Abstract

Why do countries repeal the inheritance tax? To investigate this question, we use a novel dataset on inheritance tax introductions and repeals worldwide. We argue that revenue requirements are the main determinant of repeal risks: The inheritance tax is resilient as long as it is central to the national revenue system; it becomes vulnerable to attacks once the rise of more efficient tax instruments marginalizes its revenue contribution. Devoid of fiscal purpose, its survival depends mainly on its redistributive features. Redistribution, however, is essentially contested and should be more important in democracies. The evidence is in line with our conjecture: The likelihood of inheritance tax repeal increases as other more buoyant taxes rise and non-democracies are more likely to repeal the tax than democracies.

The Rise and Fall of the Inheritance Tax

Wealth inequality is high and rising. The inheritance tax

1

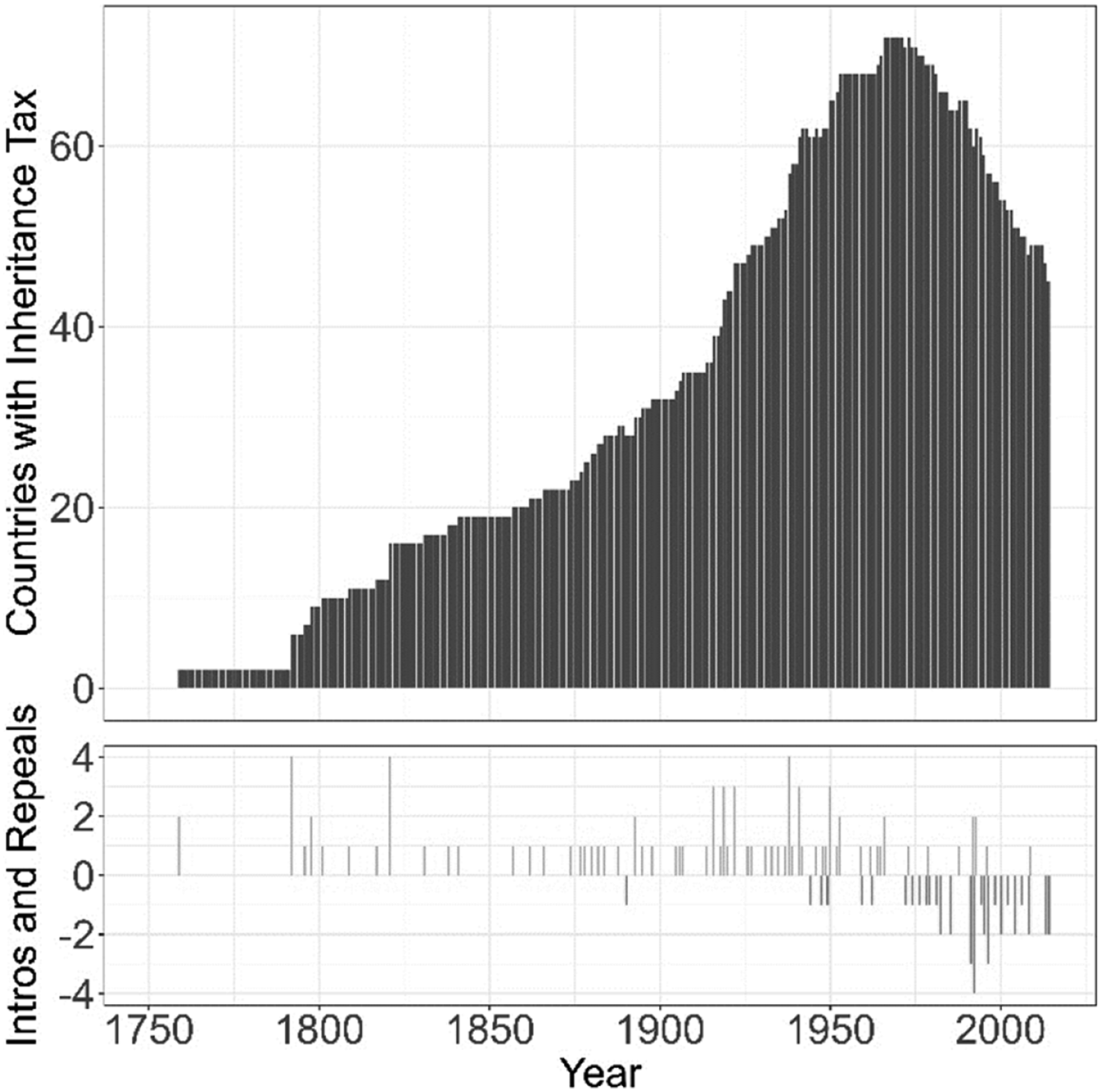

is an obvious instrument to mitigate it. Experts praise the tax for its redistributive potential and incentive-compatibility and call for its expansion (OECD, 2018; Piketty, 2020). Yet, many governments repeal the tax. After a steep increase in the number of countries levying the inheritance tax in the 19th and early 20th century, the number has declined rapidly since the 1960s (Figure 1). Why? The Global Rise and Fall of the Inheritance Tax. Sources: Seelkopf et al. (2021), own coding.

The demise of the inheritance tax is surprising given the stability of other signature taxes of the modern state. All relevant states worldwide have personal income taxes, corporate income taxes, and social security contributions, and very few states consider abolishing them (Genschel & Seelkopf, 2022; Seelkopf et al., 2021). It is true that general sales taxes have been rescinded at a fast clip since the 1970s but only to be replaced by another tax on general consumption, the value added tax (VAT) (Ganderson & Limberg 2022). Repeals of the inheritance tax, by contrast, are not usually followed by the introduction of new taxes on wealth. They are part of a general downward trend in wealth taxation (Hope & Limberg 2022; Lierse, 2022).

The demise of the inheritance tax is also surprising for theoretical reasons. In public policy research, the conventional wisdom holds that policies are rarely ever terminated (Adam & Bauer 2018; Bardach, 1976; Behn, 1978; Frantz, 1997; Zhang, 2009). Even dysfunctional and obsolete policies survive because their constituents are well placed to fend for their survival. Their interests are entrenched in the status quo while the proponents of repeal must fight in the open. As a result, policies cumulate, layer by layer, onto an ever-higher pile that burdens the administrative capacity of governments and undermines effectiveness and efficiency (Adam et al., 2019). The work horse theory in political economy, the median voter theorem (Downs, 1957; Meltzer & Richard 1981) likewise predicts stability and resilience: Since the repeal of the inheritance tax would mainly benefit an asset-rich minority (Piketty, 2020, p. 556), the asset-light majority should have strong incentives to block it. In a democracy, where numbers count, it should also have the power to effectively prevent repeal.

Various explanations have been offered why the inheritance tax is less resilient to repeal than the public policy and the political economy perspective suggest. Some authors highlight information asymmetries: Low- and medium-income voters often overrate their position in the wealth distribution, underrate the redistributive effect of the inheritance tax and therefore are indifferent to, or even supportive of, inheritance tax repeal (Bartels, 2005; Campbell, 2010; Erikson, 2015). Others emphasize fairness concerns: The poor consider the wealth of the rich as the well-deserved fruit of intelligence, hard labour, and bold risk-taking. Therefore, they oppose redistributive taxation (Durante et al., 2014; Fong, 2001). Yet others highlight representational biases in the policy process: Tax policy making is dominated by the structural and instrumental power of capital. Capital owners have a material stake in the abolition of the inheritance tax and have the means to further it. They can threaten, for instance, to move their mobile assets abroad, leaving the domestic economy with fewer investments, fewer jobs, and less economic growth. In this view, governments repeal the inheritance tax to keep capital onshore (Bakija & Slemrod, 2004; Birney et al., 2006; Culpepper, 2010; Emmenegger & Marx, 2019; Gilens & Page 2014). The short version of all these explanations is that imperfections in the political process allow economic elites to capture tax policy making and bias it against the distributive interests of lower and middle classes.

However, if information asymmetries, fairness concerns, and representational biases fuelled inheritance tax repeals since the 1960s, why did they not block inheritance introductions before? Roughly 30% of all inheritance tax introductions in our dataset happened before the end of the 19th century (Figure 1). It is hard to believe that lower income strata were better informed, that governments were more responsive to the poor, or that normative deference to the rich was less widespread at that time. To be sure, the globalization of markets may have fuelled capital flight and international tax competition in recent decades, thus increasing the structural power of capital und undercutting political support for inheritance taxation. But then barriers to cross-border capital movements were also low during the 19th century, and the levels of capital accumulation and wealth inequality were high (Our World in Data, 2022). Something else must have changed in the politics of inheritance taxation.

So far, the existing literature has focused on the demise of the tax in a few advanced Western democracies – the United States, Sweden, Austria, Switzerland, etc. – in recent decades. In this paper, we use a global sample of 87 countries and a period of observation of roughly two centuries to study the recent fall of the tax in light of its earlier rise. We probe the historical conditions of the introduction and consolidation of the tax to develop hypotheses about its repeal. We then test the hypotheses against novel data on inheritance tax repeals worldwide and check the robustness of our findings. The analysis suggests that two factors can help to explain the puzzling demise of the inheritance tax: First, the redistributive function of the tax, which is the central focus of recent analyses of inheritance taxation, and second, the revenue function of the tax, which is often strangely absent from the analysis.

The redistributive function explains why inheritance taxation is often politically contested as the tax divides taxpayers into – actual or perceived – winners and losers (Beramendi & Rehm 2016). The revenue function explains why the distributive conflict does not always dominate tax policy making: To the extent the government depends on inheritance tax revenues to fund mandatory spending requirements, the conflict over the distribution of the revenue burden is a secondary concern. The government stands by the tax regardless of the distributive preferences of its supporters (e.g. Steuerle, 2010; Wildavsky, 1986, p. 6). To the extent alternative revenue instruments are available, distributive considerations gain salience. ‘Political uncertainty’ (Moe, 1990) increases. Political attacks on the tax become more likely. The risk of repeal rises. Whether the risk materializes then depends crucially on the distributive preferences of the government.

Our analysis yields two main findings. First, the risk of inheritance tax repeal depends on the revenue function: If the tax is central to national revenue, the likelihood of repeal is low. However, if the fiscal significance of the inheritance tax is minor because other more buoyant tax alternatives are available, the risk of repeal is high. Second, at any level of risk the likelihood of repeal depends on the redistributive preferences of the government. All else equal, repeals are less likely in democracies than in autocracies.

Revenue, Redistribution, and the Introduction of the Inheritance Tax

In this section we explore the historical conditions of the rise of the inheritance tax. We show that the decision to introduce the tax was closely associated with pressing revenue needs and a lack of revenue capacity to meet them. Furthermore, we analyze the role played by redistributive concerns in legitimizing the tax. In conclusion, we derive hypotheses about how considerations of revenue and redistribution condition the likelihood of inheritance tax repeal.

Revenue

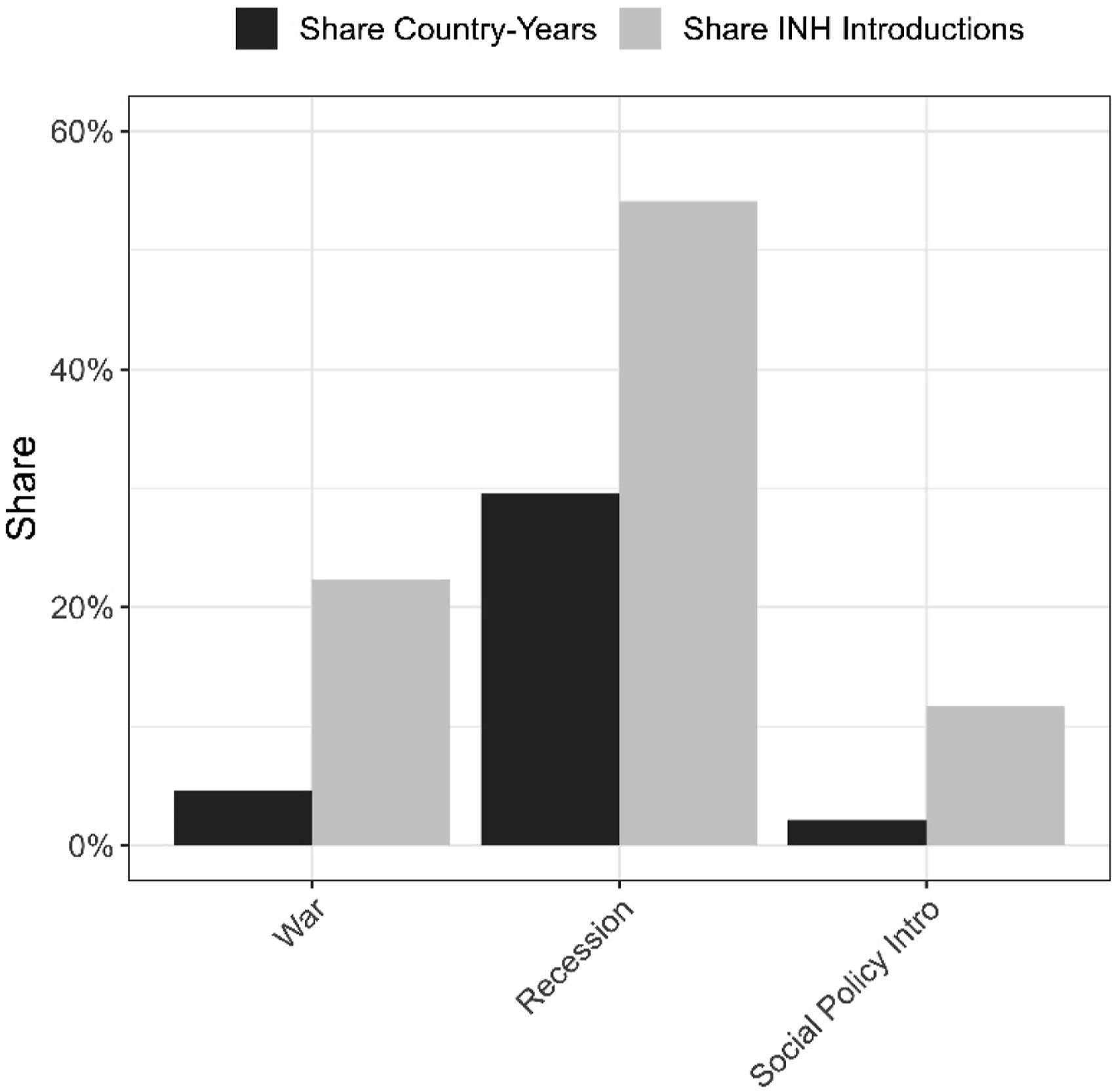

The introduction of a new tax is usually ‘a quite public event, accompanied by a high degree of negotiation from a wide range of potential taxpayers’ (Levi, 1988, p. 49). Political risks are high. Governments have good reasons to avoid them unless there is no other choice. How much choice there is depends crucially on fiscal conditions. The historical record suggests two fiscal conditions of inheritance tax introduction in particular: High public revenue requirements and weak revenue capacity. Figure 2 provides evidence of the first condition. It shows that most inheritance tax introductions were associated with three triggers of mandatory spending: Wars, recessions, and social security programs. While only 5% of the country-years in the data are years at war (dark grey column), more than 20% of all inheritance taxes were introduced during these years (light grey column). The pattern for recessions or the introduction of new social policy programs is similar as both events account for a minor share of country-years but a major share of inheritance tax introductions. There is extensive evidence to suggest that the temporal association of new revenue requirements and inheritance tax introductions is not spurious (Genschel & Seelkopf, 2022). Spending-Intensive Events and Inheritance Tax Introductions. Sources: Genschel and Seelkopf (2019), Seelkopf et al. (2021), Sarkees and Wayman (2010), Gapminder Foundation (2020), Schmitt et al. (2015). The general share of country-years looks at the years in the immediate aftermath of a war/recession/social policy introduction (5 years lag) as a share of all country-years. The share of inheritance tax introductions looks at the inheritance tax introductions in the immediate aftermath of a war/recession/social policy introduction (5 years lag) as a share of all inheritance tax introductions.

Warfare is a major driver of inheritance tax introductions. There are numerous examples of countries that introduced the inheritance tax to pay for war. Austria adopted the first inheritance tax in the dataset in 1759 to help cover the costs of the Seven Years war (Schanz, 1901, p. 62). Britain introduced an estate tax in 1796 to pay for the Napoleonic wars (Shultz, 1926, pp. 20–21). New Zealand did so in 1866 to fund the war with the Maori (Littlewood, 2014, p. 6). Various British Colonies including Jamaica (1916), Kenya (1918), 2 Sri Lanka (Ceylon–1919), and Tanzania (Tanganyika–1919) introduced the tax during or immediately after WWI (Seelkopf et al., 2021). China followed in 1939 while under attack from Japan (Li, 1991, p. 9).

Recessions have also triggered inheritance tax introductions. Boxed in between high spending needs for social and economic support, declining tax revenues, and escalating borrowing costs, governments often resort to new taxes. Greater Colombia (current day Colombia, Ecuador, Panama, and Venezuela) adopted the inheritance tax in 1821 to help compensate the end of colonial economic privileges including the trade monopoly with Spain and inter-colonial transfers from Mexico and Peru (Zuluaga, 2021). Chile, Mexico, Russia, Sweden, and Tunisia introduced inheritance taxes during the Long Depression, 1873–1896 (Papadia & Truchlewski 2022). Greece did so in 1898 after its GDP per capita had contracted by 15% the previous year (Morys, 2016).

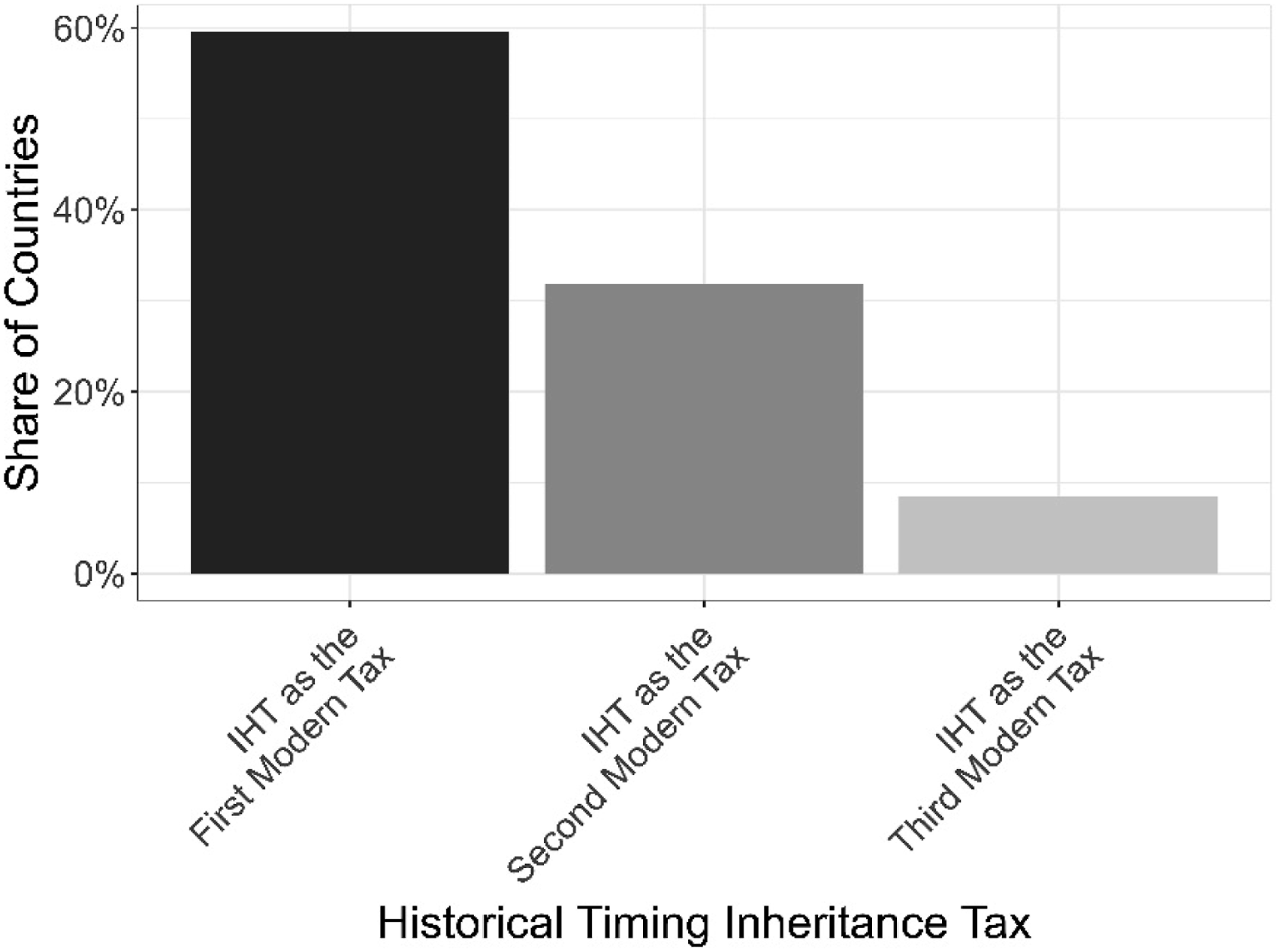

The introduction of social policy programs can also accelerate inheritance introductions. Social commitments are costly and difficult to cut (Pierson, 1996; Steuerle, 2010). The inheritance tax can help funding them. Examples include Peru (introduction of work injury insurance in 1911 and of the inheritance tax in 1916), Finland (unemployment insurance in 1917; inheritance tax in 1919), and India (old age pension insurance in 1952; inheritance tax in 1953). Yet, as Figure 3 also shows, the number of tax introductions after social policy innovation is low. Arguably this has to do with the other fiscal condition of inheritance tax introductions: weak revenue capacity. The Timing of Tax Introductions - Inheritance Tax (IHT) Versus Other Modern Taxes (Income and Consumption Tax). Sources: Genschel and Seelkopf (2019), Seelkopf et al. (2021).

The likelihood that rising revenue requirements trigger the introduction of the inheritance tax varies in the availability of other, potentially more revenue-efficient tax instruments. 3 The absence (presence) of alternative revenue instruments increases (decreases) the likelihood of inheritance tax introductions. The two most important revenue instruments today are the (corporate and personal) income tax and a general consumption tax (usually of the VAT type). When social policy programs began to spread in the 20th century, these broad-based taxes were often already in place or at least ready for adoption. This weakened the revenue argument for inheritance taxation. As Figure 3 shows, 60% of the countries in the sample introduced the inheritance tax before income and consumption taxes. Less than 10% introduced it thereafter.

During the 18th and 19th century, the revenue argument for inheritance taxation was strong. Even in advanced Western economies, governments still depended on pre-modern taxes with limited revenue potential, including direct monetary and in-kind charges on people (forced labour, poll taxes, etc.), land and its produce (e.g. the tithe), features of real assets (e.g. the number of windows or chimneys), or stamp duties on legal transactions (e.g. marriage licenses or military commissions) (Cardoso & Lains 2010; Kiser, 2021; Kiser & Karceski 2017; Peters, 1991; Seelkopf et al., 2021; Webber & Wildavsky 1986). Indirect taxes included trade taxes (at internal and external borders) and excises on specific goods (salt, beer, matches, etc.). The direct taxes were narrow-based and only loosely connected to economic activity. Revenues did not rise with nominal growth, and rich elites (the church, the nobility) were often exempted by traditional privilege. The revenue potential of excises was limited by regressivity: They fell mainly on the poor who had little taxable income to begin with. Trade taxes were more buoyant but highly distorting. Internal tolls hindered national economic unification.

The inheritance tax promised to lift these revenue constraints. In contrast to traditional direct taxes, it drew on potentially all income-bearing assets (land, real and financial capital), and taxed them at their assessed value rather than just by a lump sum (like stamp duties) or a rough proxy (like window taxes). It was also administratively convenient because the taxable event (death) was easy to observe and the taxpayer (the heir) had a self-interest in reporting taxable assets to gain legal title of them (Scheve & Stasavage 2012, p. 88). In contrast to excises, it fell on taxpayers who could afford to pay it: rich heirs (West, 1893). In contrast to trade taxes, it did not constrain domestic or international trade. In short, compared to available alternatives, revenue efficiency was high.

While historical revenue data are sketchy, there are various examples of high-yield inheritance taxation. They include the Cape Colony, one of the predecessors of modern South Africa, where the tax raised roughly 15% of public revenues in the 1850s (Gwaindepi & Siebrits 2020, p. 176), Chile where inheritance and property taxes constituted the third most important source of revenue in the 1880s (Sater, 1976, p. 328), Britain were the tax accounted for 12% of total revenues in 1900, Austria (6% of revenues in 1910) (Flora, 1983, p. 339), New Zealand (13.5% of revenues in 1915) (Duff, 2005, p. 87), and the United States (up to 10% of revenues in the 1930s) (Jacobson et al., 2007, p. 125).

The expansion of first personal and corporate income taxes and then general consumption taxes during the 20th century weakened the revenue argument for inheritance taxation. Income and consumption taxes had vastly superior revenue capacity because they drew on much broader tax bases (Genschel & Seelkopf, 2022; Keen & Lockwood 2010; Kenny & Winer 2006; Kiser & Karceski 2017; Besley & Persson 2009). They were also administratively convenient because they tapped directly into monetary flows (income and consumption). The inheritance tax, by contrast, fell on assets which had to be valued before taxation: straightforward for financial assets (e.g. savings, shares, and bonds) but difficult for real assets (e.g. family companies, real estate, or farm land) (Eisenstein, 1955; Gale & Slemrod 2000). Also, if the heirs could not pay the inheritance tax out of their own income or savings, they had to liquidate the inherited assets: again, easy with financial but difficult with real assets (Messere et al., 2003). Finally, given the salience of inheritance taxation incentives for avoidance are high as the tax is levied rarely but involves potentially very large sums. The typical form of avoidance are gifts inter vivos which are easier for financial than for real assets (Kopczuk, 2013). As a consequence, the administrative costs of the inheritance tax are relatively high (OECD, 2021). According to the United States’ Internal Revenue Service, public and private compliance costs combined amounted to seven percent of estate tax revenues – double the costs of sales tax collection (Huang & Cho 2017, p. 8). The German Council of Economic Experts claims that the inheritance tax has among the worst ratio of revenue to administrative cost of all German taxes (Sachverständigenrat, 2008, p. 223). The revenue efficiency of inheritance taxes is low compared to available alternatives.

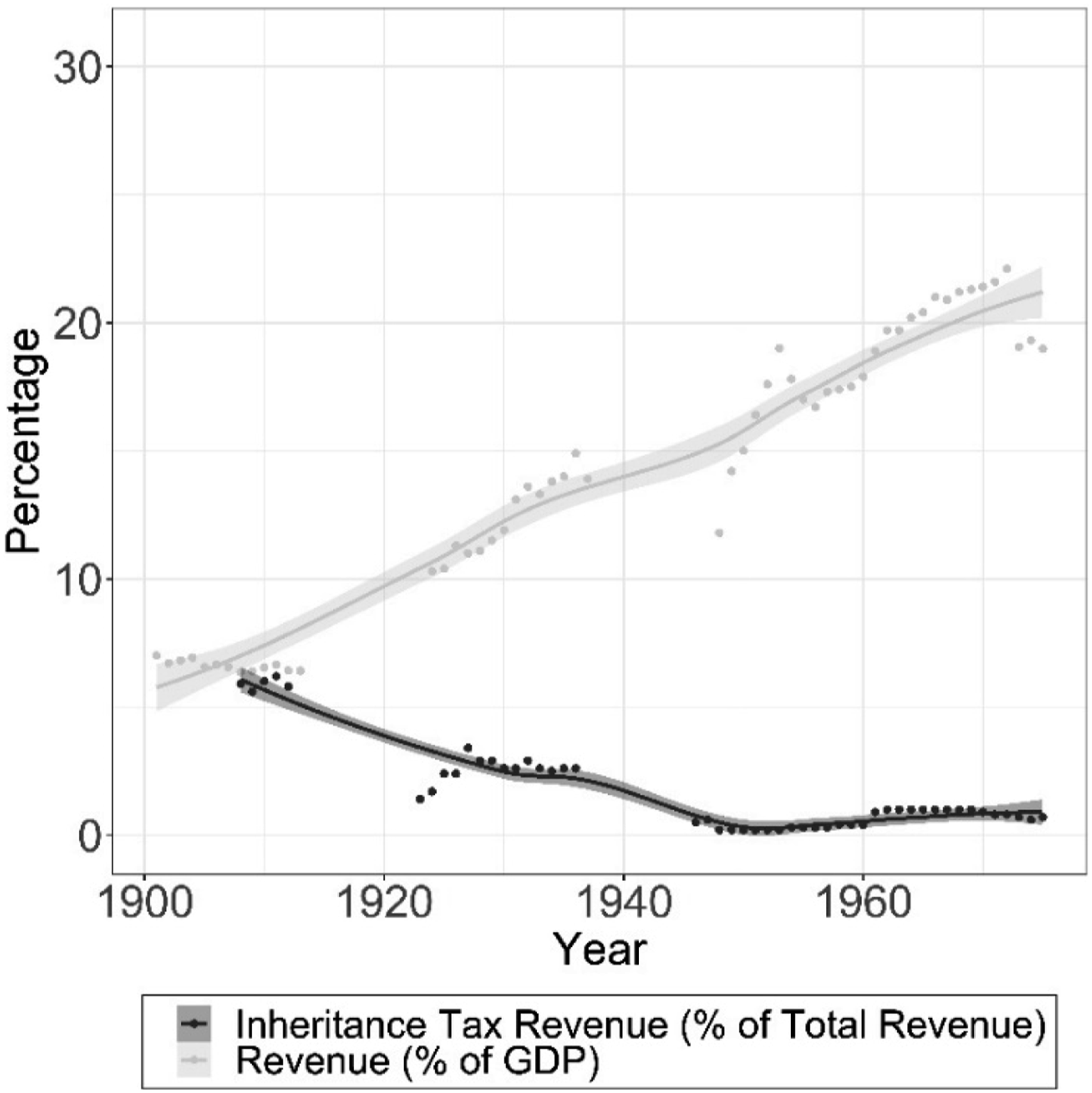

Against the backdrop of the inheritance tax’ relative revenue inefficiency vis-à-vis new tax policy tools, it is unsurprising that governments’ fiscal dependence on the inheritance tax has generally decreased. Austria, one of the very few countries for which historical data on inheritance tax revenue is available, illustrates the trend well (Figure 4). The share of inheritance taxation in total revenue declined roughly six-fold over the 20th century while the share of total taxation in GDP increased more than two-fold. In 2019, the inheritance tax accounted for only roughly 0.5% of total tax revenues, on average, in OECD countries (OECD, 2021). Revenue Development in Austria, 1900–1975. Sources. Flora (1983), Andersson and Brambor (2019).

Redistribution

While the normative critique of intergenerational wealth transfers is old and well-established (Beckert, 2008), its contribution to inheritance tax adoptions has been secondary. Some research suggests that democratic countries (in which the distributive interests of the masses should count) were not more likely to levy the tax than non-democratic ones (in which distributive fairness should count less) (Scheve & Stasavage 2012). Others claim that democracy did matter for inheritance tax introductions (Seelkopf et al., 2021; Seelkopf & Lierse, 2020). Yet, even democratic governments did not usually engage in inheritance taxation without a clear revenue requirement. 4

There are several examples of failed attempts to introduce inheritances taxes on purely redistributive grounds. For instance, US President Theodore Roosevelt proposed an inheritance tax in the 1900s to fight capital accumulation and wealth inequality. The proposal failed until the spending requirements of the first world war provided a clear revenue rationale for introduction in 1916: ‘[B]efore the 1930s, the [US] estate tax existed merely for revenue generation’ (Metrejean & Metrejean 2009, p. 37). Likewise, notionally Communist China has failed to (re-)introduce an inheritance tax on fairness grounds even though wealth inequality had grown massively since the 1980s (Piketty, 2020, p. 621): There simply was no revenue need. A Swiss popular initiative to introduce a federal inheritance tax on fairness grounds failed miserably in 2015 (Emmenegger & Marx, 2019).

While redistributive concerns failed to trigger inheritance tax introductions on their own, they facilitated the introduction of the tax on revenue grounds during fiscal crises. The ‘noisy’ (Culpepper, 2010) politics of crisis focus mass attention on issues of revenue need and taxation. This helps to clarify distributive interests and facilitates mass mobilization. It increases the likelihood that mass preferences factor into political decisions just as the median voter model suggests and decreases the likelihood that capital interests can use their structural and instrumental power to impose their preferences on the government: ‘[M]ass politics trumps interest group politics when both come into play’ (Hooghe & Marks 2009, p. 18). To the extent that a broad public consensus favours a redistributive tax for crisis fighting, it becomes difficult for a rich minority to oppose the tax on fairness grounds.

The justificatory role of redistributive arguments is illustrated prominently by non-democratic governments engaging in equity discourses to legitimate their choice of inheritance taxation for emergency finance. The Hapsburg monarchy, for example, used ability-to-pay arguments as early as 1759 to defend the adoption of the tax (Schanz, 1901, p. 62). Likewise, the imperial government in Germany used fairness arguments to justify its choice of the inheritance tax to meet military spending requirements in 1906. This pleased Social Democrats but antagonized conservative landowners (Schanz & Manicke, 1906). Equity arguments also played a major role in justifying massive wartime increases in inheritance taxation. The US and the UK, for instance, taxed bequests to direct descendants at close to 80% around the second world war (Scheve & Stasavage 2012, 2016).

Absent a revenue crisis, the political power of pro-redistribution arguments is much reduced. The ‘quiet’ politics of fiscal normalcy demobilize mass politics and enhance the structural and instrumental power of capital. Mass politicization is low because most people do not pay the tax and no vital spending programs depend on it. Rational ignorance is widespread, leaving ample scope for rich elites to lobby policy makers, threaten the government with capital flight, and manipulate public opinion against inheritance taxation (Emmenegger & Marx, 2019; Graetz & Shapiro 2005; Klitgaard & Paster 2021).

The main line of attack is usually the alleged inefficiencies of inheritance taxation (see already West, 1893; OECD, 2021; Sachverständigenrat, 2008): The disincentives it sets for savings and investment; the survival risks it poses to family farms and small businesses; the distortions it introduces through different valuation rules for different asset classes (financial assets at market price, real estate often at assessed, and highly deflated values); the cross-border evasion it triggers. With the globalization of markets, tax competition has become a prominent argument for inheritance tax repeal. Vladimir Putin claimed, for instance, that ‘billion-dollar fortunes are all hidden away in off-shore zones anyway and are not handed down here. Meanwhile, people have to pay sums they often cannot even afford just for some little garden shack’ (Putin [April 2005] 2013). The Russian inheritance tax was duly repealed in 2006.

In conclusion, the most favourable conditions for the introduction of the inheritance tax include a pressing revenue need of the government, the absence of more efficient revenue alternatives, and strong mass mobilization along class lines. The least favourable conditions obtain when more efficient revenue instruments are at hand, and an apathic mass public cedes tax policy making to elites and interest groups. Incidentally, this last set of conditions should also facilitate the repeal of the inheritance tax.

Repeal: Two Hypotheses

We summarize our historical findings about inheritance tax introduction in two hypotheses about inheritance tax repeal. As we have argued, the primary driver of introductions has been revenue. If the government depends on the inheritance tax revenue because few plausible tax alternatives exist, the risk of repeal is low. If, by contrast, the dependence is weak because more revenue-efficient taxes exist, the risk of repeal is high.

Revenue Hypothesis

The likelihood of inheritance tax repeal increases as governments adopt and expand more efficient revenue instruments including income taxes and general consumption taxes.

Whether the risk of repeal materializes depends crucially on distributive preferences. Even if redistribution was only a secondary factor in inheritance tax introduction, it may be the primary factor for inheritance tax retention. A tax instrument that was adopted for revenue reasons may be kept for equity reasons. We conjecture that this repurposing of the inheritance tax from revenue to redistribution is more likely in democratic countries than in non-democratic ones. Absent consistent mass attention and mobilization, the survival of the inheritance tax depends crucially on institutional protections of the distributive interests of lower income strata. Non-democratic systems often exclude lower income groups from political participation, de jure or de facto. Democratic systems, by contrast, operate under the normative expectation of inclusion. They have larger ‘selectorates’ and ‘winning coalitions’ that are more likely to include lower income groups (Mesquita et al., 2005). The parties representing these groups often take a long-term and comprehensive view on the distributive interests of their voters (Bardi et al., 2014; Mair, 2009). This may lead them to resist the abolition of the inheritance tax even if their voters do not really care.

Redistribution Hypothesis

At any level of revenue capacity, non-democratic governments are more likely to repeal the inheritance tax than democracies.

Explaining Inheritance Tax Repeals

To test our two hypotheses, we collect a novel dataset of inheritance taxes worldwide. We use the Tax Introduction Database (Seelkopf et al., 2021) to isolate the group of countries which have ever levied an inheritance tax on a permanent basis and to identify the precise historical date of first permanent introduction for each country. To code the effective year of inheritance tax repeal, we rely mainly on IMF country reports, Ernst & Young Worldwide Personal Tax and Immigration Guides, and Schoenblum (2008). On this basis, we first identify whether a respective country had repealed a tax by 2015. Then, we track the historical tax policy legislation in those countries that have repealed the tax to identify the timing of the first permanent repeal. We code repeals to be permanent if they are in place for at least 5 years. Next, we check whether those countries that still had an inheritance tax in 2015 had repealed it on a permanent basis before. We ignore short-term repeals. For instance, the US suspended the inheritance tax in 2010 but levied it again from 2011 onwards.

We have full information for a global sample of 87 countries which have introduced the tax at one point in their history. 42 countries then repealed the tax later (see Table A1 and Table A2 in the Appendix for an overview). In most cases, the repeal is decided by a formal act of the government. Chile, for instance, formally abolished the inheritance tax in 1890 after the end of the War of the Pacific and the onset of the nitrate boom had purportedly made the revenues of the tax redundant (Sater, 1976). India repealed the tax in 1985 purportedly because it yielded little revenue but lots of litigation (Amarendu & Abhisek, 2019). In Sweden, the Social Democratic government terminated the tax in 2004 ostensibly because of low revenues, high enforcement costs, and intense resistance of the business community (Klitgaard & Paster 2021, p. 100).

In one case, Austria, the constitutional court rather than the government repealed the inheritance tax by declaring it unconstitutional in 2007. The problem was that the Austrian (as almost any) inheritance tax applied different valuation rules to real and financial assets, thus creating inequitable tax burdens (Stefaner, 2007). Since the government could not agree on a reform to bring the tax in line with the jurisprudence, the application of the tax was discontinued in 2008 (Klitgaard & Paster 2021, p. 101). In Canada and El Salvador, the repeal of the inheritance tax remained partial. While both countries fully abolished the tax (in 1972 and 1992, respectively), they partly compensated this move by extending the scope of the capital gains tax (Canada) and the property transfer tax (El Salvador) to cover bequests (Corte Suprema De Justicia De El Salvador, 1992; Duff, 2005). While we coded both cases as full repeals, our results remain similar when running additional models excluding these two countries (Table A15 in the Online Appendix).

Based on these data, we create a binary time-series cross-section (BTSCS) dataset of countries at risk of repealing the inheritance tax. 5 Theoretically, the risk emerged immediately with the introduction of the first inheritance tax in Austria in 1759. Yet empirically nothing happened until the first inheritance tax repeal in Chile in 1890. We set the start date of our analysis to ten years prior of this first factual repeal, that is, to 1880. For countries which introduced the inheritance tax after 1880, the national introduction date marks the start date. For countries which gained independence after 1880 but kept the inheritance tax introduced by their former colonial master, the date of independence is the start date. Once a country has introduced the inheritance tax, it remains in the dataset until it repeals the tax. Then, it drops from the sample. Three countries have repealed the tax and reintroduced it later (Chile, Italy, and Thailand). These countries drop out of the sample after the first permanent repeal. The end year of our study is 2015. Countries that had not abolished the tax by 2015 are right censored.

We analyse our data by logit models with a maximum likelihood estimation technique. The observations in our BTSCS dataset are temporally dependent. The longer a country is at risk of repealing the inheritance tax, the higher the cumulative risk of repeal. Since ignoring this temporal dependence would bias our results (Beck et al., 1998), we follow Carter and Signorino (2010) and use a cubic polynomial approximation (t, t2, and t3) to model it.

Our revenue hypothesis suggests that countries become more likely to repeal the inheritance tax as they adopt other, more revenue-efficient tax instruments including most prominently taxes on income and general consumption. Based on the Tax Introduction Dataset we create a variable (major modern taxes) that measures whether and when a country has introduced taxes on income and consumption. The indicator is coded as ‘0’ if a country has neither introduced a tax on income (corporate or personal income tax) nor a tax on consumption (general sales tax or VAT); ‘1’ if a country has introduced either a tax on income or a tax on consumption; and ‘2’ if it has introduced both. We also apply alternative measures of revenue capacity to check the robustness of our results.

The redistribution hypothesis expects that democracies are less likely to repeal the inheritance tax than autocracies. To test this proposition, we include a dichotomous measurement for democracy in our models. We use the indicator developed by Boix et al. (2013) which takes the value ‘1’ if a country has a high level of participatory access (suffrage) as well as meaningful electoral contestation. We also use alternative measurements of democracy to check for the robustness of our results.

We control for other factors that potentially affect inheritance tax repeals. As argued in Section 2, the rise of the inheritance tax was associated with increasing spending requirements (war, recession, or social policy programs). By implication, the demise of the inheritance tax may simply reflect the absence of these drivers of expenditure. We control for warfare, recession, and welfare state expansion to control for this possibility. War is operationalized by a dummy variable taking the value ‘1’ when a country has experienced a major interstate war with more than 1000 battle deaths in the previous 5 years, and ‘0’ otherwise (Sarkees & Wayman 2010). Our variable for recession takes the value ‘1’ when a country’s GDP has contracted in at least one of the previous 5 years (Gapminder Foundation, 2020). Finally, we include a variable that turns ‘1’ when a country has introduced a major social policy program (pension, unemployment, sickness, family, work injury) in the previous 5 years. Data come from Schmitt et al. (2015).

Tax competition could be a major driver of inheritance tax repeals (Brülhart & Parchet 2014, p. 63). Arguably, the economic advantages associated with capital inflows incentivize governments to cut the tax burden on capital, including through the abolition of taxes on bequests. These cuts then trigger a race to the bottom in capital taxation. Small countries are more sensitive to competitive pressure because they have little domestic tax base to lose but a lot of international tax base to win. Hence, the incentive to cut or abolish taxes is particularly strong. Tax havens are typically very small jurisdictions (Bucovetsky, 1991; Kanbur & Keen 1993; Keen & Konrad 2013; Wilson, 1999). As is standard practise in the tax competition literature, we proxy competitive pressure by country size in terms of the natural logarithm of the national population (Dharmapala & Hines 2009). 6 We also control for life expectancy (Coppedge et al., 2019). Arguably, ageing societies accord a higher value to inheritance, which, in turn, may accelerate the repeal of the inheritance tax (Profeta et al., 2014). Historical path dependency is often considered an important stabilizer of policies in general (see Pierson, 1996, 2001) and of fiscal policy in particular (Peacock & Wiseman, 1961). This suggests that countries with a long tradition of inheritance taxation may be less likely to repeal the tax. We account for this effect by controlling for time since the first permanent introduction of the inheritance tax (logged values). 7 Finally, inheritance tax repeal could be a by-product of economic modernization. We include a country’s overall GDP per capita (logged values) into our models to control for this possibility.

To ensure that our results are not driven by our choice of covariates, we employ a stepwise approach. First, we just include our main independent variables that measure the adoption of major modern taxes and whether a country is a democracy or not. Afterwards, we add the variables that measure additional spending requirements and in the final model, we include the full battery of covariates.

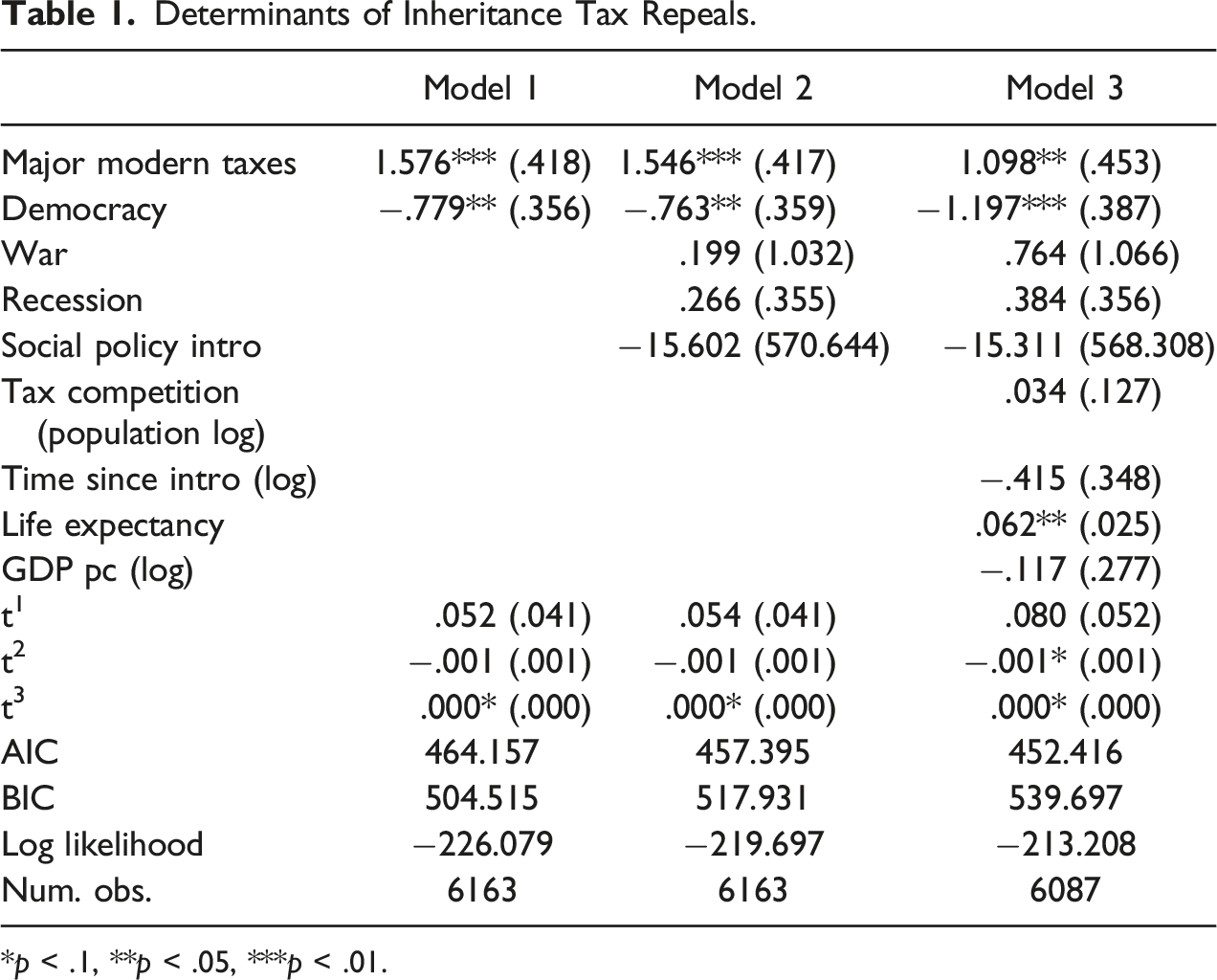

Determinants of Inheritance Tax Repeals.

*p < .1, **p < .05, ***p < .01.

The results of Model 1 hold in the expanded Models 2 and 3: Major modern taxes (i.e. income and consumption taxes) are positively and democracy is negatively related, while the spending requirements of war, recession and social policy are essentially unrelated to inheritance tax repeal. The coefficients for wars, recessions, and social policy introductions are statistically indistinguishable from zero. Also, tax competition, proxied by population size, has no significant effect on repeals. This is broadly in line with recent research on subnational tax competition in federal states which finds either no (Brülhart & Parchet 2014) or weak evidence (Bakija & Slemrod 2004) of a competitive race to the bottom in inheritance taxation. Path dependency in terms of time since introduction and economic modernization in terms of GDP per capita are not significantly related to inheritance tax repeals. Yet, life expectancy is significantly and positively associated with inheritance tax repeal as sometimes suggested in the literature (Profeta et al., 2014).

Robustness Checks

To check the robustness of our results, we test whether our revenue and redistribution hypotheses hold when using other operationalizations for the two main independent variables. Does it make a difference whether we use more continuous measures for either the availability of more efficient revenue tools or for democracy? Furthermore, we check whether our results hold for a range of alternative econometric specifications.

Revenue Hypothesis: Alternative Measures

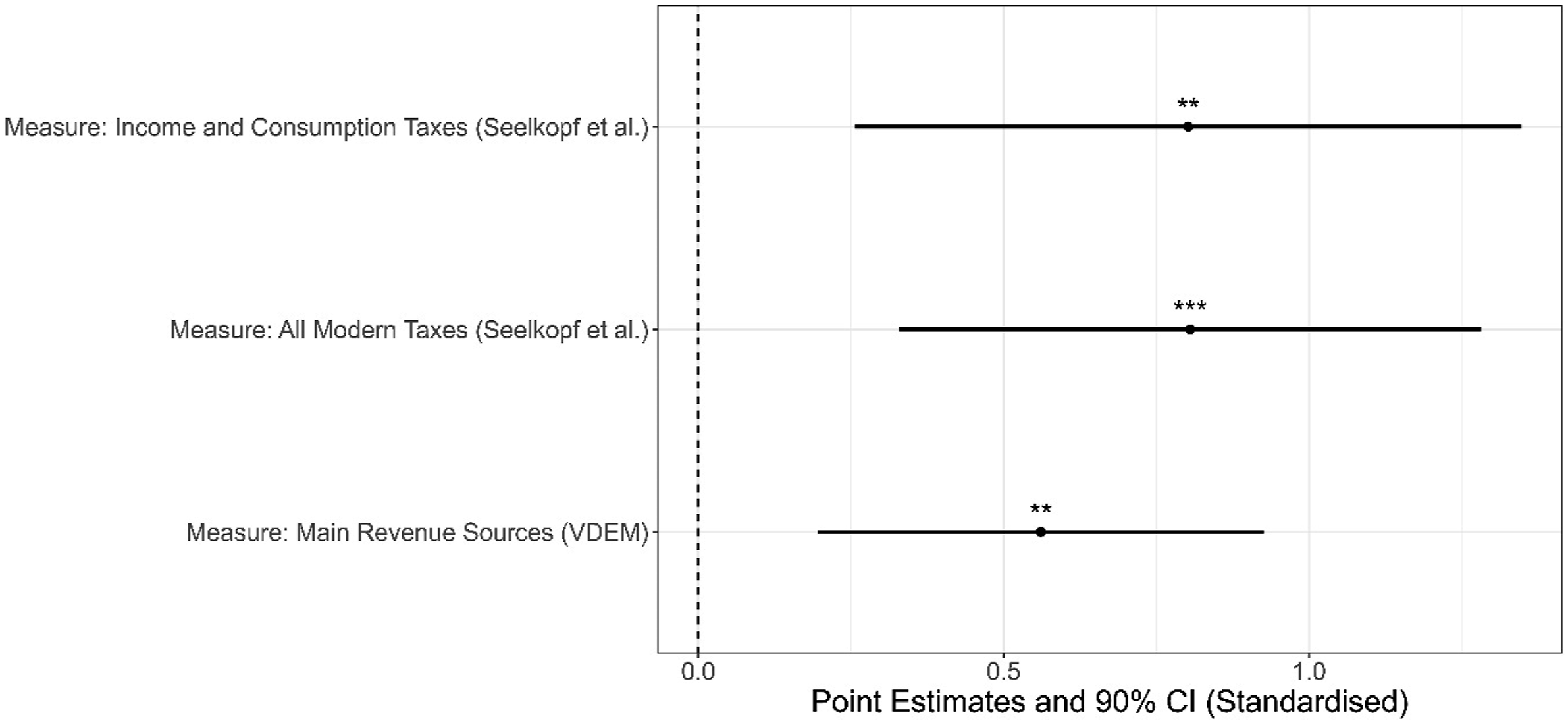

According to the revenue hypothesis, the emergence of new, efficient taxes on consumption and income has fuelled the decline of the inheritance tax. In the previous models (Table 1), we used an index of major modern taxes ranging from 0 (no tax on income or consumption) to 2 (taxes on both income and consumption) to check this conjecture. Here we use two alternative measures.

First, instead of accounting for revenue alternatives only in terms of whether a country has a tax on income and/or consumption, we create an indicator that accounts for revenue capacity in terms of different forms of income and consumption taxation. It ranges from ‘0’ for a country which has never adopted either a general sales tax, or a VAT, or a corporate or a personal income tax to ‘4’ for a country which has adopted all these taxes during its fiscal history. Second, we use a variable from VDEM which measures a country’s main source of revenue based on expert coding (Coppedge et al., 2019). Expert codes range from ‘0’ (‘the state is not capable of raising revenue to finance itself’) to ‘4’ (‘the state primarily relies on taxes on economic transactions (such as sales taxes) and/or taxes on income, corporate profits, and capital’). Responses were aggregated via item response theory models. Figure 5 plots point estimates and confidence intervals for the different measures of the availability of alternative revenue instruments. The findings stay robust when using the two alternative measures (All Modern Taxes and Main Revenue Source): Countries with efficient taxes on consumption and income taxes are more likely to repeal the inheritance tax. Other Measurements for Availability of Alternative Revenue Instruments. ***p < .01, **p < .05, *p < .10. All estimates are based on models with a full set of covariates and a cubic polynomial approximation. Point estimates and confidence intervals were standardized by multiplying them with the standard deviation of the independent variable. Full, unstandardized results are presented in Table A16.

In addition, we look at the effect of having adopted either an income tax or a consumption tax on inheritance tax repeal separately (Table A13 in the Appendix). Comparing the effect of consumption taxation (Models 1 and 3) and of income taxation (Models 2 and 4), we see that only the coefficient of the former is robustly statistically significant: The rise of modern consumption taxes seems to have fuelled inheritance tax repeals in particular. This finding is consistent with the revenue hypothesis because consumption taxes are often considered as the most powerful revenue tool currently available (Ganderson & Limberg 2022; Helgason, 2017; Shoup & Haimoff 1934). The revenue capacity of income taxes, by contrast, varies greatly across countries (Aidt & Jensen 2009; Liebermann 2001).

Redistribution Hypothesis: Alternative Measures

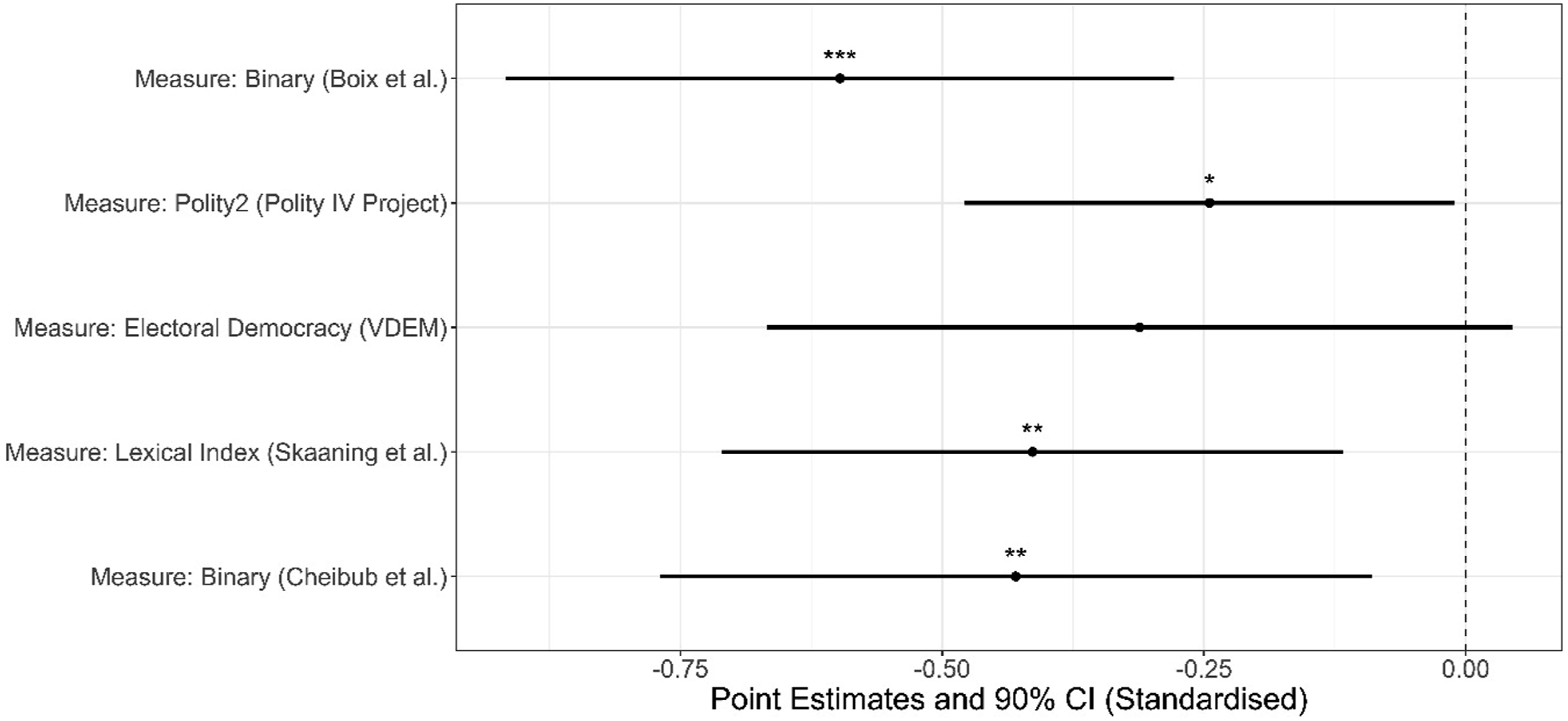

According to the redistribution hypothesis, democracies are less likely to repeal the inheritance tax. In the main models (Table 1), we used the dichotomous measure of democracy by Boix et al. (2013) to test this hypothesis. We rerun the analysis with four alternative measures. First, we use the Polity2 index (Marshall et al., 2011), ranging from -10 (total autocracy) to 10 (total democracy). Second, we use VDEM’s electoral democracy indicator which ranges from 0 to 1 and with higher values indicating higher levels of electoral democracy (Coppedge et al., 2019). Third, we use a lexical index of electoral democracy developed by Skaaning et al. (2015) which ranges from 0 (‘No elections’) to 6 (‘Universal Suffrage’). Finally, we include a different binary democracy measure which was developed by Cheibub et al. (2010). Note that this measurement is only available from 1945 onwards.

Figure 6 presents the results. Again, the plot shows standardized coefficients. In three out of the four alternative democracy measurements, the coefficient is negative and statistically significant at the 10% level. The only measure which does not have a statistically significant coefficient is the VDEM measure. Although the standardized point estimate is negative and similar to the other coefficient, the confidence interval is slightly larger than for the other measures. Crucially, the coefficients for the measure by Cheibub et al. (2010) are negative and statistically significant on the 5% level: Our results are robust even when excluding all observations prior to 1945. Other Measurements for Democracy. ***p < .01, **p < .05, *p < .10. All estimates are based on models with a full set of covariates and a cubic polynomial approximation. Point estimates and confidence intervals were standardized by multiplying them with the standard deviation of the independent variable. Full, unstandardized results are presented in Table A17.

Alternative Econometric Specifications

To check whether our main results are robust to econometric choices, we run several alternative models. First, we include a range of additional covariates (Table A3): a state’s independence from other states, the existence of regional governments, the political power of rural regions, and the inflation rate. Data come from Coppedge et al. (2019). Our main findings hold throughout all models. In addition, we run models that account for tax competition by a temporally lagged spatial lag of regional repeals rather than by country size. The spatial lag measures the number of inheritance tax repeals in the same world region while a country is at risk of repealing its inheritance tax. If tax competition is driving the demise of inheritance taxation, we would expect countries to repeal their inheritance tax as a reaction to other countries’ repeal. The coefficients for the temporally lagged spatial lag are insignificant (Table A4). Hence, we find no support for tax competition driving inheritance tax repeals. Importantly, the coefficients for the existence of more efficient alternative tax tools (major modern taxes) as well as democratic structures (democracy) remain statistically significant.

Second, we use different models to account for the time dependency of our data. We calculate Cox Proportional Hazard models instead of logit regressions with a cubic time approximation (Table A5). We also run models that include year fixed effects instead of a cubic approximation. This approach is less efficient but serves as a conservative test that our results are not driven by time dynamics. Our findings remain robust (Table A6).

Third, despite the different modelling approaches to deal with the time dependency of our data, one might still worry that the long period of observation is driving our results. After all, most repeals have happened since the 1970s when many countries had already introduced income and consumption taxes. To ensure that our findings are not driven by a spurious correlation due to the time dimension of our data, we run two additional tests. In the first test, we choose 1970 instead of 1880 as our start period: countries only enter the risk set from 1970 onwards. 8 Our main results hold (Table A7). In the second test, we use a dummy variable which turns ‘1’ if a country has introduced a modern tax in the preceding years. Thus, instead of looking at the impact of a state’s overall repertoire of modern taxes, this specification looks at the specific impact of recent tax introductions. This accounts for the possibility that the inheritance tax repeal was part of a single unobserved fiscal bargain containing such as, for instance, the promise of higher social spending from new income and consumption taxes in return for a lower tax burden on the rich. If there was such a bargain, we should observe an immediate effect of the introduction of new modern taxes on inheritance tax repeals. If, by contrast, it is the revenue efficiency of the state’s tax repertoire that puts inheritance taxes at risk, as our revenue hypothesis suggests, we should expect a time lag. New taxes typically need time to become efficient revenue raising tools: Administrative capacities need to be built, staff need to be (re-)trained, implementation processes streamlined, and accounting routines established (Aidt & Jensen 2009). For instance, the UK introduced the income tax in 1843 but took until 1857 to generate more than 2% of GDP from it (Andersson & Brambor 2019). In Mexico, the income tax was introduced in 1924, but generated revenue of more than 2% of GDP only from 1943 (for other historical examples see Appel, 2011; Einhorn, 2009). To gauge the temporal association between the introduction of new taxes and inheritance tax repeals, we use different time frames for our dummies ranging from 5 to 15 years. We expect that our dummy for new tax introductions becomes a stronger predictor for inheritance tax repeals when the time frame for previous introductions is longer, that is, when new taxes had more time to turn into efficient revenue alternatives. Figure A1 shows the findings. The empirical pattern is in line with our theoretical expectations: While the coefficient is close to zero for the relatively short time frame of 5 years, it turns consistently positive for a frame of 10 years and is statistically significant at the 5% level for a time frame of 15 years.

Fourth, unobserved country heterogeneity might bias our results. Checking for this is important since we are looking at a global and historical country sample. In time-series cross-sectional analysis with a continuous dependent variable or with repeated events, country fixed effects can control for unobserved heterogeneity. However, we look at a non-repeated event, namely, the first permanent repeal of the inheritance tax. This makes the inclusion of fixed effects problematic (Allison, 2009; Allison & Christakis 2006; Beck & Katz 2001; Beck et al., 1998). For instance, including fixed effects means that the estimation only looks at variation within countries that have repealed the inheritance tax (Beck & Katz 2001). Therefore, it is not surprising that running models with fixed effects yield results that are sensitive to modelling choices and where all coefficients are statistically insignificant (Table A8). We run two alternative models to address the issue of heterogeneity. We control for regional heterogeneity by including region fixed effects (Table A9). Although this approach does not account for different country level variation, it should capture broader differences between different world regions such as North America or Latin America and the Caribbean. Our main results hold. Furthermore, we use a random effects model as an alternative to fixed effects (Bell & Jones 2015). Again, findings are robust to this alternative specification (Table A10).

Finally, we check whether our results are robust to running additional econometric specifications. We calculate linear probability models (LPMs) instead of logit regressions. LPMs have the advantage of being easier to interpret. Hence, we can gauge the substantive significance of our results. Table A11 shows the results. On average, each year a country has an additional modern tax on income or consumption increases the chance of inheritance tax repeal by around .4 percentage points. In contrast, each year a country is a democracy reduces the probability of repeal to roughly .9 percentage points. We conclude that our results are also substantially significant. The findings also hold when using rare event logit regressions (Table A12).

The strength of our analysis is to look at the fall of the inheritance tax for a large global sample over a very long period of observation. Yet, this strength comes at a price: The analysis must rely on simple and easily accessible measures of its main variables. Obviously, tax repeal is a crude indicator of the general fall of the inheritance tax because it ignores subtler forms of cutback that could have equivalent effects such as rate reductions, or base narrowing. In the United States, for instance, the share of taxable estates in all estates was as low as .2% in 2019. In other OECD countries, however, it was substantially higher, in Belgium close to 50% (OECD, 2021, Figure 3.2). Also, those heirs who pay the tax often face high statutory tax rates: 40% in the US and the UK, 50% or more in France, Germany, Japan, and South Korea, and 80% in Belgium (OECD, 2021). The revenue contribution of the inheritance tax is often low. But it is greater than zero and highly redistributive. 9 Despite its crudeness inheritance tax repeal is a meaningful measure of the demise of the inheritance tax. Likewise, the availability of income and consumption taxes is a crude measure of revenue capacity. Even if we accept that these taxes are generally more revenue-efficient than taxes on bequests, they are clearly more efficient in some specific countries during some periods than in other countries at other times. Democracy, finally, is a crude indicator of redistributive preferences because the ability of lower and middle classes to prod the government into redistribution varies not only between democracies and non-democracies but also within these groups. Yet precisely because the measures are simple and crude, it is remarkable that they yield significant and robust results.

Revenue, Redistribution, and Democracy

The rise and fall of the inheritance tax reflects the rise and fall of its revenue function. In most countries, the tax was introduced to enhance revenue. It remained stable as long as it generated revenue. It became vulnerable to political challenge once more efficient revenue instruments including, most prominently, the income tax and the VAT made its revenue contribution all but redundant. As the fiscal purpose of the inheritance tax weakened, its retention became more dependent on the redistributive preferences of voters and governments. These preferences are fickle, subject to the vicissitudes of information problems, fairness considerations, and representational biases that various critics have blamed for the empirical failures of the median voter model (see Limberg, 2021 for a review). Yet, as our findings also show, democratic governments are less likely to repeal the inheritance tax than non-democratic ones. Democracy may provide less protection for the distributive interests of low- and medium-income groups than the median voter model suggests. But it offers more protection than any of its alternatives. Our findings have important implications for theories of public policy and political economy as well as for the politics of taxation.

From a public policy perspective, our findings are interesting because they show that policy terminations do in fact happen and can be quite frequent. A tax that loses its original revenue purpose is at risk of repeal. Since no vital spending programs depend on it, few vested interests will come to its defence leaving the tax vulnerable to attack. Vested interests tend to attach to spending programs which create beneficiaries but not to tax or other cost-imposing policies, which create payers. Vested interests defend spending programs even if these no longer serve a useful policy purpose (Moe, 2015). Payers, by contrast, tend to mobilize against taxes unless an overriding need for revenue keeps them at bay. The strong focus of the public policy literature on spending programs with concentrated benefits and diffuse costs may lead it to overrate the probability of policy survival (Pierson, 1994). Taxes, by contrast, impose concentrated costs and generate diffuse benefits. As a consequence, tax systems do not tend towards policy accumulation (Adam et al., 2019). To the contrary, national tax systems have recently tended towards simplicity, relying on fewer taxes today than one hundred years ago (Peters, 1991; Steinmo, 1993).

From a political economy perspective, the findings are interesting because they show that the redistributive politics of taxation are contingent on revenue capacity. If revenue needs are imperative and extant revenue capacity is insufficient, the redistributive effect of a new tax is incidental to its revenue function. Any tax that can plausibly claim to fill the revenue gap will do. The distributive conflict remains mute, and neither the median voter model nor its elite-capture critics contribute much to understanding tax policy choices. The distributive conflict only comes centre stage once alternative revenue instruments become available. All else equal, governments prefer revenue efficiency. They opt for taxes that satisfy revenue requirements with low deadweight loss and administrative burden. If they keep relatively inefficient tax instruments, it is for reasons of redistribution, not for revenue reasons. Whether they do depend on the regime type. Democracies are more likely to retain the inheritance tax for redistributive purposes than autocracies because they accord relatively more protections for the distributive interests of the less well-to-do. Yet, even in a democracy the survival of the inheritance tax is not guaranteed but depends on the contingencies of the political situation, including the information problems, fairness concerns and representational biases highlighted in the literature on elite capture. We do not question the insights of this literature but narrow down the scope conditions – revenue capacity and political regime type – under which they are more or less likely to hold.

From a political perspective, our findings have implications beyond the redistributive taxation of wealth and income to redistribution more generally. Take recent proposals to introduce or raise carbon taxes. The primary purpose of these taxes is to redistribute costs from harmful, high-emission to less harmful, low-emission activities and sources of energy supply. It is not to generate revenue for public spending needs. Our findings suggest that this makes carbon taxes vulnerable to political attack. The power of the gilets jaunes movement in France derived precisely from the fact that the French government did not vitally depend on the revenues from the fuel tax increase that had given rise to the protest. The increase was purely redistributive. As the example the inheritance tax shows, the best way to make a redistributive tax increase politically viable is to make it fiscally indispensable.

Supplemental Material

Supplemental Material - Revenue, Redistribution, and the Rise and Fall of Inheritance Taxation

Supplemental Material for Revenue, Redistribution, and the Rise and Fall of Inheritance Taxation by Philipp Genschel, Julian Limberg, and Laura Seelkopf in Comparative Political Studies.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

The data given this article are available at ![]()

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.