Abstract

Political economy literature documents how financial investors are more partial to right executives than left ones. Right cabinets face lower interest rates, less volatile stock prices and exchange rates, and higher credit ratings than left cabinets, even after accounting for fiscal differences. But does this advantage persist if right governments accommodate far right parties or ideas? I hypothesize that because far right populism can introduce political instability, markets’ evaluation of right executives might deteriorate if they enter coalition with far right parties or adopt their positions. Employing a panel analysis of bond spread data, and a comparative case study of the Netherlands and Sweden, I find that right executives enjoy significantly lower spreads than their left-wing counter-parts, but this advantage disappears if they rule in coalition with the far right or produce overly right-wing manifestos. These findings highlight that right parties may encounter tangible borrowing costs and market rebuke if they accommodate far right populism.

Introduction

Financial markets’ aversion to the left and appreciation of the right has been well documented. Left governments, particularly when they are newly elected and face few veto points, have been empirically linked with lower and more volatile stock prices (Betchel, 2009; Herron, 2000; Leblang & Mukherjee, 2005; Sattler, 2013; Snowberg et al., 2007), higher and more volatile interest rates and bond spreads (Herron, 2000; Mosley, 2000; 1 Fowler, 2006; Breen and McMenamin, 2013; 2 Brooks et al., 2015; 2022), and lower sovereign credit ratings (Barta & Johnston, 2018, 2021), than their rightwing counter-parts, even after controlling for economic and fiscal fundamentals. Yet does the right’s “market advantage” reach a limit on its end of the ideological spectrum? Do investors grow weary of right governments if they embrace the far right?

This question is increasingly relevant as nationalist far right parties (NFRPs) and ideas have become a formidable political force in advanced market economies 3 (Golder, 2016; Halikiopoulou & Vlandas, 2019; Mudde, 2007). As minority parties, NFRPs have been more successful at entering legislatures in countries with proportional representation (PR) electoral systems. However, anecdotal evidence (ranging from Donald Trump’s increasingly strong grip on the Republican Party, to the United Kingdom Independence Party’s and Brexit Party’s successful efforts at pressuring the Conservatives to deliver on Brexit) suggest that far right forces have also successfully commanded “accommodative strategies” from mainstream right parties in majoritarian electoral systems (Spoon & Klüver, 2020). NFRPs have also become increasingly successful at entering executives, either directly through coalitions (accomplished by the Freedom Party of Austria, the Brothers of Italy and Northern League/Lega in Italy, Pim Fortuyn List in the Netherlands, the Finns Party in Finland, and the Progress Party in Norway) or indirectly through confidence-and-supply agreements (as seen between the Danish People’s Party and Anders Fogh Rasmussen’s first, second and third cabinet, the Party for Freedom and Mark Rutte’s first cabinet in the Netherlands, and the Sweden Democrats and Ulf Kristersson’s recently formed minority coalition). Though NFRPs have exerted some influence on the immigration platforms of mainstream left parties in Europe (see Abou-Chadi & Krause, 2020), only mainstream right and Christian Democratic parties have entered formal governing arrangements with them. 4

This paper asks whether mainstream right parties lose investor confidence if they partner with the nationalist far right. I hypothesize that markets’ favor of right executives will sour if they partner with the far right or politically embrace their ideals because these parties and ideas create an instability premium. This instability premium arises from NFRPs’ promotion of right-wing populism, 5 which threatens the status quo. (Populist) far right nationalism intensifies investment risk via two channels, what I call the policy channel and the governing channel. In regards to the former, NFRPs (and their associated ideas) typically champion populist policies that run counter to market actors’ preferred policies of economic liberalism and fiscal prudentialism. Welfare chauvinism and trade protectionism are strong foci of NFRPs policy platforms (in the European context, this is also advocated via a strong resistance to European integration, see Vasilopoulou, 2009). Perhaps best seen with the economic fallout from Brexit and the impact of Donald Trump’s threats to leave NAFTA on the dollar/peso exchange rate (Benton & Philips, 2020), exiting, or threatening to exit, major trading agreements creates economic costs for firms and investors and unleashes uncertainty which weary market actors. Likewise, welfare chauvinism can enlarge fiscal deficits, which can also weary market actors if they expect that governments will have to raise taxes in the future to finance these deficits.

In regards to the governing channel, NFRPs can also create instability by being footloose coalition partners who minimize the cost of government collapse and disfunction. When governing directly or indirectly with the right especially, NFRPs have to juggle their coalition partners’ policy demands with those of their (increasingly) blue collar constituents, who oppose welfare state retrenchment and laissez-faire capitalism (Afonso, 2015; Häusermann & Walter, 2010). As protest parties, NFRPs may be more amenable to exiting co-governing arrangements, or refuse to enter them all together, when leading coalition partners insist on introducing contentious (budgetary) policies. Consequently, markets may attach a risk premium to these parties if they are more likely to trigger a fall in government or obstruct its functioning. 6

I test these hypotheses via a panel analysis of quarterly bond spreads for the OECD’s 23 advanced market economies (AMEs) 7 from 2000 to 2019, 8 as well as a comparative case study analysis of bond spread movements under the first Mark Rutte cabinet (2010–2012) in the Netherlands (whose minority cabinet was supported by the far right Party for Freedom) with the second Fredrik Reinfeldt cabinet (2010–2014) in Sweden (whose minority government refused to partner with the far right Sweden Democrats). I focus on AMEs, because they present a “hard case” for my argument. Governments in high-income countries with deep and developed financial markets should have greater “room to move” than those in middle- and low-income countries (see Mosley, 2000), and hence, their sovereign bond risk premia should be better insulated against changes in domestic politics given their relative financial and political stability. My results show that right executives enjoy prolongedly lower bond spreads than their left-wing counter-parts (over 100 basis points lower on average during their tenure), but only when they rule without the far right. Right executives also face higher bond spreads when their manifesto positions are demonstrably further to the right of those of NFRPs. These results indicate that mainstream right parties in high-income countries encounter tangible borrowing costs for partnering with the far right and advocating their ideas.

The next section discusses how IPE literature on the politics/market nexus has thus far ignored the risk premia attached to NFRPs, and how the comparative electoral politics literature on NFRPs’ policy preferences and governing style can help one theorize how these parties impact investment risk. The two sections that follow detail the methodology used to quantitatively examine whether partnering with the far right or assuming manifesto positions that are further to the right of NFRPs creates sovereign risk premia for right governments. I then present the comparative case study that provides further political context to the regression results. The final section concludes.

Politics and Investment Risk: What We Know and What We Don’t

IPE has long been pre-occupied with how politics and political events impact financial markets. How investors “price” government partisanship has received ample scrutiny (Bernhard & Leblang, 2002, 2006; Herron, 2000; Leblang & Bernhard, 2000; Mosley, 2000). A robust number of studies have consistently found that rightwing executives are empirically associated with lower investment risk than leftist ones (measured either by lower asset price volatility and interest rate premia on sovereign debt or higher sovereign credit ratings—Herron, 2000; Betchel, 2009; Fowler, 2006; Sattler, 2013; Breen & McMenamin, 2013; Brooks et al., 2015; 2022; Barta & Johnston, 2018; 2021), although the magnitude of this advantage is disputed. Explanations for why right governments command more confidence from financial markets than left ones typically center around policy expectations and power resource theory (Alesina et al., 1997). Investors care about the return on their investments, and hence privilege parties who are partial to lowering inflation, taxes, and government spending. Inflation erodes the value of financial assets, while government spending and the fiscal balance have implications for default risk. As representatives of capital, right parties typically champion low inflation and fiscal spending, while left parties prioritize low unemployment, a more generous welfare state, and higher taxes on the wealthy in order to fund it (Korpi, 2006). 9 Investors may therefore demonstrate greater confidence in right executives than left ones, because they expect that right parties will pursue policies that lead to more favorable investment conditions.

Yet scholars immersed in this literature also highlight another important political condition that markets desire: stability. Stability allows for predictability, making it easier for investors to make medium term forecasts about where they will receive the best return on their investments. Many of the cited works above have found that electoral uncertainty, periods of coalition formation, and government dissolutions increase price volatility and bond spreads, as financial investors are unable to decipher the types of policies that will be adopted and implemented. Heightened political uncertainty within a country can cause (foreign) investors to sell off its corporate or sovereign assets in exchange for safer investments (Eichler & Plaga, 2017), which raises sovereigns’ risk premium and hence their debt servicing costs. Consequently, while investors may be partial to right governments, they are also partial to stability and the status quo.

How might right governments “spook” markets by threatening stability? Investor confidence in right governments may have its limit, particularly when conditions arise that weaken the credibility of these governments’ commitment to investors’ policies of choice. Such conditions can emerge when the mainstream right decides to govern with “unlikely bedfellows,” who hold policy positions counter to their own; consequently, the right may have to accommodate these policy differences in coalition formation deals by deviating from their traditional economic positions. Betchel (2009) found that while the center-right Christian Democratic Union commanded greater confidence from investors than the Social Democrats (evidenced by lower stock market volatility), this confidence waned when CDU entered coalition with the SPD, because ideological differences between these parties made policy predictions difficult to make. How markets evaluate right governments when they enter coalitions with far right parties, however, remains unexplored.

The Far Right and Investment Risk

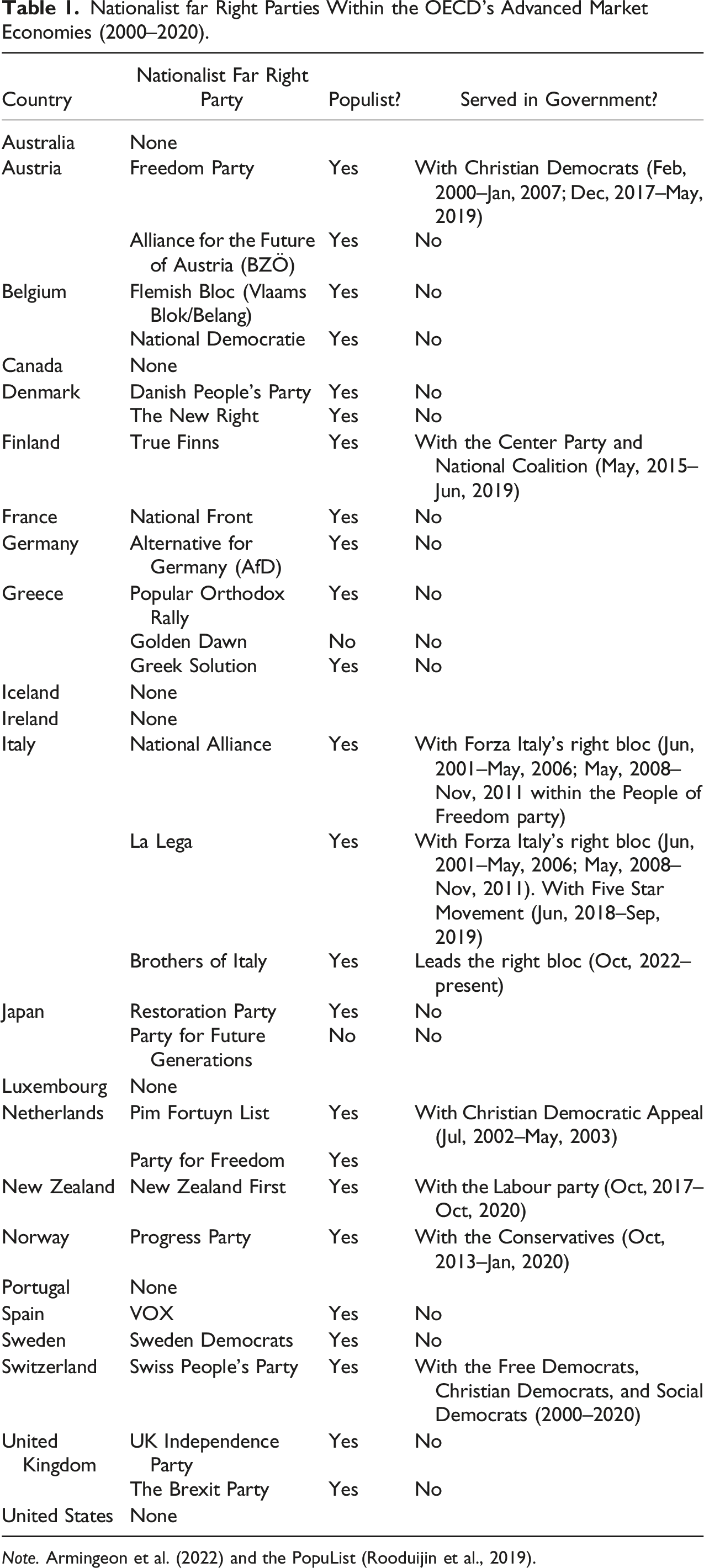

Nationalist far Right Parties Within the OECD’s Advanced Market Economies (2000–2020).

Note. Armingeon et al. (2022) and the PopuList (Rooduijin et al., 2019).

Market actors may be repulsed by populist far right parties’ success with fueling political resentments amongst the public, especially if such resentments threaten to upset the status quo and unleash uncertainty. Moreover, because NFRPs rarely rule alone, market actors’ distain towards them might also travel to mainstream parties that opt to include NFRPs within their political coalitions, including those (liberal and conservative parties) that investors typically champion. I argue that right governments may incur an instability risk premium from financial markets when accommodating populist far right parties or ideas for two reasons: (1.) NFRPs may sway right parties’ policies away from pro-market fundamentals (the policy channel) and (2.) NFRPs may prove unstable coalitions partners, threatening to exit these coalitions when right parties propose policies that upset their (blue collar) base (the governance channel).

Investment risk in the policy channel arises from the far right’s promotion of economic isolationism and their wavering commitments to “prudent” fiscal policy. Two political positions are predictably within the wheel-house of nearly all populist far right parties in high-income countries: opposition to immigration/refugees and to globalization (not only free trade and global capital, but also European economic integration—Halikiopoulou et al., 2012; Golder, 2016; Georgiadou et al., 2018). The latter, in particular, is cause for concern amongst investors, because hard borders increase the costs of trade and foreign investments. Financial actors have signaled their displeasure towards the electoral success of nativist parties and policies by selling off sovereign bonds and currencies of the countries where they arise. While this was evidenced most clearly in the wake of the 2016 Brexit referendum, after which the pound witnessed its biggest single day loss in history 11 and the UK was subsequently downgraded by Standard and Poor’s and Fitch 10 days later, similar outcomes also arose in countries where the far right assumed notable influence on government policy. After the 2018 Italian election, which introduced a populist, anti-establishment coalition between the (far right) Lega and Five Star Movement, Italian spreads (vis-à-vis the 10-year German Bund) rose considerably, jumping again when the government blatantly ignored the EU’s spending rules upon the release of its 2019 budget plans to cut taxes (a key policy priority for the Lega) and introduce a universal basic income (a priority for Five Star). UKIP’s influence on the Conservative Party during the tumultuous negotiations over the UK/EU withdrawal agreement, as well as Donald Trump’s re-evaluation of various US trade-agreements (not only NAFTA, but also his withdrawal of the US from the Trans-Pacific Partnership) highlight that populist far right ideas can even change the tune of pro-trade conservative parties in majoritarian electoral systems, where their political dominance is most protected.

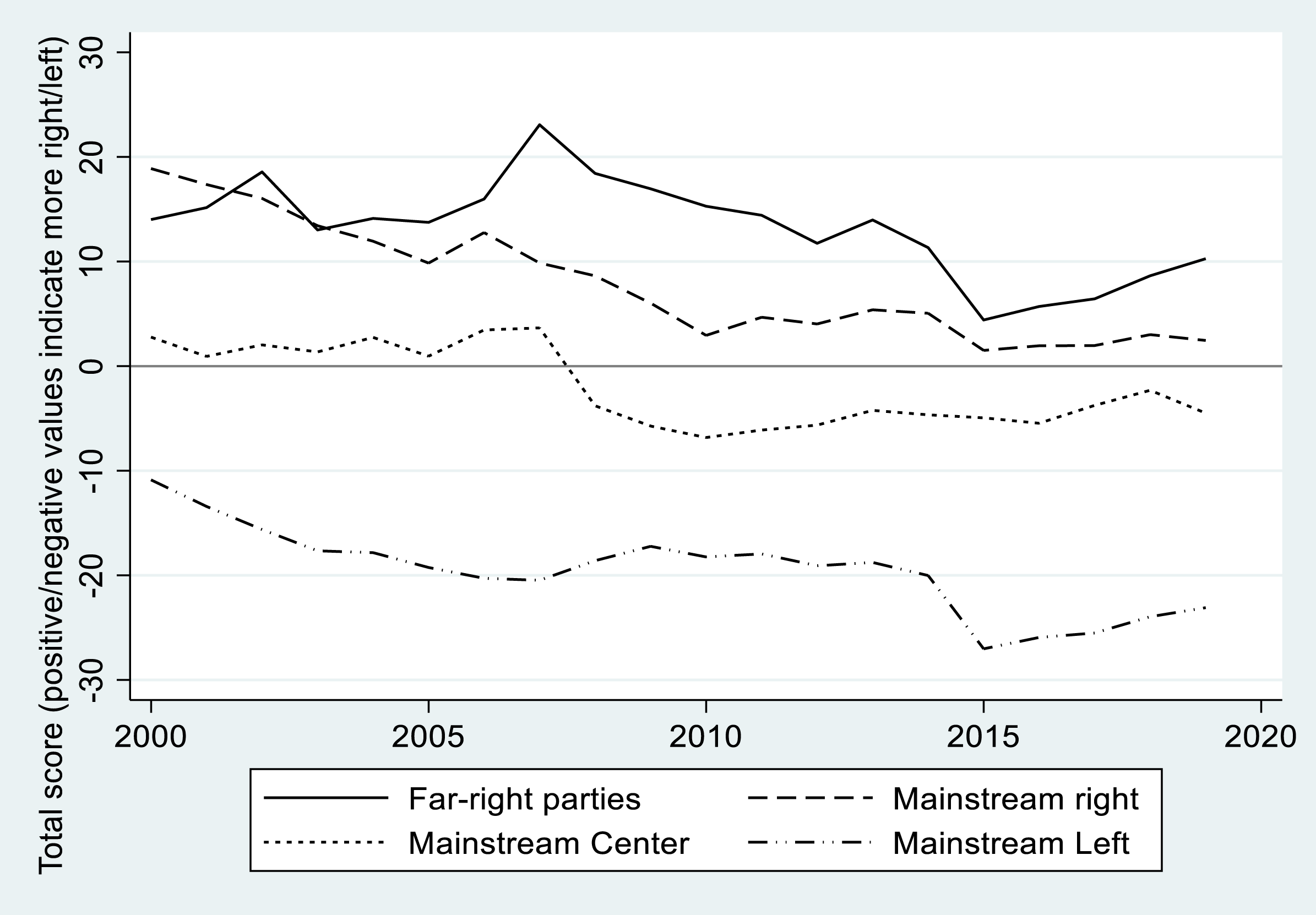

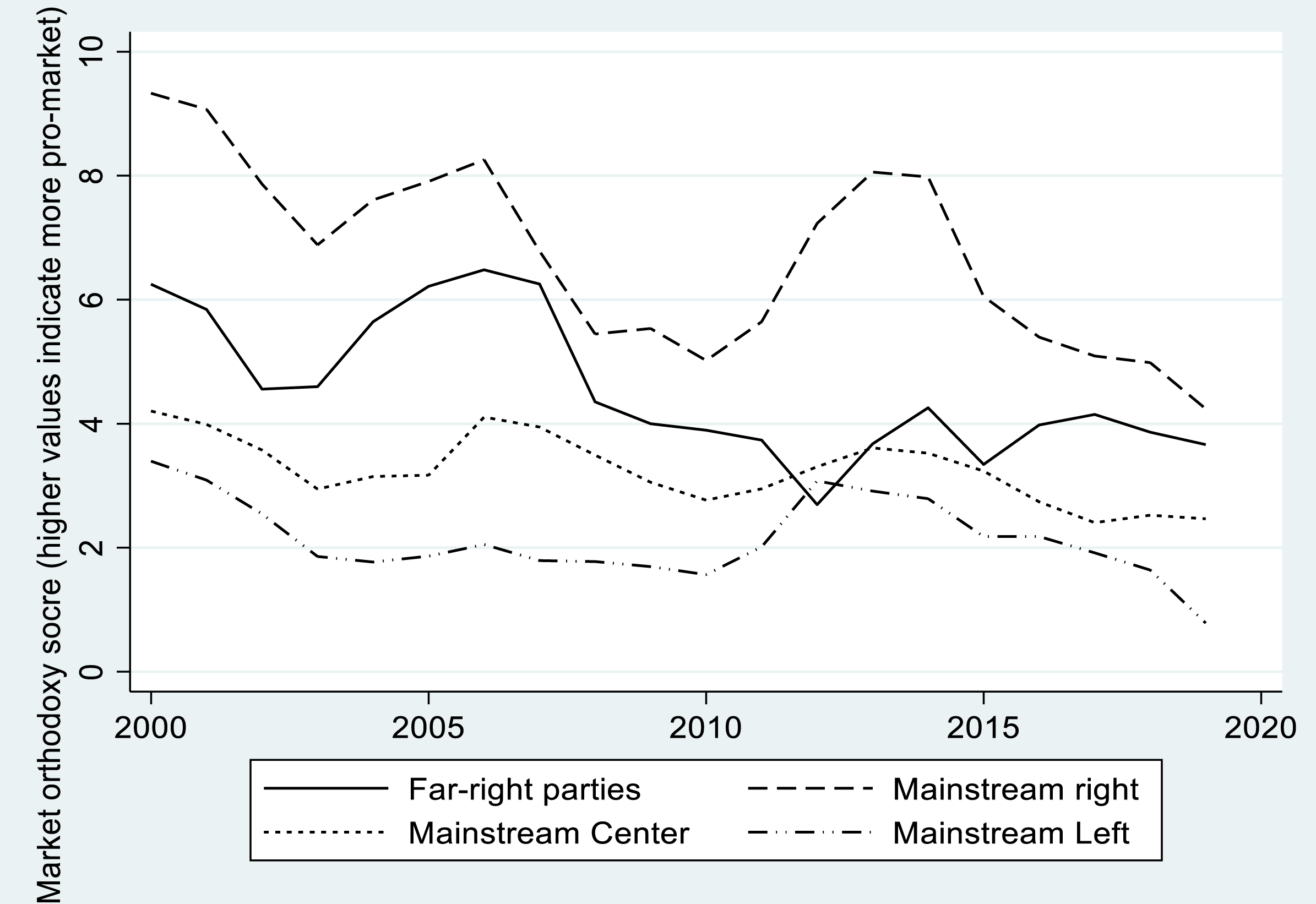

NFPRs can also shift right parties’ positions on core economic policies like fiscal prudentialism. As anti-establishment parties who are increasingly capturing the vote of blue-collar workers, NFRPs have been known to advocate for welfare chauvinism and against welfare retrenchment, as least for their core constituents (Rathgeb, 2021; Röth et al., 2018). Given that NFRPs (within Europe) routinely paint the elderly as “deserving citizens” of social benefits (see Fenger, 2018), many of them are also opposed to raising the retirement age or cutting state pensions, whose fiscal sustainability market actors have increasingly called into question (see Barta & Johnston, 2021). Examining the manifesto scores of NFRPs, in comparison with the mainstream right (Conservative and Liberal parties),

12

center (Christian Democratic and Center/farmers parties)

13

and left (Social Democratic and Labour parties)

14

for AMEs between 2000 and 2019, far right parties indeed have more “right-wing” manifestos in general (see Figure 1), but are closer to the center and left on free market orthodoxy

15

(see Figure 2, Burst et al., 2021). Afonso (2015) highlights that far right parties face a difficult political trade-off when entering government with right parties who seek to engage in welfare retrenchment, and must choose who to “betray” when welfare reforms are under discussion (their blue collar voters, or their right party coalition partners who have allowed them to enter government). Hence, far right parties may be reluctant to agree to austerity-based reforms if they threaten to make their core constituency worse off. Consequently, if mainstream right parties decide to enter coalition (directly or indirectly through confidence-and-supply arrangements) with the far right, NFRPs may dampen their commitment to prudential fiscal policy that markets value right parties for. Right-left manifesto positions by party family in advanced market economies, 2000–2019. Author’s calculations using data from Burst et al., 2021. Market orthodoxy (manifesto) score by party family in advanced market economies, 2000–2019. Higher/lower values indicate that manifestos favor/oppose pro-market orthodoxy. Author’s calculations using data from Burst et al., 2021.

Evidence of NFRPs breaking with the mainstream right on neoliberal economic and welfare reforms is abundant. Examining instances of pension reform in Austria, Switzerland and the Netherlands—countries whose right (and Christian Democratic) parties pride themselves on their “frugality”—Afonso (2015) finds that far right parties used their political influence to soften or veto proposed cuts, or in the case of PVV and the first Rutte cabinet in the Netherlands, triggered the fall of the government altogether when their demands to soften austerity remained unmet. Support for the welfare state—at least for “natives”—is a re-occurring feature of NFRPs’ political platforms, and the social policies of several prominent European far right parties more closely align with those of the left. PVV, AfD, and the National Front have openly championed increased healthcare spending and a strong state role for the distribution of welfare and social services, while they (along with Vlaams Belang in Belgium), also openly oppose pension reform (given their commitments to upholding pensioners’ interests—Fenger, 2018, p. 196–202; Enggist & Pinggera, 2022). There is also more comprehensive quantitative evidence that NFRPs have shifted the economic positions of the mainstream right. Schumacher and Van Kersbergen (2016) find that right parties become more amenable to welfare spending when far right parties emphasize welfare chauvinism.

The far right’s potential obstruction of economic reforms introduces another source of investment risk through the governance channel: far right parties may be more predisposed to exiting coalitions or confidence-and-supply arrangements due to policy differences, hence triggering a collapse in government. NFRPs (and far right factions within mainstream right parties) may also be unconcerned with government disfunction altogether. As anti-establishment parties who win seats through protest votes, NFRPs are more likely to discount the costs of governing than mainstream parties with policy-making experience. Rather than being held accountable for difficult decisions, NFRPs may opt to exit governing arrangements to save face amongst their disillusioned voters. NFRPs and radical right factions may also adopt “all or nothing” political stances by which they outright reject any alternative to their (radical) policy positions. Perhaps the most vivid—and re-occurring—example of this scorched-earth approach to politics can be seen from fringe factions within the US Republican Party and the negotiation of the federal budget and the raising of the US’s debt ceiling. Extreme voices in the Republican Party expressed little alarm at the prospect of shutting down the federal government in 2011 and 2013 over their opposition to raising the debt ceiling. 16 Likewise, Donald Trump initiated the 2019 government shut down after Congress’s refusal to include funding for his border wall within the federal budget (Gambino, 2019).

In sum, given the far right’s potential to elevate instability risk, I offer and formally test three hypotheses. The first (Hypothesis 1) re-asserts my initial partisan assumption: that right executives are associated with lower investment risk than their left-wing counter-parts, holding all else equal. I posit two conditioning effects of far right politics on the right’s bond market advantage over the left, one capturing a party effect and one an ideas effect. For the party conditioning effect (Hypothesis 2), I predict that mainstream right parties that enter coalitions with NFRPs will lose their investment risk advantage over the left, because NFRPs have the potential to distort their commitment to market fundamentalism. The alternative hypothesis to this prediction is that markets may tolerate right governments serving with NFRPs if they are more concerned about a left alternative. If this were the case, then right governments’ bond market advantage relative to the left would be unaffected by their partnerships with the far right. It is important to establish a scope condition for this hypothesis. Far right parties’ chances of entering government are most feasible in proportional representation (PR) electoral systems where outside parties are able to capture enough legislative seats to become viable coalition partners. Therefore, I also test this prediction exclusively for countries with PR electoral systems to see if results for this hypothesis are magnified for this group countries.

The ideas conditioning effect (Hypothesis 3) accounts for the possibility that mainstream right parties might internalize far right ideas in light of the rising electoral successes of NFRPs (a possibility that can manifest within PR and majoritarian electoral systems alike). I hypothesize that as mainstream right governments become more right-wing than NFRPs, they will incur higher risk premia than right governments who maintain more centric positions. While mainstream right parties may not formally enter coalitions with NFRPs—particularly in countries like the UK and France with majoritarian electoral systems that make it difficult for minority parties to gain parliamentary seats—there is the possibility that small far right parties can upset markets’ assessment of right governments if they successfully pressure them into adopting more extreme policy stances. The next two sections test these hypotheses through a quantitative panel analysis, while the comparative case study presented subsequently delves into the mechanisms underlying Hypotheses 2 and 3 using a least-likely case.

Far Right Politics and the Right’s Bond Market Advantage: Empirical Evidence for the Party Conditioning Effect

Measuring Investment Risk: Dependent Variable and Sample

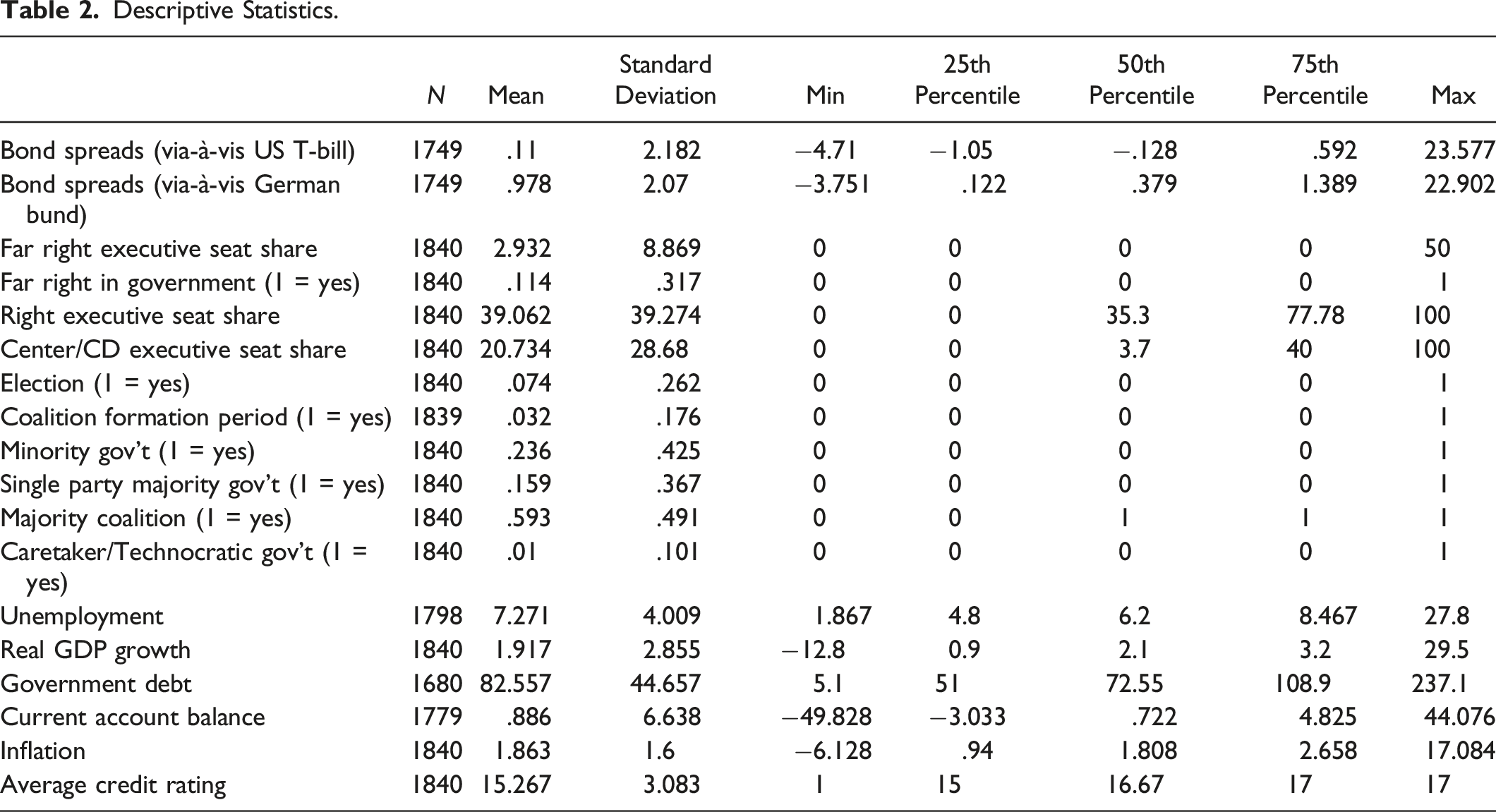

Three indicators are typically used to measure sovereign credit risk within IPE literature: bond yields (Alexiadou et al., 2022; Breen & McMenamin, 2013), bond spreads (Brooks et al., 2015, 2022; Gray, 2009), and sovereign credit ratings (Archer et al., 2007; Barta & Johnston, 2023; Barta & Makszin, 2021). I use quarterly bond spreads—the difference between the nominal interest rate on a country’s long-term (10-year) government bond and the nominal interest rate on the 10-year US Treasury Bill (positive/negative values are indicative of higher/lower risk premiums on a country’s government bond)—as my dependent variable for two reasons. First, in contrast to bond yields, bond spreads remove the “noise” in nominal interest rates that stem from global shocks, common downward trends in inflation seen within high-income countries since the late 1990s, and changes in the “world” interest rate, providing a better country-specific proxy of bond investors’ assessment of a sovereign’s risk premium. Second, in contrast to sovereign credit ratings, bond spreads demonstrate greater variation within AMEs. As Barta and Johnston (2023) point out, credit ratings for high-income countries are highly clustered towards the top end of the ratings scale, and exhibit more limited variation (i.e., fewer upgrades and downgrades) than credit ratings for developing countries (Figure A.1 in Appendix A documents the credit ratings of all countries within my sample between 2000 and 2019). This is problematic when examining how the far right impacts investment risk, because as I discuss below, the inclusion of the far right in executive cabinets is a comparatively rare event in advanced market economies (occurring in only 11.4% of the country-quarters in my sample). Of the 209 country-quarters in my sample where changes in credit ratings occur, only 10 of them happen when the far right is serving in the executive. 17 This would complicate the interpretation of beta coefficients’ significance because non-significance could be driven by either a null result or limited variation within the dependent and independent variables.

My sample includes the OECD’s 23 advanced market economies. 18 I opt for quarterly over yearly data in order to track the far right’s entry into and exit from cabinets with greater accuracy, including more fleeting episodes when the far right’s inclusion in government lasted less than a year. 19 While such movements could be better tracked with monthly data, important macroeconomic variables that impact investment risk (notably government debt and the current account balance) are unavailable for time units smaller than quarters. I select (quarters between) 2000 and 2019 as my time period, because the majority of NFRPs in AMEs—roughly 58% of those in Table 1—did not come into existence until the mid-2000s and 2010s. I select the 10-year US T-Bill as my spread benchmark because it is regarded as one of the most secure investments from default and consequently serves as a safe haven during flights to quality (Habib & Stracca, 2015). Because the US serves as the weight for my dependent variable for all other countries, it is automatically dropped from the analysis. However, as a robustness check, I also execute my models weighting countries’ long-term bond yields vis-à-vis the 10-year German government bond 20 (in these models, Germany would be excluded from the sample since it replaces the T-bill as the weight, whereas the US is included). The distribution of spreads within each country is provided in Figures A.2 and A.3 in Appendix A.

Model Specification For the Far Right Party Conditioning Effect

I start my analysis testing Hypotheses 1 and 2. Given that bond spreads are non-stationary,

21

I employ an error correction model (ECM) to test the effect of far right politics on the right’s investment risk advantage over the left.

22

ECMs present a number of advantages over simple pooled cross-section time series (CSTS) analysis. First, it rectifies non-stationarity problems with bond spreads, because the dependent variable is first differenced.

23

Second, in contrast to pooled CSTS data where all variables are first differenced (and hence would capture only short-term effects), ECMs allow one to examine both the short run and long run effect of an independent variable on a dependent variable (see Box-Steffensmeier et al., 2014). This is beneficial for two reasons. First, it enables me to test whether market favoritism of the right is immediate (i.e., investment risk falls when they assume control of the executive but this favoritism disappears thereafter) or prolonged (i.e., lasts the entirety of their tenure). Second, it also allows me to determine if NFPRs impact on right governments’ bond spread advantage is immediate or prolonged (bond investors may be temporarily “spooked” by the far right sharing power with right governments, but this uneasiness may dissipate as time passes and policy track records can be observed). One crucial assumption of ECMs is that the dependent and independent variables are co-integrated. Using the two-step Engle-Granger regression approach (see Box-Steffensmeier et al., 2014, p. 161), I find that the co-integration assumption is fulfilled for all models in Table 3.

24

The baseline ECM is as follows:

I measure government partisanship via executive seat share. I control for the (first difference and lagged level) of executive seat share occupied by mainstream right/liberal parties and Christian Democratic/Center parties (hence, the share of executive seats occupied by left/Social Democratic parties serves as the baseline 27 ). I distinguish Christian Democratic/Center parties from their conservative/liberal counter-parts, because as cross-class parties who have traditionally championed generous social insurance programs 28 they may not hold the same ideological commitment to lower social spending (particularly on pensions) as right parties. 29 Country-quarters ruled by technocrats or care-taker governments are excluded from my sample given their apolitical nature and because these governments are typically formed during periods of acute economic or political crisis, and hence, their existence is most likely to follow rising bond spreads. However, their exclusion does not alter my results: Model II in Table 3 includes care-taker governments, and the results are similar to those of all other models. If markets associate right governments with lower investment risk than left ones (per Hypothesis 1), I anticipate that the beta coefficients on the first difference and/or lagged level of right party executive seat share to be negative. The beta coefficients on the first difference and lagged level of Christian Democratic/Center executive seats relative to the left, is more ambiguous. Like left parties, Christian Democratic parties support higher spending, but for different welfare policies (social consumption/insurance, rather than social investment, see Gingrich & Häusermann, 2015; Garritzmann et al., 2021). Hence, markets may perceive these parties similarly as the left. I use Armingeon et al. (2022) to classify parties as far right, conservative/liberal, Christian Democratic/Center, and left (Figure A.4 in Appendix A provides right and center executive seat share over time for each country in my sample). Executive seat share data also stems from Armingeon et al. (2022).

Testing Hypothesis 2 requires an interaction analysis between far right inclusion in government and right/liberal and Christian Democratic/Center executive seat share. I capture the far right’s inclusion in the cabinet via a simple binary variable (1 if they are included, 0 if not) rather than via far right executive seat share for two reasons. First, the inclusion of far right parties in executives is a relative rare event, with minimal variation amongst non-zero values (Figure A.5 in Appendix A documents far right executive seat share over time by country, while Figure A.6 presents a histogram of far right executive seat share for my entire sample). The extreme limitation in positive values of far right executive seat shares will therefore complicate interpreting whether results for interaction terms are significant, because they could be reflective of limited observations rather than the impact of larger far right partners on right governments’ bond spread advantage vis-à-vis the left. 30 Second, recommended binning approaches for interpreting interaction effects between two continuous variables (see Hainmueller et al., 2019), rest on selecting consistent quantile values for the moderating variable (in this case far right executive seats). Because all values for far right executive seat shares below the 88th percentile in my sample are zero, the selection of consistent quantile values for this variable is impossible. While Durr (1992) notes that the incorporation of dummy variables within ECMs requires “more care” than continuous variables (p. 212), because it requires authors to know when they should “turn off” in the long run, using a dummy variable to measure far right executive inclusion is less problematic because the dummy will return to zero once the far right leaves the executive.

The first difference of the far right executive inclusion dummy captures the immediate effect of these parties’ entry into government on bond spreads, while the lagged level captures the long run effect. Regardless of whether the entry of far right parties into the executive has only a short run effect or a long run effect, I anticipate the beta coefficients to be positive (investment risk is elevated if they enter and/or stay in government). To test Hypothesis 2, I interact the first difference of the far right executive inclusion dummy with the first difference of right and center executive seat shares (this captures how far right inclusion impacts the short run effect of right/center executive seats on spreads), and the lagged level of the far right executive inclusion dummy with the lagged levels of right and center executive seat shares (capturing how far right inclusion impacts these governments’ long run effect on spreads). I anticipate these interaction terms to be positive; if bond markets’ response to right executive seats leads to lower spreads in the short and/or long run, I expect this negative effect to erode if right executives include the far right. Likewise, while the short and long run effects of center/Christian Democratic executive seat share on spreads (relative to the left) are more ambiguous, I anticipate that their interactions with the short and long run effect of far right executive inclusion will be positive.

Descriptive Statistics.

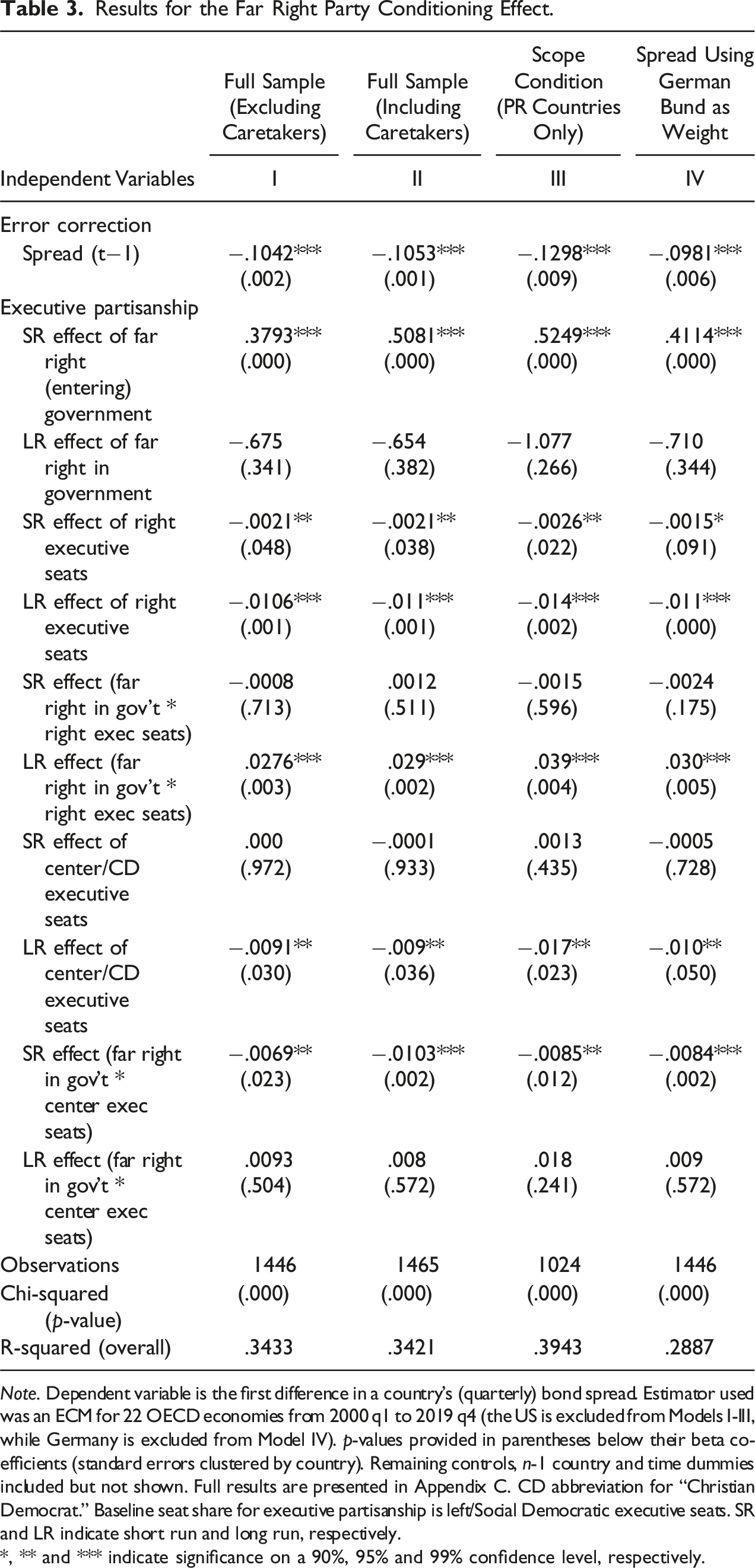

Results for the Far Right Party Conditioning Effect.

Note. Dependent variable is the first difference in a country’s (quarterly) bond spread. Estimator used was an ECM for 22 OECD economies from 2000 q1 to 2019 q4 (the US is excluded from Models I-III, while Germany is excluded from Model IV). p-values provided in parentheses below their beta coefficients (standard errors clustered by country). Remaining controls, n-1 country and time dummies included but not shown. Full results are presented in Appendix C. CD abbreviation for “Christian Democrat.” Baseline seat share for executive partisanship is left/Social Democratic executive seats. SR and LR indicate short run and long run, respectively.

*, ** and *** indicate significance on a 90%, 95% and 99% confidence level, respectively.

Results

Table 3 provides the ECM results. For the sake of simplicity, I only present the beta coefficients for the short run and long run effects of the executive partisanship variables (the short run effect is the beta coefficient on the first difference of the variable, while the long run effect is computed from the beta coefficient on the lagged level of the variable and the beta coefficient on the error correction term using the “nlcom” command), as well as the lagged dependent variable (the error correction). The table of full results—including the beta coefficients on the lagged levels—is provided in Appendix C. The first three models use the US interest rate as the weight for spreads. Model I excludes country-quarters with caretaker/technocratic governments. Model II includes country-quarters with caretaker/technocratic governments. Model III includes only countries with PR electoral systems (this model accounts for my scope condition—far right parties are only able to enter executives in countries whose electoral systems allow them to capture a meaningful number of seats). Model IV presents the results if spreads are weighted against the German bund rather than the US T-bill.

As anticipated, the entry of far right parties into the executive has a significantly positive effect on bond spreads, but only in the short run. From Table 3, bond spreads jump by 38–52 basis points when NFRPs immediately enter office. However, there is no (direct) long run effect of NFRPs inclusion in government on spreads, possibly the result of markets “learning” the intention of these parties over time. Substantiating Hypothesis 1, right executive seats has both a significant short and long effect on spreads, and in the anticipated direction (a rise in right executive seat share, relative to the left, significantly lowers bond spreads). Moreover, the long run effect is substantially larger than the short run effect. From Table 3, if a full right executive entered power (100% right executive seat share), bond spreads would immediately drop by roughly .2% within the first quarter, but spreads would remain prolongedly lower (relative to a full left executive) by 1.1–1.4% (almost half a standard deviation, see Table 2) over the length of its term.

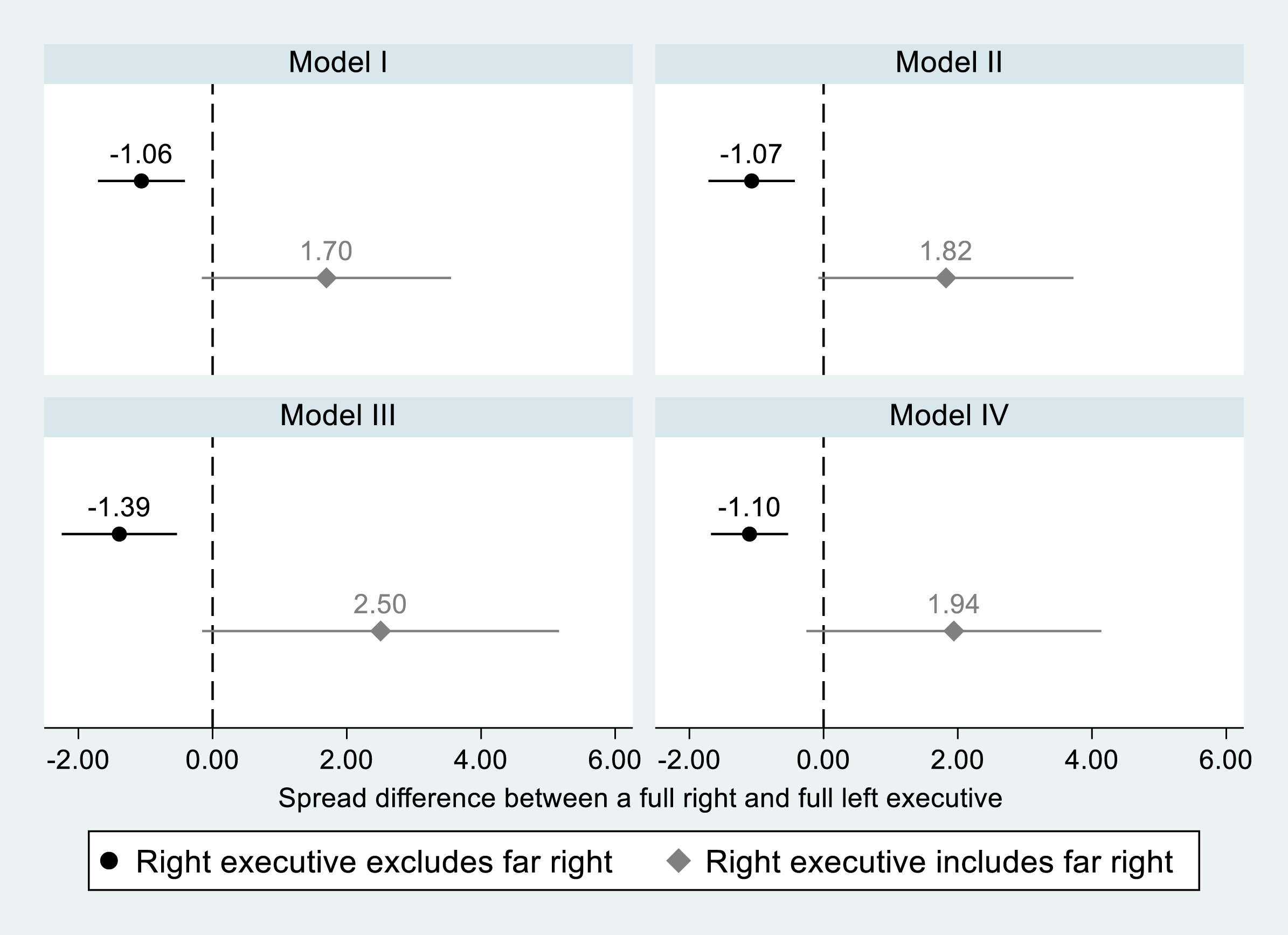

Right executives’ short run bond spread advantage (relative to the left) is not conditioned on serving with the far right (as seen by the non-significant short run interaction term—although right executives would still encounter the significantly positive direct effect of NFRPs entering the executive on spreads). However, their long run bond spread advantage vis-à-vis the left disappears when the far right is in their cabinet (the long run effect of the interaction term between the far right’s inclusion in government and right executive seats is significantly positive). Using the estimates of all four models in Table 3, Figure 3 visually presents the predicted difference (and its 95% confidence interval) in spreads over the long run between a full right executive versus a full left executive when the far right is excluded from (top estimate) and included in (bottom estimate

34

) the right government’s cabinet. The vertical line at 0 indicates a null effect (hence, if the confidence interval of the point estimate straddles that line, bond spreads under full right executives are not significantly different than those under full left ones). While full right executives face significantly lower spreads than their left counter-parts (by over 100 basis points) over the course of their tenure when ruling without the far right, they face higher spreads relative to the left when the far right is included in their government (this positive difference is not significant on a 95% confidence level, but it is significant on a 90% confidence level for all four models

35

). To put this governing penalty into perspective for right governments, the loss of over a 1% spread difference would imply that a right executive in the Netherlands would gain over 4.35 million Euros in debt servicing costs per annum if it incorporated the far right into its coalition, while a right executive in Italy would gain over 25 million Euros in debt servicing costs per annum for similarly choosing to do so.

36

Interestingly, the size of these effects appears to be unmoved by my scope condition—they are similar between the full sample and countries with PR electoral systems. These results substantiate Hypothesis 2, that far right parties are an economic liability for right governments. (Long run) interaction effect between right executive partisanship and far right inclusion in government. Figure derived from estimates in Table 3.

In regards to center executives, while a rise in center/Christian Democratic executive seats (relative to the left) does not significantly impact bond spreads in the short term (although, unexpectedly, the short run interaction between center/Christian Democratic executive seats and the far right’s inclusion in government is significantly negative), it does lead to significantly lower spreads in the long term like a rise in right executive seats does (from Table 3, spreads under a full center/Christian Democratic executive are .9–1.7% lower than a full left executive). However, in contrast to right executives, the long run effect of center/Christian Democratic executive seat share on spreads is not impacted by whether they rule with the far right (the long run interaction term is positive but non-significant), indicating that markets penalize the right for serving with the far right, but not the center/Christian Democrats.

Right Radicalism and the Right’s Bond Market Advantage: Empirical Evidence For the Ideas Effect

Model Specification For the Radical Right Ideas Effect

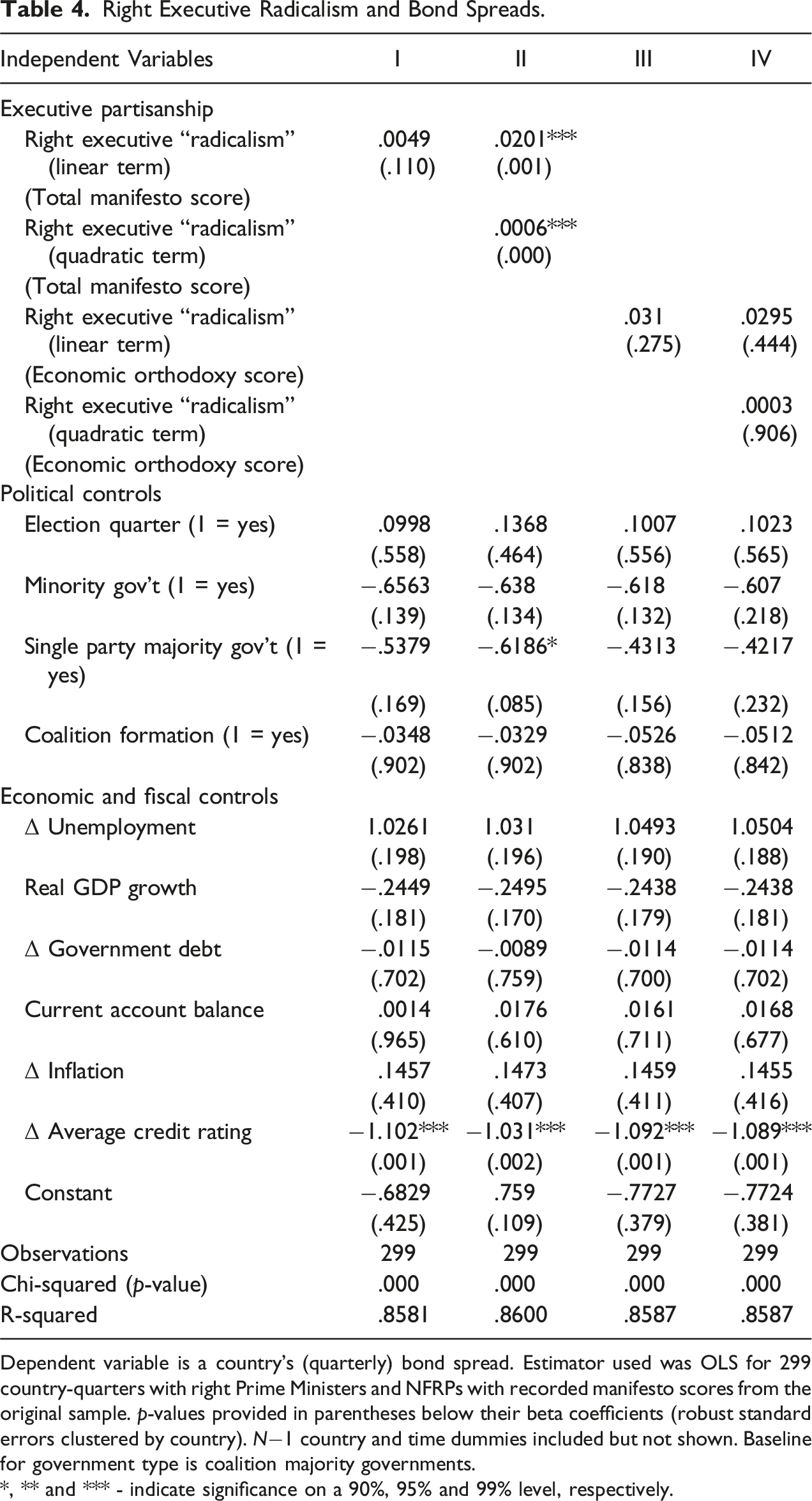

While the above interaction analysis demonstrates that far right inclusion in government eliminates right governments’ bond spread advantage vis-à-vis the left, it does not consider that mainstream right parties can internalize populist far right ideals without serving in formal coalition with NFRPs. In order to test Hypothesis 3, I estimate how right governments’ political positions—measured by their manifesto scores—impact the bond spreads they encounter. For this analysis, I examine bond spreads of right executives only, comparing spreads faced by centric right executives to more radical right-wing ones. This significantly reduces my sample size (to only 299 country-quarters), and renders all my panels unbalanced (making an ECM approach unviable). Within this limited sample, bond spread levels are stationary, but several of my economic controls (the unemployment rate, government debt, inflation, and country’s average credit ratings) are not.

37

Hence, as a conservative approach to addressing non-stationarity within these variables, I employ a partial differenced linear model, differencing variables that are non-stationary, but keeping variables that are stationary in levels. My baseline model for testing Hypothesis 3 is as follows:

To track the radicalism of right governments’ ideological positions, I utilize the aggregated “right-left position” score from the Manifesto Project (Burst et al., 2021), which is a composite of parties’ positions on: cooperative foreign policy and international relations (including trade protectionism), law and order and civil liberties, state intervention in the economy (including regulation, nationalization, and welfare spending), civic inclusivity and support for (or appeals towards) patriotism and nationalism. Higher values indicate a party is more right-wing. Rather than attempting to determine the threshold by which right parties’ total manifesto scores become “officially” populist far right (a difficult task, given that these scores are highly variable across countries and over time), I use a relative measure to ascertain when leading right parties adopt far right ideas: the difference in their aggregated right-left manifesto score with that of the largest NFRP within the country in quarter t (I term this variable “right executive radicalism” below).

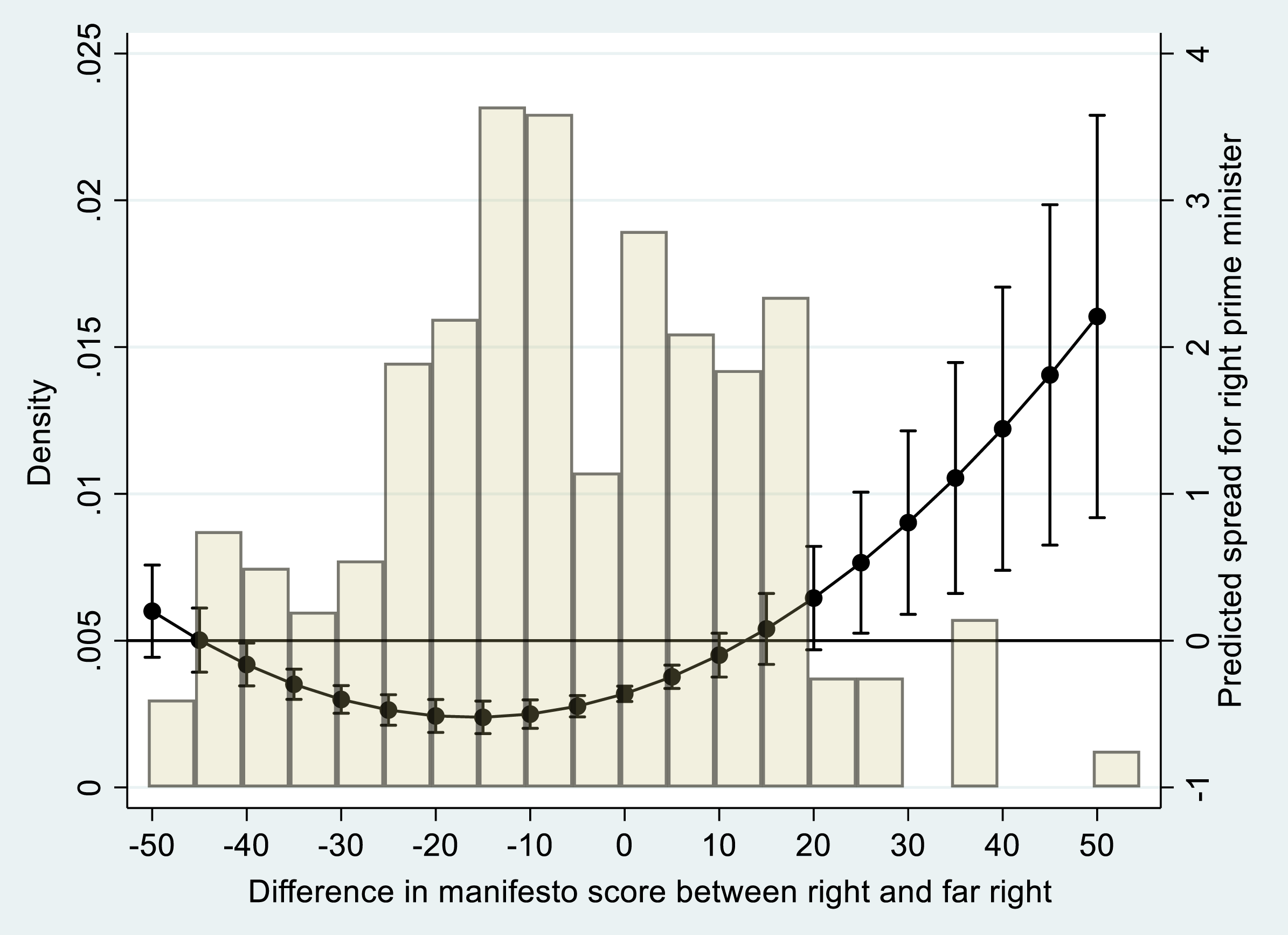

38

If this value is positive, then a country’s mainstream right party is further to the right of its leading far right party, while if the value is negative, it is further to its left (I present the distribution of this variable across right executives in Figure 4). Models I and II in Table 4 focus on differences in total manifesto scores between the mainstream and far right. Models III and IV examine differences in the economic orthodoxy (manifesto) scores only between right and far right parties. While we should expect markets to be weary of right executives that are further right of NFRPs in general, they may be more receptive to right executives that are to the right of NFRPs on economic policy (i.e., more neoliberal). Right executive radicalism and bond spreads (graphical depiction). Figure derived from estimates in Model II, Table 4. Positive/negative values indicate a right party has a manifesto score that is to the right/left of that of the country’s largest far right party. Right Executive Radicalism and Bond Spreads. Dependent variable is a country’s (quarterly) bond spread. Estimator used was OLS for 299 country-quarters with right Prime Ministers and NFRPs with recorded manifesto scores from the original sample. p-values provided in parentheses below their beta coefficients (robust standard errors clustered by country). N−1 country and time dummies included but not shown. Baseline for government type is coalition majority governments. *, ** and *** - indicate significance on a 90%, 95% and 99% level, respectively.

Results

Table 4 and Figure 4 present the results for Hypothesis 3. Model I in Table 4 presents the linear term of total right executive radicalism, while Model II includes both a linear and quadratic term of right executive radicalism (as it is possible that investors might become weary of right executives that become too left-wing relative to NFRPs, as well as of those that are too right-wing). Models III and IV present the difference in market orthodoxy manifesto scores rather than the total manifesto score (Model III includes a linear term for this variable, while Model IV includes a linear and quadratic term). Spreads in Table 4 are weighted by the US T-bill, but Table E.1 in Appendix E presents these results for bond spreads weighted by the 10-year German bond (results are the same).

While the linear term of right executive “radicalism” is positive (indicating that as right governments’ manifesto scores creep further right to those of NFRPs, bond spreads rise), it is non-significant. Rather, total right government radicalism displays a significant parabolic (U-shaped) relationship with bond spreads (this quadratic relationship in Model II is depicted visually in Figure 4, with 95% confidence intervals for each point estimate—the horizontal line at zero indicates that a country’s nominal interest rate is the same as that of the US’s. The y-axis on the left-hand side denotes the density distribution of the sample across differences in the manifestos scores, while the y-axis on the right-hand side provides the predicted spread value). Bond spreads for right governments are significantly below zero (indicating that their borrowing costs are lower than the US government’s) when their manifesto scores are to the left of NFRPs. If right executives become “too left” relative to NFRPs (with a difference in right/left manifesto scores of negative 40), their borrowing costs are not significantly different from the United States’. However, as right governments’ manifesto scores become more right-wing than NFRPs, bond spreads rise. Right executives whose right/left manifesto scores are 25 points or higher than those of NFRPs face significantly positive bond spreads (indicating that the nominal interest rates they face are higher than that for the US T-bill, see Figure 4). In contrast to differences in total manifesto scores, differences in market orthodoxy scores between the right and far right do not significantly impact spreads, either linearly or quadratically.

In sum, the results above indicate that right executives, regardless of whether they formally partner with the far right, are penalized by markets when their policy positions become overly radical relative to far right parties. Borrowing costs of right executives are only lower than those faced by the US government when their manifesto scores are to the left of those of NFRPs.

The Economic Liability of Partnering With the Far Right: A Comparative Case Study of the Netherlands and Sweden

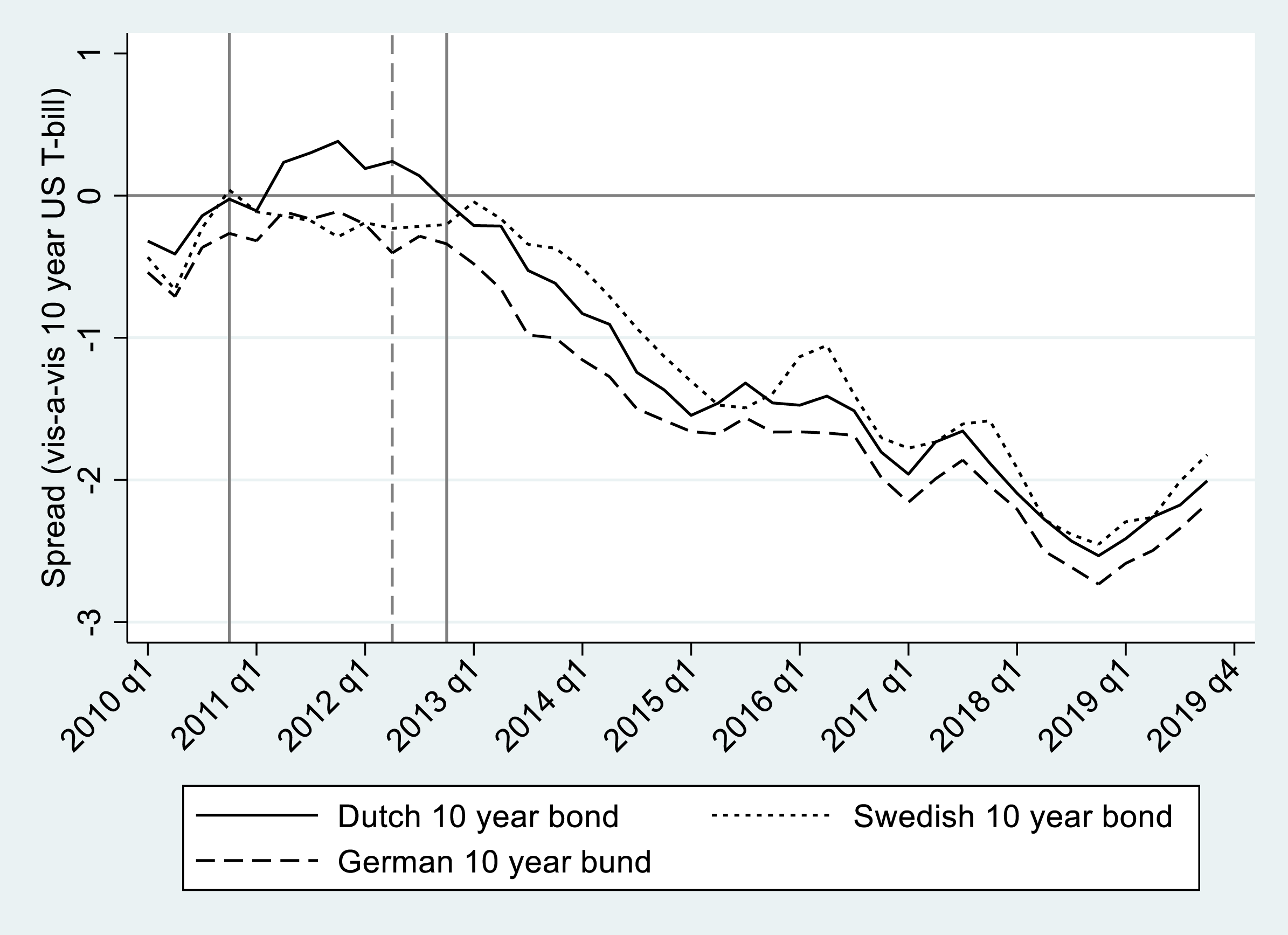

To further scrutinize the underlying causal mechanism behind the results above, I employ a comparative case study to unpack the political dynamics of the instability premia that NFRPs unleash upon their mainstream right counter-parts. Rather than selecting a most likely case, where a right government partnered with a NFRP in a country with comparatively higher investment risk (i.e., Silvio Berlusconi’s various coalitions with the Northern League and National Alliance during the 2000s in Italy), I select a least-likely case: Mark Rutte’s first center-right minority cabinet (led by the Liberals—VVD—and including the Christian Democratic Appeal) in the Netherlands. Rutte’s first cabinet served from October, 2010 to November, 2012, holding a confidence-and-supply agreement with Geert Wilders’ far right Party for Freedom (PVV) from October, 2010 to April, 2012. In order to hold constant as many extenuating factors as possible when examining bond market activity under Rutte’s first cabinet, I contrast the Dutch case with Fredrik Reinfeldt’s second cabinet in Sweden (serving from October, 2010 to September, 2014), also a center-right minority cabinet (the conservative Moderates served with the Liberals, Center Party, and Christian Democrats), but one that refused any kind of governing arrangement with the far right Sweden Democrats. Both countries have traditionally embraced “fiscal prudentialism” and public borrowing rules (public debt during the pre-crisis 2000s rarely exceeded 50% of GDP in either country, EU AMECO, 2023), produced consistent current account surpluses, and are notorious members of the EU’s “frugal four” who demanded significant austerity concessions from E(M)U’s debtor states during the height of the European Debt Crisis. Due to their fiscal prudence, both countries also escaped the collective downgrades that credit rating agency Standard and Poor’s imposed on much of the Euro-area in January 2012 (Geewax & Peralta, 2012). Consequently, if any right cabinet should have been immune from the economic costs of ruling (indirectly) with the far right, it should have been Rutte’s.

Yet examining bond spreads in the Netherlands over Rutte’s long tenure, spreads were highest (and positive) only during Rutte’s first minority cabinet (the tenure of Rutte’s first cabinet is marked in Figure 5—the solid vertical gray lines mark the full term of his cabinet, while the dashed gray line marks the quarter where PVV exited its confidence-and-supply arrangement supporting his government). Moreover, it was only during Rutte’s first cabinet when Dutch bond spreads exceed those of Sweden’s, who was also navigating treacherous waters on global financial markets with an oversized financial sector.

39

While one crucial difference between both countries is Euro-zone membership (a potential liability for the Netherlands during the most intense months of the crisis), the only other Euro-zone creditor country that was also ruled exclusively by a center-right coalition at the time (Germany’s second Angela Merkel cabinet), witnessed similar (more moderated) bond spread rises to Sweden’s. Rutte’s entry into power in 2010 marked the first time in its post-war history that the Netherlands was ruled by a right government. Yet Dutch borrowing costs were irregularly elevated when his first cabinet relied on the far right’s support. Bond spreads in Germany, the Netherlands and Sweden (2010–2019). Solid vertical gray lines mark the tenure of the first Rutte cabinet. Dashed vertical gray line marks the exit of the PVV from its confidence-and-supply agreement. Source data: OECD (2022).

What made a PVV-supported government so problematic for market confidence in Dutch bonds? I argue that PVV increased Rutte’s cabinet’s instability premium first through the policy channel, and then through the governance channel once it triggered its collapse. The IMF’s 2011 Article IV Consultation highlighted that perhaps the most problematic policy “liability” for the Netherlands after the onset of the Euro-crisis was the lack of structural reforms that “would alleviate the adverse impacts of the crisis and population aging on growth” (2011a, p. 2). While the Fund claimed that the Netherlands entered the crisis with a strong fiscal position and “no immediate fiscal credibility issue” (p. 22), it also claimed that government’s discussions with unions and employers to ensure the solvency of major pension funds were “laborious and slow-moving” (p. 17), and that “widespread uncertainty on future benefits” (p. 6) was an important challenge for the country (IMF, 2011b). Pensions were perhaps the major stumbling block in budget negotiations between the Rutte coalition and PVV. In its 2010 manifesto, the PVV claimed that raising the retirement age was line they would not cross, while their suggested cuts to deliver fiscal consolidation were a tenth of those proposed by Rutte’s VVD, driven in part by their refusal to raise the retirement age (Afonso, 2015, p. 283).

PPV’s steadfastness to defend the Dutch welfare system did not disappear even as the European Debt Crisis was intensifying. Wilders refused to agree to any proposals that would raise the retirement age and claimed that he was “happy to get his wallet out” to provide greater funding for elderly care (Fenger, 2018, p. 196). By the end of 2011, the Dutch economy considerably worsened, as jittery bond investors were concerned that the country would miss its budget targets. In April, 2012, Fitch warned the government that its AAA credit rating was at stake if it could not reduce its budget (Deutsche Welle, 2012a). Rutte became more determined to achieve fiscal consolidation, and proposed an additional 16 billion Euros in cuts to appease markets and meet the EU’s fiscal rules (BBC, 2012). One important component of this package was increasing the retirement age before 2020, a PVV redline (Afonso, 2015, p. 285). Wilders refused to agree to any of VVD’s austerity demands, stormed out of the budget discussions, and on April 23rd, triggered a collapse in government, marking the first time since the global financial crisis that a government of a Northern EMU creditor state was brought down.

Wilders’ actions, which further heightened the Rutte government’s instability premium through the governance channel, had an immediate impact on stock and bond markets. Stock prices within the German DAX dove by 3.4%, the FTSE 100 realized a triple-figure loss of 120 points, and even prices in US markets declined by 1% due to the fall in government (The Guardian, 2012; Schneider, 2012). Within hours of the government’s collapse, interest rates on Dutch bonds surged to their highest levels within three years, vis-à-vis the Germany Bund, as investors replaced purchases of 10-year Dutch bonds with German ones (Sithole-Matarise, 2012). Two days after the fall of government, elections were called for September 12th, placing further pressure on Dutch interest rates (and its AAA credit rating) with the possibility of a governance vacuum for several months (Webb, 2012). Rutte’s remaining coalition partners entered crisis mode, soliciting support for their budget proposals from opposition parties. After two days of intense negotiations—and worsening market conditions and rising bond yields—Rutte’s Liberals and the Christian Democrats managed to secure support from Democrats 66, the Green Left and Christian Union for a 2013 austerity budget. The budget included increases on value added taxes and employer levies supporting unemployment benefits, salary freezes for civil servants, and the (gradual) increase of the retirement age (Deutsche Welle, 2012b; Grünell, 2012). Investor jitters over Dutch bonds ebbed and bond spreads subsequently fell (see Figure 5). However, Dutch broadsheets accused Wilders’ and PVV of “throw[ing] the country into crisis” (Van Holsteyn, 2014). Despite the clear economic risks of political deadlock, the PVV refused to converge on the Liberals’ budgetary position, significantly increasing the Netherlands’ bond (instability) risk premium at a time when the country could least afford it.

Amidst the political turmoil in the Netherlands, Sweden appeared to be one of Europe’s last safe havens for risk-averse investors. In October, 2012, a leading investment manager from the Dutch multinational banking and financial services conglomerate ING, claimed the “Swedish government bond market to be the safest market in the world regarding default risk,” predicting that “Sweden will keep its safe haven status for the foreseeable future,” due in large part to its sound public finances (Johnson & Lannin, 2012). Calmer politics within Sweden during this period were not a foregone conclusion in the lead up to the 2010 election. Like Rutte’s Liberals, Fredrik Reinfeldt’s Moderates faced a strong electoral challenge from the new far right Sweden Democrats. The possibility of the Sweden Democrats gaining a substantial share of seats in the Riksdag even looked likely to “trigger a fall” in the krona vis-à-vis the Euro, introducing uncertainty and volatility to Swedish financial markets (Borger, 2010). Yet despite the fact that the election returned a minority center-right minority government (while Reinfeldt’s Moderate party gained seats, this was offset by losses incurred by his coalitions partners), Reinfeldt refused to enter a governing arrangement with the Sweden Democrats, rather attempting to develop an informal coalition with the Greens (Ibid).

That Sweden did not realize similar rises in interest rates during Reinfeldt’s second cabinet is all the more remarkable considering that it deliberately pursued fiscal expansion in 2010 as a response to the slow-down in the global economy. Discretionary fiscal measures in the 2011 budget accounted for 4% of GDP, with .7% of this stimulus targeted exclusively towards “crisis-related” spending aimed at supporting public sector employment within local authorities (IMF, 2011a, p. 9 and 12). Yet this stimulus was pursued at the same time as the government was reaping savings on past structural reforms reducing sick leave and early retirement eligibility, counter-acting the 4% stimulus with a savings of 2.3% of GDP (IMF 2011a, p. 12). Due to pension reforms made in the 2000s, as well as the adoption of fiscal rules which mandated fiscal surpluses and expenditure ceilings over the medium term (Flodén, 2012), major international financial institutions were unconcerned by Swedish pension liabilities. When affirming Sweden’s AAA status in October 2011 and 2012, Standard and Poor’s noted that despite Reinfeldt’s announcement for further stimulus in 2013, which prioritized spending on education and infrastructure (IMF, 2011a, p. 14), prior reforms had significantly eased the burden of rising pension payments on the state, providing the fiscal space to increase discretionary spending (S&P’s, 2011, 2012). What further aided Reinfeldt’s fiscal policies was the fact that the Sweden Democrats—who were supportive of generous pension and entitlements to Swedish citizens, in light of their capture of a substantial number of previously Social Democratic-affiliated working-class voters after the 2006 election (Hellström et al., 2012)—were never in a position to reverse these policy decisions nor to trigger a fall in government. By sidelining the far right, Reinfeldt’s Moderates avoided the instability premium that the PVV unleashed upon the Dutch Liberals, which helped the country weather the economic storm facing Europe.

Conclusion

Far right populism has become a defining feature of political systems within the West over the past two decades. Discontent with elites and status-quo politics has triggered backlash from electorates, creating the political space for NFRPs to enter parliaments and governments. Directly or indirectly, right parties across Europe have increasingly and strategically brought NFRPs into their coalitions in order to form governments and capitalize on these parties’ support. While the political consequences of right parties doing so are far from clear given electorates’ changing attitudes (see Twist, 2019), this paper shows that market actors may prove more critical of the mainstream right’s decisions to do “deals with the devil.” Because NFRPs embrace isolationist and obstructionist policies, investors attach instability premia to their inclusion in government, producing tangible borrowing costs for right executives they rule with. This paper did not consider whether similar investment risks dynamics emerge on the left (i.e., whether left governments incur further penalties from markets if they serve with the far left) because executives that include the far left are even rarer than those that include the far right (only 5.9% of country-quarters in my sample included left populist parties within the executive). However, as populist forces mobilize on the left end of the political spectrum, and as these parties also become increasingly successful in influencing left-leaning executives, examining how these dynamics unfold for mainstream left parties would be a fruitful avenue of future research.

My results have important implications for the electoral politics literature on the far right. While this literature has extensively documented the political causes and consequences of the far right’s inclusion in government—including how NFRPs view and impact welfare policies—it has focused less on how economic elites and markets more broadly have “priced” these developments. My findings highlight that right parties must not only consider the political consequences of cooperating with the far right, but also economic ones. These economic consequences may be less visible during times of economic calm, but they can be devastating during times of crisis, as Mark Rutte painfully learned (in 2018, Rutte publicly acknowledged that working with the PVV was “the biggest mistake of my career,” NL Times, 2018). The borrowing costs stemming from the far right’s instability risk premium will almost certainly intensify amidst the economic fallout from the Coronavirus pandemic and Russia’s war against Ukraine, which not only substantially increased public debt levels, but also ended the era of near-zero nominal interest rates for high-income countries.

My results also have important implications for the IPE literature examining how markets price politics. While this literature has become saturated with studies on how markets perceive the left and right, few have closely studied how investors judge the extreme end of the right spectrum. Empirically there is good justification for this, as NFRPs were not a dominant political force within in high-income countries before the 2000s. However, the rise of “anti-system” politics since the global financial crisis has completely reconfigured the political map of some advanced democracies (Hopkin, 2020), and the electoral squeeze this has placed on mainstream parties has caused some of them to reconsider their traditional economic platforms in order to appeal to voters. A consequence of this is that markets’ perceptions of the right might also become reconfigured, as investors grow weary of right parties who jeopardize stability for political gain.

Supplemental Material

Supplemental Material - So Right It’s Wrong? Right Governments, Far Right Populism, and Investment Risk

Supplemental Material for So Right It’s Wrong? Right Governments, Far Right Populism, and Investment Risk by Alison Johnston in Comparative Political Studies.

Footnotes

Acknowledgments

I thank the Max Planck Institute for the Study of Societies (and Lucio Baccaro in particular) for the time and resources needed to complete the data collection for this paper in Winter, 2022. I also thank Lucio, Virginia Crespi de Valldaura, Tim Vlandas, Daphne Halikiopoulou, participants at the 2023 Council of European Studies annual conference, three anonymous reviewers and the editors for their valuable comments. Any errors are solely my own.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biography

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.