Abstract

Climate change is intensifying the frequency and severity of weather-related natural disasters, including hurricanes, floods, wildfires, and earthquakes, with devastating effects on millions of lives annually. These events generate significant monetary and non-monetary costs, undermining individual and societal well-being. Using a nationally representative longitudinal dataset from Australia, this study explores the dynamics of well-being before, during, and after natural disasters, with a particular focus on the mediating role of social capital. We employ an event-study design with individual fixed-effects to capture both immediate and long-term effects of natural disasters on four critical dimensions of well-being: financial satisfaction, safety satisfaction, mental health, and psychological distress. Our findings reveal that the adverse impacts of natural disasters are profound and long-lasting, persisting in some cases for over 6 to 7 years, with well-being implications exceeding $1,500,000 in equivalent losses. We find that social capital emerges as a powerful buffer, significantly mitigating declines in safety satisfaction and mental health while reducing psychological distress both during and after disasters. These results suggest that social capital is an intangible asset that extends beyond economic compensation, fostering resilience and enhancing recovery outcomes in populations affected by natural disasters.

Introduction

Natural disasters, driven by the intensification of climate change, have become a profound global challenge. Recent data indicates that over 3.6 billion people reside in areas highly vulnerable to climate impacts, with an estimated 200 million individuals impacted annually by floods, storms, and droughts (IPCC, 2023). In economic and social research, natural disasters have gained increasing attention as a distinct area of study due to their multifaceted effects, including declines in mental health, life satisfaction, and heightened poverty risks. For instance, Baryshnikova and Pham (2019) identified that experiencing a natural disaster in the prior year correlates with a 0.37 point decline in mental health scores. Frijters et al. (2021) observed a reduction in hedonic well-being by approximately 6% within the first 2 weeks post-disaster. In a longer-term view, Wang and Wang (2023) noted that the Wenchuan earthquake of 2008 substantially decreased victims’ subjective well-being for nearly a decade, equating to a 67% loss in average household income. Moreover, Adeagbo et al. (2016) highlighted that floods in Nigeria had detrimental effects on 47% of housing structures, 41% of household assets, and 45% of children’s education, with significant disparities in recovery expenses between urban and rural areas, as well as between genders. In this context, identifying populations most vulnerable to the impacts of natural disasters is critical for designing effective policy interventions (World Health Organization, 2022).

This paper examines the dynamics of individual well-being surrounding the occurrence of a natural disaster, putting special attention to the mediating role of social capital. While extensive research has explored the direct physical and economic impacts of disasters (Gunby & Coupé, 2023; Lohmann et al., 2019; Sekulova & van den Bergh, 2016), the role of psychosocial factors, such as community resilience and individual perceptions of risk, has received little attention. Community resilience, defined as the collective ability of a community to adapt to, respond to, and recover from adverse situations (Salman, 2025), directly influences the efficacy of disaster response and long-term recovery. Meanwhile, individual perceptions of risk can drastically affect personal preparedness and responsiveness, with more accurate perceptions linked to better outcomes. Research indicates that communities with high resilience levels and individuals with well-informed risk perceptions exhibit stronger recovery trajectories and reduced disaster impact (Oh, 2024). Addressing this gap is crucial, as current disaster mitigation strategies tend to prioritize infrastructure development and financial compensation (Sangha et al., 2021). However, these approaches often exclude individuals who lack access to formal support mechanisms, such as private insurance or government relief programs. This exclusion is frequently driven by factors like low income, geographic isolation, or social marginalization (Boon, 2020; Nohrstedt et al., 2021). Among these populations, a lack of community ties and social networks may act as an additional vulnerability factor. The absence of such networks can intensify the psychological and material impacts of disasters, as isolated individuals may struggle to access the support systems necessary for recovery (Ahumada et al., 2024). Conversely, communities with strong social bonds are better equipped to coordinate recovery efforts, disseminate critical information, and provide mutual support during crises (Bernados & Ocampo, 2024). The main objective of this paper is to provide evidence on how social capital can influence the ability of affected groups to cope with natural disasters.

We employ data from a nationally representative longitudinal dataset in Australia, which includes detailed records on individual experiences of weather-related home damage. We simultaneously focus on four domains, namely financial satisfaction (FS), safety satisfaction (SS), mental health (MH) and psychological distress (K10). A major empirical difficulty in estimating the impacts of natural disasters on victims is that it is problematic to compare residents whose homes were directly affected by the disaster and those who were not affected, because the two groups may differ non-randomly in housing quality and residential location. Our approach, given the availability of individual-level longitudinal data, is to estimate regression models with individual, time, and region fixed-effects. Hence, identification comes from comparing changes over time in the well-being of disaster victims with changes over time in well-being of non-victims. Our event-study design shows that being a natural disaster victim is not predictable by changes in pre-disaster well-being, supporting our identification assumptions.

The study contributes to the literature on the impacts of natural disasters in several important ways. Firstly, the paper advances our understanding of the temporal dynamics of well-being around the occurrence of a natural disaster. While previous research has mostly focused on life satisfaction and happiness (Fluhrer & Kraehnert, 2022; Frijters et al., 2021; Gunby & Coupé, 2023; Wang & Wang, 2023), we extend the analysis by simultaneously considering four dimensions which have been object of little scrutiny. FS reflects economic stability, which can be significantly disrupted by disasters due to property damage, job losses, or unexpected costs, influencing savings, consumption, and long-term financial resilience. While earlier evidence finds little evidence that direct exposure affects the probability of full-time employment or household income (Johar et al., 2022), there is the possibility that, through higher perceived risk and increased financial hardships, a natural disaster raises financial dissatisfaction. SS captures the perceived security of individuals, often diminished when disasters affect housing, infrastructure, and public safety, which can deter investments and reduce property values. MH is critical because disaster-related trauma can lead to decreased productivity, higher healthcare costs, and greater economic dependency. While there is evidence to suggest that natural disasters affect negatively mental health, the available evidence is mostly based on contemporaneous or short-term (≤1 year) effects (Baryshnikova & Pham, 2019; Johar et al., 2022). Psychological distress, as measured by the K10 scale, has been found to be sensitive to housing insecurity (Scutella & Johnson, 2018). This measure highlights the mental strain disasters impose, often leading to reduced workforce participation, increased reliance on social support systems, and enduring socioeconomic challenges.

Secondly, economists are increasingly interested in quantifying the economic value of social capital, recognizing that for some individuals, it represents their most critical resource. This interest arises from social capital’s capacity to facilitate personal development and enhance social cohesion, essential elements for thriving communities. These elements are crucial for fostering thriving communities, as social capital directly contributes to the creation of supportive networks and the reinforcement of social norms that encourage cooperation and collective action. These networks and norms are instrumental in amplifying economic opportunities and improving community resilience, making the quantification of social capital’s impact increasingly relevant for economic and social policy development. Empirical research demonstrates that individuals with greater levels of social capital are better equipped to withstand socio-economic challenges (Zhang et al., 2017). Moreover, robust community networks and trust within social groups have been found to provide a safety net against poverty (Endris et al., 2022; Parvin et al., 2023; Pham & Mukhopadhaya, 2022). Evidence on the role of social capital during disasters remains scarce (Calvo et al., 2015; Johar et al., 2022; Luce et al., 2022) and is inherently complicated by the potential endogeneity of social capital, as social connectedness can itself be influenced by life circumstances and disruptive events (Sharma et al., 2024; Wang & Wang, 2023). In this paper, we explore how social capital shapes the dynamics of various dimensions of well-being after a disaster, using approaches that thoroughly address the potential endogeneity of social capital.

Thirdly, Australia’s unique geography and climate render it particularly vulnerable to extreme weather conditions, making it a compelling case study for natural disasters. This susceptibility is not unique to Australia; similar challenges are faced by other developed countries, including the United States, which contends with hurricanes, wildfires, and tornadoes (Brunetti et al., 2023), and Canada and Japan, known for significant wildfires and earthquakes, respectively (Hertelendy et al., 2022; Tanifuji, 2022). Like Australia, these nations face a range of natural disasters that are exacerbated by climate change (IPCC, 2023; Xu et al., 2023).

For instance, the catastrophic Black Summer bushfires of 2019 to 2020 in Australia burned over 18 million hectares, destroyed thousands of homes, and significantly impacted economic stability and ecological systems (Haque et al., 2023). The economic reliance on agriculture, mining, and tourism—sectors highly sensitive to environmental disruptions—amplifies the socio-economic consequences of these disasters. Despite robust disaster response frameworks like the Disaster Recovery Payment and Emergency Hardship Assistance providing financial relief, private insurance systems often fail to adequately cover the most vulnerable populations, leaving them disproportionately exposed (Booth & Tranter, 2018; Crawford et al., 2024). Similarly, developed countries globally are enhancing their response and mitigation systems to manage these threats more effectively.

By highlighting these similarities, our analysis of Australia is contextualized within a global framework, illustrating how developed countries are adjusting their strategies in response to the increasing frequency and intensity of natural events (NOAA National Centers for Environmental Information, 2025). This global perspective underscores the critical role of social capital as a primary buffering mechanism against the socio-economic impacts of natural disasters.

The structure of this study is organized as follows: Section “Literature Review”, the literature review on the impacts of natural disasters and the role of social capital in resilience. Section “Social Captial” describes the econometric model used for the analysis. Section “Data and Definition of Variables” details the data and key variables, including measures of social capital, disaster exposure, and well-being indicators. Section “Empirical Framework” presents the empirical results. Section “Sensitivity Checks” discusses various robustness checks and additional analyses to validate the findings. Finally, Section “Conclusions and Policy Recommendations” concludes with the policy implications and recommendations of the study.

Literature Review

Economic research has explored the impact of natural disasters on subjective well-being, with findings varying based on the scales, datasets, and methodologies used. In the literature on the impacts of natural disasters at the country level, some studies have reported limited or statistically insignificant effects on national life satisfaction due to disasters such as hurricanes. For example, Berlemann (2016) analyzed data from 80 countries around the globe using several waves of the integrated European/World Values Survey combined with hurricane data. The study found that while hurricane risk negatively impacts life satisfaction in relatively poor countries, where populations have limited means to take protective measures, this effect is notably smaller and often statistically insignificant in highly developed countries. Similarly, Döpke and Maschke (2016) utilized a panel data analysis covering multiple countries and various welfare measures alongside GDP, finding that natural disasters do not have a significant contemporaneous impact on alternative welfare indicators including life satisfaction, except for the Human Development Index, which showed some negative effects in disaster years. A more focused lens emerges at the regional level, with studies analyzing floods, droughts, and forest fires (Carroll et al., 2009; Frijters et al., 2021; Luechinger & Raschky, 2009; von Möllendorff & Hirschfeld, 2016). These analyses typically reveal significant negative effects, though the size and duration of these effects vary. For instance, Frijters et al. (2021) report short-term impacts lasting 2 weeks, while Carroll et al. (2009) observe flood-related consequences enduring over a year. These studies often draw on large datasets, enabling robust regional assessments, though the focus tends to remain on indirect effects of living in disaster zones.

Individual-level analyses provide more granular insights, highlighting the diversity of personal experiences. These studies explore how direct exposure, such as property damage or bereavement, influences subjective well-being, showing that severe damage can lead to substantial declines in well-being (Sekulova & van den Bergh, 2016) especially when losing loved ones over property damage (Calvo et al., 2015). Personal losses yield stronger negative effects compared to merely residing in affected areas (Hudson et al., 2019). However, analyses based on group-specific average treatment effects and staggered adoption scenarios (Callaway & Sant’Anna, 2021) fail to detect any significant effects of disaster exposure on long-term well-being, while contemporaneous effects tend to be minimal (Gunby & Coupé, 2023). Mediating factors play a crucial role in disaster outcomes, as evidenced by studies on Hurricane Katrina (Deryugina et al., 2018; Gallagher & Hartley, 2017) and Australian disasters (Baryshnikova & Pham, 2019). These studies underline the importance of insurance, displacement options, and governmental aid in cushioning economic and psychological impacts.

Social Capital

In the words of Putnam (2000, pp. 664–665), “social capital is the features of social life—networks, norms, and trust—that enable participants to act together more effectively to pursue shared objectives.” Regions with high levels of social capital tend to have better health outcomes, suggesting that the support and resources provided through social networks can lead to improved health and reduced stress (Amoah & Adjei, 2023; Pedersen et al., 2023). Moreover, social capital can significantly influence socio-economic mobility and promote resilience against adversity. For instance, research has examined how social capital enhances the resilience of displaced women in urban slums in Khulna, Bangladesh, highlighting the role of civic participation and social networks in fostering economic stability and reducing domestic violence (Parvin et al., 2023). Similarly, strong social networks improve food security, income stability, and resilience to climate variability (Yang et al., 2024).

Beyond its direct impacts on individual and household well-being, social capital plays a key role in community development and governance. High levels of social capital are often associated with increased civic engagement, trust in institutions, and collective efficacy, which can enhance the ability of communities to address shared challenges and implement sustainable development initiatives (Salinger et al., 2024). Furthermore, social capital can facilitate knowledge-sharing, innovation, and collaboration, particularly in disaster recovery contexts, by leveraging collective resources to rebuild infrastructure and restore livelihoods (Qadriina et al., 2024). Research examining pre- to post-disaster changes in happiness of 491 women affected by Hurricane Katrina found that social support is an important element for the recovery of victims (Calvo et al., 2015), while social capital may improve the resilience to financial hardships caused by a natural disaster (Johar et al., 2022). However, this evidence does not consider the potential endogeneity of social capital and its dependence upon life events, including the occurrence of a disaster.

Empirical Framework

Our baseline approach is based on an event-study design with individual fixed-effects. We allow the effect of disasters to vary with time since its occurrence to differentiate immediate from long-term effects. We assume the cardinality of satisfaction variables because treating them as ordinal versus cardinal makes little difference (Budría & Ferrer-I-Carbonell, 2019). Let I be a set of individuals, with an element i,

where

In an event-study framework, the inclusion of leading effects—variables indicating whether an individual is 1, 2, or up to 7 years away from experiencing a natural disaster—is crucial for assessing the validity of the causal interpretation of the results. These leading effects test the parallel trends assumption, a core requirement for event studies. This assumption states that, in the absence of the treatment (in this case, disaster), the well-being trajectories of the treated (affected individuals) and untreated (the unaffected) groups would have been the same. If the coefficients for these leading variables are statistically significant, it suggests that treated individuals were already on a different trajectory before the disaster occurred. This could imply that the treatment is endogenous, meaning the likelihood of experiencing damages from a natural disaster is systematically related to individual circumstances or trends (e.g., deteriorating mental health, break-ups, or unsafe environments). Conversely, if the leading effects are not significant, this supports the idea that the groups were comparable before the event, making it more plausible that the disaster was exogenous to their prior circumstances.

Data and Definition of Variables

We use the 2009 to 2021 waves of the Household, Income, and Labor Dynamics in Australia (HILDA) Survey, a comprehensive, nationally representative longitudinal study that examines the economic, social, and demographic dynamics of Australian households. Initiated in 2001 and conducted annually, it tracks individuals and households over time. The survey combines objective data on income, labor market activities, health, education, and housing, among others, with subjective measures, such as mental health and satisfaction with various areas of life, offering a rich dataset for understanding Australia’s social fabric. The original 2001 sample included approximately 7,600 households and 13,000 individuals, with periodic updates to account for attrition.

Since 2009, HILDA asks each respondent whether, within the last 12 months, a weather-related disaster (flood, bushfire, cyclone) damaged or destroyed the respondent’s home. These responses are further broken down by quarter, albeit with a reduced response rate. We therefore focus on the annual data. After excluding cases with item non-response, which represented 2.4% of the original dataset, the final estimation sample comprises 227,542 observations from 25,908 individuals. Although retention rates are remarkably high in the HILDA database (yearly average = 90%), the non-random exit and entry of individuals in panel data is a potential concern. In Section “Attrition and Reverse Causality” we conduct sensitive checks to examine to which extent our findings might be affected by attrition bias.

Well-Being Indicators

The HILDA dataset includes a battery of questions on individual well-being. In this paper we focus on four domains. The first two are FS and SS. The response alternatives are coded in a Likert scale where 0 is “Totally Dissatisfied” to 10 being “Totally Satisfied”. The third well-being indicator is MH, which is measured with a composite indicator constructed from five questions of the Medical Outcomes Study Short Form (SF-36) Questionnaire, one of the most widely used and validated self-completion measures of health status (Ware & Gandek, 1998). The SF-36 questionnaire serves as a standardized instrument in psychological evaluations, assessing multiple aspects of an individual’s mental health, such as emotional and social functioning. This facilitates a comprehensive understanding and effective diagnosis of mental health conditions.

The MH inventory has been shown to be as effective as surveys with more item surveys for detecting major depression, affective disorders, and generally, anxiety disorders (Thalmayer et al., 2023). The five questions used for constructing the MH index are based on how often the respondents have felt (a) nervous; (b) so down in the dumps that nothing could cheer you up; (c) calm and peaceful; (d) down; and (e) happy over the last 4 weeks. The candidate answers are: (1) all of the time, (2) most of the time, (3) a good bit of the time, (4) some of the time, (5) a little of the time (6) and none of the time. The MH scale is obtained by summing the answers to these five questions (items (a), (b), (d) are reversed), dividing by 25 and multiplying the sum by 100. The reversal of selected items ensures that higher scores uniformly indicate better mental health outcomes, aligning with the standard scoring procedures of the SF-36, where typically negative-oriented questions are scored in reverse to match the positive orientation of the overall health assessment.

The final measure ranges between 0 and 100, where 100 implies very good MH, and 0 implies severe health deterioration, almost dead. Finally, the fourth indicator is the 10-item Kessler Psychological Distress Scale (K10). This indicator is available only biannually in the HILDA data, which results in a reduction in sample size in the regression stage of the paper. The K10 scale measures the experience of non-specific psychological distress over the past 4 weeks and ranges from 10 to 50. To allow for comparison with the satisfaction variables (FS and SS), we re-scale MH and K10 to range from 0 to 10.

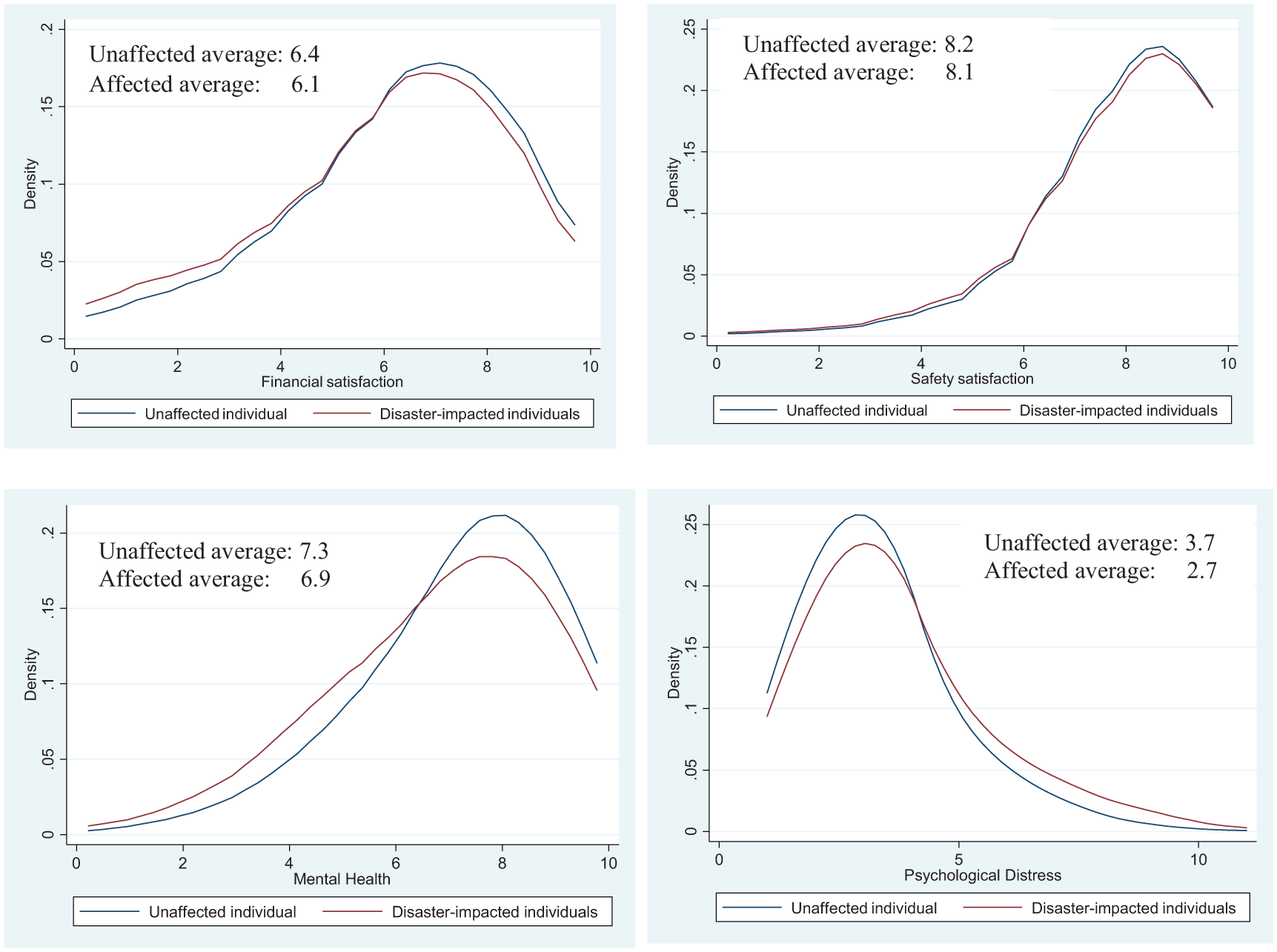

Figure 1 depicts the kernel densities of the four well-being variables. The distributions of FS, SS and MH are left skewed, while K10 is right skewed. This suggests that most individuals fare relatively well in all dimensions. However, relative to unaffected individuals, disaster-impacted individuals are significantly worse off in FS (6.1 against 6.4, p-value = .00), MH (6.9 against 7.3, p-value = .00) and K10 (3.7 against 2.7, p-value = .00), while the difference in safety satisfaction (8.1 against 8.2, p-value = .07) is significant only at the 5% level.

Kernel density of the well-being indicators.

Covariates

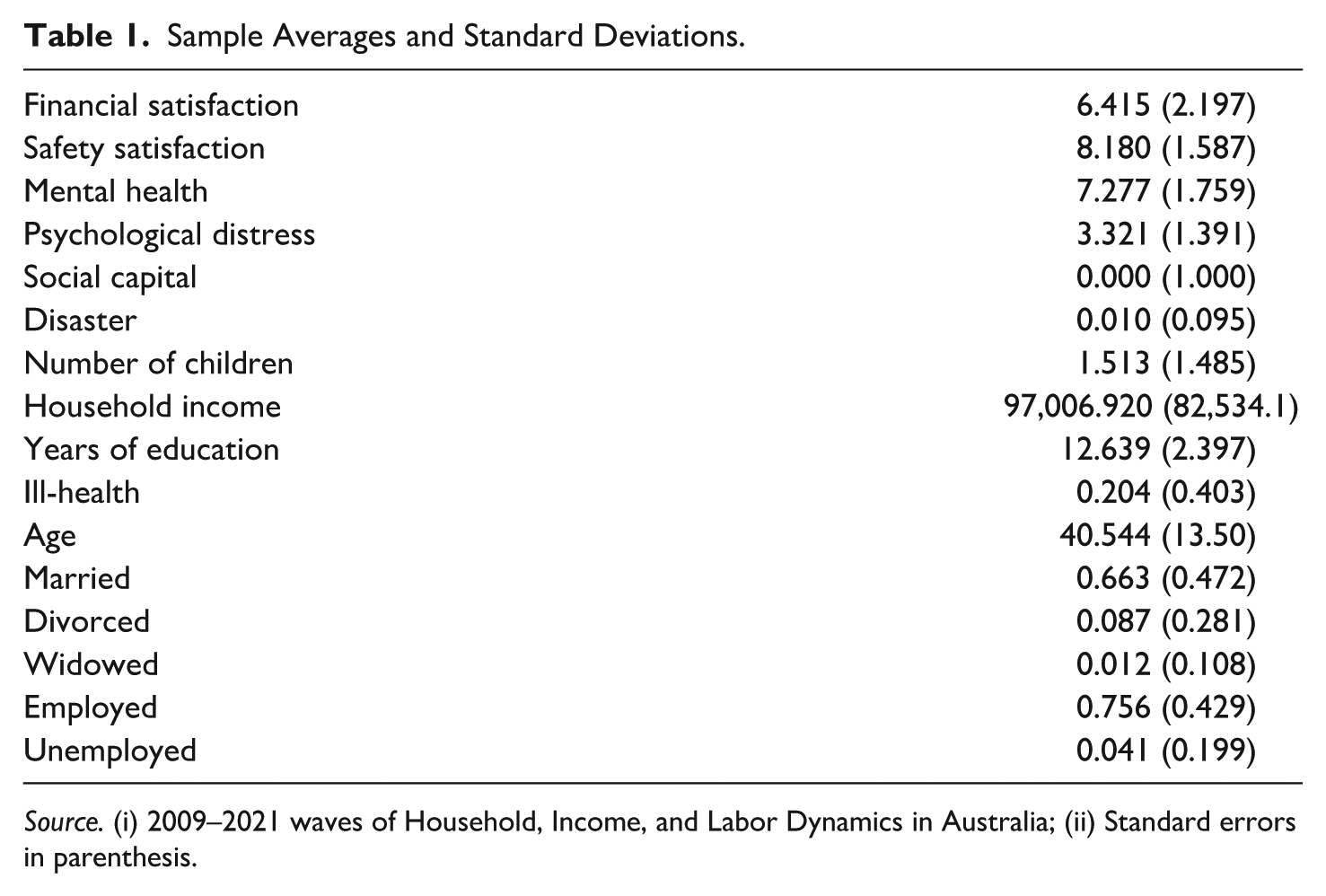

The empirical model includes a set of individual characteristics potentially relevant to account for well-being in various life domains, including employment status, age, education level, marital status, number of children and urban/rural location. In Table 1 we report summary statistics of the sample. The relevance of these variables in well-being equations has been highlighted in previous work (Bürger Lazar & Musek, 2020). We also include controls for household income and health condition, which are particularly crucial because weather-related home damage can have long-lasting repercussions on financial stability and physical health. Income was transformed by applying the OECD equivalence scale and normalized into real terms in accordance with the yearly consumer price index (OECD, 2013), while health condition is captured by a subjective health status question with a five-point response scale ranging from “1—excellent” to “5—poor.” We define a dummy variable that takes value one if the individual has an ill-health (>3). Self-assessed health has been widely used in the literature on the socioeconomic well-being-gradient (Beckfield, 2004), has been shown to be significantly correlated with physicians’ assessments (Meer et al., 2003) and predict individual labor force participation, retirement decisions, and other behaviors (Jylhä, 2009). Notwithstanding, in Section “Sensitivity Checks”, we provide sensitivity analyses when very granular controls for health status are included in the regression. Finally, we also include controls for remoteness and region of residence to account for regional disparities, and wave fixed-effects to account for the stance of the business cycle and temporal trends.

Sample Averages and Standard Deviations.

Source. (i) 2009–2021 waves of Household, Income, and Labor Dynamics in Australia; (ii) Standard errors in parenthesis.

Social Capital

We construct a social capital measure from the responses to a 10-item questionnaire in HILDA about how much support respondents were able to get from other people. This information is available in all waves of the HILDA. The items are: (a) I have no one to lean on in times of trouble (reverse coded); (b) I often feel very lonely (reverse coded); (c) I enjoy the time I spend with the people that are important to me; (d) I seem to have a lot of friends; (e) People don’t come and visit as much as I would like (reverse coded); (f) I often need help from other people but can’t get it (reverse coded); (g) I don’t have anyone that I can confide in (reverse coded); (h) There is someone who can always cheer me up when I am down; (i) When I need someone to help me out, I can usually find someone; and (j) When something’s on my mind, just talking with the people I know can make me feel better. Respondents rate the sentiments they perceive about the level of support they are likely to receive from other people, including their friends and families. Support is rated on a scale of 1 (strongly disagree) to 7 (strongly agree). The measures have good reliability and internal consistency (Cronbach’s alpha = .842). The 10 items in the scale are averaged, with lower scores indicating less social support and higher scores indicating more social support (Clark & Lisowski, 2018).

A natural concern is that social capital may be endogenous and dependent upon life shocks and events. We address this concern in two ways. Firstly, we factor out from the social capital score any effect arising from the occurrence of a natural disaster. Natural disasters can alter an individual’s network of relationships and community engagement due to physical displacement, loss of social ties, or a shift in priorities toward immediate recovery. These changes may artificially inflate or deflate measures of social capital taken after the disaster, reflecting temporary adaptations rather than an individual’s baseline capacity for maintaining social networks. Hence, among individuals affected by a natural disaster, we consider only pre-disaster social capital, which can be considered a more accurate representation of an individual’s intrinsic social capital stock.

As a second refinement, we acknowledge the fact that social capital may be affected by other individual circumstances related to economic affluence, aging and employment status, among others. Hence, we extract from the data a time-invariant component of social capital that excludes variations due to selected life events and wave-specific shocks. This adjustment ensures that our findings are not confounded by temporal changes in social capital, especially around the occurrence of a natural disaster. This is done by regressing the social capital score on a fourth-order polynomial in age and selected socio-economic factors including income, employment and marital status, where the estimated time-invariant individual fixed effect is the measure of social capital used in the paper. This procedure, which mimics (Budría & Ferrer-I-Carbonell, 2019) procedure to extract time-invariant personality scores from panel data, means that our social capital measure is time constant and free from a number of life events. In alternative specifications, we included more and fewer explanatory variables in the social capital regression and obtained very similar results. In Section “Sensitivity Checks”, we include additional sensitivity analyses.

Results

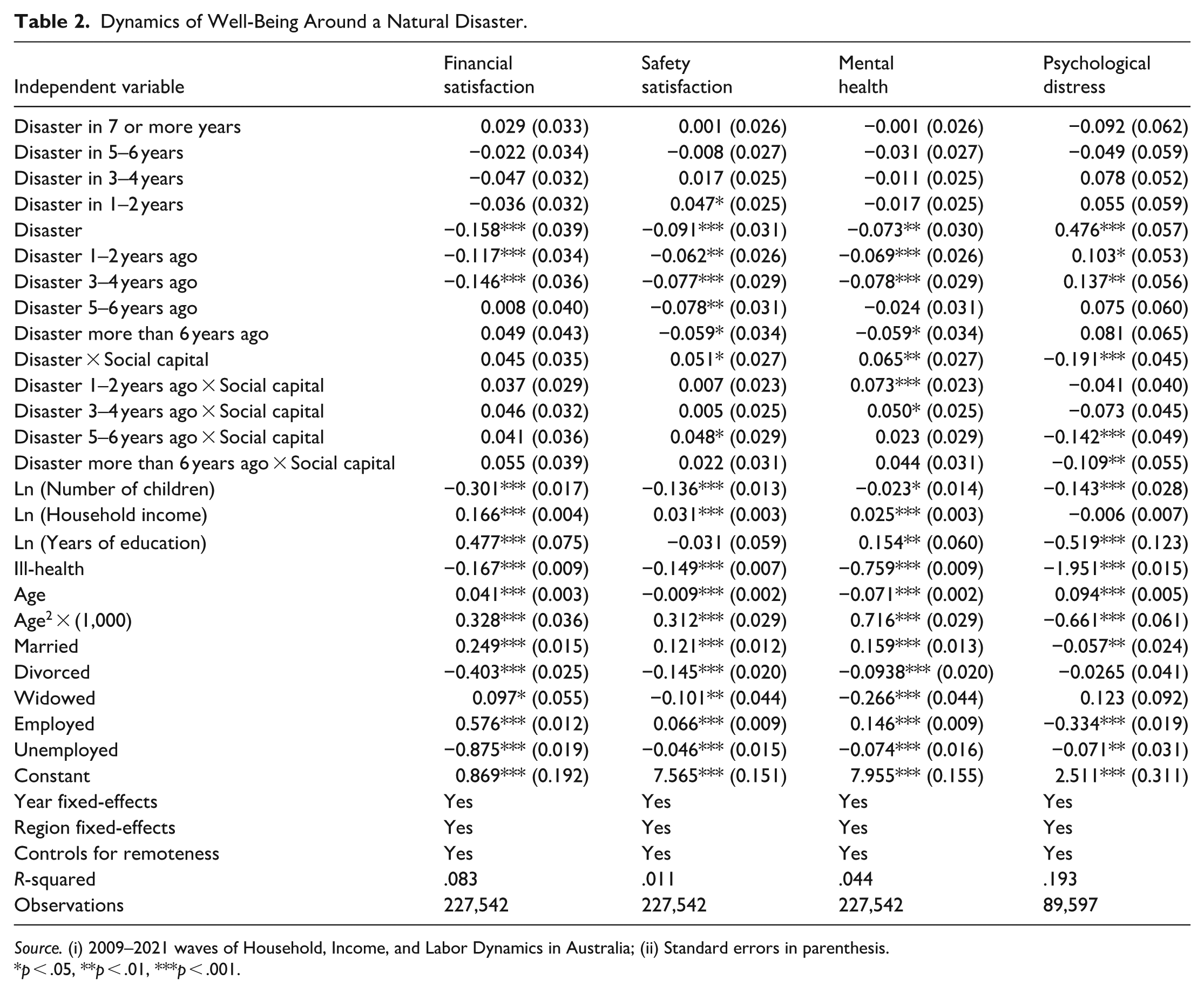

The results in Table 2 illustrate the dynamics of well-being around the occurrence of a natural disaster. Several patterns emerge. The coefficients of the leading effects are particularly noteworthy, as their significance would indicate that treated individuals (those affected by a natural disaster) were already on a divergent trajectory prior to the event. Fortunately, the non-significant coefficients of the leading effects provide evidence to the contrary, strengthening the case for the exogeneity of the treatment.

Dynamics of Well-Being Around a Natural Disaster.

Source. (i) 2009–2021 waves of Household, Income, and Labor Dynamics in Australia; (ii) Standard errors in parenthesis.

p < .05, **p < .01, ***p < .001.

The occurrence of a natural disaster is strongly associated with significant decreases in FS, SS, and MH, along with marked increases in K10. The contemporaneous impact on K10 is particularly striking, with the effect size being three times larger than that observed for FS and over five times greater than the effects for SS and MH. This disparity suggests that while financial and safety concerns are important, the psychological consequences represent a more substantial challenge. Moreover, natural disasters result in more than just short-term losses across the four domains considered in the paper. For instance, the reduction in FS during the first 4 years after experiencing a disaster ranges between 0.117 and 0.146 points on the zero-to-ten satisfaction scale. These figures are statistically significant and comparable to the impact of ill health, which reduces FS by 0.167 points. This trend is also observed in other dimensions, particularly SS, where the “scarring” effects persist and remain statistically significant for more than 6 years after the disaster, as indicated by a reduction of 0.059 points.

Next, we turn to the crux of our analysis. Social capital provides an immediate buffering effect when disasters occur. For instance, considering the K10 scale, the initial increase in distress triggered by a disaster, 0.476 points, is significantly reduced by 0.191 points among individuals with a social capital level one standard deviation above the mean, as suggested by the interaction term. Similarly, the initial decrease in mental health, −0.073 points, is significantly mitigated (+0.065)—almost vanishes—for individuals with high (+1 SD) social capital. Notably, the only domain where social capital does not show a protective effect is financial satisfaction. This finding is suggestive, as it indicates that the support provided by social capital does not primarily operate through material resources or financial aid from friends and family. Instead, its strength lies in serving as “emotional capital,” offering psychological support and comfort during the challenging circumstances of a disaster. This notion is further supported by the remaining interaction terms, which show that the buffering role of social capital may last up to more than 6 years.

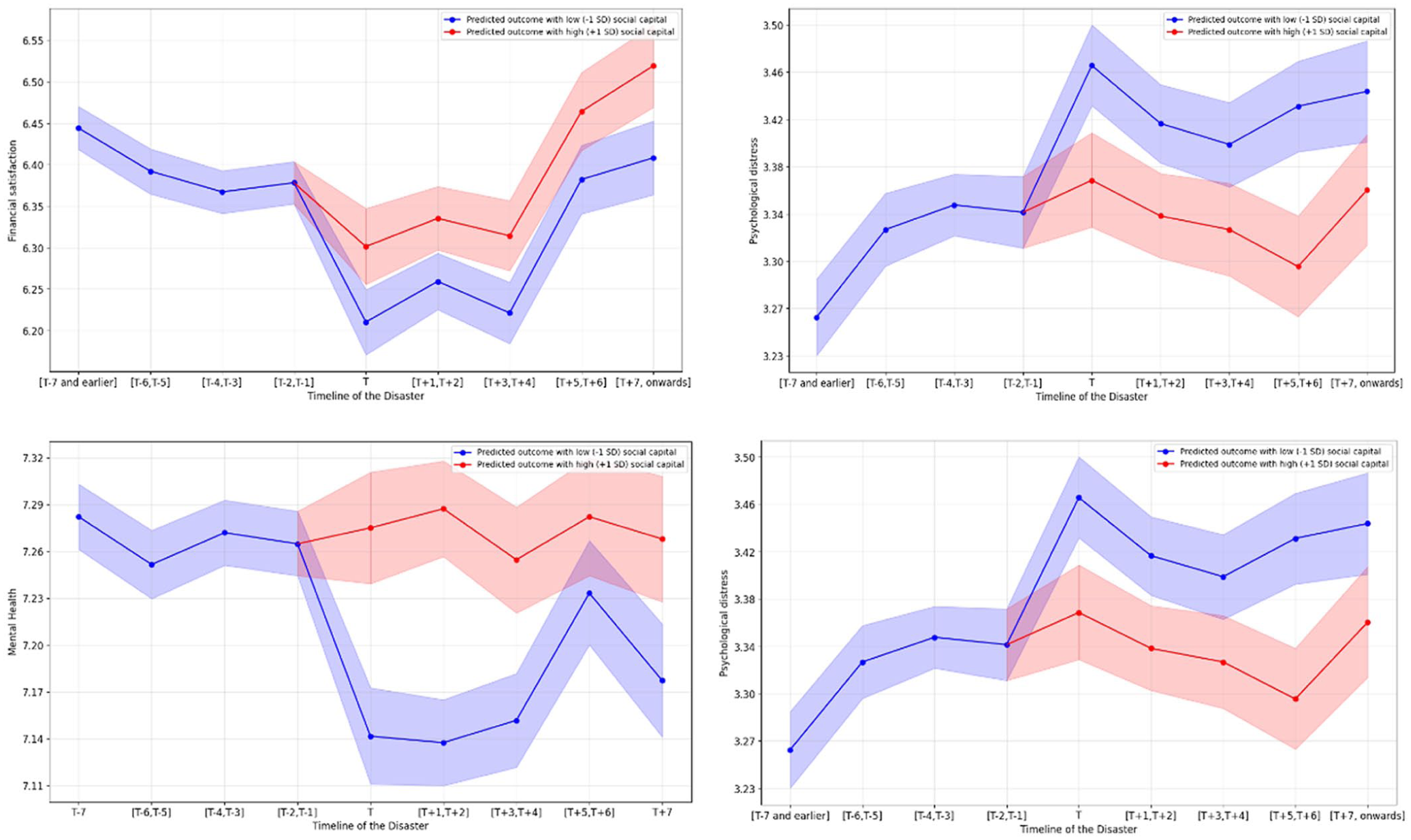

To better illustrate the role of social capital, we produced graphs in Figure 2 displaying well-being dynamics for individuals with low (−1 SD) and high social capital (+1 SD). Individuals with high social capital experience minimal changes in their mental health during and after the disaster, maintaining levels nearly equivalent to their pre-disaster benchmark. Meanwhile, their psychological distress rises slightly in the immediate aftermath but quickly recovers, ultimately exceeding their initial well-being baseline.

Well-being paths, by social capital.

As for the remaining covariates, the socio-demographic and economic variables reveal distinct patterns, with differentiated effects depending on the well-being dimension. Income, as expected, emerges as a significant determinant of well-being across multiple dimensions, aligning with previous evidence (FitzRoy & Nolan, 2022; Thomson et al., 2022). Conversely, income is not significantly related to K10, suggesting that psychological distress is loosely related to the individual economic condition. This notion is supported by the beneficial effect of unemployment on K10, which contrasts with its harmful effects on the other domains (−0.875, −0.047, and −0.074 in FS, SS, and MH, respectively). Higher educational attainment is associated with significantly larger FS and MH, and lower K10, aligning with prior studies (Ahmed et al., 2020).

The number of children has heterogeneous effects. A higher number of children consistently reduces FS (0.301 points) and SS (0.136 points), potentially reflecting the financial burden and safety concerns associated with supporting a larger family. However, individuals with children report significantly lower K10 than non-parents, suggesting a complex relationship between parenthood and well-being previously highlighted in the literature (Maia et al., 2024).

Age exhibits a U-shaped relationship with SS and MH, while for K10, it follows an inverted U-shape. This suggests an optimal age range, around 40 years, associated with peak levels of well-being in these dimensions, while psychological distress is more pronounced at the extremes of the life cycle, peaking at 72 years. In contrast, FS increases exponentially with age, reflecting the accumulation of wealth and economic stability over time. Being married is positively associated with FS, SS and MH, and negatively related to K10. Conversely, divorced individuals tend to fare worse, particularly in FS (−0.403 points), likely reflecting the financial and emotional strain associated with divorce. Finally, having a job is associated with significant improvements in all dimensions, which is consistent with prior literature emphasizing the critical role of employment in fostering financial stability and emotional well-being (Mousteri et al., 2018; Wilson & Finch, 2021).

The Monetary Equivalent of Social Capital

Well-being and satisfaction equations are valuable tools for quantifying the relative importance of various factors and constructing equivalent scales between them. For instance, by comparing the coefficient for income, identified as

where

We can apply the same intuition to infer the income equivalent of social capital. When an individual possesses high social capital (+1 SD), it significantly reduces the contemporaneous impact of a natural disaster on SS and MH by 0.051 and 0.065 points, respectively. In the respective equations, these effects correspond to an equivalent income of 411.3% ($380,236.9) and 1156.6% ($1,069,248.9). Moreover, social capital’s buffering effects extend to subsequent years, adding +0.048 points in SS for disasters occurring 5 to 6 years prior and 0.073 points in MH for disasters 1 to 2 years prior. This suggests that social capital can act as an intangible yet valuable asset, serving as a substitute for financial resources in many dimensions. In others, like K10, it offers unique support that cannot simply be replaced by income, emphasizing its role in fostering resilience and well-being after disruptive events.

Sensitivity Checks

We conduct a series of sensitivity checks to ensure the robustness of the findings. These checks address several methodological concerns, including the potential endogeneity and time-variance of social capital, reverse causality, and panel attrition.

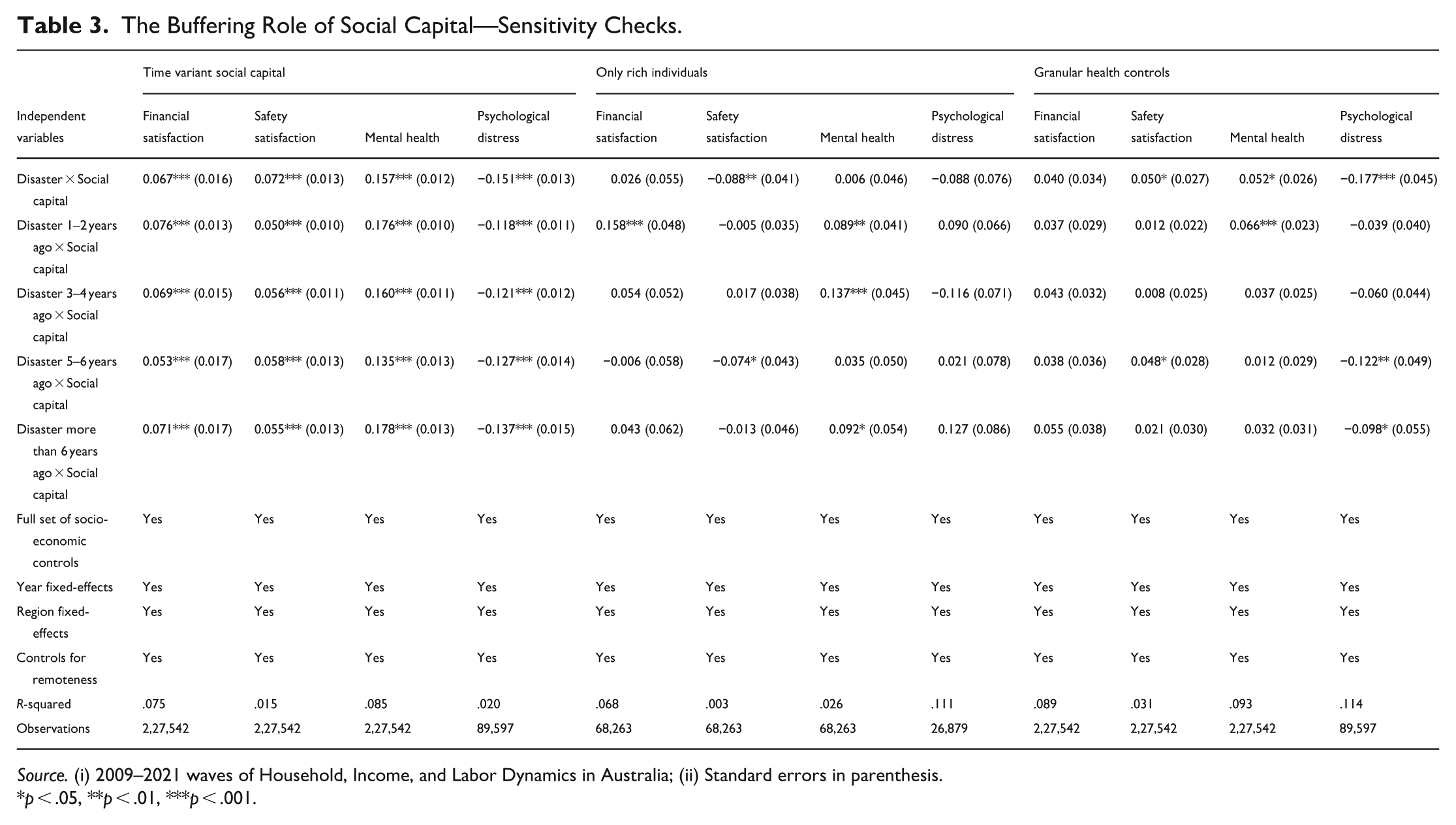

First, we relax the assumption that social capital is a time-invariant individual characteristic. Instead, we use annual social capital scores from the HILDA dataset, allowing it to vary yearly under the assumption that life shocks—such as a weather-related disaster—can influence an individual’s baseline level of social capital. This notion aligns with evidence that social capital may be responsive to life circumstances (Albrecht, 2018). Although the time-invariant measure employed in the baseline regressions is free from factors like aging, income, employment, and marital status, unobserved shocks could still reshape a person’s network of connections. For space reasons, we only report the coefficients for the interaction terms between social capital and the weather-related disaster. The results, as shown in the first part of Table 3, reveal that allowing social capital to vary over time leads to significantly larger interaction effects. Notably, the estimates become significant even for financial satisfaction, suggesting that time-varying social capital reflects a dynamic adaptation to changing socio-economic conditions, which are intricately linked to recovery and resilience. In this context, the baseline estimates of the paper can be regarded as conservative, as they do not capture the capacity of social capital to adapt and respond to external circumstances.

The Buffering Role of Social Capital—Sensitivity Checks.

Source. (i) 2009–2021 waves of Household, Income, and Labor Dynamics in Australia; (ii) Standard errors in parenthesis.

p < .05, **p < .01, ***p < .001.

Second, we provide estimates when the sample is restricted to income-rich individuals. We use the 70th percentile of the income distribution as a threshold, although other cutoffs (60th and 75th percentile) resulted in similar estimates. This exercise aims to address the concern that the social capital effects reported in the paper may be driven by income-poor households. The underlying logic for this argument is that social capital may be particularly vital for income-poor families as it compensates for limited financial resources and access to market-based services. While social capital can facilitate the sharing of tangible resources such as food, furniture, and shelter, its mediating role may diminish among wealthier households who are less reliant on community networks (Behera, 2023). However, our findings suggest otherwise, as the interaction terms are significant in the FS equation—a dimension deeply tied to economic concerns. In other words, social capital’s role transcends mere financial need. Another possibility is that wealthier families are more prone to afford professional advice, counseling, or formal support systems, while lower-income households depend on informal networks of family and community for both practical and emotional assistance. We find some evidence that this might be the case, as social capital fails to significantly enhance K10 trajectories among the wealthy after a disaster. Hence, after a natural disaster, social capital seems to act as “emotional capital” among the poor, rather than merely giving access to tangible resources. This evidence aligns with previous evidence on the link between social capital and emotional support (Kumari & Frazier, 2021). Notwithstanding, social capital also enhances MH trajectories among the rich, suggesting that they also benefit, to a lesser extent, from these support networks.

Third, relationships, support networks, and community engagement may be linked to health outcomes, particularly after a disruptive event. People affected by a natural disaster may encounter difficulties maintaining active social lives due to the physical demands of recovery, fatigue, and reallocation. These challenges can restrict opportunities to socialize and participate in community activities, potentially resulting in isolation and diminished well-being. Furthermore, the observed positive effects of social capital on well-being might, in part, reflect underlying good health rather than its independent influence. We address this issue by extending our regression to capture year-to-year variations in a battery of health conditions. These controls encompass a comprehensive range of health conditions, including blackouts, chronic pain, restricted physical activity (e.g., back problems, migraines), difficulty gripping, disfigurement, hearing problems, brain injuries, limb impairments, mental illnesses, arthritis, asthma, heart disease, Alzheimer’s, dementia, shortness of breath, speech issues, and uncorrected vision problems. The results in Table 3 suggest that the main findings of the paper do not stem from the health channel.

Attrition and Reverse Causality

The HILDA survey, launched in 2001, aims to provide a nationally representative longitudinal study of Australian households. While inherent in such longitudinal studies, selection and attrition bias could potentially affect the generalizability of our findings. However, it is important to emphasize that HILDA maintains a high average retention rate across waves, exceeding 90% (Watson, 2020). This substantial retention rate mitigates some concerns regarding attrition bias and supports the robustness of our longitudinal analysis. Nonetheless, to address this concern, we test for endogenous attrition. Although the average entry rate (individuals not in the sample in the previous period who are in the current period) and exit rate (individuals who leave the sample) are very moderate in our sample (8.9% and 7.4%, respectively), the non-random exit and entry of immigrants for reasons related to energy poverty is a potential concern. We can distinguish between those individuals who have joined the panel for the first time (“newcomers”) and those who had been on the panel previously but have returned (“returnees”). To address this issue, we regressed a dummy that takes value one for newcomers, zero otherwise on all the controls, including having suffered a natural disaster, and obtained a coefficient equal to −0.0103 (p = .245) for natural disaster. In other words, individuals’ entry in the estimation sample is not significantly related to victimization. We proceeded likewise with individuals who left the sample and obtained similar results.

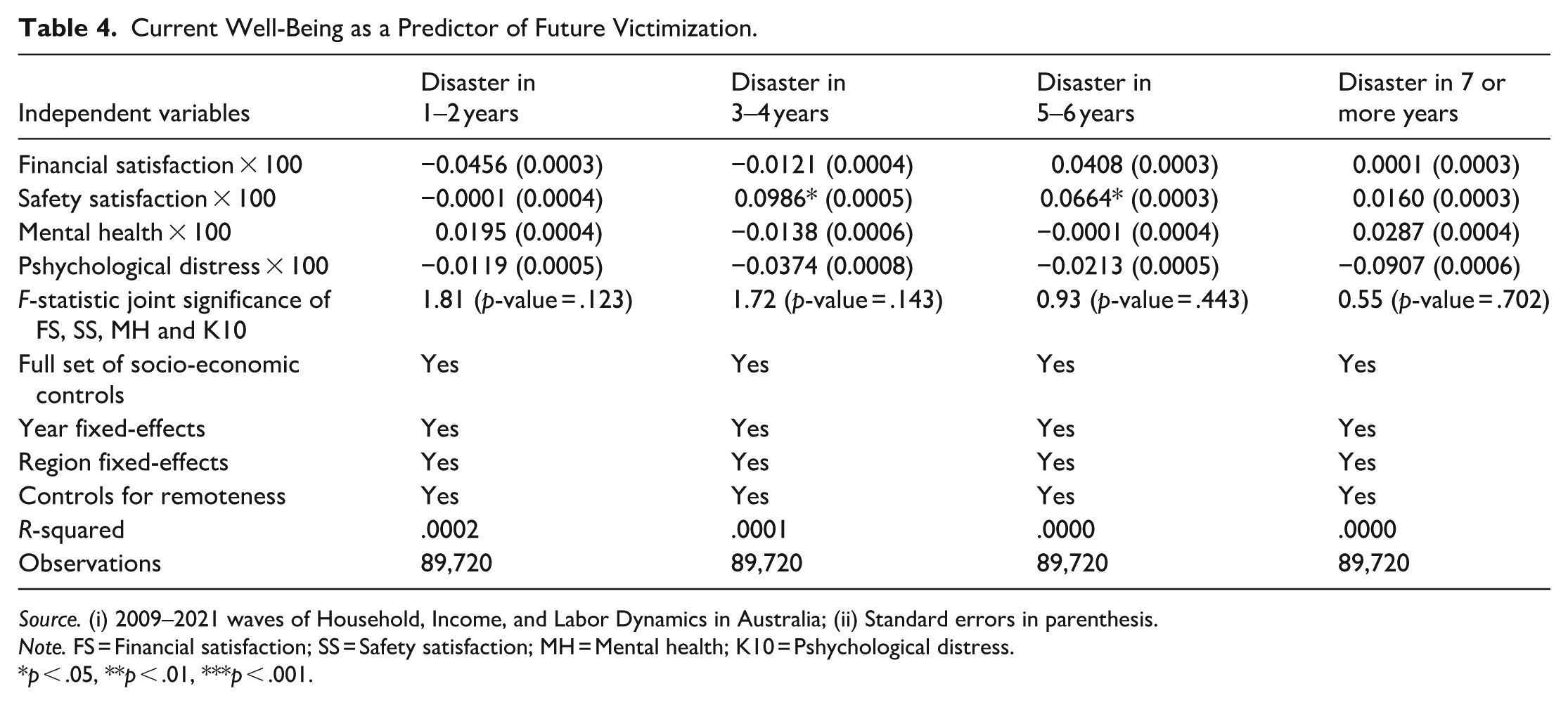

Finally, we test whether current well-being levels can predict the likelihood of future victimization, represented as a binary variable. Table 4 presents the results for various time horizons and includes tests for the joint significance of the four well-being dimensions. Although SS occasionally shows marginal significance at the 10% level, the findings overall indicate a lack of reverse causality from well-being to future victimization. This is consistent with the non-significant leading effects observed in the baseline estimates. Additionally, the low R-squared values suggest that the full set of explanatory variables, including the well-being indicators, provides minimal predictive power for victimization episodes, further supporting the exogeneity of disasters.

Current Well-Being as a Predictor of Future Victimization.

Source. (i) 2009–2021 waves of Household, Income, and Labor Dynamics in Australia; (ii) Standard errors in parenthesis.

Note. FS = Financial satisfaction; SS = Safety satisfaction; MH = Mental health; K10 = Pshychological distress.

p < .05, **p < .01, ***p < .001.

Conclusions and Policy Recommendations

This study highlights the significant and long-lasting impacts of natural disasters on individual well-being across multiple dimensions, including financial satisfaction, safety satisfaction, mental health, and psychological distress. By employing a robust longitudinal dataset and event-study framework with fixed effects, we establish that the adverse effects of natural disasters extend beyond the immediate aftermath, persisting for up to 6 to 7 years in some cases. Importantly, these findings underscore the profound socio-economic toll of disasters, with well-being implications equivalent to over $1,500,000 in losses.

The analysis also underscores the critical role of social capital in mitigating these impacts. Communities with stronger social ties and networks exhibit enhanced resilience, as reflected in improved safety satisfaction and mental health outcomes and reduced psychological distress following natural disasters. These findings reinforce the value of intangible assets like social capital, which complement but do not replace economic compensation and infrastructural recovery in fostering adaptation and recovery.

From a policy perspective, this research provides actionable insights. First, while financial interventions and infrastructure recovery are essential components of disaster response, targeted strategies to strengthen social networks and community engagement should be prioritized. Programs that foster trust, collective efficacy, and mutual support can play a pivotal role in reducing the long-term costs of disasters. Second, integrating social capital into disaster preparedness and recovery frameworks can enhance the effectiveness of existing public safety nets, ensuring that vulnerable populations are better equipped to withstand and recover from such events.

As climate change intensifies the frequency and severity of natural disasters, policymakers must adopt holistic approaches that combine economic, infrastructural, and social strategies to build resilience and reduce long-term vulnerability. Future research should explore the mechanisms through which social capital interacts with institutional support and investigate how these dynamics vary across different types of disasters, demographic groups, and cultural contexts.

Footnotes

Author Contributions

Santiago Budría: Conceptualization, methodology, supervision, econometric modeling, writing—review & editing. Alejandro Betancourt-Odio: Formal analysis, econometric modeling, visualization, writing—original draft. Marlene Fonseca: Literature review, data preparation, econometric modeling, writing—original draft.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Santiago Budría and Alejandro Betancourt-Odio thank seminar participants at the ASEPELT 2024 conference, 26th INFER Annual Conference, and gratefully acknowledge the financial support provided by the 2022 R&D&I National Projects and 2021 Strategic Projects Oriented to the Ecological and Digital Transition by the Spanish Ministry of Sciences and Innovation (Refs: PID2022-143254OB-I00 and TED2021-132824B-I00).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.