Abstract

Using a nested multiple-case study of participating ventures, directors, and mentors of eight of the original U.S. accelerators, we explore how accelerators’ program designs influence new ventures’ ability to access, interpret, and process the external information needed to survive and grow. Through our inductive process, we illuminate the bounded-rationality challenges that may plague all ventures and entrepreneurs—not just those in accelerators—and identify the particular organizational designs that accelerators use to help address these challenges, which left unabated can result in suboptimal performance or even venture failure. Our analysis revealed three key design choices made by accelerators—(1) whether to space out or concentrate consultations with mentors and customers, (2) whether to foster privacy or transparency between peer ventures participating in the same program, and (3) whether to tailor or standardize the program for each venture—and suggests a particular set of choices is associated with improved venture development. Collectively, our findings provide evidence that bounded rationality challenges new ventures differently than it does established firms. We find that entrepreneurs appear to systematically satisfice prematurely across many decisions and thus broadly benefit from increasing the amount of external information searched, often by reigniting search for problems that they already view as solved. Our study also contributes to research on organizational sponsors by revealing practices that help or hinder new venture development and to emerging research on the lean start-up methodology by suggesting that startups benefit from engaging in deep consultative learning prior to experimentation.

A fundamental challenge for new ventures is accessing, interpreting, and processing the information needed to recognize and realize an opportunity (Stinchcombe, 1965; Artinger and Powell, 2016). Although critical for new venture development (Posen and Chen, 2013; Foss, Lyngsie, and Zahra, 2015), processing external information is challenging for new ventures because venture founders—like all individuals—are prone to boundedly rational behavior (Camerer and Lovallo, 1999; Eggers and Song, 2015; Hallen and Pahnke, 2016). Bounded rationality refers to the idea that although individuals and organizations aim to be rational in their decision making, their ability to do so is hampered by imperfect information and limits in their ability to gather, interpret, and process new knowledge (Simon, 1955; March and Simon, 1958). According to Simon (1955), boundedly rational executives search to generate alternative solutions or ideas until the forecasted performance of an alternative exceeds aspiration levels. But executives are prone to information processing limitations, including cognitive biases (Tversky and Kahneman, 1974; Kahneman, Slovic, and Tversky, 1982; Nickerson, 1998), which left unabated can result in settling on suboptimal solutions.

The Carnegie School has explored how organizations are designed to attenuate the negative effects of executives’ bounded rationality (see Gavetti, Levinthal, and Ocasio, 2007, for a review). Organizations choose designs—“explicit efforts to improve organizations” (Dunbar and Starbuck, 2006: 171)—that reduce cognitive complexity for executives so as to improve firm-level information processing accuracy and speed (Simon, 1947). For example, organizations hierarchically subdivide tasks and information processing (Chandler, 1977). This allows individuals at lower levels of the hierarchy to focus on a narrower set of concerns, while allowing individuals higher in the hierarchy to focus on decisions that span their subunits and to direct the attention of subunits (March and Simon, 1958; Sah and Stiglitz, 1986; Gaba and Joseph, 2013). Firms further improve cognitive processing for executives by adopting designs that promote specialization (Cyert and March, 1963; Grant, 1996) and routines—standardized sequences of activities that are developed over time to increase speed and reliability (Nelson and Winter, 1982). Overall, the Carnegie School suggests that organizations choose designs such that information is accessed, aggregated, and coordinated throughout the firm to decrease the cognitive demands on individuals while improving firm-level decision making.

Despite the wealth of research on bounded rationality, it is not clear how well it applies to new ventures. First, extant work is generally set in large, established firms (e.g., Kownatzki et al., 2013; Foss, Lyngsie, and Zahra, 2015) or is based on simulations of large organizations (Carley and Lin, 1997; Lin and Carley, 1997; Rivkin and Siggelkow, 2003; Siggelkow and Rivkin, 2005; Knudsen and Levinthal, 2007). This leaves open questions about how new ventures address the bounded rationality of their founders, especially given the many novel and complex decisions that new ventures face and their limited ability to use recognized mechanisms such as hierarchy or routines. Second, the Carnegie School and related research focuses on solutions to mitigate bounded rationality within the boundaries of the firm and so pays less attention to solutions that may lay outside of the firm (Gavetti, Levinthal, and Ocasio, 2007), such as those that might be provided by organizational sponsors like venture capitalists, government agencies, science parks, incubators, or accelerators. Yet by simultaneously working with multiple ventures while remaining external to focal firms, organizational sponsors may marshal different mechanisms for mitigating bounded rationality in new ventures.

We leverage a novel organizational sponsor, accelerator programs, to address these gaps. Accelerators are short-term, limited duration, cohort-based educational programs for nascent ventures. Accelerator programs like Y Combinator and Techstars have become increasingly prevalent in the entrepreneurial landscape, and a third of all ventures raising “Series A” venture capital in the U.S. in 2015 had previously been through an accelerator (Pitchbook, 2016). Important from a theoretical perspective, all accelerators try to transmit large amounts of information in a short period through intensive interactions with mentors, potential customers, program directors, guest speakers, and other entrepreneurs. Such intensive access to information is likely to amplify the challenges of entrepreneurs’ bounded rationality by increasing the volume of information to be considered, processed, and interpreted (Simon, 1973; Lin and Carley, 1997). While accelerator programs universally provide access to external information by embedding ventures in information-rich environments, it is not clear what designs accelerators use to structure that information in ways that could help new ventures overcome their founders’ bounded rationality and whether differences in the ways accelerators seek to help their founders overcome bounded rationality are associated with different venture outcomes. As prior research on both mitigating bounded rationality in new ventures and on accelerator designs is limited, we use an inductive theory-building approach and exploit rich qualitative data from the participating ventures, directors, and mentors of eight of the original U.S. accelerators to fill this gap.

Mitigating Bounded Rationality in New Ventures

Bounded rationality builds on three tenets that are critical for our research. First, bounded rationality holds that individuals often have incomplete and partially inaccurate information, such that individuals neither have all relevant knowledge nor do they necessarily know where their mental maps are inaccurate (Simon, 1947, 1955; Gavetti and Levinthal, 2000). Second, bounded rationality holds that individuals are cognitively constrained and are therefore “cognitive misers” (Fiske and Taylor, 1991) who often engage in “satisficing” (Simon, 1955), whereby they stop further search when an alternative appears “good enough.” Third, bounded rationality holds that decision making is often systematically subject to common cognitive biases, such as confirmation bias whereby individuals overemphasize information that is consistent with their beliefs and discount information that contradicts their beliefs, availability bias whereby individuals rely on information that is easy to access, and social proof whereby individuals look to the actions of others to determine how to act (Tversky and Kahneman, 1974; Fiske and Taylor, 1991, Rao, Greve, and Davis, 2001).

While bounded rationality primarily focuses on the limitations of individual actors within the firm, the Carnegie School also considers how organizations mitigate the potentially adverse effects of boundedly rational individuals. It suggests that organizations design information architectures using hierarchy (Simon, 1947; March and Simon, 1958; Sah and Stiglitz, 1986; Jacobides, 2007), specialization (Cyert and March, 1963; Grant, 1996), and routines, rules, and standard operating procedures (Nelson and Winter, 1982). These information architectures help coordinate knowledge throughout the organization and reduce the cognitive processing required of individuals (Knudsen and Levinthal, 2007; Csaszar and Eggers, 2013). The organizational designs suggested by extant work, however, are often unavailable to new ventures as they are generally too small to take advantage of hierarchy and related specialization and too unstable and inexperienced to have established routines and standardized rules (Mintzberg, 1989; Uzzi, 1997). Overall, while a mature body of research details the ways large, established organizations mitigate bounded rationality within their firms, less is known about how new ventures do so.

Entrepreneurial managers differ from managers in established firms in both the type and frequency of boundedly rational behavior (Busenitz and Barney, 1997). First, new venture founders often have limited accumulated knowledge, which can cause them to misinterpret or inappropriately generalize feedback (Eggers and Song, 2015). Lack of accumulated knowledge also requires new ventures to access much knowledge beyond their boundaries (Posen and Chen, 2013), which can be particularly difficult for inexperienced ventures to absorb (Cohen and Levinthal, 1990). Second, new ventures have underdeveloped networks (Hallen, 2008), which may lead to inefficiencies in information processing. For example, Hallen and Pahnke (2016) showed that new ventures’ sparse networks limit an entrepreneur’s ability to accurately assess the quality of potential venture capital investors. Third, new ventures often pursue novel opportunities, such that not only is the knowledge of the founders incomplete, but some requisite knowledge may not exist at all (Eisenhardt and Schoonhoven, 1990; Shane, 2000; Eesley, Hsu, and Roberts, 2014). Fourth, founders’ psychological ownership of ideas may constrain adaptation if feedback on a venture’s plans is interpreted as also threatening founders’ personal identities (Grimes, 2017). Finally, new ventures have little or no historical performance and often lack a suitable industry peer group, making it difficult to know where to set aspiration levels or when to stop search. Moreover, since new firms need to make many core decisions, and the effects of those decisions are likely to persist due to imprinting and path dependency, mitigating bounded rationality is critical for new ventures. Collectively, these arguments suggest that if not allayed, bounded rationality might have an oversized and durable effect on new ventures.

Organizational Sponsors

Most research on mitigating bounded rationality focuses on solutions that are inside the firm’s boundaries (see Uzzi, 1997, for an exception). Consequently, little is known about solutions that are outside the firm, a research focus that is particularly germane for new ventures given their scarce resources, including immature organizational structures, lack of experience, and sparse networks. Organizational sponsors provide resources, including information, to new ventures, and so how they structure the provision of these resources may help ventures with information processing challenges associated with bounded rationality. Like others, we define organizational sponsorship as the “intervention by government agencies, business firms, and universities to create an environment conductive to the birth and survival of organizations” (Flynn, 1993: 129). This definition encompasses different types of sponsors, including incubators, science parks, universities, government programs, franchisors, and venture capital investors (Phan, Siegel, and Wright, 2005; Rothaermel and Thursby, 2005a; Shane, 2012; Amezcua et al., 2013; Dutt et al., 2015; Armanios et al., 2017). Research shows that sponsors provide new ventures with legitimacy via certification, help them develop capacities (Armanios et al., 2017), and provide access to knowledge in the local environment (Amezcua et al., 2013).

While research shows that sponsors such as incubators provide resources and information to ventures, including office space, connections to business services such as legal services and accounting, introductions to local businesses, and sometimes licenses to university-developed technology (Allen and McCluskey, 1990; Hackett and Dilts, 2004), it has not yet examined how sponsors effectively address the cognitive limitations of venture founders. Rothaermel and Thursby (2005a) found that knowledge flows between the sponsor and participating ventures are significant predictors of ventures’ performance, but since they examined ventures at only one sponsor, they did not explore how different sponsors’ designs might influence ventures’ ability to access information from the sponsor. Moreover, while research shows that incubators create information-rich environments that can link ventures to the local ecosystem, it also shows that incubators differ in the survival rate of participating ventures due to the interplay of differences in which services are offered and the density of local entrepreneurial activity (Amezcua et al., 2013). Existing empirical work thus leaves open questions about how organizational sponsors’ designs might help ventures process available information and which designs might be more effective than others.

Research on venture capitalists (VCs) contends that they also help facilitate learning and the improvement of ventures. For instance, investors may help provide advice on operations and strategy (Pahnke, Katila, and Eisenhardt, 2015; Garg and Eisenhardt, 2017), professionalize roles and internal operations (Hellmann and Puri, 2002), and offer connections to customers, suppliers, and other investors that may further help ventures learn (Hsu, 2006; Hallen, 2008; Hallen and Eisenhardt, 2012). Like the research on incubators, this research indicates that such advising ultimately aids ventures’ development, but that venture capitalists vary substantially in their ability to improve ventures’ outcomes (Sørensen, 2007; Fitza, Matusik, and Mosakowski, 2009). While this research suggests that differences in VCs’ impact tend to be persistent, it leaves open questions about how VCs might differ in the way they structure information provided to entrepreneurs or how such differences lead to variance in ventures’ outcomes. Overall, the question of how organizational sponsors may be designed to help new ventures better mitigate bounded rationality remains largely unanswered.

Research Context

Our research setting is accelerators—an increasingly prevalent and important part of the entrepreneurial landscape. Accelerators seek to aid the development of early-stage ventures by providing intensive mentoring and education over short, fixed-length periods to cohorts of ventures (Cohen, 2013; Cohen and Hochberg, 2014). Prominent examples include Y Combinator (Silicon Valley), Techstars (Boulder, Boston, Seattle, London, and elsewhere), and AngelPad (San Francisco and New York). An estimated 6,000 startups have participated in 650 accelerators and have collectively raised over $30B in capital. 1 As noted earlier, a third of all ventures raising “Series A” venture capital in the U.S. in 2015 had previously been through an accelerator (Pitchbook, 2016).

The first accelerator, Y Combinator, was founded in 2005 by Paul Graham, who founded it after delivering a speech about how to start a company to a group of undergraduate students at the Harvard Computer Society. During his speech, Graham suggested that the budding entrepreneurs seek funding from successful entrepreneurs, like him, who had technology backgrounds and could provide advice in addition to money. When the students turned to Graham as a potential investor, he immediately added, “Not me,” but later decided to invest in a batch of eight startups (Lee, 2006). At the time, Graham had limited experience as an angel investor, so he invited more-knowledgeable acquaintances to speak to the group. According to Graham’s blog, batching investments provided unexpected economies, and thus he and three cofounders formed Y Combinator, which continued to batch seed-stage investments and provide advice to each group. Y Combinator was originally located in Cambridge, MA, and later added a Silicon Valley program. Eventually, it closed the Cambridge office and now offers two sessions annually in the Silicon Valley.

One of the first imitators was Techstars, which launched in 2007 with a specific purpose in mind: enhance the entrepreneurial community of Boulder, CO. Techstars batched investments like Y Combinator did but added co-working space and more intensive mentorship. Techstars now has 41 different programs, including vertical programs offered in conjunction with corporate partners such as Amazon, Qualcomm, Target, Comcast, and Barclays. Over 1,300 ventures have participated in one of Techstars’ programs, including SendGrid, the first accelerated venture to complete an IPO.

Unlike other types of investors, accelerators select ventures through an open application process. Interested entrepreneurs submit a written application and often a video providing information about themselves, their business idea, and progress to date. Selected applicants are interviewed, initially via Skype and sometimes later in person (our fieldwork suggests that interviews at both stages are only 10–20 minutes). The level of consideration given to teams prior to admission is thus substantially limited relative to the typical due diligence of angels or venture capital firms. Depending on the program, between 6 and 125 startup applicants join each accelerator cohort. Although accelerators typically provide some capital to participating ventures through equity investments, the sum is generally quite small compared with the investments of most early-stage investors (Wiltbank and Boeker, 2007; Kerr, Lerner, and Schoar, 2014). At the time of our study, a typical accelerator invested $15,000 to $20,000 in two- to three-person startup teams, in exchange for 6 to 8 percent equity. 2 Participating startups often had an initial business idea but usually had not yet received external financing.

Defining characteristics of accelerators are their focus on the quick and intense transfer of information to a cohort of startups that start and end the program together (Hallen, Cohen, and Bingham, 2016). The cohort-based structure contrasts with incubators in which ventures enter on an ongoing basis and exit upon disbanding or outgrowing the incubator space, with average residency between three and five years (Rothaermel and Thursby, 2005b). Though some incubators have recently modified their philosophies, historically they have helped ventures conserve scarce resources by providing physical infrastructure (office space, internet, printers, etc.) and professional services (accounting, legal, etc.) for free or at discounted rates to participants over several years (Hackett and Dilts, 2004; Rothaermel and Thursby, 2005b). In contrast, accelerators aim to accelerate ventures’ progress toward exit by providing extensive information—both directly and indirectly through managing directors, mentors, and peer ventures. One informant equated the experience to “drinking water from a firehose.” To create substantial time pressure and increase ventures’ motivation to learn quickly, accelerator programs organize an impressive graduation event, most often a “Demo Day” when participating ventures present to hundreds of investors, the press, and the local business community. As another venture founder explained, “To be done by September 21st, 500 people get to see it, but if it’s done September 25th [no one sees it].” This combination of intense additional information plus time pressure likely amplifies the challenges of entrepreneurs’ bounded rationality, making it an ideal context for exploring different approaches to structuring external knowledge for entrepreneurs.

Methodology

We rely on an inductive, nested multiple-case study to generate novel theory from data (Glaser and Strauss, 1967; Eisenhardt and Graebner, 2007; Zott and Huy, 2007). Inductive methodologies are appropriate because we are exploring a complex phenomenon that includes inter- and intra-organizational interactions and because accelerators are novel and thus poorly understood but have the potential to make important contributions to theory as well as the “grand challenge” of how to improve new ventures’ outcomes. Specifically, we use an inductive multiple-case methodology because it is particularly effective in research like ours that seeks to develop theory around the underlying relationship between variance in organizational practices, processes, or designs and variance in outcomes (Zott and Huy, 2007; Eisenhardt, Graebner, and Sonenshein, 2016; Garg and Eisenhardt, 2017).

Multiple case studies have the added benefit of replication logic, leading to more parsimonious theory than that developed using single cases (Yin, 2009; Miles, Huberman, and Saldana, 2013). Our multiple-case, embedded design allows us to identify variance across accelerator designs as well as outcomes.

Sample

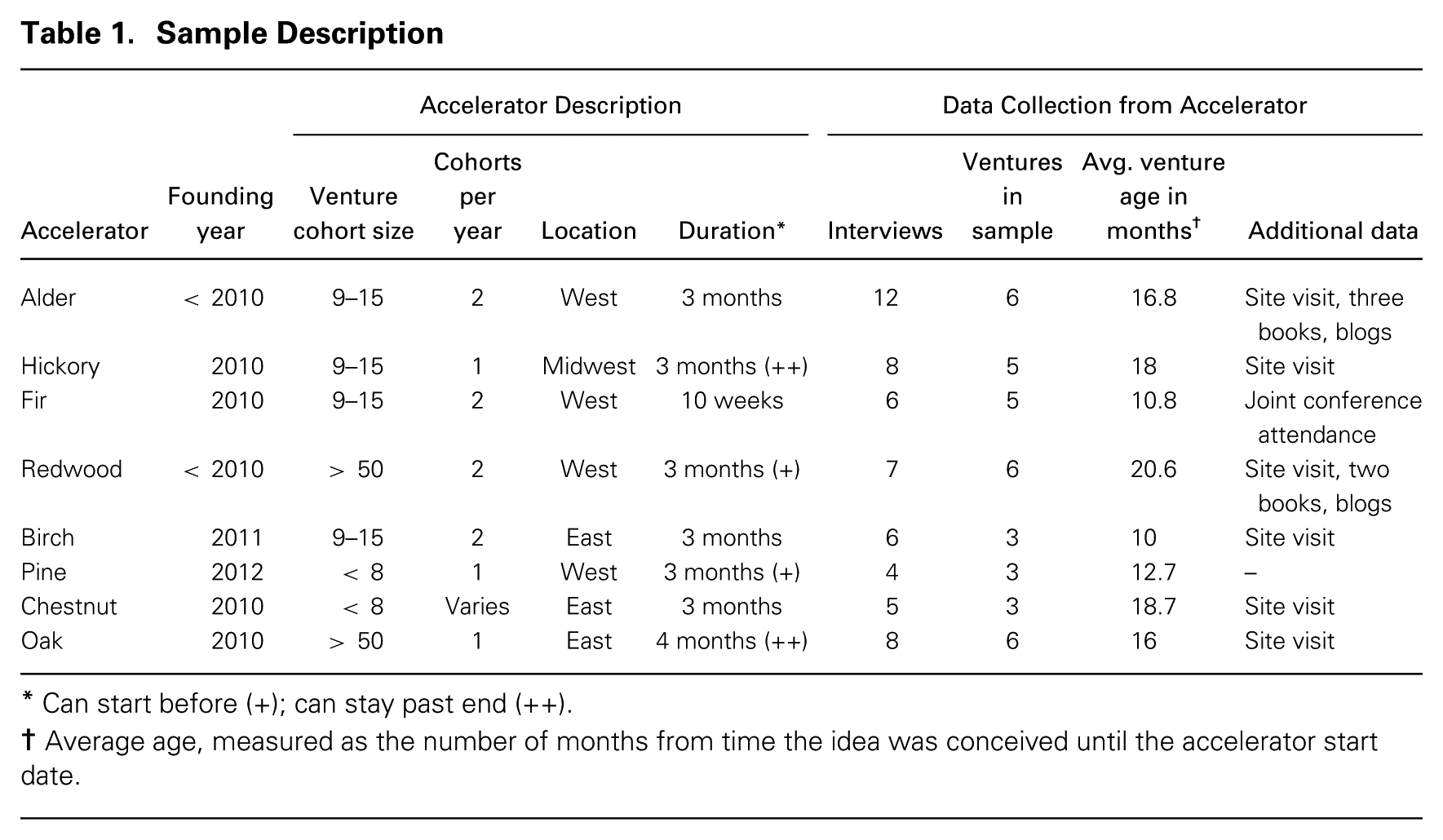

Our sample includes eight U.S. accelerator programs, with 37 ventures nested within the programs (see table 1 for our sample description; accelerator names are disguised with pseudonyms taken from tree names). A strength of our research design is that it nests informants at multiple levels of analysis (accelerator, venture, mentors), which helps explicate different accelerator designs and link differences in designs to variance in venture outcomes. At the accelerator level of analysis, we follow similar multiple-case, inductive studies (Davis and Eisenhardt, 2011; Hannah and Eisenhardt, 2017) that used a “homogenous” sampling strategy to ensure all sampled accelerators had certain theoretically relevant antecedents (Miles, Huberman, and Saldana, 2013); accordingly, we sampled accelerators with strong reputations and that were pioneers (versus newer accelerators) (Battilana and Dorado, 2010). 3 This sampling strategy not only improves the odds of identifying early and potentially distinct organizational designs (Eisenhardt, 1989b; Siggelkow, 2007) but also helps ensure ventures within these accelerators have a certain level of potential (Davis and Eisenhardt, 2011). 4 We further reduced extraneous factors by ensuring that all sampled accelerators operated independently and not inside of another type of organizational sponsor (e.g., incubators), were general-purpose programs (versus focusing on a single industry vertical), and were founded by individuals or small groups of individuals (vs. universities or corporations). Overall, sampled accelerators had a similar goal to promote venture development, making their ability to help founders efficiently and effectively mitigate founders’ bounded rationality important. Given their shared goal of aiding high-potential startups requiring minimal initial capital, all the accelerators in our sample focused on information-technology startups.

Sample Description

Can start before (+); can stay past end (++).

Average age, measured as the number of months from time the idea was conceived until the accelerator start date.

We chose entrepreneur-informants in each accelerator using theoretically driven, within-case sampling. Within-case sampling is used when individuals are nested within a group, for example children within a classroom or patients within a hospital. Within-case selection “should be driven by a conceptual question, not by a concern for representativeness” (Miles, Huberman, and Saldana, 2013: 33). We followed similar work and used polar sampling (Elsbach and Kramer, 2003), which allowed us to explore whether ventures that had better or worse performance described accelerator designs differently. Their descriptions were highly similar.

Data Sources

Data were collected from retrospective and real-time sources (Eisenhardt and Graebner, 2007; Yin, 2009), including transcribed semi-structured interviews; e-mail correspondence for clarification and updates; site visits; attendance at industry events; and archival data such as accelerator and startup websites, blogs, LinkedIn profiles, trade publications, and funding databases like Crunchbase and Seed-DB. We used archival data to supplement interviews and obtain outcome data. Collecting data from multiple sources improves the reliability and credibility of results (Yin, 2009) while site visits help enhance internal validity by offering insight into the behaviors of those in or associated with accelerator programs.

The primary source of data for this study is semi-structured interviews with participating entrepreneurs (e.g., founders of ventures), accelerator directors who run the programs, and mentors affiliated with each program. We conducted approximately 70 interviews of between 45 and 90 minutes each. We took several precautions to reduce bias. All interviews were recorded, transcribed, and analyzed by two of the authors. All informants were guaranteed anonymity and confidentiality to improve the integrity of responses. To improve recall, we relied on informants who were highly involved with the focal accelerator. We followed courtroom style questioning and directed informants to step through their program, beginning with the application process. We then asked what happened between being accepted and starting the program. Next, we asked what happened during the first day, week, month, and so on until the end of the program. Chronologically recounting events helps reduce individual informant bias (Huber, 1985) while also allowing for comparability across informants. Open-ended questions focused on different actors, such as directors, mentors, cohort members, and teammates. For example, we asked founders, “How, if at all, did you interact with your cohort?” We focused on facts, such as the practices that the accelerator used, rather than opinion, to reduce retrospective bias. We took several other steps to reduce bias: we triangulated information provided by venture founders with information provided by mentors and directors; we supplemented interview data with information on company websites and in the press; and we ended interviews by gathering factual information such as the number of employees hired and revenue earned. We conducted additional interviews with industry pundits, investors, directors of other accelerator programs, and venture founders who attended other accelerator programs. We continued conducting interviews until responses no longer added novel insights (Glaser and Strauss, 1967).

Data Analysis

Consistent with inductive research, we began data analysis with a broad lens, seeking to understand what accelerators are and how they interact with ventures. We read magazine articles, stories in industry trade publications (e.g., TechCrunch), popular books, and blog entries written by accelerator directors (e.g., Paul Graham of Y Combinator and Brad Feld of Techstars) and participating startup founders, and we spoke to members of the industry. After this exploratory phase, two of the authors reviewed field notes, transcripts, and other notes and jointly considered many perspectives. Initially we explored how accelerators accelerate learning in new ventures. As we iterated between data and theory, we realized that the bounded rationality of founders should have prohibited ventures from effectively learning quickly. While this was true at some accelerators, other accelerators seemed to overcome such challenges. We thus refocused our inquiry and explored how some accelerators mitigate founders’ bounded rationality.

We developed case histories for each accelerator and then compared each case with the others to confirm or revise emergent theory (Eisenhardt, 1989b; Eisenhardt and Graebner, 2007). One author coded the transcripts using MaxQda (version 11.01), and the other coded them by hand. Each author coded each transcript with first-order codes that indicated design elements chronologically (e.g., pre-program, first month, second month, etc.), including which actors were involved in each part of the program (e.g., mentors, founders). The authors then came together to create combined case histories. Each case included detailed descriptions of events at each accelerator and examples and quotes from the interviews. We triangulated information across informants to verify design elements, sequences, and interactions, and in the rare case when we could not triangulate with existing data, we sent e-mails to informants to clarify. We created extensive charts and tables, and whenever possible we included quantitative, factual data. We also used Excel and PowerPoint software to organize and tabulate data, which included tables, flowcharts, and timelines of each accelerator’s design elements. We then used the case histories for within-case and cross-case analyses.

Because our research explores whether variance in accelerators’ designs leads to variance in ventures’ outcomes, a key focus of our within- and cross-case analyses was identifying differences across accelerator designs. Here we drew on organizational design concepts from the organizational and strategy literatures (Baldwin and Clark, 2000; Siggelkow, 2002). Drawing on Siggelkow (2001), we define design elements as the basic building blocks of an organizational design. Each design element reflects the inclusion or absence of a practice, activity, policy, or structure. An organization’s design is the complete description of that organization’s design elements. Consistent with empirical research recognizing that interdependencies among organizational design elements are often patterned (Rivkin and Siggelkow, 2007), we focused much of our analysis on core design choices. These core choices represent competing designs, with each choice suggesting a different cluster of complementary design elements (i.e., practices, activities, policies, or structures). As an example, we observed that one core design choice the accelerators faced is whether to concentrate or space out consultation—with concentrating suggesting one set of design elements and spacing out an alternative set.

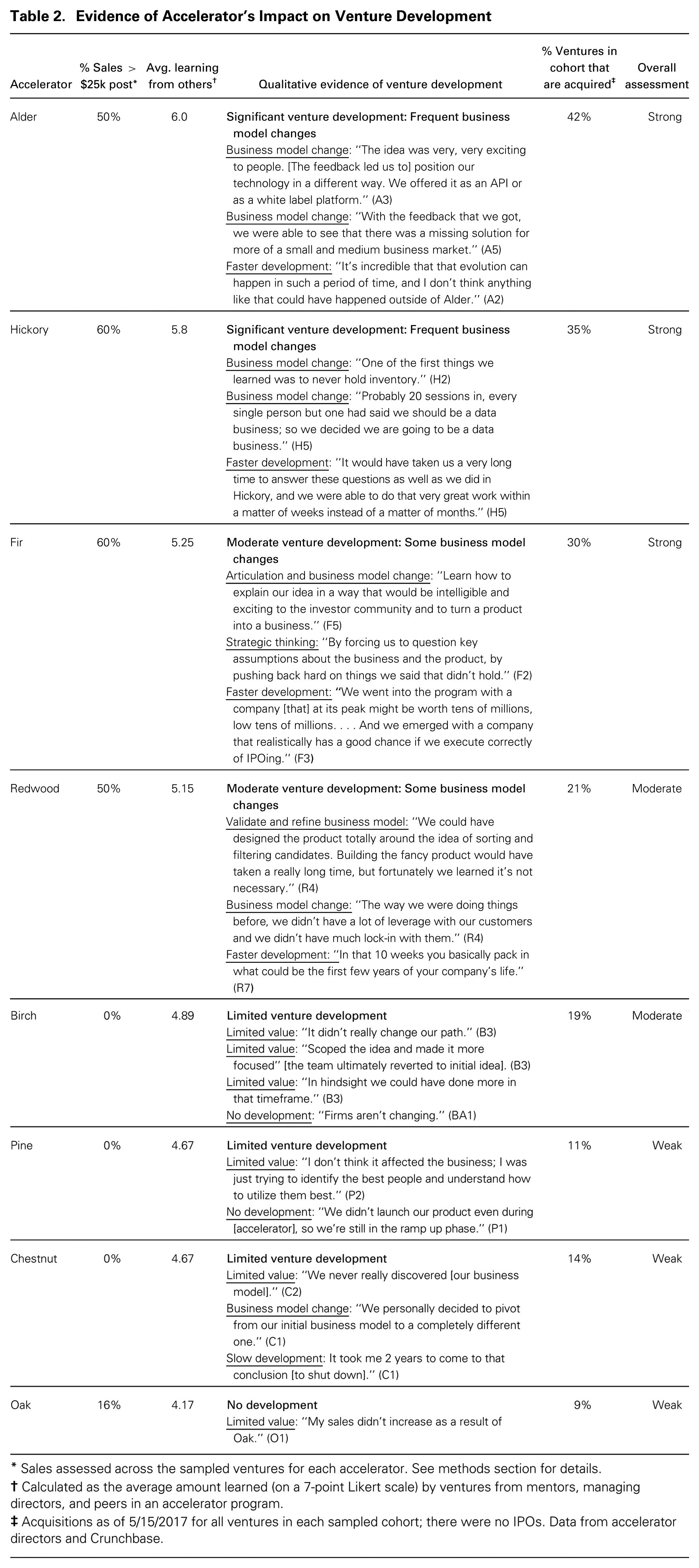

We next considered the impact of different accelerator designs by examining variance in venture outcomes. We began this process by asking our managing director informants how they measured success and triangulated using similar measures (Garg and Eisenhardt, 2017). Most of the directors responded that the ultimate measure of success was profitable exits, either via IPOs or acquisitions. Some also responded that revenue growth was a particularly important early measure because it indicated whether the company had identified product–market fit. These measures are broadly consistent with prior literature (Rothaermel and Thursby, 2005a). We examined the impact of accelerators among our informant ventures using similar short- and longer-term dimensions. First, we calculated the percentage of informant ventures at each accelerator that had over $25K in revenue one year after the program. 5 Second, as part of our wrap-up questions at the end of the interview we asked informants to rate on a 7-point Likert scale how much they learned from key constituents (managing directors, mentors, and their startup peers); we included the average response to indicate how much the venture learned from others during the program. Third, we included qualitative statements indicating evidence of ventures improving their information processing; this often took the form of refinements to their business model or strategy. For example, a Fir founder said, “We went into the program with a company [that] at its peak might be worth tens of millions, low tens of millions. . . . And we emerged with a company that realistically has a good chance—if we execute correctly—of IPOing.” We then triangulated the informants’ data with data from all of the ventures in each of the cohorts in which our informants participated. Specifically, we measured the percentage of ventures in each cohort that had exited via acquisition as of August 2017 (there were no IPOs) (Hochberg, Ljungqvist, and Lu, 2007; Garg and Eisenhardt, 2017). Collectively, data across these different dimensions indicate that ventures in Alder, Hickory, and Fir generally performed well, while the ventures in Redwood and Birch performed more moderately. Our data show that the performance of ventures in three other accelerators, Pine, Chestnut, and Oak, was lower. Table 2 summarizes evidence of the accelerators’ performance in developing ventures, supported by quotes from informants. Informants are identified by the initial letter of the accelerator, followed by an “A” if they were an accelerator director, “M” if they were a mentor, or a number if they were a venture founder. When multiple accelerator directors or mentors were interviewed, we assigned each one a sequential number.

Evidence of Accelerator’s Impact on Venture Development

Sales assessed across the sampled ventures for each accelerator. See methods section for details.

Calculated as the average amount learned (on a 7-point Likert scale) by ventures from mentors, managing directors, and peers in an accelerator program.

Acquisitions as of 5/15/2017 for all ventures in each sampled cohort; there were no IPOs. Data from accelerator directors and Crunchbase.

After within-case analysis, we engaged in cross-case analysis, which centered on comparing ventures’ experiences across different accelerator programs. In both within-case and cross-case analyses we used replication logic to confirm and develop emergent theory (Yin, 2009). As constructs (second-order themes) emerged, we recoded the data and created tables with quantitative information and illustrative quotes using the emergent constructs. We compared constructs across accelerators, refining emerging theory as cross-case analysis provided new insights.

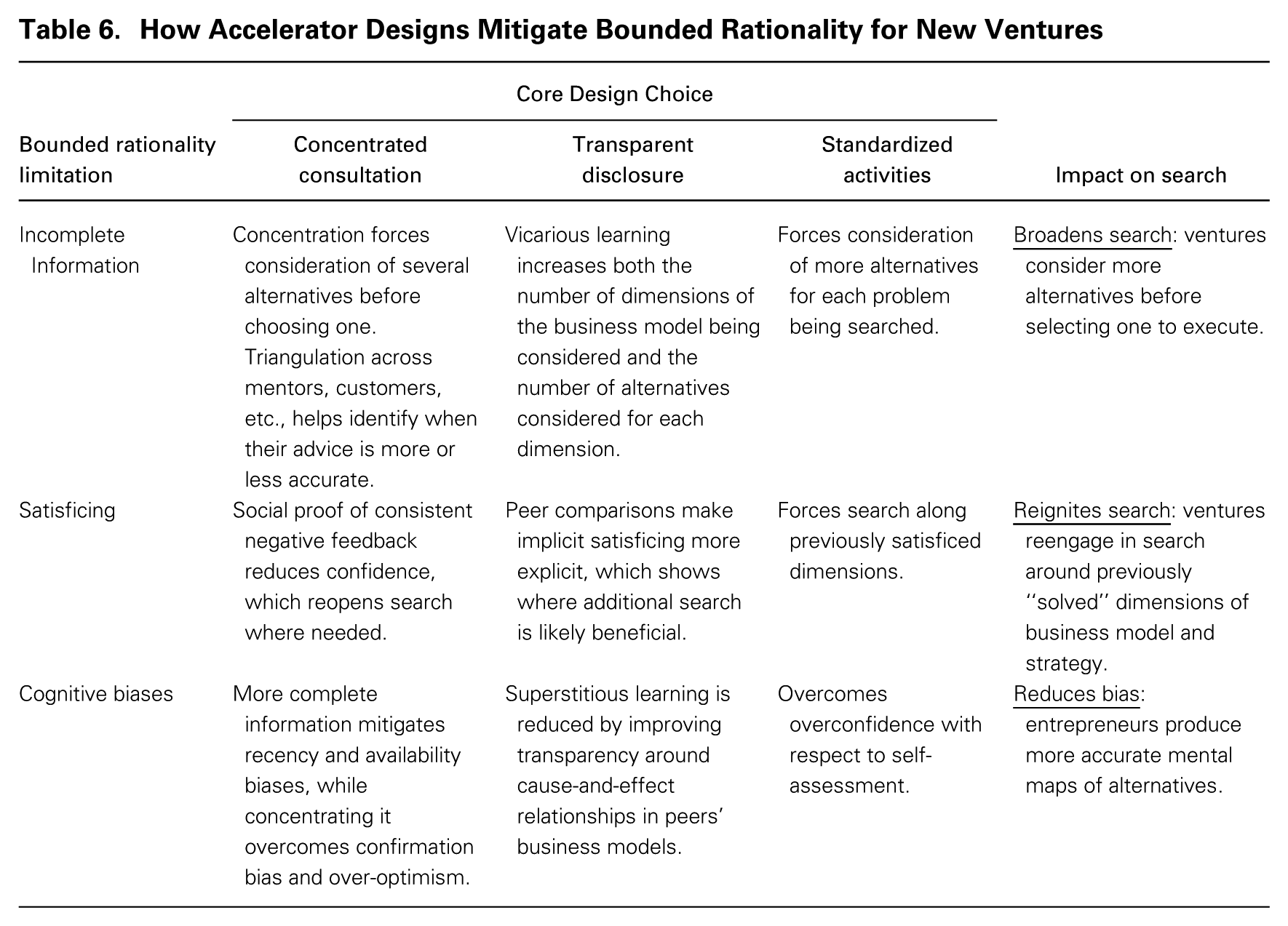

Emergent Theoretical Framework

Our data reveal that accelerators exhibited three core design choices that collectively influence their approach to addressing entrepreneurs’ bounded rationality. The three core design choices were (1) whether to space out or concentrate consultations (consultation intensity), (2) whether to foster private or transparent disclosure (disclosure level), and (3) whether to tailor or standardize the program for each venture (extent of customization). Each design choice was associated with a reinforcing set of design elements. For example, all of the accelerators that spaced out consultations adopted a similar set of design elements that encouraged ventures to space out interactions, and all those that concentrated consultations adopted a different set of design elements that encouraged ventures to concentrate them. Below, we describe each core design choice and related design elements and then compare the performance outcomes of accelerators with different core design choices. In each instance, one core design choice was consistent with the prescriptions of extant literature and the other was not. Interestingly, it was the choice that deviated from prior literature that best mitigated founders’ bounded rationality. We draw on these patterns to build theory.

Consultation Intensity

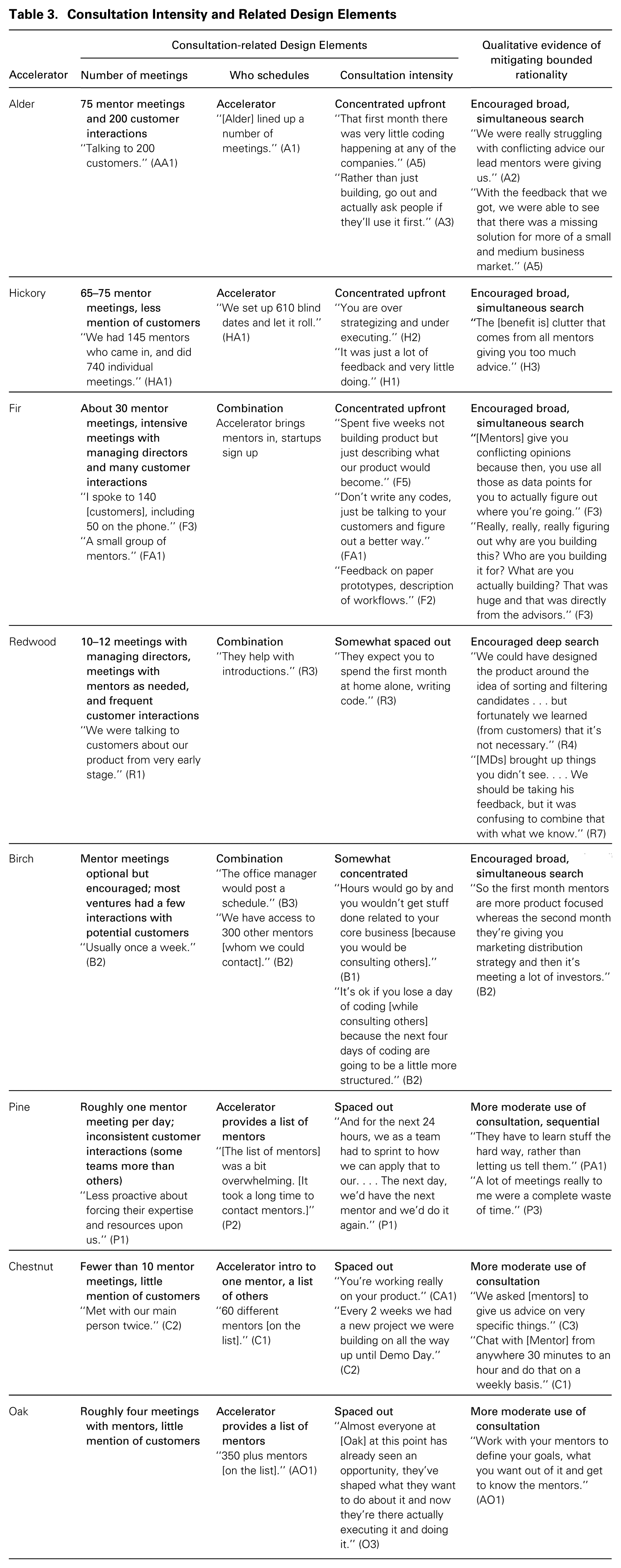

Consistent with research on open innovation (Laursen and Salter, 2006; Foss, Laursen, and Pedersen, 2010; Lakhani, Lifshitz-Assaf, and Tushman, 2013) and the learning benefits of social networks (Powell, Koput, and Smith-Doerr, 1996; Yli-Renko, Autio, and Sapienza, 2001), all accelerators encouraged ventures to consult with customers and mentors about their products and businesses, and all had similar types of mentors—including current and former entrepreneurs, corporate executives, potential suppliers, lawyers, accountants, and investors. Accelerators varied, however, with respect to the intensity of such external consultations, one core design choice. One group of accelerators encouraged ventures to space out consultations with external sources, while the other group of accelerators encouraged ventures to temporally compress such consultations at the start of the program. We thus define spaced-out consultation as those designs that lead ventures to spread interactions with mentors and customers evenly over the course of the program and concentrated consultation as those designs that lead ventures to gain feedback in an intense period preceding implementation. We assessed design choices about consultation intensity by the design elements that accelerators used to manage consultations, mainly (1) the number of consultative interactions during the program, (2) whether the interactions were scheduled by the venture or the accelerator, and (3) whether accelerators concentrated consultations upfront or spaced them out throughout the program. To help assess the impact of this choice, we also provide qualitative evidence in table 3 of how entrepreneurs engaged in search under each form of consultation.

Consultation Intensity and Related Design Elements

Extant research suggests three key benefits to temporally spacing out consultations. First, consultation that is spaced out may allow a complementary interweaving of external advice with experimentation that would allow founders to iterate between learning from others about current plans and implementing selected advice to test it (Ries, 2011). By spacing consultation out over the program, ventures could complete many cycles of advice and testing. Such designs may be especially beneficial for high-growth ventures as it might allow them to develop unique insights about the novel elements of their opportunity (Gavetti and Rivkin, 2007). Second, temporally spacing out consultation would allow for greater knowledge absorption, stemming from reduced information overload and greater time for reflection and review after each external interaction (Levitt and March, 1988; Dierickx and Cool, 1989). Finally, research suggests that limiting consultative inputs may improve decisions by reducing cognitive complexity (Mintzberg, 1973; Eisenhardt, 1989a).

Consistent with theory, several accelerators chose to space out external consultations and adopted supporting design elements, such as assigning a single mentor to meet with each team at regular intervals and providing a list of mentors that ventures could contact as needed. Spacing out consultations also allowed sufficient time between consultations for ventures to interweave consultation with implementation. Chestnut provides an illustration. Startups at Chestnut met with a handful of mentors over the three-month program, which left ample time for “doing” product development between meetings. For example, one startup, which we call Chestnut-2, had raised a small amount of money prior to relocating from the West to the East Coast to join the accelerator program. The three-person team had ten meetings with mentors over the course of the program, which left time to implement mentors’ advice between meetings. The founder said, “You get a list of people that all want to be mentors for you and then you have your main person. We met with our main person twice. . . . From there I had ongoing meetings, two meetings per mentor throughout the summer, about 10 or so meetings across 5 to 6 mentors.”

In contrast, another set of accelerators made a different design choice: concentrating consultation. Accelerators that concentrated consultation adopted a reinforcing set of design elements, such as arranging for ventures to meet with over 50 mentors who came to the accelerators’ offices and requiring ventures to interact with hundreds of customers during the first month of the program. Consultation with mentors at these accelerators typically consisted of one-on-one meetings in which founders shared their current thinking about their business model, often by delivering a short pitch. Mentors then provided critical feedback and information deemed potentially helpful. Accelerators that concentrated consultation often provided guidance on how to access customers, including providing access to alumni who might also be potential customers. Because concentrated consultation was most often front-loaded and time-intensive (vs. spaced out over the course of the program), ventures at accelerators that concentrated consultation paused product development by several weeks while they were conducting consultations. Delaying product development this long is particularly striking because these ventures had to postpone learning from trial-and-error experimentation—a central tenant of the lean startup methodology—for roughly one third of their program’s duration.

Alder is an example of an accelerator that chose to concentrate consultation. Ventures met with an average of 75 mentors and up to 200 customers during the first month of the program, which did not leave time to interweave consultation with building products, even minimally viable ones. Alder-3’s experience illustrates this. This venture began the program by speaking to a wide range of potential customers. The founder explained he “talked to travel companies that range from small to large, from hotel chains, OTAs [online travel agencies], airlines.” At the same time, the team extensively consulted with mentors. Another founder at Alder related her experience: “[Mentor meetings] were usually 15 to 30 minutes long, and they were usually with new mentors. They call it ‘mentor dating.’ You would basically pitch what your idea was. . . . In an ideal world, you would be getting as much feedback as possible, getting their thoughts, getting an understanding of why they don’t understand something or why they think something won’t work or if they think something else is a better idea.” She said that her venture had “between three and five meetings a day for basically the first four to five weeks.”

Hickory is another accelerator that chose to consolidate consultation. Hickory scheduled 65–75 mentor meetings for each venture during the first three weeks of the program and encouraged startups to speak to many potential customers. Venture founders at Hickory attended four or five mentor meetings per day, accumulating feedback from each on their firm’s value proposition. A Hickory startup founder recounted that “the first month was intense. We did 54 mentor meetings in the first 30 days.” Hickory’s managing director explained, “Mentor dating month we had 145 mentors who came in, and did 740 individual meetings this year, so 10 companies for on average 74 meetings per company in the month of June, and that’s when their business plan gets torn apart. It’s all about them and their business plan.”

We found that the core design choice on consultation intensity matters. Although extant literature favors spacing out consultations because it allows for complimentary trial-and-error learning and better absorption and reduced cognitive complexity, ventures at the accelerators that spaced out consultations had lower performance and more processing errors (i.e., Pine, Chestnut, and Oak). Returning to the example of Chestnut above, Chestnut ventures met with mentors throughout the program and interwove consultations with building products based on advice. The Chestnut-2 CEO recalled, “I was taking in every mentor’s piece of feedback and that led to way too many changes for me and my team . . . every two weeks we had a new project we were building all the way up until Demo Day.” Yet despite acting on mentors’ advice, Chestnut-2 was never able to gain traction with customers or investors, and this was generally the pattern we observed: in accelerators that encouraged spacing out external consultation, ventures often had difficulty knowing when—and when not—to incorporate feedback.

By contrast, ventures at the accelerators that concentrated consultations had higher performance and improved information processing (i.e., Alder, Hickory, and Fir). A founder at Alder explained that the abundance of mentor feedback collectively helped his venture “get off a track that was not going to be successful and may have taken us six or nine months to find out [if we had relied on experimentation].” The team then consulted with other firms in its supply chain and with mentors to generate alternative business models. It eventually adopted a more promising B2B business model. Similarly, a founder at Hickory told us that the first several mentor meetings revealed a key cash-flow issue with his venture’s initial business model: “One of the first things we learned was to just never take inventory. We had a plan to look like a distributor for [industry] and take inventory. We very quickly took that off our list of to-dos [since we learned it is] a horrible business.” Realizing this flaw reinitiated search; the team then consulted with its customers to identify a more promising offering. The founder continued, “We started realizing the problem isn’t just selling stuff to these people. The problem is they don’t even know how to do these projects themselves, so we said that for them to be successful in their contract businesses, all these small businesses need technology to automate the way they do business, and that’s how we backed into building software to support independent [industry small businesses].” The team focused on implementing this refined product during the remainder of the program.

Concentrating consultation led to higher performance for several reasons. First, it helped entrepreneurs expand and improve the effectiveness of their search, encouraging them to “reignite search” by searching along dimensions of their business model and strategy that they otherwise were likely to view as sufficient. We observed that entrepreneurs had often prematurely satisficed, settling on suboptimal solutions for many aspects of their business models and strategies. We define premature satisficing as occurring when a modest amount of additional search would likely have yielded a far more attractive solution. Although specific instances of premature satisficing can be difficult to identify, we were able to observe an overall tendency toward premature satisficing by contrasting the extent to which entrepreneurs varied in their search and the attractiveness of the identified solutions.

While individual mentors and customers often pointed out issues arising from premature satisficing, we observed that entrepreneurs often resisted such feedback when it challenged their existing plans. This is consistent with both the confirmation biases of all individuals (Lord, Ross, and Lepper, 1979; Staw, 1981) and with entrepreneurs’ tendencies to be overconfident (Camerer and Lovallo, 1999; Dushnitsky, 2010) and to resist feedback that threatens their identity (Grimes, 2017). Accelerators that concentrated consultation short-circuited these biases by providing founders a novel form of social proof—one that builds when the opinions of many others conform with each other to reduce confidence in one’s own opinion (Cialdini, 1993; Rao, Greve, and Davis, 2001). 6 Moreover, as individuals tend to overweight recent information (Tversky and Kahneman, 1974), the time compression of feedback also made triangulated social proof more salient. The overall effect of concentrating consultation on reigniting search is well summarized in the commentary of Hickory’s managing director: “Part of the process is literally breaking them [startups] down, and getting them to the point where they aren’t that arrogant startup saying, ‘My idea is the best idea in the world.’ They realize that there’s so much more to it, and that they really only have the seed of an idea.” Such reignited search is a valuable form of problemistic search in that it is “stimulated by a problem . . . and is directed toward finding a solution to that problem” (Cyert and March, 1963: 121). Whereas the literature on problemistic search has generally focused on problems identified by current performance falling below aspirations (Greve, 2003), we observed that some accelerator designs revealed problems with plans that had not yet been put into practice, and time-compressed feedback prompted further search.

Second, for ventures that were actively searching for solutions, concentrating consultation encouraged entrepreneurs to search more broadly prior to execution. The underlying challenge here was that even when entrepreneurs identified a dimension of their business model or strategy they wished to improve, they often considered only a small set of alternatives and then satisficed prematurely. Concentrating consultation forced them to learn about multiple potential solutions (i.e., alternative competitive positions or pricing strategies) without having time to implement each one. The experience of an Alder venture illustrates this. The founder recounted the evolution of their business model during the first month of the program. He said, “We realized there’s no way this is going to work. We [then] went through a lot of different things. We thought ‘What if we had a mobile app? What about if we either did this or did that?’ and we got to where we were. . . . That first month was very painful . . . taking this [information] from our mentors, from customers, from all sorts of everybody.” Overall, we observed that accelerators that concentrated consultation helped ventures overcome confirmation and experience biases by developing a more complete set of strategic choices (Gruber, MacMillan, and Thompson, 2008) before implementing any of them. Concentrating consultation encouraged them to engage in more efficient cognitive search prior to relatively costly trial-and-error experimentation (Gavetti and Levinthal, 2000).

Finally, it should be noted that despite these benefits, concentrating consultation was often initially confusing and frustrating for founders. An Alder founder told us, “Before the program you had a pretty good idea about what your company was doing. A week into the program, you have no idea at all what the f*** your company is doing.” One accelerator named the resulting confusion “mentor whiplash” because advice steers ventures in seemingly opposite directions at nearly the same time. This also meant that the benefits of concentrating consultation were often not apparent to entrepreneurs until after a certain amount of consultation—a point we return to in a later finding. As a whole, though, concentrating consultation was more likely to result in better business models and strategies because it allowed ventures to triangulate across many sources of information. This made search more effective by helping ventures determine when mentors or customers had improved insight or when these sources were offering misinformation based on idiosyncratic experiences or spurious causal relationships (Levitt and March, 1988; Denrell, 2003). Concentrating consultation made triangulation across advice easier and any differences more apparent. This helped entrepreneurs better identify misinformation, so as to avoid overreacting to inappropriate guidance. As Hickory’s managing director explained, “In the short run, it’s totally confusing and overwhelming, but in the long run, they come out stronger and smarter.”

Disclosure Level

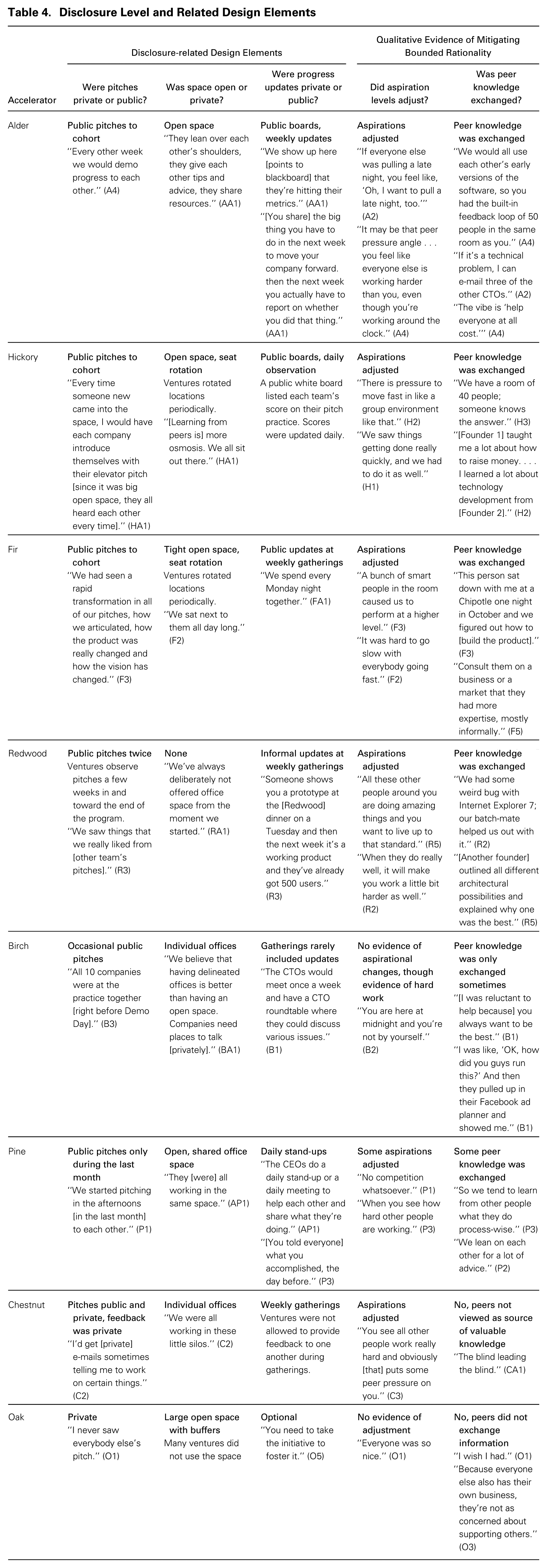

Consistent with prior work, we found that accelerators viewed peer ventures as a vital source of information (Cyert and March, 1963; Levitt and March, 1988; Haunschild and Miner, 1997). An important core design choice thus relates to disclosure—the degree to which accelerators promoted sharing information across ventures in the same cohort. We found that many accelerators were concerned that mandating disclosure might either cause founders to become protective of private information or force the disclosure of information that would otherwise provide a competitive advantage to the disclosing venture (Pahnke et al., 2015). Accordingly, two design options emerged from the data analysis. The first is fostering privacy, which we define as designs that reduce information exchange between ventures and instead emphasize protecting private information such as ventures’ behavior and performance. The second is fostering transparency, which we define as designs that emphasize peer interaction and result in the disclosure of ventures’ behavior and performance. We assessed disclosure level by examining the following design elements: (1) Did ventures practice their pitches in private or public? (2) Was the office space closed or open? and (3) Were progress reports delivered privately or publicly? To help assess the impact of this core choice, we also provide qualitative evidence of resulting changes in aspiration levels and peer knowledge exchanges in table 4.

Disclosure Level and Related Design Elements

Extant research suggests that designs that increase privacy and thus reduce the amount of sharing between ventures are likely preferable in information-rich environments (Simon, 1973; Huber, 1991). Reducing information sharing may allow mutual trust among ventures to develop over time, which would increase incentives for collaboration so that important and relevant information is eventually exchanged (Messick and Mackie, 1989; Pfeffer and Langton, 1993; Peteraf and Shanley, 1997), but irrelevant information remains private and so produces fewer distractions (Simon, 1973). Also, keeping important information private helps firms maintain their competitive advantage (Pahnke et al., 2015). Consistent with this research, several accelerators chose designs that fostered privacy by reducing information exchanges between ventures. At these programs, work areas were often private, either consisting of individual offices or an open floorplan with buffer space that allowed for privacy, and cohort-wide events were informal in that they provided an opportunity for venture founders to mingle, but ventures decided what information to disclose, when to do so, and to whom.

Oak exemplified a design that fostered privacy. It provided opportunities for founders to interact but allowed them to develop trust over time and decide when and how much to disclose. A managing director of Oak explained their philosophy when designing the program: “We were afraid of creating a negative vibe.” Instead of forcing ventures to share information, Oak’s directors thought that creating a friendly, collaborative environment would allow ventures to build trust over time and eventually share important information. At 30,000 square feet, the open office space was massive, which created a physical buffer around each team. Oak also protected each venture’s privacy by having ventures deliver their pitches “absolutely in private.” Moreover, when ventures interacted with each other at social events, the accelerator did not require ventures to disclose any information to their peers. A founder said, “[Oak] does a good job of setting up events and things so you naturally interact with your peers, nothing is really formal in that way. . . . [Oak] plants the seed to help nurture those relationships, and then you need to take the initiative to foster it.” When founders did interact, they were careful about sharing private information. A founder explained, “There was always that feeling of how much can I share in this open space that isn’t going to let out my secret sauce or be a competitive threat potentially.”

In contrast, other accelerators adopted designs that fostered transparency between ventures. They had ventures pitch to their cohort, attend regular cohort-wide meetings, update public boards to display progress, and follow other norms of publicly sharing progress. For example, each Alder cohort included between ten and twelve ventures. Participants were required to post weekly target metrics on a public display board, informing others of their goals and how they performed against those targets. Additionally, at weekly meetings, startups declared what they planned to accomplish during the following week to “move their company forward” and reported their progress to the group the next week. Actions that might be considered bragging in other contexts were acceptable, even encouraged by Alder’s director. She explained their philosophy: “We publicly surface progress that will put pressure on other teams to execute too.” Even the cramped office space increased transparency; teams worked so close to one another that it was hard to distinguish between them, making it easy for startups to monitor each other’s progress. Founders described the program as having “a lot of peer pressure,” resulting from design elements that “exposed progress” by the startups.

Redwood, a large accelerator with over 80 firms per cohort, was also designed to foster transparency. Like Alder, Redwood’s program exposed each startup’s progress to the cohort. For example, during the second week of Redwood’s program, Redwood directors arranged “prototype day,” when startup founders publicly showcased their demonstrations (sometimes minimally viable products and sometimes presentations) to their cohort. Weekly gatherings at Redwood’s offices offered a regular opportunity to see peers’ progress. One founder (Redwood 6) explained that weekly gatherings were “six to eight hours of just spending time talking to each other.” Another founder initially tried to keep the details of his company’s strategy private at weekly gatherings, but his venture quickly adjusted to the strong norms of sharing information. He explained, “Within 20 minutes of being surrounded by all these other founders . . . the ones who have been around . . . quickly pointed out that our being secretive is not going to help us and we just took their advice. We were just basically like these infants with slight brains, and we were very willing to just absorb.” Finally, the week prior to Redwood’s Demo Day, founders rehearsed their pitches in front of the cohort and received feedback from the program directors. A Redwood-3 founder explained, “We saw presentations from other companies, and we saw things that we really liked from those, then we got feedback from the [accelerator] partners on our presentation.” Although Redwood had large cohorts and ventures did not share working space, the accelerators’ practices and strong culture of sharing progress updates with peers motivated ventures to adjust their aspirations according to peers’ aspirations and progress and fostered learning among peers, while those at Oak—a similar-sized accelerator with a shared office—were unable to do so.

We found two different accelerator design choices related to disclosure, which is important because though prior research suggests the value of learning from others, it has not examined disclosure directly nor has it examined whether and how much different levels of disclosure matter. Surprisingly, we found that ventures at the accelerators that fostered privacy (e.g., Birch, Chestnut, and Oak) had lower performance. While the aim of fostering privacy was for ventures to build up trust and eventually share information, it did not seem to be as effective as fostering transparency. When we asked an Oak founder about learning from the cohort, she said, “It was hard for me to learn from them” and then later added, “I wish I had.” This pattern was reflected across our sample. When accelerators fostered privacy between ventures such that voluntary collaboration was emphasized but transparency was not, ventures were less likely to learn from their peers. By contrast, when accelerators fostered transparency, ventures helped each other and achieved higher levels of performance (e.g., Alder, Hickory, Fir, Redwood, and Pine). A founder at Alder’s comment is indicative of founders at these programs: “The vibe is ‘help everyone at all cost.’” Moreover, and despite the initial concerns of many accelerator program directors, we were not informed of any instances in which transparency facilitated the leakage of key sources of competitive advantage. Instead, proactively increasing transparency appeared to reduce concerns about direct competition, because it uncovered key differences between ventures and helped entrepreneurs recognize that their ventures were less similar than initially perceived.

It was apparent in our entrepreneur interviews that transparency also encouraged entrepreneurs to work harder. As one told us, “You want [your peer ventures] to do really well, but when they do really well, it will make you work a little bit harder as well.” Another Redwood founder said, “Someone shows you a prototype at the [Redwood] dinner on a Tuesday and then the next week it’s a working product and they’ve already got 500 users. It doesn’t get much more motivational than that.” Yet this seemed to only partially explain the benefits of fostering transparency, as working harder could have entrepreneurs moving faster in the wrong direction.

Rather, a key impact of fostering transparency was expanding and improving the effectiveness of entrepreneurs’ search via external information for refinements to their business model and strategy. First, fostering transparency reignited search related to dimensions of the business model or strategy that were already viewed as “good enough.” When accelerators provided greater transparency into the performance levels along a range of dimensions for ventures across the entire cohort, entrepreneurs often recognized where they may have engaged in premature and suboptimal satisficing (Simon, 1955). A Redwood director’s comment illustrates: “People who might come into the program thinking, ‘Oh, we’re so far along. We’re a little bit more advanced than most people that you fund’—once they start seeing what the other people are building, they’re kind of like, ‘Oh wait, I’m not as far along as I thought’.” The information provided by peer ventures helped entrepreneurs assess when additional search could produce substantial performance improvements, often reigniting search along a number of performance dimensions.

Second, fostering transparency also encouraged founders to search more broadly and consider more alternatives in areas where they were already engaging in search, because they could first observe the behaviors and outcomes of all of the ventures in their cohort and only then decide which ones to imitate. A founder at Alder explained that as ventures demonstrated leadership in certain areas by reporting progress in public, other ventures knew where to go for help: So certain teams make progress in certain areas faster than others. For us, for example, it was fundraising; we were early in the fundraising and it felt really good because we moved a lot further forward than some of the teams. . . . One of the things that I appreciated the most was I was so jammed with my schedule with so much to do—and so was everyone else—but I received help from so many different people throughout the program. I mean, they would stop what they were doing, working on their dream idea, and talked to us about you know—certain people in the program had expertise in pricing—certain people had expertise in software development. They would stop and talk to us at length about that, and then we would do the same with others in our areas of expertise.

Yet while research has long recognized that social networks between organizations may be an effective means for established firms to obtain some private information (Haunschild, 1994; Beckman and Haunschild, 2002), our data revealed that creating social networks among entrepreneurs is not sufficient. Concerns about competition inhibited mutual trust, and such concerns were often aggravated when accelerators tried to respect ventures’ privacy. Fostering transparency, though, laid a foundation for entrepreneurs to search more broadly by better understanding the experiences and knowledge across many of their peer-cohort ventures.

Third, fostering transparency also encouraged more effective search by improving the accuracy of entrepreneurs’ mental maps of potential alternatives. While entrepreneurs often seek to learn from competitors and peers, this information may be incomplete as other ventures are privately held (reducing information disclosure requirements), young (reducing media exposure), and often operating in “stealth mode” to avoid public attention. Thus entrepreneurs may be able to observe some of the behaviors or market actions of other ventures, but not the resulting performance. This may make vicarious learning for entrepreneurs especially prone to superficial understanding and making erroneous causal linkages (March, Sproull, and Tamuz, 1991; Denrell, 2003; Eggers and Song, 2015). In contrast, fostering transparency improves entrepreneurs’ understanding of cause-and-effect relationships between peer ventures’ business model decisions and performance outcomes. Fostering transparency also helps ventures know what strategies not to try. A Hickory founder’s experience illustrates this. Her venture was considering expanding into a particular product market but decided not to do so based on the experience of another venture: “We saw how hard it was for them to break into that sector—we are not touching that with a ten-foot pole.”

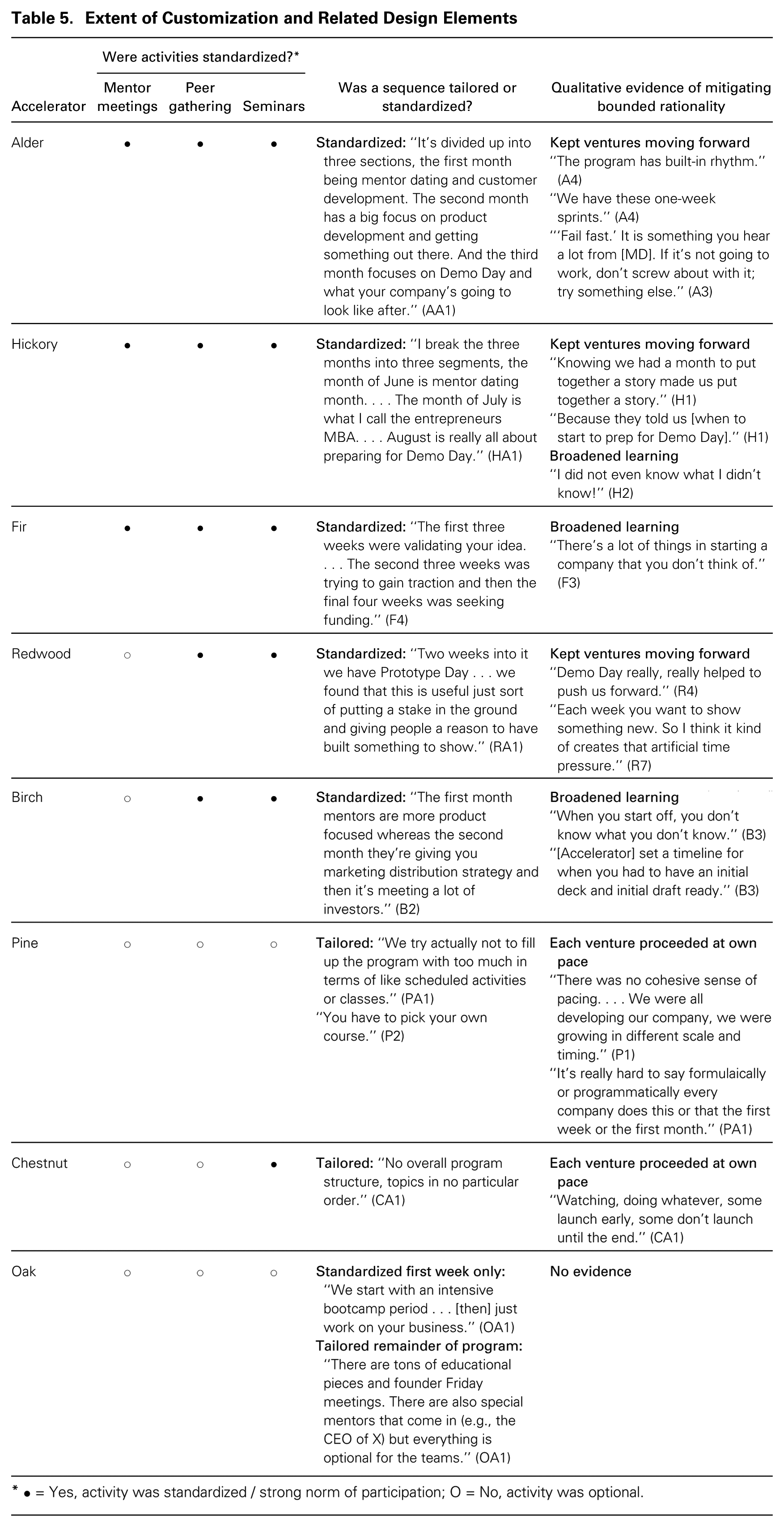

Extent of Customization

All accelerators in our sample offered similar types of learning activities for ventures, including mentoring sessions, lectures, and workshops with successful entrepreneurs, program alumni, investors, and professional experts (e.g., lawyers, accountants, marketers); peer gatherings; and meetings with the accelerators’ managing directors. They differed, however, in the extent to which they customized these activities, or the degree they allowed ventures to decide what activities to attend based on their perceived needs. We found that some accelerator program designs tailored activities, encouraging ventures to follow individualized programs to address their unique knowledge and needs, while others standardized activities, requiring a uniform set of activities and sequence of focus for all ventures. Table 5 assesses the extent of customization by examining whether accelerator designs required ventures to (1) choose their own mentors or meet with assigned mentors, (2) interact with their cohorts on an ad-hoc basis or attend regularly scheduled peer gatherings, (3) choose which seminars to attend or attend a prescribed set of seminars, and (4) follow a standardized sequence of activities. Finally, we examined the impact of customization on venture development. See table 5 for a summary of the design elements for the extent of customization and its impact.

Extent of Customization and Related Design Elements

• = Yes, activity was standardized / strong norm of participation; O = No, activity was optional.

Prior literature highlights the benefits of customization. It suggests that the knowledge requirements for each venture are idiosyncratic because founding teams have different levels of relevant past experience, and different entrepreneurial opportunities require different types of knowledge (Eisenhardt and Schoonhoven, 1990; Burton, Sorensen, and Beckman, 2002; Gavetti and Rivkin, 2007; Eesley, Hsu, and Roberts, 2014). Customization is also useful because information tailored to each venture is more likely to provide strategic value, encourage adaptation, and lead to valuable business attributes (Barney, 1991; Eckhardt and Shane, 2003; Gavetti and Rivkin, 2007). Besides potentially taking ventures in the wrong direction, activities that are not customized may further reduce ventures’ development by taking time away from more critical activities (Eisenmann, 2006). In accordance with this logic, many accelerators tailored activities.

Oak’s design featured tailored activities, and the entrepreneurs chose activities based on their perceived needs. The managing directors assembled over 200 opportunities for startups to attend workshops, guest speaker events, and informal networking events with mentors and then encouraged founders to chart their own course. To help ventures decide what to choose, each activity was coded by the target industry and life-cycle stage. Codes helped ventures process the abundance of options, but it was ultimately up to the venture to decide which events to attend. The managing director explained, “It’s not one size fits all. . . . So if you want to go to that session, great. If you don’t want to go to that session, that’s still your thing.” A founder added, The program is like an MBA. It is what you make of it. You can choose to go to class every day and go home and do your homework every single night and get straight As and try to leverage the resources and career services to get a new job, or you can choose to get involved in extra-curricular activities, you can socialize with your peers, you can go to networking events at surrounding schools, and you can really take advantage of relationships with professors that can help you outside of the classroom. . . . I think it has to do with people prioritizing on what they want to get out of it. If you choose to only focus on your business and not show up, [Oak] cannot control that.

Another way that accelerators tailored activities was by encouraging ventures to decide how to sequence available information sources. For example, Oak’s program started with a week-long boot camp that provided an overview of the entrepreneurial process and available resources. An entrepreneur at Oak-1 explained that boot camp “had just these amazing speakers who were famous entrepreneurs and masters talking about all the different things you needed to know to start a business and to make your business successful and get funding and get mentors.” After boot camp, each venture decided how to sequence accessing available resources based on its unique goals and objectives. A director from Oak explained, “The first month is all about get settled, work with your mentors to define your goals, what you want out of it, and get to know the mentors and all the resources.” Based on each venture’s individual goals, the founders then decide which parts of the program to attend.

Accelerators that tailored activities generally tailored mentor relationships as well. For example, Oak gave each venture a list of over 350 mentors with various backgrounds and then hosted informal events for mentors and entrepreneurs to mingle and then decide on their own how to proceed. The director explained, “When the program starts we probably throw around five to seven mentor matching events . . . just meet and greet with the mentors.” Overall, Oak does not force any venture to meet with any mentor. The director said, “We don’t specify that you have to work with this mentor, right. We want it to be a two-way match. There’s an online list and it’s not just a list, it’s a searchable database.” Each venture team could decide how much time to dedicate to and which resources to use to find and meet mentors.

In contrast, other accelerators chose designs that standardized activities despite differences in participating ventures. Hickory’s managing director said, “The problem is there are different [metrics] for different companies. So, some of the companies, it’s really a big deal to have some acquisition cost, and revenue per customer whatever. Other of our companies had no revenue.” Yet instead of allowing each venture to create its own path, the Hickory directors created a standardized sequence that all startups followed: the first month startups met with a large, diverse group of mentors; the second month, startups attended seminars on general business topics such as marketing, public relations, and fundraising and spent a significant amount of time building their product or service; the last month, startups developed and refined their pitches in preparation for Demo Day, when they pitched their business to potential investors. The director explained, “I break the three months into three segments: the month of June is mentor dating month. . . . the month of July is what I call the entrepreneur’s MBA . . . August is really all about preparing for Demo Day.” The standardized program sequence pushed all teams to move forward together. A founder said, “It’s very easy to get stuck in a decision or a problem and just kind of sit there and spin your wheels, and not really know what to do, and having people around [doing the same things] helps you snap out of that, and pick a direction—just get going.” Hickory also had a standardized approach to matching ventures with mentors. Instead of allowing entrepreneurs to select the mentors they believed could help them the most, each mentor met with each firm and vice versa. One of Hickory’s managing directors explained why by retelling a story: So one of our companies the first year was [venture, product] for churches, social networks, and fundraisers, and we had a mentor who was the VP of Marketing for Playboy. And the CEO [of venture] said “I can’t meet with him,” and we said “Why not?” He said, “Because he is at Playboy, and my church—if my customers found out that I had a mentor from Playboy, they would blackball me. I’d never be able to do business with churches again. I can’t be associated with Playboy.”

The managing director pushed the venture founder to go to the meeting. He recalled, “[The CEO] walked out of the meeting an hour later and said ‘That was the best meeting I had all summer long.’ It turns out that the person who is the EVP of Marketing for Playboy is actually an avid churchgoer. He has been thinking about building a social network for his church and was in the process of leaving Playboy. . . .” The managing director concluded that he would have all ventures meet with all mentors because “It’s really hard to predict who is going to have chemistry with whom.”

Like Hickory, Fir used a standard sequencing of activities for each venture, though the sequence was somewhat different from that at Hickory. Fir’s director explained the program sequence: “[We begin with the] very big picture like what are you, why are you doing this, what’s your motivation? Why these markets, why not something else, what do you really know about these markets? . . . In the middle we have a very intense kind of ‘build stuff’ period, where it’s just heads down and coding, with very few meetings. . . . The last part it’s really leading up to Demo Day, so preparation for fundraising.” To demarcate each transition, each venture was required to present to the entire cohort. As one founder said, “We had three big Friday presentations—we had the first Friday and then three weeks after that and then another three weeks after that.” Moreover, the accelerator held mandatory weekly meetings each Monday night in which industry luminaries engaged in question-and-answer sessions.

We found the choice to tailor or standardize activities matters. Unexpectedly, ventures at the accelerators that followed the advice of extant literature and tailored activities had lower performance (e.g., Pine, Chestnut, and Oak). Ventures at the accelerators that followed standardized activities had higher performance (e.g., Alder, Hickory, and Fir) because they expanded and improved the effectiveness of founders’ search for refinements to their business model and strategy. First, standardizing the sequence of entrepreneurs’ activities forced them to reconsider dimensions of their business model and strategy when they had already satisficed, sometimes unknowingly, and focused exclusively on refining a particular dimension of their plan to the exclusion of other dimensions. Standardized sequencing forced entrepreneurs to periodically turn their attention to different parts of their businesses. Such consideration often forced an explicit consideration of satisficing that had often been made implicitly, and revealed areas where reigniting search might dramatically improve future performance. Even though each venture had unique information needs, a standardized sequencing was effective because each venture also faced many common challenges. As a venture founder at Alder explained, “Your idea can be unique, but the process you go through with building products, finding—gaining traction, and raising money is very similar.” Notably, the high-impact accelerators each had somewhat different sequences, though they all started with broad search activities, which became narrower over time. This suggests that the act of enforced sequencing and not necessarily the particular sequence may be what reignites search along dimensions where entrepreneurs have implicitly satisficed.

Second, standardized activities also forced entrepreneurs to search more broadly in areas where they were engaged in search. As illustrated by the Hickory entrepreneur not wanting to meet with the Playboy executive, entrepreneurs often discounted the relevance of particular activities. When given flexibility about which activities to attend, they often chose fewer activities, engaged in more limited search, and reduced their opportunity for serendipitous insights. In contrast, a standard set of required learning activities forced entrepreneurs to explore more broadly and to consider a greater range of alternatives for each problem. Such action also addresses the subtle but substantial issue that while accelerator directors can tailor content for each venture, their limited understanding of each venture means they are likely to make errors. By standardizing sequencing, directors ensured all ventures accessed a range of information sources.

Third, standardized activities made search more effective by providing a foundation that reinforced concentrating consultation and transparency, both of which went against the natural inclinations of many founders who worried that concentrating consultation would slow down execution while providing only limited relevant information. Likewise, the activities enabling transparency were time consuming, and founders worried transparency would risk leakage of key information to potential competitors. Standardized activities forced all entrepreneurs to engage in these complementary and salutary practices.

Discussion