Abstract

Organizational theorists have extensively documented the increased likelihood that two organizations will form a relationship if they have preexisting relationships with the same third party, a phenomenon known as triadic closure. They have neglected, however, the importance of the shared third party in facilitating or reversing this process. I theorize that the collaboration outcomes and competitive concerns of the intermediary spanning an open triad play a crucial role in whether that triad closes. Using a longitudinal dataset of the investment decisions of limited partners investing in U.S. venture capital firms in the period 1997–2007, I find that an intermediary is less likely to facilitate a direct connection under two conditions: (1) the intermediary has experienced failed collaborations with one of the indirectly connected parties or (2) the intermediary has competitive concerns—driven by its replaceability and relative attractiveness—that it may lose future business to one of the indirectly connected parties. The paper goes beyond the conceptualization of indirect ties as passive scaffolding that supports creating direct ties and instills a greater appreciation for the role of the intermediary that sits across them.

The factors that drive partner selection have been a long-standing research interest among organizational scholars studying collaborative relationships, including strategic alliances (Gulati, 1995b; Stuart, 1998; Ahuja, 2000; Mitsuhashi and Greve, 2009), investment banking syndicates (Baum et al., 2005; Shipilov and Li, 2012), and venture capital syndicates (Trapido, 2007; Sorenson and Stuart, 2008; Zhelyazkov and Gulati, 2016). A central finding of this research is that two actors are more likely to establish a tie if they share a common partner, a phenomenon known as triadic closure (Simmel, 1950). This tendency has been documented across numerous empirical settings (Gulati, 1995b; Chung, Singh, and Lee, 2000; Sorenson and Stuart, 2001) and is foundational to many models of long-term industry network evolution, particularly the tendency to develop densely interconnected clusters of local relationships (Gulati and Gargiulo, 1999; Baum, Shipilov, and Rowley, 2003; Sytch, Tatarynowicz, and Gulati, 2011).

In explaining closure, extant research has generally focused on how the presence of a shared partner can create opportunities for indirectly connected actors to establish direct collaborations with one another (Rogan and Sorenson, 2014). A shared partner can provide the setting in which the two parties can meet or can introduce them directly to one another (e.g., Feld, 1981; Gulati, 1995b). A shared partner can also endorse the two parties to each other and thus alleviate any concerns about the other’s capabilities and motivation (Larson, 1992; Uzzi, 1996). Although such theories help explain the perspective of indirectly connected parties, they completely ignore the attitudes and motivations of the intermediary that stands between them. Instead, prevailing research on triadic closure has largely presumed that the intermediary by default plays the role of a selfless tertius iungens (Obstfeld, 2005), who is always willing to introduce, connect, and endorse its former partners, without regard to the particularities of the relationship or its own strategic motivations.

By contrast, I propose that two important factors could limit an intermediary’s willingness to introduce and endorse an exchange partner to its other contacts. First, collaboration outcomes can shape the intermediary’s assessment of its collaborator. In particular, a failure of the relationship can engender negative information, which can be passed to other contacts and decrease their willingness to engage with the intermediary’s collaborator. Second, the intermediary’s competitive concerns can constrain its willingness to facilitate connections for a collaborator to its other partners if the intermediary believes that the collaborator could potentially displace it as the preferred exchange partner of the other partners. Such competitive concerns will be especially acute when the collaborator and the intermediary are similar, and thus easily substitutable, and when the collaborator is relatively more attractive as an exchange partner than is the intermediary.

I theorize and test these ideas in the context of the matching between venture capital (VC) firms and capital providers, also known as limited partners (LPs). Both organizational theorists and finance scholars have long studied the investment and syndication patterns of VC firms (e.g., Podolny, 2001; Sorenson and Stuart, 2001, 2008; Trapido, 2007; Hochberg, Ljungqvist, and Lu, 2010; Hochberg, Lindsey, and Westerfield, 2015). To date, however, limited attention has been paid to the VC’s upstream relationships with the LPs, which tend to be large financial institutions, such as foundation and university endowments and public and private pension funds (for exceptions, see Hochberg and Rauh, 2013; Hochberg, Ljungqvist, and Vissing-Jorgensen, 2014). Selecting high-performing VCs is critical to such institutions due to the high dispersion of returns within the industry (Kaplan and Schoar, 2005). In this empirical context, I focus on the effect of the LP–VCA–VCB indirect ties—in which an LP (the “evaluator”) has a prior investment with VCA (the “intermediary”), which has a syndication relationship with VCB (the “evaluatee”)—on the LP’s decision to subsequently invest in VCB. I supplement the quantitative analyses with qualitative insights from interviews with five LPs and eight venture capitalists on the fundraising process.

Triadic Closure and the Role of the Intermediary

Triadic closure—defined as the tendency of actors sharing ties with the same actor to disproportionately form and maintain ties among themselves—dates to Simmel (1950) and is a highly influential concept in sociology. Granovetter’s (1973) seminal work on weak ties was based on the premise that triads with weak ties are less likely to close. Triadic closure is an elementary process of network evolution and is at the heart of creating small worlds (Watts, 1999; Baum, Shipilov, and Rowley, 2003). In interorganizational network research, triadic closure has been documented in various settings, including strategic alliances in several industries (Gulati and Gargiulo, 1999; Powell et al., 2005), venture capital syndication (Sorenson and Stuart, 2001), and investment banking syndication (Baum, Shipilov, and Rowley, 2003). Although much of this research has focused on horizontal networks in which all members of the triad play the same role, evidence is mounting on closure in what Shipilov and Li (2012: 473) called “multiplex triads,” in which one of the actors is a different type of organization than the other two. For example, a shared client can introduce two investment banks (Shipilov and Li, 2012), or a VC firm can facilitate an alliance between two of its portfolio companies (Lindsey, 2008).

Closure can be driven under some circumstances by entirely passive mechanisms such as attention and familiarity, particularly in settings in which actors cannot communicate, for example due to anti-trust concerns (Wang, 2010; Rogan and Sorenson, 2014). 1 Much of the existing scholarship, however, has highlighted the intermediary’s active role in playing the role of tertius iungens or “the third who joins” (Simmel, 1950; Obstfeld, 2005: 102; Obstfeld, Borgatti, and Davis, 2014). The key argument of this research tradition is the assumption that collaborative ties breed trust, attachment, and positive relationships among the parties involved, which then carry over at the triadic level as they introduce and endorse each other to other contacts (Larson, 1992; Uzzi, 1996). For example, the intermediary can introduce the evaluator and the evaluatee, making them aware of the potential for a beneficial match (Gulati, 1995b). To illustrate this process in my context, a limited partner shared an anecdote about a premier VC firm organizing receptions that brought together many of its investors and syndication partners, which served as a setting for informal contacts. Venture capital firms that are introduced to the LPs in this setting can leverage the informal connection to warm call the LP and thus attract its attention more effectively when seeking funding.

Furthermore, endorsements and referrals from shared partners are crucial to evaluating prospective alters (Gulati and Gargiulo, 1999; Shane and Cable, 2002). The presumption is that direct interactions between actors give them insights into each other’s qualities and character and that they will communicate such information truthfully when interviewed during due diligence. In the VC context, while LPs have significant access to hard data on the investment performance of the VCs in which they are considering investing, they attach much importance to soft information. Raw performance numbers make it difficult to assess VCs’ contributions to the successes and failures of deals, as well as strengths and weaknesses that may affect their performance going forward. Conversations with industry practitioners suggested that calls to target VCs’ co-investors with which the LP has prior relationships are crucial to the due diligence process. Said one LP, “[Other VCs] provide the best sort of feedback, because they see the VC in action, both at the negotiating table and in the boardroom. . . . They can give you insights you cannot see from the cold, hard data.” Another LP emphasized, “My starting point when I conduct a due diligence is to check with whom they have been working. . . . And if I happen to know some [of their syndication partners], they are the first people I call.” 2

Although the LPs are the ultimate decision makers about whether to invest in a particular evaluatee VC firm, intermediary VCs can play a subtle but important role by steering their attention via introductions or improving their opinion of the evaluatee by providing a favorable assessment. Also, intermediary VCs have some incentives to use their position to facilitate a connection between their exchange partners, because they can strengthen their relationship with the evaluator LP by being helpful in its due diligence process and benefit indirectly from the success of their syndication partners. In the words of one informant, “You want your good co-investors to be successful. If you want to invest together in the future, you want them to have the capital to participate in the deals.” So, in aggregate, the prediction of the closure literature—that indirect ties via an intermediary VC would increase the likelihood of an LP investment in the evaluatee VC—constitutes a compelling null hypothesis in the present study.

At the same time, however, I propose that there are two factors that could completely negate or reverse the tendency toward closure. First, the collaboration outcomes between the intermediary and the evaluatee can significantly shape the intermediary’s assessment of the evaluatee and affect its willingness to put its reputation on the line in making an introduction or a referral. Second, the intermediary’s competitive concerns—especially about whether it would lose business to the evaluatee in the future—can create powerful incentives to prevent closure between the evaluator and the would-be competitor.

Collaboration Outcomes

Despite well-documented evidence of a history of collaboration on trust, commitment, and affect between collaboration parties (e.g., Kollock, 1994; Gulati, 1995a; Uzzi, 1997; Lawler, 2001), actors participating in collaborations such as VC syndicates aim to achieve a business objective rather than just feel good with one another. As such, competence-based trust—believing that the collaborator has the capability to deliver what is expected—is extremely important in such settings and is constantly assessed in the course of the interaction (Ring and Van de Ven, 1992; Mayer, Davis, and Schoorman, 1995). Failure of the collaboration is often assessed either as poor competence of or poor fit with the partner and reduces the likelihood of a repeat tie in other settings ranging from investment bank syndicates (Li and Rowley, 2002) to film production (Schwab and Miner, 2008). This can be true even in the VC setting, in which actors are accustomed to high-risk deals and frequent failures. In the words of an informant, “. . . everyone likes a winner. If you have had a successful exit, you are going to forgive and forget your co-investors’ missteps. After a failure—even if it is not really their fault—you may still dwell on it, and their shortcomings would loom that much larger.”

Diminished assessments are likely to have negative implications for triadic closure because introducing or referring an actor puts the intermediary’s own reputation on the line if that actor underperforms (Gulati and Gargiulo, 1999). Such reputational concerns prevent employees from referring even close friends and family members to their employers if they have significant concerns about the quality or reliability of those referrals (Smith, 2005). Similar dynamics are especially likely to play out in the VC setting, where reputational concerns are particularly strong and venture capitalists depend heavily on their LPs. In fact, all VC informants with whom I spoke confirmed they would not hesitate to voice reservations they have about the collaboration partner to their LPs. Thus I expect that the intermediary’s negative evaluations that the failure engenders are likely to reach the evaluator LP and reduce its willingness to transact with the evaluatee VC.

Furthermore, diminished assessments of the partner can reduce the expected likelihood of future collaboration and therefore the intermediary’s motivational investment in the evaluatee’s future success. The weaker expectations of future collaboration can be compounded by relationship frictions, which often emerge in the course of failed collaborations and have been amply documented in other settings (Doz, 1996; Arino and de la Torre, 1998; Azoulay, Repenning, and Zuckerman, 2010; Chung and Beamish, 2010). As one of my informants noted, failure can often bring out the worst in people and strain relationships: “When things go downhill, sometimes the board dynamics can turn really ugly. . . . Some people crack under pressure more easily than others, and differences of opinion on how to fix the situation can become personal.” Such tension can have direct implications on the willingness of the parties to provide introductions and referrals for each other (Huntley, 2006) and may further color the already negative information the intermediary is likely to pass to the evaluator.

Finally, the collaboration failure not only provides a fair basis for a diminished assessment of the partner that can be passed to other contacts, but it also creates strategic incentives to emphasize the partner’s weaknesses. To the extent that an intermediary is concerned about its contacts’ evaluation of its ability, it may be willing to deflect attributions for the failure away from itself. As one venture capitalist explained, “In the end, the LPs are your clients, and you need to stand there and explain to them why they lost money on that deal. So, if you can blame it on anything beyond your control—the entrepreneur, the markets, the co-investors—you might be tempted to do it.”

Taken together, these arguments suggest that failures in the relationship between the intermediary and the evaluatee should reduce or even reverse the positive effect of the indirect tie on the probability that the evaluator would select the evaluatee (hereafter referred to as triadic closure).

Competitive Concerns

In unquestionably accepting the idea that indirect ties will increase the likelihood of forming direct ties, theorists studying closure rarely consider the incentives of the intermediary to faithfully play the tertius iungens role and actively facilitate the formation of ties between partners. The implicit assumption pervading the literature is that the intermediary can strengthen its relationship with both partners by facilitating a mutually beneficial connection, but this is not the only type of incentive faced by intermediaries in open triads. In fact, we know that actors can also benefit from keeping their counterparties separated, a behavior known as tertius gaudens or “the third who enjoys” (Simmel, 1950: 154; see also Burt, 1992). The starting point for this literature is that actors can extract brokerage rents for facilitating an indirect exchange between disconnected partners (Ryall and Sorenson, 2007). Examples of brokerage rents include fees that placement agents extract from VC firms for access to LPs (Rider, 2009), costs to employers and temporary employees for the matching role of staffing agencies (Fernandez-Mateo, 2007; Bidwell and Fernandez-Mateo, 2010), or the recognition and improved career outcomes that accrue to those who take ideas originating in one cluster of the network to a disconnected cluster (Burt, 1992). In all of these cases, intermediaries prefer that their partners remain only indirectly connected, because direct connections would result in the brokerage rents dissipating (Ryall and Sorenson, 2007; Buskens and van de Rijt, 2008; Tatarynowicz and Keil, 2016).

Although preserving brokerage rents is the most commonly studied driver of tertius gaudens behavior, such behavior can also result if the intermediary wants to preserve its connection with one of the parties and considers the other party a potential competitor (Lee, 2015). The intermediary is therefore less likely to facilitate a connection between the evaluatee and the evaluator if the evaluatee can credibly replace it in the future as the evaluator’s sole exchange partner. Venture capitalists are not immune from such pressures; in the words of a seasoned venture capitalist, “VCs can be very protective of their LPs, especially when they are concerned with their own future.” Such protective behavior can manifest in two ways. An intermediary can refrain from introducing the evaluatee to the evaluator or bringing them together in a common venue, for example, not inviting them to the same reception. More important, the intermediary can actively hinder the evaluatee’s chances by skewing the information it provides to the evaluator during the due diligence process. Soft information can be rich and illuminate dimensions not easily captured with hard data; however, this richness also increases the range of interpretations and the intermediary’s ability to emphasize negative over positive dimensions depending on strategic motivations (Dunning, Meyerowitz, and Holzberg, 1989; Schweitzer, 2002).

Two orthogonal drivers of competitive concerns of the intermediary could trigger tertius gaudens behavior: the higher replaceability of the intermediary with the evaluatee and the higher relative attractiveness of the evaluatee over the intermediary. Replaceability is based on the type of offerings the intermediary and evaluatee provide. It addresses whether the evaluator can drop the relationship with the intermediary and still receive substantively similar offerings from the evaluatee. Replaceability is thus fundamentally driven by similarity. Both organizational theorists and strategists have long recognized similarity in terms of resource bases (e.g., Sørensen, 2004), knowledge endowments (e.g., Podolny, Stuart, and Hannan, 1996), and product offerings (e.g., Hannan and Freeman, 1989) as key drivers of competition (for a comprehensive review, see Ingram and Yue, 2008). Because actors can switch easily between similar exchange partners, some organizations explicitly maintain ties with multiple similar partners to keep them honest and have a credible option if they terminate the relationship (Baker, 1990). Conversely, it is in the best interests of the partners to minimize such rivalries (Baker, Faulkner, and Fisher, 1998).

In the VC context, such pressures loom especially large given LPs’ diversification objectives. Because most LPs want to avoid excessive concentration in any specific area (such as industry or geography), VCs that are similar in terms of investment profile tend to compete for the same narrow sliver of an LP’s assets. Even if both receive their share of the LP’s investable capital, two similar VCs are highly replaceable, which means that the LP preserves the ability to reallocate its capital to one or the other VC with minimal disruption to the overall structure of its portfolio. This is an implicit threat that the intermediary VC has an incentive to minimize. I therefore expect the formation of a direct tie between the evaluator and the evaluatee when the evaluatee has similar offerings to the intermediary and can thus more easily replace it if the evaluator decides to cull its portfolio of relationships.

Relative attractiveness concerns the expected quality of an exchange partner’s offerings. In many exchange settings, quality is unobservable before an exchange; however, when it is observable after an exchange, actors can use the prospective exchange partner’s reputation—based in part on its track record of performance—as a signal of the future quality of its offerings (Shapiro, 1983; Weigelt and Camerer, 1988; Rao, 1994). If an evaluatee has a higher reputation than the intermediary and forms a relationship with the evaluator, it can represent a competitive threat that can undermine the intermediary’s future position with the evaluator (Baker, 1990; Rogan and Greve, 2015). Research has documented how competitive threat can prompt organizations to discriminate relationally and withhold exchange opportunities from higher-status would-be rivals (e.g., Jensen, 2008). I extend these arguments to the triadic setting by arguing that the intermediary would do its best to impede tie formation between the evaluator and evaluatees with a higher reputation, which can become potent competitors in the future:

Concerns about replaceability and relative attractiveness are likely to magnify one another’s effects. One can think of the intermediary’s replaceability as a correlate of the evaluator’s ability to replace it with the evaluatee with minimum disruption and switching costs; the relative attractiveness reflects the evaluator’s incentive to do so. The lower reputation of the intermediary relative to the evaluatee may not be as threatening if the two are providing completely different services such that the evaluator cannot simply replace one with the other, and both can conceivably have a place in the portfolio. Similarly, high overlap between the evaluatee and the intermediary need not be threatening to the intermediary if it has a higher reputation than the evaluatee. In this case, the evaluator could readily replace the intermediary with the evaluatee if it wished, but there is no reason to do so given that the intermediary is the more attractive option. It is only when the relative attractiveness of the intermediary is lower that it needs to be concerned about its replaceability.

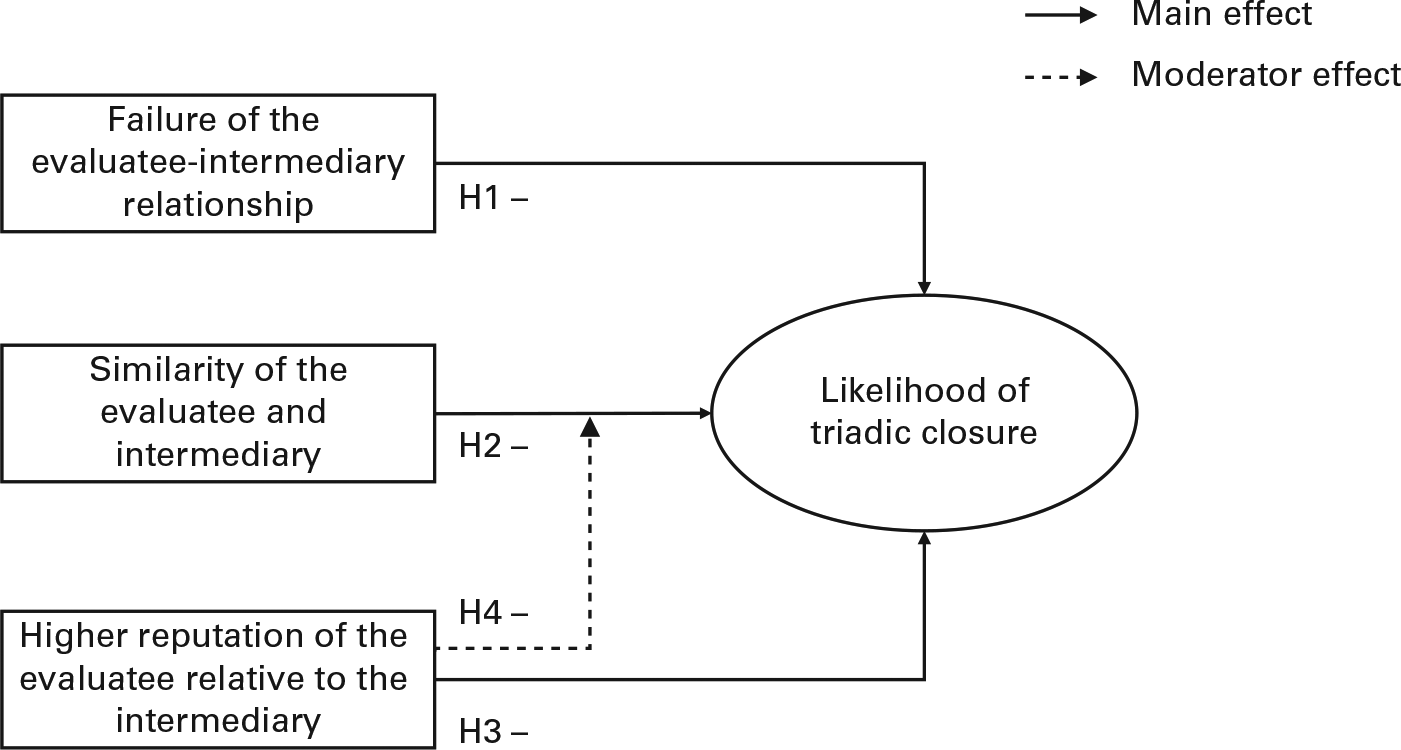

Figure 1 illustrates the theoretical framework of the paper, with the three key independent variables—collaboration outcomes, replaceability, and relative attractiveness—on the left-hand side and the dependent variable—likelihood of closure—on the right-hand side. H1 predicts that a failure of the relationship between the intermediary and the evaluatee should decrease the likelihood of closure. H2 and H3 predict that the key drivers of competitive concerns—similarity to the evaluatee and the higher relative reputation of the evaluatee, respectively—should individually reduce the likelihood of closure, whereas H4 predicts that they will reinforce each other’s effects.

Summary of the hypotheses.

Methods

The Setting: LPs’ Relationships to VCs

I investigate the mechanisms of triadic closure in the context of the investment decisions of limited partners (LPs) investing in venture capital (VC) firms. The VC industry can be conceived as a value chain in which capital cycles from the original investors (LPs) to the capital intermediaries (VC firms) to investment targets (companies in need of financing) and then back to the LPs following a successful exit. The LPs include a variety of deep-pocketed capital providers such as university and foundation endowments, private and public pension funds, the investment offices of wealthy individuals or families, and funds of funds.

Successful VC firms aim to raise a new fund every three years, typically attracting a mix of new and repeat investors. Top firms such as Kleiner Perkins and Sequoia typically have more willing investors and typically ration the access to their funds. Beyond the small group of elite VCs and the LPs that have access to them, the fundraising process is a challenge for both sides. One venture capitalist I interviewed noted, “. . . the fundraising process takes me at least as much time—and certainly more stress—than the investing side. This is the one time I feel what it is like to be in the shoes of the entrepreneur pleading for money.” On the LP side are the challenges of evaluating the most promising investments. Funds are typically raised before the final results of the previous two or three funds are revealed, and interim performance figures are sensitive to accounting assumptions and virtually unrelated to the final performance (Hochberg, Ljungqvist, and Vissing-Jorgensen, 2014). Thus soft information obtained from other sources, especially past syndication partners of a due diligence target, can play an important role in the investment decision.

Despite the importance of the fundraising process for both the LPs and the VCs, relatively little systematic research has been conducted on the determinants of LP investment decisions. Much research has focused on the patterns of LP reinvestments and has documented the information advantage that fund insiders have compared with new investors (Lerner, Schoar, and Wongsunwai, 2007; Hochberg, Ljungqvist, and Vissing-Jorgensen, 2014). More-recent work has focused on the role that geographic proximity plays in the LP investment selection and has shown that LPs overinvest in VCs in the same state to the detriment of their performance (Hochberg and Rauh, 2013). To date, however, I am unaware of any research examining the role of interorganizational networks in the fundraising process.

A distinct advantage of the setting for this study is the unambiguous mapping to the data of all the key analytical constructs within the theory. The LPs can be considered the evaluators, for whose attention the individual VCs (the evaluatees) compete, whereas the intermediary is the VC that has a syndication relationship with the evaluatee (another VC) and an investment relationship with the focal LP. By comparison, the roles in the triad are much more difficult to disentangle in horizontal networks (e.g., investment banking syndicates or corporate strategic alliances), where any single member can play the role of evaluator, evaluatee, and intermediary simultaneously.

Furthermore, many settings lack transparent data on relationships’ performance. For example, strategic alliance research has long been hampered in its ability to assess alliance performance because the data are private and there are many objectives beyond financial metrics (see Zollo, Reuer, and Singh, 2002). By contrast, in the present study’s setting, there is a clear differentiation between successes and failures. Portfolio companies are managed toward a successful liquidity event, either an initial public offering (IPO) that can allow the sale of the VC’s shares on the open market or an acquisition by an established industry player. Such outcomes can be contrasted readily to failures such as bankruptcy or liquidation of the portfolio company, which can invariably result in significant capital losses for the investors.

Data

I aggregated two major datasets. The data on VC investment and syndication activities came from the widely used VentureXpert database by Thompson Reuters, and the data on LP to VC investment came from the Private Equity Intelligence (Preqin) database. VentureXpert has been tracking VC fundraising, investments, and exits since the 1970s and is commonly used for research in both finance (Hochberg, Ljungqvist, and Lu, 2007, 2010) and economic sociology (Podolny, 2001; Sorenson and Stuart, 2001, 2008). It lists the investors in each funding round of a portfolio company. From this information, I constructed a symmetrical matrix of prior syndication relationships between two VC firms, in which the ijth entry denotes the number of times VC firm i co-invested with VC firm j within a preceding period of some length. Consistent with prior research (e.g., Sorenson and Stuart, 2008), I report a five-year rolling window and verify robustness to three- and seven-year windows as well.

Historically, the VC industry has been secretive about funding sources, which explains the very limited prior research on LP investments. The few authoritative studies on the topic typically secured access, under strict confidentiality agreements, into the investment portfolios of a small number of large institutional investors (Lerner and Schoar, 2004; Lerner, Schoar, and Wongsunwai, 2007). To fill this gap in industry data, Preqin began assembling a dataset on specific investors from three sources. As a starting point, it used Freedom of Information requests (or the equivalent in other countries) to procure investment-level data from publicly owned LPs. A significant number of the large LPs in the U.S. fall into this category, including public pension plans (e.g., the California Public Employees’ Retirement System, also known as CalPERS) or the endowments of public universities (e.g., the University of Michigan endowment). Preqin complemented this core of legally disclosable data with two sets of surveys, one to the VC firms raising the funds and one to the privately owned LPs. The final Preqin database triangulates across these different sources to reduce the selection biases in any single method. Finance scholars have recently started using the Preqin dataset and have confirmed its exhaustive nature relative to older sources of data such as CapitalIQ, VentureOne, and Venture Economics (e.g., Hochberg and Rauh, 2013). 3

Starting with the Preqin core dataset, I filtered the data in three ways. First, using only dyads in which both the LP and the VC were based in the U.S. helped ensure the homogeneity of the institutional environment. Second, for data availability reasons, I limited attention to the period January 1997 to December 2007. 4 Third, I excluded many classes, such as real estate, hedge funds, natural resources, and mezzanine financing, which are clearly outside the VC industry. 5

Because no common identifier exists between VentureXpert and Preqin, I used a fuzzy textual matching algorithm, the Datamatch© software, which compares the similarity between any two text strings, ignoring known noise such as common abbreviations (e.g., Ltd., vs. Limited). I checked each match to ensure accuracy, consulting the VC firms’ websites as applicable. As a final check on the matching integrity, I resolved any discrepancies in the address information available on each firm by consulting both databases. In total, I was able to confidently match 60 percent of the relevant firms covered in Preqin; these firms accounted for 70 percent of the individual funds raised and 75 percent of the LP–VC dyads. Supplemental analyses suggest that the sample was biased toward larger VCs raising funds in the most important states to the VC industry, such as Massachusetts, California, and New York. In my robustness tests, I examine the extent to which this bias may affect the present study’s findings.

Variables

Dependent variable

The dependent variable used across all analyses indicates whether the LP–VC tie was realized and the LP invested in the new fund being raised by the new VC firm.

Independent variables

The core independent variables relate to the count of VC-mediated ties between the focal LP and the VC firm. The naïve structural embeddedness variable of VC-mediated ties count is the logged number of different VCs in which the LP has invested within the prior five years and that have one or more syndication experiences with the focal VC across the same time frame. I restricted the syndication relationships to ones that ended (i.e., had their final round) five or fewer years before the focal year, although I verified robustness to three- and seven-year sliding windows as well. I counted only the number of discrete paths, that is, a single mediating VC counted as one indirect tie, even if it had experienced multiple syndications with the focal VC. This is the baseline variable measuring triadic closure; the key hypotheses are tested by splitting it into different subcounts depending on the features of the intermediary–evaluatee relationship and testing the differences of the effects. 6 To reduce overdispersion, I logged all those count variables.

I tested H1 by separating the overall LP–VC–VC indirect tie count into successful and unsuccessful relationships. I defined VC-mediated indirect ties count–success as the count of indirect ties that resulted in a success, defined as an IPO or an acquisition of the portfolio company in which the VC pair co-invested and did not experience any failure, defined as a bankruptcy or a liquidation of the portfolio company. Conversely, VC-mediated indirect ties count–failure was reserved for relationships that resulted in at least one failure and zero successes. 7 I also controlled for VC-mediated indirect ties count–ambivalent for ties that satisfied one of the two following conditions: (1) either no successes and no failures or (2) both successes and failures. 8 The three subcounts together add up to the total number of indirect ties between the LP evaluator and the VC evaluatee.

To test H2 on the effects of similarity between the intermediary and the evaluatee, I calculated an industry specialization overlap index using the following formula, where pik is the proportion of VC firm i’s investments in industry k over the prior five years. 9 The dyadic industry overlap measure between two VC firms ranges from 0 to 1, with 1 indicating identical distribution of investments across industries.

I then dichotomized the average industry overlap for each evaluatee–intermediary pair using the 75th percentile in the distribution of overlap between any two collaborating VCs as a cut-off. I therefore separated the VC-mediated indirect ties into VC-mediated indirect ties count–high industry overlap and VC-mediated indirect ties count–low industry overlap and predicted that the effect of the latter would be more positive than the effect of the former, as per H3.

To test H3, I needed to determine the relative reputations of the evaluatee and the intermediary VC. For that purpose I constructed the VC reputation variable using the methodology proposed by Lee, Pollock, and Jin (2001), which is being increasingly used in organizational research (Petkova et al., 2014; Pollock et al., 2015). It is composed of equal-weighted z-standardized scores of a VC firm relative to all firms existing in the industry in the focal year along six dimensions: (1) number of IPOs in the past five years, (2) total number of companies funded in the past five years, (3) total dollar amount invested in the past five years, (4) total number of funds raised in the past five years, (5) total dollar amount raised in the past five years, and (6) age of the VC firm in the focal year. This index consolidates several features that might make a VC firm attractive to an LP: performance (#1), experience (#2, #3, #6), and the mark of endorsement by other LPs that have chosen to invest (#4, #5). Based on the calculated reputations of the intermediary and the evaluatee VC, I divided the overall indirect count variable into VC-mediated indirect ties count–higher intermediary reputation and VC-mediated indirect ties count–lower intermediary reputation and hypothesized that the former would have a more positive effect on tie formation than the latter.

To test H4, I created four different subcounts of the overall indirect ties count variable based on a 2 × 2 matrix that on one dimension includes the industry overlap of the evaluatee and the intermediary (as defined for H2) and on the other dimension includes relative reputation of the intermediary vis-à-vis the evaluatee (as per the test for H3). The four different subcounts are (1) VC-mediated indirect ties count–higher intermediary reputation and low industry overlap; (2) VC-mediated indirect ties count–higher intermediary reputation and high industry overlap; (3) VC-mediated indirect ties count–lower intermediary reputation and low industry overlap; and (4) VC-mediated indirect ties count–lower intermediary reputation and high industry overlap. The argument of H4 is that a lower reputation of the intermediary relative to the evaluatee will reinforce the negative effect of high overlap on triadic closure. To test this interaction, I had to effectively check whether the difference between coefficients #3 and #4 is greater than the difference between coefficients #1 and #2.

Control variables

To credibly estimate the structural effects, I incorporated a wide variety of controls at the level of the focal VC firm, as well as the focal LP–VC dyad. To incorporate the length of the VC firm’s track record, I included the logged number of funds previously raised by the same VC firm and the logged age of the VC firm, defined as the number of years elapsed since its first fundraising. I also incorporated three indicator variables denoting the size quartile of the focal VC fund: the lower quartile equates to smaller size, with the top (4th) quartile being the omitted category. I used two sets of variables to measure the performance of the focal VC firm. I first included the outcomes of all the VC-firm-backed portfolio companies over the past five years: portfolio company IPO rate, portfolio company acquisition rate, and portfolio company failure rate. 10 I also used the average performance quartile of the previous funds raised by the same VC firm as reported by Preqin. In cases for which the average performance quartile was missing (approximately 15 percent of the cases), I imputed it from all the other independent variables using STATA’s impute procedure. For this variable, lower values indicate better performance (i.e., funds in the first quartile are the best-performing funds, whereas funds in the fourth quartile are the worst performers). With the influence of these controls partialed out in the regression, I can claim that the count of successful versus failed VC-mediated indirect ties does not reflect the unobservable, true quality of the VC firm. Finally, I incorporated the focal firm’s (logged) degree centrality in the VC syndication network to control for the fact that more central firms are more likely to have more indirect ties to the VCs but can also be more attractive because their centrality in the VC network can signal quality (Podolny, 2001).

Not all VCs are equally available for new investments. In particular, VC firms often suffer from scalability issues, because the existing partners can manage only a limited number of investments, and new partners cannot be added quickly without jeopardizing quality (Gompers and Lerner, 1999). Thus VC firms often set targets for the new fund; if fundraising exceeds these targets, it is said to be oversubscribed. And yet oversubscribed funds do not automatically stop accepting new investments. Conversations with venture capitalists suggested that most firms aim to be slightly oversubscribed by a factor of 1.1 or 1.2 of their target to signal their desirability in the market. Being oversubscribed more than that becomes problematic. Conversely, undersubscribed funds are generally desperate for new investors due to the stigma this situation entails. Correspondingly, I controlled for the VC’s availability to new investors by calculating its subscription ratio defined as the total funds raised divided by the fund target. When no fund target was available, I assumed that the fund was exactly subscribed. I logged the ratio to make it symmetric around zero; an undersubscribed firm will have a negative logged ratio, whereas an oversubscribed firm will have a positive logged ratio.

I also incorporated a large number of dyadic controls, in particular to remove the influence of proximity or homophily from the effects of indirect ties (Stuart, 1998; Sorenson and Stuart, 2001). I included an indicator variable equal to 1 if the LP and the VC were located in the same state. This variable controls for the documented tendency of LPs to invest disproportionately in geographically proximate VCs (Hochberg and Rauh, 2013). I also obtained substantively identical results using the logged distance between the LP and the VC; however, the two geographic measures were correlated too heavily to be used together in the same model.

I also controlled for the preferences of the LPs as implied by their existing portfolio. In the case of average industry overlap with LP investments, I first calculated the dyadic industry overlap between the focal VC and each of the other VCs in the LP’s portfolio and then averaged the overlap measure between the focal VC and all VCs with which the LP had invested over the prior five years. The result was an index of how similar the industry specialization of the focal VC was to the average VC that the LP had chosen previously. Similarly, I computed average state overlap with LP investments based on the average overlap in state-by-state investments to control for the geographic investment specialization of the VCs in which the LP had invested previously. 11 Together, these two variables should account for the industry and geographic preferences of the LPs.

Finally, I controlled for the presence of LP-mediated indirect ties between the focal LP and VC. These ties are formed when an LP that has prior co-investments with the focal LP has also invested previously in the focal VC. This is a potentially important channel for referrals, because LPs are highly interested in the perspective of other institutional investors who have firsthand experiences with the VCs of interest. Prior co-investment ties between two LPs means that their key personnel likely sit on the same LP boards, which facilitates the exchange of private information. Another reason an LP-mediated tie could be potentially important is because it can serve as an attention-focusing mechanism. To the extent that structural equivalence increases the perception of competition and mutual monitoring (White, 1981; Burt, 1987), LPs are likely to follow their co-investment partners’ investments. If a peer has invested in a particular VC firm, it may be regarded as social proof of its worth, which merits closer investigation. I did not attempt to differentiate between those specific mechanisms but strived to account for them all by controlling for the LP-mediated indirect ties.

Analytical Approach

I derived the dataset used for the core analyses on new tie formation using the factual–counterfactual setup common for investigating dyadic tie formation (e.g., Sorenson and Stuart, 2008). For each factual dyad, I defined the universe of counterfactual dyads in which the same LP was matched with other VCs that (1) raised new funds in the same calendar year, (2) belonged to the same fund classification, and (3) raised money from new investors during their round. 12 Because I was interested in new tie formation, I excluded from the analysis all pairs—factual or counterfactual—in which the LP and the VC had prior investment ties. I also dropped from consideration all first-time funds, because new firms start with no prior syndication experiences, which leaves my core independent variables undefined. All in all, this reduced dataset includes 4,668 factual and 59,549 counterfactual observations, including 610 LPs investing in a total of 831 discrete funds raised by 310 different firms.

I used a conditional logit model, also known as the McFadden Choice Model, to predict the factual observation within each group. This model estimates an unobserved utility function associated with each observation within the set and selects the observation with the highest value. Conceptually, the model takes the perspective of the evaluator LP during each individual selection decision and asks the question about which variables most distinguish the VC firm that has been selected (the factual) from the options that the LP has presumably considered but did not select (the counterfactual). Because it considers only within-group variation, the model effectively incorporates fixed effects at the group level. Conditional logit models are commonly used to analyze tie formation in the interorganizational networks literature because they can control for all unobservables shared across a particular choice set (e.g., Sorenson and Stuart, 2008). Given that my counterfactual sampling strategy kept the same LP, year, and fund type fixed across groups, all variables fixed within any of those levels of analyses—or permutations thereof, such as LP eigenvector centrality in a given year—were absorbed by the fixed effects and were thus not included in the model. I also used robust standard errors clustered at the group level to account for the fact that the LP is the same across all observations within the given group. In the main analyses, I allowed the number of counterfactuals to vary from 1 to 44 per group depending on the number of other VCs that raised funds of the same type in the same year, but I verified robustness to random sampling of counterfactuals.

Results

Main Analyses

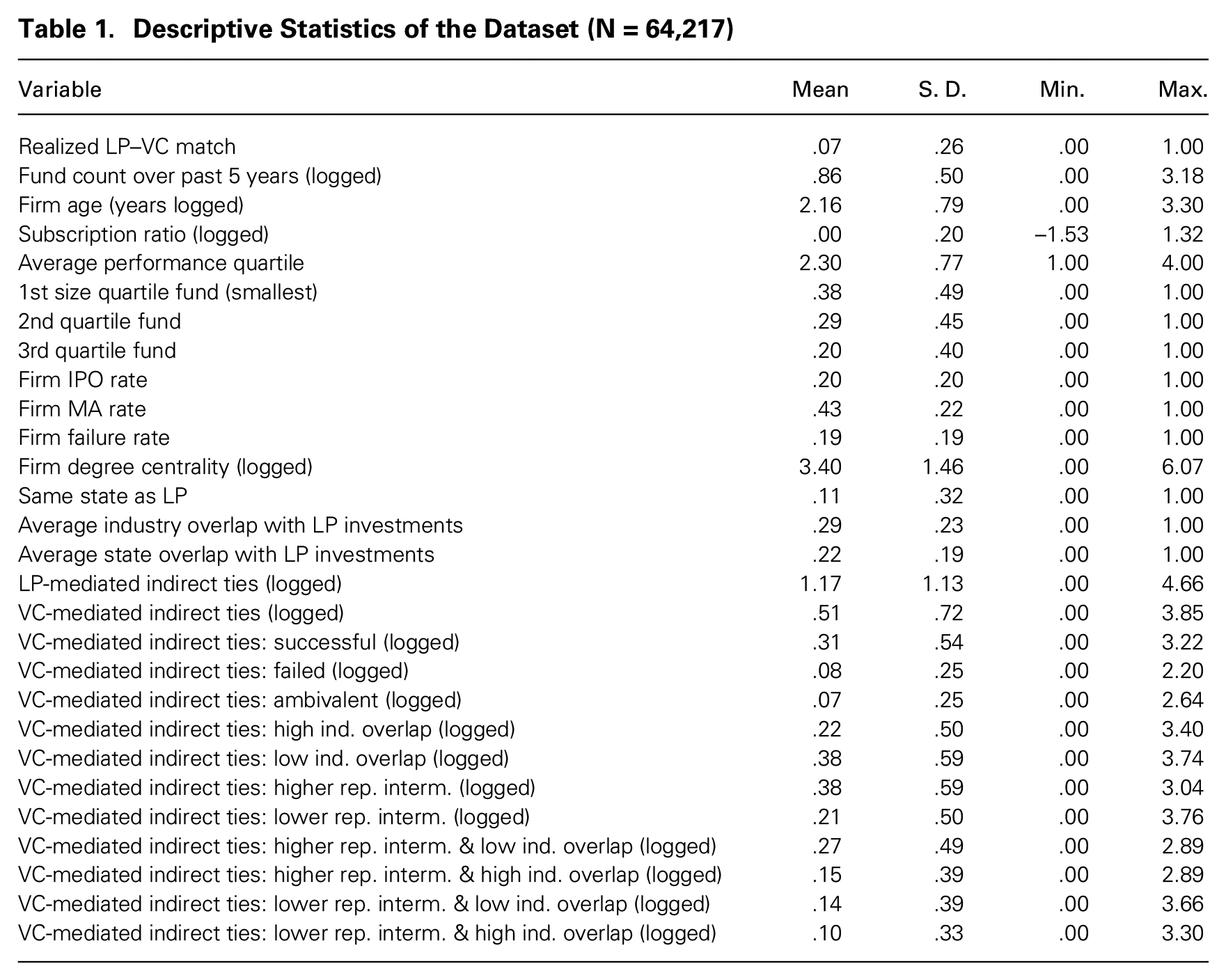

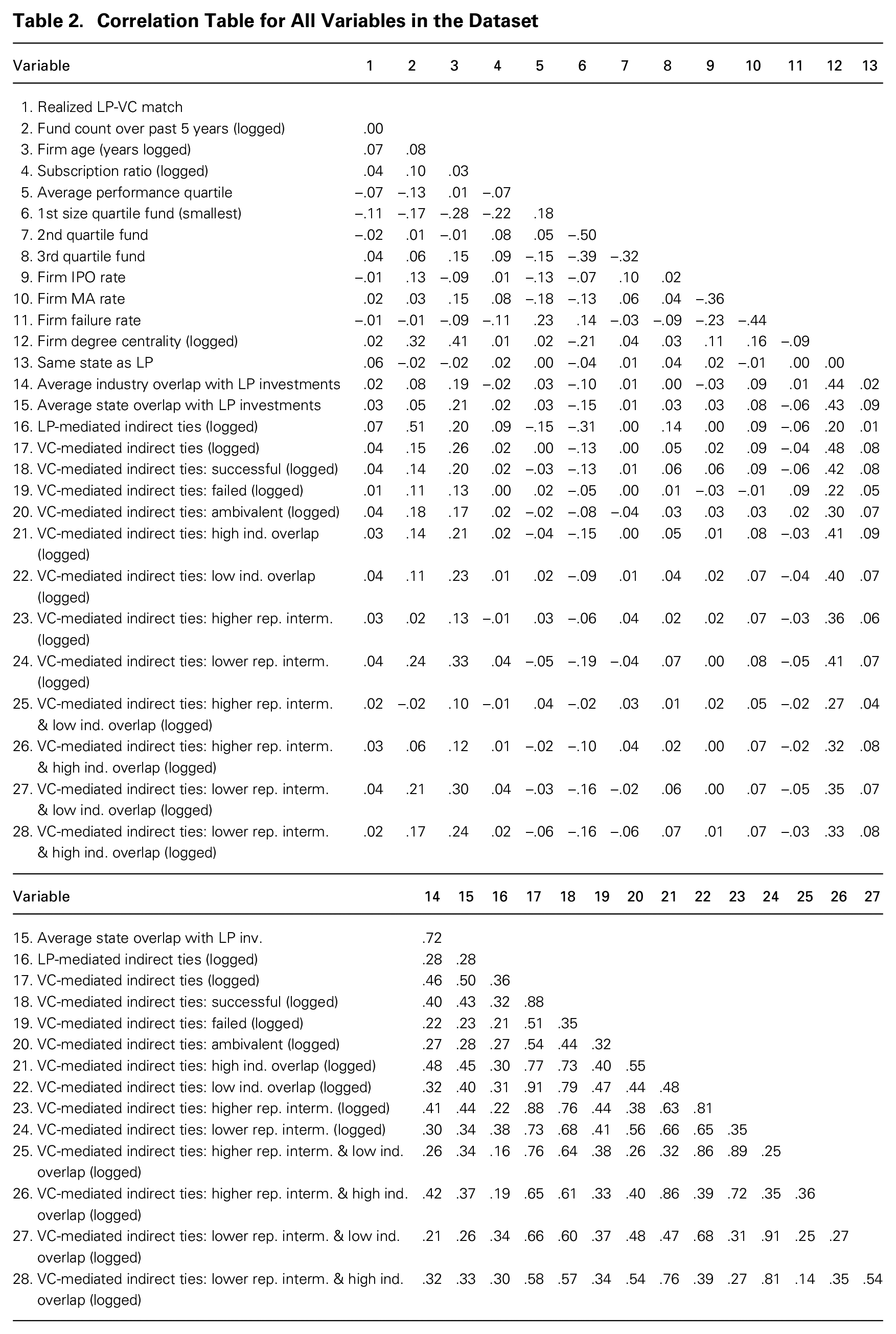

Table 1 presents the descriptive statistics for all variables of the core dataset, and table 2 shows the bivariate correlations. The correlations of the core control variables with the outcome variable are largely consistent with expectations: older firms with higher past performance (i.e., low average quartile of the prior funds) that are raising heavily oversubscribed large funds are more likely to be matched with an LP in the dataset. The dyadic covariates are also associated with tie formation. Venture capital firms are more likely to receive funding from LPs that are collocated in the same state (consistent with Hochberg and Rauh, 2013) and have LP- and VC-mediated indirect ties to them. At a glance, the bivariate correlations lend credence to some of the hypotheses. For example, successful VC-mediated indirect ties are more predictive of LP investment than failed VC-mediated indirect ties. Because those variables can be heavily correlated with other predictors of tie formation, however, we need the regression analyses to draw any conclusions.

Descriptive Statistics of the Dataset (N = 64,217)

Correlation Table for All Variables in the Dataset

The bivariate correlations also do not reveal any troubling correlations among the key variables that would raise multicollinearity concerns. The only correlation higher than 50 percent is between the industry and state average overlap measures of the VC’s portfolio with the portfolios of the other firms receiving investments from the LP. Removing either of those measures has a negligible effect on the coefficients of interest; therefore, I kept both within the final specification. Not surprisingly, the different subdivisions of the VC-mediated ties are highly correlated with the variables to which they aggregate. For example, the overall VC-mediated indirect tie count is very highly correlated (at 88 percent) with the successful VC-mediated indirect tie count. Such problematic pairs, however, never enter the model together. Overall, the correlations are not sufficiently high to create significant issues. No model specification reported exhibits a variance inflation factor (VIF) of above three, which is substantially lower than the value of 10 typically accepted as the upper acceptable bound (Kutner, Nachtsheim, and Neter, 2004).

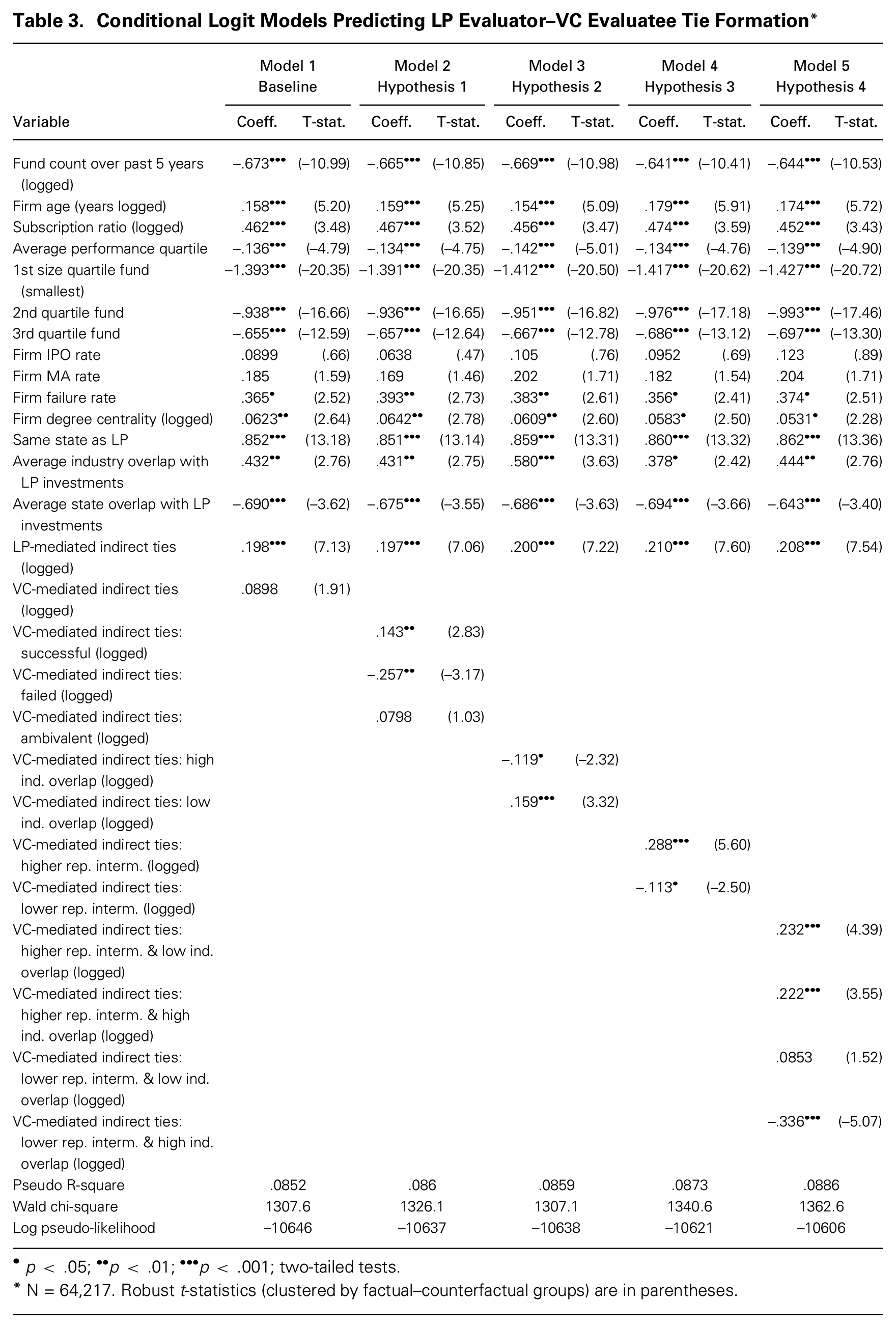

Table 3 introduces all the core analyses for the paper. Model 1 presents a baseline model of triadic closure. As expected, the main effect of indirect VC-mediated indirect ties is positive, although only marginally significant (p < .10). The effect is also quantitatively small; a move from no indirect VC-mediated ties to having a single VC-mediated indirect tie increases the likelihood of tie formation from 5.8 percent to 6.1 percent, an approximately 5-percent increase on the base rate. 13 Among the monadic controls, VC firm age, performance (measured by average fund quartile of their past funds), fund size, and fund oversubscription are strong predictors of LP–VC matching, consistent with intuition and the bivariate correlations. Interestingly, exit rates do not increase the probability of the match after the performance quartiles are controlled; VC firm failure rate is, in fact, positively related to matching. 14 Among the dyadic controls, geographic collocation of the LP and the VC, as well as the presence of LP-mediated indirect ties, has a robust positive relationship to matching. Industry and state overlap with the other investments of the LP have opposite signs, but that may be an artifact of the high correlation of those variables: when entered individually, either one has a positive association with matching.

Conditional Logit Models Predicting LP Evaluator–VC Evaluatee Tie Formation*

p < .05;

••

p < .01;

N = 64,217. Robust t-statistics (clustered by factual–counterfactual groups) are in parentheses.

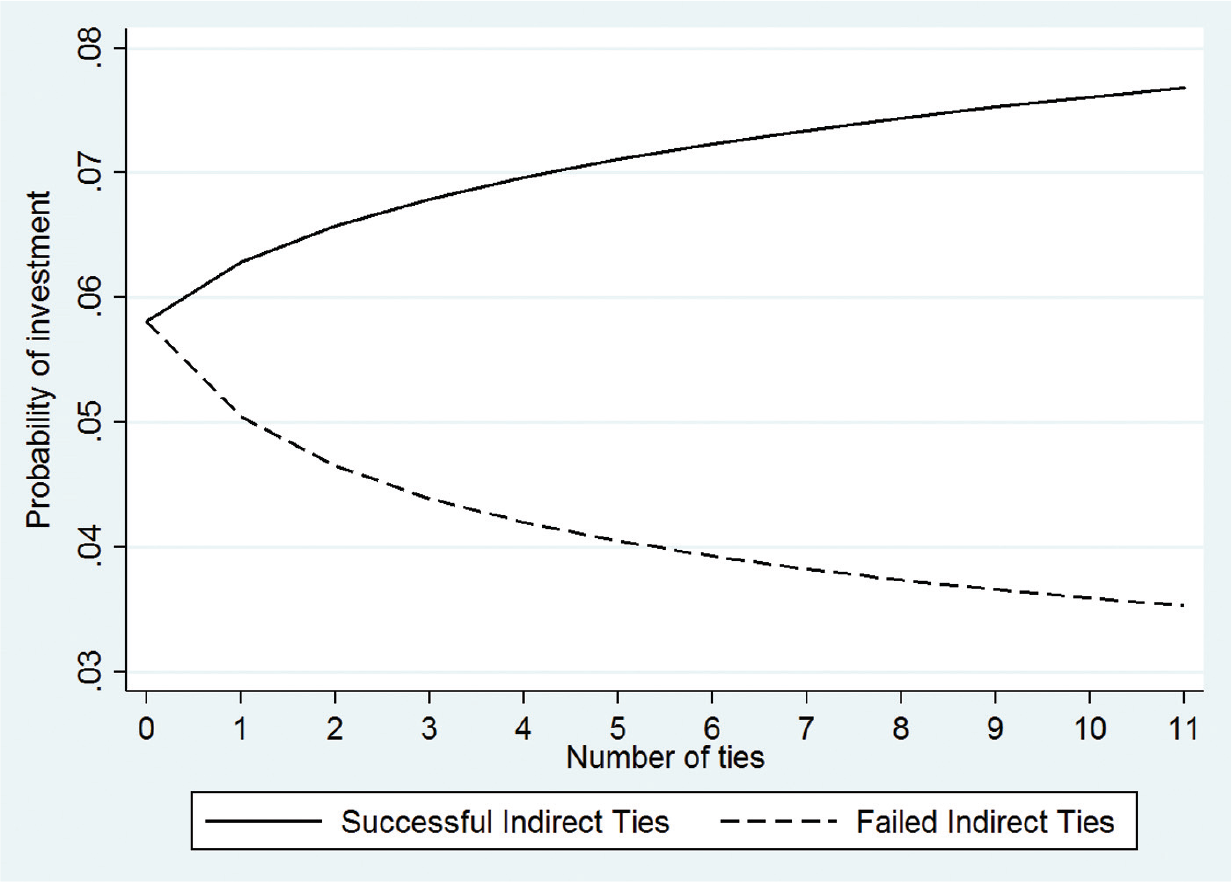

Model 2 separates the overall VC-mediated indirect tie count into successful, failed, and ambivalent ties. H1 predicted successful indirect ties will have a more positive effect on LP to VC matching than failed indirect ties. 15 The results are strongly consistent with the hypothesis: the test of equality of the two coefficients is rejected at p < .001. Whereas successful indirect ties have large and statistically significant positive effects, the failed indirect ties have a nearly double negative effect on tie formation: an LP is likely to select a VC firm to which it has had no prior indirect ties over a firm to which it is connected only via failed indirect ties, all else kept equal. Ambivalent ties have a statistically insignificant positive effect on matching. The overall pattern is consistent with the idea that the performance of a tie can dramatically transform its effects on triadic closure, beyond the already-known effects on dyadic tie renewal (Li and Rowley, 2002). In substantive terms, an average VC firm that has had no prior ties to an LP has a baseline likelihood of 5.8 percent of receiving an investment; that likelihood increases to 6.3 percent if there is a single successful VC-mediated indirect tie but drops to 5 percent if there is a failed indirect tie. Figure 2 illustrates the substantive effects of multiple successful or failed indirect ties.

Probability of a limited partner investment in a venture capital firm as a function of the number of successful and failed VC-mediated indirect ties.*

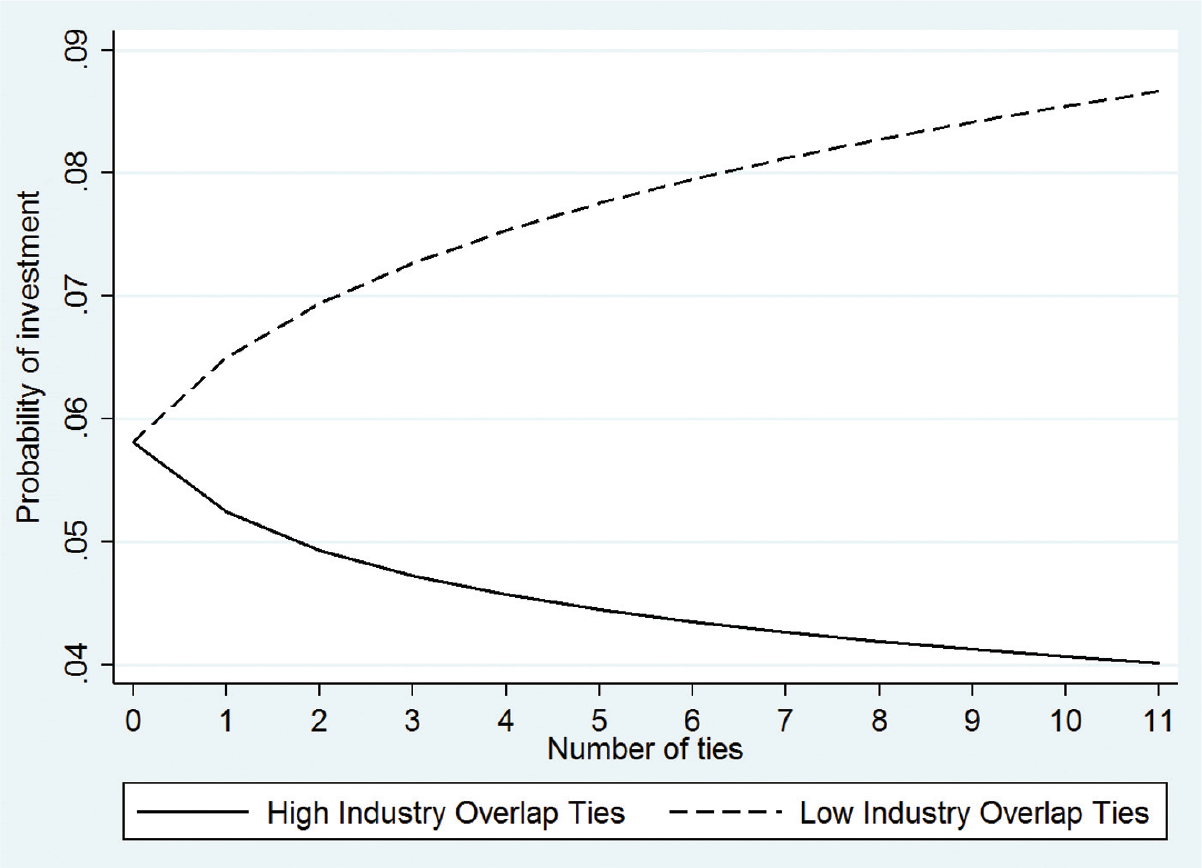

Model 3 analyzes the effect of VC-mediated indirect ties depending on the extent of the industry overlap between the evaluatee and the intermediary VC. As predicted by H2, indirect ties featuring low industry overlap between the two VCs have a more positive effect on tie formation than indirect ties featuring high industry overlap (p < .001). In fact, the likelihood of tie formation between an LP and a VC firm is reduced from the baseline 5.8 percent to 5.2 percent when their connection occurs via an intermediary highly similar to the evaluatee. In contrast, a single indirect tie via a dissimilar intermediary raises the expected probability to 6.5 percent. The effect is depicted graphically in figure 3.

Probability of a limited partner investment in a venture capital firm as a function of the number of high and low industry overlap VC-mediated indirect ties.*

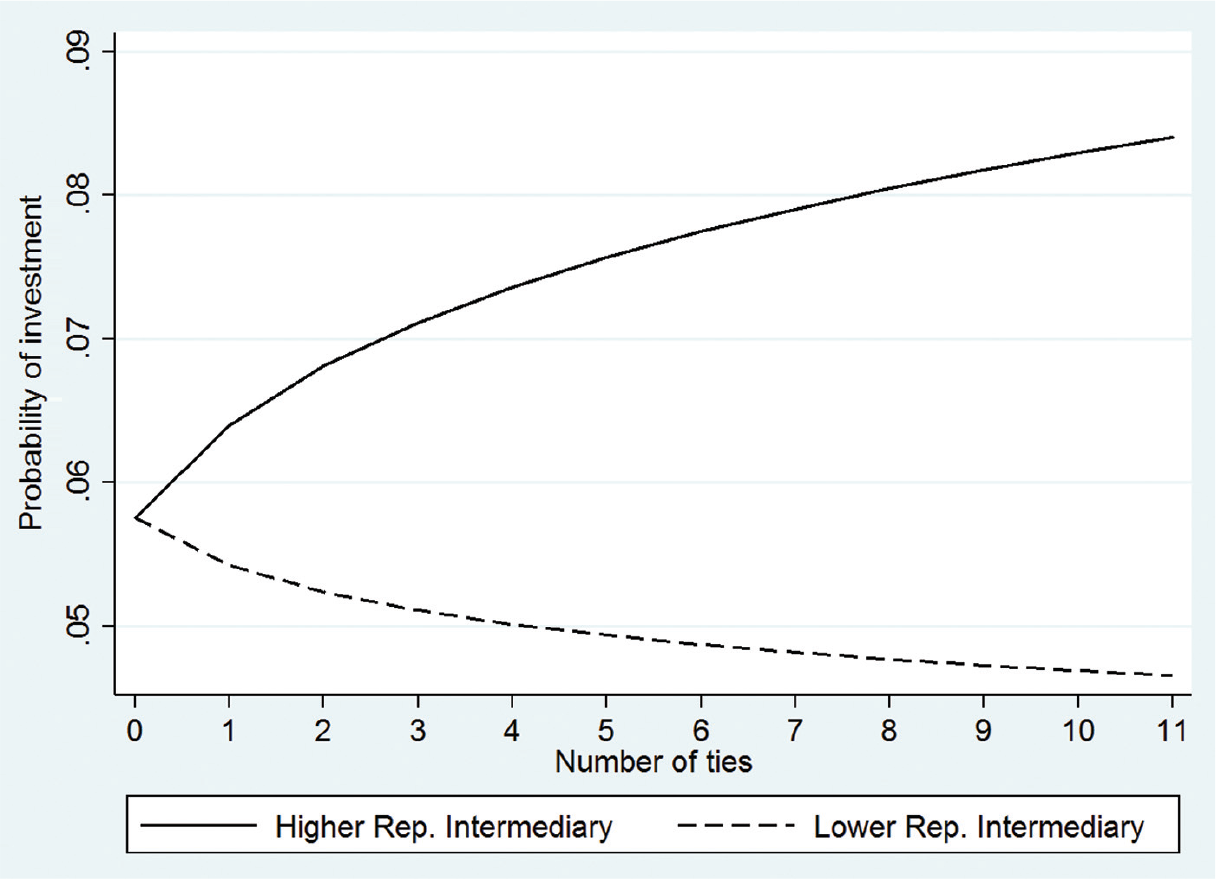

Model 4 examines the effects of the relative attractiveness of the intermediary and the evaluatee by separating the overall count of the VC-mediated indirect ties into those in which the intermediary had a higher VC firm reputation than the evaluatee versus those in which the evaluatee had a higher VC firm reputation than the intermediary. The results are consistent with H3, which maintained that intermediaries with a lower reputation are less secure and less willing to facilitate connections between their LPs and their high-reputation VC partners. The two coefficients are significantly different (p < .001) and have dramatically different substantive effects. As shown on figure 4, a single tie via an intermediary that is of higher reputation than the evaluatee increases the baseline likelihood of tie formation from 5.8 percent to 6.4 percent, whereas a single tie via a lower-reputation intermediary reduces the expected probability of matching to 5.4 percent.

Probability of limited partner investment in a venture capital firm as a function of the number of VC-mediated indirect ties in which the intermediary has a higher or lower VC firm reputation than the evaluatee.*

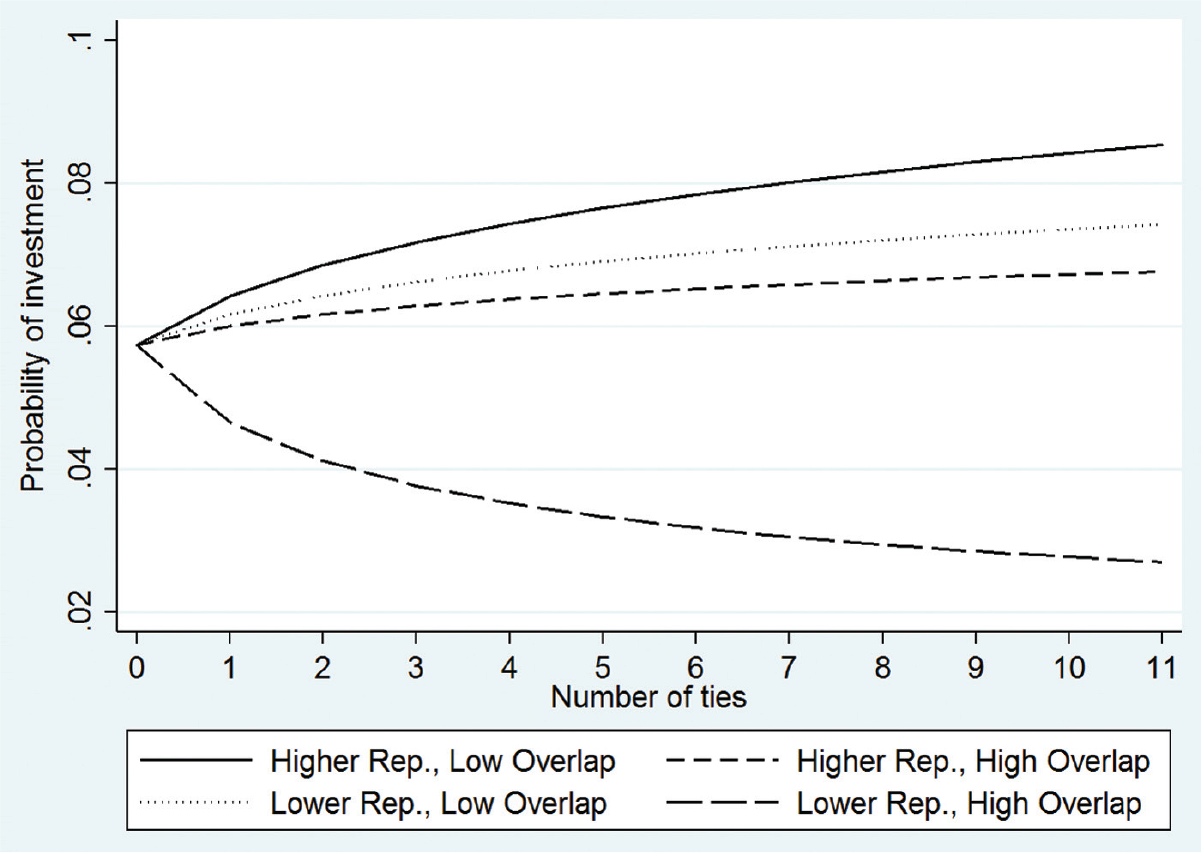

While models 3 and 4 examined the individual effects of replaceability and relative attractiveness, model 5 tests their interaction. To do this, I split the overall count of indirect ties in a 2 × 2 fashion along two dimensions: industry overlap between the intermediary high or low, and intermediary of higher or lower reputation than the evaluatee. The moderating effect of the relative reputation of the intermediary relative to the evaluatee on the effect of the industry overlap can be tested by comparing the differences between two pairs of coefficients: (Higher reputation intermediary and low industry overlap – Higher reputation intermediary and high industry overlap) versus (Lower reputation intermediary and low industry overlap – Lower reputation intermediary and high industry overlap). As can be calculated from table 3, the difference in the first set of coefficients is virtually indistinguishable from zero (b1 = .232, b2 = .222, d = .01, p > .10), whereas the difference in the second set of coefficients is more than 40 times as large (b1 = .085, b2 = –.336, d = .421, p < .001). 16 The difference in the difference between these two pairs of coefficients is significant at any conventional level, supporting the idea that the low relative reputation of the intermediary increases its sensitivity to the level of similarity with the evaluatee. Figure 5 illustrates the predicted probabilities of the different types of ties and makes clear that the only ties that significantly hinder triadic closure are those in which there is both high overlap and low relative attractiveness of the intermediary. 17

Probability of a limited partner investment in a venture capital firm as a function of the number of VC-mediated indirect ties in which the intermediary has higher or lower VC firm reputation than the evaluatee and has lower or higher industry overlap with the evaluatee.*

Post Hoc Analyses

I conducted three additional post hoc analyses to better understand the findings and rule out alternative explanations; the full tables for these three analyses are included in the Online Appendix (http://journals.sagepub.com/doi/suppl/10.1177/0001839217703935).

Interactive effect of collaboration outcomes and competitive concerns

So far, I have theoretically articulated and empirically verified the separate effects of collaboration failures and competitive concerns. The interactive effect of these two constraints on triadic closure remains an open question. One could consider three plausible scenarios. The default scenario is that collaboration failure and competitive concerns stack more or less additively in limiting the intermediary’s willingness to facilitate triadic closure. A second scenario is that failure and competitive concerns reinforce one another, particularly if VCs are more likely to discount the competitive threat from syndication partners with which they have a good relationship. A third scenario is that competitive concerns might be most salient when the intermediary and the evaluatee have had a successful relationship. When failures occur in the exchange with the evaluatee, the intermediary is likely to be unwilling to introduce or endorse the evaluatee to the evaluator, with or without competitive concerns. In contrast, competitive concerns have more room to trigger a behavioral shift if the intermediary has positive information to report on the evaluatee following successful collaborations, and the possibility of having a more reputable competitor in the LP’s portfolio becomes tangible.

To investigate the empirical support for any of those three scenarios, I divided up the successful, failed, and ambiguous tie counts depending on (1) whether the evaluatee and the intermediary had high or low similarity and (2) whether the evaluatee had higher or lower reputation than the intermediary (all variable definitions are the same as in the main analyses). I then proceeded to test those two interactions in the same way I did H4, by putting the split counts into the same model and testing for the difference in difference of their coefficients. The full model is presented as table A1 in the Online Appendix.

The first moderation test concerns whether the success of the relationship will change the effect of the similarity between the two VCs. For this, I compared the differences in the pairs (Successful tie and low industry overlap – Successful tie and high industry overlap) versus (Failed tie and low industry overlap – Failed tie and high industry overlap). In both pairs of variables, a switch from low to high overlap reduces the level of closure. Even though the difference is substantively larger and more statistically significant in the first pair (b1 = .208, b2 = –.067, d = .275, p < .001) than in the second pair (b1 = –.147, b2 = –.315, d = .168, p > .10), the difference in difference does not reach statistical significance at conventional levels (p > .10). Therefore, a high degree of overlap and the failure of the relationship function more or less additively in limiting the likelihood of closure.

I also tested whether the success of the relationship moderates the effect of the relative attractiveness on closure. The relevant pairs of variables to compare are (Successful tie and higher reputation intermediary – Successful tie and lower reputation intermediary) versus (Failed tie and higher reputation intermediary – Failed tie and lower reputation intermediary). The difference in the coefficients in the first pair (b1 = .327, b2 = –.124, d = .451, p < .001) is substantively and statistically much larger than the difference in the coefficients in the second pair (b1 = –.164, b2 = –.237, d = .073, p > .10). All in all, this result is most consistent with the third scenario. In the case of failures, intermediaries pass along negative information regardless of the presence or absence of relative attractiveness-driven competitive concerns; only in the case of successes, which ordinarily promote closure, are intermediaries’ behaviors likely to be affected by how threatened they feel by the evaluatee’s relative attractiveness.

The overall pattern of the results helps rule out concerns that passive mechanisms—for example, the greater attention that LPs might pay to the syndication partners of their VCs and the outcome of those interactions—may drive the results (e.g., Rogan and Sorenson, 2014). The passive attention-focusing properties of indirect ties may certainly account for some of the overall closure trend and the moderating effect of the evaluatee–intermediary interaction outcomes. Such passive mechanisms, however, cannot explain why LPs might be more likely to invest in evaluatees that have a lower reputation than the intermediaries. After all, theories of local search generally presume that actors select the best-performing solution from within their social network (cf. Lazer and Friedman, 2007). Furthermore, it is unclear why an evaluatee with a higher reputation is less likely to be selected after having had a successful relationship with an intermediary, which should have registered positively on the LP’s passive radar. An explanation rooted in the intermediary’s (dis)incentives to refer potential competitors can provide a much more compelling explanation for both results.

Relative reputation versus absolute reputation

I also examined whether the absolute level of the reputation of the intermediary matters as much as the relative reputation that I tested in the main analyses. Such a test can address an alternative explanation for my relative attractiveness findings, that the positive effect of higher-reputation intermediaries on closure can be explained not by their lack of competitive disincentives to provide referrals but by their ability to provide more effective and credible endorsements by virtue of their high reputation (Stuart, Hoang, and Hybels, 1999). I therefore separated the overall VC-mediated tie count into subcounts of indirect ties mediated by high-reputation versus low-reputation intermediaries. To distinguish the high- and low-reputation intermediaries I alternately used cut-offs at the 50th, 75th, and 90th percentiles based on each year’s distribution of reputation scores (for full results, see table A2 of the Online Appendix).

In no instance were the effects of high- and low-reputation intermediaries on LP to VC matching different from one another at conventional statistical significance levels (p < .05); only the 90th percentile cut-off resulted in a marginally significant coefficient difference (p < .10). Those results should be contrasted with the large and robust coefficient differences when I used relative reputation (i.e., model 4, table 3). The pattern of findings suggests that the relative reputation of the intermediary vis-à-vis the evaluatee matters more than the absolute level of the intermediary’s reputation. In other words, the very same intermediary is likely providing referrals on syndication partners that have a lower reputation while withholding referrals from syndication partners that have a higher reputation. This result is more consistent with my story of the competitive threat created by the relative attractiveness of the evaluatee than with the alternative story of the endorsements provided by high-reputation intermediaries.

Competitive concerns and reinvestment probability

Finally, I examined the extent to which the competitive fears of the intermediary are justified. Does creating a tie between the LP evaluator and the VC evaluatee ultimately threaten the intermediary’s own position? To test for this, I created a separate dataset of the reinvestment decisions of the LPs. The unit of analysis is the VC fund–LP pair for all LPs that have invested in any fund raised by the same VC firm in the past five years. I used a similar set of controls as in the main analyses and ran a logistic model of the probability that each of the prior LPs invests in the focal VC fund (all those analyses are reported in table A3 of the Online Appendix). 18 The key explanatory variable is the (logged) count of syndication partners of the VC in which the LP has invested within the past five years. If some of those previously closed triads undermine the likelihood of reinvestment, the focal VC is indeed justified in limiting its referral behavior.

I first found that the overall number of such prior LP investments to syndication partners of the focal firm has no meaningful effect on the odds of reinvestment (p > .10). So whereas the VC-mediated indirect ties, on average, promote closure for establishing new relationships (as verified by model 1, table 3), they have virtually no effect for the renewal of previous relationships. This is consistent with my earlier theorizing on the mechanisms behind triadic closure for two reasons. First, LPs are already aware of the VCs in which they have already invested; therefore indirect ties are not needed to focus their attention. Second, LPs already have in-depth, firsthand information on the VCs in which they have already invested (Lerner, Schoar, and Wongsunwai, 2007; Hochberg, Ljungqvist, and Vissing-Jorgensen, 2014); therefore they rely less on indirect ties for the repeat due diligence.

I then tested the effect of the two drivers of competitive threat. I separated the overall VC-mediated indirect count into two subcounts for past syndication partners that are of higher and lower reputation than the focal VC firm. The count of former syndication partners with a higher reputation that have received investments from the focal LP reduced the likelihood of reinvestment (p < .01), whereas the count of such firms with a lower reputation had no effect on reinvestment rates. The two coefficients were also significantly different (p < .05). This result is noteworthy for two reasons. First, it shows that VC firms are justified in worrying about their relative attractiveness: an LP tie with a higher-reputation syndication partner may just be the prelude to their firing. Second, it marks a dramatic switch of the effect of higher-reputation indirect ties on tie formation versus tie renewal. Indirect ties via higher-reputation syndication partners significantly help establish a direct relationship; however, they significantly hurt in renewing an existing relationship. The latter result is impossible to account for by the greater credibility of endorsement of higher-reputation partners. Both sets of results are wholly consistent with the view that actors try to minimize the competitive threat posed by higher-reputation partners poaching their relationships.

I also examined the degree to which the industry overlap in VC-mediated indirect ties moderated their effect on LP reinvestment decisions. I found neither a statistically significant main effect nor a moderating effect (p > .10). This could mean that VCs may be overestimating the competitive threat posed by high-similarity syndication partners. There was also no meaningful interaction with the relative attractiveness variables.

Robustness Checks

I conducted extensive robustness checks on the main analyses. First, instead of using all potential counterfactuals, I randomly selected four (or all if there were fewer than four) counterfactuals from each group. Despite the loss of a significant number of observations (from 64,217 down to 17,384), there was no change in the pattern of the results or the significance level of the supported hypotheses. These results can help address potential concerns of dyadic autocorrelation when the same VC appears in a large number of counterfactual cases.

Second, I examined the effects of different moving windows to define the VC syndication network. The main results reported are for five-year windows, but most results are robust to using three- and seven-year windows as well. 19 I also used alternative definitions, for example, all syndication relationships started within the past five years, including ones that have not concluded yet. The major results remained consistent throughout. I am thus confident that the results are not driven by the operationalization of the interorganizational network.

Third, I tested the robustness of my splits of the VC-mediated tie counts. In testing replaceability, I used as cut-offs the 50th and the 90th percentile of the industry specialization overlap distribution, in addition to the 75th percentile reported in the main analyses. I also used a different similarity metric—overlap in state specialization of the VC firms—again at the 50th, 75th, and 90th percentiles. The results were consistent with those reported in the main analyses. I also examined different measures of relative attractiveness, such as the five-year IPO rate of the VC firms. The results were consistent with the ones reported based on Lee, Pollock, and Jin’s (2011) VC reputation measure. Another specification test I conducted was to add quadratic terms for curvilinear effects in the similarity of the evaluatee to the other firms in the evaluator’s portfolio. The curvilinear effects were generally weak, and the results on the key variables of interest were substantively unchanged.

Fourth, I explored the effects of lost observations due to my inability to find matches for some firms in both databases. To do so, I created a model incorporating all VC firms from the VentureXpert database to predict whether they also appear in the Preqin database. I used a range of independent variables, including dummies for fundraising years, states in which the firms are located, size of funds raised, and fund types. I used the fitted probabilities in two ways. I first incorporated them as an independent variable in the regression models to test directly for bias. Although its effect was negative, as one would expect (i.e., the reduced probability of getting matched in both datasets is also associated with reduced likelihood of being selected by an LP), it did not materially affect any of the relevant coefficients. I next weighted the observations in the logit model by the inverse of the match probability to make the sample more analogous to the overall population. Again, no meaningful changes in the coefficients were detected.

Discussion

The results of this study highlight the important role of the intermediary in facilitating or impeding triadic closure. My analysis of a longitudinal dataset of LP investment decisions from 1997 to 2007 showed that an evaluator–intermediary–evaluatee open triad is less likely to close (1) in cases of failed interaction outcomes, which dissuade the intermediary from endorsing the evaluatee to the evaluator, and (2) when the intermediary has competitive concerns—driven by high similarity and low attractiveness relative to the evaluatee—which increase its incentives to keep the evaluator from establishing a tie with the evaluatee and thus elevating it to a potential competitor. In my post hoc analyses, I also demonstrated the asymmetric effect of the interaction outcomes versus the competitive concerns: the intermediary’s competitive concerns about its relative reputation have an effect only when it has had successful collaboration with the evaluatee. Finally, I found that the competitive concerns of the intermediary tend to be well founded: when an evaluator establishes a tie with a higher-reputation evaluatee, the intermediary is more likely to subsequently lose the evaluator’s business.

Contributions

The key contribution of this paper is bringing the intermediary back into explanations of triadic closure. Extant research has generally tried to explain deviation from closure in terms of the evaluators’ incentives, for example, to access complementary capabilities (Gulati, 1995b), to procure diverse resources (Gulati, Sytch, and Tatarynowicz, 2012), or to take advantage of low-risk experimentation (Sorenson and Stuart, 2008). In other words, existing research has treated indirect links as passive scaffolding, presenting the evaluators with the opportunity to create direct relations, which they may or may not exploit depending on their objectives. Without minimizing the importance of the evaluators’ agency, this paper highlights that the intermediary can subtly influence the process through its referral and endorsement behavior, that it may—depending on its relationships and interests—either facilitate the creation of a direct tie or reduce its likelihood below what we would expect if the indirect tie did not exist at all. My research thus opens a dialogue between the closure literature and the brokerage literature, which recognizes intermediaries’ incentives to keep their alters separated (Padgett and Ansell, 1993; Ryall and Sorenson, 2007; Buskens and van de Rijt, 2008) but has rarely presented evidence of such behavior in practice (for recent exceptions, see Lee, 2015; Tatarynowicz and Keil, 2016).

This study also enriches our understanding of the dynamics of competition and interorganizational information flow. Recent research has focused on how the leakage of competitively sensitive information across indirect ties can inhibit organizational performance (Pahnke et al., 2016) and how actors avoid or terminate open triads because an intermediary may leak such information to rivals (Gimeno, 2004; Rogan, 2014; Hernandez, Sanders, and Tuschke, 2015). In contrast, I suggest the opposite process: that in the presence of competitive concerns, existing open triads are less likely to close because of the intermediary’s unwillingness to convey referrals and endorsements between its two indirectly connected partners. I therefore establish competitive concerns as an important source of friction in the flow of information across network ties, distinct from information diffusion constraints such as bandwidth constraints and knowledge complexity, which other research has explored (Hansen, 1999; Szulanski, 2003; Aral and Alstyne, 2011; Ghosh and Rosenkopf, 2015).

Finally, this paper contributes to the growing interest in understanding factors that drive the heterogeneity of social ties. Organizational scholars have documented how factors such as the age of the ties (Baum, McEvily, and Rowley, 2012; McEvily, Jaffee, and Tortoriello, 2012), the level of resource co-specialization the ties require (Gimeno, 2004), or the interpersonal relationships among the organizational actors that represent the nodes (Gulati and Westphal, 1999; Vissa and Chacar, 2009) can dramatically transform the effects of interorganizational ties. I demonstrate two key sources of heterogeneity that can completely reverse the assumed effects of indirect ties. First, scholars have long differentiated between cooperative and conflictual ties, such as peace versus war between countries (Ingram and Torfason, 2010) or strategic alliances versus lawsuits between companies (Sytch and Tatarynowicz, 2014). There has been limited appreciation, however, for how events such as failures can undermine the quality of seemingly collaborative ties such as VC syndicates. The evidence here that failure can completely reverse triadic closure underscores the importance of distinguishing explicitly between successful and unsuccessful collaborative ties in modeling network evolution (see also Zhelyazkov and Gulati, 2016). Second, the results highlight how the competitive tension across an indirect tie—the intermediary’s level of competitive concern about an indirectly connected party—can significantly decrease the odds of closure across that open triad. This finding complements existing work showing that two disconnected parties that are competing with one another are less likely to form an indirect tie due to the high level of commitment required or knowledge leakage concerns (Gimeno, 2004; Hernandez, Sanders, and Tuschke, 2015). Those findings reinforce the importance of directly accounting for competitive forces in modeling network evolution.

Limitations and Future Research

Future research can help address some of this study’s limitations. First, future research can measure the existence and the content of the information flow directly (e.g., Aral and Alstyne, 2011). Although the idea of LPs receiving referrals and soliciting feedback from co-investors of potential targets is consistent with the limited qualitative evidence provided here, future research can use surveys of LPs and venture capitalists to capture such exchanges and their effects on LPs’ decision making directly (for a good example of such design in the VC setting, see Wang, 2010). Such research will not only conclusively demonstrate the role of information flows across social ties in the investment selection process but will also shed light on the underlying interpretation processes. Under what conditions do successes (or failures) lead to transferring positive (or negative) information to the LPs? Under what conditions do competitive concerns lead to withholding introductions or passing negative information on to a syndication partner? Under what conditions does this information affect the LPs’ investment decisions? Measuring the information flows directly can provide conclusive evidence for the mechanisms that I am only indirectly inferring from the investment decisions and network structure.

Second, future research can examine in more detail finer variations in the intensity and the valence of the informational signals. I focused on understanding the differences in behavior caused by clear contrasts: unambiguously successful relationships versus unambiguously failed ones. Within those clear categories there is more variation. In individual collaborations, some of the successes may be greater than others, for example, in the valuations that they achieve and the returns that they bring to the investors; similarly, some of the failures can involve near total loss for investors, whereas others may nearly break even. With no detailed data on the deal level, it is difficult to distinguish among such variations in successes and failures. Furthermore, even the same magnitude of successes and failures may elicit different attributions about their root sources that are critical in determining the future relationship and mutual assessments of the collaborators (Gulati, Wohlgezogen, and Zhelyazkov, 2012). What if in an actor’s view, the ultimate success has come in spite of the partner’s shirking (Carson, Madhok, and Wu, 2006)? What if a losing struggle against all odds brings collaborators closer together? Such attributions are impossible to assess without survey evidence, and future researchers can go further in exploring these off-diagonal effects. Finally, at the level of the broader relationship between the VCs, I focused on comparing ties that had only successes versus ties that had only failures. Naturally this produces a rather sizable category of ambivalent ties for which I controlled but about which I did not make any substantive predictions. In the empirical results, such ambivalent ties did not have detectable main effects, as could be expected given the mixed signals that such ties are likely to convey (Stern, Dukerich, and Zajac, 2014). Yet such ties can be the object of fruitful future investigations precisely because their equivocality gives a lot of flexibility to the intermediaries in what information to pass on and what to emphasize, flexibility that they can use to their advantage (Schweitzer, 2002).