Abstract

The level of stock prices on capital markets no longer reflects only the financial health of companies, and investors do not carry out their investment decisions based on classical fundamental analyses using accounting information. The level of the diminishing role of accounting information for investment decisions was proven by Lev and Zarowin with a sample of 1,300 companies during the years 1976 – 1996. This paper further extends this analysis and verifies the validity of the original findings until the year 2011. The low importance and impact of accounting information was confirmed in the period 1994 – 2011, but the decline in importance significantly slowed down or in some cases even stopped completely. Surprisingly, the association between stock price and change in book value plus earnings has been found to be significantly improving. This trend should be subjected to further analysis.

1. Introduction

While investors and regulatory agencies seek to improve the quality and reliability of accounting information, it seems that in today's dynamic global business environment, the usefulness of information derived from financial statements is limited. Today's accounting information is seen as not adequately reflecting the change of economic and operating conditions of companies. Moreover, the accounting profession's credibility has been significantly hindered by a series of ethical failures [1]. At the same time, reliable information on companies plays a key role in business management and financial planning not only for investors, but also other stakeholders – suppliers, lenders, employees, customers, and the public. Besides accounting documents, which companies are legally obliged to disclose, there are other sources of financial information which may influence potential investors' decisions, such as corporate credit ratings which are believed to have a significant potential to influence market opinions on a subject [2]. However, if the available accounting information is insufficient and investors are unable to acquire the missing information from alternative sources at zero-costs, such situation would imply larger transaction costs and information asymmetry, and ultimately result in a decrease of the welfare of investors and firms [3].

Lev and Zarowin [3] proved that there has been a systematic decline in the usefulness of financial information to investors over the past 20 years, as manifested by a weakening association between capital market values and financial attributes. In their paper the authors examined the changes of usefulness of earnings, cash flows and book values over the time period 1977 – 1996 with respect to corresponding stock returns. These were the years when huge business changes affected the majority of companies such as globalization of business operations, the outset of many high-technology industries and vast worldwide deregulations. However, since that time, the economic environment has further developed in terms of both internal processes and external factors influencing firms' competitiveness, which raises the necessity of reviewing the current state-of-the-art. The main goal of this paper is to verify the timeliness of past findings on this subject.

On a constant sample 1 of 1,300 firms with data in each of the 20 years examined, Lev and Zarowin [3] showed that the association between stock returns and earnings, as measured by adjusted (R2), 2 has been declining throughout the period 1977–96 from R2s of 6–12% during the first 10 years to R2s of 4–8% during the last 10 years of the sample.

The estimated slope coefficients of the examined variables 3 have been decreasing during the period 1977–96, from a range of 0.75 – 0.90 in the first five years to 0.60–0.80 in the last five years of the sample. A regression of the annual slope coefficients on time confirms that the ERC's decline was statistically significant. The declining slope coefficients of earnings complement the deductions based on declining R2s. While the declining R2s might be caused by an increasing importance of non-accounting information with no change in the informativeness of the earnings on a stand-alone basis, both together point to a declining usefulness of the income statement information.

The association between operating cash flows and stock returns, as measured by R2, was not noticeably stronger than the association between earnings and returns. That is even in accordance with the declining association between stock prices and earnings + book value, as measured by R2, which decreased during 1977–96, from R2 levels of 0.90 in the late 1970s, and 0,80 in the 1980s, to 0.50–0.60 in the 1990s. A regression of annual R2s on a time variable showed a negative and statistically significant time correlation. This technique is not sensitive to changes over time in the quality of the analysts' earnings forecasts because it does not measure the reaction to reports' announcements.

Collins, Maydew and Weiss [4] estimated the regression over the period 1953–93 and reached the conclusion that the combined value relevance of earnings and book values has not decreased. The source of disagreement appears to lie in the periods examined. Though the association between stock prices and earnings + book value may have been stable over the past 40 years, Lev indicates that the informativeness decreased in the later part of the period.

The timeliness between financial indicators and financial data was also investigated by Francis and Schipper [5], Ely and Waymire [6], Ramesh and Thiagarajan [7], Chang [8], and Brown, Lo, and Lys [9]. All these studies report a weakening returns-earnings association when the association is measured by R2. The overall results support a systematic decline in the usefulness of financial information to investors as demonstrated by a weakening association between market price and key financial variables over the 80s and 90s.

Declining informativeness may be explained by two major reasons. Accountants need to deal with evermore-challenging areas such as consolidations, leases, mergers, R&D, price-level changes and taxation charges. In other words, one of the most important reasons for the declining usefulness of accounting information may be changes initiated from within and from outside of the organization which ultimately result in increased uncertainty. The second major reason is the fact that accounting lacks an all-embracing theoretical framework, which means dissimilarities in practices have evolved.

2. Methodology

We follow the usefulness assessment procedure as proposed by Lev and Zarowin. They examined the association between capital market values and key financial variables - earnings, cash flows, and book values over the time period 1977–1996. This study thus attempts to update this research to current conditions and test the usefulness of financial statement information in the period 1993–2011.

2.1 Earnings-returns relation

The first analysis tests the usefulness of reported earnings, using a regression to estimate the association between the annual level and change of earnings and stock returns: 4

where:

Rit = firm i's stock return for fiscal year t.

Eit = reported earnings before extraordinary items of firm i in fiscal year t.

ΔEit = annual change in earnings: ΔEit = Eit- Eit-1, proxying for the surprise element in reported earnings.t = 1994–2012

Both Eit and ΔEit are scaled by firm i's total market value of equity at the beginning of year t. The significance was then measured by a regression of yearly coefficients of determination to the time variable.

2.2 Cash flow-returns relation

Investors and creditors may receive cash only when the company owns cash or its equivalents. Therefore, investors devote their time to studying the relationships between timely different revenues and costs that occur in financial statements and corresponding cash flows from sales and expenditures. For a company that lasts for a long time, it does not matter in which period the actual cash flows occur. However, especially creditors know very well that credits are paid in cash. Therefore, they want to know whether the company is able to produce cash in amounts that is sufficient to pay interest and debts, pay rents, and maintain competitiveness without qualms. Investors are interested in cash flows for many reasons. One of them is a flow of dividends, which is paid in cash and represents a part of returns on investment. Although it does not have to be apparent at first glance, the association between dividends and cash flow is much higher than association between dividends and earnings. One of the reasons for this is the variability and fluctuation of earnings which is higher than in the case of cash flows, as companies try to pay constant dividends. The decrease in dividends is usually not caused by reasons that lead to a temporal decrease in earnings. The dividends are often paid also in times of two year deficits. However, dividends are not paid in the case of a decrease in cash flows to the extent that it would threaten the debt service and capital expenditures. It is therefore possible to say that a forecast of future dividends depends on the analyst's expectation of future cash flows, stemming from a company's operations and necessary cash outflows. Cash flows are often claimed to have a higher informative value than earnings also because they are less prone to managerial manipulation than accrual earnings, and because they are less influenced by questionable accounting guidelines.

In order to confirm this claim we estimate the following regression:

where:

CFOit = Cash flow from operations of firm i in a fiscal year t.

ΔCFOit = Annual change of cash flow from operations of firm i in a fiscal year.

ACit = Accounting accruals of firm i in a fiscal year t.

ΔACit = Annual change of accounting accruals of firm i in a fiscal year.

εit = Standard error, proxying for surprise element in reported earnings.

t = 1994–2011

Two independent variables in (2) are scaled by the beginning-of-year market capitalization. Regression (2) thus estimates the relationship between annual stock returns and operating cash flows.

2.3 Earning + book value relation

It has become popular among scientists according to Lev and Zarowin to study this association.

where:

Pit = share price of firm i at end of fiscal year t,

EPSit = earnings per share of firm i per year t,

BVit = book value per share of firm i at end of year t,

εit = other value-relevant information of firm i for year t apart from earnings and book value.

t = 1994–2012

Regression (3) thus estimates the relationship between earnings plus book value and price of the stock. The results suggest that this relationship is the most significant of these three.

3. Analysis

As suggested by Lev [3], the usefulness of accounting statement information was decreasing over the period 1976–1996. We follow this concept and test this conclusion dating from 1994–2011. The conditions are set in a very similar way to make them comparable.

3.1 Earnings-returns relation

Our first analysis examines the usefulness of reported earnings, using the following cross-sectional regression to estimate the association between annual stock returns and the level and change of earnings.

Both Eit and ΔEit are scaled by firm i's total market capitalization at the end of year t.

Table 1 (Panel A) presents estimates of regression (1) for each of the years, 1993 – 2011 (1993 is “lost” due to the first differencing of normalized earnings). The sample contains 105 firms per year with data in each of the 18 years examined. Panel A of table 1 presents the association between stock returns and earnings, as measured by adjusted 5 R2. 6 It shows high variability between the observed coefficients of determination. It indicates that reported earnings explain changes in stock returns of about 6%. This figure does not show any hint of the decreasing usefulness of financial analysis.

The Association between Earnings and Stock Returns

A regression of the annual coefficients of determination in panel A on a time variable in panel B confirms no development (positive or negative) of association between stock returns and reported earnings as the change is statistically insignificant.

(The p-value is 0.74 and R2 −0.05) 7 These results are similar to the results obtained by Lev and Zarowin. Their measured association was 6–12% in 1976–1986 and 4–8% in 1987–1996. Our results (6% on average in both periods 1994–2003 and 2003–2011) therefore indicate that the decrease of this association has stabilized at a very low level.

Graph 1 demonstrates the development of usefulness as measured by adjusted R2 between stock returns and level of earnings plus change of earnings.

Development of usefulness as measured by adjusted R2 between stock returns and level of earnings plus change of earnings.

3.2 Cash flow-returns relation

The second analysis of Lev's model examines the usefulness of reported cash flows from operations and accounting accruals, 8 using the following cross-sectional regression to estimate the association between annual stock returns and the level of cash flows and accounting accruals, and its change, respectively.

All four independent variables are relative to firm i's total market capitalization at the end of year t. Regression (2) thus estimates the association between annual stock returns, on the one hand, and operating cash flows plus accounting accruals on the other hand. Table 2 reports yearly coefficient estimates of this regression.

The Association between Cash Flows from Operations

Our results suggest that the association between operating cash flows (plus accruals) and stock returns, as measured by R2, is slightly stronger than the association between earnings and returns (R2s in table 1). As to the pattern of the temporal relationship, the regression indicates that the reported cash flows from operations plus annual accruals explain changes in stock returns of about 13%. Moreover, it suggests that the usefulness of cash flows and accrual in explaining changes in stock returns has declined by 1% throughout the examined period 1994–2011. It has declined from a mean of R2 0.13 in the first nine years to R2 0.12 in the following nine-year period. Nonetheless, neither association between stock returns and cash flows plus accruals is statistically significant at the 0.05 level (see the time regression in panel B of Table 2).

Notice that the association between cash flows plus accruals and stock returns is higher than the association with earnings. Cash flows are often claimed to be more informative than earnings because they are less subject to managerial manipulation than accrual manipulation and because they are less affected by accounting principles, such as expensing on intangibles.

Graph 2 demonstrates the development of usefulness as measured by adjusted R2 between stock returns and level of cash flows plus accruals and their changes.

Development of usefulness as measured by adjusted R2 between stock returns and level of cash flows plus accruals and their changes.

3.3 Earning + book value relation

Our third test of informativeness over time based on Lev and Zarowin's results concerns the relationship between stock price and earnings per share plus accruals. It has become popular among scientists and several researchers have studied this area.

Lev [3] and other authors document the weakening association between stock price and earnings plus book value over the period 1970–1999. Collins, Maydew and Weiss [4], and Francis and Schipper [5] on the other hand claim that the association has not decreased. The source of inconsistency lies, according to Lev, in the periods examined. Lev examines the period 1977–1993, while Collins, Maydew, and Weiss [4] consider a longer period, from 1953 to 1993. After time adjustment, Lev confirms that the association was decreasing during the period 1977–1993, but was stable or increased during the period 1953–1977.

Regression (3) in our research estimates the association between annual stock returns and earnings plus book value, as measured by R2.

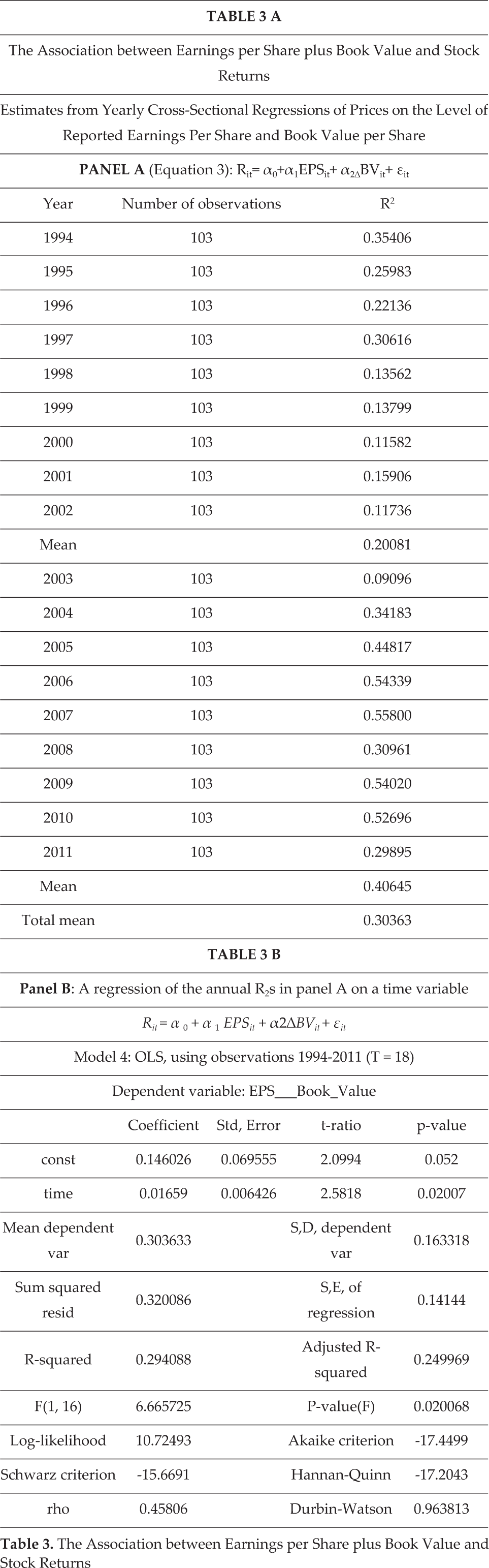

Our results (Table 3) suggest that the relationship between stock price and book value plus earnings per share is stronger 9 than in case of net total earnings or cash flows. The coefficient of determination varies by up to 55% in 2007. As to the pattern of the temporal relationship, the association has increased thorough the examined period 1994–2011. It has increased from an average of R2 = 0,20 in the first nine years to an average of R2 = 0,41 in the following nine years and the explanatory power of the book value and earnings increased almost monotonically from the year 2001. This increase is significant to a 99% level of confidence (see the time regression in panel B of Table 3).

The Association between Earnings per Share plus Book Value and Stock Returns

The increasing usefulness of these criteria is in contradiction to Lev's conclusion about decreasing informativeness. As Collins, Maydew and Weiss [4] reported, not decreasing (or increasing) the association between these attributes in the period 1953–1993, it might be the case that the relationship is influenced by cycles. Or it might just be that the informativeness of the book value and earnings has improved over the time.

Graph 3 demonstrates the development of associations measured as adjusted R2 between the stock price and the change in the book value of the stock and the average level of earnings.

Development of associations measured as adjusted R2 between the stock price and the change in the book value of the stock and the average level of earnings.

4. Conclusion

Economic and financial planning in a long-term outlook is an integral part of business management and is becoming critical for coping with the fast changing business environment of a globalized economy [11]. However, planning necessitates reliable and timely information including accurate data on accounting indicators and the financial performance of companies. At the same time, the extent to which investors rely on accounting information, as well as how this information captures the overall change, is the subject of academic debate. In this article, we examined the role and usefulness of accounting information for investment decisions.

Lev and Zarowin have documented the declining usefulness of earnings and operating cash flows during the period 1977–1996. This usefulness, especially in hi-tech industries, was found to be at a historically low level and continued to decline as disclosed financial statements were becoming less relevant to capital markets. After thoroughly examining the associations, we reject the hypothesis of the declining usefulness of financial information, in the case of the association between stock returns and earnings and cash flows respectively, to a 95% level of confidence. However, this might be only a consequence of an already very small explanatory role (6%) of earnings in the change of stock returns in the same year for reasons that we will explain in our later studies. Our assessment of this association corresponds to the findings of Lev and Zarowin.

Surprisingly, the association between stock price and changes in book value plus earnings has been found to be improving and this trend is statistically significant. On top of that, the development is temporally increasing, which is in contradiction to our original assumption. We do not aim to derive any conclusion about this, but the increasing trend is indisputable, significant and should be a subject of further analysis. In other words, our analysis revealed that further analysis is warranted. Care should be taken in drawing broad conclusions about the declining relevance of financial statements to financial markets.

All companies are facing technological change from within and outside of the company which ultimately results in increased uncertainty. Issues concerning the information content of accounting statements and other publicly disclosed documents have created important policy issues. In particular, insufficient or incorrect information could affect the allocation of capital to firms. Information asymmetry, such as a situation where insiders (fund managers) exploit their private (internal) information before uninformed capital market participants register the right information, will result in an inefficient redistribution of wealth. Last but not least, uninformed capital market participants (investors) may waste scarce financial resources as they seek to acquire the additional information.

The constant sample consists of enterprises which were present on the NYSE for the entirety of the examined period, 1976–1996.

Adjusted R2 = Coefficient of determination. It indicates how much a dependent phenomenon is explained by independent variables.

Earnings, operating cash flows and earning+book value.

Nonearnings accounting data (e.g., inventories, R&D, capital expenditures) increase the explanatory power of financial information with respect to stock returns to 15–25% [10]. We test this in an Ou and Penman model. In order to be able to compare the temporal development of the usefulness of the accounting information, we must follow the Lev model as performed in 1999.

All coefficients of determination (R2) in this work are adjusted coefficients of determination

Adjusted R2 = Coefficient of determination. It indicates how much a dependent phenomenon is explained by independent variables.

Because R2 is defined as the proportion of variance explained by the fit, if the fit is actually worse than just fitting a horizontal line then R-square is negative.

According accruals understood as the difference between reported earnings and cash flow from operations.

No conclusion should be made about comparisons to other results as price is a status (absolute) variable in contrast to stock returns which is a flow variable