Abstract

What does the state do to prevent consumers from losing access to basic services in the market due to financial hardship, and under what conditions will this occur? Bringing together the literature on regulatory governance and the welfare state, this article compares regulatory regimes that prevent loss of access to services in the UK, Sweden, and Israel in housing credit, electricity, and water, as well as to the electricity and housing credit sectors in the EU, from the early 1990s to the 2010s. The article finds that regulation to address this issue was introduced in all but the Swedish cases. This highlights the significance of the welfare state context in addressing these issues through regulation, as more residual welfare regimes are associated with more social protection through regulation.

What does the state do when consumers cannot or do not pay their bills? How are people protected from losing access to crucial services, such as electricity, water, or mortgaged housing, once they face debt and arrears? These questions have far-reaching social, political, and economic impacts, as could be seen, for example, in the 2008 global financial and housing crisis, or following the economic hardship resulting from the COVID-19 health crisis. They also pose a theoretical challenge to the literature on the modern capitalist state: the literature on social protection and on regulation of economic reform has generally overlooked these questions or offered an expectation of little or no policy to address such issues.

Scholarship on regulation has described a shift from state involvement in the economy through state ownership to regulation of liberalized markets, occurring in Europe and elsewhere since the late 1970s. This has been dubbed the transition from the positive state to the regulatory state (Majone 1997, 2011). In this view, the regulation of markets is aimed at enhancing economic efficiency, while questions of social protection and distribution, previously addressed politically or administratively under a state ownership regime, are now framed out of the design of regulation and regulatory agencies. This view suggests a normative, as well as an empirical, expectation for regulation to focus on addressing market failures, not economic hardship.

A similar expectation for little regulation addressing these types of issues arises from the literature on the welfare state. While regulation has always been part of social protection (e.g., through the regulation of the labor market), it has not been as central as social spending and insurance in the study of the varieties of welfare capitalism and the discussion of welfare state retrenchment and austerity (Esping-Andersen 1990; for an overview see Arts and Gelissen 2002; Danforth 2014; Pierson 1994; Jensen, Wenzelburger, and Zohlnhöfer 2019; Pierson 2001). When regulation is discussed in the context of social provision, it usually focuses on regulating the provision of public and privatized social services, such as education or health, rather than on the social aspect of market services, such as utilities.

What is lacking from these common understandings of the role and limits of regulation is the study of the social aspects of regulating market services. This goes beyond the welfare state’s focus on decommodification in the labor market, toward at least partial decommodification of access to services or goods in markets. It also goes beyond the well-established role of regulation in consumer protection, toward protection of those who cannot afford to be consumers. This is regulation not of market failure, but of a failure in the ability to participate in markets.

The study of regulatory welfare has increased in recent years, including the study of such areas as electricity, water, housing credit, rail, pension fees, public procurement, and immigration. Research has detailed the manner in which regulation is being used for social purposes in economic sectors (Haber 2011, 2015, 2018; Leisering and Mabbett 2011; Mabbett 2013; Levi-Faur 2014; Pflieger 2014; Benish, Haber, and Eliahou 2016; Haber, Kosti, and Levi-Faur 2018; Eckert 2017; Hartlapp 2020; Trein 2020). However, we still require a comprehensive view on how regulatory regimes in different countries and sectors address these issues, as well as the drivers of these types of policies.

To address the question of how such regimes of regulating-for-welfare (Haber 2011) develop, this article compares the regulatory regimes for social protection in the electricity sector and in housing credit in the UK, Israel, and Sweden from the 1990s to the 2010s, with additional comparisons made to the residential water sector in these countries, and to the electricity sector and housing credit at the European Union (EU) level. The article argues that existing institutions and policy context are driving (or inhibiting) the development of regulatory welfare policies. The development of regulatory welfare was an addition to existing social and economic settings, and specifically to existing policies and institutions of the welfare state. The development of regulatory welfare is thus dependent on, but also contributes to, how citizens are already protected from social risks.

The research design is a compound, comparative medium-N design (Levi-Faur 2006), allowing for comparisons across several different dimensions of interest: across the same sector in different countries, between different sectors in the same country, and across different sectors in different countries.

The case choice represents an effort to maximize relevant dimensions of both similarity and difference of both regulatory and social policy. In the case of electricity, reform occurred in the mid 1990s, including the liberalization of the sector, the creation of independent regulatory agencies, and efforts toward marketization of national providers. In the housing credit sector, the similarities lie in high rates of homeownership and a prominent role for the state in encouraging private homeownership as the dominant form of tenure. At the same time, the cases represent different models of welfare states, from a Social Democratic model (Sweden), to a Liberal model (UK), to a hybrid model (Israel), to no welfare state (EU). This can also be seen as a distinction between an institutionalized model of the welfare state, as in Sweden, to a more residual model, as in the UK and Israel. 1

The findings show that the most consistent variation between the cases is at the country, rather than the sector, level. Regulatory welfare, or regulation and other types of policy addressing service termination, developed in Israel, the UK, and the EU, but not in Sweden. This finding supports the claim that national-level context matters for the development of regulatory welfare, as more residual welfare regimes are associated with more social protection through regulation. The findings do not seem to offer similar support for alternative explanations, such as a left-right partisan divide, social need and focusing events, interest groups, or the power of ideas.

Explanatory Framework

This article asks how consumers are protected from losing access to basic services such as electricity, water, and repossession of mortgaged housing due to economic hardship, debt, and arrears across different national contexts.

However, the literature and practice of creating regulatory regimes as part of the “rise of the regulatory state” do not support an expectation for a regulatory response to social hardship. This is because of the focus of regulatory agencies on the correction of market failures, and on structuring these regimes and the regulatory agencies that oversee them as autonomous from political actors and pressures (Majone 1994, 1997, 2011).

In such regulatory regimes, we expect little scope for addressing social issues. Indeed, we might even expect regulation to formally bar social considerations from setting tariffs or providing services, as was the case, for example, when the electricity sector in Israel was initially reformed (Haber 2011). At the same time, the formal independence of regulators means that even if political pressure to address social needs might develop, there would again be little recourse for addressing these issues within these regulated sectors, as regulators were intentionally placed at arm’s length from their political principals.

The focus on market failures should not be seen just in terms of their formal effect on legislation or market structure, but also as a normative reference point for regulators and other actors in the sector. The principles of welfare economics and Pareto efficiency might be expected to inform, in this view, not just the actions but the worldviews of those involved in regulation, informing what is through a shared understanding of what ought to be. 2 The question is, then, despite these expectations, why might regulation still develop to address such issues? Below, several different types of explanations or possible answers to this question are briefly discussed.

Social needs and focusing events

First, the more severe social issues or needs are, the more likely it is that regulators and policy-makers may be prompted to react. This type of answer to the question of why such regulation develops sees policy-making as a more or less rational process of problem-solving, following from a functionalist view of social policy-making (Midgley 1986). This view can be seen as dating back to Karl Polanyi’s “double movement,” as economic liberalization is followed by a demand for social protection from the effects of liberalization (Polanyi 1946). In this view, we might expect more severe social issues to be more likely to be met with a policy response.

What might draw policy-makers’ attention to social needs are focusing events, such as economic crises or natural disasters. Such events not only highlight policy problems to policy-makers, but also mobilize those affected or those who aim to represent them, also opening opportunities for policy change (Birkland 1998).

Party politics and political actors

Even given the existence of social problems within a sector, we might expect party politics to play a role in the extent and type of regulation and policy put in place, either through the political policy-making agenda or through pressure or influence on delegated rule-making by independent regulators. Broadly, a partisan view expects social policy to be expanded by the political Left, in line with the interests of these parties’ voter base. As the power resource approach argues, the relative strength of organized labor and the political Left is the leading determinant of the extent of social policy (Korpi 1983; Schmidt 1996).

Ideas and policy diffusion

A perspective focused on the role of ideas (Béland 2009; Blyth 2013) would argue that ideas about the appropriate use of regulation—in this case, market failure rationales of regulation, as well as perceptions of acting in the public interest through maximizing economic welfare in aggregate (pursuing Pareto efficiency), rather than addressing the specific needs of one group or another (Majone 1997, 2011)—are found not only in regulation text books, but also in the manner in which regulators and economic reformers perceive their role. These perceptions can be expected to hinder regulation, which impedes efficiency or addresses the needs of a specific social group, for example by cross subsidy in prices.

Conversely, as the use of regulation as a form of social protection occurs, the manner in which it has been implemented in one sector may then play a role in introducing similar ideas about policy problems and policy solutions to other sectors, nationally and internationally. As regulation and policy regarding social hardship develops in one sector, we can expect it to be adopted elsewhere as well, offering a practical counterargument to the market failure perspective.

Interest groups

An additional explanatory perspective is one in which regulators and political actors respond to pressures from organized groups, particularly from industry. This could be because such groups pose a threat to regulatory organizations’ reputations (Carpenter 2002), or because they provide valuable resources to policy-makers, such as information and compliance.

In the context of service termination or housing eviction, a useful tool for determining the expected type of politics is the extent to which costs and benefits of regulation are allocated. In this case, one might argue that the concentration of costs to service providers, and the relatively dispersed benefits to a large number of economically vulnerable consumers, situates this type of policy under what Wilson called “entrepreneurial politics,” in which we can expect policy “heroes” to emerge and champion for a disorganized and unrepresented public interest (Wilson 1980).

Existing institutions and policy context

This perspective focuses on policies themselves: existing policies, both within and beyond the regulatory and social realms, and how these relate to the emergence of and solutions for social hardship. Existing policy is not only self-reinforcing, but it also sets the context within which new policies are made, intentionally or not. Research has argued that this constrains future policy-making, leading sectors and countries down ever increasingly self-reinforcing paths (Pierson 2000; Thelen 2003).

Thus, existing welfare policies for unemployment, pensions, and health set the backdrop within which policies regarding service disconnection or housing evictions are made. Adequate unemployment benefits may prevent service termination or repossession at an earlier stage, before this problem ever reaches regulators or service providers. This means that the welfare state impacts the way social problems develop, as well as sets the context within which further regulatory policy is decided upon.

Findings: How Does the State Address Service Termination?

Regulation and policy either preventing, delaying, or compensating for service termination due to debt and arrears exist in different forms in both electricity and housing credit in Israel and in the UK, as well as in the EU electricity and housing credit directives. Conversely, in Sweden, service disconnection due to debt and arrears may be dealt with by social services (in electricity) or not at all (housing credit) (Haber 2011, 2015). A similar picture arises when the regulation of service termination in residential water supply is compared among the three national cases.

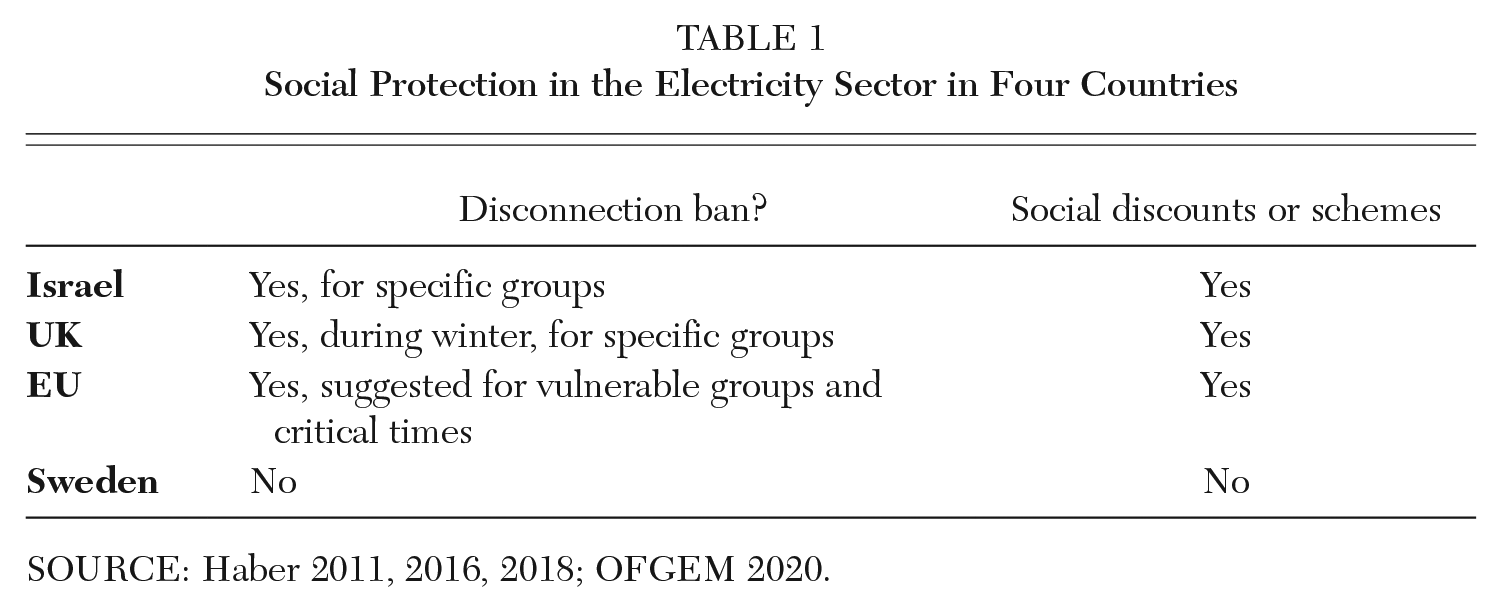

In the electricity sector in Israel, the state-owned electricity provider is required to offer a cross subsidized discount to specific groups of vulnerable consumers, such as pensioners receiving income support and people with disabilities (Haber 2016). Some of these groups are now also partially or completely protected from service disconnection (Electricity Authority 2017). 3

In the UK, the regulator, service providers, and the state are all involved in protecting vulnerable consumers, such as pensioners and people with disabilities or chronic illness, in the electricity sector. This includes social discounts, a disconnection ban during winter for specific groups, (e.g., pensioners), and a pledge by some energy suppliers “to never knowingly disconnect a vulnerable customer at any time of year” (Haber 2011; OFGEM 2020).

The EU increasingly included issues related to vulnerable consumers and “energy poverty” over time, from its first (1996) to its third (2009) directive. These changes included suggesting that Member States ban disconnection of vulnerable consumers during “critical times,” and protect vulnerable consumers through electricity-related measures or through the national social security system (Haber 2018).

Conversely, in Sweden, the protection of vulnerable consumers is left primarily to social services, rather than to the regulator or service provider. In practice, this means that social services would be notified in the case of consumer default, and may then choose to pay the debt (Haber 2011). Even after the 2009 EU electricity directive required Member States to act on behalf of vulnerable consumers and energy poverty, the regime in Sweden continued to rely primarily on social services for protecting vulnerable consumers.

Table 1 summarizes how consumers are protected from service termination in the electricity sector in Israel, the UK, and Sweden, as well as the 2009 EU electricity sector directive, focusing on disconnection bans and on social discounts or schemes to prevent or compensate for service termination.

Social Protection in the Electricity Sector in Four Countries

Source: Haber 2011, 2016, 2018; OFGEM 2020.

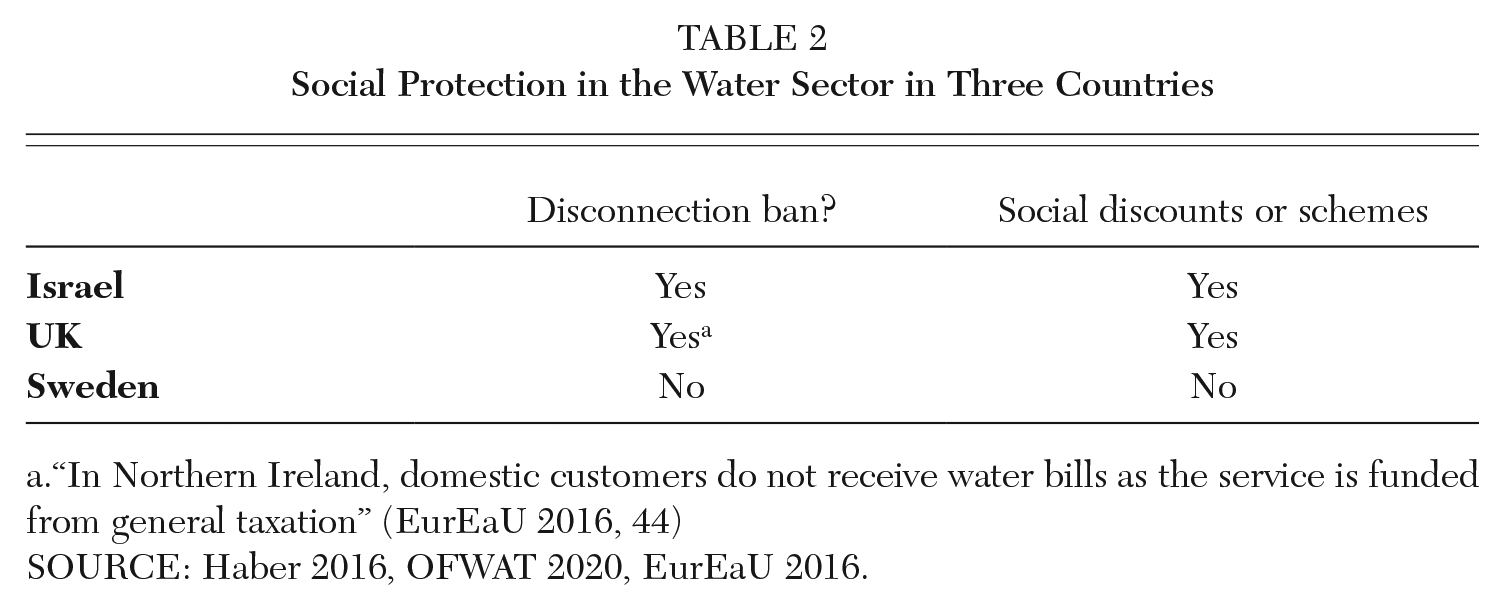

This picture is similar when compared to service disconnection in the residential water sector. In Israel, service termination due to nonpayment is forbidden, unless approved by a committee and only once the consumer’s debt has reached a certain level. This directive comes alongside a social discount for vulnerable groups, similar to those receiving discounts in the electricity sector (Haber 2016). In the UK, service termination of water at a consumer’s residence due to nonpayment is forbidden. Several schemes also exist to lower the cost of service or have the water bill paid directly from government benefits; these are again targeted at vulnerable consumers (OFWAT 2020). In Sweden, service termination due to nonpayment is permitted, unless this will result in serious harm to consumers. Service providers may reduce the flow of water, allowing for enough water for essential needs. There are no social tariffs (EurEaU 2016). Table 2 summarizes the differences.

Social Protection in the Water Sector in Three Countries

“In Northern Ireland, domestic customers do not receive water bills as the service is funded from general taxation” (EurEaU 2016, 44)

Source: Haber 2016, OFWAT 2020, EurEaU 2016.

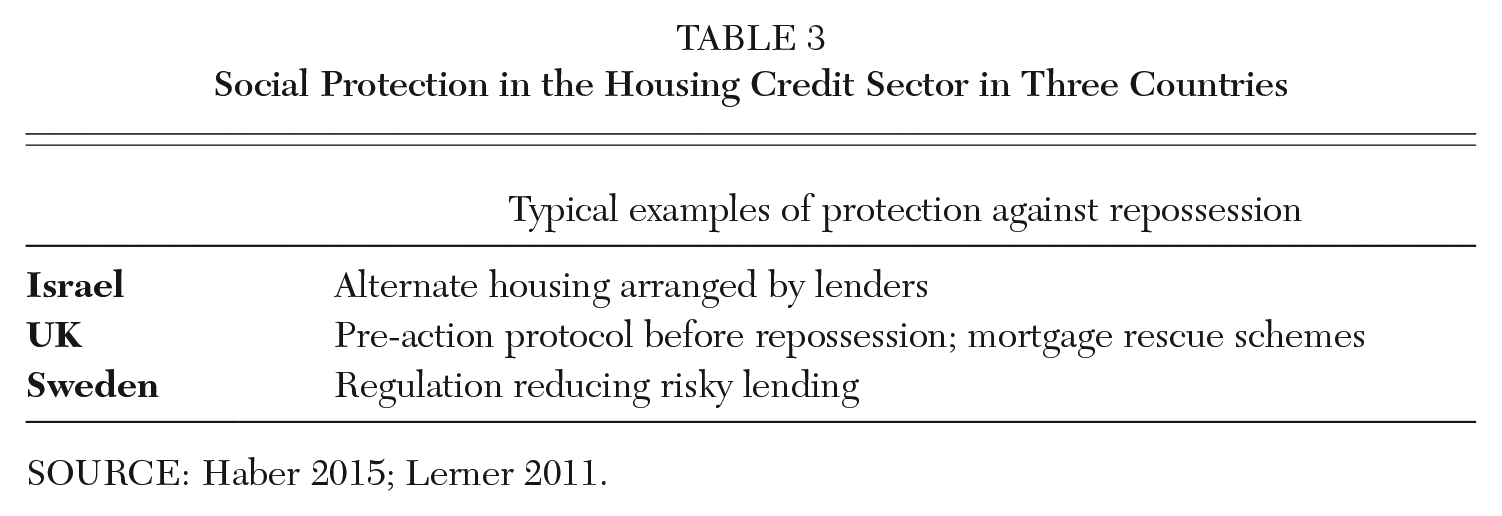

In the housing credit sector in the UK, the process of housing repossession due to debt and arrears on housing credit is regulated by a financial regulator and through a “pre-action” protocol to be followed by lenders before repossession. This process aims to ensure fair treatment of borrowers. There are also different kinds of government benefits and schemes to support mortgage borrowers, including those struggling to meet their housing credit payments. Several such “mortgage rescue” schemes, aimed at borrowers facing the prospect of repossession, were introduced following the 2008 global financial crisis; they aim to delay or prevent housing repossession. Such schemes included a variety of measures, such as loans and deferment of interest payments (Haber 2015; for current schemes see Money Advice Service 2020). 4

In Israel, legislation historically protected mortgage borrowers facing repossession, making them protected tenants of the lender, or requiring lenders to supply them with alternative housing. However, these protections were eroded over time, as clauses requiring borrowers to waive these protections commonly became part of the mortgage agreement. However, in the mid-2000s, reforms to the writ of execution law again strengthened the protection of mortgage borrowers: the first (in 2004), regulating the repossession process, prevents lenders from demanding full and immediate repayment upon default, which would result in significant losses to the borrower. The second (in 2008) requires lenders to provide a year and a half of alternative housing for borrowers facing repossession, and makes this protection one that cannot be waived (Lerner 2011).

Conversely, in Sweden, the regulation of the repossession process is relatively lighter than in the UK or Israel. The repossession process is similar to other types of property attachment (Haber 2015). It is managed by the national enforcement authority (KFM), which states that it aims to avoid repossessing one’s home, but that in some cases it has “no choice, even if the debt is small.” KFM sells the home in auction, providing some conditions are met, such as ensuring the sale of the property generates a surplus after the costs of the sale (KFM, n.d.).

A similar approach is reflected in the regulatory response in Sweden to the 2008 housing crisis, after which the financial regulator aimed to prevent excessively risky mortgage lending (for example, by limiting the maximum loan-to-value ratio), rather than preventing repossession once debt and arrears have already occurred (Haber 2015).

Thus, in the housing sector, in the UK and in Israel the state devotes more effort to mitigating the consequences of mortgage default and repossession than in Sweden. Table 3 provides typical examples of regulatory social protection in each country.

Social Protection in the Housing Credit Sector in Three Countries

Source: Haber 2015; Lerner 2011.

At the EU level, one reaction to the financial crisis has been to strengthen mortgage market regulation (Kenna 2018). This included the 2014 mortgage credit directive (2014/17/EU), 5 which requires Member States to “encourage creditors to exercise reasonable forbearance before foreclosure proceedings are initiated” (article 28). This directive was followed by guidance from the European Banking Authority on such forbearance, suggesting lenders might implement such measures as a change in the interest rate or a payment holiday (European Banking Authority 2015; for a full overview see Kenna 2018).

Summarizing the main differences between these cases, regulation and policy preventing service termination appears to vary considerably by country: while regulation addressing or even banning service termination is found in different forms in the electricity, water, and housing credit sectors in the UK and Israel, as well as in EU electricity and housing credit sectors, it is uncommon in Sweden, in which social issues in these sectors are either unaddressed or addressed by social services.

What Explains the Development of Regulatory Welfare?

Thus far, I have discussed several theoretical explanations for the drivers of regulation and social protection related to service termination. The evidence in support of each perspective is discussed in this section, which first highlights the role of existing institutions and policy context in explaining the differences among the national cases.

Existing institutions and policy context: The role of the welfare state

This explanation highlights the role of existing policy, which sets the context within which new policy is formed. Existing institutions impact the way social problems develop and set the context within which further regulatory policy is made. The consistent difference found at the country level, between Sweden and the other cases, implies that the explanation for this difference may also be found at the country level. One such common country-level contextual factor is the existing policies of the welfare state. A common factor in the UK and Israel is a residual welfare regime, which offers limited protection against the types of social risks (such as unemployment or retirement) that raise the likelihood of financial hardship that results in debt, arrears, and loss of access to market services. Conversely, the institutionalized welfare context in Sweden offers better protection against the social risks that would have otherwise resulted in consumers facing service termination.

Thus, the existing context of the welfare state in this case impacts the social problems that policy-makers face, which, in turn, impacts the extent to which they are likely to introduce regulation for social purposes, as the demand for such regulation will differ accordingly. At the same time, it also shapes the contexts within which the other explanatory factors posited above operate, such as social need, partisanship, or ideas.

That is, social need and focusing events can be expected to affect different welfare state contexts differently in how severely such social issues affect citizens, but also in terms of what is perceived as a social problem requiring public intervention and how social and economic problems should be addressed.

For example (and as I discuss further next), even while electricity prices and mortgage repossessions rose in both the UK and in Sweden, policy responses differed in the two countries. This difference may be due to how the welfare state cushioned the impact of these risks on citizens. Similarly, while ideas regarding the use of regulation strictly for efficiency purposes existed in the regulation of electricity in Sweden, Israel, the UK, and at the EU level, this principle was only fully upheld in Sweden, while policy-makers in other contexts were willing to introduce policy that did not fully follow this principle. That is, ideas about Pareto efficiency are easier to uphold when the social risks involved are already being addressed through the welfare state.

This perspective can be further demonstrated in the Swedish case, in how the EU electricity sector directives required Sweden, alongside other Member States, to take action regarding vulnerable consumers in the electricity sector. This included, for example, requiring Member States to define vulnerable consumers and take action to protect such consumers through, for example, drafting national action plans and considering bans on disconnection for vulnerable consumers during critical times. Swedish regulators were asked to transplant an existing conception of the policy problem of energy poverty, which originated in the UK policy context, through binding EU regulation (Haber 2018), even when this was not necessarily previously perceived as a policy problem in the Swedish context. However, even when this occurred, it did not necessarily change the underlying principles of the Swedish regime.

Following the directive, the electricity regulator in Sweden defines vulnerable consumers and estimates how many such consumers exist. Legislation on electricity and heating now requires service providers to follow a procedure before service can be terminated, and again stresses the obligation of providers to notify social services. However, the regulator states that vulnerable consumers are protected by social legislation that provides for their “right to receive financial assistance to cover their electricity and natural gas needs” (EI 2017). Thus, the income support benefit includes a basic national rate and “reasonable costs for other common needs such as housing and household electricity” (Socialstyrelsen, n.d.).

That is to say, even after the Swedish regulator was required to address the issue of vulnerable consumers, the regime continued to rely on social services and on the support of the welfare state as the main way of protecting consumers and funding their access to electricity. This example demonstrates the direct relation between the protection of the welfare state and social protection within the electricity sector in Sweden.

These examples demonstrate how the existing institutions of social policy impact regulation in sectors beyond the welfare state. This can occur in different ways: through reducing the impact of social risks that lead to service termination, through offering existing solutions to policy problems that occur within such sectors, or by impacting how social issues and appropriate solutions are framed and understood. As a result, countries with residual welfare states are more likely to develop regulatory welfare, while this is less likely in countries with institutionalized welfare states.

Social Need and Focusing Events

Both in the electricity and housing sectors, regulatory measures may be related to social issues and focusing events that highlighted or exacerbated them. In the UK, the death of a couple of London pensioners in 2003 after their heating was disconnected due to debt on their gas bill was cited by the UK energy regulator (OFGEM) as the cause of a later review of service providers’ conduct on disconnection, and related to a voluntary ban on disconnections during winter, which was later also mandated by regulation (OFGEM 2004). Similarly, rises in the number of housing evictions and repossessions after the 2008 financial crisis were followed by regulation and social “mortgage rescue” schemes in the UK (Haber 2015).

However, while focusing events may have prompted a regulatory response, in some cases similar policy initiatives predate the occurrence of such events. 6 For example, the UK financial regulator’s provisions on fair treatment of consumers in housing credit debt and arrears date back to 2004, and programs supporting mortgage interest payments date back to the 1990s, similarly predating the 2008 crisis. Thus, social regulation does not only follow from focusing events.

Second, the comparison with the Swedish case shows that focusing events, such as the financial crisis, may or may not elicit the same policy response. Both Sweden and the UK used macro-prudential regulation to limit risky borrowing after the crisis. But even after the number of repossessions in Sweden doubled (Haber 2015) the issues of those already facing repossession were addressed only in the UK.

A similar argument can be made about regulating in response to longer term changes in social needs in the absence of a focusing event. In the electricity sector, again, prices rose in a similar manner in the 2000s in both Sweden and the UK (Haber 2011), yet this elicited a response in the UK, but not in Sweden. At the same time, a recent example from the Israeli housing credit sector makes an opposite point: a recent piece of legislation requires banks to offer borrowers who face a sudden change in circumstances a deferral of payments for a limited time without cost. However, this measure was created despite the protests from the Israeli central bank, who claimed that repossession hardly occurs, putting the number of repossessions in the two preceding years at roughly 65 annually (Economic Committee 2017).

The connection between social needs and regulatory welfare seems, then, to be tenuous. While regulation may react to both long-term social needs and more sudden focusing events, this type of reaction does not necessarily occur, nor is such regulation necessarily a response to a clear case of social needs.

Politics and Political Partisanship

The cases above demonstrate no clear connection between the Right-Left political divide and the development (or lack thereof) in regulation for social issues. That is, the Left but also the Right enacted this type of policy, as did single-issue parties, such as religious and immigrant parties in Israel (Haber 2016). Even in the UK, where the introduction of much of these types of measures occurred under New Labour, similar measures were later introduced by conservative governments as well.

The social and economic traits of these policies do not seem to vary by partisan or ideological leaning. This type of regulation is primarily residual, similarly targeted at vulnerable groups across the different sectors in which it is has been enacted, focusing on low-income groups, such as low-income pensioners, but also groups of people with other types of vulnerabilities, such as low-income Holocaust survivors and people with specific medical conditions (Haber 2016).

Similarly, in terms of the economic efficiency of these types of policies, it is difficult to argue that parties on the Right aim only to enact policy in line with the market failure perspective: Members of Knesset (MKs) from the Likud were instrumental in mandating that social discounts be funded through electricity tariffs, rather than through the state budget. More recently, a conservative-coalition government in the UK enacted regulations that require large service providers to fund a rebate of £140 for low-income pensioners and other vulnerable groups during winter. Entitled the “warm home” discount, this measure, which has subsequently extended under conservative rule, is funded through consumers’ energy bills and has been estimated to cost each one an annual £13. The government has even set an annual “spending objective” for energy companies to meet in this scheme (Department of Business, Energy and Industrial Strategy 2018). Thus, neither the partisan affiliation of those who enact these types of regulations, nor how these types of programs are targeted or funded, seem to conform to a simple Right-Left partisan hypothesis.

However, political actors did play an important role in the enactment of these policies, often in opposition to bureaucratic and regulatory actors, as evidence shows from the Israeli and the EU cases, in which MKs and members of the European Parliament (MEPs) were instrumental in bringing issues regarding vulnerable consumers to the policy agenda (Haber 2016, 2018). This may hint at Wilson’s (1980) “entrepreneurial politics” and the role of policy entrepreneurs in advocating for this type of regulation.

The Power of Ideas

My findings show that ideas on the appropriate role of regulation, arising from a market failure perspective, and the appropriate division of labor between market regulation and social services and the welfare state play a role in preventing the use of regulation for social purposes. This is especially clear in the Israeli case, as bureaucrats, primarily from the treasury, the electricity regulator, and even from the Israeli electricity corporation all highlighted how the idea of cross subsidizing prices for vulnerable consumers from the prices paid by other consumers is detrimental to efficiency, as well as often in contradiction to existing statutes. As a representative of the service provider put it in a Knesset committee meeting: “I, as an economist, am telling you that this is wrong, it is wrong for the electricity rates to subsidize the entire country” (Haber 2011, 126).

Similarly, a recurring debate among regulators is about the manner in which social issues should be dealt with—by social services, or through the welfare state via the public purse. A recent example of this is how a representative of the Bank of Israel objected to introducing a mandatory deferral of payments for housing credit borrowers who are out of work: “We are saying that if the state wants to take care of the unemployed, it should do this directly” (Economic Committee 2017). Or as a Swedish regulator explained: “[W]e have no arrangements for people with low income. . . . We have no social tariffs in Sweden, not at all. If you cannot pay your electricity bill—if you are a poor family and need milk for your children, you cannot ask the store for a price reduction because of being poor. If you are poor, you should rely on the social welfare system, not the electricity market.” (Rubinstein Reiss 2009, 121, quoted in Haber 2011, 126)

However, the strength of such arguments was, in practice, limited, as regulation was enacted in some cases even when such arguments were raised, as can be seen in the Israeli and EU electricity sectors. However, those countering this argument often used examples from other policy sectors in which such policy has been implemented, either internationally or in other sectors in the same country.

For example, in Israel, in the discussion (already mentioned) of deferring interest payments for out-of-work mortgage borrowers, regulation of electricity and water disconnection was raised by both the representative of the banks and political actors (Economic Committee 2017). Similar exchanges occurred during the discussion of social regulation in the electricity sector, as the head of the Knesset economic committee asked “What [did] the economists at the water authority know that those at the electricity regulator did not?” (Haber 2016, 450).

Power of Interests

The evidence regarding the role of powerful interests and industry in the development of regulation preventing service termination is mixed. On one hand, while providers often objected to the social regulation of sectors, such regulation was enacted, if often in a modified form, after a process of negotiation. For example, in Israel, a final version of legislation, stipulating banks must provide alternative housing to evicted borrowers, placed the required period of alternative housing at 18 rather than 36 months, following the banks’ objections (Duanis 2008; Farkash Barouch 2009). Additionally, in the UK housing credit sector, some of the schemes protecting consumers were entered in by lenders after they received government incentives. For example, lenders agreed not to repossess mortgages of the recipients of the Support for Mortgage Interest benefit in the UK after the government agreed to pay the benefit directly to lenders (Mabbett 2011; Haber 2015).

Similarly, regulation sometimes mirrors policy already in place as commercial practice: for example, before water disconnection in Israel was banned, some providers had already ceased this practice out of commercial considerations (Haber 2016). Thus, even if industry often objected to the introduction of regulation in the first place, the policies put in place were often agreed to, similar to policies they already followed, or even favorable to the industry. Thus, industry may not dictate whether regulation occurs, but it seems to play an important role in the shape regulation takes.

Conclusion

This article asks how and why the state addresses the question of individual-level service terminations, based on evidence from a compound, comparative study of several policy sectors in different polities. These questions have significant social implications for households facing debt and arrears in these services, such as losing their homes or access to vital services. These questions also matter for markets, as losing access to such services impacts people’s ability to participate in economic life, in turn impacting service providers, lenders, and the economy more generally, as we saw following the 2008 economic crisis and the systemic impact of mortgage default. These questions also matter theoretically, for the scholarship on the regulatory state, which often assumes that regulation of economic sectors focuses on economic efficiency, and they matter for the study of the welfare state, which has typically focused on social spending.

The current study’s findings show that contrary to these expectations, in many cases, regulation was introduced to reduce and even prevent the occurrence of services termination, as well as to compensate for the social impacts of services being withdrawn due to economic hardship. The most consistent variation in the development of this type of regulation is at the national level, as it developed in Israel, the UK, and the EU, but not in Sweden. This implies that explanations based on policy context, and specifically that of differences in existing welfare policies, shape the development of regulation addressing termination and repossession due to economic hardship. This implies a substitutive relationship between welfare policy through spending to social policy pursued through regulation. Institutionalized welfare states are characterized by less regulation addressing social issues in consumer markets, while residual welfare states use more regulatory measures in this regard.

The welfare state impacts how regulation for welfare will develop within economic sectors. When compared to the residual welfare states in the study, the Swedish case demonstrates how an institutionalized welfare state mitigates social risks before they impact consumers’ ability to pay for electric power, water, or housing. The welfare state also allows regulators to rely on existing cash benefits, rather than introduce new and often less than efficient forms of regulation. At the same time, an institutionalized welfare state may also constrain the introduction of sector-level regulation through limiting what is perceived as an appropriate form and target of social policy.

What further strengthens this argument is the study’s compound research design, which highlights both within-country similarities between the different sectors, and the between-country differences, especially between the UK and Israel on one hand, and Sweden on the other. At the same time, the study shows differences between the same policy sector in different countries. These similarities and differences taken together imply that drivers of regulatory welfare should be sought out at the national level.

The current study is limited in the number of national cases, as well as by the lack of additional types of welfare states, namely conservative cases. If welfare states matter for how regulatory welfare develops, then it would be important to know how a conservative welfare state affects the development of such regulation as well as how differences between such welfare states (such as Germany or France) impact a state’s development.

The interaction between EU-level directives of the kind discussed here and subsequent regulation at the Member State–level is another driver of regulatory welfare requiring further study. Studying the impact of EU regulation on different types of Member States may also offer insight into the development of regulatory welfare and how it develops in the context of different welfare states and state traditions.

Finally, the question of fairness and efficacy of this type of social protection requires further study. The social impacts of regulatory welfare require attention, both at the individual sector level and at the national level, and beyond. How does taking regulatory welfare into account across multiple sectors impact people’s welfare, and how does it change our overall understanding of welfare efforts between different countries (Haber 2016; Howard 2007)?

This research demonstrates growth in the use of regulation for the protection of vulnerable people in markets for crucial goods and services. While theoretically unexpected and often opposed by regulators and service providers, it may be seen as part of how regulatory regimes and social protections are developing, at least in the context of residual welfare states. The study of regulation for welfare purposes matters, then, for the study of regulation of markets, showing how regulation addresses issues beyond the economic, and how it may support the functioning of markets (Haber 2011, 2018). At the same time, studying how regulation ensures access to crucial market services is important for our understanding of the welfare state and how it is changing.

Footnotes

Acknowledgements

The author would like to acknowledge the support of the British Academy for this research, as part of a British Academy postdoctoral fellowship, pf170149.

Notes

Hanan Haber is a lecturer in public management (regulation) at King’s Business School, King’s College London, and a research associate at the Centre for Analysis of Risk and Regulation (CARR) at the London School of Economics.