Abstract

Rule evasion by companies is a major driver of change in contemporary market societies. Recent research holds that periods of market instability offer opportunities to bring rule evasion under control because crises expose hidden market practices. Based on original archival evidence from the financial crisis of 1974, this article shows that rule evasion is disclosed not automatically, but strategically and selectively. To explain the ensuing dynamics, the article develops a Goffmanian framework in which regulators learn of a crisis of rule evasion backstage (in their interactions with companies) but use a conventional definition of the situation frontstage (in their presentations to the public). In an as yet unrecognized outcome, the regulators may find themselves caught between frontstage and backstage: their communications to the public limit their room for maneuver against the companies backstage, forcing them to repurpose their extant crisis-management tools. Because regulators publicly pretend to stay within their mandate, this form of crisis response renders re-regulation of rule evasion less likely. The finding contributes a new explanation for a central puzzle in the burgeoning sociology of crises: why periods of instability so rarely lead to change.

Companies increasingly seek new profit opportunities by evading rules (Carruthers 2013; Funk and Hirschman 2014; Thiemann and Lepoutre 2017). Billion-dollar markets trade in products that closely resemble regulated products but diverge from them sufficiently to escape government oversight (Duffie 2012; Pistor 2019). Recent research has identified periods of market instability as promising opportunities for regulators to bring rule evasion under control (Carruthers 2013:394–98; Funk and Hirschman 2014:682, 692; Thiemann 2018:205–7). Such periods are said to expose hidden market practices and to mobilize public support for re-regulation.

Drawing on the burgeoning sociology of crisis (Alexander 2018; Desan and Steinmetz 2015; Reed 2016, 2019; Roitman 2014; Steinmetz 2018; Zoeller and Bandelj 2019), this article argues that periods of instability do not render underlying problems transparent, but that crises of rule evasion are socially constructed. Only some actors will initially understand the situation as a crisis of rule evasion, and they strategically share this understanding with other actors or hide it from them. To analyze the ensuing dynamics, I modify the Goffmanian framework of regulatory drama (Edelstein 2011; Gibson 2014; Thiemann and Lepoutre 2017; Vollmer 2007). If a market built on rule evasion becomes unstable, companies may, on the backstage, disclose the rule evasion to regulators in the hope of receiving state support. Yet regulators have good reasons to hide that understanding from the frontstage: publicly playing down the crisis preserves confidence among so-far-uninformed market participants, minimizes interference in regulators’ backstage crisis management, and avoids blame for having failed to prevent the crisis.

In one possible and as yet unrecognized outcome, regulators find themselves caught between frontstage and backstage: hiding a crisis of rule evasion from the public limits their room for maneuver against the companies, leading regulators to stabilize the market by repurposing existing crisis-management tools. Because legislators and activists do not learn of the underlying problem, they are hard-pressed to call for bringing it under control. Regulators, in turn, possess the necessary knowledge but would risk exposing their backstage actions if they proposed re-regulation.

This article contributes to sociological research on regulation, crises, finance, and organizations. First, sociologists of regulation have noted a sustained pro-business stance of regulators that often cannot be explained by regulatory capture (Edelman, Fuller, and Mara-Drita 2001:1634; Novak 2013; Sawyer and Hovenkamp 2019). By showing that regulators can become caught between frontstage and backstage during crises, this article offers a novel mechanism to account for some of the unexplained pro-business stance. Second, sociologists who study why crises so rarely lead to significant change have focused on barriers to implementation (e.g., the fickleness of public attention), but not as much on the challenge of conceptual innovation (Alexander 2018; Balleisen et al. 2017; Hutter and Lloyd-Bostock 2017). This article shows that, during a crisis, legislators and activists may not learn of an underlying problem and may hence be limited in setting their goals. Third, sociologists of finance have tended to focus either on public statements made by financial regulators (Braun 2016; Holmes 2014) or regulators’ internal workings (Fligstein, Stuart Brundage, and Schultz 2017; Wansleben 2021). This article highlights the interplay between the two areas: not only is much internal work geared toward scripting public statements, but public statements, once made, can also shape what regulators can and cannot do behind the scenes. Fourth, organizational scholars have noted that regulatory agencies can decouple their practices from the policies prescribed by the governing statutes if the policies no longer fit with regulatory goals (Heese, Krishnan, and Moers 2016; Meyer and Rowan 1977). This article shows regulatory decoupling to be asymmetrical: regulators are relatively free to adopt practices that benefit firms during a period of market instability, but they are limited in their ability to diverge from statutes to firms’ detriment afterward.

Periods of instability in markets built on rule evasion are difficult to study empirically because data, although plentiful on presentations to the public, are usually scarce for interactions between regulators and companies. For the financial crisis of 1974, however, recently opened archives provide extensive data from the Federal Reserve and the association of the largest New York banks. The findings differ markedly from earlier scholarship on the case. A first generation of scholarship, which was based almost exclusively on public statements, cast the crisis as one that took place within existing rules. 1 Specifically, it highlighted foreign-exchange losses at Franklin National Bank, then the 20th largest bank in the United States (Grossman 2010:267–68; Helleiner 1994:171–73; Spero 1980). 2 A second generation of scholarship, inspired by disclosures that Fed governor Andrew Brimmer made after his retirement, paints the 1974 crisis as one involving rule evasion (Braun, Krampf, and Murau 2021:810–11; Özgöde 2021:16–18; Wansleben 2020:194). These scholars highlight that Franklin shifted its funding from taking in deposits (which were regulated) to attracting investments through the so-called money market (which financial companies had created to circumvent the rules governing deposits). The crisis of 1974, in this telling, was “the first major run on the U.S. interbank money market” (Braun et al. 2021:810), supercharging Franklin’s foreign-exchange losses into a threat to the stability of the financial system. According to this line of research, the Fed’s resolve to protect money-market investors from losses explains why regulators poured an unprecedented sum of money into stabilizing the situation (Özgöde 2021).

The money-market account explains important features of the 1974 crisis, but it leaves unanswered the crucial question of why the Fed, after stabilizing the situation, did not pursue regulatory changes aimed at thwarting future money-market runs. The money market could, for example, have been included within the ambit of deposit insurance (Ricks 2016). Yet to this day, money-market products “have no legal or regulatory status as such” (Ricks 2016:6). Runs through the money market similar to the one in 1974, but at an ever larger scale, occurred in the case of Continental Illinois Bank in 1984 (Mallaby 2016:297–302), in the financial crisis of 2008 (Gorton 2010; Mehrling 2011; Tooze 2018:143–55, 202–19), and in the 2020 “dash for cash” (Falato, Goldstein, and Hortaçsu 2021; Menand 2021; Vissing-Jorgensen 2021).

Drawing on the recently opened papers of Fed governor Brimmer and the archive of the association of the largest New York banks, I show that the Fed, on the backstage (in its dealings with the companies), understood the crisis as centered on the money market, that is, involving rule evasion, but on the frontstage (in its presentations to the public), cast the crisis as one limited to foreign-exchange trading, that is, within existing rules. Managing the public’s perception was a crucial task for the Fed. While today, the crisis of 1974 is overshadowed in public memory by those that came after it, at the time it “easily qualified as the most publicized” financial crisis since the Great Depression (Sinkey 1975:110). By casting the crisis as a conventional one on the frontstage, the Fed kept retail depositors from joining the run, legislators from interfering with regulators’ backstage crisis management, and journalists from asking why regulators had not prevented the crisis. Yet the Fed’s communication strategy constrained its room for maneuver against the companies backstage. Unable to bring public pressure on the banks, the Fed failed to induce them to take part in stabilizing the situation. Regulators ended up stretching the law to stabilize the money market with public funds.

The Fed’s frontstage/backstage strategy was instrumental in keeping the money market unregulated. The public could not demand re-regulation of the money market because it had been kept unaware of its role in the crisis. The Fed internally was convinced that re-regulation of the money market was desirable, but refrained from proposing legal change because such a proposal would have carried the risk of revealing the Fed’s crisis-period backstage actions.

Rule Evasion and Regulatory Drama

Rule evasion exploits incongruities between the substantive goal of regulation and its legal form. In that gray area between compliance and rule violation, companies find ways to create new products that “achieve similar results in economic substance but are sufficiently different in legal form” to avoid regulatory constraints (Thiemann 2018:10; see also Funk and Hirschman 2014:670).

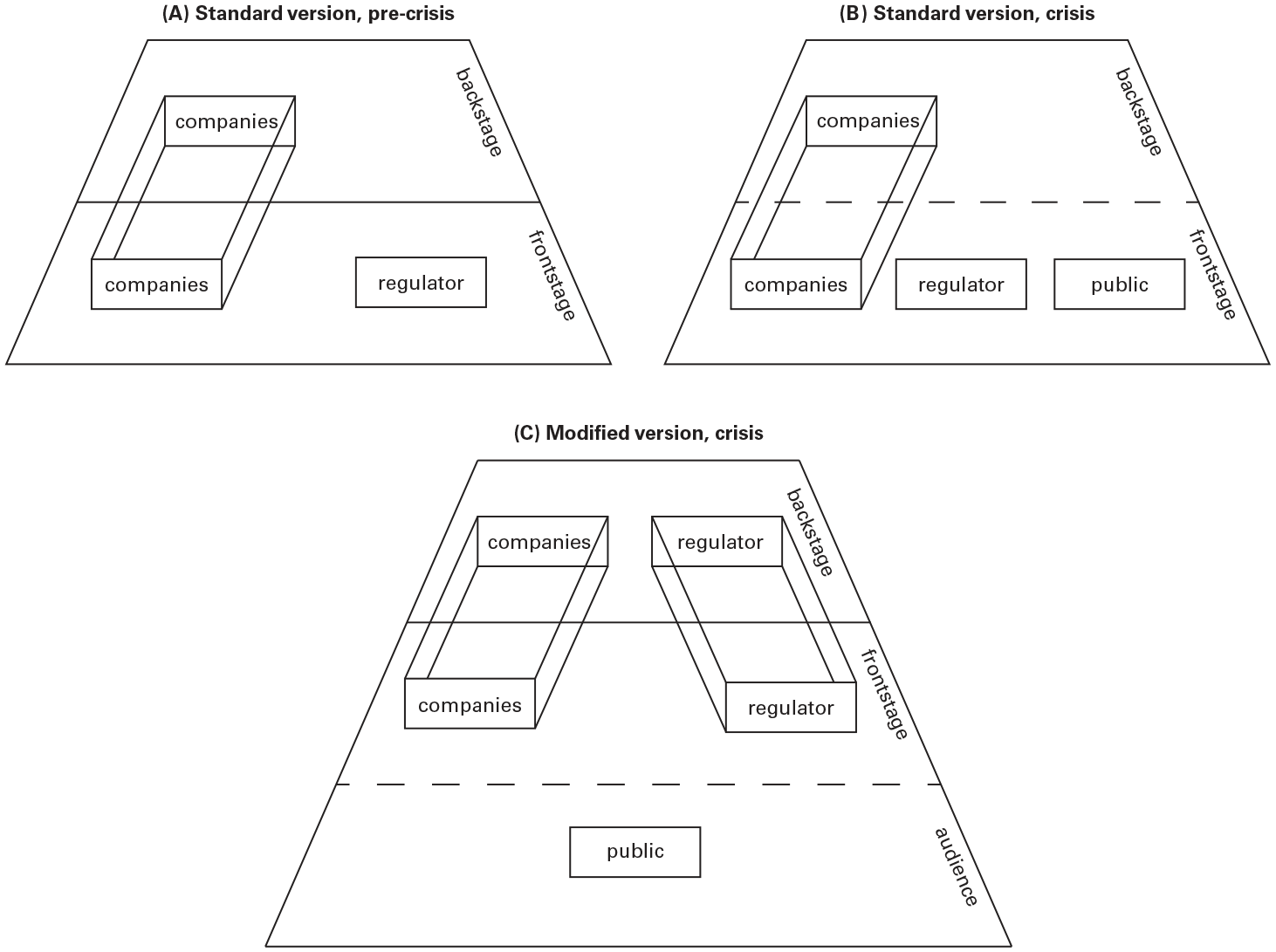

To study the interaction between regulators and companies, scholars have used the Goffmanian (1959) metaphor of frontstage and backstage (Edelstein 2011; Gibson 2014; Thiemann and Lepoutre 2017; Vollmer 2007). On the backstage, companies engage in rule evasion. On the frontstage, where companies interact with the regulator, they pretend that their business practices comply with the rules (see Figure 1A).

Goffmanian Frontstage/Backstage Framework

While the Goffmanian framework in its basic form focuses on face-to-face interactions between individuals, the regulatory drama involves organizations. Individuals switching between backstage and frontstage are often under strain, as residues of their backstage conduct may compromise the frontstage performance (Goffman 1959:121–23, 136–39). Organizations, by contrast, can strategically assign frontstage presentations to a separate division (Meyer and Rowan 1977:358).

To uncover rule evasion, it is necessary that “the regulator can move backstage” (Thiemann and Lepoutre 2017:1811). Regulators, however, are generally forced by resource constraints to rely for most of their work on documents that firms submit, for example, regulatory forms that companies fill out (Edelstein 2011:35; Thiemann and Lepoutre 2017:1795; Vollmer 2007:589–90). These forms tend to hard-wire the very categories that the new market practices circumvent, and even where they do not, companies can carefully prepare and edit documents to conceal rule evasion (Beamish 2002:92; Hilgartner 2000:15–19). More promising for regulators, although a greater burden on their resources and hence less frequent, are on-site inspections and visits to industry conferences (Thiemann 2018:98, 101; Thiemann and Lepoutre 2017:1803–4).

Moreover, regulators’ awareness that companies have created a new product does not yet constitute a sufficient basis for regulatory action. In a study of rule evasion in the emergence of swaps, Funk and Hirschman (2014:671) found that “[r]egulators understood how swaps functioned as market transactions, but they could not readily understand swaps as some kind of . . . regulated transaction.” To relate a new market to goals such as ensuring customer safety or market stability, regulators often need to collect additional data, for example, on the size of the market, the identities of participants, or patterns of market reactions to shocks.

Crises in the Frontstage/Backstage Framework

Instability is relatively frequent in markets built on rule evasion, because they lack the stabilizing hand of the state (Carruthers 2013:393; Fligstein 2001; Thiemann and Lepoutre 2017:1782–91). In line with a long intellectual tradition (see Koselleck 2006; Roitman 2014), the extant literature holds that periods of market instability render rule evasion transparent (Carruthers 2013:394, 397–98; Funk and Hirschman 2014:682, 692; Thiemann 2018:203–4; Thiemann and Lepoutre 2017:1782, 1799). For example, Thiemann (2018:1) states that “[w]hen the [2008] crisis hit, the world came to realize that, rather than spreading the risk, securitization [i.e., the packaging of mortgages for resale] had led to the concentration of risk in the banking system.” It is as if the curtain were lifted and the backstage activities exposed to the glaring light from the frontstage (see Figure 1B). Hence, no mechanisms are elucidated to explain how, in a crisis, those outside a market built on rule evasion come to understand what they did not understand before.

The burgeoning sociology of crisis has established that the link between instability and an understanding of a situation as a crisis can be loose (Beamish 2002; Clemens 2015; Desan and Steinmetz 2015; Reed 2016, 2019; Roitman 2014; Steinmetz 2018; Zoeller and Bandelj 2019). An oil spill in the Guadalupe Dunes was not defined as a crisis for four decades, even though it released more oil than the Exxon Valdez incident (Beamish 2002). Conversely, actors may suddenly label a situation a crisis when, in fact, the underlying problem is hardly new. In 1971, the Nixon administration invoked a crisis of the international monetary system “as a justification to push their . . . policy decisions,” even though the system had been under similar pressure for some time (Zoeller and Bandelj 2019:3). Finally, actors can disagree widely about whether a situation is a crisis. During the early years of what is today called the Great Depression, the Hoover administration sought to “minimize any sense of crisis,” arguing that unemployment and hunger “were to be expected in the normal course of things,” while Roosevelt’s campaign “shouted that the house was burning down and not enough people were paying attention” (Clemens 2015:10, 9, 17).

Instability in a market built on rule evasion hence does not necessarily imply a broadly shared understanding of the situation as a crisis of rule evasion. A widening circle of social actors—companies, regulators, and the public—may, at a certain moment in time, differ in whether they understand the situation as a crisis and, if so, as what kind of crisis. The onset of market instability, then, does not simplify the regulatory drama by erasing the distinction between frontstage and backstage, but complicates it by adding the public as an external audience (see Figure 1C). 3

Understandings (I): Regulator and Companies

The actors who first conceive of a situation as a crisis are, almost as a rule, market participants. Periods of instability create a reason for companies to invite regulators backstage (Figure 1C): they hope regulators will help stabilize the market. In an example from the Latin American debt crisis of the 1980s, Citibank’s leadership informed the heads of all banking regulatory agencies about a problem that, like rule evasion, fell through the cracks of regulatory categories (Seidman 1993:125–27; Zweig 1995:757).

To translate such information into a novel understanding, a regulatory agency must still achieve the organizational feat of recombining categories and data (Gibson 2012). To interact with the “buzzing, blooming confusion that constitutes the real world” (Simon 1957:xxv), organizations, even more so than individuals, tend “to restrict the categories used to a relatively small number” (March and Simon 1958:39). Market instability may provide the focus needed for a regulatory agency to adjust its understandings, as an increasing number of divisions branch out and coordinate with one another (Elyachar 2013:151–56; March and Simon 1958:153–54, 179–80). A new understanding is more likely to result if it can be arrived at by reactivating previous patterns of communication across divisions (Carpenter 2001:21–23; March and Simon 1958:159; Simon 1957:148–49), if the relevant divisions do not perceive the new understanding to be in conflict with their preexisting goals (March and Simon 1958:121–29), and if there is slack, that is, if “individuals or units hav[e] planning responsibilities without heavy operating responsibilities” (March and Simon 1958:199; see also Cyert and March 1963:278–79).

Yet market instability can also trigger organizational routines that work against the development of new understandings. Administrative scholarship has found that, in quiet times, regulators prepare for crises: they write contingency plans, run tabletop exercises, and set up early-warning systems (Boin et al. 2017:23–48; Braun 2015b:420). Such preparations allow regulatory agencies to quickly detect and act on the crises they anticipated—in Clemens’s (2015:12) felicitous phrase, these are “normal crises.” This planning, however, does little to help regulators deal with non-normal crises, such as crises of rule evasion: “In an organization that works hard to detect known risks before they manifest and cause trouble, early signals of impending novel crises may be simply put aside” (Boin et al. 2017:27, emphasis added). 4

Understandings (II): The Public

To explain how the public comes to understand a situation as a crisis, sociologists of the public sphere mostly focus on one mechanism: agents of the public (journalists and public prosecutors) expose what companies have hidden (Alexander 2018; Jacobs 2012). Translated into the Goffmanian framework, the agents of the public are said to reach into the backstage and expose the goings-on there on the frontstage.

Yet rule evasion is a kind of secret that confronts agents of the public with “potentially daunting obstacles” (Balleisen et al. 2017:8). When reporting on technical issues, journalists struggle to achieve the “code switching” (Alexander 2018:1066–68; Jacobs 2012:384) to moral language that would hold the attention of their audiences. Public prosecutors, for their part, find it hard to bring cases because rule evasion typically subverts the spirit of the law but does not violate its letter. The products at the root of market instability are in all likelihood “perfectly legal” (Thiemann 2018:64).

If the public learns of a crisis of rule evasion, it most likely does so because regulators disclose their understanding of the situation. But regulators have good reasons to hide that understanding from the frontstage. Publicly playing down the situation keeps retail customers from joining actions that would further destabilize the market, minimizes interference from legislators in the regulators’ handling of the situation, and suppresses blaming because the media cannot ask why regulators failed to prevent the market instability (Boin et al. 2017:102–25; Hutter and Lloyd-Bostock 2017:8).

Regulators, however, may find themselves forced to use public channels if they want to communicate with market participants. During a period of market instability, some communication from regulators to companies must happen fast, and the fastest modes of communication are often public (National Research Council 2013). Moreover, markets built on rule evasion often have a roster of participants that overlaps with but extends beyond the firms supervised by a regulator. Hence confidential forms of communication, such as circular letters to regulated firms, may fail to corral a sufficient number of market participants backstage.

The ensuing situation resembles the setting analyzed by Goffman (1971), in which one party needs to communicate with another party in the presence of a third party who is to be kept from learning a secret. The first two parties can communicate with one another only through “furtive signs” (Goffman 1971: 339). Regulators have been found to engage in communication that is “cryptic” to the public (Altamura and Zendejas 2020:768) but can be decoded by market participants. Yet there are limits to how differently one message can be understood. If regulators want to communicate to market participants that they understand the situation as a crisis of rule evasion, they may not be able to hide the existence of a crisis from the public; the best they may achieve is that the public thinks there is a crisis within existing rules.

Crisis Management: Regulatory Bargaining with Firms and Use of Crisis-Management Tools

If regulators hide their internal understanding of the situation as a crisis of rule evasion from the frontstage, they limit their room for maneuver against companies. Regulators and companies often struggle over their relative burden in stabilizing a market (Culpepper and Reinke 2014; Schneiberg and Bartley 2010:298–300; Woll 2014). A regulator downplaying the situation on the frontstage effectively gives up the ability to claim in its backstage interactions with the companies that it has the public on its side (Carpenter 2010:61). The longer the regulator downplays the situation on the frontstage, the more likely companies are to regard threats by the regulator to bring public scorn on them as a bluff, because the regulator can no longer do so without implicating itself in a cover-up.

If companies prove unwilling or unable to achieve a stabilization of the market, the state may be left alone to react. But the crisis-management tools granted regulators by statutory authority (Boin et al. 2017:23–48; Braun 2015b:420) almost by definition do not anticipate instability caused by rule evasion. A regulatory agency can ask legislators for new crisis-management tools, tailor-made for the task at hand, but this is unproblematic only if the agency discloses its internal understanding of the crisis.

By contrast, a regulatory agency that hides rule evasion from the public can only repurpose existing crisis-management tools, that is, decouple crisis-management practices from the policies, based in law, that are supposed to govern them. In the extreme case, regulators arguably break the law, as some legal scholars accuse the Fed of having done in 2008 (Posner 2018; Wallach 2015). Thus, regulators can find themselves caught between frontstage and backstage: as an unanticipated consequence of their communication strategy, they end up doing what they initially had no intention to do, that is, stabilize a market built on rule evasion by using public funds and bending the law.

Post-Crisis Reform

A key question in scholarship on crises concerns their ability to spark reform (Balleisen et al. 2017; Birkland 2006). For a regulatory agency, the most direct means to change a market is to tighten oversight and enforcement (Carpenter 2010; Zaring 2021). If regulators have developed an understanding of a market built on rule evasion during a crisis, they may attempt to creatively interpret their governing statutes to bring the market under control.

Yet the decoupling of regulatory practice from policy is asymmetric. If oversight and enforcement diverge from the law to the benefit of firms, companies have reason to go along (Heese et al. 2016). This often occurs during crises, when regulators stabilize a market. By contrast, one would expect corporate opposition after crises, when regulators seek to limit risk-taking. Companies may turn to the courts, which can block agencies from “pursu[ing] novel applications of old statutes” (Gershenson 2019:644).

In all likelihood, then, bringing rule evasion under control requires legal change. Extant scholarship has identified several institutional obstacles to legal reform, for example, veto points and the strength of lobbyists (see Part A of the online supplement). Yet this line of research builds on the assumption that a crisis renders the underlying problem transparent; it does not ask how rule evasion that remained hidden from the public during a crisis might become publicly known afterward.

For the public, developing an understanding of rule evasion is easier after a crisis but remains a challenge. An official crisis inquiry, which often employs staff researchers and solicits testimony from academics (Boin et al. 2017:102–25), may disclose rule evasion but still faces the problem of drawing public attention to a technical issue (Adut 2008:169–70; Hilgartner and Bosk 1988; Jacobs 2012:390). Reform-minded legislators must work out proposals that are not only technically competent but also align, or at least do not conflict, with cultural perceptions that have wide currency in society (Dobbin 1994; Steensland 2008).

For a regulatory agency that hid rule evasion from the public during a crisis, the situation afterward is ambiguous. On the one hand, disclosing rule evasion as part of a reform proposal no longer threatens to deepen a crisis by undermining market confidence, or to limit the regulator’s freedom in handling the crisis. On the other hand, there is still blame to go around. As Carpenter (2010:46–47, 68, 511–12, 626–33) points out, even a regulatory agency that managed to contain a crisis may face criticism if the public learns that the agency failed to be transparent. If such an agency proposes re-regulation, it runs the risk that “[w]hat [took] place in the background is foregrounded . . . with disastrous consequences” (Eyal 2022:121). Hence, regulators may remain caught between frontstage and backstage even after a crisis has ended.

Background: Bank Runs, Regulation, and Crisis-Management Tools

Broadly speaking, banks can fail if they are insolvent or illiquid. If insolvent, a bank’s liabilities exceed its assets. If illiquid, a bank does not have sufficient money on hand to make payments. While analytically distinct, these two forms of failure are often linked in practice. Most importantly, when depositors fear that a bank is insolvent, they may start a bank run—a classic self-fulfilling prophecy (Merton 1948)—that renders the bank illiquid.

Under the rules in place in 1974, regulators sought to prevent insolvency by ensuring that a bank could withstand losses on its assets, and sought to prevent illiquidity by making sure that the bank had a cash cushion (White 1992). There were also regulations in place to stabilize liquidity: banks could not compete for deposits outside their region, and the interest rates they could pay on time deposits were capped by regulation Q (Krippner 2011:58–63).

Regulators in 1974 had two major crisis-management tools at their disposal. First, the Federal Reserve could act as lender of last resort to banks that were solvent but illiquid (Meltzer 2003; Orian Peer 2019). Through the so-called discount window (in the early days, this was a physical teller window at the Fed), banks could, against high-quality collateral, borrow cash from the Fed. They could then use this cash to pay out depositors. Second, if a bank had become insolvent, the Federal Deposit Insurance Corporation (FDIC) paid out its insured deposits. To have the necessary funds, the FDIC collected insurance premiums from the banks and, should the resulting pool of money run out, it could tap the federal budget (FDIC 1984).

The four decades after the creation of the FDIC in 1933 were essentially free of runs. Even if depositors heard rumors about the health of their bank, they no longer had reason to run. In the few cases in which a bank’s assets had deteriorated beyond repair, the FDIC closed the bank and paid its depositors out. This happened, for example, in 1965 when the president of the San Francisco National Bank used money from the bank to gamble in Las Vegas and lost. 5

The stability of this regulatory regime, however, was undermined by rule evasion. Banks chafed under the new system of deposit regulation because they could not collect as much funding as they wanted to lend out. They were under particular pressure when interest rates rose above regulation Q ceilings. Then, in a process known as disintermediation, savers bypassed banks to lend directly to borrowers (e.g., the state and industrial firms) that were not subject to regulation Q (Cleveland and Huertas 1985:243–57).

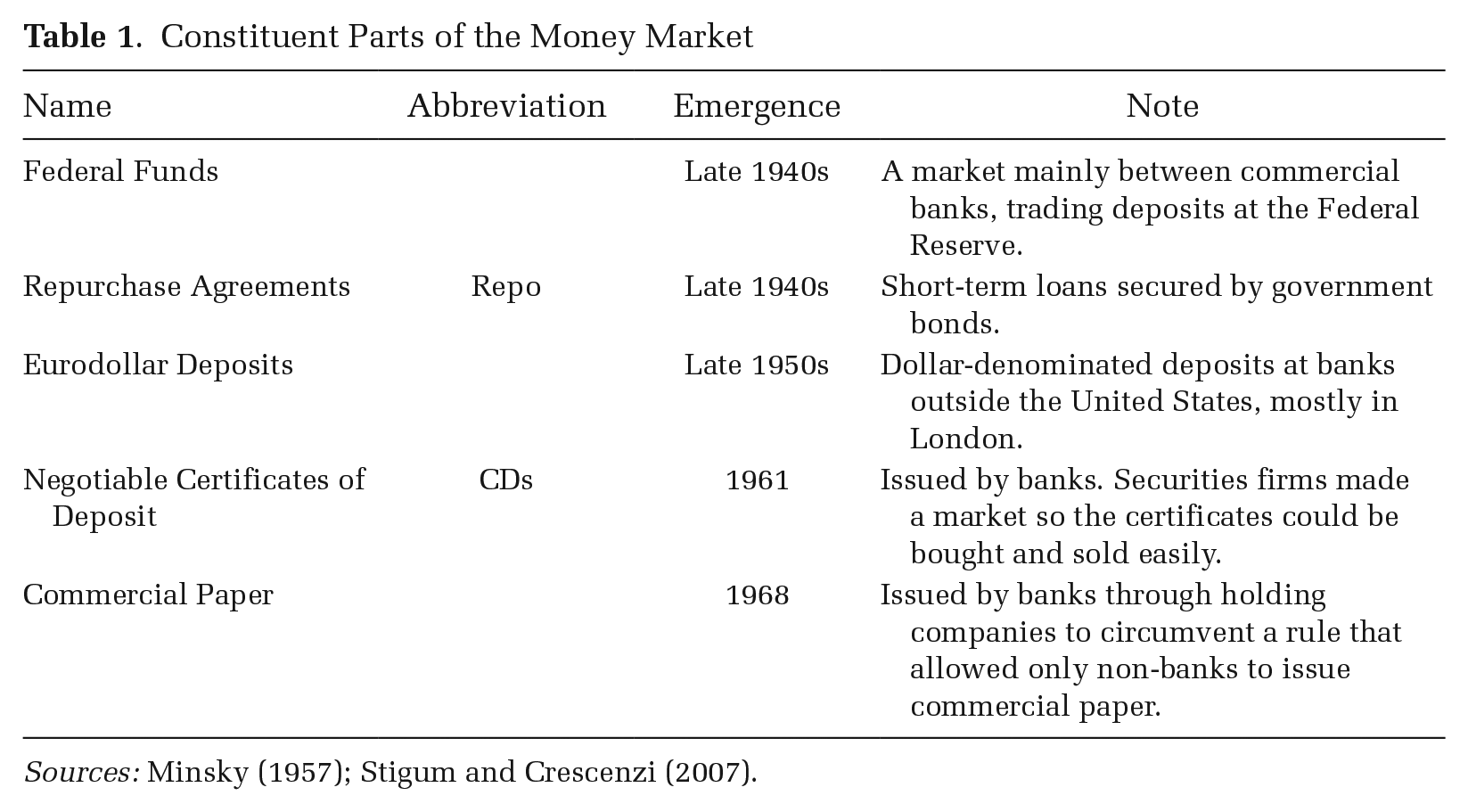

Banks responded by creating money-market products (see Table 1). These products were not de jure deposits, but banks de facto marketed them as such (Minsky 1957; Ricks 2016; Stigum and Crescenzi 2007). For example, banks in the late 1960s started to issue commercial paper. Instead of making a three-month time deposit at an interest rate limited by regulation, savers could now invest their money in a security, issued by a bank, that matured in three months and paid more interest. Because regulations expressly forbade them to do so, the banks issued the commercial paper through shell companies (i.e., bank-holding companies). Some of these new products were made available to retail customers (Krippner 2011:65–67), but the most significant customers were institutional investors: banks mainly sold their money-market products to other banks, insurance companies, and industrial firms (Stigum and Crescenzi 2007).

Constituent Parts of the Money Market

Sources: Minsky (1957); Stigum and Crescenzi (2007).

The money-market products, precisely because they had been engineered to fall outside the regulatory category of the deposit, were not covered by deposit insurance. They were protected only by the lender of last resort and, indirectly, by bank examination. Thus, the postwar emergence of the money market resurrected the threat of a bank run. 6

Data

Scholars of crises are typically faced with a dearth of data from the regulatory backstage. Even if ethnographers find themselves with access to a regulator when a crisis begins (something that cannot be planned), the limits of that access may be felt more acutely as a result of the crisis, as Riles (2013) experienced at the Bank of Japan during its response to the 2011 tsunami. 7 Documents can be similarly difficult to obtain. In 2008, the Federal Reserve shrouded important parts of its bailout program in secrecy. When challenged by a media organization, the Fed fought the case all the way to the Supreme Court, receiving support from the New York Clearing House (NYCH), an association of major banks (Tooze 2018:217).

For the financial crisis of 1974, recently opened archives provide an unusual window onto the regulatory backstage. The papers of Andrew Brimmer, a member of the Federal Reserve Board, became available at Harvard’s Baker Library in 2018. They contain a wealth of fine-grained data, including daily memos from the mid-level Fed official who coordinated the logistics of crisis management. The unusual organization of the Federal Reserve, with staff reporting to all members of the Board, meant that much of the day-to-day management of the crisis was conducted in writing and is amenable to archival research. Additional data come from the papers of Federal Reserve chairman Arthur Burns (at the Gerald Ford Presidential Library) and Secretary of the Treasury William Simon (at Lafayette College’s Stillman Library).

Data from inside the financial industry became available when the archive of the NYCH was opened at Columbia’s Rare Books and Manuscript Library in 2016. Most importantly, the archive contains minutes of secret meetings of bank executives during the crisis of 1974, some of which were also attended by Fed officials. To reconstruct the sentiment in the money market, I draw on its premier trade journal, Euromoney. Because Euromoney was published no more frequently than every month, I also use the less detailed but more frequent coverage of the money market in the Financial Times.

To reconstruct the perspective of the public, I draw on coverage of the 1974 financial crisis in the New York Times (accessed through TimesMachine) and TV evening news (accessed through the Vanderbilt Television News Archive). Congressional proceedings related to the crisis were identified through the ProQuest Congressional database. I also used the papers of Wright Patman, the chairman of the House Banking Committee, which are held at the Lyndon B. Johnson Presidential Library.

Frontstage and Backstage at the Financial Crisis of 1974

Understandings (I): The Federal Reserve and Financial Institutions

On May 7, 1974, the top executive of Franklin National Bank (FNB), Harold Gleason, and two of his deputies arrived at the Federal Reserve Bank of New York for an urgent meeting.

8

They disclosed that, sparked by rumors about foreign-exchange losses, FNB was the target of a run through the money market. The minutes taken by a Fed official put it drily: “The purpose of their visit was to express . . . fear that Federal Funds sources [Table 1], already somewhat reluctant, may dry up.”

9

A more vivid description of the view from inside FNB comes from Joseph Barr, who took over from Gleason six weeks later. Barr’s (1975:304, 302) expectation of a bank run by retail depositors was confounded:

I kept glued to the communication net we had established with the branches waiting for the news that mobs were breaking down the doors to get their money. . . . But nothing happened. . . . [T]he run on Franklin was a “financial run,” not the classic run in which people . . . rush to the bank to get their money out before it fails. By a “financial run” I am referring to a run by U.S. banks, by large corporations, and by companies or banks holding dollars outside the U.S.

Why did Gleason and his deputies alert the Fed to the run through the money market on May 7? Only weeks before, they had been adamant in making the case with the Fed that their bank was sound. 10 On May 7, however, the FNB managers faced the prospect of immediate failure. Money-market products were coming due and the bank could not pay them out. The only avenue still open to Gleason and his colleagues was to ask the lender of last resort. The Fed’s minutes recorded: “There was a discussion about borrowing and it is likely Franklin will borrow $150 million for three or four weeks.” 11

Over the next few days, financial-market participants approached the Fed with reports that the run through the money market was engulfing other banks as well. The major New York investor Morris Schapiro “expressed great concern about FNB and the general financial picture.” 12 A Wall Street analyst reported that stress was spreading from FNB to “almost any” bank. 13

To make sense of such information, the Fed had to overcome an organizational challenge. Although the Fed was not unaware of the money market, understandings of different aspects of that market were spread across three organizational domains. First, the Fed implemented its monetary policy by trading in the money market (Krippner 2011:109–14; Meulendyke 1998). But the information gleaned in this way was partial because the Fed traded only in the safest parts of the money market. Second, the Fed’s bank examiners had insight into banks’ balance sheets, including their money-market funding (Omarova and Tahyar 2011). This view, however, was limited to one bank at a time and offered no insight into the positions of non-bank participants in the money market. Third, in the late 1960s and early 1970s, the Fed undertook research on systemic risk in financial markets (Özgöde 2021). Yet this research project was not transformed into a routine tool of monitoring the money market.

Beginning in May 1974, the Fed developed a regulatory understanding of the money-market run by recombining the three previously unconnected understandings. For example, a Fed staffer observed in August 1974: “reports [from] commercial banks that were initially employed for monetary purposes, now have found regulatory uses.” 14 This coordination inside the Fed drew on previous communication patterns across divisions, for example, a 1960s project on changes in bank structure (Holland 1989:25–26). Conflict between the divisions inside the Fed (Axilrod 2011:59; Conti-Brown 2016:85, 93) was avoided because the new understanding tied into the divisions’ goals. Recognizing a run through the money market was important for the market desk if it wanted to implement monetary policy effectively; for the bank examiners if they wanted to avoid bank failures; and it provided an intellectually interesting problem for the research division. Finally, the Fed was independent of congressional appropriations and hence had ample slack that it could direct at a new problem perceived to be urgent (Axilrod 2011:91, 180–85).

Less than a week after the visit from Franklin’s top executives, the Fed had developed a deep enough understanding of the money-market run to produce a forecast that would, in its outline, prove accurate. 15 By May 20, Fed staff created statistics detailing how strongly the 50 largest U.S. banks relied for their funding on the money market. The new statistics showed that FNB had relied on the money market for about 30 percent of its funding—higher than the average across the banks, which was about 20 percent, but lower than some banks, where the number was close to 40 percent. 16 These data were so different from existing measures that they did not fit into any of the numerous existing statistical forms at the Federal Reserve, and they were seen as so urgent that Fed staffers did not even take the time to type them up but provided them in handwriting to top officials. 17 In June, a Fed staff member compiled a “Special Financial Markets Briefing” based on information obtained from money-market dealers. 18 In July, Fed officials tasked with investigating the money market conducted a survey of banks across the United States and, in greater detail, interviewed senior New York City bankers. 19

Understandings (II): The Federal Reserve and the Public

To analyze the social construction of a crisis, it is useful to consider differences in timing (Zoeller and Bandelj 2019). While for insiders, the financial crisis of 1974 began on May 7, it did not begin until May 13 for the public. It was only then that the TV evening news started covering problems at FNB, and that the New York Times reported about FNB on its front page. 20 The timing is peculiar because most of the economic facts reported on May 13 had been disclosed by FNB already on May 10. Yet the TV evening news had not picked up the story and the New York Times had relegated it to its business section.

What explains the jump in salience on May 13? The evidence clearly points to a press release that the Fed issued on May 12. Walter Cronkite mentioned the Fed’s statement when he broke the news to his viewers, and the New York Times not only led its front-page story with a mention of the Fed’s statement but also printed it verbatim on an inside page. It is thus worth looking at the Fed’s statement in full:

Inquiries have been raised in recent days about the position of Franklin National Bank. The bank has reported a poor earnings record recently, and the management of the controlling holding company announced Friday that it would recommend that the regular dividend payment on both common and preferred stock be passed. The board is familiar with this situation and looked carefully at the bank’s condition in connection with the proposed acquisition of Talcott National Corporation by the bank’s holding company. Its decision earlier this month was to turn down this proposal in part because it felt that management’s energy should be devoted to the remedial program for the bank, which is now under way. There is, of course, the possibility that—with many rumors about the bank—Franklin National may experience some unusual liquidity pressures in the period ahead. As with all member banks, the Federal Reserve System stands prepared to advance funds to this bank as needed, within the limits of the collateral that can be supplied. Working with Franklin National, the Federal Reserve Bank of New York has determined that there is a large amount of acceptable collateral available to support advances [to] the bank from the Federal Reserve Discount window if they are needed. As a matter of general policy, the Federal Reserve makes credit extensions to member banks, upon acceptable collateral, so long as the borrowing member bank is solvent. We are assured by the Comptroller of the Currency that Franklin National Bank is a solvent institution. Chairman Burns, who is in Europe, has been kept informed of developments. Since this matter does not require his personal attention, he has no intention of changing his travel plans which call for his return to Washington later this week.

21

The Fed’s statement was pivotal in creating the public understanding that there was a crisis. But what kind of crisis? Here, the statement was vague. The public did not understand the crisis to be a bank run through the money market. Indeed, when the New York Times, on May 13, sent out a reporter to determine whether a bank run was under way, he looked only for retail customers withdrawing their deposits, and reported that everything was calm. 22 What the reporter failed to see was that in the back office, where FNB’s money-market operations took place, a run by institutional investors was unfolding through telex messages and phone calls.

The few voices in the public sphere who had a hunch that the crisis was rooted in the money market were not heard. The most prominent such voice was that of Wright Patman, Democratic chairman of the House Banking Committee. In a press release issued on May 13, Patman sought to tie the crisis to the money market, specifically the market in CDs (see Table 1): “Franklin National is one of the big banks which [issued] CDs in heavy amounts and I am sure this is one of the problems which the Federal Reserve is attempting to bail out at Franklin National now.” 23 Many newspapers reported on Patman’s press release but left out his argument about the money market. 24

Public discussion was dominated instead by an understanding of the crisis based on the Fed’s reference to FNB’s “poor earnings record,” which most journalists connected to their already existing interest in foreign-exchange markets after the end of Bretton Woods. Indeed, the only explanation for the crisis that Cronkite provided to his viewers was that FNB “had lost more than 14 million dollars in unauthorized foreign currency . . . transactions in the last 6 weeks.” 25 The shorthand explanation used in a typical New York Times article traced the crisis to Franklin’s “substantial losses in its foreign exchange operations.” 26

The Fed’s Frontstage/Backstage Strategy

Why did the Fed not inform the public about the run in the money market? To begin with, it is helpful to note that between May 7 (when the Fed learned about instability in the money market) and May 12 (when it issued the press release), it remained silent on the frontstage. On May 9, senior officials “agreed that issuance of a press release was probably not advisable.” 27 The Fed’s silence was a forceful public statement to the effect that there was no crisis.

The Fed made its first public statement, on May 12, only when it perceived the problem in the money market to have worsened so much that a financial catastrophe was imminent unless the Fed reassured market participants. Over the weekend of May 11 and 12, the Fed came to fear that large parts of the money market might cease to function on Monday. 28 But because the money market was unregulated, the Fed did not possess a list of participants, and because market participants had not established an organization, there was no representative with which the Fed could communicate. Unable to corral a sufficient number of money-market participants backstage, the Fed had to speak publicly.

The May 12 press release was written so that money-market participants and the public took away different understandings of what kind of crisis was afoot. The Fed embedded a veiled reference in its statement: in the second paragraph, it announced matter-of-factly that it would help a bank experiencing “unusual liquidity pressures.” Insiders knew that under the regulatory system in place, unusual liquidity pressures were a logical impossibility as long as banks funded themselves through deposits: deposit insurance would prevent any such pressures from arising. If the Fed was aware of “unusual liquidity pressures,” so insiders read between the lines, it knew about the stress in the money market. To outsiders, the Fed offered a different understanding to latch on to, by also referencing FNB’s “poor earnings record” linked to foreign-exchange losses.

As the crisis progressed, the Fed could segment audiences. Behind closed doors, Burns stated that FNB, like other banks, had been “living off purchased money,” that is, had funded itself on the money market. 29 He shared with a confidant his fear that the run might escalate: “I . . . think I am sitting on a volcano that could blow up at any time and blow this economy apart in the process!” 30 In his public statements, however, Burns used a conventional understanding, telling Congress that “in some instances unhealthy practices have turned up—such as speculating in foreign exchange.” 31 This definition of the crisis allowed Burns to calm the nerves of retail depositors, who might otherwise have joined in the run: “the commercial banking system in the United States is entirely sound, and it can be counted on to continue to function efficiently.” 32

The regulators’ frontstage/backstage strategy was also motivated by a desire to avoid interference in their backstage crisis management. The Fed’s “strictly confidential” contingency plan for a financial crisis, drawn up in 1970, noted that “[t]he mood of Congress in this situation, it seems safe to surmise, would . . . not be dissimilar from the reactions of a beehive split open with the sudden blow of a heavy stick: violently roused from familiar behavior patterns [and] uncertain where to turn.” 33 As for journalists: “Apart from a handful of the more sophisticated papers with able financial staffs, the press in this country will have still less of a grip than Congress on why the crisis has arisen and what should be done about it.” 34

Finally, the frontstage/backstage strategy helped the Fed avoid blame. The Fed’s contingency plan predicted that during a financial crisis, policymakers would find themselves “in an extremely hot situation.” 35 In 1974, Burns wrote in a letter to the head of the German central bank that, if details of the crisis management were to “be drawn into the political arena at a high level,” this would be “a development . . . of . . . deep concern.” 36 As Barr (1975:313), who had served as a senior regulator in the 1960s, would put it shortly after the 1974 crisis: “I really do not blame Arthur Burns for getting excited. As an old government hand I can imagine the difficulty of explaining to a series of Congressional Committees just how they got themselves into such a mess.”

The Fed’s frontstage strategy succeeded in making the public believe that the crisis was one within existing rules. As weeks and then months passed, the crisis faded from public attention. The number of stories on the first page of the New York Times dropped from four in May to one each in June and July, and to zero in August. 37

Crisis Management (I): The Failure of the Fed’s Attempt to Sway Banks to Stabilize the Money Market

Among market participants, the sense of crisis grew through the summer of 1974. The leading trade magazine of the money market, which had described May as a “difficult month,” 38 wrote: “June proved that what is bad can still become worse. . . . Bankers . . . wake up in the night with nightmares.” 39 A market report for July noted that money-market investors were becoming increasingly wary of borrowers considered risky. 40 In August, some regional banks experienced “difficulties selling large CDs [Table 1], particularly in national markets.” 41 If these banks could no longer fund themselves on the money market, a full-scale financial and economic crisis was on the horizon.

Money-market investors nervously eyed the Fed. An internal Fed memo stated that its “approach to Franklin New York Corporation’s difficulties . . . will be regarded [by market participants] as a tipping of the Federal Reserve’s hand.” 42 It seemed clear that the Fed had to become involved if the money market was to be stabilized. Initially, the Fed tried to limit its role to coordinating a backstop of the money market with private funds. 43 But the Fed soon faced the same problem that had forced it to issue the May 12 press release: there was no representative of the money market with which it could engage confidentially. In lieu of that, the Fed reached out to the New York Clearing House (NYCH), which represented some of the major players in the money market. Founded in 1853, the NYCH had a history of putting member banks’ funds at risk to stop crises (Yue 2016). If regulators wanted to spur money-market participants into collective action, the NYCH, although far from an ideal vehicle, seemed the best bet.

The Fed made its most important appeal to the NYCH in a secret meeting on June 5, 1974, for which two governors of the Fed traveled from Washington, DC, to New York. The NYCH should, according to the Fed’s demand, buy money-market products issued by FNB. As Fed Governor Jeffrey Bucher put it: “the resumption of federal funds trading [between the NYCH and FNB] would have a very positive psychological effect upon the financial community.” 44 Such a private backstop of the money market, Governor Robert Holland said, was “an urgent need.” 45

But the NYCH would take almost no burden on its shoulders. Despite the Fed’s protestations of urgency, the NYCH played for time in this game of chicken. 46 When the NYCH finally agreed to resume money-market trading with FNB, it did not provide the 500 million dollars the Fed had asked for, but just 250 million dollars. 47 Even at that lower amount, the NYCH banks agreed only on the condition that the Fed provide a guarantee: if FNB failed, the Fed would reimburse them. The NYCH, then, did not actually put private funds at risk.

Why could the NYCH resist the Fed? Part of the reason was economic. Most NYCH banks were not directly exposed to a potential default by FNB because they had long since stopped lending to FNB, both on the money market and through longer-term contracts. 48 The only NYCH bank to seriously consider helping FNB was Manufacturers Hanover, which had extended a 30 million dollars medium-term loan to FNB and thus had a direct stake in its future. 49 As for their own funding, the NYCH banks actually benefited from the crisis. One financial journalist remarked: “Paradoxically, the Franklin situation has helped the Chase as well as other large banks.” 50 As money-market investors moved their funds out of Franklin and other medium-sized and small banks, they often moved the funds into the largest banks.

The Fed might have overcome the NYCH’s resistance with political pressure. But as long as it kept the public in the dark about the money-market run, the Fed could not enroll Congress and the media as allies. When Bucher spoke at the secret meeting on June 5, 1974, he could not threaten to name and shame the banks; all he could do was give “a discourse on the need for public spirited action by the large New York City banks.” 51 When such talk failed to move the financial executives, the Fed could think of only one remaining option: stabilize the money market with public funds.

Crisis Management (II): The Fed’s Stabilization of the Money Market with Public Funds

Even once the Fed had grudgingly accepted that the stabilization of the money market would be carried out using public funds, it faced challenges in implementing such a backstop. For all its independence and its ability to create money, the Fed was a creature of Congress with respect to its crisis-management tools. Because the money market had arisen in circumvention of the rules, no tool in the Federal Reserve Act fit.

In theory, the Fed could have asked Congress for legislation to provide it with new crisis-management tools. But the archival record contains no indication that the Fed ever entertained that possibility. By making the crisis look like a normal crisis frontstage, the Fed had tied its hands: if it did not want to expose the money-market run (and, as time went on, its obfuscation of that run) to Congress, it had to make do with the old tools.

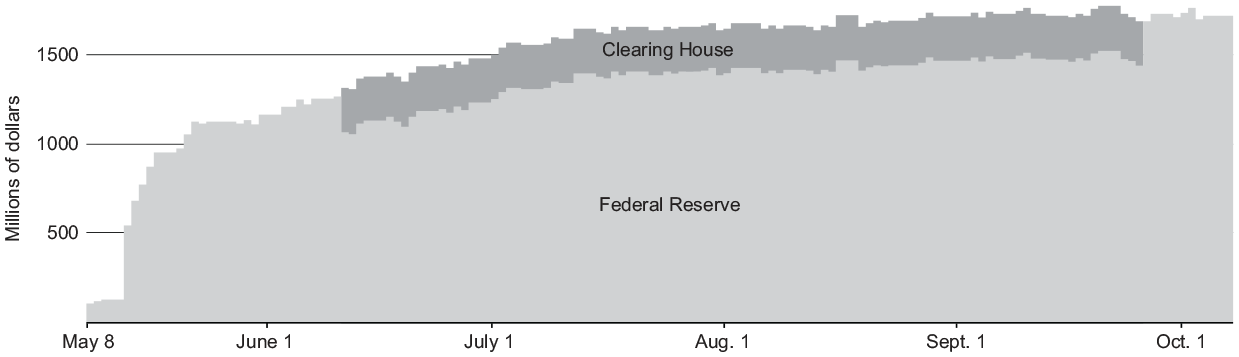

The principal tool repurposed by the Fed was the discount window. Lending through it to FNB allowed FNB to pay out its money-market commitments as they came due (see Figure 2). The law allowed the Fed to open the discount window only to a bank that was solvent and could provide high-quality collateral. Yet as early as May 14, a senior Fed bank examiner entertained the possibility that FNB was insolvent. 52 From July on, Franklin could provide only low-quality collateral. 53 To repurpose the old tool, then, the Fed was willing to stretch or break the law. Moreover, the discount window was designed to be a short-term tool, providing a bank with just enough time to convince its lenders that it was solvent. It strained credulity that the Fed kept the discount window open for five months.

Discount-Window Loan from the Federal Reserve and Federal-Funds Loan from the New York Clearing House to Franklin National Bank, from May 8, 1974, until October 7, 1974, in Millions of Dollars

The Fed cast about for crisis-management tools available to other regulatory authorities that would stabilize the money market. It hit upon a provision in the law governing the FDIC. 54 Under a so-called assisted merger, the FDIC could pay a bonus to a healthy bank that would take over FNB, and the healthy bank would then pay out all of FNB’s liabilities, including its money-market commitments. But the law governing the FDIC allowed an assisted merger only as an exception. The default option was liquidation: the FDIC would close FNB and use the FDIC insurance fund to pay out insured deposits. All uninsured lenders—including, most importantly, FNB’s money-market investors—would lose their funds, potentially sparking the very collapse of the money market that the Fed was trying to avert.

The FDIC did not interpret the crisis as one of the money market. In contrast to the Fed, its understanding of the situation flowed almost exclusively from bank examination. Looking at the situation through this conventional lens, the FDIC leaned toward the default form of action. In a conversation with the CEO of a major bank, FDIC chairman Frank Wille mentioned a possible “liquidation of FNB.” 55 By early June, the FDIC worked on a contingency plan to liquidate FNB and collected “information about insured and noninsured deposits.” 56

For months, the Fed and its allies within the U.S. government tried to convince the FDIC to forgo a liquidation of FNB in favor of an assisted merger. The Fed’s legal department suggested ways in which the FDIC could bend the deposit-insurance law to this effect. 57 On June 21, Wille and two of his deputies were summoned by the heads of the Federal Reserve and the Treasury Department: “Chairman Burns and Secretary Simon expressed their very grave concern about the impact on financial markets were FNB to be liquidated. . . . Secretary Simon said that in his view it was unthinkable that we would permit the bank to be liquidated.” 58

In the fall of 1974, after months of backstage negotiations, the FDIC agreed to an assisted merger. The Fed got what it wanted, but not because FDIC officials had come around to a money-market understanding of the crisis. The FDIC went along because the size of FNB would have overburdened its insurance fund in case of a liquidation. According to Wille, if the FDIC had paid out FNB’s insured creditors, it would have been doubtful whether the remaining insurance fund would still have created confidence should another bank get into trouble. 59 A much smaller outlay by the FDIC sufficed to make a merger with Franklin attractive for a healthy bank.

Executing the assisted merger of FNB required a tightly choreographed administrative dance, prepared in secret and carried out at speed. If FNB shareholders learned of the plan and sought an injunction, the process could easily have failed. 60 In the words of the Deputy Secretary of the Treasury, Stephen Gardner, “a premature disclosure and an aborted plan could have enormously disruptive effects on the financial markets.” 61 On the afternoon of Tuesday, October 8, 1974, the FDIC Board of Directors convened and accepted a bid submitted earlier that day by the European-American Bank to acquire FNB with assistance from the FDIC. Over the following hours, more than 200 regulators tabulated FNB’s assets and liabilities. They completed their calculations by 5 a.m. on Wednesday, October 9. That morning, FNB re-opened under the name European-American Bank. 62

As a consequence of the assisted merger, none of Franklin’s money-market lenders incurred a loss. For the Fed, it was a bitter-sweet victory. The money market was stabilized, but only thanks to public funds and the bending of rules. Going forward, the way stabilization had been arrived at would make re-regulation of the money market difficult to achieve.

Post-Crisis Failure to Regulate the Money Market

In the wake of the 1974 crisis, legislators around Henry Reuss, who became chairman of the House Banking Committee in January 1975, argued that “the largest bank failure in American history, the Franklin National,” should lead to “monumental reforms.” 63 Reuss promised “legislative action . . . for completion in the 94th Congress.” 64 Yet when that Congress adjourned in October 1976, not a single draft bill had been passed by both chambers of Congress. Much of that failure is well explained by political-institutional accounts (Balleisen et al. 2017; Birkland 2006) that focus on lobbying and veto points (see Part B of the online supplement). But these accounts cannot explain why the draft bills did not even propose to re-regulate the money market. In other words, even if all the obstacles that political-institutional accounts identify had been overcome, the money market would still have remained unregulated.

Reuss and his allies in Congress produced some information suggesting that a money-market run had taken place in 1974. The House Banking Committee, which was fast becoming the center of reform efforts, launched a study of “Financial Institutions and the Nation’s Economy” (FINE). Of FINE’s 12 report authors and 96 witnesses, two came close to describing the 1974 crisis as a money-market run: Jane D’Arista, a staff researcher for the House Banking Committee, and Donald Hester, professor of economics at the University of Wisconsin–Madison. D’Arista had been asked to study international banking; Hester, the incentives for bank managers. It was thus only as a subtext that each could make a point regarding the money market. D’Arista noted that “a high proportion of [banks’] liabilities are uninsured. . . . The hasty decision of the Federal Reserve to intervene in the Franklin case as lender of last resort on such a massive scale raises questions as to whether or not the Fed’s action actually did avert something like a modern-day panic in the banking industry.” 65 Hester similarly stated that what “seems to have been the policy [toward] Franklin National Bank” was “protecting all creditors from loss” even if their investments fell outside “deposit insurance limits.” 66 Both experts had to choose their words carefully because they were not privy to most of the relevant data, with Hester limited to the statistics the Fed routinely published, and D’Arista, as a congressional staffer, provided with only marginally better data by regulators. D’Arista suggested, intriguingly but without providing further details, “regulation and control of the interbank markets.” 67 The FINE study thus half-opened the door to putting the money market on the agenda.

Reform-minded legislators, however, did not take the next step of proposing money-market reform. What held them back was the ideational incongruence (Dobbin 1994; Steensland 2008) between such reform and the schema of the consumer activists whom the legislators sought to enroll as their most important allies. In the 1960s and 1970s, the consumer movement tended to focus on the direct point of contact between retail customer and company, an emphasis that could “obscure . . . the structural causes” of regulatory problems (Krippner 2017:13; see also Cohen 2003:345–97). Indeed, during the financial-reform debate of 1975/6, some activists called for regulatory agencies to set up new departments for “consumer protection,” but they had virtually nothing to say on what they called “traditional supervisory functions.” 68 This narrow understanding of consumer activism was adopted by the reform-minded legislators, who aimed to make laws for “the man [sic] in the street” or “the little people.” 69 As Reuss’s closest ally, subcommittee chairman Fernand St. Germain, put it: “we intend to come up with some changes and reforms that are consumer oriented . . . not for the people who can afford to put in $100,000 or $50,000, but to the people who are putting in $2,000, $5,000, $10,000.” 70 There was, in this vision, little room for the link that tied retail depositors indirectly but powerfully to the wholesale money market, where the transaction minimum was $500,000.

This left the Fed as the only plausible advocate for money-market legislation. Internally, the Fed was convinced that the money market should be re-regulated. Burns had proposed as much already in an Oval Office meeting with Nixon in June 1974. As Burns recorded in his diary:

I then [after discussing monetary policy] turned to Franklin National case, noted its peculiarities, but also remarked that what happened in that bank was largely typical of what the larger banks have been doing—living off purchased money [i.e., funding themselves on the money market], letting capital position deteriorate, leveraging common stock, etc. I concluded by saying that basic reforms in banking are needed.

71

In late May 1974, at a meeting of the Fed’s top officials in the Board Room, Alan Holmes, the head of the Fed’s market desk, also called for bringing the money market under control. To achieve “a sounder banking system,” he said, banks “certainly should be encouraged to rethink their over-reliance on liability management [i.e., their money-market activities], their aggressive approach in seeking out loans, their overcommitment position, and their investment policies.” 72 Frederic Solomon, director of the Fed’s Division of Supervision and Regulation, made a similar proposal. At a “strictly confidential” meeting of senior Fed officials in July 1974 about “possible improvements in the structure of the nation’s banking regulatory system,” Solomon said, according to the minutes: “short-term, volatile liabilities were of much greater significance than longer-term liabilities. Therefore, it might be well to create a regulatory structure in which coordinated supervisory attention would be focused on those institutions that were involved in the movement of liabilities of a more volatile nature.” The meeting participants had earlier agreed on “the vital role now played by Federal deposit insurance,” so it is safe to assume that they did not see insured deposits as a problem. The “short-term, volatile liabilities” hence referred to money-market products, and the envisaged new “regulatory structure” was intended to center on the money market. 73

As long as the money market was in turmoil, the Fed considered proposals to re-regulate it inopportune. As Burns put it to Nixon in June: “Markets are too nervous to absorb the necessary reforms.” 74 After FNB’s assisted merger in October 1974, however, the money market stabilized. 75 Two of the three reasons that had kept the Fed from disclosing its money-market understanding during the crisis hence no longer applied: neither did the Fed have to fear that disclosure would undermine market confidence, nor was there any crisis management in which Congress might meddle.

Yet the Fed’s concern with blame avoidance—the third reason why the agency had hidden the money-market run backstage during the crisis—grew more salient in the wake of the crisis. Franklin’s assisted merger, far from putting the issue to rest, made the front pages and led journalists to re-assess regulators’ crisis management. 76 According to Fortune, the regulators should have “promptly” merged Franklin in May instead of giving it a “precarious hold on life during the subsequent months . . . aided by a massive loan from the Federal Reserve.” 77 In January 1976, major newspapers reported on their front pages that regulators had kept long lists of so-called problem banks in 1974, even as they had assured the public that the financial system was sound. 78 In response, the House Committee on Government Operations held hearings into the “adequacy of the Federal bank regulatory agencies,” seeking to pierce “an unwarranted cloak of secrecy.” 79 In the House Banking Committee, Reuss and his allies pushed for legislation that would have relieved the Fed of its role in banking regulation and weakened its independence. 80 The Fed mounted a vigorous defense, with Burns giving a half-hour interview to ABC and appearing before Congress. To reject the accusations that the Fed had botched its crisis management and misled the public, Burns reiterated the understanding of the 1974 crisis as a conventional one: “Under the present regulatory structure, our banks have met satisfactorily the critical test of adversity. . . . The fact that only a handful of banks failed during the recent recession is a triumph for bank regulation in this country.” 81

The Fed, in short, found itself still caught between frontstage and backstage, hamstrung by its crisis-period actions in its ability to propose legislative reform of the money market. Without involving Congress, the Fed could regulate the money market only by tweaking its supervision and enforcement, that is, by interpreting its extant governing statutes creatively. 82 Those statutes, though, did not recognize the money market as an object of regulation, so banks could complain to the courts that the Fed was overstepping its mandate. This did not appear as an urgent problem in the immediate aftermath of the 1974 crisis, as the fate of Franklin scared many banks into a more cautious use of money-market funding. 83 But as time went on and memories faded, there was little to keep the money market from becoming as big and risky as it had been in 1974, and soon even bigger and riskier.

Discussion and Conclusions

This article developed a frontstage/backstage framework to analyze crises of rule evasion. In 1974, regulators were informed backstage of a run through the money market (built on rule evasion) by bank executives who hoped to receive state support. Internally, the Fed developed a regulatory understanding of the money-market run by recombining understandings from its monetary-policy, bank-examination, and research divisions. On the frontstage, however, the Fed communicated to Congress, the press, and retail depositors that the crisis was limited to losses in foreign exchange and hence within existing rules.

The decision to hide the money-market run from the public shaped Fed officials’ management of the crisis, enabling them in some ways but constraining them in others. It kept panic from spreading to adjoining markets, ensured that the Fed would be able to act quickly at its own discretion, and avoided the question of why the Fed had not stopped rule evasion before it could become a problem. Yet it also limited the Fed’s room for maneuver against the companies backstage, to the point where regulators became caught between frontstage and backstage. Because the Fed had left the public in the dark, it could neither ask Congress for new crisis-management tools tailor-made to stabilize the money market, nor could it bring public pressure to bear on the largest New York banks to backstop the money market with private funds. The Fed found itself forced to reinterpret and arguably break the laws governing its existing crisis-management tools in order to backstop the money market with public funds.

In the aftermath of the crisis, the Fed’s frontstage/backstage strategy thwarted efforts to re-regulate the money market. Because the Fed could not easily extend its oversight and enforcement to a market that sat outside its statutory authority, legislative action would have been necessary. Yet having hidden its money-market backstop from Congress, the Fed could not ask for reform without putting its reputation at risk. Legislators and activists did not, on their own, develop an understanding of the money market, and hence could not include its re-regulation in their draft bills.

This article contributes to sociological research on regulation, crises, finance, and organizations. First, prior work has established that regulators often act in the interest of companies but that regulatory capture explains only part of this outcome (Edelman et al. 2001:1634; Novak 2013; Sawyer and Hovenkamp 2019). This article identifies a novel mechanism that accounts for some of the unexplained pro-industry stance by showing how regulators can become caught between frontstage and backstage. While the outcome resembles that of regulatory capture, the conditions that give rise to the two mechanisms differ. In stressing the links between frontstage and backstage, my argument builds on and calls for further refinement of research in the sociology of regulation that pertains to the role of the public (Carpenter 2010; Epstein 1996). Future research could explore when and how anticipation of public involvement suffices to influence regulatory action.

Second, this article provides a new answer to a core question in the sociology of crisis: why do crises so often fail to spark significant change? (Alexander 2018; Balleisen et al. 2017; Hutter and Lloyd-Bostock 2017). Existing research has put forward convincing explanations for the difficulty of implementing change (e.g., the fickleness of public attention), but does not account for the challenge of conceptual change. If crises “unveil . . . underlying contradictions,” they should put agents of change in a position to “transcend . . . oppositions and dichotomies” in their understandings; yet again and again, “expert claims to crisis . . . and (lay) accession to those claims serve not radical change . . . but rather the affirmation of long-standing principles” (Roitman 2014:9–10, 6). This article highlighted that regulators—who figure prominently among the experts shaping the terms of crisis discourse in contemporary societies—may conceal novel understandings from the public. Future research might explore the scope conditions for regulators’ ability to hide their internal understandings of a crisis, for example, the role of so-called sunshine laws that mandate openness to the public (Luscombe and Walby 2017; Schudson 2015).

Third, this article contributes to the sociology of finance by drawing attention to the interplay between the public statements and internal workings of financial regulators. To date, attention has tended to focus on one (Braun 2016; Holmes 2014) or the other (Fligstein et al. 2017; Wansleben 2021). For the crisis of 1974, however, analyzing either in isolation would obscure important aspects of regulators’ crisis management. Not only were public statements carefully drafted with the goal of evoking certain reactions, but legislators’ and journalists’ reactions—even just the anticipation of such reactions—profoundly shaped what the Fed could and could not do backstage. Recent research suggests that this interplay matters for other financial crises as well (Abolafia 2020).

Fourth, organizational scholarship in the tradition of Meyer and Rowan (1977) has in recent years explored how regulators decouple their policy (the governing statutes) and practice (oversight and enforcement). For example, regulators allow hospitals to overbill Medicare if the hospitals treat more disadvantaged patients and provide more medical education (Heese et al. 2016). This article shows that such processes are asymmetrical: regulators cannot decouple as easily when the decoupled practices are detrimental to firms, because those firms can turn to the courts to force a recoupling. More broadly, organizational scholarship, which long tended to treat regulation as an important but exogenous factor affecting firms (Edelman et al. 2001; Gray and Silbey 2014), increasingly studies regulatory agencies as organizations (Andrews and Esteve 2015; Arellano-Gault et al. 2013). But, as this article has shown, when transposing concepts such as decoupling from firms to regulatory agencies, it is important to consider how the concepts are limited or changed in the new context.

The Fed has to navigate between frontstage and backstage in both of its principal policy domains: not only in financial regulation but also in monetary policy. A Goffmanian re-reading of Krippner’s (2007) influential account of monetary policymaking shows that the Fed may adjust its frontstage/backstage strategy in response to a crisis. 84 For much of the postwar period, the Fed kept its monetary-policy intentions secret and managed to avoid critical attention from the public (Krippner 2007:477–86). Yet when the inflation crisis of the 1970s rendered monetary policy highly salient, the Fed’s secrecy nurtured suspicions that it was creating unemployment and slowing growth. Through a series of policy experiments in the 1980s and 1990s, the Fed arrived at a new frontstage/backstage strategy built around transparency and credibility: it publicly shared the principles and data that would guide its monetary policy, and then followed through on them. By the early 2000s, market actors had learned to predict the Fed’s monetary policy and moved market interest rates in anticipation, rendering action by the Fed superfluous (Krippner 2007:501–5). Central bankers had happened upon a strategy that allowed them to keep inflation low while avoiding blame for slower growth.

To the extent that audiences perceive the Fed as a unitary actor, the Fed’s frontstage/backstage strategies in financial regulation and monetary policy interact. Recent research suggests that, in the 2007/8 crisis, the public judged central bankers’ statements about financial stability at least in part by applying the yardstick of transparency from monetary policy. When the public learned that central bankers were confining information about financial risk to the backstage, they were “blamed for not speaking up” (Velthuis 2015:334). To restore confidence in financial stability, central bankers had to “issue various calming statements to reassure [depositors] that we don’t know something nasty that we are keeping from the public” (Holmes 2014:117). The 2007/8 experience suggests that, although a regulatory agency may find it useful to employ different frontstage/backstage strategies across its policy domains, the discrepancy between these strategies, if found out, can exacerbate public criticism.

There is reason to think that regulators of industries other than finance can also become caught between frontstage and backstage, particularly if they seek to avoid a loss of public confidence in a market. Sociologists of markets have found that, while a bank run is the prototypical case, “the role of confidence is not limited . . . to the area of finance” (Swedberg 2012:530; see also Akerlof and Shiller 2009:11–18; Beckert 2009:249, 259, 261). While, over the past decades, regulators of non-financial industries have focused on market efficiency to the exclusion of almost any other concern (Berman 2022:129–53), confidence has moved up the regulatory agenda as supply chains across a range of industries were disrupted beginning in 2020 (White House 2022:191–220). Supply-chain researchers stress that a loss of confidence can lead to hoarding, which exacerbates the very problem customers seek to avoid: “like a bank can suffer a run on cash, a supply chain can suffer a run on inventory” (Bray et al. 2019:466). To the extent that regulators of non-financial industries craft their public statements with the maintenance of confidence in mind, they increase their ability to thwart self-fulfilling market instability, but they also make themselves more susceptible to becoming caught between frontstage and backstage.

Social regulators, whose responsibilities such as environmental protection and workplace safety run across industries, are less concerned with the public’s confidence in any one market, and even if they might prefer to hide backstage knowledge from the public, would find it relatively difficult to do so. Their governing statutes, passed in the late 1960s and early 1970s after pressure from mass movements intent on citizen participation, force social regulators to divulge much of the information they possess about firms (Sabin 2021). 85 Yet even social regulators may become caught between frontstage and backstage to the extent that they seek to achieve their goals by helping to create markets for new technologies, for example, in renewable energies (Mazzucato 2016). Because such markets are as yet untested, the issue of confidence reigns supreme. Firms are tempted to drop out of technology development if they fear their suppliers and customers will lose faith in the new technology. Such self-fulfilling prophecies threatened to derail the development of solar panels in the 1970s and 1980s if regulators had not shored up confidence (Ergen and Umemura 2021). With new technologies widely considered essential for tackling major challenges such as climate change, social regulators can use their public pronouncements to smooth these development trajectories, but they are also at risk of becoming caught between frontstage and backstage if they withhold negative information about a new technology.