Abstract

Despite high rates of inequality, direct taxation in Latin America remains limited, constraining both the magnitude of fiscal redistribution and the expansion of welfare systems. This article presents a novel explanation for the persistence of this pattern in democratic settings. Drawing on the literature on inequality, fairness and fiscal policy preferences, I argue that higher levels of perceived inequality reduce support for a broad-based income tax, thereby weakening the incentives for governments to implement policies towards mass taxation. An empirical analysis based on public opinion data from 18 countries and a newly developed measure of perceived inequality provides strong support for this argument. These findings offer new insights into public finance challenges in Latin America, which depart from the conventional focus on the power of elites and advance our understanding of the viability of tax reforms across the region.

Introduction

Expanding the tax base remains one of the greatest challenges that states are facing along the process of development. Earlier studies have shown that differences in the size of the tax base—rather than in top marginal rates—underlie the emergence of large fiscal states (Besley & Persson, 2014; Jensen, 2022). Countries with narrow tax bases are therefore constrained in their capacity to grapple with pressing issues such as poverty and inequality. They also struggle to scale up the provision of public services (e.g., education, health care, and infrastructure) to the level required to foster sustainable economic growth.

In Latin America, this challenge is primarily evident in the case of direct taxation and, most strikingly, the personal income tax (PIT). According to recent estimates, revenue from the PIT in the region amounts to 2.2% of GDP compared to 8.3% in the OECD countries (OECD, 2023). 1 This not only limits the ability of governments to enhance public services and extend welfare schemes traditionally known as ‘truncated’ (De Ferranti et al., 2004, p. 14) but also hinders the equalising effect of fiscal policies. As the tax base typically consists of a small minority of the population, the result is a PIT ”that is extremely progressive in nature, but that raises little revenue and, therefore, has little redistributive power” (Barreix et al., 2017, p. 30). 2

The limited role of direct taxation becomes especially puzzling considering Latin America’s high levels of inequality and the resilience of democracy throughout most parts of the region in the last decades. Against this backdrop, there is a large degree of uncertainty regarding the factors that determine individuals’ views about taxation. Existing accounts of the evolution of fiscal capacity in the region have predominantly focused on the role of economic and political elites (e.g., Cárdenas, 2010; Fairfield, 2015; Hollenbach & Silva, 2019). By contrast, research examining popular demand for fiscal transformation remains scarce (Carnes & Mares, 2014; Flores-Macías, 2018). Considering the importance of public opinion for tax policymaking (Flores-Macías, 2018) and its relevance for the implementation and withdrawal of fiscal reforms in the region’s contemporary history (Pousadela, 2013; The Economist, 2021), it becomes vital to examine tax policy preferences through a broader societal perspective. This is particularly true in the case of income taxation, where effective revenue-raising efforts require strong cooperation between state and society (Levi, 1989).

This article addresses this gap by exploring how subjective perceptions of inequality shape individuals’ preferences over the size of the tax base. The focus on perceived rather than actual inequality corresponds with an emerging consensus regarding the greater significance of the former for the formation of preferences over fiscal redistribution (see, e.g., Bussolo et al., 2021; Choi, 2019; Gimpelson & Treisman, 2018; Trump, 2023). To answer this question, I draw on extensive micro-level data from the Latinobarómetro public opinion survey (Latinobarómetro Corporation, 2020) that offers an opportunity to study preferences over the size of the tax base among individuals from 18 Latin American countries.

For the first time since its introduction, the 2020 edition of the survey asked respondents about the income bracket from which households in their country should begin to pay taxes. In essence, the responses to this question indicate whether individuals prefer a broad income tax base that consists of large segments of society or a narrow income tax base that contains only the richest households. In other words, they suggest whether respondents are more inclined towards a ‘mass tax’ or a ‘class tax’ (Rush, 1981; Steinmo, 2003). A better understanding of the conditions in which individuals are more likely to support mass taxation is key to identifying viable paths for fiscal reforms. This is crucial since changes in the size of tax bases often arise from policy choices rather than being merely a product of economic growth (Jensen, 2022). As a policy measure, the expansion of the income tax base also tends to have a greater impact on public revenues than rate increases (Amaglobeli et al., 2022). Furthermore, the broadening of tax bases has promising benefits for government performance and political participation (Baskaran & Bigsten, 2013; Weigel, 2020), which in turn can constitute an effective constraint on public spending decisions.

Drawing on the literature on inequality, fairness and fiscal policy preferences, I develop the argument that higher levels of perceived economic inequality reduce support for mass taxation in Latin America by undermining the notion that the inclusion of non-elites in the tax base is justified. To test this hypothesis, I construct the subjective Gini coefficient—a new measure of inequality perceptions derived from a question in the same survey (Latinobarómetro Corporation, 2020) asking respondents about the distribution of wealth in society. The empirical findings provide strong support for this argument by showing that at increasing levels of perceived inequality individuals are significantly less likely to favour broad-based income taxes and significantly more likely to support class taxation that includes only the top decile. These results are robust across multiple specifications. The article also reveals that not only quantitative estimates but also normative views of inequality are strongly linked to preferences over the size of the tax base. Finally, I augment the analysis by evaluating the applicability of the theory to the case study of Colombia, where mass protests blocked a proposed tax reform which intended to expand the tax base shortly after the Latinobarómetro 2020 survey, and by examining the relationship between perceived inequality and willingness to pay more taxes in Chile using data from a separate survey (PNUD, 2017).

The article makes three major contributions. First, it offers a new perspective on contemporary public finance challenges in Latin America, which enhances our understanding of the conditions in which tax reforms are more feasible. Unlike the conventional emphasis on the influence of powerful elites, the article illustrates that a widespread perception of high inequality may itself hinder the evolution of fiscal capacity by constraining the political leeway of electorally-motivated governments to enact base-broadening tax reforms. Specifically, this helps explain why governments in the region have struggled to expand redistribution beyond the achievements of the 2000s (Holland & Schneider, 2017). Second, the article develops a new measure of inequality perceptions through which it establishes new evidence on the subjective level of inequality across Latin America—an area where income and wealth disparities are ubiquitous. By doing so and illustrating its significance for concrete tax policy preferences, the article advances our knowledge of perceived inequality as an important factor for explaining the political economy of fiscal policy. This adds to previous studies on this topic (e.g., Bobzien, 2020; Choi, 2019; Gimpelson & Treisman, 2018; Niehues, 2014) both theoretically and empirically. Third, by focusing on micro-level perceptions and tax policy preferences, the article contributes to the strand of research that deals with the consequences of inequality for fiscal capacity building (Ardanaz & Scartascini, 2013; Islam et al., 2018; Sokoloff & Zolt, 2012).

Fiscal Redistribution in Latin America

Fiscal redistribution refers to the reduction of inequality achieved by direct taxes and government transfers. While redistribution through the tax system plays a prominent role in reducing inequality in many OECD economies (Guillaud et al., 2020), it remains limited in Latin America—albeit at different levels across countries (Flores-Macías, 2019). 3 The PIT in the region is typically characterised by high levels of progressivity yet it is effectively collected from a small fraction of the population (Barreix et al., 2017; Corbacho et al., 2013; OECD et al., 2018, p. 129). Conceptually, this means that the tax base is narrow. 4 As pointed out by Barreix et al. (2017, pp. 17–18), the exemption threshold for taxes on personal income is high not only within countries but also relative to the level of economic development. For most countries, the average effective tax rate and the total revenue collected are low even in the eighth and ninth income deciles (Barreix et al., 2017; Corbacho et al., 2013). The PIT thus remains, following the terminology used to describe the expansion of income taxation in Western economies, a ‘class tax’ rather than a ‘mass tax’ (Rush, 1981; Steinmo, 2003). In this setting, it has a limited impact on redistribution—either directly through the tax system itself or indirectly through in-kind transfers. According to Economic Commission for Latin America and the Caribbean (ECLAC) study, although 88% of the PIT in the region are paid by the top decile, it contributes only 2% to the reduction of inequality as measured by the Gini coefficient compared to 12.5% in the European Union (ECLAC, 2017, pp. 44–46). In addition to the size of the tax base, other factors explaining the low levels of PIT in Latin America include, among others, high incidence of tax evasion and different forms of tax reliefs (Barreix et al., 2017), as well as the magnitude of tax expenditures (Barreix et al., 2017; Campos Vázquez, 2022).

In contrast to revenue-side redistribution, government spending has a more profound influence on the level of inequality (Goñi et al., 2011; Hanni et al., 2015). A notable example is conditional cash transfer (CCT) programmes (Holland & Schneider, 2017). Yet, the combination of the two aspects of fiscal redistribution falls short of significantly reducing income and wealth gaps, among others because the spending and revenue channels are closely related to each other. As shown by Castañeda and Doyle (2019), when left-wing governments pursuing greater redistribution are constrained by widespread informality, they tend to finance social policies through regressive consumption taxation.

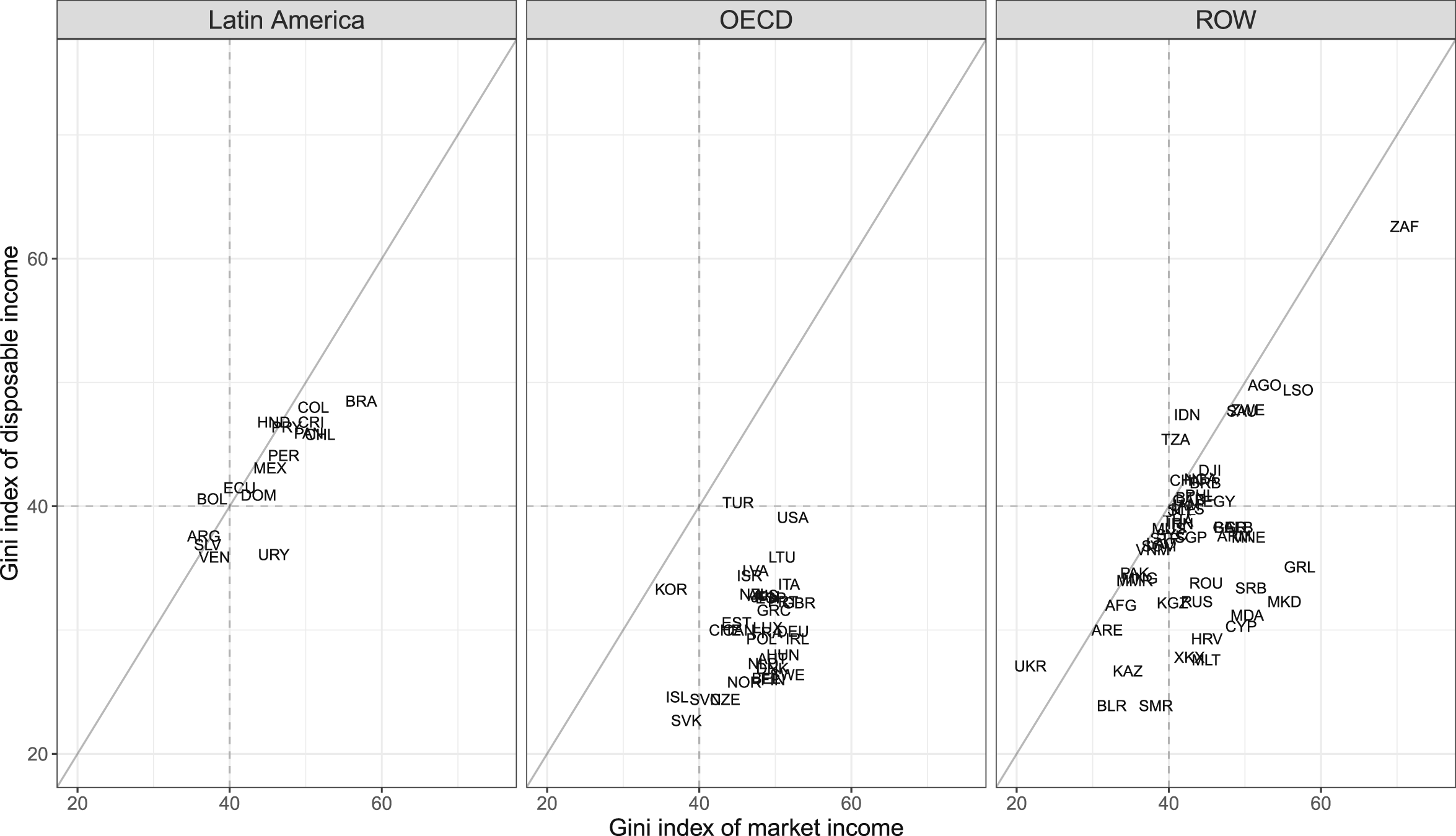

Figure 1 exhibits the modest effect of fiscal redistribution on inequality in Latin America in a comparative perspective.

5

Based on data from the Standardized World Income Inequality Database (Solt, 2019), it visualises the relationship between the Gini index of market income—i.e., inequality before taxes and transfers (shown on the X-axis)—and the Gini index of disposable income, which takes taxes and transfers into account (shown on the Y-axis).

6

In other words, these variables measure the level of inequality pre- and post-redistribution, respectively.

7

Noticeably, the figure illustrates that market income inequality is not particularly high in Latin America. On average, it amounts to 45.5, in between the OECD average (47.6) and the average for non-OECD countries in other regions (43.7), whose level of economic development is comparable to Latin American countries.

8

However, when looking at post-redistribution income gaps, the majority of Latin American societies are among the most unequal in the world. The minor impact of fiscal redistribution can be seen through the concentration of data points along the diagonal line on the left panel, indicating that income differences in society are similar before and after taxes and transfers. Consistent with this pattern, the average Gini index of disposable income in the region (42.8) is just slightly lower than its pre-redistribution level, significantly above the OECD members (30.2) as well as non-OECD countries in the rest of the world (37.3). Inequality and fiscal redistribution in Latin America in a comparative perspective. Note. ROW = Rest of world. The figure presents the relationship between market income inequality (before taxes and transfers) and disposable income inequality (after taxes and transfers). Data for 2017–2019, the latest for each country. Latin American countries that are also OECD members are included only in the former group. The dashed lines show that while Gini index above 40 is common in all groups pre-redistribution, only in Latin America this level remains widespread post-redistribution. Data source: Solt (2019).

Theory

Fiscal Capacity Building in Highly Unequal Contexts

Apart from a few notable exceptions (Carnes & Mares, 2014; Flores-Macías, 2018), the dominant approach for analysing the development of fiscal capacity in Latin America focuses on economic and political elites (e.g., Atria, 2023; Berens & von Schiller, 2017; Cárdenas, 2010; Fairfield, 2015; López et al., 2022). The elite-oriented view holds that the concentration of power and resources in the hands of a small group of individuals hampers the evolution of tax systems in a ‘top-down’ fashion that reflects the elites’ own material interests. While it is recognised that the ability of elites to influence decision-making varies across different settings (Fairfield, 2015), a recurring theme in these accounts is the examination of fiscal capacity development through the most powerful groups in society. For instance, Hollenbach and Silva (2019) found that in Brazil the more unequal municipalities not only tend to raise lower property taxes but are also less likely apply to a state initiative designed to strengthen tax collection capacity. According to Ardanaz and Scartascini (2013), who analysed data from more than 50 countries, one mechanism through which income and wealth inequalities may constrain the levels of PIT is legislative malapportionment.

These studies have made a significant contribution to our understanding of Latin America’s fiscal systems. However, the elite-oriented approach, notwithstanding its importance, remains inadequate for addressing both conceptually and empirically the transition from class taxation into mass taxation. First, by definition, a shift towards mass taxation requires the gradual incorporation of non-elites into the tax base. This underlines the need to expand our knowledge of the conditions in which non-elites are more willing to be taxed ‘quasi-voluntarily’ (Levi, 1989).

Second, as noted earlier, the current design of the PIT is highly progressive but it practically yields low revenue and redistribution. Hence, applying a broader perspective becomes empirically necessary for identifying the impediments and potential drivers of reforms that can increase the overall tax take. This is particularly true considering the tendency of base-broadening measures to have a sustainable impact on PIT revenues (Amaglobeli et al., 2022).

Third, the literature suggests that politicians tend to pay careful attention to public opinion in tax policymaking (Flores-Macías, 2018; Letelier & Dávila, 2015). This implies that narrowing down the theoretical interest exclusively to the views of the most affluent individuals is unlikely to capture the wider set of factors that determine tax policy. In fact, the contemporary history of Latin America demonstrates that non-elites play an important role in shaping the direction of fiscal policy. For instance, Carnes and Mares (2014) found that the expansion of universal social insurance programmes in the region was driven by the formation of new coalitions in the context of increasingly unstable labour market. Fairfield and Garay (2017) highlighted the promotion of redistributive policies by right-wing governments in the context of electoral competition. In Chile, the tax reform under the second government of Michelle Bachelet was influenced by demands from the 2011 student movement (Palacios-Valladares & Ondetti, 2019, p. 644). In Colombia, massive protests during the COVID-19 pandemic eventually led the government to withdraw from a tax reform that among others aimed at lowering the income tax threshold (Bernal & Ortiz, 2022; The Economist, 2021). Taken together, there are strong indications that incorporating non-elites into the analysis can enhance our understanding of the conditions in which a transition towards mass taxation becomes politically viable.

Inequality, Subjective Perceptions, and Redistribution

In principle, the broadening of the tax base allows the government to extend its revenue-raising capacity and thereby to increase social spending (Piketty, 2020, p. 462). In highly unequal settings, the possibility of expanding social protection programmes and increasing public investment in areas such as health care and education can therefore provide a strong incentive for non-elites to support the broadening of narrow tax bases. Yet, higher inequality does not necessarily produce greater public spending and redistribution. What explains this discrepancy?

A common starting point for studies of inequality and redistributive preferences is the seminal model developed by Meltzer and Richard (1981). The Meltzer-Richard framework analyses changes in the size of the government through the lens of redistributive expenditures that are fully financed through taxation. For democracies, it predicts that the size of the government is driven by the difference between the mean and median income. The expansion of this gap leads to greater redistribution and higher tax revenue—in line with the preferences of the ‘decisive voter’ with the median income (Meltzer & Richard, 1981, p. 920). The level of inequality thus affects the magnitude of redistribution, resulting in the increase of both sides of the public budget when income differences grow.

Despite its lasting influence, however, the validity of the Meltzer-Richard theory predictions has been questioned on different theoretical and empirical grounds (Besley & Persson, 2014). Two important insights arising from recent studies are that individuals tend to misperceive income and wealth differences (Hauser & Norton, 2017; Norton & Ariely, 2011) and that subjective rather than objective levels of inequality are associated with redistributive preferences (Bussolo et al., 2021; Choi, 2019; Engelhardt & Wagener, 2014; Gimpelson & Treisman, 2018; Trump, 2023). 9 These findings suggest that there is a strong case for examining individuals’ fiscal policy preferences through the lens of inequality perceptions.

Given that subjective and objective estimates of inequality often diverge, a related question is which factors influence the formation of inequality perceptions. While investigating this question in detail is an emergent cross-disciplinary effort that remains outside the scope of this article (see, e.g. Bussolo et al., 2021; Knell & Stix, 2020; Phillips et al., 2020), recent works indicate that misperceptions of inequality can originate from limited information (Iacono & Ranaldi, 2021) and the particular environment based on which individuals derive their estimates (Schulz et al., 2022). Specifically, the reference groups that individuals consider in forming subjective assessments of the income distribution misrepresent the entire population (Knell & Stix, 2020). Thus, under socio-economic segregation, increasing inequality may cause a decline in perceived inequality (Windsteiger, 2022). A diversification of the reference group, in turn, leads individuals to adjust their preferences for redistribution (Londoño-Vélez, 2022).

As Bobzien (2020) work suggests, it is important to pay attention to the possibility that the level of perceived inequality is fully captured by variation in ideology and self-interest as the control variables typically used to explain redistributive preferences. In such case, there is no practical value added from including perceived inequality as an independent predictor. This concern seems less applicable to the Latin American context considering that both factors are in general only loosely correlated with redistributive preferences with significant heterogeneity between countries (Bogliaccini & Luna, 2019). Furthermore, preferences for redistribution may diverge from preferences over the size of the tax base, reflecting two distinct instruments for reducing inequality (Barnes, 2015). Therefore, I postulate that the level of perceived inequality can substantively enhance our ability to explain patterns of taxation across the region. I evaluate this proposition empirically in the Results section.

Inequality and Tax Policy Preferences

How does perceived inequality shape individuals’ policy preferences over the size of the tax base in Latin America? I posit that support for the transition from class taxation into mass taxation hinges on the belief that the inclusion of non-elite households in the tax base is justified. Viewed from this perspective, I anticipate that the more dominant the perception that economic resources are concentrated at the top of the distribution, the lower the likelihood that the establishment of broad-based income taxation is widely accepted.

I consider the following dimensions as essential determinants of individuals’ willingness to expand the tax base: (1) The belief that the rich are paying a reasonable share of their income in taxes; (2) The belief that there is a need for public revenues that necessitates the lowering of the tax threshold. The literature provides useful insights into the way subjective estimates of inequality can influence these dimensions. Firstly, an extensive strand of research in political economy underscores the role of fairness in shaping attitudes towards taxation (Levi, 1989; Rowlingson et al., 2021; Scheve & Stasavage, 2016; Steinmo, 2003). Fairness considerations play an important part in the formation of individuals’ views about who should bear the fiscal brunt (Ballard-Rosa et al., 2017; Iacono & Ranaldi, 2021; Limberg, 2020) and the internal willingness to pay taxes (Castañeda, 2024)—commonly referred to as ‘tax morale’ (Luttmer & Singhal, 2014). Moreover, experimental evidence shows that through the activation of fairness norms, informing participants about income disparities leads to a reduction in tax compliance (Engel et al., 2020).

By reinforcing concerns about unfairness, the perception that income and wealth are heavily concentrated in the hands of a narrow elite is expected to strengthen the opposition to mass taxation. In this setting, the establishment of broad-based income taxation clashes with the basic principle of 'ability-to-pay' and the legitimacy of mass taxation is intrinsically undermined. 10 Thus, rather than leading to the expansion of the tax base, increasing levels of perceived inequality are in fact more likely to bolster demand for highly progressive class taxation. An illustration of this argument can be found in the 2011 Chilean student movement, which advocated for greater tax burden on the rich to address entrenched inequality in access to public education (Pousadela, 2013).

Secondly, there are indications that highly stratified social structures may weaken the demand for public services. This may adversely affect individuals’ willingness to broaden the tax base in a form of ‘fiscal contracting’ (Bird & Zolt, 2015) where higher tax revenues permit the expansion of public services. I refer to this channel as reciprocity (Luttmer & Singhal, 2014). For instance, Berens (2015) found that in Latin America the demand for publicly funded health care declines in the presence of large informal sector due to an alignment of interests between middle-income and high-income groups. According to Holland (2018), experiences of exclusion from the welfare system are associated with lower support for redistribution among the poor across the region. This corresponds to the fact that some of the main welfare benefits in the region—including the pension system—have long been limited mostly to individuals with higher incomes (Rofman & Oliveri, 2012). Holland and Schneider (2017) introduced the concept of ‘coalition hollowing’ to explain the declining interest of lower and middle-income groups in the expansion of the welfare state. Their analysis points out that this process can be driven by the use of informal services among low-income groups and the perception of greater value in private sector alternatives, particularly in education and health care, among the middle classes. In sum, these studies imply that individuals may have lower interest in the expansion of public services in settings they perceive as highly unequal, which in turn is likely to undermine support for mass taxation.

There are other potential channels of influence. For instance, perceived inequality is negatively associated with the belief that meritocracy shapes individual wages (Kuhn, 2019). This may have detrimental effects for the legitimacy of broad-based income taxation while at the same time reinforcing support for class taxation as a mechanism to diminish income and wealth gaps.

Based on the above discussion, I argue that the opposition to mass taxation is expected to grow when the perception that a small elite holds a disproportionate share of the pie becomes more widespread. This leads to the following hypothesis: Individuals are less (more) likely to support mass taxation when they perceive their society as more (less) unequal. Therefore, I anticipate that subjective measures of inequality are significantly and negatively associated with support for mass taxation. In other words, I expect that, all else equal, individuals who view society as more unequal believe that the tax threshold should be higher along the income distribution. Against this backdrop, electorally-motivated governments often refrain from implementing politically unpopular policies that seek to increase revenues from the PIT, which in turn remains highly progressive but with limited impact on both redistribution and public revenue generation.

Data and Empirical Strategy

Preferences Over the Size of the Tax Base

The data on individuals’ preferences over the size of the tax base are from Latinobarómetro (Latinobarómetro Corporation, 2020), a nationally representative public opinion survey that contains data from 18 Latin American countries. 11 For the first time since its launch, the 2020 edition of the survey included the following question: “…In your opinion, starting from which income bracket households of [country of nationality] should pay taxes?” 12

The respondents could choose between 1 and 10 where 1 represents the poorest household income group and 10 represents the richest household income group.

13

Alternatively, the respondents could answer that all households should pay taxes equally (coded in the raw data using the value ‘11’) or that none of the households should pay taxes (‘12’). In essence, the answers to this question illustrate the preferences of individuals regarding the size of the tax base.

14

The main variable of interest is taxthreshold which I define as follows:

where taxgroup represents the answer to the above question on the income bracket from which taxes should be paid. In other words, taxthreshold receives the actual threshold level chosen by the respondents for answers between 1 and 10 and the values 11 and 12 are recoded as 0 and 11, respectively. Thus, higher values of taxthreshold indicate lower support for mass taxation. In addition, I also consider a binary definition where support for mass taxation is inferred by the willingness of individuals to start taxing households from the fifth income bracket (or lower) as specified below.

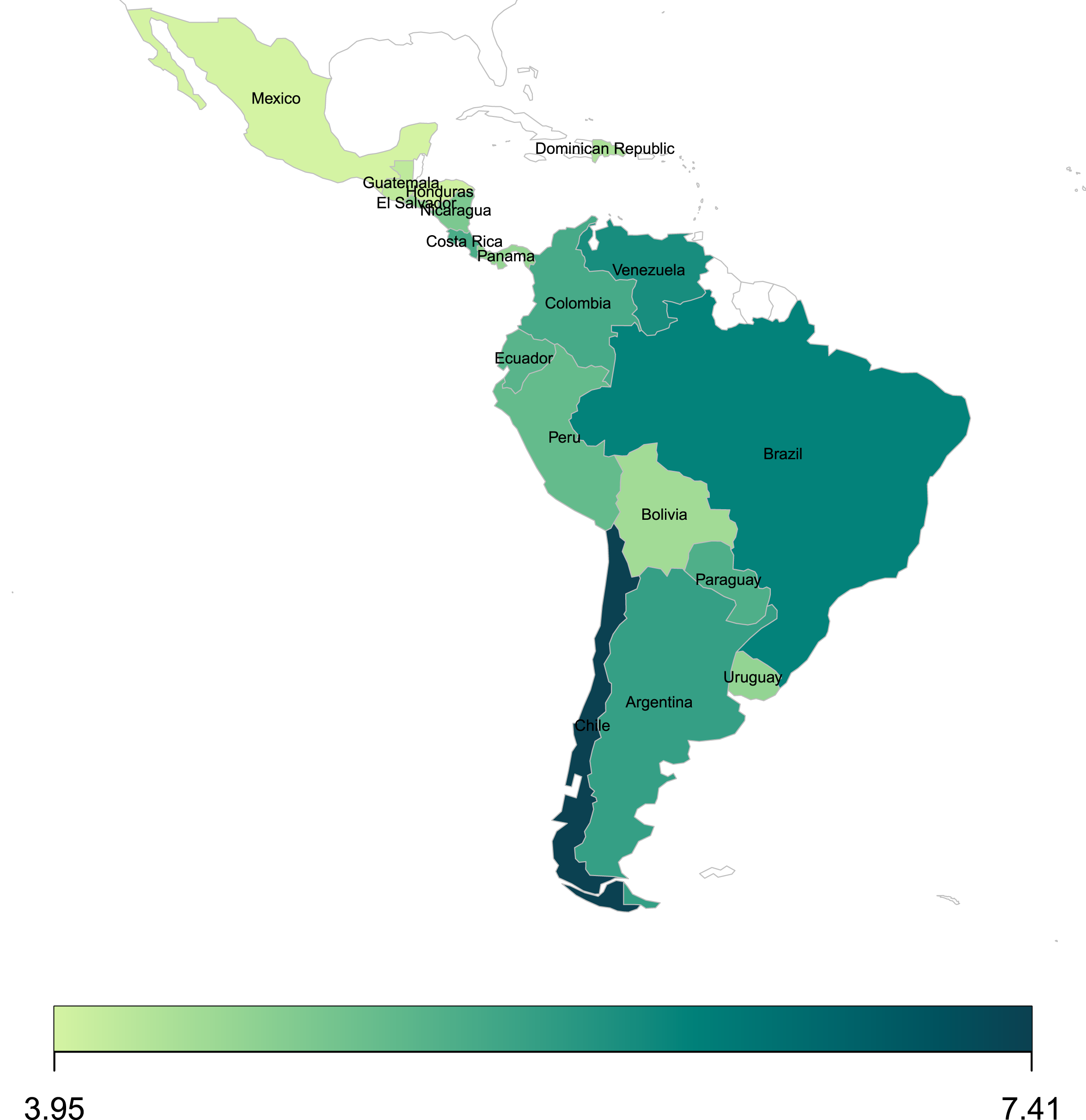

Figure 2 visualises the variation in preferences over the size of the tax base in Latin America by displaying the mean value of taxthreshold aggregated by country. Lower values of this measure—indicating greater support for broad-based income taxation—are observed in Mexico (3.95), Honduras (4.02), and Guatemala (4.18). By contrast, a general preference for smaller tax bases can be seen in Venezuela (5.98), Brazil (6.18), and most strikingly in Chile (7.41). This can be interpreted as an indication of strong support for redistribution through taxes on the most affluent in Chile, which coincides with previous findings (Atria, 2023, p. 114). As shown in Figure A1 in the Appendix, an alternative calculation based on masstax as the variable of interest leads to largely similar conclusions. Specifically, the countries with the highest levels of support are Honduras (68%), Mexico (67.6%), and Guatemala (64.5%). By contrast, support for mass taxation is particularly low in Argentina (44.3%), Brazil (40.5%), and Chile (23.6%). Preferences over the income tax threshold in Latin America. Note. The map visualises the mean of taxthreshold at the country level. This variable receives the preferred tax threshold indicates by the respondent for values between 1 (the poorest income group) and 10 (the richest income group). Responses that indicate that all households should pay the same and that none of the households should pay taxes are recoded as 0 and 11 respectively. Lower values indicate greater support for broad-based income tax. Author’s calculations based on data from Latinobarómetro 2020.

Measuring Perceived Inequality

Despite the growing interest in inequality perceptions over the last decade, research on Latin America in this context remains scarce. 15 To operationalise perceived inequality, I create a subjective measure of the Gini coefficient—the most popular indicator of actual inequality. The calculation of this variable (henceforth subjective Gini coefficient) is based on a question from the Latinobarómetro survey (Latinobarómetro Corporation, 2020) asking participants how much money they think each group has today, given that the country is divided into five groups where groups 1 and 5 are the poorest and the richest, respectively, and the total amount of money is 100. The subjective Gini coefficient is calculated at the observation level under the assumption that each group represents one-fifth of the population. In accordance, the two extreme scenarios of perfect equality (the answer 20, 20, 20, 20, 20) and perfect inequality (0, 0, 0, 0, 100) correspond to the values 0 and 0.8. 16 A graphical illustration of the calculation is shown in Figure A2 in the Appendix. 17

From a methodological viewpoint, the closest approach in the literature is, to the best of my knowledge, De Bresser and Knoef (2022), who calculated a Gini coefficient based on income quintiles to study individuals’ redistributive preferences in the Netherlands. In addition, various studies have produced estimates of the perceived Gini coefficient based on questions from the International Social Survey Programme (ISSP) either indirectly based on perceived social position (Choi, 2019) or directly using questions about respondents’ perceived type of society (Bobzien, 2020; Gimpelson & Treisman, 2018; Niehues, 2014) and their estimates for wages in different occupations (Kuhn, 2011). The subjective Gini coefficient introduced in this article advances the effort to measure inequality perceptions in two major aspects. First, it explicitly refers to the perceived economic gaps within society. In particular, the phrasing of the Latinobarómetro survey question mitigates the concern that other non-economic confounding factors shape individuals’ inequality perceptions while still focusing on the differences across the entire population. Second, as opposed to the ISSP question on perceived type of society where the respondents were asked to select a diagram that best fits their assessments from a limited number of options, the participants in the Latinobarómetro survey indicated their numerical estimates for the amounts held by each of the five groups. This can contribute significantly to the precision of measurements.

The subjective Gini coefficient is calculated based on the estimates provided by the respondents for the amounts of money held by each of the five groups. Observations in which data for all five groups are missing are excluded from the calculation. Due to data quality considerations, the analysis also excludes observations in which a poorer group has more money than a richer group as defined by the question. 2,401 of the remaining observations (22.6%) contain no response for between one and four quintiles. Considering that in the majority of cases (98.4%) the available information amounts to 100, these observations are included in the analysis and no responses are recoded as 0. 18 This decision is further justified by the fact that there are no explicit zero values in the data set for the variables that underlie the calculation of the subjective Gini coefficient. The analysis also includes a small proportion of the observations (3.1%) in which the sum of money for the five quintiles was lower or higher than 100 under the assumption that they still provide valuable information about the way respondents subjectively view the income distribution. The robustness subsection tests the sensitivity of the findings to these choices.

Overall, the mean of the subjective Gini coefficient is 0.42.

19

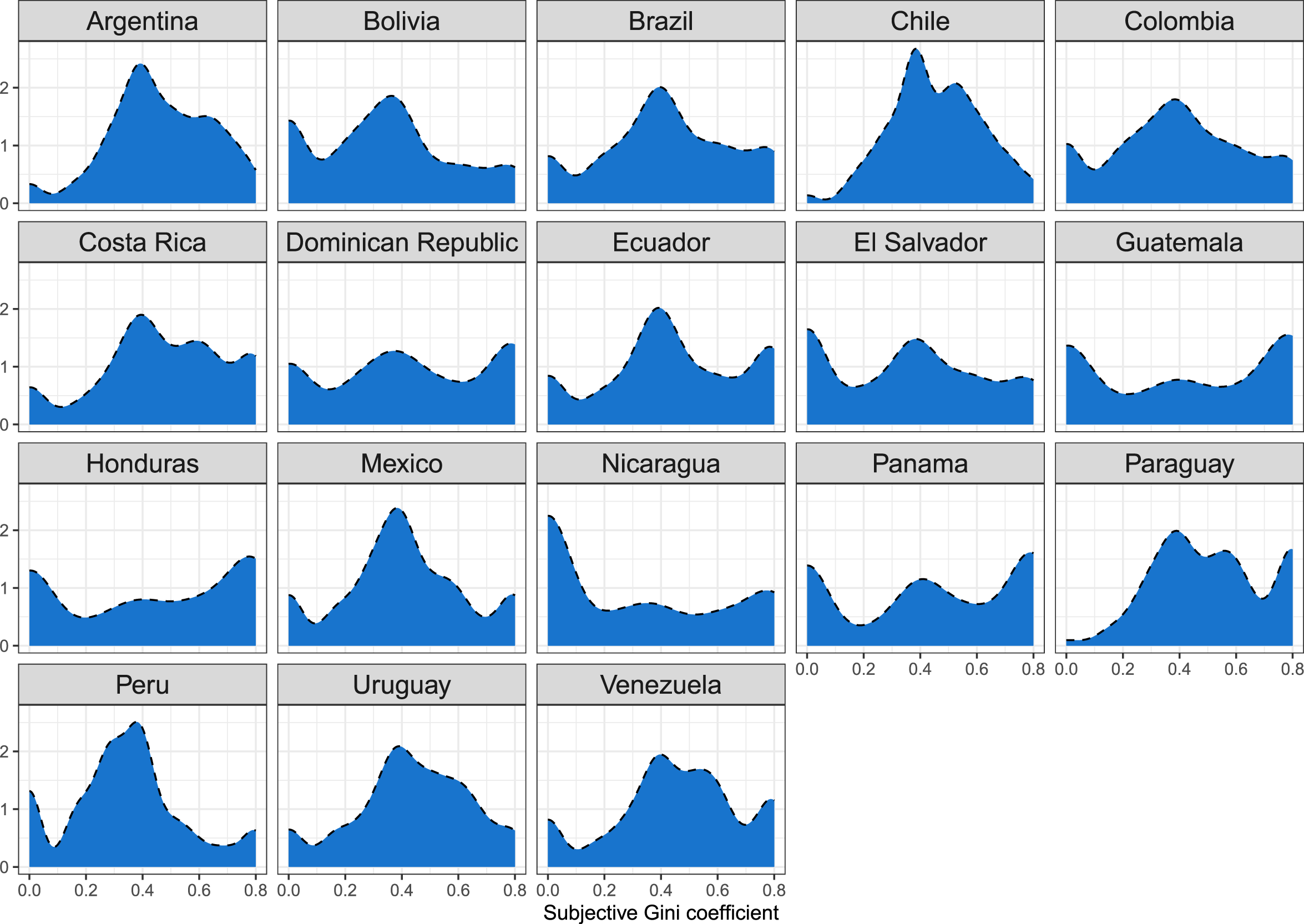

Figure 3 presents the density plots of the subjective Gini coefficient for each country. On average, perceived inequality is particularly high in Paraguay (0.52), Costa Rica (0.47), Argentina and Chile (0.46) and is comparatively low in El Salvador and Peru (0.34), Bolivia (0.33), and Nicaragua (0.29). The full results at the country level are displayed in Figure A3 in the Appendix. Density plots of the subjective Gini coefficient by country. Note. Author’s calculations based on data from Latinobarómetro 2020.

These patterns also raise the question of whether the subjective Gini coefficients are correlated with actual levels of inequality at the country level. Answering this question requires first an understanding of whether money is perceived by the respondents as a proxy for income or wealth as the latter tends to be considerably more unequal (e.g. Saez & Zucman, 2016; Sanroman & Santos, 2021). Since money is a stock variable, I assume that interpreting the subjective Gini coefficient as a measure of perceived wealth inequality is more accurate. While there is a scarcity of wealth surveys in Latin America (De Rosa et al., 2024, p. 4), the recent estimates of Gandelman and Lluberas (2023) from four countries in the region reveals that the Gini index of wealth inequality ranges between 0.7 and 0.81, implying that inequality may be underestimated by the respondents. In Figure A4 in the Appendix, however, I also present the relationship between the subjective Gini coefficient and the actual Gini coefficient of income inequality. The calculation of the latter is based on the World Bank (2022) data on the share of income held by each quintile of the population to create a comparable measure to the subjective coefficient. The figure indicates that there is no clear association between the two measures.

Empirical Strategy

To estimate the relationship between perceived inequality—as measured by the subjective Gini coefficient—and support for mass taxation, I employ linear and logistic regression models with taxthreshold and masstax as the dependent variables, respectively. 20 As noted above, the former variable represents the actual threshold level chosen by the respondents for values ranging between 1 and 10 while responses indicating that all households should pay taxes equally and that none of the households should pay taxes are recoded as 0 and 11, respectively. I examine the sensitivity of the findings for this decision in the robustness subsection. Moreover, while the use of a dichotomous dependent variable aligns with the theoretical distinction between mass taxation and class taxation, I acknowledge that in practice there is no specific value that distinguishes between the two. Therefore, the robustness subsection presents sensitivity tests for different thresholds levels other than the fifth income bracket for the variable masstax. As an alternative approach to evaluate the theoretical expectations, I also examine whether higher levels of perceived inequality are associated with increased support for class taxation by defining the variable classtax that equals 1 if the respondent indicates that only the richest household income group should pay taxes and 0 otherwise.

To account for unobserved heterogeneity across countries, country fixed effects are included in the regression models. In addition to inequality perceptions, the literature suggests that other factors might explain individuals’ preferences over the size of the tax base. Therefore, I include a range of control variables from the Latinobarómetro survey (Latinobarómetro Corporation, 2020). Following existing research (e.g., Armingeon & Weisstanner, 2022; Jaime-Castillo & Sáez-Lozano, 2016), economic self-interest and political ideology are the natural candidates although their association with redistributive preferences was generally found to be weak across the region with significant variation between countries (Bogliaccini & Luna, 2019). From a self-interest perspective, Barnes (2015) showed that the relationship is not necessarily linear across different income levels as the middle class is more likely to favour greater tax levels relative to both the poor and the rich. Therefore, I include the household income bracket indicated by the respondents between 1 and 10 where 10 represents the richest household income group and the squared term of this variable. I also include the subjective social class between 1 and 5 where 5 represents the lower class. In terms of ideological position, left-wing voters are more likely to favour greater public spending and redistribution however they might also have strong preferences for taxes on the rich. To look into this dimension, I include the respondents’ self-placement on a left-right scale between 0 and 10.

The literature also suggests that perceptions of the performance of the government (e.g., Aboagye & Hillbom, 2020; Stantcheva, 2021; Svallfors, 2013) might influence tax policy preferences. Moreover, attitudes towards taxation might be driven by satisfaction with democracy, as observed by Daude et al. (2013) in the context of tax morale. Hence, I include the respondents’ levels of trust in the three branches of government as well as their support and satisfaction with democracy. Finally, education group, age, age squared and a variable indicating whether the respondent is female are included to capture individual characteristics. Summary statistics are displayed in Table A1 in the Appendix.

After the exclusion of observations from the main dependent and independent variables, the number of observations drops from 20,204 in the original survey to 10,618, and further reduces to 7,431 in the extended models due to missing and uninterpretable data in the control variables. Table A2 in the Appendix mitigates the concern that this creates a bias by showing that there are no considerable differences in the main control variables between the sample data used for the analysis and the wider survey data set. Moreover, models with gradual addition of control variables and multiple imputation are presented in the robustness checks.

The empirical analysis also attempts to shed light on the potential mechanisms at play. For this purpose, I conduct a mediation analysis (Baron & Kenny, 1986; Imai et al., 2011). While the article adheres to the widely used terminology of mediation models (Imai et al., 2011), an important caveat is that the findings should be interpreted as suggestive rather than causal due to the cross-sectional nature of the data and given that mediation analysis requires strong assumptions. In particular, in addition to unconfoundedness, it requires the absence of unmeasured confounders in the relationship between the mediator and the dependent variable (‘sequential ignorability’). The subsection of the results that evaluates the mechanisms should therefore be seen as exploratory, laying the groundwork for future investigations. Following the theoretical discussion, I consider the role of fairness views, reciprocity, and belief in meritocracy as potential mediators using questions from the Latinobarómtero 2020 (Latinobarómetro Corporation, 2020). Fairness is measured through respondents’ evaluation of the degree of fairness in the distribution of income between 1 (‘very fair’) and 4 (‘very unfair’). Reciprocity is estimated using an index that intends to capture the perceptions of individuals towards the provision of public services. Specifically, the index is based on questions about trust in public hospitals, the likelihood that the local authority will listen to the respondents when they report a problem in their neighbourhood, and the likelihood that the respondents will complain to the police in case they are victims of a minor crime. It ranges between 0–1 with equal weight for each question. Higher values indicate a more positive perception of public services. Finally, perceived meritocracy is estimated based on whether the respondent agrees with the statement that the rich get more than they should for their effort.

Results

Main Findings

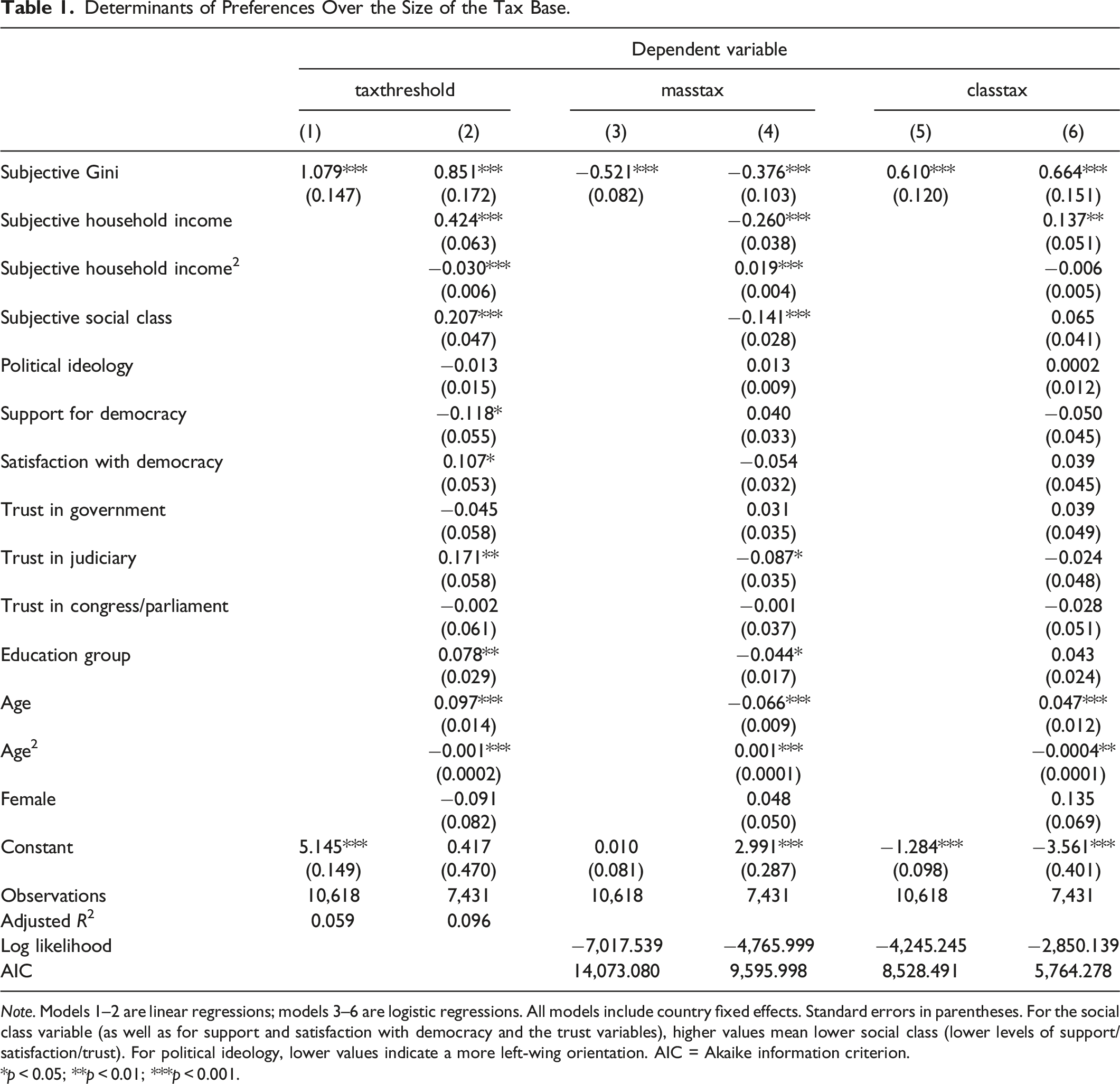

Determinants of Preferences Over the Size of the Tax Base.

Note. Models 1–2 are linear regressions; models 3–6 are logistic regressions. All models include country fixed effects. Standard errors in parentheses. For the social class variable (as well as for support and satisfaction with democracy and the trust variables), higher values mean lower social class (lower levels of support/satisfaction/trust). For political ideology, lower values indicate a more left-wing orientation. AIC = Akaike information criterion.

*p

In regard to the control variables, the coefficients for subjective household income and its squared term imply that support for mass taxation initially decreases with higher income however the relationship turns positive from a certain income level. From a class perspective, in turn, individuals that position themselves higher across the social ladder are more likely to favour broader tax bases as lower values represent higher socio-economic status. The findings also suggests that political ideology is not closely linked to preferences over the size of the tax base, thereby coinciding with Bogliaccini and Luna (2019) who draw a similar conclusion in the context of redistributive preferences. Contrary to expectations, model 2 points to a surprising positive association between support for democracy and preferences for higher tax threshold however this association is statistically insignificant in the logistic regression specification. The coefficients for trust in the judiciary in models 2,4 indicate that greater confidence in the judicial system is linked to increased support for mass taxation. Lastly, education group and age are strong predictors of advocacy for mass taxation and the coefficients imply a negative relationship for the former and a non-linear relationship for the latter where support for broader tax bases initially decreases with age but subsequently tends to increase from a certain age.

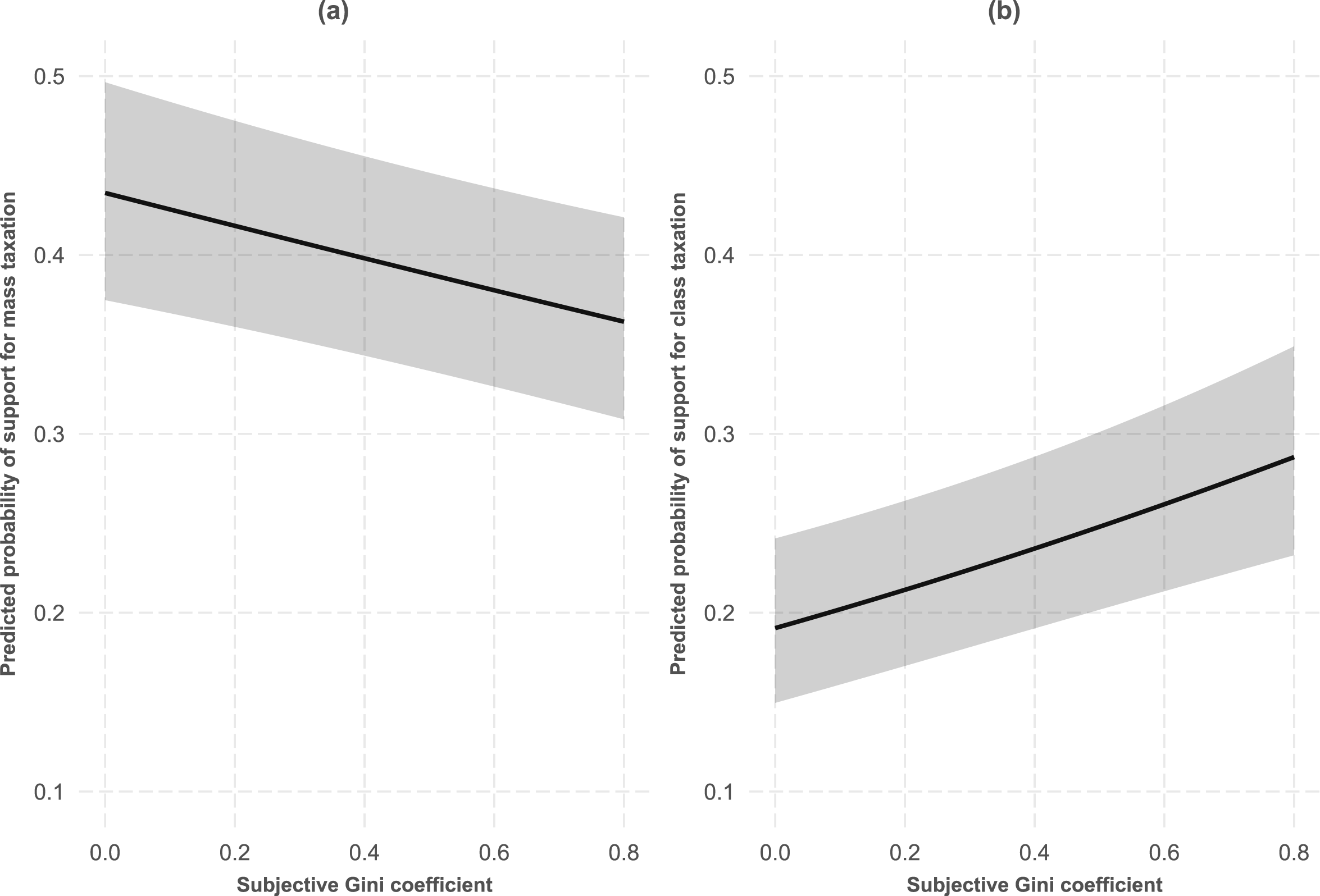

The results also show that the subjective Gini coefficient strongly predicts support for class taxation. As models 5–6 indicate, at higher levels of perceived inequality, individuals are considerably more likely to favour a narrow tax base that includes only the households in the top decile. In fact, the subjective Gini coefficient is the only variable that is significantly associated with support for class taxation apart from age and subjective household income. Figure 4 illustrates the findings by plotting the predicted probabilities for the variables masstax (Panel a) and classtax (Panel b) for different values of the subjective Gini coefficient. Taken together, the analysis demonstrates that a consensus in favour of reforms aiming at the expansion of the tax base is more likely to emerge in societies that are perceived as more egalitarian and less likely to emerge in societies perceived as highly unequal. Predicted values for support for mass taxation and support for class taxation across different values of the subjective Gini coefficient. Note. 95% confidence intervals are shown in the shaded areas. (a) Support for mass taxation, (b) Support for class taxation.

Finally, I consider the possibility that the relationship between perceived inequality and preferences over the tax threshold can be fully captured by ideology and self-interest (Bobzien, 2020). Table 1 already suggests that the association of the former variable with support for mass taxation is weak and insignificant. This pattern remains unchanged in a simple model with no control variables (Table A3 in the Appendix). Thus, whereas left-wing political orientation is associated with higher perceived inequality (models 2–3), there is no evidence that political orientation is closely linked to preferences over the tax threshold at all. In regard to social class, individuals that rank themselves lower in terms of socio-economic status are associated with higher perceived inequality (Table A3; model 2–3). Moreover, when the subjective Gini coefficient is omitted from the baseline analysis with taxthreshold as the dependent variable, the coefficient of subjective social class slightly increases (models 4–5), pointing to the possibility of a small mediation effect. Nonetheless, I interpret these findings as indicative that the variation of inequality perceptions is mostly unrelated to self-interest and ideology. First, the low adjusted R-squared in model 2 suggests that only a small proportion of the variation in perceived inequality can be explained by these two variables. Second, even if inequality perceptions mediate the relationship between subjective social status and support for mass taxation, the extent of such relationship appears to be modest. The findings thus lend credence to the proposition that the inclusion of perceived inequality in the analysis contributes to our understanding of tax policy preferences in Latin America in a way that is, at the very least, largely unexplained by the standard control variables.

Robustness Checks

To assess the consistency of the main findings, I conduct various robustness checks. First, Tables A4–A6 in the Appendix present the results with gradual addition of the control variables. As an alternative, I also fill in missing values in the control variables by applying multiple imputation using the classification and regression trees (CART) method (Table A7). 22 The results support the main findings. Second, I examine whether the results of model 1–2 are driven by my decision to recode the answers that indicate that all households should pay the same and none of the households should pay taxes as 0 and 11, respectively, by excluding these answers from the analysis. The findings remain significant. Third, I investigate whether the baseline models are sensitive to the definition of masstax. This test allows to identify whether modifying the threshold for mass taxation to other values in the neighbourhood of the baseline definition considerably affects the outcome. Specifically, I define the variables masstax6 and masstax4 as binary variables representing the willingness of individuals to place the tax threshold at the sixth and fourth (or lower) income groups, respectively. The results (Table A9, models 1–2) mitigate this concern by illustrating that the relationship between perceived inequality and advocacy for mass taxation remains statistically significantly. This conclusion holds when the threshold is set at the third and the seventh income brackets (models 3–4).

I also run the analysis only for observations that do not have any missing data in the five variables considered for the calculation of the subjective Gini coefficient. Drawing on this approach, the association between perceived inequality and support for mass taxation is in fact stronger than the baseline analysis (Table A10). Furthermore, the results hold when the other two assumptions of the baseline analysis are modified as well—that is, when observations in which a poorer group has more money than a richer group are included and when the analysis only includes observations in which the total amount for the five quintiles is 100 (Table A11). Finally, I run the baseline regressions on an alternative dependent variable named selftax, which equals 1 for respondents that include their own household income bracket in their preferred tax base or mention that all households should pay the same and 0 otherwise. Markedly, the results show that the subjective Gini coefficient is a strong predictor of this variable, indicating that individuals are more willing to be included in the income tax base at lower levels of perceived inequality (Table A12).

Further Analysis

Next, I evaluate whether the tendency of individuals to prefer narrower tax bases at higher levels of perceived inequality is mainly driven by subjective estimates of high concentration of wealth at the top of the distribution or by the perception that lower and middle-class households own little. I address this question by decomposing the subjective Gini coefficient into five components which correspond to the estimated share of wealth held by each quintile. The findings (Table A13) show that all five components are strongly associated with support for mass taxation. Whereas estimates of higher concentration of wealth among the upper quintile are linked to growing demand for a smaller tax base (model 1), the opposite is true regarding the perceived share of wealth held by the three middle quintiles and the bottom quintile (models 2–5).

In addition to quantitative estimates, I explore whether the strong association between inequality and the preferred size of the tax base carries over to individuals’ normative perceptions of inequality. Unlike the subjective Gini coefficient that reflects a quantitative estimate of inequality, the normative measures are based on questions in which individuals expressed their opinions on the level of inequality and whether they see the economic gaps in society as a major problem. First, I use a question from the Latinobarómtero survey (Latinobarómetro Corporation, 2020) asking respondents for their views on the level of inequality in their country between 1 (‘completely unacceptable’) and 10 (‘completely acceptable’). I refer to this variable as a measure of tolerance for the level of inequality. Second, drawing on a different question from the same survey asking participants to mention the worst expressions of inequality in their country out of fifteen options, I examine whether views of income inequality and views of inequality between rich and poor as the worst forms of inequality are associated with support for mass taxation. The results (Table A14) point to a negative and statistically significant relationship between normative perceptions of inequality and support for mass taxation for all three variables. The findings thus suggest that not only quantitative estimates but also normative views of inequality matter for the formation of individuals’ preferences over the size of the tax base.

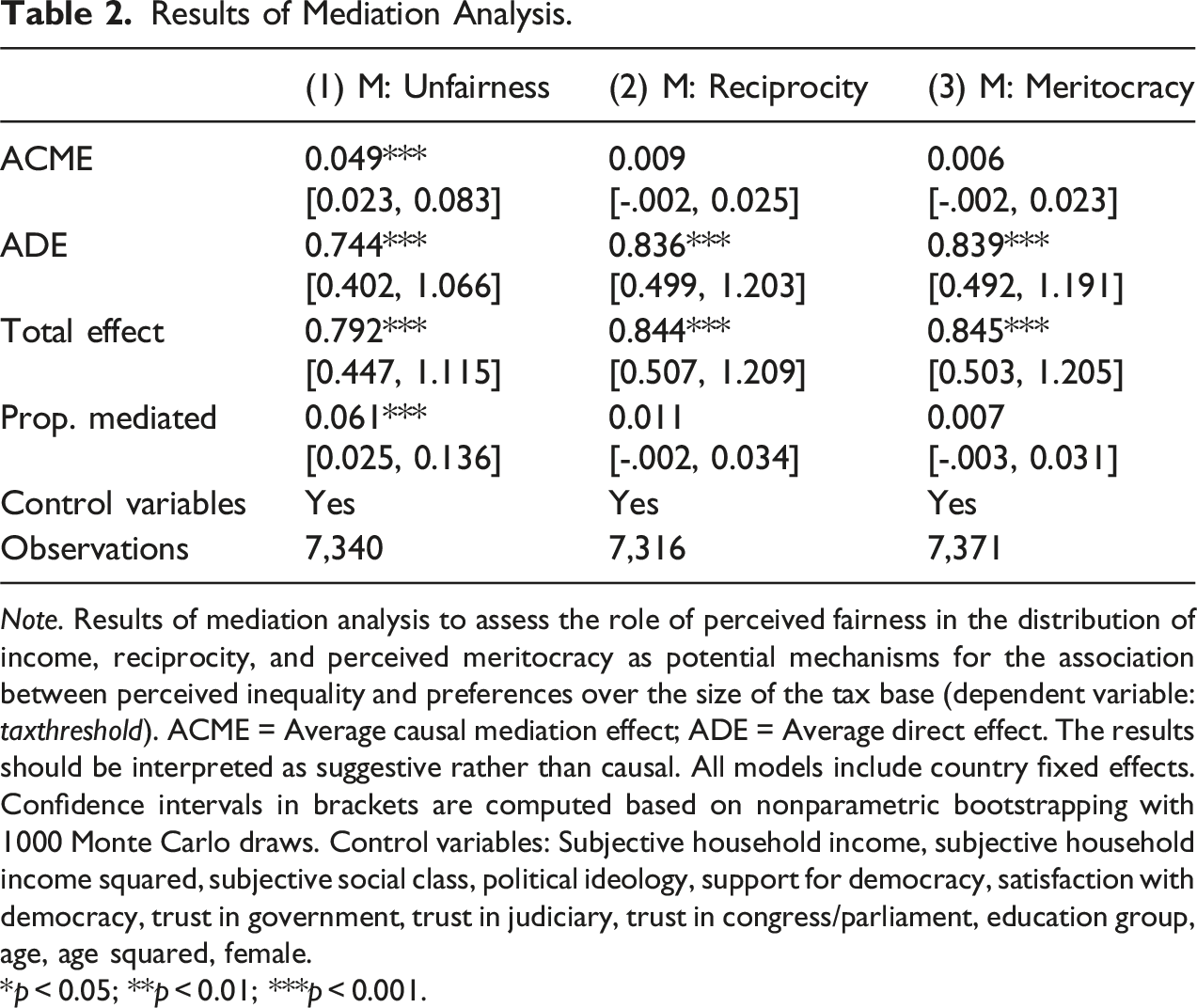

Mechanisms

Results of Mediation Analysis.

Note. Results of mediation analysis to assess the role of perceived fairness in the distribution of income, reciprocity, and perceived meritocracy as potential mechanisms for the association between perceived inequality and preferences over the size of the tax base (dependent variable: taxthreshold). ACME = Average causal mediation effect; ADE = Average direct effect. The results should be interpreted as suggestive rather than causal. All models include country fixed effects. Confidence intervals in brackets are computed based on nonparametric bootstrapping with 1000 Monte Carlo draws. Control variables: Subjective household income, subjective household income squared, subjective social class, political ideology, support for democracy, satisfaction with democracy, trust in government, trust in judiciary, trust in congress/parliament, education group, age, age squared, female.

*p

The analysis indicates that a potential channel through which inequality perceptions shape preferences over the size of the tax base is through fairness considerations. As Table A15 shows, the signs of the coefficients match the theoretical expectations. Higher levels of perceived inequality are linked to greater perceived unfairness in the distribution of income (models 1,3), which in turn is associated with support for higher income tax threshold (models 2,4). In total, 6.1% of the total effect of perceived inequality on preferences over the tax threshold is mediated through perceived unfairness and this indirect effect (also called average causal mediation effect, ACME) is statistically significant (Table 2, model 1). As noted above, these findings should be seen as suggestive rather than causal due to the strong assumptions of mediation analysis. This is particularly true considering that sensitivity analysis (Tingley et al., 2014) indicates that the results are sensitive to violations of sequential ignorability (see Figure A5). Furthermore, it is possible that individuals, given a certain level of inequality aversion, directly adjust their tax policy preferences in response to changes in perceived inequality (Iacono & Ranaldi, 2021), implying that broader views about fairness might serve as a moderator in the relationship between perceived inequality and support for mass taxation.

In regard to reciprocity and meritocracy, the signs of the coefficients are in line with theoretical expectations. Markedly, the subjective Gini coefficient is negatively associated with attitudes towards reciprocity and perceived meritocracy and in both cases the relationship is statistically significant (models 1, 3 in Tables A16–A17). Moreover, both meritocracy and reciprocity are inversely associated with taxthreshold, implying that a more positive perception of public services and stronger belief in meritocracy are linked to increased support for mass taxation (models 2,4 in Tables A16–A17). The latter relationships, however, are statistically insignificant with the exception of the association between reciprocity and support for mass taxation in the simple model. Thus, there is no evidence of a statistically significant mediation effect for both variables (Table 2, models 2–3). As the regression coefficients conform to theoretical expectations, the possibility that mediation effect will be observed in a time series framework can be evaluated in future research.

Case Study: The Colombian Tax Reform of 2021

In this subsection, I examine whether the theory developed in this article provides valuable insights into the proposed tax reform in Colombia in 2021 and the fierce opposition it generated. The reform sought to raise public funds for social expenditures during the COVID-19 pandemic by introducing significant changes to the tax system. However, in May 2021, the tax reform bill was withdrawn by President Ivan Duque following mass protests which in some cases turned violent (Long, 2021; The Economist, 2021).

This case study is important for three reasons. First, the timing of the proposed reform. The mass uprising that led to the withdrawal of the reform took place shortly after the Latinobarómtero survey, which in Colombia was held in November–December 2020. Second, one of the main pillars of the original reform was the expansion of the tax base through the lowering of the income tax threshold (The Economist, 2021), making it highly relevant for the context of this analysis. Third, there are strong indications that inequality was a major factor driving the opposition to the reform (Bernal & Ortiz, 2022; Sanin, 2022). In particular, the proposed changes were widely seen as unfair (Long, 2021; The Economist, 2021) at times of deteriorating economic conditions. The protests also had direct implications for policymaking. A modified version of the reform, which was approved in September 2021, ultimately focused on increasing taxes on corporates (Long, 2021; Vargas, 2021). My aim is therefore to assess the nature and magnitude of the relationship between inequality perceptions and preferences over the tax threshold in this particular context by estimating the baseline regression models using data from Colombia only.

The findings reveal that the association between perceived inequality and support for mass taxation in Colombia is negative and statistically significant (Table A18). The magnitude of the relationship is considerably larger than the main analysis. The results of model 2 suggest that, ceteris paribus, a one standard deviation increase in the subjective Gini coefficient is associated with 1.03 units increase in taxthreshold or 17.5% increase relative to the mean of this variable (0.21 and 3.9%, respectively, in the main analysis).

24

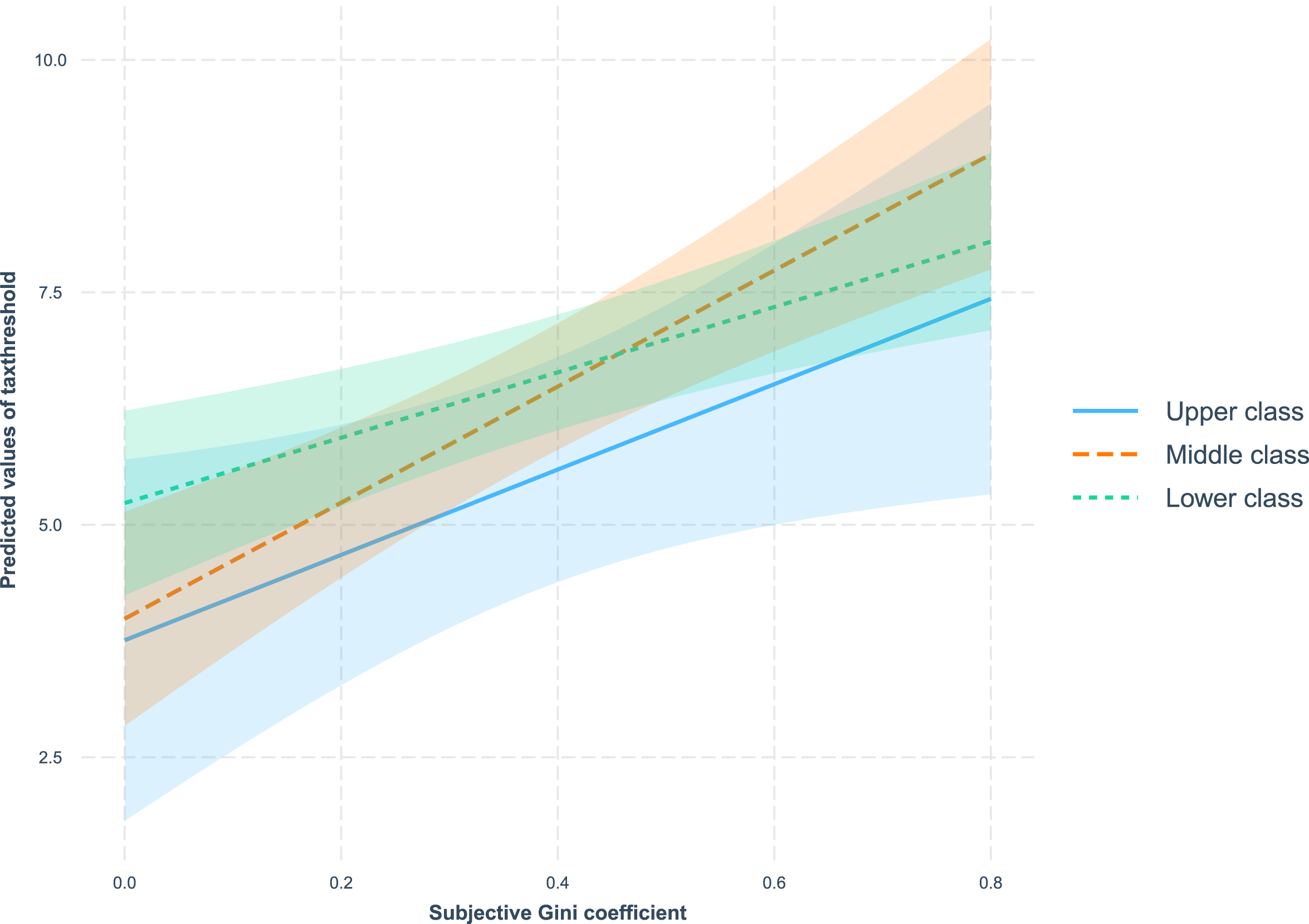

In addition, the potential fiscal consequences for the Colombian middle class and its presence in the protests have been stressed in accounts of the reform (e.g., Bernal & Ortiz, 2022). To evaluate the strength of the relationship for different groups in society, I also run a model with an interaction term between the subjective Gini coefficient and social class (Table A18, model 7). Given the likelihood of a middle-class bias (Evans & Kelley, 2004), I group individuals that placed themselves in the upper and upper-middle classes together as the upper class and respondents that placed themselves in the lower and lower-middle classes as the lower class. As Figure 5 illustrates, the association between higher perceived inequality and preferences for narrower tax bases applies to all classes however it is substantively more pronounced among the middle class. Considering the middle class itself as the reference category, the interaction coefficient is also statistically significant at the 10% level (t = −1.768) compared to the lower class and statistically insignificant relative to the upper class although the latter represents only 10.5% of the observations, implying greater uncertainty. Predicted relationship between subjective Gini coefficient and the variable taxthreshold by social class in Colombia. Note. 95% confidence intervals are shown in the shaded areas.

In conclusion, this case study illustrates the connection between perceived inequality and tax policy preferences and how such relationship can shape fiscal policymaking in general and the feasibility of tax base expansions in particular. In doing so, it also mitigates the concern of reverse causality by suggesting that it is the level of perceived inequality that influences individuals’ preferences over the size of the tax base rather than the opposite causal direction.

Perceived Inequality and Willingness to Pay Taxes in Chile

To further investigate the relationship between perceived inequality and individuals’ tax policy preferences, I analyse data from a public opinion survey of the United Nations Development Programme (UNDP) that was conducted in Chile between 2015 and 2017 (PNUD, 2017). The survey includes a series of questions on inequality perceptions in general as well as in specific domains. The answers range between 1 (‘very equal’) and 10 (‘very unequal’). In particular, my main independent variable of interest is the perceived level of inequality in income.

Although it does not include a question about the preferred tax threshold, the survey asks respondents about their willingness to pay more taxes between 1 (‘strongly agree’) and 5 (‘strongly disagree’). I consider this question highly pertinent for the analysis because base-broadening measures imply that at least some individuals will have to pay more taxes. Compared to questions about the degree of justification for tax evasion, which have been used as a proxy for tax morale (e.g., OECD, 2019), this question is also less susceptible to social desirability bias. In line with the theoretical framework presented above, I expect that individuals’ willingness to pay more taxes declines at higher levels of perceived inequality. The regression models contain similar control variables as in the main analysis with the exception of questions on the levels of trust in the branches of government that are not included in the UNDP survey. A large number of respondents (54.5%) did not indicate their political position, which in this survey ranges between 1 (right) and 5 (left). In this case, as well as for respondents that defined themselves as independents (4.6%), the mean value of this variable is used as a proxy. 25 As an alternative, I also implement multiple imputation for this variable and for missing values in the other control variables.

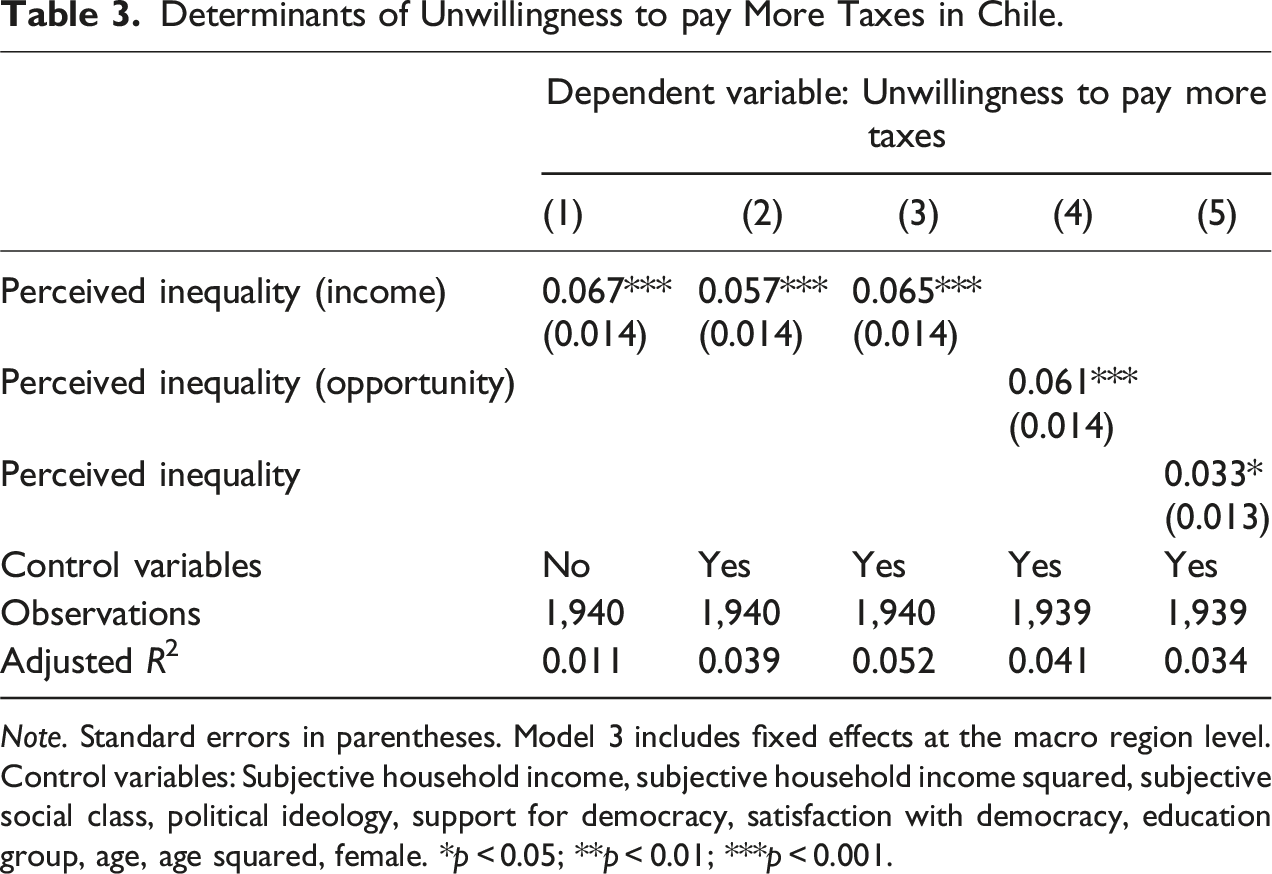

Determinants of Unwillingness to pay More Taxes in Chile.

Note. Standard errors in parentheses. Model 3 includes fixed effects at the macro region level. Control variables: Subjective household income, subjective household income squared, subjective social class, political ideology, support for democracy, satisfaction with democracy, education group, age, age squared, female. *p

It should be noted that in contrast to the findings for Colombia, in Chile the relationship between perceived inequality and support for mass taxation using the Latinobarómetro data (Latinobarómetro Corporation, 2020) shows the opposite sign with the exception of model 6 (Table A21). In other words, in models 1–5 higher perceived inequality is associated with stronger support for mass taxation. However, these results are statistically insignificant even without control variables. Moreover, the sign of the coefficients is in line with expectations in most specifications when the baseline assumptions are modified (Table A22).

Conclusion

What explains the persistence of narrow income tax bases and high levels of inequality in Latin America, notwithstanding decades of democratic consolidation? In this article, I have proposed a new explanation for this puzzle by arguing that a widespread subjective perception of high economic inequality hinders the advent of mass taxation—a broad-based income tax that includes large parts of society. As a departure from the conventional focus on elites in analysing the development of fiscal capacity in the region (Cárdenas, 2010; Fairfield, 2015; Hollenbach & Silva, 2019), this article underscores the role of perceived inequality in shaping the demand side for fiscal transformation. Specifically, I have shown that a consensus in favour of mass taxation is more likely to emerge in societies with lower levels of perceived inequality. In contrast, reforms that seek to broaden the tax base are expected to encounter greater opposition in societies widely seen as highly unequal.

By highlighting the connection between micro-level perceptions of inequality and macro-level tax policy, the findings provide a new perspective on the challenges of public finance in Latin America. To tackle inequality profoundly and embark on ‘hard redistribution’ (Holland & Schneider, 2017), states need to improve and extend the provision of public services, which in turn requires the expansion of narrow tax bases. Yet obtaining substantial public legitimacy for this purpose may become harder due to high levels of perceived inequality in the first place. In settings perceived as highly inegalitarian, individuals tend to be more supportive of class taxation that consists solely of the richest households. Consequently, high levels of perceived inequality may induce smaller governments with more limited fiscal and redistributive capacities. In a broader sense, it can be argued that economic inequality poses a dual threat for the development of fiscal capacity. On the one hand, as previous works have shown (e.g., Ardanaz & Scartascini, 2013; Hollenbach & Silva, 2019; Sokoloff & Zolt, 2012), elites are more likely to channel the direction of the tax system for their own material interests. On the other hand, as this study points out, a widespread perception of high inequality undermines the scope for tax reforms as societies perceived as more unequal are more likely to resist to mass taxation.

The article also corresponds with the wider political economy literature on the relationship between perceived inequality and fiscal policy preferences. Earlier research on this topic has mainly focused on general statements about the responsibility of governments to reduce income differences as the dependent variable of interest (Bobzien, 2020; Choi, 2019; Gimpelson & Treisman, 2018). This article, in turn, reveals that the level of perceived inequality predicts concrete policy preferences. This reinforces the claim that subjective perceptions, rather than objective measures, should be at the core of theories addressing the political consequences of inequality (Gimpelson & Treisman, 2018).

Finally, I propose several avenues for future research. First, although the theoretical underpinnings of the relationship in conjunction with the empirical findings strongly imply that the level of perceived inequality influences preferences over the tax threshold, the possibility of reverse causality cannot be entirely ruled out using cross-sectional observational data. Experimental and quasi-experimental designs can be applied to examine causal pathways. Second, future studies can look into intra-regional heterogeneity in the relationship between perceived inequality and tax policy preferences in Latin America and its underlying causes. Third, researchers can test whether the findings presented in this article extend to other countries and regions. Lastly, gaining a deeper understanding of the determinants of perceived inequality is essential to enhance our knowledge of the specific contexts in which individuals are likely to modify their tax policy preferences.

Supplemental Material

Supplemental Material - Perceived Inequality as an Impediment to Mass Taxation: Evidence From Latin America

Supplemental Material for Perceived Inequality as an Impediment to Mass Taxation: Evidence From Latin America by Guy Heilbrun in Comparative Political Studies.

Footnotes

Acknowledgments

I am grateful to Julian Limberg, Amrita Dhillon, David Hope, Yotam Margalit, Bouke Klein Teeselink, Daniel H. Alves, Amy Bruck, Irene Germani, Gabriela Aguirre, and the participants in the London Seminar in Graduate Political Science (2023) and the panel ‘Welfare States and Public Opinion’ at the General Conference of the European Consortium for Political Research (ECPR, 2023) for their insightful feedback. I also thank the editors of Comparative Political Studies and three anonymous reviewers for their valuable comments and suggestions.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Correction (June 2025):

Article updated to include reference Arel-Bundock, 2022 and in displayed reference list.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biography

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.