Abstract

Accelerating financialization and rising societal wealth have meant that democratic governments increasingly provide bailouts following banking crises. Using a new long-run data set, we show that despite frequent and virulent crises before World War II, bank bailouts to protect wealth were then exceptionally rare. In recent decades, by contrast, governments have increasingly opted for extensive bailouts—well before the major interventions of 2007–2009. We argue that this policy shift is the consequence of the “great expectations” of middle-class voters overlooked in existing accounts. Associated with the growing financialization of wealth, rising leverage, and accumulating ex ante financial stabilization commitments by governments, these expectations are suggestive of substantially altered policy preferences and political cleavages. Since the 1970s, when severe banking crises returned as an important threat to middle-class wealth, this “pressure from below” has led elected governments to provide increasingly costly bailouts with no historical precedent.

A decade after the global financial crisis, agreement on appropriate policy responses to banking crises remains elusive despite an apparent political consensus on the need to eliminate bailouts and end “too big to fail” (Binham, 2017). Furthermore, many experts doubt that measures adopted since 2008 to limit taxpayer-funded rescues will achieve this objective (Admati & Hellwig, 2013; Bernanke et al., 2019; King, 2016). Meanwhile, elected governments, most recently in Italy, continue to implement costly bailouts regardless.

The commonplace explanation that bailouts are the consequence of pressure from financial sector interests is not the whole story (Barofsky, 2012; Johnson & Kwak, 2010). 1 We argue that the emergence of “great expectations” among a large segment of society regarding financial stabilization has been a critical but overlooked factor driving long-term changes in government responses to banking crises toward increasingly extensive and costly bailouts. This evolution in the policy expectations of households and voters has been driven by three interrelated developments: the financialization of wealth, the democratization of leverage, and accumulating ex ante government policy commitments to financial stabilization. These developments have increasingly linked the interests of middle-class households 2 to financial markets and thereby broadened and intensified their effective demand for protection from the fallout from crises.

Utilizing a new data set that codes policy responses for 58 democracies in 112 systemic banking crises since 1848, we provide the first statistical analysis of government policy responses to banking crises over such an extended time frame and a large sample of systemic crises. Our findings are consistent with the claim that the wealth effect has generated a rising tendency toward bailouts. They relate to other studies suggesting that deepening ties to asset markets now challenge, if not supplant, those with the labor market as the dominant economic cleavage in politics (Ansell, 2014; Callaghan, 2015; Harmes, 2001; Langley, 2014). They also extend work emphasizing how this “democratization of finance,” often associated with a new policy narrative of individual self-responsibility for embracing and managing life cycle risks, has a tendency to disappoint (Erturk et al., 2007; Langley, 2009). Voters strongly resist the idea that they should accept personal responsibility for wealth losses in an era of great expectations.

Our findings are inconsistent with the argument that “democratic governments, constrained as they are by links of electoral accountability, are more cautious in implementing costly policies that are ultimately shouldered by taxpayers” (Rosas, 2009, p. 4). 3 This claim overlooks the dynamic forces we identify that have weakened the democratic constraint on bailouts. Great expectations effectively place modern governments under a very different standard of democratic accountability by requiring them to compromise minimizing taxpayer liability in systemic banking crises in favor of bailouts aimed at wealth protection. They thus raise doubts concerning the general claim that democratic institutions promote fiscal credibility (North & Thomas, 1973; North & Weingast, 1989).

In the next section, we elaborate our argument. We then present the new data set and the results of our statistical analysis. We conclude by considering the implications for how we can understand evolving political cleavages.

Banking Crises and Policy Responses in Democracies

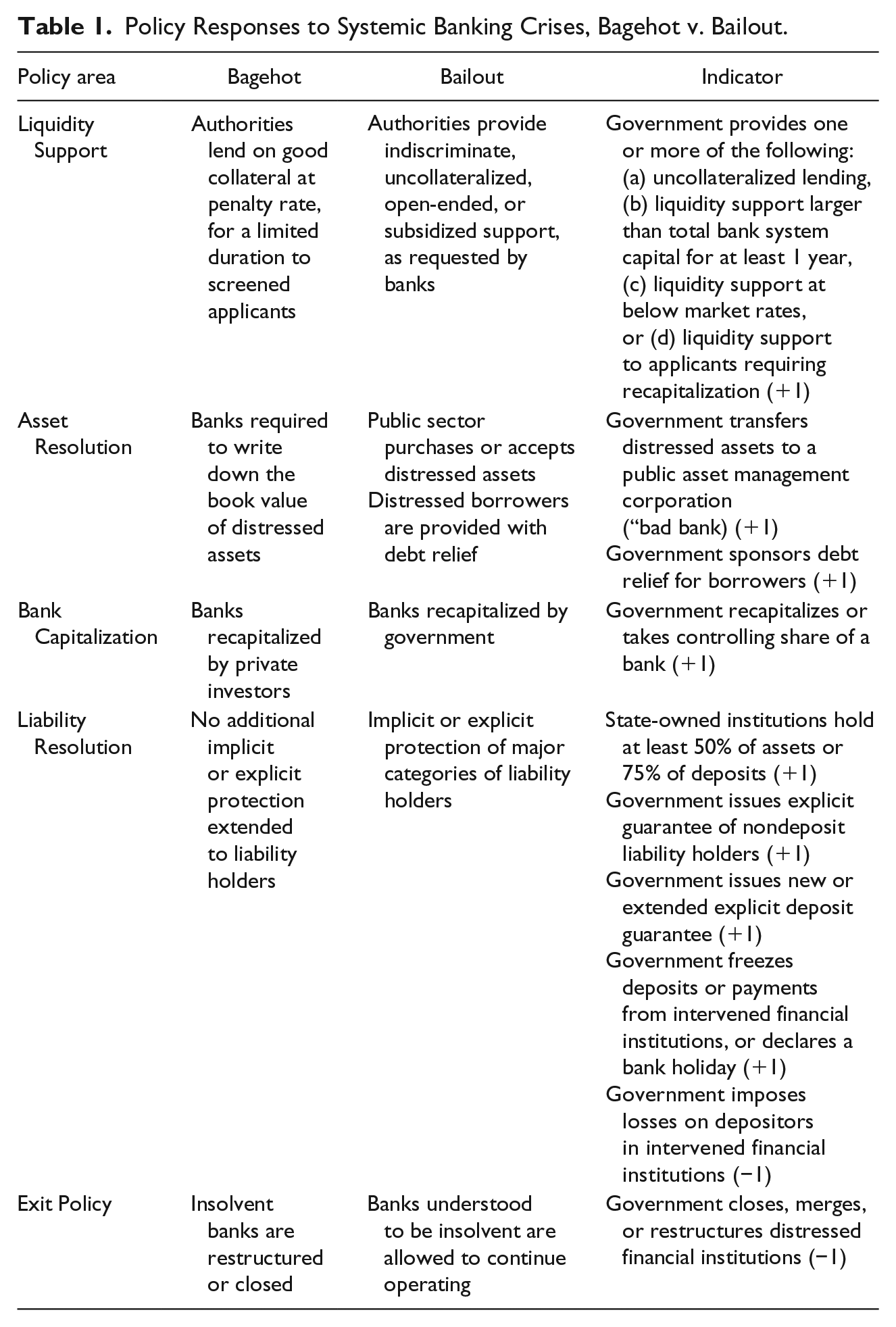

We can conceptualize policy responses to banking crises as mapping onto an abstract continuum ranging from no government intervention to complete government socialization of all banking sector losses. We label the first pole of this continuum the Market pole and the second the Socialization pole. Both poles are ideal types and in practice policy responses often fall between them, approximating what Rosas (2009) summarized as “Bagehot” and “Bailout” (Figure 1).

Conceptualizing policy responses to banking crises.

A “Bagehot” model conforms with Walter Bagehot’s (1873/1962) doctrine of crisis resolution, which called for central banks to provide lender of last resort facilities (LOLR) to solvent banks by “freely advancing on what in ordinary times is reckoned a good security” (p. 97). Such lending should be unlimited but at “penalty” interest rates in return for good collateral, to ensure that the government was not subsidizing banks in need.

Bagehot defined bank solvency in reference to “ordinary times” to indicate that the LOLR is needed only when there is some uncertainty about solvency and implies the possibility of taxpayer loss (Goodhart, 1999, pp. 347–352). LOLR support diverges from the pure Market pole in that it involves policy intervention to prevent ordinarily solvent and illiquid banks from failing. It places the burden of permanent insolvency on banks, their shareholders and related creditors rather than on taxpayers and thus can also entail enforcing the closure of insolvent banks, forcing write-downs of banks’ nonperforming loans (NPLs), permitting their recapitalization by private investors, and protecting few if any depositors.

A “Bailout” response falls closer to the Socialization pole as it involves the use of taxpayer resources that delay the closure of banks that are almost certainly insolvent in “normal” times. Even so, as these policies may entail some bank closures or private sector losses, they often differ from the pure Socialization pole. Thus, the main conceptual differences between a Bagehot and a Bailout policy response lies in the intention of the government in providing support to banks, in the targets of support, and ultimately in the willingness to impose (in the latter case) a much higher probability of loss on taxpayers.

Which factors shape the actual policy choices governments make during crises? We focus on the role of competing societal preferences under democratic competition. Arguments that democracy curbs bailouts privilege the role of taxpayer interests, assuming that governments try to resolve bank insolvency at minimum fiscal cost, resisting narrow interests favoring the socialization of their losses (Rosas, 2009). Public sector beneficiaries also have a broad interest in minimizing the fiscal cost of banking crisis interventions to avoid austerity. Both groups have grown in relative size since the early 20th century with the expansion of the national tax base and the welfare state.

However, we expect relatively weak support for Bagehot policies from these groups. First, bailout costs are widely distributed (Rosas, 2009, p. 8). By contrast, the benefits of bailouts—as well as the costs of Bagehot policies that might be imposed—are relatively concentrated. Second, as the full costs of bailouts are often highly uncertain in the short term, those actors who might lose from them often do not face strong incentives to oppose them at the time of adoption. Third, even those actors with most to lose often have composite interests as savers, investors and (sometimes) firms, diminishing their incentives to oppose bailouts. Fourth, elites might reduce opposition to bailouts by arguing that only by intervening in the short term can longer term public costs be minimized.

We argue that the wealth effect has given much of the middle-class stronger interests in and, importantly, preferences for bailout policies during crises. 4 The primary driver of the evolution in middle-class household interests has been the spectacular long-run growth in this sector’s wealth and its increasing connection to complex financial markets. Bank failures not only threaten those with deposits in distressed banks, they also now potentially affect a much wider group holding market-traded assets such as housing and pensions. In describing these changing interests, we distinguish between a size effect—rising average household wealth—and a composition effect—rising exposure to market-traded assets and growing financial inclusion, including via leverage. Finally, we argue that evolving government policy commitments, changing knowledge and media commentary, and political opportunism have all helped to modify voters’ policy preferences—in summary, creating “great expectations.”

The Financialization of Wealth

Households and firms have become increasingly dependent on the many services provided by major banks at the core of the financial network. Savers, especially in developed countries, have steadily accumulated wealth that is increasingly connected with financial markets, including bank deposits, stocks, bonds, and houses (Crouch, 2009; Finlayson, 2009; Langley, 2009; Muellbauer, 2008, pp. 293–294; Nesvetailova & Palan, 2013; Watson, 2007). As household wealth portfolios have shifted toward more volatile, market-traded assets such as leveraged housing equity and defined contribution (DC) pensions, householder anxiety concerning the value of their total wealth has likely increased over time (Watson, 2007). Even in emerging and developing countries, rising financial inclusion has linked a larger proportion of the population to the financial system (Demirgüç-Kunt & Klapper, 2012; World Bank, 2014). Financialization has also been connected to changing welfare provision, the acquisition of status goods such as housing, rising inequality, and growing reliance on credit (Ahlquist & Ansell, 2017; Frank, 2013; Rajan, 2010). In short, households now have far more to lose from financial crashes.

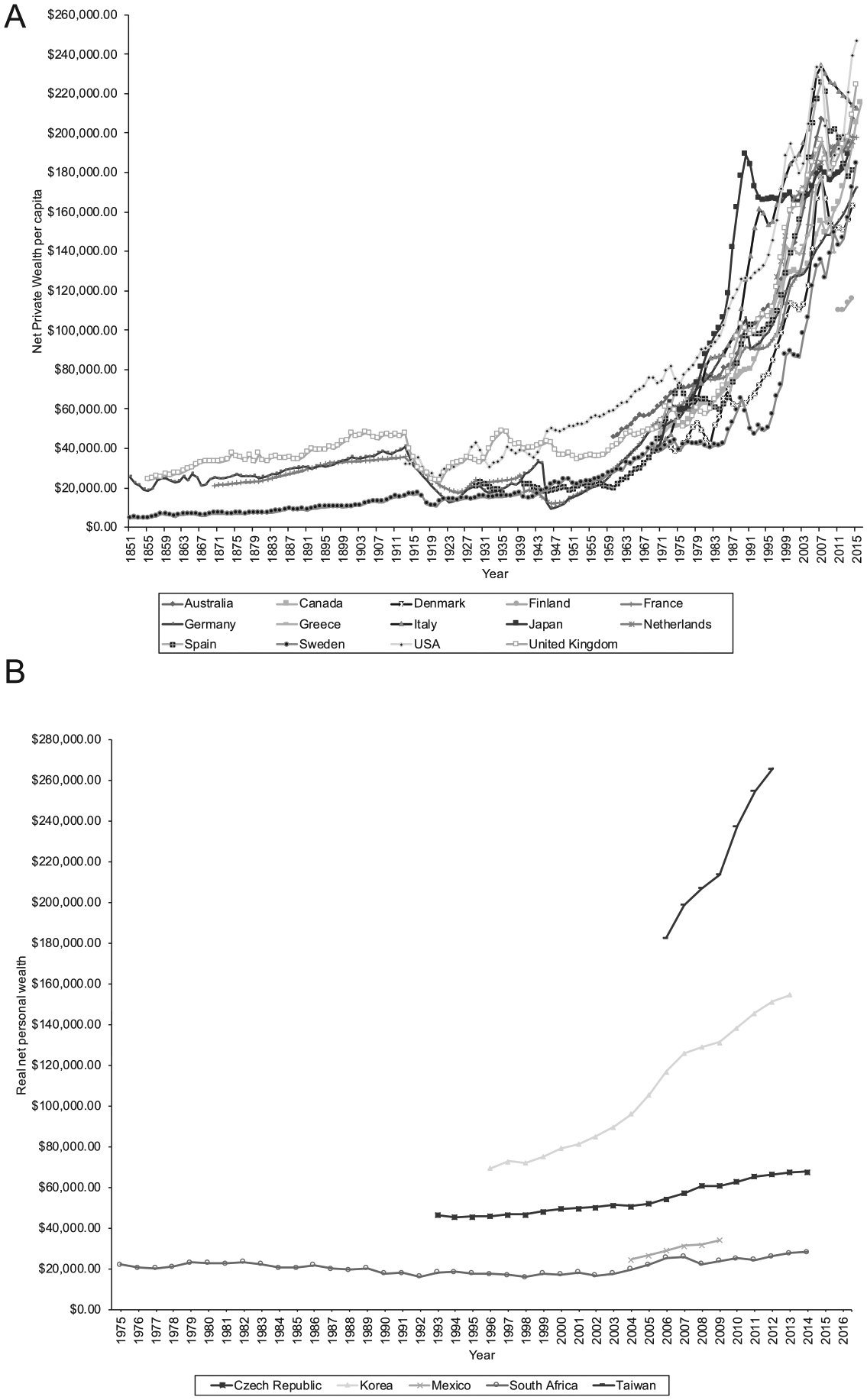

Figures 2A and 2B, which use available data to plot real net private wealth per capita wealth in many advanced and some emerging market economies, show just how dramatic the increase in average real private sector wealth—the size effect—has been since 1970 for many countries. 5

(A) Net private real wealth per capita in advanced countries, PPP exchange rates, and constant 2016 US$, 1850–2016 and (B) net private real wealth per capita in emerging countries, PPP exchange rates, and constant 2016 US$, 1975–2016.

Long-run estimates of wealth shares are unfortunately very sparse but those available suggest that wealth was highly concentrated before 1940. Piketty and Saez estimate that in the 70 years following 1870, the wealthiest 10% of households owned between 70% and 90% of all wealth in Europe and the United States, with the middle 40% of wealth-holders (the 50th to 90th percentiles of the wealth distribution) owning less than 5% (Piketty & Saez, 2014, p. 839). 6 Extreme wealth concentration meant that the richest decile was far more vulnerable than other groups to asset price collapses in the aftermath of banking crises. However, available evidence indicates that although wealth remained very unequally distributed thereafter, the share and the aggregate wealth holdings of the middle class in advanced economies expanded dramatically after the interwar period. Similarly, in India, the only nonadvanced democracy with repeated household wealth surveys in the post-war era, the middle-class share has more than doubled since the 1980s (Subramanian & Jayaraj, 2008). This evidence is corroborated by sharp increases in rates of home ownership and pensions in many countries since 1945, suggesting strongly that the real increases in per capita wealth indicated in Figure 2 substantially accrued to the middle class.

Middle-class wealth portfolios are also subject to growing risk—the composition effect. Home ownership rates rose substantially over the course of the 20th century, especially among the middle class (European Central Bank, 2013, 2016; Guiso et al., 2003; Jordà, Schularick, & Taylor, 2017; Kuhn et al., 2017; Piketty & Zucman, 2014, pp. 1280–1281; United Nations Human Settlements Program, 2006). Middle-class wealth in emerging countries is also concentrated in housing, though increasingly too in bank deposits and in some cases riskier market-traded assets (Aron et al., 2008; European Central Bank, 2013, 2016; Honohan, 2008; Subramanian & Jayaraj, 2008; Torche & Spilerman, 2008).

By the early 2000s, the proportion of households in advanced countries with direct or indirect ownership of stocks had grown significantly, reaching nearly 50% in the United States, roughly one third in Britain and the Netherlands, and nearly one fifth in France, Germany and Italy (Guiso et al., 2003, p. 9). Ownership of riskier financial assets among households in advanced economies increases significantly from the fifth decile of wealth distribution upward, as does the share of such assets in the overall wealth portfolio (European Central Bank, 2016, p. 28). This is especially true in emerging markets and developing countries, where (based on the limited data available) holdings of risky financial assets below the top 5% of wealth-holders are probably often negligible (Honohan, 2008).

The pension assets of the middle class have grown sharply in many countries since 1945. Furthermore, since the 1970s, there has been a growing policy trend toward promoting private pensions (Brooks, 2005, 2007; Organisation for Economic Co-operation and Development [OECD], 2015) and more recently a move away from defined benefit (DB) pensions toward DC schemes. These policies shift financial risk onto individuals and increase their incentive to monitor the market value of their pension assets (Pallares-Miralles et al., 2012).

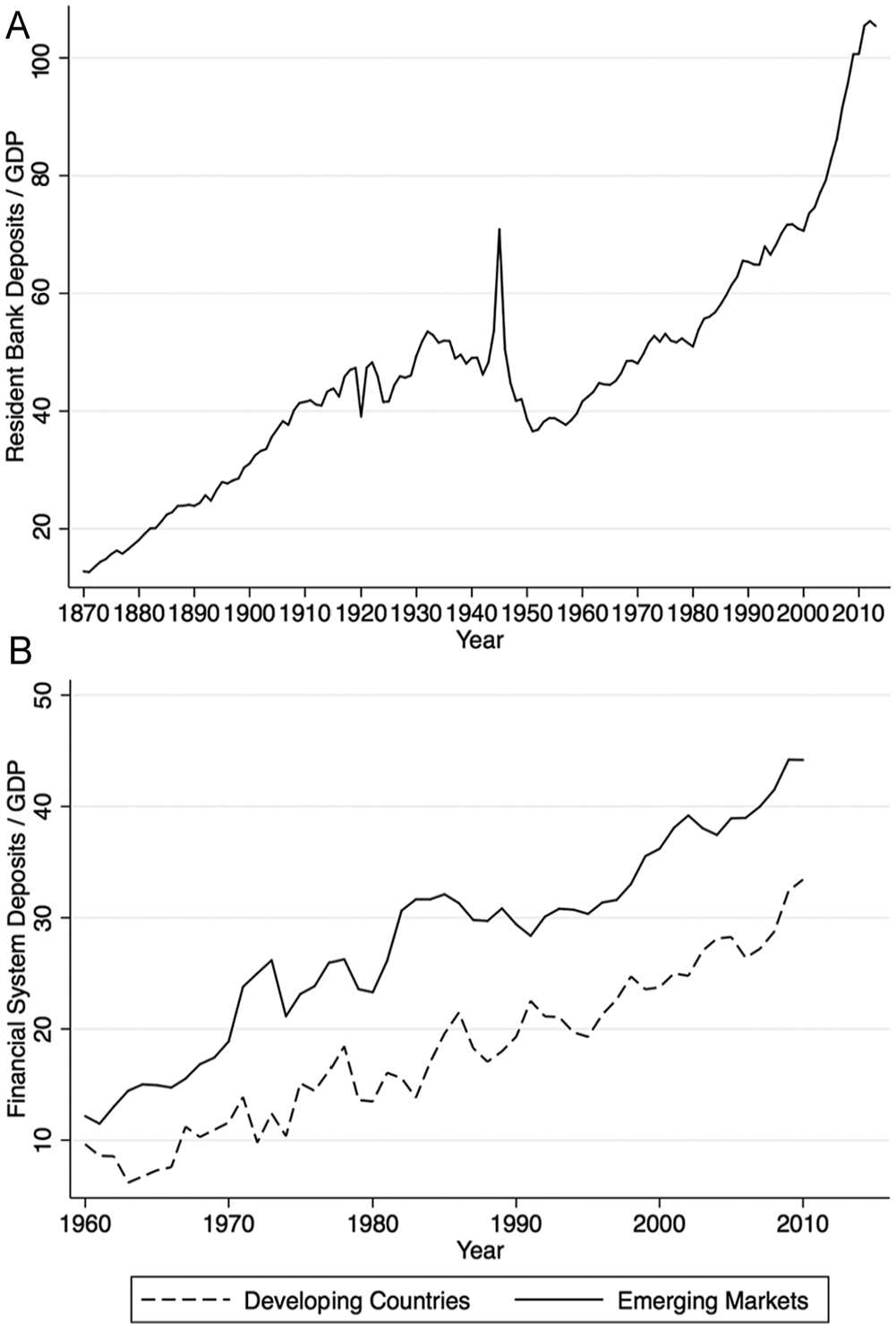

Finally, a sizable fraction of wealth is still held in bank deposits, which have also grown significantly in advanced, emerging, and developing economies since the 1970s—though in the latter two cases the aggregate levels lag considerably behind those attained in advanced countries (Figure 3A and 3B). Among advanced countries, a downward trend in the relative weight of deposits in household portfolios is evident since the 1970s, with a corresponding shift toward riskier assets (Federal Reserve Board, 2017). In emerging and developing countries, access to financial institutions and private credit to gross domestic product (GDP) ratios have generally risen since the 1970s, implying a corresponding increase in the share of households with accounts at financial institutions (Svirydzenka, 2016; World Bank, 2015).

(A) Total domestic deposits by nonfinancial residents/GDP in advanced economies, 1870–2010 and (B) total financial system deposits/GDP in emerging market and developing country democracies, 1960–2010.

The Democratization of Leverage

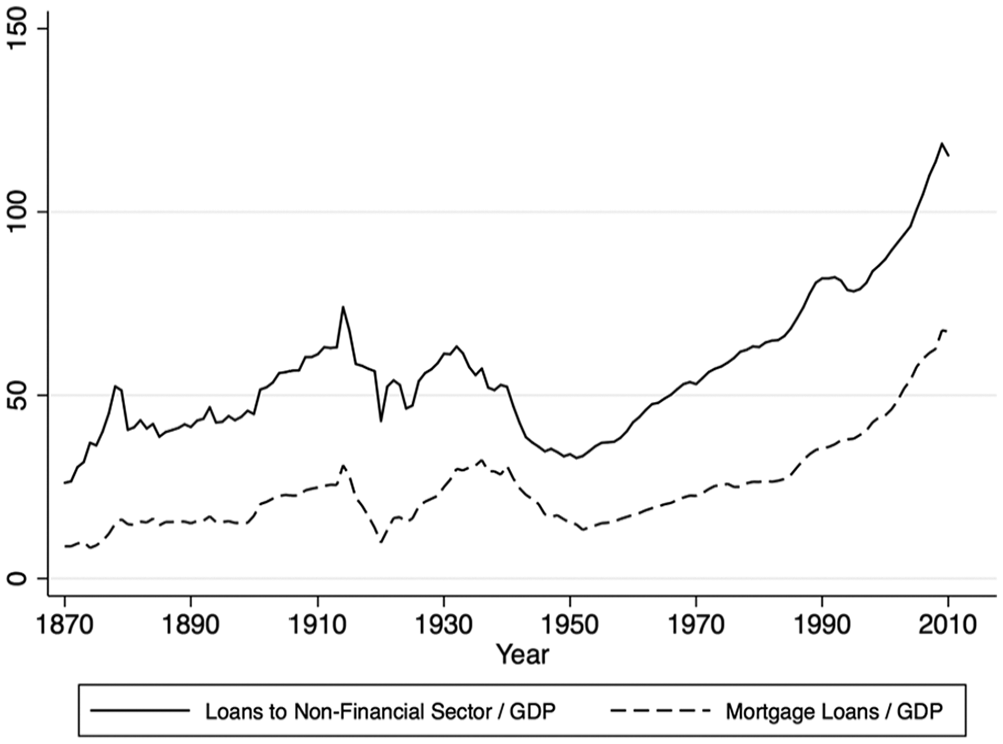

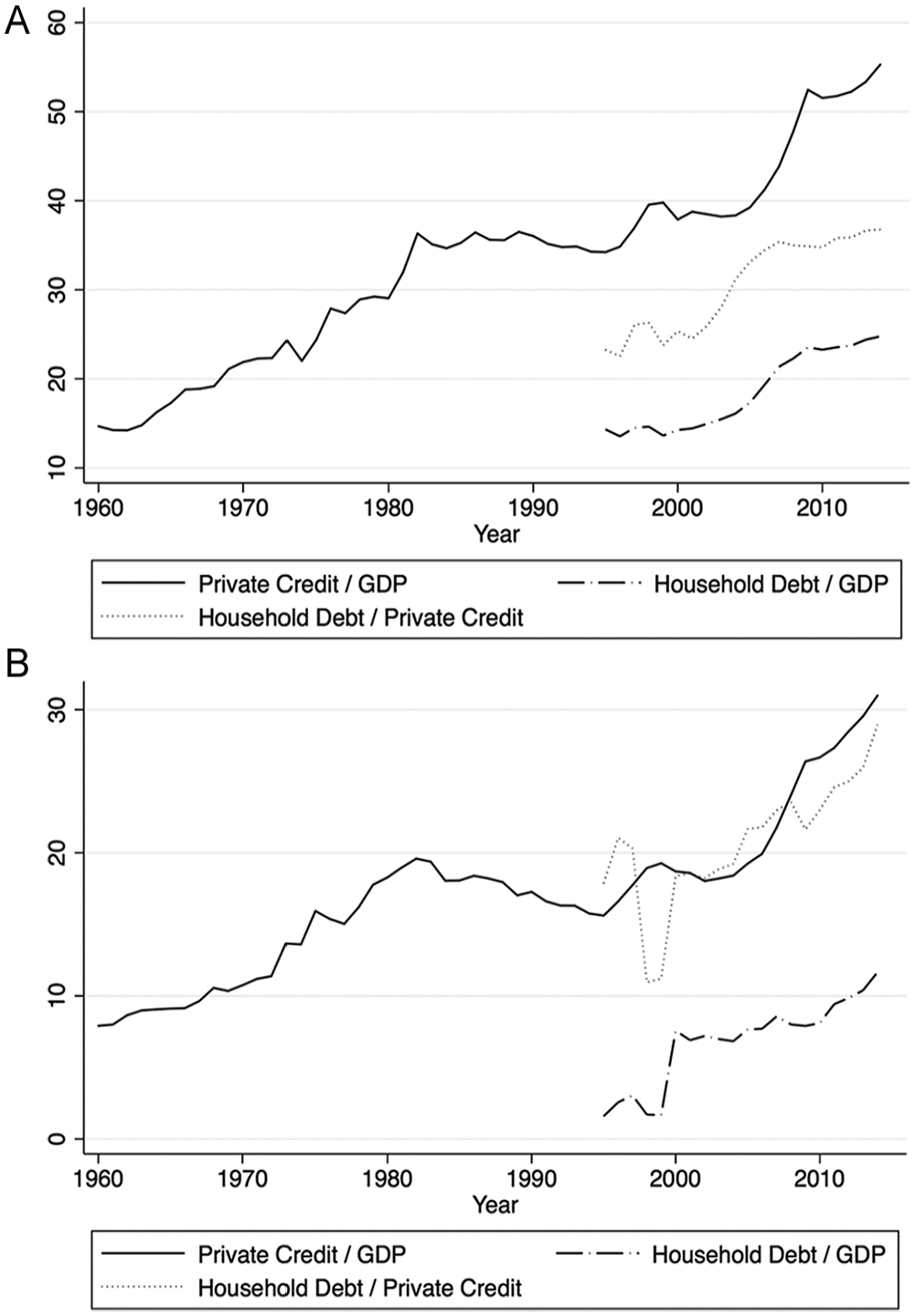

Rising household leverage has also heightened many voters’ interest in financial stabilization. Increasingly, lower and middle-income households borrow to finance consumer purchases. Mortgage lending grew especially rapidly after 1945 in advanced countries (Figure 4), aptly described as “the democratization of leverage” (Jordà et al., 2014). By 2011, the median share of mortgages in household debt for a broad set of countries was about 70% (Cerutti et al., 2015). Credit dependence among households in many emerging and developing countries has also grown, though levels remain considerably below those in advanced economies (Badev et al., 2014; Beck et al., 2012; see Figure 5A and 5B).

Total bank lending and mortgage lending in advanced democracies, 1870–2010.

(A) Private sector credit and household debt in emerging markets, 1960–2015 and (B) private sector credit and household debt in developing countries, 1960–2015.

Greater access to credit has come at the significant cost of rising household leverage and financial fragility, with a risk of substantial wealth losses if asset prices fall (Admati & Hellwig, 2013; Goodhart & Erfurth, 2014; International Monetary Fund [IMF], 2017; Jordà et al., 2015, 2016). In advanced countries, lower and middle-income households of preretirement age are most dependent on credit to acquire housing assets and to maintain consumption, whereas those in emerging markets and developing countries increasingly rely upon it to purchase marketized and expensive services, such as education and health care (Frank, 2013, chap. 5; Kuhn et al., 2017; Offer, 2014; Rajan, 2010). Processes of financialization and rising leverage common to many economies mean such households now have a stronger interest in the bailouts that would maintain the flow of credit during and following a crisis.

From Interests to Great Expectations

Do middle-class voters perceive government policy interventions as a means to protect the value of their assets during crises? Have they gradually acquired corresponding policy preferences that induce governments to respond with more bailouts? We think it is plausible that such preferences emerged after the 1930s and especially during the era of financialization. This claim is no less plausible than the common assumption in the economic voting literature that voters understand that unemployment affects their welfare and that governments have the means to manage business cycles. Indeed, much is now at stake for many modern middle-class households, who have simultaneously acquired highly leveraged housing equity and large at-risk pension assets while facing large and uncertain future health care, retirement and other liabilities. This has prompted rising middle-class anxiety, deepening, as Watson (2007) puts it, “the impression that more is now a stake than ever before when the pricing structure of financial markets looks likely to break down (p. 3)” The argument that this strongly influences political choices is consistent with the growing literature on “patrimonial voting,” which finds that asset ownership does shape voter preferences (Lewis-Beck et al., 2013; Persson & Martinsson, 2018).

There are further reasons for this expectation beyond the specific circumstances of increasingly vulnerable households. As financial firm size and interconnectedness have grown, the ability of private sector actors to support insolvent banks has diminished. This has left the state, with its unique taxation and borrowing capacity, as the residual guarantor in a systemic crisis. Moreover, the experience of deep banking crises and policy mismanagement in the 1930s led to new understandings about the role of government in financial stabilization (Berman, 2006; Eichengreen, 1992). Before the mid-20th century, most governments made very limited if any policy commitments to promote financial stability (R. S. Grossman, 2010; Schenk, 2016). After this time, governments made explicit pledges to voters to take new measures to stabilize the financial sector, including prudential regulation and implicit commitments arising from extensive state control of the banking system (Allen et al., 1938; Busch, 2009; Helleiner, 1994, pp. 25–50). 7 These new policy orientations also visibly worked. The virtual absence of banking crises in the three decades after 1945 likely reinforced voter expectations of financial stability as a politically achievable condition.

Although it would be unrealistic to expect that most voters understood the technical details of innovations in financial stabilization policy, it is not unreasonable to believe that they took notice of this broad policy reorientation and the high level of financial stability in the three postwar decades when substantial assets were being accumulated. The rapid expansion of secondary and tertiary education rates for middle-class adults in these decades provides one reason (Lee & Lee, 2016).

More importantly, we need not assume high levels of sophistication for most voters. At least as much as in “normal” recessions, the media and opportunistic politicians have strong incentives to seize on rising voter anxieties about threats to their wealth to focus their attention on government policy responsibilities during systemic banking crises. Kayser and Peress (2012) have pointed to how the media and opposition politicians provide voters facing falls in employment income during recessions with easily digestible benchmarking of national policy and economic outcomes relative to other countries. To the extent policy benchmarking also occurs during banking crises, it could promote spatial policy diffusion, a possibility we address in the empirical analysis.

Is there evidence to support our argument that modern voters have acquired great expectations? National household surveys undertaken in multiple waves in the United Kingdom from 2003 to 2007 showed that over 55% of respondents with an opinion on the matter held the view that, in a crisis, the authorities would bail out some or all failing financial firms (Financial Services Authority, 2009, p. 26). A potential problem in interpreting these results is that some respondents may have expected bailouts because of the economic and political importance of Britain’s financial sector rather than reflecting personal preference. However, when first asked in 2007 to explain this view, the main reason (18%) given was “too many consumers would be affected” in addition to “people would lose confidence in the financial system” (6%) and “government would never allow consumers to lose money” (5%). Similarly, a Dutch survey in 2010 also found that nearly two thirds of respondents agreed that supervisors must ensure that banks never go bankrupt. It is arguably more revealing of individual preferences that three quarters of respondents incorrectly assumed that supervisors will refund any deposits when a bank goes bankrupt. A substantial majority (59%) also believed that supervisors had to ensure swift reimbursement of guaranteed savings when a bank fails. Whereas 80% of respondents expected reimbursal in 3 days, the average repayment period in the Netherlands is 3 months (van der Cruijsen et al., 2013, 228).

Another potential problem with such survey results is that they could reflect a general expectation of rising government intervention in market economies. However, this possibility is not reflected in the multiple waves of the cross-national World Values Survey since 1981, which do not indicate a general rising trend among respondents that governments will intervene more (see online appendix). Furthermore, Ansell (2014) finds evidence that homeowners experiencing house price appreciation generally become less supportive of redistribution and social insurance policies. This suggests that the shift in voter expectations we identify may be issue-specific and due more to the wealth effect we emphasize.

Elsewhere, we also undertook an extensive coding of the content of national newspaper editorials discussing government policy options during systemic banking crises since the 19th century in three countries (Brazil, the United Kingdom, and the United States). This reveals two important findings consistent with our argument: first, that there was a rising tendency for editorialists to discuss intra-crisis policy interventions over the course of the 20th century, and second, that in all three countries they shifted from a stance of supporting market-conforming/Bagehot policies to favoring bailouts (Chwieroth & Walter, 2019, pp. 118–160). Such commentary can both reflect and inform voter opinion. A recent study of British media coverage of the 2007–2009 crisis found that while

many people struggled to understand the crisis . . . the media were important in establishing [key] aspects of audience belief such as the view that the part-nationalisations [of banks] had been the “only option” and that the key issue was reforming bankers’ pay structures. (Berry, 2019, p. 111)

Policy benchmarking by the media in modern crises also seems considerable. As one indication, Kayser and Peress (2012, p. 681) provide evidence that benchmarked postcrisis economic performance accounts for the surprising fact that some incumbent parties increased their vote share during the 2008–2009 financial crisis.

In addition, opportunistic politicians in recent crises highlighted the role of government in financial stabilization during modern banking crises far more than in pre-1945 crises. For example, in the United Kingdom over 2007–2008, the opposition Conservative and Liberal Democratic parties moved quickly to support public intervention to stabilize the financial system while distancing themselves from the banks and criticizing the government for the ineffectiveness and unfairness of their policies (Darling, 2011, pp. 54, 68, 174). This was also true of the Democrats in the United States under the George W. Bush administration, where majority public opinion supported financial stabilization measures but—as in Britain—also reflected strong resentment at the need to rescue wealthy bankers (Pew Research Center, 2008; Smith, 2014, p. 105). This prompted a direct appeal to voters by Bush, who said that although he understood why ordinary people abhorred a bailout, “not passing a bill now would cost these Americans much more later” (“President Bush’s Speech to the Nation on the Economic Crisis,” 2008). Members of Congress began receiving calls from constituents concerned about their life savings, which seems to have induced some to support the revised bill (Geithner, 2015, p. 221; McCarty et al., 2013, pp. 234–237; Morales, 2008). 8 By contrast, most opposition Democrats in the deep 1907 U.S. crisis opposed government financial stabilization measures. 9 Even as late as 1931–1932, Congressional Democrats were mainly pushing measures to encourage the Federal Reserve to provide liquidity consistent with the Bagehot rule (Meltzer, 2010, p. 347).

Thus, there is considerable evidence to support our expectation that elected politicians have come to understand that many voters now have a strong stake in financial stability, expect stabilization measures in crises, but are also very attentive to the perceived fairness of interventions. With these changed expectations, voter assessments of government competence plausibly also became more closely associated with the provision of financial stability.

Our argument does not depend on the empirical claim that crises have become deeper over time. By investigating systemic crises of a similar potential magnitude in our empirical analysis, we seek to rule out this possibility. Nevertheless, rising financialization and leverage have probably had the additional effect of intensifying banking crises by increasing systemic risk, shifting voter support further toward bailouts.

Government Policy Responses: Conceptualization and Measurement

Previous analyses of bank bailouts largely investigate either fiscal cost measurements (Gandrud & Hallerberg, 2015; E. Grossman & Woll, 2014; Honohan & Klingebiel, 2000; Keefer, 2007) or a limited number of policy responses (Culpepper & Reinke, 2014; Weber & Schmitz, 2011). These modeling decisions may not always be appropriate. Fiscal costs can take many years to be determined, some policy responses generate uncertain contingent liabilities (Gandrud & Hallerberg, 2015), and they are influenced by economic outcomes that flow from policy choices. The drawback of limiting the focus to a narrow set of policy indicators is that government responses to crises typically encompass a wide range of policies that can be substitutes or complements.

Thus, like Rosas, we classify different microeconomic policy measures according to whether they prevent insolvent banks from failing (bailouts) or instead support only illiquid banks, ensuring that insolvent bank losses are crystallized and borne by their investors, other creditors and employees (Bagehot measures). Our aim is to measure the overall tendency for governments to conform to either ideal type in their response to banking crises. We identify five policy areas crucial to classifying policy responses: Liquidity Support, Liability Resolution, Asset Resolution, Bank Capitalization, and Bank Exit.

Table 1 briefly summarizes in each case the response that a government pursuing a coherent Bagehot or Bailout strategy would enact. We provide more detail in the online appendix. The leftmost column identifies the five policy areas. The entries in the inner two columns, respectively, describe policy measures consistent with a Bagehot or Bailout strategy. Entries in the rightmost column refer to the binary indicators used for each policy area.

Policy Responses to Systemic Banking Crises, Bagehot v. Bailout.

For these indicators we draw on and greatly extend the dataset compiled by Honohan and Klingebiel—also the principal data source for Rosas—who compile and code government policy responses to crises observed during 1970–2000 (Honohan & Klingebiel, 2000). 10 Using a wider range of sources, we code policies consistent with the Bailout ideal type as “+1” and code those policies consistent with the Bagehot ideal type as “−1.” Liquidity Support, for instance, is coded as +1 where we observe indiscriminate, uncollateralized, open-ended, or subsidized liquidity support consistent with a Bailout response. As another example, Liability Resolution is coded as −1 where we observe losses imposed on depositors consistent with a Bagehot response. We consider all policy measures implemented within a 3-year period after the end of the crisis window, producing an aggregate score that abstracts from any variation in policy during the time-window. 11

Our primary banking crisis measure is from Reinhart and Rogoff (R&R), who provide the most comprehensive data on crises since the early 19th century (Reinhart, 2010; Reinhart & Rogoff, 2009). Their measure offers an expansive definition, identifying banking crises whenever there is any distress in the banking system. We focus only on identified episodes of systemic banking crises so as to investigate policy responses only in severe crises. 12 We also consider a measure from Laeven and Valencia (L&V, 2008, 2013). It extends from 1970 to 2011, covering only systemic crises in nearly twice as many countries. We use both data sets to produce two sets of policy responses, using the R&R crisis dating for the pre-1970 period in both sets.

We identify democracies using data from Boix et al. (2014). Importantly, in addition to free and fair contestation, this dichotomous measure of democracy requires countries to meet a minimal suffrage requirement, defined as a majority of the male adult population—a criterion omitted from many alternatives such as the Polity data set. In using this measure we aim to rule out possible objections that changing policy responses may be due to suffrage expansion alone. We also consider an alternative sample of democracies from the Polity data set, following the convention of defining a country as democratic if its summary regime type score is above 6 during the crisis spell (Marshall et al., 2017).

Our analysis begins with the raw data, with crisis start dates from 1848 to 2008. We record responses to 38 crises in 17 democracies in the pre-1945 era. 13 There are no systemic crises during 1945–1970, a period of unusual tranquility. In the post-1970 era, we record responses to 54 crises in 41 democracies using the R&R measure, and 74 crises in 58 democracies using the L&V measure.

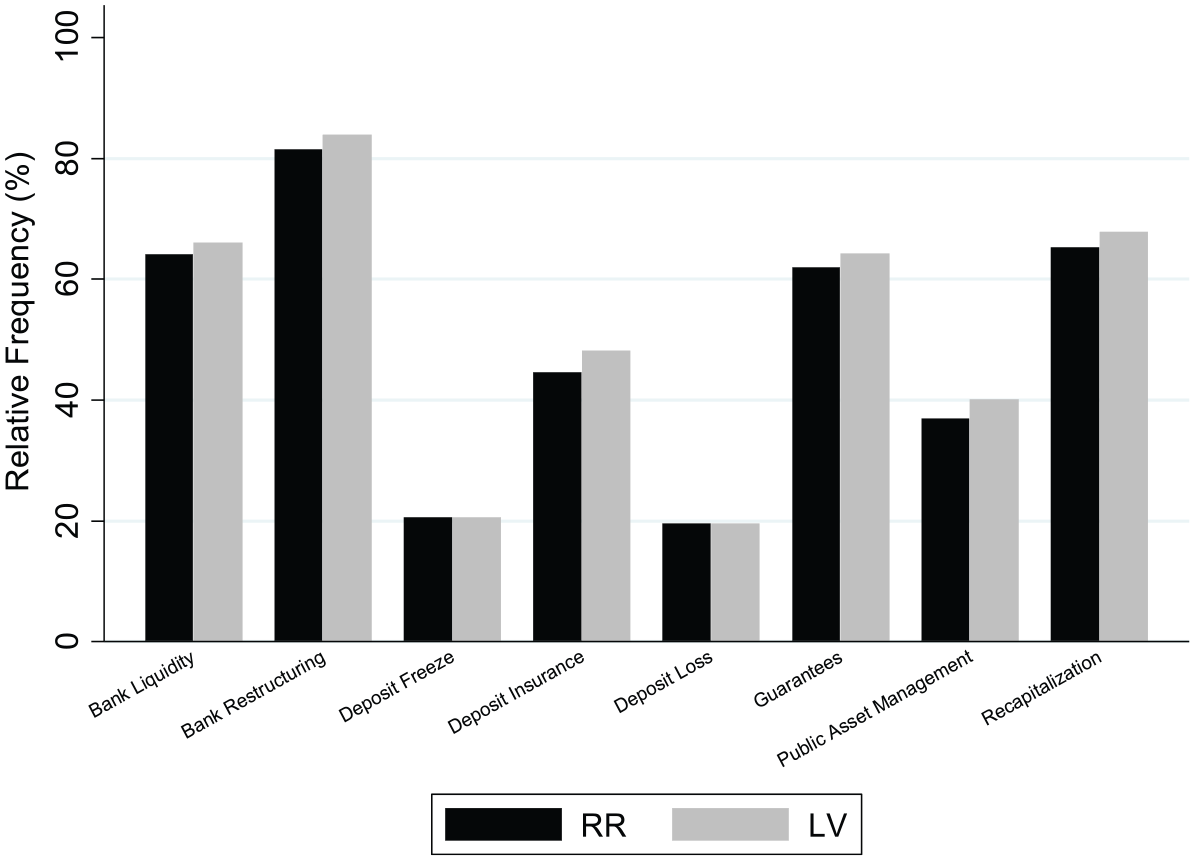

Figure 6, which plots the relative frequency of each of the policy response indicators, reports similar values for each data set. It shows that Bank Restructuring and indiscriminate, uncollateralized, open-ended, or subsidized liquidity support are the two of the most commonly used policy responses since 1848, occurring in about 80% and two thirds of all crises, respectively. It is notable that liquidity support going well beyond the Bagehot model was extended in crises during the gold standard era and in countries lacking central banks and possessing laws prohibiting liquidity provision by the government. Guarantees and public recapitalizations are also common policy responses following a crisis, occurring in about three fifths and two thirds of cases, respectively. Protection for depositors—either via the creation of new insurance arrangements or the extension of existing schemes—is the next most frequently observed response, featuring in nearly half of all crisis episodes, but with the exception of the United States during the Great Depression, was conspicuously absent in all other crises in the pre-1939 era. Public Asset Management features in about 40% of crisis episodes and is also largely a post-1970 phenomenon. Deposit freezes, bank holidays, and payment suspensions as well as deposit losses are relatively infrequent, occurring in one fifth of crisis episodes.

Relative frequency of crisis policy responses, 1848–2008.

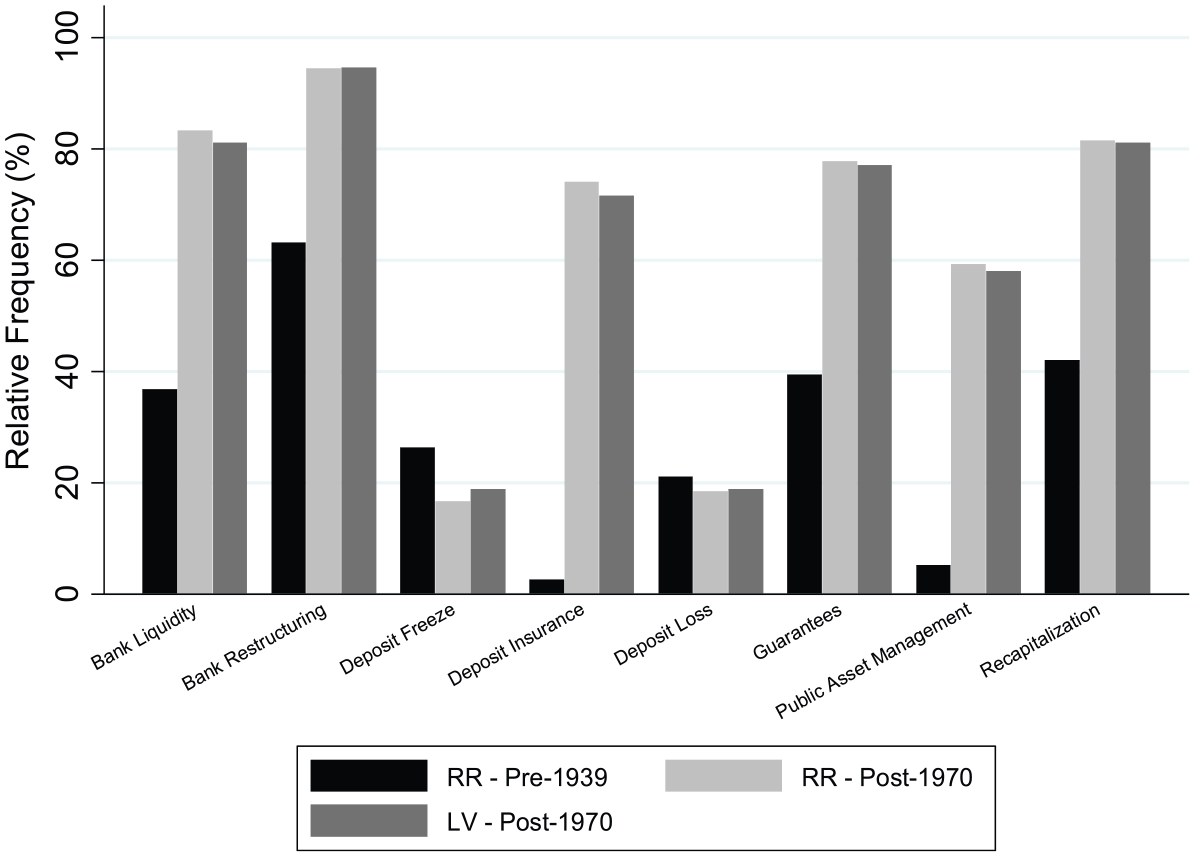

Our argument leads us to expect governments to rely more heavily on bailout policy interventions during major crises after 1970 compared with the 1939 era. Figure 7, which compares the relative frequency across both time periods for each of the policy response indicators, provides some supportive evidence, as do a series of difference of proportions tests. Post-1970 governments provided indiscriminate, uncollateralized, open-ended, or subsidized liquidity support, guarantees, and recapitalizations roughly twice as often as governments in the pre-1939 era. As suggested earlier, the most striking difference is in the use of deposit insurance and public asset management measures, which with bank restructuring were used much more frequently in the post-1970 period. We find no significant differences for the remaining policy response indicators across the two time periods.

Relative frequency of crisis policy responses, pre-1939 versus post-1970.

Our data suggest that governments typically implement an array of responses to crises. For instance, open-ended liquidity support may be provided while a government restructures and closes insolvent banks. Bank restructuring and closures often take place alongside recapitalizations and guarantees. The raw data do not reveal such correlations and potentially exaggerate the dimensionality of the data. Thus, our preferred measure of the overall tenor of government policy responses is the first principal component of our eight indicators. It indicates how policy responses covary as they move between the Market and Socialization poles, enabling us to assess the extent to which particular governments approximate Bagehot and Bailout ideal types.

This index, constructed from the R&R crisis data, ranges from −2.59 to 2.52. Higher (lower) values of this index indicate more coherent Bailout (Bagehot) policies. The index generated from the L&V data ranges from −2.78 to 2.35. Our analysis of the R&R data shows that the first principal component is strongly correlated (in order of importance) with Recapitalization, indiscriminate, uncollateralized, open-ended, or subsidized Liquidity Support, Deposit Insurance, and Public Asset Management; Guarantees have moderately high correlations. This suggests that these five policy indicators vary together. Deposit Freezes have almost no correlation with the first principal component. Not surprisingly, Bank Restructuring has a moderately high negative correlation and Deposit Loss a weakly negative correlation. The direction and magnitude for all the policy indicator correlations are broadly similar for the L&V data.

This suggests that the first principal component can be viewed as a measure of the coherence of the Bailout response. The principal component scores that comprise our policy response index show that cases with positive scores will tend to have greater values on indicators associated with delaying the exit of clearly insolvent banks (Recapitalization, Extensive Liquidity, Deposit Insurance, Public Asset Management, and Guarantees) and lower values for the indicators related to minimizing the taxpayer burden (Bank Restructuring and Deposit Losses). The opposite is the case for negative policy response index scores.

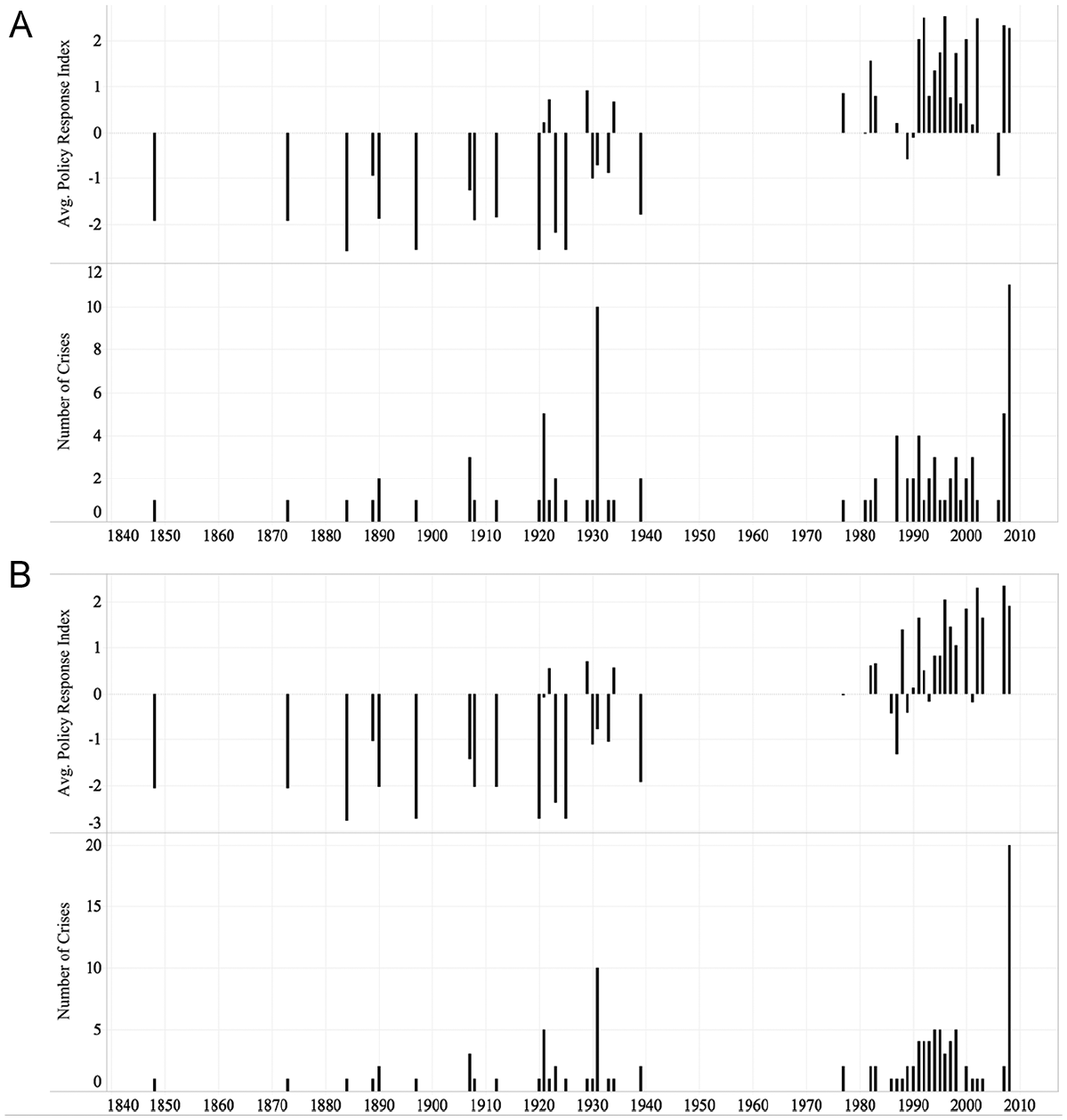

Figures 8A and 8B plot the relationship between the average crisis policy response and the number of systemic banking crises for democracies since 1848, using the R&R and L&V data, respectively. We find that bailout interventions before 1945 were infrequent, whereas by the 1990s they had become the norm. Before 1945 most of the small number of bailout cases are found in the interwar period, suggesting it was a transitional era, but one in which Bagehot responses were still dominant, representing roughly 70% of the 26 crisis episodes. For both data sets, the average measures of policy responses in the pre-war era (−1.06 on the R&R index, −1.21 on the L&V index) diverge substantially from those in the post-1970 period (1.37 and 1.15, respectively), with a difference of means that is statistically significant (t = 9.23 and t = 9.57, p < .001).

Banking crises policy responses, 1848–2008: (A) R&R sample and (B) L&V sample.

This rising tendency for bailouts is consistent with our argument that governments have increasingly aimed to protect household wealth in crises. We observe a sharp departure from pre-war policy norms since the mid-1970s, especially regarding government deposit insurance, public bank recapitalization, and government assumption of distressed assets and debts. As Figure 7 showed, these critical features of bailout interventions were used prominently in the vast majority of post-1970 systemic crises in democracies.

Empirical Tests of the Argument

We now proceed to empirical tests of our argument, providing further detail on our data sources in the online appendix. We begin with the financialization of wealth and the rising stake of households in the stabilization of the market value of housing and financial assets. Because data on household asset ownership and wealth portfolio composition are unavailable over a long period, we instead use aggregate wealth data to assess this mechanism.

For housing assets, we utilize the level of residential property prices as it helps to capture the extent of housing equity wealth within a country. 14 Higher property prices would suggest that households have more to lose if faced with a sudden evaporation of their property wealth, thus prompting more intense effective societal demand for intervention. We link two different national house price indices, setting the base of the new consolidated series to 100 in 2010 (Bank for International Settlements, 2017b; Knoll et al., 2017).

As regards financial wealth, we consider domestic deposits and ownership of DC pension assets. We measure the importance of household deposits using two different national series (Jorda, Richter, Schularick, & Taylor (2017); World Bank, 2017). Long-run data on the size and composition of DC pension assets are unavailable. Instead, we use a range of sources to identify countries with mandatory DC scheme participation for all workers or for those in specified sectors (Brooks, 2005, 2007; International Organisation of Pension Supervisors, 2017; International Social Security Association, 2017; OECD, International Social Security Association, & International Organisation of Pension Supervisors, 2008). Following the OECD (2015), we also identify countries with “widespread” participation in voluntary DC schemes where coverage exceeded more than 40% of the working-age population, as well as countries with “limited” participation where coverage fell short of this threshold.

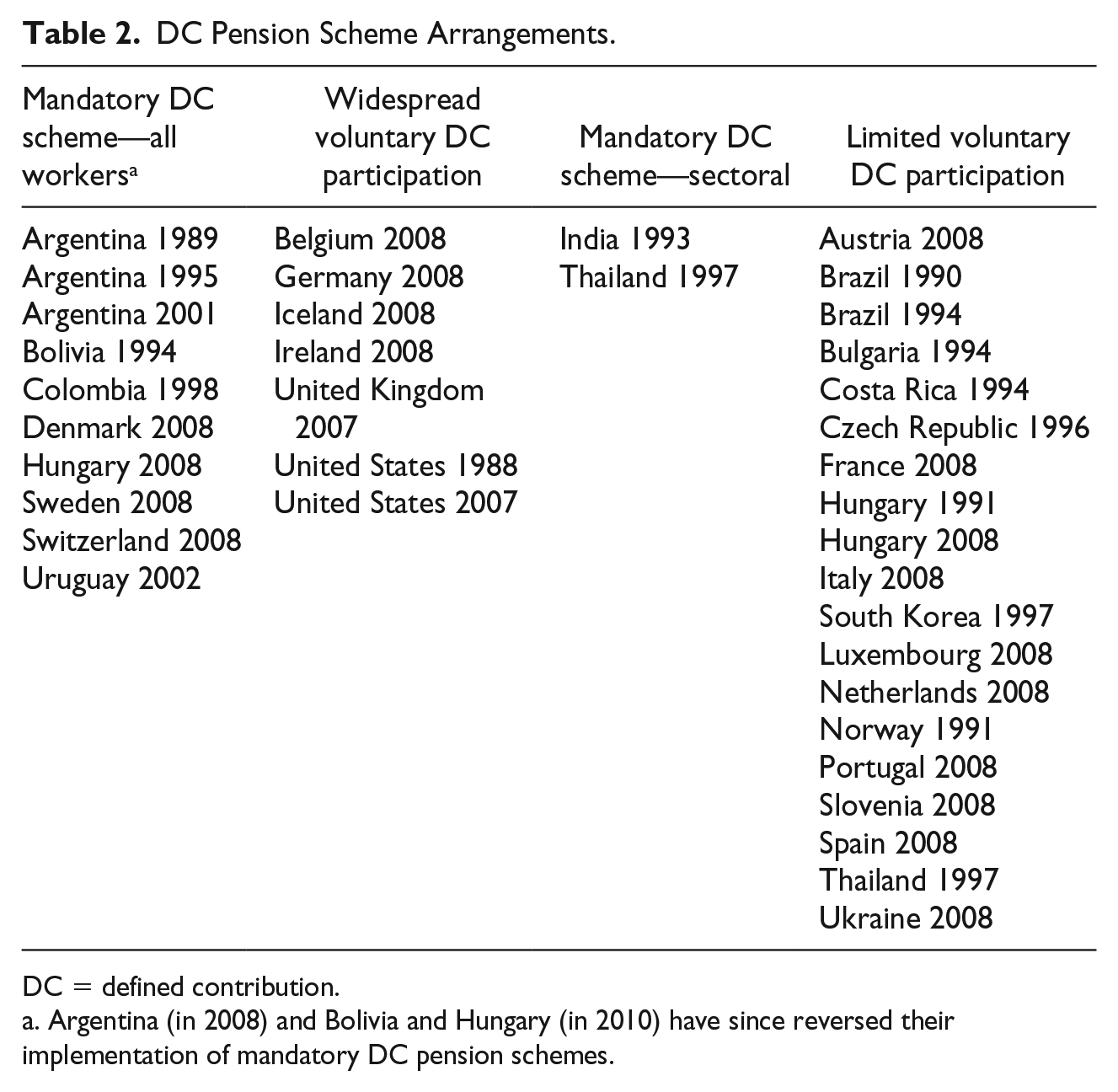

Table 2 identifies the country and L&V crisis-years where exposure to DC pension assets was present based on these four arrangements. We use these data to create two alternative binary measures that capture different configurations of the above arrangements. One measure captures cases where DC asset holdings are wide-ranging, with mandatory schemes or widespread voluntary participation. Another measure captures the presence of any of the above DC arrangements.

DC Pension Scheme Arrangements.

DC = defined contribution.

Argentina (in 2008) and Bolivia and Hungary (in 2010) have since reversed their implementation of mandatory DC pension schemes.

Turning to the democratization of leverage, we use three different national series of household mortgage and consumer debt (Bank for International Settlements, 2017a; Jordà, Schularick, & Taylor, 2017; Léon, 2017).

Finally, we wish to capture the extent to which governments have exhibited an accumulating ex ante effective commitment to financial stability as a policy priority. Our measure focuses on the most concrete forms of government precommitment: prudential regulation, the creation of financial regulatory agencies, and extensive state control of the banking system. We use the creation date of the first regulatory agency at the national level charged with responsibility for financial supervision or, alternatively, when the government took extensive control of the banking system. We view these institutional innovations as clear and vivid manifestations of government commitments to voters to prioritize financial stability. For creation dates, we draw largely on the regulatory agencies data from Jordana et al. (2011). We supplement this, where necessary, with information from the websites of national central banks and financial regulatory agencies. We use other sources to identify government ownership of the banking system and extensive state control (Abiad et al., 2008; Honohan & Klingebiel, 2000). 15

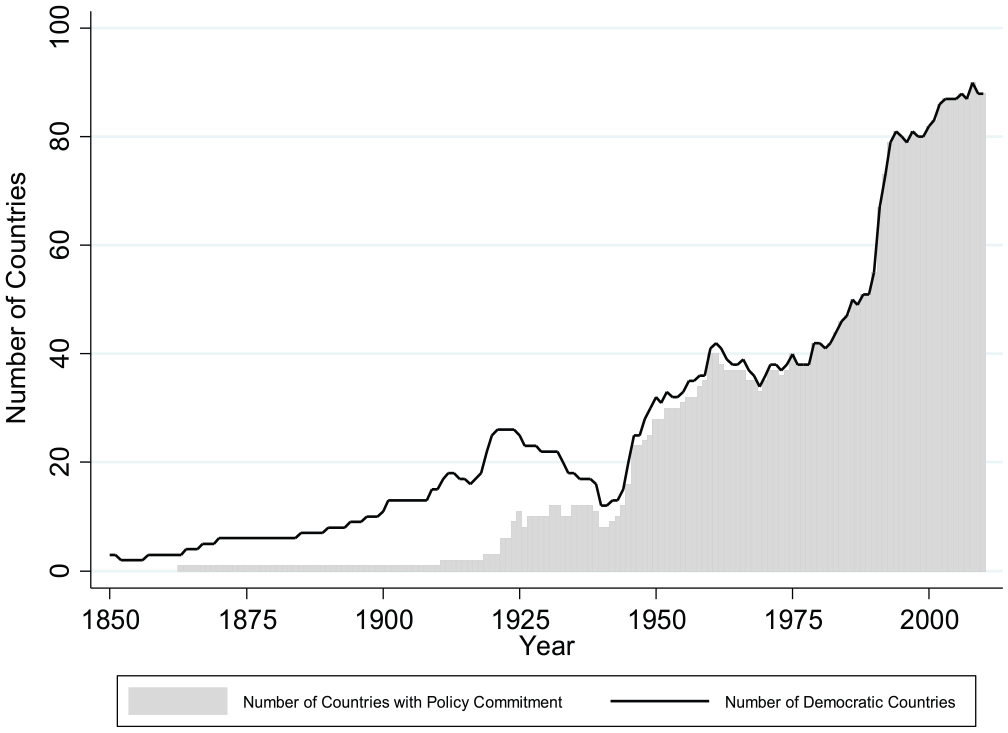

Figure 9 shows the evolution of government policy commitments to financial stability since 1850. 16 Notwithstanding a few exceptions (the United States in 1863, Sweden in 1907, and Denmark in 1919), as late as the early 1930s most democratic governments refrained from making a policy commitment. Then, from the mid-1930s onward, we observe a sharp increase in the number of democracies committing to financial stability as a policy goal; by the end of the early post-war era, it was nearly universal.

Evolution of government policy commitments since 1850.

Our argument implies that voters in countries with a prolonged period of policy effectiveness will have higher expectations of financial stability than voters in countries in which stabilization commitments turn out to be a “false promise.” We thus develop a proxy measure of stronger policy commitment to financial stabilization based on a country’s history of effectiveness in avoiding financial instability. Our measure uses the date of first appearance of a commitment to financial stabilization as the baseline for counting the number of years since a country last experienced a systemic crisis, with higher values indicating an accumulating effective policy commitment.

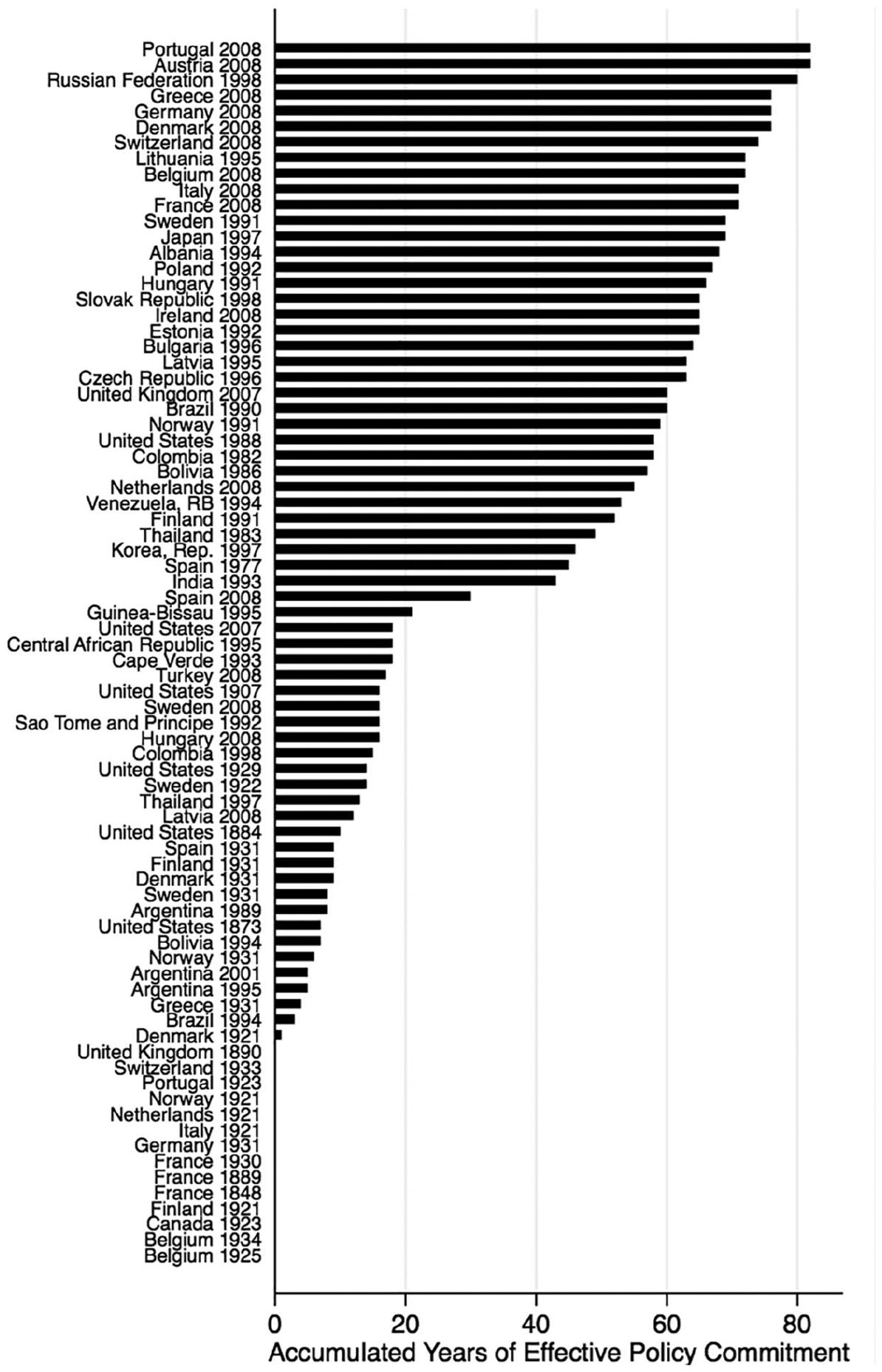

Figure 10 plots the years of accumulated policy commitment for a sample of L&V crisis-years. At the upper end of the distribution, we find crisis-years after a prolonged period of financial stability following the creation of a regulatory authority or statutory banking regulation (Austria 2008, Germany 2008, Denmark 2008, Japan 1997, Sweden 1991) or an extended period of state control of the banking system (Lithuania 1995, Albania 1994, Poland 1992, Estonia 1992). At the lower end of the distribution, we observe crisis-years where either the country lacked a regulatory authority, statutory banking regulation, or extensive state control (Belgium 1934, France 1930, Canada 1923, Netherlands 1921) or it had experienced financial distress shortly after such commitment (Denmark, for instance, experienced a crisis in 1931 and 1921 following creation of a regulatory authority in 1919).

Accumulated years of effective policy commitment.

We control for degree of democracy using the Polity data set because taxpayer interests may be better represented in regimes with stronger democratic institutions (Rosas, 2006). We also consider the level of economic development—the natural log of per capita GDP—and public debt burdens to account for the fiscal constraints on governments to afford the expense associated with bank bailouts. In some model specifications, GDP per capita is highly correlated with the measures testing our argument. To avoid complications with multicollinearity, in these specifications, we substitute a binary variable for “advanced economies” based on the IMF income classification scheme. 17 As fixed exchange rate commitments may also constrain the capacity of governments to undertake the fiscal and monetary measures associated with bank bailouts, we capture these using a binary variable. We include a measure of partisanship, coded as 1 = “Right,” 2 = “Center,” and 3 = “Left.” Finally, we include a common linear time trend to strip out the effect of unmeasured trending factors, such as technological change and the accumulation of economic knowledge concerning crisis mitigation, that could be shaping policy responses and also correlated with some of our independent variables.

We provide our sample, summary statistics, and correlation matrix in the online appendix. We estimate a series of ordinary least squares regressions that model government policy responses to banking crises and include robust standard errors with country clusters. Missing values pose some concern in this analysis. Banking crises are relatively rare events. The summary statistics show that partisanship exhibits a somewhat higher level of missingness. Inclusion of all the covariates above further depletes the already small number of crisis windows. We thus estimate both a reduced-form specification where partisanship is excluded and a more comprehensive specification where this variable included. Results are similar across both specifications.

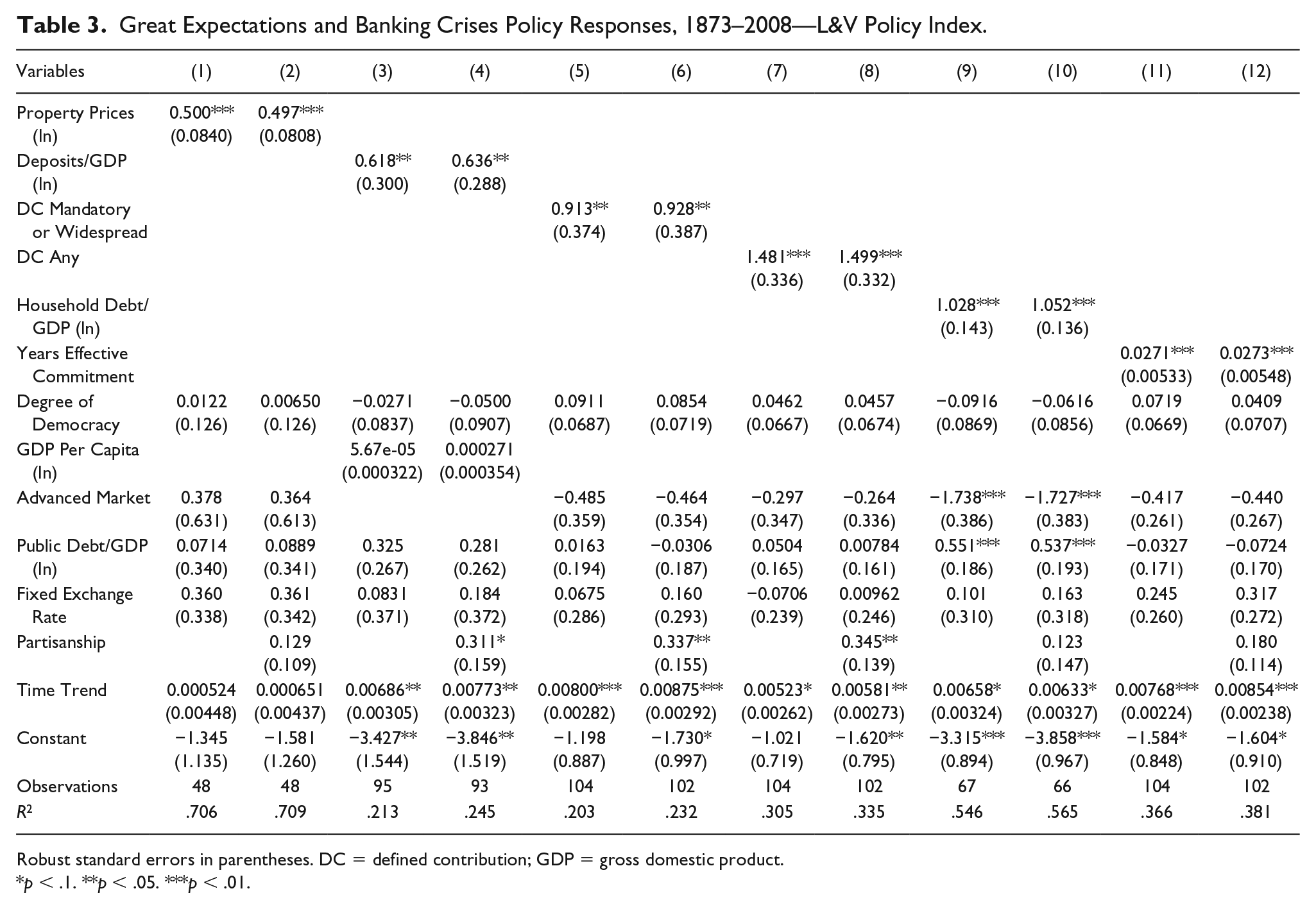

The results provide strong confirmation of our argument. Table 3 reports the results from the larger sample of L&V crises; we provide the results from the R&R sample in the online appendix. Figure 11 uses these results to provide a sense of the inter-temporal and cross-sectional variation in the effects related to our argument. It uses illustrative examples over time and across countries at given points in time to plot the simulated first difference for each variable related to our argument.

Great Expectations and Banking Crises Policy Responses, 1873–2008—L&V Policy Index.

Robust standard errors in parentheses. DC = defined contribution; GDP = gross domestic product.

p < .1. **p < .05. ***p < .01.

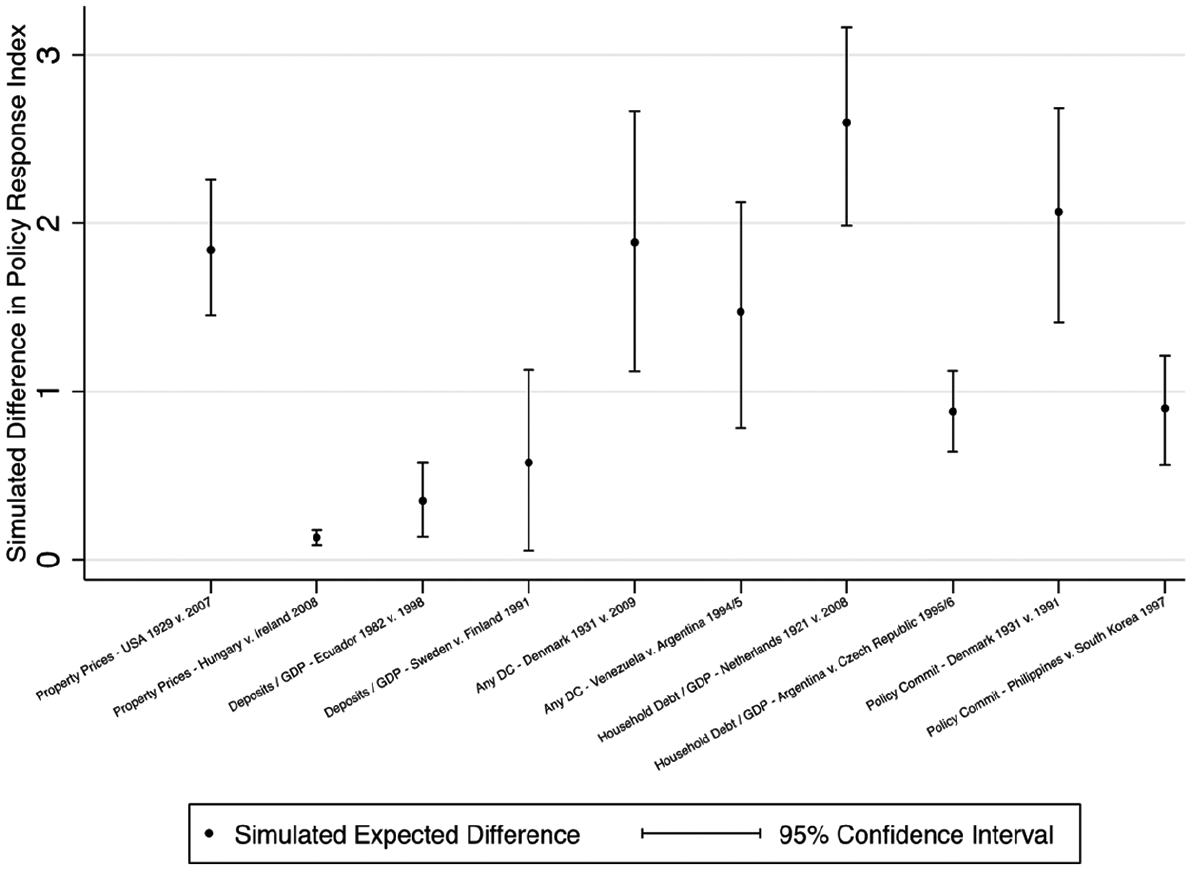

Simulated first differences.

Turning first to financialization, we find that more extensive bailouts follow crises in countries where residential property prices have reached elevated levels. The magnitude of the effect is substantively large, particularly over time as housing wealth has grown among the middle class. Based on an increase in property prices on the level experienced in the United States between the 1929 and 2008 crises (from 3.5 to 129.8 on the index), we would expect a difference in the policy response index of 1.84 [1.45, 2.26]. 18 We also find a greater tendency toward bailout (0.13 [0.085, 0.173]) in countries with higher property prices even when comparing two economies in 2008 with elevated valuations (Hungary = 108.1 and Ireland = 140.5).

Higher property prices undoubtedly tap into the build-up of concentrated wealth in housing assets among middle-class households, capturing aspects of the composition effect we discussed. Sharp falls in asset prices during crises can also quickly threaten highly exposed banks with insolvency, intensifying financial distress, generating additional wealth losses, and prompting governments to respond with bailouts.

We also find that democratic governments have tended to move sharply away from the strict implementation of Bagehot policies when households have acquired a sizable share of wealth stored in financial system deposits, demonstrative of the size effect we outlined above. Based on the more recent increase in deposit wealth in emerging market and developing countries, such as that experienced in Ecuador between its crises in 1982 and 1998 (13.4% to 23.3% of GDP), we would expect a difference in the policy response index of 0.35 [0.13, 0.58]. Alternatively, comparing Sweden (29.9%) and Finland (53.2%) in 1991, we also find a stronger tendency toward bailouts in the country with greater deposit wealth (a difference in the policy response index of 0.57 [0.05, 1.12]).

Household exposure to DC pension scheme assets also heightens the likelihood that governments will intervene with more extensive bailouts, suggesting that the composition effect associated with housing assets extends to pension assets. Comparing over time and across countries, such as Denmark in 1931 versus 2009 and Venezuela versus Argentina in 1994/1995, we find a large difference in the policy response index (1.89 [1.12, 2.67] and 1.47 [0.78, 2.13]) where any of the four DC arrangements analyzed are present. The results suggest that governments are highly responsive to growing household anxiety about the value of volatile pension assets following a crisis.

Governments also appear very responsive to rising household mortgage and consumer borrowing. An increase in household leverage equivalent to that experienced in the Netherlands between its 1921 and 2008 crises (14.5%–109.7% of GDP) would lead us to expect a large difference in the policy response index (2.6 [1.98, 3.16]). We even observe a substantively large difference when comparing two emerging market countries, Argentina (4.0%) and Czech Republic (9.5%), with limited household leverage in 1995/1996.

The democratization of leverage has been associated with more extensive bailouts, in all likelihood, due to government efforts to support consumption and to prevent “fire sales” of assets that would threaten household wealth and harm the wider economy. To avoid losing political support from households, the results suggest governments have become increasingly prone to public intervention to stabilize the financial system.

Finally, the results show that bailouts are more likely in democracies where voters have observed a longer effective policy commitment to financial stabilization. Comparing over time and across countries, such as Denmark in 1931 versus 1991 (8 vs. 69 years) and Philippines versus South Korea in 1997 (13 vs. 46 years), we find a substantial difference in the policy response index (2.1 [1.4, 2.6] and 0.89 [0.56, 1.21]) where the government has a longer effective policy commitment to financial stabilization.

Our results are robust to the inclusion of time period dummies, IMF conditionality, capital openness, central bank existence, and spatial weights capturing policy diffusion via competition and learning as additional control variables. They hold up when we undertake cross-sectional analysis in a particular crisis period and when we consider a model approximating a difference-in-differences design (see online appendix). Taken together, these results suggest that the three interrelated developments we emphasize in our argument have shaped policy responses both over time and across countries at given points in time.

Turning to our control variables, we also find some evidence that richer economies are more likely to choose bailout policies, possibly reflecting their greater policy space to engage in taxpayer-funded financial rescues. We find little evidence that exchange rate commitments or public debt burdens constrain (or enable) particular policy responses. Finally, we find no evidence to suggest that degree of democracy or partisanship drives government policy responses to crises. This is consistent with our argument that voters’ great expectations now overwhelm any constraints that partisanship and democratic institutions might impose.

Conclusion

The expectation that democratic politicians will seek to avoid extensive crisis interventions producing large taxpayer liabilities draws on a long tradition of theorizing about the impact of electoral accountability in democratic settings. However, the evidence in this article raises doubts. Instead, it suggests that democratically elected politicians in the modern era have become increasingly prone to respond to the demands of an increasingly wealthy but also exposed middle class. These great expectations arise from the three interrelated developments—the financialization of wealth, the democratization of leverage, and an accumulating ex ante policy commitment to financial stability. We have shown that each of these factors is associated with more extensive bailouts. This was true not just for all the democracies that faced systemic banking crises over 2007–2009, but more importantly we show that it is part of a longer and deeper evolution of the political economies of developed, emerging, and even developing countries.

Our findings also point to the complex and evolving interest cleavages characterizing increasingly financialized political economies. Much political economy theory has traditionally understood interest cleavages as deriving from actors’ positions in the division of labor and the way these shape flows of income to classes (capital, labor, and rentiers) or to cross-class sectoral divisions (Frieden, 1991; Hiscox, 2002; Rogowski, 1990). Financialization, by linking the wealth and consumption of many households to asset and credit markets, blurs this picture (Ansell, 2014; Gourevitch & Shinn, 2006, p. 221; Langley, 2009; Pagliari et al., 2018). Income flows still matter to middle-class households, defined (as we have throughout) as those comfortably out of poverty but still needing to work, but now these households as homeowners and DC pension-holders fret more about asset and credit market downturns. They often also value highly the ability to refinance mortgages and other debts at lower interest rates in the wake of financial crises and to maintain consumption via expansion of consumer finance and credit. Others who are less leveraged (and often older) may be less exposed, but as likely to be concerned about the threat financial instability poses to the value of their pensions and houses.

The implications of these new cleavages and coalitions defined by wealth rather than income are potentially far-reaching. It has posed challenges to the contemporary welfare state and complicated efforts to forge constituencies in support of more redistributive measures after the 2007–2009 crisis (Ansell, 2012, 2014). It may also increase political support for consumption-driven growth models linked to the expansion of credit as opposed to export-driven models based on labor cost moderation and the real exchange rate (Baccaro & Pontusson, 2016). It may make it harder to build constituencies in favor of moderating housing and asset booms and the growth of private debt (Baker, 2018). Booming housing markets may also heighten the salience of political cleavages between home owners and renters, which are often layered on wealth disparities between generations and between those living in prime versus peripheral locations (Ansell, 2017). Home ownership may also have effects on political preferences for environmental protection, fuelling NIMBYism aimed at blocking liberalization of supply-side constraints on home construction that could lower house prices.

Perceptive politicians such as Margaret Thatcher saw political advantage in policies promoting asset ownership among the working and middle classes (Francis, 2012). But our evidence suggests that her attempt to drive a wedge through the left’s constituency and generate a permanent majority for pro-market conservatives was only partly successful. The promotion of private house ownership and privatized pensions produced more extensive crisis interventions, consistent with the preferences of an increasingly asset-rich middle class. Their preferences may be time-inconsistent, favoring deregulation in credit booms and supporting heavy government intervention and re-regulation when crises strike. These interventions in turn may generate the rising moral hazard Thatcher so detested, destabilizing the market capitalism she and others sought to restore. Furthermore, in creating a policy trap that reinforces the very threat to financial stability from which many voters demand protection, it could increase political instability and contribute to rising citizen dissatisfaction with government and politics in many democracies (Chwieroth & Walter, 2017; Foa & Mounk, 2016, 2017). This link, which has been little explored to date in the burgeoning literature on populist politics, is worthy of further research.

Supplemental Material

CPS_Appendix_Revised_11_Oct_2019 – Supplemental material for Great Expectations, Financialization, and Bank Bailouts in Democracies

Supplemental material, CPS_Appendix_Revised_11_Oct_2019 for Great Expectations, Financialization, and Bank Bailouts in Democracies by Jeffrey M. Chwieroth and Andrew Walter in Comparative Political Studies

Supplemental Material

CPS_Replication_Materials – Supplemental material for Great Expectations, Financialization, and Bank Bailouts in Democracies

Supplemental material, CPS_Replication_Materials for Great Expectations, Financialization, and Bank Bailouts in Democracies by Jeffrey M. Chwieroth and Andrew Walter in Comparative Political Studies

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The support of the Economic and Social Research Council (ESRC) in funding the Systemic Risk Centre is gratefully acknowledged (Grant Number ES/K002309/1). The authors also acknowledge financial support from Chwieroth’s Mid-Career Fellowship from the British Academy for the Humanities and the Social Sciences [MD130026], from Chwieroth’s AXA Award from the AXA Research Fund, from Chwieroth and Walter’s Discovery Project award from the Australian Research Council [DP140101877], and from seed fund grants by the Suntory and Toyota International Centres for Economics and Related Disciplines (STICERD) and the Department of International Relations at the London School of Economics, and the Melbourne School of Government.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.