Abstract

Russia has declared a priority interest in developing a strong economic relationship with the Asia Pacific Region. There has been considerable internal debate over the best strategic approach to such a relationship. While a policy victory has been won by a strategy focusing on the export into the region of manufactured goods and services, a resource-export strategy is still dominant in practice and funding. Here the prospects of each strategy are assessed. Regarding resource exports, hydrocarbons, copper and iron ore prospects are reviewed, but most detail is provided on the coal sector. That involves an account of infrastructure issues, including a major debate over the expansion of the BAM and TransSiberian railways. The analysis suggests that Russia will struggle both to revitalise the Russian Far East through manufacturing exports to the APR and to replace revenues earned through resource exports to the West through an economic ‘turn to the East’.

Introduction

In recent years Russia has – not for the first time – declared a top-priority interest in developing its economic relationship with the Asia Pacific Region (APR). That can be explained by various events: Putin's questioning of Russia's partnership with the West in Munich in 2007, the severe effect on Russia's economy of the Western-originated global financial crisis in 2008, signs around the same time of political and social discontent in the Russian Far East (RFE) in the context of poor socio-economic indicators for the region, the impending depletion of natural resources oriented to Western markets and the opening of new areas of exploitation further east, and the general atmosphere that Asia is the rising powerhouse of the global economy (Lo, 2014). All these drivers have been given added force by recent events in Ukraine.

The new priority has produced a fierce policy debate (Fortescue, 2015), behind which is a tension between two reasons for economic engagement with the APR. First, there is a desire to increase national export earnings through expanding exports to Asian markets. Second, there is a desire to improve the prosperity of the RFE by providing new employment opportunities and improving local infrastructure, to reverse population decline. At the risk of some simplification, the first reason is likely to produce a policy oriented towards the export of natural resources, including many not sourced within the RFE; the second a manufacturing-oriented approach, based in the RFE and providing more employment than is likely from resource exploitation. The two goals are not mutually exclusive, but there has been clear tension between them.

This can be seen in a sudden change in strategy in 2013. Until then the policy process had produced an RFE development programme heavily oriented towards resource exports and the infrastructure needed to serve them (Gosudarstvennaia programma Rossiiskoi Federatsii ‘Sotsial'no-ekonomicheskoe razvitie Dal'nego Vostoka i Baikal'skogo regiona’, No.466-r, 29 March 2013, archive.government.ru/gov/results/23721/). It met with strong opposition, and in August 2013 the founding Minister of Far Eastern Development (MFED), Viktor Ishaev, was dismissed from his ministerial position and his post as presidential representative in the Far Eastern region. He was replaced in the latter position by Yurii Trutnev, who was also appointed a deputy prime minister, and as minister by Aleksandr Galushka. Within a month Galushka presented a new strategy based on the export into the APR of manufactured goods and services (including agricultural products), produced in a new form of special economic zone known as a ‘territory of accelerated development’ (to be called here, after its Russian name, TOR) (government.ru/news/7718/). That was not the end of the resource-export strategy. The struggle for state funding of resource projects, particularly for infrastructure, continued.

Here the commercial prospects of the two strategies are examined, with two success indicators being used. The first is commercial viability – will the projects earn a return on investment; the second – will each strategy meet the goals set by policy makers, in the case of the TOR strategy bringing increased prosperity to the RFE and in the case of the resource strategy maintaining national prosperity as supply and demand decline in the West. Given the complexity of the issues involved, data availability, and space constraints, the conclusions will be indicative rather than precise.

TOR strategy

The TOR strategy, as originally formulated, is to increase the prosperity of the RFE through the creation of new jobs and economic activity in special zones in which firms from the APR invest to produce non-resource goods for export to APR markets. This is in the context of manufacturing and equipment making up 3 per cent of total exports from the RFE and Baikal region in 2010, worth $574.7 million (77 per cent were resource exports) (Popova, 2012, p. 8). 1

Financial figures are usually presented in the currency used in the original source. Particularly since the end of 2014 the exchange rate has been highly volatile. As a rough guide for the period covered by this article, $US1 bought R32.00 on 1 January 2012, R30.54 2013, R32.86 2014 and R59.02 2015.

Investors would be attracted to the zones through attractive investment and operating conditions: tax concessions, ease of gaining approvals, good electricity connections, convenient and competitively priced logistics and transport, and so on (vedomosti.ru/politics/characters/2015/05/19/mi-ishodim-iz-prezumptsii-nevinovnosti). There was much stress on a ‘one stop shop’ approach run by MFED agencies, requiring the transfer to the new ministry of major administrative functions previously carried out by other agencies.

Early accounts were vague on what types of activity and markets were being considered. In February 2014, when asked by a clearly sceptical reporter the intended export destinations of RFE-manufactured goods and services, Trutnev replied ‘We are thinking about it’ (kommersant.ru/doc/2410187). He might have been playing his cards close to his chest, but the response was not reassuring. Much was made of Memorandums of Understanding signed with investors from Japan, China and New Zealand (government.ru/news/14040) and the interest of Mitsubishi, Mitsui, Daewoo, LG and Samsung (kommersant.ru/doc/2498003).

We now have details on three TOR projects that have been established by government decree and another five approved by the relevant government commission. Another seven have gone through the initial approval process but are not yet publicly identified. Those approved look very different from what was initially suggested. The three established by decree are:

‘Khabarovsk’ (government.ru/dep_news/18636/). Residents include a manufacturer of roofing and insulation materials, a local food distributor and supermarket operator, and a Singaporean bitumen producer (government.ru/news/16902/; kommersant.ru/doc/2723624; vedomosti.ru/politics/characters/2015/05/19/mi-ishodim-iz-prezumptsii-nevinovnosti). The federal budget is to provide R1.26 billion for infrastructure. ‘Nadezhdinskii’ (Nadezhdinskii district, Vladivostok) (government.ru/dep_news/18635/). Residents include a bakery, a timber products firm, also identified as running logistics centres, and the food distributor and supermarket operator also involved in ‘Khabarovsk’ (deita.ru/news/economy/03.04.2015/4870980-tor-nadezhdinskiy-807-gektar-chistogo-polya-i-nikakikh-obyazatelstv/). The federal budget is to provide R1.99 billion. ‘Komsomol'sk’ (Komsomol'sk-na-Amur) (government.ru/dep_news/18637/). Based in the aircraft plant in the city, the focus is metal fabrication, composite materials, and precision instruments for aircraft construction, and in one source timber products (kommersant.ru/doc/2723624); government.ru/news/17541/). Residents include an energy conglomerate with industry parks around Russia, a Moscow-based private investment company, and possibly the aircraft manufacturer Sukhoi. The federal budget is to provide R902 million.

Those approved at commission level are:

‘Beringovskii’ (Chukotka Autonomous Region). The core resident is the small Australian mining company, Tigers Realm Coal. The project is to export coking coal from the Bering coal basin. Planned output is 10 million tonnes per year (Mtpy), 5–6 Mtpy after enrichment. The deposits are situated close to an existing mine and 39 km from an operating deepwater port at Beringovskii. The port's current capacity is 0.25 Mtpy, and there are plans to expand it to 1 Mtpy. It is not clear how the remaining output is to be shipped (kommersant.ru/doc/2718943; gazeta.ru/business/news/2014/06/10/n_6220925.shtml). The project receives no funding through the TOR programme, but has received $16.3 million from the Russian Direct Investment Fund, for an 11 per cent equity share (theaustralian.com.au/business/mining-energy/tigers-realm-coal-grabs-russian-project-by-the-tail-with-625m-raising/story-e6frg9df-1226861674038). ‘Belogorsk’ (Amur region). Soya processing and animal feed (vostokmedia.com/n235691.html; amur.info/news/2015/05/13/93933). ‘Mikhailovskaia’ (Primore region). Pig farming (primorsky.ru/news/common/86699/). ‘Kamchatka’. Tourism and hothouse agriculture. ‘Kangalassy’ (Yakutiia). Thirteen residents, including two from abroad, are claimed. Those identified are transferring from the existing Tekhnopark Yakutiia and are engaged in small scale manufacturing, primarily for the building sector (ria.ru/economy/20150520/1065463981.html; tpykt.ru/residents/).

Other potential TORs that have been much discussed and could well turn up as approved projects are a recreational zone on the Russian half of Ussuriisk Island in the Ussuri River; a science park on Russkii Island in Vladivostok; and the ‘Predmostovaia’ zone in Blagoveshchensk, on the Russian side of a planned bridge across the Amur River, containing an oil refinery, cement factory, and warehousing and logistics (portamur.ru/news/detail/aleksandr-kozlov-tor-belogorsk-odobrena-k-sozdaniyu/). 2

Other projects that were on an early list of possibilities can be found at www.asi.ru/news/20192.

The announced TORs cover a wide range of activities. The broad geographical spread is presumably not driven by purely commercial considerations. As a resource project the Chukotka coal project is an odd man out. There are low and middle-tech activities, although with no sign of cheap-labour assembly operations. There are few big Russian companies involved and few foreign companies. There have been mixed messages coming from Galushka and Trutnev regarding foreign investment. Galushka is upbeat about it, claiming that Asian investors are interested but adopting a wait and see attitude. Trutnev has suggested that, given the level of domestic interest, foreign investors are not a priority (kremlin.ru/news/48085/; government.ru/news/18143/). Perhaps because of the lack of foreign investment, it is hard to see a strong export orientation in the activities so far identified.

In this context the views of Japanese and Chinese business people reported by Kommersant newspaper are telling (kommersant.ru/doc/2674988). They pointed to poor infrastructure, a small domestic market and high wages to explain their scepticism. Galushka, perhaps coming to terms with reality, says one has to start small (‘as China did with its special economic zones’) (vedomosti.ru/politics/characters/2015/05/19/mi-ishodim-iz-prezumptsii-nevinovnosti). Certainly the state's financial commitment is as yet modest. The fifteen projects so far approved will receive R33 billion in state funding, with core investors having committed R383 billion (government.ru/news/18143/). 3 The claimed 23,600 new jobs over ten years are scattered geographically and will hardly transform the RFE (although they will cover the outmigration from the region in recent times of over 20,000 per annum) (news.kremlin.ru/news/47487). While starting small, Galushka's ambitions are still considerable, seeing China, South Korea, Singapore and other Asian Tigers as both role models and competition (vedomosti.ru/politics/characters/2015/05/19/mi-ishodim-iz-prezumptsii-nevinovnosti). Even if one overcomes one's scepticism regarding each individual TOR, it is hard to see the approach leading to economic activity on the scale of a Russian Asian Tiger. It is not surprising that the resource strategy is still much in evidence.

For a breakdown of funding by TOR, see kommersant.ru/doc/2747286.

Russia's hopes in the resource sector rest primarily on oil and gas, but there are also expectations for a range of minerals, as well as fishing and forestry. Oil and gas have received attention from others, and no more than a summary will be provided here. More detail will be provided on mineral exports, specifically coal, iron ore and copper. Gold is an important mining activity in the region but is not considered here, on the grounds that relatively little is exported (lbma.org.uk/assets/blog/alchemist_articles/Alch54Pikanovskiy.pdf). Fishing and forestry will not receive any attention. In examining Russia's prospects, Australia – a major exporter into the region across most product types considered here – will be used as a comparator.

Oil and gas

Beginning with oil, since late Soviet times the main centre of Russian production has been West Siberia, shipping output westwards through a pipeline network. The peaking of those fields and the turn to new sources of oil, including in East Siberia, have roughly coincided with strategic interest in shifting market orientation from west to east. ASTO, a pipeline from East Siberia to the Pacific coast, with a spur line to China, came on line in 2010–11, and has gradually filled with 50 Mtpy of East Siberian oil. Oil is also produced offshore at Sakhalin.

Russia's other great oil hope is the Arctic shelf. Those fields are located more conveniently for delivery westwards, although the opening of the Northern Sea Route on a consistent basis could change that.

While the potential for Russian oil exports into the APR cannot be ignored, there are sceptics. Shadrina and Bradshaw (2013, p. 493) ask whether enough oil will be recovered to replace declining output in West Siberia. They suggest that the state has failed to create the conditions needed to attract the required investment.

Current Russian gas exports to the APR are small-scale LNG deliveries from Sakhalin-2 (owned 50 per cent by Gazprom, 27.5 per cent Shell, 12.5 per cent Mitsui, and 10 per cent Mitsubishi). Seven million tonnes per year of LNG are exported to Japan, roughly 70 per cent of the plant's exports (vedomosti.ru/newspaper/article/491741/gazpromu-malo-trub). That represents 10 per cent of Japan's imports. In 2012 Russia provided 2.5 per cent of China's LNG imports, and 6.0 per cent of South Korea's (Shadrina & Bradshaw, 2013, p. 483). Gazprom has plans for another 10 Mtpy LNG plant on Sakhalin, as well as a plant of the same capacity near Vladivostok (Shadrina & Bradshaw, 2013, p. 487). Rosneft in partnership with Exxon has had plans to build a 5 Mtpy plant on Sakhalin. Decision-makers face a dilemma. Putin is reluctant to offend either Gazprom or Rosneft, but there are concerns that there will not be enough gas to serve all RFE LNG plants and over allowing competition between Russian LNG exporters (news.kremlin.ru/transcripts/18824). Serious financing difficulties in current circumstances might render the dilemma moot.

The Yamal LNG project, on the Arctic coast, is privately owned, currently by Novatek (60 per cent) and Total and China's CNPC (20 per cent each). Novatek is owned by Gennadii Timchenko and Leonid Mikhelson, both considered to have good relations with Putin. Design capacity is 16.5 Mtpy, with start up in 2017. Eighty per cent of output is already contracted to Asian buyers (vedomosti.ru/business/articles/2015/05/15/novatek-hoc…ot-vneshekonombanka-garantii-na-3-mlrd-po-kreditam-na-yamal-spg). With the project suffering cost overruns, Novatek sold 20 per cent to CNPC in early 2014 and is negotiating the sale of another 9 per cent (vedomosti.ru/business/articles/2015/05/15/novatek-hoc…ot-vneshekonombanka-garantii-na-3-mlrd-po-kreditam-na-yamal-spg).

In addition to equity sales, the project has a major borrowing programme. It has been looking for $20 billion from Chinese banks and agencies, and has confirmed loans of $3 billion from Sberbank and $1 billion from Gazprombank, as well as a $3 billion credit guarantee from VEB. It has also been allocated R150 billion from Russia's sovereign wealth fund, the Fund for National Welfare (FNW) (vedomosti.ru/business/articles/2015/06/05/595300-sberbank-i-gazprombank-mogut-videlit-na-yamal-spg-4-mlrd).

On a global scale Russia's LNG plans are modest. Projections suggest that Russia will have no more than 15 per cent of the Asian LNG market by 2050 (Koch-Weser & Murray, 2014; Paltsev, 2014). Australian projections run only to 2025, in which year exports of 130 Mt are predicted (Australian Bulk Commodity Exports, 2012, p. 68), a figure which Russia would barely surpass according to the most optimistic projection by 2050.

Even before access to Western technology and funding was limited through sanctions from mid-2014, there were doubts about even these modest expectations on two grounds: would Russian output growth be enough to meet both export and domestic demand, and would prices be at the level required to bring the country the export earnings on which it depends. An Australian report (Australian Bulk Commodity Exports, 2012, pp. 48–9) doubts Russia's capacity to reach the output volumes needed, given the high capital costs involved. For Shadrina and Bradshaw (2013, p. 491) the issue is price. They conclude that it remains to be seen ‘whether or not Russian LNG can compete on commercial terms in a highly competitive market’.

While there might be doubts about Russian LNG, Russian pipeline gas is recognised as a competitive threat by LNG exporters (Australian Bulk Commodity Exports, 2012, pp. 33, 117). In May 2014, after many years of negotiation, a deal was signed with China for the delivery of pipeline gas along the so-called Eastern route, to take gas from yet to be developed fields in East Siberia to the border at Blagoveshchensk in the Amur region. Capacity is to be 15 Mtpy, at a construction cost of $7.3 billion, with an initial start up date of 2018 (Shadrina & Bradshaw, 2013, p. 487). There has been a lot of discussion on how beneficial the deal will be to Russia, with many believing that the return on investment will be minimal if not negative (www.rbcdaily.ru/economy/562949992526177).

With the Eastern route deal done, attention turned to what had been Russia's first choice, the ‘Altai’ pipeline from existing fields in West Siberia that currently serve European markets, with a pre-contract agreement signed in May 2015 for the delivery of 30 billion tonnes of gas over 30 years (vedomosti.ru/business/articles/2015/05/12/gazprom-i-cnpc-dogovorilis-ob-usloviyah-postavok-gaza-po-zapadnomu-marshrutu). With European markets in decline an alternative is needed, and with a relatively short new pipeline to the Chinese border the project is attractive in capital expenditure terms. However the fact that the pipeline arrives at the border in China's north-west makes it a less attractive option for the Chinese. The project is a long way from start up, with the decline in sales to Europe happening now. That does not help Russia's negotiating position. Because of the fixed-point nature of pipeline gas, the balance of power between supplier and customer is crucially important, and there are doubts that in the case of Russian-Chinese pipeline gas arrangements the balance is in Russia's favour (Koch-Weser & Murray, 2014).

In summary, there are expert doubts as to whether there will be enough oil and gas to sell to APR markets at an adequate profit margin to replace current revenues that are largely derived from Western Siberian sales to Europe. The doubts apply to the long term, whether prices will be consistently high enough to cover the uncertainties of both output and recovery costs in challenging locational and technological circumstances; and in the short term, in the case of oil whether an output gap between decline in brownfields in West Siberia and the arrival of replacement output from greenfields in the Arctic and East Siberia can be avoided, and in the case of gas a sales gap as markets decline in the West before they can be served in the East (Global Trends, 2013).

Other resource exports

The number of non-hydrocarbon resource projects in the RFE development programme is enormous. 4 Many are unlikely to proceed. Here brief details are given on the more prominent iron ore and copper projects, before a more detailed examination of the commodity with the most potential, coal.

Minerals projects can be found in Sub-programme 2, from page 33 of Appendix (dopolnitel'nyi material) No.1.

Both projects to be described are in the Chita region. Udokan is large (reserves of 1.3 billion tonnes) but with difficult topography and geological structure (Denisov, 1999). The licence, which includes a copper smelter producing 474,000 tonnes of cathode copper per year from 36 Mt of ore, is held by Metalloinvest and Rostekh, politically well-connected companies. It is costed in the RFE development programme at R770 million of state money, plus R930 million from the project owners, as well as separate state funding for the Novaia Chara rail station, situated on BAM 201 km from the deposit (Gosudarstvennaia programma, 2013, pp. 142, 829). However the project has not appeared in any specific funding programmes. In April 2014 licence conditions were amended to extend deadlines for mine start-up and full capacity from 2014 and 2016 to 2020 and 2024 (vedomosti.ru/newspaper/article/682001/metalloinvest-podelitsya-udokanom). Metalloinvest and Rostekh have been unable to attract Western partners for the mine, and are now looking for Chinese involvement, so far with no clear response (top.rbc.ru/economics/19/05/2014/924726.shtml).

The other Chita copper project, Bystrinskoe, is owned by Norilsk Nickel (and is not to be confused with another project by the same name on Kamchatka). It was originally touted as involving four or five copper and polymetal mines, but the scale of the project has been reduced as reserves failed to be proven. Eventually a firm commitment was made to the mining and enrichment of copper at Bystrinskoe, with claimed reserves of 2.7 Mt (Fortescue & Rautio, 2011, p. 845; polit.ru/news/2013/01/25/gok/). In September 2014 the company approved tenders for construction of the mine and enrichment plant to process 10 Mtpy of ore, with start up in May 2017 (nornik.ru/assets/files/Prilozhenie-N-5—informaciya-na-sajt—rus.pdf).

In October 2014 Norilsk Nickel head, Vladimir Potanin, reported to Putin that his company had spent R8 billion on the mine, and another R8 billion (representing 25 per cent of the cost) on a rail line connecting it to Borzia, a station on the line to the Chinese border at Zabaikalsk (news.kremlin.ru/news/46891). In September 2014 the company claimed Chinese interest in the project (kommersant.ru/doc/2567904), but with no sign of interest being converted into money in May 2015 a $1 billion credit from state-owned bank VTB was agreed (vedomosti.ru/business/articles/2015/05/18/nornikel-privlekaet-1-mlrd-u-vtb), with talk of VTB taking a 25 per cent equity stake. Norilsk Nickel has the cash reserves to fund the project, but is keen to share the cost and risk with others. Seemingly, as is ever more the case in contemporary Russia, it will share cost and risk with a state-owned bank.

Although data are vague, if both Bystrinskoe and Udokan were to go ahead (the former more likely than the latter), they would produce roughly 540,000 tonnes of concentrate and cathode copper per annum. For comparison, in 2013, Australia – not the biggest producer in the sector – exported 2.18 Mt of ore and concentrate, of which 925,000 went to China (Resources and Energy Quarterly, 2014, p. 84).

Iron ore

Most Russian iron ore is mined and fed into domestic steel making in the western part of the country. Although the world's fifth biggest exporter (25.5 Mt of total output of 102.5 Mt in 2013), Russia is well behind the two biggest, Australia (613.4 Mt) and Brazil (329.6 Mt) (Steel Statistical Yearbook, 2014, pp. 102–3).

There is no demand for iron ore for steel making east of Evraz's operations in West Siberia. 5 A number of iron ore projects are listed in the RFE development programme with a steel mill included. But there must be serious doubts that the mills will be built, meaning that, with one exception to be described below, Far Eastern iron ore projects are export-oriented. We will not look any further at iron ore projects in Magadan and Irkutsk regions that are listed in the RFE development programme.

The only steel plant further east is AmurSteel, an electric arc-fired furnace and so not a user of iron ore. It has been in constant financial difficulties and generally non-operational since the collapse of the Soviet Union.

The Priamure iron ore project is owned by the Petropavlovsk gold mining company. It involves mining at Gar in the Amur region and Kimkano-Sutara in the Jewish Autonomous Region. The Kimkano-Sutara deposits, difficult but already operational, have a design capacity of 10 Mtpy. An enrichment plant at Kimkano-Sutara entered production in early 2015, with a design capacity of 4.18 Mtpy of concentrate. There are also plans for a direct reduction plant to produce 2.5 Mtpy of granulated iron (kommersant.ru/doc/2416900). The Gar deposit is situated 148 km from Shimanovskaia station on TransSib. After primary enrichment on-site, its output of 7.25 Mtpy, is to be hauled to Kimkano-Sutara for further processing (n-dv.ru/?page=3&article=114).

The project includes a bridge across the Amur at Nizhneleninskoe (immediately to the south of Birobidzhan, which is on TransSib) to deliver output to China. Its planned capacity is 5.2 Mtpy, with possible expansion to 20 Mtpy (veb.ru/strategy/region/dv/). Construction of the bridge from the Chinese side – 1.9 km of a total length of 2.2 km – is proceeding with dispatch. Funding has not been finalised for the Russian side of the bridge, and so construction has not begun (government.ru/dep_news/17722/; vedomosti.ru/economics/articles/2015/05/15/rossiisko-kitaiskii-most-nedoschitalsya-investora; vedomosti.ru/politics/characters/2015/06/08/595566-mi-prosto-otsechem-obman). Russian Railways is committed to spending R8 billion on upgrading the rail line connecting Birobidzhan to Nizhneleninskoe (kommersant.ru/doc/2416900).

In March 2015 the Amur region governor informed Medvedev in a muddled conversation that the project had benefited from the ruble's December 2014 devaluation and was working at full capacity (government.ru/news/17303). One nevertheless agrees with Helmer (2014) that it is unlikely that the operation is profitable in other than highly favourable price circumstances.

The Timir iron ore project – situated in south Yakutia and sometimes known by the name of its first stage, Taezhnoe – is owned by Evraz. With claimed reserves of 3.5 billion tonnes the Taezhnoe deposit is 150 km north of Neryungri, which is connected by rail to Tynda, on BAM. The Taezhnoe stage – a mine and enrichment plant producing 4 Mtpy of concentrate – is currently scheduled to be operational by 2017. The state is listed in the RFE development programme as providing R836.6 million to build a rail line from the deposit to the enrichment plant (with Evraz's investment in the project shown at R164.2 billion) (Gosudarstvennaia programma, 2013, pp. 832, 1145). In March 2015 it was announced that the project would share with five other projects the modest sum of R16.8 billion through MFED's investment programme (government.ru/media/files/L2KIqkMwAvU.pdf).

In September 2014 Putin reminded Evraz's Abramov that the licence included a steel mill. Abramov undertook to reconsider the company's position not to build the mill, but suggested that the prospects were not encouraging (news.kremlin.ru/transcripts/46522). While that frees the entire output for shipment, there are claims that concentrate will be delivered to Evraz's steel plants in West Siberia, which currently bring bought-in inputs from western Russia (expert.ru/expert/2014/38/kak-ruda-zavisit-ot-protsenta/). In 2013 Evraz's West Siberian steel making took 4.54 Mt of iron ore inputs from Evraz's own mines, including some that are now non-operational, and bought in 4.29 Mt (Evraz, 2013, p. 52). We do not know how much of Taezhnoe's output will be used in-house, but it appears likely that there will be little left for export.

Regarding the scale of Russian exports more generally, in 2012, 25.5 Mt of iron ore were exported, against the 527.0 Mt of the world's biggest exporter, Australia, of which 393.4 Mt were shipped to China (Steel Statistical Yearbook, 2013, p. 99; Resources and Energy Quarterly, 2014, p. 87). We do not have data on current exports of iron ore from the Russian east, but the figures cannot be high, given the small output of the region. In 2012 the RFE produced 3.4 Mt and East Siberia 17.7 Mt. Neither reserve figures nor the projects just described lead us to expect radical increases (mineral.ru/Facts/Russia/161/529/3_05_fe.pdf, pp. 107, 111).

Russia's largest producer and exporter, Metalloinvest, operates in western Russia. In 2013 it exported 11.147 Mt of ore and pellets (of total ore output of 38.4 Mt), evenly divided between Asian and European markets. Although the company describes China as a priority market, it also stresses that its preference is for long-term contracts with domestic steel makers (Metalloinvest, 2013, pp. 6, 7, 29, 60).

Regarding costs, Helmer (2014) provides data that suggest that the east's small mines will struggle to be competitive. In summary, scale and cost issues in a highly competitive market make building an export-oriented iron ore mine in eastern Russia a very marginal proposition.

Russia's greatest hopes are for coal. It is a key part of the policy debate over RFE development, since arguably the most controversial issue – the expansion of the BAM and TransSiberian railways – is intimately linked to Russian coal exports to the APR.

There has been a steady increase in exports in recent years (see Table 1). Steaming coal makes up about 85 per cent (‘Itogi’, 2014a, p. 62). Russia is the world's fifth biggest coal exporter, third in coking coal (‘Itogi’, 2014a, p. 62). A major downturn in domestic demand, caused by declines in steel production and gasification of local markets, has made exports more important for coal producers.

Exports as share of total Russian coal deliveries, 2000–2012, Mt.

Exports as share of total Russian coal deliveries, 2000–2012, Mt.

Sources: ‘Itogi’, 2013, p. 66; ‘Itogi’, 2014a, p. 61.

Around 80 per cent of exports come from the Kuzbass, in south-east Siberia, with East Siberia contributing around 10 per cent and the RFE slightly less. Around 60 per cent of coal exports are shipped by sea, of which 53.5 per cent went through eastern ports in 2013 (‘Itogi’, 2014a, pp. 62–3).

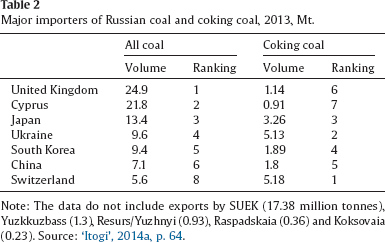

Table 2 shows the top importers of Russian thermal and coking coal. India, seen by many as a major importer in the future, imported no coal from Russia in 2012, 388,000 tonnes in 2013, and 142,000 in the first quarter of 2014 (‘Itogi’, 2014a, p. 64; ‘Itogi’, 2014b, p. 49). The data in Table 1 do not include the exports of the biggest exporter SUEK. In 2013 it exported 42.4 Mt, of which 12.6 Mt went to China. Other companies exporting to the region include Mechel (12.01 Mt exported in 2013, of which 6.3 Mt went to China, with the company providing 7.5 per cent of Chinese imports of coking coal), and Raspadskaia (3.3 Mt exported in the first half of 2014, of which 42 per cent went to the APR, of which 70 per cent, 1.1 Mt, were shipped to China) (vedomosti.ru/newspaper/article/775941/kitaj-ostanavlivaet-ugol). These companies operate primarily in the Kuzbass. However Kuzbass output is peaking, with effects on forecast exports by region to be outlined later.

Major importers of Russian coal and coking coal, 2013, Mt.

Source: ‘Itogi’, 2014a, p. 64.

Note: The data do not include exports by SUEK (17.38 million tonnes), Yuzkkuzbass (1.3), Resurs/Yuzhnyi (0.93), Raspadskaia (0.36) and Koksovaia (0.23).

In a quick survey of existing coal operations in the RFE and East Siberia, we begin with Sakhalin. In 2012 total output was 4.1 Mt, of which 1.92 Mt were exported, primarily to China, Japan and South Korea (energo-news.ru/archives/108639). The then Sakhalin governor set the goal to increase output to 9 Mtpy over the following 5–7 years, with 90 per cent exported (government.ru/news/4586). In 2013 the island exported 2.3 Mt, of which 41.6 per cent went to South Korea, 31.3 per cent to China, and 27.1 per cent to Japan (admsakhalin.ru/index.php?id=152).

The biggest producer on Sakhalin is Vostochnaia Gornorudnaia Kompaniia (Andreev, 2014). It has been hit hard by gasification and is energetically looking to expand exports. It claims to have high quality steaming coal with, given the mine's proximity to the port of Shakhtersk and then Asian markets, good export prospects. Exports increased from 450,000 in 2011 to 600,000 in 2012. It had a target of 2.5 Mt for 2013 but managed only 1.2 Mt. It hopes to ship 5 Mtpy by 2016.

Growth is limited by port capacity. Ocean-going ships cannot be loaded directly from the terminal at Shakhtersk. However the fleet of ice-capable loading barges has been renewed. The port is now able to handle 2000 tonnes per hour (a reasonable rate, although the biggest Australian operations handle four times as much or more). It is currently loading 55,000 tonne ships, with plans to receive 120,000 tonne ships.

Other exporters on the island (Gornyak-1 and Uglegorskugol’) produce below 1 Mtpy. They export to nearby APR countries, and both have output and port expansion plans (www.sakhalin.info/news/84702/; n-dv.ru/?page=3&article=114).

Mainland RFE producers include Primorskugol, north of Vladivostok. Owned by SUEK, the company mines steaming coal. Output peaked in 2011 at 5.69 Mt, the decline since the result of gasification of the domestic market. In 2013 it exported 567,900 tonnes, mostly to China (Zan'kov, 2014).

SUEK's Urgalugol, near Khabarovsk, produced 4.639 Mt of steaming coal in 2013, of which 2.937 Mt was exported to Asia. Investment of R16 billion is to take output to 8.1 Mtpy by 2019 (zrpress.ru/business/khabarovsk_24.06.2014_67007_khabarovskij-ugol-rvetsja-v-atr.html). The mine is included in MFED's investment programme (government.ru/media/files/L2KIqkMwAvU.pdf).

Existing East Siberian mines produce mainly for the domestic market, although Vostoksibugol has export contracts with Chinese companies and Korea's Posco, with an export target of 3 Mtpy over five years (www.kvsu.ru/companies/66/). Mechel's ‘Neryungrinskii’, situated close to Neryungri in Yakutia and therefore accessible by rail to BAM, exports coking coal to China, Taiwan, Japan and Korea. It is a mature mine with declining output.

Russkii ugol digs coal in the Kuzbass (c.1.3 Mt in 2013), Amur (3 Mt) and Khakasia (3.2 Mt). In 2013 it exported 1.51 Mt of steaming coal to South Korea, China and Eastern Europe. The Amur operations are to be expanded to provide coal for new power stations, one of which – Erkovitskoe – is to export electricity to China (kommersant.ru/doc/2405853). The company plans to expand its Khakasia operations to 4.5 Mtpy, of which 50 per cent would be exported (Uzhakhov, 2014).

Greenfield projects

The main greenfield developments in the region are Elegest in Tuva, Elga in Sakha, Apsat and Zashulanskoe in Zabaikal, Denisovskii-Ignalinskii in Yakutia, and the Beringovskii mine in Chukotka, which has been approved as a TOR and was described above.

Elegest is a thermal and coking coal project with claimed reserves of 850 Mt and an output target of 6 Mtpy by 2018. The thermal coal is to be sold domestically and the coking coal exported to the APR (vedomosti.ru/newsline/news/11652391/bajsarov_vzyal_ugol). We discuss its transport infrastructure issues below.

Elga, situated in South Yakutia and owned by Mechel, has an output target of 11.7 Mtpy upon completion of its first stage in 2017. As with Elegest thermal coal will be sold on local markets and coking coal exported to the APR, with a deal with Baosteel already signed (vedomosti.ru/newspaper/article/418711/desyatina_mechela). With capital expenditure set at $4.74 billion, of which $2.5 billion is required for the first stage, and in circumstances of severe financial difficulties, Mechel has been trying to attract Chinese, Japanese and Korean involvement, so far with no success (kommersant.ru/doc/2449581; vedomosti.ru/newspaper/article/677311/aziya-gotova-vesti-biznes-s-rossiej).

Apsat, owned by SUEK, is about 50 km from Novaia Chara station on BAM northeast of Lake Baikal. It has reserves of 2.2–3.5 billion tonnes (Tsinoshkin & Dulin, 2014). Exploitation of the difficult deposit began in March 2012. In 2013 652,500 tonnes were mined, of which 462,100 tonnes were exported. In the first half of 2014, 498,900 tonnes were dug and 372,500 tonnes were shipped. Fifty-four per cent of shipments were exported, with China taking 115,475 tonnes, South Korea 74,500 and Japan 11,175 (Tsinoshkin & Dulin, 2014; Tsinoshkin, Samoilenko, & Dulin, 2014). The plan is to produce 5 Mtpy by 2021 (news.chita.ru/52747/).

En+'s Vostoksibugol has a 50:50 joint venture, known as Razrez Ugol’, with China's Shenhua. In December 2013 it won the licence to the Zashulanskoe thermal coal deposit in the Zabaikal region. The coal, while of limited quantity (reserves of 252 Mt), is said to be of good quality. With both domestic and Chinese markets in view, an open cut mine is planned for 2018, with full capacity of 6 Mtpy reached by 2021. R30 billion will be spent (‘En+ and Shenhua’, 2014, p. 32; news.chita.ru/61479/; enplus.ru/press/enplus/1215/).

Kolmar is owned by the well-connected Gennadii Timchenko, although there have been reports that he is seeking to sell the company, with claimed Chinese interest (vedomosti.ru/business/articles/2015/04/27/timchenko-gotov-prodat-dolyu-v-kolmare-kitaitsam). The company has two underground projects in Yakutia. There are plans to expand the existing ‘Denisovskii’ mine, just north of Neryungri, to 2.4 Mtpy at a cost of $450 million. ‘Inaglinskii’, further to the north, is a bigger greenfield operation. At a cost of $830 million 6 Mtpy will be mined and enriched from 2016, with a second stage to take output to 10.5 Mtpy. The project includes a railway to Chulbas, on the mainline running south from Yakutsk to BAM (kolmar.ru/projects/). In March 2015 the project was included in MFED's investment programme (government.ru/media/files/L2KIqkMwAvU.pdf).

Coal forecasts

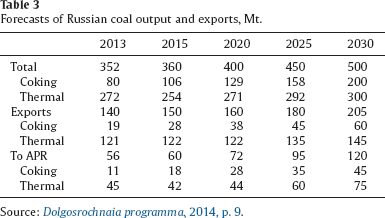

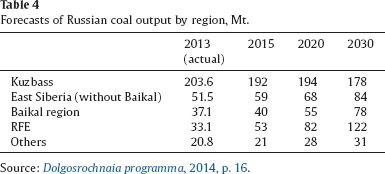

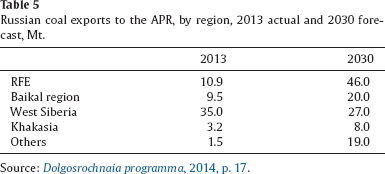

What do these projects add up to? The ‘Long-term program for the development of the coal industry of Russia to 2030’ forecasts output of 500 Mt by 2030, with East Siberia and the RFE going from 34.6 per cent in 2013 to 56.8 per cent, with the RFE making up 24.4 per cent. The RFE is also predicted to be the major source of exports to the APR (46.0 per cent), with the Kuzbass in second position (27.0 per cent) (see Tables 3–5). It is not clear where that level of RFE output will come from – none of the major greenfield projects listed above are located there and expansion plans on Sakhalin are modest.

Forecasts of Russian coal output and exports, Mt.

Forecasts of Russian coal output and exports, Mt.

Source: Dolgosrochnaia programma, 2014, p. 9.

Forecasts of Russian coal output by region, Mt.

Source: Dolgosrochnaia programma, 2014, p. 16.

Russian coal exports to the APR, by region, 2013 actual and 2030 forecast, Mt.

Source: Dolgosrochnaia programma, 2014, p. 17.

China is the great market hope. Russia delivered 19 Mt, just over 6 per cent of China's annual imports, in 2012; 27 Mt in 2013; and 15 Mt in the first half of 2014 (minenergo.gov.ru/press/min_news/20303.html). But there are clear difficulties. China's long-term demand is uncertain on a number of grounds: its growth rate, its desire to reduce coal consumption for environmental reasons, and its desire to protect its local coal industry. Minister of Energy Novak has noted with regret China's introduction of import duties in January 2015, which he claimed made some projects unprofitable (minenergo.gov.ru/press/min_news/20303.html). The new duty led to a drop in Russian exports to China in the first two months of 2014 of 40 per cent year-on-year (vedomosti.ru/business/articles/2015/03/27/otgruzki-v-kitai-energeticheskogo-uglya-sokratilis-na-40).

Projected Russian volumes are significant but not spectacular by international levels. Export projections for 2025 are 26–34 per cent of Australian export scenarios (Australian Bulk Commodity Exports, 2012, p. 68). What of costs? Russian sources show recovery, processing, and non-production costs, with transport not included, above current global prices (Dolgosrochnaia programma, 2014, p. 5; ‘Itogi’, 2014a, p. 58). Global cash cost curves not reproduced here but available at Whitehaven Coal (2012, pp. 7, 9) show that for coking coal in 2012 Russian producers were scattered through the third cost quartile, roughly $80–100/tonne. Most Australian producers were in the $60–80 range. For thermal coal Russian producers were a solid block at the very high end. Australian producers were scattered along the scale.

The Russian cost figures just mentioned do not include transport, which is said to make up nearly 50 per cent of total costs (Kontorovich, Filimonova, Eder, & Provornaia, 2013, p. 55; vedomosti.ru/newspaper/article/821481/valyutnye-relsy-rzhd). The cost curves just cited are FOB, so include transport costs only up to and including the loading of the ship in the home port. They therefore distort the costs of many Russian producers, with long internal hauls, compared to Australia, whose major transport distances are by sea.

The deputy governor of Kemerovo region (where Kuzbass is situated) claims that Russian rail is 2–5 times more expensive than competitors’ means of transport (Gammershmidt, 2014). Other sources suggest that the cost advantage to shipping could be as high as 6:1 (Liao, 1997, p. 54) or even 8–10:1(novayagazeta.ru/economy/65738.html). The distance to Shanghai from Newcastle, the most distant Australian coal loading port, is 9500 km. The distance from Mezhdurechensk in Kuzbass to Vanino is 5500 km by rail (with the Primore ports another 600 km or so); from Neryungri to Vanino is 2100 km. The shorter Russian distances are cancelled out by the higher costs of rail, without even considering the 3000 sea kilometres from Vanino to Shanghai. (The sea route from Vladivostok to Shanghai is 2000 km.)

Even if Russian rail was competitive with the shipping costs of competitors, there are major questions of rail capacity and the financing of programmes to expand it. The matter has been one of the most debated RFE policy issues. Transport issues arise at three levels: access from the deposit to the nearest main line, port capacity, and main line capacity.

Spur lines

Spur line costs are negotiated between licence holder and Russian Railways, meaning that there has been much toing and froing in each individual case. There have been various promises from the state to part-fund, including with money from FNW, Elegest's 401-km line to Kuragino (from Kuragino a main line runs south west to Taishet) (vedomosti.ru/business/articles/2015/03/30/pochemu-ziyadu-manasiru-pridetsya-rasstatsya-so-stroigazkonsaltingom). With no sign of the promises being kept, the project appeared among the agreements signed during Chinese President Xi's visit to Moscow in May 2015 (vedomosti.ru/business/articles/2015/05/12/rossiiskie-kompanii-rasschitivayut-poluchit-dostup-k-kitaiskomu-finansirovaniyu). Whether Chinese money will be forthcoming, and what will happen if it does not, remains to be seen.

Most of the $2 billion Mechel had spent on the Elga mine up to mid-2013 had gone on the 316-km line to Ulak on BAM. But as the company struggled with massive debts, the idea was floated that Russian Railways buy equity in the line, perhaps with money lent by Mechel's creditors, Russia's state-owned banks (vedomosti.ru/newspaper/article/734171/igor-zyuzin-vyjdet-iz-tupikovogo-aktiva). Russian Railways is not keen, and there is no sign of the issue being resolved as Mechel's broader struggle for survival continues.

With regard to the other greenfield mines, it appears that coal is transported the 60-odd mountainous kilometres from Apsat to Novaia Chara and the 100 km from the Zashulanskoe deposit to TransSib by road. The Apsat owners seem to be responsible for their arrangements; the Zashulanskoe operators have a Chinese loan for at least part of their costs.

Ports

Port development has been almost exclusively the responsibility of private operators. The most important are outlined here.

SUEK has 12 Mtpy capacity at Vanino, east of Khabarovsk, with plans to double that, and Kolmar is building a terminal in the area with a planned capacity of 12 Mtpy when its first stage is completed in 2016, to be doubled by 2018 (rg.ru/2013/01/23/vanino.html; vedomosti.ru/newspaper/article/714421/ugol-vmesto-nefti). Kolmar's facility is included in the list of projects to receive funding from MFED's investment programme (government.ru/media/files/L2KIqkMwAvU.pdf).

Along the Primore coast Mechel owns Poset, an ice-free coal-loading facility south of Vladivostok and served by TransSib. It currently handles 4.5 Mtpy, with plans to take it to 7–9 Mtpy (mechel.ru/sector/logistics/poset/). Nakhodka's Vostochnyi, owned by the Kuzbass coal producer Kuzbassrazrezugol’ (vedomosti.ru/newspaper/article/772451/ugolschiki-dobavili-vostochnogo), is the largest cargo port in the RFE, and has a 15 Mtpy coal terminal able to load 150,000 tonne ships at 3000 tonnes/hour. It is expanding its capacity by another 10 Mtpy by 2017 (ria.ru/interview/20140219/995778961.html). At the end of 2013 the Kuzbass producer SDS signed an agreement to build a terminal at Sukhodol, with a capacity of 6 Mtpy by 2017 and 20 Mtpy by 2021, although there is now talk of that project being abandoned (interfax.ru/business/427772).

The current official Russian forecast (Dolgosrochnaia programma, 2014, p. 14) sees coal volumes sent to Russian ports for delivery to the APR reaching 110 Mtpy by 2030 (from 49.2 in 2013). Projected RFE capacities by individual port in the same report add up to 90 Mtpy, with Poset and Sakhalin ports not included. If we add them we get close to the 110 Mtpy required. That roughly corresponds to the 120 Mtpy of exports to the APR by 2030 projected in Table 3, remembering that some coal will presumably still be shipped to China by rail.

Main line capacity

Since late 2011 main line capacity has been a matter of considerable urgency, the main issue being the capacity of BAM and TransSib, the two main lines east through Siberia. For Kuzbass coal miners the upgrading of the line from Mezhdurechensk, in the Kuzbass, to TransSib and BAM at Taishet is also a priority. In mid-2015 the government gave Russian Railways R11.05 billion for that project (government.ru/docs/18313/).

BAM leaves TransSib at Taishet, to the north west of Lake Baikal and continues around the north of the lake. It reunites with TransSib near Khabarovsk, before branching off to Vanino to the east. TransSib runs around the south of Lake Baikal, passing through the Zaibakal, Chita and Amur regions, and after rejoining BAM near Khabarovsk continues south through Primore region before ending at Vladivostok and Nakhodka.

Although it is acknowledged that coal is the most important product, the other mineral projects described above also depend on access. Of current throughput coal represents 48 per cent, minerals 5 per cent, and oil 19 per cent (Misharin, 2014). As pipelines open, the oil percentage will decline. Whether the network, particularly BAM, is currently overloaded or underutilised is a matter of debate (dvforum.ru/2009/doklads/Zaichenko.pdf; vedomosti.ru/newspaper/article/713361/i-snova-bam).

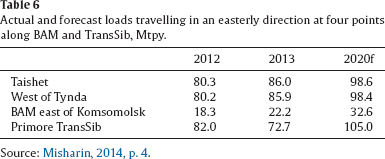

Forecasts for future traffic through various points are shown in Table 6. The first point, Taishet, includes Kuzbass coal. The second, just to the west of Tynda, shows changes to throughput as the lines pass through East Siberia. The data suggest that more goods are unloaded than are added. Just beyond this point, loads from the north, through Neryungri, are added. There is a link line at this point between BAM and TransSib. The next measurement is of loads going to Vanino and the nearby general cargo port at Sovetskaia Gavan. The final measurement is on the TransSib in Primore region, of loads bound for Primore ports. If we assume that the current 53 per cent of traffic taken by coal and other minerals is maintained to 2020, the share of rail capacity to Vanino and the Primore ports corresponds precisely to the forecast 72 Mt of coal exports to the APR that year.

Actual and forecast loads travelling in an easterly direction at four points along BAM and TransSib, Mtpy.

Actual and forecast loads travelling in an easterly direction at four points along BAM and TransSib, Mtpy.

Source: Misharin, 2014, p. 4.

To reach the forecast capacities, considerable investment is required. The state-owned monopoly rail corporation, Russian Railways, insists it does not have the money, and it is recognised that to raise rates to the level required for it to self-fund would make Russian coal exports hopelessly uncompetitive (vedomosti.ru/newspaper/article/482291/vladimir-yakunin-poprosil-na-transsib). After much debate the state has allocated just over half the R562.4 billion required, the money coming directly from the budget, FNW and bond purchases by VEB bank (Fortescue, 2015). This is to increase capacity by 66 Mtpy, divided roughly equally between BAM and TransSib. An extra provision of R42.3 billion (R29.1 billion from Russian Railways, R7.5 billion from FNW) for the section of BAM from Tynda to Vanino was announced in January 2015 (government.ru/docs/16441/).

A major part of the BAM-TransSib debate has been over whether the extra capacity will be utilised. After the expansion figure was set at 66 Mtpy, the responsible deputy prime minister, Anatolii Dvorkovich, noted that the key question remained: ‘Will the required volumes of freight eventuate?’ He answered by claiming that shippers had asked for an extra 137 Mtpy, meaning that there was plenty of room for error. He did not point out that if their bids had any basis in reality a lot of potential output will not have access to APR markets (government.ru/news/15411/).

Even if the capacity is used, will capital costs be recouped? It is claimed that a decade of public and private infrastructure investment worth $30 billion had in 2011 alone facilitated the export from Australia of 400 million tonnes of iron ore, 300 million tonnes of coal, and 20 million tonnes of LNG (Australian Bulk Commodity Exports, 2012, p. 2). The BAM–TransSib project, to add 66 Mtpy of capacity, is slated to cost R600 billion just for the rail work. Even if the recent devaluation in the ruble has reduced that from about $17 to 11 billion, it is an expensive increase in capacity, including in comparison to Russian Railways’ expansion plans in other parts of Russia (government.ru/docs/16441/). One is not surprised that there are those who believe that the capital expenditure will not be recouped (vedomosti.ru/newspaper/article/396211/slovo_za_sibiryu).

This is as prices for commodity exports into Asia are falling and predicted to remain flat at best, just as Russian projects come on line. Australian sources, in acknowledging poor price prospects, advocate maintaining revenues by ramping up supply (Australian Bulk Commodity Exports, 2012, p. 10). Whether that is a good or viable strategy for Australia could be debated. It is one which is not available to Russia, given output and infrastructure limitations. If prices are not favourable, Russian producers will be left with large debts and the Russian state with underutilised infrastructure, with very few options to redress the situation.

Russia has offered two strategies for commercial engagement with the APR, in pursuing two goals. The TOR strategy, originally presented as attracting APR investors to produce non-resource products for sale in the APR, was designed to bring prosperity to the RFE. So far the reality is very different. There is little sign of the APR in the shape of either investors or markets. The TORs so far identified are modest, involving largely unknown Russian small and medium enterprises in ‘industry park’ activities and attracting modest state investment. They are scattered around the region in a way that suggests regional policy considerations as much as strictly commercial calculations. There is nothing wrong with that: the weakness of Russia's SME sector is often noted and such activities can bring benefits to local communities. But even assuming that the TORs are successful at that level, that is not enough to transform the RFE as a whole into a qualitatively more attractive place to live and work, and certainly not to realise the most ambitious visions of a Russian Asian Tiger.

The resource strategy is essentially not an RFE strategy, since the region narrowly defined is not particularly resource rich and the strategy is not primarily designed to contribute to its prosperity but rather to that of the nation as a whole, as part of a major geostrategic and geo-commercial shift from West to East.

It could be argued that for Russia any non-negative return from coal and other mineral exports to the APR is a benefit, since it is an essentially new commercial activity. But the scale of even the most optimistic scenarios – of output and delivery capacity – is modest compared to the major players in the region, and not obviously low-cost. At best returns will be marginal, with a real risk of a negative return on capital for both the state and investors.

Capital commitments in the hydrocarbon sector are significantly higher, and eastern-oriented projects are needed to replace revenues from West Siberian output delivered to the west. If that cannot be achieved, a country with an increasingly expensive view of its place in the world will face serious problems.

For some time there has been confidence within Russia – albeit not shared by all – that the country's natural resources will provide it with prosperity for a long time to come. There is nothing about the TOR strategy to suggest that the reliance on resource exports is about to change. The belief that those resources will be found and sold in the east, although hardly new, has gained sudden urgency in recent times. There are sufficient question marks, regarding not just demand but also supply and return on investment, to indicate just what a gamble the ‘turn to the East’ is.