Abstract

Australia has proven to be a popular destination for Indian students seeking higher education qualifications. In recent years, the influx of Indian students into Australia has shown considerable volatility and so has their enrollment mix between the further, vocational and higher education sectors. An understanding of the motivations and characteristics of potential and current Indian international students along with the changing dynamics of the global higher education sector is important to be able to analyse this volatility and to ensure effective and sustainable marketing of higher education to Indian students. This paper provides a profile of Indian students studying in Australia and provides insight into their course preferences and motivations for choosing Australia. A key finding of this paper is that apart from traditional motivators such as higher rates of returns and employability associated with a foreign qualification, Indian students are very responsive to changes in Australia’s labour market, immigration and student visa policies relative to other international alternatives.

Keywords

Introduction

India has enjoyed considerable economic growth since the reforms of 1991. Prosperity in India has brought with it a higher derived demand for education, especially at the tertiary level. As the incomes of middle class Indians have steadily increased, it has brought with it a desire for training that leads to a more sophisticated skill set and qualifications that are in demand by employers both in India and abroad. While the Indian education system has tried to maintain pace with this increased demand, increasingly, Indian students are choosing overseas destinations to acquire tertiary skills.

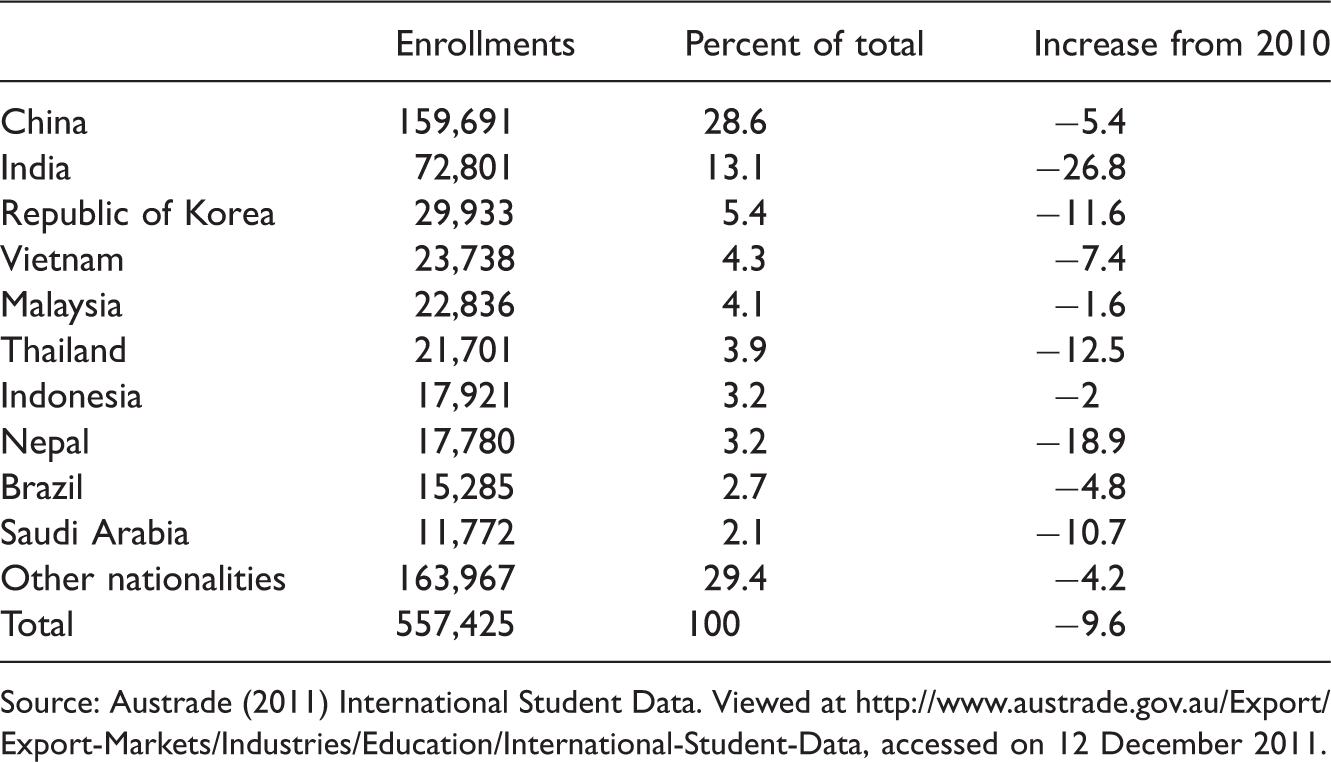

Total new international student enrollments in Australia by nationality, 2011.

Source: Austrade (2011) International Student Data. Viewed at http://www.austrade.gov.au/Export/Export-Markets/Industries/Education/International-Student-Data, accessed on 12 December 2011.

In this paper, the decision making of potential international students is analysed in the context of an established theoretical framework, including the role of push and pull factors. Push factors relate to the decision to study abroad, whereas pull factors relate to the choice of an international destination. Push factors relate to variables present in the home country, whereas pull factors relate to host country variables. Among the factors that will receive particular attention in this paper are the absence of suitable educational opportunities at home, the costs associated with studying, the relative quotas for university places in the home and host country, the reputation of host country institutions and the accreditation of qualifications acquired in the host country in the home labour market. The paper will also examine the role of visa and immigration policy on international student demand.

Explaining demand for overseas university places

Lewis established a theoretical framework to examine the growth in demand for higher education in Australia and elsewhere in the 1980s and 1990s (see, for example, Lewis, 1995; Lewis & Pratt, 1996; Lewis & Shea, 1995; Lewis & Smart, 2002). Under this framework, there needs to be a level of economic development and structural change in a Newly Industrialised Economy (NIE), which creates a demand for professional, highly educated labour. The availability of well-paid professional jobs makes investment in higher education profitable. A growing relatively-rich middle class also demands education opportunities for their children and has the wealth to finance it. The demand for overseas education arises because of the lack of supply of quality places in domestic education institutions and increasing market demand for highly skilled workers. For an NIE such as India, ensuring that there is an adequate supply of highly skilled workers is important to protect and upgrade its comparative advantage and its position in the global knowledge economy. As stressed by Kelly and Lewis (2010) and Guruz (2011, p. 198) Most jobs in the global knowledge economy require educational qualifications at the tertiary level. Jobs are disappearing, skills needed to perform existing jobs are changing, and new jobs are appearing, which require entirely new skills. These have led to an increasing demand by a tertiary age cohort for higher education worldwide.

The motivation of Indian students to pursue a foreign degree can be analysed in the context of the above theoretical framework, which highlights important ‘push’ variables. The choice of destination on the other hand is determined by a number of ‘pull’ factors. These factors have been documented by Mazzarol and Soutar (2002) and include:

the overall level of knowledge and awareness of the host economy possessed by potential international students; the level of personal recommendations or referrals regarding the host country; cost issues related to studying and living in the host country, along with other social costs; the relative host country environment with respect to lifestyle, physical climate and education system; the presence of expatriate social networks from the home country in the host country; the quality and reputation of host country institutions and an intention to assimilate into the host country’s culture and to migrate after graduation.

Indian higher education students in Australia

Our analysis of international student data is discussed in the context of the above framework. The Indian demand for Australian university places is a function of the level of economic development in India, the supply and quality constraints faced by the Indian higher education system and the cost of immigration and student visa regimes prevalent in Australia. These important factors are discussed in turn.

According to World Bank estimates, in 2010 India had a nominal gross domestic product of 1727.1 billion US dollars (USD) and GDP per capita of 3500 USD in purchasing power parity terms. The World Bank (2012) further forecasted average annual growth of 6.5% in GDP per capita between 2010 and 2014.

As discussed earlier, the demand for higher education is a derived demand closely related to economic prosperity and the rise of the middle class in India. Research by the McKinsey Global Institute (MGI) charted the rise of the middle class in India and its implications for stakeholders such as higher education marketers. The report stated that in India the global urban class, comprising those households that have annual incomes between 22,000 and 90,000 USD, will accelerate rapidly between 2015 and 2025. MGI (2007) forecasted 14% annual growth in the global urban class in India. This is estimated to result in a market segment of 15 million households in 2025 that have the capacity to pay for higher education, with an additional 2 million consumers joining this market category each year afterwards (MGI 2007, p. 70).

Furthermore, investment in education has always been important to middle class Indian households who invest heavily in education. Expenditure on education grew at 11% compound annual growth rate between 1985 and 2005. MGI (2007) predicts that this growth is expected to continue in the future with an expected increase in private education expenditure to increase to 127.9 billion USD in 2025. Saxena (2010) also identified the growth of the middle class and economic development in India as a virtuous cycle given the link between higher income levels and increased levels of consumption on goods such as higher education.

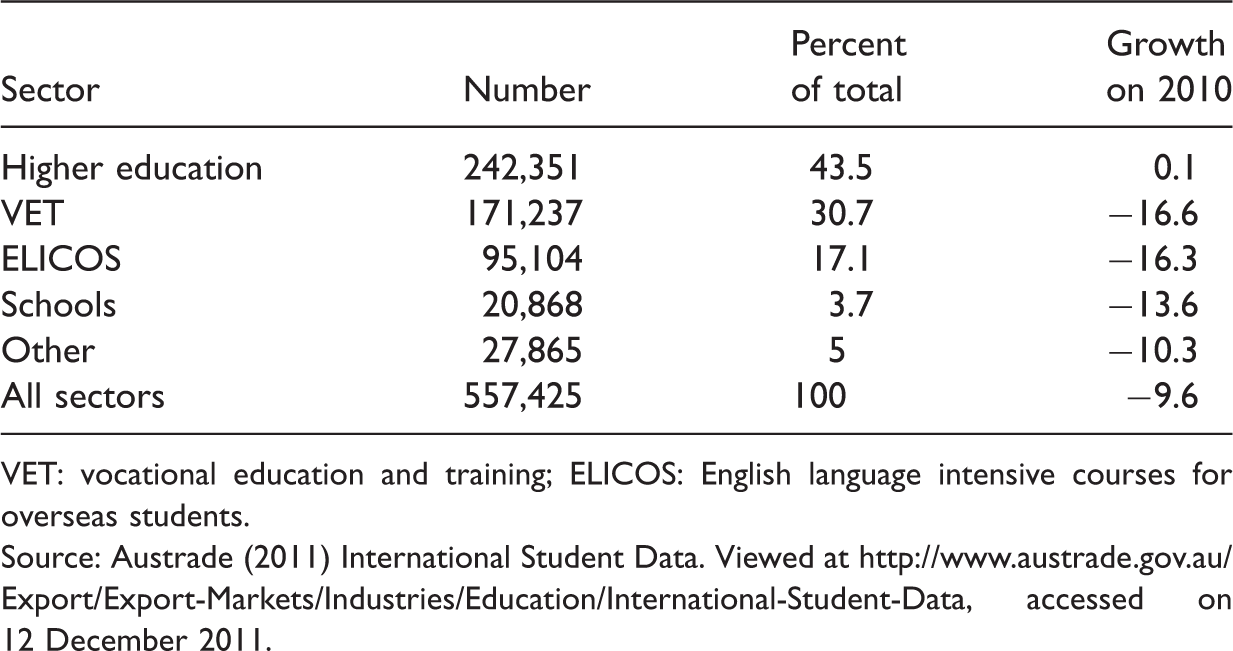

International student enrollments in Australia by sector, 2011.

VET: vocational education and training; ELICOS: English language intensive courses for overseas students. Source: Austrade (2011) International Student Data. Viewed at http://www.austrade.gov.au/Export/Export-Markets/Industries/Education/International-Student-Data, accessed on 12 December 2011.

Although this paper is primarily concerned with the higher education sector, the VET sector is used to illustrate the evolution of Indian student enrollments. The VET sector has its own unique characteristics and challenges, but a detailed discussion of these factors is beyond the scope of this paper.

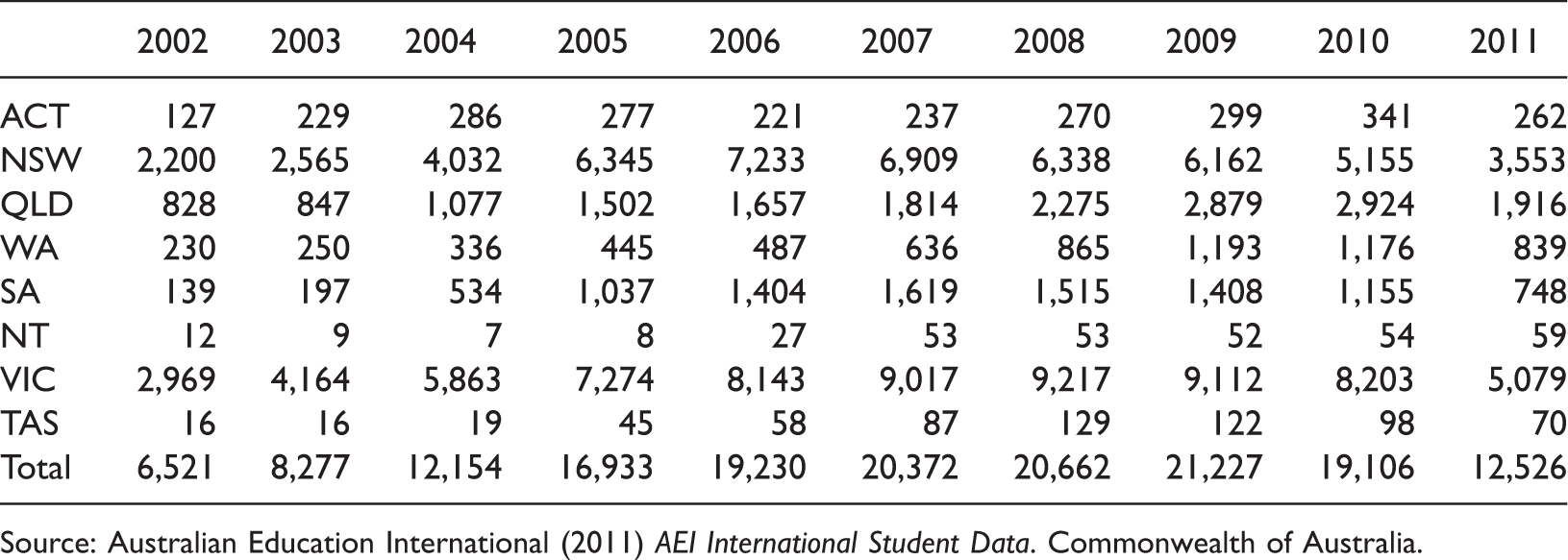

New enrollments in higher education in Australia from India, 2002–2011.

Source: Australian Education International (2011) AEI International Student Data. Commonwealth of Australia.

As shown in Table 3, Indian higher education students are predominantly clustered in Victoria and New South Wales. In recent years, Victoria has shown the most drastic drop in higher education enrollments from Indian students. In general, total enrollments peaked in 2009 and have been declining since then. However, for New South Wales the peak occurred even earlier in 2006. The popularity of New South Wales and Victoria is not surprising as Sydney and Melbourne both possess large well-established Indian communities, as well as vibrant services industries that provide opportunities for part-time employment.

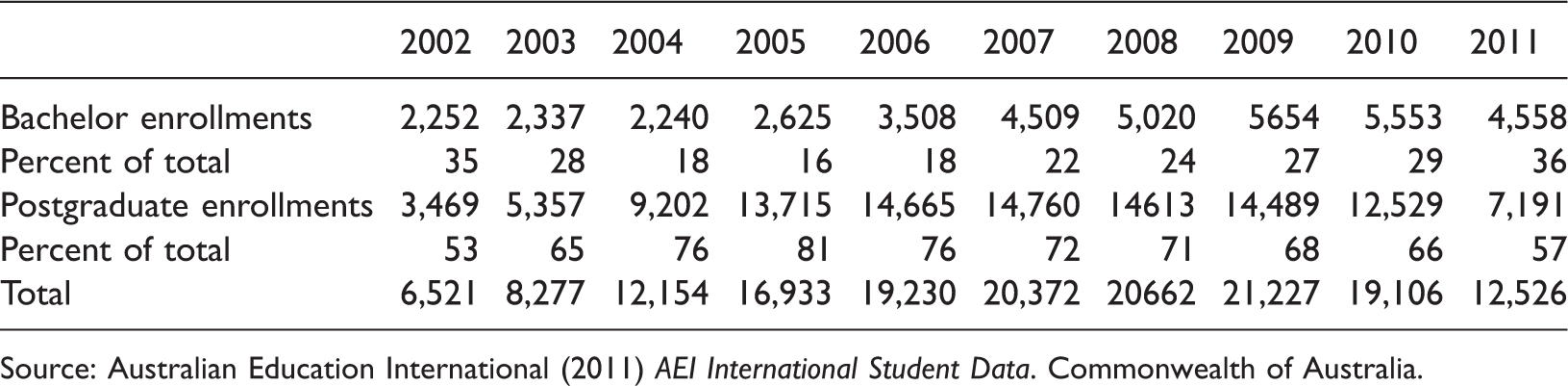

Composition of higher education enrollments in Australia from India.

Source: Australian Education International (2011) AEI International Student Data. Commonwealth of Australia.

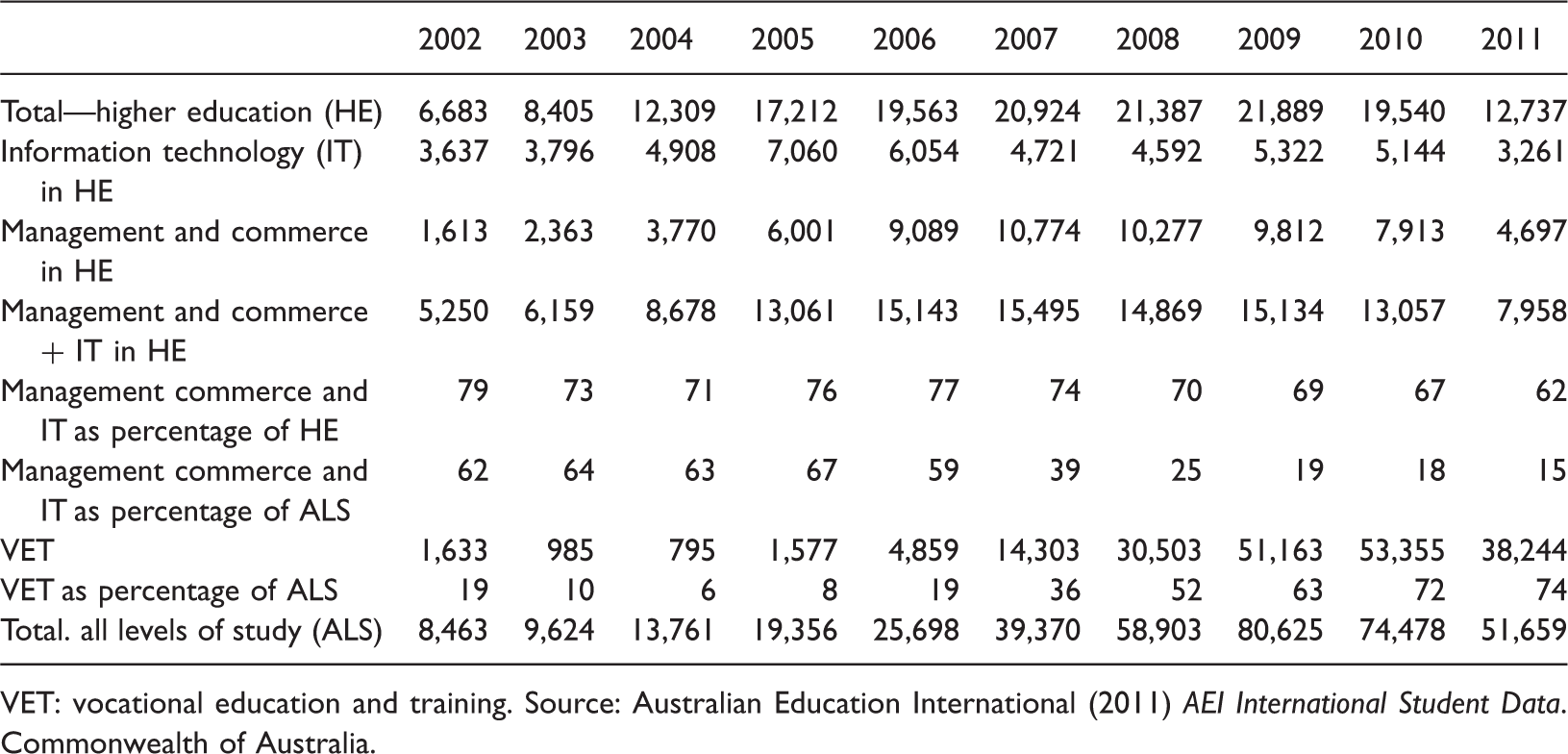

Composition of Indian enrollments in Australia by field and level of study.

VET: vocational education and training. Source: Australian Education International (2011) AEI International Student Data. Commonwealth of Australia.

Indian higher education: supply constraints, quality concerns and market dynamics

The Indian higher education sector has not been able to keep up with accelerating market demand. Sampat, Maru, and Shah (2008) provided a recent account of the Indian higher education sector stating that, at the time of writing, India had 18,000 higher education institutions and 10.5 million tertiary students. More recently, Austrade (2012, p. 12) provided estimates of the size of the higher education sector in India, stating that from 1947 to 2010, the number of universities in India has increased from 207 to 475, the number of colleges have increased from 500 to 20,677 and teaching staff increased from 1500 to nearly 500,000. The student population in higher education has also increased from 100,000 in 1950 to over 11.2 million in 2010.

However, a simple headcount of institutions is liable to lead to a misleading conclusion in India’s case. As Stella (2004) mentions, India has the second largest tertiary education sector in the world; however, the efficacy of this sector is constrained by financial, quality and social issues and at a cost of three billion USD, education remains one of India’s biggest imports (Rajan, 2006). Within India, the higher education sector is growing, but at a very uneven pace. As identified by Azam and Blom (2008), government-backed institutions still account for the bulk of the higher education sector in India. However, these are growing very slowly and suffer from poor quality. Private institutions fare much better, but their growth has been constrained by red tape and the lack of co-ordination in curriculum design and accreditation.

Azam (2010), Agarwal (2008), Kijima (2006) and Rajan (2006) document that growth of university graduates started to slow in 1993, just as the economy took off, so that demand for university graduates soon exceeded the supply of graduates. Saxena (2010) highlighted the severe shortcomings of the Indian education sector mentioning that in 2007 only 13.5% of secondary school leavers enrolled in higher education within 5 years of finishing secondary schooling. High illiteracy and attrition rates are certainly responsible for the limited supply of graduates in India; gross enrollment in India in higher education was estimated at only 6% by Kaul (2006). However, more recent estimates by Austrade (2012) place this enrollment ratio at 11%.

Research by Austrade (2012) also highlighted weaknesses in the Indian education system. According to this report, participation rates in education in India are still very low and despite recent renewed efforts by the Indian government to improve investment in education, 35% of the population is still illiterate with only 15% of Indian students reaching high school. The graduation rate for higher secondary qualification is even lower at 7%. With respect to the supply constraints, the Austrade report states that as of 2008, India’s post-secondary high schools offered only enough places for 7% of India’s college-age population, with 25% of teaching positions nationwide left vacant due to unavailability of suitable staff and faculty. As an example, the report states that 57% of college professors lack either a master’s degree or PhD (Austrade 2012, p. 7).

The quota system, designed to improve the participation rate in higher education of backward castes and ethnicities in India, is also constraining supply of higher education in India by earmarking university places for these groups. In spite of its worthy intent, it has ultimately been ineffective due to a fundamental shortcoming. As identified by Deshpande (2009), Kaul (2006) and Murthy et al. (2007), in government institutions up to 50% of total places can be reserved for students from disadvantaged backgrounds. However, this approach is ineffective as it fails to recognise that these students often have very low representation at the primary and secondary level, and it is too late to correct the social, economic and educational neglect faced by these students by the time they get to the post-secondary level. In the meantime, the use of such quotas is creating misallocation of already scarce university places; many of these reserved seats remain vacant or are sold on the black market, thus reducing the number of competitive university places.

Viswanadhan, Rao, and Mukhopadhyay (2005) argue that due to a lack of funds and poor policy decisions by the Indian government, technical education, such as engineering, has not been able to cope with demand within the existing public universities. Viswanadhan et al. (2005) highlighted some of the shortcomings of the higher education sector in India, stating that

there was a mismatch between production and demand for skilled workers such as engineers; there were uneven standards at institutions; archaic curricula was being taught at institutions; the quality of training was poor; there were meagre infrastructure facilities; there was inadequate faculty; there was an absence of R&D activity and there was a tenuous link between technical institutions and user agencies.

The most recent account of the state of and challenges faced by the Indian higher and tertiary sector is provided in a working paper released by the Indian Government as part of the 11th 5-year plan (Government of India, 2011). The report is insightful in appreciating the severe shortcomings of the sector in India and the associated supply constraints that partially explain the demand for overseas tertiary education from India. As highlighted in this report, expenditure per student with respect to tertiary education has been steadily declining rather than increasing to meet the demands of a rapidly expanding economy. This is not entirely surprising given the high illiteracy rates prevalent in India along with low participation rates at the primary and secondary education level. In the long run, it is in India’s best interest to increase expenditure on improving basic literacy and participation rates at the primary and secondary level. However, in the meantime, the implication for the tertiary sector in India is that its expansion in the foreseeable future is going to be highly constrained.

Given the low education participation rates coupled with the low standard of most Indian universities, there is a chronic shortage of highly skilled workers in the Indian labour market. This shortage has resulted in the rapid increase in wages of those workers who possess advanced technical skills in fields such as IT, commerce, engineering, finance and management. These high wages are sending important signals to Indian students and employees. A high-quality degree in these fields is highly coveted in the Indian labour market. Therefore, students who have the capacity to pay are increasingly turning to foreign institutions to acquire these skills in an attempt to improve their employability.

Cost, safety and work opportunities

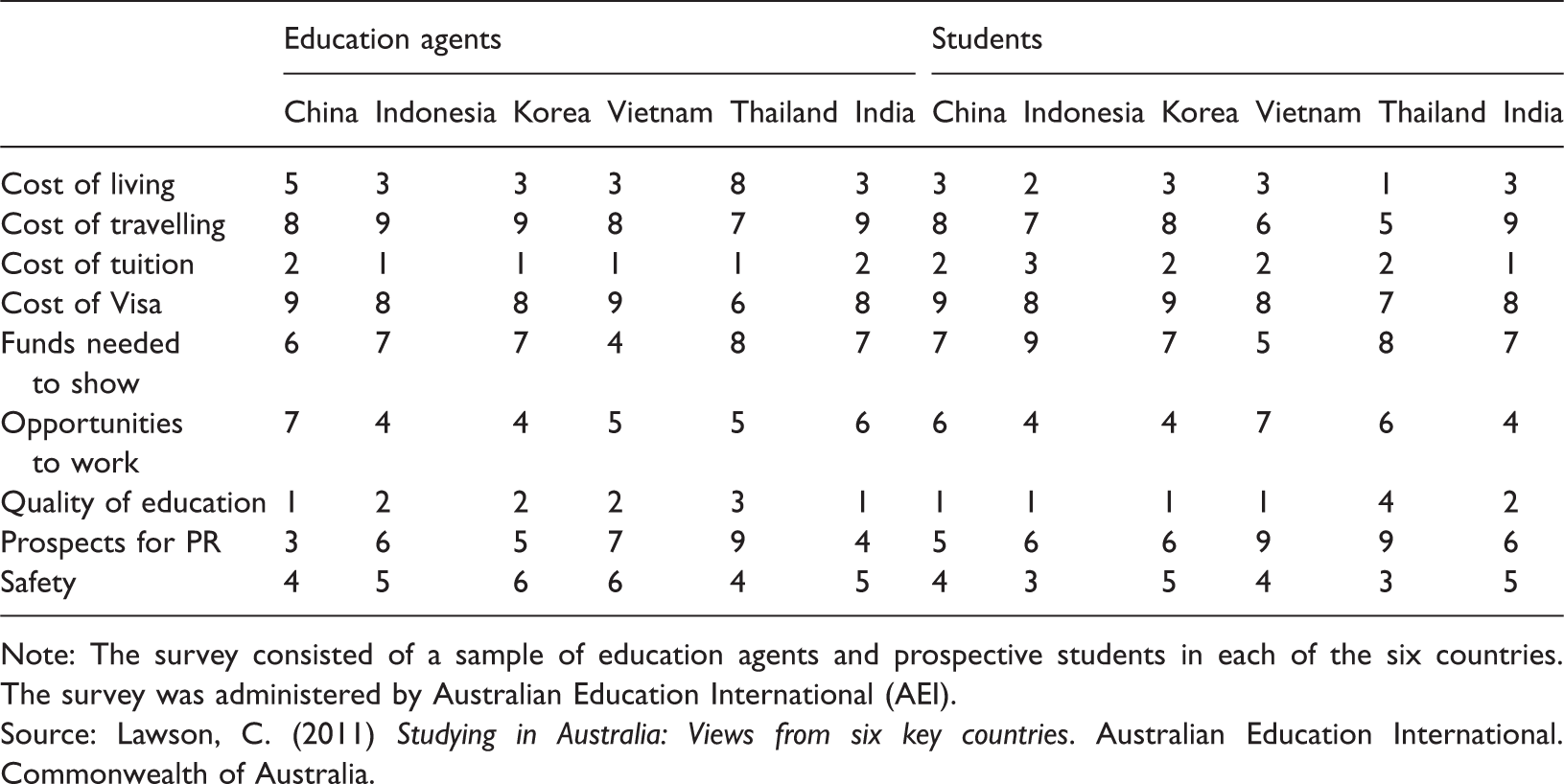

Ranked importance of factors when choosing an international destination.

Note: The survey consisted of a sample of education agents and prospective students in each of the six countries. The survey was administered by Australian Education International (AEI). Source: Lawson, C. (2011) Studying in Australia: Views from six key countries. Australian Education International. Commonwealth of Australia.

Daglish and Chan (2005) determined that the difficulty and complexity of obtaining a US visa as well as cost are two factors why Indian students choose Australia. The Australian student visa process is quite thorough and time consuming; but the 41 recommendations of the Knight review (2011) to be implemented by the Department of Immigration and Citizenship (DIAC) are intended to streamline the student visa process even further (DIAC 2011, 2012a). Once the changes are incorporated, they are expected to further increase the attraction of Australia as a tertiary destination.

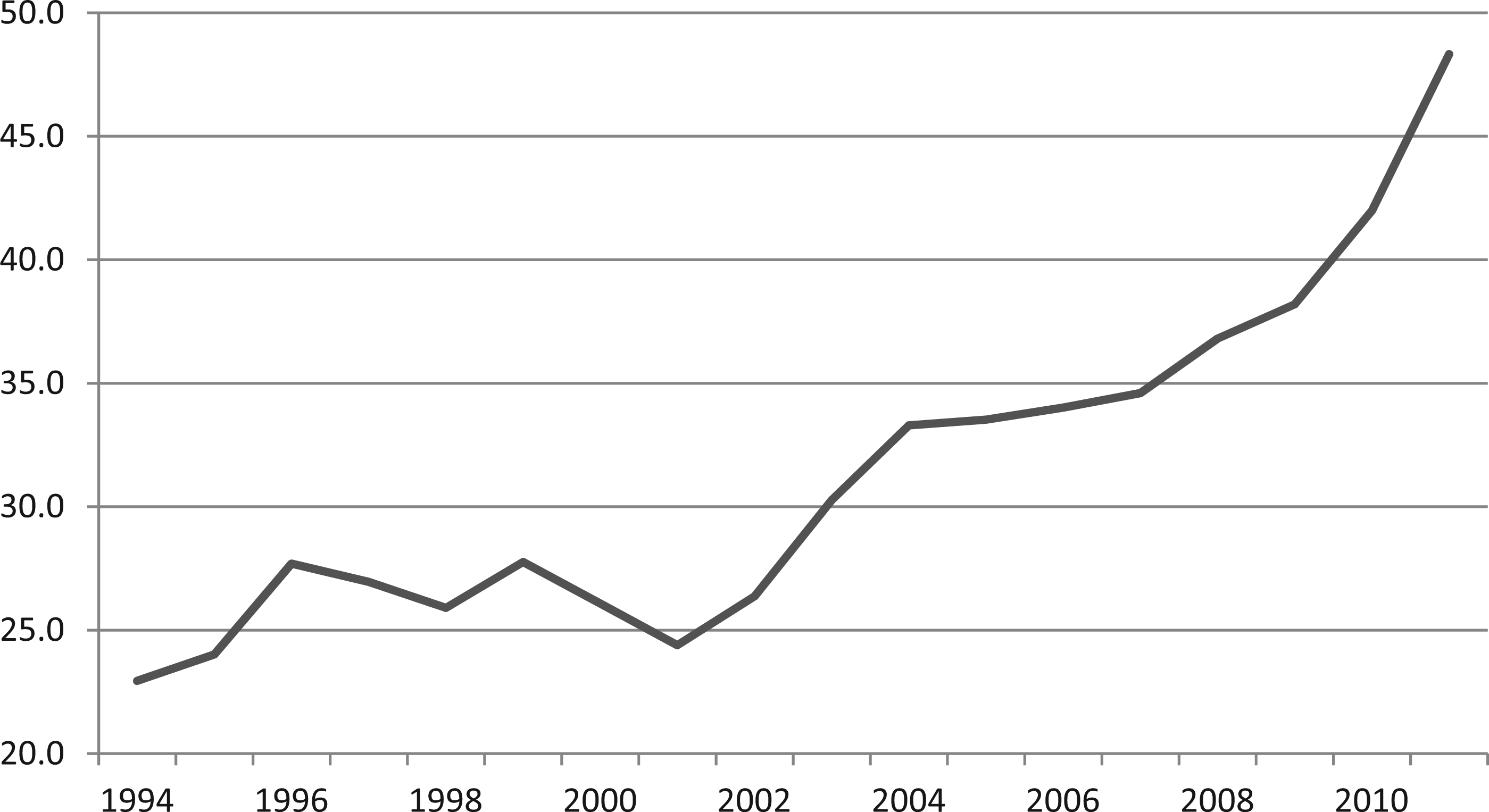

With respect to cost, as shown in Figure 1, the rapid increase in the Australian dollar – Indian Rupee Exchange rate in recent years is one factor that works against the competitiveness of the international Australian higher education sector and to some extent explains the decline in the growth of new enrollments from India illustrated in Tables 1–4.

Annual average Austrian dollar – Indian rupee exchange rate. Source: Oanda forex trading and exchange rate services. Viewed at www.oanda.com accessed on 12 March, 2012.

Other important factors identified by Daglish and Chan (2005) were the subject and course offerings and the quality of the host institution.

With regard to safety, Deumert, Marginson, Nyland, Ramia, and Sawir (2005) stated that, within the international education sector Australia was considered a relatively safe study destination as compared to other education-exporting nations. This is evident from the perception of Chinese, Taiwanese and Indonesian parents and students who preferred Australia as a destination for study over other international destinations. Mazzarol and Soutar (2001) cited by Deumert et al. (2005) also showed that the presence of a safe environment was the most significant predictor of intentions to choose an education importing destination.

Clearly, perceptions of safety on and off campus are an important factor considered by current and potential international students. This may be especially relevant with regard to Indian students, given the recent reported spate of muggings and physical violence directed at Indian international students in Melbourne. According to Singh and Cabraal (2010), in 2009 the 120,569 Indian international students in Australia compromised one third of the total Indian community in Australia and nearly half (46.9%) of Indian international students in Australia were enrolled in Victoria, predominantly in Melbourne. The very visible media profile given by the Indian press to the muggings of Indian students in Melbourne illustrates the effect that even isolated events can have on the perception of Australia as a safe destination for study. While there may not have been agreement between the Australian and Indian press on whether the attacks were racially motivated or isolated incidents, there was a reduction in the number of Indian students and tourists from India in the wake of the attacks, as admitted by the Australian Tourism Minister (The Hindu, 2010). Owens and Loomes (2010) therefore recommended that universities implement policies that enhance the social integration of international students with the wider student body and community.

The migration factor

Apart from existing factors identified so far, in relatively recent years there has been a strong relationship between Australian skilled migration policy and the behaviour of Indian students. As stated earlier, the preference for commerce and computer science courses, especially accounting and information technology (IT), by Indian students was partly due to priority processing and preferential treatment of immigration applicants graduating from Australian universities with qualifications in these fields (Knight, 2011). Immigration policy pre-2008 awarded extra points to accounting and IT graduates and other professions that were on the Migration Occupation in Demand List (MODL). This made it relatively easier to cross the threshold of 120 points required for a permanent residency visa. As advised by Skills Australia, at that time these skills were deemed critical to the Australian economy and were in short supply (DIAC, 2010c). As shown in Table 5, the popularity of IT and commerce majors persisted until 2007 and has since been slowly declining with the attempted decoupling of higher education and immigration policy by the Australian Government.

According to Birrell and Healy (2010), the initial surge of international students was due to immigration changes implemented between 1999 and 2001 by the Howard government. Revisions to skilled migration policy were announced in 2008 and have continued to shape Australia’s skilled migrant intake. Recent changes to the Australian skilled migration policy have been motivated by the realisation that there is a mismatch between the skills and competencies of graduating international students and the skills demanded by the Australian labour market. These changes include a new points test that emphasises strong English language skills and relevant work experience, rather than the possession of a particular qualification (DIAC, 2010a). The new points test along with a more frequently revised and narrower Skilled Occupation List (SOL) replaces the much wider and generic MODL. These revisions were designed to ensure that no one factor alone would determine the migration outcome but rather a combination of skills, qualifications and work experience will be required to clear the new pass mark (DIAC, 2010b).

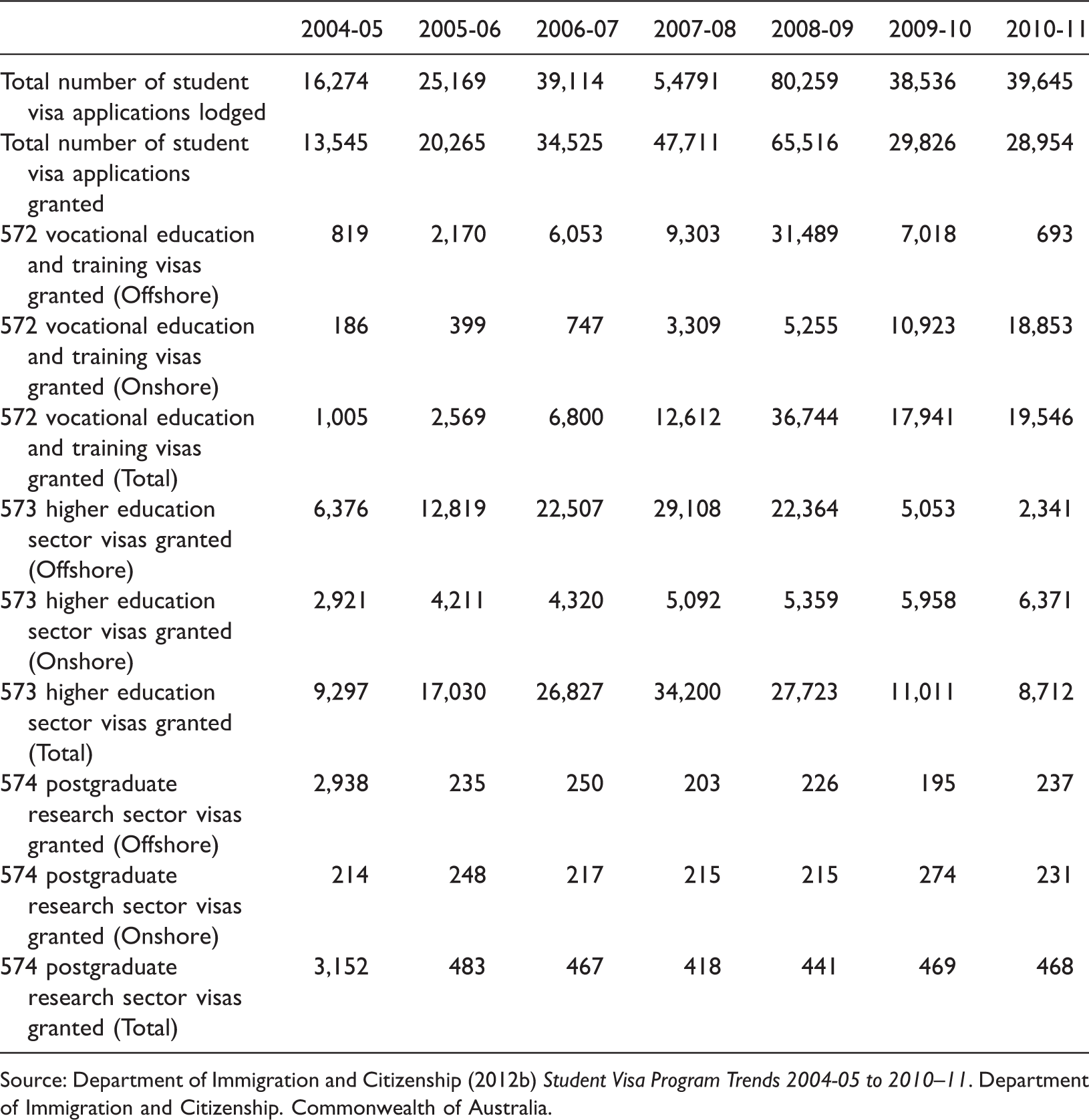

Selected student visa statistics for Indian student applicants for Australian visas.

Source: Department of Immigration and Citizenship (2012b) Student Visa Program Trends 2004-05 to 2010–11. Department of Immigration and Citizenship. Commonwealth of Australia.

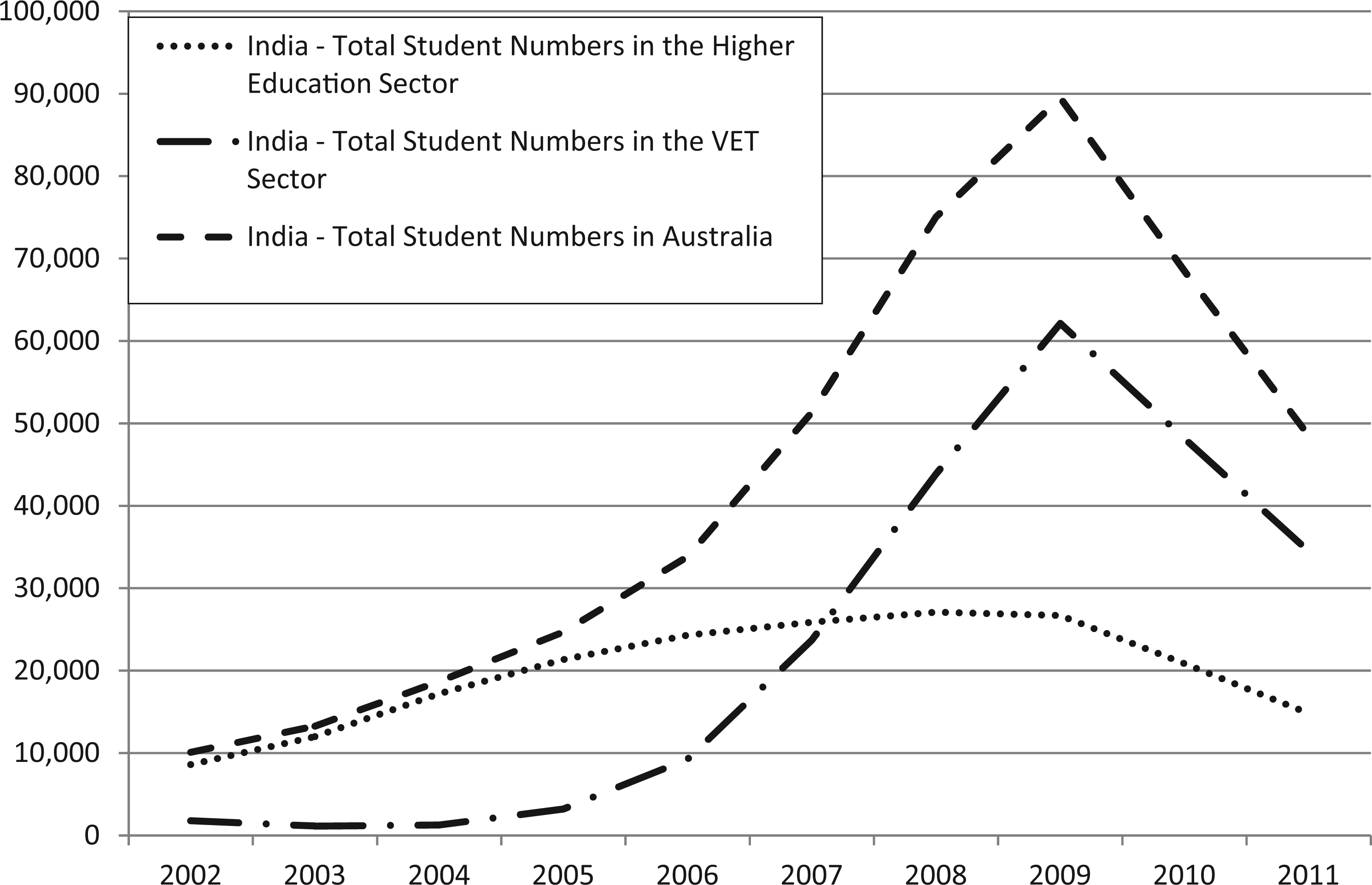

From Table 7, it is also evident that in recent years in light of changes to the student visa and skilled migration program, the largest impact has been on offshore applicants in India. This suggests that demand from new international Indian students has moderated given changes to skilled migration policy; this argument is corroborated by analysing the stock of Indian students in Australia. As illustrated in Figure 2, student numbers in Australia have displayed a marked downward trend following the rounds of policy revisions started in 2008. This may have been exacerbated by the appreciation of the Australian dollar as illustrated in Figure 1 and the perceived targeted muggings of Indian students.

Indian student numbers in Australia. Source: Australian Education International (2012) Unpublished Data.

Thus, it appears that recent skilled migration policy changes are closely related to Indian demand for Australian education as illustrated by decreasing enrollment numbers, student visas granted and student stocks. To counteract this decline based on the recommendations of the Knight review (2011), DIAC has responded by reducing the financial requirements for student visa candidates. DIAC has proposed changes to work restrictions to make them more flexible (Bita, 2012) and is planning on introducing post-study work visas from 2013 onwards that would let international students work for up to 4 years in Australia after graduation.

These steps by DIAC, along with positive publicity to emphasise the standing of Australia as a safe destination and the opportunities for part-time work in Australia compared to its competitors in the post-GFC recession, may result in a rebound in student numbers from India. Although there have been reports in the media (see, for example, Lane, 2012; Edwards, 2012) that offshore student visa applications and grants from India have again risen in 2012, the actual DIAC (2012c) data indicate little change in student visa applications from India between 2010/11 and 2011/2012. It is important to note that these policy measures were independent and outside the control of Australian universities and suggest that Australian universities have not done enough to differentiate their qualifications to Indian students relative to the alternatives, and have largely remained passive to changing market conditions.

The capacity of the higher education sector in Australia to satisfy international demand

On the supply side, there is also a limit as to how many international students the Australian higher education sector can absorb, Banks, Olsen, and Pearce (2007) analyse the sustainability and constraints of higher education exports for the OECD countries and state that Australia’s market share in the international higher education market is not forecast to grow much further. The strong Australian currency, increased competition from other education exporting countries, supply constraints in Australian universities and changes to immigration policy have all raised doubts about the future growth prospects of the industry in Australia.

Banks et al. (2007) forecast that Australia’s share of the international education market will grow from 163,345 new international enrollments to 290,848 new international enrollments in 2025. Between 2010 and 2015, growth in overseas demand for Australian tertiary places was forecast to decline from a high of 4.25% to 3%. Australian universities have also communicated their desire to maintain the mix of international students in the total student bodies to no more than 25%. However, if the number of domestic university students rises by as much as recommended in the Bradley Review (2008) and the size of the total international education market continues to grow proportionately to the size of the total domestic student body, then this may not be an issue for Australia.

However, this assumption may prove unrealistic given that Australia is not a very populous country and the supply of domestic students is unlikely to grow indefinitely. Therefore, it is possible that if Australian universities want to remain competitive in the international higher education sector they may have to increase the proportion of international students in their total student bodies. Currently, Australian universities maintain that they do have capacity to increase international student places. Banks et al. (2007) polled 38 out of the 39 universities in Australia, reporting that Australian universities will continue to increase international student places well into the future. Banks et al. (2007) predict that the growth rate of these places will start to decline from 2010, the growth rate will fall to 3% to 2012, will reduce to 2–3% per year to 2017 and will slow down to 1% to 2025. The overall capacity constraint, while being an operational and strategic consideration, is not the major problem.

The major problem has been the over concentration of overseas students, especially Indian students in disciplines such as IT and commerce. Gallagher (2002) expressed the view that this creates challenges for Australian universities, given that there are absorptive and supply constraints with regard to the intake of international students and their proportion in the total student body and across faculties and disciplines.

As pointed out by Guruz (2011), the globalisation and internationalisation of higher education have resulted in far greater choices and fewer barriers to mobility for international students and academic staff. Australian universities have to respond to the needs of the Indian market segment while emphasising and differentiating the worth of Australian qualifications relative to their competitors in the USA and the UK. Recent changes to immigration policies, the appreciating Australian dollar and the spate of violence against Indian students have shown that market perception and attractiveness of Australian qualifications can change dramatically.

This obviously creates serious challenges for the Australian higher education sector. On the one hand Australian universities want to capitalise on India’s growing demand for higher education, but this requires considerable commitment with respect to investment in physical infrastructure and human capital, as well as tailoring of courses and generic skills that appeal to international students such as those from India. This, however, carries with it a deal of risk in light of rapidly changing condition in the global higher education market.

It is possible that, in the future, to satisfy the Indian demand for higher education, Australian universities will change their mode of entry from exports to transnational education, which implies setting up of foreign campuses in India. Doing so may ultimately prove to be more cost-effective for potential Indian students while also being more responsive to their needs. At the same time, it will allow Australian universities to avoid the capacity constraints that the Australian higher education sector will likely face in its current guise. Considering a change in the mode of entry into the higher education market can also shield Australian universities from variables such as exchange rate fluctuations and immigration and visa policy revisions that are largely outside of their direct control.

Conclusion

India’s demand for Australian higher education can be explained in the light of the supply side constraints in the Indian higher education sector, and the dynamics of the Indian labour market and the Indian middle class. Australian education for Indian students is in the best interest of all stakeholders. Until recently, the trend of Indian students coming to Australia for higher education was positive and growing at a robust rate. In recent years, this trend, as measured by enrollment and student numbers, has moderated drastically. Analysis of international student data reveals that the behaviour of recent cohorts of Indian students has been influenced by changes and incentives provided by the general skilled migration program in Australia. However, this is not the only factor considered by potential Indian students as costs related to studying, safety and work opportunities all factor into their decision making.

The Australian higher education sector has a finite capacity to satisfy this demand given the supply constraints in the Australian higher education sector. Furthermore, given cost pressures and the recent volatility in enrollments from India, more targeted marketing of Australian higher education programs that emphasises the quality and employability of Australian training is necessary to deemphasise cost and migration considerations in choosing an Australian degree.

Footnotes

Declaration of conflicting interests

None declared.

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.