Abstract

Past research indicates that increasing the economic consequences of evaluations should theoretically discourage discrimination by making it more costly. I theorize that such consequences may also encourage discrimination in settings in which evaluators may be motivated by performance expectations, e.g., stereotypes. I explore this theory using data from an online lending platform whose loan guarantee policy reduced the potential economic consequences of using borrowers’ demographics during lending decisions. I find evidence that with the policy in place, lenders evaluated female borrowers less favorably than male borrowers. This finding is consistent with the theory that the policy discouraged performance-motivated discrimination (that driven by beliefs about performance abilities) and simultaneously encouraged consumption-motivated discrimination (that driven by a like or dislike of others because of their demographic traits). Because I theorize about underlying motives for discrimination, the insights developed here should apply to a wide range of types of discrimination that vary according to these motives, including classic taste-based discrimination, homophily-driven discrimination, statistical discrimination, and status-based discrimination. Economic consequences may therefore represent an important dynamic link between different types of discrimination.

Effective responses to discrimination and inequality are elusive, and policies designed to directly address people’s biases have generally been found ineffective (Kalev, Dobbin, and Kelly, 2006; Paluck and Green, 2009; Dobbin and Kalev, 2017). Attempts to promote a meritocratic organizational culture, for example, may paradoxically increase unequal evaluations within an organization (Castilla and Benard, 2010). Economic consequences, however, appear to be a fruitful starting point for discouraging discrimination, because many types of discrimination are essentially forms of costly consumption (e.g., Becker, 1957). If the economic consequences of discriminating are high enough, then overall discrimination should go down.

But this logic overlooks the full range of motives that can trigger discrimination. In this article I develop an argument for why economic consequences may not only be ineffective but may even encourage discrimination in many situations. This is because evaluators are often motivated to discriminate based on performance expectations, such as what type of person they believe will be a good employee or likely to repay a loan. Consequently, increasing the economic consequences of such evaluations should encourage the use of performance stereotypes. The dynamic relationship between different types of discrimination has been largely overlooked in the literature but has potentially important implications for understanding what drives overall levels of discrimination.

I develop the logic for why economic consequences should theoretically suppress forms of consumption-motivated discrimination, which is driven by a direct like or dislike of others based on demographic traits, but encourage forms of performance-motivated discrimination, which are driven by beliefs about performance abilities. For example, if evaluators believe that men and women are of different quality on average, then they should discriminate more, not less, when the consequence of choosing between the two genders is increased. This is important because a range of environmental characteristics at both the market and organizational level may encourage or discourage discrimination, including performance pay systems, insurance programs, and other mechanisms that alter the consequences of decisions for the people making them (Gibbons, 1998). When decisions involve the evaluation of other people, the economic consequences could theoretically motivate discriminatory behavior. As the economic consequences of such evaluations increase, discrimination motivated by performance stereotypes will likely rise, but discrimination motivated by consumption preferences will likely fall. As the potential consequences decrease, discrimination motivated by performance stereotypes will likely fall, but discrimination motivated by consumption preferences will likely rise.

I apply this theory to empirically investigate how lenders from an online peer-to-peer lending platform evaluated borrowers based on their gender. Existing research in the context indicates that women may be perceived as more reliable borrowers—that is, lenders hold positive stereotypes about women’s quality—yet still be penalized by various society-level taste preferences (Armendariz and Morduch, 2010). To examine how economic consequences may encourage the expression of these beliefs and preferences during the evaluation of borrowers, I leverage the historical implementation of a loan guarantee policy on the platform—what amounted to an insurance policy for lenders—which should reduce the perceived economic consequences of lending decisions. The policy should theoretically motivate less discrimination driven by performance expectations, because it makes underlying beliefs about performance ability less valuable. However, it should theoretically motivate more discrimination driven by tastes, which can now be expressed with less consequence. As a result, in this context the overall gap in how men and women are evaluated should theoretically widen in favor of men as a result of the policy.

I compare 25,440 lending decisions—i.e., the amount a lender provided to a borrower—from before and after the policy to measure this change in how gender is evaluated. I find evidence that the average size of these decisions in the pre-policy period was larger to female borrowers than male borrowers, but this effect flipped in the post-policy period. Thus, lowering the economic consequences of decisions in this market appears to have resulted in women being evaluated less favorably. But the evidence that a fixed set of lenders changed their behavior across periods is less compelling than the evidence that the effect was between lenders. This indicates that, similar to studies of discrimination in competitive markets, the dynamic between these two motives can function across evaluators.

By acknowledging an underlying typology of the motives that drive discriminatory behavior, this study draws attention to a more complex dynamic between economic consequences and discrimination: although altering consequences may discourage one type of discrimination, it may encourage another. Therefore, my research may provide guidance on how economic consequences help or hinder current approaches to anti-discrimination and diversity programs (e.g., Kalev, Dobbin, and Kelly, 2006; Paluck and Green, 2009). This study also contributes to the broader literature on evaluation processes—both the research specifically focused on discrimination (e.g., Botelho and Abraham, 2017) and the research focused on why audiences are motivated to respond to other markers of status (e.g., Simcoe and Waguespack, 2010; Kovács and Sharkey, 2014; Malter, 2014)—wherein one might expect to find that economic consequences also influence evaluations.

The Motive to Discriminate

Discrimination is defined as the unequal treatment of otherwise equal individuals based on an observable characteristic such as race, gender, class, or another demographic trait. Pager and Shepherd (2008: 182) noted that “A key feature of any definition of discrimination is its focus on behavior . . . the definition of discrimination does not presume any unique underlying cause.” Because discrimination is a behavior (unequal treatment), and that behavior may have many potential causes, a proliferation of theories have been proposed to describe and explain the wide range of discrimination that has been observed in practice. 1

Each discrimination theory focuses on evaluators who make judgments about people. In the organizational literature, these evaluators include both internal managers and external resource providers. Research shows that discrimination may be caused, for example, by people responsible for hiring employees (Fernandez and Greenberg, 2013; Fernandez-Mateo and Fernandez, 2016), by managers responsible for evaluating employees’ performance and rewards (Castilla, 2008, 2011), by external funders of entrepreneurs (Brooks et al., 2014; Thébaud and Sharkey, 2016; Greenberg and Mollick, 2017), or by upper management (Dahl, Dezső, and Ross, 2012; Carnahan and Greenwood, 2018).

Each discrimination theory also rests on an underlying motive for why evaluators would want to discriminate, and these motives take one of two general forms. The first is a consumption motive: discrimination for the sake of discriminating. The second is a performance motive: discrimination in the pursuit of a performance goal. The advantage of conceptualizing motives for discrimination at this level is that it allows one to abstract away from some of the theoretical baggage associated with specific theories of discrimination. Doing so ultimately helps facilitate predictions that apply to a broader range of discrimination theory.

Consumption-motivated discrimination is driven by a direct like or dislike of others because of their demographic traits. The most general version of this motive is found in theories of taste-based discrimination, in which the perceived cost of a decision is shifted from p to p(1+dk) based on how someone feels about specific demographic traits such as race or gender (Becker, 1957). Given a person’s discrimination coefficient, dk, they face perceived prices that are either higher or lower than the prices faced by actors who do not hold such tastes. Thus these types of discriminators are willing to pay to discriminate.

One version of consumption-motivated discrimination is nepotism (Goldberg, 1982; Bennedsen et al., 2007), which leads to a more favorable evaluation of someone based solely on a personal or kinship tie. More recent theories that explain where and why the consumption motive exists include the theory of activist choice homophily developed by Greenberg and Mollick (2017: 343), which indicates that women have a preference to help women in underrepresented categories succeed—i.e., to “help someone penetrate barriers she can sympathize or empathize with.” A taste for demographic traits is also the underlying premise of other forms of homophily-driven discrimination and, as McPherson, Smith-Lovin, and Cook (2001: 416) noted, has been theorized since ancient times: “we love those who are like ourselves” (Aristotle, 1934: 453). While these theories differ in specific cause, consequence, and context, they are unified by their reliance on a consumption motive to explain behavior: evaluators treat people differently because of a direct like or dislike for a demographic trait itself.

Performance-motivated discrimination, in contrast, is premised on explicit or implicit stereotypes about someone’s level of competence or performance ability. When evaluators want to make “good” decisions—for example, to hire competent employees, provide bonuses to the best workers, or make loans that will be repaid—they may discriminate if demographic traits influence their perceptions of quality. Many specific theories of discrimination in the organizational literature fall into the category of performance-motivated discrimination, because evaluators in markets are often tasked with making quality judgments.

A performance motive underlies the statistical discrimination models of Phelps (1972) and Arrow (1973), wherein evaluators act on their beliefs about correlations between demographic categories and other outcomes. For example, car insurance companies in the United States often charge younger male drivers more than older female drivers, because accidents have historically occurred at higher rates for the former group, and the insurer believes the correlation will exist into the future. 2 Car insurance companies do not gain personal satisfaction from treating men and women unequally but are motivated to do so because they believe it helps them make better decisions. 3

In other types of performance-motivated discrimination, the source of performance expectations may have little or no representation in reality. For example, status-based theories of discrimination are premised on the idea that evaluators will infer that someone is lower quality because they hold a trait that society collectively believes is associated with low ability. For example, “employers prefer men because cultural beliefs about the relative performance capacity of men and women bias cognition” (Correll and Benard, 2006: 111). In practice, this type of status-based discrimination can lead to the application of double standards (Botelho and Abraham, 2017). Other types of discrimination that are performance motivated include theories of attributional augmenting that explain how gender can change the weight given to other information (Baron, Markman, and Hirsa, 2001) and more generally how traits such as gender “frame” decisions that should rationally not directly involve such traits (Ridgeway, 2011). Performance-motivated discrimination does not even need to be conscious, as in the case of implicit biases that shape quality beliefs even when the person doing the discrimination might not be aware their beliefs are biased. Such biases lead to performance expectations that can be “implicit, often unconscious, anticipations of the relative quality of individual members’ future performance” (Correll and Ridgeway, 2003: 31).

While the consumption motive and the performance motive are theoretically separate, it is of course possible they exist at the same time or even influence each other across time. The question of where underlying tastes and performance expectations come from is beyond the scope of this article. However, both are typically assumed to be quite stable in the short term. For example, statistical discrimination explains performance expectations as a response to imperfect information, so behavior should be consistent absent a change in information. 4 Status construction theory provides an explanation for how status-based competency beliefs develop, whereby structural factors such as the historically unequal distribution of resources can lead some groups to be evaluated as higher quality than others (e.g., Ridgeway, 1991). Per this theory, without significant changes to an environment one would not expect performance expectations themselves to quickly change. Tastes are often trickier to explain, as expressed in the maxim “de gustibus non est disputandum” or “there’s no accounting for taste” (Stigler and Becker, 1977). However, culture provides one obvious source of tastes: people like or dislike cultural objects such as specific music simply because others do (Salganik, Dodds, and Watts, 2006). Therefore, one would also expect consumption-motivated discrimination to be consistent absent outside social interference.

The distinction between consumption-motivated and performance-motivated discrimination is a typology that classifies the motives underlying different types of discrimination found in the literature. This typology of motives is a useful way to conceptualize discrimination for two main reasons. First, it helps to abstract away from otherwise important nuances of specific discrimination theories. For example, statistical discrimination has theoretical baggage related to whether people are accurate or inaccurate, which is unrelated to whether that type of discrimination is performance motivated. 5 Second, the typology of consumption-motivated and performance-motivated discrimination helps to highlight similarities between otherwise disparate theories. For example, although theories of statistical discrimination and status-based discrimination have developed separately and have many important differences (Correll and Benard, 2006), both are driven by the performance motive outlined here. The typology therefore allows one to theorize about what encourages a broad range of discrimination. In the next section I develop an argument for why performance-motivated discrimination should respond one way with respect to economic consequences, while forms of consumption-motivated discrimination should respond the opposite way.

Economic Consequences and the Motive to Discriminate

The motives outlined so far are a necessary but not sufficient condition for discrimination to exist in a market. Additional considerations are necessary, including what might encourage or discourage an evaluator to enact these motives, as well as potential variance across evaluators in their propensity to enact them. This means that discrimination may increase or decrease as a function of changes to the behavior of specific evaluators, as well as changes to the set of evaluators. One prominent insight from past work is that economic consequences can make discrimination costlier and thus reduce its likelihood.

This argument is built on the logic that consumption-motivated discrimination has a cost, and changes to the environment can make it costlier. For example, in the 1940s and 1950s the set of U.S. major league baseball teams that delayed racial integration won fewer games and had lower audience attendance than teams that integrated sooner (Gwartney and Haworth, 1974). Overall discrimination slowly decreased as teams changed their behavior to become less discriminatory. In the same vein, Siegel, Pyun, and Cheon (2019) found that in the Korean market, local firms that were reluctant to hire women faced worse performance than multinational firms that hired more women. There, total discrimination slowly decreased as new firms entered the market. These examples indicate that discrimination can be reduced by increasing the competitiveness of a market. In such environments, discriminators must either reduce their discrimination or bear the cost of their tastes and risk their survival. For example, Pager (2016) showed that firms that had previously discriminated in an experimental audit study (Pager, Bonikowski, and Western, 2009) were more likely to go out of business within the following six years. In extreme cases, discrimination should go down as discriminatory evaluators are replaced by non-discriminatory ones. This means that when the consequences of decisions are high, there will be both an incentive for discriminators to eventually reduce their discrimination (e.g., Gwartney and Haworth, 1974) and an incentive for non-discriminators to enter the market (e.g., Siegel, Pyun, and Cheon, 2019). In either case, overall discrimination in a market should fall as economic consequences rise.

There is also some evidence for this dynamic within organizational settings, where the economic consequences of decisions are typically a function of incentive policies that determine how tightly or loosely evaluators bear the consequences of their decisions. Incentives have traditionally been studied from the standpoint of “principals” who calibrate how closely their “agents” should bear the consequences of decisions in order to maximize output (for an organizational theory perspective, see Eisenhardt, 1989). Gibbons (1998: 116) described this fundamental tension as “The Classic Agency Model: Incentives versus Insurance.” For example, paying workers an hourly rate versus a piecemeal rate has been shown to influence worker output in both theory and practice (e.g., Lazear, 2000). When these types of compensation systems are applied to managers they have been shown to impact how subordinates are evaluated. Using a field experiment, Bandiera, Barankay, and Rasul (2007) found that the implementation of a performance pay system caused managers to treat their high- and low-ability workers differently than they had when the managers were compensated with fixed wages. Along these lines, Ayres and Waldfogel (1994) conducted a “market test for discrimination” in the court system by comparing the bail amounts set by the court (which were high for minorities) to the subsequent rates charged by private bail bond dealers. The behavior of the bail bond dealers and the judges was theorized as a function of the economic consequences they faced for making accurate or inaccurate decisions. Using the assumption that the bail bond dealers had a stronger incentive to set fair rates than the judges, the authors inferred underlying levels of discrimination on the part of judges. These studies imply that discrimination will be a function of environmental characteristics, both because decision makers may alter their discriminatory behavior based on an environment and because an environment may encourage different types of decision makers to enter a market.

However, the expectation from the literature that increasing the economic consequences of an evaluation should discourage discrimination is derived from viewing discrimination as primarily consumption motivated. Acknowledging the possibility of performance-motivated discrimination complicates that prediction. This is because although increasing consequences should discourage consumption-motivated discrimination, it should simultaneously encourage performance-motivated discrimination. Performance expectations—regardless of their source or accuracy—should be employed more frequently when the stakes of a decision are high. For example, if a basketball coach believes tall players are more skilled than short players, then tall players should be given more playing time during championship games compared with the regular season, precisely because the cost of losing (or benefit of winning) such games is greater.

This dynamic should also function in the opposite direction. Consumption-motivated discrimination will be encouraged by environments in which the consequences of decisions are low, because tastes will be cheap to express. Performance-motivated discrimination will be discouraged by such environments, because the value of performance expectations in general will be lowered. This makes economic consequences a particularly important environmental characteristic as they should simultaneously influence consumption-motivated and performance-motivated discrimination in opposite directions. These predictions are agnostic to the sources of evaluators’ specific beliefs and preferences, which is particularly useful in the case of performance expectations. Both conscious and unconscious performance expectations, as well as “correct” and “incorrect” performance expectations, should respond in the same way to changes in economic consequences.

But because consumption-motivated and performance-motivated discrimination should respond in opposite directions to a change in consequences, additional assumptions are required to predict ex ante whether total overall discrimination will go up or down given a change in consequences. Two assumptions must come from the specific context under study: do evaluators likely (1) hold positive or negative performance expectations about the trait of interest and (2) hold positive or negative consumption preferences about the trait of interest? These two assumptions are necessary because the overall change in discrimination will be a function of the direction and strength of evaluators’ underlying taste preferences and performance expectations, which will depend on the context. These may sometimes be correlated but not always. Take for example the case of evaluators who hold positive performance expectations about a trait but a taste-based prejudice against it, potentially found in some forms of “model minority” discrimination. In such cases, decreasing the potential consequences of a decision should increase overall discrimination via a decrease in (positive) performance-motivated discrimination and an increase in (negative) consumption-motivated discrimination.

If evaluators hold both beliefs and tastes that are in the same direction, however, then the overall change is more difficult to predict. This is because one motive will be encouraged while the other is discouraged. In such cases the relative ex ante strength of one motive compared with the other will determine whether total discrimination will increase or decrease. Despite this, a specific shift in each motive may still be useful for practical purposes, as other policies may help to address whichever motive has been encouraged, an issue I consider in the Discussion section. In the next section I outline the assumptions required to make ex ante predictions in the context of this study.

The Evaluation of Gender in Microfinance

The theory developed above should function independent of the specific traits being evaluated, but a focus on gender in this study is useful for three reasons. First, gender is what psychologists refer to as a “primary category,” one of the handful of universal classification criteria that people employ when evaluating others (Ridgeway, 2011: 40). The result is that social relations are fundamentally “framed” by gender (Ridgeway, 2011). This makes gender a useful trait to examine for the purposes of testing a general theory about discrimination. It also ties this research to recent discrimination research in the management literature, which has focused on gender (e.g., Dahl, Dezső, and Ross, 2012; Greenberg and Mollick, 2017; Carnahan and Greenwood, 2018).

Second, there is existing research on gender in empirical contexts similar to this study. This is useful because it can provide the basis for assumptions about how evaluators in this context are likely to evaluate women in terms of both performance and consumption motives. The starting point for these assumptions is the traditional microfinance narrative that women are economically superior borrowers to men despite the cultural discrimination they face (Armendariz and Morduch, 2010; Roodman, 2012). These assumptions can in turn provide directionality for how each of the two foundational motives will respond to changes in economic consequences and what will happen to overall discrimination. I begin with assumptions about performance expectations in this context.

The positive performance expectations about female borrowers compared with male borrowers in microfinance contexts may be derived from a number of sources, including beliefs that on average women may have a higher incentive to repay loans because of fewer outside options, are more responsible with money because of general risk aversion, and have more limited geographic mobility, which makes collection easier (Armendariz and Morduch, 2010). This general conclusion appears consistent with research in contexts even closer to this study. On Prosper.com, one of the major for-profit peer-to-peer lending platforms in the United States, Pope and Sydnor (2011) found that after controlling for available observables, such as credit score, women were more likely to be funded than men. Chen, Li, and Lai (2017) examined data from a similar Chinese lending platform and concluded that female borrowers were more likely to receive loans and less likely to default but were charged higher interest rates (a feature of that platform); they interpreted this as evidence of positive statistical discrimination and negative taste discrimination against women. As I will discuss later, the default rates on the platform I examine in this study exhibit a similar trend. Of the loans that had already matured by the start of the study period, none of the defaults were by female borrowers, and of the loans that were actually invested in during the study period, only one of the 25 borrowers who eventually defaulted was a woman. Therefore, it seems quite plausible that lenders hold positive stereotypes about women’s performance abilities in this context.

Yet it also seems probable that taste preferences against women exist from the broader social context. China ranks similarly to the United States on the United Nations’ Gender Inequality Index (GII). 6 However, a number of sociological phenomena in the Chinese context indicate that the salience of gender attitudes is high. These include profound gender disparities, such as the “missing women problem”: the fact that the ratio between the number of women and men in China is not what one would expect (Sen, 1992; Qian, 2008). One explanation for this “son preference”—which is not exclusive to China—is the particular cultural family system that exists in countries that exhibit it (Das Gupta et al., 2003). This potentially disparate treatment continues later in life, as indicated by the derogatory term “leftover women” (“shèngnü,”剩女), which is used to refer to women as young as 25 who have not yet married (Hong Fincher, 2016). Thus, broad cultural tastes may be developed early and derived from widespread cultural preferences for men relative to women, even absent specific performance evaluations in which quality expectations might be important. If one were to make general assumptions about lenders in this context, it seems most plausible they hold favorable performance expectations about women as borrowers and negative taste preferences toward women.

The final advantage of a focus on gender in this specific context is that the above assumptions are opposite of each other. The directionality of the assumptions about performance beliefs (positive) and tastes (negative) allows for clearer predictions about how the overall evaluation of women should be related to the economic consequences faced by those who evaluate them: increasing the economic consequences should lead to overall more favorable treatment of women, and decreasing the economic consequences should lead to overall less favorable treatment of women. This is because raising the economic consequences of lending decisions should theoretically encourage more performance-motivated discrimination (more favorable treatment of women) and less consumption-motivated discrimination (less unfavorable treatment of women); both changes will lead women to be treated more favorably than they were before. Likewise, lowering the economic consequences of lending decisions should theoretically encourage less performance-motivated discrimination (less favorable treatment of women because the positive performance expectations are made less valuable) and more consumption-motivated discrimination (more unfavorable treatment of women because negative taste preferences are now easier to express); both changes will lead women to be treated less favorably than they were before.

Empirical Setting

The empirical context for this study is an online peer-to-peer lending platform in China. In a stylized version of peer-to-peer lending, a mediating platform accepts applications from potential borrowers, screens them, posts them on a website for lenders to evaluate, and then facilitates the transfer of money from lenders to borrowers and borrowers back to lenders. Loan requests are fulfilled in a piecemeal fashion, whereby many lenders each choose to contribute a portion of a given borrower’s total loan request. Once the full loan request is met, the loan is closed and the platform facilitates the transfer of funds from the lenders to the borrower. The platform then facilitates the collection of loans and periodic borrower repayments.

The prototypical and earliest peer-to-peer lending platforms in the United States were Prosper.com, Lending Club, and the 501(c)(3) platform Kiva.org, which was designed for non-profit lending (Government Accountability Office, 2011). A handful of other platforms catered to niche markets such as student loans or medical procedures. Regulatory constraints typically limited the operations of such firms to national borders, meaning there was no international competition.

Online lending is a particularly useful context for studying evaluation processes, because researchers have access to the same information used by the lenders to evaluate the borrowers. This allows researchers to strengthen the assumption that evaluations are not being driven by omitted variables that the evaluators can see but the researcher cannot. Leung and Sharkey (2013) employed the context to study perceptual factors related to the classic category-spanning discount. Pope and Sydnor (2011) and Ravina (2012) examined discrimination in the context of the Prosper.com marketplace, looking at the likelihood of borrowers receiving a loan, the favorability of loan terms (a feature of the Prosper.com marketplace), and the average financial performance of different demographic groups. Such studies have focused primarily on identifying the existence of different types of discrimination rather than on what triggered that discrimination.

Online Lending in China

At the time of this study, in 2012, Chinese peer-to-peer (“个人对个人” or “individual-to-individual”) lending differed from the American context in several ways due to differences in the historical development of the financial services industry in China and to looser regulatory constraints. U.S. peer-to-peer lending companies relied on existing third-party credit scores to screen potential borrowers. 7 China lacked an extensive national credit scoring system such as the FICO score, so the role of peer-to-peer lending companies was broader in China than in the United States and included more intensive verification of borrowers’ backgrounds.

American peer-to-peer lenders technically invested in promissory notes sold by the peer-to-peer platforms, which were tied to the repayment of specific loans issued by a bank. 8 In China, the platforms more directly facilitated the transfer of money between lenders and borrowers. In theory, this resulted in less regulation because it amounted to activity outside of traditional banking institutions. This was observable in company names. For example, Ppdai, one of the first peer-to-peer lending platforms in China, was registered as Shanghai Ppdai Financial Information Service Co., Ltd. The business name of the company I studied included “commercial advising.” Such names reflected that in 2012, the industry occupied an uncertain space in the broader scope of Chinese financial services, with most platforms functioning as some form of financial information or advising company. Lenders had to trust that platforms were honest and competent, because it was impractical to collect individual repayments without a platform’s assistance.

The number of online Chinese peer-to-peer platforms increased rapidly from just nine in 2009 to 132 in the first quarter of 2013 (Li, 2013). By 2018 media reports estimated the number of platforms in the thousands with hundreds of billions of dollars in transactions (Feng, 2018). This growth can be viewed in light of broader economic trends, as a tradition of heavy state involvement in the Chinese financial system increased the attractiveness of these companies to both lenders and borrowers (Huang, 2018). State-owned banks offered low interest rates to investors and preferential lending to state-owned enterprises, which made it difficult for individuals and small businesses to procure traditional bank loans and drove overall demand for financial innovations such as peer-to-peer lending.

Data for this study were collected from a platform that began offering peer-to-peer lending services in 2010. At its founding, loans were not guaranteed, and the platform functioned similar to U.S.-based platforms such as Prosper.com, although to my knowledge it never featured competitive bidding on interest rates. It first implemented a loan repayment guarantee policy in the first half of 2011 when total loan volume was still low. In early 2012 the company updated its loan guarantee policy to cover loans of all credit rating levels. These types of loan guarantee policies were common in the industry as a way to assuage fears about repayment and attract new lenders. For example, competitor Ppdai began offering a principal guarantee in July 2011. These guarantees were featured prominently in the companies’ marketing materials and can be viewed as a stepping stone to the eventual introduction of packaged financial products that allowed investors to put their money toward packages of aggregated loans rather than individual loans. 9 Because of the lack of a comprehensive national credit scoring system, lenders had always had to trust in the peer-to-peer companies to perform proper due diligence on potential borrowers. Therefore, the guarantees acted as a mechanism to demonstrate that the companies’ incentive to perform adequate due diligence on borrowers was aligned with lenders’ interests.

Because borrower screening was more involved for Chinese companies than their U.S. counterparts, this created the potential for mismatch between the supply and demand of money on the platform. 10 During the time period of this study, the platform attracted much more money for lending than borrowers available to accept it. This meant that all the loan requests that the platform allowed to be posted were fulfilled, sometimes in just a matter of hours. I next discuss how these features of the context influenced the empirical design.

Empirical Strategy

Data

The data for the study consisted of all realized evaluations of borrowers, that is, every decision made by lenders on the platform for a 60-day period in 2012. Each row of these data indicated how much a specific lender decided to provide a specific borrower and when they made the evaluation.

Dependent variable

The main outcome of interest was how lenders altered their evaluation of male and female borrowers based on economic consequences—whether their relative evaluations of female borrowers became more or less favorable. To measure this, I focused on the amount of money a lender decided to contribute to a specific borrower’s loan request. This empirical choice is similar to other discrimination studies that have focused on later-stage evaluations, such as the allocation of employee bonuses between men and women (Castilla and Benard, 2010), even though it is possible that inequality also existed at earlier stages, such as the promotion or hiring process. If a lender invested in the same loan more than once, the total amount invested in that loan by the lender was aggregated for purposes of analysis. 11

By using a lender’s loan size decision, it was largely possible to sidestep the selection and timing effects that are difficult to account for in non-experimental data. For example, the speed at which borrowers were funded in this particular context meant it was unrealistic to assume that all lenders viewed all borrowers, i.e., to assume that all 3,087 lenders active at least once during the period viewed all 558 loans, which would have resulted in 1,722,546 pairs. This is because at any given time only a handful of active loans were available, representing requests from between 0 and 15 borrowers at any given time; see Figure A1 in the Online Appendix (http://journals.sagepub.com/doi/suppl/10.1177/00018392211029930). Further, all borrowers during the period under study had their loan requests fulfilled. For this reason I focused on the 25,440 realized decisions and then included control variables that account for the availability of other loans at the exact time of each of these decisions.

Independent variables

The main counterfactual of interest is how the relative evaluation of women is different when economic consequences of a decision are higher or lower. This requires an interaction of two variables: a binary variable that captures the gender of the borrower and a binary variable that indicates whether the decision was made in an environment with relatively higher or lower economic consequences as compared with a separate baseline environment. The interaction between these two variables captures whether economic consequences influenced the evaluation of gender.

Control variables

The most important control variables consisted of other observable traits of the borrower. Chief among these were the direct financial characteristics of the loan itself: the company-assigned credit score category, the interest rate, the loan term, and the amount of money requested. I also controlled for a set of other available borrower characteristics. These included the purpose of the loan use and a range of other information about the personal and professional situation of the borrower; these are detailed in the notes for Table 3 below.

In addition, I created time-dependent variables that helped capture lender choice and calculated each of them based on the timestamp of the focal lending decision. These included the count of other loans that were available at the same time (mean 3.7 loans) and the number of those loans that were requested by women (mean 0.55 loans), as well as a measure of how long the focal loan had been posted on the website based on the difference between the time of the focal lending decision and the first decision from any lender to that specific loan (mean 14.7 hours).

Finally, I also created a set of lender variables to potentially control for variance in each lender’s performance expectations about borrowers. These variables included whether the lender and borrower shared a geographic location (8.2 percent of decisions), as well as measures of a lender’s past experience on the platform, and were also calculated based on the timestamp of each focal decision by a specific lender. The lender experience variables included the number of previous lending decisions the lender had made, the number of those decisions that were to female borrowers, the amount of total money lent, and the number of previous loans that the lender would likely have known to have defaulted. A lender’s personal experience with defaulted loans was inferred from a combination of the loan terms and loan outcomes of each lender’s past decisions. For example, if a lender had made a loan in January that had a six-month term, then knowledge of the outcome of that loan would be available in July. Any decisions made after July would then be made with the knowledge of whether that specific previous loan had defaulted. Less than 5 percent of the sample of lending decisions were made at a time when the lender had already experienced a default from one of their prior lending decisions.

Research Design and Methods

The goal of this study is to understand how shifts in economic consequences may alter how gender is evaluated. Variance in consequences is required to test this theory, whereby the potential economic consequences of decisions are shifted to be higher or lower than they were previously. Evaluations can then be compared before and after the change.

This study employed a setting in which the potential economic consequences of using gender during lending decisions was reduced. In early 2012 the company updated its loan principal repayment guarantee policy. For practical purposes, this guarantee amounted to an insurance policy for lenders. Unlike an existing policy implemented in the first half of 2011, this new policy covered every loan on the platform (the previous policy did not cover HR, high-risk, loans). It was funded by assessing service fees on loans ranging from 0 to 5 percent depending on the company-assigned credit rating of the loan. The policy would be expected to reduce—if not remove—the economic consequence of lending to one particular borrower over another. 12

Therefore, performance-motivated discrimination should decrease from the pre-policy period to the post-policy period given that the value of performance expectations about gender was reduced. At the same time, consumption-motivated discrimination should increase from the pre-policy period to the post-policy period because the consequences of expressing those tastes were also lowered. Combining these predictions with the context-specific assumptions outlined previously (i.e., the existence of positive underlying performance expectations and negative tastes) leads to an overall empirical expectation that the change will cause women to be evaluated less favorably than they were previously.

To test this, I used 30-day windows of data from either side of the policy change. The difference of interest is not whether men and women were evaluated differently but whether the policy altered these relative evaluations. Therefore, I employed a difference-in-differences design to measure the potential shift in relative evaluations between these two periods. In practice this takes the form of an interaction between the policy period variable (guarantee = true) and the gender of the borrower (gender = female), so that a positive coefficient on the interaction term would indicate women were subsequently treated more favorably, and a negative coefficient would indicate they were treated less favorably.

Employing 30-day windows on either side of the policy change strengthened the identification in two ways. First, it limited the potential influence of other concurrent events in the firm, industry, or broader economy. This is important given how fast both the industry and the business models of the firms were evolving (Huang, 2018). Second, it limited the potential for lender learning (e.g., Altonji and Pierret, 2001; Freedman and Jin, 2011), which could theoretically influence performance expectations. The lender experience variables outlined above also helped control for differences in lender experience.

Assuming that the women in the post-period were not significantly different from the women in the pre-period—and the same was true for men—then this basic difference-in-differences should provide a valid measure of how the policy altered lenders’ evaluation of gender. This is because the main assumption of this approach is not that men and women are identical but rather that the characteristics of borrowers of each gender are similar across the study windows. To relax this assumption, however, I ran a set of ordinary least squares regression models that included the control variables previously reviewed. Equation 1 represents the general form of these models, where DecisionSizei,j is the amount of money that lender i loaned to borrower j (contingent on making a loan), Genderj is whether borrower j was female, Policy{0,1} is a binary variable for whether the decision was made during the post-policy period, and Xj is the primary financial characteristics of the pertinent loan: the interest rate, term of the loan, size of the requested loan, and credit rating category. Xj is then expanded in stages to include the full range of borrower control variables, followed by the lender experience variables.

Descriptive Statistics

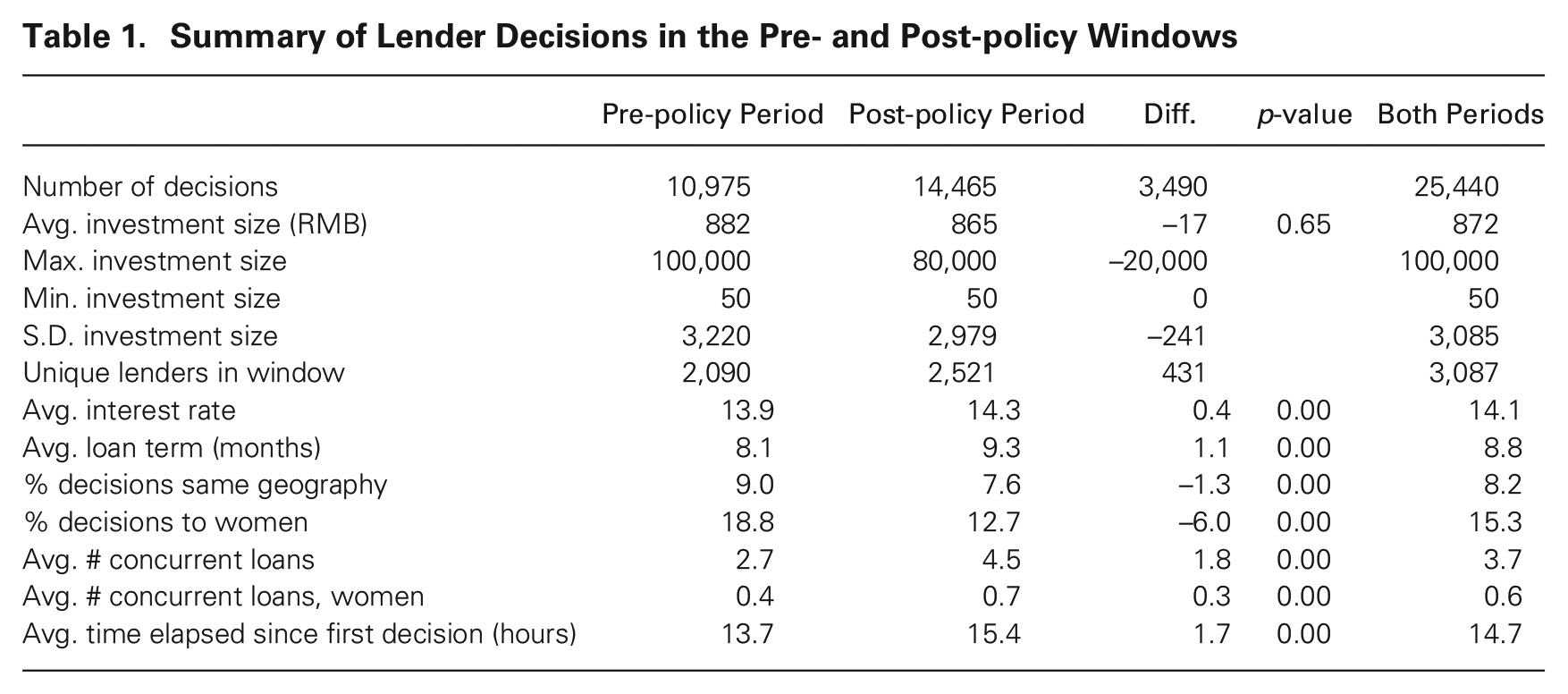

Lenders made 25,440 decisions to lend across 558 loans during the study window. The decisions during the two 30-day periods are summarized in Table 1, with 10,975 in the pre-policy period and 14,465 in the post-policy period. In total, approximately 15 percent of these decisions were to women. The average investment size was 882 RMB in the 30 days before and 865 RMB in the 30 days after the policy change. But the absolute number of decisions was greater in the second period and highlights the volatility in loan supply, with some days when a shortage of borrowers meant no loans were made (see Figure A2 in the Online Appendix).

Summary of Lender Decisions in the Pre- and Post-policy Windows

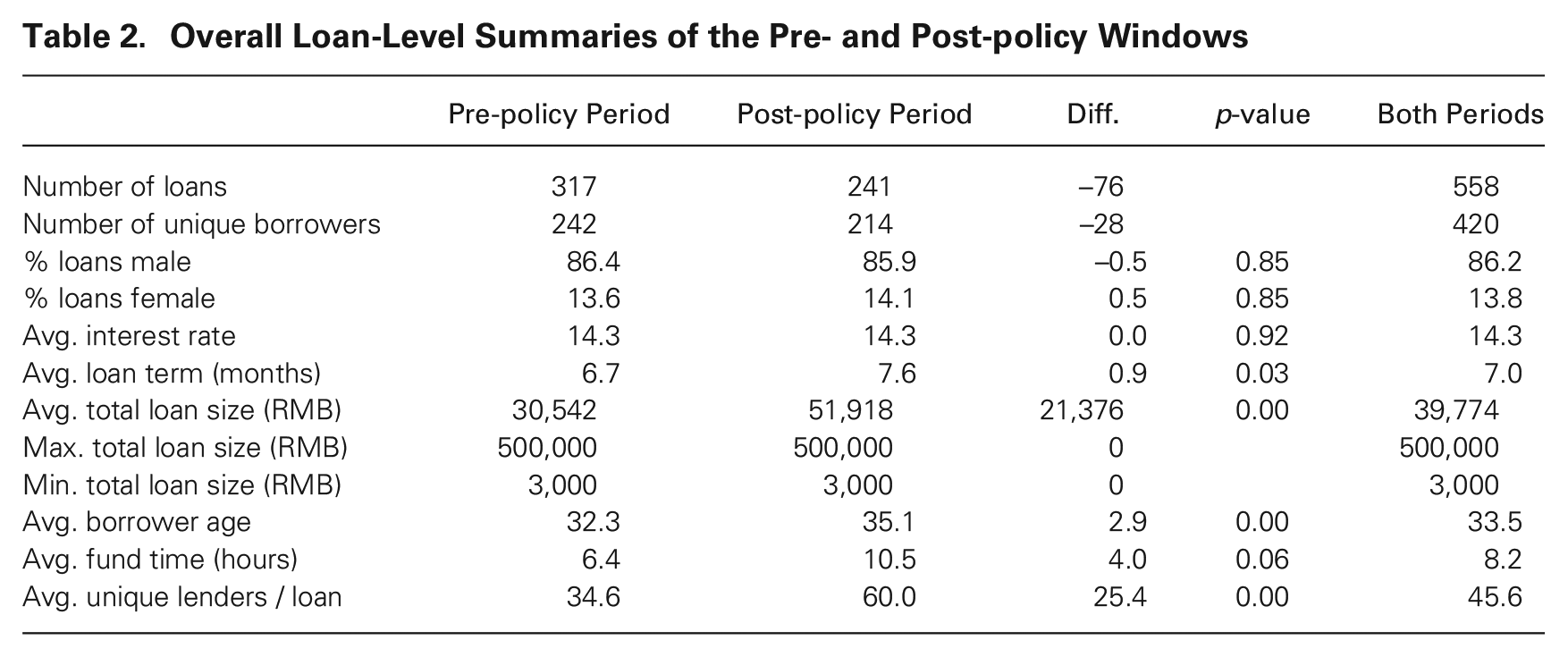

The 558 individual loans in the window (317 in the pre-policy period and 241 in the post-policy period) are summarized in Table 2. The overall loan interest rates varied from 6.1 to 24.4 percent with the most common categories of 13 and 15 percent. Loan sizes also varied from 3,000 RMB (approximately $475) to 500,000 RMB, with the majority of loans in the 3,000 or 5,000 RMB categories. The loan repayment terms ranged from three to 24 months, with the majority being three- or six-month loans. All loans were fully funded, and most very quickly, with the average taking just over eight hours. During this period, the demand from lenders therefore outstripped available borrowers.

Overall Loan-Level Summaries of the Pre- and Post-policy Windows

Additional information on the 558 loans that were open for lending at some point during the study window is presented in the Online Appendix. Only 25 of the total 558 loans ended up as “bad debt”; see Table A1. (Of the 25, only one defaulted loan was borrowed by a woman.) The majority of borrowers indicated they would use their loans for short-term turnover; see Table A2. The distribution of the company-assigned credit rating ranged from AA (highest quality) to HR (high risk). The pool of loans grew progressively larger as the quality decreased; see Table A3. About half of loans were rated in the two highest risk categories of E or HR, with only five loans rated AA or A.

A total of 3,087 unique lenders made at least one lending decision during the study period. Of these, 1,524 lenders were active in both periods, 566 were active only in the pre-period, and 997 only in the post-period. The higher number of unique lenders after the policy change may be a function of the platform growth process and supply of loans.

Results

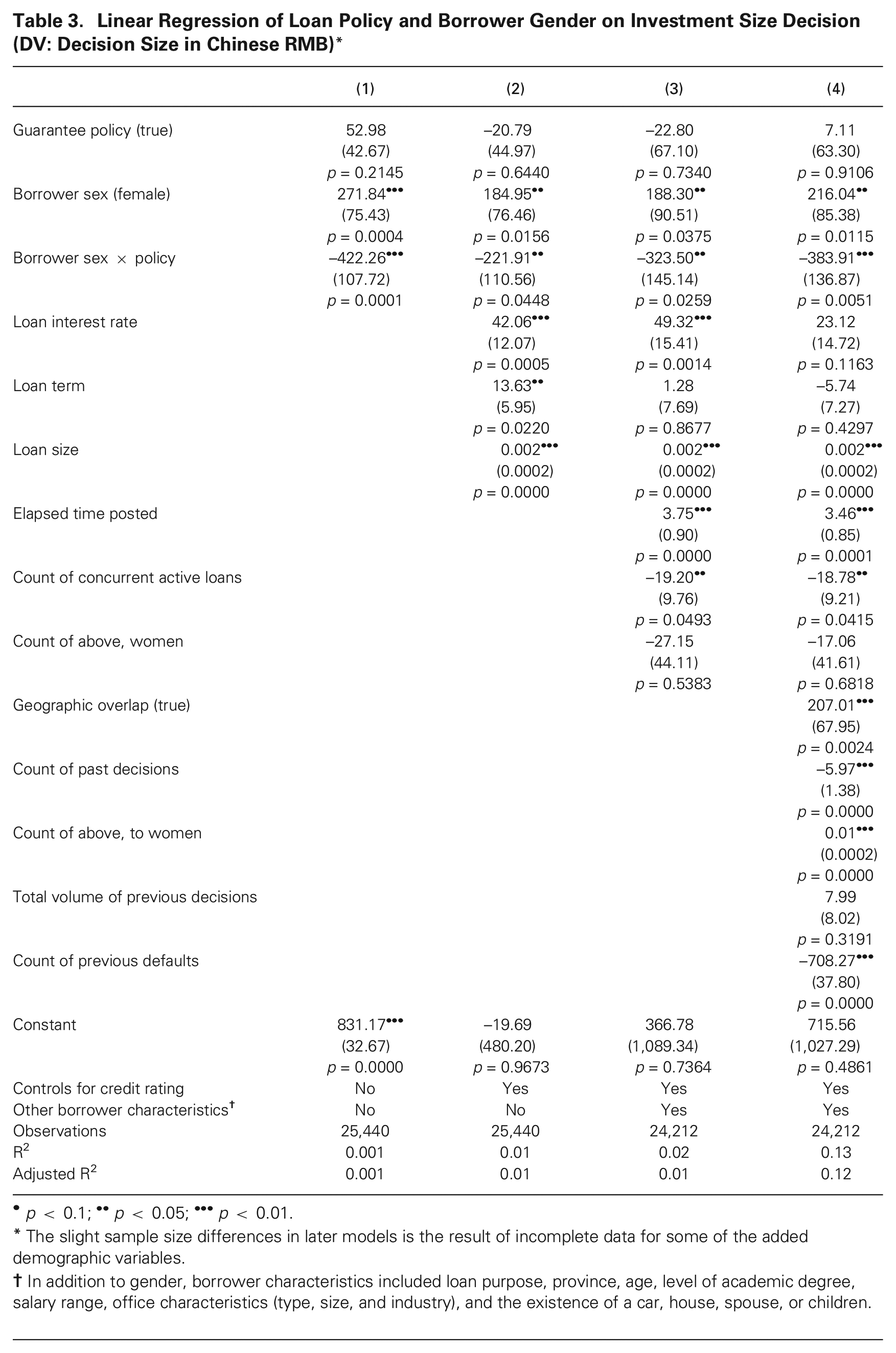

A simple difference-in-differences between the two periods with respect to gender provides preliminary evidence of how the policy altered discrimination. This calculation is produced in model 1 of Table 3 (see Table A4 for crosstabs). The coefficient on the interaction of borrower sex and the policy is –422.3 RMB, which represents the change in the relative evaluation of female borrowers. This negative coefficient indicates that the policy led women to be evaluated less favorably. Women were actually evaluated more favorably than men before the policy, but after the policy, men were evaluated more favorably than women. Using the regression model described earlier, I then introduced controls to relax the assumption that the borrowers within each gender category were the same across periods (i.e., the men were similar before and after the change, and the women were similar before and after the change). Model 2 in Table 3 adds controls for the most important “hard” economic traits of a loan: the loan’s credit rating, interest rate, term, and size. The directionality on the interaction term was the same, although the magnitude of the coefficient decreased to –221.9 RMB.

Linear Regression of Loan Policy and Borrower Gender on Investment Size Decision (DV: Decision Size in Chinese RMB)*

p < 0.1; ••p < 0.05; •••p < 0.01.

The slight sample size differences in later models is the result of incomplete data for some of the added demographic variables.

In addition to gender, borrower characteristics included loan purpose, province, age, level of academic degree, salary range, office characteristics (type, size, and industry), and the existence of a car, house, spouse, or children.

A fundamental theoretical challenge in studies of demographic disparities is understanding what exactly a demographic attribute represents. Even demographic variables such as race present serious taxonomical challenges, as definitions change over time and it is not always apparent what category membership specifically entails or how the information is interpreted (Charles and Guryan, 2011). To further complicate matters, many individual characteristics are confounded with other characteristics. Therefore, it is impossible to ever be fully certain of how people interpret demographic information. These issues are important because they influenced what an “ideal” model specification should look like.

In light of this I next ran a model with a full range of borrower information and controls for the availability of other loans at the time the decision was made. Including these additional variables slightly reduced the sample size because of missing data. These results are presented in model 3 of Table 3. The results remain consistent with previous models; the coefficient of the interaction term was –323.5 RMB. Finally, I added the controls related to individual lender experience at the time the lender made each specific decision. These results are presented in model 4 of Table 3. The coefficient on the interaction term was again consistent with previous models: –383.9 RMB.

Further Empirical Tests

The previous section tested the main effect of how evaluations of gender changed across the two periods. The following sections further explore this effect from three complementary dimensions: the set of evaluators, the heterogeneity of the effect, and the nature of the policy.

Evaluator behavior

The preceding analyses indicated that the policy led borrowers to be evaluated differently based on their gender. Two basic pathways could have contributed to this effect. The first is a within-lender channel, meaning specific lenders changed their behavior as a result of the policy. The second is a between-lender channel, meaning different individuals behaved differently across the two periods. Because discrimination is often conceptualized as a market-level outcome, these channels are not mutually exclusive, and it is plausible that both could have contributed to the effect.

I used a lender fixed effects model to investigate these two channels. The main challenge to employing lender fixed effects in this context was the extent to which it restricted the sample. Although about half of all lenders who were active during the study period made loans both pre- and post-policy, a lender must have made at least one decision to a male borrower and one decision to a female borrower in both the pre- and post-policy periods to have the minimum required amount of variance. Subsetting the data this way resulted in 405 lenders who made a total of 11,874 decisions across the span of the two windows, representing 13.1 percent of lenders and 46.7 percent of decisions from the original sample (Table A5 in the Online Appendix includes descriptive statistics). The final model described in the previous regressions was then rerun using the subsample eligible for lender fixed effects and the subsample ineligible for lender fixed effects (models 1 and 2 in Table A6). For the subsample that was ineligible for fixed effects, the results were similar to the main analyses. For the subsample that was eligible for the fixed effect model, the coefficient was in the same direction but quite noisy.

These results arguably provide stronger evidence for the between-lender channel than the within-lender channel, even though the evidence is not inconsistent with the latter. This relative importance of between-lender effects reflects other discrimination research that indicates that within-evaluator behavior may be slower to change (Siegel, Pyun, and Cheon, 2019). One explanation is the “imprinting” that can occur from an experience of specific environments (Marquis and Tilcsik, 2013). However, I found evidence that the effect was stronger (more negative) when interacted with either the total number of previous loans a lender had made or the total number of defaults a lender had experienced (Table A7). One caveat of prior experience in this setting is that more experienced lenders may also pay more attention to platform changes simply because they are more active.

To better understand the nature of potential within-lender changes, I expanded the time frame by an additional 30 days before and after the main sample window. This approach has natural tradeoffs, as such a wide window (60 days on either side of the policy) is more likely to overlap with other changes in such a rapidly developing industry. But the benefit is that a larger number of lenders (702) meet the criterion for a fixed effects estimation. I therefore ran the model using this sample as a robustness test (model 3 of Table A6). The magnitude of the coefficient is very similar to the original fixed effects model and much more precise. This strengthens the evidence for within-lender effects, although they do appear somewhat weaker in magnitude than the between-lender effects; I explore the implications of this in the Discussion section.

Heterogeneity of the effect

It is possible the measured effect is not observed equally across the range of decisions. For example, if a lender considered a sum of money to be too small to be worth an active decision, then one would expect the decision to be as good as random no matter the potential consequences. This indicates there may be some lower threshold for this mechanism to function. To test for this, I excluded small decisions from the analysis. Limiting the decisions to those equal to or greater than 200 RMB resulted in around 14,000 decisions. These data were then used in the regression model described earlier. As expected, the magnitude of the previously observed effect was larger for this subset (see Table A8).

A second form of heterogeneity may also exist if male and female lenders hold different tastes or beliefs about quality. Some studies have found evidence for how the gender of evaluators may influence discrimination (e.g., Srivastava and Sherman, 2015; Greenberg and Mollick, 2017). However, Heilman (2012: 129) concluded that “In the vast majority of studies conducted on gender stereotypes, no differences have been found in the reactions of male and female respondents.” To test whether an effect exists in this context, I reran the final previously specified model and included the gender of the lender interacted with both the borrower gender and the policy (see Table A9 and also Table A10 for crosstabs). Neither the two-way interaction between lender and borrower gender nor the three-way interaction with the policy variable was statistically significant at conventional levels, meaning I did not find evidence that women and men evaluated gender differently in this context. This finding appears consistent with the majority of studies on gender stereotypes.

Policy treatment specification

Given that the updated guarantee policy covered loans with an HR (high risk) credit rating while the previous policy did not, it seems plausible the effect would be strongest on that subset of borrowers. A blanket guarantee policy may have also reduced the perceived economic consequences for all borrower choice on the platform. If this is the case, then loans that were previously covered yet flagged as more risky (e.g., E credit ratings) may have been impacted differently than less risky categories (e.g., B credit ratings). To test for these effects, I split the sample into three subsamples: (1) loans with a credit rating of HR, (2) loans with a credit rating of AA through C, and (3) loans with a credit rating of D or E. Despite the overall prevalence of HR-rated loans (see Table A3), they were on average smaller than other categories, so they represented only 14.8 percent of the original sample of lending decisions. The majority of decisions (56.3 percent) were to D and E loans.

I then ran the same model specification across the three subsamples (Table A11). The directionality of the coefficients in the three models mirrored earlier results, but the coefficients were imprecise for both the HR and the AA/A/B/C samples. The much smaller sample size of the HR subsample may have contributed to the imprecision of its coefficient estimate. However, the larger (negative) magnitude and more precise estimate for the D/E subsample provides some support that the policy may have cued lenders to consider financial risk more broadly. This indicates that salience of economic consequences may be enough to change how borrowers are evaluated. One reason for this may be that the policy represented a fundamental shift that removed all economic consequences related to choice between borrowers. At the platform level, this represents a shift from “some risk” when choosing borrowers to “zero risk” involved in the choice. Even if such a gap is small, it may be qualitatively important. In short, economic consequences may be perceived in terms of the broader environment (i.e., the platform) as well as the narrower decision. These findings may also further support evidence of the between-lender processes explored in the lender fixed effects analysis. This is because platform-level policies are likely more salient to new lenders who join the platform as a result of advertising or other communication that may highlight such policies.

A second consideration is related to changes in the purposes of loans. The main models control for loan purpose, but the policy appears to have coincided with shifts in loan usage categories (see Table A2). This could be due to changing incentives at the platform level to prioritize certain types of loans to post on the platform or to other dynamics related to how loans are classified. Given that the most salient shift appears to be a decrease in personal consumption loans and increase in short-term turnover loans, I reran the final model from Table 3 first with only loans from those two categories and then again with only the short-term turnover loans (see Table A12). The original effect was present in both of these cases. I interpret this as evidence that even if the policy altered what types of borrowers were allowed on the platform or how they were classified, the effects do not appear contingent on such a shift occurring.

Finally, because policy changes such as the one in this study are not experimentally exogenous, I also constructed and tested two placebo policies. The first placebo test set the treatment date one month before the actual date and compared the 30-day windows on either side, so that this sample had not experienced the actual policy change. The second placebo treatment employed the same approach but moved the treatment date to one month after the actual date, so that this sample had already experienced the policy change. The analyses were then replicated for these two samples (see Table A13). The coefficients on the interaction terms were insignificant in the primary financial control models, but the coefficient was positive in the second placebo sample with the full set of controls, although this was contingent on specifically including the control for the number of other concurrent female loans. This post-treatment placebo may not be an ideal test, however, because in reality the full sample had already been treated. Further, in settings such as this in which evaluators’ most salient goal is to make money, the lack of any economic incentive at all to discriminate between individual borrowers naturally leads the industry itself to change. Indeed, firms in the industry soon began to offer automatic investment options and financial products based on bundles of individual loans so that individual choice between loans no longer occurred. The second placebo test may indicate that some borrowers had already begun to mimic this behavior by simply randomly choosing borrowers, which would lead women to be treated more favorably again as the difference between genders is ultimately equalized.

Discussion

In this study I examined the role of economic consequences in motivating discriminatory evaluations. I theorized that consequences affect discrimination by simultaneously encouraging and discouraging two separate motives for discrimination: a consumption motive driven by taste preferences for a specific trait and a performance motive driven by performance expectations about that same trait. Reducing the economic consequences of evaluations should discourage performance-motivated discrimination and encourage consumption-motivated discrimination. Increasing the consequences should encourage performance-motivated discrimination and discourage consumption-motivated discrimination. This is because economic consequences alter the value of enacting tastes and acting on performance expectations. They therefore create a dynamic relationship between otherwise very different types of discrimination.

The first step required to apply this theory in a specific context was to develop priors regarding the performance expectations and tastes of evaluators in that context. In this study, the priors consisted of positive performance expectations and negative taste preferences. The second step was to analyze a situation in which the potential economic consequences of evaluations had been altered. I found evidence that reducing economic consequences in this context led women to be evaluated less favorably. When interpreted in conjunction with the priors about evaluators, this result was consistent with expectations derived from the theory.

Organizational Implications

Although the study took place in the context of a peer-to-peer platform, the insights about economic consequences may translate to more traditional organizational contexts when one considers the role of incentive policies. Many incentive policies have been documented in the compensation literature, including “piece rates, options, discretionary bonuses, promotions, profit sharing, efficiency wages, deferred compensation,” and related approaches (Prendergast, 1999). All of these policies should increase or decrease the consequences of decisions for the people impacted by them. Even tools that are not explicitly economic in nature, such as non-monetary employee awards (Gallus and Frey, 2016), may increase the perceived consequences of evaluations and thus produce similar effects. This is because such tools link the performance outcome of an evaluation to the perceived rewards or punishments of evaluators. For example, changing managers’ financial compensation to be more or less closely tied to the performance of their employees should alter the levels at which managers will be motivated to discriminate. Therefore, consumption-motivated discrimination can be discouraged by introducing higher-powered incentives. Performance-motivated discrimination can be discouraged by shielding evaluators from the consequences of their decision.

However, organizations must also be cognizant that using economic incentives to reduce one form of discrimination may simultaneously motivate other forms of discrimination. This means generic prescriptive recommendations are not possible. The theory requires assumptions about the nature of people’s ex ante performance expectations and tastes in order to predict overall changes in discrimination. It was possible to establish these assumptions for the context of this study. But organizations will need to turn to research on specific types of discrimination, prejudice, and biases to understand how altering incentives in a specific context is most likely to impact overall levels of discrimination in that context. Luckily, this task should be made easier by the diverse body of research on discrimination in specific contexts.

Kalev, Dobbin, and Kelly (2006: 590) found that many corporate diversity programs have mixed effectiveness and generally observed that “We know a lot about the disease of workplace inequality, but not much about the cure.” One potential reason for this is that managers may not truly understand the underlying motives of evaluators, and reexamining policies in light of the distinction between consumption-motivated and performance-motivated discrimination may be fruitful. Paluck and Green (2009: 341) reviewed 985 reports of particular prejudice-reduction interventions that included “multicultural education, antibias instruction more generally, workplace diversity initiatives, dialogue groups, cooperative learning, moral and values education, intergroup contact, peace education, media interventions, reading interventions, intercultural and sensitivity training, cognitive training, and a host of miscellaneous techniques and interventions.” Some of these interventions, such as multicultural education, might be expected to affect only one motive for discrimination: to decrease consumption-motivated discrimination but have no impact on performance-motivated discrimination. This means that it might still be useful to use incentives to decrease one type of discrimination even if doing so increases another type of discrimination, assuming complementary interventions can then be subsequently employed.

The within-lender fixed effects analyses in this paper also warrant additional interpretation in light of the potential organizational implications. This is because overall discrimination can decrease via multiple channels—both selection and treatment effects—sometimes occurring at the same time. This is most clear in traditional markets. For example, women have historically been undervalued in the Korean managerial labor market (Siegel, Pyun, and Cheon, 2019). As such a market grows (i.e., the economic consequences of entering it increase), taste-motivated discrimination should decrease via both selection and treatment effects: non-discriminators such as multinational firms will be encouraged to enter to access underutilized talent, and local firms will be encouraged to reduce their own taste-motivated discrimination. Both these avenues will lead to less overall discrimination, although the former process may typically be faster than the latter. In organizational settings, however, selection processes may be more constrained. This means that if organizations are limited to a fixed set of evaluators, the overall effect of economic consequences on discrimination may be more muted than if the pool of evaluators turns over more freely. Indeed, the fixed effects results from this study are consistent with but less clear than the results from the sample ineligible for fixed effects. This may be partly due to the fact that evaluators may be slow to change—an interpretation consistent with the dynamics of traditional markets, i.e., as Siegel, Pyun, and Cheon argued (2019: 387), “the market is moving toward a new equilibrium free of discrimination, but very slowly.” The organizational implication of this would be that economic consequences will be more important when evaluator turnover is higher, which echoes the importance of selection effects that has been identified in other evaluation processes (Kovács and Sharkey, 2014).

Future Directions

While this study sheds light on the dynamic relationship between economic consequences and two different motives for discrimination, it provides only general guidance about which motive will dominate in a static setting. In settings in which evaluators are not constrained by strong economic penalties, one would expect tastes to play a larger role than would otherwise be expected, as tastes will already be relatively cheap to exert. In settings in which decisions already lead to significant economic consequences, tastes will be less pronounced because they are already prohibitively expensive. Likewise, performance-motivated discrimination should be most prevalent when consequences are already high. This insight may be useful for interpreting existing studies of discrimination: those conducted in settings such as a laboratory (where economic consequences of decisions are low) may be more prone to measure consumption-motivated discrimination, whereas those conducted in the field (where economic consequences of decisions are higher) may be more likely to capture performance-motivated discrimination.

I also advise caution when attempting to generalize my empirical results to other settings, as they represent just one particular context. Context-specific assumptions are required before directional predictions can be made. The general approach to encourage or suppress their expression, however, should apply to a wide range of settings. For example, Thébaud and Sharkey (2016) concluded that women-led small businesses had more difficulty securing loans following the financial crisis of 2007–2008. In addition to the role of uncertainty during such macroeconomic periods, one might also consider how the economic incentives within lending institutions might have changed. If recessions increase the perceived economic penalty for making bad decisions—for example, if layoffs within banks had increased—then loan officers should be more motivated to employ their beliefs about quality during such periods and less motivated by their tastes.

Future work may also benefit from attempting to directly situate these motives within the managerial research on anti-prejudice and diversity programs. In addition to economic incentives, managers have a range of tools that can moderate the perceived or real consequences of decisions. These include “social” incentives such as awards (Gallus and Frey, 2016) but also policies that foster organizational cultures that might trigger taste or performance motives. For example, Castilla and Benard (2010) found that actively promoting a meritocratic organizational culture can lead to more discrimination. One interpretation of their finding is that study participants actually did believe that men were more deserving of bonuses than women but rewarded them at higher rates only when they were told that rewarding people based on quality was critical to their own job performance. Without such a nudge people may express a taste preference to treat people equally. It is thus possible that performance-motivated and consumption-motivated discrimination can be triggered and suppressed via a range of different interventions, with economic incentives simply being the most obvious starting point.

Finally, the construct of potential economic consequences is different than “accountability” as it is typically studied in discrimination research. For example, when studying pay disparities in organizations, Castilla (2015: 315) defined organizational accountability as “a set of procedures making certain individuals (or a group of individuals) responsible for ensuring the fair compensation and distribution of rewards among employees.” This falls within a more general social psychology definition of accountability as “pressures to justify one’s causal interpretations of behavior of others” (Tetlock, 1985: 227). Of utmost importance is “accountability for what?” Accountability for diversity in and of itself should be most useful for achieving diversity, but vague accountability for the quality of a decision (thus increasing the economic consequences) might encourage more discrimination.

Beyond discrimination research, this study also speaks to the broader literature on evaluation processes and organizations. The distinction between consumption-motivated and performance-motivated discrimination presented here may be useful to explain why people respond to other forms of status: people may believe status markers help them make better decisions (i.e., facilitate a performance motive) but may also derive direct utility from interacting with high-status actors (i.e., facilitate a consumption motive). For example, Malter (2014) attempted to separate the returns to organizational status in the wine industry into two underlying components: quality signals and conspicuous consumption. He noted of the Podolny (1993) view of status that “audiences would not have to rely on status to infer quality if quality were perfectly observable” (Malter, 2014: 276), but he empirically demonstrated that conspicuous consumption matters (a consumption motive) and that status—at least for producers in the wine industry—matters in its own right independent of quality concerns. Similar results regarding how audiences separately evaluate the symbolic versus objective value of traits have been found in other contexts (Frake, 2017). I complement this and similar research by highlighting that the ultimate importance of such status traits to evaluators should also depend on the economic consequences under which evaluations are made. The evaluation of high-status producers may be motivated by tastes if there are limited economic consequences of that evaluation, but one would not expect the same to be equally true if the consequences were increased. In such cases, status traits become important because they will be used to infer quality, and performance motives should come to dominate the evaluation process. Therefore, while this paper focused on a single individual status characteristic, gender, future work might explore how economic consequences influence the evaluation of other forms of individual and organizational status.

Supplemental Material

sj-pdf-1-asq-10.1177_00018392211029930 – Supplemental material for Economic Consequences and the Motive to Discriminate

Supplemental material, sj-pdf-1-asq-10.1177_00018392211029930 for Economic Consequences and the Motive to Discriminate by Bryan K. Stroube in Administrative Science Quarterly

Footnotes

Acknowledgements

I would like to thank the associate editor and three anonymous reviewers for their constructive feedback during the review process. Earlier versions of the project benefited from feedback from audiences at the University of Maryland, the University of Wisconsin, the University of South Carolina, and London Business School. Financial support was provided by the Center for International Business at the University of Maryland and the Fulbright Student Program.

Supplemental Material

Notes

Author’s Biography

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.