Abstract

The pandemic crisis caused a severe shock to global value chains and led to supply shortages for complex medical goods such as respiratory ventilators. What followed were calls to reshore production for security, and the loss of efficiencies from foreign global value chain (GVC) operations for the multinational enterprise. This article merges internalization and GVC theory to demonstrate a dynamic hierarchy managerial response to these crisis conditions. An optimally configured GVC under hierarchy governance can resiliently eliminate global supply line ruptures yet maintain the benefits of global efficiency.

Keywords

The GVC model of disaggregated production activities to gain worldwide location advantages has been developed and honed for efficiency for much of the liberalized post-war era. 5 GVC theory has been predominantly concerned with the externalization of MNE activities and asymmetric power relations, particularly with suppliers in developing countries having upgrade potential. 6 Consequently, the GVC governance modes around “market,” “modular,” “relational,” and “captive” dominate research attention and managerial guidance. 7 As a result, we contend that hierarchy has comparatively become the forgotten sibling of the GVC governance family. The hierarchy GVC governance mode conventionally involves centralized control of internalized GVC configuration and activities, and has been considered more insular and rigid. 8 However, no GVC framework is static. For example, GVC scholars have made much use of the concept of the dynamics of upgrading for independent suppliers in external networks. And yet upgrading has been largely ignored under hierarchy governance.

It is well established by IB scholars that MNE subsidiaries can play a crucial role in the realization of the benefits of hierarchical GVC governance of the MNE by improving their operational and innovation capabilities over time, often in partnership with external local actors. 9 But some IB scholars at the intersection of internalization and GVC theory maintain that GVC theory to date has had little to say about the reasons and ways by which MNEs might keep activities in-house, and they call for research to uncover how the GVC approach can extend and add nuance to internalization theory. 10 One aspect advocated for further study is how internalization theory might better reflect the reality of GVC dynamics and how GVCs adjust over time. GVC theory on hierarchy governance mode has not sufficiently accounted for such internal upgrading dynamics and activities of subsidiaries within the MNE. Consequently, GVC theory could be extended for the internalized hierarchy governance mode by applying the core tenets around extensive upgrading developed by scholars of the more studied externalized GVC governance modes. In so doing, internal MNE dynamics of subsidiary upgrading play out under hierarchical GVC governance over time. The particular research question here is: how did a subsidiary capably upgrade within an MNE, under hierarchical GVC governance mode, to provide an effective balance between global production efficiency and supply resilience? We were afforded the opportunity to stress test an internalized GVC’s efficiency and resilience in a crisis when faced with a huge demand surge due to the generational disruptive shock of a global pandemic.

In this article, we draw from a wider longitudinal study of the evolutionary dynamics of the GVC for one product division of an MNE in the medical technology sector, Medtronic Inc. Vertical integration was evidentially deemed the applicable organizational solution to best maintain hierarchical control over internalized operations and, principally, to safeguard valuable IP. For this protracted qualitative study, we adopted an intensive single case approach 11 wherein we particularly focused on Medtronic’s foreign subsidiary in Galway, Ireland, within its internalized product GVC. We traced, in real time over fifteen years, this subsidiary’s evolution from its original role as a basic assembly operation to its current status as a center of excellence for production and product development. The guiding theoretical focus of the broader research project was on providing a contextualized explanation 12 of how the case subsidiary upgraded within its internalized GVC through advancing its capabilities in manufacturing and product development. It thereby was able to assume a measure of shared responsibility with HQ for the governance of this product’s GVC. 13 Then, when the pandemic suddenly struck, corporate HQ had full confidence in the case subsidiary’s capabilities to manage both efficiency and resilience of this GVC. Rather than reshoring, HQ organized for this competent foreign subsidiary to partner with a smaller, co-located Medtronic production site to help deliver extraordinary production and supply performance. Production of respiratory ventilators was ramped up in Galway to deliver back to the United States a 40% increase in these essential medical supplies, by the end of March 2020, and of requisite quality. 14

Theoretical Development

GVC within the MNE

The GVC framework provides an effective approach to understanding the complexity brought about by the global dispersion of once co-located supply chains. Co-located supply chains are well documented in the industrial districts and industrial clusters literature. They typically represent more optimal models of industrial organization when innovation is incremental. However, this logic was severely undermined by the emergence and diffusion of GVCs and the consequent dispersion of once co-located phases.

For an MNE, a GVC has been described as “a governance tool to organize IB activities” 15 that can be geographically dispersed across many countries to gain location advantages. 16 In the IB view, MNEs are concerned with what should be done inside the firm and outside it, and where. 17 An MNE either plays the role of “lead firm” in a networked combination of offshore and outsourced supplier firms centered on a key orchestrator (as in Buckley’s conception of a “global factory” 18 and Mudambi’s “GVC smile” 19 ) or of a network of subsidiaries within its internal boundaries 20 (conventionally with HQ as the “lead” unit).

According to the predominant stream of studies in the GVC field, the relationship between an MNE and its global suppliers is generally regulated by network-type forms of governance, such as “modular,” “relational,” and “captive.” Situated between the two governance extremes of the market and the hierarchy, these forms of coordination don’t imply any formal participation of an MNE in the ownership of the global producer. Hence, they are commonly referred to as non-equity forms of governance. These governance forms have allowed MNEs to exploit the benefits of globalization while avoiding the rigidity induced by foreign direct investments. Advocates report that, by using network-type forms of governance, MNEs have increased their profitability and global reach without impacting their overall efficiency. They suggest that, by relying on independent contractors, they have increased their flexibility and efficiency, and have also developed a lighter and more agile organizational structure.

Some scholars assert that reports of the demise of the vertically integrated MNE may have been largely exaggerated. 21 For these scholars, conditions persist where it may well be the most efficient solution to GVC organization. For instance, in certain high-technology industries, such as medical technology and pharma, where a strong imperative for the protection of valuable proprietary knowledge applies, some knowledge-intensive MNEs have good reason to maintain control over activities. Moreover, the global system is facing ever more disruptive shocks that will inevitably continue to adversely impact GVC activities and increase pressure for greater internal control. This calls for the hierarchical mode of GVC governance. Under hierarchy, activities are contained mostly within an MNE and control is typically exercised by HQ management. 22 But a hierarchical GVC is not a static framework; naturally, its coordination mechanisms and internal power dynamics evolve over time. Within the scope of internalized GVC activities of an MNE, overseas subsidiaries can upgrade to improve their position. Internal dynamics can be vibrant under hierarchy. 23 Subsidiaries cooperate on some GVC activities yet compete with sister subsidiaries for investment, resources, and upgraded mandates. Subsidiary success, as reflected in enhanced long-term survival prospects within an MNE, comes through upgrading its production and innovation capabilities over time. Subsidiaries that successfully upgrade may well gain the competence trust, and maybe later goodwill trust, of HQ in their increasingly advanced production, innovation, and organizational capabilities.

If we maintain that externalization is the only (or predominant) way a GVC is organized and orchestrated, then it’s easy to understand why efficiency and resilience of GVCs are seen as two opposing values. Indeed, efficiency is achieved by dispersing production activities to independent contractors, which inevitably leads to a sharp decrease in the control an MNE exerts over value chain functions globally. As a result, the most obvious way to enhance the resilience of an MNE and stabilize its supply chains, even more so in times of crisis, is to withdraw global operations, relocate production close to an MNE’s HQ, and increase inventories. If implemented, however, this approach may lead to the demise of many GVCs and prevent MNEs from exploiting the various benefits globalization has offered over the past two decades. In short, reshoring implies compromising efficiency for improved resilience.

Balancing Efficiency and Resilience in GVCs

Efficiency is the ratio of outputs to inputs in a production or value creation system 24 and has been one of the pivotal considerations for MNEs when growing and coordinating their GVC activities across borders and locations. The prioritizing of efficiency has led to the rise of South-East Asian countries, particularly China, as the primary locations of manufacturing and increased the dependence of GVCs on these countries for the supply of products. 25 The recent interest in GVC resilience has sparked some ideas about how the world and GVCs can deal with global pandemics 26 but has also raised inquiries about the interface between efficiency and resilience. 27 Both scholars and practitioners have highlighted the significance of resilience and the need for GVCs to diverge from the efficiency imperative and move toward a resilience imperative. 28 There is no definitive answer to whether efficiency and resilience are mutually exclusive and whether firms must sacrifice one to achieve the other. 29 There is, though, limited knowledge apropos the prospective consequences of the resilience imperative for GVCs and the efficiency-driven management paradigm that has directed the up-to-date discourse on GVC governance and expansion.

Albeit efficiency and resilience in GVCs may be at odds with each other in the short-term perspective, they are not unescapably mutually exclusive in an elongated outlook. Furthermore, a mainly in-house GVC (i.e., within the realm of an MNE) is both managerially and socially different from a GVC solely outsourced to stand-alone firms. Almost two decades ago, resilience was emphasized as one key characteristic of durable systems 30 —along with diversity, efficiency, adaptability, and cohesion. Consequently, there might be more to the interplay between resilience and efficiency than the presumed trade-off once the long-term perspective, the global aspects of the business environment, and the governance are considered.

Resilience is embodied by the long-term survival of MNEs and their GVCs amid disruptions and difficulties. 31 We define resilience in GVCs as the adaptive capability of the supply chain to organize for unexpected incidents, act in response to disruptions, and recuperate from them by maintaining continuity of operations at the desired level of connectedness and control over structure and function. 32

To achieve both resilience and efficiency, MNEs’ ability to coordinate activities and actors at a distance is imperative. For effective coordination, an MNE needs to realize three things: 33 manage bounded rationality, manage the reliability of the parties involved in the GVC, and establish an environment supportive of innovation and capability generation. These challenges are all easier to achieve within the boundaries of an MNE rather than outside its realm. Particularly, dealing with information asymmetries and constrained information processing capabilities (bounded rationality) and lessening risks with living up to open-ended or incomplete contracts (bounded reliability) is much less arduous between HQ-subsidiary and subsidiary-subsidiary within the same MNE despite that the relation might be quite distant compared with managing this between stand-alone firms.

The costs of knowledge exchange and monitoring and of avoiding knowledge leakage are more likely in relations between stand-alone firms in a market compared with relations between actors within the same ownership structure. 34 Having a subsidiary supplying from a specific environment gives an MNE increased potential to leverage knowledge access to non-business actors within that environment compared with relying on stand-alone firms’ benevolence. It does require that the HQ decentralize decision making and autonomy to the subsidiary so that it can perform to its potential regarding leveraging knowledge from non-business actors as well as from local business actors. 35 A further upside derived from ownership of a GVC unit is that instituting common norms that generate social and relational capital—essential to a more efficient flow of tacit knowledge 36 and contribution to common goals of the GVC 37 —is facilitated.

To investigate the dynamics of the hierarchy mode of governance more closely, we draw on the case of Medtronic Inc. and focus on its subsidiary units in Galway, Ireland.

Case Background: Medtronic and Its Subsidiary Sites in Galway, Ireland

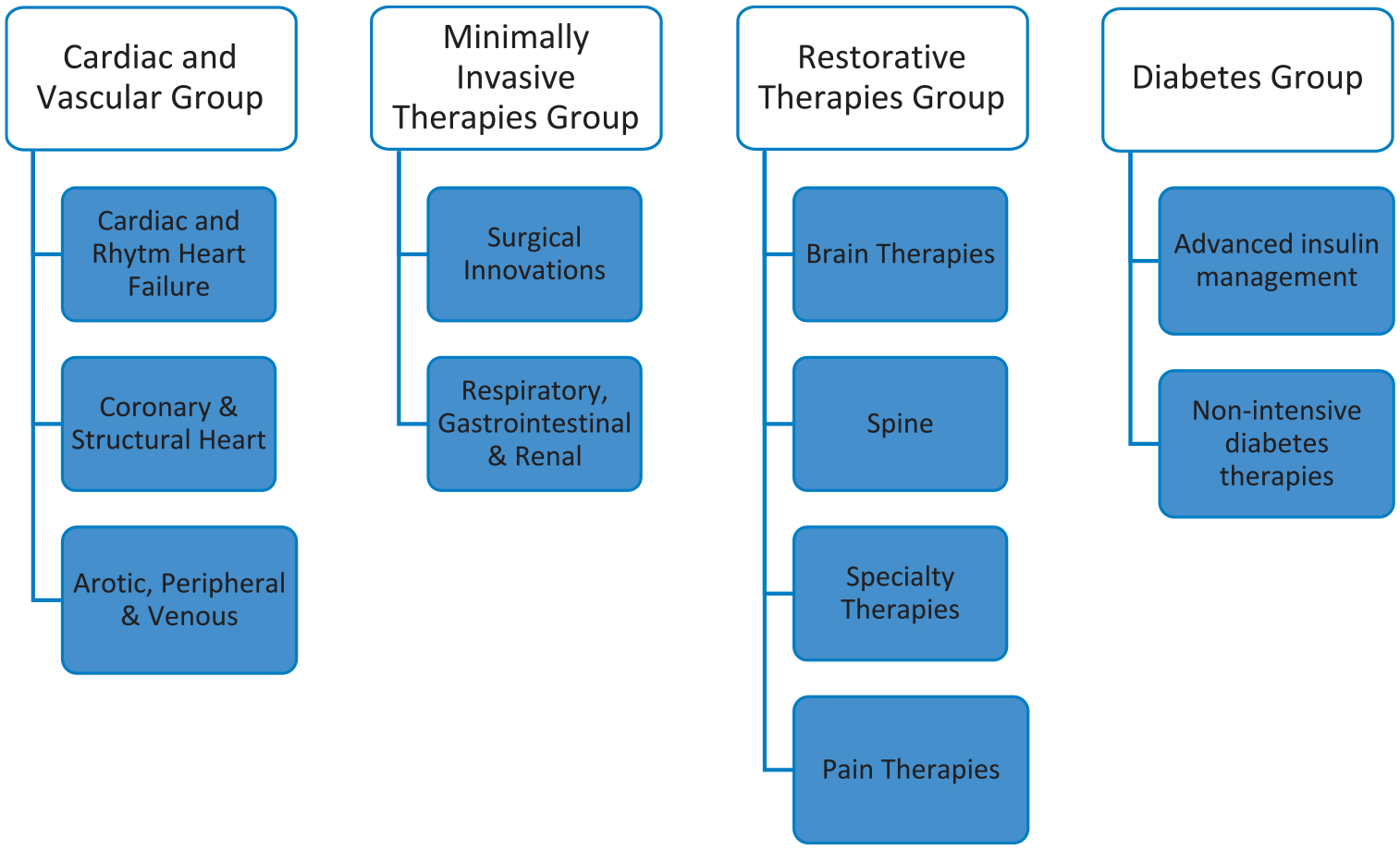

The medical equipment industry contains multiple diverse GVCs, but complex engineered goods are the focus of our study. This segment is dominated by large MNEs with huge R&D budgets and extensive global reach, often restricted to developed economies with requisite knowledge and skills and strong IP regimes. They tap into advanced knowledge repositories across the globe through dispersed subsidiaries. Medtronic Inc. is one of the world’s largest complex medical equipment corporations. It has annual revenues of almost $30 billion and approximately 90,000 employees worldwide. It is organized around four business groups centered on therapies for differential conditions, each containing multiple business divisions with respective GVCs (see Figure 1). The Minimally Invasive Therapies Group, which includes the production of ventilators that have been crucial in the pandemic, accounts for about one-third of these revenues and employee numbers.

Medtronic Inc. businesses: Groups and divisions.

Recent quarterly results 38 from Medtronic for Q3 2021 (end of the fiscal year is April) show that while revenue fell in comparison to the same quarter in 2020 in the Cardiac and Vascular Group as well as the Restorative Therapies Group by 5.9% and −0.8%, respectively, revenue grew by 4.6% in the Minimally Invasive Therapies Group and 0.8% in the Diabetes Group. The Respiratory, Gastrointestinal & Renal division has driven the revenue growth within the Minimally Invasive Therapies Group, growing by 25.4% over the same period compared with a decline of 5.3% for the Surgical Innovations activity (also within this group). The declines in other activities and Groups are attributed mainly to declines in hospital procedure volumes as a result of COVID-19 resurgences. At the same time, Medtronic reports in its Q3 2021 results that the sales of ventilators increased almost threefold. As a result, Medtronic’s net profit margin at the 2020 fiscal year-end compares strongly at 16.56% against competitors—for example, Boston Scientific’s −0.83%, Becton and Dickinson’s 5.11%, Abbott Laboratory’s 12.86%, and Johnson & Johnson’s 17.82%. 39 Of course, other competitors directly in the ventilator market that focus almost entirely on respiratory activity show larger net profit margin growth as they do not contend with the same level of offsets—for example, ResMed that achieved a net margin growth of 21.02% in 2020 and a net income growth of 53.65%. 40 Medtronic’s net income growth in 2020 was 3.41% but was again much higher than many of the other main competitors: Boston Scientific (−101.74%); Becton and Dickinson (−29.17%), Johnson & Johnson (−2.68%), and Stryker (−23.24%). 41

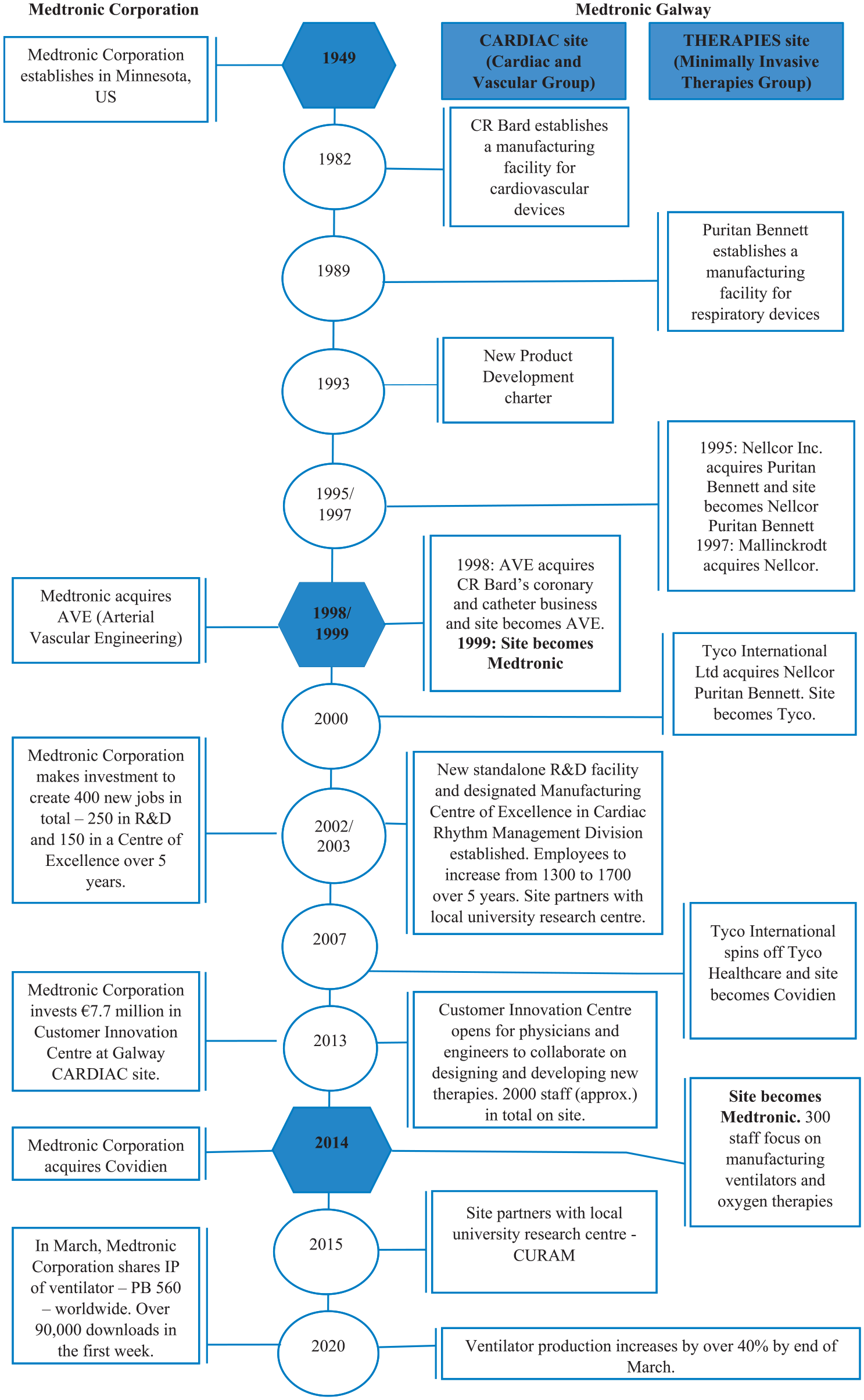

There are two main Medtronic subsidiary sites in Galway; one site (CARDIAC) operates within the Cardiac and Vascular Group of Medtronic and is known for its expertise in producing drug-eluting stents, and the other site (THERAPIES) is part of the Minimally Invasive Therapies Group and produces respiratory and monitoring solutions. Both site facilities have a long history in the region, operating under the auspices of different corporate parents at various points in time. The Galway THERAPIES site was established in 1989 as a subsidiary of Puritan Bennett, a worldwide producer of respiratory products (including critical care ventilation) since the early twentieth century. Indeed, the high-performance ventilators that Medtronic supplied during the pandemic are inherited from the Puritan Bennett era. Since its establishment, the site has experienced five acquisitions: Nellcor (1995), Mallinckrodt (1997), Tyco (2000), Covidien (2007), and, most recently, Medtronic in 2015. On the other hand, the Galway CARDIAC site—which was also first established in the 1980s—has a much longer standing within the Medtronic Corporation itself. It has experienced three corporate parents over the course of its lifetime, starting as a subsidiary of CR Bard in 1982, which was subsequently acquired by AVE in 1998 and by Medtronic in 1999. The Galway CARDIAC site is also much larger than the Galway THERAPIES site, employing about 2000 people compared with a workforce of approximately 250 in the Galway THERAPIES site in March 2020. The main events and outcomes of the sites, as well as significant decisions by Medtronic HQ over their history, are depicted in Figure 2.

Temporal evolution of Medtronic Galway subsidiaries—Main events and outcomes.

Our longitudinal study explains how the Galway CARDIAC site in particular achieved an all-important upgraded role within a particular product global value chain and shows how it could be relied upon to collaborate with the Galway THERAPIES site to meet extreme ventilator production demands during the pandemic crisis.

Method

The GVC framework is particularly useful in the investigation of the organization of product-specific value chains. For this reason, focusing on a specific product or product line represents a necessary condition for an effective analysis of the dynamics underlying a GVC. To examine the evolution of this product GVC over time, we conducted semi-structured interviews over a 15-year period (2005-2020). A process study such as our single longitudinal case seeks to lay out and explain temporal evolution. 42 Such a process research approach permitted us to chronicle the historical sequence of events and explain the evolutionary processes: in our case, the upgrading of a focal subsidiary over time. The longitudinal nature of the data set enabled us to place the focal events into the context of the subsidiary’s development over time. The result is that it allowed us to explain how and why these focal events occurred: specifically, how the changing nature of the subsidiary affected its responses, and that of the GVC, during the crisis posed by the pandemic. Our interviewees consisted of both HQ and subsidiary management. On one side were select senior management at Medtronic HQ chosen for their apposite knowledge of the Cardiac and Vascular Group division due to their executive responsibility for the Galway CARDIAC site. The preponderance of data, given our wider research interest in a subsidiary’s upgrading within a multinational’s GVC, was collected from interviews with senior executive management (past and present) as well as operations and R&D managers in the Galway subsidiary. These managers possessed first-hand knowledge of the processes under investigation. For this study, we honed in on interviews over this extensive period that we conducted with 14 senior managers, many repeatedly. Our semi-structured interviews became more fluid over time as rapport developed and confidence in our research motives grew. 43 Topics transformed over time but mainly focused on subsidiary strategies, HQ mandates, the nature of evolutionary relations and trust, engagements with local actors, confidence at HQ, and technology frontiers.

We supplemented this interview data with secondary data collated from the corporate website, press pieces, and social media on Medtronic Inc. and its Galway subsidiary. Specifically, we tracked and collated secondary sources on key events, critical happenings, and notable milestones in the case firm over the full course of the study. Much of the data in the immediate aftermath of the crisis was secondary in the form of contemporary interviews with Medtronic HQ management in the televisual, financial, and economic press and on personal and organizational social media.

Our data analysis commenced with within case interrogation of data across the years in the case folder. We digitally searched our copious interview transcripts for data on the key themes of subsidiary upgrading activities and HQ governance in this GVC. We followed the logic of narrative analysis 44 as an interpretivist technique to explain how the subsidiary’s upgrading over time furnished a measure of shared governance of this product GVC. In doing so, we identified, interpreted, and explained the meanings, decisions, and perspectives of managers across time. Pertinent quotes were selected to specifically illustrate critical insights and particularly relevant evidence. We went back and forth between our ongoing interview data accumulation and GVC theory on governance and upgrading in interpretivist analytical mode to make sense of the internal GVC dynamics under hierarchy. Finally, we further deepened our interpretation of our interview data and enhanced the reliability and trustworthiness of our findings through triangulation with the comprehensive secondary data. 45 We lastly draw on secondary media and corporate performance data to demonstrate how this engendered a simultaneously efficient and resilient GVC through foreign operation, even when confronted by a hugely disruptive pandemic.

Findings

From its establishment in 1982 to the mid-1990s, the CARDIAC facility was largely a site that executed manufacturing projects mandated by the divisional parent company at the time. The primary motivation for establishing the facility was around cost-efficiencies. One of the ex-managers who started working first as a process engineer in the facility in the early years explained, “My first job was to migrate manufacturing lines from the U.S. . . the products were pretty low-tech—catheters.” As noted in this interview, the site’s initial projects were the manufacture of simple catheters, guidewires, and then balloon catheters by the late 1980s, which were all in the field of cardiology. The manufacturing product area of expertise became (and still is to a large degree, albeit more sophisticated) balloon catheters used in angioplasty procedures where there is an obstruction in an artery wall of the heart. However, interviews with members of the original site management team showed that the subsidiary managers knew from the outset of the need to upgrade as a site to survive within a large foreign-owned corporation. As one ex-manager stated, “We had a very good, committed management team that was intent on building on all opportunities.” The strategy of the then management team was not just delivering the mandated project efficiently via replication, but to add value by using engineering competencies in the local milieu, as demonstrated in the following statement by an ex-Manager: During the migration we took products and if you take some of the manufacturing processes . . . so when I took the abrasing equipment from the U.S. I wouldn’t replicate it. I would upgrade it and get it sourced in Ireland so that it would be built in an Irish manufacturing site with upgrades . . . We also used control systems that they [the Division] didn’t do. We used PLC (Programmable Logic Controllers) technologies that were just coming into the market at the time, and we built PLCs into the equipment as we transferred it.

The site sourced processes and equipment locally (e.g., from research centers at the local university) as well as integrated new-to-market technology at the time into manufacturing projects. For instance, the site team took the initiative (independent of Corporate) to engage in a formal relationship with the local university around laser machining to add more advanced manufacturing processes. This early “process” upgrading was the beginning of corporate evolution completed by the site. As an ex-Director from the site stated, We scored an awful lot of brownie points for doing things like that with the Divisional HQ. We were all building kudos with senior corporate management teams . . . And by getting a couple of projects under our belts that showed our ability to do things, they just kept giving us more . . . We were always assuring the corporation that if they gave us the budget, we would give them the return.

In the early 1990s, the Galway CARDIAC site had the opportunity to vie for a new product development charter when a regulatory issue arose for Divisional HQ that limited the latter’s engagement in developing particular cardiovascular products.

46

Having demonstrated competencies in adding value to projects—as well as the favorable business context that the site operated in (e.g., a low corporate tax environment), access to skilled labor, and the site’s proximity to a university—the site won this charter and established a new product development team in 1993. As an R&D manager in an interview recounted, There was difficulty then with CR Bard and the FDA concerning safety and management of the company . . . the company realized that it needed to develop new products and it decided to give an ambit of responsibility to the facility in Galway to start into developing new products itself.

By the time Medtronic acquired the site in 1999, the site was affiliated to 23 patents filed in the United States, demonstrating a growing capacity for innovation. Significantly, when Medtronic finalized the acquisition deal in 1999, it continued and furthered the investment in the R&D function at the site (along with manufacturing), announcing plans shortly after the acquisition for 250 specialists to be working on-site in R&D. Furthermore, some managers from the site assumed Global R&D roles within the Cardiac and Vascular Group that demonstrated the credibility subsidiary managers had gained internally at the corporate level.

During the first decade of the site under Medtronic’s parental control, product design and development work focused primarily on the drug-eluting stent, which was the major technological development happening at the time in medical devices for angioplasty procedures. Building on its earlier expertise in balloon catheters, the site continued to develop a depth of engineering expertise in the delivery system of drug-eluting stents. As an R&D Director stated in an interview, “definitely delivery systems and balloon catheters is a key competency for this organization here [in Galway] that has grown over the years.” This was facilitated by formal linkages with local suppliers and the local university in establishing the subsidiary site’s own collaborations. An interview conducted in 2005 with an R&D manager reported the use of suppliers locally for finished components (e.g., hypotubes) as well as sub-assemblies. In response to whether the site uses the corporate network of suppliers, the manager stated (in 2005), “because of our own tie with the product in terms of developing the product, we would try and identify suppliers ourselves for those products.” Significantly the site became an industry partner to the local university’s research centers—REMEDI in 2003 and CURAM in 2015—to collaboratively develop new products or technologies under formal contracts. As the expertise of the site evolved, the subsidiary worked formally with physicians and research centers internationally as well as locally. An R&D Manager explained in an interview in 2005, “the way the sector works is that there are a number of physicians that are well respected internationally, so we [in Galway] would work with those internationally-respected ones as well as the local ones.” Engaging in this more advanced activity resulted in the cumulated number of patent applications filed in the United States linked to the site more than doubling between 2005 and 2014. Overall, during this decade, the Galway subsidiary moved from being predominantly a manufacturing unit to becoming a generator of innovation, performing new GVC functions such as R&D and product development. It was thanks to this transformation that the Galway CARDIAC site accomplished “functional upgrading” in its relevant GVC.

In the past five to ten years, the site began to act in a GVC joint coordinator role for drug-eluting stents as it started to lead global product development teams for next-generation delivery systems as well as stents and can now also choose to shift basic manufacturing to other sites abroad, such as Mexico. As a senior manager stated, “Galway has inverted. . . . We are behaving almost like an HQ. . . . we have gotten to a point where we are such a key element of the [global] organization that we actually can operate almost as we want.” This transition to a GVC joint coordinator role has not only been based on technical engineering competency, but also project management and leadership competency. A Global R&D Director for the Cardiac and Vascular Group that we interviewed confirmed that he has a team working today [in June 2019 when the interview was conducted] where the core team leader is based out of Galway. . . . She has her delivery system engineers that are based out of Galway and her stent engineers are based out of California.

This Global Director explains that for a site to gain responsibility, it must have developed leadership competencies among its people as he states: “So the biggest growth for any site in the world will be around can we grow the leadership on site. . . . If you can get the leadership, and it takes a long time to grow leadership, . . . the money follows the talent.” The existence of such technical, project management, and leadership competencies allows the site to operate as a GVC joint coordinator, and it is this status internally that Medtronic could rely on in a time of crisis.

As the virus brought devastation to New York City and across the United States, the pleadings for ventilators were vociferous.

47

In the face of such excruciating pressure, Medtronic’s CEO at the time, Omar Ishrak, conceded in an interview with CNBC that Medtronic would substantially ramp up production of these critical ventilators at its Galway subsidiary (THERAPIES site) on the West coast of Ireland.

48

For ventilators, these were the most advanced proprietary models of Medtronic, the IP for which was not shared externally, as very publicly happened for its less-advanced models both in the United States and worldwide.

49

With the onslaught of COVID-19, increased production responsibility fell on the Galway THERAPIES site to help meet the demand of these advanced ventilators. Reflecting on the period in which COVID-19 began to advance in China, one employee from the Galway THERAPIES site stated, “I always knew it would come to our door.”

50

Medtronic had planned substantial increases in ventilator production from 200 units per week in March 2020 to 700 units per week by June and 1000 by the end of that month.

51

By the end of March 2020, the Galway THERAPIES site had already increased the production of ventilators by over 40%.

52

Commenting on how this rise in production and increased responsibility was met, the leaders of Medtronic Corporation pointed to collaboration (both internal and external) as a key factor. Executive Vice President and President of the Minimally Invasive Therapies business group globally, Bob White, provided more details in a “frequently asked questions” interview posted on the Medtronic website in March 2020. He identified internal collaboration in the form of employees from the Galway CARDIAC site joining forces with the Galway THERAPIES site to help meet the commitment. In this interview on March 27, 2020, Bob White stated, We have ramped our ventilator capacity in our Galway facility [THERAPIES] up by 40% already [end of March 2020] . . . the very skilled operators . . . [they] have come over from Galway—from the CVG plant [CARDIAC] as well—to help on the MITG [THERAPIES] plant. So we are really seeing tremendous Medtronic mobilization.

53

Prior to the COVID pandemic, the two sites (CARDIAC and THERAPIES) operated largely independently of each other because they function in distinct business groups within Medtronic. However, to meet the needs of the crisis, the CARDIAC site joined forces with the THERAPIES site. An article about the operations in the Galway THERAPIES site during the pandemic reports that “CVG [Galway CARDIAC site] builders, engineers, and quality teams have joined the Mervue team [Galway THERAPIES site]. The collaboration . . . has allowed the businesses to learn about one another—and from one another—in new ways.” 54 The same article quotes an employee of the Galway THERAPIES site: “If we widen the product knowledge, there may be times in the future when we need to call on Mervue to support Parkmore [Galway CARDIAC site].”

It is clear that in this time of crisis, Medtronic turned to offshore subsidiary sites to help achieve its commitment to meeting ventilator demands. The corporation called for a collaborative effort between two subsidiary sites; one that had the expertise of manufacturing ventilators (the Galway THERAPIES site) and another at a co-located but distinct site (the Galway CARDIAC site) that over a long period had achieved an upgraded status to the point it had assumed a joint coordinator role in the GVC of a core Medtronic product. This elevated status of the Galway CARDIAC site placed it in a position of trust and reliability for the delivery of high value-added projects from Medtronic’s perspective. In achieving this status, the Galway CARDIAC site was driven by a motivation to improve its stability in terms of long-term survival as a subsidiary. In a time of crisis, this resulted in a win-win situation; Medtronic Corporate could turn to its subsidiary sites for both expertise and reliability to deliver in a period of unprecedented demand. This could be successfully provided by offshore subsidiary sites exactly because Corporate allowed a subsidiary to achieve an upgraded status, which in turn benefits the local site and milieu. Marrying the ventilator production expertise of the Galway THERAPIES site with the advanced leadership and project management competency of the Galway CARDIAC site made for a powerful offshore combination in weathering the pandemic storm.

Discussion: Dynamic Hierarchy Governance in the MNE’s Global Value Chain

GVC theory has made substantive progress in expanding IB theory beyond the boundaries of the internalized MNE. However, reaping the benefits of globalization does not necessarily entail losing control of a global supply chain, nor does it entail the transfer of knowledge, technology, and innovation to third parties located in foreign countries. For instance, internalized GVC organization may be the optimal solution for MNEs dependent on IP protection for competitive advantage. Naturally, the imperatives for efficient production and stable delivery still apply. Whereas IB theory has underplayed the benefits of externalization for efficiencies, GVC theory has neglected the internal dynamics of the hierarchy governance form. Whether hierarchy, market, or middle-ground governance form, GVCs are not static. Yet little attention has been paid to the dynamics of the hierarchy mode involving capabilities’ upgrading by internal subsidiaries and the evolution of intra-organizational trust and power relations.

Consequently, our principal contribution to GVC theory rests in our application of the tenets of externalized suppliers’ upgrading to internalized subsidiary upgrading under the overlooked hierarchy GVC governance mode. We reintroduce MNE internalization theory to the GVC discourse as called for by scholars at the nexus of MNE and GVC theories. 55 Our case study demonstrates how, even under quite stable hierarchical governance, the GVC constantly evolves and transforms whereby internal subsidiaries’ configurations, activities, and responsibilities change. Subsidiaries differentially upgrade their capabilities and variably perform to expectations. Over time, a subsidiary may potentially even wrest some power and control from HQ over GVC activities. This enhances that subsidiary’s prospects within an MNE. It also raises the confidence of senior fiat of an MNE in being able to rely on the subsidiary to deliver on both production efficiency and supply resilience, even in times of extreme disruption. Our case study shows how capabilities, intra-organizational relations, competence and goodwill trust, and power-dependency evolved under hierarchy governance. While the guiding principles of hierarchy governance of the GVC exhibited no substantial change, over time, internal relational dynamics evolved and control over activities shifted somewhat in favor of the subsidiary through some measure of shared governance. In this way, HQ and a lead subsidiary have jointly orchestrated a hierarchical GVC to retain majority control, stabilize the functioning of its global production networks, and preserve its overall resilience.

Before the outbreak of COVID-19, strategy research on GVCs mainly focused on MNEs’ economic practices and outcomes as leading actors in GVCs but disregarded the vulnerability and hazards involved in GVCs and GVC structures. 56 The risks associated with interdependence among external business activities dispersed globally and how firms can respond when this interdependence is severely obstructed came to light during the pandemic crisis and, as a result, calls to reshore activities abounded. Given this context, our case study also contributes to GVC theory by demonstrating that under the pressure wrought by a severe disruptive event, efficiency and resilience can coexist in a hierarchical GVC without deleterious compromise and costly trade-offs. In response to a sudden surge in demand for its vital category of complex medical products, Medtronic HQ strategically resolved to place its trust in the case subsidiary to manage the emergency requirements. Overall, the case MNE weathered the pandemic storm not by reshoring but, on the contrary, through a devolved reliance on its upgraded subsidiary. The internalized MNE has a much greater understanding of, and commitment from, the specific “units” in the GVC that need to “step up” during a disruptive phase or crisis. In the event of a circumstance where the GVC is critically dependent on one unit to organize particular and prompt changes, a common commitment to an entity greater than the GVC as such seems to mitigate different allegiance and dependencies among the parts of a GVC. Future disruptive shocks are inevitable, and shielding domestically is inefficient. Our study demonstrates that in a disruptive crisis, managing GVC activities in-house, but not fully at home, eliminates compromise on efficiency, provides agility, 57 and yet represents no loss of stability. It is a case of not throwing the overseas subsidiary baby out with the reshoring bathwater.

Lessons for Management: An Actionable Guide for MNEs

Our study provides important lessons for MNE management under hierarchy governance. 58 An understanding that this GVC governance form, as with others, is not static summons a requirement for attention to (and ongoing assessment of) evolving and differential capabilities across subsidiaries and to changing intra-organizational dynamics. The following are three actions that MNEs can take:

Assess subsidiaries for current and potential capabilities upgrading in the GVC—Given changing internal dynamics, HQ needs to continuously monitor and assess the current and potential capabilities of its foreign subsidiaries. Subsidiary capability development often takes time, and not all subsidiaries will evolve at the same pace and to the same degree; much will depend on factors external to the MNE, such as those that are location-based (e.g., the availability of high-skilled labor locally) as well as internal MNE factors such as the knowledge and learning they receive from HQ and other sister sites. This means that at any given time, subsidiaries will be at different stages of capability development and with varying potential for capability evolution within their GVC. HQ needs to regularly consider and assess the upgrading of the trajectory of subsidiaries to understand where current and potential capability lies within the GVC hierarchy governance structure.

Support designated subsidiaries in upgrading activities—HQ itself can be a limiting factor in balancing GVC efficiency and resilience by not supporting capable subsidiaries and those showing potential to evolve into higher value-added activities. Supporting capable subsidiaries involves investing in resources locally to develop centers of excellence built around production, innovation, and project leadership. HQ should then strenuously endeavor to cultivate competence trust with upgraded subsidiaries through the provision of supportive measures, resources, investments, improved mandates, internal championing, and, most of all, increased autonomy to engage with external local partners.

Devolve some governance control to subsidiaries with advanced upgraded capabilities—Provide upgraded subsidiaries with increased decision making and control responsibility over elements of the GVC. Co-orchestration on the GVC with HQ and the latitude to direct sister subsidiaries’ activities are examples of some shared governance in the hierarchy. This can allow for higher-order levels of trust to evolve between management at HQ and its subsidiary. It is this trust that becomes an enabling factor for resilience, allowing HQ to rely on a capable international subsidiary to deliver in disruptive times. When faced with an extremely disruptive event, such as a pandemic, an MNE’s GVC does not necessarily have to suffer the loss of efficiency that would occur through reshoring. HQ confidence in capable subsidiaries to perform and deliver in times of disruption pays dividends.

Conclusion

While our findings may not apply to every GVC across all industries, they do provide an alternative narrative to the one dominating the ongoing debate on GVCs optimal configuration. The buyer-supplier relationship can be coordinated through “non-equity” forms of governance that preserve the autonomy of independent global suppliers while providing the buyer with high flexibility. We contend that this model will remain prevalent in the study of GVCs and anticipate that globally dispersed supply lines will hardly be replaced by co-located supply chains via MNEs’ reshoring strategies. Production of consumer electronics, 59 automotive, 60 and clothing 61 will most likely remain anchored to “loosely” governed GVCs, in which leading firms’ search for efficiency will keep dictating the coordination and configuration models of future production networks.

The idea of simultaneously reaching ample efficiency and resilience through a hierarchical governance mode of the GVC (i.e., utilizing a subsidiary) and not having to trade one for the other might also assist in tackling other global enigmas, such as climate and corporate social responsibility issues. In most cases, foreign subsidiaries will adhere more to home-country perspectives on pollution and human/labor rights related to locally grown firms. This might help change things for the better without sacrificing efficiency and opportunities residing in the particular location.

Footnotes

Notes

Author Biographies

Paul Ryan is an Associate Professor at Trinity Business School, Trinity College Dublin, The University of Dublin, Dublin, Ireland (email:

Giulio Buciuni is an Assistant Professor at Trinity Business School, Trinity College Dublin, The University of Dublin, Dublin, Ireland (email:

Majella Giblin is a Senior Lecturer at the J.E. Cairnes School of Business and Economics, National University of Ireland, Galway, Ireland (email:

Ulf Andersson is a Professor at the School of Business, Society and Engineering, Malardalen University, Vasteras, Sweden and Department of Strategy and Entrepreneurship, BI Norwegian Business School, Oslo, Norway (email: