Abstract

This study investigates whether and to what extent publicly listed corporations voluntarily comply with and disclose recommended good corporate governance (CG) practices, and distinctively examines whether the observed cross-sectional differences in such CG disclosures can be explained by ownership and board mechanisms with specific focus on Saudi Arabia. The study’s results suggest that corporations with larger boards, a Big 4 auditor, higher government ownership, a CG committee, and higher institutional ownership disclose considerably more than those that are not. By contrast, the study finds that an increase in block ownership significantly reduces CG disclosure. The study’s results are generally robust to a number of econometric models that control for different types of disclosure indices, firm-specific characteristics, and firm-level fixed effects. The study’s results have important implications for policy makers, practitioners, and regulatory authorities, especially those in developing countries across the globe.

Keywords

This study seeks to contribute to the extant corporate governance (CG) literature by examining the extent to which publicly listed corporations voluntarily comply with and disclose good recommendations relating to their CG practices, and investigates whether corporate ownership and board mechanisms can explain observable cross-sectional differences in such CG disclosures with specific focus on Saudi Arabia.

Over the past decades, the adoption of CG codes by an increasing number of developing countries has generated a significant research interest on the actual extent of, and factors leading to or impeding implementation at the firm level, and on the consequences of such implementation at the macro or national level (Aguilera & Cuervo-Cazurra, 2009; Andreasson, 2011; Mahadeo & Soobaroyen, 2016; Ntim, Soobaroyen, & Broad, 2017; Salterio, Conrod, & Schmidt, 2013; Yoshikawa & Rasheed, 2009). In the main, such CG studies are motivated by an instrumental-led expectation that CG codes might help address systemic issues of corporate accountability, responsibility, corruption, and transparency (Christensen, Kent, Routledge, & Stewart, 2015; Filatotchev & Boyd, 2009; Hussainey & Al-Najjar, 2012; Samaha, Dahawy, Hussainey, & Stapleton, 2012; Soobaroyen & Ntim, 2013; Tsamenyi, Enninful-Adu, & Onumah, 2007), and thereby improve corporate performance by reducing corporate financial risk in developing countries (Bauer, Eichholtz, & Kok, 2010; Beiner, Drobetz, Schmid, & Zimmerman, 2006; Bozec & Bozec, 2012; Christensen et al., 2015; Giroud & Mueller, 2011; Gompers, Ishii, & Metrick, 2003; Haniffa & Hudaib, 2006; Henry, 2008; Klapper & Love, 2004; Ntim, 2015; Ntim, Lindop, & Thomas, 2013; Ntim, Opong, & Danbolt, 2012; Ntim & Soobaroyen, 2013a, 2013b; Renders, Gaeremynck, & Sercu, 2010; Tariq & Abbas, 2013).

To date, however, a good number of these studies report mixed results in terms of actual implementation and/or of positive consequences (Brennan & Solomon, 2008; Daily, Dalton, & Cannella, 2003; Wieland, 2005; Yoshikawa & Rasheed, 2009). More importantly, whereas prior research indicates that corporate decisions, including disclosure choices and strategies, are often decided by corporate boards and owners (Ntim & Soobaroyen, 2013a, 2013b), existing studies that empirically examine the different extent to which a firm’s board and ownership mechanisms can serve as strong or weak antecedents of voluntary compliance and disclosure of good CG practices are generally rare (Bozec & Bozec, 2007; Collett & Hrasky, 2005; Hussainey & Al-Najjar, 2012; Mallin & Ow-Yong, 2012; Salterio et al., 2013), but particularly acute in developing countries (Ntim, Opong, Danbolt, & Thomas, 2012; Rouf, 2011; Samaha et al., 2012; Tsamenyi et al., 2007). This intuition is motivated by the fact that the capacity of CG codes to achieve good governance depends largely on the extent to which senior managers, owners, and companies are willing to engage in effective voluntary compliance and disclosure (Core, 2001; Ntim et al., 2013; Tariq & Abbas, 2013).

Thus, this study seeks to explore CG reforms that have been pursued in developing countries with specific focus on Saudi Arabia. Our decision to focus on Saudi Arabia is motivated by a number of reasons. First, and in line with global developments, Saudi has pursued CG reforms in the form of the 2006 Saudi CG Code. As will be discussed further, and similar to most developing countries, the Saudi CG Code adopts a U.K.-style voluntary 1 “comply or explain” compliance and disclosure regime (Alshehri & Solomon, 2012; Piesse, Strange, & Toonsi, 2012). Distinct from most Anglo-American countries, the Saudi CG Code explicitly requires firms to go beyond the narrow financial and regulatory aspects of CG by addressing the interests of a broad range of stakeholders, such as creditors, customers, employees, local communities, and suppliers (Capital Market Authority [CMA], 2006, p. 4), and thus, investigating CG practices in the Saudi context may contribute to the extant literature by providing new insights on the effectiveness of CG reforms in developing countries.

Second, the Saudi corporate context has distinctive cultural features of having strong hierarchical social structure (Al-Twaijry, Brierley, & Gwilliam, 2002; Haniffa & Hudaib, 2007) in which greater importance is usually attached to informal relationships, such as kingship and tribal affiliations than formal CG and accountability mechanisms like corporate boards and their subcommittees (Hussainey & Al-Nodel, 2008). The Saudi corporate setting is further characterized by concentrated ownership structures (mainly by government and families), prohibition of direct foreign equity holdings, and low levels of institutional ownership, resulting in insufficient activism by shareholders and a weak capacity to implement and enforce corporate regulations (Al-Razeen & Karbhari, 2004; Piesse et al., 2012). In particular, concentrated ownership renders the capital, corporate control, product, professional services, and top managerial labor markets weak (Gillan, 2006; Haniffa & Hudaib, 2006; Ntim, Opong, & Danbolt, 2012; Ntim, Opong, Danbolt, & Thomas, 2012), which can impact negatively on the willingness of corporations to engage in voluntary disclosure. Arguably, these contextual challenges raise serious empirical questions as to whether the 2006 Saudi voluntary compliance and disclosure CG Code can improve CG standards of Saudi listed corporations (Al-Moataz & Hussainey, 2013; Munisi & Randoy, 2013; Soliman, 2013a, 2013b).

Third, despite increasing theoretical and empirical evidence that the ability of any single theory to fully explain the reasons and motivations underlying corporate voluntary disclosure behavior is limited (Branco & Rodrigues, 2008; Chen & Roberts, 2010; Ntim & Soobaroyen, 2013a, 2013b), existing studies on voluntary disclosure are either largely descriptive in nature (Alsaeed, 2006; Bebenroth, 2005; Cromme, 2005; Pass, 2006; Werder, Talaulicar, & Kolat, 2005) or rely on single theoretical perspective (Bozec & Bozec, 2007; Hooghiemstra, 2012; Hussainey & Al-Najjar, 2012; Mallin & Ow-Yong, 2012; Ntim, Opong, Danbolt, & Thomas, 2012), and thereby impairing the development of new theoretical insights, advancement, and understanding.

Fourth, and unlike most Arabic countries, Saudi Arabia is a major “G-20” economy, being the world’s largest producer of oil, as well as playing host to some of the world’s largest multinationals (Al-Filali & Gallarotti, 2012; Alsaeed, 2006; Samba Financial Group [SFG], 2009). For example, Saudi accounted for 44% and 25% of total Arab market capitalization and GDP, respectively, in 2010 (Alshehri & Solomon, 2012; SFG, 2009). This means that unlike most Arabic countries, any CG failures may have serious implications far beyond the Middle East and developing countries.

Generally, and notwithstanding the increasing number of CG Codes in developing countries, such as Saudi Arabia (Aguilera & Cuervo-Cazurra, 2009; Samaha et al., 2012), existing studies investigating the effectiveness of voluntary CG Codes in improving governance standards are disproportionately concentrated in a few developed countries (Bebenroth, 2005; Bozec & Bozec, 2007; Cromme, 2005; Hooghiemstra, 2012; Hussainey & Al-Najjar, 2012; Mallin & Ow-Yong, 2012; Pass, 2006; Pellens, Hillebrandt, & Ulmer, 2001; Salterio et al., 2013; Werder et al., 2005). It is contended, however, that in developing countries with different cultural, regulatory, CG, and institutional contexts, such as Saudi Arabia (Aguilera & Cuervo-Cazurra, 2009), voluntary compliance with CG Codes can be expected to vary from what has been found in developed countries. Therefore, an investigation of voluntary CG disclosures in developing countries, where there is a dearth of empirical evidence, is crucial in offering a more complete understanding of CG reforms and disclosure behavior. In this case, and although there have been a number of CG studies within the Saudi corporate context, notably by Hussainey and Al-Nodel (2008), Al-Nodel and Hussainey (2010), Alshehri and Solomon (2012), Piesse et al. (2012), Al-Janadi, Rahman, & Omar (2013), and Al-Moataz and Hussainey (2013), the current study differs from existing ones in terms of (a) its explicit construction of a Saudi CG disclosure index (SCGI) based directly on the 2006 Saudi CG Code, (b) its reliance on a larger panel data set drawn from the 2004 to 2010 period, and (c) its evaluation of a broader set of CG provisions and disclosures.

In doing so, the study extends, as well as makes a number of distinct and new contributions to the extant CG literature. First, using data extracted directly from annual reports of a sample of 80 Saudi listed corporations from 2004 to 2010, the study contributes to the literature by providing detailed evidence, for the first time, on the level of compliance with the 2006 Saudi CG Code by constructing a broad CG compliance and disclosure index containing 65 CG provisions. Second, the study contributes to the literature by offering evidence on the extent to which the introduction of the 2006 Saudi CG Code has helped in improving CG standards in Saudi listed corporations. Third, the study contributes to the literature by applying and informing the analysis with insights from a number of theories, including agency, legitimacy, resource dependence, and stakeholder theories. Finally, the study makes a new contribution to the literature by providing empirical evidence on the extent to which corporate ownership and board mechanisms influence the level of CG disclosure in Saudi listed corporations. This can improve current understanding of the main factors that drive the level of voluntary compliance and disclosure of CG practices in a major developing Arabic country in which various stakeholders, such as the Saudi government, the Saudi CMA, and the Saudi Stock Exchange (Tadawul, 2012) take a keen interest in CG and stakeholder issues.

The rest of the article is organized as follows. The next section provides an overview of the Saudi stock exchange, CG reforms pursued, and the Saudi corporate context. The following sections review the antecedents of the prior voluntary CG disclosure literature and develop hypotheses, describe the data and research methodology, and report empirical results, while the conclusion contains a summary and a brief discussion of policy implications, limitations, and recommendations for future research.

The Saudi Stock Exchange, CG Policy Reforms, and the Saudi Corporate Context

Although formal public trading of stocks did not start in Saudi until the 1980s, public corporations had long operated in the country in the mid-1930s, when the Arab Automobile corporation was established as the first joint stock corporation (Tadawul, 2012). By 1975, there were about 14 publicly listed corporations, increasing further to 75 listed firms by 2000 (SFG, 2009; Tadawul, 2012). The rapid economic expansion, arising from a boom in oil income in the 1970s, led to the formation of a number of large corporations and joint stock banks (Al-Filali & Gallarotti, 2012; Alsaeed, 2006). However, stock trading was not formalized until the early 1980s when the government embarked upon establishing an official stock exchange as part of the general reforms toward creating a free market economy (Hussainey & Al-Nodel, 2008; Tadawul, 2012). In 1984, the Saudi Arabian Monetary Agency (SAMA) was charged with the responsibility of developing, operating, regulating, and monitoring the market until the CMA was established in July 2003 (Al-Janadi et al., 2013; SFG, 2009). In 2003, and as a part of the CG reforms, the Saudi Stock Exchange (Tadawul, 2012) was established with the responsibility of operating the market, while the CMA remained as the sole regulatory body of the market (Alshehri & Solomon, 2012; Soliman, 2013a, 2013b). Since its establishment in 2003, the Tadawul has experienced rapid growth through greater listings and vibrant trading activities. For example, about 68 corporations were listed between 2007 and 2010 (SFG, 2009; Tadawul, 2012). This increased the number of listed corporations substantially from 77 in 2005 to 145 in December 2010 with a stock market capitalization of about US$533 billion, and accounting approximately for 44% of total Arab stock market capitalization (International Finance Corporation [IFC], 2008; SFG, 2009; Tadawul, 2012).

With respect to CG, and although legislation regulating the behavior of corporations, their directors, and officers has long existed in Saudi Arabia in the form of the 1965 Companies Act (Al-Razeen & Karbhari, 2004; Hussainey & Al-Nodel, 2008), there is a consensus that in a narrow sense, CG in Saudi Arabia was formally institutionalized by the publication of the Saudi CG Code in November 2006 (Al-Moataz & Hussainey, 2013; Al-Nodel & Hussainey, 2010; CMA, 2006; Soliman, 2013a, 2013b). In fact, attempts at pursuing CG reforms to enhance CG standards in Saudi public corporations began in earnest in 2003, but early rapid growth in the stock market diverted the attention of the CMA and the relevant stakeholders from it (Alshehri & Solomon, 2012; SFG, 2009). However, a sudden fall of about 25% in value of listed stocks in February 2006 alone, and an overall fall of 53% by the end of 2006, wiping over US$480 billion off the market’s value highlighted the need to improve CG standards in Saudi publicly listed corporations (SFG, 2009). As a result, academics, investors, and practitioners placed pressure on the CMA to urgently improve CG standards by (a) deepening the market, including increasing its size (e.g., number of listed firms) and allowing direct foreign/institutional investor participation 2 ; (b) improving disclosure and transparency (DAT); and (c) clamping down on insider trading (Alshehri & Solomon, 2012; SFG, 2009).

Consequently, a first draft of the Saudi CG Code was issued for consultation in July 2006 with the final version published in November 2006. The Code addresses a number of CG issues relating to (a) board of directors (BOD), (b) disclosure and transparency (DAT), (c) rights of shareholders and the general assembly (ROS), and (d) internal control and risk management (IRM) (CMA, 2006). 3 Noticeably, the recommendations of the Saudi CG Code were largely similar to those of the U.K.’s Cadbury Report of 1992 (Alshehri & Solomon, 2012; Piesse et al., 2012). For example, and similar to the Cadbury Report, the Saudi Code suggested an Anglo-American style unitary BOD, consisting of executive and non-executive directors, who are primarily accountable to shareholders operating within a voluntary (“comply or explain”) compliance and disclosure regime (see the appendix; CMA, 2006). Distinct from the Cadbury Report, however, it explicitly requires Saudi firms to address not only the interests of shareholders but also those of other stakeholders, such as employees and local communities, although this part of the Code is relatively less developed and clear as to their implications for CG, compliance, and disclosure (CMA, 2006, p. 4).

In addition to pursuing CG reforms, and as has been previously explained, the Saudi corporate context is characterized by (a) a highly hierarchical social structure, (b) concentrated ownership, (c) low level of institutional shareholding and weak shareholder activism, (d) the absence of direct foreign/institutional investors, (e) weak enforcement of corporate regulations, and (f) weak market for capital, managerial labor, and corporate control (Alsaeed, 2006; Haniffa & Hudaib, 2007; Piesse et al., 2012). As a result, critical concerns have been expressed as to whether, given the relative uniqueness of the Saudi corporate context, a voluntary compliance and disclosure regime like the 2006 Saudi CG Code can be effective in raising CG standards in Saudi Arabia (IFC, 2008; SFG, 2009). Consequently, we seek to examine the extent to which Saudi listed corporations are voluntarily complying with the CG provisions contained in the 2006 Saudi CG Code and investigate whether corporate ownership and board mechanisms can explain observable differences in the level of voluntary CG disclosure.

Therefore, the next section now considers the evidence and insights from previous studies, and subsequently develops the hypotheses of interests.

Literature Review and Hypotheses Development

Previous studies have employed a number of theories, including agency, legitimacy, resource dependence, and stakeholder theories 4 to examine how corporate ownership structure and board mechanisms affect (a) general voluntary disclosures (Abdelsalam & Street, 2007; Al-Janadi et al., 2013; Al-Razeen & Karbhari, 2004; Alsaeed, 2006; Barako, Hancock, & Izan, 2006; Eng & Mak, 2003; Rouf, 2011; Taylor, Tower, & Van der Zahn, 2011) and (b) voluntary CG disclosures (Al-Janadi et al., 2013; Al-Moataz & Hussainey, 2013; Alshehri & Solomon, 2012; Y. Bozec & Bozec, 2007; Collett & Hrasky, 2005; Hussainey & Al-Najjar, 2012; Hussainey & Al-Nodel, 2008; Mahadeo & Soobaroyen, 2016; Piesse et al., 2012; Tsamenyi et al., 2007). Others have examined how general firm-specific features, such as size and industry, drive corporate social responsibility (CSR) practices (Branco & Rodrigues, 2008; Fifka, 2013), while a limited number of studies have investigated how ownership and board mechanisms affect CSR disclosures (Jamali, Safieddine, & Rabbath, 2008; Ntim & Soobaroyen, 2013a, 2013b; Reverte, 2009).

Hence, and relying on insights from agency, legitimacy, resource dependence, and stakeholder theories, this study draws from these strands of the literature, supplemented by the implications of the Saudi context, to identify potential ownership and board mechanisms that might affect the voluntary disclosure of CG practices. Specifically, the study examines how corporate (a) ownership mechanisms (block ownership, government ownership, and institutional ownership) and (b) board mechanisms (board size, the presence of a CG committee, and audit firm size) 5 affect voluntary disclosure of recommended good CG practices.

Corporate Ownership Structure Mechanisms

Block ownership and CG disclosure

From an agency theory perspective, closer managerial monitoring and lesser information asymmetry that is usually associated with block ownership can be expected to minimize agency problems and improve financial performance (Botosan, 1997; Jensen, 1993; Jensen & Meckling, 1976), and hence a lesser need for increased CG disclosures to gain legitimacy (legitimacy theory) from powerful corporate stakeholders (stakeholder theory), such as creditors, employee unions, government, and shareholders, whose resources (resource dependence), for example, finance, contacts and contracts, are arguably critical to the ability of any corporation to maintain sustainable operations (Branco & Rodrigues, 2008; Chen & Roberts, 2010). Thus, in this case, block ownership can serve as a substitute for good governance arrangements, including less disclosure relating to CG practices (Bozec & Bozec, 2007). In contrast, disperse ownership requires greater monitoring, which can be minimized through increased corporate disclosures (Eng & Mak, 2003; Ntim & Soobaroyen, 2013a, 2013b).

In line with the results of past empirical studies (Abdelsalam & Street, 2007; Barako et al., 2006; Hooghiemstra, 2012; Ntim, Opong, & Danbolt, 2012; Ntim, Opong, Danbolt, & Thomas, 2012; Patel, Balic, & Bwakira, 2002; Reverte, 2009), Alsaeed (2006) reports a negative link between block ownership and voluntary disclosure for a 2003 cross-sectional sample of 40 Saudi listed corporations, whereas using a 2009 cross-sectional sample of 100 Egyptian corporations, Samaha et al. (2012) find that corporations with lower block ownership have higher levels of CG disclosure. Similarly, using a 2002 cross-sectional sample of 244 Canadian listed firms, Bozec and Bozec (2007) report a negative link between ownership concentration and disclosure of good CG practices. In addition, using a sample of 100 South African listed firms from 2002 to 2009, Ntim and Soobaroyen (2013a, 2013b) and Ntim et al. (2013) report a negative effect of block ownership on voluntary CSR and risk disclosures, respectively. Within the Saudi context, corporate ownership has historically been concentrated with control firmly in the hands of dominant royal families and government (Al-Razeen & Karbhari, 2004; Piesse et al., 2012), and hence our prediction is that block ownership is more likely to affect voluntary CG disclosure. Thus, the study’s first hypothesis is that

Institutional ownership and CG disclosure

Agency theory suggests that due to their larger ownership stakes, institutional shareholders, as influential corporate stakeholders (stakeholder theory), have extra incentive to closely monitor corporate disclosures (Core, 2001; Fung & Tsai, 2012; Jensen & Meckling, 1976). Therefore, managers will be expected to not only make more disclosures, including CG practices to meet the informational needs of institutional shareholders as powerful (stakeholder theory) corporate stakeholders (Deegan, 2002; Parker, 2005), but also secure their support to legitimize (legitimacy theory) or justify their continued stewardship of the company and its critical resources (resource dependence theory; Branco & Rodrigues, 2008; Chen & Roberts, 2010).

Empirically, and consistent with the findings of past evidence (Barako et al., 2006; Ntim, Opong, & Danbolt, 2012; Ntim, Opong, Danbolt, & Thomas, 2012), both Hooghiemstra (2012), and Mallin and Ow-Yong (2012) report a positive association between institutional ownership and voluntary CG disclosure in samples of 85 Dutch and 300 U.K.-listed corporations, respectively. Similarly, Fung and Tsai (2012) report that U.S. firms with high institutional ownership tend to have better performance and improved CG practices. Within the Saudi context, and although institutional ownership has traditionally been relatively low (Alshehri & Solomon, 2012; Piesse et al., 2012), the CMA has been keen on boosting shareholdings by institutions as part of the broader efforts at improving CG standards in Saudi companies (IFC, 2008; SFG, 2009). Also, the Saudi CG Code urges institutional shareholders to actively seek to enhance governance, performance, and disclosure practices in Saudi companies, and thus the study’s second hypothesis is that

Government ownership and CG disclosure

As a powerful stakeholder (stakeholder theory) and given the Saudi government’s (through the CMA) formal support for the recommendations of Saudi CG Code (Alshehri & Solomon, 2012; CMA, 2006), our expectation is that Saudi companies with high government ownership will actively seek to win government support (Deegan, 2002; Ntim & Soobaroyen, 2013a, 2013b) by complying with the Code’s provisions through increased disclosure of CG practices that may not only help in legitimizing (legitimacy theory) their operations (Ashforth & Gibbs, 1990), but also secure access to critical resources (resource dependence theory; Branco & Rodrigues, 2008; Reverte, 2009), such as finance that can enhance performance. Also, agency theory suggests that increased disclosure of CG practices can help resolve agency problems between managers and government as an influential shareholder (Core, 2001; Jensen & Meckling, 1976). Furthermore, potential political interference and conflict of interests’ problems between shareholders and government that is often associated with government ownership can be minimized through increased voluntary disclosure (Eng & Mak, 2003; Ntim & Soobaroyen, 2013a, 2013b).

Prior evidence relating to the connection between government ownership and voluntary disclosure is limited, although Eng and Mak (2003) and Al-Janadi et al. (2013) find that government ownership is positively associated with voluntary disclosure, while Ntim and Soobaroyen (2013a, 2013b) and Ntim et al. (2013) report that government ownership affects positively on voluntary CSR and risk disclosures, respectively. With regard to the Saudi corporate setting, the government holds significant ownership stakes in large public and private corporations through a number of institutions, including the General Organization for Social Insurance (GOSI), Public Investment Fund (PIF), and Public Pension Agency (PPA) with keen interest in CG and stakeholder issues, and thus, the study’s third hypothesis is that

Corporate Board Mechanisms

Corporate board size and CG disclosure

Agency theory suggests that increased managerial monitoring associated with larger boards can have a positive influence on corporate disclosures, including CG practices and performance (Samaha et al., 2012), whereas others have suggested that larger boards are often characterized by poor coordination, communication, and monitoring problems (Jensen, 1993; Ntim, Lindop, Osei, & Thomas, 2015; Ntim, Opong, & Danbolt; 2015), which can impact negatively on CG disclosure and financial performance. Also, resource dependence theory indicates that larger boards are associated with greater diversity in terms of expertise (Branco & Rodrigues, 2008; Chen & Roberts, 2010), experience, and stakeholder (stakeholder theory) representation (Ntim & Soobaroyen, 2013a, 2013b; Reverte, 2009), which can enhance corporate legitimacy (legitimacy theory) and reputation (Ashforth & Gibbs, 1990).

Despite the mixed theoretical predictions, a number of empirical studies report a positive connection between board size and voluntary disclosure (Barako et al., 2006; Hooghiemstra, 2012; Hussainey & Al-Najjar, 2012; Mallin & Ow-Yong, 2012; Ntim, Opong, & Danbolt, 2012; Ntim, Opong, Danbolt, & Thomas, 2012). For example, both Rouf (2011) and Samaha et al. (2012) find that board size is positively related to voluntary disclosure in a sample of 120 and 100 Bangladeshi and Egyptian listed corporations, respectively. Similarly, and employing a sample of 100 South African listed firms from 2002 to 2009, Ntim and Soobaroyen (2013a, 2013b) and Ntim et al. (2013) report that board size has a positive effect on voluntary CSR and risk disclosures, respectively. In addition, Al-Janadi et al. (2013) report a positive link between board size and voluntary disclosure in a sample of 87 Saudi listed firms. Also, the Saudi CG Code specifies that board size should be between 3 and 11, indicating that it considers board size as an important CG mechanism. Given the mixed theoretical literature, however, the study’s fourth hypothesis is that

Audit firm size (auditor quality) and CG disclosure

The appointment of external auditors to examine company accounts is an important governance mechanism for monitoring managers to reduce agency conflicts in modern corporations, whereby ownership is separate from control (Haniffa & Hudaib, 2007; Han, Kang, & Yoo, 2012). One way of determining external auditor quality is the level of disclosure, and in fact, audit firm size has been suggested to have a positive effect on corporate disclosure (Eng & Mak, 2003; Owusu-Ansah, 1998) and audit quality (DeAngelo, 1981). This is because larger audit firms have greater financial strength, experience, expertise, information, and knowledge (DeAngelo, 1981; Ntim, Opong, & Danbolt, 2012; Ntim, Opong, Danbolt, & Thomas, 2012), which can improve their independence and ability to limit opportunistic activities of managers (Alsaeed, 2006; Aly, Simon, & Hussainey, 2010).

Empirically, a number of studies have reported a positive connection between audit firm size and corporate disclosure (Eng & Mak, 2003; Han et al., 2012; Ntim & Soobaroyen, 2013a, 2013b; Owusu-Ansah, 1998). Of direct relevance to our study, Al-Janadi et al. (2013) report a positive association between audit firm quality/size and voluntary disclosure using a sample of 87 Saudi listed firms. Also, the Saudi CG Code recognizes external auditors as one of the key stakeholders in ensuring that Saudi corporations voluntarily comply with its CG provisions. Therefore, the study’s fifth hypothesis is that

The presence of a CG committee and CG disclosure

The Saudi CG Code does not require Saudi corporations to set up CG committees to continuously monitor compliance with its CG provisions. Therefore, our expectation is that Saudi listed corporations that voluntarily establish CG committees to specifically monitor their compliance are more likely to engage in good CG practices and disclose more than those that do not have CG committees (Core, 2001; Ntim, Opong, Danbolt, & Thomas, 2012). There is a general lack of studies that investigate the link between the presence of a CG committee and corporate disclosure, and this is particularly acute in the case of Saudi Arabia, where there is also a clear dearth of voluntary CG disclosure studies. The only exceptions are studies by Ntim, Opong, Danbolt, and Thomas (2012), Ntim et al. (2013), and Ntim and Soobaroyen (2013a). Using a sample of 169 South African listed corporations from 2002 to 2006, Ntim, Opong, Danbolt, and Thomas (2012) report a positive connection between the presence of a CG committee and voluntary CG disclosure, and thus the study’s sixth hypothesis is that

Data and Research Method

Data: Sample Selection, Sources, and Description

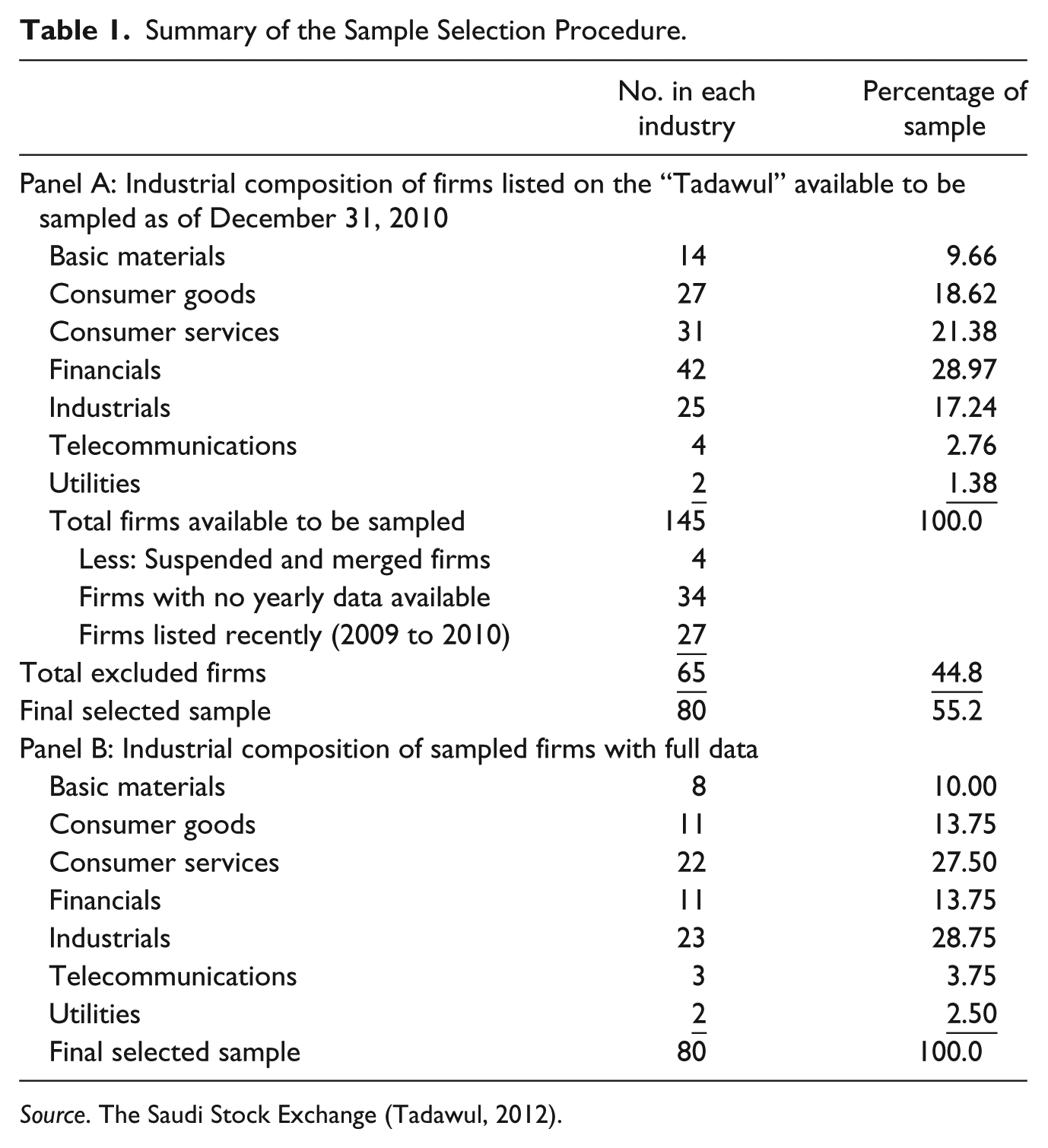

The sample for the study is drawn from all 145 corporations listed on the Saudi Stock Exchange (Tadawul, 2012) as at the end of 2010, and Table 1 contains a summary of the sample selection procedure. Panel A of Table 1 contains the industrial composition of all the corporations that were listed on the “Tadawul,” while Panel B of Table 1 contains the final sampled corporation with full data.

Summary of the Sample Selection Procedure.

Source. The Saudi Stock Exchange (Tadawul, 2012).

Board mechanisms, ownership structure, and voluntary CG disclosures were extracted from the sampled corporations’ annual reports that were downloaded from the “Tadawul” Website/Perfect Information Database, whereas the accounting/financial variables were obtained from “Tadawul” and DataStream. To be included in the study’s final sample, a corporation had to meet two main criteria: accessibility to a corporation’s complete 7-year annual reports from 2004 to 2010 inclusive and the accessibility to a corporation’s corresponding accounting/financial data for the same period. The criteria were set for several reasons. First, and in line with past studies (Barako et al., 2006; Eng & Mak, 2003; Henry, 2008), the criteria helped in meeting the requirements for a balanced panel data analysis, whose benefits have been widely articulated (Gujarati, 2003; Petersen, 2009). Third, the sample starts in 2004 because data coverage on the “Tadawul” Website/Perfect Information Database/DataStream on Saudi listed corporations is very limited prior to 2004. Starting from 2004 also allows the authors to examine CG standards in Saudi corporations pre- and post-2006 CG reforms. The sample ends in 2010 because it is the most recent year for which data are available. As presented in Panel B of Table 1, and after excluding firms that had been suspended, merged, newly listed, and with no/missing data, the complete data needed are obtained for a total of 80 firms for seven firm-years and seven industries in the study’s analysis.

Research Method: Definition of Variables and Model Specification

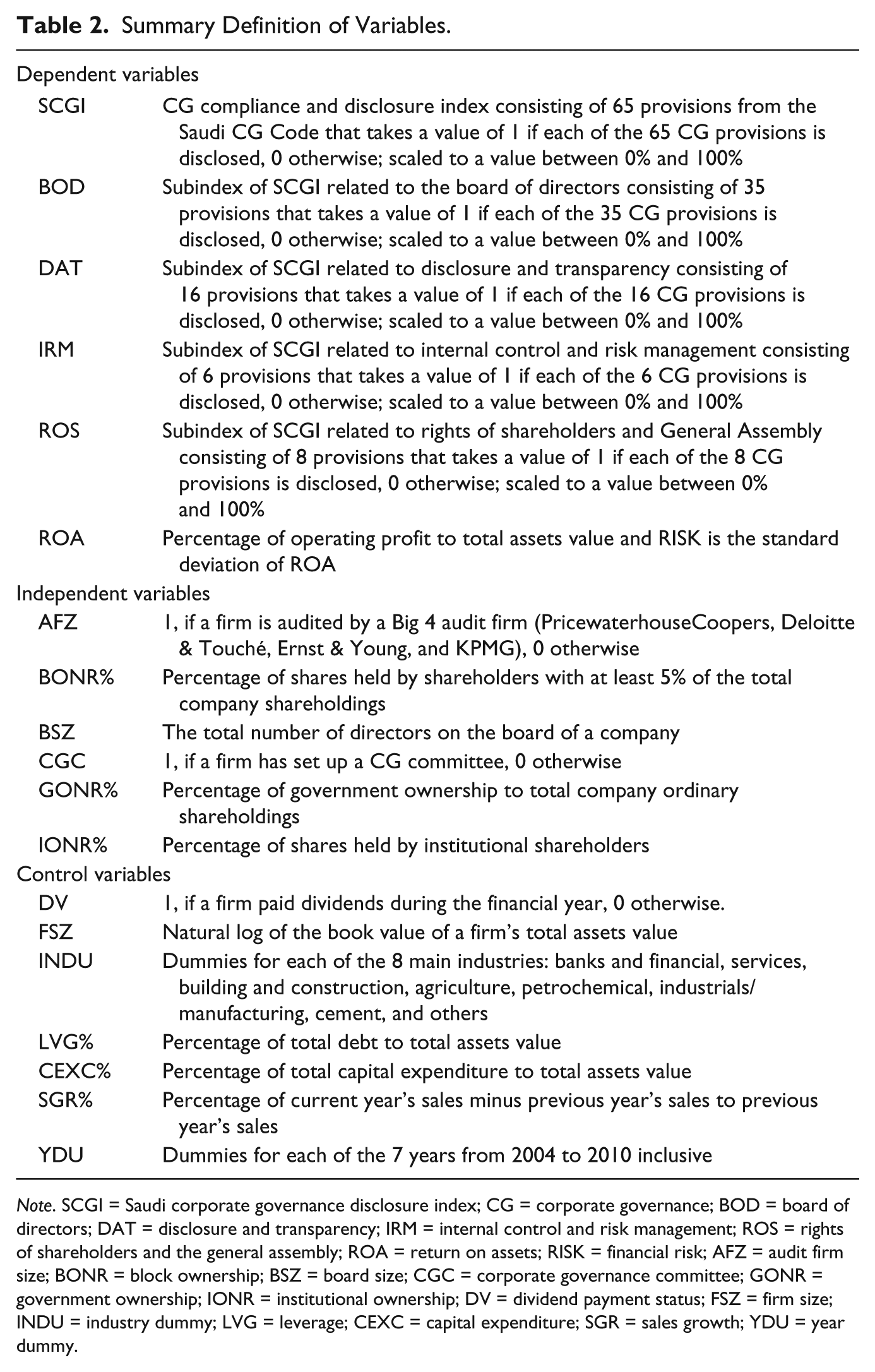

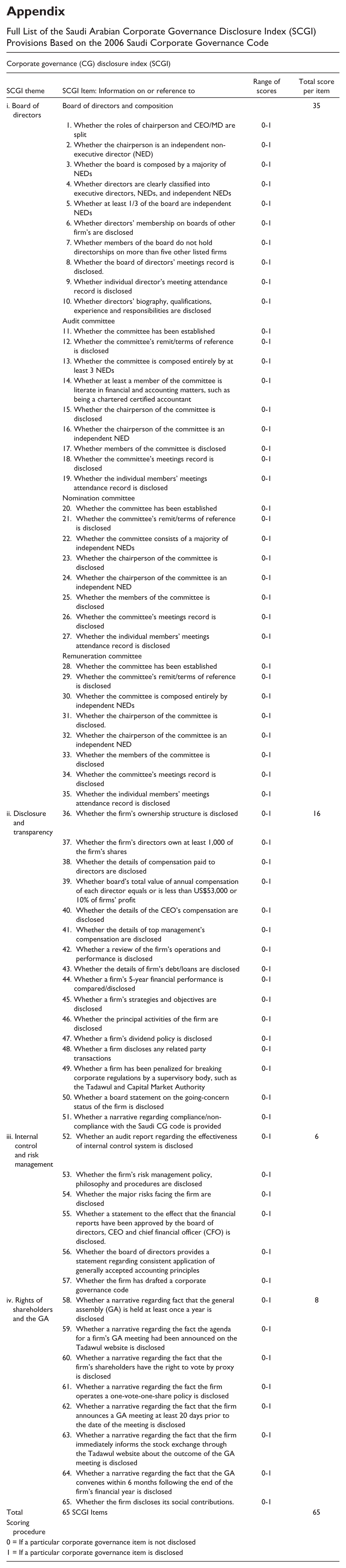

We classify the study’s variables into three main types and Table 2 contains full definitions of all them. First, and to test H1 to H6, the study’s main dependent variable is the binary 6 SCGI, which contains 65 CG provisions. The detailed provisions are presented in the appendix. The SCGI seeks to measure the extent to which Saudi listed corporations voluntarily disclose information on their CG practices based on four broad areas specified by the 2006 Saudi CG Code, consisting of (a) BOD, (b) DAT, (c) IRM, and (d) ROS.

Summary Definition of Variables.

Note. SCGI = Saudi corporate governance disclosure index; CG = corporate governance; BOD = board of directors; DAT = disclosure and transparency; IRM = internal control and risk management; ROS = rights of shareholders and the general assembly; ROA = return on assets; RISK = financial risk; AFZ = audit firm size; BONR = block ownership; BSZ = board size; CGC = corporate governance committee; GONR = government ownership; IONR = institutional ownership; DV = dividend payment status; FSZ = firm size; INDU = industry dummy; LVG = leverage; CEXC = capital expenditure; SGR = sales growth; YDU = year dummy.

Second, and to test H1 to H6, the authors collected data on ownership structures, including block ownership (BONR), government ownership (GONR), and institutional ownership (IONR), and on board mechanisms, including board size (BSZ), audit firm quality/size (AFZ), and the presence of a CG committee (CGC). Finally, and to control for potential omitted variables bias (Gujarati, 2003; Petersen, 2009), the authors included an extensive number of control variables. These include capital expenditure (CEXC), dividend payment status (DV), leverage (LVG), firm size (FSZ), sales growth (SGR), industry dummy (INDU), and year dummy (YDU). For brevity, the authors do not develop direct theoretical connections between these control variables and voluntary disclosure of CG practices, but there is extensive theoretical and empirical literature that suggests they can potentially affect voluntary CG disclosure (SCGI) (Abdelsalam & Street, 2007; Al-Janadi et al., 2013; Aly et al., 2010; Botosan, 1997; Y. Bozec & Bozec, 2007; Fifka, 2013; Hooghiemstra, 2012; Hussainey & Al-Najjar, 2012; Rouf, 2011; Samaha et al., 2012).

Assuming that all relationships are linear, the study’s main ordinary least square (OLS) regression equation to be estimated to test H1 to H6 is specified as follows:

where the variables are defined as follows: Saudi CG disclosure index (SCGI), block ownership (BONR), institutional ownership (IONR), government ownership (GONR), board size (BSZ), audit firm quality/size (AFZ), and the presence of a CG committee (CGC), and CONTROLS refers to all the control variables, including dividend payment status (DV), sales growth (SGR), capital expenditure (CEXC), leverage (LVG), firm size (FSZ), 7 industry dummies (INDUs), and 7 year dummies (YDUs).

The authors discuss the empirical results, including descriptive statistics and regression analyses, in the following section.

Empirical Results and Discussion

Empirical Results From Descriptive Statistics and Univariate Regression Analyses

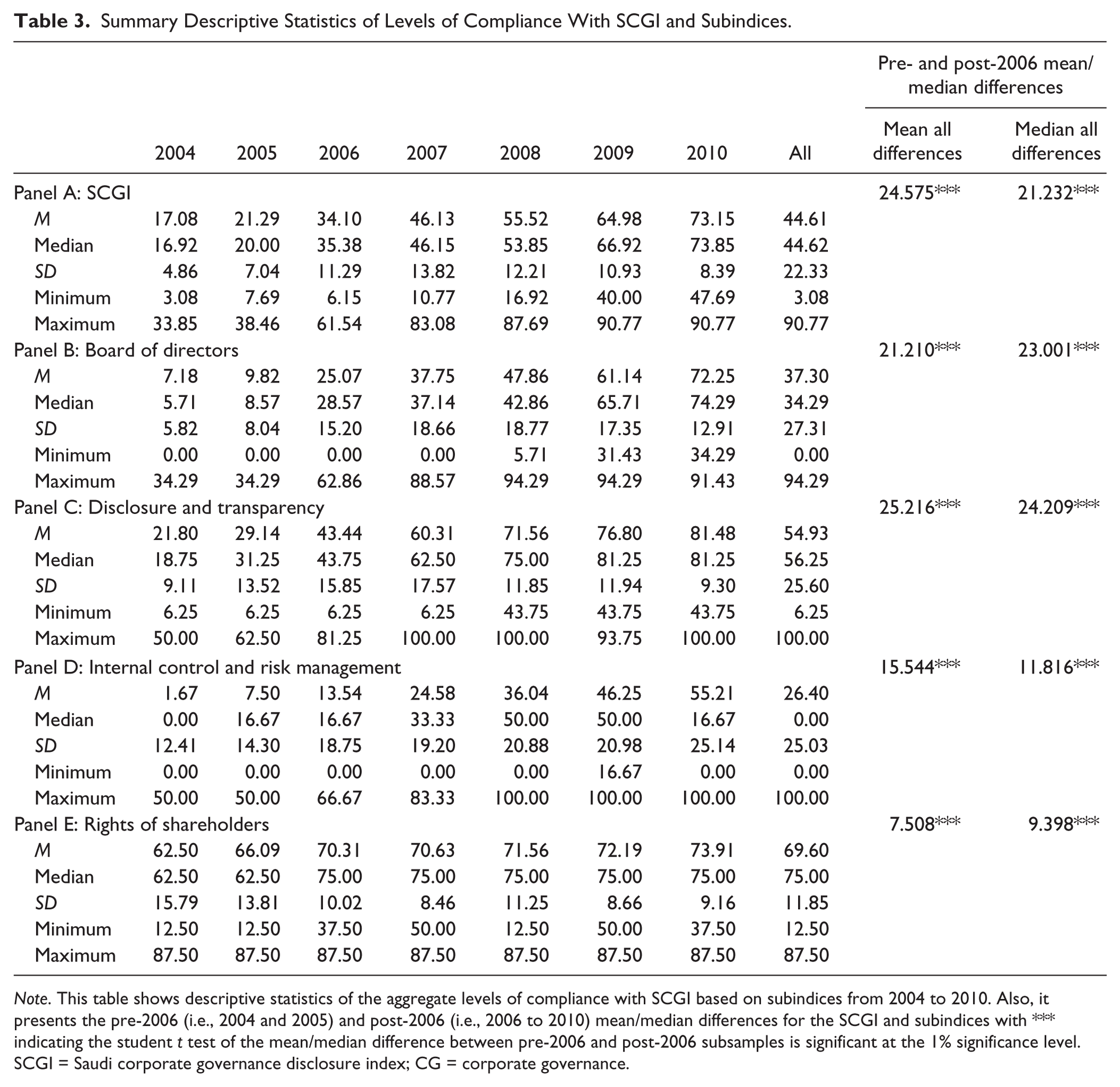

Table 3 presents the summary descriptive statistics relating to the level of compliance with the SCGI (see Panel A of Table 3) and their subindices for the pooled sample, as well as for each of the 7 firm-years examined. First, the summary descriptive statistics suggest that there is substantial degree of dispersion in the distribution of the SCGI. For example, the SCGI ranges from a minimum of 3.08% to a maximum of 90.77% with the average (median) corporation complying with 44.61% (44.62%) of the 65 CG provisions investigated. Second, and in line with the findings of previous studies (Barako et al., 2006; Henry, 2008; Mahadeo & Soobaroyen, 2016; Patel et al., 2002), the results in Table 3 suggest that compliance with the SCGI provisions generally improves over time, with the median (average) aggregate compliance levels increasing consistently from 17.08% (16.92%) in 2004 to 73.15% (73.85%) in 2010, a 56.07 (56.93) percentage point increase over the 7 firm-year period examined.

Summary Descriptive Statistics of Levels of Compliance With SCGI and Subindices.

Note. This table shows descriptive statistics of the aggregate levels of compliance with SCGI based on subindices from 2004 to 2010. Also, it presents the pre-2006 (i.e., 2004 and 2005) and post-2006 (i.e., 2006 to 2010) mean/median differences for the SCGI and subindices with *** indicating the student t test of the mean/median difference between pre-2006 and post-2006 subsamples is significant at the 1% significance level. SCGI = Saudi corporate governance disclosure index; CG = corporate governance.

Third, the authors observe similar widespread and continuous improvements in the distributions of the four subindices. For example, the BOD ranges from 0% (0%) to 94.29% with the average (median) corporation complying with 37.30% (34.29%) of the 35 BOD provisions examined. By contrast, disclosures relating to IRM are lowest with a minimum (maximum) of 0.00% (50.00%) with the average (median) firm complying with 26.40% (0.00%) of the 6 IRM provisions. Fourth, the student t test of differences between pre- and post-2006 means/medians indicates that the levels of compliance and disclosure are significantly higher over the post-2006 period than over the pre-2006 period for both the summary SCGI and its four subindices (BOD, DAT, IRM, and ROS). This suggests that, on average, the introduction of the 2006 Saudi CG code has helped in improving disclosure and CG standards among Saudi listed corporations.

Finally and in summary, the main evidence that emerges from investigating the complete sample of corporations is that despite the expectation that the introduction of the Saudi CG Code would speed-up convergence of CG practices (Alshehri & Solomon, 2012; CMA, 2006; IFC, 2008), CG standards among Saudi listed corporations still differ substantially. Whereas this is generally in line with the variability in compliance levels reported by previous CG disclosure studies (Al-Janadi et al., 2013; Y. Bozec & Bozec, 2007; Hussainey & Al-Najjar, 2012; Hussainey & Al-Nodel, 2008; Samaha et al., 2012), it suggests that a high degree of heterogeneity exists when it comes to the importance that Saudi listed corporations attach to CG. Evidence of improving CG standards among the sampled corporations, however, implies that contrary to general concerns as to whether the Saudi CG code can help improve CG standards in Saudi firms given contextual challenges (Piesse et al., 2012; Safieddine, 2009; SFG, 2009), the current voluntary compliance and disclosure regime has had a positive effect on CG standards in Saudi listed firms.

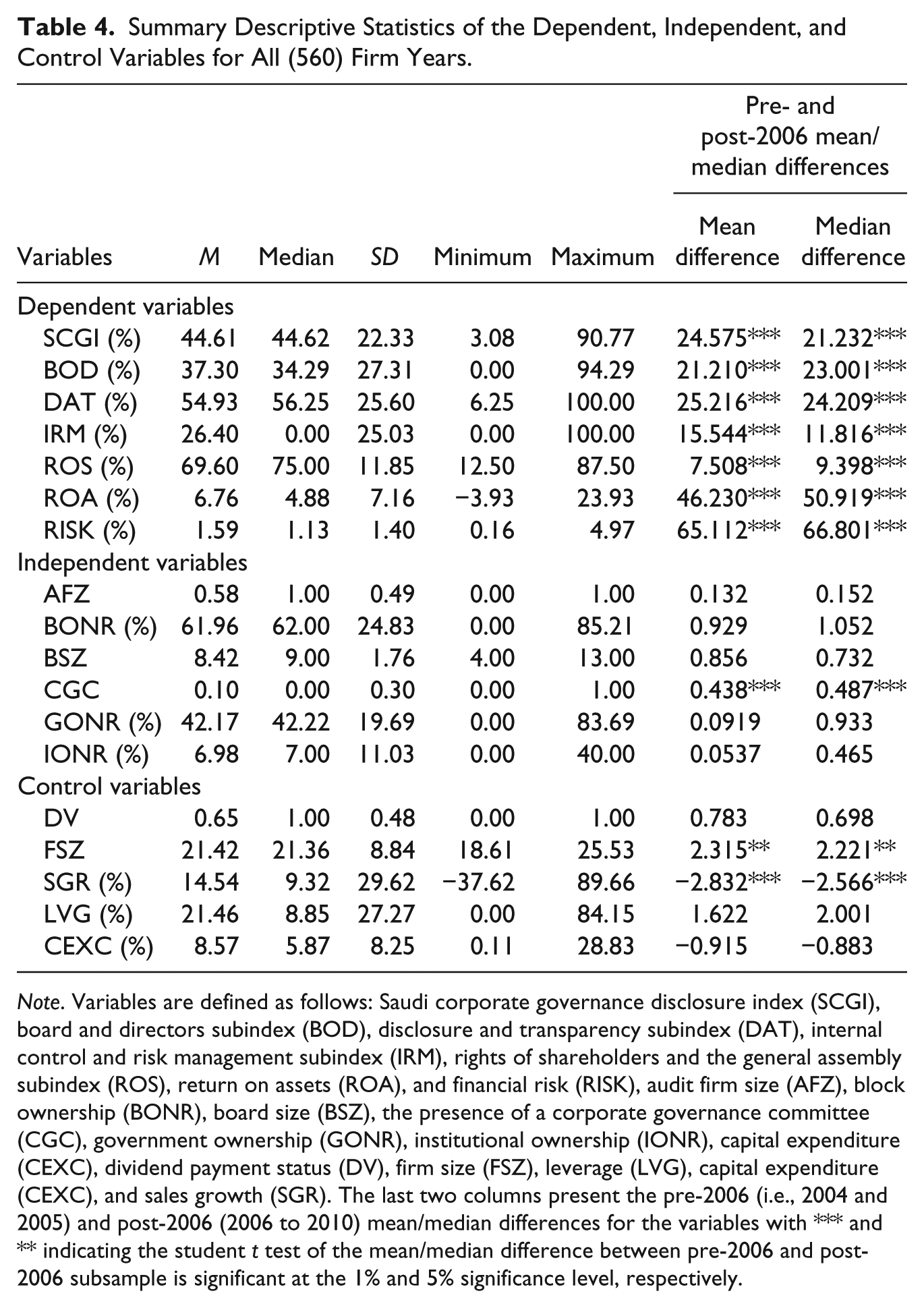

Table 4 reports summary statistics relating to the independent and control variables used. In addition, the summary statistics relating to the SCGI and its components are also repeated in Table 4 from Table 3 for the sake of completeness. Similar to the SCGI, the distribution of all the independent and control variables generally display wide variations. For example, return on assets (ROA) ranges from a minimum of 3.93% to a maximum of 23.93% with mean (median) of 6.76% (4.88%), suggesting that the average Saudi listed firm was profitable over the period analyzed. Similarly, board size (BSZ) ranges from a minimum of 4 to a maximum of 12 with a median (mean) of 9 (8.42) board members. This compares well with the findings of previous studies relating to the distribution of corporate board size (Barako et al., 2006; Haniffa & Hudaib, 2006; Hooghiemstra, 2012; Hussainey & Al-Najjar, 2012; Mallin & Ow-Yong, 2012). For instance, Haniffa and Hudaib (2006) report an average board size of 10 for a sample of Malaysian listed firms. In line with the findings of past studies (Alsaeed, 2006; Bozec & Bozec, 2007; Piesse et al., 2012; Soliman, 2013a, 2013b), BONR is between a minimum of 0.00% (i.e., no block owners) and a maximum of 85.21% with a mean (median) of 61.96% (62.00%), suggesting that Saudi firms ownership structure is relatively highly concentrated. The figures for the CG indices (SCGI, BOD, DAT, IRM, and ROS), AFZ, CGC, GONR, and IONR, as well as the control variables in Table 4 suggest substantial variation in our sample, and thus reducing any possibilities of sample selection bias.

Summary Descriptive Statistics of the Dependent, Independent, and Control Variables for All (560) Firm Years.

Note. Variables are defined as follows: Saudi corporate governance disclosure index (SCGI), board and directors subindex (BOD), disclosure and transparency subindex (DAT), internal control and risk management subindex (IRM), rights of shareholders and the general assembly subindex (ROS), return on assets (ROA), and financial risk (RISK), audit firm size (AFZ), block ownership (BONR), board size (BSZ), the presence of a corporate governance committee (CGC), government ownership (GONR), institutional ownership (IONR), capital expenditure (CEXC), dividend payment status (DV), firm size (FSZ), leverage (LVG), capital expenditure (CEXC), and sales growth (SGR). The last two columns present the pre-2006 (i.e., 2004 and 2005) and post-2006 (2006 to 2010) mean/median differences for the variables with *** and ** indicating the student t test of the mean/median difference between pre-2006 and post-2006 subsample is significant at the 1% and 5% significance level, respectively.

Observably, the student t test of the differences in means/medians of pre-2006 and post-2006 suggests that significantly more CG committees were voluntarily set up by Saudi listed firms in the post-2006 period to specifically monitor voluntary disclosure of CG practices than in the pre-2006 period. This seems to explain the observed significantly higher levels of compliance and disclosure of CG practices in the post-2006 period compared with the pre-2006 period, and implying generally that the presence of a CG committee impacts positively on voluntary disclosure of CG practices. In addition, the significantly positive and negative student t test for FSZ and SGR, respectively, indicate that Saudi firms have become relatively larger in terms of total asset value, while their growth has been significantly slower in the post-2006 period compared with the pre-2006 period, which may be explained by the negative effects of the 2007/2008 global financial crisis.

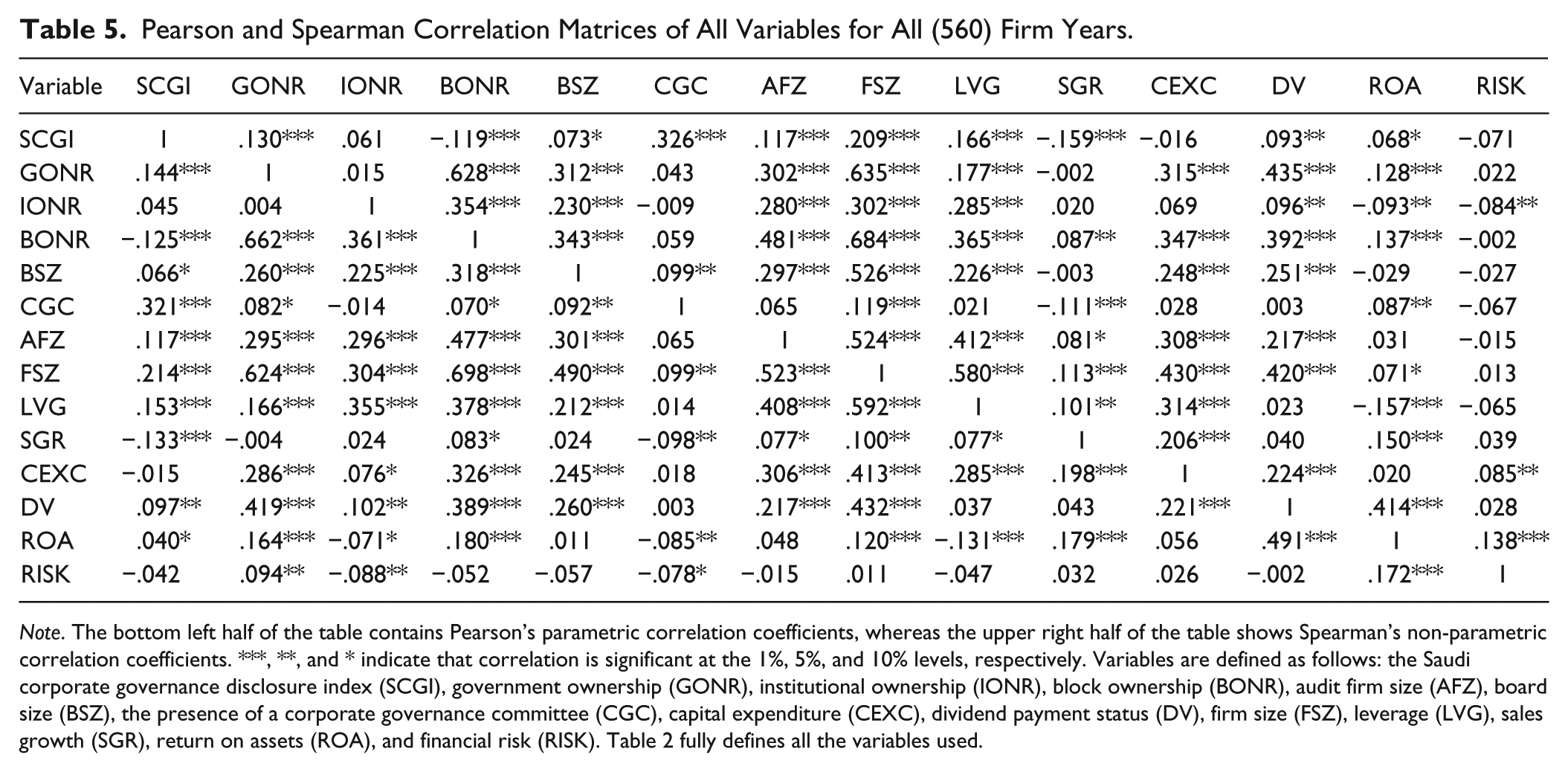

The authors use OLS regression technique to test all our six hypotheses, and thus it is appropriate to initially examine a number of OLS assumptions, including multicollinearity, autocorrelation, normality, homoscedasticity, and linearity. Table 5 reports the correlation matrix for all variables used in the study’s analysis to test for multicollinearity. As robustness check, both the Pearson’s parametric and Spearman’s non-parametric coefficients are reported and, observably, the magnitude and direction of both coefficients are very similar, indicating that no major non-normalities remain. Both matrices suggest further that correlations among the variables are fairly low, indicating that no serious multicollinearities exist. In addition, the authors investigated (for brevity not reported here, but available on request) scatter plots for P-P and Q-Q, studentized residuals, Cook’s distances and Durbin–Watson statistic for homoscedasticity, linearity, normality, and autocorrelation, respectively, with the tests suggesting no serious violation of these OLS assumptions.

Pearson and Spearman Correlation Matrices of All Variables for All (560) Firm Years.

Note. The bottom left half of the table contains Pearson’s parametric correlation coefficients, whereas the upper right half of the table shows Spearman’s non-parametric correlation coefficients. ***, **, and * indicate that correlation is significant at the 1%, 5%, and 10% levels, respectively. Variables are defined as follows: the Saudi corporate governance disclosure index (SCGI), government ownership (GONR), institutional ownership (IONR), block ownership (BONR), audit firm size (AFZ), board size (BSZ), the presence of a corporate governance committee (CGC), capital expenditure (CEXC), dividend payment status (DV), firm size (FSZ), leverage (LVG), sales growth (SGR), return on assets (ROA), and financial risk (RISK). Table 2 fully defines all the variables used.

Table 5 indicates statistically significant connections between the SCGI and the explanatory variables, and also between the SCGI and the control variables. For example, and as hypothesized, AFZ, BSZ, CGC, and GONR are statistically significant and positively associated with the SCGI, whereas BONR is statistically significant and negatively related to the SCGI. Observably, IONR is statistically insignificant, but positively associated with the SCGI.

With reference to the control variables, the findings suggest that larger (FSZ), highly geared (LVG), and dividend paying (DV) corporations make significantly more voluntary CG disclosures, whereas growing (SGR) corporations make significantly less voluntary CG disclosures. There is, however, no evidence to suggest that more capital intensive (CEXC) Saudi corporations make significantly less or more voluntary CG disclosures than their less capital intensive counterparts.

Empirical Results From Multivariate Regression Analyses

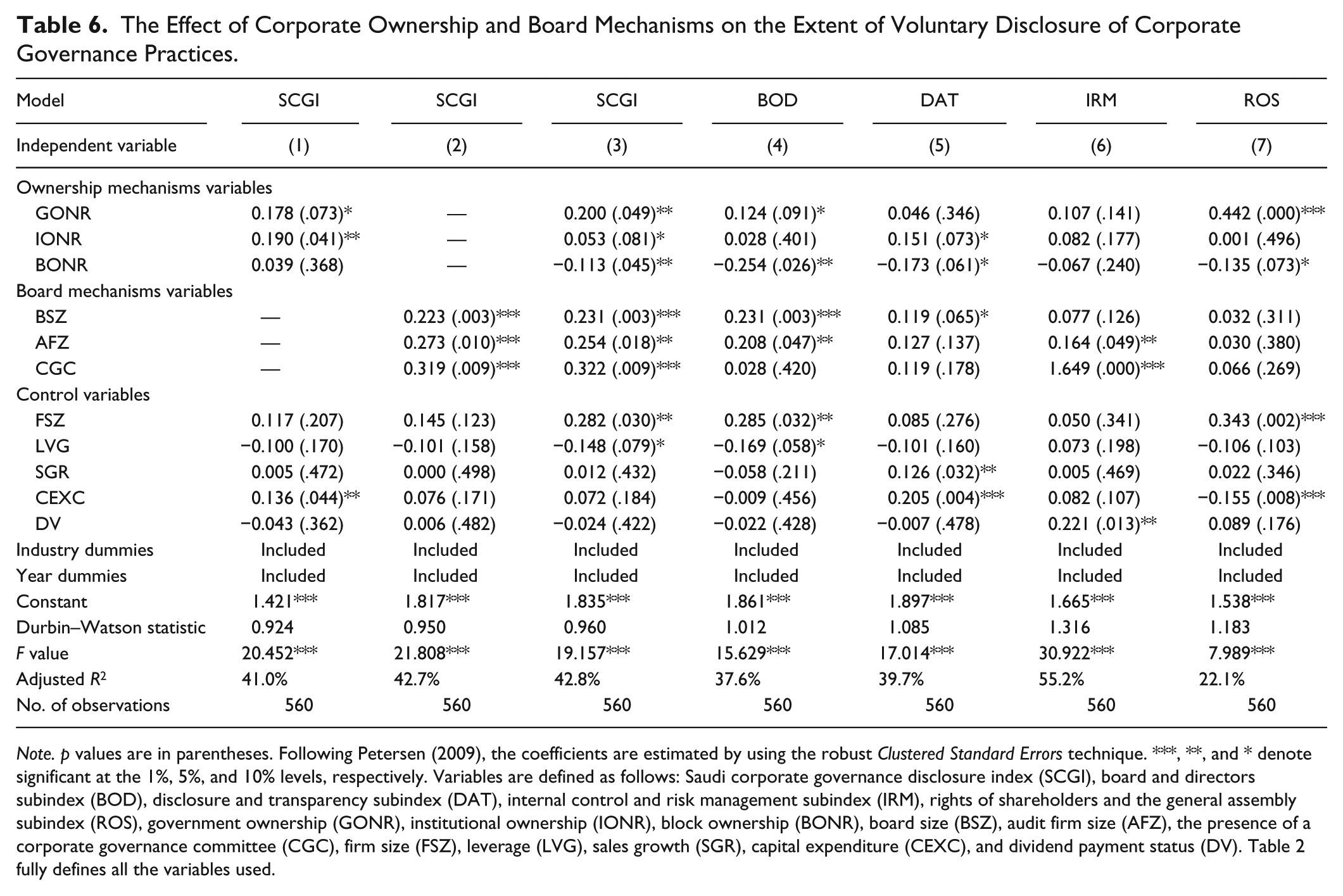

Table 6 reports the results of the regression analyses of the effects of corporate ownership and board mechanisms on the extent of voluntary CG disclosures. Models 1, 2, and 3 report the results of a pooled OLS regression of the ownership, board mechanisms, and both ownership and board mechanisms along with the control variables on the SCGI (Saudi CG index), respectively. The results contained in Model 3, which is the study’s main model, generally indicate that the independent variables (ownership and board mechanisms) are significant in explaining cross-sectional differences in the voluntary CG disclosures.

The Effect of Corporate Ownership and Board Mechanisms on the Extent of Voluntary Disclosure of Corporate Governance Practices.

Note. p values are in parentheses. Following Petersen (2009), the coefficients are estimated by using the robust Clustered Standard Errors technique. ***, **, and * denote significant at the 1%, 5%, and 10% levels, respectively. Variables are defined as follows: Saudi corporate governance disclosure index (SCGI), board and directors subindex (BOD), disclosure and transparency subindex (DAT), internal control and risk management subindex (IRM), rights of shareholders and the general assembly subindex (ROS), government ownership (GONR), institutional ownership (IONR), block ownership (BONR), board size (BSZ), audit firm size (AFZ), the presence of a corporate governance committee (CGC), firm size (FSZ), leverage (LVG), sales growth (SGR), capital expenditure (CEXC), and dividend payment status (DV). Table 2 fully defines all the variables used.

First, the study’s results indicate that the coefficients on GONR, IONR, AFZ, BSZ, and CGC are statistically significant and positively related to the SCGI, implying that Saudi corporations with high GONR, IONR, AFZ, BSZ, and CGC generally make significantly more voluntary CG disclosures.

The results in Model 3 of Table 6 suggest that BONR is statistically significant and negatively related to the SCGI, implying that Saudi corporations with block ownership disclose less on their CG practices. This finding offers empirical support for our multitheoretical framework, which suggests that closer managerial monitoring and lesser information asymmetry that is usually associated with block ownership can be expected to minimize agency problems (agency theory) and improve financial performance (Botosan, 1997; Jensen, 1993; Jensen & Meckling, 1976), and hence a lesser need for increased CG disclosures to gain legitimacy (legitimacy theory) from powerful corporate stakeholders (stakeholder theory), such as creditors, employee unions, government, and shareholders, whose resources (resource dependence), for example, finance, contacts and contracts, are arguably critical to the ability of any corporation to maintain sustainable operations (Branco & Rodrigues, 2008; Chen & Roberts, 2010). Thus, in this case, block ownership can serve as a substitute for good governance arrangements, including less disclosure relating to CG practices (Y. Bozec & Bozec, 2007). In contrast, disperse ownership requires greater monitoring, which can be minimized through increased corporate disclosures (Eng & Mak, 2003; Ntim & Soobaroyen, 2013a, 2013b). This also supports H1 and the findings of past studies, which suggest that BONR affects negatively on voluntary CG and CSR disclosures (Abdelsalam & Street, 2007; Alsaeed, 2006; Y. Bozec & Bozec, 2007; Ntim, Opong, & Danbolt, 2012; Ntim, Opong, Danbolt, & Thomas, 2012; Ntim & Soobaroyen, 2013a, 2013b; Patel et al., 2002), but is not in line with the results of those that report a positive link between BONR and voluntary disclosure (Eng & Mak, 2003; Tsamenyi et al., 2007). In addition, the economic importance of this finding is that a one standard deviation change (decrease) in BONR may lead to about 2.81% (i.e., 24.83% × 0.113) change (i.e., increase) in the level of the SCGI.

Second and by contrast, the positive association between IONR and the SCGI provide empirical support for H2 and the findings of past studies that suggest that corporations with high IONR make more voluntary CG and CSR disclosures (Barako et al., 2006; Hooghiemstra, 2012; Mallin & Ow-Yong, 2012), as well as those that report a positive link between institutional ownership and performance (Fung & Tsai, 2012). The findings also offer support for recent attempts by the CMA at increasing institutional shareholding as part of the broader efforts at improving CG standards in Saudi corporations (IFC, 2008; SFG, 2009). Theoretically, the result is largely in line with the predictions of our multitheoretical framework that draws on insights from agency, legitimacy, resource dependence, and stakeholder theories. For example, agency theory suggests that due to their larger ownership stakes, institutional shareholders, as influential corporate stakeholders (stakeholder theory), have extra incentive to closely monitor corporate disclosures (Core, 2001; Fung & Tsai, 2012; Jensen & Meckling, 1976). Therefore, managers will not only be expected to make more voluntary disclosures, including CG practices to meet the informational needs of institutional shareholders as powerful (stakeholder theory) corporate stakeholders (Deegan, 2002; Parker, 2005) but also to secure their support to legitimize (legitimacy theory) or justify their continued stewardship of the company and its critical resources (resource dependence theory; Branco & Rodrigues, 2008; Chen & Roberts, 2010). Economically, this finding implies that a one standard deviation change (increase) in IONR may be associated with about 2.10% (11.03% × 0.190) change (increase) in the level of the SCGI.

The positive connection between GONR and the SCGI provides empirical support for H3 and the results of Eng and Mak (2003), Al-Janadi et al. (2013), Ntim, Opong, Danbolt, and Thomas (2012), Ntim et al. (2013), and Ntim and Soobaroyen (2013a, 2013b) suggest that corporations with high government ownership make significantly more voluntary CG and CSR disclosures, as well as the broader objectives of government investments. Through the GOSI, PIF, and PPA, the Saudi government holds significant ownership stakes in major corporations with keen interest in positively influencing CG and stakeholder issues. Thus, this finding offers empirical support for our multitheoretical framework. Specifically, this finding suggests that as a powerful stakeholder (stakeholder theory) and given the Saudi government’s (through the CMA) formal support for the recommendations of Saudi CG Code (Alshehri & Solomon, 2012; CMA, 2006), Saudi companies with high government ownership tend to actively seek to win government support (Deegan, 2002; Ntim & Soobaroyen, 2013a, 2013b) by complying with the Saudi CG Code’s provisions through increased disclosure of CG practices that may not only help in legitimizing (legitimacy theory) their operations (Ashforth & Gibbs, 1990; M. C. Unerman, 1995) but also secure access to critical resources (resource dependence theory; Branco & Rodrigues, 2008; Reverte, 2009), such as finance that can enhance performance. Also, agency theory suggests that increased disclosure of CG practices can help resolve agency problems between managers and government as an influential shareholder (Core, 2001; Jensen & Meckling, 1976). Furthermore, potential political interference and conflict of interests’ problems between shareholders and government that is often associated with government ownership can be minimized through increased voluntary disclosure (Eng & Mak, 2003; Ntim & Soobaroyen, 2013a, 2013b). The economic relevance of this finding is that a one standard deviation change (increase) in IONR may be associated with about 3.94% (19.69% × 0.20) change (increase) in the level of the SCGI.

Furthermore, the positive coefficients on BSZ, AFZ and CGC indicate that H4, H5, and H6, respectively, are supported. The positive relationship between BSZ and SCGI is in line with the evidence of previous studies (Al-Janadi et al., 2013; Hooghiemstra, 2012; Hussainey & Al-Najjar, 2012; Mallin & Ow-Yong, 2012; Ntim et al., 2013; Ntim, Opong, & Danbolt, 2012; Ntim, Opong, Danbolt, & Thomas, 2012; Ntim & Soobaroyen, 2013a, 2013b; Rouf, 2011; Samaha et al., 2012). Similarly, the evidence that AFZ impacts positively on voluntary CG disclosure is consistent with the findings of previous studies (Al-Janadi et al., 2013; Eng & Mak, 2003; Han et al., 2012; Owusu-Ansah, 1998), whereas the positive effect of CGC on SCGI offers new empirical support for the findings of Ntim, Opong, Danbolt, and Thomas (2012), Ntim et al. (2013), and Ntim and Soobaroyen (2013a, 2013b). The positive CGC–SCGI nexus is also in line with the univariate (see Table 4) and bivariate (see Table 5) evidence, which suggests that establishing a CG committee to specifically monitor compliance and disclosure of CG practices can contribute positively toward enhancing CG standards. With respect to board size, theoretically, increased managerial monitoring associated with larger boards can have a positive influence on corporate disclosures, including CG ones and performance (Jensen, 1993; Jensen & Meckling, 1976). In a similar vein, and with respect to audit firm, larger audit firms have greater financial strength, knowledge, and independence, which can affect positively on voluntary CG disclosure (DeAngelo, 1981; Eng & Mak, 2003; Han et al., 2012; Owusu-Ansah, 1998). Economically, the implications of these findings can be quantified as, a one standard deviation change (increase) in BSZ, AFZ, and CGC may be associated with about 0.40% (1.76 × 0.231), 12.45% (49% × 0.254) and 9.66% (30% × 0.322) change (increase) in the level of the SCGI, respectively.

Third, the study’s findings so far suggest that cross-sectional differences in the SCGI can be explained by the independent variables, but as it contains voluntary CG disclosures from four different categories, it is possible for the link between each category and the independent variables to vary, with some potentially having strong connections with these variables and others maintaining weak associations. Thus, to examine the link between each voluntary CG disclosure subcategory and the independent variables, the authors reestimated Equation 1 by replacing the SCGI with the BOD, DAT, IRM, and ROS at a time, and the findings are, respectively, presented in Models 4 to 7 of Table 6.

The coefficients on the GONR (except the coefficient on the DAT and IRM), IONR (except the coefficient on the BOD, IRM, and ROS), BSZ (except the coefficient on the IRM and ROS), AFZ (except the coefficient on the DAT and ROS), and CGC (except the coefficient on the BOD, DAT and ROS) remain statistically significant and positively related to all four voluntary CG disclosure subcategories. Similarly, the coefficient on BONR (except the coefficient on the IRM) remains statistically significant and negatively associated with all four disclosure subcategories, and thus largely offering further empirical support for our previous findings. The observed sensitivities in the coefficients also reflect the differences in the levels of disclosure with respect to the four CG disclosure subcategories that are evident in Table 3, implying that Saudi corporations differ in terms of the importance that they attach to the various sections of the 2006 Saudi CG code.

Finally, the coefficients on the control variables in Table 6 are generally consistent with expectations. For example, the coefficients on CEXC, DV, FSZ, and SGR are positively associated with the SCGI, whereas the coefficient on LVG is negatively related to the SCGI. However, the coefficients relating to the control variables are not always statistically significant or consistent across the different models.

Additional Analyses

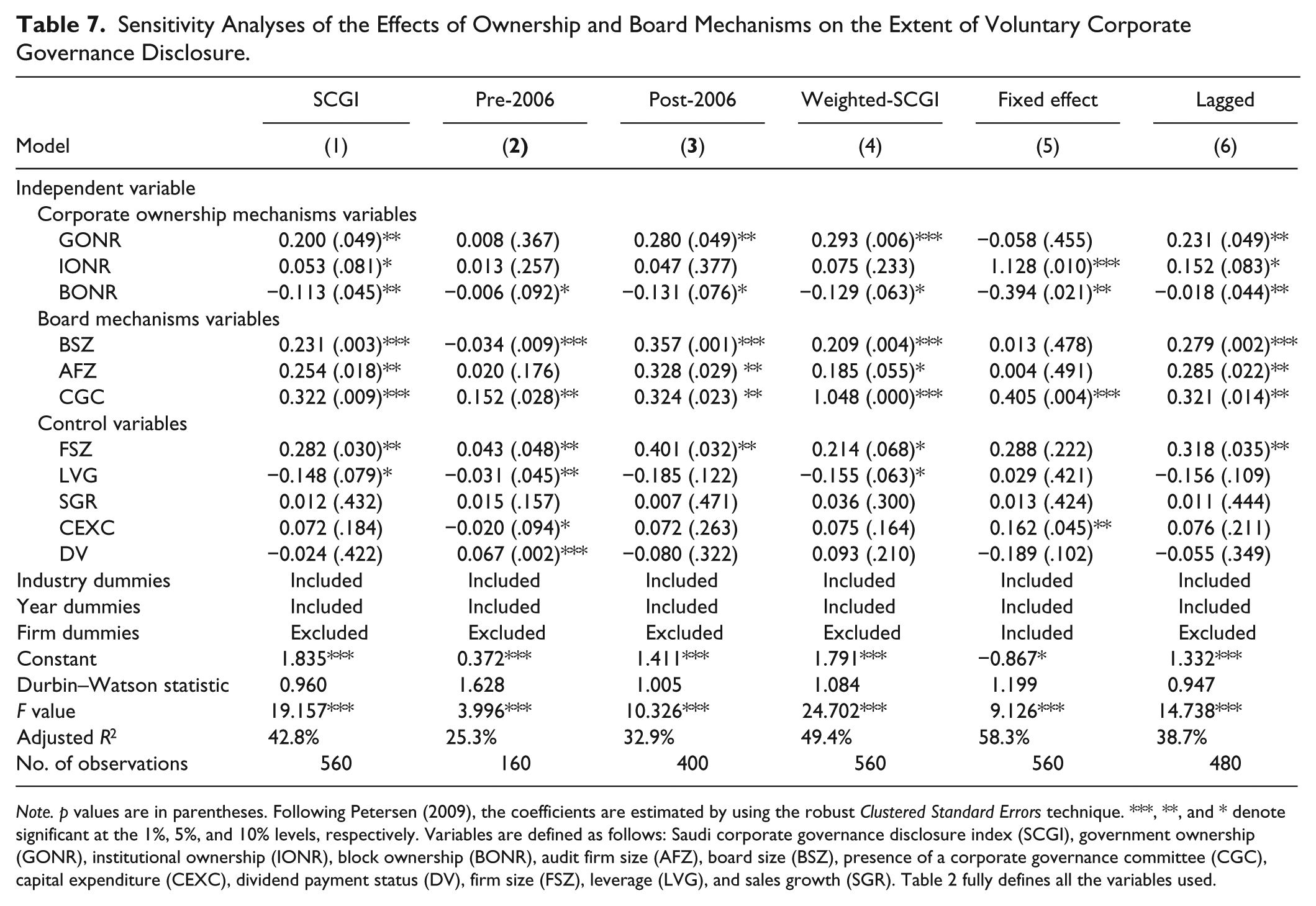

The study carries out additional analyses to investigate the robustness of our findings. First, and as previously discussed, our sample period covers the 2004 to 2010 period. Therefore, to ascertain whether there are differences in this study’s results with respect to the period of examination, the authors reestimated the study’s regression by splitting the sample into two subsamples: pre-2006 (i.e., from 2004 to 2005) and post-2006 (2006 to 2010) periods. To facilitate comparison, Model 1 of Table 7 repeats the main findings contained in Model 3 of Table 6. The results reported in Models 2 and 3 for the pre-2006 and post-2006 periods, respectively, are generally similar. However, the statistical significance of the post-2006 period findings are relatively strong compared with that of the pre-2006 period, suggesting that the introduction of the 2006 Saudi CG Code appears to have helped in improving CG practices, and consequently, a tighter association between voluntary CG disclosures and board/ownership mechanisms.

Sensitivity Analyses of the Effects of Ownership and Board Mechanisms on the Extent of Voluntary Corporate Governance Disclosure.

Note. p values are in parentheses. Following Petersen (2009), the coefficients are estimated by using the robust Clustered Standard Errors technique. ***, **, and * denote significant at the 1%, 5%, and 10% levels, respectively. Variables are defined as follows: Saudi corporate governance disclosure index (SCGI), government ownership (GONR), institutional ownership (IONR), block ownership (BONR), audit firm size (AFZ), board size (BSZ), presence of a corporate governance committee (CGC), capital expenditure (CEXC), dividend payment status (DV), firm size (FSZ), leverage (LVG), and sales growth (SGR). Table 2 fully defines all the variables used.

Second and as previously explained, all 65 provisions constituting the SCGI are equally weighted, but the number of provisions varies across the four sections, resulting in different weights being assigned to each section: BOD, 54%; DAT, 25%; IRM, 9%; and ROS, 12%. To ascertain whether the study’s results are robust to the weighting of the four sections, the authors construct an alternative SCGI, defined as Weighted-SCGI, in which each section is awarded equal weight of 25%. Although there are slight changes with regard to the magnitude of the coefficients, the study’s results reported in Model 4 of Table 7 remain essentially the same as those presented in Model 3 of Table 6, and thus the study’s general conclusions remain unchanged.

Third, differences in the opportunities and challenges that corporations encounter vary over time, implying that voluntary CG disclosure behavior may be jointly and dynamically determined by unobserved firm-specific characteristics (Henry, 2008), which simple OLS regression may be unable to detect (Gujarati, 2003; Petersen, 2009). Hence, given the panel nature of the study’s data set, the authors run a fixed-effects model to control for possible unobserved firm-specific heterogeneity. This involves reestimating Equation 1, with the introduction of 79 dummies to represent the 80 sampled corporations. The study’s fixed-effects results reported in Model 5 of Table 7 remain largely unaltered, implying that the study’s findings are not sensitive to potential unobserved firm-specific heterogeneity.

Finally, to address potential endogeneity problems that may arise from a simultaneous relationship between the board/ownership mechanisms and the CG disclosures, the authors estimate a lagged structure (i.e., by introducing a 1-year gap between the CG disclosures and board/ownership mechanisms), whereby the current year’s CG disclosures depend on the previous year’s board/ownership mechanisms. Similarly, the results reported in Model 6 of Table 7 is essentially the same as those contained in Model 1 of the same table, suggesting that the study’s findings are generally robust to potential endogeneity problems that may arise from the existence of a simultaneous link between board/ownership mechanisms and the SCGI. Overall, the evidence emerging from the study’s additional analyses make the authors reasonably confident that the study’s findings are not driven by any endogenous relationships.

Summary and Conclusion

A number of emerging countries have pursued CG reforms around the world. In this vein, Saudi Arabia, a major G-20 country, has also pursued CG reforms in the form of the 2006 Saudi CG Code, notably adopting the U.K.-style voluntary (“comply or explain”) compliance regime. However, the Saudi corporate context is characterized by a highly hierarchical social structure, concentrated ownership, low institutional ownership, and weak enforcement of corporate regulations. These have raised critical concerns as to whether a voluntary compliance regime will be effective in improving CG standards. This article has investigated whether and to what extent publicly listed Saudi corporations voluntarily comply with and disclose recommended good CG practices, and distinctively, examined whether the observed cross-sectional differences in such voluntary CG disclosures can be explained by ownership and board mechanisms. The study used a sample of 80 Saudi listed firms from 2004 to 2010 and 65 CG provisions based on the 2006 Saudi CG Code for our analysis.

Apart from applying a multitheoretical framework in interpreting the study’s findings, the authors make a number of new contributions to the extant literature. First, analysis of the levels of compliance with the constructed voluntary compliance and disclosure index generally indicates that, despite the expectation that the introduction of the 2006 Saudi CG Code would speed-up convergence of CG practices, CG standards among Saudi listed corporations still vary substantially. At the aggregate levels, the scores range from a minimum of 3.08% to a maximum of 90.77% with the average sampled corporations complying with 44.61% of the 65 CG provisions examined, as well as the mean CG score increasing from 17.08% in 2004 to 73.15% in 2010. Whereas this is line with the variation in compliance levels reported by previous studies, it indicates that a high degree of heterogeneity exists when it comes to the importance that Saudi listed corporations attach to CG. However, despite concerns as to whether a voluntary CG regime will be effective given the Saudi corporate setting, the scores indicate that compliance levels and CG standards among the sampled corporations have generally improved over the 7-year period investigated.

Second, the study’s analysis of the factors driving voluntary compliance and disclosure suggests that ownership structure and board mechanisms are generally significant in explaining differences in disclosure. Specifically, the study’s results suggest that corporations with larger boards, a Big 4 auditor, higher government ownership, a CG committee, and higher institutional ownership disclose considerably more than those that are not. By contrast, the authors find that an increase in block ownership significantly reduces voluntary CG disclosure. The study’s results are generally robust to a number of econometric models that control for different types of disclosure indices, general firm-specific characteristics, and firm-level fixed effects.

Third, the study’s evidence has important implications for policy makers and regulators. For example, evidence of increasing compliance with the Saudi CG Code implies that efforts by various stakeholders, notably the CMA and Saudi Stock Exchange (Tadawul, 2012), at improving CG standards in Saudi corporations have had some positive impact on CG practices of Saudi corporations. However, the large differences in the levels of compliance suggest that enforcement may need to be strengthened further. In this vein, establishing a “compliance and enforcement committee” to continuously monitor compliance levels among listed corporations may be a step in the right direction. Similarly, as the presence of institutional shareholders and a Big 4 audit firm is demonstrated to have a positive effect on good CG practices, it provides the CMA, “Tadawul,” and the Saudi government the impetus to encourage greater institutional ownership and a Big 4 auditing of Saudi listed corporations. Also, for managers and corporations, our evidence suggests that one way by which they can improve their CG standards is to establish a CG committee with the specific mandate to monitor their firms’ compliance with corporate rules and regulations, especially those relating to good CG practices.

Finally, while the study’s evidence is important and robust, some caveats are considered appropriate. We employ a binary scoring scheme, which treats every CG disclosure as equally important. While findings based on the study’s unweighted and weighted indices are essentially the same, future studies may improve their analysis by constructing weighted and unweighted voluntary CG disclosure indices. Similarly, as a result of data limitations, the study’s analysis is limited to a number of factors that can influence voluntary CG disclosure. As data availability improves, future studies may need to investigate how other potential factors, such as foreign ownership and the number of analysts, influence voluntary CG disclosure. Furthermore, the authors collected the study’s data from corporate annual reports to conduct quantitative analyses. However, annual reports can sometimes convey mixed messages. Therefore, future studies may improve on the study’s evidence by employing qualitative approaches, such as conducting face-to-face interviews and case studies with relevant stakeholders, such as auditors, company directors, the CMA, investors, and “Tadawul.” This may provide a holistic understanding of the different determinants of, and motives for, voluntary CG disclosures. Furthermore, the authors note that because a considerable number of popular corporate board mechanisms, such as CEO role duality, frequency of board meetings, the proportion of independent non-executive directors, the presence of board subcommittees (e.g., audit, nomination, and remuneration committees), and executive compensation information are contained in the Saudi CG Code (see the appendix), the authors are unable to include them as part of the potential factors that can explain observable cross-sectional differences in the level of voluntary disclosure of recommended CG practices. The study’s analyses are, therefore, limited to corporate board factors (e.g., board size) and other CG mechanisms (e.g., audit firm size and the presence of a CG committee), which are not already contained in the Saudi CG index. Future studies may, therefore, enhance the insights that they offer by examining the extent to which these factors may influence voluntary CG disclosure.

Footnotes

Appendix

Full List of the Saudi Arabian Corporate Governance Disclosure Index (SCGI) Provisions Based on the 2006 Saudi Corporate Governance Code

| Corporate governance (CG) disclosure index (SCGI) |

|||

|---|---|---|---|

| SCGI theme | SCGI Item: Information on or reference to | Range of scores | Total score per item |

| i. Board of directors | Board of directors and composition | 35 | |

| 1. Whether the roles of chairperson and CEO/MD are split | 0-1 | ||

| 2. Whether the chairperson is an independent non-executive director (NED) | 0-1 | ||

| 3. Whether the board is composed by a majority of NEDs | 0-1 | ||

| 4. Whether directors are clearly classified into executive directors, NEDs, and independent NEDs | 0-1 | ||

| 5. Whether at least 1/3 of the board are independent NEDs | 0-1 | ||

| 6. Whether directors’ membership on boards of other firm’s are disclosed | 0-1 | ||

| 7. Whether members of the board do not hold directorships on more than five other listed firms | 0-1 | ||

| 8. Whether the board of directors’ meetings record is disclosed. | 0-1 | ||

| 9. Whether individual director’s meeting attendance record is disclosed | 0-1 | ||

| 10. Whether directors’ biography, qualifications, experience and responsibilities are disclosed | 0-1 | ||

| Audit committee | |||

| 11. Whether the committee has been established | 0-1 | ||

| 12. Whether the committee’s remit/terms of reference is disclosed | 0-1 | ||

| 13. Whether the committee is composed entirely by at least 3 NEDs | 0-1 | ||

| 14. Whether at least a member of the committee is literate in financial and accounting matters, such as being a chartered certified accountant | 0-1 | ||

| 15. Whether the chairperson of the committee is disclosed | 0-1 | ||

| 16. Whether the chairperson of the committee is an independent NED | 0-1 | ||

| 17. Whether members of the committee is disclosed | 0-1 | ||

| 18. Whether the committee’s meetings record is disclosed | 0-1 | ||

| 19. Whether the individual members’ meetings attendance record is disclosed | 0-1 | ||

| Nomination committee | |||

| 20. Whether the committee has been established | 0-1 | ||

| 21. Whether the committee’s remit/terms of reference is disclosed | 0-1 | ||

| 22. Whether the committee consists of a majority of independent NEDs | 0-1 | ||

| 23. Whether the chairperson of the committee is disclosed | 0-1 | ||

| 24. Whether the chairperson of the committee is an independent NED | 0-1 | ||

| 25. Whether the members of the committee is disclosed | 0-1 | ||

| 26. Whether the committee’s meetings record is disclosed | 0-1 | ||

| 27. Whether the individual members’ meetings attendance record is disclosed | 0-1 | ||

| Remuneration committee | |||

| 28. Whether the committee has been established | 0-1 | ||

| 29. Whether the committee’s remit/terms of reference is disclosed | 0-1 | ||

| 30. Whether the committee is composed entirely by independent NEDs | 0-1 | ||

| 31. Whether the chairperson of the committee is disclosed. | 0-1 | ||

| 32. Whether the chairperson of the committee is an independent NED | 0-1 | ||

| 33. Whether the members of the committee is disclosed | 0-1 | ||

| 34. Whether the committee’s meetings record is disclosed | 0-1 | ||

| 35. Whether the individual members’ meetings attendance record is disclosed | 0-1 | ||

| ii. Disclosure and transparency | 36. Whether the firm’s ownership structure is disclosed | 0-1 | 16 |

| 37. Whether the firm’s directors own at least 1,000 of the firm’s shares | 0-1 | ||

| 38. Whether the details of compensation paid to directors are disclosed | 0-1 | ||

| 39. Whether board’s total value of annual compensation of each director equals or is less than US$53,000 or 10% of firms’ profit | 0-1 | ||

| 40. Whether the details of the CEO’s compensation are disclosed | 0-1 | ||

| 41. Whether the details of top management’s compensation are disclosed | 0-1 | ||

| 42. Whether a review of the firm’s operations and performance is disclosed | 0-1 | ||

| 43. Whether the details of firm’s debt/loans are disclosed | 0-1 | ||

| 44. Whether a firm’s 5-year financial performance is compared/disclosed | 0-1 | ||

| 45. Whether a firm’s strategies and objectives are disclosed | 0-1 | ||

| 46. Whether the principal activities of the firm are disclosed | 0-1 | ||

| 47. Whether a firm’s dividend policy is disclosed | 0-1 | ||

| 48. Whether a firm discloses any related party transactions | 0-1 | ||

| 49. Whether a firm has been penalized for breaking corporate regulations by a supervisory body, such as the Tadawul and Capital Market Authority | 0-1 | ||

| 50. Whether a board statement on the going-concern status of the firm is disclosed | 0-1 | ||

| 51. Whether a narrative regarding compliance/non-compliance with the Saudi CG code is provided | 0-1 | ||

| iii. Internal control and risk management | 52. Whether an audit report regarding the effectiveness of internal control system is disclosed | 0-1 | 6 |

| 53. Whether the firm’s risk management policy, philosophy and procedures are disclosed | 0-1 | ||

| 54. Whether the major risks facing the firm are disclosed | 0-1 | ||

| 55. Whether a statement to the effect that the financial reports have been approved by the board of directors, CEO and chief financial officer (CFO) is disclosed. | 0-1 | ||

| 56. Whether the board of directors provides a statement regarding consistent application of generally accepted accounting principles | 0-1 | ||

| 57. Whether the firm has drafted a corporate governance code | 0-1 | ||

| iv. Rights of shareholders and the GA | 58. Whether a narrative regarding fact that the general assembly (GA) is held at least once a year is disclosed | 0-1 | 8 |

| 59. Whether a narrative regarding the fact the agenda for a firm’s GA meeting had been announced on the Tadawul website is disclosed | 0-1 | ||

| 60. Whether a narrative regarding the fact that the firm’s shareholders have the right to vote by proxy is disclosed | 0-1 | ||

| 61. Whether a narrative regarding the fact the firm operates a one-vote-one-share policy is disclosed | 0-1 | ||

| 62. Whether a narrative regarding the fact that the firm announces a GA meeting at least 20 days prior to the date of the meeting is disclosed | 0-1 | ||

| 63. Whether a narrative regarding the fact that the firm immediately informs the stock exchange through the Tadawul website about the outcome of the GA meeting is disclosed | 0-1 | ||

| 64. Whether a narrative regarding the fact that the GA convenes within 6 months following the end of the firm’s financial year is disclosed | 0-1 | ||

| 65. Whether the firm discloses its social contributions. | 0-1 | ||

| Total | 65 SCGI Items | 65 | |

| Scoring procedure | |||

| 0 = If a particular corporate governance item is not disclosed | |||

| 1 = If a particular corporate governance item is disclosed | |||

Acknowledgements

We would like to acknowledge insightful and timely suggestions offered by the Associate Editor, Professor Dima Jamali and three anonymous reviewers. We also acknowledge useful comments received at presentations at the Accounting Workshop (University of Southampton, Southampton, 2013), and Welsh Accounting and Finance Annual Workshop (Gregynog, 2013).

The article was accepted during the editorship of Duane Windsor.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.