Abstract

Research in instrumental stakeholder theory often discusses the benefits of a stakeholder strategy that balances all stakeholders’ interests as if the firm’s managers were not constrained much in choosing a strategy. Yet, through their value appropriation behavior, stakeholders with high bargaining power can significantly constrain managers’ choices. Our objective is, therefore, to understand when powerful stakeholders give managers the latitude to balance all stakeholders’ interests, rather than forcing them to satisfy primarily their own interests. Building on enlightened self-interest and the justice literature, we identify five motivational drivers that help explain powerful stakeholders’ value appropriation behavior. We next explore the endogenous relationship between the stakeholder strategy adopted by the firm and its effect on powerful stakeholders’ value appropriation behavior. This article complements instrumental stakeholder theory by looking at powerful stakeholders’ motivation to exercise their bargaining power, and in so doing brings powerful stakeholders’ moral responsibility in the treatment of weak stakeholders to the forefront.

Stakeholder theorists see firms as “the vehicles by which stakeholders are engaged in a joint and cooperative enterprise of creating value for each other” (Freeman, Harrison, & Wicks, 2007, p. 6). In this nexus of relationships among stakeholders, managers are in a unique, central position: they make the vast majority of the decisions that shape these relationships (Freeman, 1984; Hill & Jones, 1992; T. M. Jones, 1995). Maybe because of this unique position, much work in stakeholder theory has not acknowledged that managers’ latitude to act according to stakeholder theory’s prescriptions is often constrained by stakeholders themselves (Phillips, Berman, Elms, & Johnson-Cramer, 2010). In particular, some stakeholders are powerful in their relationship with the firm (Frooman, 1999; Mitchell, Agle, & Wood, 1997): in exchange for the resources they provide these stakeholders can bargain for a substantial share of the economic value jointly created by the firm’s stakeholders. By appropriating a substantial share of the value created, powerful stakeholders may de facto force managers to adopt a strategy that prioritizes powerful stakeholders’ interests over the interests of other stakeholders (which we label a “powerful-stakeholder strategy”), because not enough value is left for managers to implement a stakeholder strategy that balances all stakeholders’ interests (which we label an “all-stakeholder strategy”). To explain managers’ latitude to pursue an all-stakeholder strategy, we, therefore, explore what may drive powerful stakeholders to refrain from appropriating as much economic value as possible.

We address this question in three steps. First, we support our claim that powerful stakeholders are able to limit managers’ latitude to pursue an all-stakeholder strategy through their value appropriation behavior. Second, next to short-term personal material outcomes, a motivational driver typically assumed in economic theories, we identify four additional motivational drivers that can drive stakeholders’ behavior and can help explain why powerful stakeholders may be willing to refrain from appropriating as much as possible. On one hand, drawing from the literature considering enlightened self-interest (Baker, Gibbons, & Murphy, 2002; Jensen, 2002; T. M. Jones, 1995; Trivers, 1971), we consider that powerful stakeholders can be driven by long-term as well as short-term material outcomes. As a result, they may see an all-stakeholder strategy as an instrument that, while it implies the sacrifice of some short-term personal material outcomes, will pay off in the longer-term through the positive impact on value creation that allocating more value to some other primary stakeholders can generate. On the other hand, we build on the recent literature on justice (Cropanzano, Byrne, Bobocel, & Rupp, 2001; Folger, Cropanzano, & Goldman, 2005), and explain that powerful stakeholders may be ready to sacrifice some personal material outcomes because fairness can fulfill important human needs: it can reduce the uncertainty surrounding future personal material outcomes, provide a positive social identity, and contribute to one’s identity as a moral person. From a need to reduce uncertainty to a need for morality, we get further and further away from personal material outcomes—and, therefore, self-regard—as the drivers of powerful stakeholders’ value appropriation behavior.

The third step in our theorizing is to consider how the firm’s stakeholder strategy can influence which drivers guide powerful stakeholders’ value appropriation behavior. Specifically, we explore the influence of an all-stakeholder strategy, compared to a powerful-stakeholder strategy, on the salience of the different motivational drivers. This implies that the article sketches an endogenous relationship between the firm’s stakeholder strategy and powerful stakeholders’ appropriation behavior: while powerful stakeholders’ appropriation behavior determines whether managers have the latitude to pursue an all-stakeholder strategy, it is simultaneously shaped by the firm’s treatment of stakeholders.

This article contributes to instrumental stakeholder theory in three ways. First, our theory complements the recent stakeholder literature that aims to be more encompassing with regard to what stakeholders value (Bridoux & Stoelhorst, 2016; Harrison & Wicks, 2013; Tantalo & Priem, 2016) by offering a more complete and nuanced picture of the multiple motivational drivers of stakeholders’ behavior, ranging from a focus on short-term personal material outcomes to a concern for fairness grounded in a need for morality. Second, our theory advances instrumental stakeholder theory by exploring how and when managerial discretion may be restricted by stakeholders’ behavior (Phillips et al., 2010). This topic has received little attention so far as stakeholder scholars tend to view managers as central to explaining a firm’s stakeholder strategy, and thereby overlook the impact of other stakeholders. Third, by investigating the role of fairness in value appropriation, our work complements the existing stakeholder literature, which has primarily focused on the relationship between fairness toward stakeholders and value creation (Bosse, Phillips, & Harrison, 2009; Bridoux & Stoelhorst, 2014, 2016; Harrison, Bosse, & Phillips, 2010). Overall, our message is that managing for all stakeholders, rather than for the powerful ones, can offer a common ground to reconcile the interests of powerful and weak stakeholders because it makes morality salient to powerful stakeholders, rather than pure material self-interest.

Powerful Stakeholders’ Value Appropriation Constrains the Firm’s Stakeholder Strategy

We want to put powerful stakeholders center stage to understand better the constraints managers face when designing their firm’s stakeholder strategy. While it has long been acknowledged that some stakeholders can influence the firm more than others (Freeman, 1984; Frooman, 1999; Mitchell et al., 1997), instrumental stakeholder theory has often discussed managerial decisions and actions as if the firm’s managers were not constrained much in choosing a stakeholder strategy (Phillips et al., 2010). For example, T. M. Jones (1995, p. 417) argued that “a firm’s behavior will, in general, reflect the moral sentiments of its top management.” Consequently, the constraining influence of stakeholders on the firm’s stakeholder strategy has been very much neglected (Phillips et al., 2010).

We understand a firm’s stakeholder strategy as the strategy used to manage the firm’s relationships with its stakeholders. In line with recent work (Bridoux & Stoelhorst, 2014; Harrison et al., 2010), we consider two stylized stakeholder strategies: on one hand, a stakeholder strategy that aims to balance the interests of all stakeholders toward whom the firm has direct moral obligations (cf. Phillips, 2003), which we label an all-stakeholder strategy, and, on the other hand, a strategy that focuses on fulfilling the requests of stakeholders purely based on stakeholders’ power, which we label a powerful-stakeholder strategy. The former strategy is known in the literature as “managing-for-stakeholders” or a “fairness approach,” while the latter has been labeled an “arms-length approach” to stakeholder management (Bridoux & Stoelhorst, 2014; Harrison et al., 2010). We choose different labels to mark clearly for which stakeholders the firm is managed: only the powerful ones versus all normatively legitimate stakeholders.

We focus on the firm’s current primary stakeholders—employees, customers, suppliers, and investors—who are individuals (in contrast to groups of individuals) and act on their own behalf (rather than on behalf of a group) to build on insights from psychology without falling prey to a fallacy of composition (cf. Rousseau, 1985). Among these stakeholders, some have power in their relationship with the firm. According to Mitchell et al. (1997), who adopted the definition of Salancik and Pfeffer (1974, p. 3), power is “the ability of those who possess power to bring about the outcomes they desire.” Psychologists define power very similarly as “the capacity to influence other individuals through asymmetric control over valuable resources and the ability to administer rewards and punishments” (Gruenfeld, Inesi, Magee, & Galinsky, 2008, p. 112; Keltner, Gruenfeld, & Anderson, 2003). We further focus on utilitarian power (i.e., power coming from the control of material resources, Etzioni, 1964), as it is the form of power most often considered by strategy scholars. Primary stakeholders have utilitarian power over the firm when they control resources that (a) are essential to the firm’s operational performance, (b) are in short supply compared to their demand, and (c) have no viable substitute (Frooman, 1999; Hill & Jones, 1992; T. M. Jones, Felps, & Bigley, 2007; Mitchell et al., 1997). 1

An all-stakeholder strategy and a powerful-stakeholder strategy differ significantly with regard to how the value created jointly by all primary stakeholders is divided among stakeholders (Harrison et al., 2010). We focus specifically on the distribution and appropriation of economic value because it is in this realm that stakeholders’ interests conflict (Tantalo & Priem, 2016). Following Bridoux and Stoelhorst (2014), we define joint economic value created as the difference between customers’ willingness to pay for the firm’s products and the sum of the payments all primary stakeholders would receive from their next best alternative. With a powerful-stakeholder strategy economic value is divided according to negotiations in which stakeholders must fight for their own interests (Harrison et al., 2010; T. M. Jones et al., 2007). As a result, value appropriation reflects stakeholders’ bargaining power. Stakeholders who have little bargaining power – for example, because they cannot easily leave the firm—are likely to end up with less value than necessary to fulfill their needs. This is illustrated by the case of low-skilled workers who struggle to make ends meet in liberalized labor markets. In contrast, with an all-stakeholder strategy, managers allocate value taking into consideration the demands and needs of all stakeholders to whom a moral obligation is owed and who, therefore, deserve to be treated fairly and with respect (T. M. Jones et al., 2007; Phillips, 2003). Consequently, firms that adopt an all-stakeholder strategy regularly allocate more economic value to stakeholders than strictly necessary based on their bargaining power because the division of value is guided by moral concerns. Such a firm can, for example, implement a minimum wage higher than what is legally required.

When they choose to exercise their power, powerful stakeholders can constrain managers’ choice of a stakeholder strategy. Frooman (1999) provided an extensive discussion of the ways in which stakeholders can exercise influence over the firm according to how much power they have in their relationship with the firm. For example, powerful stakeholders can threaten to withdraw their resources from being used by the firm and they can attach conditions to continued supply of their resources (Frooman, 1999). Powerful stakeholders constrain managers’ choice of a stakeholder strategy if they exercise their bargaining power to pressure the firm to allocate to them a larger piece of the economic value created jointly by the stakeholders. One does not need to look far for an example: renowned university professors regularly ask and get a salary increase on the basis of an offer from another university. Powerful stakeholders’ exercising their bargaining power to appropriate more value has repercussions on weaker 2 stakeholders. For example, renowned university professors who bargain for higher salaries do not suddenly become more productive but appropriate value that could have been allocated to other stakeholders (students, university administrators, etc.). As long recognized by stakeholder theorists (Harrison & Freeman, 1999; Phillips, Freeman, & Wicks, 2003; Preston & Sapienza, 1990), when managing stakeholders, firms often face tradeoffs among stakeholders’ material interests because, in the short-term, the division of economic value is a zero-sum game (Harrison & Wicks, 2013; Reynolds, Schultz, & Hekman, 2006).

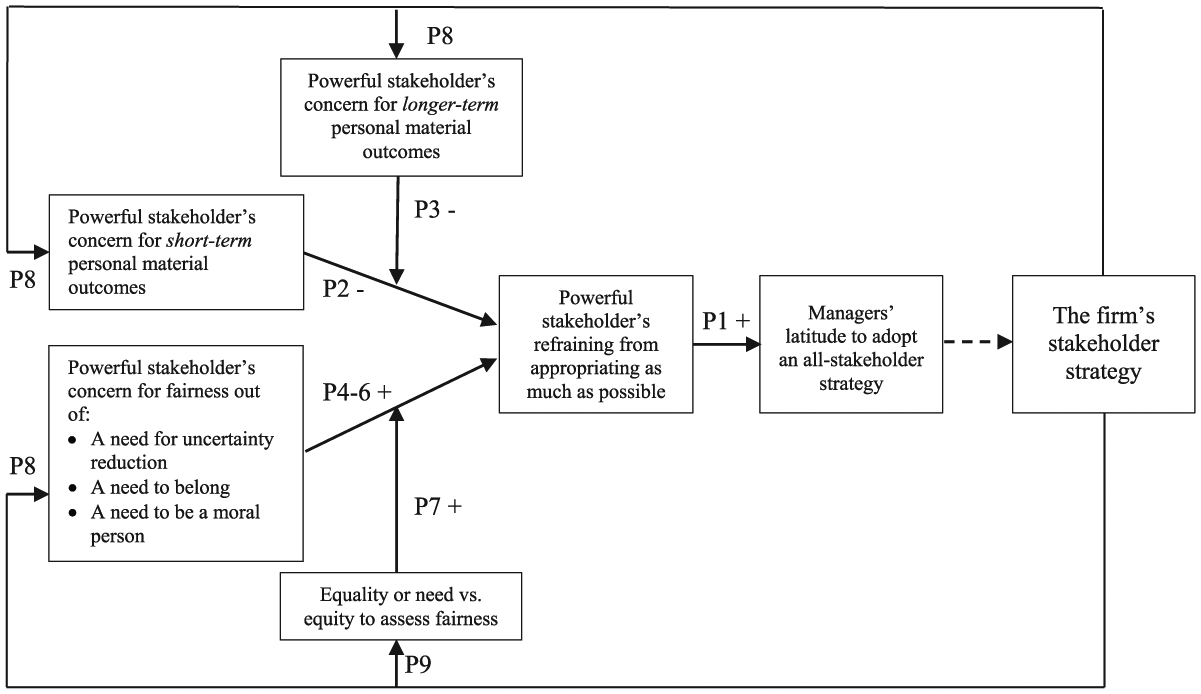

This interdependence among stakeholders with regard to value appropriation implies that together—even if acting independently—powerful stakeholders can affect the division of economic value between powerful and weak stakeholders to such an extent that they can actually restrict managers’ choice to a powerful-stakeholder strategy. We, therefore, claim that for most 3 firms, powerful stakeholders refraining from appropriating as much economic value as possible is a necessary condition for the pursuit of an all-stakeholder strategy and propose:

The Motivational Drivers of Powerful Stakeholders’ Value Appropriation Behavior

Our second step is to explore what motivates powerful stakeholders’ value appropriation behavior to understand when they would refrain from appropriating as much economic value as possible.

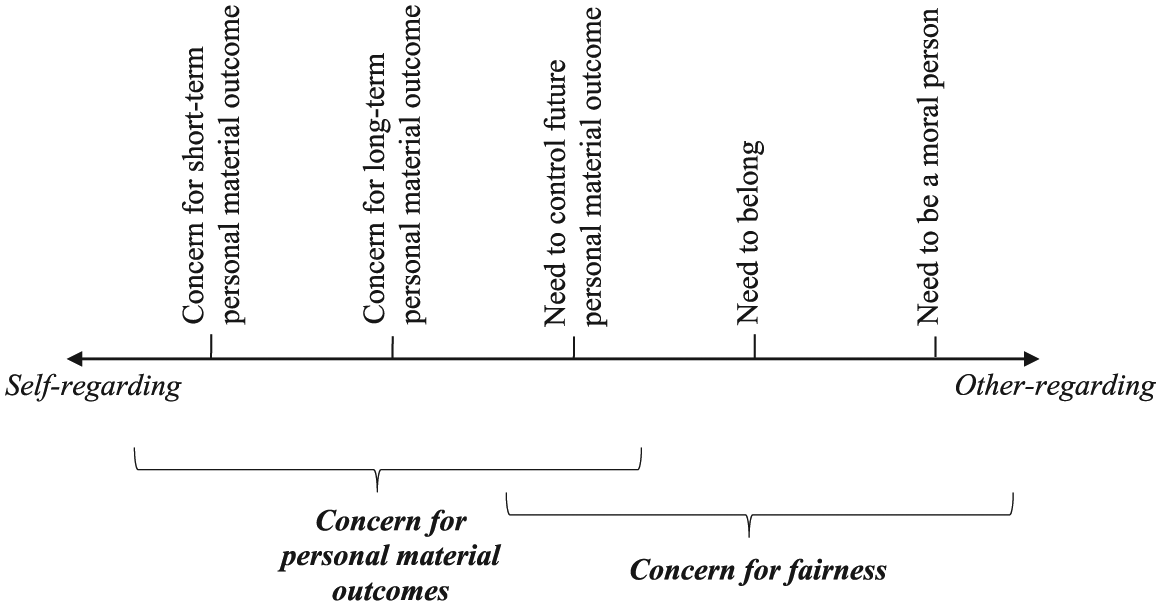

Recent work in the instrumental stakeholder literature (Bosse et al., 2009; Bridoux & Stoelhorst, 2014; Hahn, 2015; Harrison et al., 2010) has argued that a concern for fairness, as well as a concern for personal material outcomes, can drive powerful stakeholders’ value appropriation behavior. We go further by unpacking these two broad categories and identifying five more specific motivational drivers: concern for short-term personal material outcome, concern for long-term personal material outcome, need to control future personal material outcome, need to belong, and need to be a moral person. We depict these motivational drivers in Figure 1 on a continuum ranging from self-regarding to other-regarding, an often-used continuum to depict behavior in social interactions (see the overviews by Fehr & Fischbacher, 2002; Fehr & Gintis, 2007; Van Lange, 1999). Figure 1 and our discussion below reveal that concern for material outcomes and concern for fairness overlap more than usually acknowledged: one of the needs that fairness can address, namely the need for uncertainty reduction, relates directly to personal material outcomes. While we discuss each motivational driver in turn, they can co-exist 4 in shaping stakeholders’ behavior. We will come back to this point in the next section, where we discuss how the firm’s stakeholder strategy can influence which drivers dominate in guiding powerful stakeholders’ value appropriation behavior.

The five motivational drivers of powerful stakeholders’ value appropriation behavior.

A Concern for Personal Material Outcomes

First, powerful stakeholders can be driven by their personal material outcomes without regard for the needs of others (Bridoux & Stoelhorst, 2014), as long recognized by economists when they equate self-interest with the pursuit of economic reward (Simon, 1993). By personal material outcomes, 5 we mean outcomes of a material nature that individual stakeholders get through their relationship with the firm and to which one can attach a monetary value. For example, personal material outcomes for employees are pay, benefits such as a company phone or car, hours of work, and favorable work conditions. All these outcomes can be defined as “material, or instrumental, in a sense that they are concrete and of practical use” (Elizur, Borg, Hunt, & Beck, 1991, p. 23). By contrast, other outcomes stakeholders obtained from their relationship with the firm are affective or cognitive. For example, for employees good relationships with colleagues and supervisor are affective outcomes; and outcomes such as interest, achievement, responsibility, and independence are cognitive (Elizur et al., 1991).

The more a concern for their own short-term material outcomes guides powerful stakeholders’ value appropriation behavior, the more these stakeholders will leverage their bargaining power to appropriate as much value as possible as soon as possible, without regard for how exercising their bargaining power could affect other stakeholders or future value creation by the firm. This first motivational driver best characterizes powerful stakeholders who intend to have a short-term relationship with the firm, like some corporate raiders who aim to make quick profits by acquiring and then dismantling otherwise profitable firms and intra-day traders when they buy and sell of significant amount of stock within the same day:

While stakeholders who are only motivated by their own short-term material outcomes would see little benefit in the firm addressing the needs of other stakeholders, powerful stakeholders who anticipate a longer-term association with the firm can be enlightened in the exercise of their bargaining power even if they are focused exclusively on their own material outcomes (T. M. Jones, 1995). Enlightened self-interest has been used to explain behavior that is somewhat other—regarding such as reciprocal altruism (i.e., one individual making a sacrifice for the benefit another individual with the expectation that the other will repay this sacrifice at a later time; Trivers, 1971)—and the respect of relational contracts (i.e., unwritten understandings that cannot be enforced in court; Baker et al., 2002). With enlightened self-interest, the expectation of longer-term gains is what curbs the pursuit of short-term personal material outcomes. For example, relational contracts can support ongoing relationships among selfish actors as long as the short-run value of reneging is less than the long-run value of the relationship (Baker et al., 2002).

Enlightened self-interest is already familiar to stakeholder scholars, among others, through the work of Friedman (1970) and Jensen (2002). For example, Jensen (2002) argued that managers should resist the temptation to maximize short-term financial performance because such short-term maximization is “a sure way to destroy value in the longer term”: “it is obvious that we cannot maximize the long-term market value of an organization if we ignore or mistreat any important constituency” (p. 309; emphasis added). While the reasoning of Jensen (2002) is about managers being enlightened rather than short-term focused in maximizing financial value (i.e., the value for all actors who have a financial claim on the firm in the form of, among others, equity, debt, preferred stock, and warrant), the same line of argumentation can be applied to powerful stakeholders in relation to their appropriation of economic value.

Powerful stakeholders taking the longer-term into account can be willing to forgo some short-term gains to ensure more fairness if they expect that treating some other stakeholders fairly will increase sufficiently these stakeholders’ contribution to joint value creation to be personally beneficial in the longer-term. These situations where the interests of powerful and some less powerful stakeholders can be relatively easily reconciled in the longer-term have been labeled as win-win (Freeman, Harrison, Wicks, Parmar, & De Colle, 2010). For example, investors who have a long-term orientation for their investment in the firm could anticipate that compensating employees better will increase their motivation at work and decrease their turnover, which could increase profits in the longer-term and ultimately be more beneficial to investors than keeping wages low (Tantalo & Priem, 2016). Flammer and Bansal (2017) provided empirical support for this argument by showing that shareholder proposals to change executive compensation toward more long-term compensation lead to higher operating performance in the long-term (after a slight decrease in the short-term), and lead managers to invest in better relationships with stakeholders, in particular employees.

We expect that powerful stakeholders’ concern for longer-term personal material outcomes will dampen the impact of stakeholders’ pursuit of short-term material outcomes on value appropriation, but it will not suppress it. First, it is well established that when decisions involve a tradeoff among personal material outcomes captured at different times (here short-term vs. long-term), people tend to prefer more immediate personal material outcomes over delayed ones, which is known as time preference and is often captured by a time discounting rate (Frederick, Loewenstein, & O’Donoghue, 2002). Moreover, powerful stakeholders who are enlightened in the pursuit of their longer-term material outcomes perceive fairness as a means, not an end valued for its own sake. If treating other stakeholders fairly does not increase the long-term material benefits for powerful stakeholders, powerful stakeholders will not limit their value appropriation to the benefit of those other stakeholder, as refraining comes at a personal cost in the short-term. So, even if powerful stakeholders exhibit value appropriation behavior that seems to suggest that they care about fairness, a concern for long-term personal material outcomes at best tempers a concern for short-term personal material outcomes. We, therefore, propose a moderating effect of a concern for longer-term personal material outcomes on the relationship put forward in Proposition 2:

A Concern for Fairness

Our arguments so far imply that powerful stakeholders focused on their material outcomes may not refrain their value appropriation enough to leave room for managers to implement an all-stakeholder strategy, which by definition involves treating all stakeholders fairly, including the weak ones whose contribution to value creation will not be significantly increased by a better treatment. This helps explain that practices harming weak stakeholders continue despite a relatively widespread adoption of enlightened stakeholder management by firms and public outcry in the face of these harmful practices. However, that does not mean that managers will never have the latitude to adopt an all-stakeholder strategy. The pursuit of personal material outcomes is only one of the motivational drivers of stakeholders’ behavior.

There may be “a small minority of powerful stakeholders who are focused on their own self-interest at the expense of others” (Freeman et al., 2010, p. 284), but many stakeholders also care about fairness (Bosse et al., 2009; Bridoux & Stoelhorst, 2014, 2016; Hahn, 2015; Harrison et al., 2010). While the stakeholder literature has so far mostly focused on the relationship between a fair treatment of stakeholders and stakeholders’ contributions to value creation, we wish to explain value appropriation behavior. This requires digging into why stakeholders care about fairness, which the stakeholder literature has not done yet. We, therefore, turn to the large literature on justice in psychology and organizational behavior, with special attention for the growing literature on third-party justice that provides insights into why people mind how others are treated (Cropanzano, Goldman, & Folger, 2003).

The justice literature has solidly established that people’s feelings, thoughts, and behaviors are often shaped by their assessments regarding what is appropriate and fair (Colquitt, Conlon, Wesson, Porter, & Ng, 2001; Cropanzano et al., 2001; Tyler, 2012). For example, in the workplace, those who receive less than they feel they deserve have been found to be angry and exhibit behaviors such as theft, sabotage, and even violence, which are such risky behaviors that they cannot be explained by the pursuit of personal material outcomes (Ambrose, Seabright, & Schminke, 2002; Greenberg, 1990). It is not only when the outcome is personally unfavorable that people care about fairness: if they cannot contribute more or give away some of their resources, those who get more than they feel they deserve have been found to restore fairness by walking away from the unfair situation (Tyler, 2012).

Whereas justice research has traditionally focused on explaining how people respond to how they are treated themselves (Folger & Glerum, 2015), people also react to how fairly others are treated by an organization, authority, supervisor, and so on. In relation to stakeholders, the literature on third-party justice predicts for example that employees and job applicants respond positively to an organization’s corporate social responsibility (CSR) toward other stakeholders (Rupp, Ganapathi, Aguilera, & Williams, 2006; Rupp, Shao, Thornton, & Skarlicki, 2013). This is supported empirically by the findings that a firm’s CSR toward other stakeholder groups increases employees’ intention to stay (D. A. Jones, 2010), job applicants’ intention to join the firm (D. A. Jones, Willness, & Madey, 2014; Sen, Bhattacharya, & Korschun, 2006; Turban & Greening, 1997), investors’ intentions to invest (Sen et al., 2006), and consumers’ purchase intentions (unless consumers believe that the firm’s CSR comes at the cost of product quality; Sen & Bhattacharya, 2001; Sen et al., 2006).

Justice researchers have provided three complementary explanations for why people concern themselves with fairness (Cropanzano et al., 2001). First, according to the instrumental model (Thibaut & Walker, 1975), fairness provides a sense of control over future outcomes when these outcomes are (partly) under others’ control and one is, therefore, vulnerable to their opportunistic behavior. Second, according to the relational model (also referred to as identity-based view; Lind & Tyler, 1988; Tyler & Blader, 2003), fairness helps people build a positive identity, feeding their need to belong. Third, according to the deonance model (Folger, 2001; Folger & Glerum, 2015), fairness can fulfill a need to do the right thing out of a basic respect for human dignity and worth.

Applying the insights from the justice literature to powerful stakeholders’ value appropriation behavior, we propose that these stakeholders may refrain from appropriating as much economic value as possible because fairness fulfills one or several of three needs they may experience. First, the instrumental model of justice suggests that powerful stakeholders who believe they will stay with the firm in the long haul may be concerned about a fair treatment of other stakeholders because it provides a heuristic to forecast how the firm will treat them in the future and, thus, offers a sense of control over their own material outcomes (Aguilera, Rupp, Williams, & Ganapathi, 2007; Rupp et al., 2006, 2013). A need for control—known under many different labels such as a need for self-efficacy (Bandura, 1977) and need for autonomy (Ryan & Deci, 2006)—reflects a fundamental need that is biologically motivated, as it is already present in very young infants (Leotti, Iyengar, & Ochsner, 2010). The absence of control has a profound impact on the regulation of emotion, cognition, and physiology; in particular, the absence of control can be very stressful (Leotti et al., 2010). Because of a need to reduce uncertainty around future material outcomes, powerful stakeholders may be willing to limit their value appropriation now to enable managers to implement a fair division of value with the hope that managers will also divide value fairly in the future, at times where these powerful stakeholders are themselves vulnerable to other stakeholders claiming more of the value created. This fairness concern is to a large extent self-focused: it arises from a need to reduce uncertainty and increase control over one’s future material outcomes (Cropanzano et al., 2001):

Second, building on the relational model of justice, we propose that powerful stakeholders may be ready to sacrifice some economic value to the benefit of weaker stakeholders because fairness toward all stakeholders can fulfill a need to belong, in particular, to a high-status group. On one hand, a fair treatment of other stakeholders can fulfill powerful stakeholders’ need for relating to other human beings (Aguilera et al., 2007; Rupp et al., 2006), as weaker stakeholders will react to a fair treatment by liking and trusting more powerful stakeholders (Colquitt & Rodell, 2011; Yang, Mossholder, & Peng, 2009), which in turn will lead to closer relationships among the firm’s stakeholders (Cropanzano, Rupp, Mohler, & Schminke, 2001).

On the other hand, a fair treatment of other stakeholders can contribute to powerful stakeholders’ positive social identity through the prestige that associating with a fair organization bestows on them (D. A. Jones et al., 2014; Rupp et al., 2013). Fairness toward weak stakeholders, as a form of CSR, enhances the firm’s reputation in the eyes of outsiders (Brammer & Millington, 2008; Brammer & Pavelin, 2006). In turn, as people derive some of their identity through their affiliation with groups (Turner, Oakes, Haslam, & McGarty, 1994), being associated with a firm with a good reputation provides prestige to stakeholders: employees and other stakeholders may “feel proud of being part of a well-respected organization, as it strengthens their feelings of self-worth to bask in reflected glory” (Smidts, Pruyn, & Van Riel, 2001, p. 1051). Accordingly, Sen and Bhattacharya (2001) found that a firm’s CSR toward employees increases consumers’ identification with the firm, which in turn leads consumers to evaluate the firm more positively. In line with these arguments, we propose the following relationship between a need to belong and powerful stakeholders’ value appropriation behavior:

A concern for fairness may also arise from a third source, as recently recognized in the justice literature: powerful stakeholders may be concerned about a firm’s fair treatment of weak stakeholders because such a treatment is the right thing to do from a moral standpoint (Aguilera et al., 2007; Folger, 2001; Folger & Glerum, 2015; Rupp et al., 2006, 2013). In an important criticism of the instrumental and relational models of justice, Folger (1998) has argued that, beyond the self-serving benefits of control over future material benefits and relational benefits, some people care about fairness out of a basic respect for human dignity and worth. As a result, people sometimes behave in ways indicating that they feel an obligation to be fair and to hold other people and entities they anthropomorphize (such as organizations) accountable as if they also had a duty to be fair (Folger & Glerum, 2015). In line with this deonance model, work on third-party justice shows that many observers of an injustice between two parties with whom they have no relationship are willing to punish the perpetrator at a material cost to themselves, even in conditions of complete anonymity (Turillo, Folger, Lavelle, Umphress, & Gee, 2002).

Whereas Folger and colleagues tend to pitch deonance in opposition to the pursuit of self-serving benefits, we expect that stakeholders are much more likely to care for a fair division of value for the sake of morality when they experience a need to be a moral person, which we will argue is the case when moral identity is central to the stakeholder’s identity. In line with moral psychologists and biologists we see humans’ need to be a moral person as an evolutionary adaptation that facilitates long-term social interactions by aligning the benefits for others and for the self (in the form of intangible rewards such as pride and intangible costs such as guilt; Rai & Fiske, 2011). Powerful stakeholders may perceive their value appropriation behavior as belonging to the realm of morality because how economic value is divided is very often assessed based on fairness norms both by actors affected and by outsiders such as the media, as is abundantly clear from the extensive literature on distributive justice in organizations (for a meta-analysis see Cohen-Charash & Spector, 2001). A vivid illustration is the recurrent debate around CEOs’ and top bankers’ compensation where arguments around increasing inequalities and pay-for-performance are often pitched against each other.

Research on moral behavior has shown that, in interaction with moral assessments, moral identity plays an important role in explaining moral behavior (Aquino & Reed, 2002; Hardy & Carlo, 2011; Reynolds & Ceranic, 2007). Moral identity is a specific kind of self-conception (“Who am I?”) that revolves around the moral aspects of one’s self (Aquino & Reed, 2002). Moral identity is “a disposition toward valuing morality and wanting to view oneself as a moral person” (Cohen & Morse, 2014, p. 43). People do not all have the same need to be moral: people vary with regard to how central moral identity is to their overall self-concept because moral identity is stored in memory as a complex knowledge structure—consisting of moral values, goals, traits, and behavioral scripts—that is acquired through life experiences (Aquino, Freeman, Reed, Lim, & Felps, 2009).

Moral identity is organized around a set of moral traits, such as, caring, compassionate, fair, friendly, generous, hardworking, helpful, honest, and kind (Aquino & Reed, 2002). In other words, fairness as deonance (“ought to be fair,” Folger & Glerum, 2015) is one of several moral values that can constitute moral identity (Aquino & Reed, 2002; Folger et al., 2005). As a consequence, being fair may be more or less important to a stakeholder’s self-concept than other moral traits (e.g., being loyal or being caring). However, because moral traits form a network of connected components in people’s mind (Aquino & Reed, 2002), fairness (or a lack thereof) will invoke moral identity in stakeholders who see being moral as essential to who they are regardless of how important fairness is compared to other moral traits.

When moral identity is central to an individual’s self-concept, it can motivate action that is moral: it creates a need for the individual to act morally to be true to himself or herself (Aquino et al., 2009; Reynolds & Ceranic, 2007). We, therefore, expect moral identity and the attached need to be a moral person to lead powerful stakeholders to refrain from appropriating as much value as possible to support fairness. Having a central moral identity has indeed been found to be positively associated with charitable giving, increased organizational citizenship behavior, and volunteering for worthy causes, and negatively associated with counterproductive work behavior, lying, and cheating (Cohen & Morse, 2014). This leads us to propose,

We have argued in Propositions 4 to 6 that a concern for fairness, arising from one or several of three needs, leads powerful stakeholders to refrain from appropriating as much value as they could on the basis of their bargaining power. We now turn to a factor that moderates the relationships put forward in Propositions 4 to 6, namely which principle of distributive justice powerful stakeholders apply to assess the fairness of the division of the value created jointly by the firm’s stakeholders. Stakeholders can apply different normative standards in assessing the fairness of outcomes (i.e., distributive justice; Adams, 1965). Scholars have identified three core principles of distributive justice: equity, equality, and need (Deutsch, 1975). The equity principle—allocating proportionally to one’s merits—prescribes relating stakeholders’ payoffs (e.g., pay, prices, and returns) to their inputs (e.g., effort, time, cognitive resources, and money); the equality principle prescribes dividing the value created equally among all stakeholders; the need principle prescribes giving more to stakeholders who have the biggest material needs (Deutsch, 1975). The justice literature has argued that the equity principle is the most commonly applied in the organizational context, but the equality and even need principle can sometimes prevail under certain conditions (e.g., the other stakeholders involved are emotionally close rather than distant), and when certain goals are salient (e.g., group harmony or social welfare rather than productivity) (Colquitt et al., 2001; Kabanoff, 1991).

Fair value appropriation behavior is very different depending on which of the three distributive justice principles powerful stakeholders apply to guide their behavior. Powerful stakeholders who apply the need or equality principle could refrain from appropriating value to a significant extent to ensure, for example, a decent standard of living for workers in a developing country (need principle), or relatively equal pay among employees (equality principle). By comparison, powerful stakeholders who apply the equity principle are likely to limit significantly less their value appropriation because according to this principle, it is fair that stakeholders who contribute resources that are more valuable also receive more of the value created jointly. Equity is, for example, a typical argument used to defend high compensations for star employees and top executives (Wade, O’Reilly, & Pollock, 2006), while opponents argue on basis of the need or equality principle with arguments related to the welfare of the poor and rising inequalities:

We have argued so far that some motivational drivers can lead powerful stakeholders to refrain from appropriating value to the detriment of weak stakeholders, which is a necessary condition for managers to have the latitude to implement an all-stakeholder strategy. Our propositions are depicted in Figure 2. By the very definition of latitude, our theory does not imply that managers will implement an all-stakeholder strategy; we simply argue that managers are not prevented from choosing this strategy on the basis of powerful stakeholders’ claims on the value created jointly. With our focus on powerful stakeholders we have little to say about whether managers will actually choose an all-stakeholder strategy if given the latitude to do so (we, therefore, represent this relationship with a dash line in Figure 2). We refer interested readers to the existing literature, which suggests that top managers’ personal values may play a role (Adams, Licht, & Sagiv, 2011; T. M. Jones, 1995) and that shared beliefs and norms within the organization about how to deal with stakeholders should affect top managers’ choice of a stakeholder strategy (Brickson, 2007; T. M. Jones et al., 2007). Our next step in this article is to consider how the firm’s stakeholder strategy affects the salience of the five motivational drivers.

The endogenous relationship between the firm’s stakeholder strategy and powerful stakeholders’ value appropriation behavior.

The Impact of a Firm’s Stakeholder Strategy on the Salience of the Motivational Drivers

Following much of instrumental stakeholder theory (Harrison et al., 2010; T. M. Jones, 1995), we assume that the firm’s stakeholder strategy is readily apparent to stakeholders through the firm’s policies and decisions as well as through the nature of the firm’s direct dealings with stakeholders. Furthermore, for the sake of simplicity and in line with much of the existing literature, we focus on two stakeholder strategies as explained above: an all-stakeholder strategy and a powerful-stakeholder strategy. The jest of our arguments below is that, compared to a powerful-stakeholder strategy, an all-stakeholder strategy makes (1) the other-regarding motivational drivers more salient than the self-regarding motivational drivers and (2) the distributive principles of equality and need more salient and the principle of equity less salient.

Overall, we thus argue that an all-stakeholder strategy makes powerful stakeholders more likely to refrain from appropriating as much value as possible based on their bargaining power. This third step in our reasoning implies that we propose an endogenous relationship between powerful stakeholders’ value appropriation behavior and the firm’s stakeholder strategy: the causality goes both ways. This endogeneity in our theory helps to explain, on one hand, that an all-stakeholder strategy can be sustained over time because it generates the latitude necessary for its pursuit and, on the other hand, that it is difficult for firms to switch from a powerful-stakeholder strategy to an all-stakeholder strategy because managers lack the latitude to switch.

The Salience of Morality vs. Personal Material Outcomes

The adoption and implementation of an all-stakeholder strategy communicates to stakeholders that the firm prioritizes addressing the needs of normatively legitimate stakeholders over short- or long-term financial performance, at least as long as the firm’s survival is not at stake (T. M. Jones et al., 2007). By keeping true to a moral standard of caring for all stakeholders’ needs, a firm with an all-stakeholder strategy makes the two most other-regarding motivational drivers on our continuum—the need to belong and the need to be a moral person—salient compared to a firm with a powerful-stakeholder strategy.

The need to belong is more salient because such a firm is more likely to convince the general public that genuine care and concern for the well-being of all stakeholders is the principle that guides the firm’s behavior, therefore building a positive reputation for being a benevolent organization (Fombrun & Shanley, 1990). In turn, this positive reputation for benevolence and morality will make the need to belong to a prestigious organization more salient in the relationships between powerful stakeholders and the firm; a need that the firm is able to fulfill (D. A. Jones et al., 2014; Rupp et al., 2013).

The need to be a moral person is more salient because by consistently exhibiting and communicating a genuine care and concern for the well-being of all stakeholders, rather than dealing with stakeholders primarily based on bargaining power, a firm with an all-stakeholder strategy is much more likely than a firm with a powerful-stakeholder strategy to bring its stakeholders to see value creation and value appropriation behaviors as falling within the realm of morality (T. M. Jones et al., 2007) and, as a result, to make stakeholders’ need to be a moral person salient. Human beings tend to moralize their behavior when they perceive themselves to be highly interdependent with other human beings or anthropomorphized collectives such as firms, unions, and communities (Rai & Fiske, 2011). Firms with an all-stakeholder strategy humanize other stakeholders in powerful stakeholders’ eyes by explicitly justifying their decisions and practices on the basis of the harm that can be done to weaker stakeholders as well as the moral obligation to care for their well-being. This makes it easier for powerful stakeholders to appreciate weaker stakeholders’ experiential point of view and increases their sense of moral concern for these weaker stakeholders (Rochford, Jack, Boyatzis, & French, 2017).

As a result of their moralization of value creation and value appropriation behaviors, powerful stakeholders will use morality as a criterion to assess their own value appropriation behavior. They will also be more motivated to choose moral over immoral behavior because moralization increases the salience of powerful stakeholders’ moral identity. The effect of moral identity on moral behavior is context-dependent: because humans have many identities, the effect of moral identity on moral behavior is determined in large part by which of one’s identities is made accessible in a particular situation (Aquino et al., 2009). By moralizing stakeholders’ behavior, a firm with an all-stakeholder strategy makes powerful stakeholders’ moral identity more accessible and, thus, the need to be a moral person stronger. The literature on moral identity further suggests that this positive effect of an all-stakeholder strategy as a situational factor is stronger for powerful stakeholders whose moral identity has relatively low centrality and may not otherwise be active (Aquino et al., 2009).

In contrast, when a firm adopts a powerful-stakeholder strategy rather than an all-stakeholder strategy, the two most self-regarding motivational drivers on our continuum (i.e., concern for short-term and long-term personal material outcomes) are activated. A powerful-stakeholder strategy discards moral principles when it is economically advantageous to do so (Harrison et al., 2010; T. M. Jones et al., 2007). Even if managers try to compensate for these violations by emphasizing moral principles in the firm’s communication, stakeholders are not easy to dupe. In the face of inconsistent behavior over time, stakeholders infer that the firm lacks a genuine care and concern for the well-being of all stakeholders. When assessing other people’s and organizations’ benevolence and morality, people have been found to weigh negative information more heavily than positive information (Kim, Ferrin, Cooper, & Dirks, 2004): a single intentional violation is considered to offer a reliable signal of low benevolence and morality while a single moral behavior is typically discounted as a signal of benevolence and morality (Kim et al., 2004). As a result of assessing the firm as low on benevolence and morality, either powerful stakeholders walk away if it is important for them to fulfill a need to belong or a need to be a moral person in their stakeholder relationship (self-selection effect) or they turn to the satisfaction of other needs that can effectively be fulfilled with a powerful-stakeholder strategy, namely personal material benefits (motivational effect).

Instead of moralizing value creation and value appropriation behavior, a powerful-stakeholder strategy makes personal material outcomes salient to powerful stakeholders through the discourse and practices that accompany this strategy (Bridoux & Stoelhorst, 2014, 2016). The discourse of firms with a powerful-stakeholder strategy usually emphasizes individualism, competition among stakeholders, and relies on market analogies and even sometimes on arguments like “the survival of the fittest” using Darwinian evolutionary theory as a metaphor. Common practices are individual pay-for-performance and tournament systems that pitch stakeholders against each other in the pursuit of personal material outcomes (Bridoux & Stoelhorst, 2014). The literature on moral identity shows that these practices are situational factors that weaken the impact of moral identity on behavior even for the people for whom moral identity is highly central (Aquino et al., 2009). In addition to an emphasis on personal material outcomes, the discourse and practices linked to a powerful-stakeholder strategy sometimes also depict some human stakeholders as means/instruments that the firm is free to use to achieve financial goals (Rochford et al., 2017). This can lead powerful stakeholders to dehumanize these human stakeholders (Rochford et al., 2017), which in turn reduces the salience of the motivational drivers grounded in morality. On the basis of the above arguments, we propose,

The Salience of Equity versus Equality and Need

Here the argument is quite simple. An all-stakeholder strategy makes the need and equality principles salient to powerful stakeholders compared to the equity principle, as managers provide justification for the firm’s decisions and practices that involve caring for weaker stakeholders as well as the powerful ones (Sisodia, Wolfe, & Sheth, 2003). In contrast, the only distributive principle that a powerful-stakeholder strategy could trigger in powerful stakeholders’ mind is the equity principle, as bargaining power is the driving criterion to distribute the value created jointly. A distribution based on bargaining power can appear equitable to powerful stakeholders who believe that competition in the markets for stakeholders is fair (T. M. Jones et al., 2007). For example, stakeholders who believe that labor markets generate bargaining power differences among workers purely based on talent, effort, and achievement (i.e., a meritocracy) could assess a powerful-stakeholder strategy as equitable. In contrast, stakeholders who believe that luck and connections rather than talent and hard work determine bargaining power in labor markets are much less likely to find a powerful-stakeholder strategy to be equitable and therefore fair at all. Together these arguments regarding the salience of the three distributive principles with the two stakeholder strategies lead us to propose,

Discussion

In line with Phillips et al. (2010), our starting point was that managers may be more constrained in their choice of a stakeholder strategy than often acknowledged. In particular, powerful stakeholders can exercise their bargaining power to force the firm to serve their material interests, which usually comes to the detriment of weak stakeholders. We have explored when powerful stakeholders would be motivated to refrain from appropriating as much value as possible to predict when managers would have the latitude to choose an all-stakeholder strategy. We have also considered how an all-stakeholder strategy can influence powerful stakeholders’ motivation to appropriate value.

Our article makes three contributions to instrumental stakeholder theory. First, by identifying five motivational drivers of stakeholders’ behavior, we provide a finer-grained understanding of the concern for personal material outcomes and the concern for fairness that the literature had already put forward as valued by stakeholders (Bosse et al., 2009; Bridoux & Stoelhorst, 2014; Hahn, 2015; Harrison et al., 2010; Harrison & Wicks, 2013). We believe that a finer-grained understanding is an important step toward better explanations of stakeholders’ behavior because it does not reduce motivation to a simple “either self-interest or fairness” classification. Importantly, our theory reveals that, even if they share a concern for fairness, stakeholders may be driven by three quite different needs, which makes it more difficult to satisfy these stakeholders at once, with a single set of practices and discourses. While we discuss the impact of the five motivational drivers on value appropriation, future research could use them to shed new light on stakeholders’ motivation to contribute to value creation.

A second contribution of our work is to answer the call of Phillips et al. (2010) to consider the limits stakeholders impose on managerial discretion. Our conclusion is that managers have the latitude to pursue an all-stakeholder strategy when powerful stakeholders are driven by a need to control their future outcomes, a need to belong, and/or a need to be a moral person, rather than by a concern for personal material outcomes. Beyond these specific insights, our work implies that stakeholder theorists should be careful when making sense of the relationships between firms and their stakeholders. Developing a theory that casts firms and their managers as heroes or villains and stakeholders as passive recipients of good deeds or victims may distort reality in a way that decreases our relevance for practice. We may better serve our purpose of encouraging firms to do good by adopting a more neutral stance of the power dynamics at work when some weak stakeholders are mistreated: in many cases powerful stakeholders may bear a large part of the responsibility for the treatment of weak stakeholders. This means accepting that top managers are not almighty, but it also means that there are more channels through which positive change for weak stakeholders can be brought about that we could research.

We hope that our work will help generate a renewed interest in power. As our work has focused on utilitarian power, which comes from the control of material resources, further research could explore normative power, which is power coming from shared values, beliefs, or sentiments about the rights of different stakeholder groups in their relationships with firms (Etzioni, 1964). Furthermore, because stakeholder theory has generally adopted a sociological approach to power (Cobb, 2016; Frooman, 1999; Mitchell et al., 1997; Roome & Wijen, 2006), we see a lot of potential to borrow from other fields such as social psychology to understand the impact of stakeholders’ power on value creation and appropriation. Over the last 15 years, psychologists have shown that power has deep transformative effects on human psychology, shaping cognition, affect, and behavior (Keltner et al., 2003; Lammers, Galinsky, Dubois, & Rucker, 2015). “People who feel powerful think and act fundamentally differently than people who feel less powerful” (Lammers et al., 2015, p. 15). In particular, power influences individuals’ thoughts and behaviors because it leads people to focus more on the self and their own needs and goals (Fiske, 1993; Lammers et al., 2015).

The third contribution of our work is to investigate the role of fairness in value appropriation, thereby complementing the existing stakeholder literature that has primarily focused on the relationship between fairness toward stakeholders and value creation (Bosse et al., 2009; Bridoux & Stoelhorst, 2014, 2016; Hahn, 2015; Harrison et al., 2010; Harrison & Wicks, 2013). Our key message is that managing for all stakeholders, rather than only for the benefits of the powerful ones, can offer a common ground to reconcile the interests of powerful and weak stakeholders because it makes morality salient to powerful stakeholders. Stakeholder theorists like many strategy scholars often narrowly focus on stakeholders’ material well-being (Harrison & Wicks, 2013), which leads them to see stakeholders’ interests as conflicting because, in the short-term, allocating more economic value to one stakeholder usually implies giving less to other stakeholders. Complementing the recent work that has moved away from such a narrow view of stakeholders’ interests, our theory implies that it may be easier to reconcile stakeholders’ interests than often assumed. Indeed, once we acknowledge that the firm can fulfill (powerful) stakeholders’ needs to control their future outcomes, to belong, and to be a moral person, in addition to their need for material outcomes, an all-stakeholder strategy can aim to provide control, relational, and/or deontic benefits to powerful stakeholders to compensate them for the personal material outcomes that they sacrifice to enable managers to pursue this strategy. On this point, our work contributes not only to instrumental stakeholder theory, but also to the CSR literature discussing the tradeoffs among stakeholders’ interests (Bridoux, Stofberg, & Den Hartog, 2016; Rupp et al., 2013; Vlachos, Panagopoulos, Theotokis, Singh, & Singh, 2014).

We see at least three areas for future research that emerge from limitations of our work. First, we have focused on explaining the value appropriation behavior of current powerful stakeholders. It would be interesting to use our continuum of motivational drivers to investigate the behavior of prospective powerful stakeholders, that is stakeholders who are considering to join the firm. Attracting the powerful stakeholders who have the resources necessary to create value may further constrain managers’ choice of a stakeholder strategy (Mackey, Mackey, & Barney, 2007), because the motivational drivers may play out differently in guiding powerful stakeholders’ decision to join the firm than they do in guiding the value appropriation behavior of stakeholders who already have made the decision to join the firm.

Second, like almost all research in management, we have focused on fairness and harm/care as if morality could be reduced to these two moral foundations when applied to relationships with stakeholders. We would like to make the reader aware that such a focus may reflect a cultural and ideological bias as uncovered relatively recently by moral psychologists (Graham, Haidt, & Nosek, 2009; Haidt, 2007). Other moral foundations—namely, ingroup/loyalty, authority/respect, and purity/sanctity (see Graham et al., 2011)—may prove important to understand some relationships between firms and stakeholders or among stakeholders, especially in non-Western contexts.

Third, for the sake of simplicity, we have talked about powerful stakeholders as if all firms were facing some stakeholders with high bargaining power because they (a) control resources that are essential to the firm’s operational performance, (b) are in short supply compared to their demand, and (c) have no viable substitute (which is known as utilitarian power; cf. Mitchell et al., 1997). While many firms do indeed face some powerful stakeholders, it is important to acknowledge that stakeholders’ utilitarian power can be managed to some extent through the design of the value creation tasks. In particular, organizing value creation tasks so that value creation rests primarily on collective resources rather than on resources controlled by individual stakeholders will lead to lower power differences among stakeholders. With lower power differences managers should have more latitude to choose a stakeholder strategy, independently of which motivational drivers guide powerful stakeholders’ value appropriation behavior. This is in line with evidence that firms known for both their excellent treatment of stakeholders and superior value creation often create superior value not because they have access to extraordinary individual resources, but because they master something collective and quite intangible such as a more collaborative culture (Gittell, 2003). If correct, there may be a tension to explore between how instrumental stakeholder theory proposes firms could create value and the sources of value creation studied in other streams in the strategy field, for example, star employees in the human capital stream of literature.

Our theory points to an additional role for managers and activists who want to get powerful stakeholders to care for weak stakeholders: shaping the context of powerful stakeholders’ value appropriation behavior so as to activate their concern for fairness grounded in morality. We have argued that situational factors such as the firm’s stakeholder strategy can bring powerful stakeholders to moralize or not their behavior toward the firm and other stakeholders and can increase or decrease the accessibility of moral identity within the working self-concept. To bring powerful stakeholders to give managers the latitude to pursue an all-stakeholder strategy, managers and activists could thus actively shape the context of stakeholders’ interactions. For example, stakeholders’ moral responsibility can be emphasized in the communication with powerful stakeholders, as it has been shown that even subtle linguistic cues can increase the centrality of moral identity (Cohen & Morse, 2014). It is also important that managers are aware of the opposite effect uncovered in Aquino et al.’s (2009) work: situational factors such as financial incentives for task performance can decrease the current accessibility of moral identity, even in people whose moral identity has high centrality. This suggests that when designing the firm’s policies in the many domains that affect stakeholders (e.g., compensation policies, outsourcing strategy, and charitable giving) managers face the difficult task of avoiding negative interactions, by which one policy undermines the positive influence of another.

Footnotes

Acknowledgements

The authors thank special issue editor Jay Barney and an anonymous reviewer for their guidance. They appreciate helpful comments from Sharon Alvarez, Jeff Harrison, and Rob Phillips, and from participants at the pre-conference workshop of the 2017 IABS Conference in Amsterdam, session participants at the 2017 Academy of Management Annual Meeting in Atlanta, and participants at the LouRIM research seminar that took place in Louvain-la-Neuve, on March 13, 2018.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.