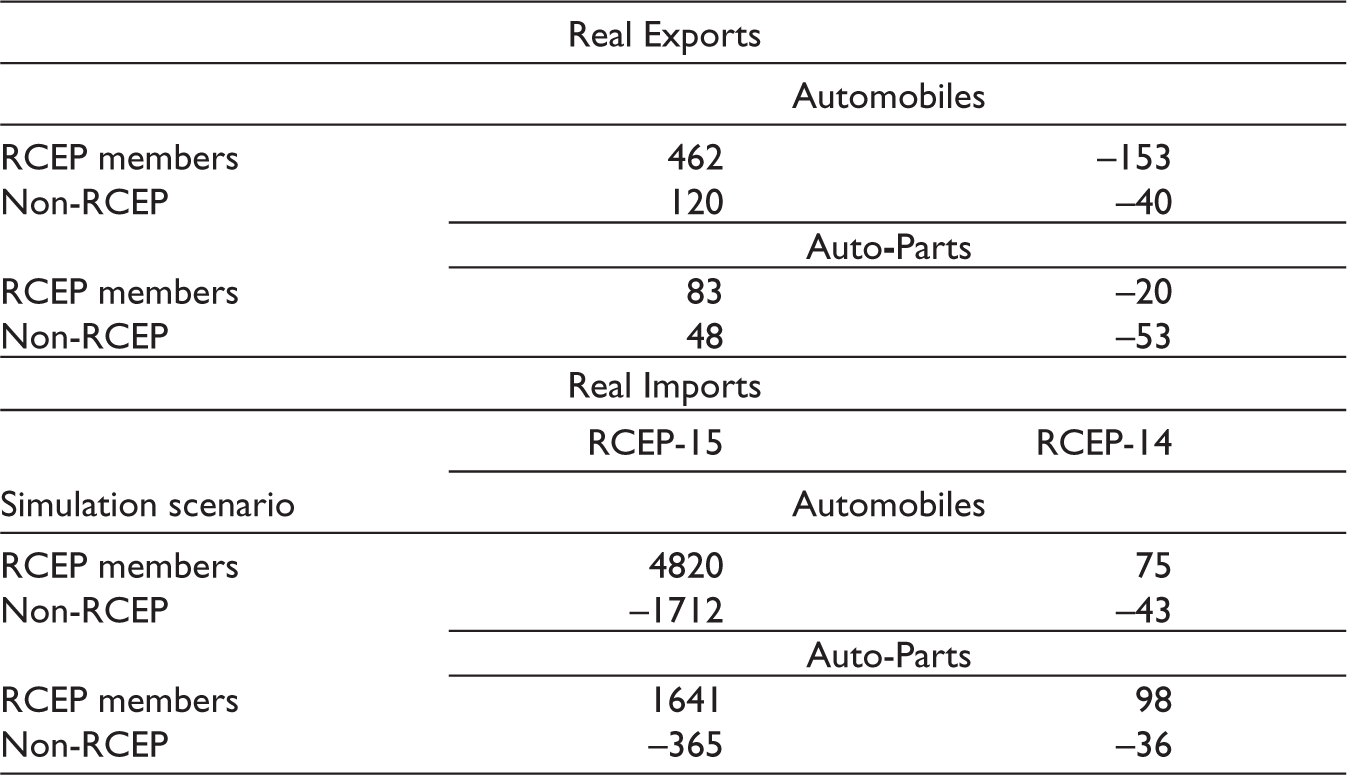

As India’s real import and export volumes changes among RCEP and non-RCEP members due to the model experiment scenarios, our model also ascertains whether these changes result in this trade agreement being net trade creating. We determine whether RCEP in auto-parts is net trade creating or diverting for India by comparing the change in its real imports and exports from/to its RCEP partners with the same from non-members of RCEP (Table 3). An agreement is net trade creating if increase in exports and imports from within the RCEP members exceed the loss in the same from non-members, and trade diverting otherwise. All reported results are medium term estimates as we utilise a static CGE simulation.

Changes in Real Trade Volumes of Automobiles and Auto-Parts for India with RCEP Members and Non-members (US $ Million).

The impact of the two simulation scenarios on quantity changes in exports, imports and on prices of both the automobile and auto-parts sectors is reported in Appendix 2. Figures 1–5 summarise these results in terms of a net change from a RCEP-14 (out) to an RCEP-15 (in) scenario.

RCEP-14 (Scenario 1)

India’s global exports of automobiles are expected to decrease by 6.7%, while those of auto-parts are expected to decrease by 3.6%, as India is not likely to receive preferential tariff treatment for its exports to other RCEP members. Bilateral exports decrease to all regions except Japan and Singapore for automobiles and parts and to Korea for auto-parts only, suggesting a loss of export competitiveness due to trade diversion. These simulation results provide evidence of the fact that tariff barriers for India in RCEP-14 scenario increases its trade costs for GVC-related exports of auto-parts.

India’s global imports of automobiles are expected to increase by 0.2%, while those of auto-parts are expected to go up by 0.4%, as India does not reduce import tariff barriers for RCEP.

A net trade creation exists, despite existing cascading tariff structure in this sector for India, making it inevitable that exports suffer to both RCEP and non-member countries. As other RCEP members reduce tariff barriers in auto-parts and India does not, an export diversion impact is observed in such a situation, potentially affecting the forward linkage flows within the GVC of this industry as exports to the EU and North America, key participants in this stage, decline. Opting out of RCEP, while protecting the domestic automobile and parts manufacturers, adversely affects its global export competitiveness.

A tariff liberalisation in RCEP-14 without India hurts eight RCEP members, including India, in terms of a decline in domestic output of automobiles and auto-parts, respectively. These do not include major RCEP members that are strongly linked to automobile industry GVCs such as Japan, Thailand or Korea. For India, opting out of RCEP protects its automobile and parts industries, generating a net increase of 3% in domestic output, compared to being a member. Korea, Japan, Vietnam, Thailand, the Philippines and Singapore gain the most in terms of the increase in domestic output of automobiles and auto-parts in such a situation.

Decomposition and evaluation of the industry demand equations in GTAP reveal that the share of domestic demand is about 90%. In the case of automobiles, this share is much higher at 93.4%. Given this is the highest for India among its RCEP members, a significant impact is expected on its domestic demand for both automobiles and auto-parts. This, in turn, is expected to impact domestic value added (DVA) in gross exports and therefore GVC participation.

To estimate the above quantitatively, we need to account for both FVA that measures backward participation, that is, imported intermediate inputs used in exports and DVA in gross exports (DVX) that constitutes a part of the measure of forward participation. The latter refers to domestic production used in importers’ exports to a third country. While backward participation can be directly estimated through the changes in qfm in the GTAP model and its share in gross exports, forward participation cannot be directly estimated in the standard GTAP model as that constitutes six different components of DVA as analysed by Wang et al. (2017) and requires detailed information on the use of exported intermediate inputs in the importing country.

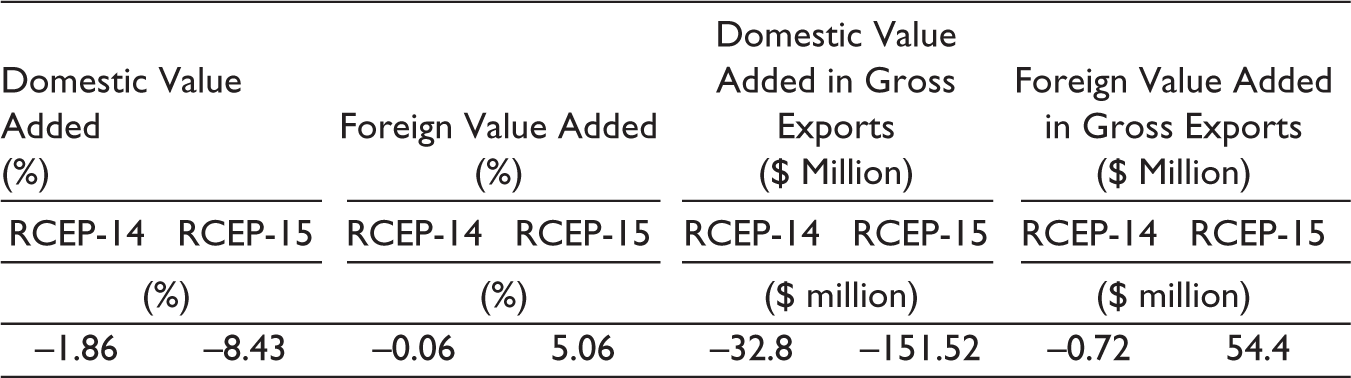

We attempt to estimate the GVC impact on both automobile and auto-parts sectors if India remains out of RCEP (the status quo). The methodology is discussed in detail (please see first part of the third section). The results are reported in Table 4. DVA of auto-parts as a share of automobile exports (DVX) declines by $33 million, with DVA of auto-parts in the finished automobile sector for final consumption declining by $73 million (1.9%). In contrast, as tariffs are not reduced for imported automobile parts under this scenario, FVA in the same declines only by $0.7 million.

Estimated GVC Impact of Changes in Auto-Parts Input into Automobiles Sector.

In terms of tracking price changes in the GVC, domestic prices fall only by 0.2%, while import prices fall by 0.5–0.7. These price changes of a small magnitude are expected as tariff barriers remain for India’s import partners in RCEP, but world prices decline due to tariff elimination among RCEP-14.

RCEP-15 (Scenario 2)

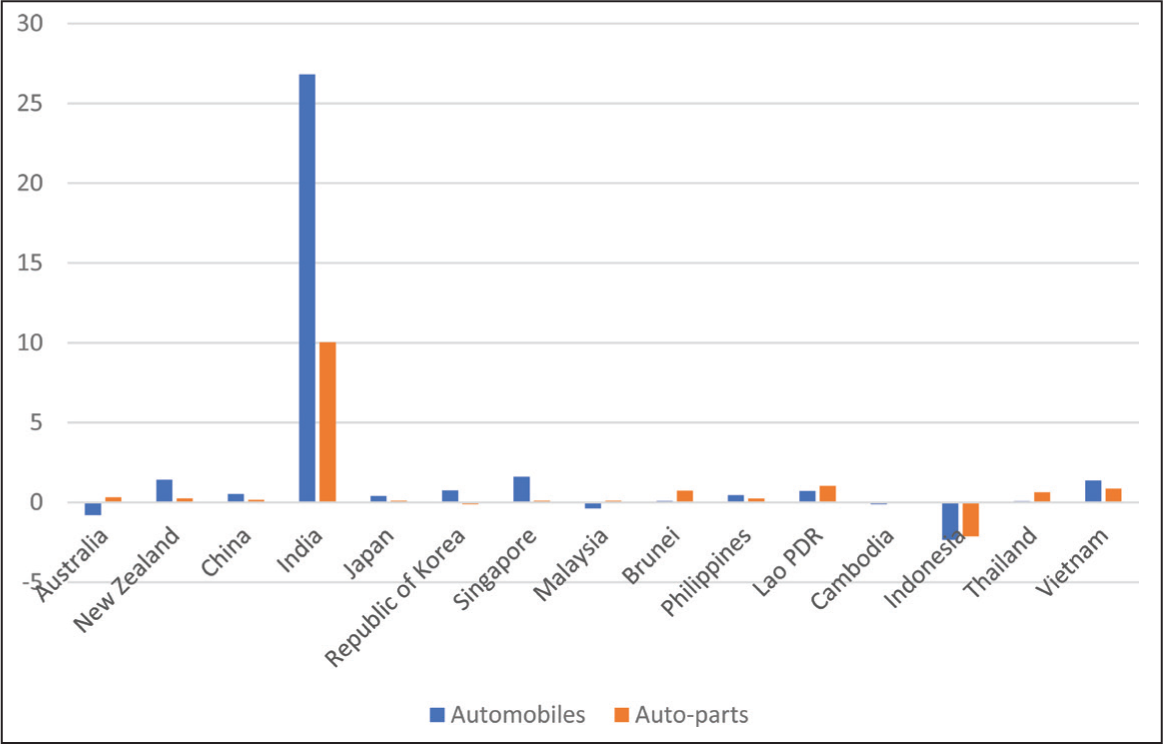

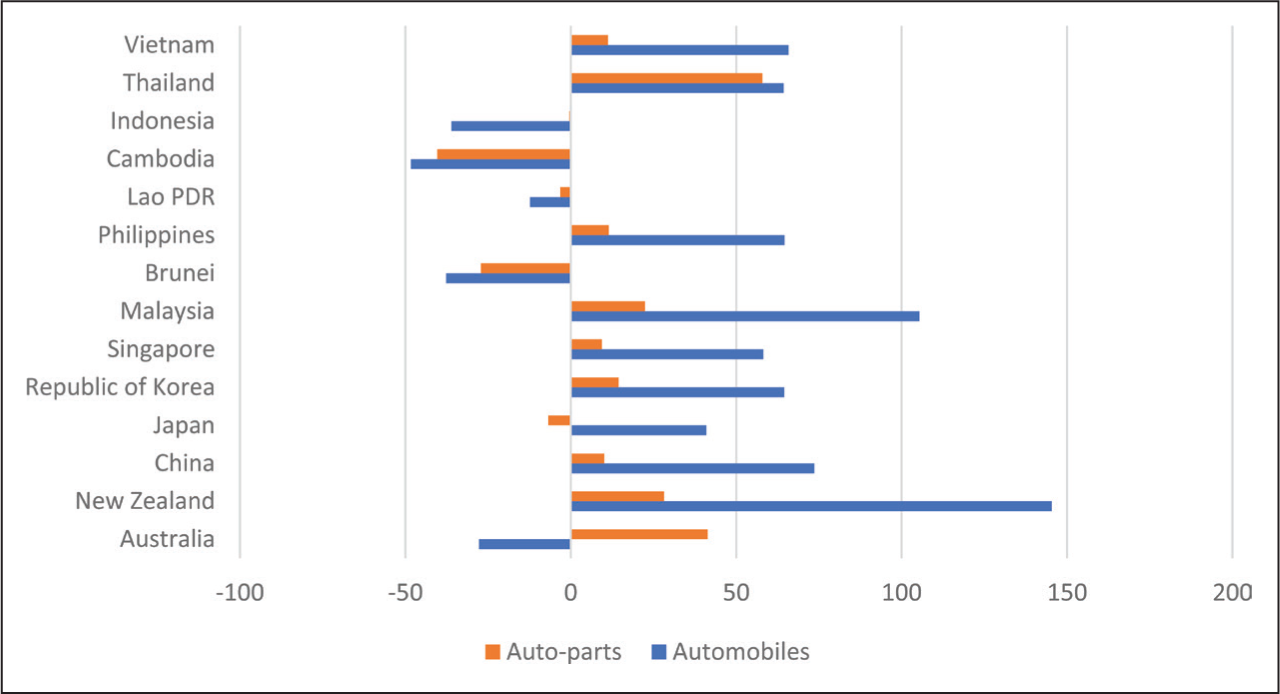

If India had joined, then under RCEP-15, exports would have increased in net terms substantially by nearly 27% for automobiles and 10% for auto-parts, respectively, compared to scenario 1. Other RCEP members would also record a net increase in their exports of both automobiles and parts, apart from Indonesia (Figure 1). Aggregate exports recorded fifth highest increase for India among all RCEP members in the case of auto-parts (after Thailand, Vietnam, Republic of Korea and Singapore) and third highest (after Japan and Republic of Korea, respectively) in the case of automobiles in such a scenario (Appendix 2).

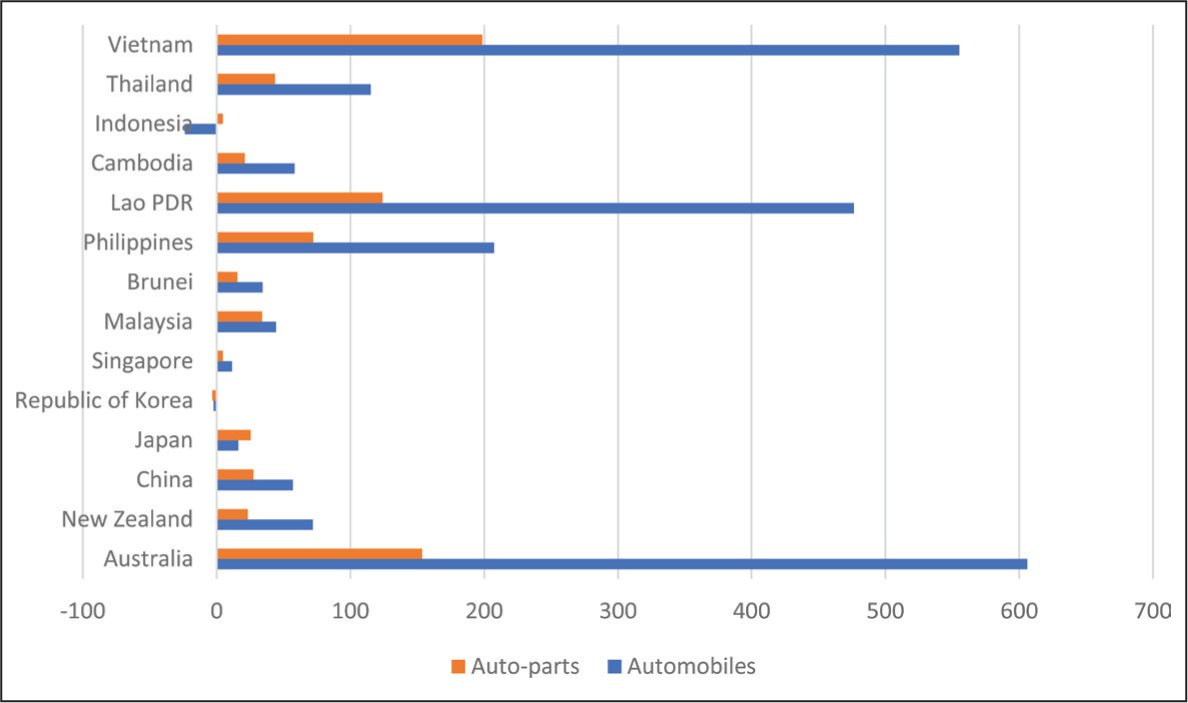

India’s bilateral exports in the automobile sector increase to all regions due to tariff reductions in RCEP-15 compared to India opting out, as expected a priori by theory (Figure 2). The magnitude of change in net exports is largest in case of India’s automobiles and auto-parts exports to six RCEP members, all of whom experienced the largest decline in market prices (pms) from India (Figures 3 and 4). These are Vietnam, Lao People’s Democratic Republic (PDR), Australia, the Philippines, Thailand and Malaysia, respectively. The results are also reflective of potential gains for India in an upcoming Economic Cooperation and Trade Agreement (ECTA) with Australia that includes tariff elimination on automobiles.

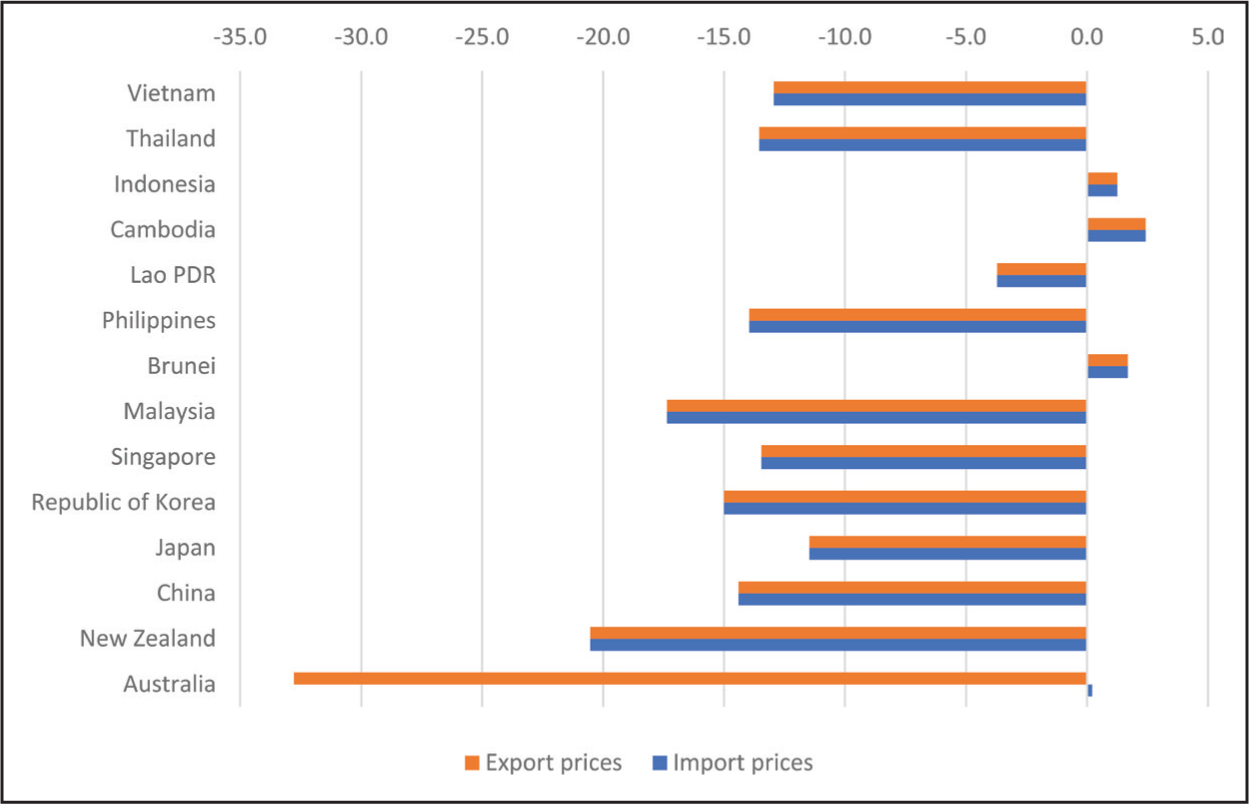

Tracking the sources behind these changes in export demand, it is noted that if India, being a small player in the world market in this sector, had joined RCEP and reduced tariff barriers, increase in its export demand for India would have been driven by a strong positive substitution effect from all RCEP partners. In particular, tariff liberalisation in auto-parts from India would have lowered market prices (pms) in Vietnam, Lao PDR, and Australia by nearly 17%, in the Philippines by 12.5% and in Malaysia and Thailand by nearly 8% (Figure 4), among others. Market price of composite imports (pim) in India under scenario 2 would have declined by nearly 9% for automobiles and by 6% for automobile parts. If India opts out, these fall only by 0.53% and 0.75% for automobiles and automobile parts, respectively. Given the higher tariff barriers in India and its low base of bilateral export volumes in finished automobiles pre-RCEP, it is not surprising to observe this translating into export growth under an RCEP-15 scenario.

Imports would have increased in net terms substantially by nearly 19% for automobiles and 7.3% for auto-parts, respectively. These estimates suggest that if India were to not opt out of RCEP, net export would be greater than imports in both industries.

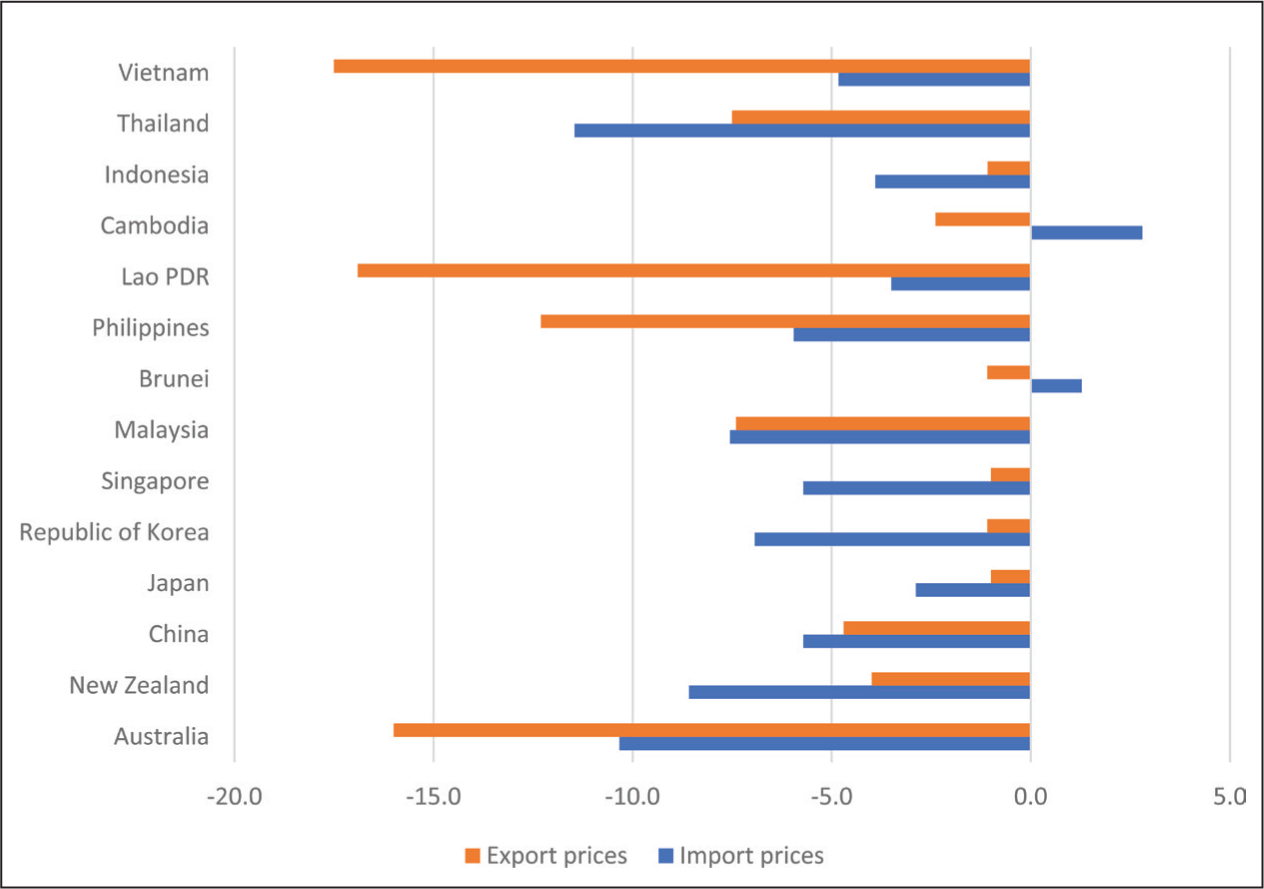

Analysing trends in region-wise changes in net bilateral imports of automobiles and auto-parts into India in Figure 5, India not opting out of RCEP leads to: (a) a higher import demand in automobiles than auto-parts; and (b) greater import competition in case of India’s auto-parts imports from Thailand and Malaysia among ASEAN members. Why does this happen? Export demand into India is driven by expansion effect from these countries as tariff liberalisation in auto-parts into India lowers market prices (pms) from them (Figure 4).

Comparing the changes in bilateral exports and imports of automobiles from and into India by RCEP members, two trends emerge. First, if India had been in RCEP for both automobiles and auto-parts, it could have achieved a greater net bilateral export growth compared to imports in only seven RCEP member countries. These do not include members who are major players in trade in GVC goods in the automobile industry in Asia, such as Japan, Republic of Korea, China, Malaysia, Singapore or Thailand. Second, for auto-parts industry, all RCEP members except Thailand, Korea, Singapore and New Zealand witness a net bilateral export increase from India as bilateral trade costs reduce. This is likely to facilitate GVC trade both upstream (imported auto-parts used in automobiles exported from India) and downstream (exports of India made auto-parts used in automobile exports from RCEP members globally).

The results obtained in Table 3 suggest that RCEP-15 will be net trade creating for India in the case of both the automobiles and automobile parts sectors, but is more likely to increase trade deficit with net real imports higher than those of exports. EU-25 is the RCEP non-member that suffers the most in form of trade diversion in terms of real imports. Entry into RCEP would have had an adverse effect on the overall automobile industry, as confirmed earlier in the empirical literature. 17

In terms of output changes, if India had been in RCEP, only five commodity sectors would have shown a decline in their domestic output growth, with that in automobiles and automobile parts decreasing by 3.6% and 4.3%, respectively. 18 This shift suggests that opting out of RCEP and sticking to protectionism is more likely to adversely affect a greater number of domestic producers at the macroeconomic level due to trade diversion.

Our analysis reveals that the decline in domestic demand in automotive parts and automobiles (by –4.92% and –4.91%) due to RCEP-15 outweighs expansion in export demand (0.61% for automotive parts and 1.33% for automobiles). The drivers are a strong decline in industry demand for domestic intermediate inputs, substituted by the same for imported intermediate inputs. The reduction in supply price of auto-parts in India is 0.21% if it opts out of RCEP compared to 1.25% if it had not, while that for automobiles is 0.23% compared to 1.43%. This explains why the protection accorded in an RCEP-14 scenario reduces the magnitude of decline in domestic output compared to if it had been taken away under RCEP-15.

What about job losses in both scenarios? Analysing the changes in demand for endowments used in finished automobiles and parts industries in our model, the estimates suggest that this declines across skilled and unskilled labour by about 2.8% and 3.5%, respectively, if India joins RCEP. This demand is still on a decline, although to a lesser extent in the range of 1.1%–1.4%, respectively, in both industries if it does not join the agreement. These simulation results indicate that opting out of RCEP prevents some job losses from import competition, but the adverse impact on export competitiveness continues to affect job creation, affecting both backward and forward linkages in the GVC trade, as argued also by Dixon et al. (2020).

The GVC impact on both the automobile and auto-parts sectors if India re-joined RCEP shows that DVA of auto-parts in automobile exports would have decreased by $151.5 million, with DVA of auto-parts in the finished automobile sector declining by $390 million (8.4%; Table 4). This is expected given the sharp decline in overall domestic demand for auto-parts observed in this scenario. In contrast, as tariffs are reduced for imported automobile parts under RCEP-15, FVA by this sector in final automobile sector increases by $54 million. Note that some of this could be part of the DVA that returns home through the importer’s exports back to India, facilitating forward participation as well.

In terms of tracking price changes in the GVC due to joining RCEP, domestic prices fall by 1.4%, while import prices fall by 9.2%. The significant drop in import prices results from the greater tariff cuts that India must undertake in this scenario compared to other RCEP members. The effects of these price changes on overall terms of trade are discussed in detail in Table 6 (see fourth part of the fifth section).

Welfare Effects and Changes in Gross Domestic Product (GDP)

The changes in overall welfare and the source of those welfare changes are analysed through the welcome decomposition analysis described by Huff and Hertel (2001) and Hanslow (2001). The region-wise changes in welfare are measured in money metric in terms of changes in EV in the post-shock compared to the pre-shock period. A priori, by theory, we expect members of an RTA to gain, with non-members expected to lose.

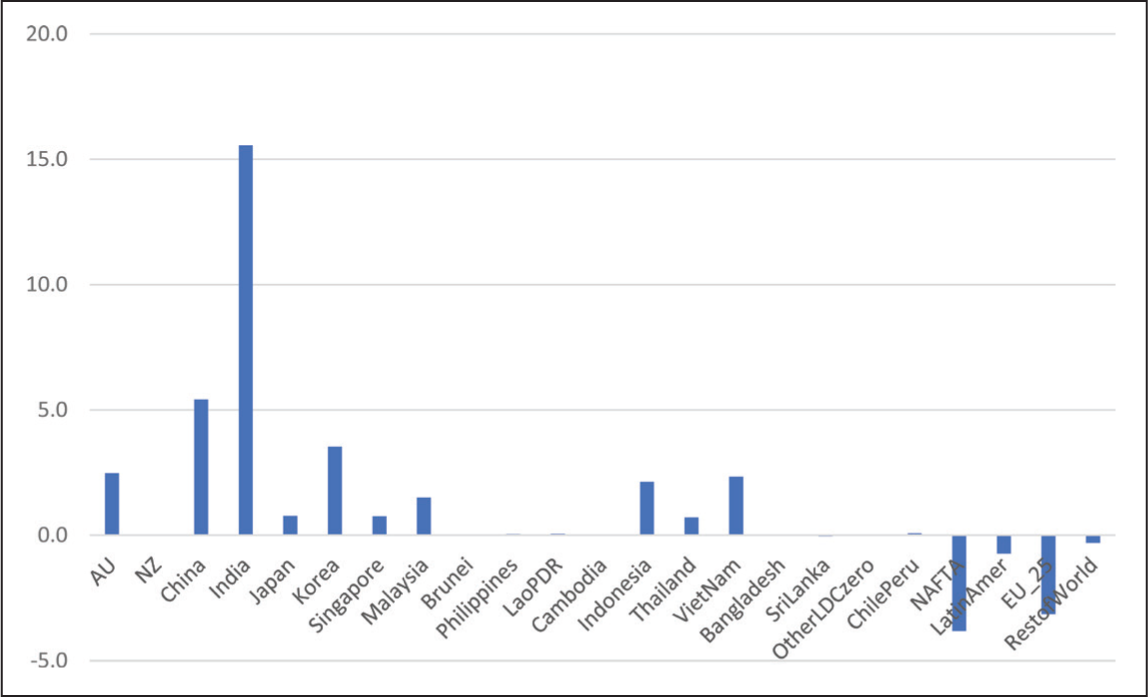

The results from our simulations conform to our theoretical expectations. Under scenario 1, India loses by staying out of RCEP as a non-member by about $2.3 billion, wherein it stands to gain an estimated welfare of US $13.3 billion from being in it purely in terms of tariff liberalisation only, and the net welfare gain of being in this agreement was worth $15.6 billion. A total of 10 of the largest RCEP-14 members would have improved on their net welfare reduction if India stayed in, that includes China ($5.4 billion), Korea ($3.5 billion), Australia ($2.5 billion) and Vietnam ($2.3 billion), respectively (Figure 6).

RCEP-14 scenario models Tariff liberalization 20 across 14 RCEP members, without India and excludes Myanmar due to lack of data availability.

RCEP-15 scenario models RCEP agreement assuming India did not opt out.

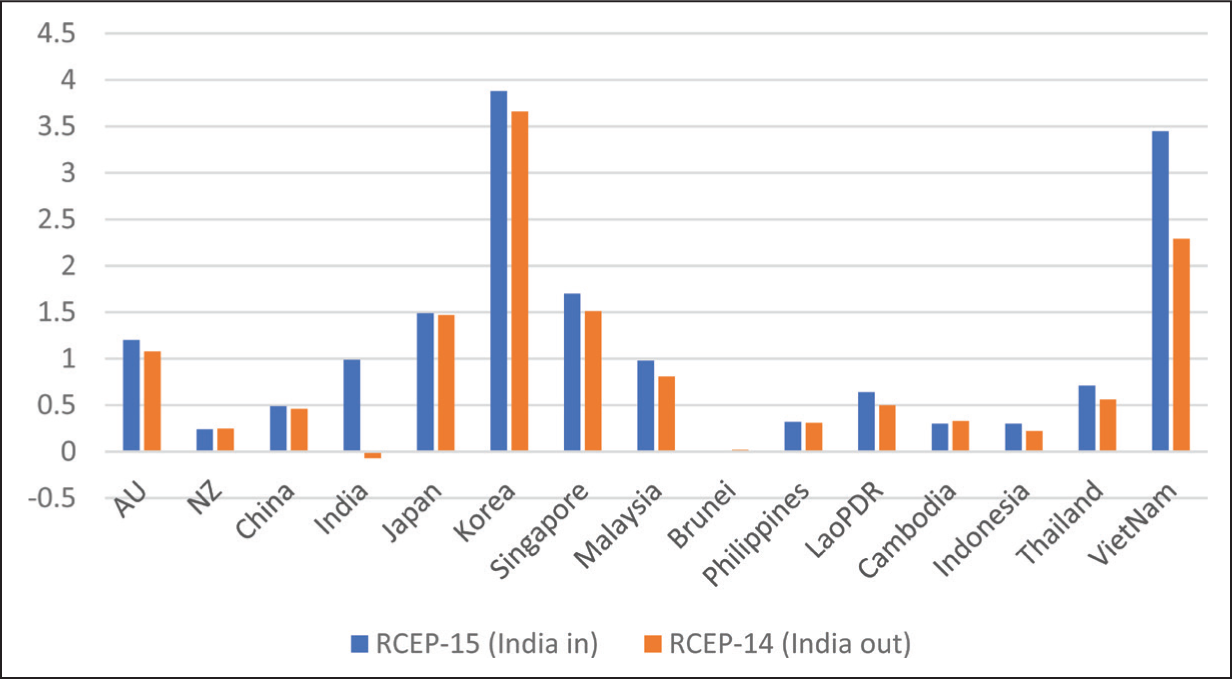

Figure 7 shows the changes in real GDP for RCEP members under both scenarios. Our results estimate that India gains from tariff liberalisation by staying in RCEP by about 1%, 19 while it loses by –0.1% in terms of real GDP by opting out it. Except for three small open economies (New Zealand, Cambodia and Brunei), all other RCEP members will experience a net reduction in real GDP growth if India opts to stay out of it. The highest net reduction is observed for Vietnam (1.2%). If India had decided to join, welfare gains would have been higher among RCEP members for the Republic of Korea, Vietnam, Singapore, Japan and Australia. 21 It is notable that except for Republic of Korea, the others are members of the already implemented CPTPP agreement. From a macroeconomic perspective, opting out of RCEP for India has been a missed opportunity. 22

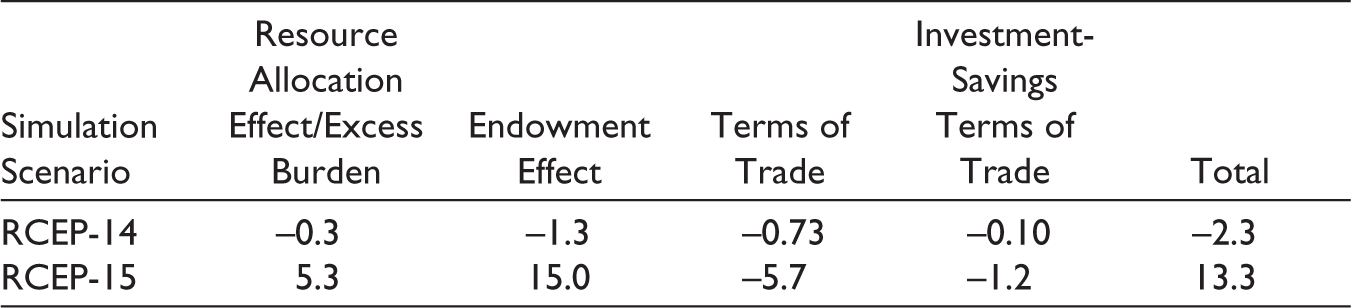

Furthermore, analysing the sources of these welfare changes for India in Table 5, we observe that if India opts to stay out of RCEP, compared to joining it, endowment effects (estimated as gross depreciation), in skilled and unskilled labour 23 and allocative efficiency of resources (due to changes in import taxes)—contribute to net welfare losses of US $16.1 billion and 5.6 billion, respectively. If India did decide to be an RCEP member, a welfare gain of US $5.3 billion 24 in scenario 2 of a tariff liberalisation is estimated. The largest source of net welfare gains for India due to opting out of RCEP is due to a positive net terms of trade effect resulting from not being a part of the tariff liberalisation, although it is estimated that RCEP-14 will lead to higher import prices for India compared to export prices, so negative terms of trade effect would persist even if India were to opt out.

Welfare Impact on India Decomposed by Main Sources (US $ Billion).

What about the impact on trade deficits? The trade deficit for India in automobiles is estimated to be US $2.6 billion, while that for auto-parts is estimated to be around US $1.1 billion, if India had been in RCEP. In contrast, when it opts out, these deficits reduce to US $165.8 and US $16.3 million, respectively. The negative values for changes in India’s trade balance for these sectors in the GTAP model 25 in both scenarios 1 and 2 confirm this further. While trade deficits maybe reduced if India opts out of RCEP, it is important to understand that reducing them by restricting imported intermediate inputs would affect both backward and forward linkages in GVCs that involve such inputs, as per Antràs (2020). This will hurt India’s automobile industry as well, albeit being protected in the short term.

Terms of Trade

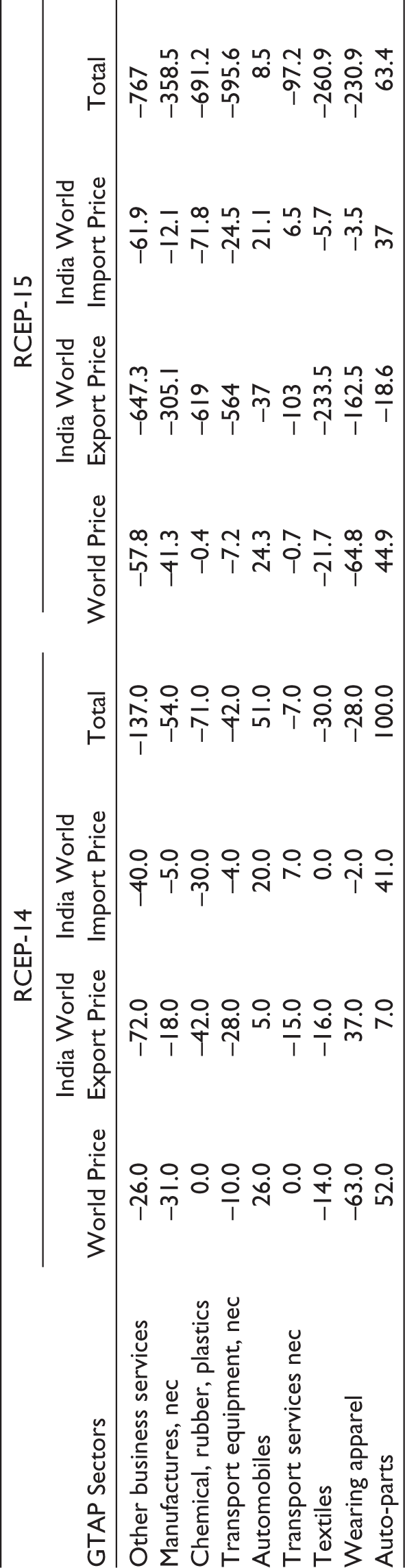

To further understand what drives the changes in terms of trade due to the policy simulations, the terms of trade effects for India for both scenarios are decomposed. The results are presented in Table 6 for our focus sector of automobiles and auto-parts, as well as those that contribute to these negative terms of trade effects through the input–output linkages.

Decomposition of Terms of Trade Effects on India (All Prices) by Selected GTAP Sectors (by Value US $ Million).

Among the three components of the terms of trade effects, 26 it is the world export price effect for India, which is largely negative and contributes to the overall negative terms of trade effects on total welfare if India had been an RCEP member. These results are due to the implicit Armington assumption in GTAP that products are differentiated by their country of origin. The export price effect depends on whether the country’s free-on-board (fob) export price for its variety of a commodity declines or increases relative to that of competing suppliers globally.

India has a strong negative world export price effect in manufacturing, including automobile and auto-parts sectors. A reduction in domestic production in India due to tariff liberalisation contributes to this effect. Net imports of automobiles and auto-parts increase and the India variety lowers in relative price compared to competing suppliers from RCEP members. The explanation for this is that India has higher baseline tariffs than other RCEP members, implying that it faces a greater price cut, relatively speaking, compared to other RCEP partners. This phenomenon is stronger for automobiles as a final good sector than auto-parts for India, given the cascading tariff structure in the former rather than the latter.

The contribution of the terms of trade losses in an RCEP-15 scenario also comes from a decline in relative fob price of India’s manufacturing exports in intermediate input sectors that contribute to automobiles (including chemical rubber, plastics, textiles and wearable apparel), as well as services sector (transport and other business services). Import prices for India in these sectors increase more than export prices in a status quo situation wherein India opts out of RCEP (scenario 1), adversely affecting export competitiveness and contributing to terms of trade losses, albeit much smaller than if it were to be a part of the agreement.

The above imply that pre-existing policy distortions in related intermediate input sectors, by way of taxes, quantitative measures, or non-tariff barriers, need to be removed to reap any benefits of export competitiveness in a mega-regional RTA like RCEP. As observed by Narayanan et al. (2010), the presence of ‘false competition’ between ASEAN members and India is likely as their competitive strengths differ between automobile parts and finished automobiles. The separate focus on automobile parts and automobiles informs policymakers that while India stands to gain due to a tariff liberalisation on auto-parts, where it is already a major player among the RCEP members, this is not the case for automobiles, except for small and compact car segments.

Several data limitations and caveats are in order. First, our analysis compares a retrospective and a status quo scenario, which implies that our results are conservative compared to the actual policy implementation. Our article has attempted to model the extreme scenario of substantial tariff liberalisation within RCEP in a ‘what if’ scenario. We have not attempted to further model the effect of non-tariff barriers (NTBs) in this sector, which itself involves data challenges, especially for newer ASEAN members. Existing NTBs in the automobile sector would add up to the GVC-link trade costs for India in terms of backward as well as forward linkages and could be better studied in a GTAP-MVH model as proposed by Dixon et al. (2020).

Second, ours, being a static version of GTAP, focuses only on the outcome of the policy change. Finally, data aggregation is a common issue in GTAP studies, and although attempts have been made here to specifically separate automobiles and auto-parts, a simplistic market structure of perfect competition 27 is assumed as we do not have complete market knowledge on firm behaviour, pricing and costs across all RCEP members needed to model an imperfectly competitive market in our study. 28

Conclusions and Policy Implications

The above limitations notwithstanding, our article informs policymakers whether opting out of RCEP was a missed opportunity for India, both at the economy wide level and for the sector-specific GVC trade sector of automobiles. Our results suggest that, from a macroeconomic perspective, this decision implied that welfare improvement and associated allocative efficiency effects with trade liberalisation were foregone. However, from a microeconomic perspective, the decision accorded domestic protection to automobile and auto-parts sectors of India. The decline in India’s output of finished automobiles and its parts and components sectors was lesser compared to if it had been a part of RCEP. This further implies that due to export diversion observed in the auto-parts sector globally, as India faces terms of trade losses due to higher import prices in an opt-out situation, both backward linkages and forward linkages in the GVC of its automobile industry are negatively affected.

Our findings suggest policymakers that membership in RCEP would have provided an opportunity for Indian exporters to plug into trade in GVC goods within Asia and globally in two ways. First, by strengthening the forward linkages with greater exports to non-RCEP members, especially EU and the USA, as well as strengthening the existing backward linkages with RCEP members through imports. However, greater job losses could result in import competing industries being displaced due to cheaper imports, unless steps are taken to improve domestic factor productivity growth, irrespective of whether India joins new RTAs or not.

While short-term reconfiguration of its domestic economic priorities post-pandemic while being engaged globally makes sense, the longer-term post-COVID-19 recovery strategy cannot ignore engaging in global trade through Indo-Pacific RTAs. This is evident from our simulation results, as greater export diversion from other trading partners of India joining such RTAs will not be in its favour. 29 Further, rising trade costs associated with supply chain disruptions in the pandemic period have renewed the urgency to strengthen regional GVC linkages that require the reduction or elimination of bilateral tariff barriers, among others.

Against this backdrop, Indian policymakers focus on contemplating joining any new trade agreement from a negotiating position of strength. This requires developing resilience and productivity growth through critical domestic reforms. Our analysis informs policymakers that tariff barriers in key industries that are linked to GVCs, such as automobiles, are best avoided eventually. This is because it directly and indirectly hurts export growth and job creation in these industries. Proactive policies that involve investment pushes, such as the recently announced 10-sector Production Linked Incentive (PLI) scheme in 2020 that focuses on boosting manufacturing capabilities and thereby exports, should be properly implemented and be part of the preferred policy mix. These policies are essential if Indian industries, such as automobiles, are to become competitive in international markets in the face of any future mega-regional trade agreements.

Supplemental Material

Supplemental material for this article is available online.

Footnotes

Acknowledgements

The authors would like to thank participants at the Australasian Trade Workshop and the Sixth International Conference on Empirical Issues in International Trade and Finance (EIITF) in New Delhi, ARTNet secretariat for their valuable comments and suggestions on earlier versions of this article.

Declaration of Conflicts of Interest

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.