Abstract

This article reports on a case-based, longitudinal study of the micro-foundations of business sustainability development in the Royal Bank of Scotland (RBS) in the turbulent years between 2002 and 2012. The study proposes an emerging 3-i process model, mapping the role of bounded, shared, and embedded intentionality; operational, functional, and strategic integration; and constraining, accelerating, and stabilizing institutionality as they relate to the micro-foundations underpinning the development of corporate sustainability from an operational capability to as a dynamic capability as it evolved across multiple levels of context and over time. The research extends extant literature exploring transformations toward sustainability as part of the strategic change process, the micro-foundations of capabilities as well as discussions on sustainability and temporality.

Interest in sustainability has been growing in studies of management and organization literature (Amui et al., 2017; Bansal, 2005; 2014; Gao & Bansal, 2013). Research studies have been focused on exploring wider conceptualizations of sustainability, taking a closer look at its economic, environmental, and social dimensions (cf. Elkington, 1997; Fergus & Rowney, 2005; Hahn et al., 2014; Hahn & Figge, 2011). Extensively the literature has been focused on debating and defining the sustainability construct as well as on exploring the outcomes of embedding sustainability practices in organizational strategy and performance. Fewer research studies have focused on “how sustainability emerges, not through “stable and stipulative definitions of the concept, but through its translation, use, and daily practice . . . from this perspective, the meaning of sustainability emerges across time” (Hallin et al., 2021, p. 1950). Researchers have argued that taking a more performative approach, for example, taking an organizational capability perspective, could unveil how sustainability acquires meaning across time and how it emerges as people perceive and interpret it when performing practices (Hallin et al., 2021).

Although sustainable practices help firms to create long-term value by managing economic, social, and environmental risks, essential prerequisites are organizational practices that reflect sustainability in managerial attitudes as well as in actions (Chakrabarty & Wang, 2012). Recent systematic reviews on sustainability indicate only a few articles exploring how sustainability can become a capability, enabling an organization to adapt and change, toward more sustainable paradigms (Amui et al., 2017; Bari et al., 2022). Although there are some studies applying the resource-based view and competency view to examine corporate environmental performance, there is less research examining a company’s capability to make sustainability more strategic and dynamic, transforming the company’s strategy (Amui et al., 2017; Dangelico et al., 2017; Russo, 2003). The limited number of articles (Aragón-Correa & Sharma, 2003; Hart & Dowell, 2011) adopting the capability perspective examines mainly the organizations’ strategic approach to the environmental objectives and less so the balancing and alignment of social and business objectives. In fact, recent studies have called for more empirical research to advance knowledge on capability development during a sustainability-related organizational change (Dangelico et al., 2017; Strauss et al., 2017). To understand the challenges and the changes related to integrating sustainable practices across the organization, scholars have highlighted the appropriateness of strategic management theories such as the dynamic capability perspective in providing insight into how these dynamic processes unveil (Amui et al., 2017; Cooper et al., 2016). Besides the calls for further empirical research in this domain through a more integrative approach, research remains limited. Undoubtedly, the ambiguity surrounding the sustainability construct makes it challenging for conducting empirical research. As a factor for this challenge, Hallin et al. (2021) point out the potential temporal character of the sustainability construct. This study agrees with the temporal view of the construct and adopts a processual analysis to shed light on the “how,” the decision-making, and the doing of sustainability especially when organizations have to deal with unstable environments and unpredictable changes. As Amui and colleagues (2017, p. 309) notice, to respond to institutional complexities, “organisations have been looking for ways to make sustainability a dynamic capability, integrated with strategies and business models.” However, there is limited research work examining this development process.

In this phenomenon-driven research study, we explore processualy how a leading banking organization, the Royal Bank of Scotland (RBS), engages in a sustainability-oriented change as a result of an exogenous shock—the Global Financial Crisis of 2008. We seek to examine sustainability as a multilevel phenomenon, which can be understood through the alignment between micro-foundations at different levels of context through time. Thus, our research explores

In this study, we look at sustainability dynamic capability as a high-order organizational capability that enables the organization to change its social, economic, and environmental practices as a result of the changing institutional context (Strauss et al., 2017). Although we shed some light on organizational practices oriented toward the environment, our study speaks more about the organizational dynamics related to social and business competences and processes as these were more affected as a result of the global financial crisis.

The literature exploring how to maintain sustainability practices within organizations and turn them into important dynamic capabilities is yet to be developed, although there are few conceptual attempts in this area (Amui et al., 2017). In a recent conceptual study, Strauss et al. (2017) propose sustainability dynamic capabilities to be those capabilities that enable an organization to reconfigure its resource base in response to the changing institutional environment to develop more proactive environmental strategies. The authors argue that depending on the level of uncertainty and dynamism in the institutional context, different micro-foundations underlie sustainability dynamic capabilities. Similarly, a systematic literature review by Amui and colleagues (2017) reminds us that few studies (Leonidou et al., 2015; Schrettle et al., 2014) define sustainability-oriented dynamic capabilities as capabilities enabling an organization to adapt, change and innovate toward new, sustainable paradigms. Other studies highlight the importance of sustainability-oriented dynamic capabilities for renewing/changing companies’ sustainability-oriented ordinary capabilities. Today, most of the research work focuses on environmental sustainability and less so on economic and social sustainability. Furthermore, with few exceptions, most research remains conceptual.

We contribute to the literature in the following ways: First, this study offers a rich empirical account of the process of developing sustainability from being an operational/ordinary capability to a more strategic or dynamic capability for an organization in the changing institutional context. To do so, we follow a micro-foundational approach as it offers a promising line of inquiry for a fine-grained analysis of how sustainability organizational capability is developed through time (Eisenhardt et al., 2010; Felin et al., 2012; Gavetti, 2005; Van de Ven & Lifschitz, 2013). This perspective directs attention toward the individual behaviors and interactions as well as the emergent processes and outcomes underpinning such aggregate concepts (Felin et al., 2012; Hodgson, 2012). A micro-analysis of the mechanisms that drive sustainability has been treated largely as a secondary consideration to more macro-analysis of the companies, institutions, and organizations that grapple with it (Cooper et al., 2016). This has led to calls for multi-level perspectives on business sustainability (Sharma et al., 2007; Starik & Rands, 1995; Strauss et al., 2017). This study responds to calls for bridging micro-macro level approaches to sustainability as there is limited research showing how individual-level factors aggregate to the collective level (Barney & Felin, 2013; Strauss et al., 2017).

Second, in this study, we build an empirically grounded synthesis of the micro-foundations by focusing explicitly on the interaction between the composing of different sets of micro-foundations on the individual, organizational, and structure levels involved in the development of sustainability dynamic capability, which advances theoretical research agenda initiated by Teece (2007) and Felin and colleagues (2012). We track the capability development process at the firm level, trying to build a picture of the internal and external dynamics influencing the process. This led to the construction of a process model, mapping the occurring transformations in the micro-foundations of capabilities before, during, and after an exogenous shock. Drawing on an emerging 3-i process model, the case study contributes to understanding the role of bounded, shared, and embedded intentionality; operational, functional, and strategic integration; and constraining, accelerating, and stabilizing the influence of institutionality as they relate to the micro-foundations underpinning the development of a dynamic sustainability capability from an ordinary capability. Thus, this research study provides empirical evidence in practice of how one type of capability can evolve due to changes in the interaction between different micro-foundations as a result of the changing institutional dynamics.

We observe that variability in the alignment of capability micro-foundational constructs tends to impact the form, as well as the function, of sustainability as an organizational capability for the bank when explored over time and across levels of analysis. We note that the development of a strategic/dynamic capability may occur only when there is a triadic alignment between individual behavior, organizational processes, and structure, empirically illustrated through synchronization between senior management objectives, organizational processes, and structure supporting sustainability across the organization. In the case where there is a lack of micro-foundational alignment, for example, when sustainability decisions are only limited to a particular function of the organization and group of managers, and detached from the rest of the organizational processes and structure, sustainability capability resembles what the literature defines as ordinary or operational capability (Cepeda & Vera, 2007). Moreover, our findings echo Helfat and Winter’s (2011) suggestion of a possible blurry line between operational and dynamic capability in the case of a sustainability-oriented organizational change. We observe a dyadic alignment between some of the micro-foundational constructs (individual-based and structure-based micro-foundations), which led to what we entitled a transitional capability. In the case of RBS, the exogenous shock in the face of the global financial crisis led to a shared intention to transform the bank into a sustainable organization and changes in the structure-based micro-foundations (e.g., a complete restructuring of governance, the introduction of new sustainability practices of the organization) but less so in the process-based micro-foundations. The organizational inertia and to a large extent the organizational fear across the bank, due to the high level of external institutional pressures, obstructed the process of initiating and legitimizing the sustainability agenda equally across the various management teams.

Furthermore, most research on dynamic capabilities provides a singular focus on strategic change (e.g., a specific function of the organization such as R&D), rather than organizational change more broadly (Helfat and Martin, 2015). This study contributes to the latter as the explored empirical case of the RBS is a story of sustainability-related organizational change and sustainability capability development as a result of an exogenous shock.

Conceptual Background

Our aim in this section is to set the conceptual context of the study by, first, presenting the multiple interpretations of the business sustainability construct. We then outline some recent thinking on sustainability as it relates to the macro, meso and micro levels, and highlight the scarcity of multilevel studies. Finally, we draw the link between micro-foundations approaches to understand business sustainability and how it emerges from being an operational capability—for an organization to become more strategic, to be a dynamic capability—shaping the rest of the organization’s resources and capabilities. We argue that an empirical research gap exists in exploring business sustainability from a more performative approach, understanding the role that individuals and their interactions as well as organizational processes (e.g., inter and intra-organizational communication) and governance structures play in an organization’s sustainable development over time.

Business Sustainability and its Multiple Interpretations

Interest in business sustainability continues to grow in strategic management and organization studies literature (Andersson et al., 2013; Aragon-Correa, 2013; Starik & Kanashiro, 2013; Starik & Rands, 1995). The bourgeoning interest in the area has resulted in a number of conceptual ambiguities (Bansal & Song, 2017). In fact, there is no single definition but a range of explanations of the concept (e.g., corporate social responsibility, corporate citizenship, triple bottom line). Exploring the literature, the plethora of semantic explanations of what constitutes business sustainability can be divided into three main typologies—being synonymous with the notion of corporate social responsibility and its variants (Van Marrewijk & Werre, 2003), being a higher-order construct incorporating corporate social responsibility (Van Marrewijk, 2003), as well as being significantly different from CSR. Fergus and Rowney (2005, p. 19) argue that “to some extent the term has become a cliché . . . applied to almost anything remotely related to the business processes, the society in which those processes operate, and the environment in which both processes and society are embedded.” The interpretations of CSR and sustainability by companies and authors which examine different organizational settings vary as a result of trade-offs between various forms of value (sustainable and economic), institutional logics, different organizational identity as well as company size, embedded in the business models of organizations (Hallin et al., 2021, p. 1948). Dahlsrud (2008), for example, counted 37 definitions of CSR, adding to the confusion. However, the bottom of almost every view on business sustainability and CSR is that it considers simultaneously economic prosperity, environmental integrity, and social equity.

Previous research studies point out that most of the current interpretations of business sustainability tend to be more ostensive in nature, meaning that they explain things in principle by borrowing from other theoretical constructs. Hallin et al (2021, p. 1950) argue that the problem with ostensive definitions is that they tend to integrate different existing concepts and may “be variously interpreted in every case.” Thus, they call for adapting a more performative approach which allows exploring “how sustainability emerges, not through stable and stipulative definitions of the concept, but through its translation, use, and daily practice.” The performative approach allows exploring how a concept acquires meaning across time and how it emerges as people perceive it and interpret it when performing organizational practices (Hallin et al., 2021).

The complexity of the field, then, calls “for a fresh consideration and reconceptualization of theory for practice in the sustainability field” (Cooper et al., 2016; also see Aragon-Correa, 2013) are timely. Moreover, researchers have called for a more performative approach when defining the concept, exploring the transition to sustainability in organizations as well as the underlying drivers which facilitate or inhibit the development process. To deal with economic, environmental as well as social risks, researchers have highlighted the fact that sustainability should be part of the organizational strategy. Thus, they have called for more studies exploring how sustainability can become a more strategic or dynamic capability, which drives the company’s transition and change toward a more sustainable future (Amui et al., 2017). However, recent systematic reviews of the literature show that besides such calls, few research studies are using the capability view to study business sustainability (Amui et al., 2017; Russo, 2003).

In this article, we adopt a temporal view of the business sustainability construct (Hallin et al., 2021; see also Pettigrew, 1997; Winter, 2012), which suggests that the issues, drivers, and trajectories of the micro-foundations of organizational behavior and sustainability are best understood as a process rather than a state (MacKay & Chia, 2013). In this study, we looked at sustainability dynamic capability as a high-order organizational capability that enables the organization to change its social, economic, and environmental practices as a result of the changing institutional context (Marcus & Anderson, 2006; Strauss et al., 2017). Our interest in this article is to investigate through a multi-level perspective, the micro-foundations of the sustainability capability development process.

Business Sustainability at Macro-, Meso-, and Micro Levels

Empirically grounded studies of organizations and business sustainability in the extant literature can be divided broadly into three levels. They include research that focuses on the macro level of the environment, the meso level of the organization, and the least developed of the three areas—the micro level of the individual. A hallmark of sustainability studies is that they have often taken place within a single level of analysis, and predominantly at the macro and meso levels, which at times implies, and at other times obscures the multilevel contexts that sustainability is embedded in (Aguinis & Glavas, 2012; Bansal & Song, 2017; Morgeson et al., 2013; Starik & Rands, 1995). Research into business sustainability at the macro level of the environment has shed light on the institutional conditions for sustainability (Bansal, 2005; Hoffman, 1999; Hoffman & Ventresca, 2002, 1999; Husted et al., 2016; Jennings & Zandbergen, 1995; Ortiz-de-Mandojana & Bansal, 2015; Russo, 2003), industry self-regulation (Bansal & Hunter, 2003; King & Lenox, 2000), media influence (Bansal, 2005), environmental deregulation and regulation (Delmas et al., 2007; Delmas & Tokat, 2005), the strategic management of stakeholder groups (Buysse & Verbeke, 2003; Delmas & Toffel, 2008; Sharma & Henriques, 2005), institutional change (Hoffman, 1999), and social movements (Lounsbury et al., 2003; MacKay & Munro, 2012). For instance, Bansal (2005) finds that, in the Canadian oil and gas sector, institutional pressures emanating from the media in the wider macro-context were important for catalyzing sustainability innovation early in the adoption cycle but then began to decline in importance over time. Factors residing at the macro-level context, be they from the media, stakeholders, or regulations, clearly influence lower levels of context, even if the precise nature of that influence is not well understood (cf. Morgeson et al., 2010; O’Leary & Almond, 2009; Rousseau & Fried, 2001).

At the meso or organizational level, studies range from stakeholder integration (Sharma & Vredenburg, 1998) and responses to shareholder activism (Reid & Toffel, 2009), to the role of boards and senior leadership teams in the diffusion of base-line environmental practices in organizations (Walls & Hoffman, 2013), ecological commitment, embeddedness and sensemaking (Valente, 2012; Whiteman & Cooper, 2011), innovation (Nidumolu et al., 2009; Sharma & Vredenburg, 1998), R&D expenditure and intensity (Arora & Cason, 1996; Khanna & Anton, 2002), and board composition and experience (De Villiers et al., 2011; Walls & Hoffman, 2013). Bansal (2003), for instance, tracked the development of environmental issues in two organizations over the course of a year. Of the factors influencing the scale, scope, and speed of organizational responses to environmental issues, they found that two factors, in particular, organizational values and individual concerns, were necessary conditions for addressing the issues.

Finally, at the micro, or individual level, studies have directed attention toward managerial perceptions of corporate environmentalism and stakeholder pressure (Banerjee, 2001; Sharma & Henriques, 2005), CEO cognition, interpretation and passion (Branzei et al., 2004; Robertson & Barling, 2013), compensation (Russo & Harrison, 2005), and employee interventions (Unsworth et al., 2013). For instance, pro-sustainability behaviors have been shown to stem from pro-sustainability attitudes (Bissing-Olson, 2013). Closely related studies have shown that pro-sustainability attitudes, behaviors, and passion are influenced by the pro-sustainability attitudes, behaviors, and passion of leaders (Robertson & Barling, 2013).

Despite the increasing attention to sustainability-related issues in the study of business ethics and business and society, there is still a relative paucity of work that focuses on micro-level factors contributing to sustainability, such as individual behaviors and ethics, their drivers, and the contexts in which intra-organizational processes unfold (Cooper et al., 2016). An explicitly micro-foundations approach to analyzing organizational behavior and, particularly, the development of sustainability capability within organizations offers an opportunity to address this gap while raising a number of issues about how micro-foundations relate to different levels of organizational context.

To date, with few exceptions, there are limited research studies which adopt a multilevel micro-foundational perspective. For example, an inductive study by Del Giudice et al. (2017) discusses the owner-managers’ crucial role when engaging in sustainability activities jointly with employees and other stakeholders, through which individual-level actions enhance collective organizational-level sustainability practices. Nevertheless, research in this area is still at a nascent stage (Buzzao and Rizzi, 2021). For this reason, scholars call for sustainability to be studied as a multilevel phenomenon that both incorporates the relatively under-researched micro-foundations of organizational behavior and sustainability, and the wider meso and macro contexts that shape and are shaped by them (Alcaraz & Thiruvattal, 2010; Cooper et al., 2016; Porritt, 2007; Sharma et al., 2007; Starik & Rands, 1995).

Business Sustainability, Organizational Capabilities, and Micro-foundations

Recent reviews of the sustainability literature indicate that most research on sustainability is “underlined by a static view, focusing on the initial development of social and environmental practices”, calling for studies adapting a more dynamic view on how sustainability practices can become strategic capabilities over time (Amui et al., 2017, p. 311). However, few studies have applied the organizational capability and more specifically the dynamic capability view to the concept of business sustainability (Buzzao and Rizzi, 2021). The majority of studies applying the dynamic capability view to examine organizations’ approach to developing proactive environmental strategies and whether a company’s proactive environmental behavior leads to a competitive advantage (Aragón-Correa & Sharma, 2003; Dangelico et al., 2017; del Rosario Reyes-Santiago et al., 2019). Hart (1995) argued that a company’s capacity to develop an organizational capability will be determined by the relationship the company has with the nature environment. Hofmann and colleagues (2012), on the contrary, tried to identify firm capabilities as drivers of environmental management and sustainability practices in the context of small- and medium-sized manufacturers. Dangelico et al. (2017) explore the relationship between sustainability dynamic capabilities and green innovation and eco-design capabilities and the impact on the market performance of green products.

Besides little research on how sustainability can become a capability, there is less research examining the micro-foundational factors that drive sustainability as a dynamic capability, as the literature in this direction has yet to be constructed (Amui et al., 2017).

The recent “turn” toward micro-foundations research in studies of organizations seeks to re-direct attention toward the role of individual attitudes, behaviors, choices, expectations, motivations, propensities, and purposes (Felin & Foss, 2005). It rests on the assumption that collective phenomena, be they organizations or sustainability, are aggregations of lower-level phenomena (Abell et al., 2008; Felin et al., 2012). A micro-foundations approach suggests how individual behaviors play out or become translated through organizational hierarchies (Bapuji et al., 2012; Gavetti, 2005). Organizational capability, which is a key construct in the organization, management, and strategy literature, is a useful lens for exploring the micro-foundations of organizational behavior and sustainability (cf. Barney & Felin, 2013; Felin et al., 2012; Foss, 2011). Organizational capabilities can be divided into two categories. The first pertains to operational or static ordinary capabilities. These involve mostly the administrative, operational, or governance-related functions of an organization; and dynamic capabilities govern these organizational functions and define their strategic intent (Teece, 2014). A review of the organizational capability literature indicates a wide range of conceptualizations when it comes to defining and examining the relationship between ordinary and dynamic capabilities (Cepeda and Vera, 2007; Schriber & Löwstedt, 2020; Teece, 2014; Winter, 2003; Zahra et al., 2006). According to Collis (1994), an ordinary capability refer to the ability of an organization to perform basic functional activities. On the contrary, Winter (2003, p. 991) defines them as “a high-level routine (or collection of routines) that, together with its implementing input flows, confers upon an organization’s management a set of decision options for producing significant outputs of a particular type..” In their empirical study on information technology and communication sector in Spain, Cepeda and Vera (2007, p. 426) relate them to the operational functioning of the firm. According to the authors, these are “how we earn a living now” capabilities. In this study, we adopt the definition of Helfat and colleagues (2007) which is also in line with the conceptualization proposed by Collis (1994). The authors define operational/ordinary capabilities as the ability of a firm to perform a particular practice. CSR activities, for example, often take the form of lower-order, or operational capabilities when used for marketing, public relations, and reputational enhancement (Lo & Sheu, 2007).

Dynamic capabilities, by contrast, are higher-order capabilities and imply change (Helfat et al., 2007; Teece, 2007; Teece et al., 1997). Teece and colleagues (1997, p. 516) suggest that the term “dynamic” “refers to the capacity to renew resources so as to achieve congruence with the changing business environment [. . .].” Winter (2003, 2012) argues that change is often the result of a force majeure from the wider environment, and incorporates the manifold influences of the element of time. It can also originate in anticipation of shifts in the environment through (a) sensing and shaping opportunities and threats, (b) seizing opportunities, and (c) transforming the enterprise (Teece, 2007). Whatever the catalyst for the change, it suggests an organization-wide, or strategic direction of travel. According to Barreto (2010), a capability is considered dynamic when it enhances the firm’s ability to make decisions, solve problems, and identify opportunities and threats in more complex environments. Furthermore, company’s dynamic capabilities are developed through a set of behavioral activities and cognitive processes (micro level) which shape the organizational behavior and routines (Zollo & Winter, 2002) but also impact the overall strategy of an organization (meso level; Fallon-Byrne & Harney, 2017) which assist organizations to adapt to the changing business environment (macro level). Barney and Felin (2013, p. 138) have called for more research studies exploring the dynamics on the micro-meso-macro levels—“an issue that [should be] at the very core of any microfoundations discussion.”

While extensive literature exists on both operational and higher-order dynamic capabilities (see Peteraf et al., 2013), work on their micro-foundations is still nascent (Felin et al., 2012; Teece, 2007; 2012; Winter, 2012). Empirical studies that explore the role that individuals, processes and interactions, and structures play in capability development (cf. Felin et al., 2012), and their development over time are even more limited (cf. Winter, 2012). Questions remain, for example, about individual intentionality, and how they purposefully scale and integrate sustainability behaviors as well as the conditions and contexts that it takes place (cf. Felin et al., 2012; Gavetti & Levinthal, 2000). Yet there is obvious relevance for the issues, drivers, and trajectories underpinning the micro-foundations of organizational behavior toward sustainability. In particular, it remains important to understand how individual orientation and behaviors, as well as organizational processes and structures within sustainability operational capabilities, develop into wider sustainability dynamic capabilities at a strategic level for the organization (Cooper et al., 2016, p. 2).

The micro-foundations approach to studying sustainability has the potential to contribute to a more fine-grained understanding of how sustainability behaviors become aggregated, both within organizations and society at large (Barney & Felin, 2013). This research seeks to address this aim through a longitudinal study of a U.K. financial enterprise, the RBS, as it sought to develop a sustainability dynamic capability from a sustainability operational capability. We have also sought to understand how such micro-foundations (individual behaviors, and organizational processes and structures) evolve across levels of micro, meso, and macro contexts, which lies at the core of the micro-foundations discussion (cf. Barney & Felin, 2013; Johns, 2001; Winter, 2012). Based on these curiosities, we seek to examine sustainability as a multilevel phenomenon that can be understood through the alignment between micro-foundations at different levels of context through time. Thus, our research explores:

Method

To address this study’s research questions, we base our work on a qualitative, inductive, longitudinal research methodology (Denzin & Lincoln, 2011). This research approach and the adopted case-based method enable a fine-grained investigation of the behaviors and individuals, processes and structures, and the institutional influences and emergent outcomes relating to the development of a dynamic sustainability capability from an operational capability. The research setting for this study is the RBS. Given that we were studying an emergent phenomenon (Pettigrew, 1997; Siggelkow, 2007), we selected our case based on the novelty of circumstances that RBS found itself in as it sought to retrench itself after being partly nationalized amid the 2008/2009 financial crises. RBS had become, briefly, the largest bank in the world by assets (circa $2.4 trillion) in 2008 (The Economist, 2008), which contributed to our interest in the organization (Siggelkow, 2007). RBS is a particularly interesting case of an organization that has survived a near-death experience during times of immense institutional turbulence. The case is special for the richness of organizational and behavioral sustainability-related changes that assisted in tracing the main events and processes related to sustainability. We focused specifically on the dynamic sustainability capability micro-foundations, and following widespread advice on embedded, longitudinal, interpretive case-based research designs (Dawson, 1997; Eisenhardt, 1989; Pettigrew, 1997; Siggelkow, 2007; Yin, 1994), their multi-level contextual interactions over time (see also Alcaraz & Thiruvattal, 2010; Porritt, 2007; Sharma et al., 2007; Spector & Meier, 2014; Starik & Rands, 1995). The selection of RBS as our critical case is based on the extraordinary transformation that the bank has been undergoing before, during, and after the 2008 financial crisis (Siggelkow, 2002, 2007; Yin, 1994). The organization’s journey through the experienced exogenous shock empowered us to understand the relationship between micro phenomena as expressed through a micro-foundations approach of sustainability as an organizational capability.

In this section, we give an overview of our research setting, research design, data collection, and analytical approach.

Research Setting and Historical Overview of RBS

The RBS was founded in Edinburgh, the United Kingdom in 1727. The post-First World War era was a steady period of expansion and growth for the bank, mainly through a mergers and acquisitions strategy. In 1985, RBS merged with Williams & Glyn’s Bank in response to takeover threats by HSBC (Hong Kong and Shanghai Banking Corporation) and Standard Chartered Bank. It was at this time that RBS developed from a small, well-respected Scottish bank into a nationwide high-street bank, which began expanding internationally with the acquisition of the American-based Citizen Financial Group in 1988 (RBS Heritage Archives, internal documents). Through the 1990s, RBS, led by CEO George Mathewson, continued to expand and innovate, which culminated in the £21 billion hostile takeover of the much larger London-based bank NatWest in 2000, making RBS the seventh-biggest banking group in Europe. Following the takeover of NatWest, Sir George Mathewson stepped down as CEO, assuming the role of Deputy Executive Chairman, and then in May 2001 Chairman of the RBS Group. Fred Goodwin, then Deputy CEO, became CEO in January 2001.

With the promotion of Goodwin to CEO, the Bank’s goals changed from the ambition of becoming a serious U.K. player to that of becoming one of the largest banks in the world (Fraser, 2015). It was also at this time that RBS established its Corporate Responsibility department. Between 2001 and 2008, the global aspirations of RBS executives resulted in a number of international acquisitions (e.g., Charter One; 10% stake in Bank of China in 2005 making RBS the largest company in market capitalization in the United Kingdom and number five in the world; Kennedy et al., 2006, p. 368). Business sustainability at this time was understood only in financial terms. However, the intense rivalry across the banking industry increased the appetite of both RBS executives and the corporate culture to take riskier management decisions and activities.

As a result of its ambitious global strategy, RBS entered the global financial crisis with an inadequate capital base, resulting in higher dependency on its wholesale capital market and difficulty financing its balance sheet. Consequently, RBS suffered the biggest crisis in its history, culminating in 80% of the bank being nationalized in October 2008 with a £45 billion bailout by the U.K. government (Martin & Gollan, 2012). Goodwin resigned as CEO, and Stephen Hester took over the same month. Hester quickly turned his attention toward saving the bank through a large-scale internal restructuring, including changing organizational behaviors, processes, structures, and the strategic direction of RBS by focusing on developing a sustainability capability. With the resignation of Sir Tom McKillop as Chairman, the new Chairman, Philip Hampton who took over in 2009, reduced the size of the RBS Board to improve governance and increased the proportion of non-executive directors to executive directors.

Research Design

This research study adopts a single case-based research design (Siggelkow, 2007; Yin, 1994). Case-based research designs allow for a contextual and holistic exploration of the researched phenomenon (Dubois & Gadde, 2002; Gomm et al., 2000). The single case-based research design fit with our aim of studying the micro-foundations of organizational behavior and sustainability as they relate across levels of context and as they unfold temporally through time (Eisenhardt, 1989; Ghauri, 2004; Siggelkow, 2007). As Felin and colleagues (2012) state: “The micro-foundations approach focuses on collective phenomena that need explanation, specifically [their] creation and development . . . an analysis of micro-foundations considers both initial conditions and evolutionary processes” (pp. 1352–1353). Our selection of RBS for the case study was made based on critical case sampling based on the extraordinary transformation that RBS has been undergoing, both before and after the 2008 financial crisis (Siggelkow, 2002, 2007; Yin, 1994).

Data Sources

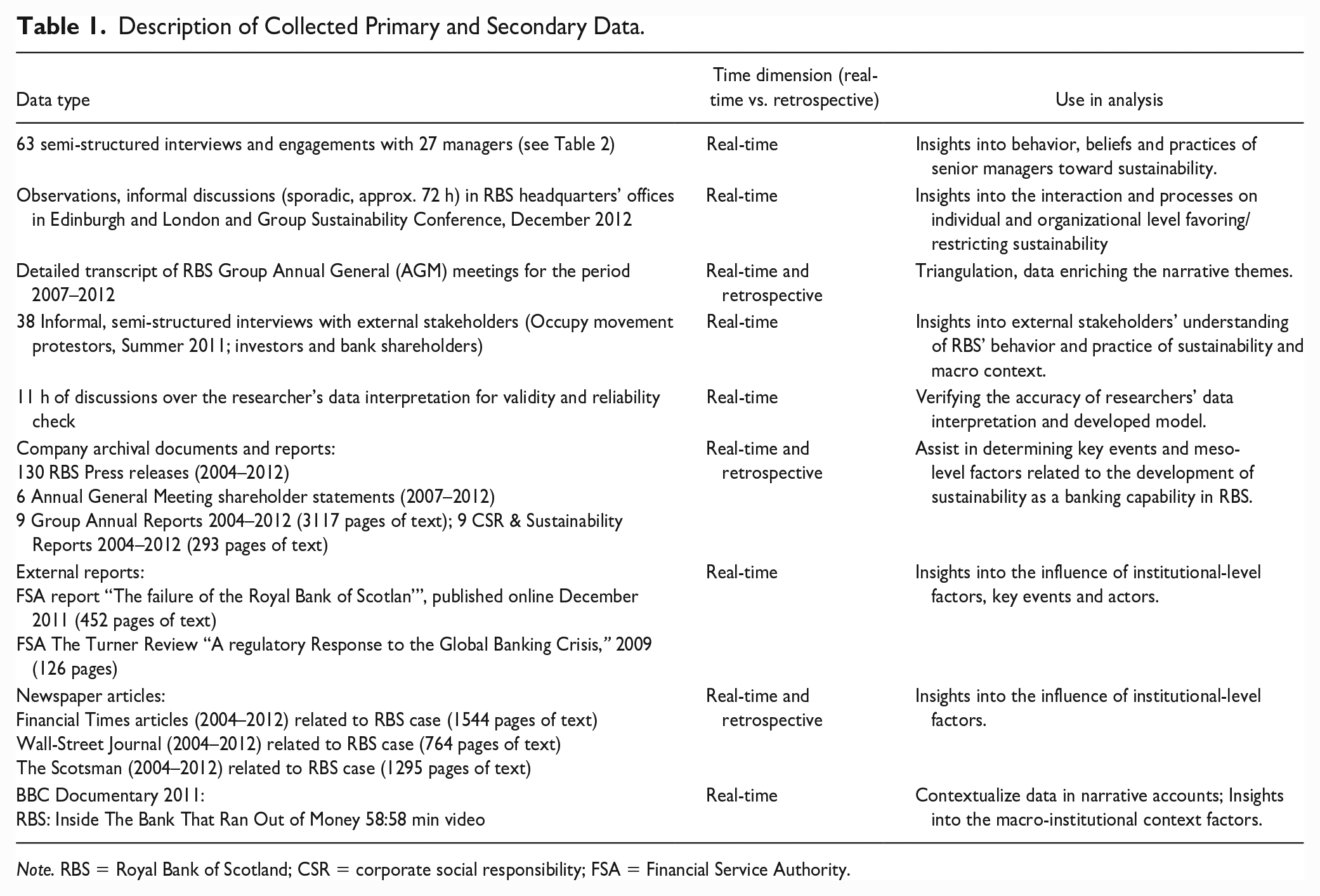

To develop a rich case study, a variety of real-time and retrospective primary and secondary data was collected (Pettigrew, 2012). Table 1 summarizes the collected data between 2009 and 2012 and its use in the data analysis. The combination of primary and secondary data assisted in triangulating the data, and minimizing doubt about the accuracy of process data representation (Soulsby & Clark, 2011). The primary data included interviews with senior managers across the different functions of the bank and stakeholders of the organization as well as observations in the Bank’s headquarters in Edinburgh and offices in the city of London. Primary access was gained and informants were recruited through a snowballing within-case sampling approach (Patton, 2002). An initial informal conversation with the company’s head of group sustainability during a social event in Gogaburn, RBS headquarters in Edinburgh planted the initial seeds of the recruitment process of other informants. The head of sustainability of the bank was a key figure who introduced the researchers of the study to other informants, allowing a trustworthy relationship with the managers to be established. This on the contrary allowed for further snowballing and internal data access in other parts of the organization. Initially, nine familiarization interviews with senior managers from the CSR, finance and investment, human resource, group charitable programs, and group communications and marketing among others were conducted. During these interviews, every time an interviewee would refer to a colleague of his who had a key role in an activity or event related to organizational changes or/and challenges when it comes to sustainability, the researchers of the study would ask to be put in contact with this manager. Although two out of five managers would agree to refer us to other senior managers, gaining access to senior-level management in turbulent times was a recognized challenge.

Description of Collected Primary and Secondary Data.

Note. RBS = Royal Bank of Scotland; CSR = corporate social responsibility; FSA = Financial Service Authority.

Another highlight event for the data collection process was RBS Group Sustainability Conference, an internal and private but very strategic event for the bank, to which we were invited. It took place at the beginning of December 2012 in London. During the conference key sustainability priorities were debated among the group’s executives, senior managers as well as representatives of external stakeholder groups (nongovernmental organizations [NGOs] and investors) as well as internal stakeholder groups (managers from different parts of the business). The head of sustainability of the banking group introduced the first author of the article as an independent researcher interested in the organization’s journey to sustainability and encouraged the audience to establish contact during lunch and coffee breaks. Further interviews were scheduled later that month with managers interested in the research. The secondary data sources comprised multiple sources of written internal, archival documentation, external reports, and articles.

Interviews

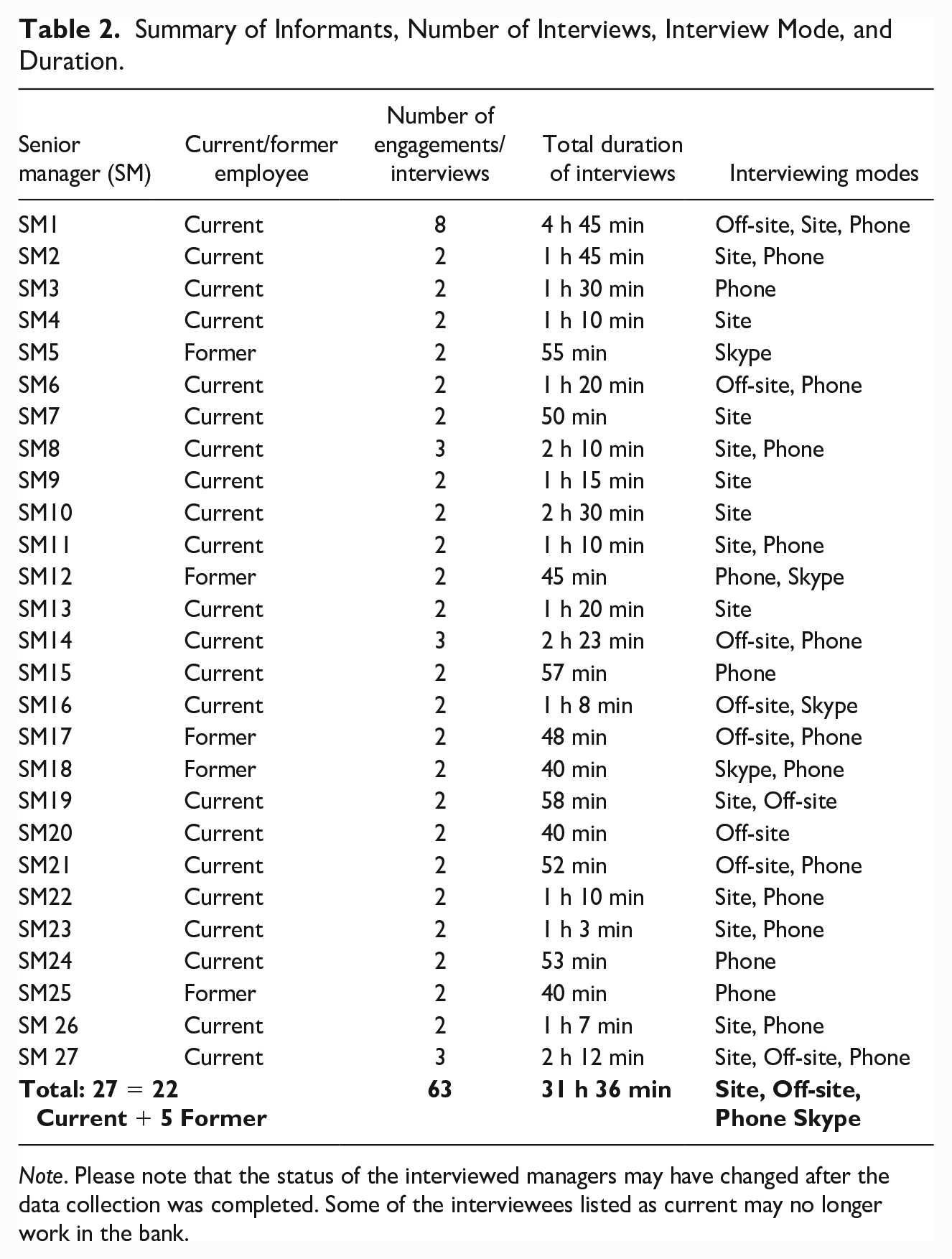

The primary data sources were 63 in-depth interviews and engagements with 27 managers and senior managers (some of whom became board members after the restructuring of the bank after the financial crisis) involved in the decision-making of the organization and representing different departments of the organization. On average, all of the senior managers were interviewed at least twice during the data collection between 2009 and 2012. This allowed the researchers to observe changes in the managerial intentionality toward sustainability as well as its integration into organizational practice. Interviews were semi-structured in nature and lasted between 30 min and 2 hr on average and followed a story-telling approach (Czarniawska, 2004). Participants who represented various departments were asked to talk about their beliefs, experiences, and understanding of sustainability at RBS and what it meant for their specific function in the organization. Interviews were recorded and transcribed verbatim. Nine participants declined to have the interviews recorded. These interviews were transcribed based on detailed notes, by following a “24-hour” rule (cf. Eisenhardt, 1989; Yin, 1994). This helped the researchers to limit any bias in the interpretation of the data due to incorrect transcription. Table 2 provides a summary of the interview data.

Summary of Informants, Number of Interviews, Interview Mode, and Duration.

Note. Please note that the status of the interviewed managers may have changed after the data collection was completed. Some of the interviewees listed as current may no longer work in the bank.

Moreover, to avoid the retrospective bias associated with the collection of secondary data and primary interview data based on past experiences and managerial practices, the collected data were triangulated by interviewing senior managers, representing the company’s key departments on their experiences of the changes and dynamics within the development of the sustainability-banking capability process. Each of the informants was interviewed at least twice. The first interview with a respondent usually tended to have a familiarization character during which key events, practices, and perceptions were identified. The data were then further verified through available secondary data mainly archival sources and reports as well as through further interviews with members of the senior management community in the bank. After approximately 4 to 6 months, a second and in some cases third interview was conducted with the same interviewee. These follow-up interviews allowed verification of the logical connections between emerging events and practices constituting a chain of evidence. Furthermore, some of the follow-up interviews further enriched the research data. Several interviewees happened to recall and share further insightful stories that contributed to the construction of the case study.

Archival and Secondary Sources

Archival data and secondary sources were collected on-site at RBS headquarters between March and December 2012. RBS gave access to their corporate archives, which were systematically searched for material relating to corporate responsibility and sustainability, and recorded. In addition, the Sustainability Department also opened its records to the researchers during site visits. These included internal secondary data, such as press releases, annual and sustainability reports, and annual protocols from shareholder meetings (2007–2012). External secondary data included two Financial Service Authority (FSA) reports, journal articles from international newspapers such as Financial Times, Wall Street Journal, and local newspapers such as the Scotsman, collected using Factiva, a full-text media database. The collected secondary data facilitated the researchers to validate the majority of retrospective accounts that the interviewees provided as well as to build a rich case study.

Data Analysis

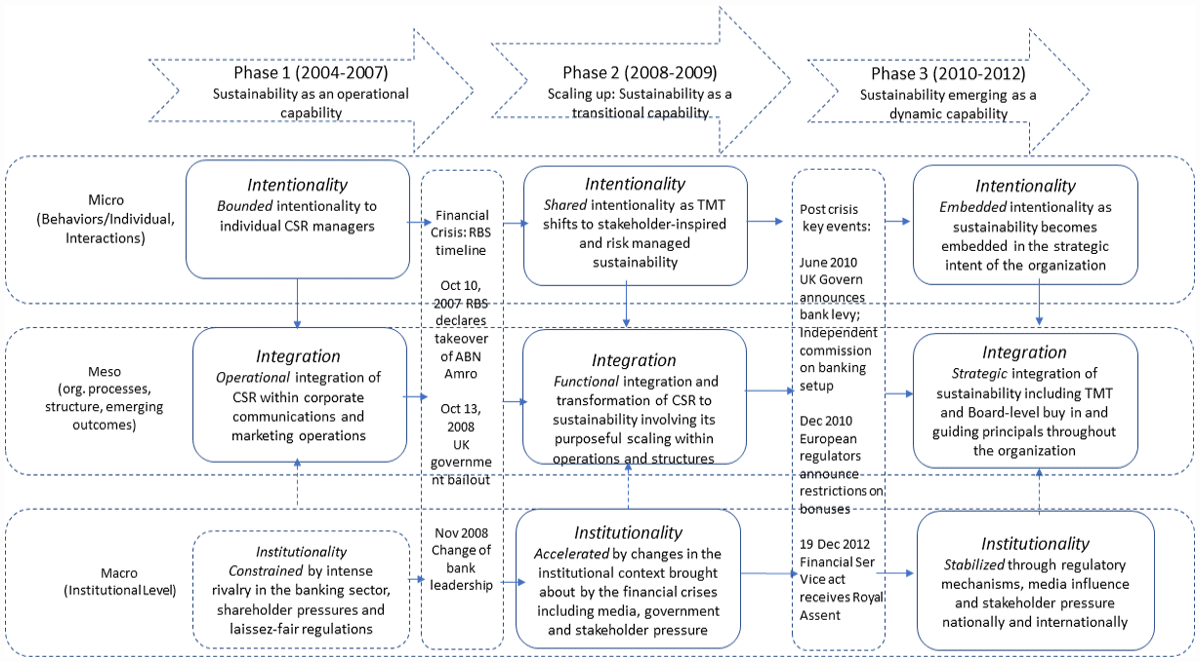

Our data analysis approach consisted of two stages. In the first stage, drawing on the archival, interview, and secondary data, we constructed a descriptive, detailed narrative story and timeline focusing on the evolution of sustainability at RBS (2002–2012; Burgelman, 2011; Langley, 1999; Mills & Mills, 2011). Reflecting on our questions around the micro-foundations of sustainability, and how they relate across levels of context and time, we developed a detailed account of the behaviors and individuals, processes and structures, and emergent accounts and events underpinning the transformation of an operational sustainability capability into a dynamic sustainability capability (Balogun & Johnson, 2004; Pettigrew, 1992). In the second stage, when developing our chronological account, we identified three specific phases of critical importance. The labeling of the observed three phases (operational, transitional, and strategic) occurred after the coding of both secondary and primary data was completed. As part of the coding process, data and the assigned codes were continuously revisited throughout the analysis process. The first phase, which we identified, was between 2002 and 2007 and involved sustainability being an operational capability in RBS. This phase marked the starting point of the investigation, namely, the period from the development of the first CSR team in RBS, which was also consecutively the period before the global financial crisis and lasted until the end of 2007. The second phase we identified was between 2008 and 2009 and involved the transition of sustainability from an operational capability to a more strategic capability for RBS. This phase was a turning point in the history of RBS and marked a period of a major shift favoring the integration of sustainability in the bank during the financial crisis. The third phase unfolded between 2010 and 2012 and saw the emergence of a dynamic sustainability capability. This phase represents the period after the financial crisis and the alignment between collective intentionality and integration, which enabled the emergence of a strategic dynamic sustainability capability.

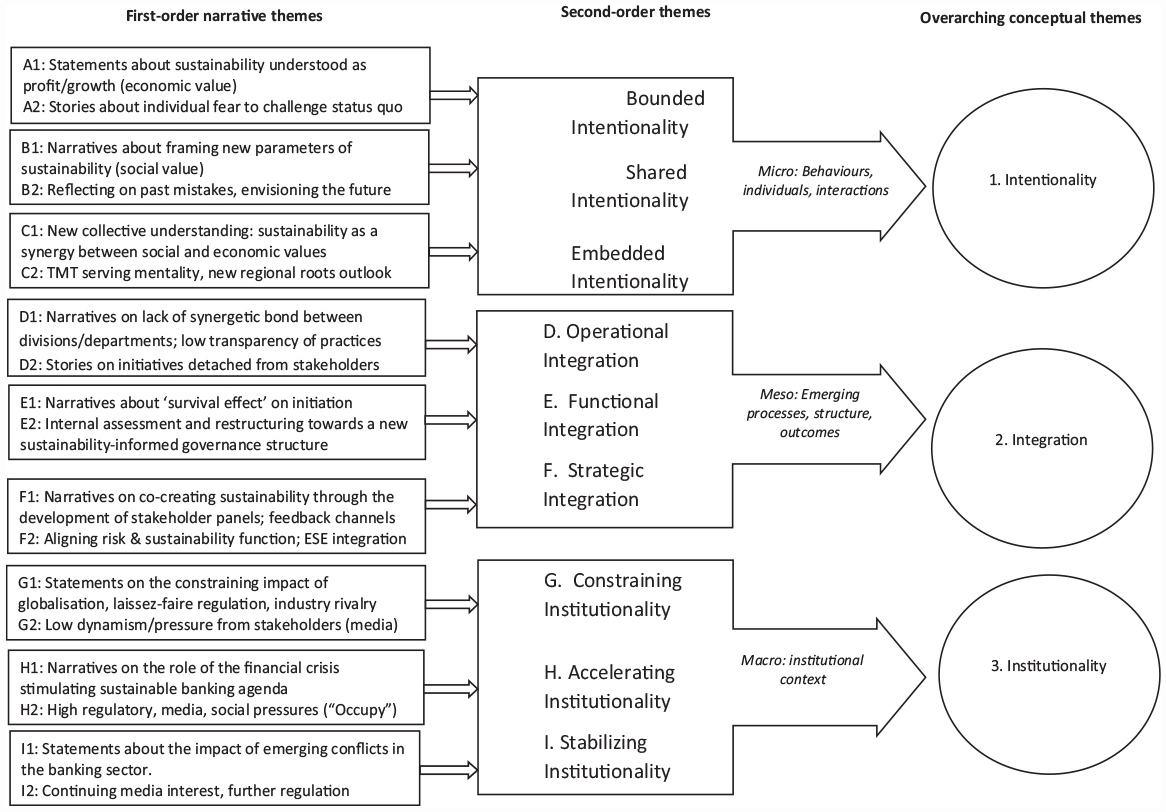

During the data analysis, we drew on an adapted version of the inductive methods outlined by Gioia et al. (2013). Our first-order coding consisted of “open-coding” to identify themes emerging from the data itself (Corbin & Strauss, 1990). Figure 1 presents a static picture of the emerging first-, second-, and conceptual-order themes.

Emerging First-, Second-, and Conceptual-Order Themes.

Using protocols for identifying micro-foundations outlined in the literature (Barney & Felin, 2013; Felin et al., 2012), including behaviors, individuals, interactions and processes, structures, and emergent outcomes, as a guide, we then began developing our second-order themes. Through this analytical process, we also coded for factors influencing sustainability from the wider institutional context (Winter, 2012). This allowed us to identify multilevel contextual interrelationships over time (Also see Alcaraz & Thiruvattal, 2010; Cooper et al., 2016; Porritt, 2007; Sharma et al., 2007; Spector & Meier, 2014; Starik & Rands, 1995). Finally, as Figure 1 shows, we identified three conceptual categories—intentionality, integration, and institutionality—that we found inductively to be mechanisms shaping the micro-foundations of sustainability in different ways, at different levels of context, and in different phases. In addition, we also found that the macro institutional context is a crucial mechanism influencing the micro-foundations for organizational behavior toward sustainability. We used the label intentionality to define the changing managerial behaviors, understanding, and attention toward sustainability before, during, and after the financial crisis. The category, integration, refers to the process of integrating sustainability agenda and principles in the organizational processes and structures of the bank. Finally, we used the label, institutionality, to define the institutional-level factors and market dynamism that drive organizational and behavioral changes which constrain, accelerate, or stabilize sustainability in RBS before, during, and after the financial crisis.

The analytical approach we adopted reflected several of the criteria for “naturalistic inquiry” for establishing the trustworthiness of research designs (Lincoln & Guba, 1985). They included a prolonged engagement with the research setting and informants between 2009 and 2012, which allowed for the accumulation of tacit knowledge and negotiated outcomes throughout the research process. We shared our findings with the participants in the study, both informally and as part of successive interviews to elicit feedback. Multiple sources of data allowed for the triangulation of the findings. Finally, our research was audited by four academic peers familiar with the study (Balogun & Johnson, 2004). The academic peers were all renowned professors in top North American and European universities, whose published works on CSR and sustainability field have paved the ground for our intended contribution. Approaching academic peers served a very important dual role. First, on the implementation side, they guided the research design and informed the analytical practices. Second, on the positioning side, they confirmed the importance of our findings and their overall fit within the sustainability literature. To ensure intercoder reliability, we undertook a 10-step process explained in Appendix (Miles & Huberman, 1994; Olson et al., 2016). And while we think that many of the findings in our study are likely to be generalizable to other research settings, we acknowledge that our inductive, longitudinal, single case-based study, while empirically rich, internally consistent, and demonstrating explanatory power, makes the trade-off with some external validity (Eisenhardt, 1989; Langley, 1999; Lovas & Ghoshal, 2000).

Findings

In this section, we report on the development of sustainability organizational capability from being an operational capability for our explored case study to becoming more strategic or dynamic in the aftermath of the Global Financial Crisis. We organize our findings around the three phases identified in our longitudinal process research design. They include Phase 1: sustainability as an operational capability (2002–2007; Phase 2, as a transitional capability to sustainability (2008–2009); and Phase 3, sustainability as a dynamic capability (2010–2012). In each of these phases, we discuss the managerial intention and understanding of sustainability objectives and how it is inhibited or accelerated by organizational processes, structures, and the wider institutional context. Thus, we focus closely on the factors leading to either alignment or misalignment of the micro-foundations which constitute business sustainability over time. We explore the development process by mapping how managerial intentionality toward sustainability becomes shared across the organization and how this leads to the strategic integration of new processes and structure supporting the bank’s sustainability agenda. In addition, we explain the constraining, accelerating, and stabilizing impact of institutionality on the micro, meso, and macro levels of context.

Phase 1: Sustainability as an Operational Capability (2002–2007)

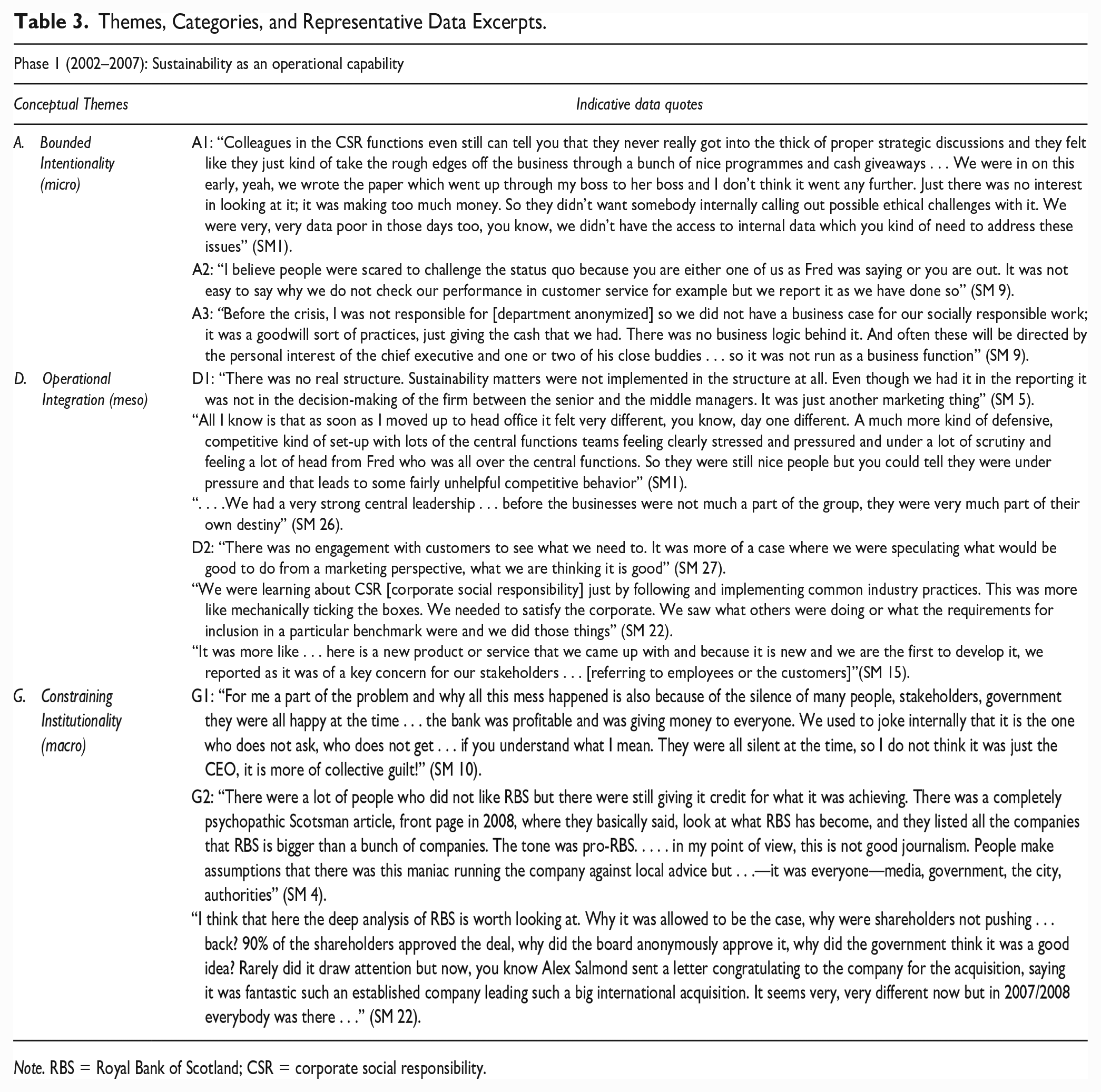

Following the acquisition of NatWest in 2000, and with the promotion of Fred Goodwin to CEO in 2001, RBS established a small CSR team in 2002. While their operational activities varied, they included benchmarking with other banks, report writing, and, particularly, corporate philanthropy, such as donating money to charities (see Table 3 for supporting data relating to phase 1).

Themes, Categories, and Representative Data Excerpts.

Note. RBS = Royal Bank of Scotland; CSR = corporate social responsibility.

Bounded Intentionality

Both the meaning and the function of sustainability were confined to the intentionality of the CSR team in Phase 1, which, at the time, was situated within the Public Policy department, operating as a sub-division of the RBS’s marketing department. The main activities of the newly established CSR team were restricted to the practice of writing group reports at a time when the business was expanding further, both domestically and internationally. There was a lack of shared understanding across the Bank of what CSR was. For the top management team (TMT) of the organization, CSR referred to the Bank’s corporate philanthropic activities aimed at improving the RBS brand and corporate reputation, while sustainability referred to maximizing financial returns. The operational orientation of the company’s practices and intentionality toward sustainability was a reflection of the company’s culture and TMT goals. The decision to initiate a particular sustainability-oriented activity was tightly related to the decisions of the company’s powerful executive, and, given the climate in the Bank at the time, these decisions were often impossible to challenge.

Operational Integration

RBS, in Phase 1, lacked a strong internal communication function, and with the TMT and the majority of RBS’s divisional leaders focused almost exclusively on acquisition-fueled growth, key sustainability issues for the business were neglected (e.g., accurate assessment of stakeholder demands, warnings from the CSR teams such as an issue in 2005 with paper indicator assurance). The CSR team focused on developing a CSR operational capability by accumulating knowledge, externally, from the sector through international benchmarking assessments, external auditors, and consulting rather than from internal, group-led intentionality integrated within the wider organizational processes and structures. Our findings demonstrate that to a large extent, the difficulty to initiate and integrate certain sustainability practices was a result of the weak governance systems in the Bank, which did not support collective goals and sustainability principles in practice, instead, embedding financial agendas in their activities. As one manager points out, Yes, on paper it was, but in practice, things were not like that. In terms of global reporting, it was easy. You just ask people to give some contribution and contacts and you put it together, but actually getting involved in the decision-making or coordinate actions was difficult as you need to have the structure for that. (SM 7)

In the period before the financial crisis, only the economic value created by the company managers was rewarded through HR practices and compensation schemes. During Phase I, sustainability as an organizational capability was integrated solely as a business operation of the CSR team. It was not a part of the governance committee of the Bank, nor was it part of the wider RBS strategy.

Constraining Institutionality

During the first phase of capability development, several exogenous institutional factors appeared to influence the development process of sustainability as an organizational capability. In particular, the analysis of the data indicated institutional dynamics such as the globalization of the banking sector, the laissez-faire regulatory approach of the U.K. banking system (FSA, 2011), together with the low dynamism in the stakeholder landscape to play a relatively inhibiting impact on the development of sustainability as a more strategic capability across the bank. The inhibiting effect was in the significantly dormant character of the exogenous forces in the industry. During this period the RBS group was facing intense competition in all the markets it served, especially in the U.K. retail and commercial banks, and building societies, as well as from a number of international competitors headquartered in London such as Barclay’s Group and Citi Group (RBS Annual Reports; The Turner Review). The intense rivalry across the banking industry increased the economic rationalization of the company’s executives and provoked riskier management decisions (informal conversations). Thus, the normative style of the majority of banking institutions including RBS was oriented toward “maximizing shareholder value” rather than on other sustainability dimensions.

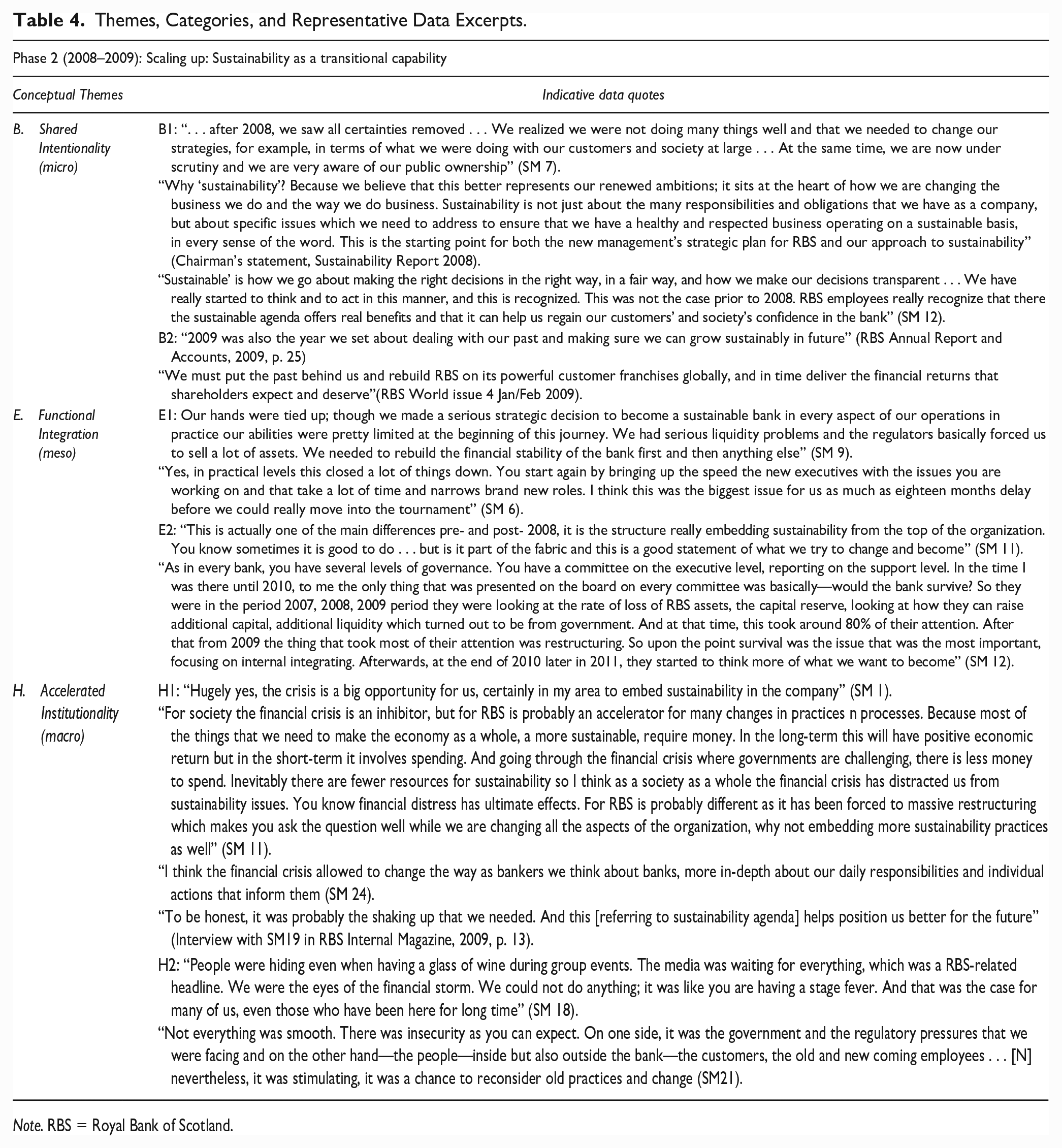

Phase 2: Scaling up: Sustainability as a Transitional Capability (2008–2009)

Accelerating Institutionality

The macro-environment in the year 2008 was very challenging for RBS. With the financial crisis in full swing, RBS had the worst performance in its history and its period of market leadership came to an abrupt end. RBS only survived due to a government bailout, which resulted in the bank being placed under public ownership and scrutiny. RBS faced numerous challenges. It needed to regain clients’ trust, ensure that its activities were ethical, provide trustworthy expert advice, and repay the taxpayers’ investment. If in the first phase, the bank’s management felt it has control over the dynamics of the institutional environment, in this period, the power shifted to the hands of its stakeholder groups. Pressures for change emanated from the government, emerging social movements such as “Occupy Edinburgh” movements, and negative media coverage. Nevertheless, the global financial crisis and the turbulent macro context broadened managers’ intentionality toward sustainability. There was a new-found emphasis on sustainability which was intended to symbolize the ambitious renewal of RBS. During this period the logic and practice of sustainability started to be shared as a distinct framework by the divisional managers beyond the original intentions of the sustainability team. As a former manager suggests: “Sustainability has a different connotation, it talks about long-term sustainable business. . .” (SM 2). A contributing factor to the changing managerial intentionality toward sustainability during this phase was the change in the Bank’s leadership. After the appointment of a new chief executive, Stephen Hester, in November 2008, the Group’s chairman Sir Tim McKillop was replaced along with the seven Group non-executive directors. A new, smaller board of directors, headed by the Group’s new chairman Phillip Hampton, was formed (RBS Annual Report and Accounts, 2009; Sustainability Reports; see Table 4 for supporting data relating to Phase 2).

Themes, Categories, and Representative Data Excerpts.

Note. RBS = Royal Bank of Scotland.

Toward Shared Intentionality

The majority of RBS senior managers saw an opportunity in changing the organizational culture and rebuilding RBS into a “sustainable” bank following its partial nationalization (informal conversations; participant’s observation). An essential part of the recovery process was to revise the meaning and the practice of sustainability across the organization’s various divisions. Toward the end of 2009, CSR developed into a transitional capability, which was used to help traumatized employees to change behaviors and buy into a new character for the bank. This happened mainly through the process of reflecting on past mistakes, evaluating the various processes and activities in the Bank in terms of their “sustainability” and framing new sustainability behaviors in the Bank (informal conversation; participant observation). During this phase, the CSR team, which was renamed the Sustainability team, became a key mechanism for this transition, acting as an internal adviser during the recovery process. Nonetheless, it was not a straightforward process for RBS. To stimulate the restructuring process, the new CEO initiated a group-level Strategic Review in November 2008. It aimed at substantial changes in internal processes such as prioritization of stakeholders, management of organizational risks and uncertainties, and integration across the organizational divisions and multiple businesses in the Group.

Toward Functional Integration

As a result of the strategic review, two main structural changes took place. One was the simplification of the Group’s strategy to manage a variety of risky assets that were discovered (e.g., banking products, trades, deals, portfolios, and businesses owned in emerging market countries). The second was the efforts by the TMT to integrate the sustainability agenda into the corporate governance structure of the Bank through the development and inclusion of a Group Sustainability Committee formed from the same sustainability team. It had an overarching role in assessing sustainability behaviors across the different functions of the Bank and advising on areas requiring development. Internally, the sustainability team became highly respected within the organization, as many employees believed that “it made our opinion heard on board level” (informal interview with employee 5). This was a small step toward rebuilding the Bank’s internal confidence.

However, our findings also identified two ambiguities that constrained the full integration of sustainability within RBS and its development from an operational capability to a strategic dynamic sustainability capability within the Bank. On the one hand, besides the restructuring plan that the new executive team initiated at the beginning of this period and their attempt to change dysfunctional habits in various parts of the organization, the TMT was often reticent to be the first in the industry to introduce certain practices or products related to a sustainability agenda. A senior manager recounts, He used this interesting phrase which was just to brain me a bit: . . . Just remember planers get the arrows, settlers get the land,’ so the first people to explore a new territory got shot and the winners are those behind them. So this was the kind of attitude. (SM 6)

On the contrary, although shared intentionality and understanding toward sustainability beyond profit maximization and market growth started to develop within the Bank, its dependency on the U.K. government, which owned 70% of the Bank, challenged the TMT’s efforts to fully invest in the areas that the newly established Group Sustainability Committee recommended.

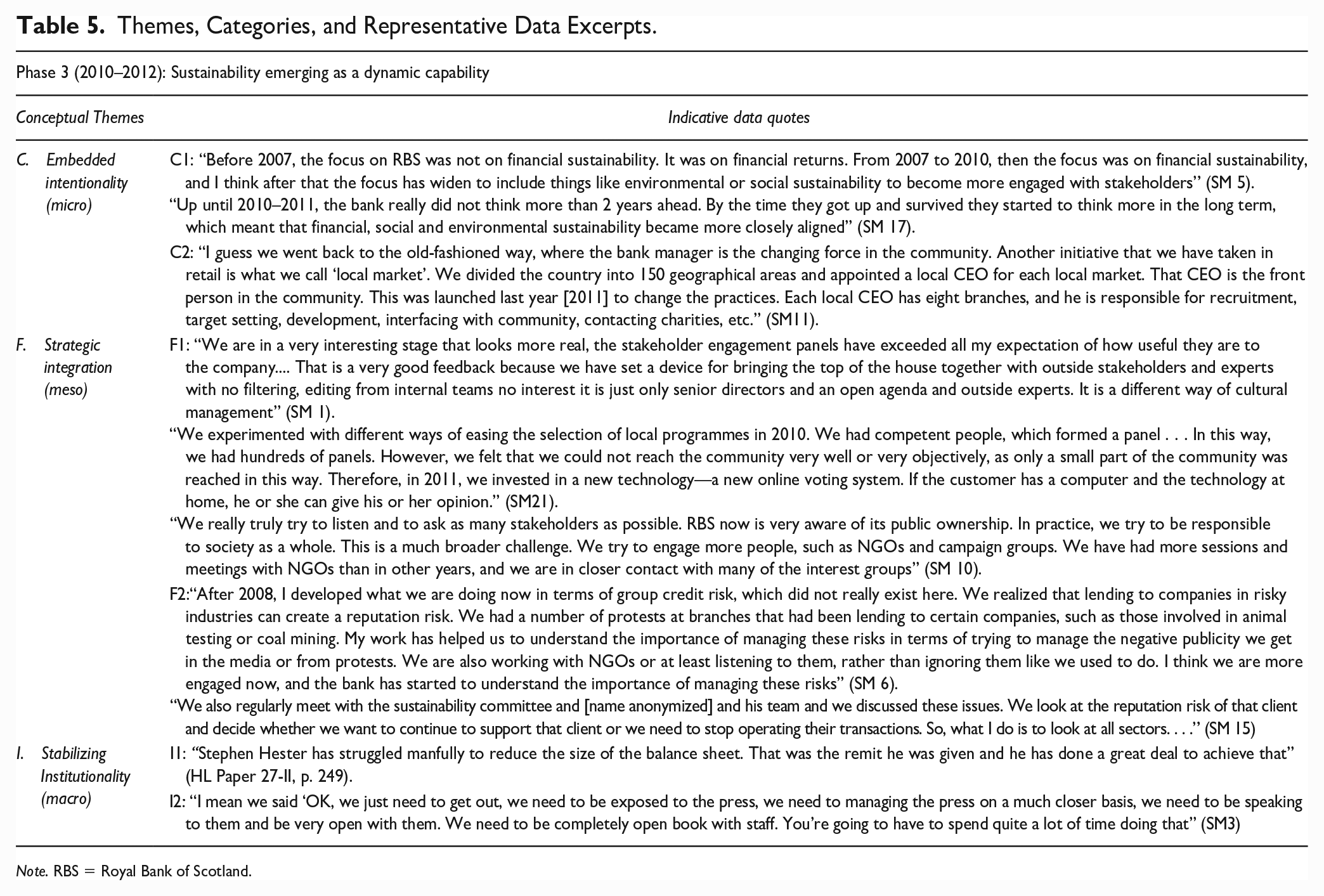

Phase 3: Sustainability Emerging as a Dynamic Capability (2010–2012)

In Phase 3, sustainability took the form and function of a strategic dynamic capability for RBS. The process was supported by embedded intentionality toward sustainability and its strategic integration into the Bank’s governance structure and processes (see Table 5 for supporting data relating to phase 3).

Themes, Categories, and Representative Data Excerpts.

Note. RBS = Royal Bank of Scotland.

Embedding Intentionality

Two main developments allowed intentionality toward sustainability on the micro level to develop from being shared in Phase 2 to becoming embedded in RBS’s strategy. First, there was a growing collective view across the Bank that sustainability could drive synergies between economic, environmental, and social value. Second, RBS was focusing on retrenching as a regional Bank with a more local focus on its business operations. During this phase, and guided by the Strategic Review during the 2008–2009 period, RBS management focused on improving its internal and external stakeholder relationships through the creation of strategic unity about sustainability across the Bank. As one of the interviewees explained, the focus was no longer a top-down approach but there was an emphasis on shared learning, learning from each other” (SM 10). Another former manager also stated: “In contrast to Fred, Stephen understands the value of making friends across the organization. He often says that pure face-to-face communication is the best cure for the crisis. (SM 3)

An emphasis was placed on internally motivated initiatives such as sustainability-oriented workshops, conferences, and open discussions with RBS’s primary stakeholder groups, which were organized through the Sustainability function of the Bank. Their purpose was to enable group interaction and stimulate a collective understanding of sustainability built on the synergy between economic, environmental, and social values (participant observation, diary notes). For example, one such conference took place in December 2012 in London (participant observation). Participants referred to the event with different names, but mostly they used expressions such as “idea generator,” “brainstorming exercise,” and “building a shared common sense” (diary notes, participant observation). According to one of the participants “disseminating our own and our stakeholder narrative stories enable us to connect but also to introspectively assess and learn from past practices and mistakes.”

In contrast to the second phase of capability building where the management aimed to communicate one single meaning and definition of sustainability across the organization, during the third phase they agreed that there are multiple stakeholder parties with different, even conflicting preferences and goals which often manifested in different behaviors (interviews, informal conversations). As a result, the TMT objective became to accommodate the different visions of a “sustainable bank” by allowing ambiguity in the way people across the Bank envision the concept, but at the same time focusing on communicating the underlying issues associated with it.

Toward Strategic Integration

In this phase, RBS adopted a relational approach to developing sustainability as a strategic dynamic sustainability capability. One of the first activities undertaken in support of the new approach was the revision of the Bank’s stakeholder list to include previously overlooked stakeholder groups. This move was mainly triggered by fears of continuing shifts in the industry as well as increasing pressure from affected customer and community groups. To accelerate learning about customers’ and employees’ needs, the Bank integrated a number of support mechanisms and practices, such as a new voting-software system for customers and internal channels for employee feedback.

This new relational approach to engagement with various stakeholder groups was accelerated through an increase in group-level communication across divisions and departments. Previously during Phases 1 and 2, managers rarely discussed issues with colleagues outside their departmental silos. However, the restructuring of the organization and, in particular, the inclusion of a Sustainable Committee represented by the head manager of every department encouraged knowledge sharing and consensus building. Furthermore, following the objective to enable communication, coordination, and learning across various levels of the organization, the Bank introduced its RBS Ambassadors Program, based on internal volunteers who act as ambassadors of ideas and opinions emerging across their local divisions or branches as well as intermediaries between the top management and the lower levels of management. According to the head of the program, this initiative helps to “influence opinions of people outside and inside the organization.” Taken together, the data suggest that the development of a dynamic sustainability capability was initiated collectively through interaction with stakeholders both externally and internally and an alignment of their perspectives.

The majority of structural transformations observed during the third phase of capability development established the context for information processing, interaction, and collective action both from the inside and the outside of the organization. The observed structural micro-foundations can be represented by the following four themes: less codification of knowledge realized through the reduction of the number and the pages of policies related to sustainability; bringing together conflicting practice-based logics through the creation of new frameworks of operations; changes in the structure of decision-making, as well as a continuous integration of sustainability within the governance structure through the involvement of the Sustainability committee and internal promotions.

Key structural changes included the alignment between the risk and sustainability logic through the development of the Group’s new ESE (ethical, social, and environmental) policy framework initiated in 2010 (RBS World, Issue February 2012). The framework was designed for managing environmental, social, and ethical risks related to key clients. The primary objective of the new framework was to manage reputation and credit risk by integrating sustainability principles. Continuing stakeholder protests in the sector triggered this initiative. Moreover, during this phase, the structure of the decision-making process was further restructured through the integration of stakeholder engagement panels where senior managers, outside experts, and stakeholders form a dialogue based on an open agenda. During this period, the established Sustainable Business Committee established in Phase 2 continued to play a key role in integrating and embedding sustainability practices in the core of the Bank’s operations and overall strategy. It was further developed to include not only members of the sustainability team but also representatives, such as the head manager of every department. Such minimal restructuring was strategic and aimed to further encourage knowledge sharing and consensus building in the group’s governance structure (interviews, internal documents). Broadly, the main purpose of the Sustainable Banking Committee is to supervise and challenge how the Bank’s management is taking into account sustainable banking and reputation-related issues, making decisions, and implementing actions that consider the long-term stakeholder interests (internal documents). Furthermore, the bank introduced a new position—head of conduct and regulatory affairs, who was assigned to directly supervise the implementation of the sustainable principles and code of conduct within the risk function of RBS and report directly to the CEO. Sustainability principles were also integrated as a guiding framework for RBS’s strategy. Overall, the third phase of developing a dynamic sustainability capability was triggered by a need to engage external and internal stakeholder groups in a continual conversation about sustainability.

Stabilizing Institutionality

During the third phase, the institutional pressures affecting the development of sustainability as a more strategic capability for RBS can be characterized briefly as moderate in intensity. They involved continuing customer dissatisfaction over high executive bonus compensations (e.g., Stephen Hester’s possible compensation of 750,000 and £1.1 million salary) and the occurring IT problems in June 2012 (HL Paper 27-II). However, the data show also regulatory and political recognition by the governor of the Bank of England at the time Sir Mervyn King over the progress of the executive team toward a more sustainable bank (HL Paper 27-II, p. 249). Furthermore, toward the end of 2012, numerous stakeholders already started to appreciate the steps that RBS has started to take to become a more sustainable bank (informal conversations with stakeholders, perception of interviewees). The more positive view and satisfaction of the U.K. government toward RBS CEO’s efforts in rebuilding the bank after the financial crisis gave more confidence to the bank managers to continue the process of strategically integrating sustainability in core operations and strategy. To ensure that the bank is responding to moderate but existing institutional pressures and regulation while embedding sustainability across the organization, the senior management undertook some structural organizational changes such as introducing a new post—head of conduct and regulatory affairs. Moreover, this change in the governance structure of the bank stimulated the collective intention, knowledge sharing, and consensus building toward the sustainability agenda.

Discussion

In the present research, we sought to address two research questions. The first question is, what are the micro-foundations of a dynamic sustainability capability, and how do they become aggregated at different levels of context? In addressing this question, we also sought to answer calls for multilevel studies by adopting a case-based processual study of RBS (cf. Alcaraz & Thiruvattal, 2010; Cooper et al., 2016; Porritt, 2007; Sharma et al., 2007; Starik & Rands, 1995). The micro-level foundations “turn,” which seeks to understand the origins of aggregate concepts like capability or sustainability by looking at their constituent parts, such as the organizational behaviors underpinning them, shares a concern with contextualization (Barney & Felin, 2013; Felin et al., 2012). In the following section, we develop a conceptual framework to explain our findings and the contributions we seek to make toward a fresh consideration and reconceptualization of the micro-foundations of organizational behavior toward sustainability.

Emerging Process Model of Sustainability Dynamic Capability Development (2002–2012)

The importance of context has been emphasized by scholars of organizational behavior. For instance, Fisher and Hutchings (2013, p. 805) state succinctly that “context matters,” while Rousseau and Fried (2001, p. 2) argue that contextualization “makes our models more accurate and our interpretation of results more robust.” Indeed, context over time is at the heart of processual studies (Pettigrew, 1997). In this study, we identified three distinct periods in which the micro-foundations of a sustainability capability developed at RBS. They included Phase 1 (2002–2007) Sustainability as an operational capability; Phase 2 (2008–2009) Scaling up: Sustainability as a transitional capability, and Phase 3 (2010–2012) Sustainability as a dynamic capability (see Figure 2 for our 3-i process model).

Process Model of Dynamic Sustainability Capability Development (2002–2012).

In general, capability development concerns the transformation of individuals’ intentions into new, coordinated patterns of knowledge, interests, and coherent actions. The few empirical studies focused on exploring the capability development process define the process as being gradual and cumulative rather than sudden and response to existing capabilities (Montealegre, 2002). The explored case of the RBS confirms the cumulative character of the process development when it comes to the development of sustainability organizational capability but pinpoints the centrality of sudden exogenous shocks as essential triggers in the transformation of existing capabilities through time.

The empirically rooted capability development model involved micro-foundations on the micro and meso level as well as institutional inhibitors and accelerators on the macro-level which shape the development process. The study shows that the interrelationship, referred to as alignment in this study, between the explored micro-foundations defines the nature and the form that sustainability capability would take through time. The remainder of the section is organized around the development of the micro-foundations of organizational behavior and sustainability capability over the three phases.

Behaviors and Individuals

Between 2002 and 2007, sustainability was largely confined to the communications, marketing, and PR activities of the Bank. While the small team making up the Corporate Responsibility department framed their intentions in terms of the wider sustainability of the Bank at the micro level of context, the senior management and Board viewed CSR in terms of the Bank’s image, exercised through corporate philanthropy at the meso level of context. At this stage, CSR was having little impact on the wider behaviors of individuals in the Bank. Several reports identifying systemic risks pertaining to various products and services, such as the illegal selling of payment protection insurance (PPI) and systemic risks, for instance, were ignored. This was due to two reasons: First, all the banks were engaging in these activities, and second, it was profitable. This, however, began to shift, particularly with the resignation of the CEO, Fred Goodwin, in 2008, and the appointment of Stephen Hester as Group CEO, who was charged with rescuing RBS. With the rescue of RBS, and intense pressure on the Group at the macro level of context, CSR took on new urgency, and sustainability intentions began to be shared throughout the Group. At the end of the study embedded sustainability principles were embedded in the operations and strategic direction of the Group.

Previous research has directed attention toward the relationship between pro-sustainability attitudes, behaviors and passions of employees (Banerjee, 2001; Sharma & Henriques, 2005), and those of leaders (Branzei et al., 2004; Robertson & Barling, 2013; Sharma, 2000; Unsworth et al., 2013). Indeed, our study shows a direct correlation between the two. The higher-order goals held by the senior management team and Board between 2002 and 2007 emphasizing financial returns, growth, and reputational management dominated lower-order sustainability intentions embedded in the Corporate Responsibility department. With the change in CEO and restructuring of the Board, corporate responsibility, and eventually sustainability were elevated as higher-order goals, thus shifting the “psychological climate” within the Group (Norton et al., 2017). Intentionality, including the attitudes, beliefs, passions, and orientations of employees, and their scaling is, therefore, a key micro-foundation of organizational behavior and a sustainability capability. However, intentionality at different levels of context also takes on its own character, suggesting that such micro-foundations also change over time and at different levels of context as they scale.

Interactions and Processes