Abstract

This study investigates the pivotal policy question of whether a firm’s corporate governance influences its political spending disclosures. Using a sample of S&P 500 firms from 2011 to 2019, we find empirical evidence that a board of directors’ monitoring and resource provision roles affect a firm’s political spending disclosure. Extending agency theory-driven expectations, we provide evidence that measures of a board’s monitoring role such as female monitoring directors, shorter board tenure, audit committee size, audit committee meetings, and audit committee education enhance a firm’s political spending disclosures. Second, drawing from resource dependence theory and examining a board’s resource provisions, we find evidence that female advisory directors, CEO duality, additional directorships, and audit committee characteristics (i.e., size, number of meetings, age, and education) promote political spending disclosures. The study contributes to corporate governance and corporate political activity literatures by outlining different types of governance that may drive a firm’s political spending disclosures, a key component of a firm’s political responsibility.

Keywords

Firms face increasing pressure from stakeholders demanding more transparent corporate political spending disclosures (PSD), especially after the U.S. Supreme Court’s 2010 decision in Citizens United v. Federal Election Commission, which allowed corporations to make unlimited political expenditures with no strict public disclosure requirement (Beets & Beets, 2019; Cohen et al., 2019; Goh et al., 2020; Skaife & Werner, 2020). According to the Center for Responsive Politics, firms spent $3.5 billion on corporate lobbying in 2020, and these expenditures are expected to increase significantly in the future (Ali et al., 2022). Although firms disclose political action committee contributions and lobbying expenditures, firms are not required to disclose other types of political expenditures such as contributions to trade associations, social welfare organizations, and super political action committees (Baloria et al., 2019; Beets & Beets, 2019; Jia et al., 2021). Furthermore, political spending can be channeled and concealed via financial intermediaries such as social welfare organizations and thereby expenditures remain undisclosed in any public record, leaving corporate owners with significant information-asymmetry gaps (Ali et al., 2022; Goh et al., 2020). 1

Given the large amount of funds that firms expend on corporate political activity and the growing societal demand for PSD, firms have a fiduciary responsibility to disclose this information to demonstrate their accountability to the public (Richter, 2014). In addition to fiduciary responsibilities, researchers have also called on firms to focus on their corporate political responsibilities (CPRs) defined as “a firm’s disclosure of its political activities and advocacy of socially and environmentally beneficial public policies” (Kaplan et al., 2022; Lyon et al., 2018; Rehbein et al., 2020). In defining, CPRs, Lyon and colleagues (2018) underscore that political transparency is “the crucial safeguard to protect society from capture by private interests.”

Moreover, firm stakeholders and many other prominent entities, such as the Global Reporting Initiative, the Organization for Economic Co-operation and Development, and Vigeo Eiris, 2 are demanding greater corporate political accountability (Lyon et al., 2018). In fact, stakeholders’ demand for political transparency has intensified to unprecedented levels (Baloria et al., 2019). In the United States, the Securities and Exchange Commission (SEC) has been facing mounting pressure from various stakeholders (investors, politicians, employees, and consumers) to require corporations to disclose their political contributions (Cohen et al., 2019; DeBoskey et al., 2021). Similarly, the heated demand for PSD has led to a surge in the number of proxy proposals that institutional investors are submitting, demanding firms to provide more political transparency. Correspondingly, leading institutional investors in the United States recently pushed their investee firms to exhibit transparent PSD (Bebchuk & Jackson, 2013; Goh et al., 2020). 3

Even though a firm’s political transparency may provide benefits such as reducing information asymmetry and cost of debt (DeBoskey et al., 2021; Hillman & Hitt, 1999), many firms have not been convinced that political transparency is warranted (Baloria et al., 2019; Jia et al., 2021). Without PSD, shareholders are left in the dark about significant decisions that influence their firms’ bottom line. Shareholders may be uninformed about possible investment risks when their investments are allocated to political efforts that have uncertain outcomes (Lyon et al., 2018). Worsening the situation, dark money 4 (i.e., political donations made without public disclosure; Chand, 2017; Mithani, 2019), have increased after the Citizens United decision (Massoglia, 2020). This type of unobservable corporate political activity represents another channel for managerial opportunism and increases the divergence between a firm’s social responsiveness and political responsiveness (Lyon et al., 2018). Given this lack of political transparency (Jia et al., 2021; J. Wang & Zhang, 2022), it is critical to study the drivers of a firm’s political spending transparency.

Our research question focuses on how corporate governance in particular the board of directors shapes a firm’s decisions concerning corporate political disclosures (CPA, 2022a, 2022b). To address this question, we draw from previous research that focuses on how a firm’s corporate governance may shape a firm’s political actions as well as research that has examined the drivers of PSD. For example, Dahan and colleagues (2013) find that a firm’s weak corporate governance systems allow executives to abuse corporate political activity, which may diminish political sustainability and cause additional conflicts with shareholders. Prior research has also analyzed the drivers of PSD, including the political connections of board members, institutional ownership, and corporate lobbying (Goh et al., 2020), ownership structure (Ali et al., 2022), specialized political committees (DeBoskey et al., 2018), corporate Twitter accounts (Lei et al., 2019), and shareholder proposals (Baloria et al., 2019). We extend this research theoretically by looking at PSD through the lens of corporate governance and applying a dual theoretical perspective that incorporates insights from both agency theory and resource dependence theory (Goh et al., 2020).

Since a firm’s political donations may contribute to severe agency and information-asymmetry problems (Aggarwal et al., 2012), boards of directors need to exercise their monitoring role by overseeing corporate political activity and reducing agency costs by enhancing PSD. Simultaneously, from the perspective of resource dependence theory, board members, who are well positioned to advise the firm about recent corporate social responsibility practices and current societal expectations, may insist on engaging in higher levels of CPR to achieve access to critical financial resources (Pfeffer & Salancik, 2003). Hence, our dual theoretical framework predicts that board members’ monitoring role will reduce agency costs, improve a firm’ ethics, and address societal responsiveness, and their advisor role will enhance firm’s reputation, achieve strategic advantage, and secure access to resources (de Villiers et al., 2011; Hillman & Dalziel, 2003; Pugliese et al., 2014). Both roles are expected to motivate board members to pursue PSD to achieve these benefits.

This study offers several different contributions. First, this study is a direct response to calls for a better understanding of PSD (Ali et al., 2022; Beets & Beets, 2019; DeBoskey & Luo, 2018; Goh et al., 2020; Mithani, 2019). Second, we contribute to corporate political activity research by investigating how corporate governance shapes corporate political decision-making, with a specific focus on political transparency (Mithani, 2019; Schuler et al., 2019). Third, this study explores whether audit committees (AC), a corporate governance mechanism, play a role in promoting more political transparency. Prior research provides evidence that AC, a watchdog for financial and non-financial reporting transparency, may enhance the transparency of non-financial disclosures, such as corporate social responsibility disclosures and sustainability reporting, but there has been little exploration of whether audit committees play a role with respect to political disclosures (Al-Shaer & Zaman, 2018; Li et al., 2012; Raimo et al., 2021). Fourth, we contribute to corporate governance literature by emphasizing the importance of combining agency and resource dependence theories to investigate how corporate boards promote PSD and provide evidence consistent with both theories.

The next section presents the theoretical framework. Then we review the extant empirical literature and develop research hypotheses, present the research design, and discuss the empirical results. The final section of the article outlines concluding remarks and discusses implications and recommendations for future research.

Dual Theoretical Framework

Previous research emphasizes that a firm’s board of directors has two roles: to monitor (agency theory-driven role) and to increase access to resources (resource dependence theory-driven role) (Hillman & Dalziel, 2003). According to agency theory, managers initiate and execute, whereas directors are there to monitor the actions of top managers (Jensen & Meckling, 1976). Resource dependence theory emphasizes that directors increase access to resources through their expertise in and knowledge about corporate strategies (Pfeffer & Salancik, 2003). We use this dual theoretical framework to understand why boards of directors may be concerned about a firm’s political transparency. First, corporate boards are responsible for making strategic decisions, such as identifying the firm’s threats/opportunities, shaping long-term strategy, monitoring and evaluating strategy execution, building external relations, bolstering their company’s reputation, and advising on major decisions, such as corporate political affairs (Hillman & Dalziel, 2003). Indisputably, if firms spend significant funds on corporate political activity, this may lead to risky opportunities causing numerous stakeholders including shareholders to be concerned about these political expenditures.

Second, corporate political spending is naturally associated with acute agency costs that may threaten corporate legitimacy and credibility. Moreover, shareholders are concerned about how their investments are injected into the political arena without their consent (Beets & Beets, 2019; Mithani, 2019). Thus, boards of directors have an incentive to monitor political expenditures to enhance PSD which reduces agency costs and demonstrates an ethical stance. Third, boards of directors also have an incentive to exercise their advisory role by emphasizing the strategic opportunities associated with PSD, bringing competitive and reputational advantages, enhancing their relationships with stakeholders, and securing access to resources (DeBoskey et al., 2021; Lyon et al., 2018; Skaife & Werner, 2020). Hence, our dual theoretical framework fully elucidates boards’ behaviors regarding corporate political transparency, as boards of directors can utilize PSD to monitor their firms’ managers (agency theory) and to tighten relationships with stakeholders (resource dependence theory).

Agency Theory

Agency theory focuses on the monitoring role of the board and the goal conflict between the management and shareholders. The conflicts between executives and owners can be mitigated through a strong board of directors that closely monitors a firm’s management (Aguilera et al., 2021). According to agency theory, the board is primarily responsible for monitoring the firm’s activities that have a significant impact on the organization’s financial resources and reputation. Therefore, a firm’s board of directors should be motivated to monitor corporate political spending since some types of political expenditures can destroy firm value and create inevitable agency problems (Ali et al., 2022; Goh et al., 2020; Hillman et al., 2009; Shi et al., 2021). Prior literature provides evidence of the strong effect of board oversight on corporate transparency (Al-Shaer & Zaman, 2018; Beji et al., 2021; Raimo et al., 2021), suggesting the effective monitoring role of the board to reduce information asymmetries. Additional research provides evidence that institutional investors and board members, as critical corporate governance monitoring mechanisms, may put firms’ executives under significant pressure to exhibit higher PSD (Ali et al., 2022; Goh et al., 2020).

Resource Dependence Theory

Resource dependence theory emphasizes the important advising role of the board and argues that directors through their resource-provision role provide advice and counsel, improve information flows, and better access to resources (Pfeffer & Salancik, 2003). Hence, directors are considered “resource rich” as they possess more firm-specific information and operational expertise, extensive experience, and prior relationships, making them business experts, support specialists, and community influencers (Aguilera et al., 2021; de Villiers et al., 2011). The resources that board members have can in turn shape their strategic advice and enhance firm value (Beji et al., 2021; Sultana et al., 2015; de Villiers et al., 2011).

Resource dependence theory explains how entities use their relationships with the outside environment to reduce uncertainty (Pfeffer & Salancik, 2003). Specifically, it suggests that corporations strategically utilize some options to lessen environmental dependencies, such as engaging in political actions (Hillman et al., 2009). 5 For example, firms are motivated to lobby to take advantage of new legislation or lessen the impact of unfavorable policies (Shi et al., 2021). 6 With this in mind, and given the opaqueness of corporate political activity, resource-rich directors (i.e., directors with superior advisory capabilities due to their experience and education) are more likely to be knowledgeable about the importance of CPR and are well placed to ensure that firms pursue PSD to reduce uncertainty and to enhance a firm’s legitimacy (Goh et al., 2020).

Corporate Political Transparency and Hypothesis Development

Corporate Political Transparency

Many corporations limit their PSD, as public disclosure can attract public scrutiny, reputation threats, and potential boycotts (Beets & Beets, 2019). Relatedly, Prabhat and Primo (2019) show that investors respond negatively to mandatory PSD, arguing that such requirement gives a firm’s competitors an opportunity to attack the firm and create unfavorable media coverage. Hence, corporate executives may limit the release of potentially risky information about political expenditures to maintain the firm’s reputation (Carlos & Lewis, 2017; McDonnell & King, 2018). Firms may use different approaches to hide their political spending from their stakeholders and public at large. 7 One approach is that firms conceal their political spending through 527 organizations, super political action committees, state-level spending, and 501 organizations (Baloria et al., 2019). However, some of the recipients must disclose the sources of political contributions. Also, some nonprofit entities, such as the Sunlight Foundation, 8 oversee such payments using the information that recipient entities provide (Beets & Beets, 2019). From a shareholders’ perspective, these one-sided disclosures mean that political spending information can be scattered across many separate filings from different sources, making the collection of corporate political spending costly and time-consuming (Jia et al., 2021).

Conversely, firms may need to exhibit greater political transparency as more and more stakeholders are clamoring for more political transparency. Currently, shareholder proposals on PSD are among the leading proposals submitted to the SEC and are the most commented-on proposals in the SEC’s history, with roughly 1.2 million comment letters (Goh et al., 2020). Exhibiting PSD enables firms to prove their political accountability, ethical behavior, and CPR to various stakeholders and helps in reducing information asymmetry and cost of debt (DeBoskey et al., 2021; Lyon et al., 2018). Supporting this view, Werner (2017) documents a positive investor reaction to PSD because of reduced information asymmetry about corporate political expenditures. Notably, various corporations including Facebook, Amazon, and Microsoft exhibited greater PSD after the violent incidents at the U.S. Capitol on January 6, 2020 (BBC, 2021). This change indicates that firms review and amend their political donations and transparency policies to deal with external environmental needs and to gain shareholders’ support (Hillman & Hitt, 1999; Sutton et al., 2021; Yoffie, 1987). Therefore, if corporate political spending makes firms vulnerable to agency costs, firms’ PSD can help to eliminate this vulnerability and to tighten relationships with the external environment.

Hypothesis Development

The following hypotheses address how board’s monitoring and advising roles shape the likelihood that a firm will increase its political transparency. In terms of directors’ monitoring role, we examine female monitoring directors, board tenure, AC size, AC meetings, and AC education, as board characteristics related to the directors’ ability to monitor corporate political spending through demanding greater PSD. In terms of directors’ resource advising role, we look at female advisory directors, CEO duality, additional directorships, AC size, AC meetings, younger AC age, and AC education, as board characteristics related to directors’ ability to provide increased access to additional resources through advising on exhibiting greater PSD.

Female Monitoring and Female Advisory Directors

Female directors enhance board effectiveness by increasing managerial oversight and bringing a diverse range of ideas, views, perspectives, and skillsets (Hoobler et al., 2016). Indeed, prior research shows that female board representation is associated with better firm performance (Post & Byron, 2015), and stronger business and equity practices (Glass & Cook, 2018). Similarly, female directors are more likely to advance socially responsible practices because their psychological characteristics, backgrounds and experiences, and leadership styles and beliefs make them more likely to consider stakeholder interests (Cook & Glass, 2017; Galbreath, 2018). In their significant roles in enhancing firm value and promoting positive change (Glass & Cook, 2018), female directors, like all board members, perform both monitoring and advisory roles on boards.

Female directors may exercise their monitoring role by sitting on monitoring committees, such as audit, compensation, nomination, and governance, and dedicate substantial time to oversight (Post & Byron, 2015; Zalata et al., 2019). From an agency perspective, female directors may improve board monitoring as they are not part of the “old-boys’ club,” which makes them inherently independent directors (Zalata et al., 2019). Indeed, rigorous meta-analytic studies indicate that, compared with men, females have more stringent ethical standards, tend to report unethical behaviors and become internal whistle-blowers, and are more likely to challenge the management and demand transparent information (Pan & Sparks, 2012; Post & Byron, 2015). In this case, the stronger ethical standards of female directors are expected to translate into stronger monitoring capabilities that reduce agency costs (Post & Byron, 2015). Also, women are more likely than men to need higher credentials to advance into leadership positions because they face greater levels of public scrutiny (Cook & Glass, 2017). Consequently, female directors tend to have MBAs and doctorate degrees, which are associated with a greater commitment to ethics and transparency, including those associated with corporate political activity. Given female directors’ superior monitoring ability to detect corporate threats and their broader care for stakeholders’ concerns (Galbreath, 2018), female monitoring directors can transform the discreditable nature of corporate political activity into responsible behavior through PSD.

Hypothesis 1a (H1a): Female board members who are performing their monitoring roles will promote PSD.

Female directors exercising their advisory role may sit on advisory committees such as investment, finance, risk, and strategy, provide strategic counseling to the firm’s executives, and engage in decision-making on how firms compete in the marketplace (Faleye et al., 2011; Post & Byron, 2015). Drawing on resource dependence theory, Hillman and colleagues (2009) argue that female directors provide strategic counseling by bringing valuable resources, including expertise, creativity, commitment, and diversity of thinking. Indeed, firms appoint female directors not only to benefit from their legitimacy but also to take advantage of their unique advice and counsel (Post & Byron, 2015). Consistent with resource dependence theory, female directors bring strategic resources to their boards, generate new ideas, promote responsible practices, and improve corporate transparency (Lawati et al., 2021; Turrent, 2021). For example, compared with their male counterparts, female directors are more likely to bring a set of societal interests that include philanthropy and community service (Cook & Glass, 2017). Bringing these resources to corporate political activity, along with their propensity for community orientation, female advisory directors are more likely to advance responsible practices related to political ethics. Hence, we predict that female directors may advise top management to enhance firm’s PSD because it strategically relieves shareholders’ apprehensions about corporate political spending. Formally:

Hypothesis 1b (H1b): Female board members who are performing their advisory roles will promote PSD.

Board Tenure

Drawing on agency theory, we argue that longer board tenure reduces PSD because long-tenured directors have lower monitoring capabilities. The empirical results concerning the impact of director tenure on a board member’s monitoring capabilities have been inconclusive. According to the expertise hypothesis, long-tenured boards, (i.e., boards with members who have a long tenure) have more experience and understanding of their firms’ policies, monitoring processes, and internal capabilities (Katmon et al., 2019). Nonetheless, Chen (2013) argues that long-tenured boards are less likely to pursue innovative initiatives, as they tend to be risk-averse. Similarly, Katmon and colleagues (2019) argue that long-tenured directors tend to repeat the same processes, as long service on a board keeps them in their comfort zone; thus they tend to produce the same informational content. Likewise, directors’ independence deteriorates with longer tenure because long-tenured directors often form significant social ties or friendships with management, which compromises their monitoring capability and increases information asymmetry and agency problems (V. Sharma & Iselin, 2012). Given these findings, we argue that boards with longer tenured directors will resist supporting PSD, a new and emerging corporate disclosure practice, because it pushes the directors outside their comfort zone (DeBoskey & Luo, 2018; Katmon et al., 2019). Formally:

Hypothesis 2 (H2): Boards with longer tenured directors are less effective as monitors and as a result less likely to support PSD.

CEO Duality

The independence of the board can be impaired when the CEO chairs the board (de Villiers et al., 2011). According to agency theory, the concentration of power in the CEO can minimize the board of directors’ monitoring function and enable the CEO to engage in opportunistic behavior or irresponsible corporate behavior, which can inhibit CPR (Jensen & Meckling, 1976). As CEO duality implies a concentration of power in management and a reduction in the control of shareholders exercised by the board of directors, corporate decisions are more likely to benefit the managers rather than shareholders who are demanding greater political transparency (Husted & Sousa-Filho, 2019). Thus, boards with CEO duality are expected to have weaker monitoring capabilities, which results in less transparent PSD and more agency problems in the form of increased information asymmetry. Relatedly, prior literature shows that CEO duality is associated with lower environmental, social, and governance reporting (Husted & Sousa-Filho, 2019), forward-looking financial disclosures (M. Wang & Hussainey, 2013), and earnings forecasts disclosure (Lakhal, 2005). Similarly, and given the inherently unfavorable implications of publicly disclosing corporate political spending and the possible opportunistic nature of powerful CEOs, we surmise that CEO duality will reduce PSD. Formally:

Hypothesis 3 (H3): CEO duality leads to weaker monitoring capabilities and therefore, less PSD.

Board Busyness

Although additional directorships may lead to unfavorable consequences, such as director overload (V. Sharma & Iselin, 2012), the resource dependence theory supports the favorable implications of additional directorships (de Villiers et al., 2011); directors accumulate precious insights from their external experiences. Consistent with the reputation effect of busy directors, additional directorships foster directors’ advising capabilities because directors can gain additional insights and experience from serving on other boards (Elnahass et al., 2020).

We argue that companies with busier directors will demand more PSD, as busier directors may have experienced CPR or other forms of responsible behaviors in their service on other boards (Beji et al., 2021; Rupley et al., 2012). For example, busy directors might have gained experience of political crises and the effects of such crises on firm reputation, stakeholders, and financial performance. Drawing on resource dependence theory, we argue that the connections of busy directors enable them to experience valuable and multi-dimensional experiences (including political advising and reporting experiences) from their additional directorships, which provides them with the skills and incentives to seek corporate legitimacy from society (Lawati et al., 2021). Furthermore, in light of the significant increase in the percentage of S&P 500 firms that exhibit PSD (Ali et al., 2022), busy directors may proactively promote a firm’s political transparency with an eye to public perception to access public resources and enhance firm reputation. 9 Therefore, busy directors will be more likely to bring light and transparency to corporate dark money and be conversant about the competitive advantages that firms may obtain from CPR. Furthermore, given busier directors’ expanded networks, they may have more political interactions than their counterparts, which makes them resource-rich political capital who care about CPR. Formally:

Hypothesis 4 (H4): Busier board members will be stronger board advisors and advocate for PSD.

Audit Committee Size

According to the agency theory, the larger the AC committees are, the more intense the monitoring of management will be, in turn fostering management’s accountability to exhibit transparent disclosure policies to reduce agency costs. Accordingly, Bédard and colleagues (2004) argue that larger ACs are more likely to have credible monitoring to unveil possible issues in the financial and non-financial reporting. Larger ACs promote more effective oversight and monitoring over several reporting dimensions, including corporate social responsibility disclosures (Appuhami & Tashakor, 2017), intellectual capital disclosures (Li et al., 2012), and integrated reporting (Raimo et al., 2021). Hence, larger ACs can increase the monitoring capabilities of AC directors over corporate political activity through PSD, reducing agency costs.

Resource dependence theory suggests that larger ACs accumulate various experiences and perspectives to prudently counsel the board and respond to the changing needs of the outside environment (Lawati et al., 2021). Since larger boards bring more experience, more knowledge, and superior advice, they tend to include experts on specific issues such as corporate political affairs or directors who have been exposed to CPR (de Villiers et al., 2011). Furthermore, the uncertainty of the opportunities (and threats) associated with corporate political activity could prompt corporations to seek political expertise by appointing more directors on ACs. Given various stakeholders’ significant need for information on PSD, larger ACs will satisfy stakeholders’ needs regarding the firm’s political spending. The more directors that are on the AC, the more diversity, expertise, and accumulated knowledge there is to promote ethical behavior regarding corporate political activity and CPR and to ensure access to critical resources. Formally:

Hypothesis 5 (H5a): The size of the AC leads to board members exercising their monitoring and advisory roles more effectively so that they will support PSD.

Audit Committee Meeting Frequency

Since AC meetings are the heart of AC work, AC members should allow sufficient time for these meetings as full discussions are needed (Li et al., 2012). Furthermore, AC meeting frequency signals the AC’s diligence and commitment to remaining vigilant and informed. Therefore, ACs that meet more frequently have more time to execute their monitoring and advising functions over corporate reporting (Karamanou & Vafeas, 2005).

Prior studies on the frequency of AC meetings consistently show that frequent meetings enhance firms’ transparency and responsibility (Jizi et al., 2014; Karamanou & Vafeas, 2005; Li et al., 2012; Raimo et al., 2021). According to agency theory, more frequent AC meetings imply high-level oversight of all corporate reporting issues, including PSD. In response to the inherently opportunistic and speculative nature of corporate political activity, AC directors may devote a considerable portion of their monitoring to corporate political spending to address issues related to political transparency. Likewise, in their role within resource dependence theory, active ACs have greater awareness of changing business needs and the complexity of corporate political activity, and they can leverage their diverse skills, knowledge, and experience to enhance CPR. Since PSD has drawn significant attention from various stakeholders, active ACs can advise firms on how to promote CPR through PSD. Formally:

Hypothesis 5a (H5b): AC meeting frequency enables board members to exercise their monitoring and advisory roles more effectively so they will support PSD.

Audit Committee Age

Directors’ age is a critical corporate governance factor, as younger directors tend to provide unconventional and inspiring proposals (Adegbite, 2015; Giannarakis et al., 2020). Psychologically (Vroom & Pahl, 1971), older individuals tend to have risk-averse attitudes. Similarly, Katmon and colleagues (2019) argue that while older directors can be relatively reluctant and cautious with regard to risky decisions, younger directors have a positive attitude toward risk-taking. Consistent with resource dependence theory, Vroom and Pahl (1971) argue that since younger board members received their education recently, they have advanced technical knowledge, are familiar with changing business needs, are considered a rich source of innovative ideas, and are more capable of performing their advising duties diligently. Nevertheless, older directors are found to have superior negotiation and communication skills, more extensive networks and greater experience, and a more mature understanding of organizational behavior, which allows them to play an important role in managing risk appetite (Sultana et al., 2019).

Regarding PSD, while PSD reduces information asymmetry, it also triggers reputational risk and scrutiny (Goh et al., 2020). We argue that older AC directors can be reluctant to increase PSD because of their conservatism, which hinders the dissemination of risky information, such as PSD (Prabhat & Primo, 2019). According to resource dependence theory, younger AC directors—who offer fresh perspectives, have more positive attitudes toward risky proposals, and are more familiar with recent trends in corporate social responsibility, such as CPR—will be more likely to transparently communicate such risky political information. Formally:

Hypothesis 5c (H5c): Younger board members who are part of the AC committee are likely to be advisors willing to take risks and are more likely to support newer initiatives such as PSD.

Audit Committee Education

Chiang and He (2010) demonstrate that board education is the most critical element in fostering a firm’s transparency and argue that ACs with higher educational levels are more likely to ensure trustworthy information disclosure. Moreover, corporate governance guidelines underscore AC members’ need for continuing education to handle emerging problems and knowledge gaps and implement corporate best practices. Prior research provides evidence that directors’ educational level is positively associated with transparent disclosure policies and public accountability (Beji et al., 2021; Elmagrhi et al., 2019; Post et al., 2011; Reeb & Zhao, 2013).

According to agency theory, more educated directors have superior monitoring capabilities, higher ethical standards, and more rigorous oversight behaviors that enable them to monitor managers effectively (Hillman & Dalziel, 2003). Hence, highly educated AC directors can serve as a robust corporate governance monitoring mechanism over corporate political spending and can reduce agency costs by demanding greater PSD. Similarly, resource dependence theory argues that board education level is associated with innovative ideas, unique solutions to problems, and awareness of recent responsible practices (Beji et al., 2021; Elmagrhi et al., 2019). Educated directors are held to higher professional standards, have superior understanding of the legal environment, and are more able to handle politically sensitive endeavors such as PSD. Their professional status enables them to relate to diverse social networks and to have intellectual zones where corporate political affairs are discussed, which makes them more cognizant of CPR as an emerging responsibility domain. Accordingly, AC directors’ education can enhance their political awareness regarding the importance of CPR and motivate them to advise their firms to exhibit PSD to gain strategic political advantage and secure access to critical resources. Formally:

Hypothesis 5d (H5d): More educated board members who are part of the AC committee are more likely to exercise their monitoring and advisory roles and support PSD.

Research Methodology

Data and Sample

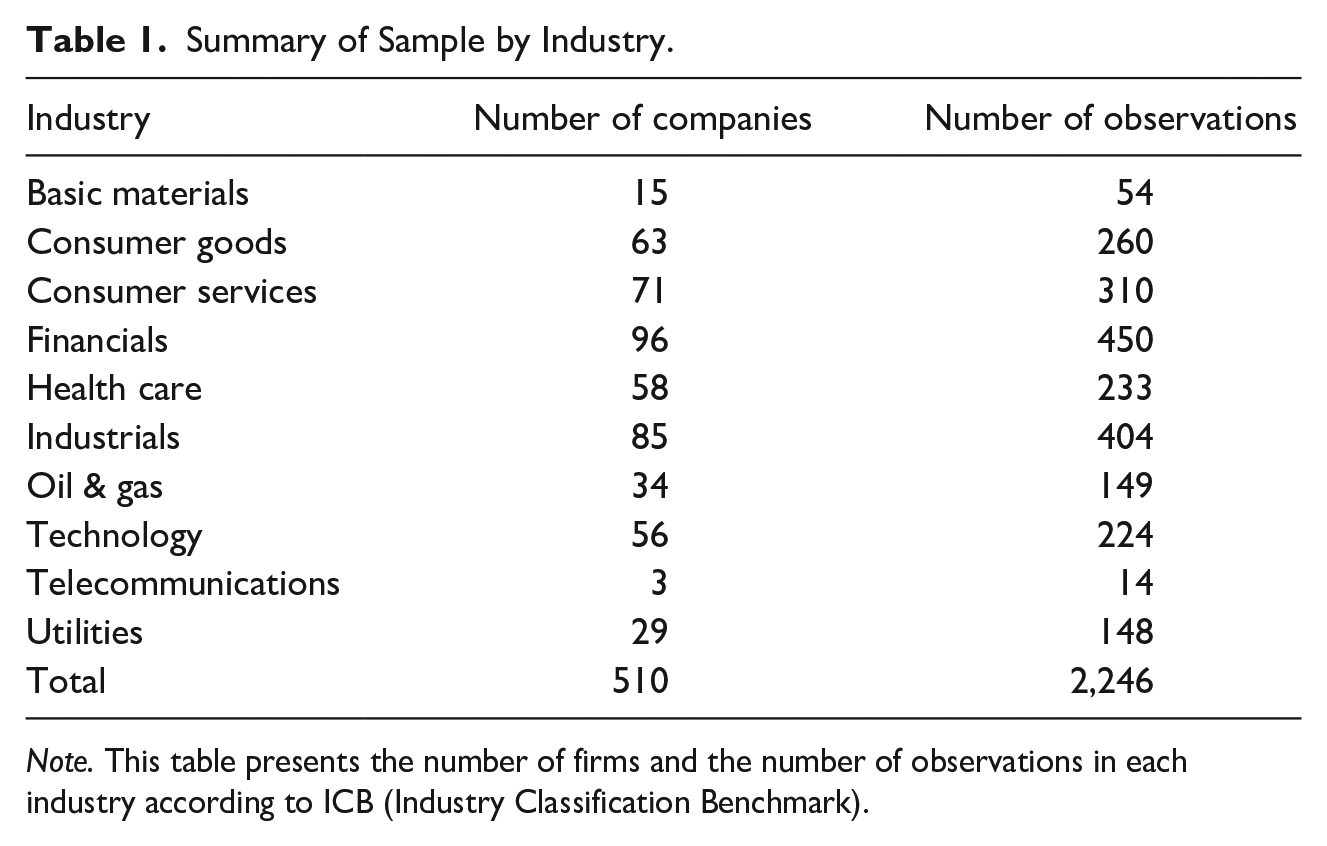

The initial sample includes all publicly traded firms in the S&P 500 index with available corporate political accountability data in the CPA-Zicklin Center from 2011 to 2019. Our sample starts from 2011, as this is the first year in which the PSD index was available. 10 It ends with 2019, with the most recent data at the time of analysis. Data regarding female monitoring and advisory directors, AC age, and education were collected from BoardEx. To the extent that biographical data were incomplete on BoardEx, we conducted an exhaustive internet search and used alternative sources, including LexisNexis Academic, Complete Marquis Who’s Who (R) Biographies, MarketScreener, Bloomberg personal profiles, directors’ LinkedIn, Business Wire, proxy statements, and Official Board Biographies. Finally, we merged these data with financial and governance data obtained from Bloomberg. After we exclude companies with missing data, companies not covered by the CPA-Zicklin database, and outlier observations identified by the DFFITS test (Belsley et al., 1980), the final sample consists of 510 firms (2,246 firm-year observations.) Table 1 exhibits the number of companies within industries.

Summary of Sample by Industry.

Note. This table presents the number of firms and the number of observations in each industry according to ICB (Industry Classification Benchmark).

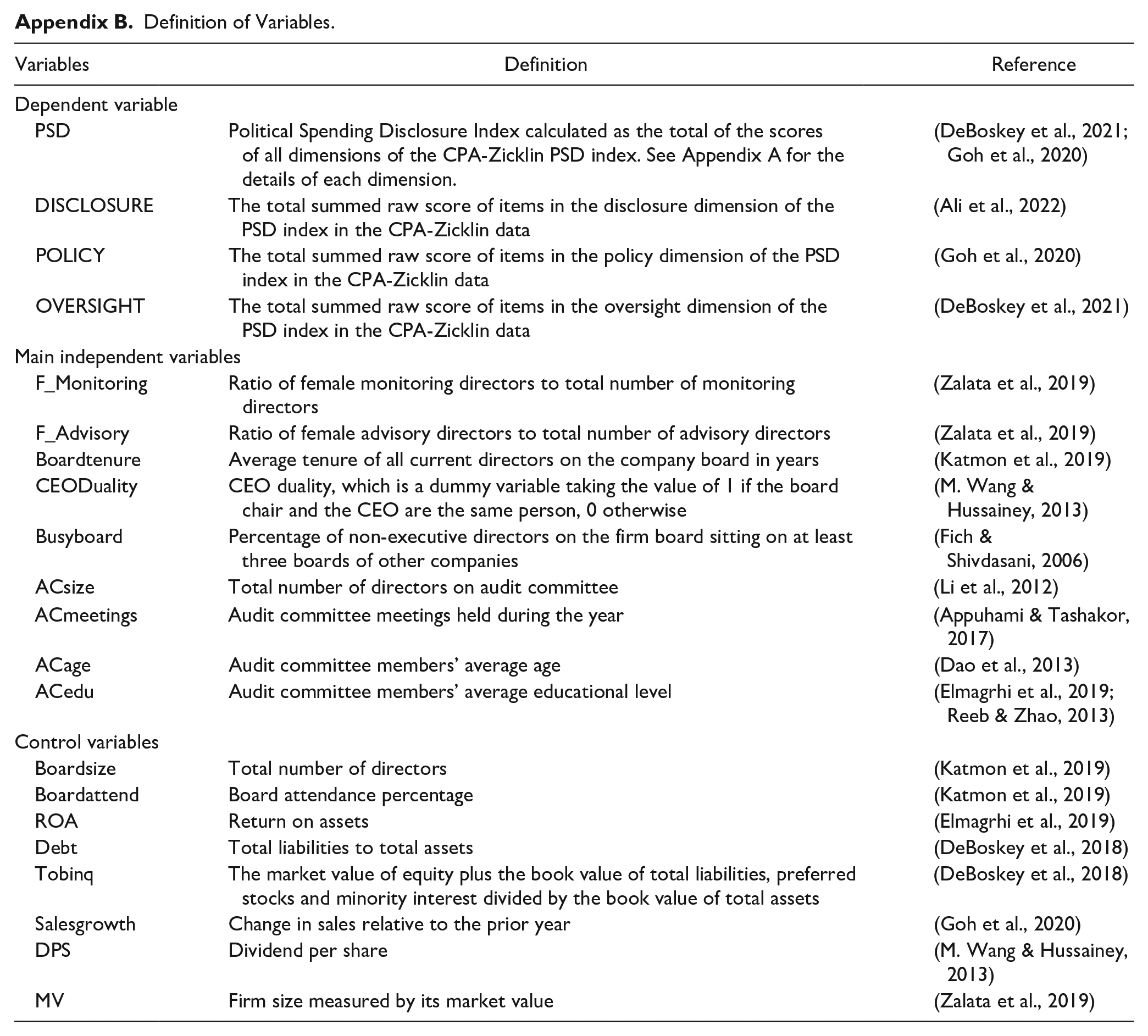

Measurement of Variables

Dependent Variable: PSD

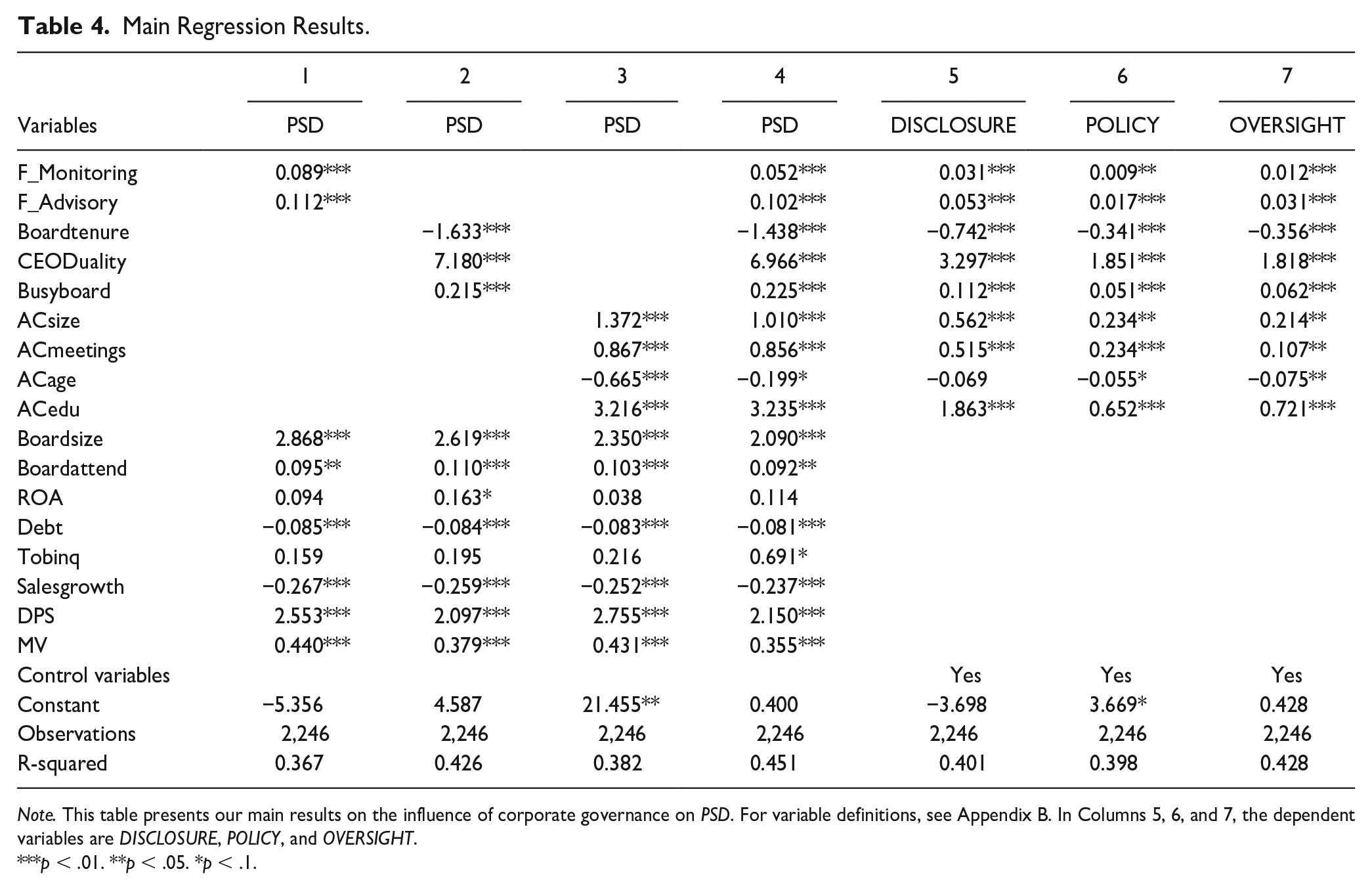

Employing the CPA-Zicklin Index (Ali et al., 2022; Baloria et al., 2019; Cohen et al., 2019; DeBoskey et al., 2018, 2021; Goh et al., 2020), which is a distinctive dataset supplied by a joint collaboration of the Carol and Lawrence Zicklin Center for Business Ethics Research at the Wharton School of the University of Pennsylvania and the Center for Political Accountability, we calculated the PSD index for each firm. The index is based on 24 items that are grouped into three main dimensions: disclosure, policy, and oversight. The Disclosure sub-index includes firms’ disclosure of political donations to government associations, tax-exempt organizations, trade associations, political parties, or any political entity. The Policy sub-index includes firms’ disclosure of their policies regarding political spending and the types of recipients the firms deem acceptable. The Oversight sub-index includes the standards of the board committees that review and approve firms’ political spending, the public production of the political spending report, and the adoption of internal measures to ensure compliance with policy. Appendix A presents all the PSD index components and score assignments. Correspondingly, we computed the PSD variable by summing up all points awarded in the three categories of disclosure, policy, and oversight. Following prior research (Ali et al., 2022; Goh et al., 2020), we focused on the aggregate CPA-Zicklin index because each dimension includes different forms of political transparency. For example, the disclosure dimension represents the disclosure of political spending itself. Similarly, the policy dimension captures the transparency of political spending policies. Likewise, the oversight dimension proxies the transparency of the oversight mechanisms that govern political spending. Therefore, the aggregate PSD index is a comprehensive measure of political transparency. Nevertheless, we re-perform our analysis using the three dimensions separately. The results for disclosure, policy, and oversight dimensions are in Columns 5, 6, and 7, respectively, of Table 4. The results are generally consistent with the overall PSD index.

Monitoring and Advisory Female Directors

Board committees can typically be classified into either monitoring committees (such as audit, nomination, compensation, and governance committees) or advisory committees (such as investment, finance, risk, and strategy committees). Since directors often sit on several board committees, we follow Zalata and colleagues (2019) and Faleye and colleagues (2011) in defining a monitoring director as a person sitting on at least two of the four major monitoring committees. As mentioned by Faleye and colleagues (2011, p.164), the majority of directors usually sit on a maximum of two committees; therefore, directors sitting on two committees are unlikely to sit on other committees. Namely, a great proportion of their work is monitoring-related. Subsequently, we identify a female director as monitoring if she serves on two or more of the four monitoring committees. Consequently, we calculate (F_Monitoring) as the ratio of monitoring female directors to the aggregate number of monitoring directors. 11

A director can be defined as an advisory director if he or she does not sit on any monitoring committee, especially the AC (Hsu & Hu, 2016). Specifically, we follow Zalata and colleagues' (2019) and Faleye and colleagues’ (2011) holistic definition and classify a female director as advisory if she does not sit on any monitoring committee. Accordingly, we calculate (F_Advisory) as the ratio of female advisory directors to the aggregate number of advisory directors.

Tenure, CEO Duality, and Board Busyness

Board tenure is identified as the length of time directors serve on board positions (Katmon et al., 2019). Accordingly, we define (Boardtenure) as the average tenure, in years, of all current directors on the board. We define (CEODuality) as a binary variable taking the value of 1 if a single person serves as the CEO and board chair simultaneously, 0 otherwise (M. Wang & Hussainey, 2013). Fich and Shivdasani (2006) define a director as busy if he or she sits on three or more boards. Accordingly, we define (Busyboard) as the percentage of non-executive directors who sit on at least three boards.

Audit Committee Variables

We define (ACsize) as the number of directors who serve on the AC (Li et al., 2012). We define (ACmeetings) as the number of meetings conducted by the AC during the fiscal year (Al-Shaer & Zaman, 2018). We define (ACage) as the average age of AC members (Dao et al., 2013). In defining AC educational level, we follow prior studies in constructing education scores (Elmagrhi et al., 2019; Pérez-Cornejo et al., 2019; Reeb & Zhao, 2013) of 0, 1, 2, and 3 if a director has no university education, an undergraduate degree, a master’s degree, and a doctorate degree, respectively. We also consider the director’s attainment of professional qualifications such as Certified Public Accountant, Chartered Financial Analyst, or Certified Management Accountant by giving each qualification a value of 1. We then add these scores for each director-level observation in each firm in each year. Finally, we define (ACedu) as the average education score of AC directors. 12

Empirical Equation

We use the following ordinary least squares multivariate regression with robust standard errors to consider possible heteroscedasticity and serial correlation:

Appendix B elaborates definitions and measurements. We control for firm-level characteristics that may affect PSD, including board size (Boardsize), board attendance percentage (Boardattend), profitability (ROA), debt (Debt), growth opportunities (Tobinq), dividend per share (DPS), firm size (MV), and sales growth (Appuhami & Tashakor, 2017; Goh et al., 2020; Katmon et al., 2019; M. Wang & Hussainey, 2013). Finally, we control for year and industry effects. All continuous variables are winsorized at 1st and 99th percentiles.

Results

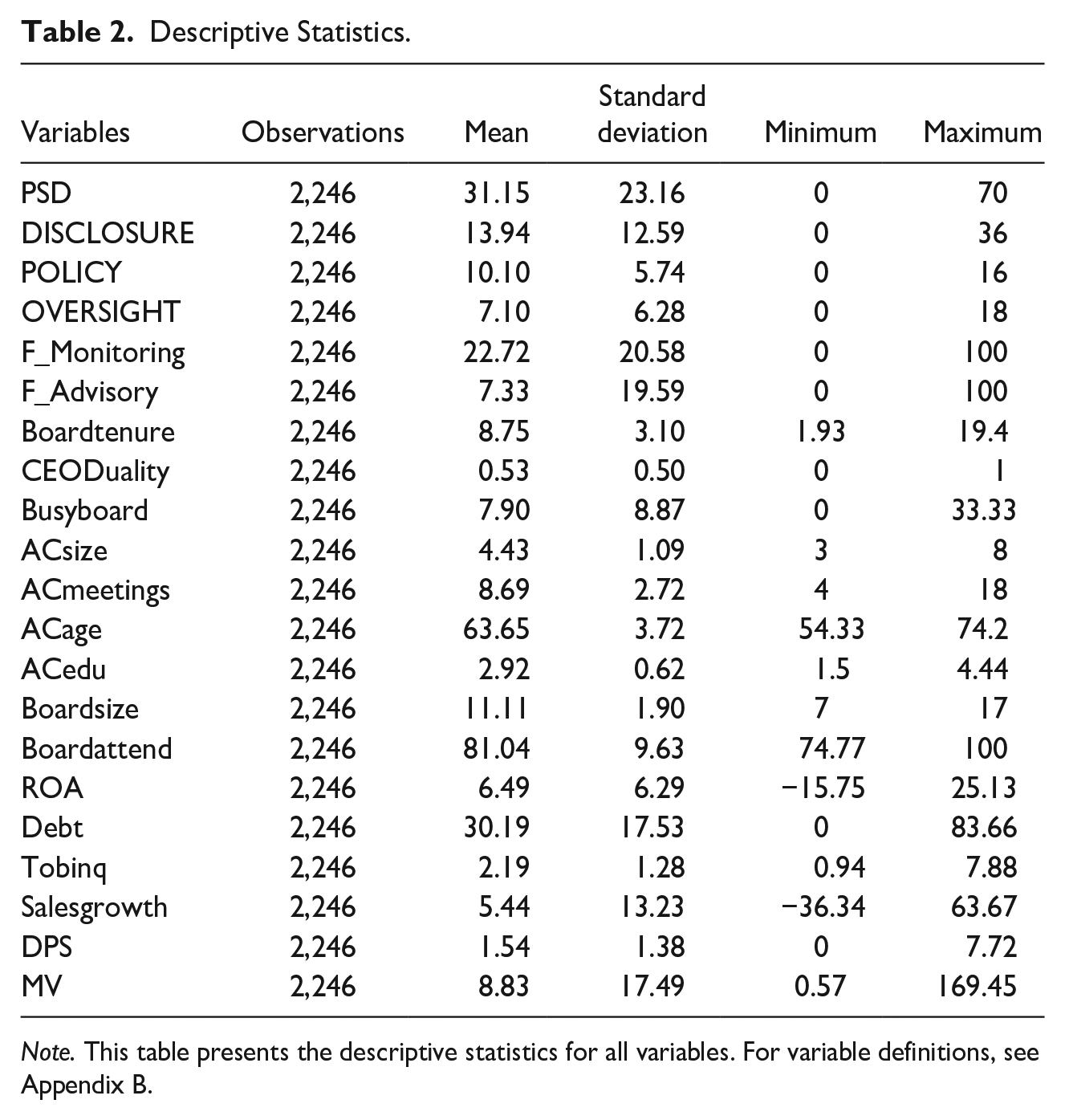

Table 2 shows that the PSD average is 31.15 and ranges between 0 and 70, indicating a considerably weak overall level of political spending transparency (approximately 44%), although there is considerable variation across companies. Of the three PSD Index dimensions, POLICY has the highest score, with an average of 63% (10.1 points out of 16). DISCLOSURE and OVERSIGHT are significantly lower in score, averaging 38.7% (13.94 points out of 36) and 39.4% (7.1 points out of 18), respectively. These statistics suggest that the disclosure of actual political donations and the oversight of the political spending process are substantially lower than the description of political spending policies. Such a high score in POLICY and such low scores in DISCLOSURE and OVERSIGHT could imply a symbolic application of transparent political spending policies.

Descriptive Statistics.

Note. This table presents the descriptive statistics for all variables. For variable definitions, see Appendix B.

F_Monitoring and F_Advisory have averages of 22% and 7%, respectively, implying that female directors generally serve on more monitoring committees than advisory committees. These results are comparable to those of Zalata and colleagues (2019), who report means of 14% and 6% for F_Monitoring and F_Advisory, respectively. The average of Boardtenure is 8.75 years, which is comparable to the result of Cai and colleagues (2014), who report an average tenure of 9 years. About 8% of directors are classified as busy directors ranging from 0% to 33%. Although SOX requires a minimum of three AC members, the ACsize mean is 4.43, indicating that AC size is considerably higher than the required minimum. ACage has a mean of 63 and ranges from 54.3 to 74.2. ACedu has an average of about three and ranges from 1.5 to 4.44, which suggests that most AC members have a graduate degree. 13

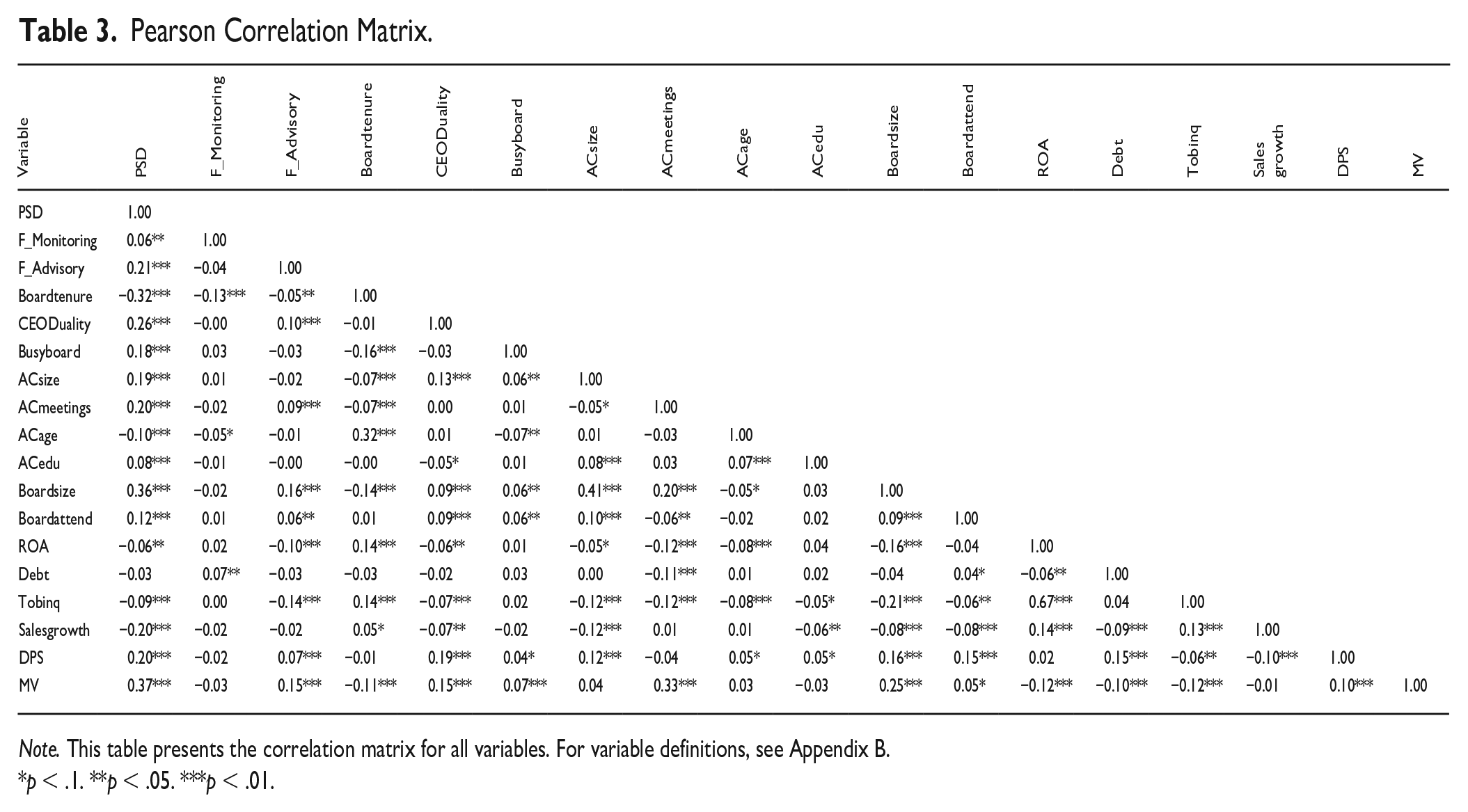

According to Table 3, PSD scores are positively and significantly correlated with the following variables: F_Monitoring, F_Advisory, CEODuality, Busyboard, ACsize, ACmeetings, and ACedu. In contrast, PSD is negatively and significantly associated with the following variables: Boardtenure, and ACage. Generally, there are low correlations among variables. We also computed variance inflation factors (VIFs) and found that the highest VIF is 1.92, suggesting no multicollinearity concern (Gujarati, 2003).

Pearson Correlation Matrix.

Note. This table presents the correlation matrix for all variables. For variable definitions, see Appendix B.

p < .1. **p < .05. ***p < .01.

Table 4 reports the results on the influence of corporate governance variables on CPR as measured by overall PSD. Columns 1, 2, and 3 report the findings of each category of independent variables, and Column 4 reports the findings of all independent variables in one model. Columns 5, 6, and 7 report the findings of each part of PSD including disclosure, policy, and oversight, respectively. The results remain generally consistent.

Main Regression Results.

Note. This table presents our main results on the influence of corporate governance on PSD. For variable definitions, see Appendix B. In Columns 5, 6, and 7, the dependent variables are DISCLOSURE, POLICY, and OVERSIGHT.

p < .01. **p < .05. *p < .1.

Column 1 of Table 4 shows that the coefficients of F_Monitoring and F_Advisory are positive and significant (p <.01), supporting H1a and H1b and the important roles that female directors play in promoting CPR as a new responsibility domain. Column 2 of Table 4 shows that Boardtenure is negatively associated with PSD (p < .01), which supports H2 and suggests some unfavorable implications of long-tenured boards from a corporate political transparency angle (Huang & Hilary, 2018). The results in Column 2 of Table 4 provide evidence that CEO duality enhances firms’ PSD (p < .01), suggesting that powerful CEOs can promote CPR of their firms to maintain their legitimacy and reputation. These results are inconsistent with our prior expectations in H3. The coefficient of Busyboard is statistically significant and positive (p < .01), supporting H4. This result lends empirical support to the reputation hypothesis of board busyness and provides evidence about some of the favorable implications of busy board members. Regarding AC variables, Column 3 of Table 4 suggests that a firm’s PSD is influenced significantly by ACsize, ACmeetings, ACage, and ACedu, all at the p < .01 level, supporting H5a, H5b, H5c, and H5d and suggesting that the monitoring and advising roles of AC could be extended to PSD. Overall, the results suggest that corporate governance plays a significant role in shaping CPR.

PSD is significantly higher for firms with larger boards (Boardsize), higher board attendance (Boardattend), larger size (MV), and higher dividends per share (DPS). However, the significant positive association between PSD and DPS should be considered with caution. If political donations attract a negative response from shareholders, firms may strategically increase dividends distributed to reduce such a negative response and to convince them that the firm is acting according to shareholders’ interests. Furthermore, PSD is significantly lower for firms with higher leverage (Debt) and higher sales growth (Salesgrowth). Other variables are insignificant.

Additional and Robustness Analysis

Different Proxies

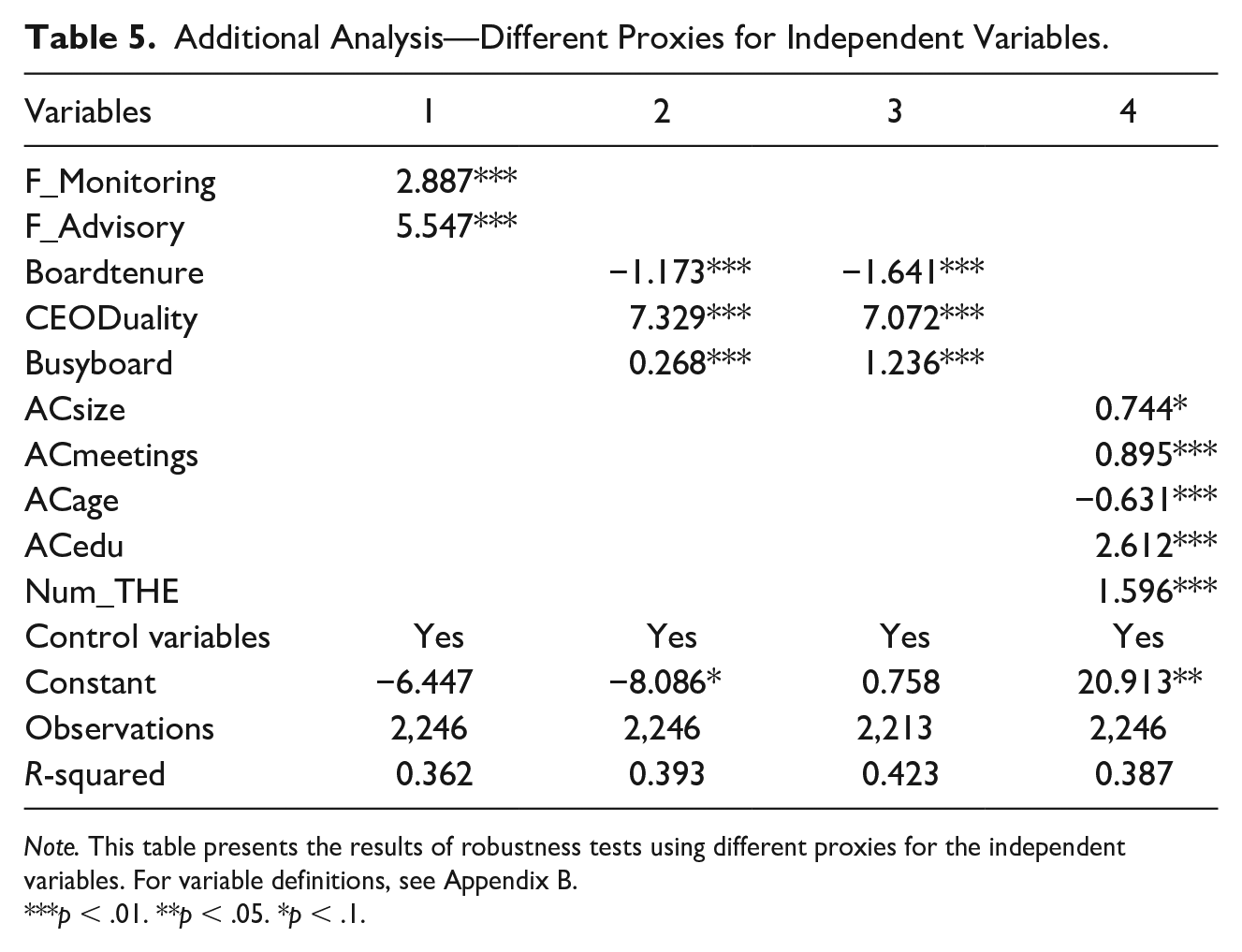

We test the influence of the presence of female monitoring and advisory directors on PSD. Specifically, F_Monitoring will equal 1 if the company has at least 1 female monitoring director, 0 otherwise. Likewise, F_Advisory will equal 1 if the company has at least 1 female advisory director, 0 otherwise. The findings in column 1 of Table 5 are consistent with the main analysis.

Additional Analysis—Different Proxies for Independent Variables.

Note. This table presents the results of robustness tests using different proxies for the independent variables. For variable definitions, see Appendix B.

p < .01. **p < .05. *p < .1.

Readers may be interested in examining AC female diversity influence on PSD. Since AC attributes (size, meeting frequency, age, and education) significantly influence firms’ PSD, AC gender diversity can significantly shape PSD. Consistent with prior studies (Appuhami & Tashakor, 2017; Bravo, Reguera-Alvarado, 2019), our untabulated results document a positive association between AC female directors and PSD.

We set Boardtenure to equal the percentage of board members who have been serving for 5 years or more. We argue that the higher this percentage, the greater the board tenure and the less PSD. The results in Column 2 of Table 5 confirm our main results: Long-tenured members are less politically transparent (Hidalgo et al., 2011). Furthermore, we rerun the model using the percentage of board members serving for 10 years or more, and the results (untabulated) still hold. Following de Villiers and colleagues (2011), we measure Busyboard by using the average number of directorships (i.e., the mean of board seats held by board members). The results, presented in Column 3 of Table 5, remain similar.

We are also interested in board members who have attended elite universities as they may obtain direct and indirect connections with the elite class (Reeb & Zhao, 2013). Accordingly, AC directors who attended elite educational institutions have stronger ties with the upper level of social classes and thereby may have significant influence on AC outcomes. Utilizing www.timeshighereducation.com, we include the number of AC board members who graduated from the top 10 elite universities as an additional education variable (Num_THE). In Column 4 of Table 5, we document a significant positive association (p < .01), providing original evidence that an elite university education benefits society by enhancing firms’ PSD. Since university ranking may not be unanimous across different ranking systems, we also used QS ranking. Noticeably, the correlation between the two ranking sources yields very high correlation of 0.95 and yields identical conclusions. We argue that AC directors who graduate from elite institutions have greater monitoring capabilities and more political awareness and are more likely to respond to stakeholders’ demand for greater political transparency. These findings are in line with prior studies, which argue that a CEO’s educational background plays a pivotal role in shaping a firm’s political investment (Rudy & Johnson, 2019).

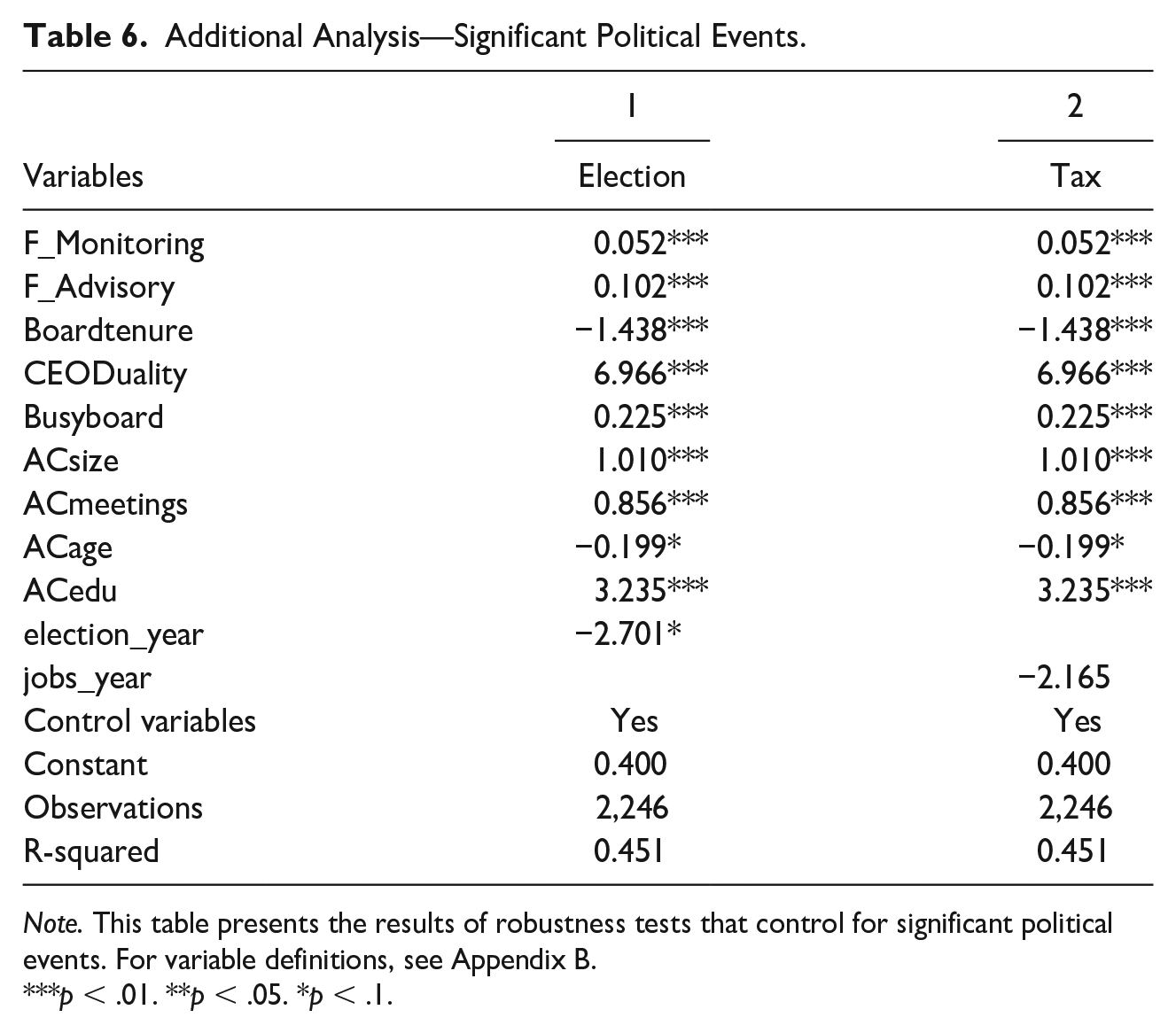

Significant Political Events

Given that political transparency is inherently tied to politics, we wanted to test whether significant political events affect our findings. For example, some corporations may increase their PSD in an election year due to increased media attention. Therefore, we include the election year of 2016, which equals 1 if the year is 2016, 0 otherwise. Likewise, given the enactment of the Tax Cuts and Jobs Act in 2017, we include a binary variable, which equals 1 if the year is 2017, 0 otherwise. These findings are reported in Columns 1 and 2 of Table 6, respectively. Our results remain unchanged. 14

Additional Analysis—Significant Political Events.

Note. This table presents the results of robustness tests that control for significant political events. For variable definitions, see Appendix B.

p < .01. **p < .05. *p < .1.

Corporate Political Activity

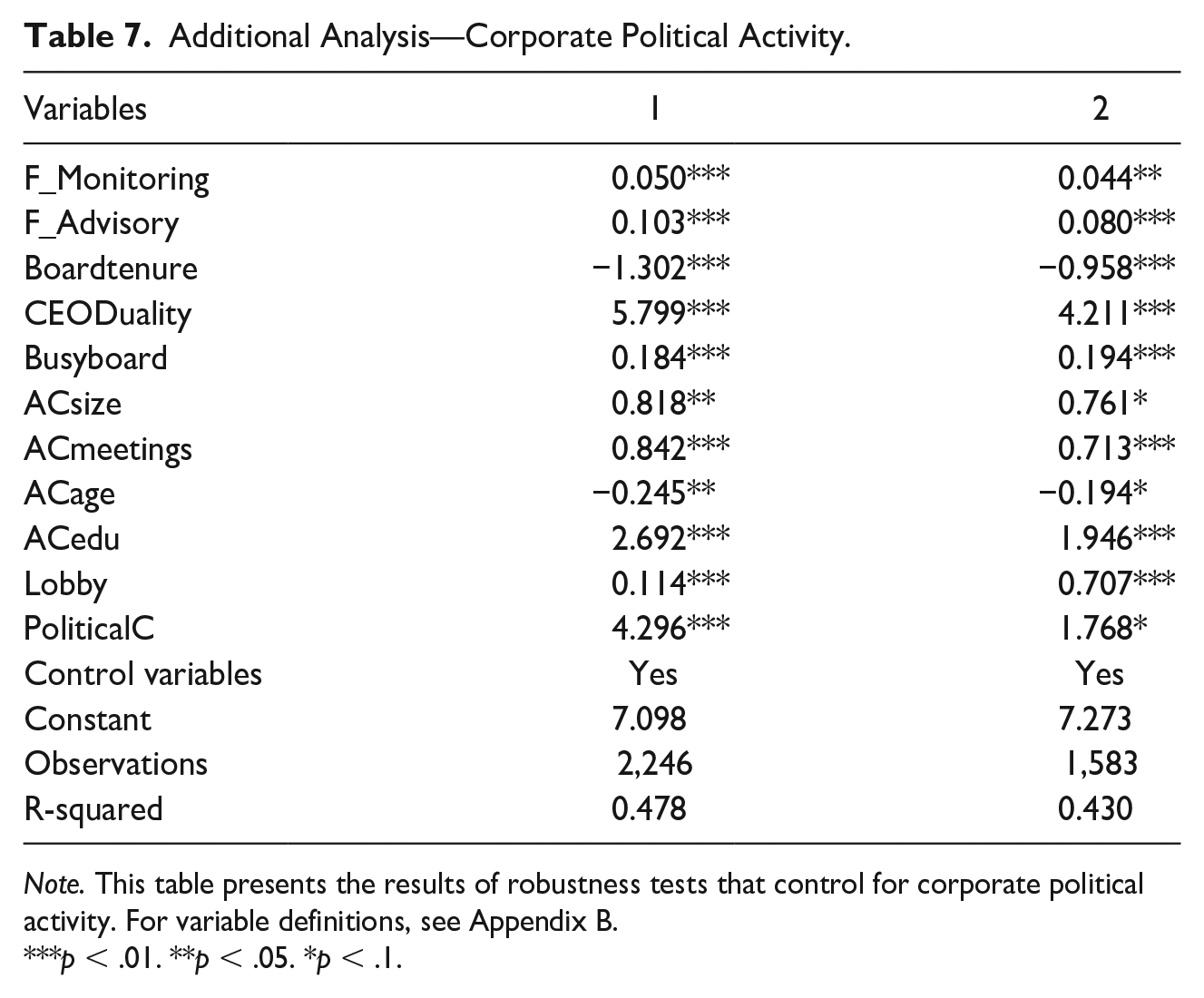

As the firm’s political transparency can be affected by its political involvement, we include two measures of a firm’s political participation. First, we include lobbying expenditures (Lobby), which we manually collected from the Center for Responsive Politics (OpenSecrets.org). Second, we include a firm’s political connections (PoliticalC), which equals 1 if board members have political connections, 0 otherwise. Using BoardEx data, we recognize board members who have a past or current relationship with the Republican or Democratic party or who have been members of Congress, the Senate, the White House staff, party-affiliated associations, or a campaign organization (Goh et al., 2020). The results, reported in Column 1 of Table 7, are unchanged. Furthermore, high-lobbying firms may exhibit higher PSD than low-lobbying firms. Given prior evidence that firms that lobby the most are the least transparent about their political spending (Schepers & Gardberg, 2011), we repeat the prior analysis by focusing only on high-lobbying firms (i.e., those whose lobbying expenditures are greater than the sample mean). The results, reported in Column 2 of Table 7, are unchanged.

Additional Analysis—Corporate Political Activity.

Note. This table presents the results of robustness tests that control for corporate political activity. For variable definitions, see Appendix B.

p < .01. **p < .05. *p < .1.

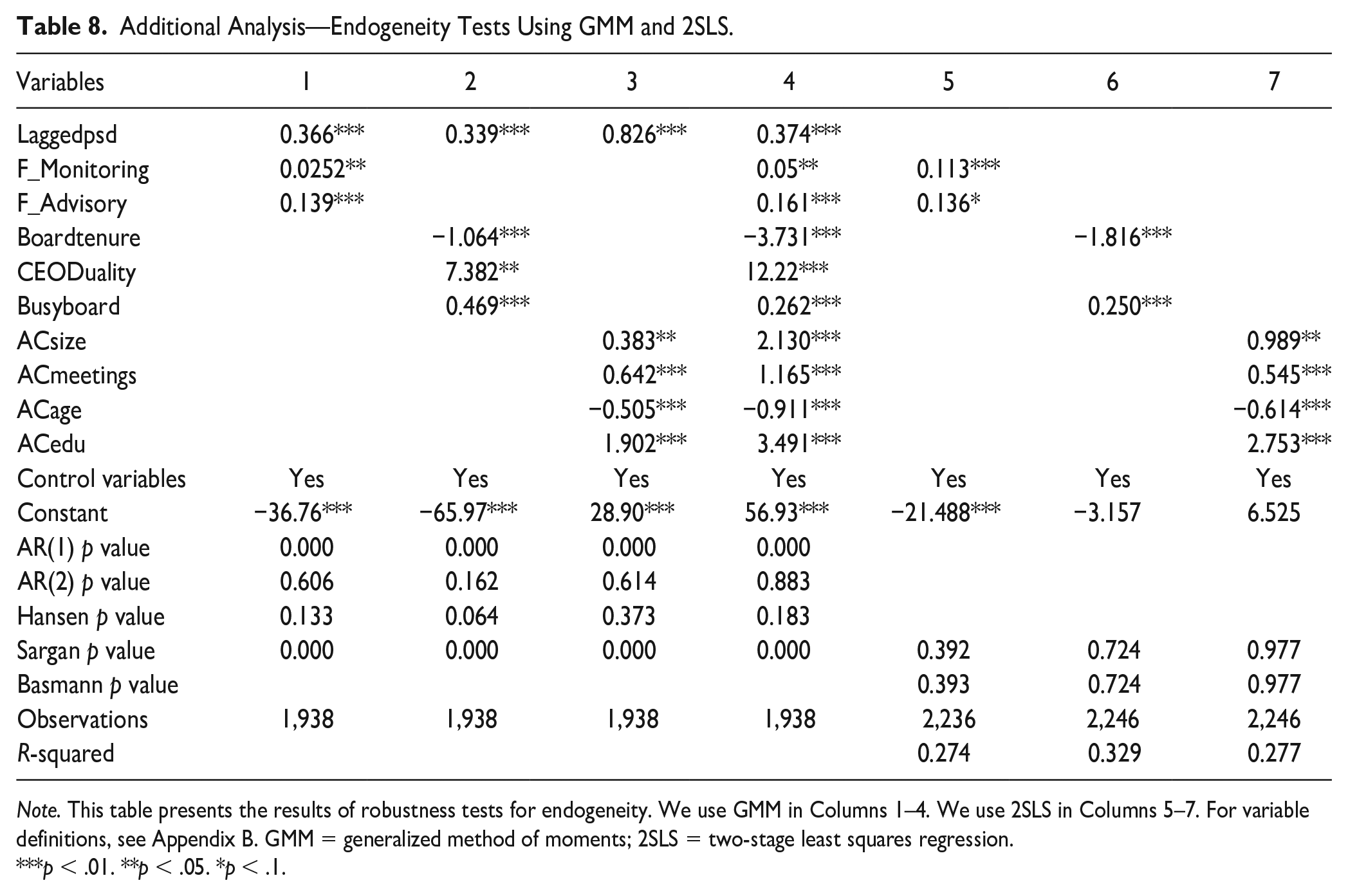

Endogeneity

We follow Elamer and colleagues (2020) and employ a dynamic two-step generalized method of moments (GMM) estimator to control for unobserved heterogeneity, simultaneity, and potential endogeneity problems. The results, reported in Columns 1 to 4 of Table 8, remain unchanged, suggesting that our results are robust to different endogeneity problems. All model specifications (AR1, AR2, and Hansen/Sargan tests) assert the model’s validity, the absence of second-order serial-correlation, and the instruments’ validity.

Additional Analysis—Endogeneity Tests Using GMM and 2SLS.

Note. This table presents the results of robustness tests for endogeneity. We use GMM in Columns 1–4. We use 2SLS in Columns 5–7. For variable definitions, see Appendix B. GMM = generalized method of moments; 2SLS = two-stage least squares regression.

p < .01. **p < .05. *p < .1.

We also perform two-stage least squares regression (2SLS) to consider possible endogeneities. Regarding F_Monitoring and F_Advisory, we use three instrumental variables. First, we use the percentage of female directors on the board in each industry. Since the appointment of female directors can be significantly influenced by the nature of the industry (Zalata et al., 2019), we conjecture that the appointment of female directors to monitoring roles or advisory roles depends on the female cluster in each industry. Second, we use the percentage of male monitoring directors. We argue that the appointment of male directors to monitoring roles affects the probability that the firm will appoint female directors to monitoring and advisory roles. Third, we use female chairperson as a dummy variable that takes the value of 1 if the firm’s chairman is female, 0 otherwise, based on the argument that if the firm’s chairman is female, this may increase the likelihood that the firm will appoint female directors to the board. We use the lagged values of Boardtenure and Busyboard as instrumental variables. Their lagged values are expected to influence their current-year values and are not expected to be correlated with current-year PSD (Husted, Sousa-Filho, 2019). Similarly, we employ the lagged values of ACsize, ACmeetings, ACage, and ACedu as instruments. The results in Columns 5 to 7 of Table 8 support the main analysis. Sargan and Basmann statistics confirm the instruments’ validity. 15

Discussion

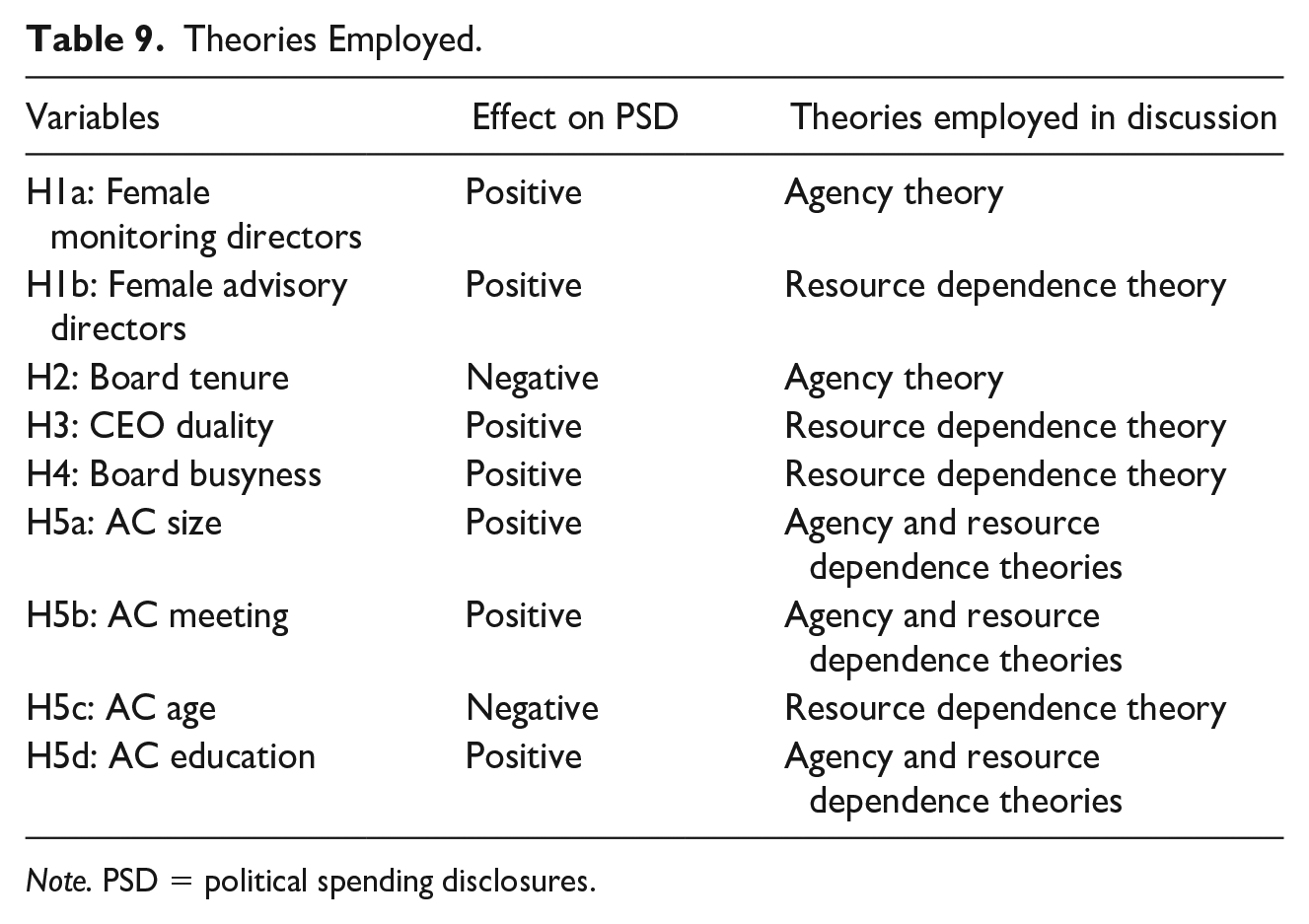

Recent research highlights the importance of CPR for reducing a firm’s agency problems and achieving strategic advantage (DeBoskey et al., 2021; Lyon et al., 2018). Given the unprecedented rise in corporate dark money, we investigate whether corporate governance influences PSD which is an important component of CPR. According to agency theory, corporate boards exercising their monitoring role have an incentive to promote political transparency. Our empirical results provide evidence that the monitoring role of the board emanating from female monitoring directors, shorter board tenure, larger AC size, more frequent AC meetings, and higher AC education increases a firm’s PSD. In addition, resource dependence theory suggests that the board performs its advisory role to secure access to critical resources by promoting PSD. Empirically, we show that the advisory role of the board emanating from female advisory directors, CEO duality, additional directorships, larger AC size, more frequent AC meetings, younger AC age, and higher AC education increases a firm’s political transparency. Table 9 outlines how we used our dual theoretical approach in explaining our results.

Theories Employed.

Note. PSD = political spending disclosures.

First, female monitoring directors significantly enhance PSD. This empirical finding is in line with prior studies showing that female directors enhance the board’s monitoring capabilities and enhance corporate social responsibility (Beji et al., 2021; Zalata et al., 2019). This result also confirms the claims of agency theory, which asserts that gender-diversified boards improve board monitoring effectiveness and increase managers’ accountability. These findings suggest that the strict ethical standards of female monitoring directors may reduce agency costs by promoting political transparency and subsequently improving a firm’s CPR. Next, we provide evidence that female advisory directors significantly increase PSD. According to resource dependence theory, female advisory directors may possess characteristics such as morality, diligence, and stakeholder orientation, which makes them inherently more effective advisors to their businesses (Turrent, 2021). In this case, we argue that female advisory directors respond to societal needs by pressuring firms to increase their political transparency. Given the ability of female directors to provide strategic counseling (Hillman et al., 2007), our findings suggest that appointing female directors to key advisory roles may enhance a firm’s CPR by increasing a firm’s PSD.

Second, board tenure is negatively associated with PSD. This result confirms previous research about the unfavorable implications of long board tenure (Huang & Hilary, 2018; V. Sharma & Iselin, 2012). Our result is consistent with agency theory in that long-tenured directors are less effective in monitoring managers with respect to new important strategic areas such as PSD. Furthermore, long-tenured directors may be more rigid and have more commitment to established practices, which makes them reluctant to embrace risky new endeavors; therefore, they may not promote PSD. Given the attendant unfavorable consequences of corporate political activity in general and PSD in particular (Prabhat & Primo, 2019), long-tenured directors may prefer their current stability over corporate political transparency.

Third, CEO duality is positively associated with PSD. Although this result is inconsistent with our expectation in H3, it supports the findings of other studies that found a positive relationship between CEO duality and corporate transparency concerning firm information (Donnelly & Mulcahy, 2008; Hidalgo et al., 2011; Jizi et al., 2014). For S&P 500 firms, it seems that when the same individual serves as both CEO and chairman, he or she favors PSD. Drawing from resource dependence theory, Pfeffer and Salancik (2003) argue that the duality role of CEOs fosters more flexible and dynamic leadership that facilitates organizational effectiveness and awareness of outside environment needs. Considering the serious activism of shareholders demanding greater political transparency (Mithani, 2019), CEOs who have dual roles are in a better position to advise their firms with strategic political advice because of their firm-specific political knowledge and are more likely to respond to demands for more political transparency, ensuring their continuous access to resources, legitimacy, and reputation. Alternatively, it could be that CEO power associated with CEO duality may motivate them to increase PSD to enhance their reputation and prestige (Walls et al., 2012). Overall, we extend resource dependence theory arguments and claim that increased CEO power through CEO duality may provide CEOs with opportunities to better advise their companies about the importance of CPR.

Fourth, board busyness increases PSD, lending empirical support to the reputation hypothesis of busy boards (Elnahass et al., 2020; D. Sharma et al., 2020; Trinh et al., 2020). We argue that busy directors respond to stakeholders’ increased interest in enhancing corporate political accountability by increasing PSD. Our results complement those of prior studies (Beji et al., 2021; de Villiers et al., 2011), demonstrating that busy directors enhance environmental responsibility, human performance, and business ethics. In this respect, we contend that busier directors show that they care about CPR by implementing PSD. Extending resource dependence theory, we argue that board interlocks allow directors to accumulate various political experiences from other firms and experience new forms of corporate responsibility, which enables them to provide strategic advice to their firms on recent responsible behaviors including CPR. The richer experiences of busy directors and their diverse interactions with several socially responsible companies can promote CPR and inspire the board to seriously consider illuminating corporate dark money.

Fifth, we provide evidence on the positive influence of AC size on PSD. This finding is consistent with agency theory, which asserts that monitoring by larger ACs enhances the veracity of PSD and reduces information asymmetry. Theoretically, enhanced managerial monitoring associated with larger ACs has a positive effect on corporate disclosures and financial reporting quality and can reduce agency costs (Beasley et al., 2009; Jensen & Meckling, 1976; Li et al., 2012). We argue that companies with larger ACs are more effective in performing their supervision and monitoring responsibilities; hence, firms’ political accountability and transparency improve. Likewise, resource dependence theory suggests that larger ACs imply greater diversity of directors, richness of knowledge and expertise, and openness to new responsible endeavors. Building on that, larger ACs are more capable of advising senior management on “new” responsible behaviors such as CPR. Thus, larger ACs can signal their responsiveness to stakeholders who demand increased PSD, which helps firms to obtain better access to politicians and financial resources; in this way, larger ACs help the board fulfill its resource-provision role (DeBoskey et al., 2021).

Sixth, AC meeting frequency is positively associated with PSD. This lends empirical support to prior studies showing that AC meeting frequency is associated with higher financial reporting quality and transparency (Jizi et al., 2014; Li et al., 2012; Raimo et al., 2021). Consistent with agency theory, active ACs are more likely to hold managers accountable for corporate political spending and reduce political opportunism. Given the serious demands to shed some light on corporate dark money, active ACs may enhance the decency of corporate political activity by increasing PSD. Through their enhanced monitoring function, active ACs can detect discrepancies, improve political monitoring, and ensure the objectivity of non-financial reporting through greater PSD. This result also supports resource dependence theory, which suggests that board members devote their time, expertise, and efforts to create opportunities for long-term sustainability by responding to changing stakeholder needs and the external environment. Thus, active ACs will fulfill such needs by fostering political transparency and subsequently CPR. By providing expertise, advice, and vigilance, active ACs can act as crucial conduit for achieving PSD.

Next, AC age is negatively associated with PSD. Our results are consistent with Post and colleagues (2011), who evidence that board age negatively affects corporate social responsibility disclosures and contribute to the limited literature on AC age (Dao et al., 2013; Sultana et al., 2019). According to resource dependence theory, younger directors bring different outlooks and experiences that provide boards with new perspectives on competing in the fast-changing business environment; this makes younger directors judicious corporate advisors. Moreover, younger AC directors may be more active, dynamic, and open to making significant changes to their firms’ business strategies if necessary, which makes them important resources for promoting new responsible business behaviors, such as CPR (Dao et al., 2013; Katmon et al., 2019; Sultana et al., 2019). Advancing resource dependence theory, we claim that in addition to fulfilling their main duties of maintaining financial reporting quality, younger AC directors may be concerned with other important issues such as PSD to foster continuous relationships with the external environment. Also, since PSD can be classified as a risky type of information that brings higher public scrutiny and potential threats (Goh et al., 2020), younger AC directors’ tendency to embrace risky and new proposals would encourage them to support their firms’ PSD.

Finally, AC educational level predicts a firm’s PSD. These results are consistent with prior studies showing that a board’s education level enhances firms’ transparent disclosure practices (Elmagrhi et al., 2019; Reeb & Zhao, 2013) and with Pérez-Cornejo and colleagues (2019), who argue that AC education enhances firms’ risk-management strategies and reputation. Consistent with agency theory, our findings suggest that more educated AC members exercising their monitoring role are more likely to pressure firms to publicly disclose information about their political expenditures. Likewise, our findings are also consistent with resource dependency theory, suggesting that more educated AC members are performing their advisory role by supporting PSD which is a relatively new reporting trend that promotes potential corporate opportunities and relieves stakeholders’ concerns about corporate dark money (Skaife & Werner, 2020). Finally, more educated AC members can show their commitment to the external environment and access external resources by increasing PSD.

Limitations, Implications, and Conclusion

Our research has some limitations that suggest avenues for future scholarship. First, researchers can extend our work by investigating the optimal gender balance for board effectiveness. Second, researchers can extend our work by investigating how diversity of age, tenure, and education influence corporate political decision-making. Other corporate governance factors could also be investigated, such as directors’ renumeration and evaluation. Furthermore, our proxies for advisory and monitoring female directors may or may not reflect the actual practice. Hence, future researchers can obtain interesting insights by developing better measures and by conducting in-depth interviews with politicians, directors, and regulators. In addition, future researchers could examine how the political climate the firm is operating in shapes its CPR. Finally, although we made every effort to address potential endogeneity problems that may influence our results, we acknowledge that our results should be interpreted with some level of caution in terms of inferences of the regression analysis.

Our results highlight the need to combine agency and resource dependence theories to better explain the dual role of the board of directors in relation to PSD. Our decision to use a dual theoretical approach was inspired by the fact that the typical duties of board members require them to monitor management and provide resources to assist the management in formulating its strategies. Utilizing agency theory, our study provides evidence on how the monitoring role of the board enhances PSD through female monitoring directors, shorter board tenure, larger AC size, more frequent AC meetings, and higher AC education level. Simultaneously, utilizing resource dependence theory, our study provides evidence on how the advisory role of the board fosters PSD through female advisory directors, CEO duality, additional directorships, larger AC size, more frequent AC meetings, younger AC age, and higher AC education level. Our approach recognizes the diverse and dual roles that board members play in promoting corporate political transparency. As corporate political activity is inherently associated with agency problems, the monitoring function of the board can minimize agency costs by promoting PSD, and the advisory function of the board can provide a competitive advantage by promoting PSD.

This study has important implications for policymakers, business leaders, politicians, and investors. First, the results indicate the important role of female directors in enhancing ethical corporate political activity. Second, our findings support the call for limits on excessive board tenure because of its unfavorable implications for PSD. Third, we show that board busyness offers economic benefits to societies by enhancing firms’ political transparency, which contributes greatly to our understanding of the implications of director interlocks. Fourth, contrary to the prevalent argument that the AC’s role is limited to financial reporting oversight, we demonstrate that the AC’s role extends to PSD. This finding is in line with prior studies that call for increasing ACs’ responsibilities. Finally, the results suggest that boards should think strategically about the composition of the AC committee, with respect to educational backgrounds and the age of the board members. Current AC-related codes do not generally address the importance of AC age and education; rather, they generally focus on AC independence, composition, and financial expertise.

In conclusion, because of the rapidly growing attention to political issues, CPR is becoming an inescapable priority for businesses and societies. Moreover, the Supreme Court’s decision in Citizens United to remove limits on corporate campaign donations has triggered continuing debates over the governance challenges of increasing PSD. Using the CPA-Zicklin index to create measures of corporate political transparency, we provide strong evidence that board governance characteristics have an impact on corporate PSD. Specifically, we find that when board members are exercising their monitoring and advising roles, firms exhibit better PSD. Finally, we find that AC can play a pivotal role with strengthening board roles and enhancing corporate political transparency. Collectively, we provide evidence that boards with female monitoring and advisory directors, shorter board tenure, CEO duality, additional directorships, larger AC size, more frequent AC meetings, younger AC age, and higher AC education are more progressive in promoting important aspects of CPR.

Footnotes

Appendix

Definition of Variables.

| Variables | Definition | Reference |

|---|---|---|

| Dependent variable | ||

| PSD | Political Spending Disclosure Index calculated as the total of the scores of all dimensions of the CPA-Zicklin PSD index. See Appendix A for the details of each dimension. | (DeBoskey et al., 2021; Goh et al., 2020) |

| DISCLOSURE | The total summed raw score of items in the disclosure dimension of the PSD index in the CPA-Zicklin data | (Ali et al., 2022) |

| POLICY | The total summed raw score of items in the policy dimension of the PSD index in the CPA-Zicklin data | (Goh et al., 2020) |

| OVERSIGHT | The total summed raw score of items in the oversight dimension of the PSD index in the CPA-Zicklin data | (DeBoskey et al., 2021) |

| Main independent variables | ||

| F_Monitoring | Ratio of female monitoring directors to total number of monitoring directors | (Zalata et al., 2019) |

| F_Advisory | Ratio of female advisory directors to total number of advisory directors | (Zalata et al., 2019) |

| Boardtenure | Average tenure of all current directors on the company board in years | (Katmon et al., 2019) |

| CEODuality | CEO duality, which is a dummy variable taking the value of 1 if the board chair and the CEO are the same person, 0 otherwise | (M. Wang & Hussainey, 2013) |

| Busyboard | Percentage of non-executive directors on the firm board sitting on at least three boards of other companies | (Fich & Shivdasani, 2006) |

| ACsize | Total number of directors on audit committee | (Li et al., 2012) |

| ACmeetings | Audit committee meetings held during the year | (Appuhami & Tashakor, 2017) |

| ACage | Audit committee members’ average age | (Dao et al., 2013) |

| ACedu | Audit committee members’ average educational level | (Elmagrhi et al., 2019; Reeb & Zhao, 2013) |

| Control variables | ||

| Boardsize | Total number of directors | (Katmon et al., 2019) |

| Boardattend | Board attendance percentage | (Katmon et al., 2019) |

| ROA | Return on assets | (Elmagrhi et al., 2019) |

| Debt | Total liabilities to total assets | (DeBoskey et al., 2018) |

| Tobinq | The market value of equity plus the book value of total liabilities, preferred stocks and minority interest divided by the book value of total assets | (DeBoskey et al., 2018) |

| Salesgrowth | Change in sales relative to the prior year | (Goh et al., 2020) |

| DPS | Dividend per share | (M. Wang & Hussainey, 2013) |

| MV | Firm size measured by its market value | (Zalata et al., 2019) |

Acknowledgements

The authors greatly appreciate the constructive guidance of Dr. Kathleen Rehbein and the three anonymous referees at Business & Society for their great comments and suggestions. They would also like to acknowledge constructive and useful comments received from the participants at the PhD accounting conference in Nottingham University Business School and the 6th Emerging Markets Inspiration Conference.

Author’s Note

Tam Huy Nguyen is also affiliated with Vietnam National University, University of Economics and Business, Vietnam.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by Egyptian Ministry of Higher Education.