Abstract

Physical goods producers routinely collaborate with digital platforms to extend their distribution capabilities. They usually realize that digital platform firms differ from them in their strategies and capabilities, and that significant opportunities arise from innovating digital platforms being able to collect, analyze, and leverage behavioral customer data related to the consumption experience. However, collaborating with digital platforms is likely to put competitive pressure on the incumbent’s margins, and, in extremis, encourage entry by the platform into the incumbent’s business. These threats can be moderated by limiting access to the incumbent’s technology and supply chain, or by building an in-house digital platform.

As noted by many previous writers, digital platforms often generate strong network effects as their attractiveness increases when there are more users. 1 This creates the possibility for established digital platform firms to provide the incumbent producer with access to customers beyond those provided by the distribution system the incumbent producer already possesses. The digital platform’s ability to access new customers can be augmented by the platform’s capacity to “know” the customer on account of their ability to collect and process data about customer purchasing preferences. 2 Such has been the case with Amazon’s shopping platform. They have provided an expanded retail channel for a wide variety of physical goods.

Furthermore, in the wholly digital world, where artifacts are easily modified without physical or human intervention, some platforms (e.g., Google and Apple) have gathered information not only about how purchasing behavior takes place but also on user experience; and they have used these insights to improve the actual offering. 3 However, for the case of physical goods providers, leveraging platform knowledge gained from consumers’ consumption patterns regarding the design of the offering is generally more difficult. Even though the platform has access to information about consumer preferences that might be superior to the physical goods producer, it is rare that the platform can reconfigure the physical good without either taking control of the production process or working closely and in cooperation with the producer of the physical good.

In this article, we adopt the posture of the physical good producer. We ask when and how it should form a distribution arrangement with an established platform. In particular, we ask how it should assess the costs and benefits of the relationship, bearing in mind that platforms often differ in their capabilities.

Even though digital platforms vary greatly in scale, scope, and the services they offer, we follow the suggestions of Annabelle Gawer and consider aggregating them into two groups to assist analysis: those that emphasize transactions and those that emphasize innovation. 4 Those that emphasize transactions include firms such as Facebook, where firms and users can post social comments that encourage use, and Amazon Marketplace, where buyers can seek out the firm’s offering (if it is listed). Those that emphasize innovation are platforms such as Apple, which (for example), in the context of home appliances, use their Smart Home app to augment the appliance’s capabilities and usefulness. Gawer admits that there are cases where businesses lie on the boundaries between the groups, but she suggests most major digital platforms can be clearly classified as one or the other.

Innovation platforms seem to achieve the best results in terms of improving the consumption experience when they can access consumers and consumer data. Although, to date, there are relatively few concrete examples of such data orchestration, the ones that exist indicate what these innovative platforms can do.

Forming an alliance with a digital innovation platform with the goal of having the platform firm improve the alliance partner firm’s offering through its superior data orchestration capabilities brings risks that may outweigh the benefits. This is because the innovating digital platforms often have ownership of or access to data orchestration capabilities that are superior to those held by—or able to be created by—the durable goods producer. By using consumption data, the platform firm may be able to disrupt the innovating producer’s existing distribution system, and, in extremis, the platform firm may be able to enter the incumbent producer’s business and compete vigorously. 5 To be clear, this is not a re-contracting risk of the kind discussed by Oliver Williamson. 6 Rather, as we explain below, it is a capability enhancement feature associated with data control and management associated with the competitive dynamics of almost any alliance.

These observations mean that the safest option for many durable goods producers wishing to increase their reach to new consumer groups is to transact exclusively with transactional platforms (such as Amazon Marketplace) and shun relationships of a deeper kind with more innovation-oriented platforms such as Apple. Of course, allying with transactional platforms also brings risks, including alienating some of the physical producer’s existing distributors. And, as with all alliances with distributors, there is always a risk that the distributor will bring pressure on margins (especially where the digital distributor has buying power) and that the distributor will look to supply goods under a “private label” competing with the producer’s branded offering. Such risks are well known and extensively discussed in the literature. 7

There is a final course of action: building one’s own platform. It seems there are very few examples of physical goods firms achieving this goal. Building a (successful) platform that will almost certainly have to compete with established giants is not easy. First, there is the question of accessing or building the dynamic capabilities required for data orchestration. Secondly, there is the challenge of competing with established giants that have already established a consumer franchise. When it built its platform, Apple did not face well-established platform competitors. It built its successful digital platform in stages, developing its capabilities for data orchestration over a long period of time. 8 Most producers of physical goods would be concerned about the costs and efficacy of building their own digital platforms to achieve success.

In the rest of this paper, we explore more deeply the differences between transactional and innovation platforms, and use this distinction to examine carefully and critically the threats and opportunities posed from forming alliances with different kinds of digital platforms to the (incumbent) producers of physical goods. To do this, we apply insights from the existing academic literature coupled with relevant examples form practice that explain why an innovative producer needs to consider using platform firms as complementors to assist in bringing its goods to market and allow it to capture greater value. 9

We pay special attention to the challenge that producing firms face when they consider building their own platforms, and the importance of building “dynamic capabilities”. Our analysis has implications not just for those interested in the fate of physical goods producers, but also those who wish to understand the power and opportunities posed between different kinds of digital platforms, with respect to what they offer, and provide deeper insights with respect to super-modularity. 10

Literature Review

Teece (over several papers) provides a framework for thinking about the value of complementary assets and technologies in the creation and capture of value from the innovator’s offering in the physical world. However, Teece’s “Profiting from Innovation” (PFI) model does not directly consider the case of the digital and the physical goods firms interfacing with each other 11 and has yet to fully explore the idea that it is not complementary assets at a point in time, but rather complementary assets and capabilities that the platform partner builds over time that may enable it to get the upper hand through alliances. This competition threat is another example of something long noted in the alliance literature; making an alliance with a company carries dangers as well as opportunities. Those partners that offer the greatest value may be the same partners that pose the greatest compeitive risks. 12

Teece points out the circumstances in which innovators need to consider forming partnerships (alliances or distribution contracts) with holders of complementary assets to capture value. 13 Such partnerships can not only give access to the complementor’s assets, but they can also leverage the knowledge embodied in those assets. 14 Some of the necessary complementary assets are quite generic (such as wholesaling and retailing), but some may be very specific—such as providing detailed product-specific training and advice. 15 It’s the latter that pose strategic issues. All partnerships carry risks, including that the partner will learn about the producer’s business and will then pose a threat by entering the business in competition with the producer. 16

The likelihood of the complementary-asset alliance-partner provider in a partnership posing a competitive risk will be impacted by the extent to which the producer of the physical good is well positioned with respect to any bottlenecks in the supply chain. In digital businesses, risks of disintermediation are high, as it is not easy to control the activities of complementors in general and platforms in particular. 17

As noted, our focus is on incumbent physical goods producers partnering with digital platforms. To understand how a digital platform can add to (or subtract from) an incumbent’s physical goods offering, one needs to understand the different types of platforms, as some pose bigger competitive threats than others. Building on an extensive literature in economics and strategic and operations management, Gawer defined digital platforms as meta-organizations that “(1) federate and coordinate constitutive agents who can innovate and compete; (2) create value by generating and harnessing economies of scope in supply or/and in demand; and (3) entail a modular technological architecture composed of a core and a periphery.” 18 She stressed that digital platforms are evolving organizations with different capabilities and behaviors. Cusumano, Gawer, and Yoffie further examine platform heterogeneity, distinguishing between transaction platforms and innovation platforms. 19 They argue that the main function of a transaction platform 20 is to facilitate exchange across sides, in contrast to an innovation platform that seeks to create (new) value by facilitating innovation on the platform (itself). X (formerly Twitter), Uber, Airbnb, eHarmony, and Amazon Marketplace, along with the digital platforms owned by retailers such as Walmart, are examples of digital transaction platforms, and Microsoft Windows, Google Android, and Apple iOS are examples of digital innovation platforms. 21

There are diversified firms that own both kinds of platforms within the same organization. In general, this is not a challenge for the producer as, typically, each platform is run separately. But links between the different platforms should be noted; recently, the EU commission complained that the policies of Apple’s app store (a transactional platform) were influenced unfairly by the profit-seeking activities of Apple’s streaming services. Apple was accused of forcing its app store to favor its own streaming service over that of other streaming services listed on Apple’s app store. 22

The examples above suggest that digital (transaction) platforms are likely to provide rather generic services that are focused on increasing the reach of the producer’s offerings beyond that already achieved through the producer’s current distribution system (as with Amazon Marketplace). In contrast, digital innovation platforms offer the opportunity to add more value which we now analyze in greater detail.

Value-Added Possibilities from Engaging with Digital Platforms

Type 1: Alliances with Transaction Platforms (Nudging Customers Toward Purchase)

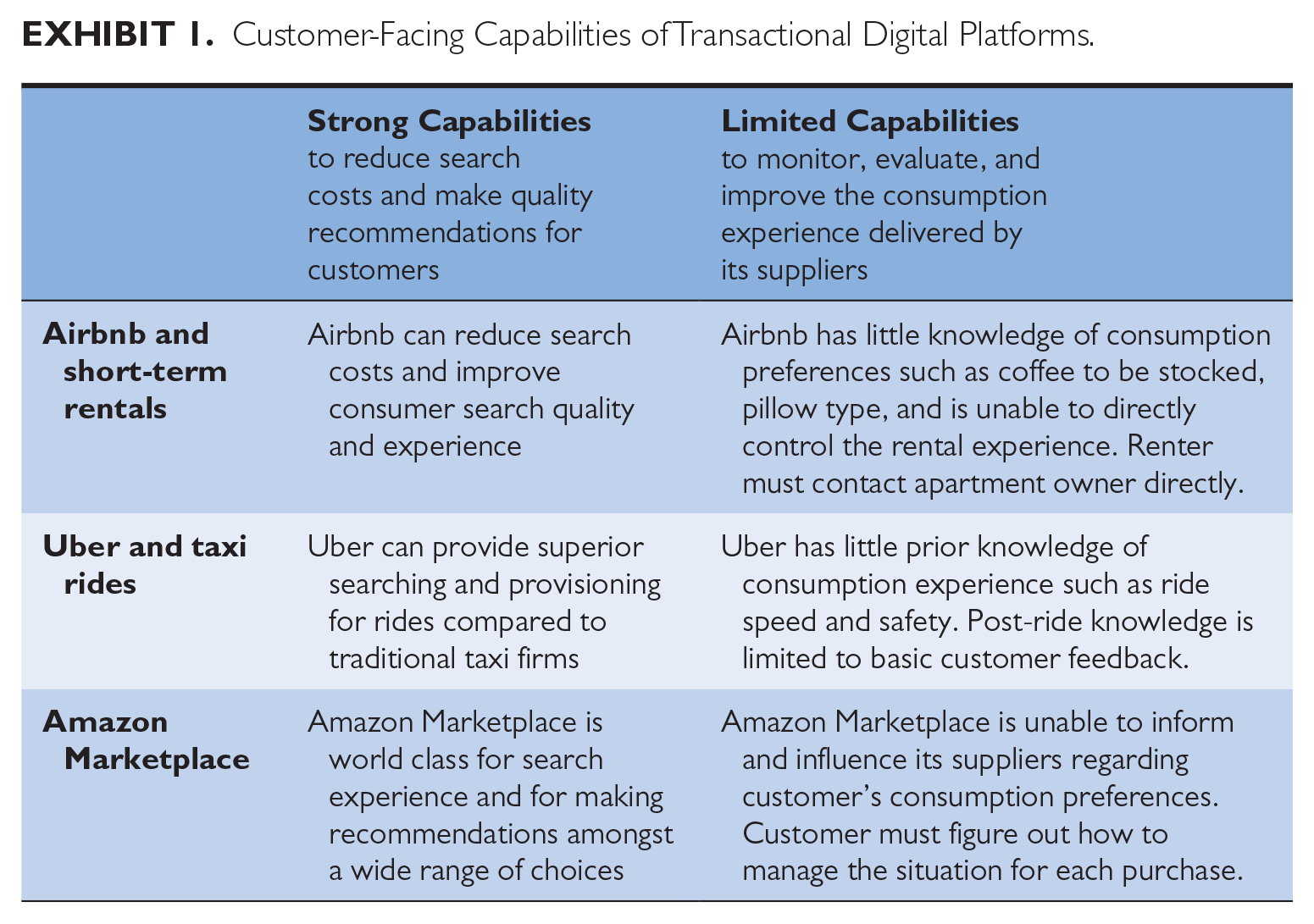

Transaction platforms focus on connecting different parties. 23 Producers of physical goods engaging with these platforms typically use simple contracts. Little information is exchanged between the parties. Three examples of transaction platform firms—Airbnb, Uber, and Amazon Marketplace—highlight their areas of capability strength and weakness, thereby shaping opportunities for both value creation and risk for the physical goods producer (see Exhibit 1).

Customer-Facing Capabilities of Transactional Digital Platforms.

We suggest that where a digital firm engages in directing consumers to purchase a physical product, its influence on the physical goods producer’s forward trajectory will be modest and “evolutionary”. By “evolutionary,” we mean that the platform firm will have some influence on the design of the offerings of the physical goods firm and some influence on its profits, but it will not substantially alter the supply chain for the core offering and its related services. We recognize that “directing” consumers to purchase an item can take on many dimensions and many forms, including operating a platform that allows consumers to purchase the product (and related services), curating third-party reviews, describing the offer in a novel manner that is attractive, giving it prominence, and providing easy physical delivery. These dimensions of influence have limited potential to dramatically improve the consumption experience.

Airbnb is a good example. From the consumer perspective, this platform has had a profound influence on the marketing, availability, and pricing of places to stay, showing itself to be, in many instances, much more competitive in the customer’s eyes than the traditional rental placement agencies—and in some cases more competitive than the franchiser firm in a franchised hotel chain. The influence of Airbnb on its direct competitors (other renting agencies) has been salutary, as has its influence on the overall hospitality industry. 24 But these are not the industries of concern to us here. Our concern is with the suppliers of the physical goods that are being offered to the consumer, namely, apartments or houses. There is some evidence that in tourist destinations, Airbnb has pushed up some construction prices and profits. 25 But there is little evidence that Airbnb has influenced the way apartments are designed and constructed, and there is little evidence that they directly influence the hospitality experience in any substantive manner. When renting an apartment, Airbnb does not ensure that the heating and cooling are set to customer preferences, nor that there is the right kind of coffee left in the kitchen or the right kind of sheets and pillows on the beds. Rather, Airbnb expects the renter to contact the apartment owner directly with their requests, and Airbnb has invested considerable effort in training their apartment providers to be responsive. 26 As customers of Airbnb know (to their frustration), Airbnb is unable to force its providers to collect data on user’s needs and then recirculate it for future stays. Moreover, Airbnb has barely been able to prevent travelers from being charged cleaning fees, tasked with check-out chores, and other conditions imposed by hosts. Consistency and reliability are hard for Airbnb to secure when they don’t control the asset. If Airbnb undertakes small but important improvements to the physical dimensions of the offering of their apartment owner partners and their partner’s customer service, they will become even more attractive. 27 However, backward integration into the housing-apartment-hotel industries to get better control would be very costly and break the business model. The opportunities for extra value creation are, therefore, quite small relative to the costs.

Similarly, as noticed by many, Uber’s taxi/rideshare service has had a profound effect on the availability and pricing of transportation services in many markets and the related demand for drivers, where there are either a myriad of small ineffective aggregators or, in some cases, a monopoly regulated by the local authority. 28 The entry of Uber, Lyft, Blacklane, and other rideshare platforms has greatly improved the availability of taxi services in many regions, to the benefit of consumers. Yet, despite the widely touted benefits of digitization, Uber has not been able to promise a uniformly good ride experience. Riders’ preferences regarding the kinds of music played, the speed of the taxi, and other factors are not recorded by the Uber system and so they are not incorporated into the rideshare design or service. Many modern cars are sufficiently digitalized so that these kinds of preferences could be transmitted and orchestrated for the passenger, but such moves would probably require cooperation from drivers and in some cases from the auto-manufacturers. So far, there is no evidence of any such moves. We know that Uber is engaged with partners in the design of future cars, with a special emphasis on self-driving, but we do not know if these plans also include ways to make the ride more experientially comfortable. We suspect they will.

Amazon Marketplace, another transaction platform with arguably the largest retail distribution system in the Western world, has displaced many other distributors. It has had some influence on its supply chain through its use of exclusive purchasing contracts and selective backward integration. These initiatives appear to have been undertaken in areas where the supply of goods is very competitive, with few entry barriers of either capital or capability. It is notable that these moves have been directed at improving the efficiencies of the supply chain, including making it more responsive, rather than making fundamental changes in the underlying offer. 29 We observe suggest that Amazon Marketplace does not yet attempt to improve the final consumer consumption experience by changing the physical good. 30

Type 2: Alliances with Innovation Platforms—Improving the Customer’s Consumption Experience

We now consider the case of the producer of the physical good linking with a digital innovation platform (as defined above), where the platform adds significant value to the producer’s offering by improving the consumption experience. (And to be clear, the producer has a choice: form an alliance or build its own platform.) Sometimes, a digital innovation platform can alter the performance of a physical good without interacting with the actual producer. For example, Netflix, a digital platform, has used its understanding of the differences that exist between mobile phones (a physical good) to alter its digital streaming algorithms to improve the experience of the consumer. Rival digital platforms have found it difficult to replicate this set of capabilities. 31 We know much less about the ability of innovation platforms to improve physical goods when they interact with the physical goods producer and encourage them to alter their physical product (that includes getting access to the digital elements that the producer has attached).

We know from the extensive service marketing literature that improving the consumption experience of the physical offering gives rise to significant value for many goods. We also know from that same literature that to achieve this effect, a firm needs to have a very good understanding of the details of the consumption experience and must have the capability to improve the underlying offer. 32 We also know from the servitization literature, which mainly relates to producer and not consumer goods, that adding sensors or data collection of the interactions between the customer and the product gives rise to valuable data that can be used to achieve these purposes, often with profitable results. 33

The research cited above suggests that for an innovation platform to add to the physical consumer goods firm’s offer, the platform firm must be involved in activities that traditionally lie within or close to the boundaries of the consumer goods firm. By “involved,” we mean that the digital platform, in conjunction with the producer, requires sensors to be embedded in the physical product (and possibly in its use environment). The platform must also become involved in the product design process. In this way, it can influence the product’s performance during consumption. When the firm owns its own platform, the relationship will be easy, but when it is an alliance with a third party, it will be difficult.

As will become clear below, relationships between the producer of the physical good and a digital innovation platform are likely to be complex, involving knowledge exchange that extends beyond a simple contract and morphs into something akin to a complex alliance. While there are many platforms that distribute physical goods or their direct services (such as Amazon and Airbnb mentioned above), very few digital platforms have the capabilities required to successfully engage fully with physical producers to give a complete end-to-end superior experience.

Apple and the iPhone serve as the most obvious example of an innovation platform influencing the design of a physical product. Apple has integrated its platform into its physical goods manufacturing system—it not only makes phones (and other connected devices), but is a designer of complementary devices and manages complex supply chains. Many Western independent mobile phone companies have been put out of business since Apple’s entry. Only a few remain, most notably Samsung—itself highly vertically integrated. There are nonetheless scores of competitors, many of them Chinese, even though they may use what were once Western brands, for example, Blackberry (TCL) and Motorola (owned by Lenovo). When we unpack the components that Apple provides, we see they are the camera, the screen, and the primary system chip. Apple has certainly altered the way cameras are designed, and to a lesser extent altered screen design, which has arguably influenced the profit margins of the producers of those items. However, Apple has had less direct influence on chip design rules and the profit margin of the chip producer. 34 The leading chip producer ARM has collaborated with Apple but in a very special manner. ARM has managed to keep Apple at a distance and not allowed Apple to dictate prices, because ARM possesses very strong patents and has built over many years a deep and strong network of partners, which together allows ARM control over the key component that Apple relies on—namely, the foundational software of the chip that enables Apple’s functionality. 35 Apple has not (yet) supplanted these capabilities. This may help explain why historically over the longer run ARM’s profit margins rival have been favorably compared to those of Apple. 36

Many other companies have tried to replicate Apple’s influence as a platform on the physical product, but few have succeeded. Collecting and analyzing customer behavioral data is not sufficient to influence the consumption experience. Considerable work is required to enable translate these data into improvements to the final consumer offer. Insurance companies use mobile phones to collect data on their customers’ driving habits and use the data to adjust the price of their insurance policies. 37 However, it is clear that they have not yet found an easy way to link this knowledge to the way people drive their cars because they lack access to the design of the automobile and its internal controls. 38

For a platform to influence the design and performance of a physical good, the evidence indicates that there has to be a close relationship between the digital platform and the producer of the physical goods. The process of improving the consumer’s consumption experience and managing behavioral customer data requires many steps and feedback loops, elaborated more fully in the next section. Briefly put, the platform firm (or the incumbent producer) needs to collect, store, and analyze behavioral customer data in an integrated manner that relates to the actual behavior of consumers throughout the whole consumption process. Then the platform firm has to feed these data into improving the consumption experience either by altering the product directly or by changing the way the product is designed and operated. The challenge to platform firms in managing behavioral customer data is significant because these data differ from many other forms of data, such as retrospective data on what products consumers own, environmental data about where consumers are located, and data about consumer characteristics that are not specific to an actual purchase decision. The latter are often scraped from social media websites, whereas the former data can only be collected at the time of purchase from systems that record the actual purchasing and consumption decisions of consumers that are often tacit and unseen to the consumer in question. 39

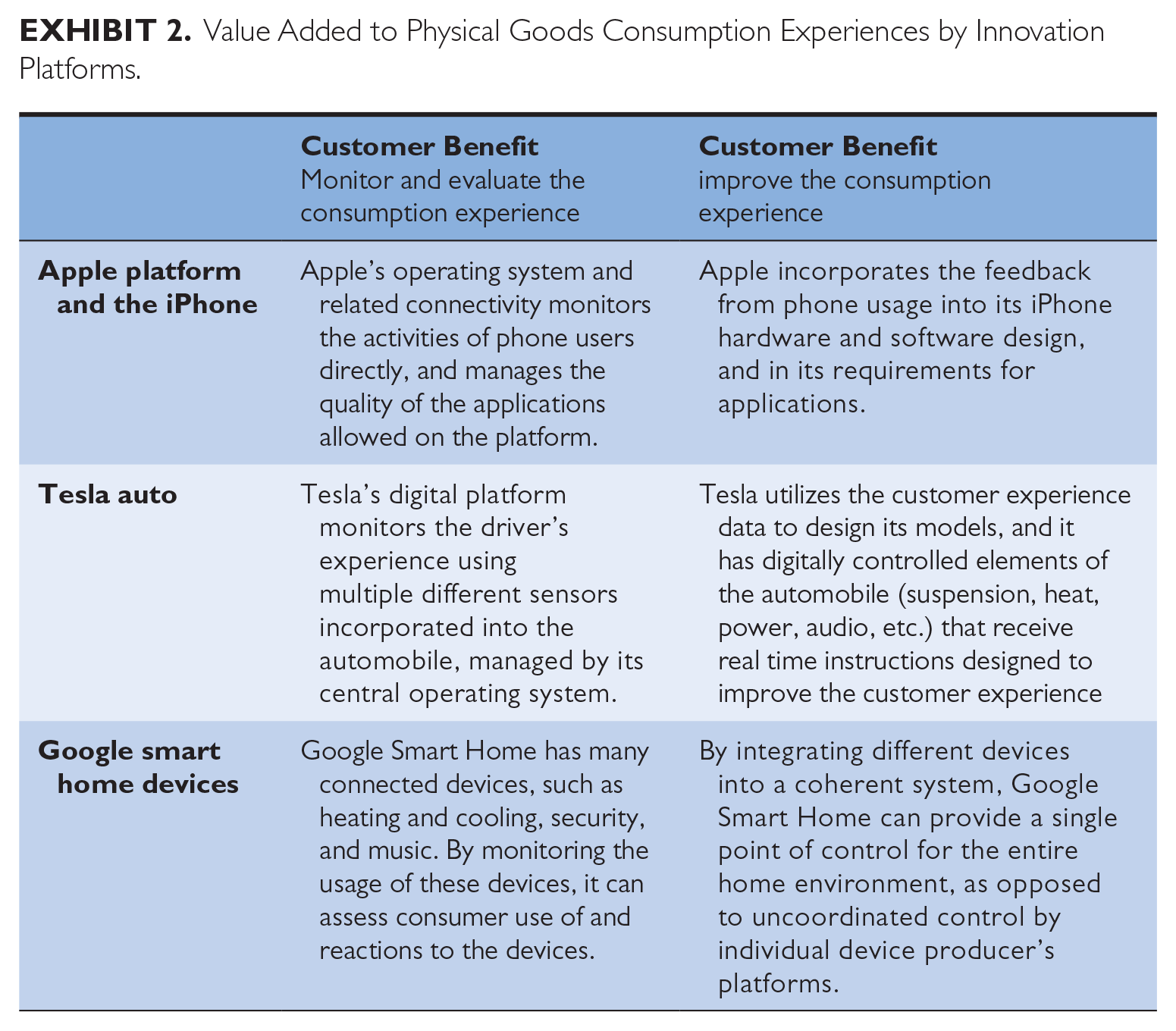

Exhibit 2 presents several examples of companies that have linked their physical goods to an innovation platform that collects data on customers and their experiences with the aim of improving the quality of the consumption experience. Our first example is Apple’s iPhone. The second example is Tesla, the electric car producer that uses its wholly owned digital platform to integrate complementary services such as music and maps into the physical car system to give the user an enhanced experience. Like Apple with the iPhone, Tesla designs both the platform and the automobile whose features are being altered. Other cases include the smart home platforms—operated by Apple, Google, and Amazon’s Alexa—that seek to integrate independent producers of home heating, cooling, security, and music playing into one user-friendly system. To fully understand the challenges faced by firms considering either building their own innovation platform or forming an alliance with an existing platform, we probe into the nature of the challenge and the capabilities and competencies needed to be effective.

Value Added to Physical Goods Consumption Experiences by Innovation Platforms.

Data Management: An Enabling Capability for Improving the Customer Experience

The Difficulties of Managing Behavioral Customer Data

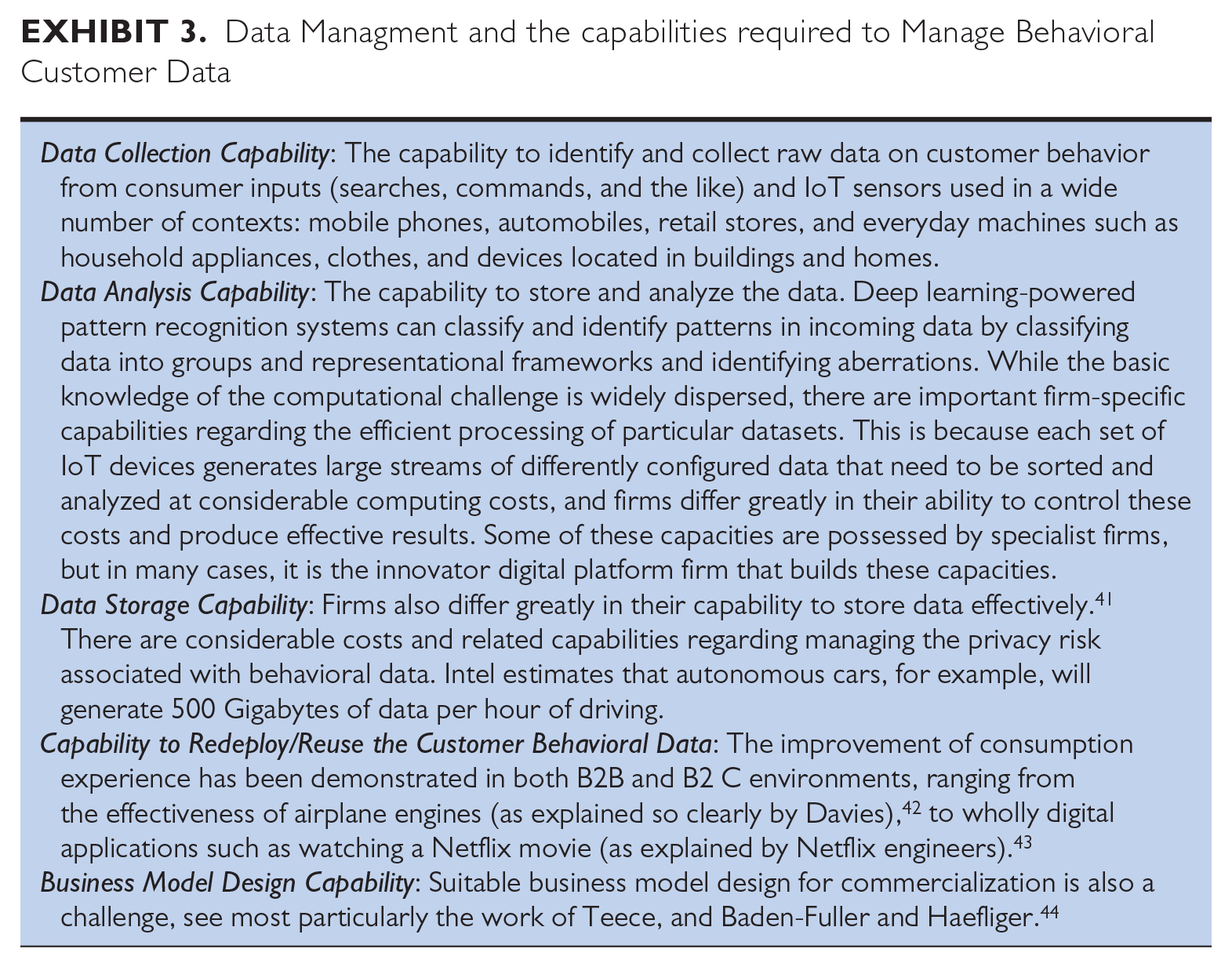

Behavioral customer data are very useful to firms because the data can be used to improve the characteristics of the firm’s offerings. 40 The data are typically dynamic because customer preferences change over time, so the data need continual updating. When collecting and curating behavioral customer data, it is important to realize that the data itself is not the source of value; rather, it is the combination of the data and the capability to collect, store, and analyze the data that is critical. The traditional goods producer is unlikely to possess these capabilities and will find them hard to acquire. An alliance with an innovation platform is likely to be necessary, as further amplified in Exhibit 3.

Data Managment and the capabilities required to Manage Behavioral Customer Data

The capability to effectively collect, store, analyze, and deploy customer data quickly and cheaply is what the dynamic capabilities literature labels an asset orchestration capability. Behavioral customer datasets are typically large, complex, and nontrivial to sort, store, and analyze. Utilizing such datasets requires significant skills and knowledge. The value of behavioral customer data can also be augmented by other kinds of data, which provide an additional contextual understanding of consumer behavior and preferences. These other data are typically located in large “data lakes” that contain vast amounts of data about customers’ characteristics and general behaviors. For example, data lakes may contain location data from mobile phones on millions of customers, and when these data are combined with other much more granular data on consumption, powerful inferences may be drawn. To be effective, firms not only have to collect substantial amounts of behavioral data, but they also need to be able to create (or have access to) these data lakes. Even though digital costs are falling, creating the necessary general and highly specific data sets requires significant investments, as does analyzing the data itself.

The need for data assets and associated analytics capabilities to be married together to create benefits is quite different from traditional economic framing. That framing assumes that, although they are costly to collect, data, once collected, can be easily stored and reused. Data are seen as assets that are valuable in their own right. This may be true when the data do not involve customer behavior. For example, automobile firms collect data on the performance of vehicle components for the purpose of quality control and systems integration. Manufacturing companies collect data on the location of their inventories all the way from the supplier to the final product for the purpose of optimizing the production flow and minimizing errors and overall costs. The situation discussed here highlights behavioral customer data, the generation of which requires a dynamic interaction between the customer and the firm. To be able to use data effectively, data analytics and interpretation capabilities are key.

Traditional economic analysis views the orchestration of data as a relatively simple problem, in part because preferences are assumed to be exogenous and can be revealed by firms putting choices in front of consumers. Baskerville et al. 45 suggest that, in the digital age, preferences may not be fully known or understood by consumers. They may also be determined endogenously. Firms can create novel valuable experiences by developing and exploiting their capabilities of leveraging their customer behavioral data. 46

Innovation Platforms and Dynamic Capabilities

Data collection involves many situations with many different business actors that may or may not lie inside the firm’s boundary. Challenges can arise due to poor connectivity with sensing devices and because the data of importance are not always apparent ex ante to either the generating or collecting enterprise. The required capability in this sphere must be dynamic in the sense that the firm desiring to orchestrate/manipulate the data must sense the opportunities for use without necessarily having a precise idea of the potential value before negotiating contracts to secure the data.

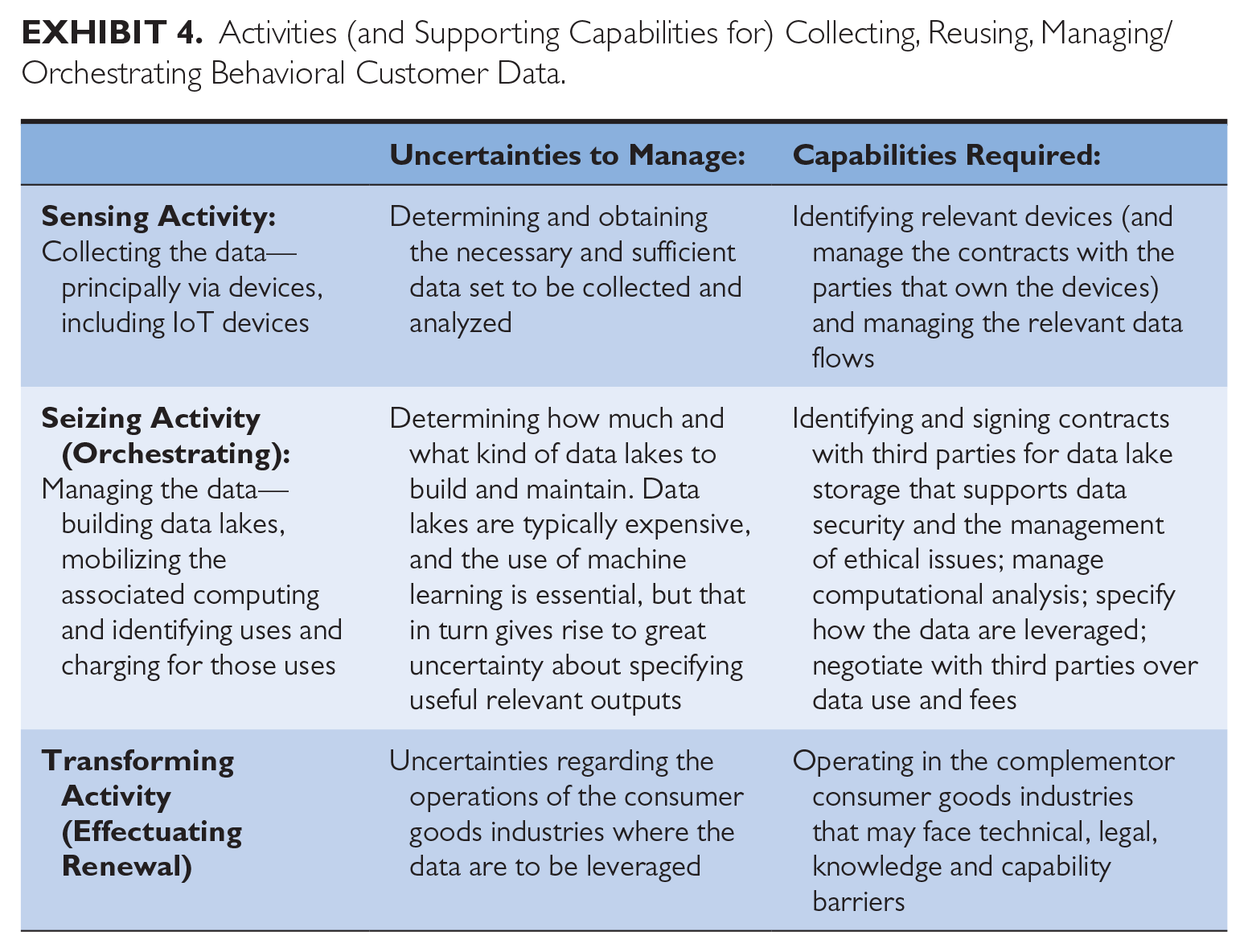

The importance of dynamic capabilities becomes apparent when we consider the uncertainties involved in orchestrating and monetizing customer behavioral data. These uncertainties are related to each of the three phases of sensing, seizing, and transforming (see Exhibit 4). 47

Activities (and Supporting Capabilities for) Collecting, Reusing, Managing/Orchestrating Behavioral Customer Data.

The management, storage, and analysis of data, due to its volume and analytical complexity requires considerable skill. Machine learning (including artificial intelligence) plays an important role in classifying raw data and in making forecasts or predictions. Knowing in advance how much data to store, for how long, and what kinds of analytical algorithms to perform is beset with uncertainty because final usage is often unclear. We call this process of storing and analyzing data seizing.

Determining how and where to use the results of the analysis is also challenging. Again, the value of the refined data is uncertain because it can potentially be used in many situations beyond the contexts where it was collected.

The original innovator and consumer goods provider will find it hard to replicate the functionality of a digital platform. For example, Rolls Royce has become not only the producer of airplane engines with built-in sensors, but it has also developed a mastery of collecting and mobilizing user data. However, building these capabilities took considerable time and effort. Rolls Royce had a singular advantage: their customer list was small. Few consumer goods providers likely have the capabilities to undertake the task of collecting and managing their data in the way undertaken by established platforms.

Tesla is a consumer goods firm trying to overcome these challenges. Urban middle-class auto-owners spend many frustrating hours in their vehicles moving between locations. Frustrations exist because the urban driving experience consumes much time and effort. The opportunity for improvement requires two simultaneous developments: assisted (autonomous or, more plausibly, semi-autonomous) driving coupled with connectivity and the provision of entertainment (or business) services for occupants.

Tesla is currently attempting to resolve the first challenge (assisted driving), but solving this challenge is only an enabling feature. The value-added dimension will likely come from the digital platform firm that can provide the best connectivity with appropriate value-added services. Tesla has yet to demonstrate this latter, more demanding capability.

Entry Threat from Digital Platforms: Barriers, Bottlenecks, and Likely Outcomes

The producer of physical goods needs to consider the dangers of forming an alliance with an innovation (digital) platform firm, less so with a transactional one. One issue is that the fees charged may seem high for the services offered; the second and more significant danger is that the platform will obtain an entry point into the incumbent producer’s business, thereby reducing profit opportunities. The isolating mechanism protecting the incumbent producer’s business will be a key factor influencing both outcomes.

We predict that when the producer is engaging with a transaction platform to extend the customer reach for its offering, the dangers of deep disruption are slight. In almost all consumer goods spheres (and in most of the producer goods’ spheres), there are many such platforms, with Amazon Marketplace and eBay being the two largest firms in the consumer space. The fees charged for listing services in the consumer space are subject to strong competition as evidenced by the relatively modest margins admitted by Amazon for its marketplace business (approximately 5% on sales). All partnerships have risks, and there is always a possibility that the digital platform may enter, threaten to enter, or sidestep the incumbent’s business (for instance, by offering a private label). This is serious only in those cases where the incumbent producer has weak isolating mechanisms. Amazon has chosen to integrate backward into some of the businesses of those who list on its platform, but these are typically situations where there are easily accessible supply chains.

In sharp contrast, the situation with an innovation platform will be different since the platform firm can often improve the consumption experience directly at the point of purchase and indirectly by improving the product design and delivery system. The power of the digital platform arises less from scale, scope, and network effects and more from the superordinary and dynamic capabilities it may have to collect, store, analyze, and utilize data related to the use and purchasing preferences of consumers. These capabilities are resident in only a small number of platforms. Google and Apple appear to have strong, superordinary, and dynamic capabilities, resulting in good margins. Such capabilities typically require excellent management, and managerial shortfalls can result in market positions unraveling fast.

Leading U.S. innovation platforms utilizing the capabilities discussed above have proven to have considerable capabilities for vertical integration into the physical goods businesses—Apple into the business of making smartphones and smartwatches, and Google into the business of designing integrated circuits. Any alliance with any innovator platform will draw the platform firm close to the producer’s business and allow it access to typically closely held information about product design and the processes of production. The threat that the platform will eventually enter is real. Unless the traditional consumer goods firm has the relevant dynamic capabilities and makes the investment to run its own digital platform, it will be left with the choice of whether to ally or not ally, with the latter leading to being closed out of a superior digitally enhanced offering. Neither are attractive options.

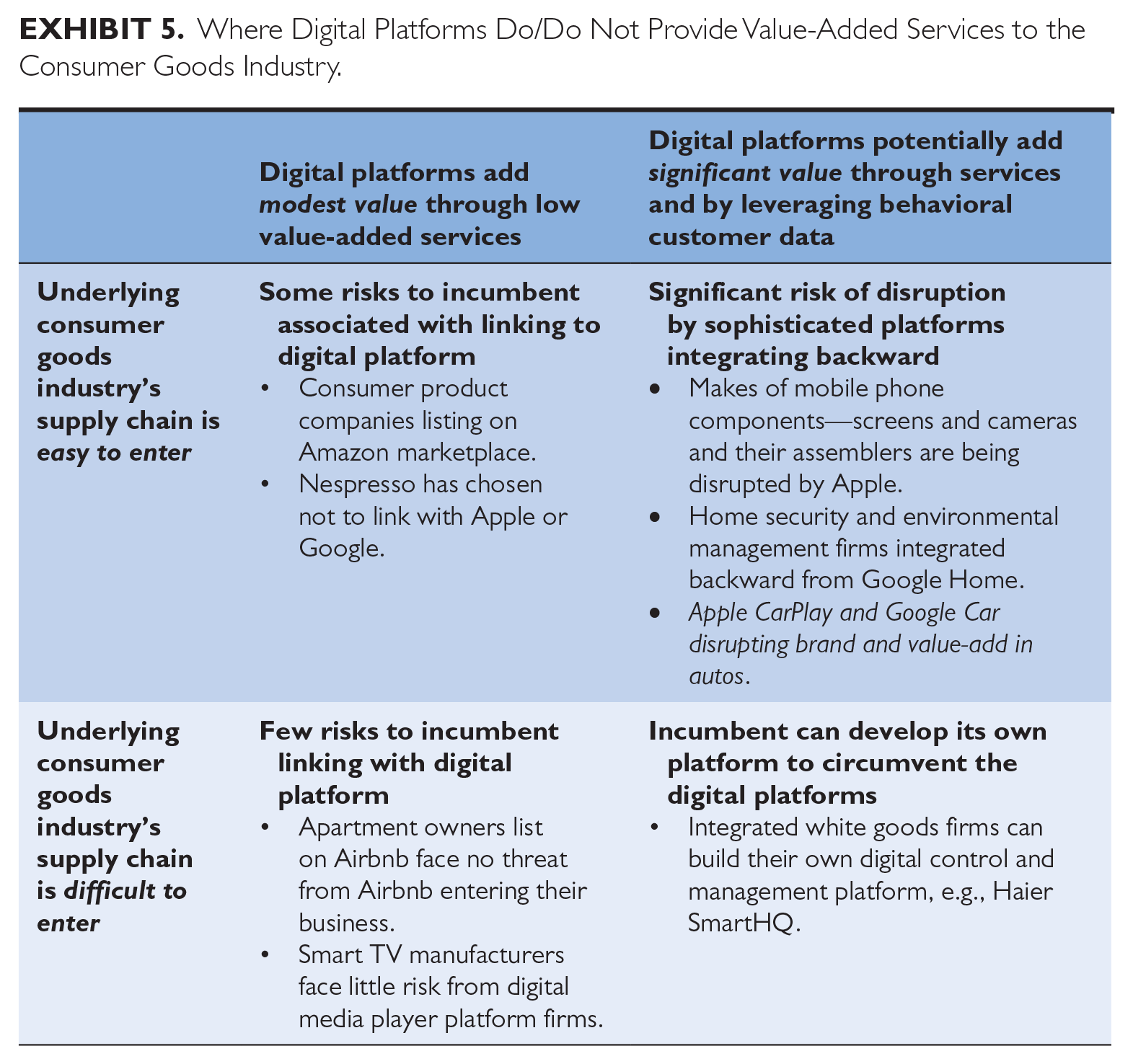

We summarize our predictions for bargaining positions and entry risks in Exhibit 5, with isolating mechanisms/entry barriers on the vertical axis and the type of platform on the horizontal. On the left side of Exhibit 5, we show the examples discussed earlier of firms linking with either Amazon Marketplace or Airbnb. Here, we mention Nespresso, a firm that has tried to add a digital dimension with little success, as the Nespresso machine has not been able to significantly improve the consumer’s experience of drinking coffee beyond providing a machine that is well-designed and convenient. Despite holding patents, Nespresso has not been able to prevent rival coffee producer-distributors from producing coffee pods to fit its machine, and it has sought alliances with Starbucks (a physical platform) and Amazon (a digital transactional platform) to distribute its coffee more effectively. 48

Where Digital Platforms Do/Do Not Provide Value-Added Services to the Consumer Goods Industry.

Regarding the right-hand side of Exhibit 5, relating to innovation platform firms invading the incumbent producer’s business, we return to our earlier example of the mobile phone. Innovation platforms, particularly Apple with its iOS operating system, have been able to significantly alter the functionality of a mobile phone, transforming it from a phone with a limited number of related applications (contacts, messaging, etc.) to a mobile media computer with a phone app. This functional inversion has allowed Apple to capture a commanding share of the profits generated without having to backward integrate into the production and assembly of mobile phones. It has encouraged platform partners and curated the final customer experience via the App Store. A significant proportion of the phone’s value added is captured by Apple, with most of the rest being shared by digital application providers. 49 Very little profit is left for those making the phone and its components. Although Google has only embraced a limited strategy for integration back into assembling and supplying the physical phone with its Pixel devices, it has also been able to capture significant value from adding its operating system and core applications, leaving phone suppliers in the position of supplying what seems to be a “commodity like product” in a high-income generating ecosystem.

In sharp contrast to the mobile phone industry, we place “smart television” in the bottom right-hand corner, a place where innovative digital platforms have alliances with innovation platforms, but where these platforms (Google and Apple and others) are unable to challenge incumbent producers of physical goods. It seems that two factors are at work. First, existing mobile devices can be relatively easily connected to smart TVs, and second, high-quality televisions are essentially two components: the screen and a sophisticated control unit; both the production of screens and the development of control firmware are subject to very significant scale economies and complexities that make it difficult for an outsider to enter.

The automobile is now presenting a fertile ground for enhanced digital experiences. Established innovation platforms such as Apple (with Apple Play) and Google, and newer innovation platforms such as MirrorLink and Baidu CarLife in China, have the (yet unrealized) potential to transform the experience of the driver and passengers in the automobile along multiple dimensions that range from route finding, various levels of autonomy, improved safety and navigation, improved audio, and (for passengers) visual stimulation via network-delivered music and movies. Given that many U.S. consumers spend a lot of time in their cars, the opportunity to bring improved connectivity, entertainment, and other information services into the vehicle is a significant business opportunity. Currently, existing innovation platforms can achieve some limited performance enhancement by connecting a mobile device (such as a phone or tablet) to the automobile’s electronic systems. However, as Tesla has shown, significant adjustments to the entire user interface are required to achieve any significant breakthrough. Unlike the internal combustion powertrain, the electric auto, with its combination of motors and control systems, has been shown to be amenable to some specialist outsourcing— potentially presenting the same opportunity for disruption that was discussed above in connection with smartphones.

The transition from internal combustion to electric engines also affords an opportunity for digital platforms to create strategic choices for the incumbents. One possibility is that existing auto-assemblers can form alliances with Apple and Google to access advanced digital services. To date, many of the leading auto-producers have kept these firms at arm’s length with partnerships that have limited scopes. 50 Another combination has already occurred, namely, the arrival of an entrant—Tesla—that is already commanding a significant share of the EV segment with software-hardware systems that have been shown capable of controlling a wider variety of experience-enhancing services.

However, as evolution in electric vehicle platforms increasingly lowers powertrain-related barriers to entry, there will be new opportunities for innovator platforms to try to enter the industry. If they succeed (by no means assured), they will have an opportunity to command a significant share of the value created by digital enhancement, while the component suppliers of drivetrains and chassis may be relegated to the position of “mere actors in the extended supply chain system.” 51 Provocatively, we place the future electric auto-industry in the top right-hand box of Exhibit 5 because it is possible that digital enhancement will disrupt the traditional auto-environment.

Our framework suggests that the incumbent automobile companies are confronted with a deep dilemma. They recognize the benefit of popular features like Apple CarPlay provided by digital platforms. On the other hand, adoption means that over time, Apple and other platforms may be in possession of data assets and user information that will give them a privileged position with users and hence, ultimately, with customers. As with Apple CarPlay (and similar technologies that platforms such as Google already has, and Microsoft could develop) a larger and longer part of the customer experience with the automobile is likely to define the mobility experience. This would enable the platform’s brand, if developed properly, to usurp the automobile manufacturer’s brand. The realization of this potential risk might explain why GM has abruptly dropped Apple CarPlay. We interpret this move as GM’s belated recognition as to the merits of our predictive framework. This epiphany is supportive of the predictive framework developed here. However, it’s not clear whether GM has a viable alternative.

Finally, we examine the actions of an established producer of physical goods into the data orchestration sphere, in this case, for home ecosystems. This firm is Haier, located in the People’s Republic of China, originally a state-owned firm, now listed. It is the world’s largest producer of domestic appliances with extensive international operations. It is well known for its innovative approach to manufacturing and distribution, and it has inspired several academic articles pointing out some of its exemplary management approaches to quality and customer engagement. In March 2019, Haier launched its “Smart Home Solution” strategy in recognition of the importance that Haier attaches to these initiatives. On July 1, 2019, Qingdao Haier Co., Ltd. officially changed its name to “Haier Smart Home Co., Ltd.” Haier Smart Home is organized using what the company refers to as its “5 + 7 + N” system. These systems are related to five home scenarios: smart living room, smart kitchen, smart bathroom, smart balcony, smart bedroom, and seven whole-house solutions for air, water, clothes care, security, voice control, health, and information. N represents user customization of the experience.

Based on public announcements and conversations with executives in the company, it seems clear that Haier intends to build in-house capabilities to orchestrate the collection, storage, analysis, and leverage of customer behavioral data. As indicated above, this will be a significant task. Outsiders may be lulled into thinking that the task facing Haier and similar firms is easy because data orchestration can be cheaply achieved using outsourced platforms such as ChatGPT. Such strategies are fraught with risk. Large language models have been shown to produce “hallucinations.” For data orchestration to work in the context of this article, we follow the thinking of data scientists who argue that there needs to be a careful approach involving the building and employment of dynamic capabilities. These will include the capability to balance supervised learning, large language models, formal modeling, and human intervention when manipulating data. It will be a few years before the superordinary 52 and dynamic capabilities needed to launch a successful in-house platform become commoditized. Meanwhile, firms such as Haier have an expensive and difficult road to travel.

Haier appears to have strong superordinary and (dynamic) capabilities in many areas; it may be able to establish itself as an important innovator platform firm. This may help Haier migrate its brand identity and its source of profits from the underlying appliance hardware toward being a data orchestrator and innovator of services—feeding continuous customer feedback and IoT data streams into product services and design evolution.

Discussion and Conclusion

In traditional physical goods industries, our understanding of the economic issues has been shaped by the writings of great industrial economists such as Ed Mason, Joe Bain, and Mike Scherer, economic historians such as Alfred Chandler, and strategy scholars such as Michael Porter. Observing the pre-digital era, they argued that the producer’s profits are typically derived from production and distribution scale and scope economies, coupled with (in the case of Porter) the choice of industry and position in the industry. More recently, economists have argued that in digital goods markets, competitive advantage is also anchored by similar production and distribution scale and scope economies with the added issue of network effects.

We offer a different perspective. In digital markets, the advent of digital orchestration capabilities has recently signaled an innovation pathway that involves engaging with customers, collecting data about how customers choose and consume, and using these data to improve the offering. These capabilities are quite different from those of traditional product innovation, and they benefit from very different scale and scope economies. These economies arise from utilizing data orchestration capabilities rather than traditional production economies.

To date, there has been limited discussion in either the academic or business practice literature of what happens when physical and digital industries collide, and when data manipulation to add consumer value is taken into consideration. How do scale and scope economies related to physical goods marry up with the digital scale and scope economies related to data orchestration? A full discussion of the complexities of this issue is beyond the scope of this article, but we suggest they are best considered as complementary (rather than substitutable) challenges that take place in different, but linked, organizing spheres.

A key issue is the isolating mechanisms surrounding the physical goods firm’s supply chain; if these are strong, an alliance may work well, enhancing profits for all parties. However, where the isolating mechanisms are weak, alliances may bring dangers to the incumbent physical good’s producer resulting in difficult negotiations and, in extreme situations, deep disruption.

The opportunities to ally with a value-adding (innovation) digital platform come from accessing that platform’s capacities to sense, collect, store, analyze, and leverage behavioral customer data that subsequently reshape the consumer’s experience in radical ways. It is not the behavioral data (an asset) alone, but rather the data combined with strong dynamic capabilities possessed by the platforms that lead to these consequences. Moreover, the required digital capabilities are not easily assembled by established consumer goods firms. The uncertainty thus created means that physical goods producers cannot fully anticipate the benefits of the alliance until after it has begun. Our analysis also points to the risks of incumbents allying with innovation platforms. The threats from these platforms come from their ability to enter the physical world, significantly altering the dynamics of industries as they did with mobile phones.

We did consider, albeit briefly, the situation where the physical goods producer can credibly set up its own internal digital data orchestrating platform. We noted that the technical challenges to this pathway are currently very great, although the rapid evolution of digital technologies may change this in the coming years. These challenges include the competitive challenges for the producer in achieving the necessary scale and scope required to collect the relevant data and amortize the costs of running the operation.

Finally, the framework here is in many ways an extension of the “profiting from innovation model.” 53 However, the focus is less on the impact on the innovator (in this case, the digital platform) and more on the impact on owners of complements, especially complements associated with the production of physical goods. It indicates how and when the complementor (the physical goods incumbent) is likely to be disrupted. Of course, when this happens, the digital platform is likely to keep a greater share of the profits from innovation. The article indicates how complementors with strong “sensing” can avoid pitfalls and experience epiphanies before it is too late.

Footnotes

Notes

Author Biographies

Charles Baden-Fuller is Centenary Professor of Strategy, Bayes Business School (formerly Cass), City St Georges (formerly City), University of London; Senior Fellow, Wharton School, University of Pennsylvania; and Fellow of The British Academy. (

John Blair is a co-founder and managing director at Berkeley Research Group. He has been a strategic advisor to some of the world's largest technology firms, including IBM, Apple, Adobe, and Oracle. Prior to coming to the United States, he led the software engineering team that brought to market the Dulmont Magnum, the world’s first 16-bit laptop computer. (

David Teece is a Professor at the Graduate School at the Haas School of Business at the University of California, Berkeley. He is also the founder and executive chairman of Berkeley Research Group. (