Abstract

The article describes the measures taken by government officials to aid Russia's economy in emerging from the depths of the financial crisis. The authors describe the complexity of this task by focussing on how objective policy-making is complicated by the personal interests of Russian political and business leaders. The political considerations involved in Russian recapitalisation schemes serves as the main political focus in the creation of a desirable recovery strategy. Elements crucial to the recovery of the Russian economy are discussed, including government efforts to support medium and small business, and the unique Russian strategy of dealing with system-forming enterprises.

The main characteristic of the last year—the one that will make it stand out in the economic history of both Russia and the world—is the rapidity with which the current economic crisis developed, as well as the rapidity with which the initial euphoria was replaced by the anticipation of doom. The crisis quickly spread across a country which had been experiencing an especially favourable macroeconomic situation—one with a double surplus (of its budget and balance of payments).

Among the major sources of the crisis, one could single out the following factors: the beginning of global deceleration of economic growth; the fall in the price of oil and other Russian exports; the emergence of a deficit in the balance of payments, which resulted in the country's growing dependence on an inflow of foreign investments; the rapidly increasing external debt of Russian companies and a high probability that they would become incapable of repaying their debts without being helped by the state in the event of a crisis; and the dubious efficiency of many investment projects that had been started on the crest of the boom and were unlikely to survive a trial by crisis. Finally, in the course of its eight years of plenty, Russia produced a generation of politicians accustomed to ‘managing the growth of affluence’ who quickly forgot anything concerned with crisis management Table 1.

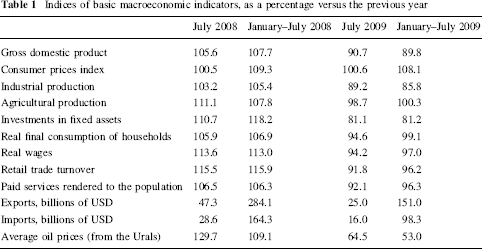

Indices of basic macroeconomic indicators, as a percentage versus the previous year

It should be noted that against the background of a drastic shrinkage in the current accounts of Russia's balance of payments, the problem of their sustainability was further complicated by the huge foreign debt accumulated by Russian corporations, including quasi-public ones (i.e., banks and non-financial companies in which the public administrative bodies and monetary and credit regulators hold, directly or indirectly, more than 50% of the capital or otherwise exercise control over them). According to the Bank of Russia, as of 1 October 2008, the aggregate debt of quasi-public companies amounted to $146.1 billion, including $14.4 billion in short-term (up to 1 year) debt. The aggregate external debt the private sector had accumulated as of the date in question was $351.6 billion, including $87.5 billion in short-term liabilities. So in 2009 national corporations will have to repay $136 billion worth of external debts (including repayment of the principal of the debt and interest payments).

In 2008, the balance of capital accounts slid substantially to $128.4 billion. This was a consequence of the financial turmoil on the global and national markets provoked by the drop in energy prices. The 2008 balance of capital transfers accounted for $6 billion. So apart from capital transfers, the 2008 deficit in the financial accounts amounted to $129 billion.

As in the prior year, the federal administrative bodies likewise were net payers in relation to non-residents. Their external liabilities slid by $7.4 billion resulting from the repayment of Russia's external public debt. The balance of external liabilities of all subjects of the Russian Federation remained unchanged. The liabilities held by the monetary and credit authorities amounted to $4.7 billion. The intensifying global financial crisis sharply diminished possibilities for Russian economic agents to secure (refinance) their overseas borrowings. Consequently, the surplus in the banking sector's liabilities (+$9 billion) plunged by 87.4% compared with the same period of 2007.

The foreign assets of residents (foreign economic agents' liabilities minus those of Russians) grew by $216.5 billion over 2008 (in 2007 they grew by $112.8 billion), with the bulk of the increase being secured by the private sector's operations.

Foreign assets of the federal administrative bodies rose by $2.4 billion, while those of the monetary and credit authorities remained practically unchanged.

Because of the turmoil on the national financial markets coupled with the decline in prices for major Russian exports and, consequently, expectations of a significant depreciation of the national currency, Russian banks in 2008 began aggressively accumulating foreign assets. More specifically, by the end of the year the increase in the banks' foreign assets amounted to $66.4 billion, while the same figure for 2007 did not exceed $25.2 billion.

Thus, as in the previous years, the main factor that determined the value of the worth of current accounts was the balance of trade, whose balance in turn appeared to a significant degree dependent on the dynamics of international markets for energy and other major Russian exports. A decline in price for major Russian exports led to a massive capital flight out of the country. The huge debt that the private sector had accumulated to by the end of the year caused the negative balance of investment earnings to grow, despite the sizeable investment revenues that the monetary and credit regulatory agencies collected from investing the nation's international reserve assets.

Beginning in late August and September 2008, the negative trends on the domestic debt market and the Russian stock market began to be felt more strongly against the background of the deepening financial crisis. Over the past year (2008), the Russian stock index (MICEX) suffered a record drop of 1,287.33 points (from 1,906.86 to 619.53 points, or by more than two-thirds) from its registered value as of the close of trading on 9 January 2008 (in 2007 its growth amounted to 20.16%). Thus in 2008 the stock market, in contrast to the previous year, demonstrated an impressive rate of decline.

The financial crisis has been central to Russia's monetary and credit sphere since September 2008. Up to the end of 2008 the increase in the availability of foreign currency was fuelled by the influx of currency from overseas and its sale by the non-financial sector within the country. This resulted in the rising real effective exchange rate of the rouble—over the year it appreciated by 5.1%, primarily because inflation rates were higher in Russia than in the countries that are Russia's major trading partners. To maintain the exchange rate, the Bank of Russia began selling its foreign reserves. But in September the rouble began to gradually depreciate against the bi-currency basket 1 —this was done in order not to expend all of the Bank of Russia's foreign reserves. The pace of the rouble's depreciation accelerated along with the decline in prices for major Russian exports and with the acceleration of capital outflow. By the end of 2008, the rouble had plunged against the USD from 24.55 to 29.38 and against the Euro from 35.93 to 41.44, while the bi-currency basket rose from 29.67 to 34.81. A rapid decline in exports and the private capital outflow noted in the fourth quarter of 2008 have resulted in the contraction of the nation's foreign reserves for the first time since 1998.

Bi-currency is a working indicator used by the Bank of Russia in its currency policy. It consists of 45% of rouble/euro exchange rate and 55% of rouble/US$ exchange rate.

We should note that the policy of the monetary authorities has undergone considerable changes in 2008. Underpinning these changes were crises on the national financial markets. First, despite problems with liquidity, in 2008 cash balances on the credit organisations' corresponding accounts with the Bank of Russia grew by nearly one-third. The trend is explained by the fact that with the crisis unfolding, the Bank of Russia provided banks with a sizeable volume of financing, particularly on a non-collateralised basis. But facing mounting risks, banks opted to scale back their volume of lending and placed the funds with the Bank of Russia. Second, by the end of the year the volume of credit organisations' compulsory reserves shrank dramatically, as the Bank of Russia had lowered the rate of their contributions to the compulsory reserve fund in order to provide credit institutions with additional liquidity.

In these crisis conditions, it is the Bank of Russia's actions on refinancing credit organisations which has gradually become a major source of shaping the money supply—the practice long in use in most developed economies. In such a situation, interest rates set by the Bank of Russia's credits play a far greater role, since by these means the Bank of Russia can exercise a substantial influence on the situation in the monetary and credit sphere.

Throughout 2008 the decrease in the rate of economic growth was determined by the simultaneous reduction in external and internal demand. The slowdown in the dynamics of investment and consumer demand occurred against the background of the considerable decrease in the volume of goods and services imported. Starting with the third quarter in 2008, a sharp drop in world prices for raw materials and the contraction in global demand was accompanied by the reduction of export volumes both in physical and value terms.

In the current year the decrease in the growth rate can be observed for nearly every kind of economic activity. As compared with the corresponding period in the previous year, from January to April 2009 the contraction in the manufacturing industry reached 14.9%, with declines of 6.4% in mineral extraction and 22.0% in the processing industries. The absolute decrease in the volume of output defined the contraction in demand for the services of the natural monopolies. Freight turnover went down by 17.7%, including a decrease in railway transportation of 24.3%, and electricity, gas and water production and distribution was down by 4.6%.

It should be noted that over the first quarter of 2009 the investments made by medium- and large-scale enterprises decreased in real terms by 4.8%, while the investments of small and other enterprises declined by more than 55%. Because of the curtailment of investment, work in the construction sector declined by 18.4% in the period from January to April 2009, and investment in fixed assets over the same period was only 84.2% of the corresponding figure for the previous year. In the current year there has been a higher rate of decline in foreign investment in the Russian economy as compared with the domestic investments in fixed assets.

The trend for investments in fixed assets to grow at a higher rate than GDP has been observed in the Russian economy since 2002. In 2008 this ratio was sustained, although, as compared with 2007, the growth rates of both GDP and investments in fixed assets have slowed considerably. In 2008 the growth in GDP was 5.6% versus 8.1% in 2007, while investments in fixed assets were up by 9.8% versus 21.1%.

In the second half of 2008, the progressive deterioration in the financial health of economic agents inevitably entailed a decline in budget revenues and put into question the financial stability of the national budgetary system as a whole.

The dynamic of the main parameters of the budgetary system of the Russian Federation in 2008 was substantially different from trends prevailing over the prior year. While in 2007 revenues and expenditures of budgets at all levels were on the rise vis-à-vis their respective figures of 2006, in 2008 changes were in the opposite direction—against the backdrop of the economic crisis the revenues of all levels of government fell fairly significantly to 38.5% of GDP (a decline of 1.7 percentage points vs. 2007) and so did revenues to the federal coffers (down to 22.3% of GDP, a decline of 1.3 percentage points).

The fall in the revenues of all levels of government against the 2007 figures was determined primarily by the contraction of tax revenues (by 0.5% of GDP). 2 It was at the federal level that tax revenues slid most notably (by 0.1 percentage points, down to 21.2% of GDP), while the decline in non-tax revenues (by 0.4 percentage points, to 1.1% of GDP) and uncompensated receipts from other areas of the budgetary system (by 0.7 percentage points, to 0.03% of GDP) 3 have been major factors behind the overall decline in federal budget revenues in 2008. The growth in the revenues of regional budgets is related solely to a 0.8 percentage point rise in transfers from the federal budget—up to 2.7% of GDP (meanwhile, both tax and non-tax revenues were on the decline).

For the purposes of the present analysis, tax revenues include insurance premiums to the compulsory medical insurance scheme and revenues from foreign trade (in compliance with the relevant provisions of the Budget Code of the Russian Federation, these categories of revenues are counted as nontax).

This contraction is related to the fact that in 2007 this revenue item reflected the contribution to the federal budget of additional revenues from YUKOS, while in 2008 there were no such transfers to the budget.

Vectors of change in the volume of expenditures were also different across budgets at different levels. While the federal and regional budgetary expenditures rose by 0.1 and 0.5% (to 18.2 and 15.1% of GDP, respectively) vis-à-vis the 2007 figures, budgetary expenditures of all levels of government, on the contrary, tumbled by 0.4%, to 33.7% of GDP. The rise in the federal and regional budgetary expenditures in 2008 versus the 2007 figures was fuelled mostly by interbudgetary transfers and, accordingly, this rise cannot help but affect the volume of budgetary expenditures of all levels of government.

The rise in federal budget expenditures versus the 2007 figures took place against the background of plunging revenues, which resulted in a shrinking surplus in the federal budget (by 1.4%, down to 4.1% of GDP). Because of the higher levels of growth in expenditures of the budgets of the Russian Federation's constituent parts, the latter ran minor deficits in 2008, which equalled 0.1% of GDP. While the budgetary expenditures of all governments plunged in terms of the share of GDP equivalent, they did so to a far lesser degree than did revenues. This resulted in a substantial decline in the surplus by 1.3%, down to 4.8% of GDP.

Huge oil and gas revenues collected in the prior year provided a substantial financial reserve in the form of a budget surplus, which made it possible for the government not only to fulfil its expenditure obligations but also to replenish the Reserve Fund and the National Welfare Fund. The rise in the federal budget expenditures in 2008 versus the 2007 figures took place against the background of plunging revenues, which resulted in a shrinking surplus in the federal budget.

The Russian authorities offered a number of sufficiently radical measures to soften the crisis. To a certain extent, these measures were similar to those taken by the governments of the most developed countries, but in some important aspects they differed considerably from the initiatives of the latter.

A collapse of the credit system was prevented. Considerable financial resources were allocated to banks in an attempt to overcome the liquidity crisis. Naturally, there were some unavoidable dubious schemes. The banks which received liquidity from the state preferred to convert it into foreign currency as much as they could—in order to insure themselves against currency risks or to repay some of their debts to foreign creditors. From the point of view of economics, this behaviour was quite reasonable, although it did not correspond to the intentions of the monetary authorities who had allocated the funds. Also, there emerged some situations where the re-allocation of state-allocated funds involved bribe-taking, which is not surprising when a resource in short supply is being allocated at an underestimated price. (It was expected that the monies received by primary recipients would be allocated to second-level borrowers not at the market rate but at a much reduced rate, which would only slightly exceed the interest rate at which the initial allocation of funds had been effected.)

The state made a half-hearted attempt to prop up plunging stock markets, but quickly abandoned this initiative. Although the dynamics of stock indexes are breathtaking and dramatic, this is not the sphere where the state's resources should be concentrated today. Any attempt to support the stock exchange in the present situation would mean only one thing: helping the fleeing investors to sell their shares at a higher price and to depart with the money.

Now the situation has changed. There are no available credits, and the securities placed as collateral for credits are rapidly losing value. Of these debts, about $43 billion has to be repaid by the end of the year. The state expressed its readiness to allocate, via the Russian Bank for Development, a sum of $50 billion to eliminate the bottlenecks.

In this crisis situation the state's involvement in the economy remained on a stable high level. Of course, the state has increased its potential to influence the owners of big business because of their significant dependence on one or another form of state support, especially the recapitalisation of their indebtedness. However, the situation with the biggest problem enterprises (Norilsk Nickel, the assets of Oleg Deripaska etc.) shows that the state does not seek to change owners, even when it could easily achieve this purpose by civilised methods.

Finally, the government put forth a broad package of incentives—primarily in the sphere of taxation—which are designed to encourage the development of actual production; these include tax cuts. It initiated a number of measures aimed at supporting small businesses and compiled a list of the system-forming enterprises enjoying special attention from the state. The value of some of these measures is rather ambiguous.

In its anti-crisis policy the Russian government is gradually withdrawing from direct methods of support such as direct public participation in the recapitalisation of problematic private companies and banks, and moving towards stronger indirect control through a small number of banks supported by the government, the formation of preference lists of ‘significant’ enterprises, and through the continued activity of state corporations and state holdings (those few market players which have an opportunity for new mergers) and the inevitable (though these are not as extensive as expected) nationalisation of problem assets as part of its ‘hard’ or ‘soft’ options.

The results of the forecasts for the basic macroeconomic indicators of the Russian Federation, based on several scenarios, suggest that the most probable scenario (the default one) is that Russia has a chance to survive the year with minimal macroeconomic shocks, and that this might form a favourable starting position for exiting from the crisis. But the positive forecast is very unstable, and the range of fluctuations of exogenous parameters under which the situation is favourable appears to be extremely narrow.