Abstract

Constituting a central historical link between war and long-term fiscal capacity, war taxes are generally perceived to be a thing of the past. This article corrects the picture by presenting new, global data on war taxes, 68 in total, introduced between 1960 and 2020. Far from having been abandoned, war taxes have remained a crucial war-time fiscal instrument, leaving long-term imprints on tax systems across the contemporary world. Serving the twin imperatives of revenue maximisation and generation of taxpayer consent, I argue that the use of war taxes is conditioned by the relative intensity and the perceived legitimacy of a war, be it civil or inter-state. The proposed logic aligns with case evidence, further supported by macro-quantitative analysis. The results speak to the large literature on war and state-building, challenge the standard disintegrative view of civil wars, and provide new empirical insights into the political economy of conflict-affected countries.

Exceptional taxes to pay for war were the seeds from which modern fiscal states emerged. In the immediate, the choice to finance wars and their associated costs with taxes has been lauded for placing popular checks on belligerent governments (Smith, 1976 [1776], p. 926) and providing for a fair sharing of war-time burdens (Keynes, 1940; Piketty, 2019, p. 518). Its disappearance in the West is therefore deplored (Kreps, 2018); its apparent absence in the rest of the world, merely aligning with the disintegrative nature of contemporary conflicts (Herbst, 1990). Yet, as shown in this paper, war taxes have in no way disappeared.

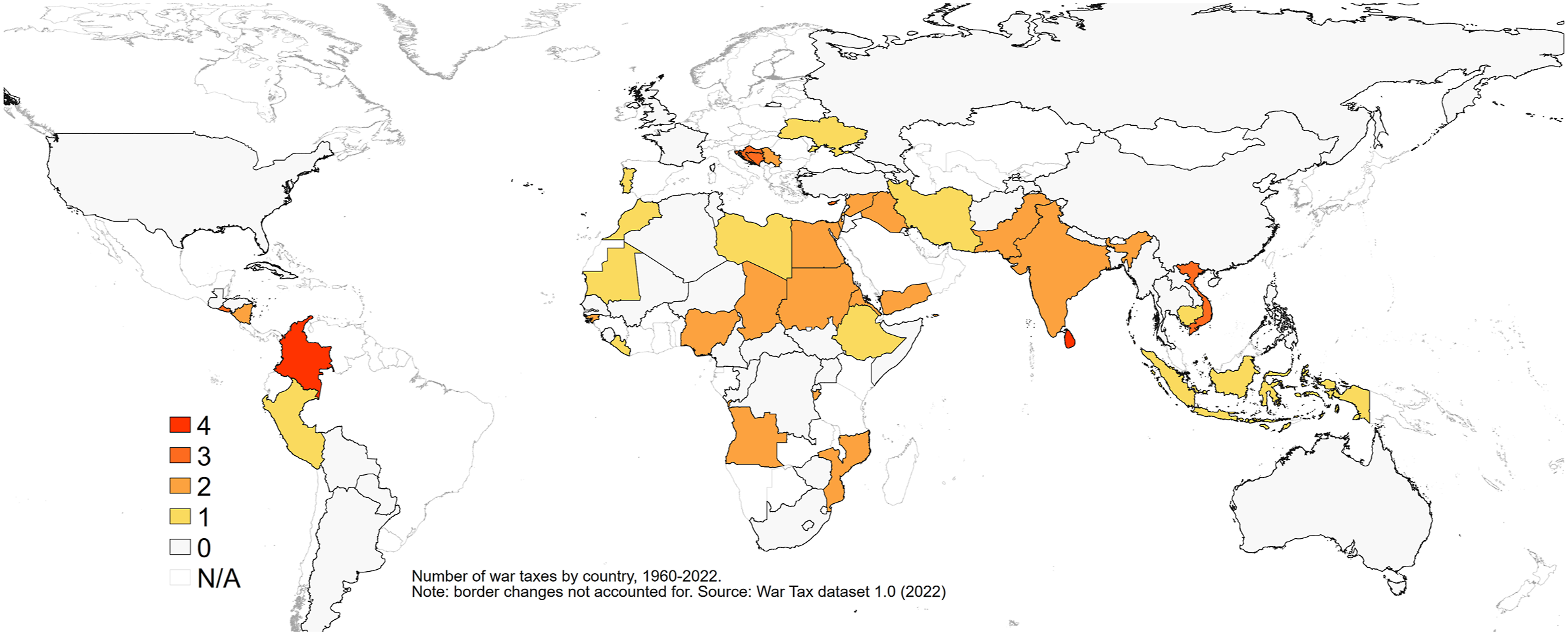

Indeed, newly collected data covering the totality of war-affected countries between 1960 and 2020 indicate that war taxes – understood as distinct tax instruments explicitly motivated by the cost of war or its direct consequences – have continued to be a central mechanism for war-time revenue mobilisation (Figure 1). But why and under what conditions do governments impose war taxes? War taxes across the contemporary world.

Drawing on studies of Western war finances and the political economy of taxation, I will argue that war taxes have continued to answer to the twin war-time imperatives of revenue generation and taxpayer consent. Accordingly, they are introduced when (1) the stakes are so serious, and the resulting war costs so high, that it necessitates a substantial increase in government resources, and (2) when the war is deemed both necessary and legitimate by the taxpayers. These basic conditions go a long way in explaining the prevalence of war taxes in the contemporary world as a whole – as well as their relative absence in the West.

Their pervasiveness, substantive revenue generation, and their often long-term imprint on national tax systems – elaborated below – make war taxes important to study in their own right. By adopting a comprehensive geographical perspective, the paper will further provide insights into the processes that shape their emergence, and inversely the conditions that may hinder it. Finally, by studying tax reforms under the compelling circumstances of war, we may gain wider insights into processes of tax bargaining in the contemporary world in general and the Global South in particular.

The paper proceeds as follows. First, the function of war taxes corresponding to a basic logic of war-time revenue mobilisation is elaborated. Second, a time-series cross-section analysis covering all conflict-affected countries (79 in total, 1960–2020) provides for identification of conditional factors and to test the observable implications of the proposed logic. Third, the population of 68 war taxes is reviewed along key dimensions – timing, linking, revenue generation, termination, and policy legacies – which, together with brief investigations of a handful of diverse cases, allows to further probe the validity of the proposed mechanisms and, importantly, assess the substantive significance of war taxes in the contemporary world.

Wars, Taxes, and Contemporary States

War has been a fundamental driver for the long-term expansion of fiscal capacity. The positive association, albeit not unconditional, holds in regions beyond the West (Thies, 2007; Queralt, 2019), and for various types of armed conflicts, including civil wars (Frizell, 2022; Han & Thies, 2019; Kisangani & Pickering, 2014). Beyond the macro-correlational perspective, a rich and varied literature has moreover uncovered insights into the more immediate war-time processes linking cause to potential long-term outcomes.

First, seeking to explain the long-term developments of fiscal institutions and state capacity, historically oriented research has precisely highlighted the key role of war-time tax reforms, including extraordinary war taxes. It includes studies on fiscal administration (Ardant, 1971), fiscal-military history (Brewer, 1989), and sociological/political science studies on state-building and taxation (Dincecco, 2011; Levi, 1988; Mann, 1986; Scheve & Stasavage, 2016; Tilly, 1992). So far, however, only limited attention has been given to non-Western regions, the contemporary era, or civil wars.

Second is a literature which addresses war taxes in its own right, albeit with a heavy focus on the United States. Whether approached through historical comparison (Bank et al., 2008; Cappella Zielinski, 2016; Flores-Macías & Kreps, 2013; Kreps, 2018) or through investigations of contemporary public attitudes (Flores-Macías & Kreps, 2017; Kriner et al., 2018), they all grapple with the recent disappearance of this otherwise so typical – indeed, American – form of war finance. While providing new insights into the logic of war-time tax bargaining, the geographic generalisability of its conclusions remains unknown.

Finally, a nascent research strand has turned the focus to the Global South and the contemporary era, while shifting the perspective to non-state armed groups. By investigating ‘rebel taxation’ in contemporary civil wars, these studies aim to understand variance in ‘rebel governance’ and their finance strategies (Breslawski & Tucker, 2021; Revkin, 2020; van Baalen, 2021) or uncover the mechanisms of embryonic state-building (de la Sierra, 2020). If the parallels between ‘state-making’ early-modern monarchs and contemporary rebel groupings remain contentious, the literature has nonetheless highlighted the continued centrality of war-time revenue mobilisation, and the necessity of consent, in addition to coercion, to this end.

But what about the state? In the move from historical European state-builders to increasingly stationary ‘bandits’ (Olson, 1993) in the border zones of contemporary Africa and Latin America, the war-time fiscal conundrum of actually existing, contemporary states have generally been overlooked (cf. Rodríguez-Franco, 2016). To the extent that it has been studied, the focus has been on external rents, informal levies, or outright plunder (de Waal, 2015; Heydemann, 2000; Reno, 1998). In contrast, I argue that formal taxation has continued to form an important part of the fiscal toolbox during armed conflicts, including civil wars, and that beyond coercion, consent remains crucial for its success.

Revenue Mobilisation and Tax Compliance in Times of War

The relationship between wars and the expansion of taxation plays out, and can thus be analysed, over different time-scales. But the seeds of long-term developments lie in the immediate. Increased spending requirements (Peacock & Wiseman, 1961) and investment in administrative capacity (Besley & Persson, 2008) will lead to little if the initial, political hurdle of effectively introducing and consolidating new taxes cannot be overcome (Ardant, 1971, p. 538). The immediate, war-time dynamic is neatly summarised by Herbst (1990, p. 120): ‘War affects state finances for two reasons. First, it puts tremendous strains on leaders to find new and more regular sources of income. […] Second, citizens are much more likely to acquiesce to increased taxation when the nation is at war, because a threat to their survival will overwhelm other concerns they might have about increased taxation’. In contrast to Herbst, however, I argue that this applies as much to contemporary wars as to those of early-modern Europe – and that war taxes constitute primary manifestations of this logic. To get there, we start by elucidating the fiscal considerations of a war-time government, before turning to the effect of war on taxpayer consent.

The history of taxation is one where rulers, seeking enrichment or survival, have tried to extract increasing resources from their subjects while not provoking them to give up their economic activity, hide their wealth, or start a rebellion (Ardant, 1971). Emphasising different aspects of this account, scholars have come to different theoretical conclusions about what factors shape governments’ tax decisions and what options they have at hand. Three of these, equally influential, are worth highlighting.

Olson (1993) formulated the problem in its most skeletal form, where the time-horizon of the ruler determines its actions. The potential for coercion is unlimited, but subjects can always give up production – and will do so once extraction becomes too onerous. A ruler with a short time-horizon (a ‘roving bandit’, or one faced with war) will prioritise immediate gains by maximising extraction. One with a longer time-horizon (a ‘stationary bandit’, or one in peace) will instead preserve a sufficient margin to incentivise continued production.

The story of Tilly (1992) is similar but less abstract; the ruler may choose to extract as much as possible from a small pie (coercion intensive), or tread lightly, calculating that something can be skimmed off from a growing pie (capital-intensive). Time-horizons matter, but are partly endogenous to revenue extraction, as rulers can choose to invest in defence to ensure their survival. Moreover, coercion itself – not only its indirect consequences – is costly, many times insufficient, and its success crucially depends on the existing economic structure. To avoid wealth-holder resistance or mass rebellion, rulers can engage in bargaining, trading rights and privileges for more taxes.

Levi (1988), finally, while denying neither the importance of time-horizons, coercive capacity, nor material bargaining, puts consent centre-stage. For when populations resist or rebel against taxes, they do so not simply based on material cost–benefit calculations but importantly based on notions of fairness. On the part of the ruler, the means for mitigating resistance is not simply those of (costly) coercion or (equally costly) material bargaining but also one of increasing the quasi-voluntary compliance by convincing taxpayers that their financial contribution is necessary and fair.

In essence, governments must maximise revenue while minimising political costs (Rose, 1985). In times of war, the premium of extraction increases as a function of the seriousness of the threat posed against the government and the material needs necessary for averting it. Notably, as long as the government seeks its own survival, and for any given level of threat, the source of that threat, be it a rebel group or another state, ought to have little import (Goenaga et al., 2023; Kisangani & Pickering, 2014). 1 Accordingly, war pushes governments to seek an increase in revenue to meet its fiscal needs – but it does not absolve them from the necessity of popular consent (Feinstein & Wimmer, 2023).

Fortunately for them, the threat posed by war can also drastically affect the conditional compliance of its taxpayers, driven by two complementary mechanisms. First, from the point of view of a rational and self-regarding individual, the premium for certain public goods (defence, but also reconstruction) rises drastically in relation to the cost of a tax-payment (Levi, 1988, p. 66). In other words, war can increase the taxpayers’ sense of getting something valuable in return for their contribution. Second, the threat of war increases national identification (Gibler et al., 2012) and in-group cohesion (Stein, 1976), and thus the willingness, beyond individual cost–benefit calculations, to make individual sacrifices for the benefit of the collective (Gangl et al., 2016; Konrad & Qari, 2012). The patriotic solidarity induced by war accordingly leads to increased taxpayer consent (Feldman & Slemrod, 2009). Complementary and largely observationally equivalent, we can subsume these two mechanisms under the wider process of war-induced fiscal patriotism.

The effect, however, is not unconditional. As pointed out by Mann (2013, p. 175) ‘Rallies round the flag come after the war has started – and they don’t last long’. That is, surges in patriotism result from the materialisation of a threat, not the anticipated risk thereof, and is likely to wane as the war turns into precarious normality. Moreover, any war will not do. If taxpayers perceive their stakes to be low (Centeno, 2002, p. 159), or that the cost of continued fighting outweighs its benefits (Feldman & Slemrod, 2009), taxpayer consent will decrease. Hence, wars that are understood as aggressive, unnecessary, or simply have yet to materialise do little to increase taxpayer consent (Levi, 1988, p. 105), and designated war levies may further accentuate opposition to the war itself (Flores-Macías & Kreps, 2017). In this way, war taxes also pose political risks. However, as long as the war-effort is perceived as a legitimate and necessary response to a real, immanent threat, it is likely to shift individual cost–benefit calculations and induce a sense of solidarity among the relevant taxpayer constituencies (Rodríguez-Franco, 2016).

Importantly, but contrary to common assertions (Besley & Persson, 2008; Herbst, 1990), this should hold true whether the threat arises from another sovereign state or from an ‘internal’ non-state actor. Civil wars certainly reinforce social divisions, negating polity-wide solidarity. But as long as a sense of (parochial) patriotism emerges among the government constituents (Wimmer, 2017), constituting one side of the conflict, it will lead to increased willingness to contribute for the benefit of their own group, in the struggle against an often perceptively external enemy (see Liebermann, 2001). While empirical research on civil war finance is still sparse, the example of the American civil war (Bank et al., 2008), and more recently, the Colombian civil war (Rodríguez-Franco, 2016), makes clear that while the dynamics may not be identical to inter-state wars, given an equivalent level of threat, they too are likely to give rise to both the requisite demand (fiscal pressure) and supply (fiscal patriotism) for the introduction of war taxes. 2

Yet, however strong a wave of fiscal patriotism, its translation into taxpayer consent rests on a final condition: the credibility of the government to deliver the promised goods. Whether motivated by perceived individual gains or the benefit of the collective, taxpayers need to be convinced that their contribution is employed for the purpose rendered imperative by the war. To do so, rulers can employ strategies of pre-commitment (Levi, 1988, p. 61). By explicitly linking the tax to a designated purpose – whether through legal provisions or public statements – governments signal their commitment to use the money according to taxpayers’ priorities (Fairfield, 2013; Flores-Macías, 2022). Accordingly, the act of linking a new, distinct tax to the cost of war – the central feature of a war tax – is an effective expedient for harnessing citizens’ fiscal patriotism in times of war. Doing so, governments can decrease resistance to new taxes when most needed.

In sum, the postulated logic implies that war-time governments are revenue-maximisers heavily constrained by the quasi-voluntary consent of its constituent taxpayers. More precisely, at any given time, the chosen level and form of revenue mobilisation will be a function of (1) current fiscal needs and (2) the political and economic costs of a given revenue mobilisation strategy. In contrast to Olson’s (1993) idealised ‘bandit ruler’, seeking only self-enrichment, the government’s principal aim is to survive (maintain power), 3 and does so, first, by defeating military challengers and, second, by fulfilling minimal obligations vis-à-vis citizens (basic goods and services) and allies (e.g. debt repayment). Thus, irrespective of underlying motives, the government will seek to introduce new revenue measures corresponding to the additional requirements imposed by the war. Likewise, and again in contrast to the unrestrained ‘bandit’, the government will seek the consent of its taxpayers to minimise its cost.

The logic constitutes a simple, and here preferred, explanation to the ubiquitous nature of war taxes throughout the contemporary era, and for civil as well as inter-state wars. Whereas neither the calculus of a war-time government nor the conditional consent of taxpayers can be directly observed, the validity of the logic can be assessed though a series of observable implications, which will guide the empirical analysis.

The postulated logic implies, first, that the probability of introducing and maintaining a war tax (I) varies with the seriousness and urgency of the threat. A larger military threat (1) directly implies a risk towards the ruler’s survival (shorter time-horizon) and an increase in the objective material requirements to avert it (2) and, given that the threat is evident also for the population, increases the conditional solidarity of constituent taxpayers. Empirically, therefore, war taxes should be more prevalent whenever I. (a) conflict intensity is high. I. (b) extant military capacity is low. I. (c) allied support is low, or inversely, enemy support is high. I. (d) the government is a primary, rather than supporting party.

While these correlational expectations must necessarily hold for the logic to be valid, they are not sufficient. Most pressingly, they do not allow us to differentiate between the proposed logic of restrained revenue-maximisers and an Olsonian logic. Indeed, each of the above implications can likewise be derived from the reduced time-horizon of an unrestrained and profit-seeking bandit ruler.

Looking closer at the structural conditions of the economy, and the administrative capacity of the state does, however, allows for a first differentiation. On the one hand, given a strong bureaucracy and a buoyant economy, modern fiscal instruments like the progressive income tax have allowed many governments to overcome the fundamental challenge of combining revenue efficiency with distributional precision. On the other hand, in contexts of low economic surplus and restricted capacity to supervise economic activity, revenue efficiency, always restrained, will typically come at the expense of a fair and tolerable distribution of the fiscal burden (Ardant, 1971).

4

Quick tax increases will thus generate meagre revenue, considerable economic cost, and significant taxpayer opposition – not least since the inequities of war tend to accentuate popular demand for distributive fairness (Scheve & Stasavage, 2016). Whereas increased disregard for such (deadweight) costs is precisely what pushes an unrestrained bandit ruler to accelerate extraction as time-horizons shrink, the restrained revenue-maximiser is characterised instead by his continued consideration of political and economic costs, seeking additional revenue to fund the war, but not at the expense of fuelling a tax rebellion. Thus in line with, for example, Centeno (2002) and Kiser and Linton (2001), we should expect war taxes to be less prevalent when II. (a) economic development is considerably low. II. (b) state capacity is considerably low.

An abundance of external rents or credit is moreover likely to mitigate the need for potentially costly taxes. For whereas a self-enriching bandit whose rapaciousness is only determined by his time-horizon, and being inconsiderate of political costs, would maximise all available revenue sources at his disposal, a politically restrained revenue-maximiser is expected to (III) prefer alternative revenue sources, such as resource rents and credit, over taxes, when available (Centeno, 2002; Queralt, 2019). Accordingly, war taxes should be less prevalent when III. (a) natural resources rents are abundant. III. (b) sovereign credit is available.

Finally, in contrast to an idealised Olsonian bandit, the inclination of a restrained revenue-maximiser to introduce war taxes will vary according to the perceived legitimacy of the cause and its ability to credibly commit the solicited resources to the said cause (IV). As argued above, a war perceived to be illegitimate, unnecessary, or simply too burdensome will generate little patriotism from which to rally consent. War-time governments wary of the political costs of additional taxes will therefore pay attention to public expressions of discontent. However, even with a surge of war-time patriotism, its translation into taxpayer consent depends on the credibility of the government to deliver on its promises. With limited taxpayer oversight, this credibility largely depends on the government’s apparent commitment to the cause (Flores-Macías, 2022). In the context of war, then, nationalist governments should have higher a priori credibility among taxpayers.

5

Hence, the probability of introducing and maintaining war taxes should IV. (a) decrease with manifestation of public discontent. IV. (b) increase with the presence of a nationalist government.

Empirical Analysis: War Taxes in the Contemporary World

Delimitations and Empirical Strategy

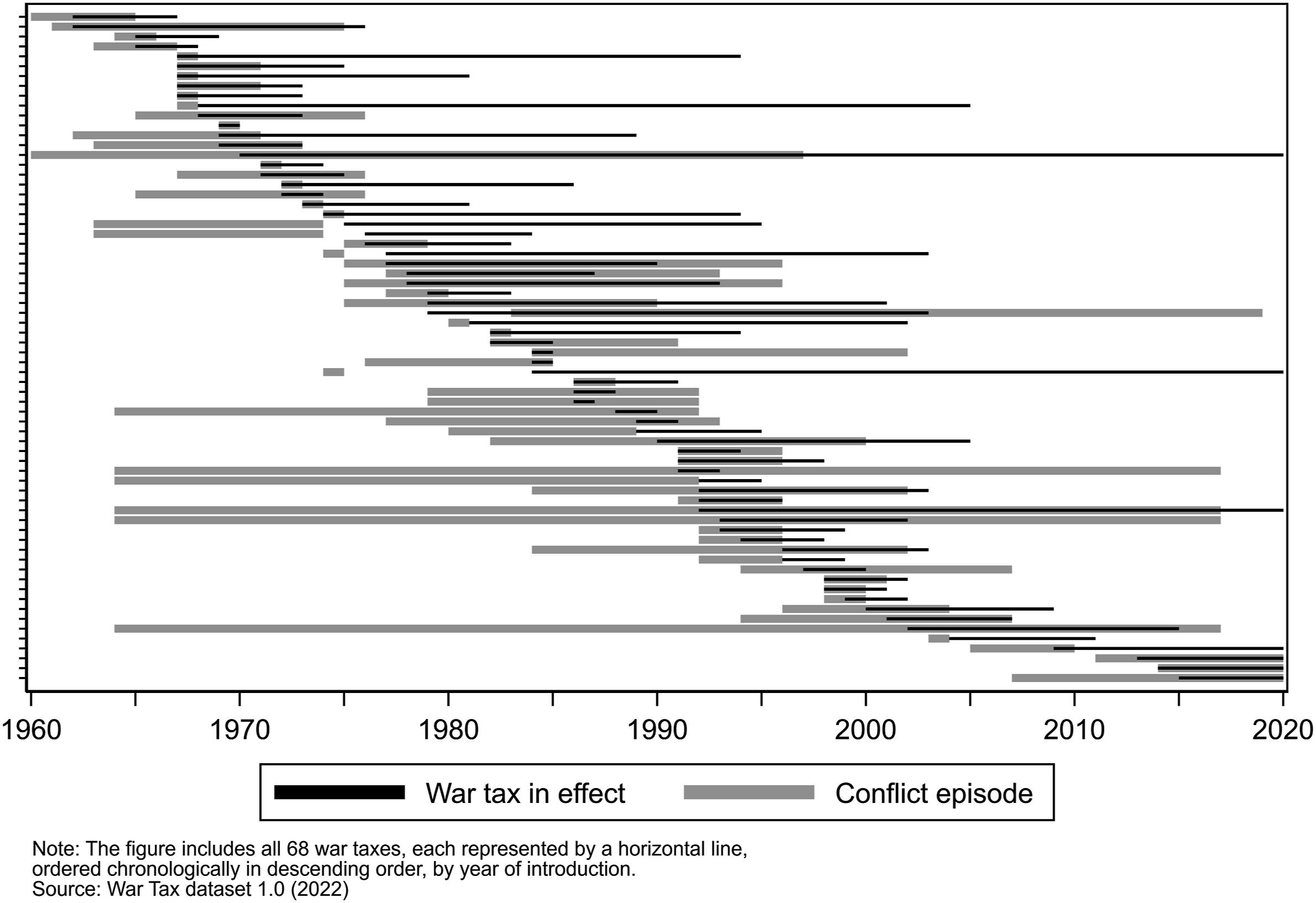

In a first step, the research problem is approached through a series of logit regressions covering war-affected countries between 1960 and 2020, serving two purposes: first, and most concretely, to elucidate under what conditions war taxes are likely to be employed, providing substantive meaning to the geographical and temporal variations observed (Figures 1 and 2), and, second, to test the logic behind them. However, while the extensive sample allows for initial generalisable insights, it is less suited for verifying the more intricate manifestations of the logic. War taxes across time.

The second empirical section therefore shifts the unit of analysis to cases of war taxes, approached both through a review of the population in its entirety as well as a handful of selected cases. The first, macro-perspective, serves several purposes: (1) descriptively, providing an overview of a hitherto overlooked phenomenon, including their revenue yield and policy legacies; (2) analytically, to further assess the fit of the population as a whole to the theoretical expectations; and (3) methodologically, to situate the selected micro-cases within the overall population.

In further aiming to verify observable manifestations of the mechanisms underlying the logic, individual cases are chosen by virtue of either diverging or confirming particularly well to expectation, together forming a diverse sub-sample. No single case is expected to either prove or disprove the logic, but taken together they may increase our confidence in the proposed logic, and more specifically, that the statistical macro-associations observed are plausibly driven by the proposed mechanisms.

Two delimitations are worth emphasising. First, the analytical ambition is not primarily causal – this would be next to tautological. As defined here, war taxes must be plausibly motivated by actual (realised or prospective) wars. Instead, the analysis centres on uncovering central mechanisms shaping war-time fiscal expansion, for which war taxes constitute plausible pathway-cases (Gerring, 2007).

Second, the analysis restricts itself to a single fiscal instrument – constituting a historically central link between war and long-term fiscal capacity, the contemporary manifestations of which has remained unexplored – hypothesised to be a response to these mechanisms. This is not to deny the existence (or importance) of alternative financing instruments, such as sovereign bonds, external rents, monetisation, or general tax rate increases. War-time governments often use a wide variety of instruments (Cappella Zielinski, 2016). 6 But if the proposed logic is correct, war-time governments cannot pick and choose at their own discretion. The goal of this study is to unveil the logic of war taxes and the conditions determining their utilisation; I leave to future studies to explore their alternatives.

War Tax Data

The empirical analysis is based on newly collected data covering a quasi-totality of war taxes introduced between 1960 and 2020. The sample covers 79 countries (see Table B1 in Codebook) which during the same period were involved in an armed conflict resulting in at least 1,000 battle-related deaths. The data was collected through extensive year-by-year reviews of relevant country-periods using IMF country reports as well as tax consultancy reports, complemented by keyword searches in news archives and consultations with country experts. A full 68 war taxes (Figure 2), introduced in 36 countries, have been identified.

The dataset 7 contains information on the name and legal basis of the tax, year of introduction and termination, type of tax instrument, apparent incidence, and information on rates, exemptions, and allowances. It further codes the motivation of the tax, legal earmarkings, revenue yield, and policy legacies. Contextual information is available in the form of data on tax structure in the years preceding the introduction and type and intensity of referent-conflict, 8 as well as a brief description of its timing, motivation, and implementation. 9 Table A1 in Appendix lists all war taxes along with a unique tax-id, used as reference in the analysis.

Statistical Analysis

To probe the logic and determinants of war taxes in the contemporary world, we begin by analysing country-year panel data covering the full sample of 79 countries, in a series of logit regressions. The binary dependent variable is coded as 1 for any year in which a war tax is in place. In the basic model, a country is coded as ‘at risk’, and thus included in the sample, beginning 5 years prior to an engagement as a primary or secondary party to a conflict; it ceases to be ‘at risk’ 10 years after the last engagement.

10

Compared to the now standard event-history model, in which only the first year of an event is taken into account (Beck et al., 1998), the present model avoids discarding most of the relevant data. Given the assumption that subsequent extensions are determined by the same fundamental logic as first introductions, it provides an effective and straight-forward way to approach the question of when (under what conditions) war taxes are employed.

11

To account for time-dependency in the dependent variable, a duration variable – natural log of continuous years with war tax – is included in all models.

12

To facilitate interpretation, the operationalisation of the variables is kept as simple as possible in the main models. I. Data on conflict are from UCDP/PRIO Armed Conflict Dataset (v.21.1). To allow for a delayed, cumulative effect, all conflict variables are constructed as rolling averages of the preceding 5-year period, with values ranging from 0 to 1. The simple conflict variable thus indicates whether the government has been a primary belligerent in an ongoing armed conflict in the preceding 5 years. Other variables indicate whether the conflict was high-intensity (Major),

13

whether it was a civil (Major civil) or inter-state war (Major int.), and whether the government or the opposing party had active second-party support (Gov./Op. support). A separate variable (Intervention) codes whether the government itself has been a secondary party to a conflict. High military capacity is proxied by a dummy coding permanent membership of the UN Security Council or NATO membership. II. GDP data from the Maddison Project (Bolt & van Zanden, 2020) is used to annually classify each country into one of four income classes, with dummies representing low, lower-middle, upper-middle, and high income, respectively. State capacity is measured using an index constructed by O'Reilly and Murphy (2022) based on V-Dem indicators. To allow for directly interpretable, non-linear associations, four dummies representing sample-quartiles are used. III. To account for the influence of alternative revenue sources, a dummy coded as 1, if oil and gas production reaches 5% of GDP, is constructed from data by Ross and Mahdavi (2015). Another dummy coding whether a country is currently in default on its external, private creditor debt is adopted from (Beers et al., 2022), proxying for the availability of external credit. IV. A nationalist ideology variable captures the extent to which government uses nationalism to legitimise its rule (Tannenberg et al., 2019), plausibly increasing its credibility in committing to war-related causes. Finally, an index capturing the intensity of public protests and its relative concentration to the capital city is constructed based on data from V-Dem (v.12).

In addition to these indicators, derived from the observable implications outlined above (I–IV), there are other factors which have been argued to affect the propensity of governments to utilise war taxes. First, democracy features prominently in the literature on war finance, but its effect remains ambiguous. Democrats could be more prone to finance war through transparent means such as dedicated taxes – but may also have better access to alternatives such as sovereign debt (Cappella Zielinski, 2016; Kreps, 2018). A dummy accounts for universal male suffrage (V-Dem v.12). 14 Second, ethnic fragmentation, particularly when accentuated by war, could inhibit fiscal patriotism (Herbst, 1990, p. 129). On the other hand, as argued above, what matters most acutely for the government is the consent of its (ethnic) constituents – not peripheral minorities (but see also Walter & Emmenegger, 2023). Nonetheless, a variable counting the number of politically relevant ethnic groups is adopted from EPR data (Vogt et al., 2015). Finally, a measure of the extent to which the economic elite holds disproportionate political influence (Oligarchy) is taken from V-Dem (v.12). On the one hand, economic elites have been prone to resist war-time taxation (Centeno, 2002; Tilly, 1992);on the other hand, credibly linking tax revenue to the exigencies of war is precisely what may generate their consent (Flores-Macías, 2022).

Statistical Results

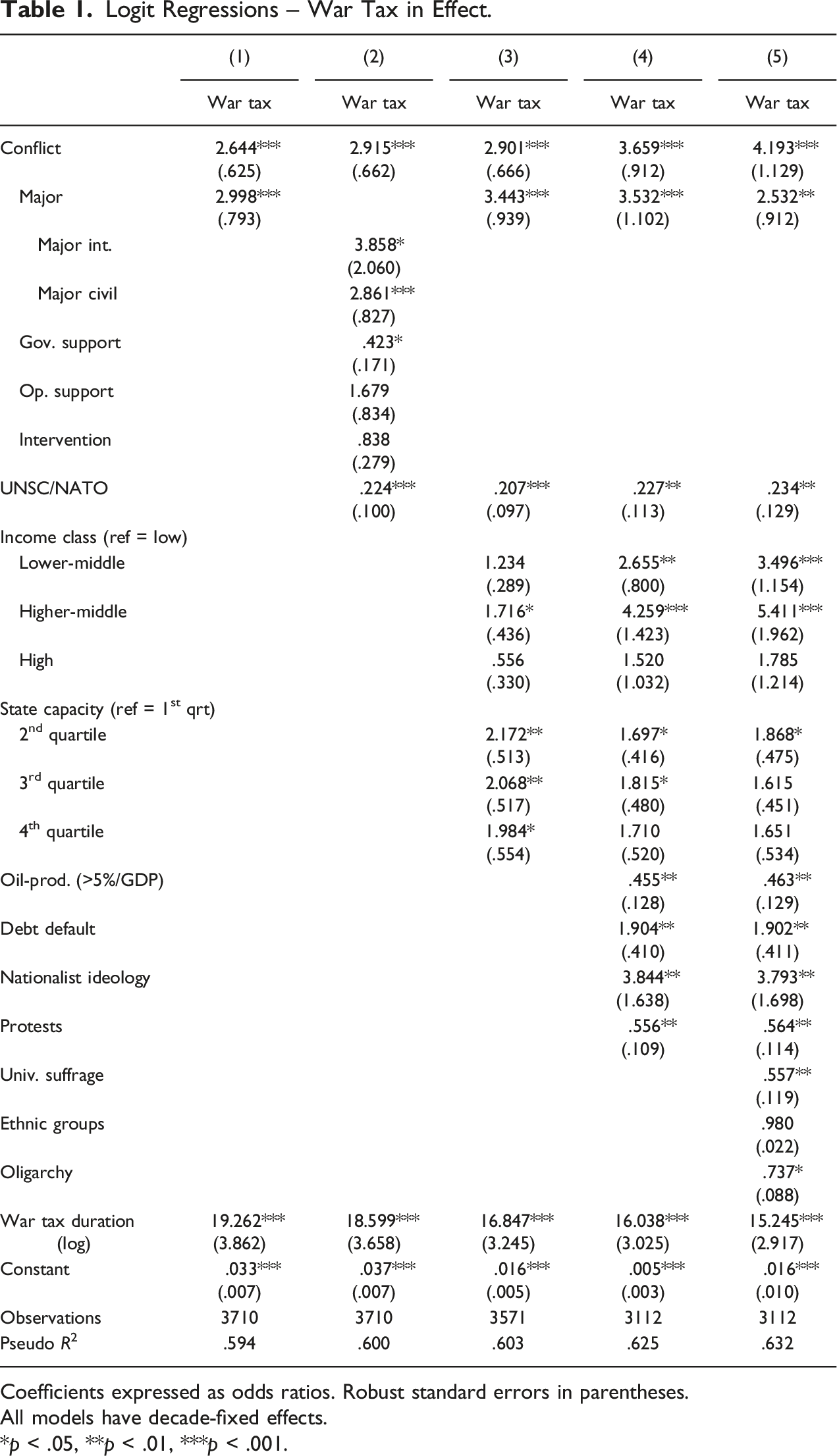

Logit Regressions – War Tax in Effect.

Coefficients expressed as odds ratios. Robust standard errors in parentheses.

All models have decade-fixed effects.

*p < .05, **p < .01, ***p < .001.

The strongly positive logged duration variable indicates an increasing policy-inertia, whereas during its first years in effect, having had a war tax in place in the previous year only weakly predicts its presence in the current year; after around a decade in place, the predicted probability converges to 1. 15

Model 2 disaggregates the conflict variables and adds engagement as a secondary party (Intervention). While the coefficient for Major inter-state wars is particularly large, equally striking is that major civil wars – dominating in the sample – have a substantially large and statistically significant association with war taxes. Indeed, the confidence intervals (95%) for the predicted probabilities at full inter-state war completely overlap those for civil war, precluding conclusions about difference in effects. What can be safely concluded is that civil wars are by no means antithetical to the phenomena of war taxes. On the whole, what matters is the intensity of the war – not whether the military challenger is another state or a rebel group.

The coefficients for foreign support are in the expected directions. Given involvement in an armed conflict, the presence of active external government support, plausibly decreasing both threat and fiscal pressure, is associated with a decreased probability of employing war taxes (significant at the 95% level) in the order of four percentage points. Inversely, the coefficient for external support for the opposition is above 1 but fails to reach statistical significance.

As opposed to being a primary party to the conflict, military interventions show no association at all with the probability of employing a war tax, in line with I. (d). It is worth emphasising that secondary-party involvements may be of significant scale and engender massive human and material sacrifices (e.g. the US and Russian involvement in Vietnam and Afghanistan, respectively). Nonetheless, as argued above (I), they are often unpopular and seldom seen as a response to an existential threat. Finally, the UNSC/NATO coefficient indicates that being a major military power or under its protection is associated with a lower probability of employing war taxes, in line with I. (b).

Model 3, turns the attention to structural conditions (II), introducing dummies accounting for different levels of economic development and state capacity. First, with the low-income category as reference, the coefficients for the remaining categories indicate an inverted-U relationship between economic development and the probability of having a war tax. However, only the lower-middle income category is statistically different from the poorest category. The coefficients for State capacity are clearer, with war taxes being less probable in countries with the least capacity. While not conclusive, the results support implication II.

Model 4 introduces variables accounting for fiscal alternatives (III), as well as two variables seeking to account for the a priori credibility of the government and expressions of popular discontent (IV). That alternative income sources matters is supported, in line with, for example, Centeno (2002) and Queralt (2019). First, the coefficient for high oil-production indicates that natural resource rents can moderate the need for additional taxes. Second, the positive association with default suggests that when foreign credit becomes unavailable, the need for increased taxation to fund the war is accentuated. Nonetheless, and while both associations are substantial, 16 neither would indicate that alternative revenues fully offset demand for taxes. Thus, moving to the supply-side, the coefficient for nationalist ideology is positive and statistically significant, indicating that strongly nationalist governments are around 50% more likely of introducing and maintaining war taxes than non-nationalist governments – plausibly because of their inclination to, and credibility in, mobilising popular support against threats to the nation. Inversely, however, the probability declines sharply with the presence of mass protests. Both suggest that credibility and popular legitimacy matters, in line with the argument above (IV).

Finally, Model 5 adds three variables accounting for factors that feature prominently in the literature on war-time taxes, but going beyond the direct implications of the theory. First, and most surprisingly, given the allegedly democratic nature of taxes as war finance mechanism, universal suffrage is associated with a lower probability of employing war taxes. While we cannot interpret this causally, it clearly refutes the assumption that war taxes, and, by implication, the need to acquire taxpayer consent in times of war, would be a feature specific to democracies. Second, and strikingly, given a population of countries largely ravaged by civil war, the number of politically relevant ethnic groups shows no association at all. This could indicate, in line with the reasoning above, that it is the consent of government constituents that matters – not that of potentially antagonistic and peripheral minorities. However, it could also support the argument of Walter & Emmenegger, 2023, whereby minorities can be swayed by war-time fiscal patriotism – but only as long as the tax is targeted and non-permanent. Third, the coefficient for Oligarchy – capturing disproportionate political influence by the economic elite – would indicate a slight negative association, in line with, for example, Centeno (2002).

When entering all variables in the same model (5), the extant variables moreover retain their substantive interpretation. While the models prioritise parsimony and completeness of coverage and should not be directly causally interpreted, the results are sufficiently clear and robust 17 to provide a general picture of when – under what conditions – war taxes are introduced and kept in place, 18 as well as a test for the proposed logic. First, conflict intensity and relative military balance is decisive, in line with the above reasoning (I), whereby the threat posed by the war, and the material needs it gives rise to, is what prompts government to seek additional revenue. Whether the opponent is another state or a non-state armed group matters little. Second, war taxes are less common in very poor and weak states, where the short-term net benefit of new taxes can be assumed to be low (II); as well as when politically convenient alternative revenues are abundant (III). Finally, nationalist governments are more likely to attempt to rally fiscal patriotism in war, whereas mass protests inversely discourage it (IV). The results conform to the calculations of a politically restrained revenue-maximiser, while contravening that of an unconstrained bandit, expected to act solely based on time-horizons.

In order to further probe the mechanisms underpinning the statistical correlations, and get an understanding of the substantive nature and potential long-term consequences of war taxes, the following sections shift the unit of analysis, zooming in directly at the outcome of interest.

Timing War Taxes

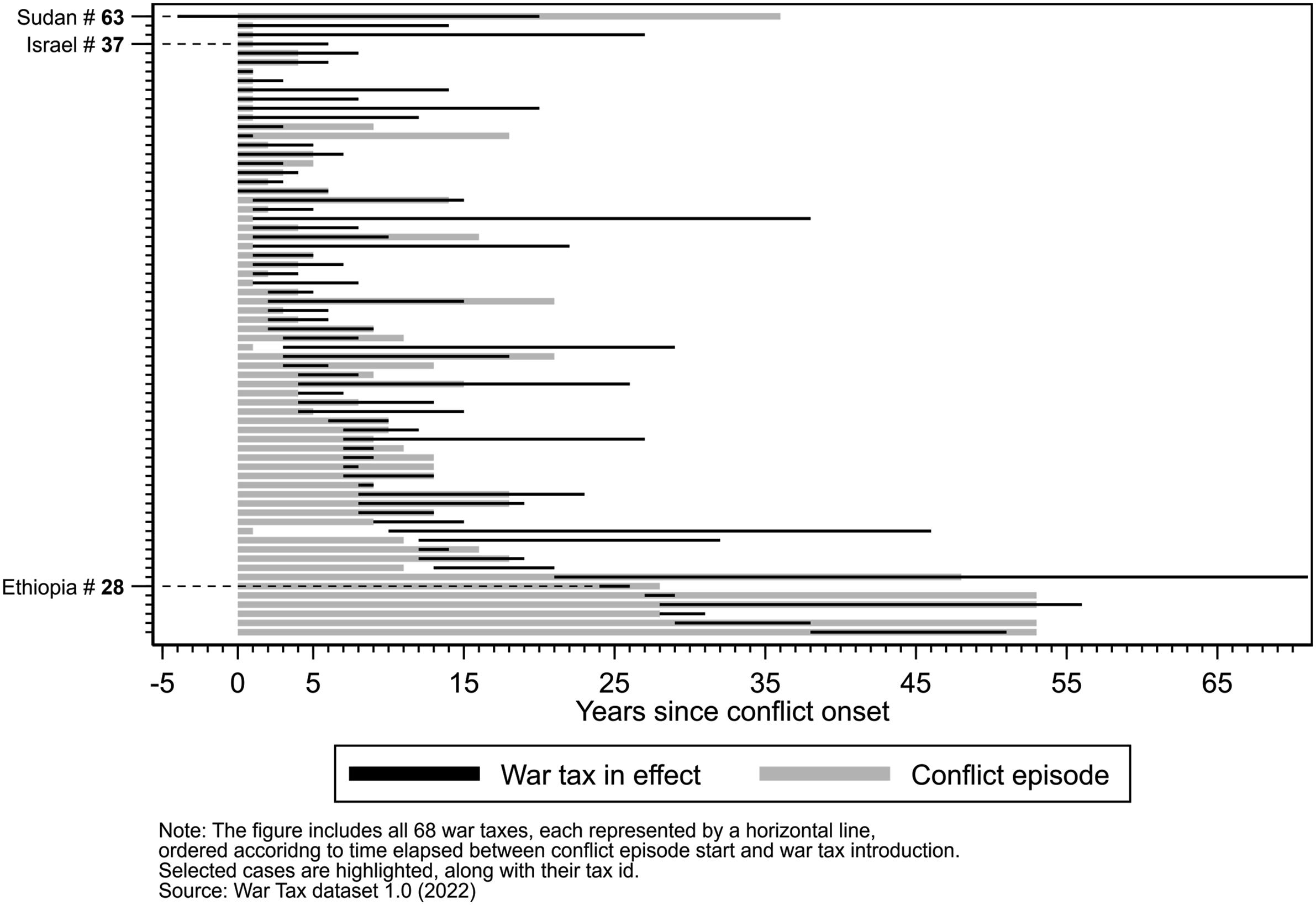

Having thus concluded that war taxes are strongly associated with actual involvement in overt armed conflict, how, more precisely, do governments time their introduction? Figure 3 visualises each of the 68 war taxes, ordered chronologically, in relation to the conflict episode to which they are linked. A full quarter were introduced in the first year of the conflict, and another quarter in the following 3 years.

19

The pattern aligns with the postulated logic, according to which even the most fiscally foresighted government must defer tax increases until the war has broken out and there is actually patriotism to rally. First looking closer at two cases, one that deviates from the theory (Sudan, tax-id #63), and one that fits it exceptionally well (Israel, tax-id #37), highlights the role played by fiscal patriotism. War taxes, by timing of introduction.

The Sudanese Defence and Security Tax (tax-id #63, 1979) was the only war tax introduced before conflict onset. The popular resistance with which it was met suggests why. With the government expanding its control over newly discovered oil-fields in the south, contradicting the 1972 peace accords with the Anya-Nya rebels, the prospect of renewed conflict was clear. But while defence spending sky-rocketed, the military front remained silent. Instead, the reaction came from the home-front in Khartoum and was directed at the war tax supposedly necessary for assuring their security. Coupled with anger over the economic situation, the Defence and Security Tax became a rallying-point for labour, student, and opposition protests that escalated during the summer of 1979. US diplomats worriedly reported that the government may have to backtrack, or else risk faltering (US Embassy, 1979). Nonetheless, with IMF backing the government ultimately weathered the storm, and – defying the general pattern (IV. (b)) – the tax remained in place with only minor adjustments. 20

Wiser then to wait until the war has materialised, as did the Israeli government in 1967. Having clearly anticipated the Six-Day War, it had also prepared the fiscal measures necessary for meeting its costs. On presenting them before parliament on June 5th, mere hours into the war, Minister of Trade and Industry Zeev Sherf asserted their absolute necessity as well as his conviction that the population would willingly shoulder them. After several concurring speeches by MPs, a near-unanimous parliament approved the government’s proposed Security Levy (tax-id #37) along with a compulsory ‘special defence loan’ (Knesset, 1967). In waiting until the war had materialised – but only just – the government could pitch into an exceptional wave of taxpayer patriotism, with government coffers being filled by advance payments (Wilkenfeld, 1973, p. 112). The two contrasting cases illustrate how consent can be harnessed through linking, but only if the cause is imminent and evident also for the taxpayers. Both governments had clearly anticipated the conflict, but the Sudanese made the mistake of acting before it materialised.

The clustering of introduction around the very beginning of conflicts is further in line with the observation that initial surges of solidarity tend to recede as conflicts drag on (Cappella Zielinski, 2016, p. 119; Mann, 2013, p. 175). For governments that wait until the treasury is empty, there may be little patriotism left to rally.

Nonetheless, a quarter of war taxes were introduced without apparent connection to conflict outbreak (or termination). The proposed logic and the regression results suggest that these cases can be explained by the intensity of the conflict itself and the evolving political and military context surrounding it. The Ethiopian Income War Levy, officially ‘Contributions for the unity and territorial integrity of the Motherland’ (tax-id #28), is potentially informative, having been introduced a full 24 years after conflict onset. The civil war between government forces and Eritrean secessionist rebels was initially limited in scale, but escalated periodically in the 1980s, as government forces launched a series of bloody offensives. It was only in 1988, however, with Soviet support waning and following the devastating battle of Afabet that the Ethiopian government finally introduced the much-needed war tax under the new mobilisation slogan ‘Everything to the warfront!’ (Sasaran, 1989, p. 66). Without steadfast external support and for the first time on the defensive, the fiscal cost–benefit analysis of the government as well as the popular sentiments on which it could draw clearly changed. What until recently had been officially dismissed as a fight against northern ‘bandits’, was suddenly described – and popularly understood – as an existential threat far worse than the looming famine (LA Times, 1988).

Hence, not only do conflicts have to materialise before they permit a forceful fiscal response but also reach a scale whereby the necessity of additional taxes becomes evident for both governments and taxpayers.

Conditional Consent

The argument is not simply that war-induced patriotism may decrease the cost of otherwise unpopular decisions, but critically, that explicitly linking a tax to a war-related cause is a crucial policy mechanism for translating patriotism into taxpayer consent (IV). A first indication – indeed, a smoking gun evidence – that linking is indeed crucial in this respect is the very ubiquity of its employment. Moreover, the two complementary mechanisms that were subsumed under the phenomena of fiscal patriotism above – rational and emotional – are both clearly manifested in the way governments link taxes to their cause. First, in line with the rational mechanism, most war taxes are linked – whether through legal earmarking (27 cases) or not – to specific spending categories, likely to be prioritised by taxpayers, be it reconstruction (19 cases), the military (18), or war victims and veterans (7). At the same time, highlighting the emotional aspect, few governments limit themselves to factual budget designations. Instead, war taxes are named and officially justified with the apparent purpose of evoking patriotic sentiments, emphasising necessity, urgency, and the ideal of collective sacrifices for the nation.

Notably, in the invocation of patriotic ideals, there is little discernible difference between the majority of war taxes introduced in relation to civil wars (46) and the minority related to inter-state wars (22). In fact, much indicates that for both populations and concerned governments, legal or scholarly distinctions remain largely irrelevant. As long as the conflict is perceived as a necessary and legitimate response to a real threat – be it external as in Israel in 1967 or internal as in Ethiopia in 1988 – governments seem convinced that linking and the invocation of nationalist sentiments will allow them to harness some of the resulting patriotism. But does linking really make a difference?

Again, it is the exceptional cases, such as the decidedly unpopular Mauritanian Contribution to the National Defence Effort (tax-id #41), that are most illuminating. Faced with the risk of forfeiting its long-standing territorial claims on neighbouring Western Sahara, suddenly evacuated by Spain, the Mauritanian government stumbled into war in December 1975, pitting it against Polisario forces. A few weeks later, it introduced the new war tax on business turn-over and wage incomes. With the army expanded by a factor of three in a few months, military spending soon reached 60% of the total expenditure – alone outstripping all domestic revenue. The levy was no doubt financially necessary. The problem was that the war-effort motivating it was itself perceived as neither necessary nor legitimate by a majority of the population, who prioritised development before financing a ‘fratricidal war between Africans’ (Le Monde, 1976). Accordingly, not only was the tax unpopular but further diminished the support for the war, the latter being ‘only as popular as its success and inversely as popular as its burden’ (Zartman, 1979, p. 135).

The case illustrates not only how populations are inclined to take linking seriously but also how the resulting consent (or rejection) crucially depends on the subjective understanding of the war – not its formal classification as either internal or external. Thus, as has been argued with reference to recent US history, irrespective of the fiscal necessity, whenever the necessity of the war is questionable and its legitimacy contingent on minimising burdens, taxes motivated by its cost will not only be resisted but undermine support for the war itself (Kreps, 2018). In this respect, poor developing countries appear no different than military super-powers. The fact that the Mauritanian government – hardly unaware of the ambiguous support for the war – nonetheless explicitly tied the tax to the ‘National Defence Effort’ would further suggest that it perceived linking as its only viable option.

In sum, nothing indicates that the linking of exceptional war-time taxes is either purely ornamental or an expression of accounting rigour. Instead, it is an effective, indeed imperative, means for convincing constituent taxpayers of the designated purpose of their contributions. However, as such, war taxes are also double-edged swords: if the war turns out unpopular, the linking can result in significant political costs.

Maximising Revenue, Minimising Costs

Nonetheless, the linking of a tax to the costs of war remains a means to an end, namely, revenue generation. In virtually all cases, governments have been faced with severe revenue needs, whether imminent or realised, at time of introduction, and, as it transpires, war taxes have generally been effective in responding to the fiscal gaps they are intended to fill. Revenue data, though often difficult to access, have been successfully collected for 51 of the 68 war taxes during their first 3 years in effect. The results show that war taxes on average represented 5% of total government revenues, or 1% of GDP – regardless of the type of conflict. 21 It can first be noted that the figures correspond closely to the average increase in military expenditure in contemporary armed conflicts (Armey & McNab, 2019, p. 578; Collier & Hoeffler, 2007), further underlining their function as responses to actual war-related fiscal needs – not accelerated self-enrichment. More generally, considering the painstakingly slow historical process of increasing tax collection, the figures are striking, representing an additional appropriation of a non-negligible part of societies’ economic output. By way of comparison, outside of the OECD, total revenues from personal income taxes, having been in place for decades, still hovered between 1% and 2% of GDP during much of the concerned period (Genschel & Seelkopf, 2016, p. 328). Many war taxes more or less immediately yield as much.

Nonetheless, a restrained revenue-maximiser must balance the potential yield against political costs. As argued (II), beyond the perceived legitimacy of the cause, taxpayer consent also depends on the fair distribution of the financial burden. While the typical solution for war-time governments has been to make use of distinctly progressive war taxes, these have on average yielded much less revenue. 22 Indeed, for the least developed countries, the choice between substantial revenue yield and distributive fairness concerns may be fully dichotomous.

Take the case of the National Solidarity Contribution (tax-id #6) introduced in Burundi (among the least developed countries in the sample). The tax, legally adopted in January 1997, consisted of a flat 6% levy on public employees and an unequivocally regressive fixed-amount poll tax on the rest of the adult population. But despite an economy in free-fall, military expenditure consuming one-third of government spending, and revenues dominated by transfers from the state brewery (EIU, 1997, pp. 44–45), it nonetheless took months of wavering before the government finally fully imposed the tax. In an interview with the minister of interior from mid-1997, the political concerns can be read between the lines of the ostensibly assertive defence of the tax: ‘The population needs to make an effort in this war. Those who are capable will be asked to contribute. The measure was taken globally, but it will not be asked of the regrouped [forcibly displaced] and others who cannot pay. It was the population that asked for a way to support the war – not the people in bad conditions, but the businessmen, civil servants, peasants, because many of them do have the means’. Nonetheless, the report adds, ‘lower level government officials […] indicate that the war tax is expected of all citizens, not simply those capable of paying’ (HRW, 1998, p. 180). While many citizens may have been sympathetic to the cause of the tax, it remained unpopular. Not only was it strikingly regressive, arbitrarily imposed, and onerous in an economy based on subsistence agriculture, but in areas otherwise weakly penetrated by the state and partly controlled by rebels, the proof of payment constituted a dangerous sign of ostensible government support (BBC Monitoring, 1998). Yielding a mere 1% of domestic revenue, it failed to reach even half of the modest expectations.

Evidently, a highly developed economy and strong administrative capacity are not necessary conditions for the introduction of war taxes; but as both the regression results and the case of Burundi suggest, with very little of either, political costs may outweigh the meagre benefits, inciting governments to opt out from extraordinary taxes in favour of alternative strategies.

In sum, contemporary war taxes have been highly successful in generating additional government revenue to pay for defence, reconstruction, and rehabilitation. Clearly, they are no mere symbolic policies. While signalling commitment is a crucial component to generate consent, the end goal is to increase badly needed revenue.

Contestation, Abolishment, and Legacies

Given the general success of war taxes, why do governments not make them permanent? In fact, many times they do: despite right-censoring, 12 out of 68 war taxes were kept in place for at least 20 years. But the lifespan varies greatly, and looking at cases at different points of the spectrum yields some insights into factors shaping their relative longevity.

The shortest duration in the sample was that of the Tax for the Defence of National Sovereignty (tax-id #25), a progressive wealth levy introduced in El Salvador in 1986. Motivated by the cost of the conflict with the FMNL guerrilla, and ‘intended to demonstrate to the country’s long suffering population that the rich were making their contribution’ (EIU, 1987, p. 17), it would survive for a mere 4 months. Upon its introduction, President Duarte pleaded with the exceptionally powerful economic elite (LeoGrande & Robbins, 1980) on whose behalf the war was waged: ‘we are in a war and in this war we must suffer, endure and resist together. It is not possible that only a few suffer. We who have something must contribute something’ (Associated Press, 1986). The argument fell on deaf ears. Following business strikes and virulent media campaigns, and with rumours of an impending military coup circulating, the levy was declared unconstitutional by the Supreme Court. Hence, in seeking to avoid the popular discontent provoked by the indiscriminate Burundian war tax in the case above, the Salvadoran wealth levy was instead defeated by an intransigent oligarchy. All was not lost, however. As the levy was revoked, the government had already integrated much of it into the standard tax system, effectively doubling the weight of the regular wealth tax.

More commonly, however, war taxes are extended beyond their initially planned duration – not least as wars tend to drag on for longer than expected – and, as attested by the regression models, after a certain duration their termination becomes increasingly unlikely. The Libyan Jihad Tax (tax-id #40), introduced in 1970 and still in place, is only the most extreme example.

With an average of around one decade in place, most war taxes are nonetheless formally terminated once its professed direct cause has ceased – even if the revenue needs remain. The Sudanese ‘Emergency/Defence Tax’ (tax-id #62), introduced in 1969 (predecessor to the ‘Defence and Security Tax’ discussed above) is illustrative. Having relied on ‘National Defence Bonds’ to finance the brutal war against Anya-Nya rebels, sky-rocketing defence expenditures forced the new military government to introduce a 1-year income surcharge. Failing to crush the rebellion, the tax was extended but also reformed in response to vociferous criticism of its alleged effect on prices. When the war finally ended in early 1972, and despite heavy costs for post-conflict rehabilitation, President Numayri announced that ‘the taxes levied to raise revenue for defense would be abolished since the country had established peace’ (Middle East Journal, 1973, p. 68). Other times, taxpayers beat the government to it, as in Chad in 1987, where the prospect of peace led to a spontaneous halting of payments of the War Effort Contribution (tax-id #10). Le Monde (1987) reported that despite a continuously precarious fiscal situation ‘the military successes in the North has considerably demobilised the population, which has suddenly stopped paying the war tax’ [author’s translation]. As the war nonetheless continued, and in spite of popular resistance to it, the tax remained in place until late 1990, when rebel commander Idriss Deby managed to take the capital, immediately announcing that ‘There would be no more war fund, and no more political prisoners’ (EIU, 1991, p. 35).

The clustering of abolishments around conflict termination (see Figure 2), together with case evidence, indicates a continuous process of tax bargaining between war-time governments and taxpayers. Specifically, the linking that once helped rulers introduce taxes to some extent also ties them (or their successors) to terminate them once the cause has definitely expired, in line with the medieval fiscal principle of cessante causa, cessat effectus (Levi, 1988, p. 107).

On the other hand, and contrary to assertions that only ‘permanent’ (Ames & Rapp, 1977) or ‘global’ wars (Rasler & Thompson, 1985) leave lasting fiscal legacies, less than one-third of war taxes were outright abolished. Instead, governments tried to preserve their revenue gains by integrating them into the general tax system, as exemplified by the Salvadoran wealth levy. Beyond the dozen cases that have become quasi-permanent, 23 governments have integrated them either by way of consolidating them into a completely new tax (12 cases), incorporating them by raising existing tax schedules (6), by substituting (9) or re-introducing (3) equivalent taxes albeit lacking the original motivation. Through such manoeuvres, not only have war taxes allowed governments to appropriate substantial resources during war to pay for defence, rehabilitation, and reconstruction but also left an enduring imprint on national tax systems, extending the long-term fiscal reach of the state.

Conclusion

Combining case- and population-level analysis of contemporary war taxes around the world with statistical analysis of macro-level data, this study has aimed to explain when and why governments introduce and maintain war taxes, while simultaneously providing insights into the mechanisms structuring the process of war-time fiscal expansion.

It showed that war taxes have continued to be a common war-time policy expedient, which while ultimately motivated by the imperative of additional revenue serve the crucial purpose of generating taxpayer consent by way of signalling commitment to a popular cause. Their introduction and relative longevity are crucially linked to a set of conditional factors, aligning with a logic of war-time governments as revenue-maximisers in need of consent.

First, the use of war taxes is primarily a function of the character of the conflict itself. What matters is the seriousness of the threat and the perceived necessity to counter it. Whereas few war taxes have been introduced in response to interventions in foreign conflicts, a host of contemporary civil conflicts, however divisive, have pushed governments to appeal to the fiscal patriotism of their constituent taxpayers – particularly when the military balance has turned against them. Not denying the disruptive consequences of civil wars, it nonetheless suggests that the logic of war-time fiscal expansion applies equally, if not identically, whether the military challenger is a recognised state or a rebel group.

More important then is the political and economic context, again in line with the proposed logic. War taxes are less likely in very poor or weak countries, where the revenue pay-off may simply not be worth the political risk. The availability of politically appealing revenue-alternatives further decreases the inclination for war taxes. Finally, the statistical results suggest that nationalist government are more prone to employ war taxes – but only as long as war-time manifestations of discontent is limited.

Together with case evidence, these macro-patterns suggest that war taxes are at the centre of a continuous bargaining process between governments and taxpayers, where the compliance of the latter is acquired through the spending commitments of the former. In war, no less than in peace, taxpayer consent is essential; it can be generated by rallying the fiscal patriotism of constituents, but remains contingent on the perceived legitimacy of the cause, the credibility of the government, and the fairness of the resulting burden. Granted, the need for taxpayer consent is not absolute. For one, the results suggest that it may be partly circumvented through loans and resource rents; other fiscal strategies – money printing, budget reshuffling, even discrete tax rate increases – may likely complement, if seldom fully substitute for new, dedicated taxes. Exploring such alternatives and their comparative consequences, though subject to serious data constraints, constitutes a promising avenue for future research.

Nonetheless, nothing indicates that taxpayer consent would be optional, or only apply to some war-time governments. Notably, the logic is in no way restricted to democracies. Indeed, the quantitative evidence suggests a consistently negative association between indicators of democracy and the employment of war taxes. Whether driven by confounding factors insufficient accounted for in the models (e.g. budget capacity, credit access), or related to an inherent property of democracies (e.g. input vs. output legitimacy), the results imply that a minimum of consent is essential, also for the least-likely autocrat. Dictators may be specialists in coercion, but when in need of additional revenue, even they are forced to rely on the quasi-voluntary compliance of their subjects. In other words, war may increase a ruler’s chances of reaching a valuable fiscal bargain, but bargain they must.

On the other hand, in line with the historically observed ‘ratchet-effect’, once in place, war taxes tend to stick. Given their substantial yield, often matching that of decades-old taxes, governments try to stretch their lifespan beyond their initial expiration date. When that is no longer possible, they often manage to discretely integrate them into the general tax system rather than give them up completely. For while taxpayers will not be duped, they can get used to what is already there. Having thus triggered processes of tax bargaining between governments and their constituents; allowed for a more progressive sharing of war-time burdens; and further expanded the fiscal reach of states; war taxes have remained a link in the chain connecting wars with potential long-term societal change.

Supplemental Material

Supplemental Material - Rallying Fiscal Patriotism: War Taxes in the Contemporary World

Supplemental Material for Rallying Fiscal Patriotism: War Taxes in the Contemporary World by Jakob Frizell in Comparative Political Studies

Supplemental Material

Supplemental Material - Rallying Fiscal Patriotism: War Taxes in the Contemporary World

Supplemental Material for Rallying Fiscal Patriotism: War Taxes in the Contemporary World by Jakob Frizell in Comparative Political Studies

Footnotes

Acknowledgements

The article is largely based on data collected as part of a PhD thesis at the European University Institute. I wish to thank colleagues at the EUI and the thesis jury, in particular Kenneth Scheve, for encouraging me to expand on the analysis of this data. Further valuable comments provided by Bastian Becker, Philipp Genschel, Herbert Obinger, the members of the Political Economy Working group at the University of Bremen, and finally the three anonymous reviewers, have all contributed to a significantly stronger article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Deutsche Forschungsgemeinschaft (374666841—SFB 1342).

Data Availability Statement

The data for this study is available through Comparative Political Studies Dataverse (Frizell, 2023): ![]()

Supplemental Material

Supplemental material for this article is available online.

Notes

Author Biography

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.