Abstract

In this paper, I explain variations in international investors’ reactions to International Monetary Fund (IMF) programs. Investors react favorably if a borrowing government is credibly committed to implementing essential IMF conditionality. Instead of engaging complex information processing about economic reform, however, investors rely on a heuristic device to assess the borrower’s domestic political conditions. I argue that a borrowing government’s popularity is an important cue for investors to assess the prospect of an IMF program. Investors associate higher government popularity with better implementation of the program and react more favorably to more popular borrowers. Using annual data from up to 52 emerging market economies from 1998 to 2017, I find robust statistical evidence supporting these claims: an IMF program alone does not restore investor confidence. Rather, an IMF program carried out by a strong government does. My findings have important implications for the study of global financial governance and credible commitment.

Keywords

When does an International Monetary Fund (IMF) program work? In May 2010, the Greek government agreed to implement extensive austerity measures and structural reforms in exchange for a 3-year, €110 billion loan from the IMF, the European Commission, and the European Central Bank. Combining the largest loan in the IMF’s history with an “ambitious” policy package, the bailout program was supposed to “restore market confidence” (IMF, 2010). The outcome was, however, disappointing. Throughout the 22 months of the program duration, investors became increasingly reluctant to lend to Greece. They asked the Greek government for an interest rate of 7% at the beginning of the program, and it spiked to a whopping 29% in February 2012 when the program was eventually canceled and replaced with a new program.

Why did the Greek bailout program fail to restore investor confidence despite the unprecedentedly large loan, coordinated support from the IMF and the European Union, and the government’s overt commitment to extensive economic reforms? To use an IMF term, the Greek program failed to trigger “catalytic effects”: it did not catalyze private financing. When private financing does not follow an IMF program, a borrower economy falls into a lengthened economic crisis, as was the case for Greece. Under what conditions can an IMF-participating government successfully attract international private financing?

A substantial body of literature explores this question, with many studies focusing on political and economic structural factors such as a borrower’s macroeconomic fundamentals and political institutions. However, because structural factors tend to remain constant over a short period of time, they provide limited explanations for within-country variations, including the exacerbated investor reaction for Greece during 2010–2012. In this paper, I suggest that explaining investors’ reaction requires much more than an examination of a borrower’s macroeconomic or political institutions. International investors reward borrowing governments that are credibly committed to implementing IMF conditionality. Investor reaction therefore depends on the domestic politics within which the government carries out the IMF-mandated reform.

Instead of processing all the information associated with complex austerity measures and economic reforms, however, investors rely on simple cues readily available for them. Specifically, I argue that a borrower’s political popularity plays a critical role in shaping investors’ perceptions about the credibility of IMF participants. Investors expect governments with lower levels of public support to have greater difficulty fully implementing IMF conditionality. Consequently, investors react favorably if a borrowing government gains public support.

My theoretical framework suggests that the terms of IMF programs as well as investors’ reaction could depend on a borrower’s popularity. IMF officials, for example, can grant more lenient programs to more popular borrowers because they appear more credible and thus more likely to make a program a success. In the interests of space, I focus only on investor reactions in this article, while I fully control for the terms of IMF programs in the empirical analysis.

To test my theory, I perform time series regression analyses on the original annual dataset covering 52 emerging market economies during the period of 1998–2017. For the selection bias inherent in IMF participation, I use a compound instrumental variables approach applied in two-stage least square models. Note that because investors use government popularity as a cue, government popularity has independent explanatory power even if it is not entirely independent of the underlying economic conditions. Nonetheless, to set aside endogeneity concerns about government popularity, I fully control for various economic and political conditions in all my analyses. Additionally, as a robustness check, I match countries based on similar economic and political conditions, and I test the effect of popular support on investors’ reaction in the matched sample.

Throughout all my analyses, I find strong and supportive evidence that an IMF borrower’s popularity is associated with international investors’ reaction. I find that an IMF program alone does not restore international investors’ confidence in the borrower’s economy, consistent with the existing findings. Instead, I demonstrate that IMF programs restore confidence primarily when provided to strong governments. These findings contribute to the expanding literature on IMF programs’ catalytic effects by explaining how investors update their beliefs about the same IMF participant’s credibility at different points in time as well as why we observe variations in the success of catalytic financing across IMF participants.

Beyond explaining variations in catalytic financing, this article contributes to important areas of the literature on international relations. This research fills a crucial gap in our understanding of the relationship between public opinion and the outcome of IMF programs. I gather and investigate comprehensive data on government popularity for 52 emerging market economies and demonstrate how mass-level opinion has a substantial impact on international investors’ pricing of an IMF-participating government’s debt. These findings suggest that a country’s domestic political environment, especially public opinion, plays a more critical role in international financial markets than commonly assumed. Relatedly, this research joins the IMF conditionality debate by highlighting that external conditionality triggers favorable investor reactions only when it is combined with local support. Last, my findings contribute to the abundant literature on credible commitment and international institutions by suggesting that domestic public opinion mediates international institutions’ function as a commitment mechanism.

IMF Program and Its Catalytic Effects

Every year, approximately 40–60 countries borrow from the IMF through conditional lending programs. Most of them approach the Fund because they cannot borrow from the international private market due to the lack of private investors’ confidence in the country. In exchange for lending, the IMF demands that the borrowing state restructure its economy by implementing policy conditionality. Conditionality aims to instill confidence in creditors by tightening government spending and increasing government revenues. Theoretically, therefore, commitment through the Fund is to purchase a good housekeeping seal of approval. A borrowing state sends a costly signal about sound economic policies by partially giving up its monetary and fiscal autonomy. However, despite the costly signal, not every borrower successfully regains market confidence or catalyzes private financing (“the catalytic effect”).

There is an expanding literature on the catalytic effect of IMF programs, although with decidedly inconclusive results. Regarding the question of whether catalytic effects exist, most studies have found null or negative results, while some recent studies have shown catalytic effects (Bird & Rowlands, 2002; Breen and Egan, 2019; Cottarelli & Giannini, 2002; Edwards, 2006; Gehring & Lang, 2020; Van der Veer & De Jong, 2013). Findings on the impact of IMF loan size and conditionality also disagree (Chapman et al., 2017; Corsetti et al., 2003; Díaz-Cassou et al., 2006; Eichengreen & Mody, 2001; Mody & Saravia, 2006; Woo, 2013). One line of thought is that countries with “intermediate” economic fundamentals, such as foreign reserves and debt, are able to restore investors’ confidence (Eichengreen & Mody, 2001; Bird & Rowlands, 2002; Mody & Saravia, 2006; Arabaci & Ecer, 2014). This notion, however, provides little explanation for short-term within-country variation, as macroeconomic fundamentals tend to change slowly.

Recently, political economy scholarship has explicitly investigated IMF participants’ credibility to explain varying catalytic effects. Chapman et al. (2017) make a compelling argument that countries that are geopolitically important to the United States experience the smallest catalytic effects because they receive weak conditions and little enforcement from the Fund due to U.S. influence. Bauer et al. (2012) maintain that democratic leaders are more credible than autocratic leaders because they have more flexible and fluid support coalitions. When a constituency opposes reform, a democratic executive has flexibility to build a new coalition of support, while a nondemocratic executive cannot easily do so. In addition, Cho (2014) finds that a left-wing government generates more credible signals about commitment to reform than a right-wing government because they are less likely to prefer to borrow from the IMF. All of the studies confirm that the key to successful catalytic effects is the borrowing government’s credible commitment to fixing the economic problems that have led them to borrow from the IMF in the first place.

However, there are still important empirical cases that remain to be explained. For example, during the IMF programs for the Papandreou government in Greece between 2010 and 2012 and the Yeltsin government in Russia between 1996 and 1998, investor confidence increasingly deteriorated to the point of causing regional crises. However, the economic and political factors that existing studies identify as critical mostly remained constant in these periods. My research engages this gap by focusing on a borrower’s domestic political environment and how it affects investors’ perceptions about the borrower’s credibility.

A Theory of Government Popularity

My argument has two central components. First, international investors reward governments that are credibly committed to implementing IMF conditionality, which will help resolve the government’s balance of payment (BOP) problems and stabilize the economy. Constrained by the costs of collecting and employing information, investors search for cues to predict the successful implementation of IMF conditionality. Second, I argue that a borrower government’s popularity is a powerful and useful cue for international investors as an indicator of the government’s political capacity to implement tough reforms. As a result, more popular governments receive more favorable investors’ reactions under IMF programs.

International Investors and IMF Programs

Among the different types of lenders that can be catalyzed by IMF programs, private financial institutions have dramatically expanded their volume and importance since the 1980s (Gould, 2006). Currently, most catalytic effects depend on private financing. The focus of this study is, therefore, private market participants such as investment banks, mutual and hedge funds, and individual bond traders, which I aggregately call international investors in this study.

International investors have good reasons to be skeptical of a country under an IMF program. Investors want to maximize the real value of their investment; however, BOP problems foster significant threats to investors. BOP problems can easily translate into defaults on debts unless borrowers quickly acquire liquidity large enough for debt remuneration. Moreover, the real value of an investor’s assets will diminish substantially if borrowers suggest debt restructuring. 1 Given that no legal institution guarantees debt service from foreign sovereign borrowers, international creditors are left with few protections. For example, creditors can join together to extend fresh funds to a cash-strapped government to prevent a default, but this requires effective coordination among international investors, which is challenging due to geographical dispersion and the large number of creditors. Creditors can also try to deter a default by refusing to lend again in the future. However, this strategy means that creditors lose along with debtors, giving their threat little credibility.

With few alternative tools available for creditors, IMF programs aim to shift the center of gravity among panicky creditors from skepticism to a belief in a borrower’s recovery. By giving a borrower government guidance on “sound” economic policies through policy conditionality, the Fund tries to attenuate investors’ concerns about sovereign default or debt restructuring. IMF conditionality does not exactly overlap with what investors want to demand from borrower governments. 2 Nonetheless, IMF conditionality does include essential reforms that creditors want to see, not only because the program’s core objective is to catalyze private financing but also because private investors have direct contact with Fund officials and deliberately demand that certain conditions be included in Fund programs (Gould, 2006). IMF conditionality includes orthodox austerity measures that will strengthen borrowers’ solvency, such as reducing government expenditure, selling off unprofitable state-owned enterprises, and raising government revenue. Despite the changing rhetoric about IMF conditionality over recent years, external debt management remains the single most frequent conditionality in IMF programs (Kentikelenis et al., 2016).

Key for investors, then, is whether the borrower government will successfully implement the conditionality. Investors are not interested in seeing every single condition delivered, but committing to essential reforms related to debt sustainability is a necessary condition to catalyze private financing. Unfortunately for investors, governments’ conditionality promises are plagued by the time-inconsistency problem. After securing IMF loans, governments may defect from their commitments to austerity conditionality, catering domestic supporters with large government spending. In fact, “[the overall] compliance with IMF conditionality is rather low” (Dreher, 2009, p. 249). 3 Given the low implementation records, investors react favorably only if an IMF borrower is credibly committed to implementing their program.

How do investors evaluate a borrower’s credibility? While investors employ information to maximize their expected returns, they are constrained by the costs of collecting and processing information. 4 The costs associated with information processing are especially higher when investors deal with emerging market economies than developed economies because of questionable quality of information as well as difficulty in accessing them. Investors thus economize the use of information by relying on “a narrow set of indicators” or heuristics as a cognitive shortcut (Mosley, 2000; 2003; Gray, 2009; 2013; Brooks et al., 2015). Studies find that investors rely on a few macroeconomic indicators, such as inflation rates, fiscal balance, and bond defaults, to assess a country’s credit risk (Mosley, 2000; Archer et al., 2007). Simultaneously, investors utilize noneconomic classifications such as a country’s membership in international organizations and geographic location as well as their views of similar “peer” countries as shortcuts in their estimation of a country’s credibility (Gray, 2009; 2013; Brooks et al., 2015).

Importantly, these heuristics have a strong impact on investors’ perceptions even when they do not align well with the country’s actual policy choices (Brooks et al., 2015; Gray, 2009, 2013). That is, heuristics have an impact on investor reaction independent of the actual changes associated with the heuristics. This is due to investors’ incentive to gain short-term benefits and minimize relative loss (Brooks et al., 2015; Gray, 2013; Mosley, 2000). Because investment returns depend not only on a country’s actual performance but also on other investors’ perception of the performance, investors can benefit in the short term by following market sentiment even when the cues that generate market sentiment do not necessarily correlate with policy changes on the ground.

The above discussion suggests that investors are likely to rely on a cue to identify credible IMF borrowers. Instead of processing all the information associated with austerity measures and reforms in foreign countries, investors will make inferences based on an easily accessible measure. The cognitive shortcut shapes investors’ perception, not necessarily because it exactly predicts the implementation of IMF programs but because it generates a satisfactory expectation among investors about the programs’ implementation.

Government Popularity and Implementation of IMF Conditionality

I suggest that a borrower government’s popularity is a useful shortcut for investors to assess the implementation likelihood of IMF programs. Government popularity is easily available information through polls and media reports, and it sends clear messages about the government’s political capacity. Furthermore, government popularity is particularly relevant for investors because it can change day-to-day, being almost a real-time barometer for nationwide public sentiment. Although public sentiment may be reflected in other measures of power structures, such as the share of government seats in a legislative body and electoral results, institutional measures are not updated as frequently as government popularity. The real-time component is critical for international investors who quickly reallocate funds as new information about a government becomes available (Ahlquist, 2006; Mosley, 2003). For example, if a borrowing government wins in a legislative election but quickly loses popular support afterward, investors will react to the deteriorating public sentiment. Therefore, while other domestic political environments, such as a government’s control of legislative bodies and divided versus unified governments, might affect investor behavior, public opinion captured by government popularity has an impact independent of these institutional factors.

In making this argument, I suggest that government popularity during IMF programs is not simply a reflection of underlying economic conditions but is an important concept on its own.

5

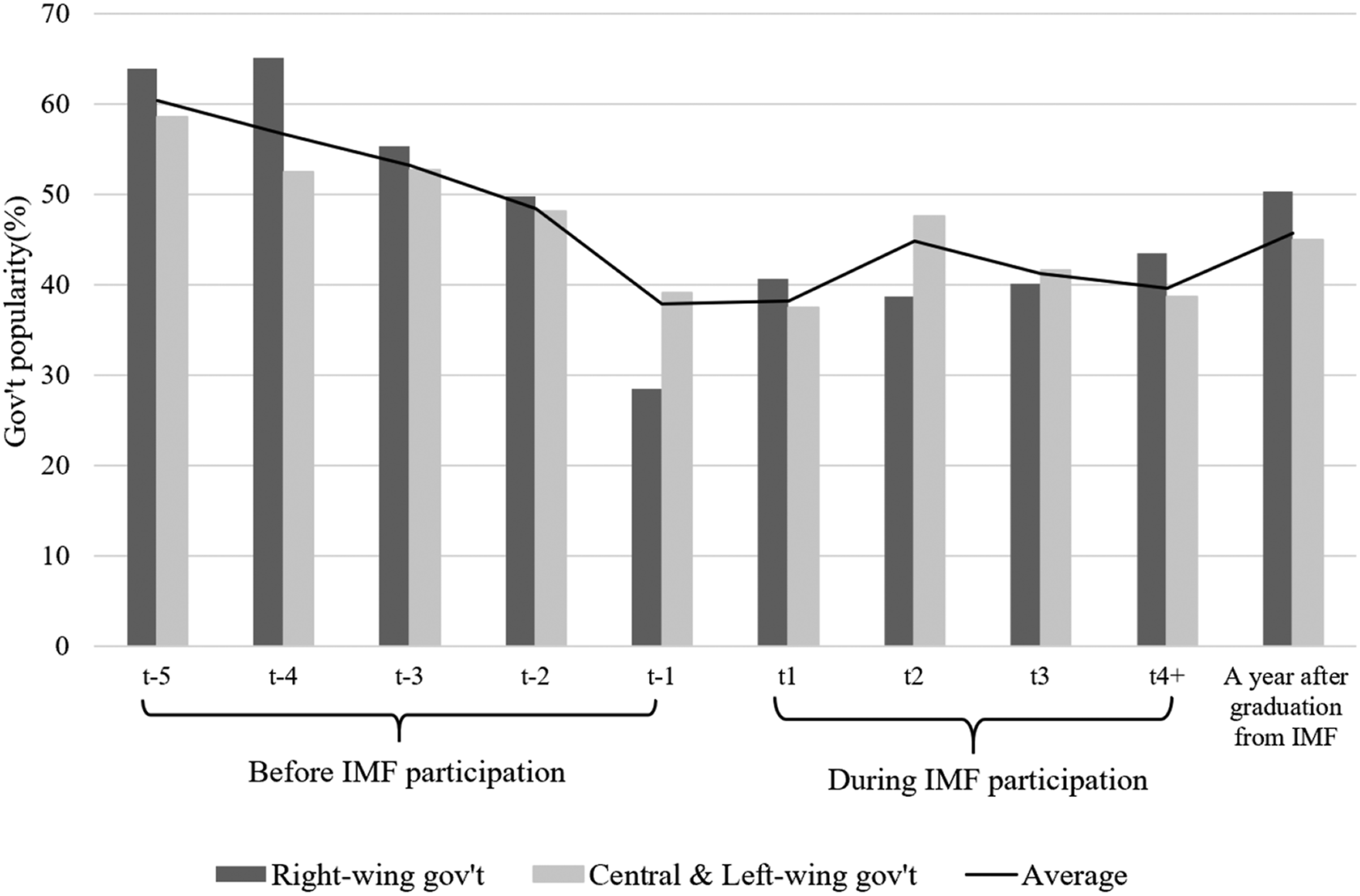

Figure 1 shows the average development of government popularity before, during, and after conditional IMF programs for 52 emerging market economies. Several patterns are noticeable. First, government popularity consistently declines during the 5 years prior to IMF programs, and the average popularity is lowest a year before IMF participation, t-1. Note that government popularity during IMF programs is not significantly different from that at t-1, which suggests that, consistent with existing findings, government popularity does not invariably drop as an IMF program is announced (Dreher & Gassebner, 2012). Rather, the deteriorating economy that leads a country to pursue an IMF program seems to have already reduced popular support before the program is implemented. Importantly and second, once a country participates in IMF programs, government popularity does not move in a clear direction. This echoes the established idea that IMF programs do not produce negative public opinion about the government’s economic policies (Beissinger & Sasse, 2014; Imam, 2007). Third, the average government popularity a year after graduation from IMF programs is not much different from that in the midst of the programs, which implies that the link between IMF programs and government popularity is weak. Last, all these patterns hold across government partisanship. Right-wing governments (dark gray bars) are not more or less popular than others (light gray bars) under IMF programs. Perusing the data, in summary, suggests that government popularity moves rather idiosyncratically during IMF programs. Government popularity and IMF programs, 52 emerging market economies, 1998–2017.

In fact, notwithstanding the dire macroeconomic conditions, some IMF participants manage to build strong public support. The South Korean government during the Asian financial crisis illustrates how appealing to nationalism can be one way to obtain popular support. Upon signing a Stand-by Arrangement with the IMF in 1997, the Korean Minister of Finance and Economy said in a televised speech, “I have come here to beg the forgiveness of the Korean people… please understand the necessity of the economic pain we must bear and overcome.” 6 Major media described the day the government appealed to the Fund for financial assistance as a day of national shame, a nationalist framework that evoked public unity and support despite the bad economy. For example, in 1998, more than 3.5 million people nationwide voluntarily donated gold to the government, contributing 227 tons of gold worth approximately $2.2 billion. As nationalist rallying continued, the government enjoyed strong nationwide support with approval ratings between 65 and 78% during the whole IMF program period. 7 The South Korean case illustrates that not all IMF participants lose politically. While every IMF borrower wants a high level of public support, each government shows unique popularity dynamics as a result of their culture and history. 8

Although cues investors use do not have to be entirely correct, it is plausible that high government popularity is associated with successful implementation of an IMF program because strong public endorsement facilitates enactment of IMF conditionality and generates better public compliance with the conditionality. First, higher government popularity leads to a higher bill-passage rate in legislatures because legislators take government popularity as a signal of a public preference for the government agenda and because popular leaders can alter citizens’ positions (Calvo, 2007; Ostrom & Simon, 1985). This effect is particularly pronounced if the bill in question holds some degree of public salience and issue complexity (Canes-Wrone & de Marchi, 2002). As IMF programs are almost always salient and complex, a more popular government is more likely to receive legislative approval for IMF programs. For instance, in the early 2000s, the IMF consistently demanded tax system reform in Argentina. Multiple governments in Argentina with little public support had attempted such reforms but could not get these programs past the Congress. Only when there was a large upward surge in government popularity in 2003 was the tax reform bill successfully enacted.

Second, high government popularity can lead to public compliance because people tend to support government policies if they have a favorable opinion of the government. Meneguello (2005) finds that in Brazil, support for various economic reforms, such as currency reform, pension and tax policies, is highly dependent on the evaluation of the government. Support for a policy moves with government approval ratings over time and across different partisan administrations. Similarly, Franklin, van der Eijk, and Marsch (1995) show that referendum outcomes in Europe are tied to the popularity of the government in power, resulting in (un)favorable outcomes for (un)popular governments. The positive relationship between government popularity and public support of new government policies seems to remain strong under IMF programs. During the Eurozone crisis in 2011, the Portuguese parliament quickly passed a set of IMF conditionalities. However, the government with an approval rating below 20% could not enforce the reform as the Portuguese public refused to comply with the reform package and held nationwide demonstrations against it. The theoretical speculation therefore suggests that government popularity may well be critical political capital for the successful implementation of IMF conditionality.

Note that my argument is centered around the public’s support for the government, not for IMF programs. This focus is because the public’s perception of their IMF programs reflects a wide range of factors that are not necessarily related to the specific IMF conditionality. For example, the Greek government held a referendum in 2015 to decide whether Greeks wanted to accept the austerity measures attached to its loans, and the outcome was heavily influenced by whether they supported or opposed “Grexit” (Walter et al., 2018). Likewise, the South Korean example previously illustrated suggests that the public’s views of an IMF program can be shaped by the government and the media, which implies that the public’s view may have nothing to do with the IMF conditions. Thus, when investors are curious about whether the government can credibly commit to the program, the public’s views of the program do not necessarily provide helpful information. Investors take credibility cues not from how the public perceives the program but from how much the public is willing to support the government that is attempting to implement IMF conditionality.

To summarize, my theoretical framework suggests that local support for government strengthens the government’s credibility and ultimately leads to favorable investors’ reactions. Before testing the theory, I clarify two theoretical scope conditions. First, my theory is about countries that actively participate in international financial markets. Low-income countries that rarely participate in international financial markets give little reason to international investors to react to their IMF programs. Second, my theory holds for nondemocracies as well as democracies. High government popularity in nondemocracies could suggest two different aspects of government capacity, both of which predict credibility in carrying out IMF conditionality. On the one hand, high approval ratings in nondemocracies could indicate genuine popularity, that is, strong government capacity validated by the people. On the other hand, high popularity may be the result of government management. In this circumstance, high popularity implies government competence and autonomy from public opinion. It signals that the government can get things done, and managing public opinion is another one of the things the government can do. Therefore, for both cases, high popularity signals strong government credibility in carrying out economic reforms. Although dictators do not have electoral constraints, investors could still take an important cue regarding government capacity based on popularity.

Empirical Strategy

In this section, I base my argument on robust statistical tests and analyze 52 emerging market economies from 1998 to 2017. I rely on JP Morgan’s Emerging Market Bond Index (EMBI) dataset to define the population, which includes only countries that are active participants in the international financial markets.

9

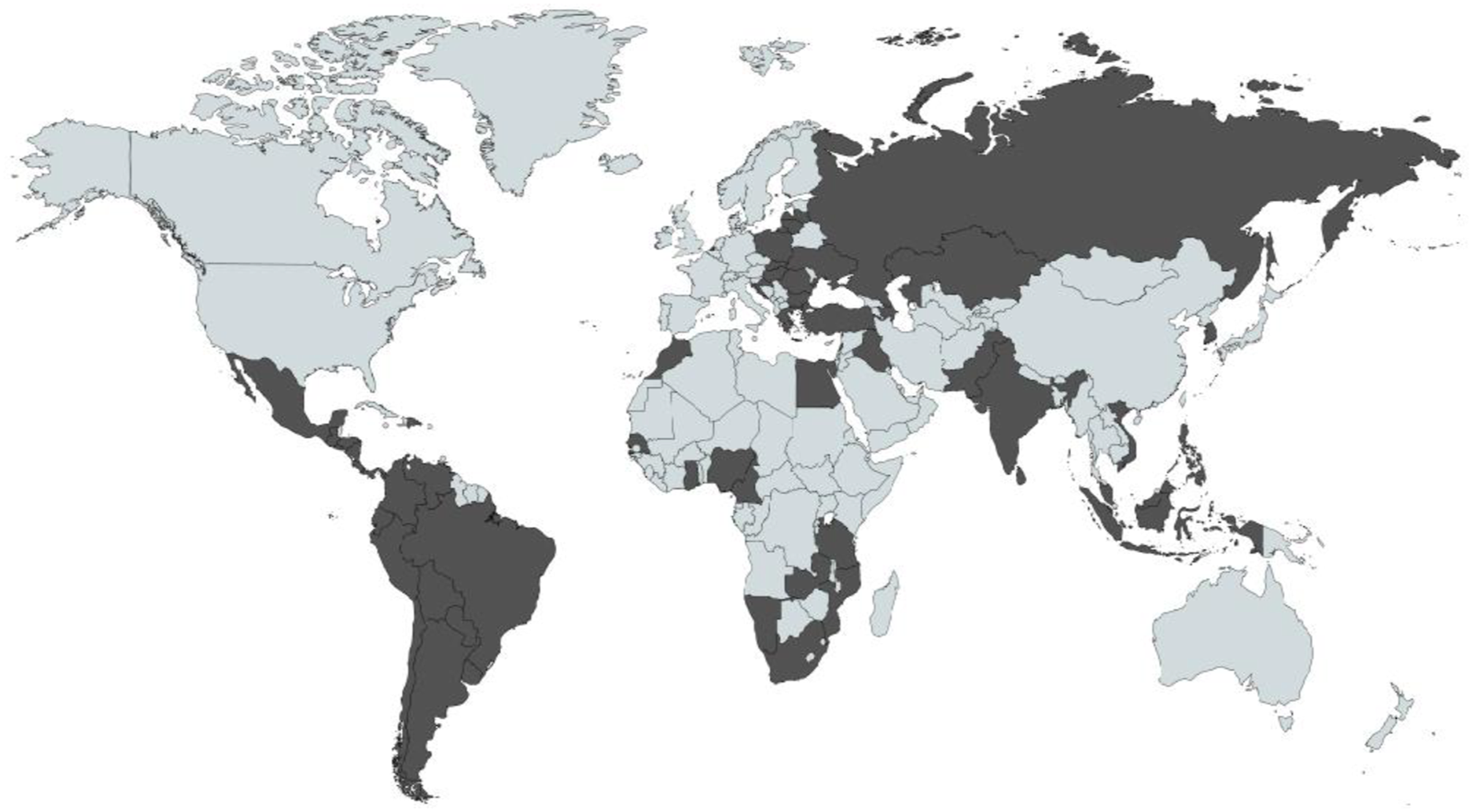

The EMBI included 23 states in 1997, and the number increased to 67 in 2017, of which data availability limits my sample to 52 states (Figure 2). The launch of the EMBI coincides with the shift toward portfolio-market-based government financing in the developing world, and the termination of the EMBI coincides with a shift toward a developed world. Countries exit my sample when they “graduate” from the EMBI by becoming a developed economy. A list of countries and years included in the EMBI and analyzed in the sample is available in the Appendix (Supplemental Table A2). Sample countries (shaded).

The main outcome of interest is international investors’ assessment of each country. Following previous studies, I use sovereign bond spreads to measure this outcome (Chapman et al., 2017; Eichengreen & Mody, 2001; Mody & Saravia, 2006). Specifically, I use yearly averages of sovereign bond spreads from the EMBI. 10 Sovereign bond spreads show international investors’ risk evaluation of each economy compared to the U.S. economy, with larger spreads reflecting investors’ higher skepticism toward the issuing government. Sovereign bond spreads are a better measure of market confidence than capital flows because capital flows reflect numerous factors not related to market confidence, such as a government’s external financing needs. Similarly, the recent literature shows that there is little relationship between actual FDI inflows and market confidence in the host country (Blanchard & Acalin, 2016). In contrast, sovereign bond spreads are generated precisely by a group of people who have incentives to get the risk perception right: traders of sovereign bonds.

Independent Variables

Public Support for Government

I use a government’s approval rating to measure the level of public support for the government. To cover all the countries in the sample, I assemble a comprehensive popularity dataset using various sources, including the Executive Approval Projects (Carlin et al., 2019) and regional and global polls such as Eurobarometer and Gallup polls as well as country-specific polls.

11

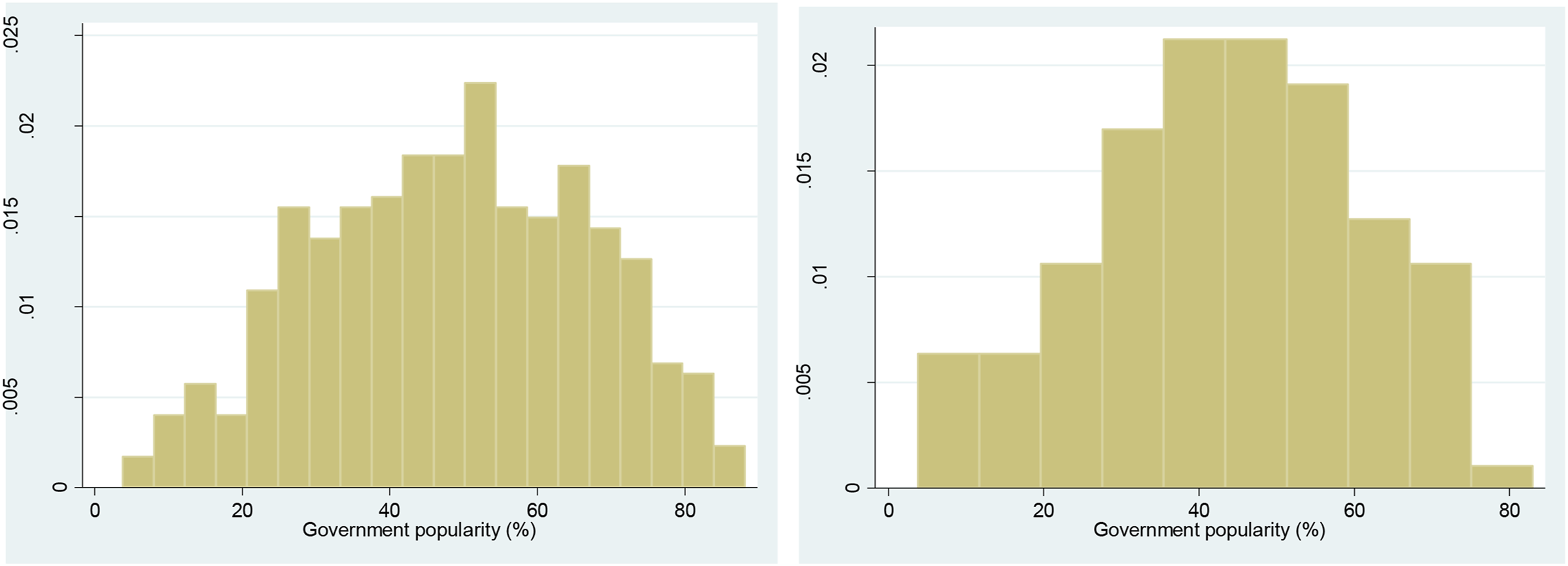

Most polls show reasonable distributions with mean approval ratings between 35 and 66%. Polls from Eurobarometer and Razumkov Center (Ukraine) show much lower average approval ratings, 24% and 13%, respectively. In the appendix, I provide descriptive statistics for each poll (Supplemental Table A3). To alleviate concerns about bias that might arise from combining different polls, I limit my analysis to the variation within a poll by including country fixed effects. Government popularity in the full sample is roughly normally distributed, ranging from 3.8% (Ukraine, 2009) to 88.2% (Namibia, 2014), with a mean of 48.2% (Figure 3, left). Note that popularity for IMF participants is also normally spread out between 3.8% and 83%, with a mean of 40.9% (Figure 3, right). Histogram of government popularity: whole sample (left) and IMF participants (right).

Some may raise concerns about the endogeneity of government popularity to the state of the economy because economic performance is critical for public evaluations of leaders (Lewis-Beck, 1988). Importantly, key in my argument is that government popularity is used as a heuristic device by investors. Because heuristics are perception independent from reality on the ground, they have their own effect even if they are not entirely independent from the country’s economic conditions. Furthermore, most “economic voting” theory evidence has been found in advanced Western democracies during normal times. 12 Empirical studies focusing on reform periods consistently report that a bad economy does not necessarily reduce government popularity (Echegaray & Elordi, 2001; Laredo, 1996; Przeworski, 1996; Stokes, 1996). At the same time, other factors, including IMF programs and globalization, mediate any impact of the economy on government popularity (Anderson & Hecht, 2014; Hellwig, 2001; Laredo, 1996; Przeworski, 1996). 13 Nonetheless, to account for potential endogeneity, I control for economic and political variables that could affect government popularity in all my main analyses. Additionally, I perform a matching analysis to pair countries with similar economic conditions but different levels of government popularity as a robustness check.

IMF Participation and Selection Bias

Coding IMF participation to tease out the program effect is not a simple task because IMF-participating governments may be systematically different from nonparticipants. To adjust for any selection bias, I follow recommendations from Stubbs et al. (2020) and employ an instrumental variable approach with two-stage least square models. Borrowing the novel approach developed by Lang (2021),

14

I construct the following instrumental variables for IMF participation

The IMF program is a binary variable, with a value of 1 if a country is under a conditional IMF program in a given year and zero otherwise (Dreher, 2006, updated). Past IMF participation is the share of years a country has been under IMF programs between 1970 and year t. IMF liquidity is a (logged) ratio of IMF liquid resources over IMF liquid liabilities. 15

The compound instrumental variable approach by Lang has been widely used in the recent literature.

16

I suggest that

Another source of concern is whether

UN voting is a proxy for a country’s policy dissimilitude with the United States at year t, measured as the two countries’ voting differences in the United Nations (Bailey et al., 2017). To increase the power of instrumentation, I add

A binary measure of the IMF program could mask substantial differences among IMF programs. Thus, I also use an alternative measure of IMF participation by focusing on the conditionality in each program. Utilizing data from Kentikelenis et al. (2016), I count the sum of binding conditions for each country in a given year and call it IMF conditionality. Following Stubbs et al. (2020), I instrument this variable with an interaction term between Past IMF conditionality—a measure of the average IMF conditionality for a country between 1991 and year t—and the IMF liquidity ratio. Data from Kentikelenis et al. (2016) extend to 2014; therefore, my analysis with IMF conditionality examines the period of 1998–2014. I include

Controls

I include controls that, when excluded, could confound the relationship among the key variables. First, given the studies that find a relationship between terms in IMF programs and the catalytic effects (Chapman et al., 2017; Corsetti et al., 2003; Woo, 2013), I control for the number of binding quantitative conditionalities and the (logged) loan amount relative to the borrower’s quota. I also take into account a borrower country’s macroeconomic conditions by controlling for budget balance, GDP growth rate, sovereign default, and current account balance because these indicators are accessible to the public and could affect bond spreads. 20

Next, I control for geopolitical interests because close ties with the United States could affect government popularity, IMF program implementation rates (Stone, 2004), and investor behavior (Chapman et al., 2017). I include the ideal policy point difference between the United States and the borrower country in question to operationalize the affinity between the two by utilizing dyadic similarity in UN General Assembly voting (UN voting) (Bailey et al., 2017).

To account for the range of possible domestic political factors that might affect implementation and government popularity, I control for veto players using the Political Constraints Index (Henisz, 2002) and regime type (Polity2) as well as national elections with indicators from the Database of Political Institutions (Cruz et al., 2018). Additionally, I include a right-wing government dummy to account for the partisanship effect on IMF program implementation and market reaction (Beazer & Woo, 2015; Cho, 2014). Descriptive statistics for all variables are available in the Appendix.

Model Specification

Because every government has different baseline popularity, it is important to consider both the changes and the levels of government popularity. For example, investors might reward governments that experience rising popular support from a low baseline more than those that have declining support from a high baseline. To measure the impact of both the changes and the levels, I employ error correction models (ECMs) (De Boef & Keele, 2008). ECMs simultaneously model both short-term deviations (i.e., changes in popularity) and long-term equilibrium (i.e., levels of popularity). In doing so, ECMs also alleviate the concern about spurious regression that arises from the potential nonstationarity of bond spreads and government popularity (De Boef & Keele, 2008). This is important because regressing one nonstationary time series on another results in inconsistent estimates and leads to the use of inappropriate tests for statistical significance.

Utilizing ECMs, I regress a first-differenced sovereign bond spread on (i) its lagged level, (ii) the lagged levels of all covariates, and (iii) the first differences of all (nondummy) covariates. The theory in this paper suggests that the effect of IMF programs on sovereign bond spreads is conditional on a country’s government approval ratings. I use the following ECM specification to estimate these interactive effects

Results

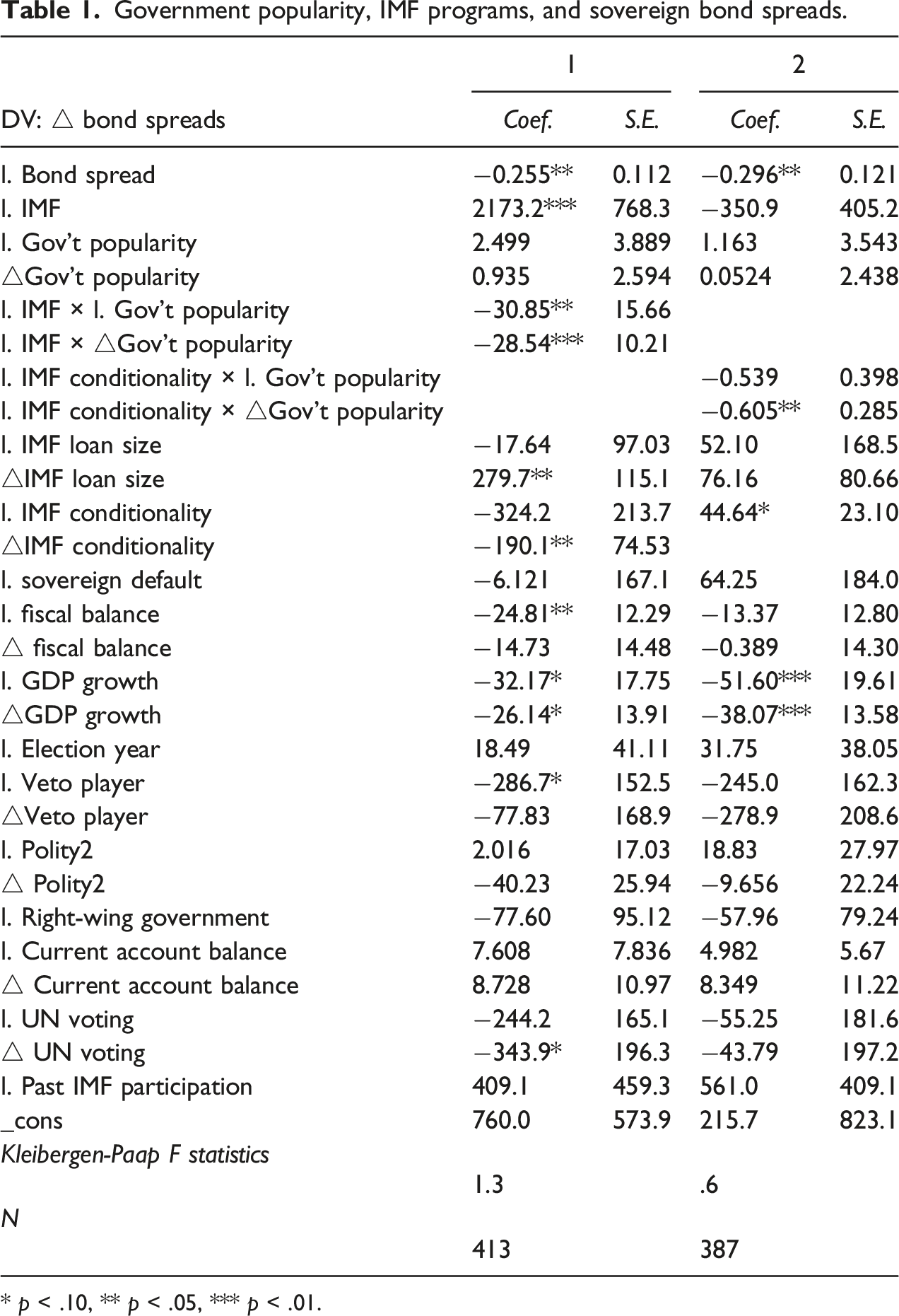

Government popularity, IMF programs, and sovereign bond spreads.

* p < .10, ** p < .05, *** p < .01.

My results suggest that an IMF program alone does not have consistent effects on bond spreads across different models, in line with the mixed results in the literature. Likewise, the coefficients of IMF loan size and the number of IMF conditionalities do not show consistent results. However, when the IMF program interacts with government popularity, a completely different picture emerges.

Let me first focus on the short-term effects, or the effect of the changes in government popularity. The first differences of the X variables estimate whether short-term changes in X bring changes in Y. I find that changes in government popularity during IMF programs bring significant short-term changes in the government’s bond spreads. A 1% increase in government popularity leads to an immediate 28.5 basis point (bp) decrease and a further 2.3 bp decrease in the next year (see model (1)). The unit here is JP Morgan’s indexed basis point. Considering the sample mean of bond spreads, this is a 6.5% decrease in bond spreads within a year. The results are similar when IMF programs are measured as conditionality. The results from model (2) indicate that more IMF conditionality with an increase in government popularity is systematically associated with lower spreads.

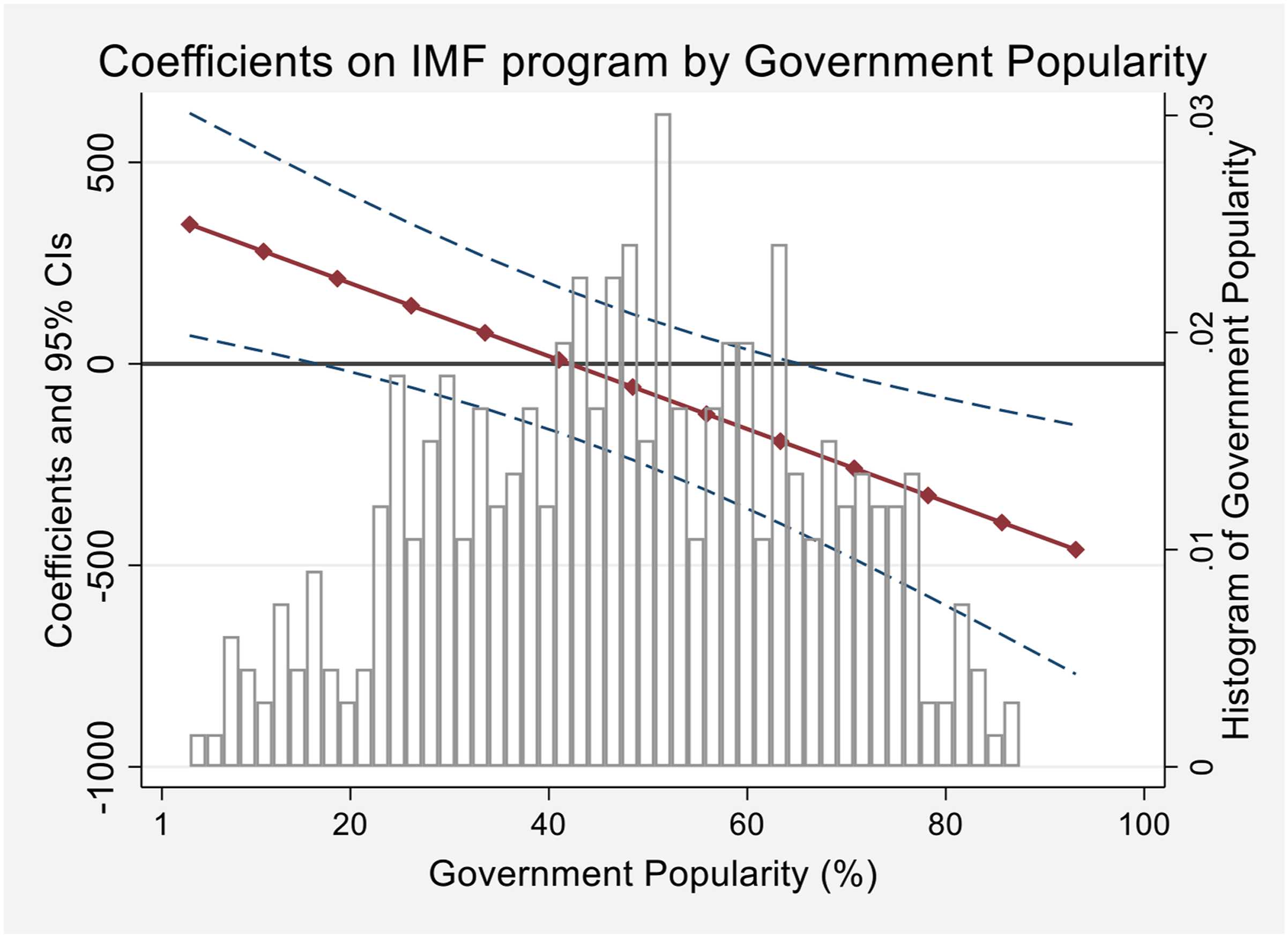

Next, I examine how the effect of IMF programs varies across different levels of a borrower’s government popularity. The coefficient of lagged independent variables indicates the long-term equilibrium relationship between those variables and sovereign bond spreads. The magnitude of the relationship, however, depends not only on those coefficients but also on the coefficient of the lagged dependent variable (l. Bond spread), which captures the rate at which changes in Y return to equilibrium. Specifically, the parameter calculating the long-term effect (long-term multiplier) is defined as Marginal effect of IMF program on sovereign bond spreads across different levels of government popularity.

The control variables show the expected signs. Existing studies consistently find that domestic political factors affect international investor behavior not during normal periods but during periods of financial stress (Archer et al., 2007; Baldacci et al., 2011; Ballard-Rosa et al., 2021). My analysis indeed finds that government popularity does not have a systematic impact on investors’ risk perception of a country during non-IMF periods. I believe this is both because investors pay little attention to domestic politics during non-IMF periods and because investors have a fuzzy picture of the policy changes enabled by strong government popularity for non-IMF participants. Consistent with existing findings, various political variables, including government partisanship, level of democracy, and elections do not affect sovereign bond spreads for emerging market economies (Brooks et al., 2019). Among other controls, GDP growth rates consistently achieve statistical significance with the expected signs.

Robustness Check and Empirical Extension

I perform a series of robustness checks and empirical extensions to increase confidence in my results. All of the results discussed in this section are available in the Appendix. First, as an alternative way to control for the endogeneity of government popularity, I perform regression on a “matched” sample. This approach is designed to allow for more reliable causal inferences in observational studies for which randomization is not possible. The crux of the method is as follows: Based on a number of observed background conditions captured in the “propensity score,” those in a treatment group are matched to a group of similar others in a nontreatment group. Matching thus creates two relatively similar groups, one exposed to a treatment and the other not. After matching, outcome analysis can proceed using the matched sample as if those samples had been generated through randomization (Stuart, 2010). Regressions on the matched sample therefore can yield more accurate estimates of treatment effects, although they do not remove all the difficulties associated with endogeneity in the estimation of the treatment effect.

Borrowing this approach, I first identify a treatment group, or the borrowers that enjoy high levels of public support. Given the earlier findings that governments with approval ratings above 60% experience the catalytic effect (see Figure 4), I designate observations with approval ratings above 60% as a treatment group and those below 60% as a control group, thereby making a binary indicator of treatment. Then, I match “popular borrowers (treated group)” to “unpopular borrowers (control group)” whose underlying economic and political conditions are closest to the treated observation. Following the recommendation from Stuart (2010), I include a battery of political and economic variables to calculate the propensity score. 23 Based on the propensity score, I use the nearest-matching method with replacement while keeping all ties.24,25 During this process, each observation in the control group (unpopular borrowers) receives a frequency weight that reflects the number of times they are selected as a match. Those that do not get matched automatically drop, resulting in a matched sample with 113 treatment observations and 204 control observations. The diagnoses indicate that the matching significantly reduces bias for all covariates and yields a much more balanced sample (Supplemental Figures A4 and A5). I replicate my main analysis on the matched sample, while incorporating weights generated during the matching. The results (Supplemental Table A6) are very similar to the main findings in Table 1. Having strong public support during IMF programs makes a statistically significant difference in a borrower’s bond spreads, leading to, on average, a 16% spread reduction.

Second, I examine whether my findings hold across different regime types by interacting the main independent variables with a democracy dummy. I have argued that high government popularity leads to favorable investor reactions in nondemocracies as well as democracies because it signals strong government capacity. The results (Supplemental Figure A6) support the theoretical argument: An increase in government popularity is negatively associated with sovereign bond spreads for both democracies and nondemocracies, and the effect is larger for nondemocracies. This result, however, should be interpreted with caution because of the small number of observations (121 obs.) for nondemocracies.

Additionally, I test whether the effect of government popularity varies by different political systems within democracies—presidential versus parliamentary. I find that a higher level of popularity reduces sovereign bond spreads in presidential systems, but not in parliamentary systems. However, an increase in popularity is strongly associated with reduced bond spreads in both systems, and the effect of government popularity is larger in presidential systems than in parliamentary systems (Supplemental Table A7). This is because unlike executives in the parliamentary system, presidents are directly elected by the public and are not controlled by a major party, which makes them more susceptible to public opinion. Considering my analyses on different regime types, the results altogether suggest that political and electoral institutions do not significantly mediate the impact of government popularity as a heuristic device on investors’ perception. In other words, although investors exploit government popularity as a cue, they care much less about how government popularity brings actual reforms.

Next, I test for an alternative mechanism in which a new government temporarily enjoys higher popularity while investors allow them a grace period with lower bond spreads. To see whether this is driving the results, I replicate my analysis excluding all new governments, which occupy 16% of the sample. Alternatively, I run the analysis with the whole sample while controlling for the years a government is in office. In both analyses, I find strong and consistent short-term effects, but I do not find long-term effects when new governments are excluded (Supplemental Table A8). The results indicate that changes in government popularity bring significant short-term changes in bond spreads regardless of government turnover, but they do not affect the long-term equilibrium bond spread relationship unless there is government turnover.

Another alternative explanation for my finding is that government popularity could be a proxy measure of the government’s seat share in a legislative body, and therefore, it could be merely a seat share or majority control of government, rather than popular support, that investors react to. To examine this possibility, I replace government popularity with the share of seats held by all government parties in a legislative body. 26 I do not find a significant effect of government seat share on bond spreads (model (1) in Supplemental Table A9). Alternatively, model (2) estimated in Supplemental Table A9 includes the measure of government seat share as a control, and the main findings remain consistent and strong. Altogether, these analyses squarely reject the alternative explanation.

Furthermore, because IMF programs often produce uneven distributional consequences, I control for distributional consequences with Gini coefficients for each county-year. Central bank independence, which may mediate the impact of public opinion on economic policy, is also controlled. Additionally, I control for a borrower’s debt sustainability by including its total reserve (% total debt) or government’s long-term debt in the model. As expected, none of these changes affected my results in any substantial way (Supplemental Tables A10 and A11). In fact, incorporating distributional consequences and debt sustainability strengthens the main results.

A final question is whether government popularity has a different impact on investors depending on IMF conditionality. Recall that I use the sum of quantitative performance criteria (QPCs) and structural performance criteria (SPCs) in my main analysis (Table 1, model (2)). However, it is possible that investors pay more attention to one condition than another. For example, international investors might care mostly about QPCs in the wake of IMF programs because QPCs include targets regarding fiscal and monetary policies that are directly relevant to government debt service capacity and that are relatively easy to implement. In contrast, SPCs include a wide range of reforms, ranging from appointing external panels on a certain issue to central bank reform, which may not be directly relevant to debt service. SPCs are also politically more contested and take longer to implement (Reinsberg et al., 2021).

Thus, Supplemental Table A12 replicates the primary analysis, with counts of QPCs and SPCs included as separate covariates. QPCs show results very similar to the main findings: QPCs themselves are positively associated with bond spreads, yet when they interact with changes in government popularity, QPCs are highly statistically significant, with the coefficient signed in the negative direction. On the other hand, neither SPCs nor the interaction term between SPCs and government popularity show statistical significance. These results indicate that investors put more weight on QPCs than on SPCs. Investors care most about whether a borrowing government will improve its debt sustainability by adjusting quick fixes rather than correcting deep structural fundamentals.

Conclusion

When does an IMF program successfully restore international investors’ confidence in a borrower’s economy? I identify public opinion as a key driver of credibility that explains both within- and across-country variation in investors’ reaction to IMF programs and determines when and where IMF lending generates the desired catalytic effect among private international investors. I present robust evidence from statistical tests that a rise in borrower governments’ approval ratings leads to a favorable investor reaction.

The findings have an important policy implication. A well-planned IMF program will do little good if the government tasked with implementing it has weak domestic political support. This will be critical during the current COVID-19 crisis, when many governments have received or planned to receive IMF funding while the pandemic has dramatically swayed their approval ratings. For those whose approval ratings have surged, such as Colombia’s president, Ivan Duque, this is a window of opportunity because “improved popularity for Colombia’s president Ivan Duque through coronavirus crisis could help the government pass difficult reforms,” as Fitch, a major credit rating agency, concisely noted. 27 However, for many others whose popularity has plummeted during the pandemic, the Fund must be aware that overcoming the current health and economic crisis will be extra challenging.

I also join the conditionality debate by underscoring that conditionality triggers favorable investor reactions only when it is combined with local support. In other words, IMF conditionality does not have a linear effect on investors’ reactions. Extra conditionality means more credible debt service only to the point where extra conditionality does not hurt the borrower’s political capacity. IMF economists and borrower government representatives should consider the trade-off between reforms and political costs to maximize the catalytic effect.

This research also speaks to an important area of the political science literature. There is a large and growing literature on public opinion in the international political economy, most of which focuses on variations in public opinion as the dependent variables. Building on the literature, I use the variations as a key explanatory variable and demonstrate why such variations matter for international financial outcomes and what signals international investors take from them. In doing so, my findings contribute to the political economy literature on IMF lending and international finance. With regard to IMF lending, this research identifies the conditions under which IMF lending leads to favorable investor reaction. I demonstrate that government popularity during IMF programs varies both across and within countries and, more importantly, that varying public support has a significant impact on the consequences of Fund programs. My results therefore provide concrete evidence on why IMF bureaucrats and government representatives should take into account mass reaction while they embark on a new program: maintaining strong public endorsement is necessary not only for the survival of the government and the reputation of the IMF but also for a quick recovery of the borrower’s economy.

For scholars of international finance, this research joins the literature on investor behavior and clarifies how investors make inferences about an IMF participant’s credibility. I show how the terms in the external commitments, such as IMF loan size and the stringency of conditionality, are less important than the domestic political context within which the commitment is implemented. Neither the factors that lead governments to sign on to IMF programs nor the macroeconomic conditions before and during IMF programs should be dismissed in explaining investors’ response. I demonstrate that the level of political support for a borrower has substantial effects. Since government popularity varies in a short period of time, unlike macroeconomic conditions or structural political factors, this finding makes a strong statement about why investors’ response varies over time.

Finally, this research contributes to the literature on credible commitment and international institutions by suggesting that domestic public opinion mediates international organizations’ function as a commitment mechanism. While many studies have focused on political institutions and power structures to explain the credibility of a state’s external commitment, 28 I suggest that a state’s credibility is subject to change in a short period of time depending on domestic public opinion. It would be fruitful for future studies to examine whether the role of public opinion as a “credibility cue” has similar effects for various policies that need domestic enactment and compliance.

Supplemental Material

sj-pdf-1-cps-10.1177_00104140211060280 – Supplemental Material for Who Is Credible? Government Popularity and the Catalytic Effect of IMF Lending

Supplemental Material, sj-pdf-1-cps-10.1177_00104140211060280 for Who Is Credible? Government Popularity and the Catalytic Effect of IMF Lending by Sujeong Shim in Comparative Political Studies

Footnotes

Acknowledgments

I thank Mark Copelovitch, Axel Dreher, Jon Pevehouse, Adrian Shin, James Vreeland, Jessica Weeks, and participants at workshops at the University of Wisconsin—Madison, the Graduate Student International Political Economy, the International Political Economy Society Annual Meeting, the Virtual International Political Economy Society Meeting, the American Political Science Association Annual Meeting, and three anonymous reviewers for helpful feedback. I also thank officials of the IMF, Index Licensing Team at JP Morgan, Valentin Lang, and Ryan Carlin, who were gracious with their time and resources.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was made possible by the generous support of Horowitz Foundation for Social Policy.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.