Abstract

There are relatively few empirical studies on the impacts of corporate social responsibility (CSR) policies and programs. This article addresses the research gap by analyzing the incidence of, and the conditions that affect, decoupling (defined as divergence) among CSR policies, implementation of CSR programs, and CSR impacts for various environmental and social issues. Complete decoupling is a condition of full divergence among policies, programs, and impacts amounting to purely ceremonial CSR. Using ratings from a sustainability rating agency on a sample of about 1,000 large companies in 24 countries, the authors find empirical evidence not supporting a conclusion of complete decoupling. The empirical evidence suggests four levels of nondivergence in the sample. First, for most CSR issues examined, CSR policies of high quality (as measured by scope and level of detail) do have relatively strong effects on CSR implementation. Second, CSR programs of high quality (as measured by scope, the use of targets, and the use of strict deadlines) do have relatively strong effects on CSR impacts. Third, for most CSR issues, even low-quality CSR policies enforce the incidence and quality of programs in comparison with having no policy at all. Fourth, weak programs have more impact on the realization of CSR goals than having no program at all. The authors also find that the quality of CSR reporting (as measured by the implementation level of Global Reporting Initiative guidelines) and locating the responsibility for CSR at the board level reduce decoupling by strengthening the quality of CSR programs.

More and more companies now employ various kinds of corporate social responsibility (CSR) policies and instruments, such as codes of conduct, memberships in global initiatives like the UN Global Compact, ISO certifications, and various types of cooperation with stakeholder initiatives. Several studies have been performed to analyze the factors that influence the adoption of these practices (Brown, Vetterlein, & Roemer-Mahler, 2010; Lin & Ho, 2011). But the impacts of these policies and instruments in terms of the realization of social and environmental goals are uncertain. Therefore, Banerjee (2008) can argue that CSR initiatives are really nothing more than window dressing. Other critical authors argue that whereas the triple bottom line approach calls on companies to weigh effects on stakeholders and the environment alongside profit, in practice companies have co-opted it and shifted toward a business ethics agenda that supports rather than questions business practices and only adopted CSR insofar it can be aligned to narrow strategic interests (Marens, 2008).

Various models on corporate social performance (CSP) have been developed that explicitly distinguish CSR policies, CSR implementation, and their impacts (Carroll, 1979; Mitnick, 1995; Orlitzky, Swanson, & Quartermaine, 2006; Wood, 1991). By studying the relationship between CSR policies, implementation, and their impacts, we can identify whether CSR is merely ceremonial or whether it is really substantive. CSR is ceremonial if companies decouple policies from implementation and/or impacts. Institutional theory states that the main reason for companies to decouple is the tension between a company having to gain social legitimacy from its (often competing) stakeholders, while also facing pressures to maintain internal efficiency (Meyer & Rowan, 1977). Decoupling is expected to be especially tempting in a complex, globalized world order, as decoupling is more likely in loosely coupled organizational fields, characterized by ambiguity, uncertainty, multiple conflicting expectations, high transaction costs, limited regulatory commitment, and the absence of mechanisms to monitor compliance (Greenwood & Hinings, 1996). Therefore, it seems particularly relevant for CSP which typically encompasses activities beyond regulatory compliance and therefore will be more relevant in environments in which decoupling is expected to be more present. Also competing stakeholder interests can make it attractive to uphold an ideal image to gain legitimacy of enough stakeholders (Harrison & Freeman, 1999). Several studies found that such legitimacy pressures can result in decoupling processes whereby corporate responses to external demands vary in the extent to which they are symbolic or substantive (Jamali, 2010; Meyer & Rowan, 1977; Okhmatovskiy & David, 2012).

Bromley and Powell (2012) distinguished two types of decoupling. The first type concerns the link between policies and implementation: Although companies may pretend to do well by communicating policies, and therefore gain legitimacy, these policies might not result in the implementation of these CSR issues. Without implementing policies by using programs and management systems, the effectiveness of CSR may be at risk. The second type concerns the link between the implementation of programs and the concrete results of these programs: When programs are not adequately implemented, impacts may be lacking.

Several empirical studies on CSP show the relevance of the first type of decoupling, whereby managers tend to respond to external pressures by adopting policies that are decoupled from core processes (Greening & Gray, 1994; Weaver, Treviño, & Cochran, 1999b). Only a few studies have looked yet into the incidence of the second type of decoupling (Bromley & Powell, 2012). With respect to environmental impacts, Friedman and Miles (2001) and Ammenberg and Hjelm (2003) studied the impacts of environmental management systems and found that the establishment of a joint environmental management system in Britain and Sweden, respectively, resulted in environmental improvements. However, both studies are based on a limited number of case studies of small- and medium-sized enterprises, and the results are therefore difficult to generalize. Also Annandale, Morrison-Saunders, and Bouma (2004) studied the first type of decoupling but only on the basis of interviews among representatives of 40 companies from Australia. They found that the implementation of environmental management systems substantially improves environmental performance and is more effective than environmental reporting. Furthermore, no empirical studies are available that consider social and environmental impacts simultaneously in a framework in which also the organization of CSR at the business level is included. Because of this limited evidence, it remains uncertain to what extent the combination of CSR policies and their implementation with programs really leads to impacts. This gap is a very serious one in the field of CSR research, because if CSR fails to have favorable social and environmental impacts on society, the whole concept may become redundant.

This article aims at filling this gap in the literature and studies four hypotheses on the incidence of both types of decoupling and how they depend on conditions regarding the quality of reporting and the degree of centralizing responsibility for CSR in the company. By employing data from rating agency Sustainalytics, we test these hypotheses on a large sample consisting of about 1,000 companies from 24 countries for various concrete social and environmental issues.

The remainder of this article is structured as follows. The “Conceptual Framework” section develops a conceptual framework on CSP that explicitly distinguishes CSR policies, the implementation of CSR programs, and their impacts, and presents the four hypotheses. The “Method” section describes the methodology and the measures used in the empirical analysis. The results of the empirical analyses are presented in the “Results” section. The final section presents the conclusions and policy recommendations.

Conceptual Framework

Defining CSR Policies, Implementation, Impacts, and Decoupling

The authors specify a model for the impacts of CSR at the business level that resembles the structure of CSP models in literature. In line with Wood (1991, 2010) and Jamali and Mirshak (2007), we distinguish a policy part, an implementation part, and an impact part: First, companies set CSR policies; second, they make decisions about implementation of CSR programs; and third, the CSR programs may lead to certain desirable CSR impacts.

Policies refer to “a company’s environmental [or social] intention declared externally or internally in formal arguments, including written and published symbolic statements, declarations and slogans about environmental [or social] management” (Rhee & Lee, 2003, p. 177). By stating their policies, companies acknowledge and define their responsibility for specific issues (Skjaerseth & Wettestad, 2009). The development of an environmental policy, for example, is considered by many authors as the first major step toward commitment to environmental issues within the business agenda (Gray, Bebbington, & Walters, 1993).

Implementation consists of programs companies use to integrate CSR in the company’s organization. As implementation is guided by CSR policies, CSR implementation can be considered as the action part of the model and the mediator between policies and impact. The more CSR policies are integrated into a company’s practices by the use of high-quality CSR programs, the more likely it is to be successful in terms of impacts and sustainable over time (Hess & Warren, 2008).

The impacts of CSR refer to the realization of CSR goals in the social and environmental dimension at the business level. Examples are employees’ health and waste production by the company.

Whereas the literature on CSP has improved our understanding of the various elements that constitute CSP, the theoretical and empirical analysis of the relationships between these elements is still underdeveloped. Studying these relationships is very important, as the literature on decoupling strategies shows that it cannot simply be assumed that policies encourage companies to implement CSR programs and that these programs generate favorable impacts.

The first type distinguished by Bromley and Powell (2012), policy-practice decoupling, concerns the relationship between policies and the implementation of programs. Most current studies on decoupling only focus on this type. An example of this type of decoupling is the case of British Petroleum (BP). In 2000, BP reportedly spent US$ 7 million on researching the new “Beyond Petroleum” Helios brand and US$ 25 million on a campaign to support this brand change (Hawn & Ioannou, 2015). Greenpeace later concluded that “this [was] a triumph of style over substance. BP spent more on their logo [that] year than they did on renewable energy [the previous] year” (Visser, 2011). BP seemed to make many efforts to show its intentions to the public instead of making the more costly effort of also implementing it into the company.

The second type of decoupling distinguished by Bromley and Powell (2012), means-ends decoupling, concerns the relationship between the implementation of programs and the impacts. In this second type, programs are implemented but with uncertain relationships to impacts. For example, many pharmaceutical companies had implemented social initiatives that involved donating drugs to developing countries. These drugs, however, appeared to be frequently past their expiration date. This problem was so widespread that the World Health Organization had to issue guidelines to prevent such “dumping” (Joshi & Sanger, 2005). Therefore, although companies could gain legitimacy by saying they were donating drugs, and also really acted on these words, the impacts of their drugs donation were found to be negligible or even negative.

In a study to the compliance of Chinese suppliers with Swedish toy retailers’ code of conduct, Egels-Zandén (2007) showed that Chinese suppliers had consciously developed methods for deceiving the monitoring organizations. The suppliers had seemingly successfully managed to decouple the formally monitored part from the actual operational part of their programs, leading to few areas of noncompliance being detected by the monitoring organizations, despite the fact that in practice there were multiple areas of noncompliance. Therefore, although programs were in place, no concrete impacts would have been detected. Indeed, Nash and Ehrenfeld (2001) showed that two organizations that implement identical (environmental) management systems can realize very different results. Results depend on the motivation behind adoption and how the rules and resources demanded by the environmental management system (EMS) are integrated into the culture of the organization (Nash & Ehrenfeld, 2001). This circumstance furthermore implies that even companies that act in good faith and adopt seemingly identical social initiatives may have significantly different impacts on society based on the amount of resources devoted to the project and its integration with the companies’ strategy and culture.

Whereas the examples of decoupling discussed above can be associated with low moral standards, it should be noted that impacts are not always unilateral in companies’ own hands to determine as they also depend on the cooperation of other partners. For example, companies have limited power to guarantee that environmental and/or social standards are respected in the supply chain. Although they can take many actions to reduce the chance of low performance (in the selection of partners or controlling their working conditions and putting pressure in case of low performance), they cannot completely control or force supply chain partners to undertake specific actions to maintain these standards.

Hypotheses

As theoretical background, we use the framework that Delmas and Burbano (2011) developed for conditions of greenwashing. 1 Greenwashing is a phenomenon related to decoupling. Whereas decoupling refers to the combination of promising policy statements and poor implementation of programs and impact, greenwashing is defined as the intersection of positive communication about performance (e.g., through reporting) and poor performance (Delmas & Burbano, 2011, p. 4). Delmas and Burbano explain the incidence of greenwashing from (a) nonmarket external drivers (regulatory environment and nongovernmental organization [NGO] monitoring), (b) market external drivers (consumer demand, investor demand, and competitive pressure), (c) organizational drivers (firm characteristics, effectiveness of intrafirm communication, incentive structure and ethical climate, and organizational inertia), (d) and individual drivers (optimistic bias, narrow decision framework, and hyperbolic intertemporal discounting).

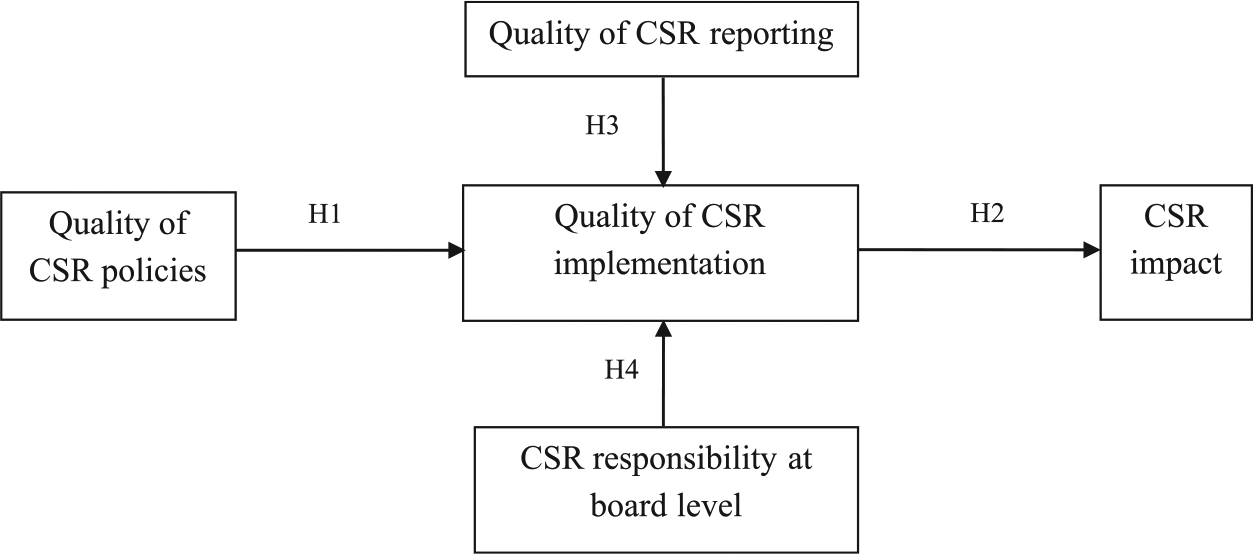

The research question addressed in this study is if and when decoupling between CSR policies and implementation and between implementation and impacts takes place. The authors posit (see Figure 1) two hypotheses on the incidence of decoupling (Hypotheses 1 and 2) and two hypotheses on the conditions that make decoupling less likely (Hypotheses 3 and 4).

Conceptual framework and hypotheses.

The initial two hypotheses concern the relationship between policy-practice decoupling and quality of CSR policies, and between means-ends (practice-impacts) decoupling and quality of CSR implementation. Our framework separates among the two kinds of decoupling identified by Bromley and Powell (2012). The degree of decoupling is not the dependent variable in this framework, rather the degree of decoupling refers to the magnitude of the estimated coefficient of the independent variable on the dependent variable in each hypothesis. The hypotheses thus do not take the conventional form of positive or negative association between dependent and independent variables. Policy-practice decoupling is present if having a high-quality policy does not lead to a higher incidence of having a better CSR program than a low-quality policy or not having a policy. A similar interpretation holds for the other hypothesis as well. The final two hypotheses examine how quality of CSR reporting and allocation of CSR responsibility to the board of directors improve implementation quality. The study thus tests for relationships among CSR dimensions to provide evidence for degree of decoupling. Presently, we can only test pieces of this framework in isolation. However, the more the evidence against complete decoupling that can be found in the sample data, the stronger the likelihood that complete decoupling is not occurring and therefore by inference the stronger the relationships between CSR policies, implementation, and environmental and social impacts are likely to be.

The incidence of policy-practice decoupling can be studied by analyzing the magnitude of the effect of CSR policies on CSR programs. The smaller the effect of having a CSR policy on having a CSR program implemented, the higher the degree of decoupling. Hypothesis 1 goes beyond this notion by also taking into account the quality of CSR policies. Taking also the quality into account allows a more accurate identification of policy-practice decoupling as one would expect that policy-practice decoupling is more likely for companies with policies of low quality than for companies with policies of high quality. Policy-practice decoupling is then present if the magnitude of the effect of CSR policies on (the quality of) CSR programs is not higher for high-quality CSR policies than for CSR policies of low quality. Complete policy-practice decoupling would imply that even companies with policies of high quality do not show a higher implementation level of CSR programs than companies with no policy at all. Reversely, if the estimation results show that having a weak policy significantly increases the incidence or quality of a program, we can conclude that even weak forms of decoupling are not present. We define the quality of a policy by the following three procedural criteria (Sustainalytics, 2012): Companies have a stronger CSR policy when it (a) is a formal and written statement, (b) applies company-wide, and (c) describes responsibilities in a detailed instead of only generic way. Based on these three criteria, we distinguish four different qualities of policies—A: no policy, B: weak policy (the company has a written policy statement that is not very detailed), C: adequate policy (the company has a detailed, written, policy statement, but it only addresses a few issues), and D: strong policy (the company has a detailed, written, policy statement for all important issues).

The intuition behind Hypothesis 1 can be argued as follows. A written, company-wide, policy statement on CSR reduces the ambiguity about the intentions of the company. By formulating detailed commitments that cover a large part of its operations, the company thus decreases the ineffectiveness of intrafirm communication (the third condition in Delmas and Burbano’s framework).

Furthermore, when formal CSR policies are an organizational facade intended to promote positive external perceptions, working behind that facade is likely to negatively affect insiders’ perceptions of legitimacy (Nystrom & Starbuck, 1984) and crowd out the ethical climate in the company. MacLean and Behnam (2010) found that policy-practice decoupling negatively affects internal legitimacy perceptions, enabling the institutionalization of misconduct by company members and ultimately leading to a loss of external organizational legitimacy. It is therefore expected that companies that have strong CSR policies also will implement them in such a way that impacts will result.

Third, formal and written statements with detailed commitments raise the expectations of external stakeholders. A company that formulates a strong policy in this way but generates no impact, because the CSR policy is not implemented by a (high-quality) program, will be regarded as a hypocrite and, given a well-functioning reputation mechanism, be punished by its stakeholders. This negative reputation effect links to Delmas and Burbano’s first condition for greenwashing, the threat of exposure by NGOs or the media. Companies with no CSR policies or weakly stated policies raise fewer expectations among NGOs and will therefore be less severely criticized for low CSP. Indeed, Janney and Gove (2011) found that when companies possess an enhanced reputation for a given dimension of CSP, violations for not acting on words related to that dimension are more harshly sanctioned. Companies with high-quality policy statements will therefore have a stronger incentive to install strong CSR programs.

The means-ends decoupling thesis holds that implementation of CSR activities does not necessarily lead to impact. But, again, it is likely that the incidence of decoupling depends on the quality of the CSR program. Only if companies implement CSR activities in a superficial manner, it may be expected that they will not lead to major impacts. In our framework, Hypothesis 2 is tested by analyzing the influence of the quality of CSR programs on CSR impacts. Complete means-ends decoupling would imply that even companies employing CSR programs of high quality do not produce better CSR impacts than companies having no CSR programs at all. Following Sustainalytics (2012), we define the quality of CSR programs by the following three procedural criteria: Companies have a high-quality implementation program if (a) the program covers a large part of the company’s operations, (b) the company sets targets for improving CSR impacts, and (c) the company applies strict deadlines for realizing these targets. 2 Based on these three criteria, we distinguish four different qualities of programs—A: no program; B: weak program that only applies to part of the company’s operations; C: adequate program that applies to all operations, but no quantitative targets or clear deadlines; and D: strong program with quantitative targets and clear deadlines.

The intuition behind Hypothesis 2 is as follows. Broad coverage is an important condition for quality. If CSR programs are only applied to a small subset of the company’s activities, their impacts for the company as a whole will be negligible. Second, target setting is a proven management tool for initiating change and improvement (Palmer & van der Vorst, 1997). The use of targets for CSR requires identification of indicators. After the selection of indicators, the management will have to develop methods to collect data for the indicators to set appropriate targets. This data collection offers quantitative or qualitative information of the organizational performance. High-quality implementation programs will thus stimulate managers to develop a systematic framework for tracking issues, bringing focus and discipline, and providing better documentation, which will improve social or environmental awareness (Annandale et al., 2004). As a result, the ambiguity and uncertainty about what CSR comprises are reduced and internal mechanisms to monitor compliance improved, which will reduce the probability of means-ends decoupling. This reduction of ambiguity and uncertainty about what CSR comprises links to the third and fourth conditions in Delmas and Burbano’s framework: by clarifying what CSR implies, the internal transfer of knowledge about CSR improves, and coordination of CSR between different divisions in the company is facilitated. Better information also reduces bounded rationality of the managers of the organization (such as unrealistic positive self-evaluation) by giving them tools to improve their evaluation of the CSR of their company. The third element of high-quality implementation programs (strict deadlines) is necessary, as targets will only stimulate action if they are defined within a clear time framework. If thus well integrated into the company’s organization, implementation of CSR programs can be considered as “built-in” CSR, rather than only as “bolt-on” CSR (Barth & Wolff, 2009).

Hypothesis 3 links to one of the recommendations of Delmas and Burbano that they derive from their framework, namely, that transparency of CSP should be increased. The transparency of CSP depends on the quality of CSR reporting. Criteria for high-quality reporting are the statement of objectives, an account to society, disclosure to the intended audience, and the inclusion of nonmanipulated, and therefore often preferable raw, data (Gray, Owen, & Maunders, 1987).

The Global Reporting Initiative (GRI) gives guidelines for CSR reporting. The GRI was established in 1997 after the acknowledgment that companies were increasingly receiving multiple, diverse, and incompatible requests for information, and the difficulties to compare companies rose also because of the increasing numbers of reporting guidelines and frameworks being introduced in various sectors and countries (Willis, 2003).

Hypothesis 3 now states that a higher quality of CSR reporting will induce companies to improve the quality of their CSR programs, which will reduce policy-practice decoupling. As Delmas and Burbano (2011) argued, an increase in the transparency of CSP will enable consumers and investors to hold companies accountable for communication about their performance, strengthening the external market drivers to reduce decoupling. If companies report on their CSR programs and impacts in a credible and clear way, they enable outsiders to check the company’s CSP (Mitnick, 1995). The visibility of their CSP will reduce its ambiguity, which is one of the causes of decoupling. More transparency on CSP enforces the reputation mechanism (Hess, 2007). The more information is available, and the higher the quality of this information through better reporting practices, the easier it is for its stakeholders to reward or punish the company. More transparency will raise the probability that negative social and environmental incidents are communicated to the public, which can destroy reputations and lead to lower turnover. As predicted by the resource-based view of the company, intangibles like CSP reputation are important mediators through which CSP improves the (long-term) financial performance of the company (Surroca, Tribo, & Waddock, 2010). Better reporting practices, therefore, reinforce the incentive to install a high-quality implementation program for CSR to secure good CSR impacts and prevent reputation loss caused by negative incidents.

Furthermore, Delmas and Burbano (2011) argued that increasing the availability of information about the company’s performance will provide managers with readily available information by which to compare their company’s performance with communication about this. High-quality CSR reporting will therefore also improve the effectiveness of intrafirm communication and make inconsistencies between policy statements and impacts more visible within the company. This improved visibility of inconsistencies might stimulate the cooperation between CSR of public relationship managers and other division managers in the company to reduce the gap between policy statements and impacts by improving the implementation of CSR. Besides, information about the company’s performance will enable managers to make better informed decisions, thereby reducing psychological limitations to rational choice.

The integration of CSR policies into the organizational processes is likely to be supported by organizational structures that make managers accountable to it. Those companies that rate CSP as a highly important issue will assign organizational responsibility at board level rather than at lower levels in the company. Delmas and Burbano (2011) argued that the company’s leaders play an important role in implementing an ethical climate change in the company, which is one of the organizational drivers to reduce greenwashing in their framework. This role will also affect the quality of the company’s CSR programs. The commitment of the top management is an important factor that influences the quality of implementation of CSR (Christensen, Mackey, & Whetten, 2014; Swanson, 2008; Weaver, Treviño, & Cochran, 1999a; Weaver et al., 1999b). If top management is genuinely committed to CSR, it will take responsibility by itself that CSR policies are well embedded into processes, practices, and performance appraisal. 3 Committed board members will not be satisfied with communications that can easily be decoupled from practices but also require more deeply embedded organizational activities. Their questions will stimulate the employees’ awareness and thinking about how socially responsible outcomes can be achieved (Waldman, Siegel, & Javidan, 2006). Indeed, without managerial commitment, employees may feel that they can easily ignore issues of ethical responsibility in their working lives (Collier & Esteban, 2007). If companies delegate the responsibility for CSP to lower levels in the organization, chances are higher that companies only pay lip service to stakeholders’ expectations without coupling them to serious implementation, as without a clear commitment of top management, the company’s CSR practices may be easily ignored by employees. Furthermore, allocation of CSP responsibility at the top level of the company is also a strong signal to external stakeholders that the company is really committed to CSR and will therefore increase the societal expectations. Higher social expectations will provide the company with another incentive to take care that CSR is well implemented so that impacts are consistent with the signal of commitment toward CSR to avoid reputational damage. Hypothesis 4 therefore relates the quality of the CSR implementation programs to the allocation of responsibility for CSP at the top level of the company.

Method

Sample

To provide information on CSP, independent rating systems (often called “environmental, social and corporate governance (ESG) ratings”) have been developed by rating agencies such as Kinder–Lydenberg–Domini (KLD), Thomson Reuters’ ASSET4, Vigeo, and Sustainalytics. In our study, we use indicators from Sustainalytics, because, in comparison with other rating systems, the Sustainalytics rating system more explicitly distinguishes among ratings of the quality of policies (like policies on discrimination), use and quality of implementation (like programs to increase workforce diversity), quality of reporting, allocation of responsibility in the company, and impacts. These indicators match the concepts distinguished in our conceptual framework well.

To test the validity of the data of Sustainalytics, we did a comparative statistical analysis of overall ESG ratings of Sustainalytics and the ESG ratings of Thomson Reuters’ ASSET4 for companies that are rated by both rating agencies. For 2010, we found a bivariate correlation coefficient of .664 (p < .01) which indicates a high convergence. We did a similar analysis for Morgan Stanley’s ESG ratings (previously KLD) and found a bivariate correlation coefficient of .631 (p < .01) for the ratings in 2010 for companies that are rated by both Sustainalytics and Morgan Stanley’s ESG. These results indicate the validity of the ESG ratings of Sustainalytics.

To test for common method bias, we carried out Harman’s single-factor test. If a substantial amount of common method variance exists in the data, a single or general factor that accounts for most of the variance will emerge if all the variables are entered together (Podsakoff, MacKenzie, Lee, & Podsakoff, 2003). An unrotated principal components analysis on the 19 indicators taken from the Sustainalytics database that we use revealed seven factors with eigenvalues greater than 1.0, which together accounted for 60% of the total variance. The largest factor did not account for a majority of the variance (22.6%). This finding indicates that common method bias is not a great concern.

Empirical Framework and Measures

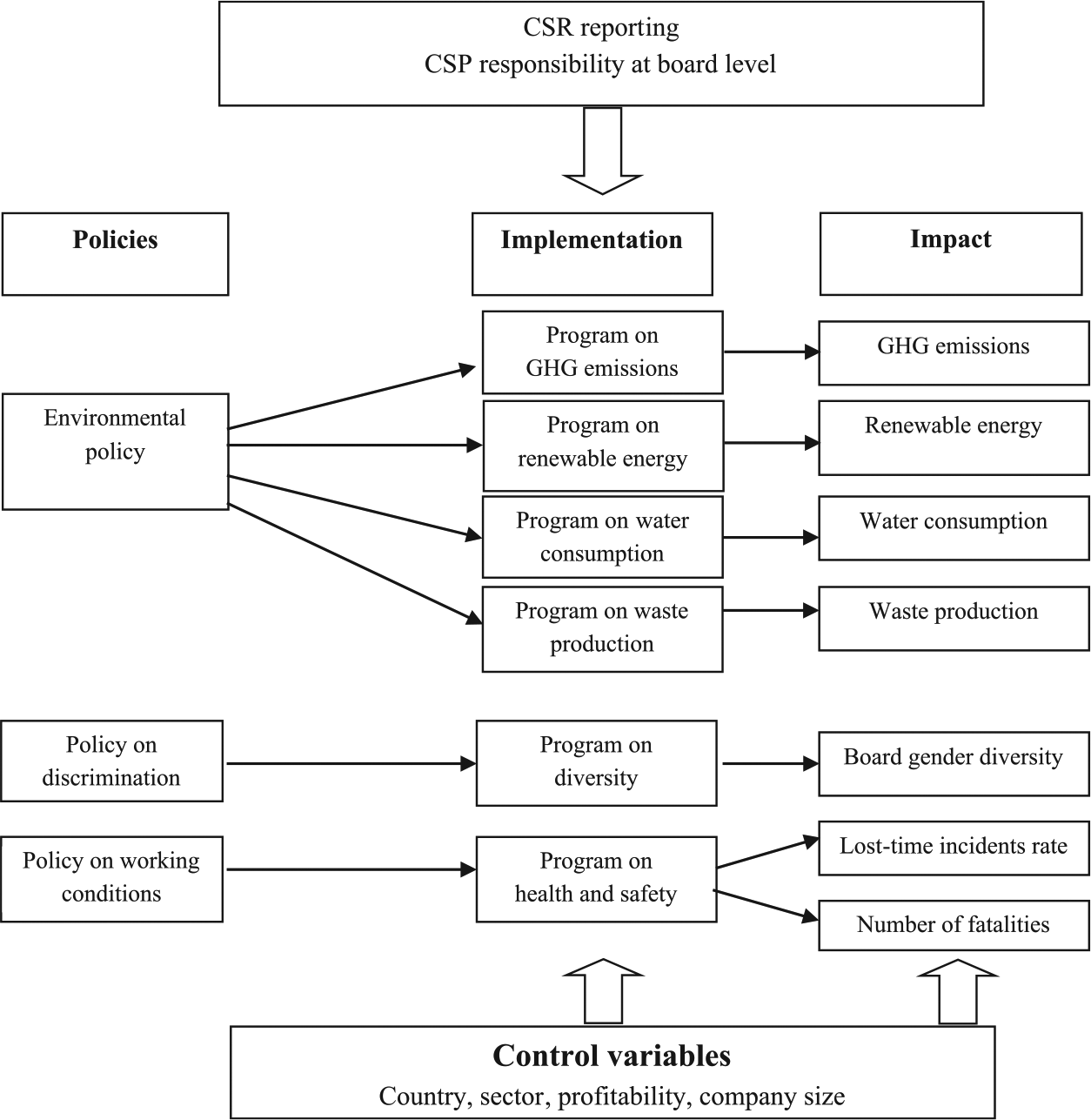

We selected CSR issues for which sustainability has indicators on CSR policies as well as on CSR implementation and on CSR impact. Based on the available indicators in the Sustainalytics data set, we distinguish four environmental chains and two social chains linking CSR impacts to CSR implementation and CSR implementation to CSR policies (see Figure 2). A chain is the relationship between a policy on a specific issue (e.g., greenhouse gas [GHG] emissions), a program on that issue, and the realized impacts on that issue.

Operationalization of conceptual framework.

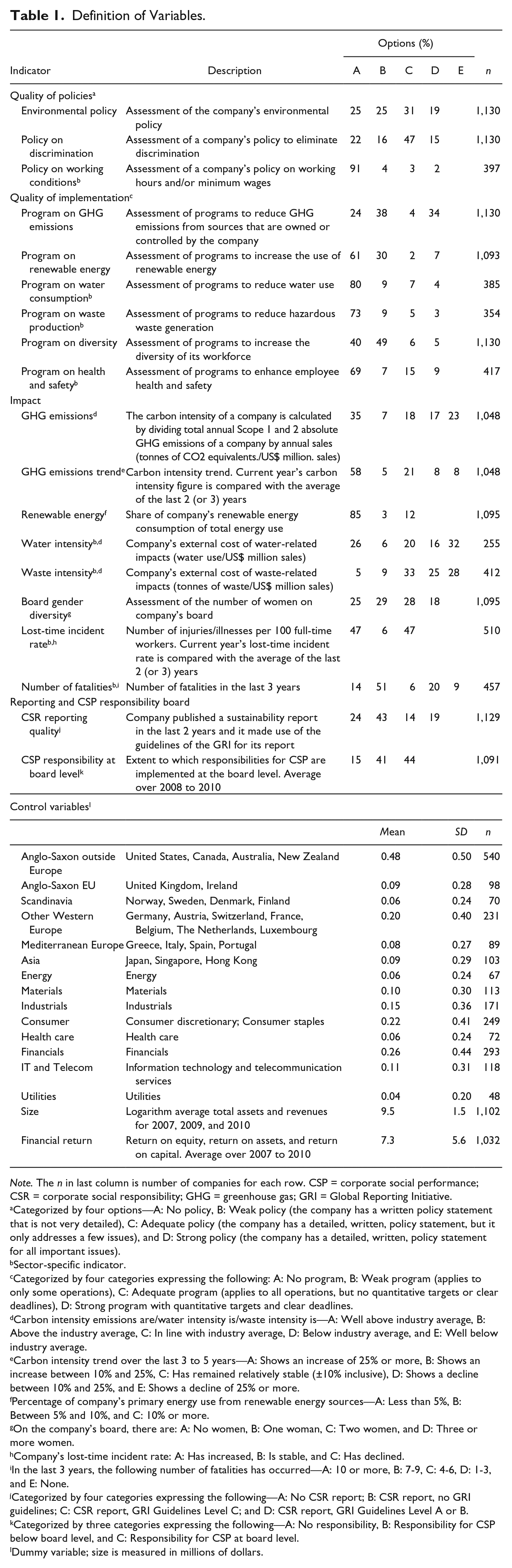

Table 1 summarizes the various indicators that we use. The first set of variables concerns various CSR policies in 2008. Based on the criteria presented above, Sustainalytics distinguishes four categories for the quality of CSR policies (no policy, weak policy, adequate policy, and strong policy). We therefore created four dummies for each different category to estimate the different effects of different qualities in CSR policies. For CSR policies as dependent variable (in Table 4), we used the Sustainalytics data which are defined as a weighted average of these dummies. For environmental policies, Sustainalytics uses one measure that indicates the extent to which a company makes use of a formal environmental policy that guides its environmental CSR activities. For social policies, we use two variables. For gender diversity, we use the Sustainalytics data on policies on discrimination, which includes statements on equal opportunity and elimination of discrimination based on gender (as well as other topics, such as discrimination on grounds of race, religion, etc.). For working conditions, we use Sustainalytics measure of “policies on working conditions,” which is a sector-specific indicator and therefore only applies to specific sectors, reducing the sample to, in this case, 397 companies.

Definition of Variables.

Note. The n in last column is number of companies for each row. CSP = corporate social performance; CSR = corporate social responsibility; GHG = greenhouse gas; GRI = Global Reporting Initiative.

Categorized by four options—A: No policy, B: Weak policy (the company has a written policy statement that is not very detailed), C: Adequate policy (the company has a detailed, written, policy statement, but it only addresses a few issues), and D: Strong policy (the company has a detailed, written, policy statement for all important issues).

Sector-specific indicator.

Categorized by four categories expressing the following: A: No program, B: Weak program (applies to only some operations), C: Adequate program (applies to all operations, but no quantitative targets or clear deadlines), D: Strong program with quantitative targets and clear deadlines.

Carbon intensity emissions are/water intensity is/waste intensity is—A: Well above industry average, B: Above the industry average, C: In line with industry average, D: Below industry average, and E: Well below industry average.

Carbon intensity trend over the last 3 to 5 years—A: Shows an increase of 25% or more, B: Shows an increase between 10% and 25%, C: Has remained relatively stable (±10% inclusive), D: Shows a decline between 10% and 25%, and E: Shows a decline of 25% or more.

Percentage of company’s primary energy use from renewable energy sources—A: Less than 5%, B: Between 5% and 10%, and C: 10% or more.

On the company’s board, there are: A: No women, B: One woman, C: Two women, and D: Three or more women.

Company’s lost-time incident rate: A: Has increased, B: Is stable, and C: Has declined.

In the last 3 years, the following number of fatalities has occurred—A: 10 or more, B: 7-9, C: 4-6, D: 1-3, and E: None.

Categorized by four categories expressing the following—A: No CSR report; B: CSR report, no GRI guidelines; C: CSR report, GRI Guidelines Level C; and D: CSR report, GRI Guidelines Level A or B.

Categorized by three categories expressing the following—A: No responsibility, B: Responsibility for CSP below board level, and C: Responsibility for CSP at board level.

Dummy variable; size is measured in millions of dollars.

For CSR implementation, Sustainalytics developed measures for each of the four environmental and two social chains. Based on the three criteria for program quality discussed in the “Conceptual Framework” section, we created four dummies per quality type of programs (expressing no, a weak, an adequate, and a strong program). The environmental variables measure the quality of the programs that companies have implemented to decrease GHG emissions or increase the use of renewable energy. We also use two sector-specific implementation variables: the implementation of a program on water consumption and a program on waste production. Besides these four environmental implementation variables, we use two implementation variables concerning social issues, namely, programs that foster diversity in the company and programs to reduce health and safety incidents. All measures refer to 2009. For CSR programs as dependent variable (in Table 5), we used the Sustainalytics data which are defined as a weighted average of these dummies.

The quality of CSR reporting is measured by Sustainalytics by five categories ranging from no CSR report, CSR report not written according to GRI guidelines, and CSR report written according to GRI Level C+, B+, or A+, respectively. Based on this, we constructed four dummies (taking the last two categories together). To measure the location of responsibility for CSP in the company, we used the Sustainalytics “Responsibility for CSP at the Board Level,” which distinguishes three categories: no allocation of responsibility for CSR issues, below board-level allocation of CSR responsibilities, and board responsibility for CSR issues.

We measure CSR impact with four environmental and three social variables. Sustainalytics uses three to five categories for classifying the company’s performance for these variables (see Footnotes f-k in Table 1). All measures are measured in 2010, except the waste production, for which we only have data for 2009. The first environmental impact variable concerns the carbon intensity of the company and is measured as an average of the assessment of the ratio between the absolute emission level and turnover in 2010 and the trend in the past 2 or 3 years relative to industry average. Sustainalytics uses the methodology developed by the GHG Protocol to categorize GHG emissions. The second environmental impact variable, the trend in carbon intensity in 2010, is not measured relatively to other companies but relatively to the company’s past performance. For this purpose, Sustainalytics compares the 2010 intensity with the average of the 3 (or 2) previous years (2007, 2008, and 2009). The third environmental impact variable concerns the share of renewable energy that the company consumes. Water consumption and waste production are sector-specific indicators and therefore not available for all the companies in our sample; these variables are again measured relative to industry average. Of the three social measures, one measures the number of women in the board, whereas the others measure the trend in lost-time incidents and the number of fatalities related to health and safety issues. Both the trend in the lost-time incident rate and the number of fatalities are sector-specific indicators.

Control Variables

In testing the core relationships in our conceptual framework, we control for various influences in the external and internal business environment. First, institutional theory states that the different institutional settings in which companies operate may affect their CSP (Brammer, Jackson, & Matten, 2012; Matten & Moon, 2008). As Delmas and Burbano (2011) argued, the regulatory context will also affect greenwashing. If regulation of CSP is weak, it is easier for companies to get away with decoupling. We therefore control for region with six regional dummy variables. We used the categorization proposed by Moon, Brunn, Hardy, Slager, and Steen-Knudsen (2012), which is based on different types of capitalism.

Delmas and Burbano (2011) also argued that company characteristics, such as industry, profitability, and company size, influence the overall strategies available to the company. We therefore control for the sector in which the company operates, financial return, and company size. The nature of the production processes or products determines the type of social and environmental externalities that a company creates (Brown et al., 2010). Also the incentive to translate CSR policies into implementation programs and impacts may differ for different sectors, as market external pressures vary among sectors (Brammer & Pavelin, 2006). For sectors, dummies were used for eight categories. Sectors were classified according to the Global Industry Classification Standard (GICS). We aggregated the information technology (IT) and telecommunication sectors for parsimonious reasons, as both sectors will resemble each other in terms of CSP.

Furthermore, companies will find it easier to translate their CSR policies into (costly) CSR implementation programs if the companies are more profitable. Slack resource theory predicts that better economic performance potentially results in the availability of slack resources, which provides opportunities for companies to invest in CSR (Waddock & Graves, 1997). Due to a lack of resources, in answering to the pressure of stakeholders, companies could end up with formal policies and stated commitments that they cannot uphold in practice. Profitability may, however, also be positively related to decoupling, as Delmas and Burbano (2011) argued that more profitable companies are better able to withstand bottom line shocks from reputational damage when being accused of greenwashing. To measure financial return, we use, as suggested by Griffin and Mahon (1997), a combination of various measures for financial performance: return on assets, return on sales, and return on equity. All the financial data in our analysis are taken from the S&P Capital IQ database. 4 The use of 3-year averages reduces the impact of possible accounting inconsistencies (Johnson & Greening, 1999).

Not only lack of financial resources but also knowledge about how to implement them may be lacking. Especially the size of the company is expected to influence this. In particular, smaller companies are often organized on a more informal basis and, due to a lack of experience, are often less able to explicitly implement CSR programs (Lepoutre & Heene, 2006). The size of the company was measured by the logarithm of the average of total revenues and total assets of the company during 2007 till 2010. By taking the average, we reduce possible biases due to temporary influences.

Endogeneity

Although we control for various control variables, it is still possible that there is endogeneity bias in our analysis, for example, due to unobserved heterogeneity, omitted variables, or simultaneity. To test the endogeneity of CSR policies in the regression analysis for CSR programs and the endogeneity of CSR programs in the regression analysis for CSR impacts, we used Hausman’s endogeneity test. For the three policies on environment, discrimination, and working conditions, we use the average score of the respective policies for the peer group to which the company belongs as instrumental variable. Sustainalytics distinguishes 38 peer groups of companies that are comparable with regard to type of products and production processes. It is likely that the practice of companies in the peer group informs a company, in its own decision, to introduce a policy statement. For programs, we use policies as instrumental variable, as it is likely that policies only influence impacts through their effects on programs. If the null hypothesis (hypothesizing there is no endogeneity) holds, that is, policies are exogenous to programs and programs are exogenous to impacts, the p value of the coefficients of the residuals of policies and programs should be insignificant in the equation for programs and impacts, respectively (Gujarati & Porter, 2009, p. 705). As will be shown below, the Hausman endogeneity test shows that CSR policies are exogenous to CSR programs, whereas in seven out of eight cases, CSR programs are exogenous to impacts.

Results

Before performing statistical analyses, we tested for heteroscedasticity. Plots showed no heteroscedasticity between the independent and the dependent variables. Given the fact that our sample is reasonable large, nonnormally distributed variables will not pose serious problems.

Bivariate Correlation Analysis

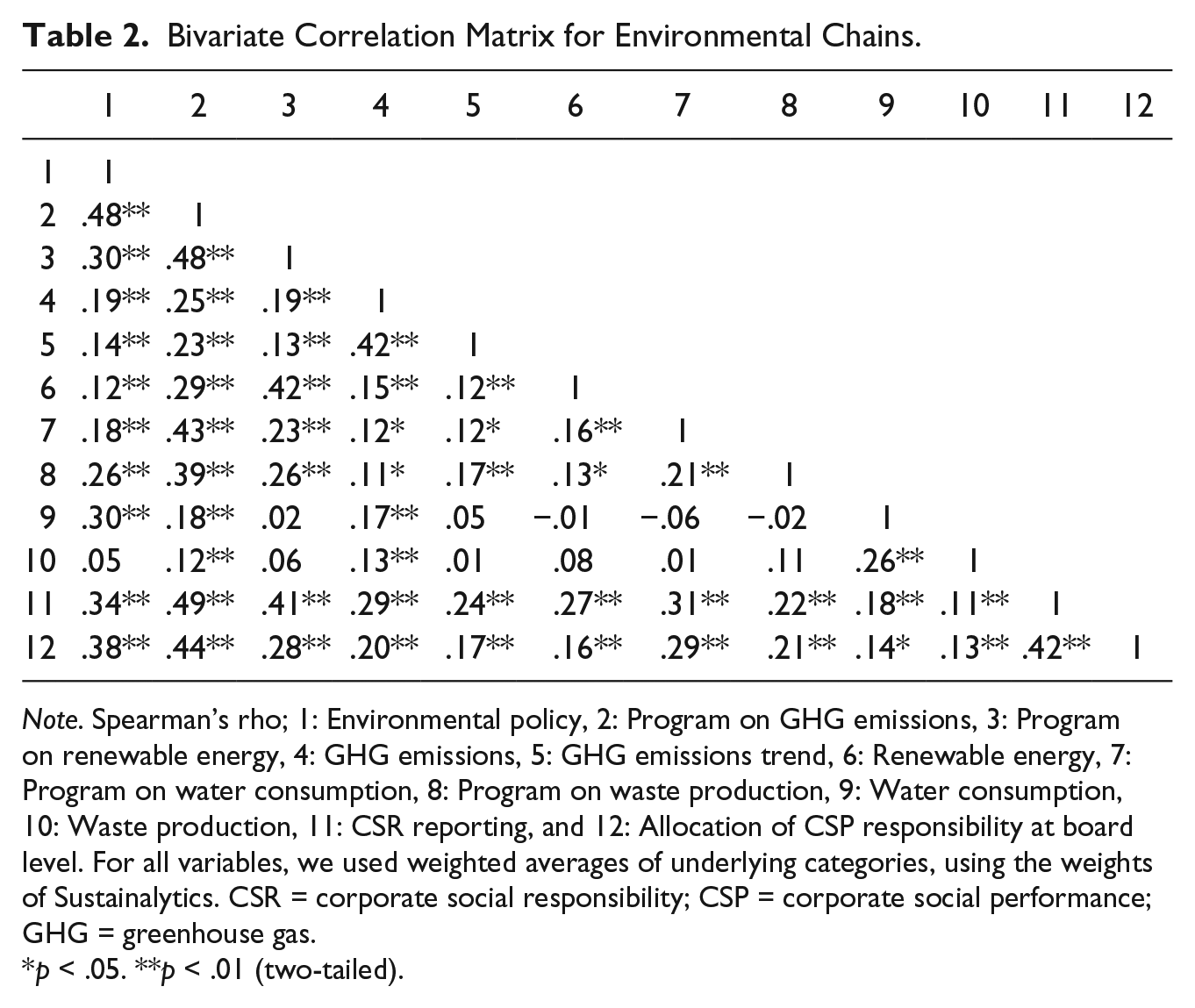

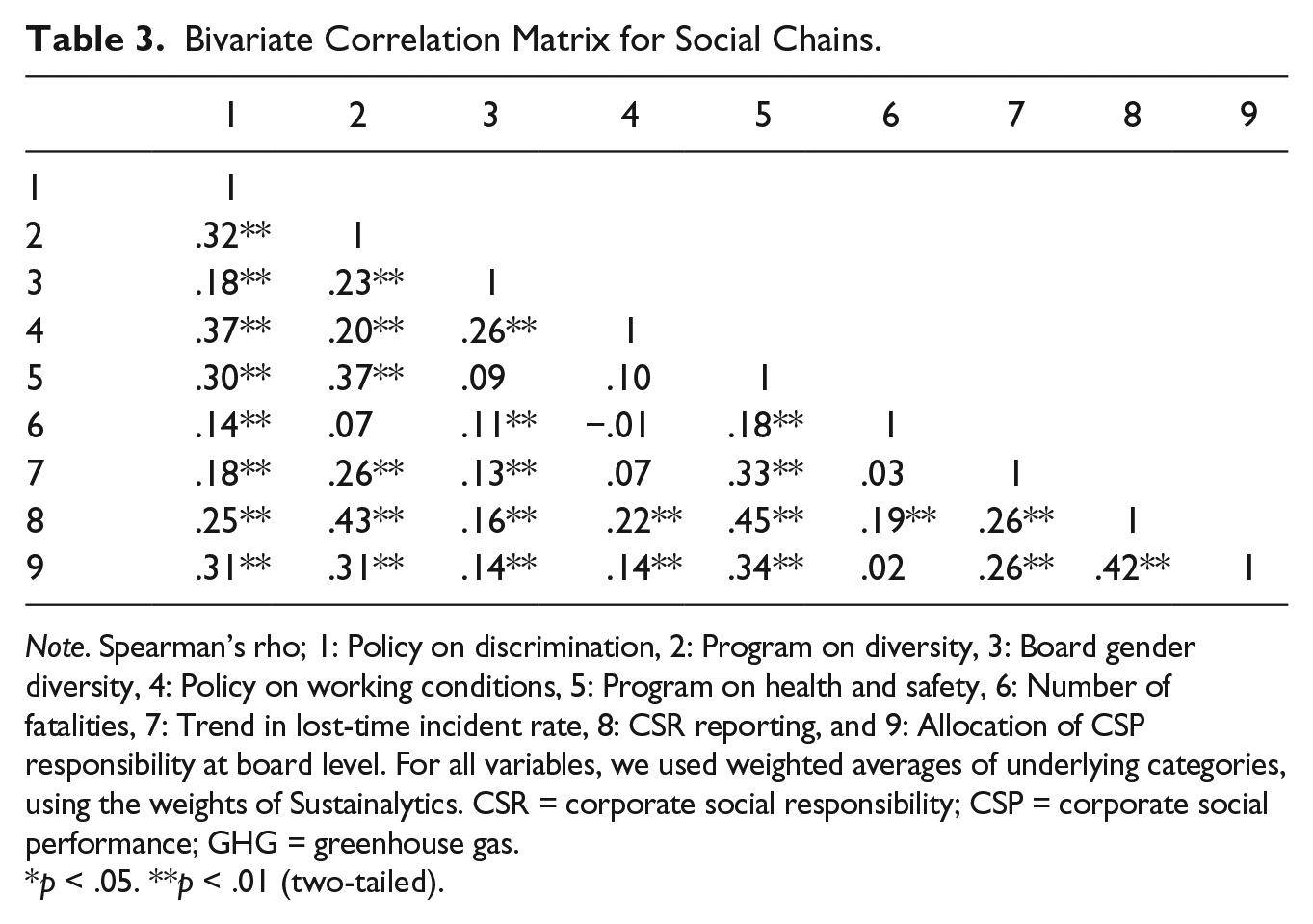

We first conducted bivariate correlation analysis to investigate the simple relationship between the various variables. Table 2 shows the correlation between the variables in the environmental chain. As the table shows, many correlations are significantly different from zero. The correlation coefficients, however, are not very high. This information indicates that the relationships seem to be quite complex. Table 3 shows the correlation coefficients of the various social indicators. As with the environmental indicators, many correlations are significantly different from zero, but the absolute value is not very high, again indicating a complex causal structure.

Bivariate Correlation Matrix for Environmental Chains.

Note. Spearman’s rho; 1: Environmental policy, 2: Program on GHG emissions, 3: Program on renewable energy, 4: GHG emissions, 5: GHG emissions trend, 6: Renewable energy, 7: Program on water consumption, 8: Program on waste production, 9: Water consumption, 10: Waste production, 11: CSR reporting, and 12: Allocation of CSP responsibility at board level. For all variables, we used weighted averages of underlying categories, using the weights of Sustainalytics. CSR = corporate social responsibility; CSP = corporate social performance; GHG = greenhouse gas.

p < .05. **p < .01 (two-tailed).

Bivariate Correlation Matrix for Social Chains.

Note. Spearman’s rho; 1: Policy on discrimination, 2: Program on diversity, 3: Board gender diversity, 4: Policy on working conditions, 5: Program on health and safety, 6: Number of fatalities, 7: Trend in lost-time incident rate, 8: CSR reporting, and 9: Allocation of CSP responsibility at board level. For all variables, we used weighted averages of underlying categories, using the weights of Sustainalytics. CSR = corporate social responsibility; CSP = corporate social performance; GHG = greenhouse gas.

p < .05. **p < .01 (two-tailed).

Regression Analysis of CSR Policies

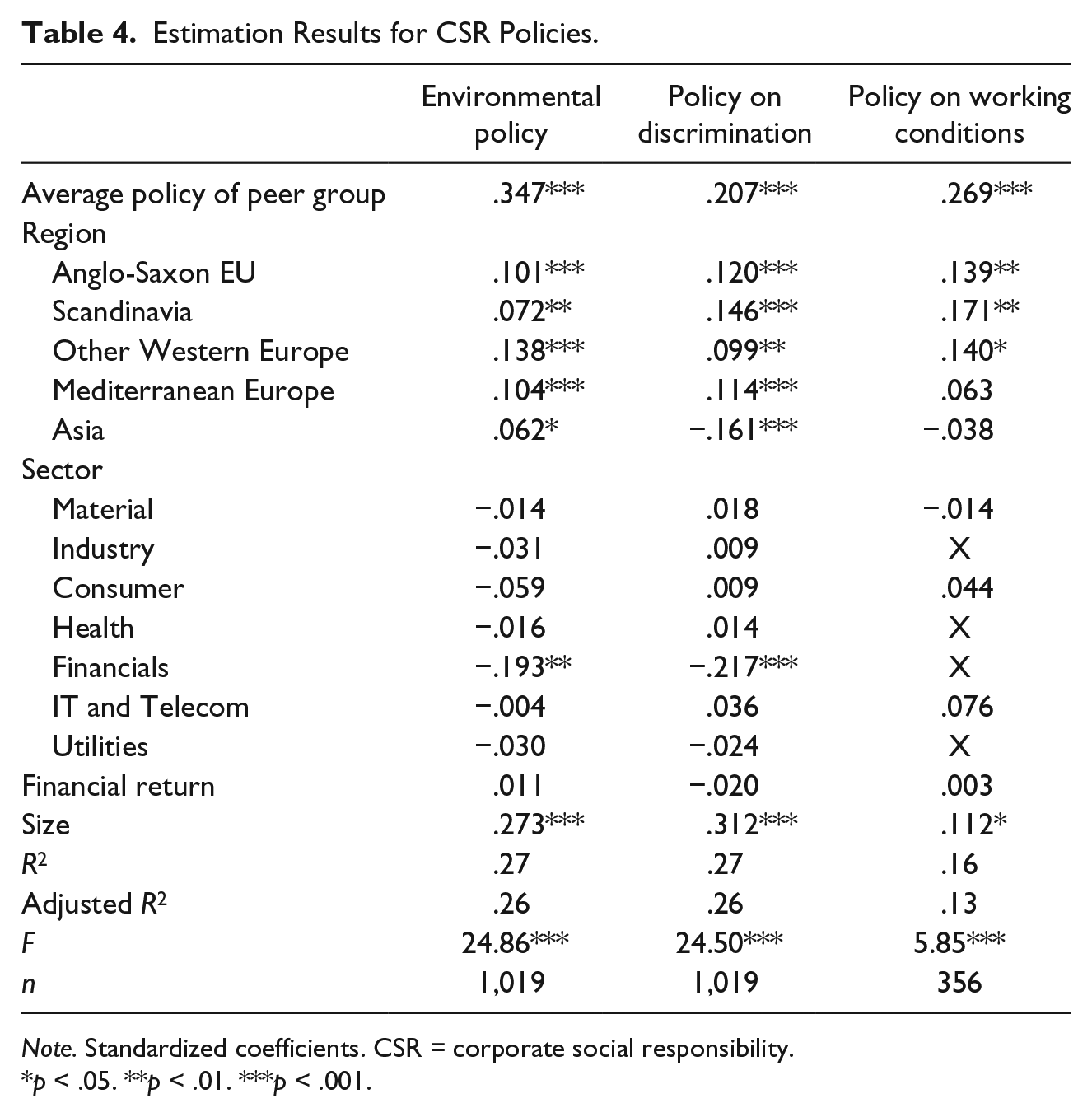

Before presenting the results of the regression analysis for CSR programs and CSR impacts, we first perform regression analysis for CSR policies. The results are reported in Table 4. For each policy, we included the control variables. For region, we used the Anglo-Saxon region outside Europe as reference variable. For sector, we took the energy sector as reference variable. When the dependent variables are only available for specific sectors (namely for working conditions), the sectors that are not included are indicated by an “X” in the table.

Estimation Results for CSR Policies.

Note. Standardized coefficients. CSR = corporate social responsibility.

p < .05. **p < .01. ***p < .001.

The estimation results show that the average score for the CSR policies of the peer group to which companies belong is highly significant (t-values vary between 4.41 and 9.50) and therefore qualifies as a strong instrument. Furthermore, we find that the quality of CSR policies depends positively on company size. Companies in Anglo-Saxon countries outside Europe and companies in the financial sector lack behind companies from other regions or sectors.

Regression Analysis of CSR Programs and Impacts

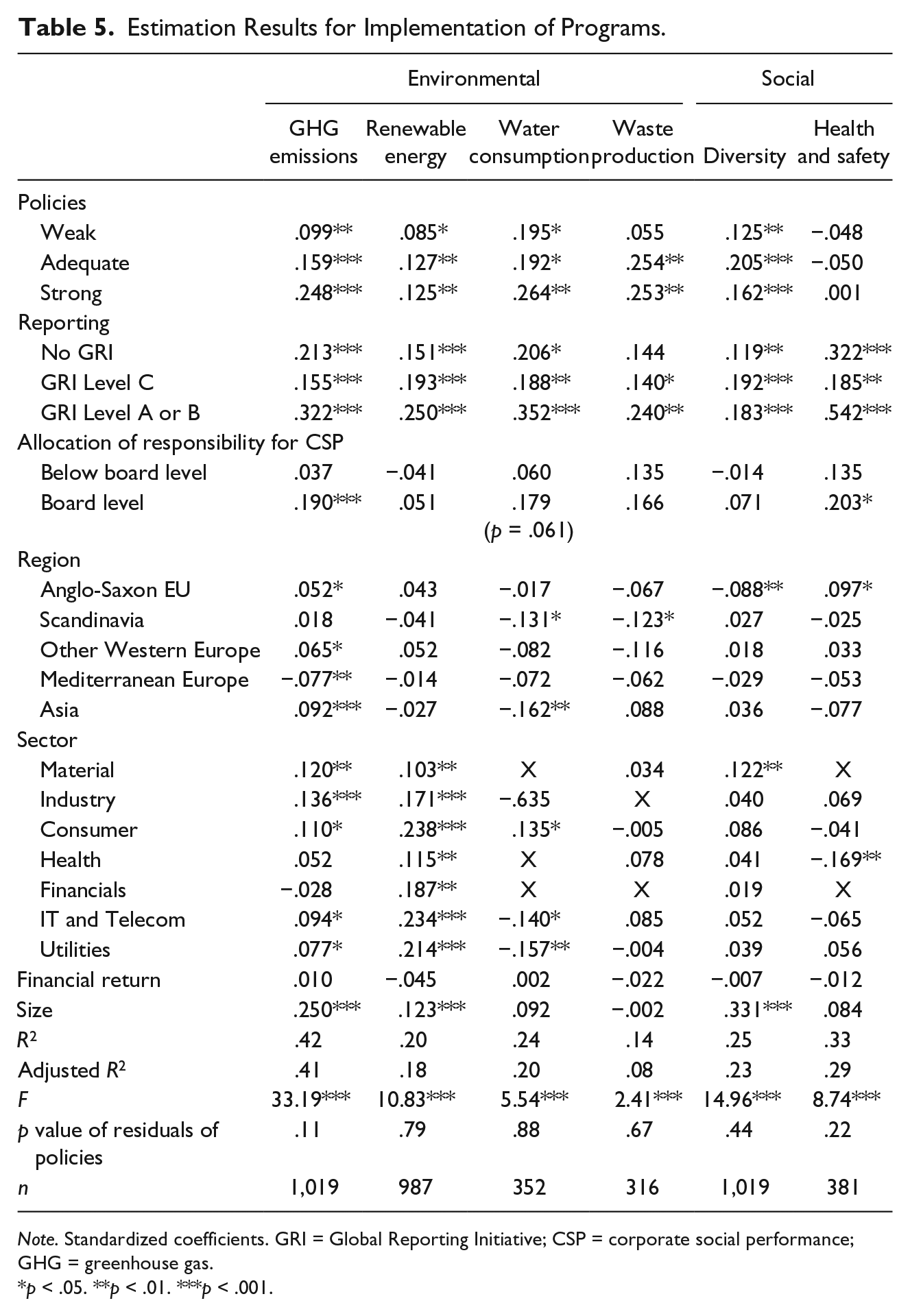

As noted above, we distinguish four environmental chains (GHG emissions, renewable energy, water consumption, and waste production) and two social chains (workforce gender diversity and working conditions). For each chain, we performed multiple regression analyses that correspond to the various paths as depicted in the framework in Figure 2. Table 5 reports the results for the implementation part, and Table 6 for the impact part. For implementation programs, policies, reporting, and the allocation of responsibility for CSP, we used the dummy for Option A (no program/no policy/no reporting/no responsibility) as reference variable.

Estimation Results for Implementation of Programs.

Note. Standardized coefficients. GRI = Global Reporting Initiative; CSP = corporate social performance; GHG = greenhouse gas.

p < .05. **p < .01. ***p < .001.

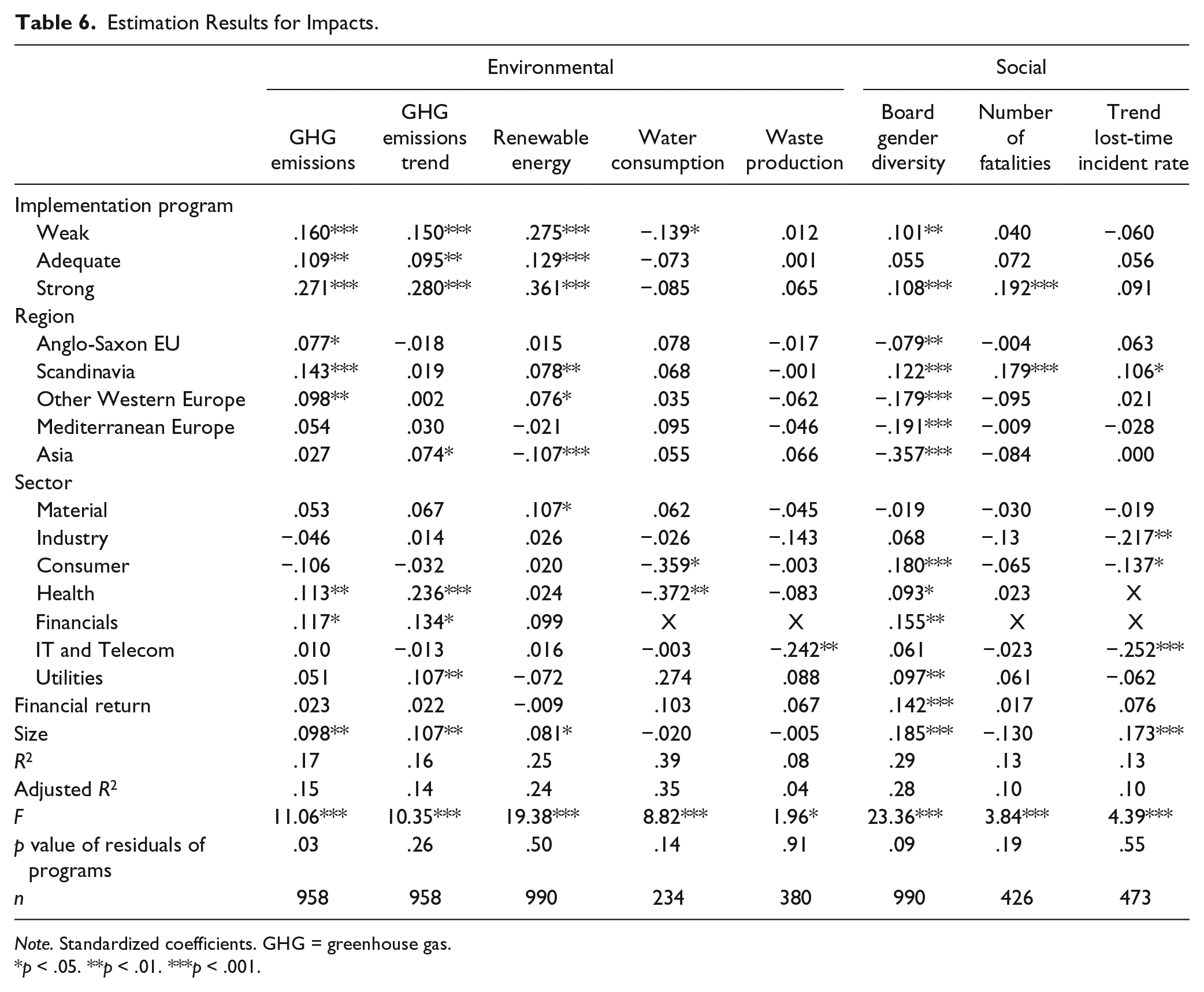

Estimation Results for Impacts.

Note. Standardized coefficients. GHG = greenhouse gas.

p < .05. **p < .01. ***p < .001.

Table 5 reports the estimation results for CSR implementation programs. Hausman’s endogeneity test shows that the residuals of CSR policies are insignificant; hence, CSR policies are not endogenous. The results in Table 5 show that the existence and quality of policies have a significant positive influence on the implementation of programs for GHG emissions, renewable energy, water consumption, waste production, and gender diversity. The higher the quality of the policy, the better the quality of the implementation program is. Therefore, Hypothesis 1 is supported for all the four environmental issues as well as for one social issue. Only for the implementation of a program on health and safety, we do not find a significant positive influence from a policy on working conditions on the implementation of such a program. We should, however, keep in mind that this model concerns sector-specific issues, and therefore also the sample is much smaller. Furthermore, the distribution of companies over the four options is highly uneven: A vast majority of 91% have no policy on working conditions (see Table 1).

In contrast with our expectation, we find that weak policies are not completely decoupled from the quality of the implementation programs. Although the effect of strong policies exceeds that of weak policies in all cases, the effect of having a weak policy (rather than no policy) is still significantly positive in four out of the six dimensions of CSP that we study.

Furthermore, we find significant and substantial positive influences of reporting. For all six dimensions of CSP, the effect of CSR reporting on the quality of CSR programs is higher if the CSR report meets the A or B level of GRI than if the company does not apply the GRI guidelines in its CSR report. This finding supports Hypothesis 3 that the quality of CSR implementation increases with the quality of CSR reporting.

The allocation of responsibility for CSP at the board level significantly improves the implementation of programs in two out of the six relationships. 5 In all relationships, we find that the estimated coefficient is higher if the responsibility for CSP is located at the board level rather than at below board level. Therefore, Hypothesis 4 is partly supported. 6

For the control variables, we find various regional influences (compared with Anglo-Saxon countries outside Europe) and sectoral influences (compared with the energy sector). We find that impacts on gender diversity in the Anglo-Saxon region outside Europe (the reference region) outperform the impacts in all other regions, except Scandinavia which has a very good performance in terms of the presence of women in the company’s boards. Also with respect to other dimensions of CSP (GHG emissions, renewable energy, health issues), Scandinavian companies have more favorable impacts than companies from other regions. With regard to CSR implementation, we find that companies from the Anglo-Saxon region outside Europe pay less attention to high-quality programs that foster the use of renewable energy than companies from other regions. In comparison with the energy sector (the reference sector), all other sectors are doing relatively well in terms of gender diversity (particularly in the consumer sector). On the contrary, the energy sector performs relatively well with regard to employee safety (trend in lost-time incident rate). Finally, no evidence is found for the slack resource theory: Only in the case of diversity, financial return significantly contributes to impacts. In line with expectations, we finally find in many models a significant positive influence of company size on CSR impacts as well as on CSR implementation, showing that small companies are often less able to implement CSR programs and improve impacts because of lack of experience and returns to scale. 7

Table 6 presents the estimation results for CSR impacts. We find that in seven out of eight cases, Hausman’s endogeneity test indicates that the quality of CSR programs is not endogenous. Only in the first regression analysis of GHG emissions, the residual of CSR programs is significant. However, if the impact on GHG emissions is measured by the GHG emissions trend, the quality of CSR programs is not endogenous. 8 The findings regarding the link between implementation and impacts are mixed. For both GHG emissions and renewable energy consumption, we find a significant positive relationship between the three dummies for CSR implementation and impacts. For GHG emissions, this relationship holds both for the absolute GHG emissions in 2010 (relative to industry average) and for the change in GHG emissions. However, we do not find such a relationship for water consumption and waste production. This absence of relationship might be due to the fact that those issues are sector specific and therefore the sample is smaller, and because the distribution of companies over the four options is highly uneven: A vast majority of 80% and 73% have no program for reduction of water consumption and waste production, respectively (see Table 1). For the social dimensions of CSP, the relationship between implementation and impact is found to be significant for two out of the three relationships, namely for gender diversity and the number of fatalities. 9

In all cases where implementation programs have significant effects on impacts, the effect of strong programs exceeds that of weak programs, supporting Hypothesis 2 that impacts depend on the quality of the implementation programs. However, it is remarkable that in almost all these cases, even weak programs are found to generate significant positive impacts. This finding indicates that even weak programs do not imply a complete decoupling between implementation and impacts for these four issues. Introducing a weak program is still better than having no program at all.

If we do add the dummies for the quality of policies as additional explanatory variables (not reported in Table 6), in none of the regression analyses direct effects of policies on impacts are found. This absence of direct effects supports the structure of our conceptual framework that presupposes that, if at all, CSR policies change CSR impacts only through fostering the quality of CSR implementation.

Discussion and Policy Implications

In this article, the authors analyze the relationships among CSR policies, programs, and impacts, and the incidence and conditions that prevent or reduce decoupling. Two types of decoupling can be present. The first type concerns policy-practice decoupling where communicated policies to gain legitimacy do not result in serious implementation of CSR programs. The second type concerns means-ends decoupling where the implementation of programs does not generate concrete impacts.

In contrast to earlier research on decoupling, we explicitly take into account the quality of CSR policies and CSR programs, as one would expect that policy-practice decoupling is particularly relevant for companies with weak CSR policies and means-ends decoupling for companies with low-quality CSR programs. By focusing on differences in the quality of policies and implementation, our conceptual framework facilitates a more accurate identification of the extent of decoupling. Another theoretical contribution of the article is that the quality of CSR implementation mediates the influence of (the quality of) CSR policies, CSR reporting, and the allocation of CSR responsibility on CSR impacts. For example, Mahoney, Thorne, Cecil, and LaGore (2013) found that companies that voluntarily issue CSR reports generally have higher CSP scores. But they did not research the mediation paths through which CSR reporting affects CSR impacts. In our model, the influence of CSR reporting is mediated by the quality of CSR implementation.

In the empirical part, we test the conceptual framework for four environmental issues (GHG emissions, renewable energy, water consumption, and waste production) and two social issues (gender diversity and working conditions). Although the analysis is necessarily limited to a small subset of all social and environmental issues that fall under the CSR umbrella due to the scarce data availability, the findings largely support our hypotheses.

The regression analysis shows substantial support for Hypothesis 1 that policy-practice decoupling is negatively related to the quality of CSR policies. For five of the six CSR issues, we find a significant positive influence of high-quality CSR policies on the quality of CSR implementation. In all these cases, companies with a high-quality CSR policy have, on average, also better CSR implementation programs than companies with a low-quality CSR policy. As CSR impacts depend positively on the quality of CSR implementation in most cases, we can conclude that CSR policies indirectly contribute to better CSR impacts. Furthermore, in four out of six cases, companies that have only introduced a weak policy still have significantly better programs than companies that do not have any policy. This information indicates that policy-practice decoupling is rather rare.

We also find support for the second hypothesis that means-ends decoupling decreases with the quality of implementation programs. This hypothesis is supported for GHG emissions, GHG emissions trend, the use of renewable energy, board gender diversity, and the reduction of the number of fatalities. For water consumption, waste production, and the trend lost-time incident rate, we find no significant influence of using high-quality CSR implementation programs on impacts, but this might be due to a combination of a much smaller sample (as these issues are only applicable for companies in specific sectors) and the uneven distribution of companies over the four options. Surprisingly, we find that in half of the estimated relations for impacts, a weak program is still significantly more productive in generating CSR impacts than employing no program. This finding indicates that, although the chance of means-ends decoupling increases if the company applies CSR programs of low quality, having a low-quality program is still better than having no program at all.

In almost all cases, the results show that better CSR reporting helps raising the quality of CSR implementation, supporting Hypothesis 3. Companies that apply the A- or B-level guidelines of GRI have better CSR programs than companies that do not apply GRI standards in their CSR reporting. However, we find that if CSP is not reported in accordance with GRI guidelines, it still significantly encourages companies to implementation programs of higher quality in comparison with companies that do not have a CSR report, as the coefficient is significantly positive for five out of six dimensions of CSP. Hence, even CSR reporting of low quality (in the sense that GRI standards are not respected) contributes to CSR implementation and therefore indirectly to CSR impacts.

Hypothesis 4, that the quality of CSR implementation depends on the allocation of responsibility of CSP at the board of the company, is partly supported. For most issues, the estimation results show that the quality of implementation programs is improved if the responsibility for CSP is transferred from below board level to board level. This finding shows that the institutionalization of CSP in the company by measures that make explicit that CSP is part of the professional responsibilities as a business leader fosters the implementation of CSR programs. Signaling commitment of the board by taking responsibility for CSP is therefore likely to reduce policy-practice decoupling.

These results have important policy implications. First, it implies that stating policies, even weak policies, is an achievement in itself. Only by stating its policies, companies subject themselves to the reputation mechanism and therefore risk their strategic resources. Formulating policies will initiate a process within the company in which the internal organization will tend to a recoupling (Haack, Schoeneborn, & Wickert, 2012). When companies start talking about something, a productive narrative starts in which company members are triggered to address inconsistencies between actual and idealized realities. Furthermore, formulating policies may generate a sense of entitlement, conviction, and rationality of action in the company, which may ultimately lead to full implementation (Zilber, 2009). Also Zeffane, Polonsky, and Medley (1994) indicated that a published environmental policy statement is a starting point for organizational commitment to implement a program. Industrial organizations, business schools, and network organizations can help to create awareness of the company’s responsibilities toward society. Industrial organizations can provide their members a platform for learning and experimenting with CSP and provide tools that help developing CSR policies that fit the company’s values, culture, and context as well as inform the company about instruments to implement their policies. In this way, the industrial organization acts as a promoter of good CSP. Companies can also cooperate in networks that are aligned to business schools. Business schools may provide information and training that form the mind-sets of executives. Fligstein (1990) found that corporate executives’ management styles were dependent on the type of training they received in business schools. Hence, executives will be more likely to acknowledge CSR responsibilities if their teachers in business schools paid serious attention to it and if business schools continue to inform them through business publications on CSR.

Second, policies can only merge into impacts when they are effectuated by high-quality implementation programs. As noted earlier, we do not find any direct effects of policies on impacts besides implementation. Whereas implementation without policy guidance is blind, policies without implementation are empty. In our model, therefore, policies and implementation are not two opposite concepts, as scholars often pose (Ashforth & Gibbs, 1990; Rodrigue, Magnan, & Cho, 2013), but two mutually dependent concepts. These relationships can be argued by the various kinds of motivations companies might have to align rhetoric and reality. First, companies whose impacts are not in line with the promises formulated in their policies run the risk of harming their reputation even more than companies with similar (or worse) social impacts that did not raise expectations by such policies. Using high-quality implementation programs decreases the risks of a visible and harmful gap between policies and impacts. Furthermore, following the resource-based view of the company, an asset that is valuable, rare, inimitable, and nonsubstitutable gives companies a competitive advantage. Whereas policies are relatively easy to copy, implemented CSR issues are much more company specific and therefore more difficult to copy.

Third, as our results show that CSR policies lead to better implementation programs and implementation to impacts, CSR seems to have an impact, and therefore self-regulation is found to positively contribute to societal welfare. We therefore conclude that skepticism with regard to CSR is not supported by our findings. Various measures can be taken to help companies to implement CSR and assess the impacts of their actions. Various global management systems have been developed which companies can use to integrate specific CSR issues like the European Eco-Management and Audit Scheme (EMAS), the Occupational Health and Safety Management System (OHSAS 18000), and SA8000.

Fourth, an adequate organization of CSR requires reporting of CSP. By fostering transparency, reporting will stimulate companies to narrow the gap between policies and impacts. The regression analysis shows that a high quality of reporting indirectly stimulates impacts through fostering implementation. Governments could take several measures to enhance the process. For example, it could help improving the reporting quality by stating minimum requirements for reporting as well as fostering the comparability of social reporting by subsidizing efforts to standardize reporting formats, such as the GRI. However, the government should be aware of the high degree of diversity in CSP in different sectors and maintain a good balance between self-regulation and government regulation. Policy makers should therefore also think more about how top executives can be motivated to take more responsibility for CSP, as winning the commitment of executives will enforce the integration of CSR policies in the organizational activities.

Footnotes

Acknowledgements

The authors thank several anonymous reviewers and Professor Windsor for helpful comments on an earlier version of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors thank the European Union for financial support under the Seventh Framework Program (Theme SSH-2009-2.1.3).