Abstract

The improvement of the investment climate in Russia and its positive effect on the inflow of foreign direct investment into the country's economy is being declared at the highest levels of the Russian government as an important objective for the further economic development of the country. One of the most important instruments for that improvement should be the consideration of foreign investor's opinions and ideas and reaction to the most urgent and critical issues which serve as obstacles to their investment activities in Russia.

This paper considers the case of Japanese investors in Russia. It is based on the results of a survey of Japanese companies doing business in Russia (members of the Japanese Business Club Moscow) and content analysis of a set of interviews with the representatives of the Japanese business and academic community and also of non-governmental organizations.

We identify which factors attract Japanese capital to Russia and which hinder investment activities. Studying Japanese investment in Russia reveals the particular challenges and obstacles that make Japanese companies reluctant to engage in business activities in Russia. The research reveals and systemizes the factors restricting the development of investment cooperation and their roots, and identifies possible ways of overcoming these challenges.

The analysis shows that the constraining factors can be divided into 3 groups by the origin: external – associated with the problems of the investment climate in Russia, internal – associated with specific features of the Japanese production and management system, and other factors – non-economic factors which mainly concern business culture and informational issues.

Introduction

Investment climate analysis, especially in the context of institutional framework building in developing and transition economies, arouses great interest among researchers. A number of large international projects, such as EBRD Business Environment and Enterprise Performance Survey (BEEPS) 2 and Doing Business by the World Bank Group, 3 are focused on investment climate research and provide scholars with an extensive database of characteristics and indicators for different aspects of the issue which allow comparative studies to be conducted. Thus, in the paper of Hellman, Jones, Kaufmann, and Schankerman (2000), the authors summarize the results of a subset of questions from the BEEPS relating to governance and corruption in transition economies and its influence on the environment faced by businesses in different countries. The issue of entry regulation for start-up firms in 85 countries including developed, developing and transition economies was investigated in Djankov, Porta, Lopez-De-Silanes, and Shleifer (2002) and regulation of labour markets through employment, collective relations, and social security laws in Botero, Djankov, Porta, Lopez-De-Silanes, and Shleifer (2004).

Business Environment and Enterprise Performance Survey (BEEPS) – a project

conducted under the auspices of EBRD (European Bank of Reconstruction and

Development) and examining the quality of a set of aspects of the business

environment. Five rounds of survey have been already conducted (1999, 2002,

2005, 2009 and 2012–14).

Doing Business is a yearly report of business regulation elements assessment

implemented yearly since 2003 in 189 economies by the World Bank Group.

Moreover, since 2004 the World Bank has extended its methodology to regional studies. As far as Russia is concerned, regional reports on business climate have been issued twice: in 2008 when they covered 10 cities and towns (primarily regional capitals) (Doing Business in Russia, 2009) and in 2011 when the focus was extended to 30 towns (Doing Business in Russia, 2012). Later in 2013–2014 the Agency for Strategic Initiatives 4 in cooperation with business associations conducted a research project aimed at measuring the investment climate related indices in Russian regions and rated them by different criteria (regulative environment, business-related institutions, resources and infrastructure, small enterprise support) (National Rating of Business Climate in the Regions of Russian Federation, 2015). Moreover, the investigations of the investment climate in Russia are carried out under the auspices of an official specialized advisory body – the Foreign Investment Advisory Council (FIAC) (Doing Business in the Russian Federation, 2014; Investment Climate in Russia – Foreign Investor Perception, 2015; Russia's Investment Climate, 2012).

Agency for Strategic Initiatives – a non-government organization established

by the Russian Government in 2011 to promote new priority economic and

social projects. Website: https://asi.ru/eng/ Accessed

on 27 June 2016.

As far as the Japanese research of business climate in Russia is concerned, the leading agencies are Japan External Trade Organization (JETRO) and ROTOBO (Japan Association for Trade with Russian and NIS). The JETRO Survey reports 2014 and 2015 on the activities of Japanese-Affiliated companies in Russia provide a comprehensive view of Japanese companies on the business conditions in Russia (Japan External Trade Organization (JETRO), Europe, Russia and CIS Division, Overseas Research Department, 2014; 2015; ROTOBO Report Industrial Investment in Eurasia, 2011).

In recent years investment relations between Russia and Japan have experienced significant development. According to the Japan External Trade Organization (JETRO) 5 data during 2005–2014 Japan's FDI stock in Russia increased 29 times (JETRO Reports and Statistics, 2015). 6 Despite volume growth, Japanese FDI in Russia also experienced major shifts in terms of structure and technology. The share of FDI inflow into manufacturing industries of higher technological complexity and capital intensity increased significantly. Regional distribution of Japanese FDI is becoming more diversified; apart from regions which have been traditionally attractive for Japanese capital (Moscow, St. Petersburg and the Far East), investment cooperation with regions of the Central, Volga and Ural Federal districts is developing intensively.

JETRO Reports and Statistics, Japan's Outward and Inward Foreign Direct

Investment, FDI stock (Based on International Investment Position, net),

Outward http://www.jetro.go.jp/en/reports/statistics/ Accessed on 16

October 2015.

From 87 million USD in the beginning of 2005 up to 2,5 billion USD in the

beginning of 2014 (JETRO).

However, despite recent progress in investment relations and complementary economic interests of the two countries the level of cooperation is far below its potential. The share of the two countries in the structure of mutual trade and investment relations is rather modest: Russia accounts for 2,26% of Japan's foreign trade turnover and 0,24% of Japanese FDI outflow (in 2014 according to JETRO), while the Japanese share in Russian foreign trade turnover is almost 4% (in 2014 according to the Russian Federation Federal Customs Service, Foreign Trade Statistics, 2015 7 ), 1,54% in the inflow of all types of foreign investment, 3,93% in the FDI inflow (in 2013 according to the United Interagency Information and Statistics System, 2013 8 ). Japan is ranked 10th in the list of top investors in the Russian economy in terms of investment stock of all types and 16th in terms of FDI stock in 2013. 9

Russian Federation Federal Customs Service, Foreign Trade Statistics

http://stat.customs.ru/apex/f?p=201:7:34916493764136::NO

Accessed on 16 October 2015.

United Interagency Information and Statistics System, Foreign Investment

Inflow https://www.fedstat.ru/indicator/31335.do Accessed on 16

October 2015.

Ibid.

Therefore using the case of Japanese investment in Russia we can observe that there might exist particular challenges and obstacles that make Japanese companies reluctant to engage in business activities in Russia. Revealing those obstacles and finding ways to neutralize them may give additional impetus to the development of investment cooperation between Japan and Russia.

This paper analyzes the factors attracting Japanese capital to the Russian economy and challenges that Japanese business faces during the process of adaptation to the Russian business environment. The purpose of the research is to reveal and systemize factors restricting investment cooperation development and their roots and to find out possible ways of overcoming these challenges using the strengths of investment ties between the two countries.

The research is based on the results of a survey of Japanese companies – members of the Moscow Japanese Business Club (JBC). The survey was conducted by the National Research University – Higher School of Economics (HSE, Moscow), Institute for Industrial and Market Studies in April–June, 2015 in the framework of a research project “Russia's Business Climate through the Eyes of Foreign Firms”. Basically the target of the survey was to see how the members of foreign business associations in Russia evaluate the business climate in Russian regions and how current political and economic events affect their activities. Another objective of the study was to identify the main problems foreign firms are facing in the current political and economic situation in Russia, to gather ideas how these problems can be addressed by Russian regional and federal administrations and to find out what regional administrations in Russia can do to make their regions more attractive for foreign investors. However, is this paper the use of the survey data will be mostly limited to the factors of attractiveness of Russia as an investment destination and the problems and challenges that Japanese companies face. The survey was administered online: member companies of the JBC Moscow received an Internet link (URL) to the online questionnaire form. The form was available in Japanese, Russian and English. Below is a short description of companies that participated in the survey.

More than a half of the companies (55%) started doing business in Russia after 2005, while about a quarter have been in Russia since before 1991. The number of employees of the Russian branches or subsidiaries in most cases does not exceed 50 people (71%). And as a rule the survey participants are under foreign ownership (86%). Most of the companies (62%) are engaged in importing to Russia with following sales on the domestic market. However, some companies produce goods and services in Russia in order to sell them on the domestic market (19%) otherwise on both domestic and foreign markets (12%). The overwhelming majority of Japanese companies that participated in the survey (more than 82%) do not invest in R&D in Russia.

As far as the sectoral distribution of the answers is concerned, 53% of respondents are working in manufacturing, 20% in business and investment consulting, 13% in trade and 7% in both transport and financial services. More than a half of the companies are represented in 1 or 2 regions only (55%), while the distribution between other groups is quite flat: 22% work in 3–10 regions and 22% in more than 10 regions (some in more than 20 regions of Russia). Although companies may be engaged in business activities in a number of regions, for the majority of them Moscow is the most important region for their business (65%). Only 4 more regions were marked in this question: Kaluga region, Kursk region, Moscow region and Saint Petersburg.

So according to the statistics, the prevailing group of companies in the sample is represented by companies registered in Moscow and engaged in importing and selling manufacturing goods or providing consulting services in different regions of Russia. However, there are several limitations to the dataset used in this paper. First of all the major limitation is a small sample due to the low response rate. Although the survey link was sent to about 187 companies (members of the JBC Moscow), the maximum number of responses for some questions was 32, which gives us a response rate of approximately 17%. Moreover the number of blank responses increased towards the end of the questionnaire leaving some gaps in the dataset. Therefore the low response rate presumably makes the sample biased by the nature of companies and the sphere of their activity.

As an addition to the survey we used the results of content analysis of several interviews with representatives of Japanese business, academic community and non-governmental organizations to illustrate the main findings. The interviews were partially conducted by the author and partially available in open Internet sources. In the interview analysis we were trying to reveal challenges, problems and obstacles that have been mentioned by the interviewee and categorize them depending on the frequency of occurrence.

The interviews were given by the representatives of the business community (70%), non-governmental organizations (20%) and academic people (10%) and took place in 2008–2015. As for the distribution of the business representatives by spheres of activity, these were mostly companies producing machinery and electronics, and those involved in manufacturing industries (62% in total). The rest were companies from the banking sphere, IT, construction, pharmaceuticals and trade. 90% of the interviewed representative's firms have offices or branches in Russia. During the interviews and further analysis we concentrated on the questions concerning factors attracting investment and challenges for foreign companies.

The limitations to the interview sample might be the small number (20 interviews) and some possible gaps in content in the open-source interviews which were conducted under a different topic outline. Due to the informal nature of some interviews and according to the will of interviewees not all interviewee names are available in this paper.

The interview results have also provided additional subjects reflecting the challenges for Japanese business in Russia that could not be directly revealed through the survey. These relate to business culture and management practices rather than drawbacks relating to the business climate. Therefore on the basis of the interview content analysis we could also suggest a general classification of challenges for Japanese business in Russia. It is assumed that each problem or challenge can be assigned to a particular group depending on the origin of the problem.

The first group includes factors emerging from the socio-economic, institutional and cultural environment and the characteristics of the investment climate of the country in general. These factors, which could be called external, are faced by all investors doing business in Russia, not only foreign but also local, however, foreign firms are additionally affected by the factor of an unfamiliar business environment as well as cultural differences.

Another group of factors concerns the organization of internal processes within a firm and originates from the cultural specifics and models common for the home country business environment. These factors, which mostly include the issues of personnel management and production organization, can be specific for foreign firms representing different countries. The special features and characteristics of the Japanese model of business organization make this group of factors extremely important and illustrative.

We could also distinguish the third group of challenges relating to the compatibility of business cultures of the home and host economy and informational issues such as the availability of experience of doing business in the host country and the image of the country as an investment destination. It was revealed that both of them are quite important for the perspective of the development of Japanese business in Russia.

Given the variety of problems that foreign firms can face in a different business environment, the ways of addressing the challenges differ a lot depending on their origin. Consideration of different aspects and layers of challenges may allow us to suggest comprehensive and systematic recommendations that could be useful for the further development of investment cooperation between Japan and Russia.

Results

Attracting factors

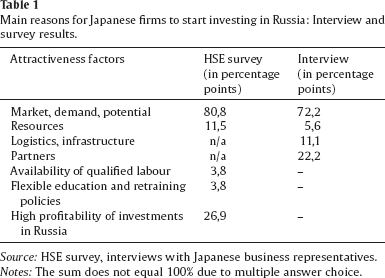

Before providing the detailed analysis of challenges that Japanese firms have to face in Russia it is necessary to describe the main reasons for companies to enter the market and engage in production activities. In order to reveal the main factors attracting Japanese investors to Russia we asked about the main reasons for starting to do business in Russia. The distribution of answers to this question is presented in Table 1. According to the answers of companies participating in the survey the most popular reason was gaining access to the Russian market (81%). The interview results correspond to the survey findings. The interviewees noted the developing and promising Russian market as the most important (sometimes the only) factor attracting Japanese investors. The respondents also pointed out the high development potential of the market and the growth of personal consumption underlying demand expansion. Almost 70% of interviewees mentioned that the “Russian market is the biggest and most promising market in CIS region and is growing continuously” (Analytical Agency AUTOSTAT, 2012), 10 moreover, “within the market the demand for high-quality goods goes up due the increase of solvency and that attracts Japanese firms as the segment of high-quality and expensive good is the target for Japanese producers”. 11 On the other hand, many representatives of the Japanese business community agree that while the Russian market is expanding fast, it is very dynamic and characterized by a rapid change in consumer preferences that are difficult to predict and forecast, especially in the long term. The problem is that the Japanese management style focuses on long term strategic planning, therefore the low predictability of the Russian market is regarded as a significant disadvantage.

From the interview with Junichi Okishima, Director of Yokohama company,

2012. Analytical Agency AUTOSTAT http://www.autostat.ru/news/view/9434/ (in Russian,

Accessed on 27 June 2016).

From the interview with representatives of the Japan Association for

Trade with Russia and NIS (ROTOBO), 2012.

Main reasons for Japanese firms to start investing in Russia: Interview and survey results.

Another quite popular reason highlighted by a quarter of companies was the high profitability of investment in the Russian economy. The availability of infrastructure in particular regions and the presence and support of business partners were mentioned as quite important factors by some interviewees. It was surprising that only a few respondents mentioned the availability of natural resources as a factor attracting investment. Previously most Japanese investment projects in Russia were associated with the development of natural resources. Nowadays the share of manufacturing projects is growing, and the quality of human resources is becoming increasingly important. Japanese investors note the high educational level of Russian employees, but labour costs in practice often turn out to be much higher than expected. In many cases it is caused by hiring process and staff turnover problems. The Japanese management system is based on the principles of high loyalty, motivation and commitment to the corporate culture (Ouchi, 1981). Trying to adapt this model in Russia, Japanese companies face high personnel turnover because of the differences in the business cultures and management practices. This factor will be additionally analyzed in Section 3.3.

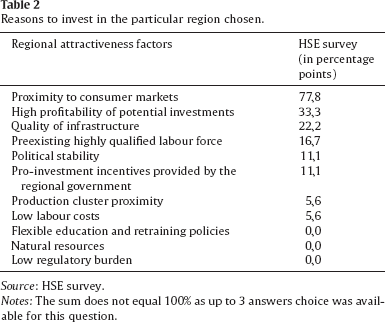

Slightly more detailed results were obtained for the question on investment incentive factors in particular regions that were most important for the company's investment activity in Russia. Although the proximity to consumer markets and high profitability of potential investment are still the main factors (78% and 33% respectively), the quality of the infrastructure and the availability of a qualified labour force also play an important role in the investment decision (see Table 2). However, these results can be applied only to a narrow range of regions prevailing in the survey, namely Moscow, Kaluga region, Kursk region, Moscow region and Saint Petersburg.

Reasons to invest in the particular region chosen.

Recent tensions in Russian international relations and the economic crisis have inevitably affected the activity of Japanese companies in Russia. About a half of the respondents (48%) believe that the investment climate has become somewhat (28%) or significantly (20%) worse during the last 3 years, while only about a third think that it has become slightly (32%) or significantly (4%) better.

However, they stay quite optimistic about the prospects: according to Fumitaka Kawashima, the vice-president of Toyota Motor RUS “although the Russian market is shrinking due to the crisis, the company's market share is increasing steadily… we understand that current market instability is temporary and … we are expecting recovery and growth of the market” (Analytical Agency AUTOSTAT, 2014). 12 According to the HSE survey two thirds of the respondents admit that despite the crisis and market shrinkage Russia remains an attractive investment destination. 24% of respondents state that doing business in Russia became somewhat less (14%) or much less (10%) attractive than a year ago.

From the interview with Fumitaka Kawashima, Vice President of Toyota

Motor RUS, 2014. Analytical Agency AUTOSTAT http://www.autostat.ru/news/view/17784/ (in Russian,

accessed on 27 June 2016).

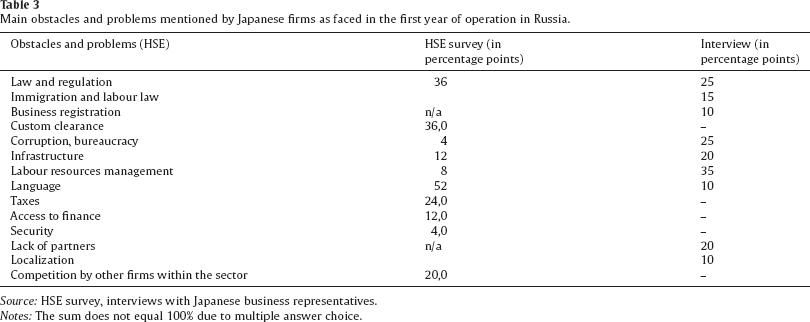

As far as the risks and challenges are concerned there is a various range of factors mentioned in the interviews and the survey. In the question about the main difficulties and obstacles faced by Japanese companies during the first year of operation in Russia, the respondents mentioned various spheres and factors. The results are shown in Table 3. It was surprising that half of the companies had difficulties associated with the language barrier. However, it corresponds to the structure of respondents who were actually answering the survey questions: a half of respondents did not speak Russian at all and 27% spoke only some. It is worth noting that 86% of respondents were representing top- or middle-level management.

Main obstacles and problems mentioned by Japanese firms as faced in the

first year of operation in Russia.

Source: HSE survey, interviews with Japanese

business representatives.

Notes: The sum does not equal 100% due to multiple

answer choice.

Main obstacles and problems mentioned by Japanese firms as faced in the first year of operation in Russia.

According to the interview and survey results there are a number of important factors mentioned in both sources. These are corruption, bureaucracy, different types of regulatory procedures (especially labour and immigration law, and the complexity of company establishment procedures), law and regulation in general, the lack of infrastructure and the problems of labour resources, especially labour cost and availability, and hiring problems. At this point interviews served as a substantial source of detailed information about challenges and problems mentioned in the survey.

More than a third of the companies marked regulation and customs clearance as significant difficulties for their business. Concerning regulation, many companies specified labour regulation, company establishment procedures and GOST as the most important regulatory obstacles. Interview respondents often mentioned the difficulty and the complexity of the registration process and the establishment of the company. Construction seems to be the most problematic case in this issue. Greenfield investments (especially in the manufacturing sector) involve major facilities and construction investment, while Russian procedures for obtaining building permits serve as a serious barrier to the project: the process takes an average of 540 days and requires about 53 documents. As a result, the cost of obtaining a permit turns out to be several times higher than in other BRICS countries, for instance. 13

Industrial investment in Eurasia (report), ROTOBO (The Japan Association

for Trade with Russia & NIS) 2011, p. 79.

Results of questions about corruption, labour retention and perception of the investment climate dynamic should be mentioned among other interesting survey results related to the issue of obstacles for the Japanese business. 20% of companies supposed that the situation with corruption became better during the last 3 years, while 4% think that it has become worse. On the other hand, about a third of survey participants answered that nothing has changed and the corruption problems remained at the same level, while a quarter of interview respondents confirmed that doing business in Russia is usually associated with corruption. In one of the questions survey participants were asked to assess the amount of informal payments to different regulatory agencies and officials. Only one firm assessed them as 6–10% of total annual sales, or estimated total annual value, while other respondents answered that they have never heard or do not know about such payments.

Obviously, red tape, corruption and lack of transparency of bureaucratic procedures and competitive tendering practices damage the country's investment image. Japanese investors are also concerned about inconsistencies and shortcomings in the Russian legislation, which causes increased costs for legal services burdening the budget of investment projects. The issues of property rights (especially intellectual property rights) protection and contractual obligations enforcement mechanisms are also mentioned as quite important issues by Japanese specialists (Japan Overseas Enterprises Association, 2011).

Concerning the problem of recruitment and retention of skilled personnel (especially in regions), the majority (63%) of the companies do not have them. However, 25% face these problems sometimes and for 13% it is a considerable problem. Respondents specified that there might be difficulties with recruiting specialized engineering staff with good English and also in the Far Eastern region of Russia. However, interview respondents claimed that labour turnover is quite a problem. Yuichi Tsujimoto, the Hitachi Construction Machinery President says: “Personnel training is an important area, we recruited Russian employees, sent them to study in Japan, organized programs in professional colleges led by Japanese specialists” (Vedomosti, 2014). 14 And this practice of personnel training is quite typical for Japanese companies. Therefore labour turnover causes big losses of investment in human capital and staff development.

From the interview with Yuichi Tsujimoto, President of Hitachi

Construction Machinery, 2014. Vedomosti http://www.vedomosti.ru/newspaper/articles/2014/08/19/pozicii-ssha-i-yaponii-nevovsem-absolyutno-sovpadayut-yuiti

(in Russian, accessed on 27 June 2016).

Actually all the top-list obstacles mentioned by the interviewees are associated with additional expenses and lead to a decrease in profitability. For example, changes in laws and regulation cause increased spending on lawyers and specialists and so on. Many problems are caused by the lack of infrastructure. At the stage of plant construction Japanese companies face a lot of delays of business plan implementation due to additional time and capital expenses on solving problems of access to the infrastructure (Ide, 2012). Registration process usually takes longer time than expected, however, recently the procedures-related obstacles seem to decline.

Another major problem that Japanese companies have to deal with is balancing between production localization and import. A lack of reliable partners forces companies to import parts and materials while the governmental Memorandum, as well as economic sense, requires an increase in production localization. Localization of production at Japanese factories in Russia in general does not exceed 15–20%. 15 “We have to admit that Japanese manufacturers do not trust the quality of the components and materials produced by Russian suppliers; therefore they are quite reluctant to localize production although they have to follow the terms and conditions of the governmental agreements on industrial assembly. They prefer to purchase materials and components from their subsidiaries or suppliers with whom they work in the Japanese market; move their own component production facilities closer to the assembly plant or to work with the subsidiaries of European or American companies. Japanese companies also try to persuade their suppliers from Japan to enter the Russian market, however, the partner companies and suppliers of the Japanese manufacturers are reluctant to do so because given the existing output of Japanese enterprises in Russia (in particular automotive) the transfer of production facilities is considered unprofitable for them.” 16 Furthermore, the potential Japanese suppliers also face the problem of high-quality material supply on their level of the production chain.

From interviews with Japanese company representatives from factories in

Yaroslavl’ and St. Petersburg.

From the interview with representatives of the Japan Association for

Trade with Russia and NIS (ROTOBO), 2012.

Thirty of the top-100 biggest world automotive component suppliers are Japanese companies, however, only 4 of them have production facilities in Russia. These are Asahi Glass in Nizhny Novgorod; Toyota Boshoku (Toyota's subsidiary) in St. Petersburg; Takata in Ulyanovsk region and one of the leading global suppliers of automotive components – Denso – which has signed an Industrial Assembly Memorandum with the Russian Ministry of Economic Development in 2012 (Forum “Avtoevolutsiya”, 2012). 17

Forum “Avtoevolutsiya”. Vedomosti business newspaper annex

08.02.2012.

Lack of modern infrastructure, effective logistics and connectivity also add problems to the foreign investment projects in Russia. Weak infrastructure in some regions does not allow effective matching of the raw materials market and consumer markets and this increases transportation and logistics costs. For Japanese companies operating both in the Far East and in the European part of Russia the development of logistics and transport infrastructure is among the priorities.

All these major risks emerge from the weaknesses and drawbacks of the Russian investment climate, therefore each of them should be addressed directly to facilitate the procedural and regulatory part of it and make the climate more foreign-business friendly. In general there is no consensus between Japanese investors in the perception of change in the Russian investment climate during the last 3 years among the HSE survey respondents: 36% of firms think it has become slightly or significantly better while 48% believe it is deteriorating.

As for the activities of the regional governments that attract investment, half of the respondents think that some or most regional administrations are actively trying to attract foreign investors. The other half supposes that only few or no regional governments are involved in such activities. These results correspond with the answers to the question about whether the regional administration is rather helpful or a hindrance for foreign investors. The answers were divided into two halves again (20% each), while 30% said government of the regions does not help, but does not hinder. That points to the fact that regional administrations in Russia have very different policies towards supporting foreign investors, each case is unique. That may reflect the level of ‘saturation’ of the region by foreign investment or simply the competence of the regional administration.

In addition to the challenges described for the last 3 years, foreign investors as well as locals suffered the influence of international sanctions and the economic crisis. Actually this aspect has come to the fore for foreign investors and to some extent obscured common challenges of the investment climate. In this respect the survey showed that international tensions, sanctions and the economic crisis have made business in Russia significantly more difficult for 38% of the respondent Japanese companies, somewhat more difficult for 43%.

The main risks and problems concern the exchange rate fluctuations and ruble devaluation. About 76% of respondents noted the decline of competitiveness due to ruble devaluation. More than a half of companies (57%) complained that their products or services have become significantly less competitive on the Russian market. With regard to global operations, Japanese companies have also marked several types of risks emerging from the current economic and political instability: besides exchange rate fluctuations (71%) respondents were also concerned about problems with the import of raw materials, components and equipment (24%); restriction on participation in global deals by foreign regulatory authorities, problems with processing of payments on international transactions, introduction of additional trade barriers (14% each); restriction in access to foreign credit (9,5%) and problems with the import of raw materials, components and equipment (5%).

Whatever the local investment climate characteristics are an investor has to adapt not only to its institutional and economic factors, but also to the peculiarities of the local business environment and business and management practices. Of course, these issues are relevant not only for Japanese firms, but for all companies involved in foreign operations. However, in the case of Japanese business, companies are often trying to implement a production and management model, which was developed in the specific framework of Japanese economic, social, psychological and cultural conditions and functions effectively in terms of a full range of appropriate conditions, in a foreign environment. But in a different business and cultural environment, Japanese management and production practices may not only be ineffective, but even inapplicable.

In the analysis of adaptation of Japanese production and management systems to Russian conditions we partially used the framework of the approach described in the research on the performance of hybrid factories carried out by Abo et al. (2007) (Japanese Multinational Enterprise Study Group). 18 Companies primarily representing the manufacturing sector were looked at when talking about the application of Japanese production and management practices since the tertiary sector represents a limited range of distinctive features of Japanese production and management system. Eventually we can find out which practices in business organization and management can be useful and effective for Japanese companies operating in Russia and which cannot be adopted. The analysis was based on the Japanese automotive production plants in Russia (see details in Ershova, Lavrov, & Plotnikov, 2013).

The approach deals with the analysis of transferability (applicability

and adaptability) of Japanese-style management and production systems

across different regions abroad and assesses 23 aspects of these

systems. According to the author's methodology 23 elements

characterizing the Japanese system of management and production are

assessed using a 5-point scale by representatives of the Japanese TNCs’

affiliates abroad for their compliance with the typical Japanese

practices applied on national enterprises. The study allows us to

compare those elements and see to what extent Japanese common practices

can be applied to the overseas branches, in particular countries or

groups of countries. Research is conducted primarily among manufacturing

companies (transportation machinery, electronic and electrical

engineering), especially because the production process includes the

maximum number of common practices and elements to be considered.

The issue of product diversification and production line flexibility seems to be quite an important part of the production organization process in Japanese plants in Russia, given the rapid changes in the preferences of the market. For example, the Nissan factory in Kamenka (St. Petersburg) has only one production line but unlike the Japanese plants, process automation is extremely low – about 10%. All welding and painting is performed manually, even the transportation of parts is not automated and is done manually using special trolleys (Nissan, 2010). 19 Such a low level of automation does not allow the company to increase the efficiency of individual employees. This in turn limits the speed of the production line and hence the output.

Nissan's factory in Kamenka from inside http://www.autopeople.ru/article/nissan/producer/25297.html

(in Russian, accessed on 27 June 2016).

Japanese equipment and mostly imported parts produced in Japan help ensure the quality of products, for example, there are almost no cases of defects at the Toyota plant in Russia. The system of stopping the production line for quality control is applicable at every stage of production because the level of automation on the plant is very low. The admissible share of defects at the Nissan factory is 2%. Most defects are eliminated in 5 minutes on the production line (Nissan, 2010). 20

Ibid.

Regarding “just in time” production system applicability, it is almost impossible to implement it in Russian factories given the low level of localization of component production and the fact that the delivery period for imported parts from Japan is up to 2 months. Therefore the arrangement of logistic systems or local supply channels seems problematic and time-consuming while the organization of cluster productions in collaboration with Japanese sub-contractors in Russia will be possible only with the rapid growth of output on the partner's assembly plants and guaranteed sales stability. But unfortunately the problems of implementing the Japanese production model in many cases do not allow output to be raised to either potential or even planned levels.

As far as personnel management is concerned, some companies localize management because they admit that the Japanese management system is too specific to be used in most business cultures unchanged. In particular, Sony uses management localization widely. Its aim is to develop local human resources and to provide an opportunity for professional growth and development. 21 The training programme is an important part of the personnel management strategy for all Japanese companies. Many firms organize training and practical experience in factories in Japan and Europe. However, unlike in Japanese companies, opportunities for interdepartmental staff rotation are limited due to the narrow specialization of employees.

From the interview with S. Arai, Director General of Sony CIS, 2005.

Although as in most countries, the Japanese principle of lifetime employment cannot be applied unchanged, the focus on long-term cooperation and clear criteria for promotion corresponds to the preferences of Russian employees. The main hiring criteria are qualification and motivation, and the competition is rather high. However, the turnover, especially at the beginning (and for those reluctant to adapt to the Japanese management system), is also high.

In general according to the “hybrid” factories approach developed by the Japanese Multinational Enterprise Study Group, the overall level of application of elements of the Japanese management and production system is rather low. Systemic, interrelated elements of the model were the least applicable in a foreign business environment because they are originally based on the specifics of the organization of the company's external relations as well as on the economic and social environment in Japan. These elements include primarily the “just-in-time” supply and production system, participation in the “quality circles”, and the system of recruitment, remuneration and promotion.

Among the most applicable elements of the Japanese management and production system are those related to the maintenance of harmonious teamwork, as well as coordination of work processes. Also quite applicable are indicators related to the technical support of production, equipment and characteristics of the production line that is the most “autonomous” and not fundamental elements of the Japanese production model.

In general, the model of adaptation of Japanese companies in Russia is close to that of Japanese companies in CEE countries. These have a higher degree of localization of management and low applicability of Japanese methods with a fairly strong control of the parent company. On the other hand, such a strategy is typical for the initial stage of Japanese business development, because over time we can expect an intensification of implementation of elements of the Japanese system and growth of branch autonomy.

The interview analysis allowed us to distinguish some factors that cannot be classified either as emerging from the investment environment drawbacks (external) or from Japanese production system applicability (internal). These concern the informational issues and compatibility of business cultures.

One of the major factors hindering the development of investment cooperation between Russia and Japan is the perception of the Russian investment climate in Japan and the underlying lack of information about the Russian market and the business climate. The insufficient experience of doing business in Russia and the lack of research on business opportunities has a negative impact on the decisions of potential Japanese investors trying to avoid the risks associated with uncertainty. Therefore it is necessary to promote a favourable image of the Russian business environment and investment climate to provide potential investors with information about the conditions for doing business.

The impact of the next important factor – the compatibility of business cultures of Japan and Russia – is activated on the stage of business collaboration development. Actually internal restricting factors emerge largely from the problem of compatibility of the host and home business cultures. Despite all the differences, we managed to find certain characteristics that can serve as a basis to provide mutual understanding in business relations.

On the one hand, the value system of Russian and Japanese employees, and as a result the approach to the working process, differs radically, not least in terms of the motivation system. Due to unclear corporate culture and values, Russian workers lack moral incentives which is an extremely important tool for human resource management in the Japanese model. In addition, there are fundamental differences in approaches to the development of projects and assignments: the Japanese pay great attention to the details of a project that may seem minor to the Russian side. While the conceptual approach of the Russians and the lack of planning accuracy can cause tension and delays in negotiations with the Japanese.

On the other hand, both cultures share the principles of collectivism and high context (Hall, 1959). Business relationships in Russia and Japan are largely based on interpersonal relations and informal methods for resolving problematic issues. These common features can serve as a basis and a “start point” for the development of mutually acceptable ways of organizing productive business cooperation.

Conclusions

The Russian economy is quite attractive for Japanese investors as it provides a range of opportunities and advantages that Japanese companies usually seek in their foreign expansion strategies. But on the other hand, almost each advantage entails some kind of a challenge caused either by factors of the business environment and institutional framework or by conflicts with the Japanese approach towards organization and management.

As a result of analysis, the constraining factors can generally be divided into 3 groups according to their origin – external, internal and other (non-economic) factors. External factors include the weaknesses and drawbacks of the Russian business environment and investment climate. In other words, these are the factors faced by all investors doing business in Russia. The perception of the Russian investment climate by Japanese investors also turned out to be quite important. The internal group of factors is more specific and concerns the process of adaptation of Japanese companies to the Russian business environment. In the case of Japanese investment they might be common for overseas branches of Japanese companies, in other words based on the distinctive features of Japanese business culture. Other or non-economic factors are associated with the compatibility of business cultures and information issues.

In order to overcome the challenges for investment projects on the basis of our analysis we could develop the following recommendations for both sides.

For the Russian side: Promote development of infrastructure:

modernization of railways and ports (especially in the Far East region)

to raise their capacity; construction of roads with possible attraction

of foreign investors; Implement the programmes of gas, electricity and

water supply systems construction with possible attraction of foreign

investors; Develop social and educational facilities in the

regions that attract FDI in order to provide labour supply, retraining

programme support; Loosen immigration policy and regulation,

simplify the work permit related procedures; Provide informational support for foreigners

working in Russia, promote language schools and courses; Simplify and optimize business registration and

customs clearance procedures, reduce paperwork; Support active interaction with foreign business

via such mechanisms as International Council for Cooperation and

Investment (an advisory body of the Russian Union of Industrialists and

Entrepreneurs (RSPP)) in order to react on business needs and receive

feedback.

For the Japanese side: Apply more aggressive and active strategy for

entering Russian market. Timely response and quick adaptation to the

changing market conditions is essential; Use the opportunities of innovative and

technology-intensive industries. Many interviewers stressed the low

level of innovation and technology saturation of the market and the wide

perspective for IT development; Implement Japanese know-how and expertise in

production organization: unlike labour management, the production

management has shown rather high applicability at the plants in

Russia; Localize the labour management in the factories

in Russia as much as possible (as in the case of Sony); Take into account the difference in Japanese and

Russian business cultures. On the one hand, a friendly, positive work

climate seems to receive positive response, but on the other hand, the

difference in motivation and value system should be addressed as, if

neglected, this aspect leads to increased labour

turnover; Address actively the position of business

community to the Russian governmental bodies via a collective voice that

can be provided by the Japanese Business Club in Moscow.

Thus, the solution to the problem of improving Russian–Japanese investment relations and promotion of cooperation lies in several areas. In terms of economic factors, the improvement of the investment climate is a priority. We need not only to provide comfortable conditions for doing business in Russia but also to clearly inform potential investors of new opportunities. Problems in the adaptation of the Japanese production and management system to Russian conditions seem resolvable and the aspects of the compatibility of business cultures seem to be rather helpful at this point. A much more difficult task is to overcome the information barriers and improve the perception of the Russian business environment among potential Japanese investors.

Acknowledgements

The article was prepared within the framework of the Basic Research Program at the National Research University Higher School of Economics (HSE). The author acknowledges the support and assistance of the Japan Foundation and Kyoto Institute of Economic Research (Kyoto University, Japan) during the Japan Foundation Japanese Studies and Intellectual Exchange Fellowship Program (2011–2012). The author also expresses special gratitude to the Japanese Business Club (Moscow) for support and assistance in the survey organization, and to all companies which took part in the survey and interviews.