Abstract

To cope with demographic ageing trends, the Dutch government has implemented a wide range of institutional reforms. With this, the government has targeted public finances, the risk-taking capacity of the economy and scarce human capital as its main areas of challenge. This paper details the most prominent reforms, looking particularly at social insurance, public pensions and health care. As reforms tighten eligibility criteria and reshape institutions it is to be hoped that the emphasis will shift to capitalise upon individuals’ capabilities rather than to focus on their handicaps.

Introduction

The ageing of the population demands major institutional reforms in social insurance, public pensions and health care. In the Netherlands, the old-age dependency ratio (i.e., the ratio of people older than 65 to those between the ages of 15 and 65) is projected to double by 2040 to around 2:5. As a direct consequence, in the absence of reforms, public spending on health, social insurance and pensions is expected to increase by more than seven percentage points of GDP [2] until then. Containing these expenditures constitutes a major challenge to the political system. Indeed, as the electorate ages, older voters may well block the needed reforms. A conflict then arises between the political power of the older generation, who depends on public transfers, and the economic power of the younger, working generation. Accordingly, the reforms should be announced and implemented sooner rather than later [1].

In the Netherlands, the burden on the public finances of an ageing society was put on the policy agenda in 2000. In that year, the Netherlands Bureau for Economic Policy Analysis–-the official planning bureau of the Dutch government–-calculated the consequences of ageing for public finances. These calculations found that the government should run a substantial surplus of about 1.5% of GDP if it wanted to ensure that current institutional arrangements are sustainable in the future. With this surplus, public debt was expected to fall to zero by 2025. Even though the Balkenende cabinets I–-III (2002-2006) implemented substantial institutional reforms, updated calculations in 2006 showed that an even larger government surplus of 3% would be needed to ensure that current public institutional arrangements are sustainable [2]. This increase of a further 1.5% was due, among other things, to higher life expectancy and lower interest rates. An alternative policy to ensure the sustainability of public finances is to promote greater labour force participation. Although Dutch labour force participation reached a reasonably high level of 74% in 2007, Scandinavian countries report substantially higher rates. The Balkenende cabinet IV (2007-2011) therefore aims not only to cut public expenditures but also to raise labour force participation.

This paper surveys Dutch policies aimed at addressing the challenges posed by an ageing society. The policy reforms with respect to unemployment insurance are described in “the Unemployment and welfare benefits” section. Reforms in disability insurance are discussed in “the Disability benefits” section and health care reforms in “the Health care” section. “The old-age pensions” section explores how the Netherlands has reformed its pension system. In addition to discussing reforms actually implemented by Dutch governments during the last decade, this paper also considers some proposals on unemployment and pensions that were put forward in June 2008 by the Bakker Committee, which was appointed by the government to come up with proposals to raise labour force participation. Indeed, the consequences of ageing, not only on public finances but also for the labour market, are more and more at the centre of the policy debate in the Netherlands. The last section presents our conclusions.

Unemployment and welfare benefits

Between 2000 and 2003, the Dutch government's general budget balance deteriorated by almost 5.5 percentage points of GDP as a result of an economic downturn. Although public spending remained within the spending ceilings through 2002, temporary social expenditure windfalls, on account of strong economic activity during the economic boom at the end of the previous century, were used to finance permanent increases in public spending on health care and education. Among other things, the economic downturn at the beginning of the century raised the number of those claiming wage-related unemployment benefits from 165,000 in 2001 to 320,000 in 2004. In view of both this short-run increase and the long-run budgetary costs of ageing, the coalition agreement in 2002/2003 implemented substantial budget cuts–-especially with respect to unemployment benefits.

In particular, in 2003 the government decided to abolish the so-called follow-up unemployment benefits for the long-term unemployed. At that time, the maximum duration of unemployment insurance benefits (which are not means-tested) was 5 years, but this period could be extended by another two and a half years for people older than 571/2. The abolition of this extension of the maximum duration of unemployment benefits thus served to eliminate the possibility for employers to effectively retire their employees at 571/2 years of age by supplementing their unemployment benefits with relatively small additional transfers. The reinstatement of a job search requirement for older unemployed individuals in 2003 also helped to raise employment of older workers. Furthermore, following a unanimous recommendation of employers and unions represented in the Social Economic Council (SER), 1 the maximum duration of unemployment benefits was shortened from five years to three years and two months. In addition, eligibility requirements were tightened. In view of the impact of ageing on the availability of labour resources, however, several observers argued for further reforms in unemployment insurance in order to raise the quality and quantity of labour force participation by improving the employability of the workforce.

The SER is the most important advisory body to the Dutch government on socio-economic issues. It consists of representatives of employers’ organisations and unions, as well as independent members (known as ‘crown members’).

Consistent with these calls for further reforms, the Bakker Committee proposed converting the current unemployment insurance system into a system of work insurance. The proposed system consists of three phases, which together last a shorter period of time than current unemployment benefits. First, during a transfer period of a maximum of 6 months, the employer will be required to continue to pay the employee while helping that employee to find another job. If the worker has not found a new job during this transfer period, responsibility for finding work for the unemployed worker is transferred to a “Site for Work and Income” (LWI), 2 while the unemployment benefit is paid by the industry concerned. A worker who remains unemployed for more than half a year enters a third phase, during which the municipality participating in the LWI takes over financial responsibility. The proposals enhance the incentives for job seekers to accept work through three channels: first, the duration of wage-linked unemployment benefits is cut; second, job seekers are required to accept a job below their previous income level earlier; and third, employers and municipalities participating in LWIs bear the risk of paying unemployment benefits and thus are induced to help and encourage the worker to find another job.

An LWI is a labour market office in which municipalities and the current administrative body that pays out unemployment benefits (UWV) participate.

Indeed, important elements in the Bakker work insurance proposal are enhanced financial incentives for employers (during the first phase) and the municipalities (during the third phase) to prevent long-term unemployment. The enhanced incentives for municipalities are in line with the successful Social Assistance Act introduced in the Netherlands on 1 January 2004. The Act provides the basis for welfare benefits paid to households that have no other ‘means of existence’. A key aim of the new act was to get more welfare benefit recipients back to work by giving more authority and financial responsibility for benefits to risk-bearing municipalities. Research shows that the stronger financial incentives faced by municipalities have indeed stimulated these municipalities to cut welfare rolls substantially [7].

Disability benefits

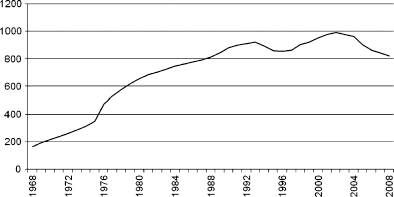

An important benefit programme in the Netherlands is the disability programme, which covers an employee's loss of income due to long-term sickness and disability. Since its introduction in 1967 until the beginning of the 1990s, the number of disability benefit recipients has increased steadily (see Fig. 1). Indeed, disability schemes came to be used increasingly as an attractive route to exit the labour market. Between 1994 and 1996, the number of disability recipients decreased somewhat. This temporary decrease was due mainly to a tightening of the eligibility criteria in 1993–-in particular, the definition of disability–-and to more frequent reassessments based on these stricter criteria. However, the number of disability beneficiaries started to rise again between 1996 and 2003–-even though an economic boom created strong job growth. As a result, the number of disability recipients approached one million (13% of the labour force) in 2003. The disability rate in the Netherlands is among the highest in the world. In particular, women and older workers face a high risk of becoming disabled [4]. With female and older workers constituting an increasing share of the future workforce, the number of disability recipients could be expected to substantially surpass one million recipients during the next decade.

The number of people in the Netherlands collecting disability benefits (thousands)

In contrast to similar public insurance schemes in other European countries, the Dutch Disability Insurance Act (WAO) covered both work-related injury (professional risk) and non-work-related injury (social risk). It also allowed access to the scheme without taking into account the recipient's previous working history. Moreover, employees could apply for benefits as soon as their earning capacity was reduced by only 15% due to long-term sickness or disability. Finally, the disability benefit lasted longer (as long as the disability applied) and was at least as high as other social security benefits (such as the unemployment insurance benefit and social assistance). All of these factors explain why disability insurance became a very popular arrangement for early retirement during the past few decades. The government tried to reduce benefit levels in 1993 not only by tightening the eligibility criteria but also by limiting the duration of wage-based benefits. This latter measure was ineffective, however, because social partners agreed to take out additional (private) insurance policies to insure against the tighter criteria in the public insurance scheme. The number of disability benefit recipients therefore continued to increase at the end of the 1990s.

At the beginning of 2001, a group of experts was commissioned. This group's recommendations (the “Donner proposals”) were based on the premise that maintenance and use of available labour capacity should have the highest priority, and that the main responsibility for ensuring this rests with both employers and employees. In September 2003, the coalition agreement of the Balkenende cabinet I included a major regime change in disability insurance, mainly based on the Donner proposals [9]. The government intended to limit eligibility by tightening entry conditions and reducing benefit levels for the partially disabled. People who are partially disabled (with a degree of disablement of at least 35%) or who face a good chance of recovery can either collect a supplement to the wage they are earning (if they are working) or qualify for an unemployment benefit (if they are not working). After expiration of the unemployment benefit, the benefit equals the share of the social minimum income level that corresponds to their degree of disability. Those employees who are partially disabled with a degree of disability less than 35% no longer have access to disability benefits and must make their own way through the labour market, preferably with the same employer as before. Moreover, applications for disability benefits are subject to a more rigorous screening of the loss of earning capacity, and the primary responsibility of employers and employees for limiting absence due to illness is extended from one to two years. The new Disability Act (WIA) was implemented on 1 January 2006, while the enhanced responsibility of employers and employees for limiting absence due to illness was in force from 1 January 2004 and the more rigorous screening of the loss in earnings capacity started on 1 October 2004. 3 There is another new element in the system: for insuring partial disability employers can choose between private insurance (based on experience rating) or public insurance (not based on experience rating). As a result of these measures, the number of disabled persons has dropped in recent years (Fig. 1). 4

Disabled persons with a benefit who collected this benefit before July 2004 and who were younger than 50 in July 2004 were also subject to more rigorous screening. In the coalition agreement of Balkenende IV, the age of 50 was lowered to 45.

The smaller inflow was also caused by the gatekeeper improvement act of 2002. This act put more requirements on both the worker and his or her employer to do their utmost to reintegrate the worker. Only if these requirements were met could the worker become eligible for disability benefits.

New concerns have recently arisen, however, about an increasing number of disability benefits for handicapped young persons without any work history. The present government has proposed additional measures to contain this rise by encouraging young people with a handicap to work–-if necessary in an adapted work environment with job support, in which the disability scheme supplements earned income. Indeed, the focus should be on what people can still do instead of what they cannot do. Moreover, income protection for vulnerable people should not discourage young people from work.

Health care

The Dutch health insurance system is divided into three pillars. The first pillar is compulsory national health insurance (AWBZ). The AWBZ provides coverage to the whole population against catastrophic risks such as hospital care exceeding one year, nursing homecare and institutional care for mentally and physically handicapped persons. It accounts for about 44% of total health expenditure [8]. Up to a certain income level, the AWBZ premium is income-related. The second pillar is the basic health insurance scheme, which covers physician services, hospital care (up to one year), prescription drugs, essential dental care and some physiotherapy, and comprises about 53% of health expenditure. In 2006, a major reform took place in the second pillar, allowing private health insurance companies to compete on price and quality. The premium for (most) employees is neither income-related nor risk-rated, with a compulsory deductible of €150 per person. Finally, the third pillar consists of luxury health services such as hotel services within a hospital, luxury dental care and prolonged physical therapy. The premium is risk-rated. This pillar is rather small, accounting for only 3% of total health expenditure.

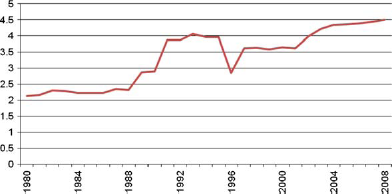

From the point of view of an ageing society, the first pillar is especially important. In recent years, the expenditure on nursing homecare has accelerated. As a percentage of GDP, AWBZ expenditures have doubled since the 1980s (Fig. 2).

AWBZ care costs as % of GDP

Moreover, in the absence of further policy measures, AWBZ spending is projected to rise to 6.4% of GDP by 2020. In addition, the care sector already suffers from staff shortages. According to projections of the Ministry of Health, Welfare and Sport, 500,000 additional employees will be needed in the care sector in 2020, while aggregate labour supply is expected to increase only slightly during this period.

Recently, the SER recommended some fundamental reforms to the AWBZ aimed at improving efficiency, increasing both competition and decentralisation in care delivery and strengthening the position of the patient more generally [6]. First, in order to target AWBZ care towards catastrophic health problems, eligibility criteria for AWBZ care should be tightened. In particular, claims should be assessed on the basis of objective medical protocols. Second, the current AWBZ claims geared towards social support should be taken out of the AWBZ and transferred to municipalities (on the basis of the Social Support Act). If they bear the risk of this support, the municipalities will have incentives to contain spending–-for example, by providing support on a means-tested basis. Third, temporary care related to medical interventions aimed at curing should be transferred to the second pillar of health insurance. Fourth, the financing of care should be separated from the financing of housing, so that accommodation is no longer reimbursed by the AWBZ. Institutions should thus charge rent separately. By unbundling housing and care, this reform is expected to give rise to more innovative combinations of housing, medical care and personal services. Indeed, the elderly can be expected to have more freedom of choice with regard to where they receive long-term care so that they can remain in their familiar surroundings longer. Related to this, SER favours a fundamental shift away from the current supply-side financing to more demand-oriented financing. In particular, resources should follow the choices of the patients by flowing to the health providers that are selected by the clients. We believe that the central position of the client can be best implemented through a voucher system, which offers substantial freedom of choice and good steering possibilities for individuals [10]. Currently, the Dutch government is discussing the Council's proposals in order to make the AWBZ more “ageing proof”, especially now that AWBZ spending is increasing rapidly.

Old-age pensions

As with health insurance, the Dutch pension system consists of three pillars. The first of these pillars is the AOW, which is the basic minimum pension provided by the government to all residents. The second pillar involves occupational pension schemes, which are part of collective labour agreements. The third pillar comprises individual provisions. In pension insurance the third pillar is also relatively small. We thus focus on the first and second pillars.

Public pensions

The AOW is the public pension scheme and was introduced in 1957. It provides a flat-rate pension benefit, which is related to the net minimum wage for all residents of the Netherlands from the age of 65. 5 The AOW is a mandatory insurance scheme financed on a pay-as-you-go basis. To finance the AOW, people below the age of 65 pay AOW contributions over their income up to a certain income ceiling. Benefits are not means-tested. Due to population ageing, the costs of the AOW are projected to rise from 4.7% of GDP in 2006 to 8.8% of GDP in 2040 [2].

A single household is entitled to a benefit of 70% of the minimum wage, while an individual living in a two-person household receives 50% of the minimum wage.

The Bakker Committee proposed two main avenues for addressing this burden. The first involves gradually increasing the retirement age at which people become eligible for a public pension. Commencing no later than 2016, the age at which people can start to draw their state old-age pension would be raised by 1 month each year, in line with increased life expectancy. By 2040, the state pension age would then be 67. An alternative route to cut spending would be to individualise the basic pension scheme, so that everyone above 65 years of age receives 50% of the minimum wage, irrespective of the household type. Single households with low incomes would then be compensated by the means-tested social assistance scheme.

The second route proposed by the Bakker Committee involves funding the state old-age pension from general taxation. This broadens the base for financing the pension because not only would those younger than 65 (who currently pay the AOW premium) pay taxes, but so would those older than 65. Indeed, as a result of this proposal, the elderly with supplementary pension income from the second pillar would pay additional taxes on their pension benefits. 6 As of 2011, the state old-age pension would gradually be funded completely from general taxation over a period of 15 years (people born before 1946 will be exempt). After the new system has been phased in completely, people would have to work approximately one year longer to compensate for the higher tax burden on their pensions. A possible alternative route for reducing the burden of the AOW on those younger than 65 years of age is to pay tax credits out of general tax revenues (which are paid by all age categories) rather than out of AOW premiums (which are paid only by those younger than 65) [3].

In fact, citizens presently older than 65 years of age already contribute to financing the AOW. The reason is that the contribution rate levied on those younger than 65 has been fixed since 1999. With the ageing of the population leading to increased spending, a deficit has emerged. This deficit is financed from tax revenues. Seniors also contribute to these taxes and are thus going to pay an increasing share of pay-as-you-go pensions.

Most Dutch political parties are not yet in favour of a higher eligibility age for the public pension or of financing public pensions only out of general taxation. The current cabinet has plans for raising taxes on occupational pensions only for those who did not work up to the age of 65. A possible alternative to the proposals of the Bakker Committee is to cut public spending on categories other than AOW spending. The budgetary savings could then be used to cut public debt and thus reduce interest payments. Just as in the case of raising the eligibility age for the AOW system, however, cutting down public debt by running substantial surpluses provides a big challenge to the political system, and no political party has thus far come up with concrete proposals to completely eliminate the so-called sustainability gap in this way. An important advantage of raising the eligibility age of the AOW pension is that it yields a double dividend by not only enhancing the financial sustainability of the public finances but also by raising aggregate labour supply, thereby addressing the looming staff shortages in the health care and education sectors.

Occupational pensions

Occupational pension schemes supplement the flat public benefit for workers who earn more than the minimum wage. These schemes are thus earnings-related, and cover about 90% of the labour force. The pension scheme is part of the labour contract, which is typically negotiated between unions and employers in collective agreements. Up to a certain ceiling, these pension savings are eligible for consumption tax treatment: premiums are deductible for income tax (and the AOW premium), returns are tax exempt and benefits are taxed (although these benefits are exempt from the AOW premium if the beneficiary is older than 65). The occupational schemes are funded and the value of assets in these schemes currently amounts to about 125% of GDP. Industry-wide pension funds are organised for workers in a specific sector of the economy. These sectoral funds own more than two-thirds of the assets in the second area and account for more than 80% of the active participants.

The occupational plans are run like defined-benefits plans, which aim at a certain annuity level during retirement. Years of service and a reference wage typically determine the benefit entitlement. The reference wage used to be the final wage, but in recent years most funds have moved to career-average schemes. In these schemes, entitlements to deferred annuities accrue based on a percentage of the average wage level during a career. These schemes typically aim at an annuity level of about 80% of average pay (including the flat public benefit) after 40 years of service. This corresponds to an accrual rate of about 2% per year.

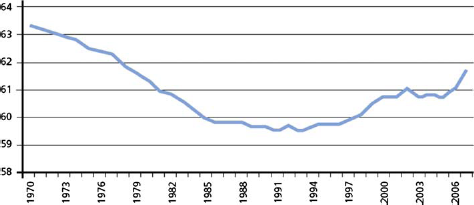

Early Retirement Schemes (VUT) are separate from occupational pension schemes and are financed on a pay-as-you-go basis. They were introduced in the early 1980s as a means of combating youth unemployment. In view of the increasing costs for employers as a result of the ageing workforce, some reforms were implemented. In particular, replacing VUT schemes by funded early retirement schemes encouraged higher labour force participation because, contrary to VUT schemes, pre-funded early retirement schemes are actuarially fair. Older workers are faced with the costs of retiring early in terms of a lower pension benefit: workers can retire earlier with a lower pension, or can retire later with a higher pension. The next step to discourage elderly workers from retiring early was to gradually eliminate tax benefits for early retirement schemes and VUTs. Moreover, during the phase-out period, these schemes continue to be eligible for tax benefits only if older workers are rewarded for retiring later by receiving an actuarially fair higher pension benefit. These reforms have had a large impact on the labour participation rate of the elderly. While the participation rate for the group between 60 and 64 was below 10% around 1995, it is projected to increase to close to 50% by 2011 (Fig. 3).

Average retirement age, 55-64 years

To help phase out the early retirement culture in the Netherlands, the Bakker Committee proposed further reforms, consisting of three steps. The first step is to introduce a tax bonus for elderly persons who continue to work, which would be financed from higher taxes on supplementary pensions. The second step is to lower tax benefits of private pensions. In particular, the maximum accrual rate for tax-favoured career-average schemes should be cut from 2.25 to 2%, in part to create budgetary room for providing tax benefits to the life-course saving scheme, which can be used to finance or supplement income in case of income loss at any point during the life cycle [5]. The last step is to correct annuities for increased life expectancy so that individuals bear the risk of higher life expectancy at retirement. As life expectancy increases, workers face the choice between working longer or collecting lower pensions.

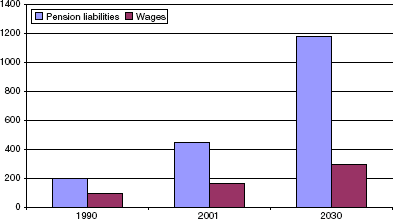

Funded systems are vulnerable to an ageing population not only because of increased longevity but also because risk sharing has become more difficult. In particular, the ageing of the members of the funds expands the obligations of the funds in relation to the premium base (Fig. 4). This implies that unanticipated shocks in financial markets and longevity require larger changes in pension contributions in order to shield pension rights from these shocks. Guaranteed pension obligations have thus become more expensive in that they result in greater volatility in payments from the contributors.

Liabilities and premium base of Dutch pension funds, 1990-2030

In the face of these developments, pension funds in recent years have more moved to aspired annuity levels rather than guarantees. In particular, the pension funds aim to index the pension rights to prices or wages, but this indexing is not guaranteed. In particular, indexing is conditional on the financial performance of the fund. One can thus view the current occupational pension system as a hybrid system of guarantees and ambitions; nominal annuities are guaranteed, but the degree to which pensions rise in line with prices and wages depends on the performance of the investments of the pension funds.

Through the shift from final-pay to career-average systems with conditional indexation of nominal pension rights, pension funds have made the indexation of the pension rights of not only already retired members but also active members conditional on the financial performance of the pension fund. These reforms have thus strengthened the steering capacity of the indexing instrument because the indexing of all accrued liabilities (including the entitlements of active members to deferred annuities) now depends on the solvency position of the fund. As a result of these reforms, the active working population absorbs more risks in terms of their pension rights. Moreover, members (rather than participants and employers who pay the pension contributions) have become the main risk bearers of the fund.

Conclusions

Over the past decade, the Netherlands has implemented major reforms in social insurance, health care and pensions. The Dutch systems in these areas are traditionally characterised by hybrid systems in which both private and public responsibilities play a role. In recent years, more tasks of the welfare state have been delegated to private parties. In particular, private insurance companies play an increasingly important role in disability and health insurances. Moreover, as the private occupational pension sector matures, private pensions account for an increasing part of pension benefits.

Another important trend is a shift towards more competition in social and health insurances and the delivery of health services. This is being accomplished by giving individuals more freedom to choose; for example, in selecting their own health care provider or health insurance company. In addition, employers can choose how they want to deal with the risk of disability and sickness leave. Within the public sector, responsibilities are increasingly decentralised to risk-bearing municipalities; for example, in social assistance, labour market policies and social services provided to the elderly population. This allows more tailor-made policies that prevent moral hazard on account of conditions that are difficult for the central government to verify. In private disability and health insurances, individual employers and workers are taking on more risk in order to combat moral hazard and contain spending pressures that result from ageing.

A major remaining challenge facing the Dutch economy is to increase labour supply, as an ageing population is expected to result in labour shortages in non-tradable sectors that produce and maintain human capital and are to a large extent publicly financed (such as the education and health care sectors). Indeed, the major problems resulting from ageing involve not only the sustainability of public finances and the reduced risk-taking capacity of the economy but also the possible scarcity of human capital. To contain possible cost rises in the public sector and a loss of international competitiveness in the private sector as a result of wage pressures, policymakers should continue to improve further the flexibility of the labour market for elderly workers so that the talents of these workers are better used.

In this respect, the proposals of the Bakker Committee to increase the financial responsibilities of employers and employees for maintaining the employability of the workforce are welcome. By giving decentralised parties more responsibilities for unemployment insurance and the maintenance of human capital, these proposed reforms build on the successes of recent reforms in disability insurance and social assistance. In line with the Bakker proposals, the possible uses of the life-course saving scheme should be extended so that individuals not only face more responsibilities for investing in their human capital but also obtain more instruments for maintaining their employability. These life-course savings are transferable across jobs and thus help to transform job security into work security, thereby enhancing the flexibility of the labour market for the elderly. This will help to further raise the effective retirement age, which is the most powerful instrument to protect labour supply in the face of the upcoming shortage of staff in several key sectors of the ageing Dutch economy.

Footnotes