Abstract

Before the 19th century, nearly all central banks financed government spending, but as the centuries passed direct government financing became taboo. Using original data from 69 central banks established between 1600-1914, this study traces a shift away from government financing and towards increased support for private sector credit via discounting commercial bills of exchange beginning in the 18th century. What drove this transformation in central bank credit policies? Evidence suggests that central bank credit policies are driven by the composition of a government’s supporting coalition, rather than structural economic forces. Security-minded interest groups motivate governments to establish central banks that lend back to themselves, while economic interest groups motivate governments to establish central banks that discount bills of exchange. Discrete time survival analysis supports these contentions. This research highlights how political-historical context and the preferences of specific interest groups shaped the long-term evolution of central banking.

A consensus in political science and economics research finds that most of the earliest central banks were established to either enhance the efficiency of settling payments or to provide direct financing to their government (Bindseil, 2019a; Broz, 1998; Cameron, 1967; Goodhart, 1988). The latter rationale is particularly intriguing for several reasons, not least because this arrangement may have served as a crude but effective early mechanism for a government to credibly signal its commitment to repaying its debt (Knight, 2021; Poast, 2015). Be that as it may, fast forward several centuries and the practice of central banks directly financing government expenditure in the primary debt market is now decidedly taboo (Jácome et al., 2012). 1 One of the contributions of this article is an original dataset demonstrating that as central banks shifted away from direct government financing, they progressively enhanced their ability to support private sector credit access, particularly through the discounting of commercial bills of exchange. Considering the strong incentives governments had to retain a direct financing arrangement with their central bank, what explains this transformation in central bank credit policies?

The shift in focus to facilitate the private sector’s access to credit was a critically important step in the modernization of central banks (Mehrling, 2010). Despite this, there are surprisingly few concrete explanations for this transformation. In the economic history literature, studies often focus on other aspects of central banking, such as their role in facilitating payments (Bindseil, 2019a), standardizing and consolidating banknote issuance (Bordo & Siklos, 2018; Siklos, 2002) or their evolution into lenders of last resort (Goodhart, 1988; Gorton, 1985). Other studies focusing on the modern period are often grounded in the central bank independence literature and focus on the incentives governments have to restrain themselves from direct central bank financing. These incentives may include to attract international capital (Bodea & Hicks, 2015a), achieve a lower rate of inflation (Garriga & Rodriguez, 2020), or to enhance their central bank’s crisis-fighting capability (Gavin, 2020). With a focus on the transformation in central bank credit policies, this study advances our understanding of the political forces propelling a critical aspect of the modernization of central banks, from their role as agents directly financing governments to agents that predominantly support the private sector.

I develop and test a simple political economy theory of central bank credit policies. My theory implies that central bank credit policies hinge on the relative standing of certain interest groups, particularly those the government deems essential for maintaining power. When a government considers military interests critically important, central banks are more likely to lend directly to the government due to the greater need to allocate funds for the military and to enhance internal and external security. Conversely, when business interests are key to a government’s hold on power, central banks are more likely to support the credit needs of private actors.

Supporting evidence is derived from an original dataset cataloguing the historical functions of central banks. 2 In total, the dataset codes primary sources including charters, laws, and statutes for 69 central banks established between 1600-1914. The dataset aims for worldwide coverage and includes institutions in Asia and South America not typically covered in studies of early central banking. The dataset shows that starting in the 1780s central bank charters became more likely to mention private sector discounting, decades earlier than would be expected if central banks were merely financiers of their government. Furthermore, the transition away from government financing picked up speed following the Napoleonic wars. Thus, between 1750 and 1914 there was a dramatic transformation in central bank credit policies: in 1750, 100% of central banks lent to their governments and only 22% engaged in discounting while in 1914 a modest plurality continued to lend to their governments while nearly all central banks discounted bills of exchange. Discrete time survival analyses corroborate the theory that central banks are more likely to be tasked with financing their government or discounting bills of exchange when their government’s supporting coalition contains key military or economic interest groups, respectively.

The turn away from direct government financing and towards supporting private sector actors was one of the most consequential transformations in central banking in the last several hundred years. This shift not only redefined the operational priorities of central banks but also laid the groundwork for their modern roles as stabilizers of financial systems and lenders of last resort (Mehrling, 2010; Schneider, 2022). By documenting the influence of political dynamics and the relative salience of different interest groups, this research underscores the significance of political context in shaping the long-term evolution of central banking. Thus, quintessential central banking functions did not, as argued famously by Goodhart (1988), evolve “naturally” from structural economic tendencies, but from deeper political processes brought about by industrialization and rising prosperity that incentivized governments to curtail their own desires for direct financing in order to prioritize the preferences of private sector actors.

The Origins of Central Banks and their Functions

A central bank serves as the primary monetary authority of a state (or group of states) and derive their authority from their public charter. Charters grant banks the legal authority to operate and detail their legal framework, responsibilities, and permitted activities. The privileges and opportunities specified in the charter often enhance the bank’s value and importance. Though the issuance of public charters has been an integral aspect of central banking since at least the 15th century, the functions assigned to central banks have undergone dramatic changes since that time. Contemporary central banks are typically tasked with managing the currency, coordinating economy-wide interest rates, and influencing credit creation, primarily with the intent to target inflation and/or the exchange rate. Although ubiquitous today and having largely converged on a basic set of aims and functions, many of the world’s central banks began from very different starting points.

Economic historians have traditionally interpreted the emergence and long-term evolution of central banking as a matter of economic rationality. Under this view, governments established central banks to overcome an economic or financial problem. For example, in the early 17th century, a plethora of domestic and foreign coins, many debased and of uncertain value, were flooding hubs of European merchant trade. In this context, Quinn and Roberds (2006) argue that the City of Amsterdam founded the Bank of Amsterdam (BOA) in 1609 to settle payments between merchants directly on its balance sheet rather than through an exchange of coins. As a “ledger-money bank”, Roberds and Velde (2014) argue that the BOA was one of the very first central banks. The BOA model was also applied in other merchant trading cities, most notably when the City of Hamburg founded the Hamburger Bank (HB) in 1619. Payments continued to motivate the founding of central banks into the 19th and 20th centuries, as several central banks were established, in part, to consolidate and standardize banknote issuance. Examples include the Norges Bank (Bank of Norway, established 1816) (Siklos, 2002), the Oesterreichische National-Bank (Austrian National Bank, established 1816) (Jobst & Kernbauer, 2016), and the Schweizerische Nationalbank (Swiss National Bank, established 1907) (Bordo & Siklos, 2018).

A focus on payment system efficiency is characteristic of the functional approach evident in the recent literature on early central banking. The functional perspective shifts the focus from defining what central banks are as institutions to examining what central banks do (Ugolini, 2017). A functional approach to central banking has several practical advantages. First, although specific practices and institutional forms of central banks have evolved significantly over time, the essential features of core central banking functions are comparatively stable. As argued by Ugolini (2017), even if the manner in which a central bank performs particular functions, such as issuing banknotes, acting as the government’s banker, or discounting bills of exchange, changes over time, the concepts defining these functions remain recognizable across large stretches of time. Second, because some central banks perform only one or a handful of functions, while others perform many, the functional approach captures institutions that perform central banking functions even when these institutions are not recognized as fully formed central banks. Declaring a central bank as any institution that issues central bank money – money of the highest possible quality used to settle payments – Bindseil (2019a) concurs that the BOA and HB were genuine central banks and that the earliest plausible central bank may have been Taula de Canvi established in Barcelona in 1412.

Aspects of the lending capabilities of central banks feature in the literature on the origins and evolution of central banks. Goodhart (1988) famously argues that modern central banking, and particularly the lender of last resort function, emerged naturally from a tendency for the bulk of a banking system’s gold and silver reserves to migrate to a single large institution. Mehrling (2010) likewise argues that in the case of the Bank of England (BOE) periodic financial crises led it to recognize its unique role as the central repository of cash reserves for the entire banking system, resulting in the development of central bank management principles that prioritized system stability over shareholder profits. This recognition also influenced the BOE’s unique approach to discounting bills of exchange, the function through which the BOE facilitated emergency lending during times of crisis. Gorton (1985) also argues that the Federal Reserve was, in part, established to act as a lender of last resort as it replaced the privately organized clearinghouse system that managed bouts of illiquidity in the United States.

The political science literature examining the emergence and evolution of central banking, though less extensive than that in economics, is also grounded in the unique lending capabilities of central banks. Broz (1998) and Elgie and Thompson (2012) argue that governments, particularly in times of war, created central banks to secure crucial access to credit, often granting these institutions special privileges such as the monopoly to issue banknotes or the authority to act as the government’s banker and thereby hold government deposits, facilitate payments, and manage its debt. 3 The BOE exemplifies this dynamic, as its special status was designed to offset the risks associated with lending to a sovereign at war (Knight, 2021; Poast, 2015). Calomiris and Haber (2015) similarly show that government fiscal motives were instrumental in shaping central bank design. The case of Brazil is a straightforward example in this respect. As the authors note, the Banco do Brazil was founded in 1808, in part, to finance state operations primarily by issuing currency to buy government bonds, thus enabling Brazil to raise funds without directly taxing its elites.

Beyond their own fiscal needs, governments must also navigate the competing demands of different interest groups when designing central banks, often shaping policies to accommodate both public goals and private pressures. (Meltzer, 2010, 2011) highlights how the Federal Reserve’s creation in 1913 was heavily influenced by banking interests seeking a central bank that would stabilize financial markets. Similarly, the Banque de France, established by Napoleon in 1800, served both the state’s financial needs and the interests of private bankers who sought control over credit and a stable currency (Rouanet, 2021). This influence of interest groups extends to modern central banking practices as well. Vukovic (2021) demonstrates how political lobbying influenced government decisions during the 2008 global financial crisis, with firms that had stronger political ties receiving more favorable bailout terms.

The literature therefore advances important insights into the economic and political factors driving aspects of early and modern central bank credit policies. The valuable contributions from across the broad themes of economic rationality, government fiscal motives, and interest group pressures notwithstanding, there remain several important unanswered puzzles. Why did some governments prioritize their own credit needs while others prioritized the preferences of the private sector? What explains the transformation in credit priorities we observe over long time scales? As the dataset introduced below shows, government credit was a priority for nearly all early central banks and still a significant fraction well into the late 19th century. However, there is also a clear trend towards assisting the private sector starting in the 18th century. In the next section, I outline some brief case studies that demonstrate that certain governments prioritized lending to themselves, others prioritized the private sector, and others still prioritized both. The aim is to use the cases to inductively build a theory to explain why governments opted to endow their central bank with the credit policies they did, both across space and time.

Central Bank Credit Policies, Some Illustrative Cases

England

It is generally acknowledged that the establishment of the BOE in 1694 was driven by the desires of the English Crown to fund its war effort against France. Parliament accepted the plan of William Paterson, which involved raising £1.2 million from subscribers, which was then loaned to the Crown in exchange for securing several exclusive privileges, including being the only joint stock bank allowed in England, being the sole authority to manage government loans, and having the right to issue banknotes. This quid pro quo has been described as an arrangement enabling the Crown to resolve issues of time inconsistency and to enhance the credibility of debt repayment commitments (Broz, 1998).

In addition to funding the Crown, the BOE also made strides to enhance the private sector’s access to credit. Credit to the private sector was facilitated by discounting bills of exchange and, on occasion, advances on deposit facilities (Bindseil, 2019a) 4 . Bills of exchange were the BOE’s most important private asset, with primary dealings being with large corporations like the East India Company, the South Sea Company, and the Hudson’s Bay Company (O’Brien & Palma, 2023). Furthermore, the BOE also provided some limited low-interest loans to manufacturers (Pincus & Wolfram, 2016). As advances were often made in the form of deposits or banknotes, the BOE’s banknotes were also a genuine effort to improve the payment system and not merely a source of rents for the BOE. Indeed, rather than merely funding the Crown, Paterson’s vision was to establish a “Bank…for the convenience and security of [making] payments, and [to]…better…facilitate the circulation of money” (Paterson, 1694, p. 1). Overall, while the BOE allocated most of its credit to the Crown for decades following its creation, private sector interests were also evident in the BOE’s founding charter.

Ottoman Empire

Large-scale borrowing by the Ottoman government began in 1853 during the Crimean War, which necessitated substantial military expenditures. Subsequently, the government continued to seek loans to manage the redemption of paper money and stabilize the fiscal budget (Eldem, 2005). Seeking to reduce its dependence on its traditional source of financing, the infamous Galata bankers, the Ottoman government established the Imperial Ottoman Bank in 1863. Funded by French and British investors, the Imperial Ottoman Bank played a pivotal role in financing the Ottoman government. This was done primarily by organizing foreign loans and providing short-term credit. The Ottoman government hoped that the Imperial Ottoman Bank would streamline the government’s financial operations by offering an orderly system of credit. Although credit flowed as desired, the Ottoman Empire’s debts to the Imperial Ottoman Bank and foreign creditors would burden it heavily until its final days (Clay, 2001).

The Imperial Ottoman Bank was founded during the Tanzimat (Reorganization) period. Beginning in 1839, the Tanzimat was a sustained modernization drive that sought to arrest the slow decline of the Empire. A key goal of the Tanzimat was to reform the military by modernizing the army along European lines. By providing much needed financial support, the Imperial Ottoman Bank was one plank of a strategy that aimed to arrest the Empire’s slow decline and strengthen its resistance against internal nationalist movements and external aggressive powers (Uyar & Erickson, 2009). The military was therefore a key member of the Ottoman’s ruling coalition and continuously received a large share of Ottoman financing, irrespective of whether a war was currently taking place.

Efforts by the Imperial Ottoman Bank to support the private sector, whether by direct lending or by discounting bills of exchange, were minimal. Perhaps the best indicator of the low priority accorded private sector interests was that the Imperial Ottoman Bank never set an official interest rate (Tunçer & Pamuk, 2014).

Russia

Early banking institutions in Russia were primarily established to meet the government’s credit needs. The Assignation Bank, founded in 1768, was created exclusively for state loans. It issued assignation rubles, which were backed by copper reserves, to manage state finances. Despite its intended purpose, the bank struggled with issues of public trust and mismanagement, undermining its effectiveness. In 1817, the Imperial Bank of Commerce was established to succeed the Assignation Bank. Like the Assignation Bank before it, the Imperial Bank was primarily an instrument to facilitate government borrowing, reflecting the state’s credit needs and its dominant role in the economy (Arnold, 1937).

Russia in the early 19th century was expanding its empire through military conquests in Asia and the Caucasus, Georgia, parts of Azerbaijan, Armenia, and the Ottoman Empire. Tsar Nicholas I was also dubbed the “gendarme of Europe” for his aggressive suppression of revolutionary movements, especially the Polish revolt of 1830 and the Hungarian Revolution of 1849. The persistent focus on securing and expanding Russia’s borders reflects the strategic importance of military strength and regional dominance in Russian policy during this period.

Following Russia’s defeat in the Crimean War, officials sought to develop its private sector and modernize the economy. A key reform in this regard was the transformation of the Imperial Bank into the State Bank of Russia in 1860. Although the State Bank continued to lend to the Russian government, it was also tasked with supporting industrialization and economic growth by extending credit to private enterprises (Raffalovich, 1902). These steps notwithstanding, it was not until reforms introduced during the charter renewal of 1894 that the State Bank’s discounting and private sector loan operations were truly modernized and the Bank could support industrial and commercial enterprises on a larger scale. Despite this shift towards favoring the private sector, the government maintained significant control over the State Bank, ensuring that its strategic interests were prioritized. As Gerschenkron argues, in Russia, “clearly, a good deal of the government’s interest in industrialization was predicated upon its military policies,” (Gerschenkron, 1937, p. 20).

Belgium

The backdrop to the founding of the National Bank of Belgium in 1850 was a financial crisis two years prior. This crisis forced two of Belgium’s main banks, the Société Générale and the Bank of Belgium, to suspend payments. From this crisis, the Belgian government sought to establish a central bank that could stabilize the nation’s financial system and grow the private economy. The government had a clear mandate for the National Bank: it would not be permitted to lend directly to the private sector or the government, and it would focus on the core functions of being a banker to the government and discounting commercial paper. Every effort was made to limit the Bank’s assets to short-term self-liquidating bills, which Buyst and Maes (2008) note was a business that kicked into high gear almost immediately. In contrast, government financing was tightly controlled and strict limits were placed on the number of Treasury notes eligible for discounting. Compared to its peers elsewhere in Europe and abroad, the National Bank of Belgium was designed with financial stability in mind from the outset. Such was the success of the National Bank that in subsequent decades, it served as a model for other countries, influencing the design of central banks in the Netherlands in 1864 and Japan in 1882 (Conant, 1910).

The establishment of the National Bank of Belgium was significantly influenced by the rise of the first Liberal government in 1847. Key figures such as Liberal Finance Minister Walthère Frère-Orban played crucial roles in enacting free-trade policies and supporting infrastructure investments to further Belgium’s industrialization and commercial growth. With Belgium being the second country to successfully industrialize after Britain, the strong influence of business interests in government policymaking was unsurprising. The Liberal government’s support from key business interests therefore facilitated the creation of a central bank that exclusively prioritized the private sector.

Argentina

In 1872, Argentina’s national government founded Banco Nacional, a bank which lent to the federal government and the private sector, discounted bills of exchange, managed the government’s accounts, and introduced banking practices to many of Argentina’s interior provinces via an extensive branch network (Moyano, 2019). Banco Nacional’s diverse functions matched the diverse priorities of the national government. At the time Argentina was led by liberal Presidente Domingo Faustino Sarmiento, who sought to expand public services, most notably public education (Criscenti, 1993). However, at the time Argentina was also seeking military modernization following the costly War of the Triple Alliance.

Banco Nacional operated until 1890, when it collapsed during the infamous Baring crisis. In 1891, amid the turmoil, the Banco de la Nación Argentina (BNA) was established in its place, taking over many of the central banking functions performed by Banco Nacional. BNA performed these functions until Argentina’s present day central bank, Banco Central de la República Argentina, was established in 1935.

The Argument

Details from these cases highlight several gaps in our understanding of the politics of central bank credit policies. As a straightforward empirical matter, given the relative high frequency of war and the low frequency of central bank formation, theories that attribute central bank formation to heightened warfare expenditures over predict the extent of actual central bank formation. 5 Indeed, even though governments have historically devoted significant portions of their budgets to war (Brewer, 1989), it has been uncommon for war to be financed with central bank resources. Rather, issuing debt has been the most common means through which governments have financed wars since at least the early 19th century (Eichengreen et al., 2019; Krainin et al., 2022; Zielinski, 2016).

This empirical matter notwithstanding, the need to finance warfare is frequently invoked as a theoretical driver for central bank formation. On this score, the cases suggests that military concerns do influence central bank formation and their credit policies, but primarily by shaping the political coalitions behind these institutions rather than from immediate financing needs stemming from an ongoing war. For instance, the Imperial Ottoman Bank was established amid the Tanzimat, a period marked by a strong commitment to military modernization. Similarly, a military modernization drive, rather than wartime expenditures per se, drove the founding of Banco Nacional. Lastly, early Russian banking institutions emerged as part of a broader strategy driven by enduring military interests rather than short-term war expenditures. These examples demonstrate that prominent and sustained military interests within a ruling coalition, and not the direct fiscal pressures of wartime, ultimately shaped the orientation of central bank credit policies in a large number of cases.

Other cases beyond those considered above show that even when war drove governments to borrow from their central bank, they may not fully appropriate central bank resources for themselves. Consider Bindseil (2019b), which notes that the Royal Bank of Berlin, established by King Frederic II of Prussia in 1766, was “…considered a source of government income, government funding, and funding of politically desired development…” However, even then, Niebuhr (1854) notes that in 1806, in the midst of the Napoleonic wars, the vast majority of the Bank’s outstanding credit was allocated to the private sector. Although credit to the public sector amounted to 6 million thaler, the bank also held mortgage loans of 13 million thaler, Lombard lending of 10 million thaler, and held precious metals stocks of 9 million thaler. Another example is Sweden’s Riksbank, established in 1668. Owing to the failure of a previous attempt at a central bank, Stockholms Banco, the Riksbank was initially prohibited from issuing banknotes or lending to the government. Although the latter restriction was relaxed in due course and the Riksbank extended credit to the Swedish Crown during the Scanian War, the Riksbank still faced considerable restrictions with respect to financing government activities, a constraint which proved detrimental during the Great Northern War (Hendrickson, 2020). 6

These examples demonstrate that governments consider more than just security concerns when setting their central bank’s credit policies. Economic stakeholders, such as merchants, industrialists, and financiers, prioritize their economic well-being, seek credit to enhance production capacity, facilitate trade, and fund new ventures. Consequently, when economic interests become more influential to governments, there is heightened pressure on those governments to have their central banks bolster support for the private sector. This is especially true prior to the 20th century because, with a few notable exceptions among the most highly developed countries in Europe and North America, financial systems were generally underdeveloped and a government founded central bank may be the best source of credit available.

The establishment of the National Bank of Belgium is a canonical example of a state founding a central bank to support commercial activities and stabilize the financial system. In England, although the founding of the BOE is one of the clearest cases of a central bank founded to finance war, its charter also provided for private sector functions, even if these were depreciated in the banks early years. In Argentina too, in addition to lending to the government, there was also a focus on supporting the private sector via discounting bills of exchange. A plausible “least likely” case in this respect came after the Crimean War, where even in Tsarist Russia, some of the lending capacity of the State Bank of Russia was allocated to supporting Russian private sector industrial development.

Rather than states attempting to appropriate resources in the face of existential war, the cases reveal that central bank credit policies reflected a negotiation between military exigencies and commercial interests. The cases therefore demonstrate that central bank formation is less a direct response to the fiscal pressures of warfare than a reflection of the political coalitions governing state priorities. While warfare undoubtedly raises a government’s need for additional financing at the margin, it is the presence and relative strength of military interests within the broader ruling coalition that ultimately shapes both the decision to establish a central bank and the orientation of its credit policies. In cases where military interests were strong, the result was the formation of a central bank whose credit policies were oriented towards government credit. Conversely, governments aiming for modernization and industrialization, often driven by crucial economic interest groups, are more likely to establish central banks that facilitate greater access to credit for the private sector.

My argument does not imply that governments driven by military interests exclusively prioritize their own access to credit, or that governments driven by economic interests exclusively prioritize support for the private sector. As evidenced by the cases of England, Argentina, and late nineteenth-century Russia, governments often navigate a delicate balance between placating the security and economic interest groups that support their claim to power. This balance is never static, as it can shift over time and be reshaped by events. For instance, the onset of WWI prompted most combatant nations to utilize their central banks for direct financing, regardless of their previous emphasis on security or economic interests (Broadberry & Harrison, 2005). The critical point is that governments with military interests face stronger incentives to direct central bank credit towards themselves while governments with economic interests face stronger incentives to prioritize credit access for private sector actors. The two hypotheses to be tested are therefore as follows.

A New Dataset on Central Banking Functions

To test the two hypotheses, I create a new dataset cataloguing central banking functions worldwide between 1600-1914. Given the ongoing debate over the criteria upon which an institution qualifies as a legitimate central bank, careful thought is required to determine which institutions should be included in a dataset such as this. Existing studies are generally insufficiently systematic when compiling their lists of historical central banks and the result is a wide disagreement regarding which institutions were genuine central banks before 1900. Capie et al. (1994) argue that “…there were no real central banks before 1800 (unless a case can be made for the Bank of England)…” (Capie et al., 1994, p. 51) and then list 19 institutions that meet their criteria before 1900. Broz (1998) identifies 21 central banks also before 1900, which includes the same list as Capie, Goodhart, and Schnadt as well as the First and Second Banks of the United States and the Bank of Prussia, but excludes Banca Naţională a Romăniei. Finally, Poast (2015) identifies 30 central banks before 1900 using Central Bank Directory (2005). Interestingly, the literature has progressively expanded its scope and identified a greater number of central banks over time.

Given that there is no definitive list of central banks in existence before WWI, for central banks before 1800 I utilize Bindseil (2019a) when selecting which central banks to include in the dataset. Bindseil (2019a) identifies central banks as institutions that “issue financial money of ultimate quality” (Bindseil, 2019a, p. 8). Central bank money arguably underpins all other central bank functions such as acting as the lender of last resort (only the issuer of central bank money can lend at high quantities during crises) and being the government’s banker (governments naturally prefer to settle payments and manage debt in central bank money). For central banks founded after 1800, I follow Archer (2009) and include in the dataset banks whose banknotes had a privileged position and/or were the central government’s banker. According to Archer “the earliest progenitor central banks were the dominant issuers of banknotes and bankers to the government. Indeed, often these functions went hand in hand,” (Archer, 2009, p. 19). Denoting central banks in this way aligns with Bindseil (2019a) as these functions are highly plausible indicators of a bank that issues central bank money.

The dataset is coded using primary sources including central banking laws, charters, and statutes. Given that many of these primary sources are centuries old, documents were collected from a variety of sources. The vast majority of documents were collected from digital national archives, national gazettes, and books compiling and reproducing collections of laws. Some documents were also archived on central bank websites, especially those by the Banco de España. In four cases no primary sources could be located and a secondary source quoting the original law, charter, or statute was used instead. 7 Documents not in English were translated using either Google Translate or DeepL.

The dataset includes 69 banks across 44 countries established between 1600-1914. Table A10 in the Online Appendix presents the list of banks. As the dataset aims for worldwide coverage, it includes institutions not typically covered in studies of early central banking, such as those in Asia and South America. The dataset codes for when a particular function is in existence. For example, the Nederlandsche Bank was founded in 1814 and lent to its government between 1834-1839 (Uittenbogaard, 2015). Thus, in the dataset government lending by Nederlandsche Bank is coded as 1 between 1834-1839 and as zero in all other years. In total the dataset codes for six central banking functions, which are as follows. • • • • • •

Central Bank Credit Policies over the Long Term

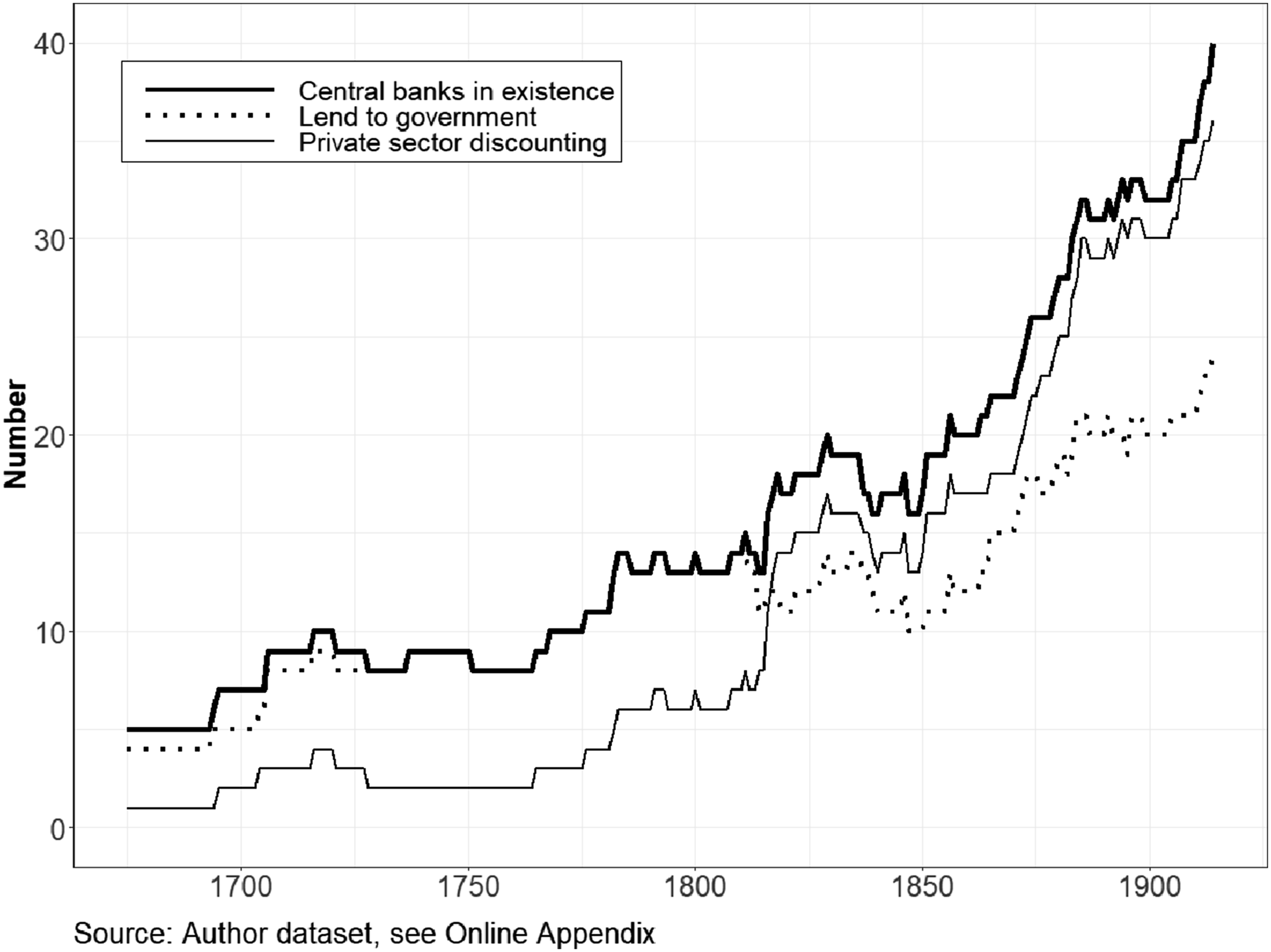

Figure 1 sets out how the total number of central banks, the number that lent to their government, and the number that engaged in private sector discounting evolved from 1650 to 1914. Several intriguing patterns can be observed. In line with other studies, there was a steady increase in the number of central banks since the 17th century, with noticeable growth seen in the latter half of the 19th century. Also in line with other studies, in the very early years – although the number of central banks is small – nearly all central banks in existence focused on lending to their government. Then, beginning in the 1780s the number of government-lending central banks levels off for several decades. Their numbers do not grow appreciably again until the 1850s when several central banks in South and Central America with a government lending mandate were established. Evolution of central bank credit policies.

The trend in the number of central banks that discount bills of exchange is different. Discounting private sector bills of exchange was not a priority for the majority of central banks in the first three-quarters of the 18th century. Although the number of central banks in existence at this time was modest, things began to change from the mid-to-late 18th century, as more and more central banks that were established were tasked with discounting bills of exchange. Then a sharp upturn took place following the Napoleonic Wars. This uptick was driven largely by developments in Europe, as several central banks were closed and replaced by new institutions that had a clearer private sector orientation. From approximately 1815, the number of discounting central banks overtakes the number of government financing central banks for the first time and the gap between these grows throughout the 19th century. Indeed, in 1750, 100% of central banks in existence lent to their government while only 22% engaged in private sector discounting. By 1914, matters had dramatically reversed, as only 59% could lend to their government while over 90% engaged in private sector discounting.

Empirical Analysis

Dependent Variables

In the empirical analysis two dependent variables are used, Government lending and Discounting (as described above). For all 69 central banks, I carefully reviewed each primary source document for language that indicated that the central bank could lend to its government and/or discount bills of exchange. Government lending captures instances where central banks were authorized to provide financial support to their governments, either through direct loans or advances. This variable is coded as 1 when a central bank’s charter, law, or statute explicitly authorizes the central bank to lend to its government, and zero otherwise.

An example is Uruguay’s Banco De La Republica, established in 1896. The Banco De La Republica is coded as a central bank that lends to its government because Article 19.10 of law 2480 states: Article 19: The Bank’s operations will be:…10. Make loans to the State and the Boards duly authorized by the Legislature.

Given the large number of central banks in the dataset and their variable founding dates, language indicating lending to governments varies from charter to charter. A second example is the charter of the Imperial Ottoman Bank. In its founding charter, Article 16 states Article 16: The Bank will open for the Imperial Government a credit not exceeding twelve and a half million francs, or one hundred thousand pounds sterling, to be applied against revenues at a rate of 6% per year. If the Bank finds it convenient to increase the figure of this credit, the conditions will be the subject of special negotiation.

Discounting captures a central bank’s role in supporting private credit markets by discounting commercial bills of exchange. This variable is coded as 1 when a central bank is explicitly authorized to discount bills of exchange, and zero otherwise. For example, Spain’s Banco De San Fernando, established in 1829, is an example of a central bank coded as discounting bills of exchange. This coding is derived from Article 3 of its founding charter, which states Article 3: The operations of the Bank will be reduced to: First, discounting commercial bills and promissory notes, whether their bearers are merchants or not, not exceeding their period of one hundred days, and having the guarantees prescribed in Article 22.

A second example is found in Article 11.1 of the 1853 charter of the Banco do Brazil, which states Article 11: The Bank may: …1. Discount bills of exchange, and other commercial titles on order and with a fixed term, guaranteed by at least two signatures from well-off people, resident in the place where the discount is made; as well as Customs writings and Treasury notes.

Independent and Control Variables

The hypotheses state that a government’s responsiveness to military and economic interests are key variables explaining a central bank’s credit policies. Testing these hypotheses therefore requires finding a variable that indicates whether a government is likely to be responsive to military or economic interest groups. A variable from the Varieties of Democracy (V-Dem) database, v2regsupgroups, meets these criteria as this variable categorizes the groups in society a government relies on to maintain power. Constructed from surveys of country experts, v2regsupgroups identifies groups that are “…supportive of the regime, and, if they were to retract support would substantially increase the chance that the regime would lose power” (Coppedge et al., 2025). 9 From this I derive two independent variables, Military and Economic. These variables range between zero and 1, where a zero indicates expert consensus that a regime was not supported by either the military or business elites and a 1 indicates expert consensus that a regime was supported by either of these groups. Although Military and Economic can take values between zero and 1, 85% of observations take one or the other value.

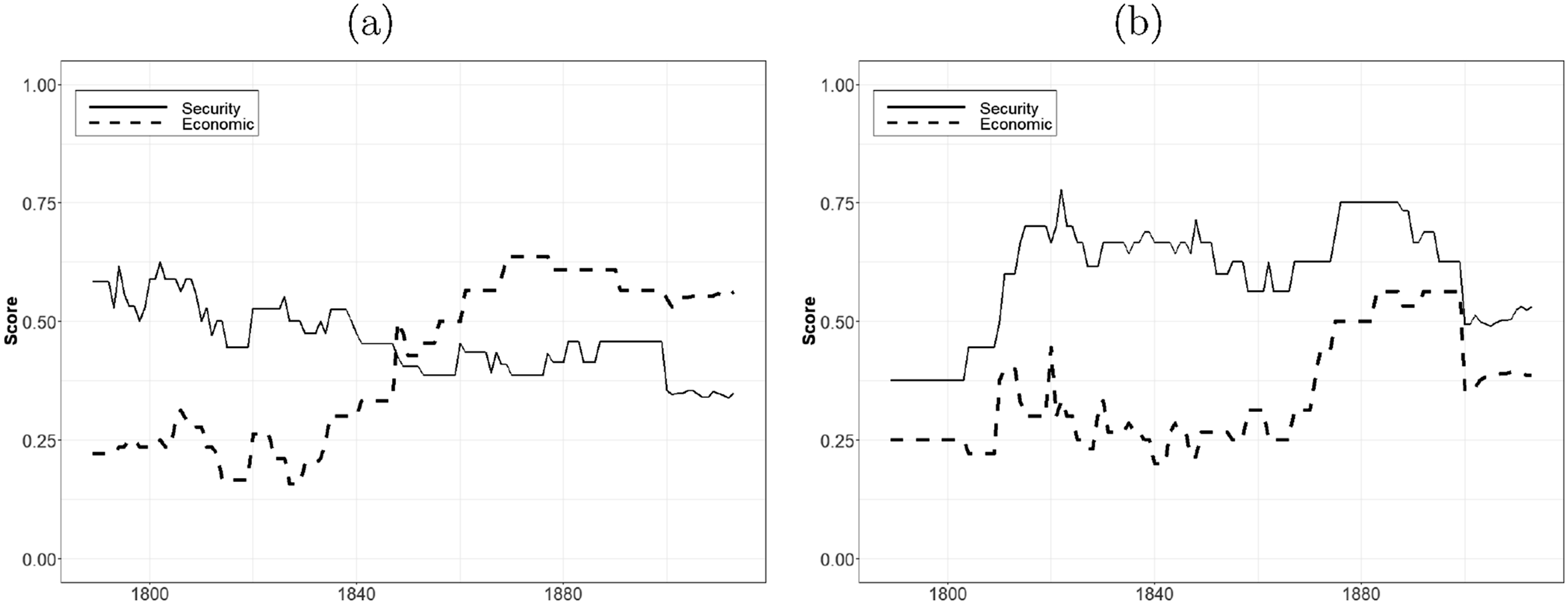

Trends in these variables are shown in Figure 2. The left panel of Figure 2 shows the average levels of government reliance on security and economic interests between 1789-1914 in the now developed world, which includes states in Europe plus the United States, Canada, Australia, New Zealand, and Japan. Military interests show a steady decline over the entire period, indicating that despite a heavy reliance on the military to maintain power in the late 18th century, the necessity of this support waned over time. In contrast, economic interests show considerable growth, especially starting in the 1830s. By the late 1840s, economic interests supplant military interests as the more numerous set of interests supporting governments in power. Security versus economic interests. (a) Europe and other developed. (b) Non-Europe and non-developed.

The right panel of Figure 2 shows the same variables for all other countries. Here military interests remain dominant for longer and economic interests do not overtake military interests at any point in the sample. Nevertheless, starting in the 1860s economic interests begin to close the gap with military interests and by the turn of the century the average levels of both variables are more comparable.

In the empirical analysis, I control for other potential factors that may influence central bank credit policies. Four control variables are drawn from V-Dem. War ongoing (e_miinteco), indicates whether a country is participating in an international conflict. This variable is coded as 1 for countries involved in an international conflict in a given year, and zero otherwise. This variable helps account for the influence of ongoing wars and the fiscal pressures this entails on a government’s decision to establish a central bank. Regime type has been shown to be relevant to general financial development (Keefer, 2007; Menaldo & Yoo, 2015) and the performance of independent central banks (Bodea & Hicks, 2015b; Garriga & Rodriguez, 2020). Legislative constraints (v2xlg_legcon) is a continuous variable and ranges from 0-1, where higher values indicate stronger legislative constraints on the executive. Greater constraints reflect stronger legislative checks on the executive, implying that policy changes are more difficult. Fiscal capacity (v2stfisccap) considers the capacity of the central government to raise revenue. This variable ranges from zero to 4, where zero signifies no capacity to raise revenue, and 4 indicates the ability to raise revenue through income, capital, and sales taxes. This control accounts for the possibility that states with higher revenue-raising capabilities may have less need to establish a central bank with a government lending function, as they can rely on alternative sources of funding. GDP per capita (expressed as the natural logarithm of e_gdppc) controls for the possibility that a country’s level of economic development influences the likelihood of establishing a central bank.

Three control variables are drawn from Reinhart and Rogoff (2008). Sovereign default is an indicator that a government has defaulted on its debt. A value of 1 indicates that a government has defaulted on its debt in a particular year, while zero indicates no default occurred. If government lending is a motivation for establishing a central bank, a government in default may have a stronger incentive to create a central bank to alleviate constraints on its spending. Two variables indicate the presence of particular types of economic crises. Inflation crisis takes a value of 1 if inflation breaches the threshold of 20 percent per annum, and zero otherwise. Systemic crisis takes a value of 1 if a systemic banking crisis occurred in a given year, and zero otherwise. These variables control for the possibility that governments establish a central bank as a solution to economic and financial turmoil. Summary statistics for all variables are in Table A1 in the Online Appendix.

The analysis uses discrete-time survival analysis. In a discrete-time survival analysis, the dependent variable equals zero for each country-year observation until the year that a particular central bank function is introduced. In that year the dependent variable equals one and all subsequent observations for that country are dropped from the analysis. If a central bank ceases operations, the country re-enters the sample and the coding for the dependent variables begins anew. The analysis is right censored because some states do not establish central banks prior to 1914. Although the dataset stretches back to 1600, the availability of independent and control variables limits the starting date of the analysis to 1789. Despite this limitation, the analysis includes more than half of the central banks in the dataset and more than 2800 country-year observations. As the dependent variables are binary, I estimate complementary log-log models that account for duration dependence as advised by Carter and Signorino (2010). Complementary log-log models are particularly appropriate in discrete-time survival analysis when the probability of an event is especially small or large, which is the situation here given the relative rarity of central bank formation. Standard errors are clustered by country.

Results

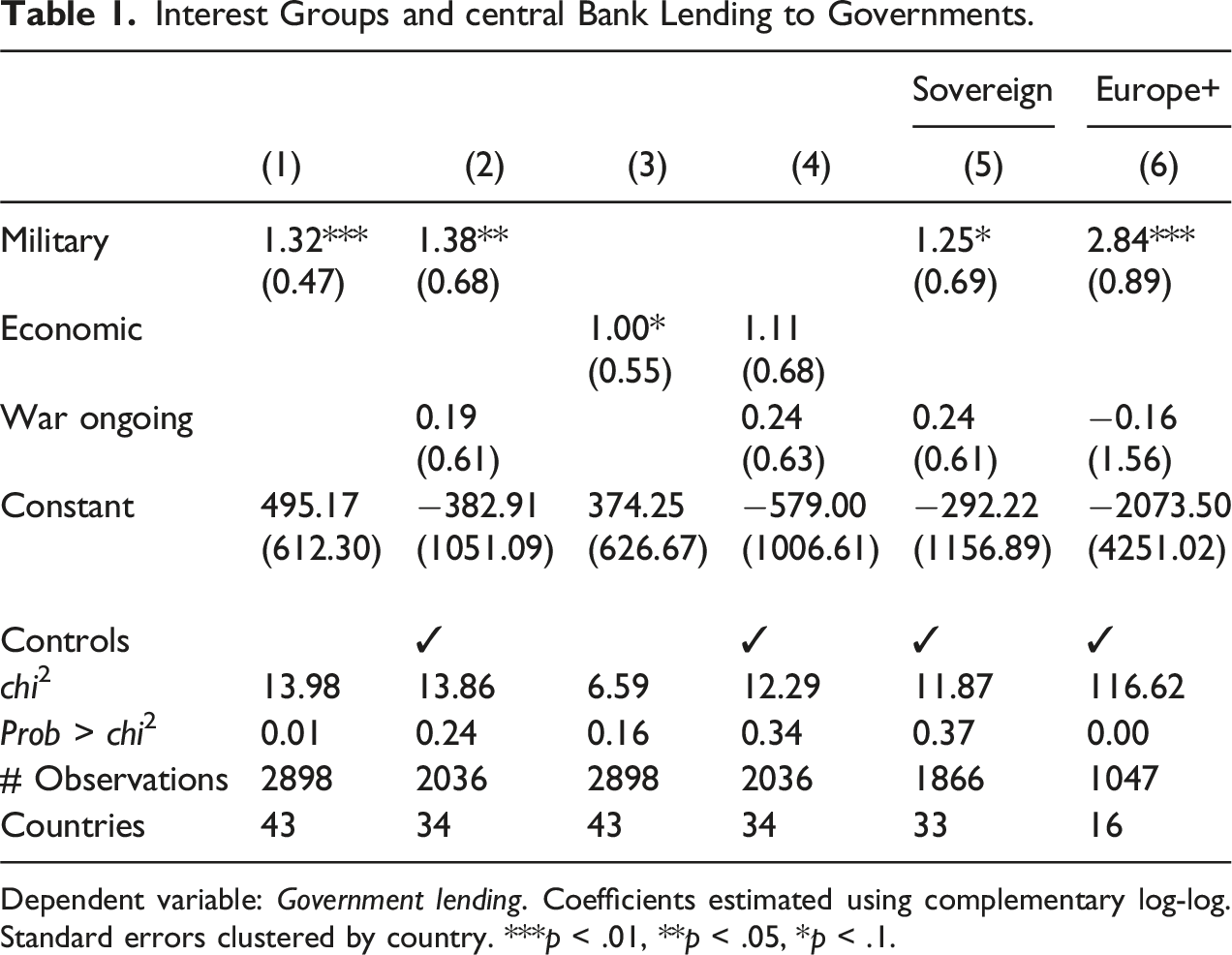

Interest Groups and central Bank Lending to Governments.

Dependent variable: Government lending. Coefficients estimated using complementary log-log. Standard errors clustered by country. ***p < .01, **p < .05, *p < .1.

Coefficients on Economic are not strongly associated with the establishment of a central bank that lends to its government. Although the bivariate specification in model (3) shows a positive and statistically significant association at the 10% level, compared to the other bivariate specification in model (1), the size of the coefficient and the level of statistical significance are far lower. Overall, models (3) and (4), especially compared to models (1) and (2), suggest that economic interests do not strongly motivate governments to establish a central bank that lends back to itself. The full set of results, including all control variables, are shown in the Online Appendix. The only control variables to show any level of statistical significance are in model (6) where Legislative constraints and GDP per capita are statistically significant at the 5% level.

War ongoing does not have a statistically significant relationship with central banks lending to their government. This null result can be understood in two ways. First, because wars are far more common than central bank formation, the absence of statistical significance is, in fact, the expected result. Despite theoretical accounts and historical cases that suggest that governments facing significant military pressures may use their central banks to secure funds for military purposes, the frequency mismatch in wars versus central bank formation implies that even though some central banks are established amidst war, few wars actually lead to the establishment of central banks. Second, ongoing war does not capture the more nuanced and sustained institutional salience of military interests. These findings indicate that while war may be a factor in raising security concerns, it does not serve as a robust proxy for the underlying political salience of military interests in setting central bank credit policies.

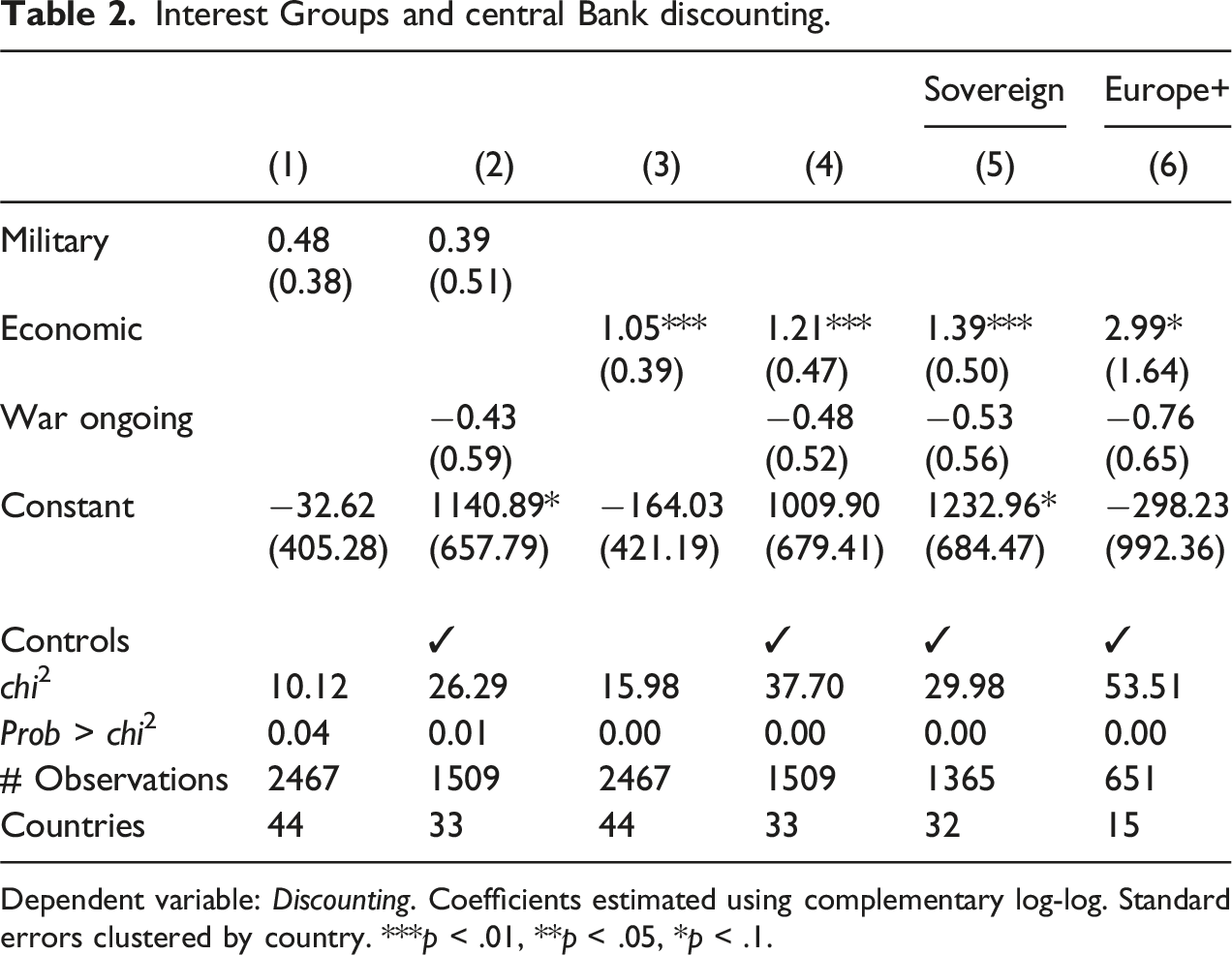

Interest Groups and central Bank discounting.

Dependent variable: Discounting. Coefficients estimated using complementary log-log. Standard errors clustered by country. ***p < .01, **p < .05, *p < .1.

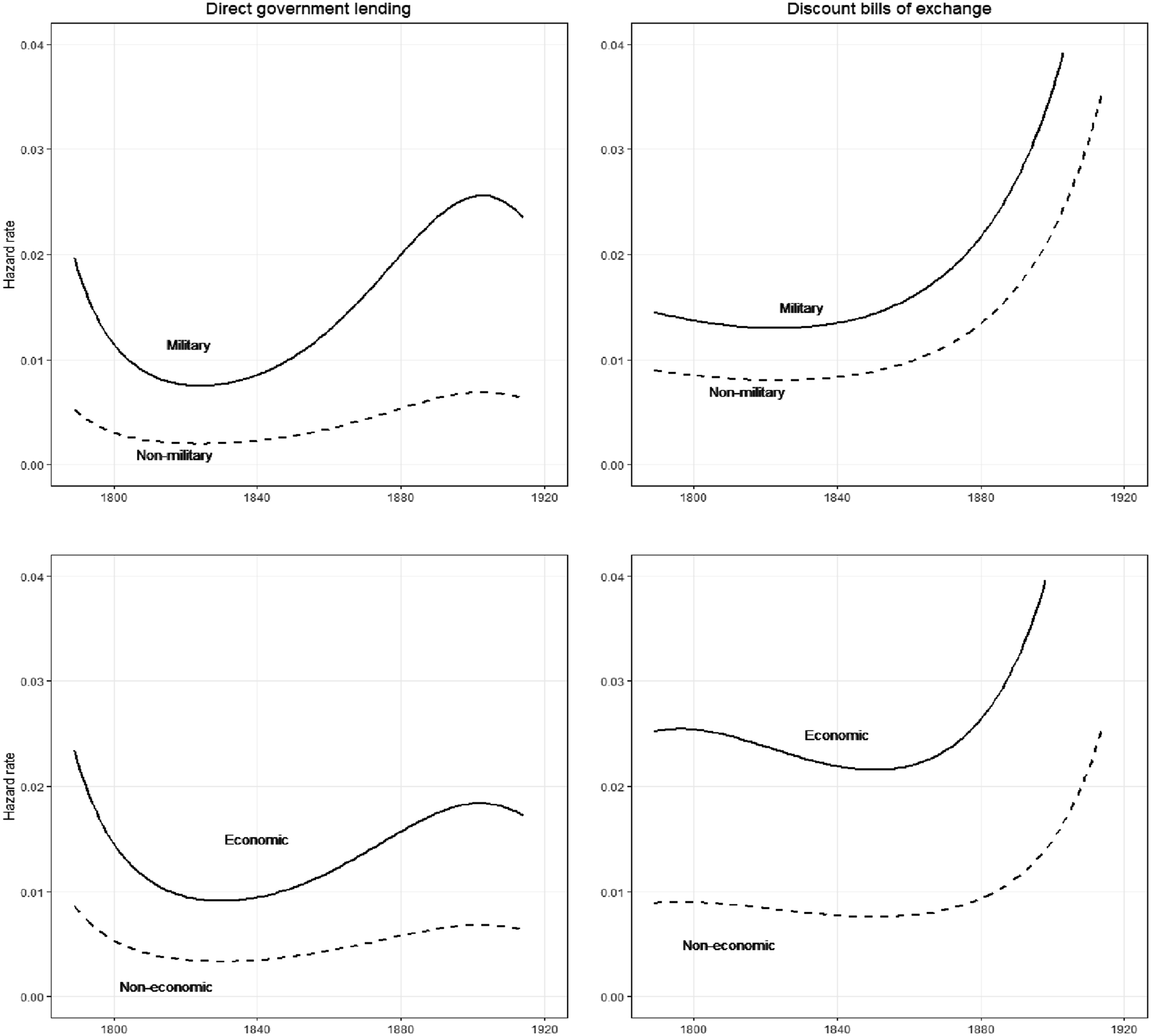

Figure 3 displays hazard functions derived from the analyses in Tables 1 and 2. These functions represent the probability that a central bank will begin lending to its government or discount bills of exchange within a given year among those that do not perform those functions. The top left panel and the bottom right panel support the two hypotheses. In the top left panel, the likelihood that a central bank will begin to lend to its government is significantly higher in a regime where the military is a key member of the ruling coalition. For example, in 1880, for a government responsive to military interests, but no central bank that lends back to itself, there was a 2% chance that such a central bank would be established. This compares to 0.5% for governments without military interests. In the bottom right panel, a government responsive to economic interests exhibits a greater likelihood of founding a central bank that discounts bills of exchange compared to regimes lacking economic interests. Again considering 1880, for a government with economic interests but no central bank that discounts bills of exchange, there was a 2.6% chance that such a central bank would be established. This compares to 0.9% for governments without economic interests. Conversely, the top right panel shows that states with and without military interests do not differ substantially from one another with respect to founding a central bank that discounts bills of exchange and the bottom left panel shows the same with respect to economic interests and founding a central bank that lends to its government. Hazard functions.

Robustness Checks

I corroborate these results with several robustness checks, which I show in the Online Appendix. There I show that support from other interest groups including the aristocracy, agrarian elites, party elites, religious groups, local elites, the urban middle class, rural middle class, or a foreign government have no strong, statistically significant effect on either central banks lending to their government (Table A4) or discounting bills of exchange (Table A5). I also show that the results do not change when estimated using logit models rather than complementary log-log (Tables A6 and A7). I also report instrumental variables estimations (Table A8) to address the possibility that a regime’s security or economic interests may introduce bias due to endogeneity (Bartik, 1991) and a series of Autoregressive Distributed Lag models (in error-correction form) to show that the results continue to hold when all observations are used and the analysis is not structured as a survival analysis (Table A9). Collectively these robustness checks provide further evidence that military and economic interests are the critical factors that explain why governments select the central bank credit policies they do.

Conclusion

The modernization of central banking occurred along several dimensions, with the development of payment systems, the lender of last resort, tools for financial and price stability, and their transition from profit to non-profit financial institutions occurring at different times and in different places. This article argues that the modernization of central banking is also evident in the transformation of their credit policies. Initially, many central banks were primarily focused on providing direct financing to their governments, particularly in times of war. However, starting in the late 18th century there began a relative shift away from this practice as governments began to prioritize discounting bills of exchange in order to support the credit needs of the private sector.

Political dynamics and the interests of influential groups played a crucial role in this transformation. As governments deemed different interest groups essential for maintaining power, the focus of central bank lending policies shifted accordingly. When military interests were paramount, central banks were more likely to lend directly to governments. Conversely, when economic interests gained prominence, central banks increasingly supported the credit needs of private sector actors.

Central bank credit policies therefore did not develop from economic rationality alone, as they were significantly shaped by political processes and the imperative for governments to accommodate the preferences of key interest groups. This underscores the importance of understanding central banking, and institutional development more generally, within their historical and political context. The lesson for us today is that, for better or for worse, the credit policies and general functions of central banks are not static, but are subject to political forces originating beyond the monetary policy and financial committees that move markets. As central banks are likely to continue to be subject to heightened political scrutiny (Gavin & Manger, 2023), how these political forces condition central bank effectiveness and independence should be a subject of ongoing research.

Supplemental Material

Supplemental Material - Interest Groups and Central Bank Credit Policies: Evidence From 1600-1914

Supplemental Material for Interest Groups and Central Bank Credit Policies: Evidence From 1600-1914 by Michael A. Gavin in Comparative Political Studies

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets and analysis used in this study are available at the Comparative Political Studies Dataverse (Gavin, 2025): ![]() .

.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biography

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.