Abstract

The purpose of this article is to explore the development of Russian military spending in light of weak and negative growth of the Russian economy and to look at the reasons for the economic decline that has developed after the economic crisis in 2009 and is due to long-term internal structural factors that have existed since the mid-2000s. The confidence crisis resulting from Russia's aggression against Ukraine 2014, Western sanctions and falling oil prices has further aggravated these tendencies and the economy is now contracting. The main conclusions are that the share of the defense budget in GDP has risen substantially, but there is still a trade-off between defense and other public spending in the budget. Political reform would be necessary to implement market institutions and revive the economy.

Introduction

Russia's aggression against Ukraine in 2014 and the intensified economic decline that followed have changed the conditions for Russian military spending. For a decade Russia's geopolitical ambitions have been reflected in increased defense spending. Since the economic crisis in 2009, however, Russia has experienced low growth for several years; in 2015 it is facing a substantial contraction of GDP, and growth prospects are weak for the foreseeable future. It follows that continuing to give high priority to defense will become more costly in terms of other public spending. How far is Russia ready to go in giving precedence to defense over other public expenditure under these new circumstances? Will the high level of defense spending be maintained or will it be adapted to the new economic conditions?

Russia's military expenditure became increasingly noteworthy as it rose in the 2000s, and it became even more relevant to study its development as Russia started to challenge the new security order in Europe that had been formed after the end of the Cold War. In his speech to the Federation Council on 25 April 2005, President Vladimir Putin (2005) claimed that “the collapse of the Soviet Union was a major geopolitical disaster of the century”. Two years later, in his address to the Munich Conference on Security Policy he described the unipolar world that developed after the Cold War with the US as the only superpower as “unacceptable” (Putin, 2007). The war with Georgia in 2008 made it clear that Russia's geopolitical ambitions were real and not just slogans for an audience at home. 1 It showed that Russia was ready to use force to protect its “sphere of influence”. A military reform was introduced in 2008 aiming at modernizing the Armed Forces and giving them a “New Look”, 2 thereby building contemporary military capability in terms of both advanced technology and professional personnel. The reform signaled that the defense budget would continue to be a priority and also that the leadership was opting for more capability per ruble spent. In support of the reform, a new ten-year state armament program was launched in 2011, which aimed at rearming the Armed Forces with up-to-date arms and support systems up to 2020. 3 The armament program led to yearly arms procurement rising as share of GDP, and concerns about cost-efficiency and value for money became more pronounced in the Ministry of Defense's procurement policy. 4

When Georgia and Ukraine pursued attempts to join NATO in 2008, this was too provocative for Moscow.

“Novyi Oblik”. For an account of the military reform in 2008–2011, see Carlsson and Norberg (2012, pp. 97–111).

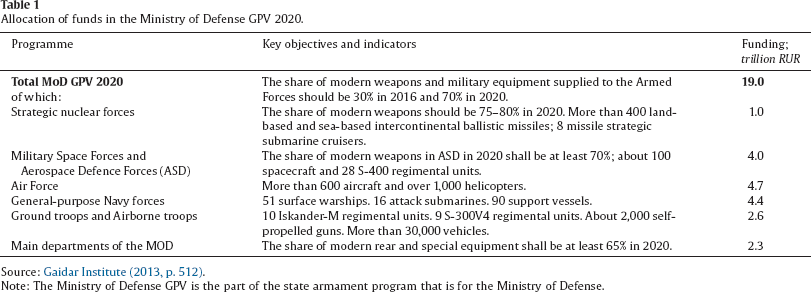

The state armament program for the period 2011–2020. RUR 19 trillion were to be spent and as a result 70 percent of the armed forces’ arms were to be modern by 2020 (Oxenstierna & Westerlund, 2013, p. 2).

Over the ten-year period 2000–2010 arms procurement as a percentage of GDP rose from 0.7 to 1 percent. With the new state armament program that share would double to 2 percent up to 2014. Then Defense Minister Anatoly Serdyukov challenged the industry over prices and opened it up for competition from abroad (Oxenstierna & Bergstrand, 2012, pp. 50–51).

The purpose of this article is to explore the development of Russian military spending in light of the changed economic situation and also to look at the reasons for the economic decline that has developed after the economic crisis in 2009. Attempts to modernize the economy have failed, which is due to a number of long-term internal structural factors that have existed since the mid-2000s. The confidence crisis resulting from Russia's aggression against Ukraine, Western sanctions and falling oil prices has further aggravated these tendencies and the crisis.

The article starts by investigating the economic situation and military expenditure up to 2013 (section 2). In this section the factors behind the rise in the defense budget since 2011 are explored. The third section analyzes the long-term reasons for Russia's weak economic growth after the economic crisis in 2009. Section 4 discusses Putin's economic policy after he came back to the presidency in 2012. In section 5 economic policy and defense spending after 2013 are discussed, including the amendments to the original federal budget law for 2015 that were made in early 2015. Finally, the conclusions are drawn in section 6.

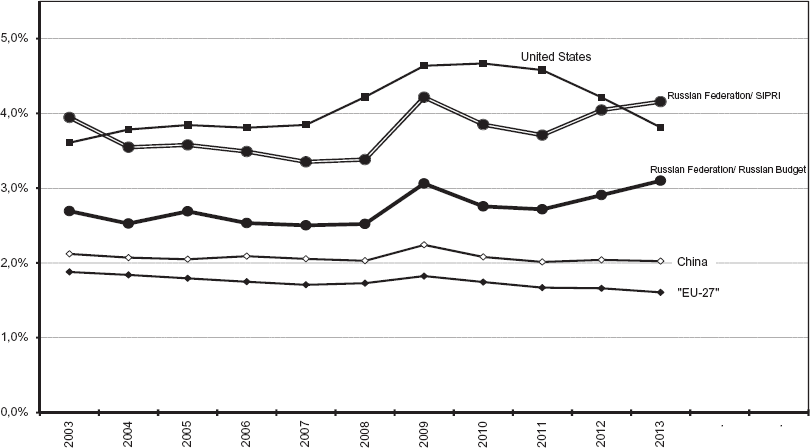

Over the ten-year period starting in 2003, Russia's military expenditure doubled, and in 2013 Russia was the third largest country in terms of military spending in the world, with annual expenditure of USD 88 billion and a sizable share of GDP – of 4.4 percent (SIPRI, 2014). This was on par with the share of GDP of the USA but high in comparison with the EU (27) countries’ average of about 2 percent (e.g. France has 2.3 percent and the UK, 2.5 percent; SIPRI, 2014). In value terms Russia's defense spending was now considerably higher than that of France (USD 61 billion) and the UK (USD 58 billion), countries whose military spending was twice as high as Russia's ten years earlier (SIPRI, 2014). Over just a decade Russia had managed to substantially enlarge its defense budget, a strategic precondition for developing its military strength, for further reform of the Armed Forces and for pursuing the geopolitical agenda.

Figure 1 shows the GDP shares of military expenditure for Russia and the EU (27) countries in accordance with SIPRI's data which are based on a common definition, which allows international comparison. It also shows the GDP share of the Russian defense budget which is based on a more narrow definition than SIPRI's. The defense budget is the magnitude used in the discussions of allocations in the federal budget.

Estimated military expenditure as share of GDP for Russia and selected countries 2003–2013; per cent.

A fundamental condition for the increase in Russia's military spending was its exceptionally high economic growth during the 2000s. Yearly average growth between 2000 and 2008 was 6.9 percent, a growth rate only challenged by China (10.4 percent) and India (6.7 percent) among the developing and emerging economies (IMF 2014; Kudrin and Gurvich, 2015: 4). During the later period, 2009–2013, including the financial crisis, Russia's average growth was 1 percent, those of China and India 8.9 and 7.0 percent respectively (IMF 2014). The high growth rate in the first period was due to the economic reforms in the 1990s that led to structural change, productivity increases, integration with Europe and the rise in the oil price from an average of USD 19.60/bbl 5 in the 1990s to almost USD 150/bbl before the dip in 2008. After that oil prices increased again, but growth did not pick up as expected after 2009–2010; instead it declined gradually.

In constant 1999 USD, bbl = barrels of oil.

Taking the 2000s as a whole, the Russian economy grew at an average rate of 6 percent per year, and so did the defense budget, with a fairly stable share of GDP of around 2.7 percent. Russia's total military expenditure according to SIPRI's definition amounted to about 4 percent of GDP during this period of high growth.

In 2011, when the military reform was introduced, the defense budget rose to 2.9 percent of GDP and the three-year budget for 2012–2014 anticipated an increase to 3.2 percent of GDP in 2012, to 3.7 in 2013 and to 3.9 percent in 2014 (Oxenstierna & Bergstrand, 2012, 63). The actual result for 2012 was a defense budget of 2.9 percent of GDP, thus lower than planned, and in the three-year budget for 2013–2015, the defense budget's share of GDP had been lowered to 3.1 of GDP for 2013. The shares of 2014 and 2015 were maintained at high levels of 3.8 and 3.5 percent respectively (Oxenstierna, 2013, p. 116).

On the cost side several factors have affected the size of the defense budget. The main reason is the state armament program for 2011–2020, the increased personnel costs due to a higher share of contract soldiers is another, and finally the need to modernize the unreformed defense industry represent three major factors. The new armament program caused the yearly state defense orders (gosudarstvennyi oboronnyi zakaz, GOZ) to rise steeply, and this presented challenges to the existing procurement system which then Minister of Defense Anatoly Serdyukov started to address in order improve cost-efficiency in procurement. 6

An account of the organizational and economic problems of the procurement system see Oxenstierna (2013, pp. 113–115). See also Malmlöf et al. (2013, pp. 127–136) for an assessment of what has been delivered.

The main factor behind the rise in the defense budget for 2012–2014 was the new state armament program (gosudarsvennaya programma vooruzhenii, GPV) 2011–2020, which doubled the yearly procurement budget of the Ministry of Defense between 2011 and 2013, and planned high levels for subsequent years resulting in arms procurement at 2 percent of GDP by 2014 (Oxenstierna & Bergstrand, 2012, 49, 51). The military objective behind this cost increase is that by 2020, 70 percent of the Armed Forces’ arms were to be modern.

With Vladimir Putin back in the presidency in 2012, the GPV and the defense industry received strong support. Among the first actions taken by Putin (2012a) after his inauguration was his signing Decree No. 603 on the modernization of the defense industry and setting the pace for the realization of the GPV 2020. Later the same year, in his budget address to the Federation Council, Putin (2012d) announced that the Russian defense industry should be a driver in economic development. In 2013, the government economic program stated that the technological modernization of the defense sector should be accelerated. It planned for increased GOZ and special investment programs for the defense industry (Government, 2013, 23).

Of the total budget for procurement of the GPV 2020, RUR 19,000 billion were reserved for the Ministry of Defense and between 2011 and 2020 as much as 80 percent of the total will be spent on purchases of arms, while 10 percent is set aside for research and development (R&D) and 10 percent for repair and upgrading of older equipment (Oxenstierna & Westerlund, 2013, 5). Table 1 shows the allocation of the Ministry of Defense GPV's aggregate funds by major functions in the Ministry of Defense program. The Military Space Forces, Aerospace Defense Forces (ASD), Air Force and Navy would get the lion's share of the funds. In addition, the government planned investment to modernize the defense industry and has issued several Federal Target Programs (FTPs) for this purpose (Westerlund, 2012). The Ministry of Defense website (2013b) gave the yearly targets (in percentages of the totals) for achieving this within different types of arms. As noted by Barabanov, Makienko, and Pukhov (2013, 19), almost 75 percent of the costs are planned to fall in the period after 2015.

Allocation of funds in the Ministry of Defense GPV 2020.

Allocation of funds in the Ministry of Defense GPV 2020.

Source: Gaidar Institute (2013, p. 512).

Note: The Ministry of Defense GPV is the part of the state armament program that is for the Ministry of Defense.

It is already a tradition that before the full period of one ten-year GPV has elapsed, a new one is developed and launched, which makes it difficult to assess to what degree these programs are fulfilled. Not surprisingly, during the present GPV, the new GPV for 2015–2025 was developed, and some deliveries will be postponed. The first official sign of this procedure was an agreement between the Ministry of Finance and the Ministry of Defense of 22 May 2013. The Minister of Finance, Anton Siluanov, proposed to postpone parts of the GPV 2020 for between two and four years due to the expected fall in budget revenues, causing a higher budget deficit, and because the Ministry of Finance must find an additional RUR 1.3 trillion over the period 2013–2016 to fund infrastructural investments prioritized by President Putin (Vedomosti, 2013a, 2013b). The substantial increases in the military budget compared to other budget items over several years constituted an additional argument (Kommersant, 2013a). The cuts appear to have been accepted by the Minister of Defense, Sergei Shoigu, who made reference to the procurement plans being overoptimistic and noted that delays in contracting were already causing delays in production. In July, Vedomosti (2013a) reported that the Ministry of Defense had accepted postponing RUR 87 billion of the GPV, which would be spent in 2014–2016 instead. In addition, the Ministry of Finance proposed to cut the funding of the GPV in general by 5 percent per year over the period 2014–2016 in an attempt to cut all state procurement. 7 Moreover, Shoigu made cuts in foreign orders for defense equipment; for instance, an order for 1275 Iveco LMV-65 light multi-role vehicles was cancelled in December 2012 (Kommersant, 2013b).

This proposal was not accepted at the time, but in the new budget proposal for 2015, the defense allocation has been cut; see Table 4.

Shoigu thus opted for a less confrontational approach (compared to Serdyukov) toward the industry by demonstrating greater flexibility on terms and pricing and promises that future contracts would be awarded primarily to domestic firms (CSIS, 2015). Nevertheless, in 2012, it was still foreseen that limited amounts of foreign equipment would be purchased for experimentation and to spur domestic manufacturers, since the Russian defense industry could not match the technologies produced in the West (The Telegraph, 2012).

The loss-making companies in the Russian defense industry are obviously a strong lobbying power in the Russian military establishment and they continue to get funding and soft credits to cover their losses in exchange for loyalty to the political leadership. Former Defense Minister Anatoly Serdyukov tried to introduce some efficiency into this system. However, his economic approach to procurement and outsourcing of non-military functions led to his fall. Instead, Putin promised continued subsidies and received substantial support from the big defense companies in his election campaign in 2011–2012. Yet keeping the old companies alive comes at a cost. The Audit Chamber noted in its report to the Duma Defense Committee in 2012 that 30 percent of the defense industrial companies were loss-making and that using state credits in the GOZ preserved this unprofitable structure (VPK, 2013). Only 20 percent of the companies were deemed to be in such a shape that they could be modernized. The remaining 50 percent were assessed to be in such a bad state that it would be meaningless to restructure them; instead it would be better to set up new companies and replace them (VPK, 2013).

The use of state-guaranteed credits in the GOZ is another way of perpetuating cost inefficiencies and inhibiting productivity improvements in the defense industry. As shown by Cooper (2012), as much as 22 percent of the GOZ for 2011–2015 was funded from such credits. State credits that are fully backed by the government are very similar to direct allocations. The maneuvering between the Ministry of Finance and the Ministry of Defense in 2013 suggested that credits and budget assignments were, in fact, the same kind of money for the companies since the state even pays the interest rate on credits (Vedomosti, 2013a, 2013b). If state-guaranteed credits are to supplement direct budget allocations, expenditure on the GPV becomes higher than what the budget figures so far have revealed, since the federal budget excludes extra-budgetary spending (spending funded from other sources outside the budget). Apparently, the use of state guarantees in the GOZ has become costly, and in the federal budget for 2015–2017 the state guarantees for the GOZ had been abolished (Cooper, 2014).

How far the GOZ is implemented and arms are delivered is difficult to assess, not least because the breakdown of each yearly GOZ has been secret, although in recent years the GOZ has become more transparent regarding its volume and breakdown into new equipment, renovation and modernization (Malmlöf, Roffey, & Vendil Pallin, 2013, 127). Actual deliveries are also difficult to assess since information is scattered and analyses are usually based on results reported by the Moscow-based Center for Analysis of Strategies and Technologies (CAST) and reports in Russian newspapers. Oxenstierna and Westerlund (2013, pp. 19–24) have attempted to assess the deliveries for the GPV 2020 up to 2011. They concluded that orders for Sineva SLBMs, MiG fighter aircraft, helicopters, diesel-electric submarines and lorries were likely to be met (Oxenstierna & Westerlund, 2013, p. 23). However, on the basis of an assessment of defense industry performance, they found it unlikely that the GPV 2020 would be fully achieved. Moreover they point out that large producers have difficulty developing production capacity and serial production, and that even in the strategic missile and air defense sector companies have had trouble coping with orders (Oxenstierna & Westerlund, 2013, p. 20). Malmlöf et al. (2013, pp. 127–133) compare known deliveries in six branches of armaments in 2011–2012, with the goals of the GPV 2020. Due to the incompleteness of the data, the authors cannot draw far-reaching conclusions but among their findings are that for fixed-wing aircraft only half of orders in 2011 were fulfilled, and in 2012 two-thirds; all contracts for helicopters were fulfilled; but the production of new submarines has been fraught with difficulties (Malmlöf et al., 2013).

Personnel costs

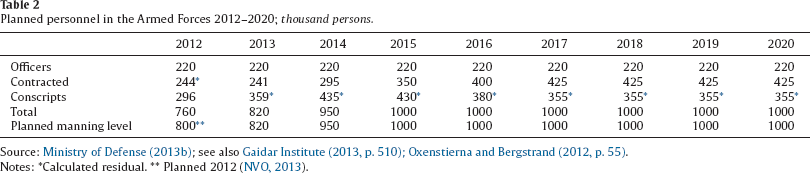

In 2013, Russia entered a period of a sharp decline in the working-age population, and the cohorts of young men of conscription age are small. In the next ten years, the cohorts of 18-year-olds will number below 700,000 a year, and at times the number will be down to ,00 (Oxenstierna, 2013, pp. 109–111). Putin's (2012c) Decree No. 604 on military service requires that the number of contract soldiers should rise by 50,000 per year up to 2018. This boost is a reaction to the shortage of conscripts. The Ministry of Defense (2013b) has published its plans for manning on its website, and Table 2 shows what this will entail for the numbers of contract and conscript soldiers up to 2020. 8

It may be noted that increasing the number of contract soldiers at the pace suggested, and keeping the total target number, 1 million, would entail over 400,000 conscripts being needed every year up to 2016. This is hardly realistic since in these years the cohorts are very small. Either the goal of 1 million men needs to be modified or other reserves need to be mobilized. After 2016, the mix of 425,000 contract soldiers and 355,000 conscripts seems more achievable.

Planned personnel in the Armed Forces 2012–2020; thousand persons.

Source: Ministry of Defense (2013b); see also Gaidar Institute (2013, p. 510); Oxenstierna and Bergstrand (2012, p. 55).

Calculated residual.

Planned 2012 (NVO, 2013).

Having a higher proportion of contract soldiers increases costs. Using the information on military wages and planned personnel gathered by the Gaidar Institute and presented in Oxenstierna and Bergstrand (2012, p. 55), it can be seen that cutting the number of conscripts by 300,000 per year, and replacing them with contracted personnel, would increase the yearly total wage fund by about 40 percent as compared to the original calculations based on 700,000 conscripts. In 2012, the salaries and benefits in the Armed Forces were raised in accordance with a new law on monetary benefits (Oxenstierna and Bergstrand, 2012). The Ministry of Finance estimated that the reform would cost another 1 percent of GDP (Oxenstierna and Bergstrand, 2012). According to the Ministry of Defense (2013a), salaries and benefits have risen 2.5–3 times since the law was adopted and were on average RUR 23 000–35,000 per month in 2013. In July 2013, the Audit Chamber reported that the Ministry of Defense had overspent on salaries by RUR 88 billion in 2012, due to the fact that the actual number of individuals employed was 760,000 rather than 1 million, which the budget for wages was based on (Izvestiya, 2013). The same source estimates the share of personnel in total defense costs at around 30 percent in 2012.

It may also be noted that, even with higher salaries, there is no guarantee that the Ministry of Defense can find all the contract soldiers that are needed. The whole population in the able-bodied age groups is shrinking and the Armed Forces will have to compete with the civil labor market for recruits (Oxenstierna, 2013, p. 105).

The decline of the Russian economy is due to a multitude of factors and is not due just to the process that has evolved since Vladimir Putin came back as president in 2012. The Russian economy has suffered from structural problems since the early 2000s, and unfortunately the modernization program launched in 2009 by then President Dmitry Medvedev – which addressed problems such as the need for diversification from the heavy reliance on the export of hydrocarbons, too much state involvement in the economy, the weak business climate for small and medium-sized businesses and corruption – was too much of a challenge for the ruling political elites and never materialized. 9 Yet the popular protests in the fall of 2011 and early 2012 against electoral fraud, and against Putin's standing for president again, showed that a considerable part of society wanted a change in the political sphere as well.

The modernization program “Russia, forward!” was launched in September 2009 (Medvedev, 2009, discussed in Oxenstierna, 2009, pp. 43–45). This program saw the whole energy industry, nuclear energy, the pharmaceutical industry and IT as the core areas. Generally the program aimed at improving the conditions for development – better institutions, more investment, developed infrastructure, innovation and support to intellectual achievements. Medvedev's analysis of the situation in 2009 was in many respects a strong criticism of the results of Putin's previous two terms: the economic structure was backward, corruption was out of control and society was too paternalistic (Oxenstierna, 2009, pp. 43–45).

A big difficulty for any modernization program in Russia is that the economic system that has developed since the reforms in the 1990s still bears features of the Soviet command system. Despite the change of system from a command economy to a market economy, the institutions that normally support market allocation are weak, and in many ways they are overruled by the informal institutions surviving from the Soviet era. That Russia's institutions are deficient is reflected in the Worldwide Governance Indicators (WGI, 2014). The WGI project constructs aggregate indicators of six broad dimensions of governance: political stability and absence of violence/terrorism; voice and accountability; government effectiveness; regulatory quality; rule of law; and control of corruption. When these indicators are studied over time, it is found that in Russia they have generally been low, that they improved up to the early 2000s, but that since 2004 there has been a marked deterioration in vital institutions like “rule of law” and “control over corruption” (Oxenstierna, 2014). “Voice and accountability” shows a downward trend over the whole period of Putin's leadership since 2000 (Oxenstierna, 2014). Weak institutions create scope for “manual management” of economic matters, which is also a reason why institutions need to be kept weak – so that political goals rather than economic goals can be pursued. In fact Oxenstierna (2014) concludes that growth cannot be restored within this economic system.

The present Russian economic system may be characterized as a hybrid of the old Soviet heritage with inefficient state-owned or state-controlled subsidized enterprises and state intervention, on the one hand, and a market economy consisting mainly of the small and medium-sized business sector that evolved after the change of system, on the other hand. In Putin's power balancing system, the loss-making “Soviet-type enterprises” 10 are subsidized to ensure continuing support for the regime. Rents from high oil prices have been distributed in what Gaddy and Ickes (2010, 2015) call a “rent management system”, and economic behavior has been labeled “rent addiction” (Gaddy and Ickes, 2010, 2015), alluding to the fact that when rents from natural resources are invested in inefficient production by loss-making firms – “addicts” – they will continue to demand resources in order to save jobs and capital already installed. Oxenstierna (2015, pp. 101–102) argues that this preservation of the old industrial structure and the resulting rent management system inhibits the growth of the private market-oriented sector. It provides an explanation for the weak institutional framework and poor business climate in Russia. The old industrial sector is not interested in institutional reform and more competition; “more market” would upset the power balance (Oxenstierna, 2015).

This refers particularly to companies in the defense sector that receive substantial state support in the form of state orders, e.g. the tank and rail car producer Uralvagonzavod.

Nevertheless, liberal economists in Russia have argued for a renewed market reform in order for Russia to be able to compete in the global environment, overcome capacity constraints and support innovation. They have also emphasized the need for real democracy to enable modernization (Åslund, 2012, p. 382). However, the regime under Putin has become more authoritarian and since he came back to power in 2012, civil society has been repressed and civil liberties have been severely restricted. Tax policies and anti-corruption campaigns have had an adverse effect on the establishment and growth of new businesses, and small businesses have shut down or become part of the informal economy instead of expanding and increasing their share in the formal economy. Without political reform it is difficult to see how performance of the economy could improve (Oxenstierna, 2015).

For the European countries that were formerly part of the Soviet bloc, the possibility of EU accession was seen as an effective external anchor for structural reforms in the 1990s. Some observers considered that accession to the World Trade Organization (WTO) might support Russia's improving competition and its internal market (Tarr & Volchkova, 2013). By joining the WTO in 2012, Russia committed itself to bringing its trade laws and practices into compliance with WTO rules. 11 However, the aggression against Ukraine and the sanctions that followed appear to have wiped out any type of benefit that Russia could have exploited from this opportunity. In addition, counter-sanctions and Russia's attempts at import substitution have now led to more protectionism and less competition, and any positive effect of WTO membership will be frozen until the security situation changes.

These commitments include non-discriminatory treatment of imports of goods and services, binding tariff levels, ensuring transparency when implementing trade measures, limiting agricultural subsidies, enforcing intellectual property rights for foreign holders of such rights, and forgoing the use of local content requirements and other trade-related investment measures (Connolly, 2013, p. 61).

Another external factor in Russia's economic policy is the Eurasian Customs Union (ECU) that Russia established together with Kazakhstan and Belarus on 1 January 2010. However, most observers seem to agree that the ECU is primarily a geopolitical instrument and that it will not result in significant economic or institutional gains for its members (Dragneva & Wolczuk, 2013). Russia wants the ECU to include more countries in its “near abroad”, but recruitment to the union has so far produced only meager results. 12 Ukraine was invited to join this union but refused in its attempt to get an accession agreement with the EU in 2013. With isolation from the West, the ECU has become more important for Russia.

On 1 January 2015 Armenia and Kyrgyzstan became members of the ECU.

On the macro level the Russian economy performed well in the 2000s, and its fiscal management won praise. Economic policy under former Minister of Finance Alexei Kudrin was commended for its restraint and low government debt. The crisis management during the 2009 economic contraction resulted in Russia recovering from the crisis, and growth in 2010 was 4.5 percent (World Bank, 2013). After Kudrin's resignation in September 2011 and Putin's return as president in May 2012, the direction of economic policy has been less consistent, and the idea of Russia taking its own route with a “Russian economic model” has seriously challenged the liberal paradigm.

President Putin presented the main directions of his economic program immediately after his inauguration in May 2012. In his first decree, No. 596, on economic policy, Putin (2012b) spelt out the economic improvements that should be achieved by 2018–2020. These included: the creation of 25 million highly productive workplaces by 2020; an increase in the share of investment in GDP to 27 percent in 2018; an increase of investment in state priority industries; an increase in labor productivity by a factor of 1.5; preparations for the privatization of state assets outside the commodity-energy sector; and an improvement of the rating of Russia in the World Bank Doing Business Index from 120th place in 2011 to 50th in 2015 and 20th in 2018.

Also, despite the Soviet experience and evidence from other countries that high military spending does not guarantee high growth, the increased role of the defense industry was stressed in Decree No. 603 and in the budget address 2012, where the defense industry is named “a driver” in economic development (Putin, 2012a, 2012d). The government's economic program also stressed the technological modernization and importance of the defense industry (Government, 2013, p. 23).

Several of Putin's goals appeared difficult to achieve even before the sharp decline in growth in 2013. Raising the investment ratio to 27 percent would have been a difficult task even before the surge in capital flight in 2013–2014. Creating 25 million highly productive workplaces would also have be difficult before the present economic stagnation since the rent dependent companies hoard labor in order to motivate continuous subsidies, and Russia is experiencing labor shortages due to the decline in the working-age population and the low geographical mobility of the workforce (Oxenstierna, 2014). The labor market is tight and for new jobs to be manned old, inefficient “Soviet-type” jobs need to be scrapped and labor motivated and helped to move. As the reform economist Vladimir Mau (2013, p. 14) remarked, there is no labor surplus to employ in these new jobs. Mau also notes that a large part of the educated middle class living in the big cities is ready to leave the country. Moreover, Russian surveys indicate that 70 percent of Russians with an income over the average want their children to study and work abroad and over one third would prefer their children to go abroad permanently (Mau, 2013).

The weak business climate has been a characteristic of the Russian economy despite years of reform efforts to improve it. Nevertheless, Russia's ranking in the World Bank Ease of Doing Business index has improved since Putin's Decree No. 596. In 2013 it had improved to 92nd among 189 countries (from 120th place in 2012). In 2014, Russia had reached place 64 in the ranking and in 2015, 62 (World Bank, 2015). The aspects in which Russia still has substantial disadvantages are “getting electricity”, “obtaining construction permits” and “trading across borders”. Moreover, between 2014 and 2015 the rank of the indicator “getting credits” has deteriorated. The economy did not meet Putin's goal of being ranked 50th in the world in 2015, but nevertheless there is a substantial improvement. This index reflects performance with respect to six different indicators, and it does not capture the balance between old, large enterprises with political influence existing outside market competition and small and medium-sized firms struggling to stay in business and expand. But it is worth noting that with respect to the business climate Russia has taken some steps in the right direction, although the credit crunch will probably stay for the foreseeable future.

Economic policy and the development of defense spending since 2013

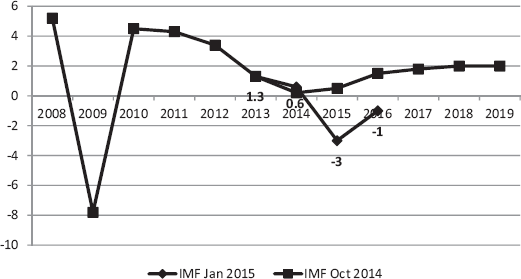

In 2013, Russian growth plummeted to 1.3 percent a year instead of the 2–3 percent forecast. The confidence crisis following Russia's annexation of Crimea in March 2014 and its continuing aggression against Ukraine lowered growth expectations, and in October the IMF (2014) revised its forecast to 0.2 percent growth for 2014, 0.5 percent for 2015 and a recovery to 1.5 percent only in 2016. In January 2015, however, the preliminary result for 2014 was 0.6 percent growth, and the IMF (2015) now projected a contraction of −3 percent for 2015 and −1 percent for 2016. Ongoing Western sanctions, Russian counter-sanctions and the dramatic fall in the oil price had added to the negative trend (Fig. 2).

Economic growth 2000–2019.

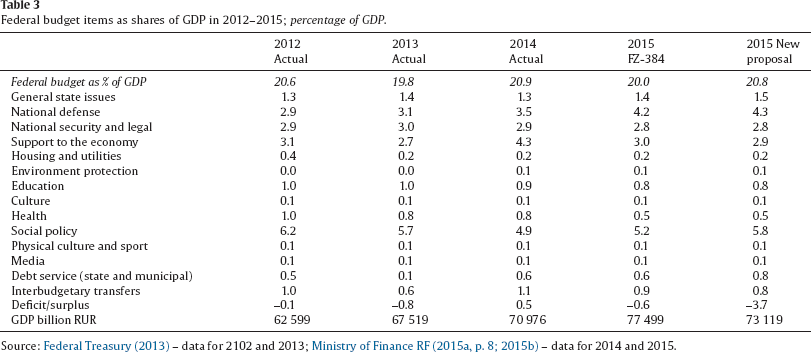

In the initial three-year budget for 2014–2016 there was an aim to reduce the federal budget as a share of GDP from 20 to 18 percent by 2016 (Oxenstierna, 2013, pp. 115–116). Social policy expenditure, which has had high priority since 2009, was to fall from 6 to below 5 percent of GDP. The shares of education and health were also to decline. Defense spending remained at a high level and was planned to rise from 3.1 percent of GDP in 2013 to 3.8 percent by 2016. Fiscal policy during 2013 remained restrained and actual budget expenditures were slightly lower than approved (Oxenstierna, 2013). Table 3 shows the actual federal budget shares for 2012–2014 and here the austerity in 2013 is reflected: the federal budget's share in GDP dropped to 19.8 percent. However, in 2014 the share increased again to 20.9 percent, and in the amendments to the federal budget the aim of reducing the federal budget has been dropped and a share of 20.8 percent is expected for 2015. The share of national defense rose from 2.9 percent in 2012 to 3.1 in 2013 and to 3.5 percent in 2014. For 2015, the budget law implies 4.2 percent and the new proposal 4.3 percent (Table 3). As seen in Tables 3 and 4, forecast GDP in 2015 is much lower in the new proposal: the estimate is almost 6 percent under that in the budget law (Table 4).

Federal budget items as shares of GDP in 2012–2015; percentage of GDP.

Source: Federal Treasury (2013) – data for 2102 and 2013; Ministry of Finance RF (2015a, p. 8; 2015b) – data for 2014 and 2015.

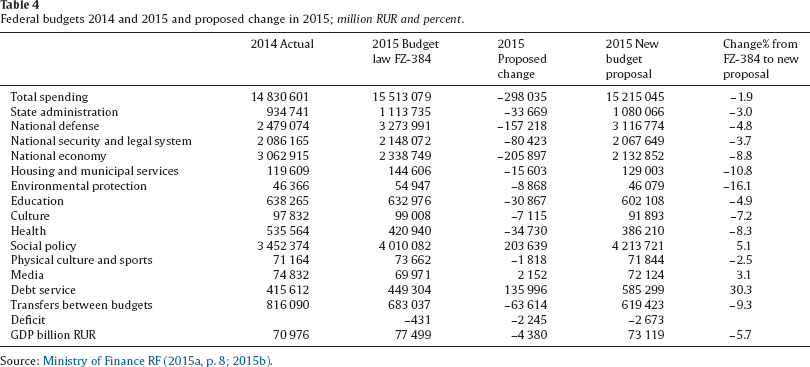

Federal budgets 2014 and 2015 and proposed change in 2015; million RUR and percent.

Source: Ministry of Finance RF (2015a, p. 8; 2015b).

The budget for 2015–2017 was adopted by the Duma in November 2014. The Ministry of Finance had opted for a minimal budget deficit of under 1 percent, and fierce discussions had accompanied the budget process in the government on where the cuts should be made, and not least on how far defense spending could be preserved at high levels when other public spending had to be reduced. In October, Minister of Finance Anton Siluanov (Reuter, 2014) signaled that a new defense program needed to be developed that took into account the changed economic situation, even though the deputy prime minister in charge of the sector had been ruling out any cuts in military spending. 13 This was an echo of his veteran predecessor, Alexei Kudrin, who quit in protest when the rise in military spending was initially proposed under President Medvedev in September 2011. At that time, however, the funding of the military reform and the rearmament program were based on the assumption that Russia would maintain its unprecedentedly high growth rate, of 6 percent per year, throughout the decade. Now times had changed and Siluanov stated quite bluntly, “Right now, we just cannot afford it” (Reuter, 2014). The lower growth due to the dip in oil prices, the halving of the value of the ruble against the US dollar, and the Western sanctions 14 impeding Russian banks’ free access to Western capital markets and restricting exports of advanced technology to Russia, had clearly shattered the hopes of the Minister of Finance for a quick recovery.

Deputy Prime Minister Dmitry Rogozin had previously said that modernization of the military would continue as envisaged by Putin's initial decrees (Putin, 2012a, 2012c). In an interview for the daily Kommersant newspaper, Rogozin had insisted that “The idea is that by 2015 we should have upgraded 30 percent of military equipment, and by 2020 70 percent”. He also claimed that state defense orders could not be transferred “blindly” at the whim of the Finance Ministry – at least not without revising the presidential decrees – and that neither the program nor the funds allocated for it is subject to revision (Reuter, 2014).

One of the more spectacular consequences of the sanctions is that on 25 November 2014, France announced that it had suspended indefinitely the delivery of the first of two Mistral-class amphibious assault ships, which is part of an EUR 1.2 billion agreement between France and Russia signed in 2011 (BBC, 2014).

The discussion continued into 2015 and the Ministry of Finance worked on amendments with budget cuts of up to 10 percent. Different proposals flourished: in some defense spending was to be sheltered, in others not. In the original budget for 2015 the oil price was set at USD 100/bbl. With the oil price going under USD 50/bbl in January 2015, Janes (2015) reported that Russian defense expenditure would be reduced by 10 percent from its intended level in 2015 in the attempt to reduce overall state spending, according to government officials. According to a statement of Deputy Defense Minister Tatyana Shevtsova on 28 January, however, the new measures would not be applied to the state armament program (Janes, 2015). Bearing in mind that Defense Minister Sergei Shoigu had announced a quite substantial reduction of the funding of the next GPV (for 2015–2025) in December 2014, it seemed unlikely that the GPV 2020 plans would be untouched by the budget cuts. 15

The cost of the state armament program up to the year 2025 would drop from RUR 55 trillion to 30 trillion through the development of strategic weapons and equipment types with similar characteristics, Defense Minister Sergei Shoigu said on 19 December 2014 at the enlarged collegium session of the military. “The work has been completed on a type of perspective samples of weapons and equipment, have similar features and specifications. This will reduce the cost of the GPV up to 2025, with 55 trillion to 30 trillion rubles, while maintaining the necessary amount of equipment”, the report said (Global Security, 2014).

Finally, Putin signed a law that would allow the government to finance the budget deficit out of the Reserve Fund in 2015. This is the first time this fund would be used since the global financial crisis (Reuter, 2015). With this backing, the Ministry of Finance could amend the budget and submit a new proposal to the Duma. Table 4 compares the existing budget law (FZ-384) with the new proposed budget. As can be seen, the defense budget has been cut not by 10 percent as envisaged by some observers in January, but by almost 5 percent in nominal terms compared to the original FZ-384. National security – much less discussed but also an item that has had high priority and grown during the Putin era – also sees reductions. Support for the national economy is cut by 8.8 percent in nominal terms, which is quite courageous of the government considering the difficulties Russian companies are experiencing under present circumstances. Furthermore, spending on many of the items that affect the population most, such as the health sector, protection of the environment, education and culture, has been reduced and it may be interesting to see if this has any effect on public opinion. Nevertheless, social policy has got increased funding compared to the old budget, which may be needed when the economy contracts.

For a decade Russia's geopolitical ambitions have been reflected in increased defense spending. However, the failure to modernize the economy and make it less dependent on hydrocarbons and more innovative led to weak growth after 2009, which means that rising defense spending has become more costly to the economy. With the addition of the confidence crisis resulting from the aggression against Ukraine in 2014, the resulting capital flight and the expected contraction of the economy in 2015, the preconditions for further growth of military and other public spending have changed dramatically.

From the study of the federal budget share of defense it is evident that defense still has high priority in terms of a rising share of GDP. Yet defense spending has been reduced in light of the deteriorating economic situation in 2015. Thus there is still a trade-off between defense and other spending in the budget, even though it is evident that other items are being reduced significantly, such as health services, support to the economy and environmental protection. Russian Minister of Finance Anton Siluanov has argued since the fall of 2014 that defense spending must be reduced since at the moment Russia cannot afford this spending and that a new, more realistic defense program had to be developed. Even though the cut in the defense budget has been less than foreseen by the Ministry of Finance, the budget item has been cut by almost 5 percent nominally compared to the November budget. How this will affect the building up of military capability in terms of the armament program and personnel needs to be the subject of a separate study, but we already know that the funding of the new armament program up to 2025 was reduced considerably during the fall of 2014.

The amendments to the federal budget law 2015 imply a higher budget deficit than originally planned and that the government will use the Reserve Fund to finance it. This means that about USD 50 billion will be drawn from the Reserve Fund, which corresponds to about 60 percent of the whole fund. This reduces Russia's fiscal maneuvering room for future years if the economy does not recover or Western financial markets do not open up for Russian state banks.

This study of Russian military expenditure has shown that defense spending as a share of GDP is still on a rising trend, but cuts have been made to it at a time of great economic distress. It follows that defense spending is still high, but it does not have absolute priority and there is still a trade-off between defense and other public spending. However, Russia will have trouble restoring growth and keeping up its military ambitions as long as the economic system is not reformed and productive private economic actors cannot grow. Some improvement has been achieved regarding the business climate in recent years, but the rent management system and the continued maintenance of “Soviet style” producers – “addicts” – in exchange for political support have not been addressed. Rent addiction and the rent management system hinder a thorough institutional reform that could establish “rule of law” and “voice and accountability”, which are two of several important institutional conditions for a healthy economic development.

Acknowledgements

Research for this paper was funded by RUFS, the Russia project at the Swedish Defence Research Agency (FOI), and was also supported by the RUECGRO project “Russian Defence Industry – an Engine for Economic Growth?” which is financed by the Research Council of Norway. I am grateful to two anonymous referees whose comments have helped me to significantly improve the article. I am also indebted to Julian Cooper, Birmingham University, Vasily Zatsepin, Gaidar Institute, and Cecilie Sendstad, Norwegian Defence Research Establishment (FFI), for helpful comments on earlier versions of the paper.