Abstract

Saudi Arabia's petrochemical sector accounts for a significant portion of non-oil exports and has the potential to contribute significantly to the Kingdom's diversification. In this study, Autometrics—a machine learning method, was first employed to estimate export equations of chemicals and rubber-plastics for 1993-2020. The estimated equations were then integrated into a macroeconometric model called KAPSARC Global Energy Macroeconometric Model (KGEMM) and a scenario analysis was performed for the diversification effects of foreign and domestic price shocks till 2035.

The scenario analysis showed that a 10% increase in foreign prices leads to 0.40 percentage point and 0.13 percentage point more diversified exports and economy on average for 2023-2035. Regarding domestic prices, a 19% increase in industrial fossil fuel prices and a 10% increase in ethane price result in less than a 0.1 percentage point contraction in the diversification of exports and economy if the revenues from the price reforms are not recycled back to the economy. The reforms can boost economic diversification by 0.05 percentage point if the revenues are recycled back to the petrochemical sector as an investment. If domestic price reforms are coupled with the investment in the petrochemical sector and 50% of this investment goods are locally produced, then diversification of Saudi export and economy enlarge considerably—by 0.20 percentage point and 0.26 percentage point, respectively.

Keywords

Introduction

Needless to justify that diversification is important for inclusive growth (Estmann et al., 2022; Usui, 2012). This is more so for the resource (e.g., oil) exporting economies as the existing literature discusses that one-resource-based development can lead to issues that can harm long-term sustainable development (Sachs and Warner, 2001; Manama, 2016; Ross, 2019; Djimeu and Omgba, 2019). In the diversification policies, one of the things that decision-makers should have a clear view on is each sector's role and contribution in the economy. This, inter alia, necessitates a comprehensive analysis of each sector.

In this regard, there are at least four reasons for a deep analysis of the petrochemical sector in Saudi Arabia. First, Saudi Vision 2030 (SV2030), the Kingdom's development roadmap, through its realization programs, such as the National Industrial Development and Logistics Program (NIDLP 2021) and the National Transformation Program (NTP2020) identifies the petrochemical sector as a leader in diversifying Kingdom's economy. SV2030 has set aspirational targets for the diversification of the Saudi Arabian economy for the period 2016-2030. A few of these targets are: Non-oil GDP growth is expected to double compared to 2016; non-oil exports to reach 50% of non-oil exports from 16% in 2016; increase in non-oil government revenues from SAR (Saudi Arabian Riyal) 163 billion to SAR 1 trillion; lowering unemployment from 12% to 7%; increase private sector contribution to GDP from 40% to 65%. Achieving these and other goals will require rapid growth in economic activity sectors including petrochemicals identified in the SV2030 realization programs. Second, the petrochemicals sector makes up a large portion of Saudi non-oil exports. It is worth noting that the share of the chemicals group in non-oil exports averaged 37.15%, and the share of the rubber-plastics group was 25.04% during 1991-2020. If we consider recent developments, the shares of chemicals and rubber-plastics in the non-oil exports averaged 30.42% and 33.70%, respectively in 2016-2020, making more than 64% in total (WTIS online database 1 ). The so-called export-led growth concept states that exports can be an engine for long-term economic growth (e.g., see Giles, 2000 and Krugman et al., 2015). This can be considered for Saudi Arabia, but there are very limited studies exploring this option for the Kingdom (we are aware of Kalaitzi and Chamberlain, 2021, and Hasanov et al., 2022 only). Hasanov et al. (2022) list four major channels, through which non-oil exports can play crucial roles in sustained inclusive economic growth in Saudi Arabia, namely reducing total export instability, creating new jobs in the private sector, establishing a positive spillover effect by generating demand for other tradable and non-tradable sectors' goods and services, and attracting foreign direct investments that can contribute to productivity and efficiency enhancement in the entire economy via technology transfers and positive externalities. In this respect, the development of the petrochemical sector and its exports can contribute significantly to the diversification of the non-oil sector's production and exports. Third, the government has provided significant support for the development of the sector in the form of investment and energy incentives in the past and plans to continue this support in the coming years in line with SV2030. Fourth, there is a favorable environment for the development of the sector when it comes to production inputs such as cheap energy and feedstock.

Against the backdrop above, we particularly leverage the first and second points above and investigate the exports of the petrochemical sector in this paper. We consider two export product groups related to the petrochemical sector: chemicals and rubber-plastics. Precisely, this study aims at examining the driving forces of the Saudi petrochemical sector's export and its role in the diversification of the economy to derive insights that can be useful in designing related policies. With this aim, the study has two objectives: to econometrically estimate how petrochemical exports are shaped by their theoretically articulated determinants historically. Second, to integrate the estimated relations into the KGEMM, a general modeling framework representing economic, energy, and environmental linkages in Saudi Arabia. This incorporation allows us to simulate KGEMM up to the year 2035 with different scenarios to assess to what extent the petrochemical exports can contribute to the diversification in the Kingdom.

This work makes some contributions to literature. This is the first study investigating petrochemical export and its role in the diversification of the Saudi economy to the best of our knowledge. Second, it assesses the petrochemical and diversification effects of domestic energy and feedstock price reform for industry with mitigation and localization measures. This is important because, in line with SV2030, the Kingdom is going through various reforms including domestic energy price adjustments, and their effects on different dimensions of the economy including non-oil exports should be evaluated (e.g., see Gonand et al., 2019; Blazquez et al., 2017). In addition, mitigation measures during the economic reforms and localization are important elements of SV2030 realization programs, such as Fiscal Sustainability Program (the former Fiscal Balance Program), National Industrial Development and Logistics Program (FBP, 2017; NIDLIP, 2021). Third, the theoretical framework we employed considers not only the demand-side factors of exports but also the supply-side element of them, whereas previous studies mostly considered the demand-side factors. The development of petrochemical exports is important to SV2030's economic diversification plan. Hence, to better inform the decision-making process, not only the demand-side but also the supply-side factors of the exports should be investigated. Fourth, for the petrochemical exports analysis, this study adopts a two-stage modeling framework following Ballantyne et al. (2020), Hasanov et al. (2022), Hasanov and Razek (2023) unlike many other studies in this field. The first stage estimates export equations for chemicals and rubber-plastics. This provides an examination of the historical impacts of the theoretically articulated determinants on the exports of chemical and rubber-plastics products. Autometrics-a machine learning modeling algorithm with supersaturation is employed in this stage. Autometrics is a cutting-edge econometric modeling technology with certain advantages over traditional, and even some machine learning, modeling methods (Pellini, 2021; Ericsson, 2021; Castle et al., 2021a, b). The second stage incorporates the estimated equations into KGEMM, a general modeling framework for Saudi Arabia. This integration possesses two merits: (i) not only the effects of the variables included in the export equations but also impacts of other variables of interest (e.g., domestic energy and feedstock prices) on Saudi exports of chemicals and rubber-plastics can be assessed, and (ii) what extent these exports can contribute to the diversification of total exports and economy in coming years till 2035. To this end, policy insights of the present study are not only based on the result of single-equation estimations (which is the partial equilibrium framework used in most previous export studies), but also simulations using a general modeling framework (that is, the KGEMM—energy and environmental sectors augmented, semi-structural, hybrid macro-econometric model). As it is documented in the literature, macro-econometric models can provide more comprehensive representations and understanding of economic relationships than single equations or other partial equilibrium frameworks. This is mainly because the former ones allow for both feedback loops and the effects of other variables and policy levers in addition to those variables in a single equation, which are especially important for forecasting/ projections of the dependent variable (e.g., Cusbert and Kendall, 2018; Hasanov, 2019; Ballantyne et al., 2020; Elshurafa et al., 2022a, b). This study not only estimates the historical relationship between chemicals and rubber-plastics exports and their determining factors but also provides insights into the outlook of these exports until 2035 using scenario analysis. As none of the existing studies focused on Saudi Arabia's petrochemical exports, we reviewed studies on other dimensions of the Saudi petrochemical sector, such as financial performance, sustainability, competitiveness, and investment. A review of these studies is presented in online Appendix A.

The rest of the paper is structured as follows. Section 2 describes the theoretical framework. Online Appendix B presents the data and variables, their definitions and sources, and econometric methodology due to the space limitation. The estimation and test results are reported and briefly discussed in Section 3. Section 4 documents the KGEMM scenario analysis. Section 5 concludes the study with some policy insights.

Following the existing empirical literature on trade, this study used a reduced-form export equation to examine the determinants of Saudi Arabia's petrochemical exports. We adopted the following export equations for the exports of chemical and rubber-plastics based on the theoretical framework presented in Hasanov et al. (2022) and references therein. The econometrically estimable equation for Saudi Arabia's chemicals export is as follows:

Where, xgnoil_chem is chemical exports, and reer_chem is the real effective exchange rate for the exports of the chemical products. An increase in reer_chemt means an appreciation of the domestic currency (i.e., SAR) against the basket of the currencies of the trading partners. gvamanno is gross value added in the non-oil manufacturing sector, which is a proxy for domestic production capacity. gdpf_chem is the real income (GDP) of the main importers of chemical products from Saudi Arabia. Lowercase letters indicate that a given variable is in the natural logarithmic form. ε is the error term. Subscript t denotes time. It is expected that ß1 <0,ß2> 0, ß3 > 0.

The estimable equation for Saudi Arabia's rubber-plastics export is:

Where, xgnoil_rp is the Saudi Arabia's exports of rubber-plastics, reer_rp is real effective exchange rate for the exports of rubber-plastics and its increase means appreciation of the local currency. gdpf_rp is real income (GDP) of the main importers of rubber-plastics products from Saudi Arabia. u is the error term. It is expected that γ1 < 0, γ2 > 0, γ3 > 0.

Online Appendix C documents the results of the unit root tests (see C1) and explanations of the long run estimates (see C2). The conclusion from the unit root tests results is that all variables are non-stationary in their log levels, but stationary in the first differences of their log levels. In other words, they are I(1) series. This conclusion is derived from the results of the ADF, the PP, and the KPSS tests.

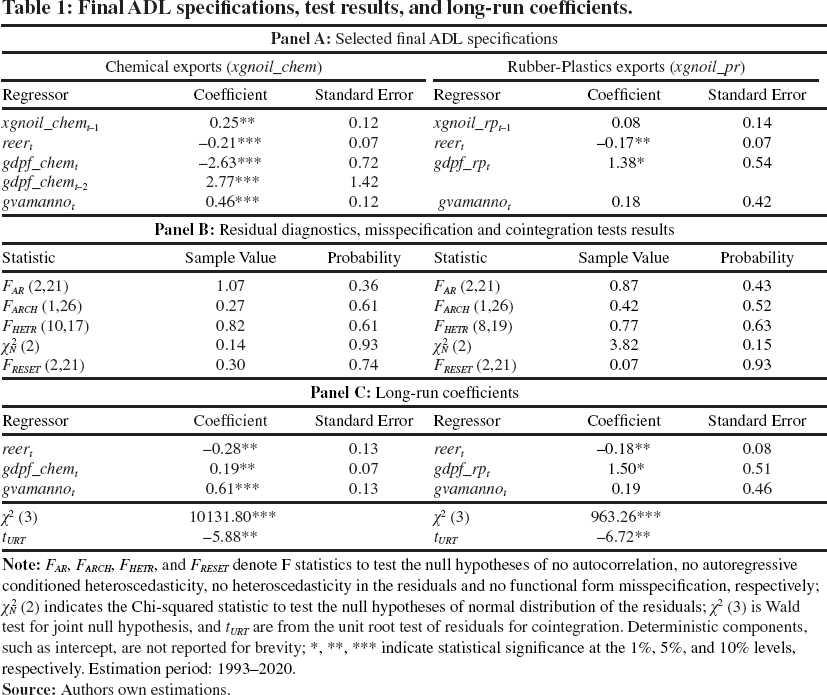

A general unrestricted model (GUM) of ADL specifications for equations (1) and (2) are formulated with two lags of all variables and contemporaneous values of the explanatory variables. The estimations are performed in the general to specific modeling framework (Gets) using Auto-metrics. The estimated GUM specifications for both export equations have successfully passed all residual diagnostic tests as well as the recursive estimation stability tests. Table 1 presents the final estimation results.

The cointegration test was conducted to check whether the variables establish a long-term relationship. The calculated test statistics are -5.88 for chemicals equation and -6.72 for rubber-plastics equation. Both values are greater than the corresponding critical value at the 1% significance level in absolute terms, indicating that the variables are cointegrated.

The long-run estimation results in Panel C of Table 1 show that a 1% appreciation (depreciation) in the real effective exchange rate of SAR, i.e., the Saudi riyal leads to a 0.28% decrease (increase) in chemical exports and a 0.18% decrease (increase) in rubber-plastics exports, with the other factors remaining unchanged. The intuition behind this result is that domestic goods and services become cheaper (more expensive) for foreigners when the national currency depreciates (appreciates).

Final ADL specifications, test results, and long-run coefficients.

Final ADL specifications, test results, and long-run coefficients.

indicate statistical significance at the 1%, 5%, and 10% levels, respectively. Estimation period: 1993-2020.

We find that a 1% rise in the partner countries' GDP increases Saudi Arabia's chemicals export and rubber-plastics export by 0.19% and 1.50%, respectively, ceteris paribus. Saudi Arabia's main trading partners for chemicals export are East Asia and the Pacific, particularly China while the main trading partners for rubber-plastics are two regions—the MENA and East Asia and Pacific. Exports of rubber-plastics are more diversified in terms of destination, and maybe this is the reason why the foreign income elasticity is larger compared to that for the chemicals export.

Finally, the long-run results show that a 1% increase in the value-added of non-oil manufacturing leads to 0.61% and 0.19% expansion in the exports of chemicals and rubber-plastics, respectively.

This section describes scenario analysis using KGEMM from 2023 to 2035. The aim of the scenario analysis is to quantify the effects of domestic and foreign price shocks on the petrochemicals sector, and the contributions of the latter to the diversification of total exports and economy in Saudi Arabia. 2 As foreign prices, we use the international prices for chemicals and rubber-plastics export groups. Regarding the domestic price, we consider the prices of energy products and feedstock. In other words, we simulate the impact of domestic energy and feedstock price reform given its relevance and importance for policy making process. Interested outputs are chemicals export, rubber-plastics export, value added of the petrochemical sector, non-oil value added, export diversification, and economic diversification. The export diversification is measured as the percentage share of non-oil export in total exports and the economic diversification is the percentage share of non-oil value added in GDP. The section first briefly introduces the KGEMM and the scenario design for the simulation analysis, then discusses the results of the simulations in the respective sub-sections.

Abada and Ehrenmann (2018), among other studies, highlight a crucial role of export strategies and policies for resource-based economies.

4.1. KGEMM and its representations for the petrochemical sector—a bird's eye view

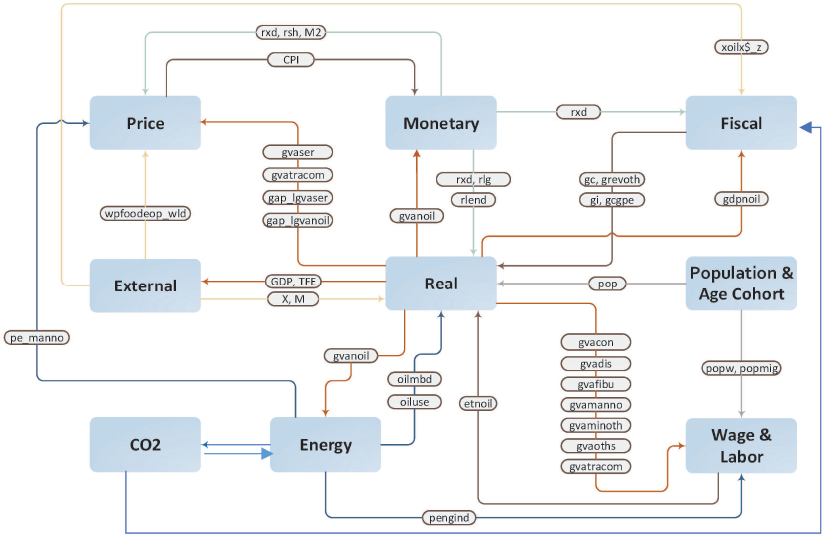

The KGEMM is a policy tool to evaluate the influences of domestically made decisions and global changes/shock on Saudi Arabia's energy-environmental-economic indicators at aggregate and disaggregate levels (see e.g., Hasanov et al., 2023). It is an energy and environmental sectors augmented macroeconometric model. It is hybrid as it incorporates Input-Output Model (IOM) elements, such as intermediate and final demands, into the macroeconometric framework. Also, it is semi-structural as KGEMM brings together theory- and data-driven approaches. The literature notes that a hybrid type macroeconometric models outperform structural, i.e., theory-based, models, such as a dynamic stochastic general equilibrium model or a computable general equilibrium model, and data-based models, such as autoregressive univariate or multivariate models (Hasanov, 2019; Bal-lantyne et al., 2020; Jelick and Ravnik, 2021). Having IOM elements brings a sectoral granularity to KGEMM as it can investigate demand at the economic activity sectors level unlike standard macroeconometric models. The KGEMM comprises nine blocks to represent Saudi Arabia's economic (macro and sectoral), energy, and environmental linkages. This is demonstrated in Figure 1.

The KGEMM version employed here is slightly different from the version documented in Hasanov et al. (2023) as we incorporated the export equations for chemicals and rubber-plastics developed in this study into the KGEMM and made necessary changes. In addition, this version of the model contains more than 800 annual time series variables grouped as exogenous and endogenous. The exogenous ones are mainly domestic policy variables (e.g., value-added tax rate), and global energy and economic indicators (e.g., export and import prices, demand for Saudi oil, foreign direct investments). Behavioral equations and identities are used to explain the endogenous variables. The former ones are econometrically estimated, while the latter ones mainly follow the System of National Accounts. The long-run and short-run relationships among the variables are estimated using the cointegration and error correction modeling (ECM) frameworks, respectively. Therefore, there are two versions of the model: the long-run version based on the estimated long-run (cointegrated) equations, such as the Fair models, Fair (1979, 1993). The short-run version is built based on the estimated ECMs, such as (Buenafe and Reyes, 2001; Welfe, 2013). We use the long-run version of the KGEMM in this study following Weyerstrass et al. (2018), Welfe (2011), Khan and ud Din (2011), Weyerstrass and Neck (2007), Musila (2002), Fair (1979, 1993), inter alia. This is because of two reasons: the simulation sample is long, i.e., 13 years and to rule out endogeneity issue.

KGEMM long-run behavioral equations and identities are presented in Online Appendix El while E2 describes the variables used in the model. The estimated short-run equations, i.e., ECMs associated with the long-run equations are reported in Appendix B of Hasanov et al. (2023). A discussion of the methods used in the KGEMM including its econometric estimations and testing are given in Chapter 4 (KGEMM Methodology) and detailed in Appendix A (KGEMM Methodological Framework and Philosophy) of Hasanov et al. (2023). Generally, the KGEMM methodology mirrors that of other contemporary macro-econometric models (see Ballantyne et al., 2020; Jelic and Ravnik, 2021; Cusbert and Kendall, 2018; Welfe, 2011). Additionally, advanced econometric methods (e.g., Autometrics—a machine learning modeling algorithm) are employed for estimating individual equations within the KGEMM.

Schematic illustration of KGEMM.

We incorporated the estimated export equations for chemicals and rubber-plastic into KGEMM. In addition to these two equations, petrochemical sector is represented in KGEMM through the following relationships: behavioral equations for demand, potential output, employment, investment, producer price, demand for feedstock components—ethane, methane, LPG, naphtha, as well as identities for output gap, capital stock, unit labor cost, intermediate demand, final demand, total demand, weighted average price of energy, weighted average price of feedstock. Moreover, petrochemical value-added feeds into 13 economic activities' intermediate demand identities. Furthermore, the above-mentioned elements of the petrochemical sector, that is, value-added, employment, investment, capital stock, and exports feed into the identities of the same elements of the non-oil sector (e.g., petrochemicals employment is the part of the non-oil employment). Notably, the above given representations of the petrochemical sector and their links to the other relations in the KGEMM provide a comprehensive framework to assess the various developmental aspects of the sector and their role in the overall development and diversification. To make the scenarios analysis easy to understand for readers, the above-mentioned behavioral equations and identities of the petrochemical sector are placed in Table Dl of online Appendix D, while Table D2 reports variables' definition.

4.2. Underlying Assumptions of the Scenario Analysis and Policy Relevance

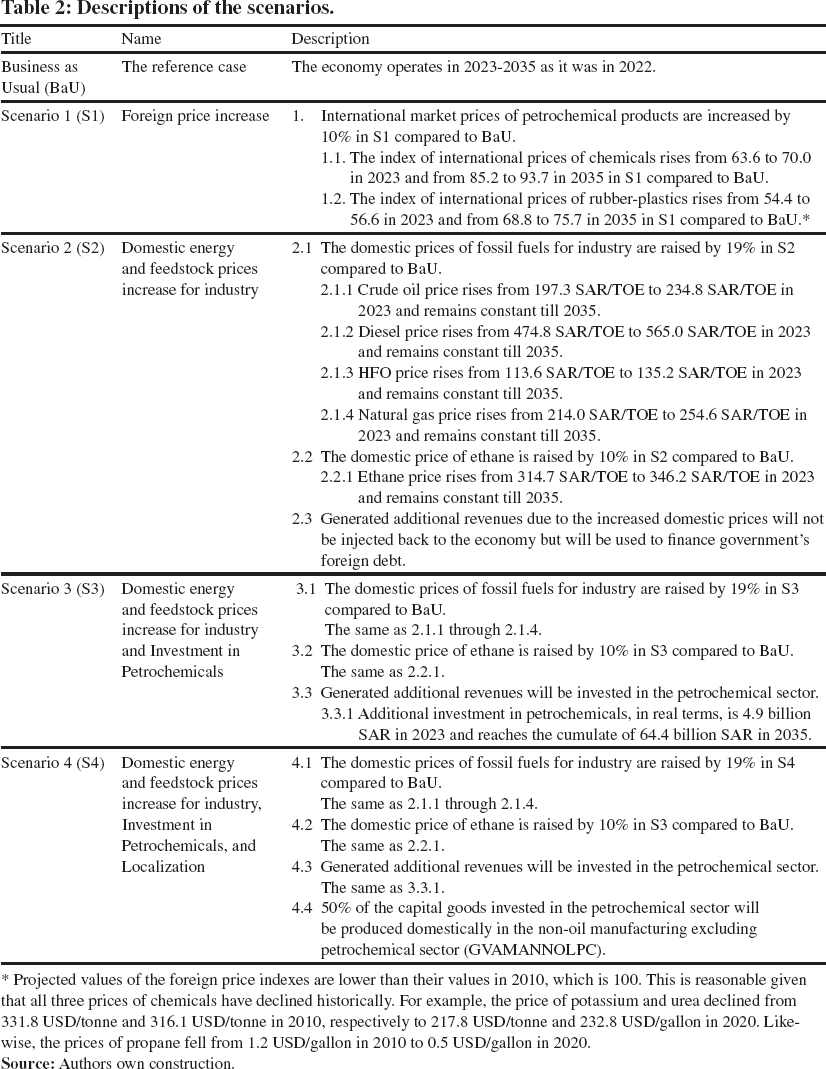

We perform four scenarios (S1-S4) in addition to Business as Usual (BaU). BaU is the reference case scenario with the purpose of comparing the other scenarios with it. Scenario 1 explores the impact of the foreign price shocks, while Scenarios 2-4 analyze the effects of the domestic price shocks. Table 2 documents the scenarios.

In the BaU case, there is no change in the exogenous variables and assumptions made in the model. KGEMM, as a large-scale model, has 397 exogenous variables. Hence, discussing the projected values of each exogenous variable is out of the scope of this study. However, we here briefly discuss the explanatory variables of the export equations of chemicals and rubber-plastics (see Table B1 of Online Appendix). They are PGDPPETCH, PF_CHEM, PF_RP, GDPF_CHEM, and GDPF_RR The first one is projected to grow with an average annual rate of 2% for 2023-2035 following projected average inflation rate for Saudi Arabia. The projections for PF_CHEM and PF_RP mirror growth rates of the world commodity index price for non-fuel goods for the same period obtained from the Oxford Economics Global Economic Model Database, OEGEM (2021). The reason for this assumption is that the historical patterns of the former two variables quite closely follow that of the latter one. We assumed that GDPF_CHEM and GDPF_RP will grow with growth rates of 6.7% and 5.89%, respectively—their average growth rates for 2015-2019, i.e., the last stable 5 years disregarding COVID-19 and post-COVID-19 recovery.

In Scenario 1, the magnitude of the increase, i.e., 10% in the index of the international price of chemicals (PF_CHEM) and in the index of the international price of rubber-plastics (PF_RP) is assumed by the authors. Meaning that it is not based on any report or announced policies. We simply want to quantify the impact of the foreign price shocks on the exports of petrochemical groups and other indicators of interest, such as export diversification and economic diversification. Figure 2 illustrates how Scenario 1 operates.

Transmission channel from foreign prices to the selected indicators.

As mentioned above, Scenarios 2-4 quantify the effects of increases in domestic prices of fossil fuels and ethane for industry and their combination with mitigation and localization measures. The idea is to see to what extent the pure effects of domestic price reform (in S2) are different from when this reform is accompanied by investments (in S3), and both investments and localization (in S4).

Descriptions of the scenarios.

Source: Authors own construction.

Projected values of the foreign price indexes are lower than their values in 2010, which is 100. This is reasonable given that all three prices of chemicals have declined historically. For example, the price of potassium and urea declined from 331.8 USD/tonne and 316.1 USD/tonne in 2010, respectively to 217.8 USD/tonne and 232.8 USD/gallon in 2020. Likewise, the prices of propane fell from 1.2 USD/gallon in 2010 to 0.5 USD/gallon in 2020.

The idea of Scenario 2 is to examine that if fossil fuels and ethane prices are raised for industry and there are no mitigation measures in place, the budget spending is the same as that in BaU, to what extent economic activity and export performance may contract compared to BaU. The scenario is designed based on the already implemented and upcoming policy measures on domestic fossil fuels and feedstock prices. The authorities increased the price of diesel from 0.63 SAR to 0.75 SAR by 19% in January 2023. In addition, the Ministry of Industry and Mineral Resources has announced that it will adjust the fuel and feedstock prices for the industrial sector from the fourth quarter of 2023, according to Arab News. Precisely, the price adjustment policy will be applicable to Arab heavy and light crude oil, heavy fuel oil, natural gas, and ethane. It is important to assess the effects of these implemented and upcoming policy measures on the performance of the petrochemical sector and the whole non-oil economy. Given that diesel price has been increased by 19% and it is not available to the authors how much the ministry of industry and mineral resources will increase the prices of energy products and feedstock, we applied the same growth for crude oil, heavy fuel oil, and natural gas. As for ethane, we assumed a lower price increase compared to fossil fuel prices, which is 10%. This is because of the following reasons: a feedstock is different from energy products, SV2030 considers petrochemicals as one of the strategic sectors for future development and diversification, accordingly the government supports the development of the sector, ethane is the key feedstock in the Saudi petrochemical sector (e.g., see KSA Petrochemicals, 2022). Of course, one can consider other magnitudes of increases than what we assumed here as there is no announcement for the magnitudes of increases to our best knowledge. Domestic energy price reform is part of initiatives highlighted in Saudi Vision 2030, particularly in the Fiscal Sustainability Program (the former Fiscal Balance Program). The purpose is to further rationalize the domestic consumption of energy products while generating additional revenues for the government budget that can be allocated to socio-economic development projects (FBP, 2017). In scenario 2, we additionally assumed that the generated additional revenues, due to the increased domestic prices of fossil fuels and ethane, will not be injected back into the economy as consumption or investment expenditures. These revenues will be used to finance the government's foreign debt. KGEMM has 5 consumption items and one investment item of the government budget spending: government wages and salaries, allowances, government maintenance and operation costs, government administrative expenses, government transfers to households, government other consumption, and government investment. These are the final demand components of the government budget to boost economic activity (see Fiscal block of KGEMM in Hasanov et al., 2023). In Scenario 2, we keep the values of the aforementioned items unchanged, that is, they are the same as they are in BaU. Again, as mentioned above, the idea is to examine to what extent economic activity and export performance may shrink in Scenario 2 compared to BaU if fossil fuels and ethane prices are increased and there are no additional spending or mitigation measures in place. Apparently, this is quite a pessimistic scenario.

Scenario 3 combines Scenario 2 (of domestic price reform) with a mitigation measure. The idea behind Scenario 3 is to explore how domestic price reform with mitigation would be different from that without mitigation, i.e., to evaluate the role of mitigation. In other words, the purpose of the scenario is to assess the performance of the petrochemical sector and the entire economy if the domestic price increase policy will be accompanied by mitigation measure of additional investment. Accordingly, we assumed that the generated additional revenues due to the increased prices of fossil fuels and ethane for industry will be invested in the petrochemical sector. We calculated that these additional revenues amounted to 4.9 billion SAR in 2023 and to 5.2 billion SAR in 2035.

To consider these additional revenues as an investment in the petrochemical sector, we deflated them by the investment deflator (where 2010 is the base year) to obtain values in real terms. The resulting real value of investments at the constant prices of 2010 is 4.3 billion SAR in 2023 and accumulates to 52.8 billion SAR in 2035. To give an idea of the size of this additional investment, it is equal to 2.2% of petrochemical sector investment and 0.6% of non-oil investment in BaU on average for the period 2023-2035. From a policy perspective, this additional investment for the petrochemical sector is obviously a mitigation measure, although its amount is quite small. The importance of the mitigation policies is highlighted in the Fiscal Sustainability Program of the Saudi Vision 2030 (e.g., see FBP, 2017). The program emphasizes the importance of mitigation measures in the case of domestic energy prices and other reforms being implemented. Moreover, note that we keep the government budget spending items unchanged as we did in Scenario 2. In other words, the government budget expenditures will be the same as they are in BaU. Thus, the only difference between Scenario 2 and Scenario 3 is the additional investment in the petrochemical sector.

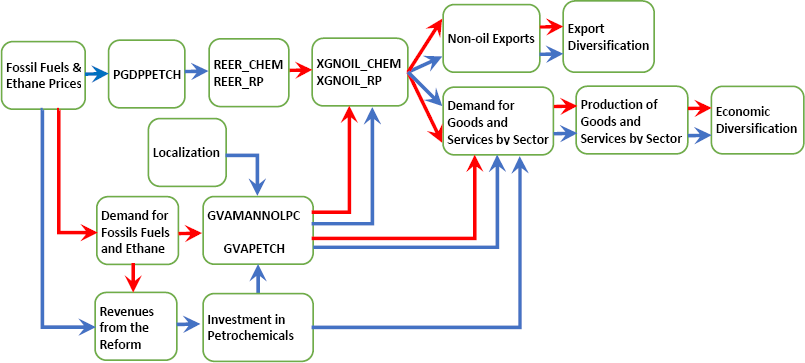

Scenario 4 adds one more policy-relevant dimension to Scenario 3, which is localization, put differently, import substitution. The aim of the scenario is to evaluate how the petrochemical sector and the entire non-oil economy respond to the domestic price reform if the additional revenues due to this reform are invested in the sector and if half of these investment goods is produced locally in Saudi Arabia. This assessment is intended to show how the domestic price reform only (i.e., S2) is different from if it is implemented with the other two policy measures of mitigation and localization. Note that the assumption of 50% of localization is an arbitrary choice and other ratios also can be simulated. The localization assumption implies that the value added of the non-oil manufacturing less petrochemicals (GVAMANNOLPC) producing capital goods will be increased to cover import substitution. Note that local content and localization are important elements in the Saudi Vision 2030 realization programs, particularly in the National Industrial Development and Logistics Program. The program highlights increasing the percentage of local content in non-oil sectors, localizing new industries and promoting exports, adopting policies and procedures to promote local content for government procurement among other related initiatives and targets (NIDLIP, 2021). Increasing local content in the non-oil sectors to SAR 1.24 billion local content policies and localization of industry value chain are important items of the policy agenda in Saudi Arabia as it is highlighted. This is because the share of import in meeting aggregate demand is considerable in Saudi Arabia. For example, on average total imports were 30% of GDP, in nominal terms, during 1970-2020. Lastly, in Scenario 4, the government budget spending is the same as that in BaU—the same assumption that we made for Scenarios 2 and 3. We illustrate operational channels of Scenarios 2-4 in Figure 3.

Transmission channel from domestic fossil fuels and ethane prices (and with mitigation and localization) to the selected indicators.

4.3. Results of the Scenario Analysis

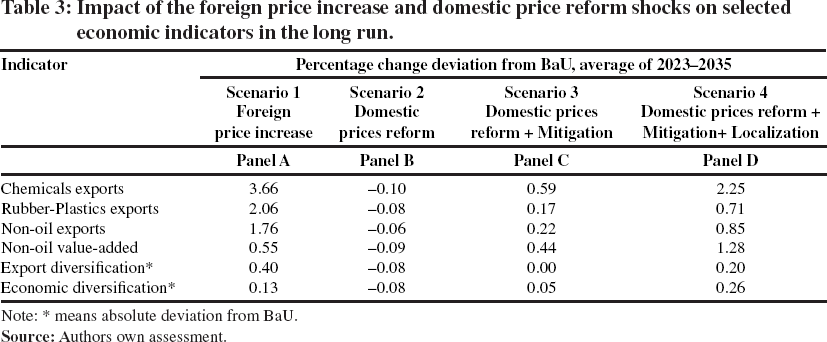

This sub-section briefly discusses the findings of the scenario analysis starting chemicals and rubber-plastics exports, followed by total non-oil exports and value-added, and lastly export and economic diversification. The discussions are based on the deviations of a given variable's values in respective scenario compared to those values in BaU. Table 3 reports the results of the scenario analysis. As mentioned above the scenario analysis covers 2023-2035 but we do not report every single year as it can make Table 3 to convey more noise than signal to readers. Instead, we report average values of the selected indicators for 2023-2035 in the table. In Table D3 of online Appendix D, we also report 5-year averages for those who are interested in detailed results.

Impact of the foreign price increase and domestic price reform shocks on selected economic indicators in the long run.

Note:

means absolute deviation from BaU.

A raise in foreign prices creates a favorable situation in international markets to export more petrochemical products. Panel A of the table records that a shock in PF_CHEM and PF_RP by 10% in Scenario 1 causes both chemicals and rubber-plastics exports to grow higher by 3.7% and 2.1%, respectively on an average of 2023-2035 compared to BaU. Numerically, chemicals export benefit more than the export of rubber-plastics from the favorable international market condition. This is because the former export group is more responsive to the real exchange rate and hence foreign price changes than the latter export group (see Panel C of Table 1). Expectedly, an increase in exports in the petrochemical sector leads to an expansion in total non-oil exports, simply because the former is part of the latter. Non-oil exports grew 1.8% more in Scenario 1 compared to BaU. In addition, an increase in the petrochemicals export generates additional demand for goods and services from the other sectors in the Saudi economy. In KGEMM, this channel works through final demand of exports for 13 economic activity sectors' goods and services. This spillover effect boosts overall economic activities as it was postulated by the export-led growth theory (Edwards, 1993; Balassa, 1978) and found by empirical studies on the Saudi economy (Kalaitzi and Chamberlain, 2021; Faisal et al., 2017; Saeed, 2017). The non-oil sector's value-added rises 0.5% more in S1 compared to BaU. Moreover, Panel A of Table 3 shows that an increase in non-oil exports and value-added result in more diversified total exports and economy. This implies that both non-oil exports and non-oil value-added grow more than total exports and total GDP in S1 compared to BaU, otherwise the positive numerical values (i.e., 0.40 percentage point and 0.13 percentage point) for diversification cannot be materialized.

Panels B-D of Table 3 report the numerical effects of the domestic price reform and its combination with mitigation and localization on the selected indicators. One can expect conceptually that a price reform without any mitigation policy can slow down exports and economic activity. Panel B shows that this expectation holds true for the results of Scenario 2. It is noteworthy, however, to highlight that the magnitude of the effect is quite small—at the highest, it does exceed even -0.10%. Both chemicals export and rubber-plastics export diminished but very slightly, that is, 0.10% and 0.08% for each in S2 compared to BaU. In the KGEMM, the domestic price reform influences petrochemicals exports via the transmission channel illustrated in Figure 3: An increase in the price of ethane (and energy) raises the cost and price of the petrochemical production (see equation #17 in Table Dl of online Appendix), as it is the main feedstock component of the sector (KSA Petrochemicals, 2022). A higher domestic price for the petrochemical sectors makes its products less attractive for the trading partners as we have estimated a negative impact of the domestic price of petrochemicals (as part of real effective exchange rates) on its exports in Panel C of Table 1, being consistent with the theory. However, the scenario analysis shows that the price of petrochemicals increased only by about 0.5% on average due to the raise in the prices of ethane and fuels by 10% and 19%, respectively. This explains why the effect of the domestic price reform, in particular the ethane price increase, on exports of petrochemicals is quite limited. Obviously, diminished petrochemical exports cause the same in total non-oil exports, but again the magnitude of the impact is quite small, i.e., -0.06%. Slightly tightened petrochemical and total non-oil exports lower their demand for goods and services from the other sectors of the Saudi economy. Accordingly, non-oil value added declined by 0.09% in Scenario 2 compared to BaU. It appears from the scenario analysis that exports and value-added of the non-oil sector decline whereas total exports and total GDP slightly increase, both of which include oil. This is because increased domestic prices for fossil fuels (i.e., crude oil, diesel, HFO, and natural gas—see Table 2) lower domestic demand for these fossil fuels, and thus, their exports increase. As a net effect (of the slight decline in non-oil exports and value-added and the slight increase in total exports and GDP), diversification of exports and economy contract mi-norly, i.e., by 0.08 percentage point.

The scenario results of the domestic price reform with mitigation policy, i.e., Scenario 3, are documented in Panel C of Table 3. The key observation from the numerical results compared to Scenario 2 of domestic price reform only is that the mitigation measure of additional investment in petrochemicals, albeit quite small in amount, makes the economy not only recover back to the initial state, i.e., BaU case, but also growing more. This shows the importance of two things in boosting the economic development of the Saudi economy: mitigation policy and the petrochemical sector. Going over the selected indicators, both petrochemical export groups are positively affected by the mitigation measure. The transmission channel in KGEMM is as follows (see Figure 3): additional investment in the petrochemical sector translates to expanded capital stock to produces more goods in petrochemical. The non-oil manufacturing value-added increases too, as the petrochemical is part of it (see identities # 20 and 21 in Table Dl of online Appendix). Resultantly, petrochemical exports rise as we estimated a positive impact of non-oil manufacturing value-added on the said export groups in the long run (see Panel C of Table 1). Moreover, this additional investment in petrochemicals also increases demand for other sectors' goods and services, which translates to an increase in their output (see Figure 3). Apparently, chemical exports rise more than rubber-plastics exports, i.e., 0.59% versus 0.17%. We believe this is because of their long-run responses to the domestic production capacity measures, which were estimated to be 0.67 and 0.19, respectively (again, see Panel C of Table 1). Not surprisingly, non-oil exports and non-oil value-added increases since they comprise petrochemical exports and value-added, respectively, as a result of additional investment. Finally, export diversification recovers back to BaU while economic diversification even exceeds driven by the additional investment in the petrochemical sector. The key message from Scenario 3 is the importance of the implementation of mitigation measure (as an investment to the petrochemicals in our case) together with the domestic industrial price reform in order to boost export and economic growth and thus diversification. Note that this message is supported by the findings of the previous scenarios analyses for the Saudi Arabia, as they found that energy and fiscal price reform with mitigation measures would foster economic growth in the long run. For example, Hasanov et al. (2020) concluded that the economy will gain from energy price reform in the long run, mainly through increased investments and greater efficiency. Blazquez et al. (2021) highlight that the effects of structural reforms primarily depend on how oil exports are impacted, and government revenues are recycled, and in this regard, energy price reform can lead to a welfare gain in the long run.

The last column of Table 3 reports the scenario results of the domestic price reform coupled with the mitigation and localization policies. In general, this scenario yields the highest growth for exports and value-added whether they are in the petrochemical sector or in the entire non-oil economy among scenarios 2-4. This is expected, as substituting imports with domestically produced goods reduces leaking money outside, which is used domestically to boost aggregate demand in the short run and capital and supply in the long run. Earlier studies also found the positive impact of localization on economic growth and exports in Saudi Arabia (e.g., see Elneel and AlMulhim, 2022; Hasanov and Razek, 2022; Alhakimi, 2018). The transmission channel of localization in KGEMM operates as it is illustrated in Figure 3: in order for the non-oil manufacturing less petrochemicals sector (GVAMANNOLPC) to produce half of the investment goods, which is put in the petrochemicals sector, it increases its demand for goods and services from the other sectors of the economy. As a result, production of goods and services increases both in the non-oil manufacturing less petrochemicals sector and the other related sectors and thus, in the entire economy. Recall from Scenario 3 that investment in the petrochemical sector leads to both more production in the sector and more demand for goods and services in the other sectors of the economy and thus, more production. As we discussed in the previous scenario, growing production in non-oil manufacturing brings more exports of petrochemicals, which makes non-oil exports grow more. This also results in more value-added in the non-oil sector. Lastly, Panel D presents that diversifications of the exports and the economy expand by 0.20 percentage point and 0.26 percentage point, respectively. This indicates that non-oil exports and non-oil value-added grow faster than total export and GDP. Numerically, non-oil exports grow by 1.28% while total exports rise by 0.85% in Scenario 4 compared to BaU. In the same token, 0.85% and 0.16% increases are recorded for the non-oil value added and GDP, respectively.

It is worth noting that the numerical outcomes obtained from the scenarios are heavily conditional upon the assumptions we have made for the input variables and obviously, other numerical outcomes can be obtained if other assumptions are adopted. A few things should be mentioned in this regard. First, the magnitudes of increases in the foreign and domestic prices we assumed. Second, for recycling reform revenues back to economy, we selected investment in petrochemicals, but one can consider investment in other sector(s) or even other recycling options. Third, we assumed 50% of the localization of the investment in petrochemicals, but other percentages can be assumed as well. Fourth, for localization we selected non-oil manufacturing, but another sector or more than one sector can also be considered.

4.4. Results of the Sensitivity Analysis

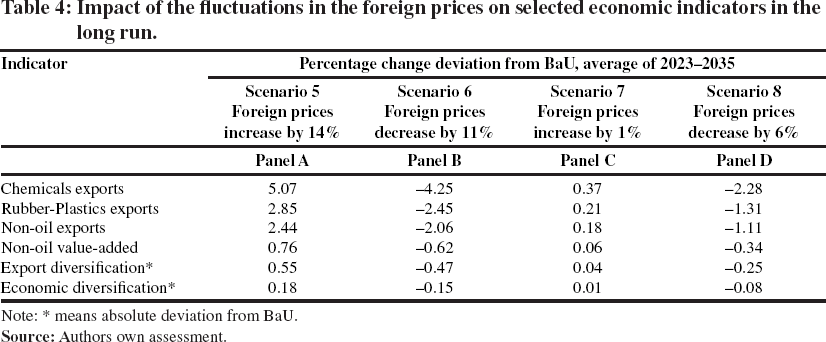

In this sub-section, a sensitivity analysis is conducted using price fluctuations to assess the robustness of the results obtained from the scenario analysis discussed in the preceding sub-section. 3 The analysis focuses on fluctuations in the foreign prices of both export products: chemicals and rubber-plastics. Their domestic prices are administratively adjusted by the government and thus kept constant for a certain period and raised based on policy decisions. Therefore, assuming fluctuations in these prices is not realistic. Since a fluctuation means an irregular rise and fall, we increased and decreased the foreign prices in the scenarios below. Moreover, to shock the model more severely and thereby make the sensitivity test more difficult for the model and its results, we deliberately made ups and downs of the fluctuations highly contrasting in terms of their magnitudes. To be precise, in the first scenario here (S5), we increased the index of the international price of chemicals (PF_CHEM) and the index of the international price of rubber-plastics (PF_RP) by 14% compared to those in the reference case (BaU) outlined in Table 2, maintaining this increase permanently during the period from 2023 to 2035. In the second scenario (S6), we decreased these indices by 11%. Furthermore, in the third scenario (S7), we raised them by 1%, and in the fourth scenario (S8), we reduced them by 6%. Table 4 presents the detailed results of the sensitivity analysis.

We thank the anonymous referee for suggesting this analysis.

Impact of the fluctuations in the foreign prices on selected economic indicators in the long run.

Note

means absolute deviation from BaU.

In brief, the primary observation from the table is that the model produces results that are both theoretically and statistically coherent. Theoretically, one would anticipate a positive correlation between foreign prices and the chosen economic indicators: an increase in foreign prices should correspond to an increase in the indicators, and vice versa. Indeed, the table reveals that the selected indicators rise when foreign prices increase (scenarios 5 and 7) and decline when foreign prices decrease (scenarios 6 and 8). Furthermore, it is evident that the model responds to shocks in a numerically consistent manner—large shocks result in substantial changes (scenarios 5 and 6), while small shocks lead to small alterations (scenarios 7 and 8). Thus, drawing from the findings of the sensitivity analysis outlined here, it can be concluded that the results of the scenario analysis documented in Table 3 exhibit robustness and can provide insights for policymaking.

We examined petrochemical exports and their role in the diversification of exports and the economy in this research. We considered two export groups of petrochemicals, namely chemicals and rubber-plastics. A long-run analysis was carried out using Autometrics in the extended export function framework, and then scenario analysis was performed.

The long-run estimation results showed that foreign incomes, domestic production, and the depreciation of the real effective exchange rates all have positive impacts on the exports of chemicals and rubber-plastics. From the conducted scenario analysis, we concluded that these export groups can play an important role in the diversification of exports and the economy in Saudi Arabia. The scenario analysis further concluded that rising foreign prices create a favorable situation for the expansion of petrochemicals export and through it for export and economic diversification. Domestic industrial energy and feedstock price reform without any mitigation measures does not have a sizeable effect on either export diversification or economic diversification. The said reform can not only make the economy recover back to the pre-reform level but also can make it grow and diversify more if the reform related revenues are circulated back to the economy as an investment to the petrochemical sector, although the amount of it is fairly small. The reform with both mitigation measure and localization can lead to increased non-oil exports and value-added, and thus, a further diversification of the exports and the economy.

Policymakers may wish to take measures leading to increases in the exports of chemicals and rubber-plastics. In this regard, they should consider that rubber-plastics exports are more responsive to foreign income, measured by GDP of MENA and East Asia and Pacific regions, than chemical exports. So, there is not so much for decision-makers to do rather than monitoring developments in the said regions regularly. Instead, chemicals exports are more responsive to domestic production, measured by the value-added of the non-oil manufacturing sector, than rubber-plastics exports. This implies that further development of non-oil manufacturing, including petrochemicals, is an important factor in increasing the exports of chemicals.

Moreover, decision-makers should note that the real exchange rates, as measures of price competitiveness, play a similar role in the development of both export groups. Since the fixed exchange rate of the Riyal to the U.S. dollar is implemented in Saudi Arabia, policymakers should pay attention to evolvements of the foreign and domestic prices of these products. In this regard, any increase in foreign prices creates a favorable environment for an expansion of petrochemical exports and thus diversification. So, Saudi policymakers do not have much to do with foreign prices but they can monitor development regularly. Instead, Saudi policymakers have more control over domestic prices, particularly when it comes to domestic price reforms. The authorities may wish to note that if reforms are implemented with the mitigation measure of injecting revenues collected from the reforms back into the economy as an investment, even though with a small amount, then the economy even grow more in the long run. One of the successful examples of such mitigation policy was the implementation of support packages for the industrial branches during the reforms implemented in 2016-2018. The package, covering industry-agnostic and industry-specific measures with six main themes, was aiming at mitigating the effects of the domestic reforms and transforming energy intensive industries to more energy efficient and globally competitive ones (see Fiscal Balance Program 2017).

Another point that deserves the attention of policymakers is localization, as the scenario analysis showed that it can further boost exports, economic activity, and diversification. The authorities should consider designing policies that encourage substituting imports with locally produced goods and services. Increased local content would greatly contribute to diversifying the economy, which is the key policy strategy of Saudi Vision 2030.

One of the things to be considered is to further enhance the coordination among the various policies that are currently being implemented to achieve various targets of SV2030. For example, domestic energy price and fiscal reforms with the aim of increasing efficiency and government budget revenues, which may end up with the increased domestic prices, should be effectively coordinated with the policies aiming at raising international competitiveness position of the Kingdom to among the top 10 globally, and achieving the 50% share of non-oil exports in non-oil GDP by 2030.

Finally, finding the validity of the export-led growth strategy for Saudi Arabia put forward the implementation of direct or indirect administrative, legislative, structural, and institutional measures to foster the exports of chemicals and rubber-plastics. Formulation of supply chain and export market strategies for the petrochemical products, consideration of potential customers, marketing, and legal support of petrochemical companies would be examples of such measures. Moreover, e-commerce, product certifications, export exemptions, financial support, discovering international markets for petrochemical products also can be considered. Many of the listed measures are well established by the Saudi Export Development Authority, an independent national agency that seeks to develop Saudi non-oil exports.

Footnotes

Acknowledgments

The earlier version of this paper was presented and discussed at the 24th Federal Forecasters Conference, 44th IAEE Conference, and 24th Dynamic Econometrics Conference. We thank the participants of these conferences for their comments. Additionally, we would like to express our appreciation to an anonymous referee and the editor for their insightful comments and suggestions. Any errors and omissions remain the responsibility of the authors alone. The use of generative AI and Al-assisted technologies in the writing process to improve the language and readability of the paper is acknowledged. The views expressed in this paper are the authors' and do not necessarily represent the views of their affiliated institutions.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.