Abstract

This article discusses how Chinese multinational enterprises internationalize in an era of increasingly fractured globalization. It introduces new perspectives that identify and describe four strategic pathways these multinationals employ while acquiring strategic assets and building and leveraging capabilities to increase value from their international presence. The pathways—bouncing up, down, sideways, and back—depend on the multinationals’ strategies and the evolution of their internationalization. The pathways are distinct yet intertwined and influenced by powerful non-market forces, including geopolitical tensions (U.S.-China rivalry in particular) and Chinese domestic regulatory intervention. These dynamics manifest themselves in globalization, de-globalization, and re-globalization shifts.

This article is about the rise of Chinese multinational enterprises (MNEs). Understanding their internationalization is crucial for several reasons. With the rise of China as a major global superpower, for the time being second only to the United States, 1 Chinese MNEs have become increasingly important in international business. 2 The revenues of Chinese companies on the Fortune Global 500 list in 2022 exceeded those of U.S. companies. 3 The volume of Chinese outward foreign direct investment (FDI) was consistently ranked in the top four in the world between 2012 and 2021. 4 In many industries, including the manufacture of electric vehicles and commercial drones and solar power and shipping, Chinese firms are among global leaders. 5 Increasingly, Chinese MNEs successfully operate in high-value and high-technology sectors such as artificial intelligence, supported by their home-country government. The rise of Chinese MNEs is also intermeshed with a worldwide geopolitical rivalry, especially between the United States and China.

The rise of Chinese MNEs requires a re-evaluation of both well-established and more recent explanations of MNEs’ internationalization. Without such re-evaluation, it is difficult to understand Chinese MNEs and provide helpful implications for their managers and managers of their competitors. To address this, the present article is informed by and contextualizes the following sets of MNE concepts: capability-based strategy 6 (capability building, capability leveraging, and the related concept of strategic asset acquisition 7 ); the evolution of firm internationalization (including the related concept of springboarding 8 ); and non-market forces (U.S.-China rivalry, domestic regulatory intervention, 9 and the related concepts of globalization, de-globalization, and re-globalization, which underpin the notion of fractured globalization). 10 Overall, Chinese MNEs deserve very close attention as a stand-alone subject of research instead of bundling them with MNEs from other countries. A more nuanced and up-to-date understanding of these MNEs’ internationalization strategies is also critically important for their competitors and regulators.

De-Globalization, Re-Globalization, and Non-Market Forces Impacting Chinese MNEs

Recent developments point to the advent of de-globalization—a decline in the global levels of interdependence and integration among countries—as a new challenge for companies strategizing across borders. 11 De-globalization is associated with periods when international trade, investment, and other interactions between countries (e.g., flows of people and intangibles) weaken. 12 It manifests itself in phenomena such as the home reshoring of value creation; global value chains’ reconfiguration toward more regional sources 13 ; increased regulatory scrutiny of foreign trade and acquisitions; policy and regulatory changes that favor domestic interests/agendas; and other restrictions on international trade, investment, travel, work, and residence (e.g., pandemic induced).

De-globalization introduces several difficulties for Chinese MNEs. 14 First, it makes it more challenging for them to acquire applied technology, advanced machinery, key components, crowdsourcing, latest instruments, sophisticated materials, and industrial designs from advanced country firms or subunits. This results in reduced transferability of capabilities between host and home countries. Second, the increasing political and economic separation and disengagement of China and the West make it difficult for Chinese MNEs to execute their internationalization strategies due to new laws and regulations that explicitly target Chinese firms. For example, the new U.S. export restrictions on semiconductors effectively bring all of China under the special rule formerly reserved for Huawei. Other countries, such as Canada and Australia, have also targeted Chinese firms with restrictions in sectors ranging from metals to power generation. Third, de-globalization further increases institutional distance—understood as the differences in regulations, norms, and cultural cognitions 15 —between China and Western countries. This constitutes an obstacle to the global expansion strategies of Chinese MNEs. For example, the increasing data surveillance in China starkly contrasts with growing concerns about data privacy in the United States and the European Union, creating additional costs and accelerating difficulties for Chinese firms operating overseas.

The difficulties Chinese MNEs face relate to two salient non-market forces. First, they are associated with the increasing geopolitical tensions and decoupling of China and the United States, the process of weakening interdependence between these two global powers, which is related to their differences over economic rules, values, and national security. 16 The intensifying rivalry between the world’s two largest economies has consequences for MNEs’ strategic decision-making and actions. 17 For Chinese MNEs, it can lead to unfavorable treatment by foreign governments, especially the United States and its allies. For example, Chinese tech firms Huawei, ByteDance, and Alibaba, as well as shipping giant COSCO, have been impacted by the geopolitical tensions not only in the United States but also in their operations elsewhere. Huawei’s operations in Europe and Alibaba’s and ByteDance’s in India are cases in point.

De-globalization faced by Chinese MNEs is also associated with the increasing impact of the Chinese state regulatory intervention that has hit internationalizing domestic players. 18 For example, the Chinese regulatory crackdown on Chinese tech firms, particularly Chinese MNEs listed in the United States, has profoundly impacted several firms, including Alibaba (listed on the New York Stock Exchange since 2014), Tencent, and ByteDance. The crackdown affected some firms from outside the tech sector, such as Chinese retailer Suning, the owner of the Inter Milan (Milan, Italy) soccer club. 19 Other domestic regulatory interventions affecting Chinese MNEs include fines, restricted capital outflows, and in-depth investigations of tax fraud or corruption allegations.

The Chinese state’s acquisition of “golden shares” (i.e., 1% stakes with special rights over business decisions) in private tech companies, including ByteDance’s and Alibaba’s subsidiaries (with talks of acquisition of similar shares in the whole Alibaba Group and Tencent), reinforces this point and shows that the impact of geopolitics and Chinese regulatory intervention are inter-related and possibly mutually reinforcing. 20 Chinese state intervention can exacerbate the impact of geopolitical tensions and resulting regulations in the United States and its allies, and U.S.-China rivalry can spark new regulations in China and abroad in the areas of technology and data privacy.

Under such political pressure, Chinese firms’ efforts to gain legitimacy in their Western locations could be ineffectual. Consider this: despite the $1.5 billion Project Texas initiative to further improve the protection of TikTok’s U.S. users’ data (already housed in the United States on U.S. tech firm Oracle’s servers from 2022), TikTok has still been banned on public sector devices in the United States and in several other countries and faces an outright ban or forced sale in the United States after the Congressional Hearing in 2023. 21 The non-market forces exert a complex and cumulative impact on Chinese firms’ internationalization in the current global environment. This arguably requires revisiting old truths and generating new research insights.

Globalization/de-globalization is not a simple dichotomy; there is the possibility of re-globalization. Re-globalization can be interpreted as a relaxation of de-globalization 22 (e.g., a somewhat “reduced temperature” in the U.S.-China rivalry after the Bali G-20 summit or the seeming lull in Chinese regulatory crackdown on local tech firms in late 2022). 23 For example, Hesai Technology, a Chinese sensor maker, was listed in the United States in February 2023 in the biggest Initial Public Offering (IPO) by a Chinese firm in the United States since 2021. This resulted from progress in late 2022, as the Public Company Accounting Oversight Board in the United States reached an agreement with the Cyberspace Administration of China and the Chinese Ministry of Finance to inspect audit documents of Chinese companies listed in the United States. 24 At a deeper level, re-globalization can also be characterized as a structural reshaping of globalization that changes its nature and renews the trend of globalization, albeit in a different form. 25 For example, the recent “Cold War II” and decoupling between the United States and China are reshaping allied economic blocs, 26 resulting in the need to better understand which countries are “friends,” “foes,” or (somewhere in between) the so-called “frenemies.” 27

The implication of re-globalization for Chinese and other MNEs is that it may be important to carefully select investment locations in relatively politically friendly or neutral territories. 28 This strategy of friend-shoring (relocating to countries that offer suitable context for a firm’s activities and are allies of China, or at least unlikely future allies of the United States) is particularly relevant for Chinese firms in industries with relatively higher strategic importance. 29 Re-globalization is a logical next phase as the phase of de-globalization transforms into a new form of globalization. 30 While re-globalization can be interpreted as the bifurcation between U.S.- and China-led blocs due to their decoupling, it is also important to consider the cohesiveness, changing composition, size, and growth of these blocs; the dynamics of interdependence within and between them; and the degree to which countries are aligned or not aligned with the blocs. Considering the above discussion, fractured globalization can be defined as the shifts in globalization, de-globalization, and re-globalization. Given the dynamic nature of the international business environment, we view fractured globalization as a process rather than an end result of these shifts. 31

To summarize, the ongoing uncertain and conflicting processes of globalization, de-globalization, and re-globalization constitute new realities that could reshape and redefine Chinese MNEs’ internationalization strategies and pathways. These strategies are linked to non-market forces, including the evolving geopolitical tensions and related policies and regulations by the United States and other governments, especially in the West, and the home-country regulatory intervention by the Chinese state. In both areas, we will likely see continued uncertainty about whether the geopolitical tensions and/or regulatory restrictions and state intervention will ease, resulting in re-globalization, or continue and escalate, leading to de-globalization. 32 Finally, while there is evidence of de-globalization in some areas, the world has become incredibly interconnected, and many expensive-to-break ties will continue to bind us in the new realities. 33

Understanding Chinese Multinationals’ Internationalization Strategies: New Realities Require New Perspectives

In light of the shifting non-market forces just described, it is important to understand the context of changes in Chinese MNEs’ internationalization strategies in general and in their cross-border mergers and acquisitions (M&As) in particular. M&As have been an important strategic tool for Chinese MNEs’ international growth since the early 2000s and were encouraged by China’s Go Out policy, a national strategy for economic development. 34 De-globalization trends after 2015 included new national priorities and led to less emphasis on “going out” and increased attention to domestic high-tech development, as indicated in the Made in China 2025 strategic plan released in 2015, 35 as well as the increasing Western pushback against Chinese M&As since 2016. 36 Both trends have significantly dented Chinese firms’ cross-border M&As. As a result, China’s share of global cross-border M&A value has fallen substantially from the peaks of close to 20% in 2013 and 2017 to about 4% in 2018-2021. 37 There was a notable shift of M&As to domestic deals by Chinese firms in 2020; outbound M&As from mainland China remained below pre-pandemic levels in 2021 38 despite global cross-border M&As surging to an all-time high in 2021. While the first half of 2022 saw a mild resurgence of Chinese outward M&As, their value was still four times smaller than their peak in 2016, and 2022 saw a 52% annual decline. 39

The changing trends in Chinese outward M&As can be attributed to non-market and firm-level factors. The latter refer to many Chinese firms being in a relatively more advanced stage of their internationalization and to improved capabilities of Chinese MNEs and other Chinese firms in areas of technological innovation. 40 For example, Chinese firms in the automotive industry have made significant improvements in technological innovation related to electric vehicles. 41 This may have resulted in less need for acquisitions abroad and more opportunities for domestic acquisitions and organic growth at home and abroad via exports. 42

Firm Internationalization Evolution and MNE Strategies

In addition to non-market forces, Chinese MNEs’ internationalization can be further understood by considering two additional perspectives. The first relates to the evolution of firm internationalization—from an initial stage through an intermediate stage (characterized by a moderate degree of internationalization and internationalization experience) to an advanced stage (associated with a significant global presence and rich internationalization experience). The second perspective relates to firms’ strategies in selecting and executing growth paths and potential cross-border M&A targets. These strategies can be strategic asset acquisition, capability building, or capability leveraging. 43

Chinese firms have accumulated substantial financial resources that have empowered them to employ strategic asset acquisition abroad (e.g., acquiring foreign firms with cutting-edge technologies and know-how) as a way to achieve global competitiveness more rapidly than traditional advanced economy MNEs. 44 Chinese MNEs typically commence these acquisitions in the early stage of internationalization, subsequently focusing on capability building (including further M&As that facilitate it) in the intermediate internationalization stage. 45 Their aims include capability transfer from the locations of the acquired firms to China and China-centered capability upgrading. 46 In the advanced internationalization stage, Chinese MNEs often evolve to focus on capability leveraging. 47 This strategy centers around global expansion with stronger capabilities; the strategies (including M&As) focus on how they can facilitate home-centered capability transfer and upgrading and leverage capabilities into multiple other global markets. Capability building and leveraging link to firm internationalization strategies, that is, strategic motives and the pursuit and execution of the motives and plans, such as M&As, building wholly owned overseas operations, exporting, and transferring technology.

Capability leveraging focuses on the complex exploitation of capabilities, while capability building is primarily about creating, assembling, and applying new capabilities. 48 Capability leveraging implies capability use for maximum global advantage and relates to leveraging existing organizational strengths as opposed to launching new initiatives in MNEs. Chinese companies have excelled in global capability leveraging in recent years. For example, Haier, Huawei, ByteDance, Tencent, and Alibaba made huge leaps in the 2010s toward global ascendancy via a strategy of accelerated (primarily technological) innovation. Chinese companies have built and leveraged capabilities in various areas of innovation, 49 often sparked and fueled by cross-border M&As. For example, Chinese car maker Geely’s acquisition of Swedish Volvo in 2010 has contributed to improved innovation capabilities of Geely through introducing more innovative technologies and better design. A joint R&D center established in Sweden in 2013 led to a new modular vehicle platform used by both firms, resulting in a new automobile brand Lynk & Co, launched in 2017.

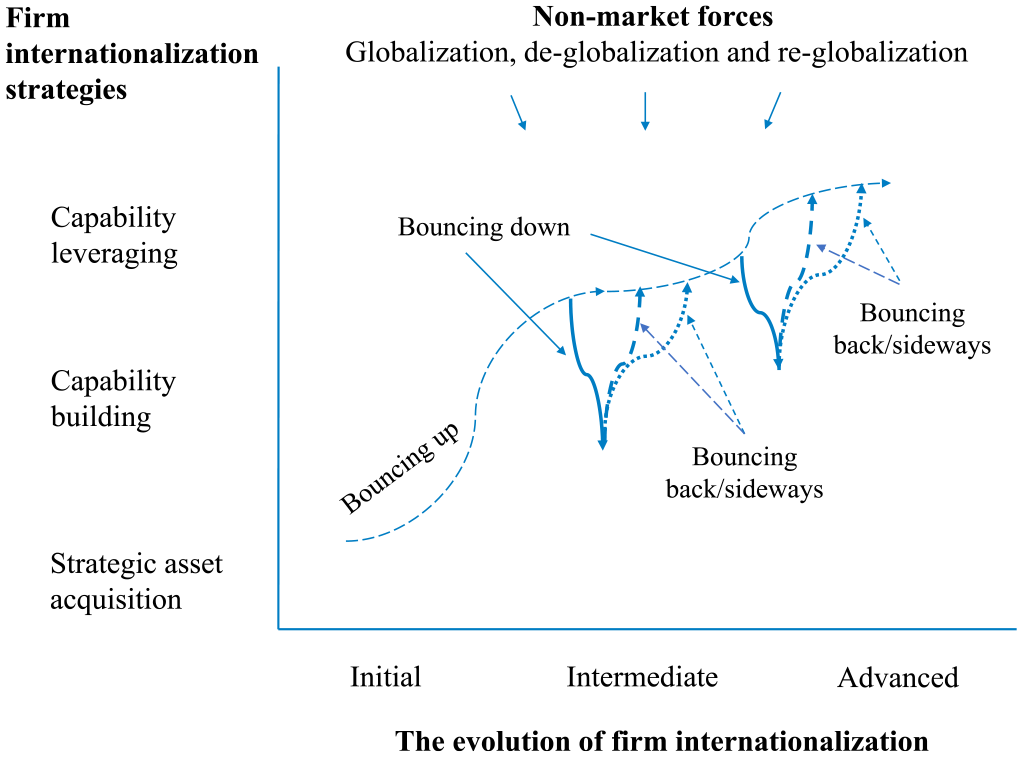

Figure 1 positions four pathways of internationalization in relation to key perspectives that can help to understand them: the evolution of firm internationalization, firm internationalization strategies, and non-market forces affecting MNE strategies and internationalization.

Firm internationalization pathways.

Four Pathways of Chinese MNEs’ Internationalization

Bouncing Up: Haier and Ctrip

Bouncing up is employed by Chinese firms that have adopted the “springboard” strategy. 50 Springboard MNEs aggressively acquire critical assets (technologies, brands, talents, and expertise), 51 typically via M&As in developed countries. 52 Many large, leading Chinese MNEs are prominent examples of this strategy, such as Geely’s acquisition of Volvo (Sweden) and Lenovo’s acquisition of IBM’s PC division (U.S.). However, Chinese MNEs are not always successful in their attempts to bounce up. For example, in 2009, Chinalco (Aluminum Corporation of China Limited) failed to acquire an 18% stake in Rio Tinto, the largest Anglo-Australian mining company, due to political intervention from the Australian side. Such non-market interference in global business likely plays an even bigger part in today’s business environment. 53

The bouncing-up pathway involves two elements related to MNE capabilities. The first is capability building in the intermediate stage of internationalization when firms have moderate internationalization experience and international presence, typically in the Chinese firms’ home region of Asia Pacific rather than globally. The second element involves capability leveraging, which includes capability-leveraging acquisitions after a successful capability transfer home. This is followed by combining and upgrading global capabilities to proceed with global expansion, with stronger capabilities, in the advanced internationalization stage. The firm has significant internationalization experience and global presence in this stage, typically beyond the home region.

Haier, a leading white goods manufacturer, is an example of this type of pathway. It proceeded from acquisitions of relatively smaller targets in the Asia Pacific in its intermediate internationalization stage to a transformational acquisition of targets in more distant regions, in the advanced stage, with the intent of becoming a global leader in home appliances and smart home solutions. For example, in 2012, it acquired Sanyo (Japan) for about $130 million and Fisher & Paykel (New Zealand) for $766 million. These acquisitions helped Haier with capability building, for example, in the areas of design and marketing of premium appliances. 54 In 2016, Haier acquired General Electric Appliances (U.S.) for $5.4 billion; it continued to leverage its capabilities in 2019 when it acquired Candy (Italy) for about $547 million.

The online travel firm Ctrip is another example of a Chinese company bouncing up. It has stayed the course and focused on expansion and acquisitions at home, in the Asia Pacific, and in the United Kingdom before proceeding with a global expansion at its advanced stage of internationalization. For example, Ctrip’s key acquisitions included the 2015 purchase of a 45% stake in Beijing-based online travel rival Qunar for $3.4 billion, followed by deals in the United Kingdom, including a 2015 purchase of transactional-payment platform Travelfusion for $160 million, and the $1.74 billion purchase of price comparison search engine Travelfusion, resulting in stronger capabilities. These deals were followed in 2017 by the acquisition of U.S. firm trip.com (with 3.5 million registered users) and the 2020 acquisition of Travix, a boutique Dutch travel group, to enhance synergies and leverage capabilities. 55

However, the bouncing-up pathway may be constrained under the pressures of de-globalization. In this case, the focus of this Nasdaq-listed company’s strategy may turn to the domestic market. It may also develop new technologies and business models in China first, then gradually expand to international markets when possible, especially since the Chinese government has started to ease the COVID lockdown/control measures and travel restrictions. Ctrip may also consider delisting from Nasdaq if the geopolitical situation or domestic regulatory intervention worsen and affect even firms in what seems now like relatively less sensitive or strategic sectors.

We offer three recommendations to managers of firms on this pathway. First, cross-border M&As should be driven by overall strategy (i.e., regional expansion and technological capability building) and should not be a purely financial investment. Second, synergy should be created between the MNE and the acquired firm. Third, do not lose sight of the home market, which should be the hub for technology, management, and business model innovations.

Haier is a good example of a company that did not forget about its holistic management system linked to its HQ, despite its aggressive international expansion. It uses its home-grown 人单合一(Rendanheyi) approach: Ren stands for people, in this case, the employees; dan refers to the value of customers or customer orders; and heyi means to become one, the alignment and coupling of employee benefits and customer needs. 56 Haier has consistently applied this approach as the foundation of its overall business and organizational model to transform acquired overseas companies.

Bouncing Down: Huawei and HNA Group

The bouncing-down pathway involves a rapid movement within one internationalization stage, from capability leveraging and aspirations to become a global player to more home- or home-region-centered capability building, including M&As with downgraded global ambitions. 57 While globalization has facilitated strategic asset acquisitions that served as a springboard for bouncing up, de-globalization and associated non-market forces may be seen as a ceiling that impacts firms and leads to bouncing down. For example, Huawei, with about two-thirds of its 2020 sales in China and about 20% of sales in Europe, Africa, and the Middle East, significantly pared down its global ambitions following sanctions by the United States and its allies. Sales in the Americas fell about 25% compared with 15% growth in China in 2020. In December 2022, the U.S. outright banned the sales of new Huawei equipment, 58 which is likely to further demolish this MNE’s global competitiveness.

Failing to manage the disruption brought about by unfavorable geopolitical pressures can also cause a company to lose its global competitiveness, which drives it to follow the bouncing-down pathway. Huawei’s previous ambitious acquisitions abroad (its 2013 purchase of Belgian photonics company Calopia and 2014 purchase of Neul, a U.K. maker of chips for the internet-of-things sector) aimed at accelerated global expansion, did not continue. Fortunately for Huawei, China alone represents a huge market. Consequently, the company was able to turn to home-centered acquisitions. It bought Shenzhen Xunlian Zhifu Network in 2021 to gain a mobile-payment license in China and acquired several local chip makers in 2020 to insulate itself from foreign risks.

In May 2019, the United States barred Huawei from receiving American components vital to the systems it sells, a clear demonstration of U.S.-China geopolitical tensions. As a response, Huawei started its own investment firm, Habo Investment, in 2019, which focuses on the semiconductor industry outside the U.S. market and especially in China, where it has invested in more than 60 Chinese domestic tech firms since its inception. Overall, Huawei’s domestic-centered investments have allowed it to reconstruct its supply chain and rebuild its semiconductor manufacturing and testing capabilities. The geopolitical challenge Huawei faced was “war-like.” 59 It was no longer the United States vs. China, as the United States encouraged many countries to boycott Huawei, including Australia, the United Kingdom, Singapore, and many EU countries, resulting in several bans on Huawei 5G telecommunications equipment. 60

Companies in an advanced internationalization stage can bounce down and sometimes even crash. An example is HNA Group, a conglomerate based in Haikou, China. It grew dramatically from a domestic airline to a Global Fortune 500 conglomerate through international acquisitions, including stakes in Hilton Hotels, Deutsche Bank, and Virgin Australia, fueled by debt. The firm was affected by both domestic and foreign regulatory scrutiny in 2017. In China, the government targeted it as it tried to curb debt-fueled M&As by Chinese firms, with concerns about the implications for the health of the Chinese financial system. In the United States, HNA Group abandoned its $416 million investment in U.S. in-flight services firm Global Eagle Entertainment after failing to clear a U.S. national security panel, partly due to data storage and privacy concerns. This added to the already significant uncertainty over Chinese deals with U.S. companies in 2017 in the early era of de-globalization. HNA Group’s rise came to a grinding halt after its overambitious acquisition spree unwound during the COVID-19 pandemic. From over $147 billion in assets in 2017, the company came close to liquidation in 2021, unable to repay its massive debt—a drastic paring down of its global assets and reach. The case of HNA Group shows that unbridled ambition to reach a leading global position in multiple industries can be hard to achieve. Instead, a more disciplined, focused approach to internationalization should be the preferred option.

We offer three recommendations to managers of firms on this pathway. First, think carefully about M&A synergies. HNA Group, for instance, did not pay enough attention to this during the acquisition of non-airline assets in Europe and the United States. Often, the MNE needs to turn around the acquired company; building synergy with the help of the acquired company can improve financial performance. Second, clearly define the roles of global and local subsidiaries. Third, do not keep global and local M&A companies isolated while pursuing business diversification. In the de-globalization era, MNEs may often experience poor connectedness between entities in various nations.

For example, BYD, the world’s biggest seller of battery electric vehicles and plug-in hybrids, delayed its launch of new EVs in the Australian market multiple times in 2022 due to its inability to comply with Australian regulations. This was mostly caused by the miscommunication between BYD HQ and its Australian distributor and network. To manage geographically diversified assets, MNEs should fully utilize their market experience and management models obtained during overseas expansion to decrease isolation and improve global network linkages.

Bouncing Sideways: ByteDance and Tencent

The bouncing-sideways pathway involves a gradual movement from capability building and related acquisitions to capability leveraging and related acquisitions. De-globalization makes this pathway more difficult. For example, there can be new restrictions on foreign acquisitions and fewer opportunities to conduct in-depth, in-person due diligence on the target firm, such as during the COVID-19 pandemic. However, this pathway may be enabled by re-globalization—the phenomenon that occurs after a period of de-globalization—which provides opportunities for friend-shoring or redirecting attention to acquire or leverage capabilities in relatively friendly or neutral territories. 61 While, at present, China may be viewed negatively in some Western countries that increasingly perceive it as a foe (e.g., the United States, the United Kingdom, Canada, and Australia, which have rather conflicted relations with China), other countries have a less negative view of China. Some view it as a friend (e.g., many African and Latin American countries that have cooperative or neutral relations with China). Others view it as a frenemy, for example, many countries in Asia, Europe (such as Germany, France, Italy, and Greece), and the Middle East (such as Saudi Arabia)—all of which have ambivalent relations with China. 62

ByteDance demonstrates the bouncing-sideways strategy. It operates TikTok, which, despite being the world’s most downloaded app in 2022, derived most of its $63 billion sales in 2021 from its China-based variant Douyin. The company executed capability-building acquisitions of French NewsRepublic (2017), Indonesian Baca Berita (2018), and U.K. Jukedeck (2019) as well as capability-leveraging acquisitions of Chinese/U.S. Musica.ly (2018) and Chinese virtual reality headset maker Pico (2021) in broadly the same internationalization stage. While ByteDance’s acquisition of Musica.ly in 2018 was motivated by capability leveraging and a desire to become a global player, its more recent move in 2021 was targeted at acquiring Beijing-based Pico, pitting it against its global archrival Meta, mirroring Facebook’s acquisition of virtual reality company Oculus in 2014. The acquisition of Pico will help ByteDance develop its metaverse ecosystem integrating social media, games, and virtual/mixed reality hardware. In 2022, ByteDance also acquired Amcare Healthcare, one of China’s biggest private hospital chains, for over $1 billion (closely following U.S. rival Amazon’s acquisition of One Medical) and was pushing into at least half a dozen other industries.

The ByteDance case shows that companies can reevaluate and reconfigure their internationalization and acquisition strategies. For example, global expansion with stronger capabilities can be accomplished with acquisitions closer to home or in politically neutral countries (e.g., acquiring a strong, innovative target at home can be motivated by leveraging its capabilities to gain global prominence) or other strategic actions related to location choice. With the United States and its allies increasingly viewing ByteDance as a potential national security threat, the company’s decision to locate the CEO of TikTok in Singapore could be seen as an attempt to bounce sideways. However, this move has been questioned, with the CEO balancing being an autonomous leader and meeting the demands of the Chinese parent company. 63 Also, similar doubts were raised about TikTok’s latest Project Clover initiative—establishing an EU-based data center to gain legitimacy from the EU regulators. Therefore, ByteDance’s bouncing-sideways efforts such as Project Clover may not be enough if geopolitical tensions increase. The United States, Canada, the United Kingdom, and New Zealand have forbidden the use of TikTok on government devices, with EU institutions and countries such as Belgium and Denmark adopting similar bans. There have also been suggestions of a total ban or forced sale of TikTok in the United States, and the Congressional Hearings on TikTok in March 2023 further increased the company’s vulnerability to geopolitical pressure. 64

ByteDance has also suffered from Chinese regulatory interventions like the crackdown on local acquisitions in China in 2022 and new regulations on social media use by teens. Therefore, caution is needed as de-globalization is sparking sweeping changes to domestic regulations in China; indeed, the link between home-country regulations and internationalization strategies/processes should not be underestimated. 65 For example, in 2022, the Cyberspace Administration of China released a new regulation that limits investment by Chinese tech giants in China-based startups with customer bases of 100 million or more or significant revenue (RMB 10 billion or over) due to cybersecurity concerns. As a result, several Chinese tech giants, including ByteDance and Tencent, significantly and abruptly reduced their home-centered investment teams. Tech companies also faced stringent new social media and online gaming regulations in China in 2021-2022, with regulatory risk and uncertainty remaining high in 2023. 66 This may likely push Chinese tech MNEs to attempt to acquire targets in other innovation hubs such as Silicon Valley, Singapore, and Berlin, although they may face increased regulatory and political scrutiny there, too.

For example, Tencent Games, the gaming division of China’s internet giant Tencent Holdings, undertook an internationalization strategy via acquisitions, resembling bouncing sideways. Most notably, in 2013, Tencent Games acquired a 40% stake in Epic Games (U.S.)—which owned Unreal Engine, the industry-leading game development program used by worldwide game developers—and developed several major gaming titles, such as Gears of War and Fortnite. In 2015, it fully acquired Riot Games (U.S.), the developer of League of Legends—a long-standing professional e-sports competition (this title joined Major League Gaming, U.S., in 2011). These acquisitions helped Tencent Games become one of the world’s largest gaming companies alongside Microsoft (Xbox) and Sony (PlayStation). It absorbed its overseas assets while expanding and reinforcing its domestic and Chinese market dominance. Specifically, Tencent’s acquisition of Riot Games has contributed to the global market dominance of Tencent’s gaming division by allowing it to create new games based on the existing popular gaming franchises previously owned by the acquired firms. 67

In recent years, with the pressures of economic decoupling and de-globalization, Tencent Games shifted from focusing on U.S. acquisitions to somewhat more neutral territories. For example, in 2017, it bought 13.5% of Krafton (South Korea), the developer of PUBG: Battlegrounds, a popular game on par with Fortnite and League of Legends. It has also ramped up dealmaking in Europe amid regulatory overhang at home (e.g., a crackdown on local acquisitions and limiting under-18s in China from playing online games more than three hours per week), with Europe and Asia eclipsing the United States as the top regions for Tencent’s gaming M&A targets in 2019-2022. Tencent also bought stakes in European game studios based in Sweden, Finland, France, Germany, the United Kingdom, and the Czech Republic. Seven of Tencent’s top 10 M&A deals in 2020-2021 involved companies in Asia Pacific, and another two involved European targets.

We offer three recommendations to managers at firms on this pathway. First, create an innovation center to connect with key innovation hubs in friendly or neutral territories at home and/or abroad and move away from a focus on Silicon Valley. 68 Second, establish an investment team with local deal experience. Actively seek strategic investment opportunities in target companies in the early stages of their life cycle. Chinese firms funded many U.S.-based tech startups, including geopolitically sensitive space technology, but may redirect this funding to other territories. Third, do not ignore the need for synergy between home- and host-country entities. Some of the Chinese tech giants’ operations in Silicon Valley failed due to the lack of synergy between Chinese and U.S. units. This was partially due to technology transfer limitations related to Chinese and/or U.S. regulations but also reflected different market dynamics in the two countries.

Bouncing Back: Alibaba and COSCO

The bouncing-back pathway involves recovering from a bounce down and, shortly after a period of pared-down global ambitions, regaining vigor and resuming capability-leveraging strategies, including international M&As and operations aimed at global expansion with stronger capabilities. This is a developing strategy discerned during the advanced or post-de-globalization era, and it is too early to establish clearly which companies can execute it successfully and how. While Chinese tech giants such as Huawei and Alibaba have arguably experienced a bounce down, there are signs that they are both starting to attempt to bounce back. Bouncing back requires a thorough reconfiguration of growth strategy in the face of the uncertainty created by de-globalization and re-globalization. 69

Alibaba’s initial bounce down was related to its retreat from major capability-leveraging acquisitions, such as Lazada of Singapore for $1 billion 70 and Trendyol of Turkey for $750 million, to smaller acquisitions at home (e.g., China-based table-booking app named Delicious Without Waiting), and in near abroad (e.g., HungryNaki from Bangladesh). However, the company is attempting a bounce back. Alibaba’s acquisition of Sun Art Retail in Hong Kong for $3.6 billion in 2020-2021 can be seen as a capability-leveraging move that could help it to diversify to grocery retail (e.g., for developing its Hema Fresh supermarket chain) and improve its hybrid retail options globally, mirroring a similar strategy employed by Amazon in its acquisition of Whole Foods in 2017.

More recent developments indicate an additional change in Alibaba’s investment strategy in 2022. Because of domestic regulatory developments like the crackdown on acquisitions of local targets, Alibaba suspended almost all of its domestic acquisition activities. 71 The new rules limited its new investment and exit strategy, namely, the initial public offering. 72 During Alibaba Investor Day 2021, Alibaba Group’s CEO Daniel Zhang announced the restructuring of the Group from function-based (business-to-business and business-to-consumer) business groups to domestic- and international-focused business groups. This had the potential to push international-focused M&As/investment further, although Alibaba may face increasing restrictions in many countries because of its involvement in a government-sponsored race to develop world-leading artificial intelligence capabilities. An additional geopolitics-related setback was that Alibaba’s cloud computing business had been examined by the United States in 2022 to determine whether it posed a risk to U.S. national security. Hence, Alibaba faced the significant impact of both rising China-U.S. rivalry and Chinese regulations. In 2023, Alibaba announced a major restructuring into six groups, which was hailed as a move to make it more agile and better able to withstand regulatory pressures. 73

COSCO offers a powerful example of how Chinese firms can reach an advanced stage of internationalization and bounce back to leverage and further expand their capabilities to gain competitiveness as global players. COSCO is the world’s largest shipping company by revenue, with about a 50% global market share in shipping container manufacturing. However, it has not all been easy sailing for COSCO. For example, former President Trump forced COSCO to relinquish Port of Long Beach ownership over national security concerns. The Trump administration also imposed sanctions on two COSCO subsidiaries because these companies continued to import Iranian oil in contravention of the U.S. secondary sanctions on Iran. COSCO responded to these initial de-globalization setbacks by acquiring a company closer to home, namely Hong Kong-based OOCL. This move made it the biggest container carrier shipping goods to the United States.

COSCO’s acquisitions of ports in Greece and Germany illustrate how the company bounced back to become a global player. In Greece, it was intent on the Port of Piraeus, one of the global top 50 ports, since the global financial crisis and Greece’s near-bankruptcy in 2009. COSCO faced several difficulties in the acquisition process, including pressure from the European Union and the United States. It eventually succeeded in 2016 when the Greek government approved the privatization of the Port of Piraeus, given the value added by COSCO for the local community. 74 In 2021, COSCO successfully raised its stake in the Port of Piraeus to 67%. In 2022, the company faced even stronger geopolitical concerns when it attempted to buy a stake in the Port of Hamburg in Germany. After the Russian invasion of Ukraine and the subsequent controversies around China’s strategic partnership with Russia, Europe is increasingly reevaluating its dependence on these two countries in strategic industries. For example, Germany’s intelligence service chiefs warned in late 2022 that China could use stakes in critical infrastructure as leverage to pursue political aims amid a debate in Berlin over whether to let COSCO invest in the Hamburg port. 75

Despite political opposition, the German government approved COSCO’s acquisition of 24.9% of the Port of Hamburg instead of the initially proposed 35% stake. The justification was that COSCO would bring needed investment and, with a minority stake, would not significantly affect the port’s operations and management. COSCO’s example shows that, with the right strategy (in this case, a more hands-off approach and smaller stakes acquired), Chinese MNEs can become or remain leading global players even in relatively sensitive sectors. They can bounce back after being impacted by economic decoupling in the era of de-globalization and re-globalization. 76

We put forward three recommendations to managers at firms on this pathway. First, get involved with governments and stakeholders in target nations. This can remove the hurdles when acquiring sensitive assets. Ant Financial’s failed attempt to acquire MoneyGram is an example where Congress blocked the deal during the U.S.-China trade war. At the same time, COSCO’s engagement with the Greek government and the local community is an example of involvement with governments and stakeholders. Second, build strong post-M&A management capabilities. Chinese MNEs often focus on deal management rather than post-M&A management, typically resulting in slow turnaround and lower-than-expected performance. Third, move beyond limited delegation to the local management team. Most Chinese MNEs’ overseas acquisitions tend to be driven by the HQ’s management team and sideline local management. This results in limited information flow and capability transfer from the host country to China.

Pathways’ Interdependence and How Non-Market Forces Influence Them

Shifts between Pathways

Companies can move from one type of internationalization strategy to another. This can happen via bouncing up, which commences with strategic asset acquisition typical of the initial stage of the evolution of Chinese firm internationalization. Early bouncing up is mostly about aggressive radical M&As in a relatively short period at the initial stage; it focuses on acquiring strategic assets without being concerned much about capabilities. The initial bouncing up is followed by internationalization (including M&As) typically associated with capability building at the intermediate stage, and by internationalization (including M&As) typically associated with capability leveraging at the advanced stage. This tends to be the traditional internationalization pathway of Chinese MNEs. 77

However, as shown in Figure 1, some companies have departed from the traditional bouncing-up pathway onto a pathway we label bouncing down. This pathway corresponds to a retreat from a focus on capability leveraging to capability building within the same internationalization stage. Another pathway is bouncing sideways, proceeding relatively gradually from capability building to capability leveraging, focusing on expansion in relatively politically friendly or neutral territories rather than global expansion. Finally, there is a possible pathway to bounce back from a home/near-abroad-oriented growth strategy more forcefully and rapidly shortly after bouncing down. This involves capability leveraging for a worldwide expansion to reach a high degree of internationalization and become a global player.

The four pathways are not independent; there are close links between them, and together they constitute a pathway system across the evolution of firm internationalization under different contextual conditions. While bouncing up has been the default/desired pathway for Chinese MNEs, the contextual conditions of de-globalization and re-globalization create pressure to depart from this pathway. What starts becoming more likely is bouncing down to capability building within one internationalization stage (especially under de-globalization), bouncing sideways to capability leveraging in relatively friendly or neutral territories within one internationalization stage (especially under re-globalization), or bouncing back to capability leveraging on a global scale (relatively more challenging to do under de-globalization and potentially enabled by re-globalization).

Shifts between pathways are possible and likely as corporate strategies and the global business environment are constantly changing. For example, companies on the bouncing-down pathway—think Huawei—can transition to bouncing sideways or back. For example, despite security concerns, German rail operator Deutsche Bahn chose Huawei for its digitalization project in 2023. Moreover, firms from different industries, with different levels of strategic importance and sensitivity to specific non-market forces, may experience the non-market pressures differently. For example, what ByteDance may perceive or experience as de-globalization in the geopolitical arena or relatively weak re-globalization in terms of Chinese regulations, Tencent may perceive as re-globalization while facing political obstacles and see a potential to shift its strategy from bouncing sideways to bouncing back. Hence, firms could employ different strategies depending on the realities they are experiencing. Moreover, a firm’s strategic business units could have different strategies and pathways. In addition, while pathways are influenced by non-market forces, they are also affected by management and mismanagement, such as various management biases inherent in global M&As. 78 Companies are routinely trying to bounce up and bounce back from multiple setbacks brought about by poor change management as well as normal competitive dynamics.

Impact of Non-Market Forces on Chinese MNEs

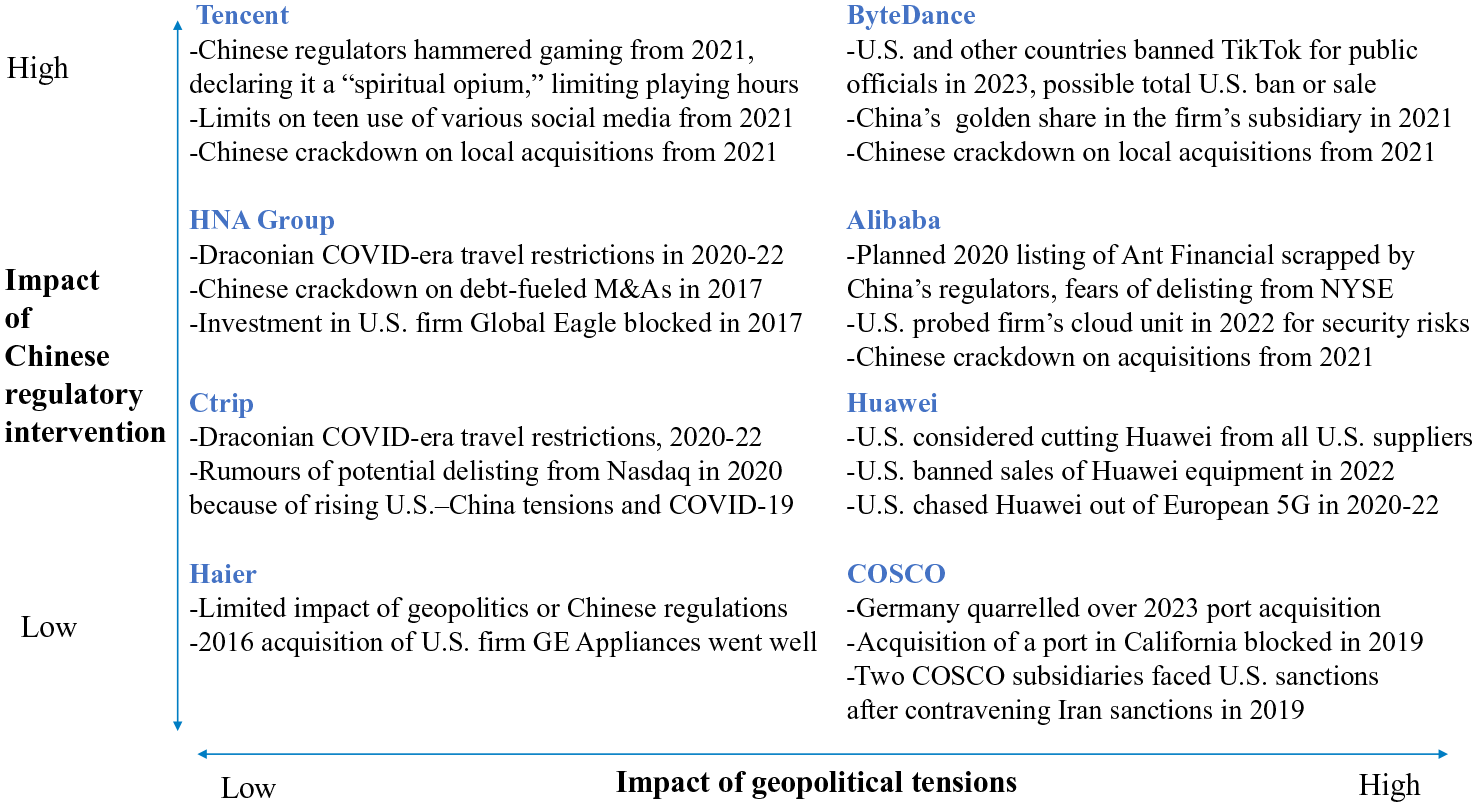

Our discussion of the four pathways shows that firms are impacted differently by globalization, de-globalization, and re-globalization. It also reveals some of the limits of these concepts and the need to consider specific non-market forces like the varied impact of geopolitical tensions and/or home-country regulatory intervention. Figure 2 illustrates these two forces’ possible range of impacts across the firms we analyzed. Figure 2 aligns with Figure 1 (zoom-out perspective) by highlighting non-market forces impacting Chinese MNEs and their internationalization, as illustrated above. 79 While non-market forces can positively impact firm internationalization (e.g., China’s Go Out policy of the 2000s), 80 the detrimental impacts of Chinese regulatory intervention and constraints came to the fore recently. Based on the case examples we used, Figure 2 illustrates how Chinese MNEs have attempted to respond to and manage such non-market pressure while continuing to compete globally. It also elaborates and contextualizes Figure 1 by demonstrating how Chinese MNEs are likely to experience the shifting dynamics of globalization, de-globalization, and re-globalization in light of how these firms are impacted by geopolitical tensions and regulatory intervention at home.

Impact of geopolitical tensions and regulatory intervention.

Geopolitical tensions have also had a range of impacts on firms and industries. Research on measuring geopolitical risk recognized that firm-level geopolitical risk embeds three components: aggregate geopolitical risk common to all firms and industries, industry exposure, and firm-level geopolitical risks that are not reflected at the aggregate and industry levels. 81 We extend these considerations by recognizing more explicitly that geopolitical risk and impact are related to a firm’s home country. We highlight geopolitical risks, tensions, and fallout from Chinese regulatory intervention specific to Chinese MNEs.

Figure 2 is inspired by research on the consequences of de-globalization and decoupling in terms of the negative impact of “black swan events”—rare, difficult-to-predict events such as the 2008 Global Financial Crisis and the COVID-19 pandemic, with severely negative consequences on firms. 82 The figure indicates that some firms will face a relatively low impact of non-market forces associated with globalization. The top-left and bottom-right quadrants correspond to the relatively strong impact of one of the two non-market forces linked to de-globalization: the high impact of geopolitical tensions or the high impact of Chinese regulatory intervention. Both factors’ cumulative negative impact can lead to severe de-globalization (top-right quadrant). Finally, the business environment can change back toward a less bleak outlook (moving from the top-right corner to the bottom left), which we associate with conditions of re-globalization.

Figures 1 and 2 should be viewed together and are not meant to be prescriptive or proscriptive, as both firm strategies and environmental conditions vary and change over time. Non-market forces will accordingly exert a range of changing impacts on firms. They can also have sudden or gradual impacts, reinforcing themselves through complex systemic interactions. The perspectives we offer in this article respond to calls for strategic management frameworks defined broadly enough to account for systemic geopolitical and regulatory considerations. 83

Non-Market Forces and Firm Internationalization Pathways

As shown in our case illustrations and depicted in Figures 1 and 2, the pathways are influenced by non-market forces including globalization, de-globalization, and re-globalization. Globalization, which increases the interdependence and integration of nation-states around the world, has created conditions favorable to the pathway of bouncing up. For example, the impact of geopolitical tensions or Chinese regulation has been relatively low for Haier and Ctrip (Figure 2). However, de-globalization often makes capability-leveraging strategies more difficult to execute, increasing pressures for bouncing down from capability leveraging to capability building. Huawei and HNA Group have both faced de-globalization; Huawei felt the impact of the U.S.-China geopolitical rivalry, while HNA Group was hit by China’s strict COVID-19 restrictions.

Re-globalization enables firms to gradually bounce sideways from capability building to capability leveraging, especially in relatively friendly or neutral territories beyond the home market. Tencent and ByteDance have employed this strategy—Tencent to respond to the high impact of Chinese regulatory intervention (top-left quadrant), while ByteDance is strategizing around the high impact of geopolitical tensions (top-right quadrant). Re-globalization may also exercise and increase pressures for bouncing back, depending on its nature, strength, and specific facet relevant to a particular MNE or industry. COSCO and Alibaba have attempted this strategy to counteract strong geopolitical headwinds 84 and Alibaba to counter domestic regulatory crackdown.

Overall, Figures 1 and 2 show that the internationalization pathways are affected by firm internationalization strategies, the stage of firm internationalization, and non-market forces. The weak impact of domestic regulatory intervention and geopolitical tensions favors bouncing-up strategies. Bouncing-down strategies can be associated with the relatively high impact of non-market forces. Moreover, firms can make their own strategic choices and embark on both bouncing-sideways and bouncing-back pathways to respond to the high impact of one or both of the non-market forces (geopolitical tensions and domestic regulatory intervention). In other words, non-market forces influence but do not pre-determine firm internationalization.

Finally, it is important to consider the specific industries in which firms operate, as this has implications for pursuing different pathways. In some industries, firms are subject to relatively high geopolitical pressures. 85 Examples are high-tech and infrastructure firms such as Huawei and COSCO. In other industries, firms face both high geopolitical and domestic regulatory pressures (like tech firms ByteDance and Alibaba); mostly domestic regulatory pressures (e.g., Tencent and HNA Group); or relatively less impact of non-market forces (as in the cases of Ctrip and Haier). Bouncing up, for example, is easier for firms like Haier as it operates in a relatively less-strategic industry. It is also important to consider the restrictiveness of FDI regulations and M&A screening policies 86 in specific countries and sectors 87 and the fact that national priorities, and perceptions of which industries are strategic, change over time. 88

Conclusion

De-globalization is reshaping strategic pathways for organizational success. The new realities also reflect elements of re-globalization and structural reshaping of globalization. 89 The increased fracturing of globalization will cause further uncertainty for the global economy in the foreseeable future; thus, Chinese MNEs, with ambitions to become global leaders through accelerated internationalization, need to reconsider and reconfigure their strategies. Attaining status as a global player is far from guaranteed. It may not be desirable either—most companies in the Global Fortune 500 have most of their sales in their home region. 90 A deep understanding of the complexity of global organizational dynamics is required to prevent mismanagement and fatal errors such as HNA Group’s fate.

Bouncing back from the adverse effects of de-globalization requires careful management of cross-border M&As and knowing when it is wiser to pursue domestic M&As or other strategies, such as partnerships and organic growth that can still help with global expansion. Many Chinese firms suffer from being negatively stereotyped, adversely impacting their cross-border M&As and internationalization. 91 This effect might be exacerbated if China gets more involved in its strategic partnership with Russia. Private companies from a wider range of industries may be exposed to geopolitical fallout if the line between private firms and the state becomes more blurred in China. 92

Implications for Chinese MNEs’ Competitors

We suggest that managers of MNEs that compete with their Chinese rivals try to understand them more comprehensively 93 and consider gaining knowledge and developing capabilities for managing geopolitical risk and uncertainty. The latter will likely be increasing. For example, non-Chinese competitors should thoroughly refresh their risk frameworks and guidelines to reflect the new geopolitical shifts and bring stakeholders from various countries together to cultivate cohesiveness and reduce the risks of conflict. Moreover, Western MNEs in China should engage in scenario planning around the impact on their business of the tightening regulatory environment in China. If they stay engaged with and in China, they may need to revisit existing partnerships to strengthen ties with domestic firms that will gain privilege. They also need to approach China’s regulatory environment with an emphasis on aligned value creation, and they should localize operations and leadership while being pragmatic, maintaining their company’s core values, and mitigating risks.

More broadly, managers of competitor MNEs should consider preparing for multiple contingencies such as possible U.S./allied sanctions on China if it more directly supports Russia in its war in Ukraine, 94 and they should consider recalibrating their involvement in and with China. A recent example of a Western company making important decisions about its engagement with Chinese firms is Ford partnering with Chinese electric battery maker CATL. Ford has faced criticism about its move, both in the United States and China. To put it bluntly, recalibrating involvement in and with China may include seriously considering leaving China or reducing dependency on the Chinese market and partners. 95

Western managers must also develop corporate diplomacy skills. As much as it may be challenging to manage state interventions while doing business in China, coupled with the impact of geostrategic pressures, 96 foreign firms striving to succeed in China may need to develop deeper relationships with relevant policymakers and regulators. Moreover, they may need to consider expanding the remit of their corporate mission to contribute to broader national strategic priorities to preserve the foundations of social, political, and economic systems in which they most want to be embedded in the future. The neoliberal system on which Western nations are founded involves a combination of market, non-market, and anti-market processes—these will have to be considered jointly and more seriously than ever before.

Managerially derived concepts associated with MNEs—based on business strategy, organization structure, and decision-making (e.g., firm internationalization strategies and MNE strategy and structure) and even market-centric and economics-derived international business concepts (e.g., the international product life cycle and globalization phases)—are no longer sufficient to explain what is happening with regard to Chinese MNEs. The current geopolitical tensions and stricter national regulations are testing the limits of such concepts and offer opportunities for rethinking, problematizing, questioning, and either reframing them or developing novel ways of viewing both the forces at play and how they influence MNEs.

Non-market forces can overwhelm MNEs and alter their evolution, as we have shown in the case of Chinese MNEs. Hence, the saga of Chinese MNEs does require a profound conceptual shift and intellectual expansion in our thinking and writing about MNEs. For example, fundamental frameworks and concepts, such as firm-specific and country-specific advantages, may need rethinking to account for the increasingly blurred boundaries between “firm” and “country” in China. Moreover, the dominant thinking in international business research has viewed globalization in a positive light; critical analyses and reflections are needed on its essence as a multi-faceted fracturing process with MNEs at the epicenter. In the era of increasingly fractured globalization, MNEs face new realities which require new thinking, strategies, and pathways.

Footnotes

Acknowledgements

The authors express their gratitude to the Editor of California Management Review Professor David Vogel and three anonymous reviewers for their developmental critique and guidance throughout the review process.

Notes

Author Biographies

Peter Zámborský (PhD from Brandeis University, U.S.) is a Senior Lecturer in International Business at the University of Auckland Business School, New Zealand (email:

Zheng Joseph Yan (PhD from Monash University, Australia) is a Lecturer in International Business at the University of Auckland Business School, New Zealand (email:

Snejina Michailova (PhD from Copenhagen Business School, Denmark) is a Professor in International Business at the University of Auckland Business School, New Zealand (email:

Vincent Zhuang has over ten years of global strategy consulting experience. He has provided professional consulting services to many Chinese companies as well as leading multinational corporations (email: