Abstract

This study examines the characteristics of Africa's tech sector and its implications for development. Using a database of technology firms in Africa, we show that start-ups are increasingly attracting funding across Africa, especially in underdeveloped sectors such as finance, retail, and transportation. We then illustrate that African start-ups’ digital technologies are often tailored to local contexts to attract, connect, and retain customers. Finally, we discuss transmission channels and review the existing evidence on the impact of digital technologies, particularly platforms, in Africa. We conclude that digital platforms hold significant development potential by addressing key market and government failures, as documented for the expansion of mobile money, but that the impact of other platforms, such as e-commerce, may be more ambiguous than expected. Consequently, there is an urgent need for more evidence on the impact of emerging digital technologies on African individuals, firms, and farms to guide effective policy responses.

Introduction

In recent years, several African economies have experienced a rapid expansion of their technology sectors. Across the continent, there has been a growing adoption of digital technologies in various sectors, including finance, transportation, retail, and agriculture, potentially yielding significant development gains. Many of these home-grown innovative digital products and services have been carefully adapted to the local context in which they were created, and in some cases have spread from there to the rest of the continent or even the world (Tafese, 2022). The most prominent example of an African home-grown digital technology is the invention of mobile money in Kenya, which has since spread to almost every African country, as well as dozens of low- and middle-income countries outside of Africa.

The rise of digital technologies in Africa is increasingly being driven by African tech start-ups, whose digital services and products are adapted to, and in part address, the barriers and constraints to economic development on the continent. As digital technologies fundamentally change the way African individuals and businesses work and interact across various sectors, their impact extends far beyond the narrow information and communication technology (ICT) sector. For example, a recent report by GSMA (2021), the largest industry organisation of mobile network operators, estimates that mobile technologies and services generated 8 per cent of GDP in sub-Saharan Africa (SSA) in 2021, with indirect productivity benefits in non-ICT sectors accounting for 5 per cent.

Because Africa's tech sector is developing so rapidly, and because the market and the digital services it offers are in constant flux, the characteristics of the sector are not well documented. Moreover, there is little conceptual or empirical work on the development implications of home-grown digital technologies, particularly platforms. In this analysis, we seek to fill these gaps by (1) providing a brief assessment of Africa's growing connectivity, (2) taking stock of Africa's tech sector and its key characteristics based on a dataset of African start-ups, and (3) providing a conceptual framework for the potential development impact of digital platforms in Africa and reviewing the available empirical evidence on it.

By exploring these areas, we aim to highlight the transformative potential of digital technologies for Africa's development, while acknowledging that their adoption may also create losers or cause outright harm if left unregulated. In doing so, this study draws on several strands of literature. First, it builds on conceptual and theoretical discussions at the intersection of digital technologies and entrepreneurship that gave rise to the concept of digital entrepreneurship (Nambisan, 2017; Paul et al., 2023). A recent review of digital entrepreneurship literature by Paul et al. (2023) illustrates the evolution of the concept, with more recent work emphasising how digital technologies have transformed innovation and entrepreneurship in significant ways. Second, our study adds to the literature on digital entrepreneurship in the African context. Previous work, for example by Friederici et al. (2020) and Ndemo and Weiss (2017), highlights the transformative potential of digital technologies to address infrastructure challenges, spur innovation, and drive economic growth in the region. However, these studies also point to the constraints to digital enterprises (Friederici et al., 2020) and the limits to the transformative potential of digital technologies (Ndemo and Weiss, 2017). Our study complements this body of work by providing an empirical analysis of African tech start-ups, offering a framework for understanding their role in addressing key market and government failures, and focusing on the specific development impacts of digital platforms.

The Backbone of Africa's Tech Sector: Growing (Mobile) Connectivity

Connectivity is an important prerequisite for the development and application of digital technologies. Over the past two decades, Africa has become increasingly connected as more Africans have gained access to the internet and mobile phones. This increasing connectivity is largely due to investments by the major telecom companies (“telcos”) operating in Africa – notably MTN, Orange, Vodacom/Vodafone, and Airtel – which have rolled out their broadband networks across the continent. These investments, particularly in mobile broadband, have led to significant improvements in internet access and mobile phone adoption in Africa over the past two decades. As of 2020, a total of 30 per cent of sub-Saharan Africans used the internet, compared to only 6 per cent in 2010 and 1 per cent in 2000 (World Bank, 2022a). Over the same period, the number of mobile cellular subscriptions per 100 people increased from two in 2000 to forty-five in 2010 to eighty-three in 2020. Importantly, a growing literature has shown that the expansion of digital infrastructure has already had considerable employment and income effects (Deichmann et al., 2016; Hjort and Poulsen, 2019; ITU, 2019; Ndubuisi et al., 2021). 1

However, despite these gains, Africa still lags far behind the global average of 85 per cent internet usage and 106 mobile phone subscriptions per 100 people. In addition, significant digital divides remain between and within African countries, which is reflected in the disparities in (1) internet usage and mobile phone adoption across the continent, and (2) the cost of accessing the internet. For example, internet usage is as high as 58 per cent in Ghana but only 14 per cent in the Democratic Republic of the Congo (DRC), and the number of mobile cellular subscriptions (per 100 people) for the same two countries is 130 and 46, respectively. Similarly, the cost of 1 GB of data is about 2 per cent of the average monthly salary in Ghana and 30 per cent in the DRC (ITU, 2020). Much of this disparity is due to the geographic location of African countries, as subsea internet cable landing sites and data centres naturally favour countries on the coast. The lack of terrestrial (or inland) cables to provide “last-mile” connectivity to households and businesses has also led to digital divides within countries, as metropolitan areas often have much better access to the internet than secondary cities and rural areas.

While connectivity gaps between and within countries remain, they are likely to narrow in the coming years as multi-national tech giants have identified the largely untapped African market as a huge investment opportunity. Two prominent examples are Google's and Meta's respective investments in the Equiano and 2Africa subsea cables. While the Equiano subsea cable has just become operational, the 2Africa cable is expected to become operational in 2025. Both cables are expected to significantly increase overall total network capacity, internet speed and penetration in Africa, and to cut the cost of internet access.

The Rise of African Tech Start-ups

Enabled by enhanced connectivity, a new wave of digital tech companies has emerged in many African countries in recent years. This new wave of tech start-ups – defined as start-ups that focus on developing and bringing to market innovative technology-based products or services – is growth-oriented and, unlike the small and mostly informal businesses typical of Africa, needs significant investment even in early stages. Local and international investors – primarily venture capital firms, but also large tech firms and development finance institutions – have recognised the potential of African tech start-ups and have massively increased their early-stage investments in them, making the African tech ecosystem one of the fastest growing start-up ecosystems in the world. At the time of writing, eight African tech start-ups had already achieved “unicorn” status, meaning a valuation of more than USD 1 billion, and tech or tech-enabled start-ups are among the fastest growing companies in Africa (Financial Times, 2022), increasingly reaching market sizes and valuations similar to the incumbents in the sectors in which they operate.

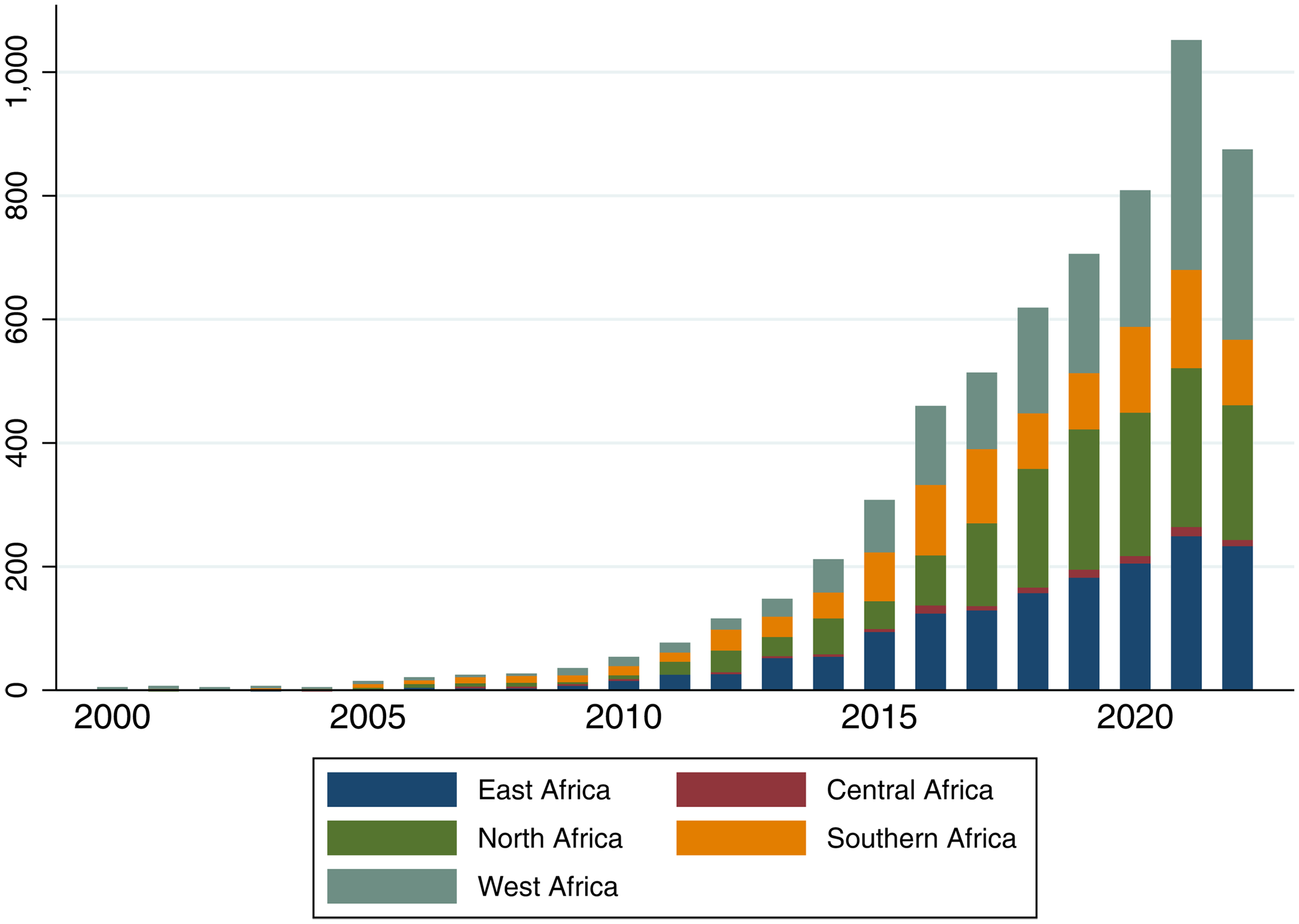

The increasing dynamism of the African tech ecosystem is reflected in the rising number of venture (capital) funding 2 rounds for African start-ups over the past two decades, as shown in Figure 1 using data from Crunchbase (see the Appendix for details on the Crunchbase database). Venture funding is a good indicator of the dynamism of a tech ecosystem, as it primarily targets tech start-ups. In the first decade of the century, the number of venture funding rounds was negligible, but this changed dramatically in the second decade, when the number of rounds increased rapidly and exceeded 1,000 for the first time in 2021. Figure 1 shows that of Africa's five regions, West Africa has experienced the strongest growth in venture funding rounds, especially in recent years, closely followed by East and North Africa. Southern Africa, on the other hand, saw a larger increase in earlier years but has recently stagnated, while the numbers in Central Africa have remained negligible.

Number of Venture Funding Rounds by African Start-ups across Regions, 2000–2022. Source: Authors’ own construction from data from Crunchbase. Note: See Footnote 2 for the type of financing included in venture funding.

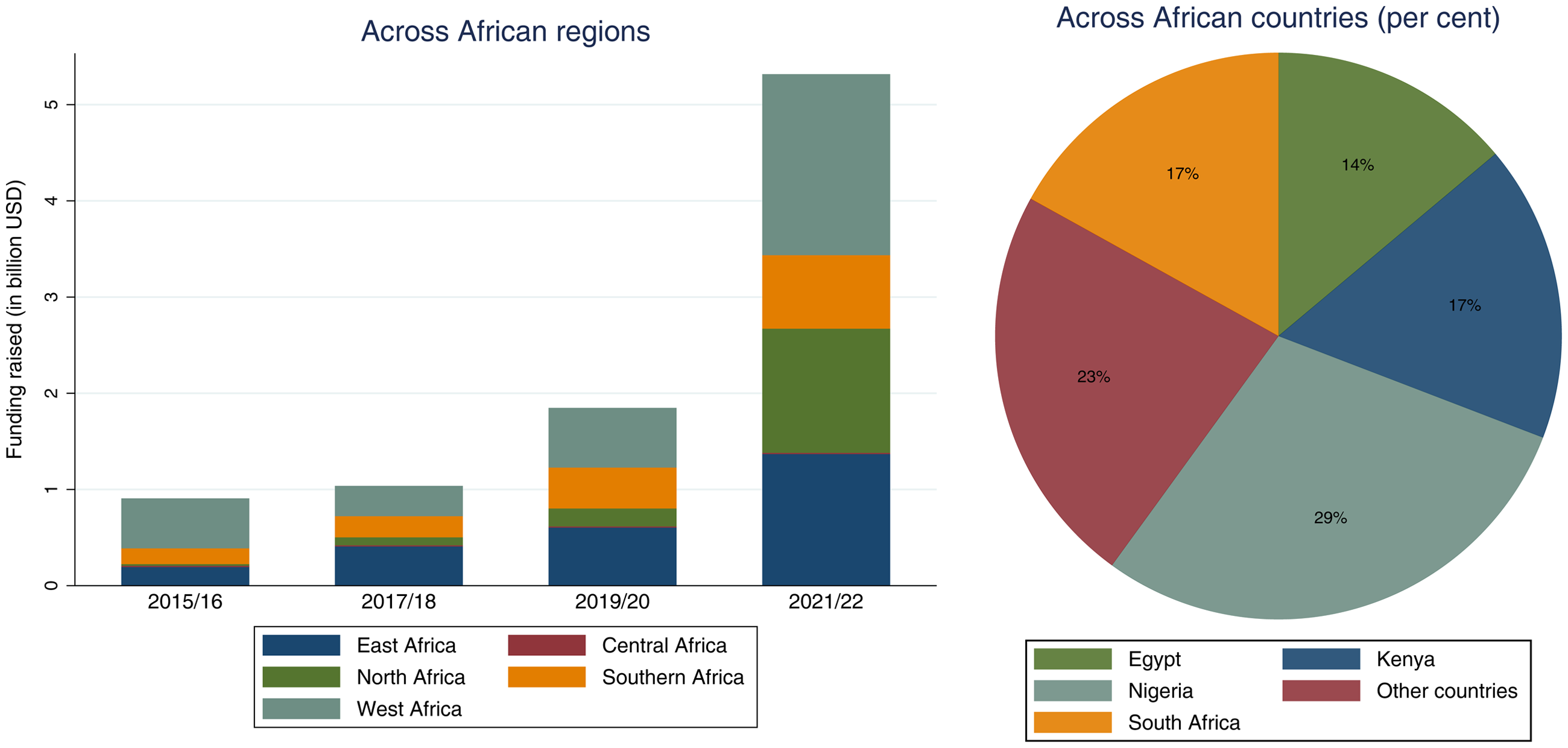

Consistent with the overall increase in the number of venture funding rounds over the past decade, the left bar graph of Figure 2 shows that the amount of funding raised by tech start-ups – here companies founded in 2010 or later 3 that received venture funding – has also increased significantly, especially very recently after the 2020 pandemic outbreak. In West, North, and East Africa, funding volumes raised over two years are well above USD 1 billion. These include domestically raised funding and foreign investment from within and outside Africa (Michael, 2022). 4 To put these figures into perspective, note that net Foreign Direct Investment (FDI) inflows into Nigeria were USD 3.3 billion in 2021 and about USD 500 million in Kenya, compared to around USD 980 million and USD 200 million in funding, respectively, raised by Nigerian and Kenyan tech start-ups in 2021. 5 Tech start-ups from West Africa are clearly in the lead, having attracted the lion's share of funding, followed by East African tech start-ups, which are roughly on par with their West African counterparts. Similarly, North African start-ups increased their funding by several orders of magnitude in 2021/2022, while funding for Southern African tech start-ups increased more moderately and remained negligible for Central African start-ups.

Funding Raised by African Tech Start-ups, 2015–2022.

However, in each of the four regions where funding increased, a single country accounted for the vast majority of funding: Egypt in North Africa, Kenya in East Africa, South Africa in Southern Africa, and Nigeria in West Africa. Because of their dominance in Africa's tech ecosystem, these countries are often referred to as the “Big Four.” In fact, the Big Four have attracted more than 75 per cent of the total funding for start-ups in Africa between 2015 and 2022, as shown in the right pie chart in Figure 2. Within the Big Four, funding is highly concentrated, with most of it going to start-ups based in the urban centres of Lagos (Nigeria), Nairobi (Kenya), Cairo (Egypt), and Cape Town and Johannesburg (South Africa). These urban centres are also the most developed start-up ecosystems on the continent according to a 2022 ranking from StartupBlink (2022). Factors that make these locations particularly attractive destinations include the size of the home country's economy, the regulatory environment, the development of digital infrastructure and technology adoption, and the level of digital literacy. 6

Recent data from 2023 suggest that start-up funding has fallen by around a third from 2022 to 2023 (Disrupt Africa, 2023). However, this decline is not specific to Africa but reflects broader global economic trends, largely influenced by the monetary tightening in the West, which has impacted investor behaviour globally. In particular, rising interest rates in the United States and the associated increase in the cost of capital have led to less funding for African start-ups, as the majority of investors are from the United States. Still, the number of funded ventures and total funding has increased by several orders of magnitude since 2015. While it may take some time for funding to fully recover, as investors now emphasise profitability over growth, the fundamental drivers that have made African start-ups attractive – such as increased connectivity, growing technological adoption, a young and increasingly urban population, and significant market gaps in critical sectors (more below) – remain strong. In fact, the shift in investor focus from pure growth metrics to profitability may lead to a healthier, more sustainable, and resilient start-up ecosystem in the long run, which will attract more long-term investments. 7

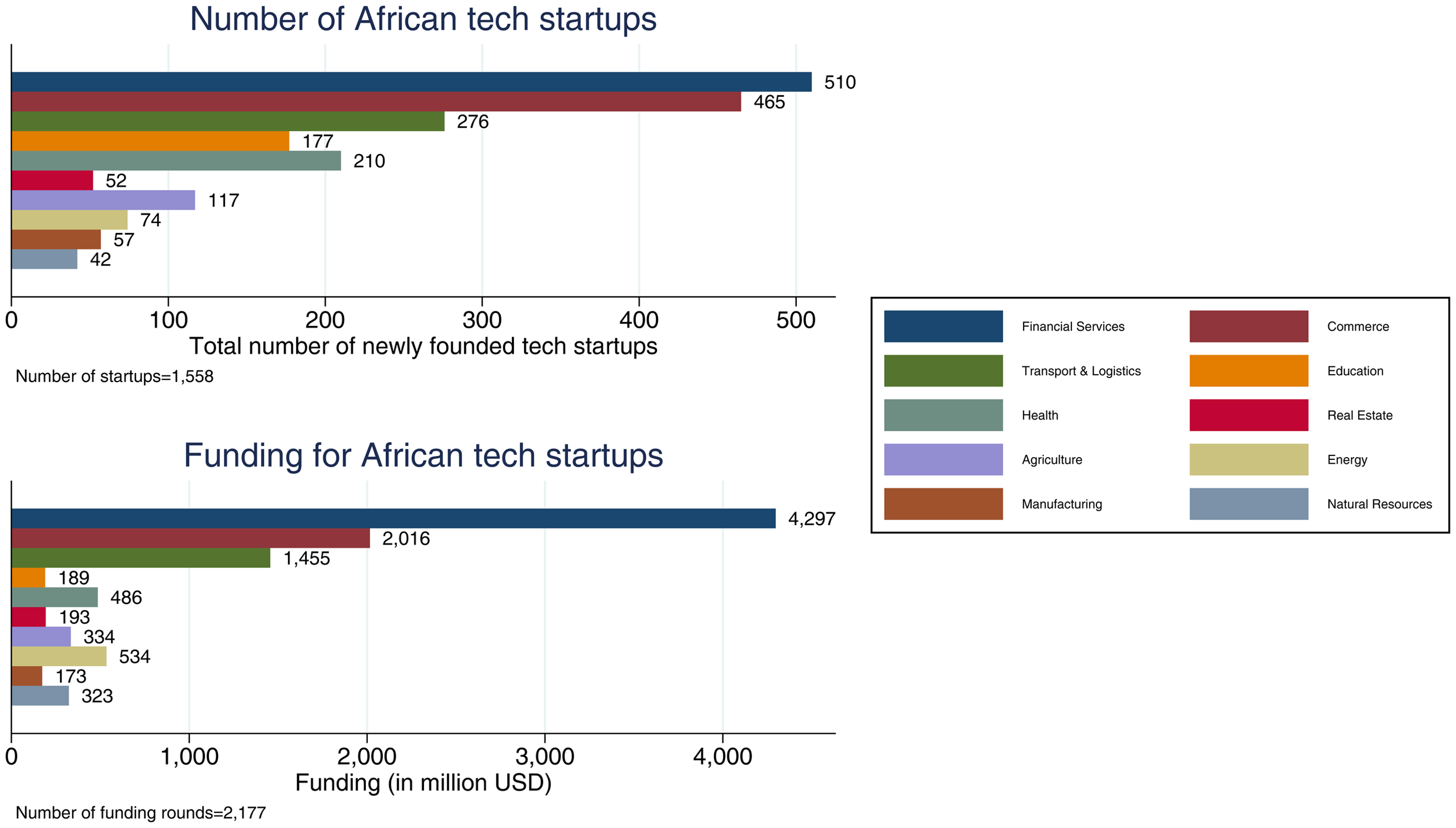

Many of Africa's tech firms can be found in sectors that remain underdeveloped and that have often been identified as obstacles to economic development. These include first and foremost the financial sector, but also trade and commerce, as well as the transport sector. Financial services tech (fintech) start-ups clearly lead the way, both in terms of their number and the funding they attracted between 2015 and 2022. With more than 510 new fintech start-ups created (top panel, Figure 3) and more than USD 4 billion in funding attracted (bottom panel, Figure 3), fintech start-ups have clearly outpaced tech start-ups in all other sectors. Most fintech start-ups use technology to deliver financial services, such as mobile applications, application programming interfaces, artificial intelligence, blockchain and cryptocurrency, and data analytics. Using such technologies has allowed some of them to grow rapidly. Of the current seven African unicorns, six are fintech start-ups. One of the main reasons for the dominance of fintech start-ups is that they usually pursue asset-light business models, which in principle allow them to scale and become profitable more quickly. 8

Number and Funding of African Tech Start-ups for Top Ten Sectors, 2015–2022.

After financial services, the most popular sector for investment in African tech was the commerce sector, with 465 new tech start-ups created since 2015 (top panel, Figure 3) and more than USD 2 billion in funding raised (bottom panel, Figure 3). Most tech start-ups in this sector use e-commerce business models, which have at their core a platform that connects buyers and sellers and, to varying degrees, also organise the logistics between the demand and supply sides. Other tech start-ups in the sector offer technology-based management solutions for businesses, such as app-based bookkeeping, as well as customer, store, and sales management tools.

Aside from tech start-ups in the financial services and commerce sector, only tech start-ups in transport and logistics were able to raise more than USD 1 billion. Tech start-ups in this sector include urban ride-hailing start-ups – which cater to individuals in African cities – and end-to-end logistics start-ups – which organise and implement the logistics and warehousing of goods for businesses. The remaining sectors in Africa's top ten in terms of start-up activity are more nascent and have not yet reached the same levels of start-up funding and digital technology penetration. 9

Business Models of African Tech Start-ups

Start-ups in Africa's tech sector can be broadly divided into those that primarily serve individual customers (B2C) and those that primarily serve businesses (B2B) with their products and services. Both types of models can be found in Africa. While this is typical of businesses elsewhere, we will now focus on three specific aspects of tech start-up business models that are particularly relevant in the African context, highlighting the roles played by (1) platform businesses, (2) embedded services and products, and (3) agent-based models. 10

Platform Businesses

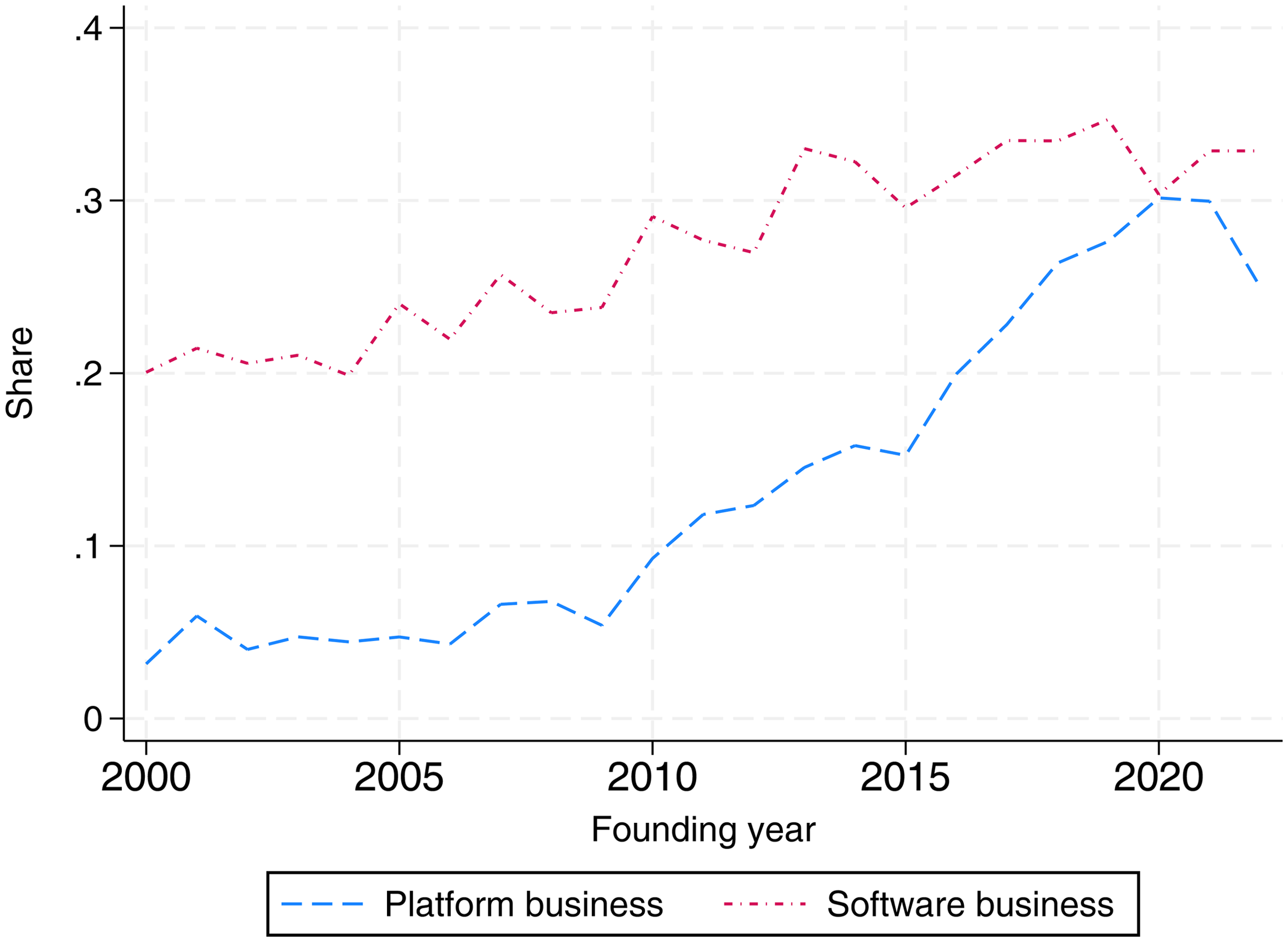

Digital platforms bring together different market actors in order to distribute or exchange products, services, and information. They have become ubiquitous around the world (ILO, 2021) over the past decade, including in Africa. Since 2000, the share of African platform businesses in all businesses has grown from less than 5 per cent to about 25 per cent in 2022, as shown by the dashed blue line in Figure 4. In fact, comparing the dashed blue and yellow lines shows that the share of platform businesses in software businesses in Africa has grown rapidly over the past decade. The expansion of platform businesses has been driven by increases in all major sectors, particularly in the commerce and transport and logistics sector, where platform businesses have accounted for between 40 per cent and 60 per cent of newly founded businesses in recent years (Figure 1A in the Appendix). It is therefore important to note that platform businesses come in different types due to their sectoral focus and are often classified according to their main purpose. 11

Share of African Platform and Software Businesses, 2000–2022.

The rapid expansion of platform businesses in Africa coincides with, and has been mainly driven by, the increasing availability of venture capital for growth-oriented tech start-ups since the 2010s (see Figure 1), 12 as well as the expansion of mobile networks and the proliferation of mobile phones. The popularity of platform business models, particularly among venture capital firms, stems from their growth potential due to network effects and their “asset-light” nature, meaning that they typically require little or no investment in traditional capital assets – such as cars, machinery, or buildings and warehouses – as the key function is to connect the supply and demand sides on the platform, who make the investments themselves. Importantly, while many African tech start-ups start out as pure asset-light platform businesses that simply connect the demand and supply sides, after a while many realise that they need to invest in other upstream or downstream parts of the value chain – that is they integrate vertically – to improve their service or product. As a result, many tech start-ups end up as “asset-heavy” companies, even though they started out with “asset-light” business models. 13

Embedded Services and Products

Another related key feature of Africa's tech sector is that many start-ups offer products or services in more than just one sector – that is they integrate horizontally – to retain or capture more value from customers (World Bank, 2022b). It is common for African tech start-ups that have built a relationship with their customers around a core product/service in one area to leverage the existing relationship with customers, including data on them, to offer additional complementary products/services. As a result, customers, who may be individuals or businesses, may be able to access products/services to which they would not otherwise have access.

In particular, financial services such as payments, lending, and insurance, which are traditionally offered by banks and other financial institutions, are often embedded by non-fintech start-ups in their non-financial apps and platforms. For example, the platform businesses Wasoko, mPharma, and Twiga all offer their customers – retailers, individuals, and smallholders, respectively – short-term financing through “buy now pay later” services, in addition to simply connecting them to the other side of the marketplace. To monetise their existing customer relationships, several tech start-ups such as Safeboda, Opay, MNT-Halen, and Yassir are even developing into so-called super-apps that offer or facilitate a wide range of products and services to customers (Mastercard, 2021).

Agent-Led Business Models

Finally, agent-led business models have been at the heart of many of the African tech success stories. Through large networks of agents who are well known and well trusted in their local communities, tech start-ups are thus able to onboard new customers and provide them with products and services. This business model therefore solves the key challenge of serving the so-called last-mile – individuals, smallholders, or retailers who are difficult to reach through traditional sales and advertising channels, for example because they live in remote rural areas or informal settlements, and/or are not online.

Without agent-led business models, Africa's mobile money revolution probably would not have occurred. The mobile money platform M-Pesa, for example, relies on a network of more than 600,000 mobile money agents in both rural and urban areas to enable customers to easily deposit into and withdraw money from their mobile money wallets wherever they live. More recently, fintech start-ups such as Wave and Kuda Bank have built huge agent networks, often comprising thousands of people, to deliver their mobile money and other fintech services to customers. However, agent-led business models are not limited to the consumer fintech sector, as start-ups in other sectors such as retailtech and agritech have similarly used large networks of thousands of agents to bring new smallholder farmers and retailers/vendors onto their platform and offer various products and services through them.

Development Implications of Africa's Emergent Tech Sector

The rise of “home-grown” digital technologies by African start-ups with locally adapted business models is taking place in an economic environment that is still characterised by mostly small-scale and informal agriculture and services and an immature state of manufacturing in Africa. 14 As such, digital technologies are most likely to drive “leapfrog development” and thus improve people's livelihoods by addressing key market and government failures that hold back Africa's agricultural and service activities. 15 In the following, we will focus on digital platforms and (1) discuss several plausible transmission channels through which they may impact on development and (2) present some early evidence on their development impact.

Transmission Channels of Digital Platforms

First and foremost, digital platform solutions can significantly expand access to a wide range of services and products, which in turn can reduce transaction costs. For example, the expansion of mobile money services across Africa has enabled millions of Africans to participate in the formal financial system, driving account ownership from 23 per cent in 2011 to 55 per cent in 2021 (World Bank, 2021). 16 Increased access is not only desirable in itself, but can also make individuals and firms much more productive, creating new employment opportunities, higher incomes, and improved living standards (Ahmad et al., 2020; Nan et al., 2020).

Second, many of the aforementioned apps and platforms address information failures and asymmetries by revealing critical information about transactions and the parties involved to both buyers and sellers (Deichmann et al., 2016). Better information can lead to more efficient outcomes, including the better use and allocation of resources. For example, through a tractor-sharing app, tractors, which have considerable fixed costs, can now be booked and used by many more farmers, making the investment in tractors worthwhile and potentially increasing the overall supply of tractors.

Third, digital services may increase the formalisation of previously informal segments of the economy. Employment through a digital platform implies that the related economic transactions leave a digital trace that could be used to integrate workers and (smaller) firms into the formal economy (Lakemann and Lay, 2019). A case in point is ride-hailing apps that usually only allow drivers to operate on their platforms if they have obtained certain licences, are registered with the tax authorities, and possess the relevant social protection. This could also lead to the modularisation and standardisation of services – similar to what has happened in manufacturing – leading to economies of scale, innovation, and productivity gains in traditionally unproductive, informal services.

Fourth, when digital solutions create digital marketplaces, they often lead to more competition and competitive prices. The impact on prices can be large when this happens in regulated sectors, such as the taxi industry. When prices fall, this is good for consumers but may hurt producers, that is traditional or “analogue” taxi drivers. Competitive pressure may also come from tech start-ups entering oligopolistic and monopolistic markets. A case in point is the French-speaking West African mobile money market, which had been dominated by telecom giant Orange until the start-up Wave entered the market with much lower prices for the same service. Typically, more efficient markets and lower prices will lead to increased consumption and more people being able to consume/have access to certain services.

Fifth – and arguably most important from a policy perspective given the continent's rapid population growth – larger markets/higher demand on digital marketplaces may generate more employment opportunities. While the direct contribution of tech start-ups to employment generation – the first-order effect – is usually negligible, the employment opportunities that arise on the supply side of platforms – the second-order effects – can be significant, with an army of workers in between wage employment and self-employment finding “gigs” on them (ILO, 2021). 17 In addition to more “gig” work, there is third-order job creation, which includes a very large number of agents who facilitate the transaction on platforms, 18 as well as fourth-order indirect job creation through increased efficiency/lower prices and/or new products/services.

While these are all plausible transmission channels through which digital technologies and services may affect economic development, the effects may not be unambiguously positive, especially on labour markets. For example, it is not clear whether digital technologies lead to net employment gains, as the first- to third-order job creation on and through platforms is not additional if individuals would have had similar “offline” jobs even in the absence of digital technologies. In fact, the broader fourth-order effects on employment and incomes of non-platform “offline” workers may even be negative due to increased “digital” competition, as illustrated by the impact of emerging ride-hailing platforms on traditional taxi industries in many economies. 19 Moreover, even when digital technologies lead to net employment gains, the additional jobs created on and through platforms may not necessarily be “decent” jobs. In fact, in almost all cases, platform workers are classified as “semi-formal” independent, self-employed contractors who receive irregular and low wages and are not protected in the event of unemployment or accidents at work (Anwar and Graham, 2021; Graham et al., 2017). 20 Therefore, rigorous quantitative studies, ideally based on (quasi-)experimental research designs, are needed to assess the net effects of digital technologies.

Evidence on the Impact of Digital Platforms

Overall, there is only limited rigorous empirical evidence on the economic impact of digital platforms – be it on productivity, employment, or living standards – in Africa. Probably the main reason for this is that digital platforms, increasingly driven by tech start-ups, have only recently taken off in Africa, as shown in Figure 4. A notable exception, however, is research on the impact of mobile money platforms, which have already been around since 2007, when M-Pesa was launched by Safaricom, Kenya's largest telco, followed by the proliferation of mobile money platforms developed by other major telcos in other markets.

Early evidence from Suri and Jack (2016) suggests that the impact of M-Pesa in Kenya, where it has more than 30 million active users (The East African, 2022), has been enormous, lifting approximately 2 per cent of Kenyan households out of poverty. According to the authors, the platform achieved this by formalising the financial arrangements of previously unbanked households and integrating them into the formal financial system. Specifically, M-Pesa has increased households' financial resilience and savings, and improved labour market outcomes for individuals, particularly women, by enabling them to transition from agricultural to non-agricultural employment. A review by Aron (2018) concludes that there is robust evidence that mobile money fosters risk-sharing. She argues that the evidence on the positive welfare impacts, including higher labour market incomes and higher savings, is less convincing (Aron, 2018). Accordingly, Suri and Jack's (2016) findings on M-Pesa's impact in Kenya have recently been challenged due to important omissions and errors in their analysis (Bateman et al., 2019). Overall, however, there is growing evidence of the positive socio-economic impacts of mobile money in African countries where it is present (Ahmad et al., 2020; Nan et al., 2020).

While similar rigorous quantitative evidence on the impact of other digital platforms – be the other fintech, e-commerce, or transport-tech technologies – is much scarcer, some lessons can be learned from other places. For example, the expansion of e-commerce in China and the United States teaches us about the potentially ambiguous effects of digital platforms and that they are unlikely to be a panacea for development. For example, Couture et al. (2021) found no broader effects on labour supply (measured as hours worked), annual and monthly income, or local store prices 21 in randomly selected “treated” rural villages in China that were connected to an e-commerce platform between 2014 and 2018. Similarly, Liu et al. (2021) find that the adoption of e-commerce by Chinese apple farmers led to only moderate gains, as higher selling prices for farmers on platforms were partially (though not entirely) offset by higher marketing costs. For the US case, Chava et al. (2023), even find negative effects on retail workers’ wages, as well as on retail sales and employment in counties where e-commerce fulfilment centres have been established. Importantly, many of these findings are in contrast with existing case studies, which tend to show only the positive effects of digital technologies, highlighting the need for rigorous quantitative studies to inform appropriate policy responses.

Finally, evidence from the United States suggests that a small number of high-growth start-ups – so-called gazelles – contribute disproportionately to job creation, output, and productivity growth (Haltiwanger et al., 2013, 2017). Moreover, in the US economy, start-ups have been shown to play an important role in the reallocation of labour from low-growth to high-growth firms across sectors, that is the process of structural transformation (Dent et al., 2016). Particularly in Africa, with its large gap between the formal and informal sectors, the direct contribution of start-ups to economic development through employment, output, and productivity growth, as well as accelerating structural transformation, can be substantial. However, the increase in venture capital funding for start-ups can also have downsides. Kwon and Sorenson (2023) have shown for the United States that this has led to a “Dutch Disease” phenomenon, where the booming tech sector in Silicon Valley has led to increased demand for local non-tradable goods and services but has reduced the number of firms and employment in the non-high-tech tradable sector in the region, as it attracts most high-skilled workers and venture funding. These structural changes have also increased inequality in the region. It is conceivable that such a mechanism could be even more pronounced in Africa, where the gap between large urban centres and semi-urban or rural areas is already very wide.

Conclusion and Outlook

Digitalisation is gaining momentum in Africa, with significant improvements in Africa's digital infrastructure and a vibrant start-up ecosystem transforming large parts of African economies in recent years. Based on a database of African start-ups, this study shows that digital technologies, and digital platforms in particular, are increasingly attracting large-scale funding in key sectors in a growing number of African economies, particularly the “Big Four” – Egypt, Kenya, South Africa, and Nigeria. Our review of business models of African tech firms shows that they are adapting their services to the African context, and in doing so, they are – to some extent – different from solutions elsewhere, with asset-heavy platform businesses, embedded services, and large agent networks playing a key role in attracting, connecting, and retaining customers.

Most African start-ups are found in the financial services, retail, and transport sectors, which are characterised by low productivity and high degrees of informality. By addressing some of the key market and government failures that hold these sectors back, digital technologies from African tech start-ups can have transformative impacts on individuals, firms, and farms beyond the specific tech start-up, potentially leading to broader employment and productivity gains and ultimately living standards. While rigorous empirical evidence on the expansion of mobile money in Africa clearly demonstrates the potential of digital technologies for economic development on the continent, our knowledge of the impact of other, more recent digital technologies in Africa is still very limited. Indeed, early evidence on the impact of e-commerce expansion in China and the United States, for example, suggests that the impact of some digital technologies may be more ambiguous than expected, as increased competition may also create losers.

Government policies play a critical role in shaping the growth and impact of digital technologies in Africa. Several African countries have taken proactive steps to encourage local entrepreneurship and technological innovation by enacting, or planning to enact, start-up acts that aim to streamline the process of starting, operating, and scaling businesses by providing clear investment standards and financial incentives for young companies. 22 On the other hand, African policymakers and regulators have recently investigated tech giants for anti-competitive practices against their smaller local competitors that could stifle innovation, and have scrutinised unregulated technologies that could harm consumers, such as predatory lending by digital lenders. 23

While these policies are crucial, more empirical evidence is urgently needed to understand why certain technologies are adopted and achieve scale but not others. Here, future work should investigate the contribution of different enabling factors, such as market size and the regulatory environment, including those factors that shape the availability of both domestic and foreign start-up funding. In addition, it is pertinent to better understand the differential impact of digital technologies on individuals, firms, and farms. Such knowledge is very policy-relevant, as it may allow us to identify those policies and development interventions that both anticipate and prevent potentially harmful impacts and harness the development potential of start-ups and digital technologies.

Footnotes

Acknowledgements

The authors gratefully acknowledge funding from the Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) under the “Future of Work” programme funded by the German Federal Ministry for Economic Cooperation and Development (BMZ). This study is a product from the GIGA project “Platforms and online workers in India and Africa: Challenges and opportunities for decent work.” The opinions expressed in this publication are those of the authors. They do not purport to reflect the opinions or views of the GIZ or the BMZ.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by GIZ.

Notes

Appendix

Crunchbase database

Launched in 2007, Crunchbase is a relatively new commercial database on innovative, often venture-backed, companies from around the world. Company information in the database is compiled and curated from four main channels: (1) a large investor network of more than 4,000 investment firms that submit monthly portfolio updates; (2) community contributors such as executives, entrepreneurs, and investors who contribute to company profile pages; (3) AI and machine learning (ML) algorithms that validate the data and flag anomalies; and (4) an internal team of data analysts who manually validate and curate the company information.

Crunchbase's crowd-sourced and AI/ML-driven approach to data collection represents important innovations compared to other commercial and public data sources, making the database unique in terms of its timeliness and scope. As a result, it has become one of, if not the single-most, widely used databases in the venture capital industry. Researchers and academics are also increasingly using the database to analyse the tech/start-up world – according to Dalle et al. (2017), more than ninety scientific articles had already been published using the Crunchbase database as of 2018.