Abstract

As industry boundaries dissolve and digitalization grows apace, ecosystems are becoming increasingly important. Yet for all the excitement and Big-Tech envy, there is little guidance for how to create ecosystems. How should a firm best engage? Should it become a partner to someone else’s ecosystem, or build its own? Should it focus on a broad range of digitally connected services, or narrow down? How should we think about ecosystem value proposition, governance, and complementor choice? And, what is the case for investment in ecosystems? Drawing on recent research and projects with leading firms, this article offers a framework for understanding, engaging in, and building business ecosystems.

These shifts are driven by two main forces. First, digitization is allowing us to reconfigure activities like never before. Who would have believed just a few years ago that our fridge would be able to detect when it was out of milk and order more on the Internet? Such miracles can only occur via a web of connected firms coordinating through a stable web of interactions enabled by an ecosystem. Second, (de)regulation means that the boundaries between previously well-delineated activities have dissolved, opening up the realm of competition. With a myriad of new building blocks, and so many industries digitizing and colliding, firms have a golden opportunity to rethink how to add value to the end customer by engaging in more creative ways to develop broader and more encompassing solutions. These forces have given rise to a proliferation of ecosystems of interconnected entities, interdependent yet independent, that challenge existing ideas about the best way to organize. 2 Standalone companies are yielding their thrones to ecosystems: fluid networks of organizations combining to deliver bundles of products and services in new and unfamiliar ways.

Ecosystems are both enabled by and result from big changes in the ways we consume and produce. They are developing at remarkable speed, and academic research on business ecosystems is growing fast. 3 On the practitioner side, a McKinsey report suggests that by 2025—just three years hence—today’s 100-plus industries and value chains will have collapsed into around a dozen colossal ecosystems accounting for some $60 trillion in revenues, or one-third of the global total. 4 BCG found that the use of the word “ecosystem” in large companies’ annual reports had grown 13-fold over the last decade, and that firms using and acting on it grew much more rapidly than those that didn’t. 5 Along with other consultancies, 6 BCG considers ecosystems to be a critical driver for future growth.

We have recently seen a burgeoning of literature on how best to compete in ecosystems in broad terms. 7 But, welcome as this literature is, it leaves open the challenge facing managers who wish to lead their firms through this increasingly complex business environment. How can managers make the right decisions in a world of ecosystems? This article outlines a step-by-step framework for doing just that, drawing on academic research and work with senior executives from several leading firms from early 2019 to early 2021. Based on our analysis of ecosystems both successful and unsuccessful, as well as our work helping clients to develop an ecosystem strategy, we identify the key choices that firms must make as they consider their ecosystem engagement.

First, we distinguish between multi-product and multi-actor or experience ecosystems. Multi-product ecosystems, born out of the ability to digitally stitch together services around broader customer needs, define the scope of the offering. This scope should be defined by carefully studying the landscape of ecosystem competition, with a keen eye on the customer target group. The first two steps of our framework explain how to set the boundaries of a multi-product or experience ecosystem. Once the scope has been established, firms need to look at each part of their value proposition and consider whether they should provide the offering themselves, act as a system integrator, or become part of a multi-actor ecosystem. The next five steps in our framework help firms decide whether they should orchestrate their own multi-actor ecosystem or participate in someone else’s as a partner or a complementor. We also explain how best to engage in an ecosystem, in terms of its value proposition, governance, and complementor relations. As a final reality check, we explore how to verify the business or investment case for ecosystem engagement and, on that basis, identify key performance indicators (KPIs). Overall, we set out the key questions that firms need to consider as they embark on this complex but necessary and potentially rewarding journey.

This article draws on two major four-month-long projects (among others) done through Evolution Ltd (https://www.evolutionltd.net), a boutique advisory firm that explored ecosystems in depth, investigating what makes the difference between success and failure, as well as how data are used and the part played by regulation. These projects were preceded by a comprehensive literature search designed to help us form hypotheses on how to think about ecosystems and their success factors, as well as the kind of framework that might be most useful to managers.

More specifically, initial hypotheses formed through our project work and informed by the literature were tested, refuted, refined, and recast on the basis of evidence. 8 In pursuit of this framework, we conducted 95 interviews, ranging from 45 to 90 minutes each, which offered invaluable guidance. These interviews covered a broad range of participants, including top-level executives and operating managers from Big Tech firms, leaders from their partners, smaller complementors, consultants, investors, analysts, tech pundits, entrepreneurs, politicians, regulators, and academics. 9 The framework was shaped by iterative discussions of the core group that had participated in EvolutionLtd assignments, and it included Martin Bruncko and Rene Langen, Senior Advisors, Nikita Pusnakovs and Elena Sedova, Engagement Managers and Kriss Cerpins, Consultant. 10 The framework emerged from engagements with executives in a broad set of settings, and was further refined by interactions in conferences large and small, corporate events focused on ecosystems, executive courses, and a consortium on ecosystems put together by two leading global business schools, in which senior executives from five large corporates met to discuss issues in setting up their ecosystems. Finally, our framework was tested in action in projects that Evolution Ltd undertook with corporates working on their own ecosystem strategies, most of which appear by way of examples in this article. These included an Asian Big Tech firm, a Chinese manufacturer, a Spanish telco, an Italian utility group, a European tech company, a Swiss insurance firm, a global re-insurer and its clients, an European Union (EU) industry association, and smaller tech ventures and incubators in the United States, Canada, and Greece. 11

The framework also benefited indirectly from discussion with executives beyond work through Evolution Ltd, given the author’s role as an Academic Advisor to BCG—both to the Global Advantage Practice and the BCG Henderson Institute, and collaboration with consultancies such as Keystone Strategy and McKinsey & Co on a more ad hoc basis, and on advisory boards of digital businesses. Also, involvement with the policy community 12 and multi-stakeholder groups such as the World Economic Forum (including a number of events organized in Tianjin, San Francisco, New York, and London) has informed this approach.

Multi-product versus Multi-actor Ecosystems

As a first step, it is worth getting clear on the meaning of the terms that are used around ecosystems. Here, we have found remarkable confusion—among managers, analysts, and even academics. First, there is a confusion between platforms (which are the technologically based solutions that allow multiple actors to interact) and ecosystems (which are groups of connected products or services and the players that collaborate to produce them). 13 Put simply, platforms are made of technology, while ecosystems are made of products, people, and organizations.

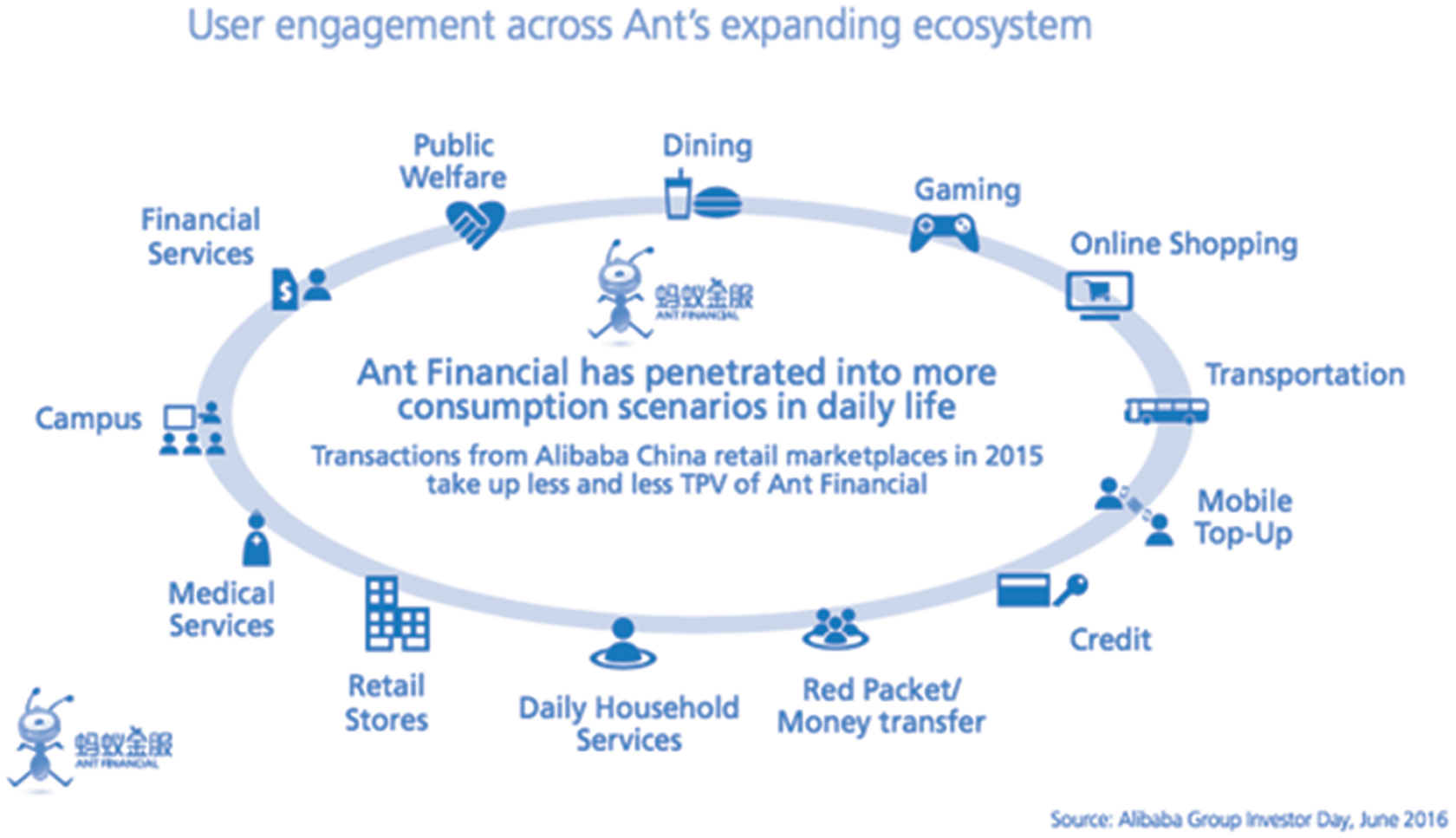

However, even the word “ecosystem” itself causes confusion. In lay terms, it usually denotes a group of connected products and services that we consume. So when we consider Google’s ecosystem, we think of services such as Search, Maps, YouTube, and Google Mail, alongside products like Android’s mobile OS and cloud storage. In the case of Apple’s ecosystem, we group all the different products and services that Apple bundles and offers to its customers, from iPhones to streaming music, TV, and more. This is also how the term “ecosystem” has been familiarized by the major Chinese players—be they in the digital realm, like Alibaba’s Ant Financial (an example from its own self-described “ecosystem” is shown in Figure 1) or the physical realm (such as the ecosystems developed by Haier, the device manufacturer).

How mega ecosystem creators want to envelop the final customer’s every move.

However, in business parlance the term is used differently, and with good reason. In the commercial context, “ecosystem” denotes an alternative to the conventional make-or-buy decision. Consider, for instance, Google’s Android shown in Figure 2. Android is the expression of Google’s desire to afford phone users the benefit of apps that leverage the technological opportunities of an effective mobile operating system. Google does not aim to do this itself—and therefore does not develop its own apps. Nor does it use a traditional supply chain, potentially white-labeling the resulting software as its own. And it does not even act as a traditional system integrator, bundling solutions produced by others and presenting the buyer with an integrated package. Instead, it pursues a completely new way of assembling a product/service package, focused on one particular “vertical” (the phone and its OS). Within this vertical, it orchestrates an ecosystem: a group of actors that are co-specialized (so they can work together) and produce a collective (usually novel) product or service. This is the key definition of an ecosystem used in the popular and academic business literature. 14

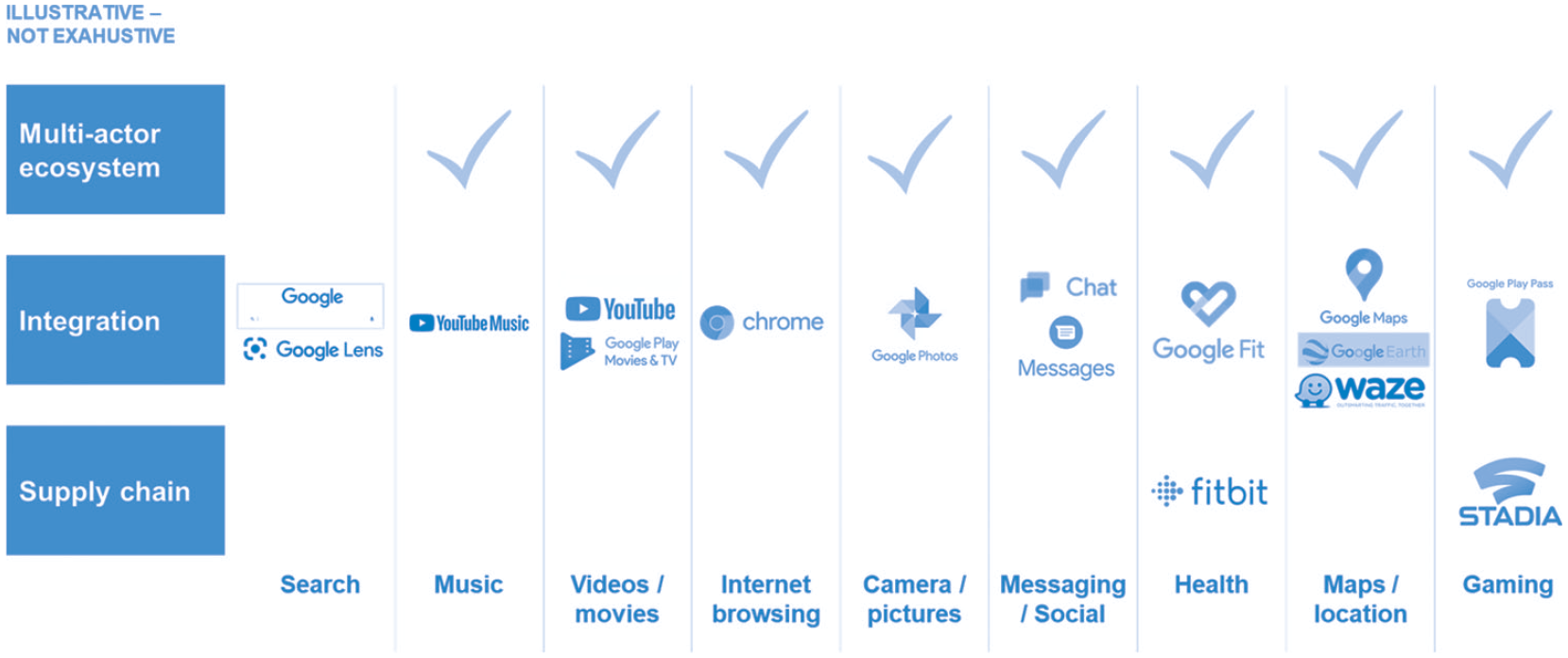

The multi-product (experience) and multi-actor ecosystems of Alphabet (Google).

Ecosystems come in two very distinct kinds: multi-product and multi-actor. This largely neglected distinction has been yet another source of confusion—not least among regulators. 15 Multi-product or experience ecosystems deliver new forms of integrated or bundled products or services that offer solutions for customers. Multi-actor ecosystems, meanwhile, denote a different organizational form. For their orchestrators, they represent an alternative to using the open market, a captive supply chain, or vertically integrated production. 16 The confusion arises because some Big Tech ecosystem orchestrators use both these approaches at the same time—as the figure below shows for Google (Alphabet) and Google Mobile Services, which focuses on mobile devices. Moreover, the two types of ecosystems are causally related. The more products and services a firm offers, the harder it becomes for it to cover them all, and the more likely its need to engage with complementors. Thus, the orchestrator of a multi-product or experience ecosystem will probably also need a multi-actor ecosystem to deliver it. 17 This is precisely what we see Big Tech firms doing.

Despite these links, the drivers and logic for each type of ecosystem remain distinct. The question of how broad a multi-product ecosystem should be is related to the scope benefits for consumers, the desirability of the overall value proposition, the possibility of locking customers in with a narrower (vs. broader) scope, and how all this relates to the current competitive landscape versus other ecosystems. The question of engaging in a multi-actor ecosystem, however, is about where to draw a firm’s boundaries: what should it do for itself, where should it work with partners, and how should this arrangement be set up? Multi-product ecosystems are about “Where should we play?” while their multi-actor counterparts are about “Who will be on our team, and what are the rules?” Our framework offers tools to answer both questions.

Deciding Multi-product Scope and Experience Bundles: Thinking “Outside-in” and “Inside-out”

The first big choice a firm must make is where to play. What experience, service, functionality, or benefit will it offer to its customers? How broad will the overall offer be, and how could it be delivered or integrated through digitization?

One way to reflect on this is through what we call “outside-in” thinking. What external trends and events, probably involving digitization, could the firm exploit or serve? Many ecosystems emerge from new opportunities to combine products and services, transcending traditional boundaries. In health care, for instance, new platforms and ecosystems provide a holistic solution to patients’ needs, from seamless hospital and acute care to support for chronic conditions, nutrition, and well-being. Integrated delivery network firms such as Kaiser Permanente in the United States, or tech-savvy insurers such as Ping An in China (through its subsidiary GoodDoctor), or independent specialists such as the United Kingdom’s Babylon Health (which works with the U.K. National Health Service and external providers) provide a patient-centric suite of offerings centered around customer convenience, but with a watchful eye on the total costs to the health care system. 18

A few firms aim to manage every aspect of customers’ experience—for example, by creating “SuperApps.” 19 However, broader isn’t necessarily better; cramming in ever more elements in the quest to win and lock in customers does not always work.

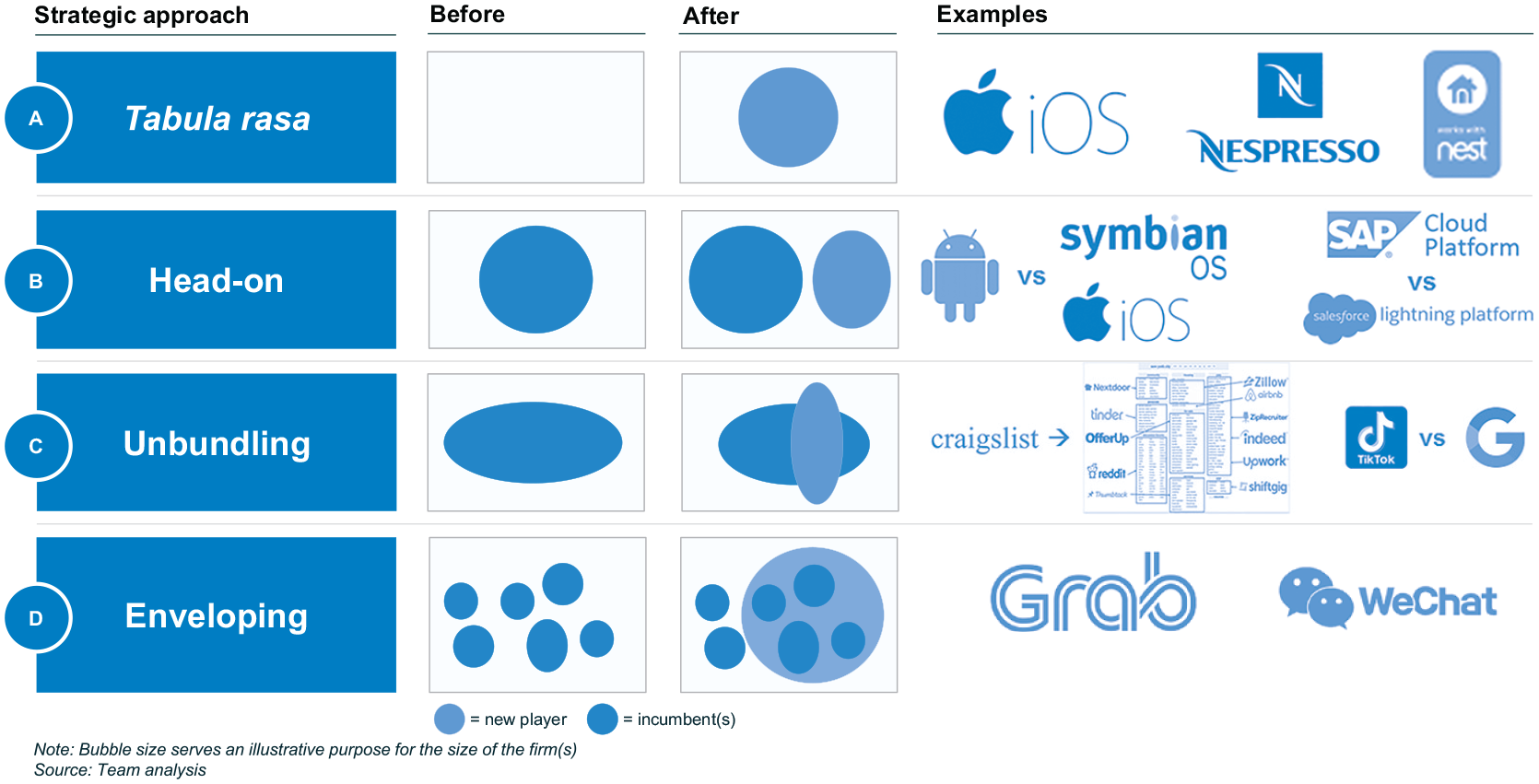

Our research suggests four “outside-in” strategies that firms can employ to define their scope, illustrated in Figure 3.

Some firms take what we call a “tabula rasa” approach—that is, they elect to become ecosystem first-movers in their industry. This is what Apple did with its App Store, or Nespresso with its ecosystem for coffee lovers. Once upon a time, building a multi-product ecosystem was novel in and of itself—but today, the terrain is far more crowded.

As other firms realize the opportunity, they purposefully create an ecosystem to compete head-on with a rival—just as Android with the support of Google went up against Apple iOS, and SAP aimed (with less success) to counter the growth of the complementor ecosystem at Salesforce.

More radically, companies can aim to reshape competition. Consider, for instance, the growth of firms such as Match.com and Zoopla. Both were born by unbundling—carving out a smaller niche within a space owned by previous incumbent Craigslist. 20

Yet another option is to become broader and more enveloping, in the hope that by extending its scope, an offer can not only leverage existing customers, but also create an unassailable lock-in. Grab, the Southeast Asian ride-hailing company, understood that its core service was hard to defend. So it expanded into financial services and other transport-related features to build a hub that was powerful and attractive enough to lock customers in. Uber, meanwhile, is reeling from failing to do something similar early on—and is now trying to make up for lost time. 21 At the same time, firms like PayPal are trying to broaden out, tracking customers’ ambitions. Or, consider the increasingly ambitious “customer envelopment” strategies pursued by firms such as Alibaba or Tencent’s WeChat in China, and Google and Apple in the EU and the United States. This has led to the race for “SuperApp” supremacy—one of today’s key strategic battlegrounds.

An “outside-in” analysis of ecosystem competition landscape.

Thus, the first and most crucial step is to understand the current situation in the industry in order to figure out how best to compete. Each approach requires a set of products and services to be orchestrated in a certain way, each has a slightly different audience, and each focuses on different features and differentiators. Firms will also want to consider the potential value of the total addressable market that each option could open up.

The picture gets more complicated when there is more than one ecosystem in play. Consider, for instance, the mobility sector. 22 Here, multiple, partly overlapping ecosystems coexist at different levels of granularity. Some may be nested (e.g., “train-related” and “last mile,” which are nested within overall mobility solutions), while others are only partly overlapping (such as “mobility as a service,” “ride sharing/hailing as a service,” “fleet as a service,” and “logistics as a service”). Public service operators, who blend fixed (traditional) with on-demand services and who combine their own ecosystems with other transport modes, are a case in point.

Some operators can even leverage the complexity of a space and cut across all the ecosystems. Consider, for instance, the upstart Velocia—an app that rewards travelers for not driving alone. Velocia partners with public transit and mobility-as-a-service providers to reward commuters whose behavior reduces environmental impact, working with cities such as Miami-Dade to help shift customer behavior. 23

To complement this structured “outside-in” approach, it is useful to undertake the reverse “inside-out” analysis, where a firm considers its own skills, assets, and opportunities as a starting point for defining its offer. What does the company possess that is unique and valuable? What could usefully be bundles with other features and other players to add significant value to what is offered today? These are what we call the firm’s “anchors”: the assets, capabilities, and processes that can be broadened, strengthened, and exploited by engaging in multi-product ecosystems.

Consider, for instance, the Italian energy giant Enel, and its subsidiary for new business development, EnelX, with which we worked. Historically, one of Enel’s activities had been the provision of street lighting for municipalities across the globe. As a consequence of this business, it found itself the owner of close to three million lamp-posts. With the advent of digitization, EnelX began asking itself how broad its offerings could or should be. If the lamp-posts were the physical anchors, what else could the firm do with them to create services that citizens—and thus voters and public authorities—would value? The answers ranged from adaptive lighting to urban advertising and e-buses.

Another company that we supported in ecosystem development was Spanish telco MasMovil. What needs could it cover, starting from the links and trust it had built with customers? How could it combine its core services with additional value-add to meet a need—such as monitoring the condition of the elderly or vulnerable? Or consider the Chinese manufacturer Haier. How could it move from making fridges and cooking hobs to being a player in an “Internet of Food”? What would be the right scope to adopt, or the best way to engage?

The “inside-out” analysis should also explicitly consider what a firms’ assets could do in the service of someone else’s ecosystems. That is, we should consider how value could be added if, rather than orchestrating a broader value-add system of its own, a firm contributed its know-how and assets to another multi-product and multi-actor ecosystem. How could it become a valuable partner or complementor? What would the broader bundle look like? What orchestrator and which partners would be potentially interested in engaging with the assets and capabilities at hand? Could we leverage these anchors to solve someone else’s problems? How could awareness be raised for such a value-add?

While ecosystems might have emerged in the tech world, they are becoming common not only in the B2G and B2B world, as the EnelX example demonstrates, but also in B2C, where firms like Nike have shifted from selling shoes and sporting gear to offering a broad array of services that involve runner communities, health tracking and wellness. Even coffee companies such as Lavazza have recently started working on how they can shift from selling a product - coffee, to selling experiences around coffee, emulating Diageo’s success in establishing the Bar Academy which engages and entices bartenders and thus drives sales.

When and Why Should a Firm Engage with a Multi-actor Ecosystem?

Looking at scope, and at the need to collaborate with other firms, we come to the question of how the offering can be assembled and delivered. Should the firm provide it internally, or engage outsiders? And if it does provide it internally, should it structure a supply chain, become a system integrator, or orchestrate a multi-actor ecosystem? Or should it become a partner in an existing ecosystem? On one level, this is a governance choice, where firms have to consider the merits of organizing work in different ways. However, it is also about creating a platform for innovation, since multi-actor ecosystems can bring forth new ideas and complements that the founding firm would never have thought of.

Multi-actor ecosystems can be tricky to manage, since they demand tight coordination between parties, yet also depend on the independent choices that firms make in pursuit of new ideas. The solution usually lies in a modular design supported by the guiding hand of the orchestrator.

For instance, when MasMovil decided to expand into a new area, it followed the example of Google/Android. It would neither do everything itself nor appoint suppliers, but rather build a multi-actor ecosystem to support its multi-product ecosystem. This made sense, as its broad product scope required it to attract partners from far and wide. In the event, MasMovil was able to leverage the strengths of complementors in both hardware and services to create a device that would function as the gateway for its offerings for the elderly and anyone else who would benefit from engaging with its new ecosystem.

EnelX grappled with similar questions. Should it offer all the potential new services itself, or partner with collaborators? Or, taking its cue from the app economy, should it simply open up the possibility for new players to take part by creating their own complements—precisely because it is difficult to know in advance what will add value for end users?

To answer these questions, firms need clear criteria to decide when a multi-actor ecosystem is preferable to making in-house or building a supply chain. 24 Research suggests, and recent experience confirms, that business ecosystems are particularly effective when there is a need for coordination and mutual adaptation. At the same time, the products, services, or processes involved need to be modular enough that they can operate with relative autonomy. 25

Of course, the best choice might not always be available. For whatever reason, the right partners might not be ready or willing to get involved. For instance, although Apple was one of the earliest to flirt with the idea of an electric car, to our knowledge no product has yet emerged. This could be partly because automobile OEMs and their key partners are reluctant to operate under the Apple banner. 26 Or it could be that potential partners calculate that a short-term revenue boost would not outweigh longer-term costs, making them wary about engaging.

Finally, it would be a mistake to think that multi-actor ecosystems are solely for large firms. Consider Zoom, which, despite its relatively small size, opened up a third-party ecosystem to cement its advantage. 27 In China, Internet giant Alibaba focuses on providing tools to enable firms to digitize and participate in, or build their own ecosystems, which benefits both Alibaba and the smaller firms that engage with it. 28 From DIY stores developing one-stop-shop solutions through ecosystems of plumbers, electricians, and installers, to health care players creating ecosystems to link their patients, doctors, insurance providers, and wellness organizations at a local or national scale, there is significant scope for value-add, supported by new technology firms such as Grapevine, or larger technology providers. 29 Small firms can also build their own ecosystems, as we saw with Velocia, provided they find the right approach which can excite final customers and partners alike.

For firms small and large with ecosystem aspirations, it is increasingly powerful to leverage social motivations. Consider Traipse, 30 and its offshoot MyLocalToken, which focus on urban regeneration through the creation of a purpose-built “local currency” that is honored by businesses in a downtown urban area, allowing users to support communities by “buying local.” 31 Even large ecosystems draw on the desire to contribute, as evidenced by the gamified social purpose ecosystems sponsored by Alibaba, such as AntForest which is used by 200 million Chinese to not only support daily activities, but also reduce carbon emissions. 32 Ecosystems such as these can galvanize participants by, over and above the promise of a convenient product (for final customers) and revenue (for partners), providing a compelling context for firms and consumers who share the same social objectives.

Building an Ecosystem, Not an Ego-System—And Why Prior Success Can Be a Trap

So far, we have seen that ecosystems demand careful thought, solid homework, and clear choices. Firms need a clear ecosystem game-plan in terms of where to play, its scope, market position, and likely complementors. One of the biggest challenges in drawing up such a plan is identifying reasons why either customers or complementors would want to engage with the new entity. The issue we have seen in many of the firms we studied is that they are too focused on what they themselves can do, which leads them to create an ego-system, rather than an ecosystem. This self-centered mindset is often rooted in the success of past endeavors and can be hard to overcome. 33 The combination of outside-in and inside-out approaches discussed earlier is an effort to redress this normal but unhelpful tendency. Yet constant vigilance is needed.

Look, for instance, at Swiss insurer Helvetia. Having decided to broaden out, Helvetia acquired the biggest Swiss digital mortgage broker, MoneyPark, on the sensible reasoning that people choose to buy insurance during major life events, such as moving to a new house. Its ambition was to build a multi-product ecosystem that would cover multiple needs at critical points in a customer’s life, supporting it with multi-actor ecosystems that could bring the necessary variety. But the big question is: why would customers want to engage with this ecosystem? Whatever the excitement to the company in assembling a broader service bundle, what would the value to customers be? How would their life be made easier, and how would the ecosystem be able to replicate the convenience provided by the likes of Ant Financial?

In contrast to the simpler, standalone products that the latter’s customers use on a daily basis, Helvetia products would be bought in sequence, often months or even years apart. While this might look “integrated” from the firm’s perspective, it offers no real extra convenience for the customer. It is therefore crucial to consider whether customers will perceive the offering as adding value, and if the supposed integration and convenience apply to them. This has been a challenge for many insurers as they have begun to engage with the world of ecosystems. 34

Let’s suppose the value proposition to the final customer has been crisply defined. The next big question is how an ecosystem should be put together? Our experience with leading companies is that implementation is often a major stumbling block—even when the overall value proposition is clear, the promise to consumers and complementors is straightforward, and a bold new move makes good commercial sense.

Consider, for instance, General Electric’s ambitious Internet of Things Predix platform, which was meant to combine advanced analytics with engineering solutions. 35 In 2016, GE triumphantly predicted that Predix would deliver over $8 billion in annual revenues. But by 2018, it had been ignominiously spun off after it failed to live up to anything like those early expectations.

Why was Predix such an abject failure? First, there was a presumption in GE that, putting together the firm’s reputation, reach, and financial might with significant investment in the new unit, complementors would flock to the platform. Sadly, a high profile isn’t enough to guarantee the success of a multi-actor ecosystem. Second, GE’s approach lacked focus. It tried to be everything to everyone, forgetting that ecosystems must offer a clear value proposition for both the final customer and complementors. Third, complementors’ incentives and engagement were mismanaged, resulting in sluggish and sub-par offerings. Fourth, there was a limited understanding of the shifting competitive context, and GE’s emphasis on its own in-house cloud offering was a mistake alongside the growing role of hyper-scalers such as Google, AWS, and Microsoft. Fifth, there was poor management of the governance and structure of the ecosystem itself, leading to a vicious circle of sub-par quality that discouraged potential complementors. Finally, the organization was too product-centric, and it struggled to engage with ecosystem-generated services.

These challenges are by no means unique to GE. Such inertial forces have plagued a number of proud incumbents that believed that their strength and reach were sufficient to ensure success. Engaging in platforms and building ecosystems, though, is very different from “business as usual”—as IBM also painfully found out with Watson, which, despite attracting significant early interest, failed to create the momentum it needed in the world of AI developers.

Success in multi-actor ecosystems requires clear choices and the skills to follow through on them. It is about making the tough either/or choices, such as deciding what not to do, or who not to serve. This requires focus and discipline, in both thought and deed. It also requires flexibility and openness to change to adjust to such new requirements. This is a tough challenge when established partnership models have a “gravity” of their own, and organizations have inherited routines that served them well in a previous era. Consider, in this context, the fascinating challenges faced by SAP, a leader in Enterprise Resource Planning (ERP) software, which recently embraced the cloud-based industrial services ecosystem.

SAP, a rare European Big Tech firm with its fair share of digital transformation challenges, 36 may be one of the earliest firms to have used the term “ecosystem.” However, for SAP, the concept has traditionally applied to downstream partners such as Accenture or Deloitte, which used SAP technology to propel the early wave of digitization in enterprise systems. These “ecosystem partners” were largely independent from SAP and would use SAP solutions to add value to B2B proposals, and thus drive their own volume and revenues. With the transition to the cloud, though, a new set of challenges arose. Cloud delivery allows firms to offer more customized, all-in-one solution sets to address novel and unmet customer needs. One consequence is that complementors now have to be co-creators of innovation—which in turn demands new ways of recruiting, managing, and motivating them. At the same time, moving to the cloud means that complementors will compare firms like SAP to Microsoft and AWS, which have traditionally been more open in the way they managed their ecosystems. So, what worked well for firms like SAP in the past may not necessarily be the right strategy for the future.

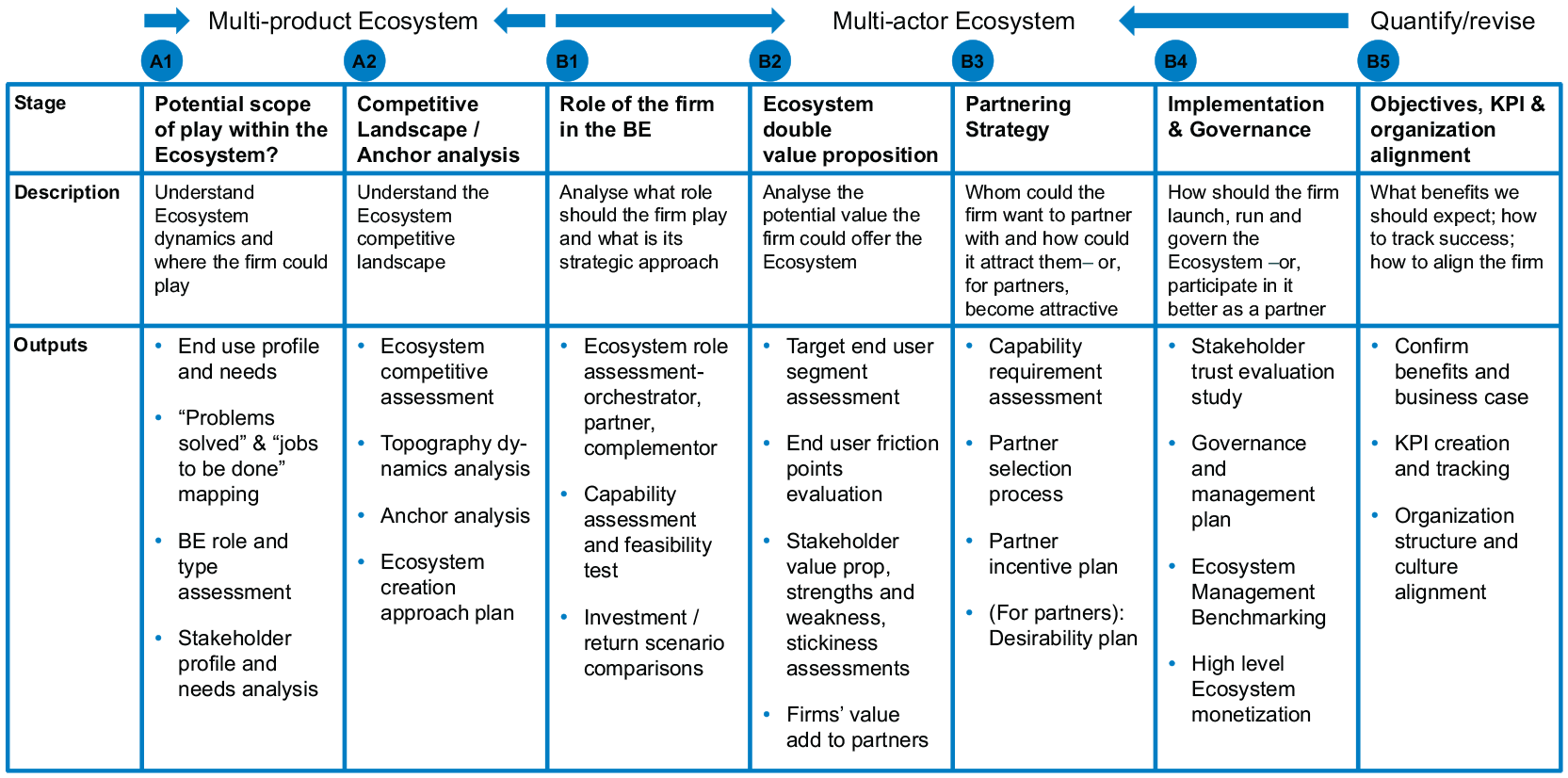

Bringing It All Together: A Seven-Step Framework for Building an Ecosystem

As our analysis so far suggests, firms wishing to compete successfully through ecosystems, whether their own or someone else’s, have a long to-do list to work through. When we worked with companies attempting to craft an ecosystem strategy, we found that, apart from a thorough understanding of the essentials, their most pressing need was for a framework for action. This is what we set out to create.

Our framework was developed iteratively, based on research into what drives ecosystem success and failure and our experiences of working with real-world firms. It builds on the preceding analysis and crystallizes it into a seven-step (or, more accurately, a two-plus-five-step) process encompassing all the domains that underpin a firm’s ecosystem strategy. It will help to frame the right questions, take the appropriate decisions, and fine-tune the strategy’s implementation. Our hope is that it will help managers not only to set strategic direction, but also to communicate that direction to internal and external stakeholders.

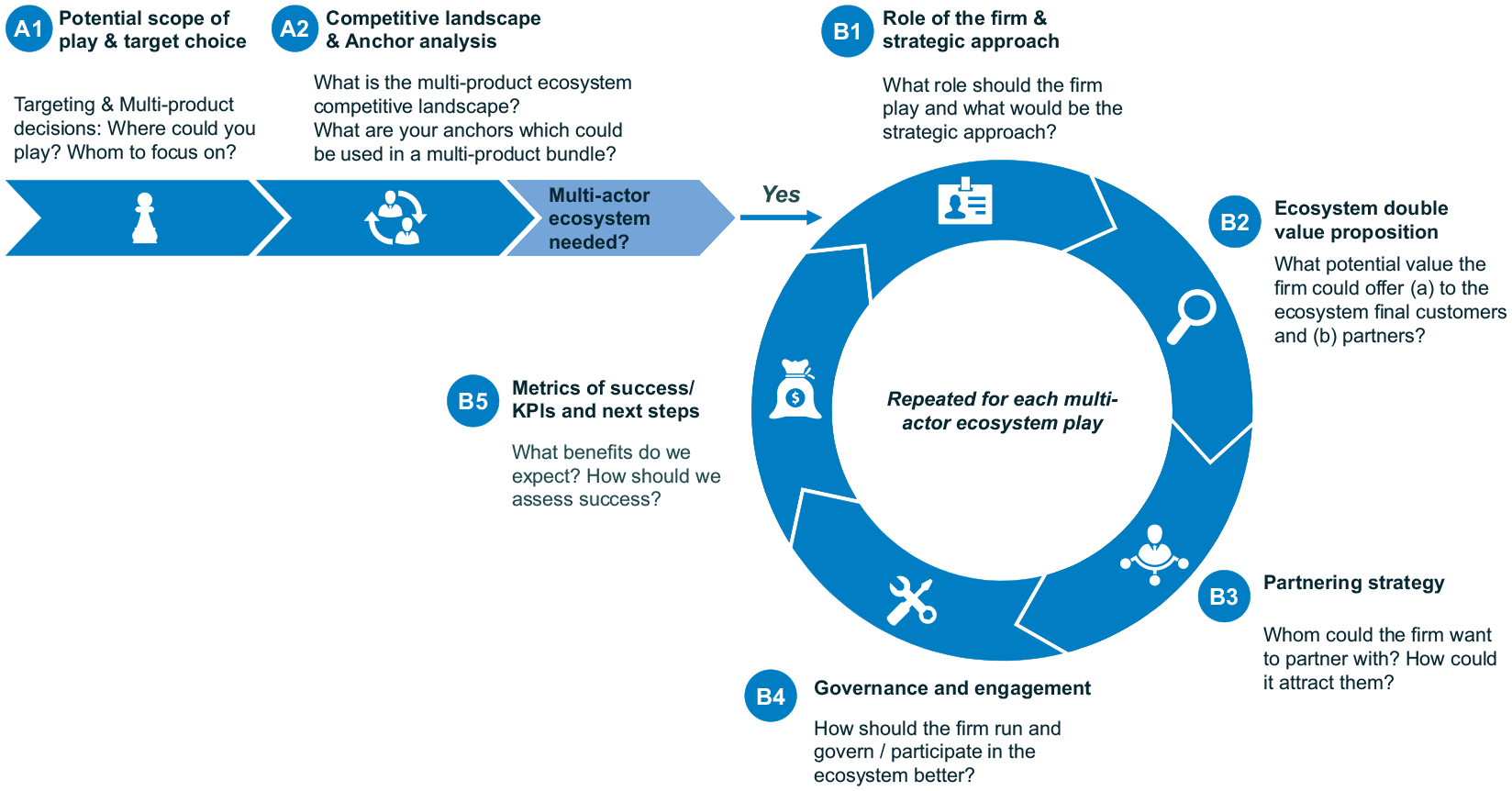

The first two steps (A1 and A2) concern the identification of scope: deciding how broad or narrow the ecosystem should be. This entails considering the “art of the possible,” looking at customer focal groups and the competitive ecosystem landscape. These steps should be supported by an “anchor analysis” that consists of an “inside-out” examination of what can add value in a broader context.

The analysis of scope helps define whether a firm can usefully be part of a multi-product ecosystem. It also often suggests areas where the use of complementors is needed. Energy giant Enel, for instance, knew that it needed complementors, much as telco MasMovil did. Inasmuch as there was no intention to do everything in-house, the question for both firms was whether to build their own delivery capacity, use a captive supply network, or construct an ecosystem. Provided building a multi-actor ecosystem is a compelling option, we then move to the second part of the framework.

The next step, then, is to drill down to multi-actor ecosystem issues. For firms that have a broad scope with multiple offerings (as do all the Big Tech firms, active as they are in a dizzying array of activities), this exercise will need to be repeated multiple times, mirroring their participation in many multi-actor ecosystems to deliver their multi-product offering. Firms that are narrower in scope and wish to focus on their role as partners may have a smaller number of multi-actor ecosystems to consider—sometimes just one. Yet, scale and complexity aside, all should consider the same basic questions, namely:

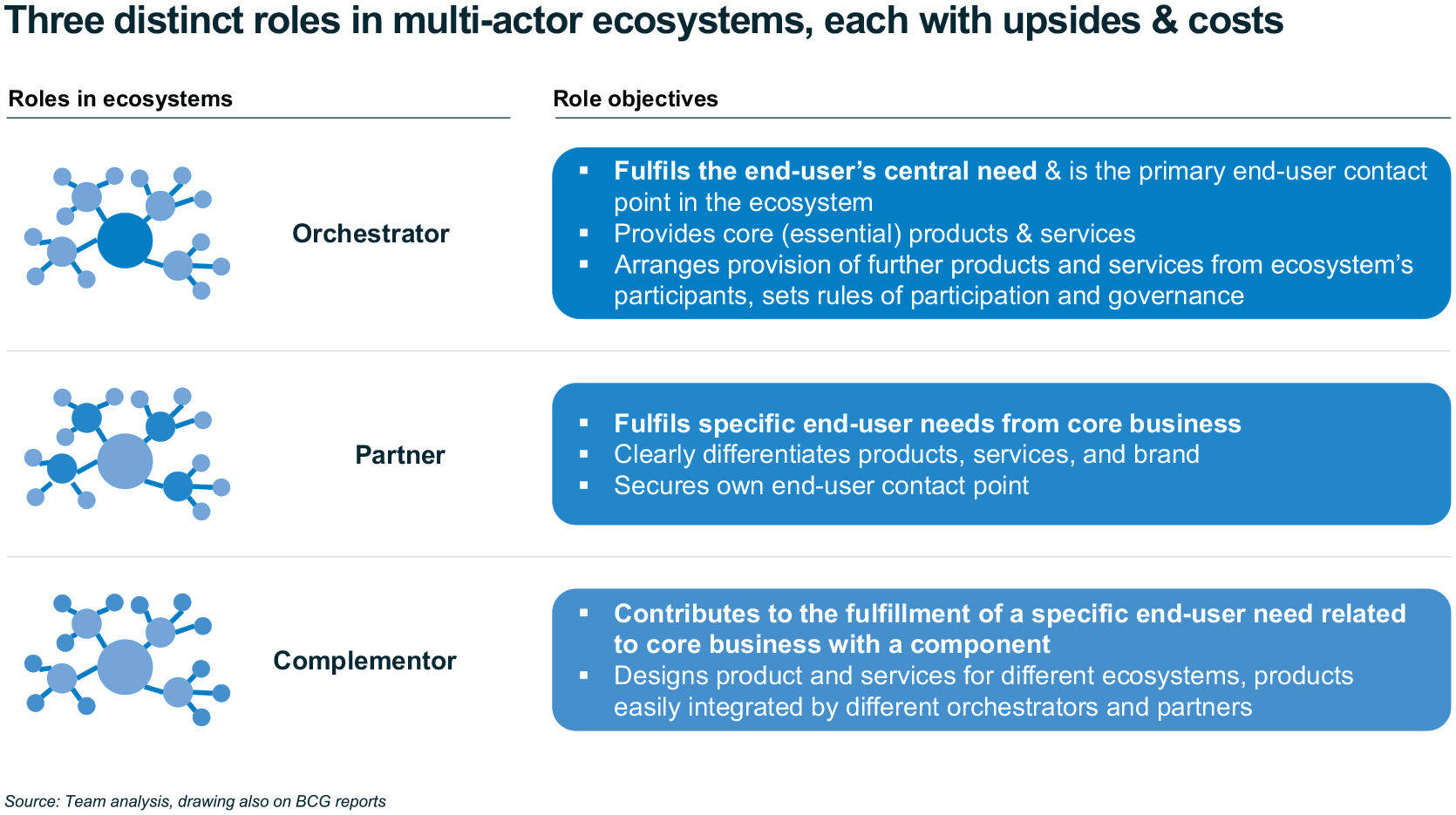

What role should a firm play within a multi-actor ecosystem? Should it be an orchestrator, or might it be better to be a partner (or a complementor?) (B1)

What is the value proposition to the end customer, and what value does the firm itself bring to the ecosystem? (B2)

Which partners does the firm want to attract, and how can it do so? How should the ecosystem be governed? (B3)

If a firm is an orchestrator, how should it set up the rules of engagement? If it is a partner, how should it try to engage with the orchestrator(s)? (B4)

Finally, what benefits does the firm expect to reap, and how can it choose KPIs to measure them, to ensure that the plan is implemented? (B5)

Figure 4 shows these steps in more detail.

An ecosystem development framework.

Steps A1 and A2: Scope, Ecosystem Competitive Landscape, and Topography

The framework begins by focusing on the multi-product ecosystem’s scope - its experience ecosystem.This has two steps: narrowing down where a firm should be active within an ecosystem (A1) and comparing this to the competitive landscape as it appears to customers and competitors (A2). This corresponds to the “inside-out” and “outside-in” perspectives.

Remember that early- or first-mover advantage is no guarantee of ecosystem success; even a “tabula rasa” strategy can fail. 37 Rather, the key is to choose the right “ecosystem topography”—that is, the best positioning vis-à-vis other ecosystems and solutions, with a focus on the value added for the customer. This is where bridging the digital and the physical may be valuable. Consider, for instance, mall-owner and operator Majid Al Futtaim, one of GCC’s largest organizations. Its traditional role was the provision of physical ecosystems for retail owners (where it partly vertically integrated by managing key retailers like Carrefour itself, and partly used multi-party store ecosystems). Yet, to compete more effectively with the digital retailing giants, it aimed to deliver a double value proposition, which would allow the customer to integrate their physical and digital interactions with a retail space, and which then meant it needed to build a digital connection to its ecosystem complementors as well.

When choosing scope, we have found that the best approach is to drop the idea of a single “representative customer” and focus instead on specific customer groups that have the most pressing needs. This is more likely to result in a customized approach that will be highly appreciated; a narrow target group also facilitates customer acquisition and the spread of an innovation. In health care, for instance, firms such as Omada have built multi-product ecosystems shaped around the needs of patients with chronic diseases like diabetes, while others such as Tia focus on women’s health. Or consider how PinDuoDuo managed to swiftly overtake JD.com to become China’s number two Internet retailer by bundling shopping and gamification, ensuring its appeal to a demographic obsessed with gaming. Such tailored ecosystems can provide a package that is innovative and adds value precisely because it responds to a need that is not yet met.

What is desirable, though, is not necessarily realistic. Establishing the latter is where anchor analysis comes in handy, with its focus on what a firm has to contribute—not only as an orchestrator, but also as a potential partner or complementor. Using the “inside-out” and “outside-in” analyses, the desired scope will be clear. The next step will be to consider how many multi-actor ecosystems a firm should engage in, and for each of these ecosystems to delve into its ecosystem strategy, as illustrated through Sber’s compelling example (and experiment) in Russia. 38 For each of the potential multi-actor ecosystems needed in support of the appropriate multi-product scope, a firm will need to proceed through five steps.

Step B1: What Role Should You Play?

Many companies only ever consider owning and managing their own ecosystem, as if there were no other choice. However, for many firms, a far smarter move is to engage in other ecosystems as a partner—or, to start even more cautiously, as a complementor. While many firms would like to resemble Big Tech (and a few, like Sber, attempt to emulate them), few have the clout—technological and management skills, competitive position, access to data, and AI know-how—to do so. We suggest starting with a realistic sense of the best role—not necessarily the largest. Then, be prepared to revise it if it is too costly, too difficult, or too risky. This should first be considered in terms of the multi-product ecosystem, where the question is, “Should I be orchestrating this suite of offerings for the final customer, or be a partner in the process?”

To tackle this question, we need to consider how each part of the value-add should be offered: through vertical integration, conventional suppliers, or a multi-actor ecosystem. Big Tech firms, as in the Google example we examined earlier, are orchestrators of both multi-product and multi-actor ecosystems. Other, smaller firms can choose to orchestrate one of the two dimensions. So, when is it better to be an orchestrator rather than a partner or complementor?

Our research suggests that firms aiming for a role as orchestrator need something that makes them uniquely suited to attracting both partners and customers. This may be pre-existing customer access of the kind that Big Tech and SuperApps enjoy. Or it may be a unique new position that, while indirectly complementing their business models, it is not in the interests of the major players to offer. Spotify, for instance, rose to fame because it allowed music labels to monetize their catalogs at a time that they were bleeding money; it was successful up until it decided to go to artists direct, potentially undermining its complementors (music labels), which backfired. Understanding the context of the sector is crucial.

This is what not only large tech firms can do, with the support of their funding and customer base, but also newer entrants, such as unicorn Babylon Health, which brokers links with key players in the health care arena; or small upstarts such as bookstore.com, which grew by offering a virtual storefront and fulfillment services to independent booksellers seeking to survive the pandemic; or Velocia, Traipse, and MyLocalToken, which focus on being attractive to partners for maintaining sustainable relations rather than initiating disruption alone. Beyond that, would-be orchestrators must have the financial resources to deliver the functionality needed to support both customer and complementor interfaces.

Another possibility, often in our opinion more viable, is for the firm to elect to be a partner as Figure 5 shows. In other words, it becomes a nodal collaborator, perhaps enjoying direct contact with the end customer, and capable of developing smaller ecosystems of its own within the broader context. Take, for instance, the ecosystem that orchestrator WeChat offers for Chinese tourists in Europe, allowing them seamlessly to make payments and receive recommendations and discounts in key European cities. To make this system work, WeChat has collaborated with KPN, the Dutch telco giant, which offers pre-paid SIM cards for Chinese customers to use to consume WeChat services through WeChatGo Europe. 39 WeChat also orchestrates local ecosystems of retailers and discounts, crucial in making the experience seamless for the final customer. Although KPN is “just” a partner in the WeChat ecosystem, it realizes significant benefits from this arrangement. Aspirant partners need the reach and skills to make them attractive to more powerful complementors, as well as the ability to engage with smaller complementors.

Roles in multi-actor ecosystems.

Steps B2 to B4: Building and Governing the Multi-actor Ecosystem

The next three steps demonstrate how to put the ecosystem together as an orchestrator or how to compete more effectively as a partner or complementor.

The first step (B2) focuses on two objectives: establishing the value proposition of the multi-actor ecosystem for both the end customer and for other ecosystem participants. For instance, Majid Al Futtaim needs to consider the value proposition it offers to the customers, via its malls, and at the same time it needs to consider its value proposition vis-à-vis its shop owners, using both physical and digital means, using things like a “mall-level reward scheme” and services as a means to achieve both. Our experience suggests that this “double scorecard” is a vital tool to maintain strategic focus. It also helps reveal the “pain points” that an ecosystem can resolve for the end user, articulate the stakeholder value proposition, and explain the potential “stickiness” for the final customer. This is enhanced by direct or indirect network externalities—that is, the extent to which ecosystem members value the presence of other participants, which help with customer lock-in when ecosystems grow, leading to “tipping.” 40

The next step (B3) takes a deep dive into the capabilities of the focal firm and its relationship with partners. It asks what skills, resources, and capabilities are needed; who can bring them to bear; and how partners will be attracted into the ecosystem. This encompasses the partner selection process, the incentives for partners, and the onboarding and development plan. This will differ depending, for instance, on whether the ecosystem is local, multi-domestic, national, or global. 41 This capability audit is crucial in both ensuring that the emerging role and strategy can be implemented, and identifying capabilities to build—and, if appropriate, the M&A to consider.

B4, the next step, covers how the ecosystem is governed—the rules and roles that pertain to its organization, how decision rights are allocated, and what processes underpin trust and buy-in from stakeholders. This is an important area that has only recently attracted research attention. 42 Governance requires tools to monitor the health of the ecosystem as a whole, and they will need to be tailored to the objectives at hand and the particular position of the firm. It’s crucial if a firm builds an ecosystem but also important to guide participation strategy for a partner or complementor.

Step B5: Translating Strategic Intent into Measurable Objectives and Changing the Organization

With the plan for the ecosystem laid out, the final part of the framework returns to the question, “What do we expect from this ecosystem? What benefits do we hope to see?” The reason for this is twofold. First, it helps translate the expected strategic benefits into concrete outputs that can serve as a reality check. This will also bring clarity in terms of potential monetization of advantage, with a particular focus on the role of data and its use, and the ability to access customers—hugely important topics that relate to the evolving context of regulation. Second, and more important yet, it helps articulate the ecosystem’s KPIs—the key measures that will indicate whether the entity is delivering on its promise or not.

As some recent research points out, the objectives of an ecosystem, and its KPIs, will shift and evolve over the lifecycle of the sector. 43 However, it is still important to construct the measures that assess the contribution of the ecosystem and to identify the attributes that need to be tracked. Our experience is that many an ecosystem can become a flash in the pan in the absence of such discipline.

Beyond measuring success, we also need to articulate the changes that the organization must make. The challenge here is that ecosystems require a much more agile and responsive organization than is the norm—especially for incumbent firms and non-digital natives, with their slower response times and more insular processes. While our framework may give a clear mandate and Figure 6 summarizes the concrete steps and deliverables we used in our projects, there will still be much hard work to be done to enact it and ensure that the organization is restructured appropriately.

Ecosystem development framework tools and outputs.

To illustrate just how far organizational redesign might go to accommodate these changes, consider the case of Haier, the leading appliance manufacturer, 44 which radically restructured itself around a bottom-up set of “ecosystem micro-enterprise communities.” These were incented to drive ecosystem revenue, measured on some of the systemic benefits that Haier is interested in. This took a bold restructuring effort aimed at giving impetus to innovation and responsiveness on the front line. Such examples raise the broader question of what changes may be needed to the organization and its leadership style in order to thrive in an ecosystem world.

Finally, our framework helps firms ask the right questions, elicit the right data, and open up appropriate discussions. It is intended to be iterative. Once a particular stage is completed, it is important to take a step back and ask, “Now, based on what we know, do we still think this is the best answer?” Using the framework in this way makes it possible to develop a strategy that can be revisited as the environment evolves. Our approach provides a structured set of investigations, illustrated below, aimed to assist ecosystem development.

Ecosystem Strategy: From Metaphor to Roadmap to Corporate Priority

One of the challenges raised by evocative words such as “ecosystem” is that everyone has a slightly different sense of what they mean—and, as such, what action they should lead to. Yet business and digital ecosystems are here to stay, and they are changing the nature of our competitive environment. To navigate our way through this landscape, we need shared optics: a shared language, shared tools, and proven best practices.

This article draws on both our academic work and our practical experience of advising firms to explore why some ecosystems fail while others succeed. This yields fresh insights, including the distinction between multi-product and multi-actor ecosystems; the identification of four different multi-product positioning strategies (tabula rasa, head-on, unbundling, and enveloping); and the importance of complementing outside-in analysis with inside-out work on firms’ anchors.

Our work also underlines the importance of choosing which role a firm should play in an ecosystem—orchestrator, partner, or complementor—and the capabilities needed to assume a more ambitious role. We also highlight the due diligence that needs to be performed at the level of each multi-actor ecosystem, in terms of the dual value proposition (to the final customer and to partners), the process of selecting and developing partners; ecosystem governance, metrics, benefits, KPIs; and requirements in terms of organizational change. Equipped with this framework, firms can ensure that ecosystem strategy is much more than an abstract phrase, but rather a practical tool to reinvigorate their fortunes.

An important aspect, implicit in our discussion but crucial in practice, is to understand how regulatory conditions might affect the current context. 45 Given both the growing power of Big Tech and increasing pushback from regulators and legislators, ecosystem strategies must be based on a solid assessment of both the current regulatory reality and how future changes might reshape the competitive landscape. 46 Regulators are weighing what they consider are appropriate business models, monetization strategies, and ecosystem architectures. In doing so, they shape the strategic contours of markets across the economy and across the world. As Big Tech will likely be constrained in some activities, and new rules instituted accordingly, regulation will fundamentally modify the landscape of opportunity and threats, and with it the shape of ecosystem strategies. Our tool, in conjunction with a solid analysis of regulatory trends, can provide a guide rail for firms in a world where technology, deregulation, and regulation are melting industry boundaries. It also provides a conceptual framework (especially with steps A2 and B2) for companies wanting to map out and reflect on the dynamics of inter-ecosystem competition. 47

Yet even the most forward-looking plan, with a solid foundation and a plausible implementation program, will be unable to drive a business forward in the absence of focused buy-in from the senior leadership. When asked to account for the firm’s success where others had failed, the chief innovation officer of Ping An, the world’s most valuable insurance company and a poster-boy for the champions of ecosystem thinking, had this disarming response: “It is that our CFO spends half their time thinking about the right KPIs for new businesses [for our ecosystem moves].” 48 As this suggests, the seriousness with which a firm takes its ecosystem ventures is a crucial element in its continuing progress. Unfortunately, many traditional firms are held back by heritage and legacy processes and the agonizingly slow approval and onboarding of new relationships and partners, not to mention lack of due attention to the factors that make ecosystems a success. 49 It takes hard work to overcome such constraints: digital entrants have fungible capabilities and are generously funded by the capital markets. 50

Whether for defending incumbents or an aspiring entrant, a framework such as the one we have outlined constitutes a valuable tool for forging a shared understanding of ecosystem components as well as a solid analytical backbone for ecosystem strategy. While we do not claim to offer a silver-bullet answer to the question, “What should I do tomorrow morning to make my ecosystem work?” we provide a practical guide to management action leading from the definition of essential terms through to implementation, which is the only way that proper guidance can be provided.

Footnotes

Notes

Author Biography

Michael G. Jacobides is the Sir Donald Gordon Chair of Entrepreneurship & Innovation and Professor of Strategy at London Business School and is the Lead Advisor to Evolution Ltd, Academic Advisor to Boston Consulting Group, and Chief Digital Economy Advisor to the Hellenic Competition Commission (email: ![]() ).

).