Abstract

Climate change has risen to board level on the corporate agenda. Under pressure from institutional investors, companies are reformulating their strategies for a low-carbon world. A novel aspect of the emerging corporate response is that executive compensation is being linked to climate performance. This article examines the different ways that climate-linked incentive pay is used at European and U.S. energy majors, and it develops a framework—aimed at companies in “hard-to-decarbonize” sectors—to understand the benefits, challenges, and key design options. It also makes recommendations on how this organizational practice might be refined over time.

Keywords

Pressure from institutional investors is an important driver of this process. In 2015, Mark Carney, as Governor of the Bank of England, warned the financial community about the implications of climate change for the value of investment portfolios. 2 Since then, investors have mounted increasing pressure on listed companies to measure and disclose their exposure to climate change—and to formulate “Paris-aligned” corporate strategies. A central role is played by investor coalitions such as Climate Action 100+, which controls over $50 trillion in assets. 3 Closely related, the Task Force on Climate-Related Financial Disclosures has developed a set of principles for the voluntary disclosure of climate risks. Unlike national climate policies, investor-driven corporate climate action has global reach. 4

Deep decarbonization looks more feasible to the corporate sector than it did even a decade ago. Advances in clean technologies, looming government regulation, and evolving societal preferences have relaxed the traditional trade-off between firm value and emissions reductions. Clean technologies such as solar and wind power and battery storage have seen costs decline by around 80%. 5 Businesses are discovering that cutting carbon—increasingly aided by technologies such as artificial intelligence—can cut costs because it reduces waste. Customers are increasingly willing to pay extra for greener products. 6

A novel aspect of the emerging corporate response is that executive compensation is starting to be aligned with climate performance. In December 2018, Shell announced that it would, from 2020 onwards, tie the incentive pay of its CEO and senior management to company-wide carbon targets. During 2019, several other major oil & gas companies, including BP and Chevron, under shareholder pressure resolved to incorporate carbon targets into executive pay. Leading companies in other carbon-intensive sectors, including aluminum, chemicals, and mining, are embedding their climate performance in CEO pay. In short, companies are beginning to use carbon emissions as a key performance indicator for management.

This article addresses the “why” and “how” of linking executive pay to climate metrics. As a business practice, this raises important questions that straddle environmental concerns and corporate governance—the “E” and the “G” in ESG. The analysis speaks to companies across the “hard-to-abate” sectors in heavy industry and transport—including airlines, aluminum, cement, chemicals, mining, shipping, and steel—that have recognized that their long-term value depends on cutting carbon.

Climate-Linked Incentive Pay at the Energy Majors

Given its public visibility and carbon-intensive ways, the oil & gas industry has been at the forefront of ESG-related concerns from institutional investors. With increasing pressure for corporate climate action, linking executive pay to climate performance is emerging as a business practice at some of the world’s largest companies. The experience of the energy sector holds lessons for companies in other emissions-intensive sectors that will need to confront the challenges posed by climate change.

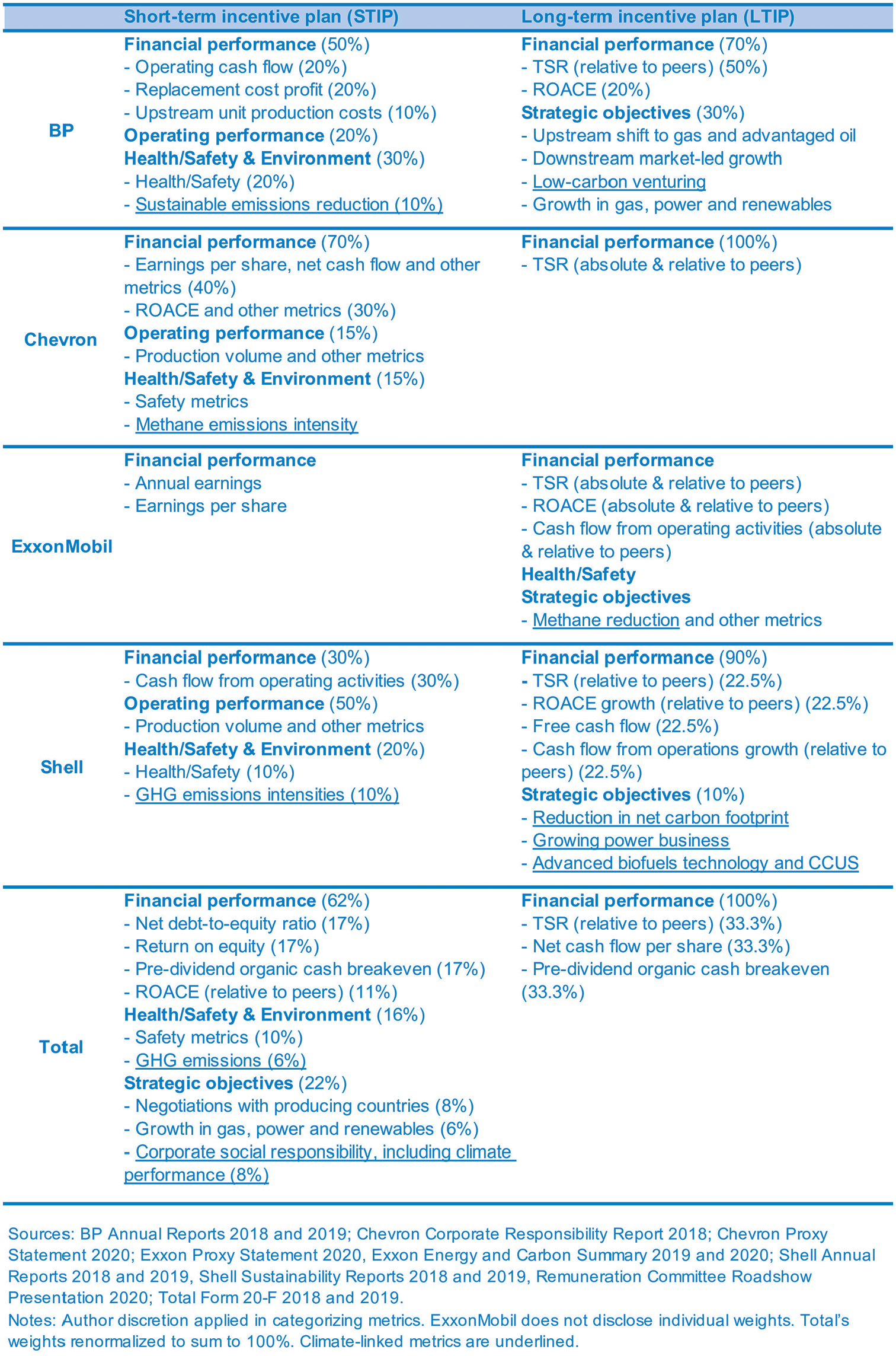

The largest oil & gas companies—BP, Shell, and Total in Europe and Chevron and ExxonMobil in the United States—all incorporate climate metrics into CEO pay. Figure 1 presents a high-level overview of CEO remuneration plans at these five companies. It distinguishes between two types of incentive pay: the short-term incentive plan (STIP) underlying annual bonus payments and the long-term incentive plan (LTIP) typically paid out as stock-based compensation. 7 Despite their superficial similarities as energy majors, there is large variation in compensation practices across these companies.

Performance metrics in energy majors’ CEO incentive plans.

Traditional financial metrics dominate short-term and, especially, long-term incentives. Unsurprisingly, all companies use total shareholder return (TSR) as a key performance indicator in their LTIPs; its weight, however, varies widely from 100% at Chevron, over an undisclosed weight at ExxonMobil, to 22.5% at Shell. Moreover, all companies make use of relative performance evaluation against a peer group, most notably on TSR. On average, financial metrics such as TSR and return on average capital employed (ROACE) account for 62% in STIPs and 90% across LTIPs.

Against this background, each company has a CEO incentive plan that is, in quite different ways, linked to climate performance. For short-term incentives, most use a metric on the reduction of greenhouse gas (GHG) emissions, with weights up to 10%, while ExxonMobil is the only company that relies solely on financial performance. Total is the only company with a performance measure on “corporate social responsibility” that includes its climate performance. Overall, climate-related metrics make up 8% of CEO bonus pay plans on average across the five companies. 8

Long-term incentives linked to climate are employed at BP, ExxonMobil, and Shell. BP and Shell do this by way of “strategic objectives” that relate to CEO milestones. BP includes venturing into low-carbon businesses and growth in its power and renewables businesses; Shell has a dedicated energy-transition metric that features a reduction target for its life-cycle emissions. Unlike other firms, ExxonMobil uses the reduction of methane emissions in its LTIP. At the opposite end, Total’s long-term incentives are tied solely to financial performance, and Chevron relies exclusively on TSR. On average, climate-related metrics make up 4% of long-term incentive pay. 9

The divergence between European and U.S. companies is evident. European players, notably BP and Shell, use broad climate-linked incentives that relate to corporate strategy, for example, growing their low-carbon businesses and reducing company-wide emissions. Chevron and ExxonMobil employ narrow incentives related to emissions cuts in individual business units. This picture is consistent with European players so far embracing the clean transition more strongly than their U.S. peers.

Shell has, for the time being, emerged as the leader among the large oil & gas companies, with ambitions to “thrive in the energy transition” and “sustain a strong societal license to operate.” 10 This includes long-term goals of reducing the net carbon footprint of its business, and, as of April 2020, a “net-zero” target for 2050 oil & gas production. 11 It is currently unique in that climate-linked metrics represent 10% of both its STIP and LTIP. As the transition gains pace, it is likely that the weight on climate metrics placed by the oil & gas majors will further increase. 12

Leading companies in other hard-to-abate sectors are beginning to embrace a similar practice: Alcoa, a U.S. aluminum producer, has a 5% weighting on emissions in its CEO bonus plan; BHP, an Anglo-Australian miner, which recently resolved to increase the climate-change weighting in its scorecard to 10%; and ThyssenKrupp, a German steelmaker, that uses a “sustainability multiplier” in its short-term incentives. 13

Principles for Incentive Design

Incentive plans for top management are a key ingredient of corporate governance. Yet the history of organizations is littered with examples of well-intentioned programs that turned out to be dysfunctional. These often involve managers gaming the performance measure (e.g., using accounting tricks) or being induced to pursue a different goal from what is good for the firm (e.g., pumping short-term results at the expense of long-term value). 14

A large literature on the economics of incentives provides guidance on the design of executive pay: which performance metrics to use and how to combine them. 15 This literature can be distilled into three high-level principles that will be useful for thinking about the “why” and “how” of linking incentives to climate performance. 16

Principle 1: Align Executive Pay with Corporate Strategy and Long-Term Value

Executive pay should be designed to align closely with corporate strategy, which in turn should aim at value creation over the long term. At major corporations, especially in the United States, this is associated with linking pay to TSR—to help align the interests of shareholders and management. Since the Global Financial Crisis in the late 2000s, value creation for many sectors is increasingly tied to government regulation; mounting stakeholder concerns over ESG topics raise new challenges for the formulation of corporate strategy.

Principle 2: Use Actionable Metrics that Reflect Management Value-Added

In a world in which financial, labor, and product markets all operate efficiently, linking incentive pay to the stock price would be enough to align the interests of shareholders and management. In practice, additional performance measures are useful insofar as they contain extra information about management’s value-added. 17 One reason is that stock markets can be “noisy” and short-termist, so a company should also rely on other metrics for a holistic perspective on its performance. These should be actionable in that management can appreciably influence them; common examples include operating metrics such as production costs and volumes, as well as non-financial metrics.

Principle 3: Balance Incentives across Multiple Proximate Objectives

With multiple—and perhaps competing—proximate objectives, management incentives need to be well-balanced. Otherwise, a danger is excessive focus on a subset of tasks at the expense of everything else. A classic example is that too strong a focus on increasing market share—for example, by way of aggressive product pricing—can come at the expense of long-run value. Such potential tensions are an inevitable feature of any balanced scorecard that, for good reason, goes beyond relying solely on the stock price. 18

Judgment is required in applying these principles; compensation practices differ across sectors and often even vary widely for seemingly similar companies operating in the same sector—as in the energy industry.

Why? The Case for Linking Executive Pay to Climate Performance

The strategic context for hard-to-abate sectors—such as aluminum, aviation, cement, chemicals, mining, and steel—is similar to that facing the oil & gas majors: increasing pressure to align corporate strategies with the ambition of the Paris Agreement. Transformation has two parts: one is to extract the remaining value from higher-carbon units; the other is to grow low-carbon business. For example, steel companies are developing new technologies using fossil-free electricity and hydrogen to, over time, replace traditional coal-based steelmaking. Carbon-heavy activities will therefore often operate side-by-side greener initiatives.

The design of incentives linked to climate performance begins with accurate information. Financial metrics such as ROACE and TSR are produced during the normal course of business; increasingly, this also includes carbon. Regulation has made companies invest in accurate emissions measurement; for the purpose of providing incentives, this now comes at zero incremental cost. An increasing number of companies are providing voluntary disclosure. Accurate measurement helps to create an actionable performance measure (Principle 2). A caveat is that this has so far focused on emissions from a company’s own operations (“Scope 1”); the measurement of value-chain emissions (“Scope 3”) is trickier and still less well-developed. 19

Given that a firm’s emissions are adequately measured, should they be part of incentive pay? Pay offers a powerful lever for hard-to-abate sectors to align incentives for top management with evolving corporate strategies (Principle 1). Advances in clean technology, looming government regulation, and evolving consumer preferences have relaxed the traditional trade-off between firm value and emissions reductions. Linking executive pay to emissions cuts embeds a corporate pledge to align with the Paris Agreement directly in management incentives. At its most basic level, the idea is “you get more of what you pay for”: increasing the likelihood of delivering on a climate pledge. Given the public attention paid to executive pay, this provides a positive signal to stakeholders about the firm’s strategic commitment to help combat climate change.

Companies undergoing a long-term structural transformation are likely to have complex strategies—with carbon-heavy and green businesses under a single corporate umbrella—and pursue high levels of innovation. These are precisely the circumstances under which the non-financial metrics like carbon emissions are particularly attractive because they allow this complexity to be reflected in the balanced scorecard for top management (Principle 2). Indeed, the evidence suggests that non-financial incentive metrics are used more heavily by companies that are more exposed to regulation, have more innovation-oriented strategies, and have “noisier” stock prices. 20

Principles 1 and 2 together justifier a broad link to climate performance in incentive pay by companies, like Shell, that are seeking to align with the low-carbon transition. These firms are explicitly accounting for climate change in their corporate strategies, and embarking on a complex transformation. However, Principle 2 alone also justifies a narrower pay link to the carbon emissions of individual business units, like ExxonMobil. One reason is that emissions reductions often involve cutting waste; an example is the flaring of methane that occurs during the extraction of natural gas. Hence emissions cuts can be a signal of management value-added even for a company that has been reluctant to embrace the low-carbon transition in its strategy.

A broader reason for carbon-intensive companies to tie incentive pay to climate performance stems from the fact that many sell into commodity markets (such as iron ore, oil, and steel) that are prone to boom-bust swings. Likewise, their corporate mindset also swings back-and-forth between a focus on growth and on profitability. This is reflected in scorecards: metrics such as production targets and market share are the “growth mode,” while others such as ROACE are the “profitability mode.” A greater sectoral focus on climate targets can impart greater discipline in capital allocation, favoring profits over growth (Principle 3) and reducing the appeal of high-cost, environmentally suspect investment projects. While executive pay will not solve the underlying problem, it may provide a nudge toward value over volume.

Investor backing for corporate climate action is supported by mounting evidence that companies with better environmental performance also have superior financial performance. The traditional argument is that ESG-related activity cannot be value-enhancing as it diverts resources from directly productive action but might still be pursued to benefit the reputation of management. 21 Yet, over the last 20 years, studies have found evidence that manufacturing firms with lower emissions have higher intangible asset values and that firms with higher environmental responsibility have lower equity financing costs. Case studies have shown how corporate initiatives at BP, Dow Chemical, and DuPont cut emissions and also cut costs, and there is evidence that companies that adopted high-sustainability practices enjoyed superior long-term stock-market performance. 22 While this remains an active—and sometimes controversial—research topic, there is growing belief among companies and investors that making money and “doing good” can go hand-in-hand. 23

When Is Incentive Pay for Climate Performance Not Needed?

Suppose again that financial, labor, and product markets operate smoothly—except for the problem of climate change. The most efficient economic policy is a global carbon price that reflects damages to the planet, which covers all countries and sectors of the world economy. 24 This induces firms to factor climate change into their decision-making so that it feeds through to the prices of their products and their profits. The role of companies is to respond efficiently to market signals, including the carbon price—there is no need for additional voluntary corporate climate action. Linking executive pay to the stock price is enough to provide suitable incentives.

Real-world markets and policy fall short of this ideal. While the World Bank estimated that the Paris Agreement requires a “target-consistent” global carbon price rising to $50 to 100 per ton of CO2 by 2030, 25 carbon prices currently cover around 20% of global emissions with an average price below $10. 26 Countries have introduced a plethora of policies (such as subsidies for renewables and electric vehicles), yet bottom-up analysis suggests that these still fall short of the Paris ambition. 27 Against this backdrop, investors are asking the corporate sector to take on a leadership role in the low-carbon transition—and this also opens a role for climate performance in incentive pay.

How? Designing Climate-Linked Incentive Pay

Companies in hard-to-abate sectors are reaching the diagnosis that their long-term survival depends on cutting carbon, and they are pledging to align their strategies with the Paris Agreement. Yet there are important differences in recent corporate net-zero pledges, notably that some relate to own production while others also promise a carbon-neutral value chain. The direction of travel, however, is clear, with increasing pressure from institutional investors for net zero based on value-chain emissions.

How should a corporate climate target be reflected in executive compensation? The most immediate answer is that, consistent with Principle 1, incentive pay should be linked directly to progress toward a company-wide climate target. Compensation practice, specifically Principles 2 and 3, raises additional challenges relating to the finer details of how incentives are structured. In some circumstances, boards need to consider more nuanced incentive pay that departs—to a degree—from the overarching climate target underlying a company’s strategy.

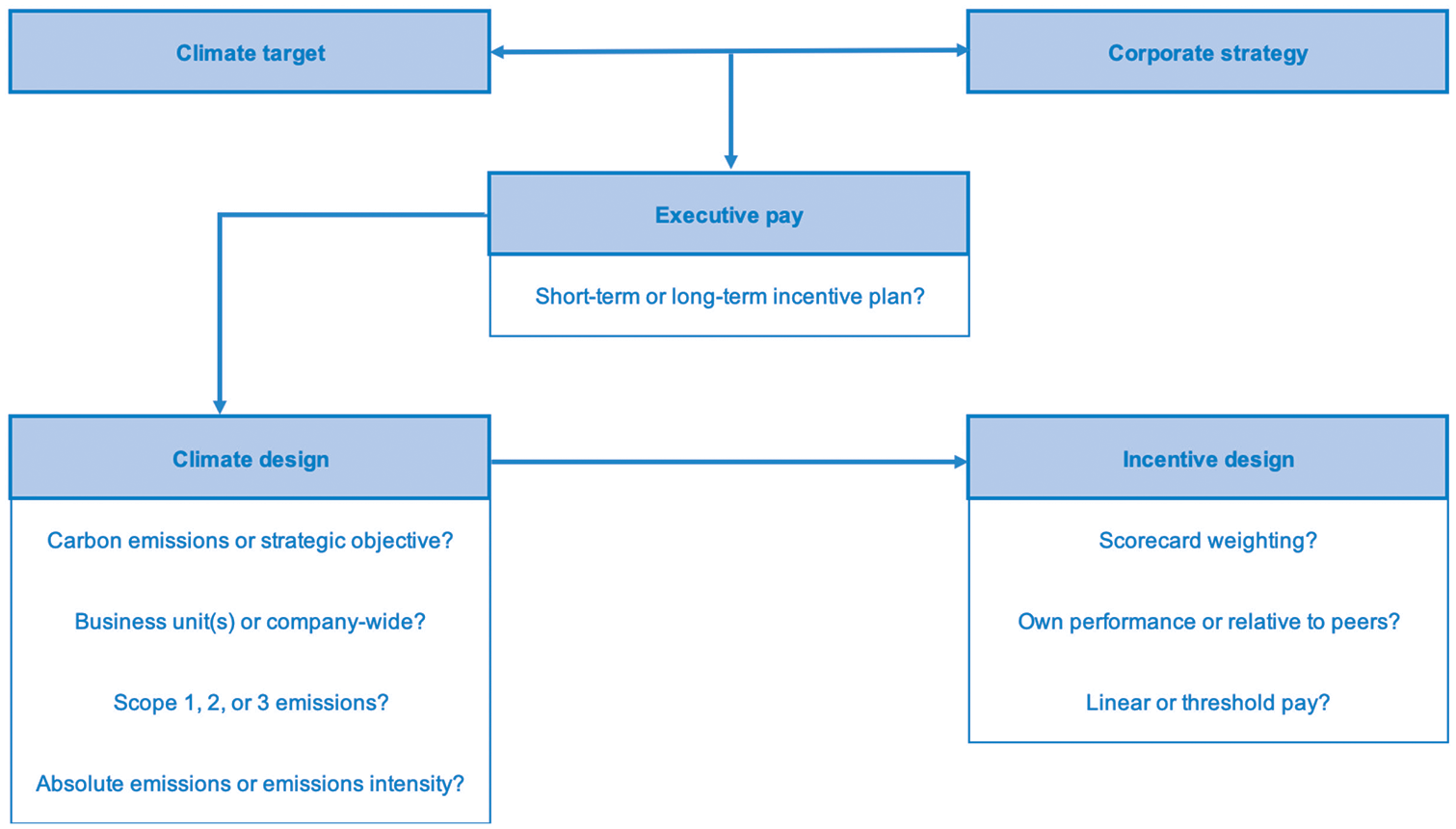

A Framework of Key Design Choices

Figure 2 presents a framework for the key choices in linking executive pay to climate performance. Given the development of a company’s climate ambition and corporate strategy, what are the different ways in which its climate performance can be incorporated into its short-term or long-term incentive pay for top management? The first set of choices concerns the climate metric itself. This can relate directly to carbon emissions or be a wider strategic objective related to the growth of low-carbon business or technology. It can be designed narrowly, pertaining to individual business units or broadly, covering the whole company. A key issue is the scope of emissions: Does the metric cover Scope 1 (direct production), Scope 2 (purchased electricity), or Scope 3 (value chain)? Finally, targets can be designed as a reduction in absolute emissions or in a business’ emissions intensity (emissions per unit of production).

Key choices in linking executive pay to climate performance.

The second set of choices is about the incentive design for this chosen design of the climate metric. This begins with its weighting in the scorecard underlying the incentive plan. It also covers whether the incentive pays according to a company’s own performance on the climate metric or whether there is relative performance evaluation, for example, against a peer group. Finally, it determines whether pay occurs incrementally with progress toward the target or only once a threshold is reached.

Applying the principles of incentive design to this framework yields insight into the relative merits of different ways of structuring short- and long-term incentives for climate performance.

Short-Term Incentive Pay

Linking incentive pay to a company’s climate performance begins with the balanced scorecard for annual bonus pay. Leading companies in carbon-intensive sectors such as oil & gas, mining, and steel have adopted this practice. In particular, a company should incorporate progress toward a climate pledge, such as net zero, as a scorecard metric (Principle 1). Sufficient materiality in the context of the incentive mix (Principle 3) suggests a weight of at least 10% alongside financial and other non-financial metrics (including ESG). Industry leaders may prefer a higher weighting.

An important lesson from the history of executive pay is that “non-linear” incentives can lead to distortions. Consider a sales target under which a manager receives a fixed bonus if the threshold is met at year-end and gets no bonus otherwise. Incentives are very weak if the target looks unattainable, very strong when it is almost reached, and zero if it is locked in before the year is over. This variability in the return to managerial effort is unlikely to be well-aligned with value creation. Moving the goal posts around once the target has been met risks undermining the credibility of the incentive program in the first place. A continuous reward for performance—like additional carbon cuts—is usually a better choice.

Metrics used in annual bonus pay are typically internal to the firm, precluding the use of relative performance evaluation against a peer group. This opens up the possibility that other climate-linked metrics may give extra information about management value-added (Principle 2). One challenge with paying for carbon cuts is that emissions may fall because of a recession or others drivers that are beyond management control. This provides a rationale for using a link to emissions intensity to give a stabler, more informative perspective on management’s environmental value-added. Companies should therefore consider using both absolute emissions and emissions intensity as short-term performance metrics.

Closely related, a company’s value-chain emissions are difficult to measure and significantly beyond management control. This lessens their appeal as an incentive metric: they give a blurred signal about management performance and expose executives to uncontrollable risk (Principle 2). 28 This suggests instead relying more narrowly on Scope 1 and 2 emissions, which are more directly controllable. Over time, opportunities will increase for management to influence Scope 3 emissions by switching to cleaner suppliers and finding ways to help customers reduce emissions. This will strengthen the case for using value-chain emissions in the balanced scorecard underlying incentive pay.

A well-known concern about “pay for performance” is that it can undermine radical innovation for the long term. Established companies have a natural tendency to pursue incremental innovation over drastic innovation that encroaches on their core business. 29 In a similar way, linking pay to carbon cuts immediately incentivizes reductions based on current technologies. This can achieve surprisingly quick results. However, there is also a risk that it crowds out the search for more drastic ways to cut emissions by developing new technologies. For greater balance, by Principle 3, it makes sense to additionally employ one or several strategic milestones for the CEO that relate to the growth push of new low-carbon lines of business.

Long-Term Incentive Pay

Linking long-term incentive pay to climate performance is the current frontier of this organizational practice. Especially at U.S. corporations, incentive pay for the CEO and top management is closely tied to shareholder returns. This means that any link to climate performance will displace financial metrics—even if the latter are likely to remain dominant. Nonetheless, companies seeking Paris-aligned strategies need to consider reflecting this in their long-term management incentives (Principle 1). The climate metric should be based on company-wide emissions, again with a weighting of at least 10% for materiality (Principle 3).

Institutional investors are putting pressure on companies to formulate plans for long-term value-chain climate neutrality. Directly incorporating this into LTIPs (Principle 1) raises challenges related to measurement and control of Scope 3 emissions (Principle 2). Indeed, the recent corporate history of measuring consumer emissions is not a happy one, as illustrated by Volkswagen’s “Dieselgate” scandal. Despite these concerns, strategic considerations increasingly point to a focus on Scope 3 emissions—especially as measurement improves across the value chain. There is also potential for a feedback loop: due to its Scope 3 targets, one firm puts pressure on its suppliers to reduce the emissions arising from the use of their products; these suppliers then put pressure on their suppliers, which in turn put pressure on upstream resource-intensive companies—which may themselves then be more inclined to take on a Scope 3 target of their own.

Executive compensation can be susceptible to concerns about “paying for luck.” For example, the profitability of many energy companies varies strongly with the price of crude oil—which is essentially beyond management control (Principle 2). Nonetheless, the evidence is that energy CEOs are paid systematically more when the oil price happens to be high. This transfers wealth from shareholders to management—and is sometimes interpreted as evidence of excessive value extraction by CEOs. 30 Incentives linked to climate performance raise a similar prospect of pay for luck. If global climate policy turns out to be tighter than expected, this will push down corporate emissions without being evidence of management performance. With incentives linked to Scope 3 emissions, things become even more complex: Should a CEO get extra pay if one of the company’s suppliers finds a lower-carbon way of delivering its product?

To sidestep such concerns, long-term incentive pay can be based on a company’s performance relative to a peer group of comparable companies. This filters out the “noise” that can make a mediocre management effort look brilliant (and vice versa). It is also common practice for financial metrics: a company’s TSR is often compared to a peer group (Figure 1). In a similar way, climate-linked incentives could be based on a company’s emissions cuts relative to its peers. A concern is that this requires confidence that peers’ emissions are accurately measured—and indeed sufficiently comparable. As carbon measurement improves over time, opportunities for relative performance evaluation should be enhanced.

Climate-Linked CEO Incentives at Shell

Shell has, for the time being, emerged as the climate leader among the energy majors. In December 2018, it announced tying the incentive pay of its CEO and senior management to company-wide carbon targets from 2020 onward. In introducing the new energy-transition metric, Shell reduced weights placed on financial measures (specifically on ROACE). Figure 3 applies the framework of key design choices to Shell’s CEO’s STIP and LTIP.

Climate-linked performance metrics in Shell CEO incentive plan.

Shell’s short-term CEO incentive is based on reductions in the emissions intensities of several business units—refining, chemicals, upstream, and integrated gas—in terms of Scope 1 and 2 emissions. This is in line with capturing management’s environmental value-added (Principle 2), but the incentive design may be seen critically in environmental terms for failing to not rule out increases in the absolute level of emissions. Relatedly, there is a tension with other parts of the scorecard (Figure 1) that incentivize growth in production volumes. Incentive payments accrue incrementally with reductions in emissions intensities—rather than only once when a threshold value is reached—with the remuneration committee retaining some discretion.

The LTIP uses an “energy-transition metric” with both carbon cuts and strategic objectives. It features long-term company goals for emissions reduction to 2030 and 2050, measured in terms of “net carbon footprint” that includes value-chain emissions. It also features a set of strategic CEO milestones for the growth of new low-carbon businesses and technologies in power, advanced biofuels, and carbon capture systems (CCUS). Hence there are both lagging and leading indicators that are explicitly linked to innovation. The remuneration committee can decide to allocate greater emphasis to the carbon footprint metric and expects the weighting on the energy-transition metric to increase over time. In sum, the long-term climate incentive is significantly broader and more explicitly quantified than its short-term cousin.

Shell’s incentive design is pioneering the strategic use of value-chain emissions. In May 2019, it sold two carbon-neutral cargos of liquefied natural gas (LNG) to Japanese buyers, Tokyo Gas and GS Energy, for which the life-cycle emissions of the natural gas will be offset by carbon credits from Shell’s portfolio of “nature-based solutions”: forestry assets that act as carbon sinks with negative emissions. This is an initial example of how a strategic focus on value-chain emissions creates a product that is valued by greening customers. Over time, as measurement and control of Scope 3 emissions improve across the energy industry, the incentive design could be refined to include relative performance evaluation against a peer group.

Caveats and Pitfalls

There is no silver bullet: linking pay to carbon cuts will, on its own, not be sufficient to drive successful corporate change in hard-to-abate sectors. Any single incentive metric, perhaps aside from shareholder returns, usually has only a modest impact on a CEO’s compensation and wealth. Climate-linked incentives are therefore best implemented as part of a wider package of organizational tools to support a low-carbon transformation. This can include an internal carbon price to test new investments, or adjusting hurdle rates to account for a project’s climate characteristics.

Conversely, climate-linked executive pay is not necessary for a successful low-carbon change. A few companies have already undergone full-scale transformations from “brown” to “green.” While each has its own unique features, a notable example is Ørsted, previously Denmark’s state-controlled oil & gas company, and now widely hailed as one of the world’s largest and highly valued renewable energy companies. The steep decline in the cost of wind power, supported by government subsidies, and the sale of its disadvantaged legacy oil & gas business, helped make this transformation successful in a short time span—without involving a climate component in executive pay. 31

As is always the case with executive pay, boards need to be mindful of the potential for distorted incentives. A corporate pledge to cut emissions can affect M&A: many companies have scored a “quick win” with the divestiture of a high-carbon business unit, notably those involving coal. Similarly, outsourcing a polluting activity to a supplier can look increasingly attractive. The global climate benefit of such moves is less clear—the emissions just resurface under a different corporate roof. 32 While climate-linked pay is not the root cause, it might exacerbate such incentives. A solution is to net out the impact of such activity. This is standard practice in financial accounting: for example, earnings per share are routinely adjusted for one-time gains from the sale of an asset. Likewise, appropriately adjusted climate metrics can help avoid “gaming.”

Finally, it is important to stress that there is no systematic evidence yet on the ex post performance of climate-linked executive pay. The same is true for many new business practices that companies will have to adopt to thrive in the low-carbon transition. Understanding the performance impact of different ways of linking pay to climate metrics would require carefully measuring their impact—in terms of a company’s financial performance and carbon emissions—relative to a counterfactual without the incentive. This will be an important topic for future empirical research at the interface between climate, finance, and management.

Conclusion

Under increasing pressure from institutional investors, companies across virtually all sectors of the economy are pledging to cut carbon and, over the longer haul, aim for climate neutrality. Now, these companies need to identify and implement business models and organizational tools to deliver on these climate commitments. The challenge is most acute for hard-to-abate sectors—such as oil & gas, aviation, aluminum, cement, chemicals, steel—in which managers simultaneously need to extract the remaining value from legacy businesses and invest in new low-carbon products and technologies for future growth. In a way that would have seemed surprising even five years ago, carbon has become a key performance indicator, and the financial sector may turn out to be a major force in solving the climate problem.

Linking executive compensation to climate performance is emerging as a novel element of the corporate response to the low-carbon transition. Climate-linked incentives strengthen the alignment, at the board level, between corporate strategy and management incentives. The narrow variant includes a climate metric in the balanced scorecard underlying annual bonus pay; the broader variant links the LTIP to climate change, typically displacing some weighting on shareholder returns. The practice is not yet widely adopted, with a recent analysis of UK FTSE 350 companies finding that less than 2% of performance conditions in annual bonuses for board members relate to “sustainability” and “environmental” metrics. 33 Leading companies in hard-to-abate sectors that wish to transform their business should consider a weighting to climate metrics in STIP and LTIP. Climate-linked executive pay is no silver bullet, but it sends a constructive signal to investors, customers, and suppliers—and to current and prospective employees—about the future of the business.

So far, the use of climate-linked incentive pay involves a degree of experimentation, and there will be scope for refining the practice over time. This is good business practice: see what works and then make adjustments so as to avoid unintended consequences. A central challenge is whether to design incentives based on emissions from own production or to include the value chain; principles of incentive design point to the former while strategic considerations increasingly favor the latter. Over time, as emissions measurement improves across the value chain, holistic incentives will become more attractive. Unlike the traditional metric of TSR, climate-linked pay so far does not include evaluation against a peer group. As the practice becomes more widespread, the scope for relative performance evaluation will increase to better reflect management contribution rather than “pay for luck.”

Footnotes

Acknowledgements

The author is grateful to Simon Dietz, Felix Grey, Jennifer Howard-Grenville, Thomas Kansy, Kevin Massy, Julian Metherell, David Pitt-Watson and David Reiner for helpful comments and discussion and to Olivia Chen for excellent research assistance. All views expressed and any errors are my own.

Notes

Author Biography

Robert A. Ritz is Assistant Director of the Energy Policy Research Group at Judge Business School, University of Cambridge (email: