Abstract

The choice of market mechanism is key to success for any online marketplace. In recent years, as peer‐to‐peer (P2P) lending has seen phenomenal growth, leading P2P lending platforms have used various market mechanisms and, in some cases, even switched from one mechanism to another, chasing higher market share and overall growth. While Prosper.com, a leading P2P lending platform, has switched from the auction lending model to a fixed price lending model, recent studies show that overall social welfare was higher with the auction lending model. While the auction lending model gives more power to the lenders, the success of the auction lending model hinges on the accuracy of lenders’ assessment of the credit risk of the borrowers. Building on extant literature and in support of the auction lending model to increase social welfare, we design an artifact to dynamically estimate borrower reputation to help the lenders and improve the allocative efficiency in P2P lending markets. We posit that borrowers’ reputation built on transactional data, readily available on P2P lending platforms, represents the collective perception of the lenders about the borrowers. We propose a dynamic latent class model of reputation and use the latent instrumental variable approach to deal with endogeneity. We test our artifact using real‐world P2P lending data. We show that accounting for reputation improves the model's explanatory power and provides a way to empirically model the evolution and impact of reputation in online platforms where repeated transactions are performed.

Keywords

INTRODUCTION

In contrast to traditional lending institutions, online peer‐to‐peer (P2P) lending platforms

1

facilitate a direct connection between borrowers and lenders. P2P lending, also known as

P2P lending platforms aim to eliminate traditional financial intermediaries such as banks and stand to disrupt traditional lending (Rigbi, 2013), especially the lower end of the market, by offering unsecured loans without collateral (Herzenstein et al., 2011). The traditional lending approach in financial markets requires intermediaries (e.g., banks) to evaluate potential borrowers based on their credit history (fair isaac corporation scores). In contrast to the traditional approach, on P2P lending platforms, a loan is approved if several lenders are willing to participate (lend), and the market decides whether a borrower should get a loan with the proposed terms. With its popularity, growth, and value proposition, P2P lending, considered a threat by traditional lenders, has now attracted interest from large traditional financial institutions. 2 Market research shows that global P2P lending is expected to increase from 64 billion USD in 2015 to 1 trillion USD by 2025. 3

Since lending money to strangers entails more risk, compared to many other online product/service transactions (Yum et al., 2012), the problem of adverse selection (Akerlof, 1970) becomes more severe in P2P lending. However, these risks can be mitigated by the platforms and market regulations. For example, to register on P2P lending platforms, borrowers must undergo a rigorous identity verification process and provide information such as a driver's license and social security number. However, despite this, borrowers’ propensity to default on a loan remains difficult to assess for the lenders, partially because lenders have no formal training in risk assessment. Therefore, lending platforms need to play a crucial role, not only in providing enough information to mitigate adverse selection but also in facilitating/designing a market mechanism that attracts both the borrowers and the lenders (Hortaçsu & McAdams, 2010).

Information asymmetry (Akerlof, 1970) between transacting parties on online platforms is inevitable, and therefore scholars and practitioners have developed trust‐building mechanisms such as reputation systems (Dellarocas, 2003) to mitigate information asymmetry. Unlike many other online platforms, P2P lending platforms usually do not provide an explicit reputation system to mitigate information asymmetry and assess borrowers’ trustworthiness. Lenders do not rate borrowers because there is no single outcome that can be used to evaluate borrowers. The lack of a reputation system that can assess borrowers’ reputations in P2P markets leads to adverse selection, lower market efficiency, and loss of surplus. This research aims to fill this gap by developing a borrowers’ reputation system for lenders on P2P lending platforms.

Practitioners and academic scholars have long used online activities or behavioral patterns to classify and predict/explain users’ decision‐making in online markets. For example, Amazon.com has recently started a lending program for sellers on Amazon.com. Amazon uses sellers’ activities on the platform

4

(e.g., sales history) to estimate their credibility (reputation) to determine whether and how much to lend. Similar to other online platforms, P2P lending platforms provide a wealth of information on virtually all the activities of the borrowers on these platforms. In addition, P2P lending platforms also provide hard credit information such as credit grade, debt‐to‐income ratio, and the number of delinquencies, which can be used to estimate borrowers’ reputations. Therefore, in this research, we use borrowers’ transactions and activities to estimate their reputation in P2P lending markets, which can aid lenders in their decision‐making. We posit that this virtual repository of transactional data on the borrowers in the P2P lending community helps them build

In this study, we propose an artifact to assess the borrowers’ reputation using a dynamic latent class (DLC) model of reputation. We evaluate our artifact with real‐world data from a leading P2P lending platform. Since literature has shown that the auction model of lending leads to a higher social surplus (Luo et al., 2021; Z. Wei & Lin, 2017), we will evaluate our artifact with the data based on the auction model of lending. Our results show that the constructed reputation of the borrowers, estimated by the proposed artifact, explains the

This research contributes to the existing body of research at the interface of operations management and information systems (Kumar et al., 2018), particularly the recent stream of studies on P2P markets in operations management literature. Scholars have explored the role of P2P marketplaces and the dynamics of P2P lending (Luo et al., 2021; Juanjuan Zhang & Liu, 2012), in traditional supply chains (Jiang et al., 2017) and crowdfunding environments (Z. Li et al., 2020). These studies show that participants in these markets use a variety of signals to assess the risk of transactions and the reputation of the other party to mitigate the adverse selection problem, inherent in these markets. Indeed, transacting with individuals with lower reputations contains more risk than transacting with ones with higher reputations. Since participants cannot adequately assess the risk, they often follow other lenders and resort to herding (Juanjuan Zhang & Liu, 2012) to mitigate their risks. We contribute to this literature by proposing a reputation system to mitigate adverse selection problems in these markets.

The paper is organized as follows. We highlight the relevant literature in Section 2 and discuss our conceptual model in Section 3. In Section 4, we discuss our proposed model of reputation and the parameters that need to be estimated. In Section 5, we discuss data and estimation, and in Section 6, we provide and discuss the results. We discuss an alternative approach for estimating reputation in Section 7, and, finally, conclude in Section 8.

LITERATURE REVIEW

The concept of reputation has been widely studied in operations management and other academic disciplines such as economics, strategic management, and organizational theory (Fombrun & van Riel, 1997). Our study relates to the literature on social capital accumulation and reputation building in consumer‐to‐consumer online platforms. P2P lending, like most other instances of electronic commerce, is a form of online exchange in which most transactions occur between strangers (Ba & Pavlou, 2002; Jiang et al., 2017), giving rise to information asymmetry between transacting parties (Akerlof, 1970). Therefore, lenders’ trust in borrowers is critical for the success of these online platforms. Trust‐building mechanisms such as reputation systems are the norm in online markets because they can reduce the perceived uncertainty and risk associated with online transactions and help consumers get more actively involved in online activities like exchanging personal information and purchasing goods and services (Burtch et al., 2021; Greiner & Wang, 2010; Kokkodis & Ipeirotis, 2016).

Scholars have studied reputation mechanisms that help online commerce participants better understand members’ types and future actions based on their previous activities (Despotovic & Aberer, 2006; Kokkodis & Ipeirotis, 2016; Marti & Garcia‐Molina, 2006). While the literature has examined the impact of reputation on an agent's decisions and performance on platforms such as eBay (Houser & Wooders, 2006; Melnik & Alm, 2002; Resnick & Zeckhauser, 2002), most of the existing reputation and trust literature focuses on institution‐based trust or the evolution of reputation and buyers’ trust in sellers (e.g., Ba & Pavlou, 2002; Greiner & Wang, 2010). In contrast, both borrowers and lenders in the P2P lending environment are embedded in a community, and therefore it is important to explore a community‐based reputation system (Collier & Hampshire, 2010), which would be more appropriate in this context. Therefore, this research aims to develop a dynamic and community‐based reputation system for borrowers to help lenders assess borrowers’ trustworthiness.

Existing research on P2P lending can be categorized into two broad areas. The first group of studies focuses on the effects of social network structure (e.g., Lin et al., 2013; Lu et al., 2021), intermediaries, and features of P2P lending markets, such as groups and friendships on the performance of P2P lending. Performance in this context is measured by loan performance, loan default, and so forth. This stream of literature focuses on lenders’, borrowers’, and lending platforms’ strategies and their payoffs. For example, lenders try to use borrowers’ social ties and associations to assess borrowers’ types to minimize their risks of lending. Since lenders are not experts in assessing borrowers’ types, they also display herding behavior as they aim to maximize their payoffs (Berger & Gleisner, 2009; Collier & Hampshire, 2010; Lin et al., 2009, 2013; Xiao et al., 2021). Borrowers use association with groups and other users to signal their types and strategize via various market mechanisms (Luo et al., 2021).

On the other hand, lending platforms attempt to minimize their risk and maximize their payoffs using their power as market makers (Cheng & Guo, 2020; Z. Wei & Lin, 2017). The second group consists of studies that apply existing economic theories to P2P lending, develop new ones, and explore the effectiveness and efficiency of P2P lending marketplaces for creating a more open and competitive credit market (Herzenstein et al., 2011; Iyer et al., 2016; Rigbi, 2013; Y. Wei et al., 2015; Juanjuan Zhang & Liu, 2012). Our study falls in the first group. Next, we elaborate on studies related to our work and highlight our contributions to the literature.

Greiner and Wang (2010) examine lenders’ decision‐making in P2P marketplaces and find that borrowers’ hard credit information and social capital influence lenders’ trust in borrowers and eventually lending decisions. They argue that borrowers’ hard credit information is a major driver in lenders’ decision‐making, and borrowers’ social capital is merely a peripheral cue. However, recent studies have detected a more substantial influence of borrowers’ social networks and capital in P2P lending markets (e.g., Freedman & Jin, 2017; Lu et al., 2021). While it is true that borrowers’ friendships and social ties impact their likelihood of success in these markets, there seems to be significant heterogeneity in lenders’ ability to assess risk associated with P2P lending, and partially due to that, we observe herding among lenders (Juanjuan Zhang & Liu, 2012). Tang and Whinston (2020) study the effect of imposing reputational sanctions against companies with large spam volumes and find that the threat of reputational sanctions resulted in significantly reduced spam indicating the importance of reputation to organizations. We extend this line of research by proposing a borrowers’ reputation system to assist lenders in this market. We simultaneously assess the success of a loan, the interest rate, and the risk of default, accounting for serial correlation and potential endogeneity. Our results show that borrowers’ reputations can explain the heterogeneity in the

Collier and Hampshire (2010) argue that by embedding individual reputations within a community reputation, incentives become aligned for peers to select highly qualified borrowers and produce information signals to reduce the information asymmetry issues of any principle–agent relationship. They focus on groups and memberships in a P2P lending system and utilize agency theory to examine signals that enhance community reputation. However, scholars argue that a borrower's mere association with a community or group may not decrease their risk of default (Everett, 2015). Hildebrand et al. (2016) even find evidence of perverse incentives in crowdfunding that are not fully recognized by the market, such as the bids by group leaders in the presence of origination fees resulting in loans with lower interest rates and higher default rates. Therefore, we argue that borrowers’ hard credit and their transactional activities should be taken into account along with their social capital to assess their creditworthiness.

Lin et al. (2013) analyze a sample of listings from Prosper.com to find that online friendships of borrowers act as signals of credit quality. They find evidence that friendships increase the probability of successful funding, lower interest rates on funded loans, and are associated with lower

In P2P lending, interactions between lenders and borrowers are akin to repeated games where strategies could differ significantly from a single game. Prior research has argued that repeated game strategies are a sequence of rules that might depend upon the preceding outcomes (Rubinstein, 1979). Because of the repeated plays, agents can respond to each other's actions, so they must consider this and other players’ reactions before choosing their actions (Gossner & Tomala, 2007). Information asymmetry is present in online transactions, more so in P2P lending because of higher stakes. Therefore, reputation and reputation building is vital; assuming the agents (borrowers) are heterogeneous, reputation works as a means for agents to signal their type (Guda et al., 2021).

CONCEPTUAL MODEL AND RESEARCH FRAMEWORK

An issue inherent to P2P lending platforms is adverse selection due to the information asymmetry between borrowers and lenders. While a reputation system seems to help lenders in P2P markets, developing a reputation system for P2P lending platforms has its challenges. First, unlike online markets for products and services, where transacting parties rate each other after the transaction is completed, lenders and borrowers do not give explicit ratings to each other on P2P lending platforms. Second, transactions in P2P lending are different from transactions in retail markets, where the transaction is between a seller and a buyer. In P2P lending, many lenders fund a loan, so it is not easy to rate the borrower after a successful loan application. Third, even if we have explicit ratings, recent research has questioned the integrity and credibility of these reputations/ratings (e.g., Bolton et al., 2013). Scores of studies and reports 5 show that online reputations/ratings are inflated, partially due to fraudulent 6 or reciprocal behavior of transacting parties. Therefore, researchers are exploring fixes for reputation systems while the industry is scrambling to find alternatives 7 to existing reputation systems. We posit that a reliable reputation system is critical for the long‐term success and survival of online markets such as P2P lending platforms.

To address the problems with current reputation systems, Moreno and Terwiesch (2014) proposed that reputation/ratings should be built on both structured and unstructured measures. Structured measures refer to numerical ratings, and unstructured measures refer to textual comments (praises or complaints) assigned to each other by transacting parties. We argue that users’ transactional history should also be taken into account along with structured and unstructured measures to develop a robust reputation measure in online markets such as P2P lending platforms. We posit that the transactional data generated on P2P lending platforms could alleviate information asymmetry and potentially lead to higher efficiency than those driven by algorithmic procedures of financial institutions (Brabham, 2008; Kittur et al., 2007).

We hypothesize that every borrower establishes some form of identity through participation in the online lending community, which signals their trustworthiness. Following the literature in economics, we refer to this directly unobservable identity as the borrower's reputation. This is possible because all the users in the P2P lending market are uniquely identified and tracked, and borrowers cannot reset their history of actions and start afresh. So there are lasting consequences to decisions and actions the members take. From a modeling point of view, this unobservable reputation can be modeled as a latent construct, the value of which changes over time due to borrowers’ actions. From an empirical point of view, two levels of heterogeneity are relevant here. First, borrowers are heterogeneous in their reputations, which change with time. Second, lenders are also heterogeneous in their perception of borrowers’ reputations. In other words, different lenders might consider different criteria in evaluating the borrowers’ reputation and therefore have different evaluations of their level of reputation. For example, some lenders might put greater weight on a borrower's age and experience in the lending community. Our model does not try to capture this level of heterogeneity in lenders in defining and measuring reputation. Instead, we consider the average reputation of the borrowers within the lending community.

To address market inefficiencies and expedite the loan approval process, in December 2010, Prosper.com, switched from auctions to a fixed‐price model of P2P lending. 8 In the auction mechanism, lenders compete and determine the interest rates on a loan application. In the fixed‐price model, Prosper calculates fixed interest rates for every loan, akin to traditional lending institutions (e.g., banks). While the fixed‐price mechanism aims to deploy funds quickly, recent studies (Luo et al., 2021; Z. Wei & Lin, 2017) show that the auction mechanism is better than the fixed‐price model from a social welfare perspective. The fixed‐price model results in higher interest rates and, hence, a higher likelihood of loan default (Z. Wei & Lin, 2017), which hurts both borrowers and lenders. The drawback of the auction model is that the lenders may not be able to assess the risk of their investments because, unlike online markets, P2P lending platforms do not have reputation systems to assess the borrowers’ trustworthiness. This research aims to fill this gap by designing an artifact to assess borrowers’ reputations based on their prior transactions.

One could argue that, at least in the short term, the fixed‐price model is favorable for Prosper.com because Prosper gets all its fees paid at the time of loan origination and does not suffer losses in case of a default. In other words, while higher interest rates in the fixed‐price model increase the propensity to default, they also increase the bottom line for Prosper.com. Therefore, instead of continuing with the auction lending model, which was open and transparent in determining loan interest rates and borrowers’ trustworthiness, Prosper.com now estimates borrowers’ reputation/creditworthiness, and an acceptable interest rate for every loan request, behind the curtain. Overall, it appears that Prosper has transitioned from an open and transparent market to a closed one, which benefits Prosper but lowers social surplus (Z. Wei & Lin, 2017).

While market participants, in any marketplace, choose different information revelation strategies (G. Li et al., 2021; Tsunoda & Zennyo, 2021), scholars argue that

We contend that an open and transparent reputation system helps assess the trustworthiness of the trustee (borrower), improves market allocation and liquidity, and eventually benefits all the stakeholders—lenders, borrowers, and the lending platform. Such a reputation system can be developed based on the borrowers’ activities and transactions on the platform. While a reputation system helps all the lenders to assess the borrowers’ reputation, the heterogeneity in lenders’ risk appetite drives the allocative efficiency of the market.

In the auction model, borrowers choose how much money they want to ask for when creating the loan listing. Borrowers also must specify the maximum interest rate they are willing to pay for the loan and the duration for which the listing will be active. Once the loan listing is created, it will be posted on the platform, among other listings. Lenders can browse the available listings and decide whether they want to invest in a listing or not. If a lender chooses to invest, she should submit a bid. Bids include an amount and the minimum interest rate the lender is willing to accept (which cannot be greater than the maximum interest rate posted by the borrower). By bidding on a listing, a lender effectively commits to invest in the loan. They use the financial and personal information about the borrowers and the information available on borrowers’ prior activities on the platform when making these decisions. To mitigate risk, most lenders choose to diversify their investment portfolios and lend only small amounts to any single borrower.

Suppose the aggregate number of bids submitted by the lenders on a given listing reaches the amount requested by the borrower. In that case, new lenders who want to invest in the loan must compete with the existing ones by lowering the interest rate they submit. Therefore, the final interest rate of a loan could be lower than the borrower's specified maximum rate. The final interest rate and the winning lenders are decided through an auction. The auction mechanism is similar to a Dutch auction in that the bidders who have submitted the lowest interest rates are selected until the full amount is funded. All the winning bidders receive the same interest rate, the lowest losing interest rate.

When creating the listing, borrowers can let the listing be active until the end of the selected duration or have the auction clock stop once the total amount submitted by the lenders reaches the amount requested by the borrower. This choice will be displayed on the listing information page. When one of the conditions to end the listing auction is triggered, that is, either the listing is fully funded for those who have selected the option or the duration of the listing ends, the listing expires. Then if the total amount requested is covered by the submitted bids, the P2P platform owner will take the money from winning bidders and consolidate and transfer the funds to the borrower. Next, the borrower starts paying back the principal and interest on the loan through monthly installments.

EMPIRICAL MODEL

Using our empirical model, we examine the role of borrower reputation in different stages of P2P funding. We first propose a latent class model to describe the borrowers’ unobserved reputation states, based on both structured and unstructured measures. Next, we explore how borrower reputation explains the success/failure of a listing and the decrease in the interest rate for a successfully funded listing. Finally, we explain how borrowers’ reputation can explain their propensity to default on loans. Note that the success of a listing and the decrease in interest rates are

DLC model of reputation

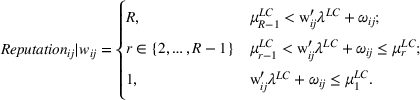

We propose a DLC model of reputation and assume that there is a finite number of states of reputation in which a borrower can reside at any point in time. The reputation states are not directly observable but can be observed through their impact on a set of observable outcomes. Our primary goal in this model is to characterize the evolution and impact of reputation. Our approach effectively segments the borrowers at any time into

To characterize the latent class model, we use an ordered Probit model, which is essentially a model with

Since the coefficients of the ordered Probit model are not state‐dependent, the vector of coefficients of the underlying stock of reputation,

Listing success model

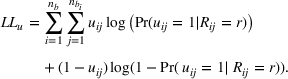

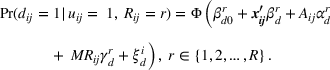

We utilize a binary Probit model to investigate the probability of a listing being successfully funded or, in other words, the probability of converting a listing into a loan. Specifically, the probability of observing the successful conversion of a listing into a loan for borrower

Description and summary statistics of the listing variables

Interest rate model

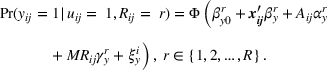

In the online P2P lending community we study, borrowers post listings stating the amount needed and the maximum acceptable interest rate. Lenders compete via an auction by submitting the amount they intend to invest and the minimum interest rate they are willing to accept. Suppose the listing is fully funded and the number of bids submitted exceeds the amount of loan requested. In that case, the process of selecting lenders boils down to a competition based on the minimum interest rate they have submitted. Therefore, the final interest rate of a successful listing,

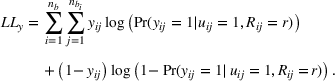

Similar to the listing success model in (4), the probability of observing a reduction in interest rate is modeled as depending on a reputation‐dependent intercept,

The log‐likelihood function can be modeled as follows:

Default model

Next, we elaborate on how borrowers’ reputation can explain their propensity to default on loans. Note that default on loan is an

Similar to the interest rate model in Equation (6), the default is only relevant in the case of successful listings. Therefore, we model the default decision conditional on listing success. Specifically, the covariates of the model are similar to Equations (4) and (6). The intercept and the vector of coefficients

Interdependence and error structure

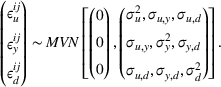

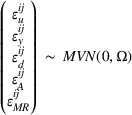

It is reasonable to assume that the contemporaneous random shocks in the conversion model (Equation 4), the interest rate model (Equation 6), and the defaulting model (Equation 8) could be correlated, as the unobserved factors conducive to a listing's success might also help achieve a lower interest rate and might be related to the unobserved factors that drive borrowers’ propensity to default on a loan. To account for this potential interdependence, we assume the following covariance structure for the normal idiosyncratic error terms in each model and later estimate the parameters of the covariance matrix along with other model parameters. For identification purposes, we fix the standard deviation of

LIV

The requested amount,

A common approach to dealing with endogeneity is the instrumental variable estimation approach, which is often challenging due to a lack of required data (e.g., Rutz et al., 2012; Staiger & Stock, 1997). Therefore, in this paper, we utilize the LIV approach, an instrument‐free method proposed by Ebbes et al. (2005). Instrument‐free or frugal approaches to dealing with the endogeneity problem utilize statistical procedures that do not require observed instruments and, therefore, circumvent the instrument availability and validity issues. The LIV approach is a likelihood‐based method that assumes we can separate the endogenous variable into two parts, an endogenous part and an exogenous part. The unobserved exogenous part is approximated using a latent discrete variable with a finite number of levels (Ebbes et al., 2009). Researchers have successfully applied the LIV approach to account for endogeneity in marketing applications (e.g., Rutz et al., 2012; Jie Zhang et al., 2009). Using the LIV method, we can decompose each of the endogenous variables as follows:

DATA AND ESTIMATION

The data used in this study was collected from one of the largest online P2P lending websites in the United States, Prosper.com. The P2P platform owner is in charge of receiving the money from the borrowers and dividing it between the lenders. In the event of late payments or default by the borrowers, the P2P platform owner attempts to collect late payments on the lenders’ behalf through various collection practices (Herzenstein et al., 2008). Serious delinquency could result in the account being sent to collections. The platform owner reports the borrowers’ activities to major credit bureaus, so late or missed payments may damage borrowers’ credit scores and make it more difficult for them to get a loan in the future (Steinisch, 2012). The P2P platform earns money by charging a transaction fee on listings that are fully funded and successfully transformed into loans. The borrowers are charged a one‐time origination fee as a percentage of the loan amount when a loan is successfully initiated, and the lenders pay an annual loan servicing fee as a percentage of the outstanding principal balance of the corresponding loans.

Since we aim to test the value of a reputation system on a P2P platform, we used the data when Prosper.com allowed an auction model for lending on its platform and provided a wealth of data on past individual activities. Prosper.com switched from the auction lending model to a fixed interest rate lending model in December 2010 (Luo et al., 2021), so our dataset includes complete data on all activities, that is, the listings, bids, loans, and members, from early 2006 to the end of April 2009. We also supplemented the dataset with payment data until September 2012 for the loans created in 2006–2009. This provides us with around 37 months of data on all the listings, loans created, and bids submitted by the lenders.

For this study, we only considered borrowers with at least three of their listings successfully funded and converted into loans. This is done because the notion of reputation building and being able to model and capture it heavily relies on having a reasonable number of prior activities and available information. Otherwise, it may suffer from the so‐called cold‐start problem (Lam et al., 2008; Lu et al., 2015), common in online recommender systems. Therefore, the reputation effect cannot be identified unless historical information is available. Moreover, the large size of the data makes it computationally prohibitive. This criterion narrowed down our dataset to 3191 listings from 364 unique borrowers. Table 1 shows the listing‐level variables and constructs studied in this research, accompanied by a short description and their means and standard deviations for our selected data. The covariates included in our three structural equations,

Table 2 provides information on our reputation level variables out of which we have selected the covariates to be included in our underlying model of reputation stock,

Description and summary statistics of the reputation variables

We utilize an empirical Bayesian approach and estimate the model using a Markov chain Monte Carlo (MCMC) estimator with multiple Gibbs and Metropolis steps. The estimation details are provided in Appendix 1 in the Supporting Information. Since the LIV method is a likelihood‐based approach, it is amenable to MCMC estimation. A benefit of the Bayesian approach is that it allows us to get draws of the model's parameters, whereas in the frequentist approach, only point estimates are attained. From the practitioners’ point of view, the Bayesian approach allows the platform designers to estimate the distribution of the parameters for each of the borrowers separately. This provides a flexible random component specification that allows us to incorporate both observable and unobserved borrower heterogeneity (Agarwal et al., 2011).

One of the challenges with the Bayesian analysis is deciding on the prior distribution of the parameters, as in many applications, ours included, no useful prior information exists. This issue is highlighted in the context of hierarchical models when the number of parameters is large and their interpretation is complex. One way to deal with this is using empirical Bayes, in which the existing dataset is used to get the prior distribution parameters. They are made as uninformative as possible such that the weight of the prior is minimal in determining the posterior distribution. In this study, we use empirical Bayes, particularly a class of empirical Bayes priors called g‐priors, for our second‐level coefficients (Hoff, 2009).

Although the joint posterior distribution of the model is non‐standard, we use an iterative algorithm that constructs a dependent sequence of parameter values whose distribution converges to the parameters’ joint posterior distributions (Hoff, 2009). At each step, we form the full conditional posterior distribution of a group of parameters by conditioning on the current values of all other parameters that are being estimated. The details of the estimation steps are provided in Appendix 1 in the Supporting Information.

RESULTS AND DISCUSSION

To get the initial values for the parameters, we first drew 50,000 samples for each of the three equations separately. Then we used the mean of the last 20,000 draws as initial values for the coefficients in each of the models. To estimate models M1 (the baseline model) and M2 (the DLC model), we implemented the MCMC code in R for estimating each model. To ensure that the effect of initial values has dissipated, out of the 25,000 resulting draws, we discarded the first 5000 as the burn‐in samples and used the remaining 20,000 samples to draw inferences. To reduce the correlation and to be able to easily compare the estimated coefficients, the variables are mean‐centered, normalized (dividing by their standard deviation), and scaled down by a factor of 10. Since our data spans several months, we control for the effects of the state of the economy by including year and month dummies and the daily averages of the Dow Jones Industrial index in our models.

We estimated a model with three simultaneous equations with no explicit reputation component (M1—the baseline model) and a DLC model (M2). Deviance information criteria (DIC) was calculated for both of these models. DIC is a measure of fit for Bayesian model estimation that values both fit and parsimony by penalizing models that have a larger number of effective parameters (Aktekin, 2014; Z. Li et al., 2020; Spiegelhalter et al., 2002). In both models, we use LIVs with the same number of categories to account for potential endogeneity. As we see in Table 3, our DLC model, M2, with three states (the best latent class model in terms of fit), outperforms the baseline model (M1).

Model comparison

Therefore, we only report the estimation results for the DLC model of reputation. To estimate a latent class model, we need to determine the number of states as an input to the model. Table 4 shows the deviance information criterion for DLC models with 2, 3, and 4 reputation states. The model with three reputation states provides the best comparative fit as it has the lowest DIC among the three models. The three reputation states will hence be labeled as low, medium, and high reputation levels.

Comparison of DLC models for different number of states

The LIV approach is generally robust to the specification of the number of categories as long as there are at least two categories (Ebbes et al., 2005; Rutz et al., 2012). However, in order to decide on the number of categories for each of the LIVs, we estimated our three‐state DLC model with combinations of 2, 3, and 4 categories for each of the LIVs. As we can see in Table 5, the model with three categories for the listing amount LIV and two categories for the maximum interest rate LIV outperforms the other models.

Comparison of latent instrumental variable (LIV) latent class models for different numbers of categories

After deciding on the number of reputation states, and the number of latent categories for each instrument, we estimate the model and provide the results in Tables 6

–10. Table 6 shows the posterior means of the coefficients of the Probit model of listing success. Credible intervals (Edwards et al., 1963) or Bayesian confidence intervals are calculated as the empirical quantiles of the drawn samples. As usual, if an interval contains zero, it indicates that the coefficient is not significant at

Listing success model estimates (

A careful inspection of the coefficients for each reputation state reveals some interesting patterns. The intercept shows that borrowers with a higher reputation state are more likely to get funded, which is intuitive. Also, the coefficient for the amount for low‐reputation and medium‐reputation borrowers is negative and significant, meaning that the listings for a higher amount from lower‐reputation borrowers are less likely to be funded (Lin et al., 2013). As expected, the opposite is true for the high reputation borrowers. For high‐reputation borrowers, lenders are even more willing to lend if the amount requested is higher. While significantly negative for low‐reputation borrowers, the coefficient for the maximum interest rate in listings is positive and significant for medium and high‐reputation borrowers and improves their chances of getting a loan. Our findings also confirm that without other credit‐related information, soft information helps build lenders’ trust in borrowers (Duarte et al., 2012; Hildebrand et al., 2016). For example, bids from friends can help build trust in borrowers and increase the probability of getting funded.

Tables 7 and 8 present state‐level posterior means of the coefficients for interest rate and default models, respectively. We observe trends similar to the listing success model (Table 6). The magnitude of the intercepts in the interest rate model is increasing with reputation. In other words, the probability of obtaining lower interest rates on loans is lowest for low‐reputation borrowers and highest for high‐reputation borrowers. Further, the maximum interest rate is negative and significant for low‐reputation borrowers. We argue that lenders are risk‐averse and distrust listings with a higher interest rate from low‐reputation borrowers. Interestingly, the number of delinquencies of the borrowers is only significant in the interest rate model for low‐reputation borrowers. We acknowledge that it is possible that there is not enough within‐class variation for some of these variables, and their effects are captured indirectly through the borrowers’ reputation level. Therefore, we suggest further investigation is needed in future research.

Interest rate model estimates (

Default model estimates (

According to the estimates in Table 8, all else being the same, lower‐reputation borrowers are more likely to default as the intercept for them is decreasing in the Probit model of default. Higher loan amount with higher interest rates by low‐ and medium‐reputation borrowers is more likely to result in default, but the coefficient is significantly negative for high‐reputation borrowers, which indicates that high‐reputation borrowers may even be less likely to default when they get larger loans. A higher number of friends’ bids (

Table 9 shows the posterior means and statistical significance of the ordered Probit model of reputation evolution. Some insignificant variables are also included to provide insights. The cumulative number of bids to income ratio, the cumulative number of friends’ bids, the change in credit grade, and the number of friends all have positive and significant estimated coefficients. This means that a borrower with a larger value of these variables is likely to have a higher reputation. The estimated coefficient for the cumulative number of listings, loans, and defaults are negative and highly significant, meaning that previous defaults adversely impact borrowers’ reputations. The estimated thresholds of the ordered Probit model are also reported in Table 9. The significant and well‐separated estimates of the LIV category means in Table 10 provide evidence that the LIV model is well‐identified.

Reputation model estimates (

LIV parameter estimates

ALTERNATIVE MODEL: A HIDDEN MARKOV MODEL (HMM)

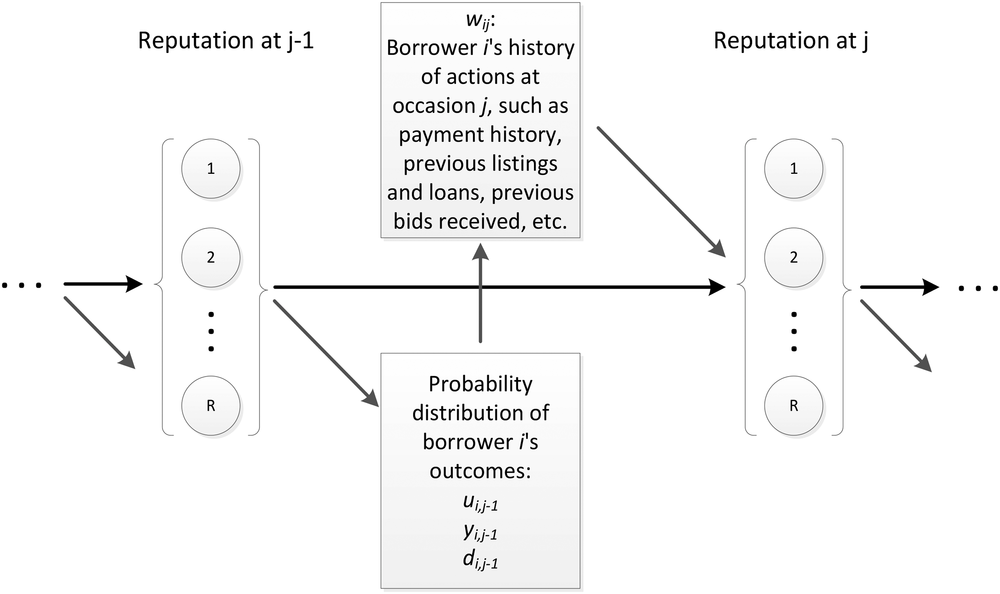

A counterargument to our approach to estimate the reputation model discussed in Section 4 is that reputation at any moment may depend on borrowers’ reputation in the previous period. In online markets, sellers’ ratings/reputations are based on their prior transactions and predict their future performance. Literature in organizational behavior also argues that users’ performance in the current period is anchored with their performance in previous periods (Huber, 1989). Therefore, in this section, we examine if reputation in the current period depends on the reputation in the previous period. We present an alternative approach to estimate borrowers' reputations using transactional history data along with structured and unstructured measures (Moreno & Terwiesch, 2014). Our alternative approach is based on a HMM in which a borrower's latent state of reputation in a period directly depends on her reputation in the previous period through a state‐dependent transition probability matrix. Similar to our main model, we assume that each borrower is in one of a set of

As shown in Figure 1, our HMM captures the dynamic evolution of reputation and the impact of reputation on the outcomes of interest. The outcomes at any time period depend on a borrower's reputation only through the borrower's reputation at that period. A borrower's reputation at any period depends on her past reputation only through the borrower's reputation in the previous period. We provide the details of our HMM model in Appendix 2 of the Supporting Information Figure 1.

The hidden Markov model of reputation

To compare our estimations from the HMM with the DLC model discussed in Section 4, we follow a similar estimation approach as discussed in Section 5. Although we have already established in Section 6 that the DLC model performs better than the baseline model with no reputation component, we still include our baseline model here for comparison. Further, following the results in Table 4, we estimate the HMM with three states of reputation. The values of the DIC measures in Table 11 show that the DLC model outperforms the HMM and therefore is a robust approach for estimating a borrower's reputation in P2P lending platforms. This supports the notion that the lenders’ perception of a borrower's reputation is determined solely through the available information on the borrower, and the stochastic updating of the reputation in the next period does not explicitly depend on the current state of reputation. This is reasonable, as there are many lenders in the community, each of whom evaluates a borrower's reputation at a given time, regardless of the borrower's reputation in the prior period.

Model comparison

CONCLUSIONS AND LIMITATIONS

P2P lending platforms offer unsecured loans without collateral (Herzenstein et al., 2011) and compete with traditional lenders, especially at the lower end of the lending market. In a way, P2P lending platforms, such as Prosper.com, have democratized lending by giving lenders the necessary information and power to assess borrowers’ risk and trustworthiness and offer unsecured loans.

In recent years, P2P lending markets appear to be transitioning from a lender‐driven auction lending model to a platform‐controlled fixed interest rates model, despite the superior performance of auction lending models (Luo et al., 2021; Z. Wei & Lin, 2017). The transition from auction to fixed‐interest rates lending model has been attributed to challenges associated with the lack of lenders’ expertise in assessing borrowers’ risk. To address this challenge, we develop a borrower reputation system based on borrowers’ activities on these lending platforms.

A borrower's type, that is, her creditworthiness, is private information to the borrower, leading to information asymmetry in this context (Xiao et al., 2021). To mitigate this information asymmetry, lenders use the available information about the borrowers as signals to infer the borrowers’ types. Since not all lenders are experienced in assessing borrowers’ types, this could lead to an inefficient market. We posit that our proposed dynamic reputation model, which is open and available to all the lenders in the community, mitigates the information asymmetry, helps P2P lenders, and increases allocative efficiency in this market. Lenders’ beliefs about borrowers are updated based on their activities on the platform, and we posit that a borrower's reputation affects her outcomes in the P2P community. In fact, along with borrowers’ hard credit information, P2P lending platforms also provide information about borrowers’ transactional activities such as details of the borrowers’ prior loan requests, successful loans, loan payback information, social networks, and so forth. In this study, we extract value from borrowers’ transactional and social activities by developing a borrower reputation system.

We propose two ways to model a borrower's reputation, a DLC model and an HMM as a robustness check. The difference between the two is that the transition probabilities between states in the HMM directly depend on borrowers’ current states. We are also among the first to use the LIV approach to account for potential endogeneity in the amount requested and the maximum interest rate posted by the borrowers in P2P lending.

We utilized an MCMC estimator with Gibbs and Metropolis steps and estimated the two models using a pseudo‐hierarchical Bayesian approach. We used DIC, the deviance information criterion (Aktekin, 2014; Z. Li et al., 2020; Spiegelhalter et al., 2002) to measure the goodness of fit of the models and found that the DLC model of reputation with three states outperforms the others. We provided parameter estimates for each reputation state and showed that our modeling approach provides a means to tease out the varying effects of covariates on the outcomes of interest for borrowers in different reputation states. One way to interpret the findings is to assume that the estimated coefficients for each state represent a model through which the outcomes for a borrower at that stage are decided. A borrower's updated reputation can be estimated, every time a piece of new information about the borrower is available.

Overall, we contribute to the growing literature related to interdisciplinary operations management research on crowdfunding (e.g., Hildebrand et al., 2016; Z. Li et al., 2020; Luo et al., 2021; Xiao et al., 2021) by proposing a novel artifact to model borrowers’ reputation and evaluated this artifact with real‐world data from a P2P lending platform. This approach is readily extendable to other online markets where agents’ reputations can be extracted from their actions and transactions. Our approach can also be used to classify borrowers on P2P lending platforms or users on similar platforms. As there are usually numerous issues with traditional instrumental variable estimation, our LIV approach could provide a viable alternative for investigating empirical questions in the presence of endogeneity. We are among the first studies to utilize the LIV approach to deal with endogeneity issues in applied operations management research.

While we believe our approach to modeling reputation combined with the LIV model to deal with potential endogeneity is helpful to many P2P platforms, our study also has many limitations. First, the data used in this study are about 10 years old. Since we developed a borrower reputation system that can be used in the auction model of P2P lending, we had to test our artifact using the data from when the auction model was used at Prosper.com. The dataset we use in this study also tracks all the actions and transactions of borrowers and lenders and their actions are traceable through their unique identification numbers. Moreover, as we discussed earlier in the paper, the auction mechanism is superior in terms of social welfare (Z. Wei & Lin, 2017). Due to the nature of our data, we could not compare the effectiveness of our measure of reputation against the metrics provided more recently by platforms such as Prosper.com, and this is an opportunity for future research.

The second limitation of our proposed mechanism is related to the number of states in our dynamic reputation model. Based on our dataset, the model with three states provides the best fit. However, from a practical standpoint, if the platform keeps updating the model with new data, the best number of states may no longer be three. To address this issue, the platform can periodically test models with various states and change the model if a model with a different number of states significantly outperforms the current model. Finally, we use the LIV approach to deal with the potential endogeneity in the amount requested and the maximum interest rate. This instrument‐free approach does not require finding instruments that satisfy exclusion and inclusion assumptions. However, it relies on distributional assumptions for endogenous and outcome variables and our ability to identify the distributions of the exogenous and endogenous parts of the endogenous variables. Ebbes et al. (2005) prove that the usual results on the consistency of maximum likelihood estimation can be applied to LIV models. Further, they confirm via Monte Carlo simulations that the LIV model yields unbiased results for many types of distributions for the instruments and that the model is robust to misspecification of the error distribution. Finally, our estimates of the LIV coefficients are well‐separated, which supports our assertation that the latent instruments in our model are correctly identified.

Footnotes

1

For example,

2

3

4

5

For example,

6

7

For example,

8

9

As a robustness test, we also used a linear regression approach to estimate the interest rate model and used a logit transformation (i.e.,

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.