Abstract

Using manufacturing survey data from China, we study the relationship between firms’ anticipatory investment (or in other words, willingness to invest) in the short-run future and their perception of the current power crunch for small and medium-sized enterprises (SMEs). Our findings reveal a robust and significant negative association, suggesting a sizable persistent negative impact of the power crunch on firms’ investment lingering over at least a couple of months. The dynamic impacts are very different at the industry level, with electricity-dependent industries appearing to take more hits. However, we find no statistically significant evidence to support the channel of electricity dependence in comparison with the channel of capacity utilization. Moreover, we show that firms of smaller size suffer disproportionately larger damage in future investment, which highlights the importance of caring about SMEs, relative to big firms.

1. Introduction

The power crunch has emerged as headline news since the third quarter of 2021. The energy crisis has been sweeping across the entire world. China and India, the world’s top two coal producers, are on the verge of running out of coal, Europeans are paying skyrocketing prices for natural gas, and Americans are contending with rising gasoline prices amid the fears of severe electricity shortages and even blackouts over the winter and beyond IEA (2022). The power crunch poses another threat to the global economy that has been grappling with the new variants of the coronavirus. Worse still, the electricity shortage derails the production of goods and tightens supply chain bottlenecks from the very far upstream. The ongoing war between Russia and Ukraine, the summer heatwave sweeping much of Europe and China, and the limited rainfall across the Northern Hemisphere have contributed to making the situation even worse.

Media headlines focus on the challenges caused by the power crunch for large manufacturers, such as the big automakers (e.g., Tesla and General Motors) and giant semiconductor foundries (e.g., Nvidia and TSMC), as well as the implications for their profitability that are crucial for investors in the financial markets. However, relatively little is reported by the mainstream media about the power crunch striking small and medium-sized enterprises (SMEs) that absorb the vast majority of employment throughout the world (Hardy and McCasland, 2021), which are also arguably the economic growth engine for much of the developing world. To fill this void in the literature, we look into the impacts of the power crunch on SMEs using manufacturing survey data from China.

There is a small yet burgeoning empirical literature that explores the impacts of the power provision on firm performance. Reinikka and Svensson (2002) provides the first empirical evidence that unreliable and inadequate electricity reduces firm investment in Uganda, which is reconfirmed by Abeberese (2020) using Ghanaian data. Recent studies show that the electricity shortage has negative impacts on firm employment, input sourcing, output, sales, profitability, and productivity with the help of microeconomic data primarily from low-income African countries (Hardy and McCasland, 2021; Abeberese et al., 2019; Cole et al., 2018; Carlsson et al., 2020) and the world’s two largest developing economies, China and India (Abeberese, 2017; Allcott et al., 2016; Rud, 2012a; Chen et al., 2022). 1 In response to the power shortage, firms are found to strategically invest more in self-generation, especially in large and productive firms (Alby et al., 2013; Rud, 2012b; Elliott et al., 2021), and use less flexible inputs such as intermediates and labor (Elliott et al., 2021). Among these studies, only Hardy and McCasland (2021) and Abeberese et al. (2019) explore the effects of power outages on small firms using data from Ghana. We aim to extend their work by investigating the impacts of the power crunch on SMEs in China, which has a much larger economic size than and very different economic setting from Ghana or other African countries.

Exploring the impacts of power crunch has renewed interest and bears important policy implications. Traditionally, power crunch occurs only in developing countries that have insufficient or unreliable supply (Bernstein and Hegazy, 1988). While it has been declining in the developing world due to economic development, the reliability of power system is being challenged in the developed world due to new factors such as cyberattacks, natural disasters, and the energy transition. In order to limit global warming, the developed world and some developing countries including China, have committed to transitioning their energy system toward low carbon renewables, mainly solar and wind power. Before storage technologies can be deployed economically and in a sufficient scale, the power crunch will likely occur because these renewables are variable (Wang et al., 2019). Understanding the impacts of power crunch on firms’ anticipatory investment thus reveals an extra cost of the energy transition and such information is critical for governments to make informed decisions on climate policies. Moreover, even in the developed world, power crunches are expected to occur more often. Except the war and other geopolitical accidents, the more frequent extreme climate events due to global warming and increasingly penetration of variable renewable energies may cause more power crunches than otherwise.

Unlike the existing literature, including Hardy and McCasland (2021) and Chen et al. (2022), that analyzes the contemporaneous effects of the power shortage on firm inputs and output, this study examines how firms’ willingness to invest in the short-run future responds to a current power crunch. While we have a good understanding of the size of the impacts of the electricity shortage on firm investment, relatively little is known about the dynamics, or in other words, the persistence of these impacts. The policy implications can be very different when the impact is shortlived for just one period versus long-lived for multiple periods. Our manufacturing survey from China records firms’ perception of the current power shortage and the willingness to invest in the next three months, enabling us to directly estimate the effects of the power crunch on anticipatory investment in the short-run future. 2 To the best of our knowledge, we are among the first to study how current infrastructure provision impacts firms’ anticipatory investment behaviors. In general, there is a lack of studies on firms’ anticipatory investment. Modigliani and Weingartner (1958) is a rare case that employs firm anticipatory investment information to conduct economic forecasting. However, research on what determines firms’ investment expectations (or equivalently willingness to invest, and in our words, anticipatory investment) is basically missing. 3 Hence, our research goal is to fill the gap by revealing the impacts of power crunch on firms’ anticipatory investment.

Our findings reveal that the power crunch has a significant negative impact on firms’ anticipatory investment in the short-run future. In combination with the existing negative evidence on current investment (e.g., Abeberese, 2020), it indicates that the impact of the power crunch on firms’ investment is persistent, as both firms’ current and future investment plans are disrupted. 4 It also suggests substantial underestimation of the negative effects of the power shortage if we only look at current investment reduction. Furthermore, the overall result using pooled data masks the important heterogeneity at the industry level within the manufacturing sector. For most of the industries (e.g., chemicals, smelting, machinery), the negative impact is larger than in the pooled case. The negative effect also seems to be rising with electricity dependence.

We further empirically explore potential mechanisms through which power crunch suppresses firms’ anticipatory investment. The data availability allows us to consider two channels, the channel of electricity dependence (measured by electricity intensity) and the channel of capacity utilization (measured by capital utilization). We obtain no significant evidence for the former but strong empirical support for the latter. It seems that the power crunch tends to free up production capacity and results in more idle capital stock, which in turn suppresses firms’ incentive to invest in the near future.

Next, we conduct a pair of additional analyses to address the endogeneity concern. We employ the product of industry-location average of power crunch and month-location extreme temperature span to instrument for the potentially endogenous firm-level power crunch. The IV results reconfirm a negative association between power crunch and firms’ anticipatory investment, and we obtain slightly larger magnitudes for IV estimates, suggesting that the baseline estimations include an upward bias. We also transform categorical variables in the baseline cases into binary variables to get better economic interpretations for the estimates. It reveals that firms are

The rest of the paper is organized as follows. In Section 2, we introduce our microeconomic survey data on SMEs, and provide summary statistics for key variables. We first establish the baseline regression model to examine the impacts of power crunch on anticipatory investment in Section 3, and then present the baseline regression results using linear and ordered probit estimations under different specifications. We also explore heterogeneous effects of power crunch on firms’ anticipatory investment, and look into the mechanisms through which power crunch may suppress firm investment in the near future. In Section 4, we conduct a host of additional analyses to address the concern of endogeneity and economic interpretation of the estimates, and highlight the importance of studying SMEs. We conclude and discuss policy recommendations in Section 5.

2. Data

The microeconomic survey data we use in this paper are from the monthly Small and Medium-sized Enterprises Dynamic Survey (SMEDS). 5 The SMEDS dataset includes firm-level records on production and balance sheet, as well as the responses to subjective questions for SMEs located in Zhejiang Province, China. Zhejiang Province is one of the most developed provinces in China with a significant share of SMEs. More details about the survey and its contents can be found in Cheng et al. (2021). Our sample spans the time period from August 2015 to August 2016, and focuses on the manufacturing sector, which has more than 30,000 observations. 6

The SMEDS dataset has several intriguing features. First, it is a unique dataset that includes subjective information on firms’ anticipatory investment in the near future and the perception of a current power crunch. Unlike most datasets that record only current investment, the SMEDS data survey firms’ expectation of investment in the next three months. It also collects firms’ current perception of the electricity shortage, which is another variable missing in other datasets. 7 As far as we know, the SMEDS dataset is the only data source that has information on both power crunch and anticipatory investment at the firm level. Second, the monthly frequency allows us to examine the short-run dynamic relationship between firm investment and the power crunch. For SMEs, the investment appears to be more flexible than that of large firms, given their relatively smaller size. Therefore, a more frequent data is better for exploring their investment decisions, especially with the dynamic feature of those decisions.

Third, our data for the manufacturing sector includes a complete set of disaggregated industries such as foods, textile, chemicals, smelting, machinery, and instruments. The granularity of data allows us to explore heterogeneous responses at the industry level, which is masked by the pooled analysis for the entire manufacturing sector. Fourth, the SMEDS dataset is a highly representative sample for SMEs. In Zhejiang Province, 97% of firms are SMEs, and the majority of those SMEs are private firms. Zhejiang is actually hailed as the cradle of private enterprises in China. Its liberal local institutions, favorable social environment and affluent high-skilled labor have given SMEs the large potential to grow into giant firms. 8 Since local governments regulate private firms less, relative to state-owned enterprises, our dataset provides us an ideal context to explore how the current power crunch impacts firms’ optimal decisions about investment in the near future.

Although the SMEDS dataset only has firms from Zhejiang Province, we believe the lessons learnt can be generalized. First, even being just one province in China, Zhejiang Province is a large economy. Its GDP in 2015 was around 467 billion US dollars, and can be ranked, according to data from the World Bank, as the world’s

The two primary variables of this study are firms’ anticipatory investment and the perception of the current power crunch. Both variables are constructed from firms’ subjective responses to survey questions. The dependent variable-anticipatory investment-is an ordered categorical variable (taking values from 1 to 3) from the survey question: What is the firm’s anticipation of investment in the next three months (1-decrease, 2 -no change, or 3 -increase)? The main independent variable-the power crunch-is an ordered categorical variable (taking values from 1 to 3) from another survey question: What is the firm’s perception of a current power shortage (1-no shortage, 2-medium shortage, or 3-high shortage)? The monthly frequency of our data improves the credibility of anticipatory investment. One can expect firms to have more reliable expectations about decisions to be made in a couple of months than those to be made in a year or more, especially for SMEs relative to big firms. It also contributes to the higher accuracy of subjective responses, as firms have a better understanding of the real economy within a short period compared to that over the long term. We control for other factors available in the data that may affect firms’ anticipatory investment in the short-run future, including current investment, credit constraint, productivity, and exporting participation. 10

2.1 Summary Statistics

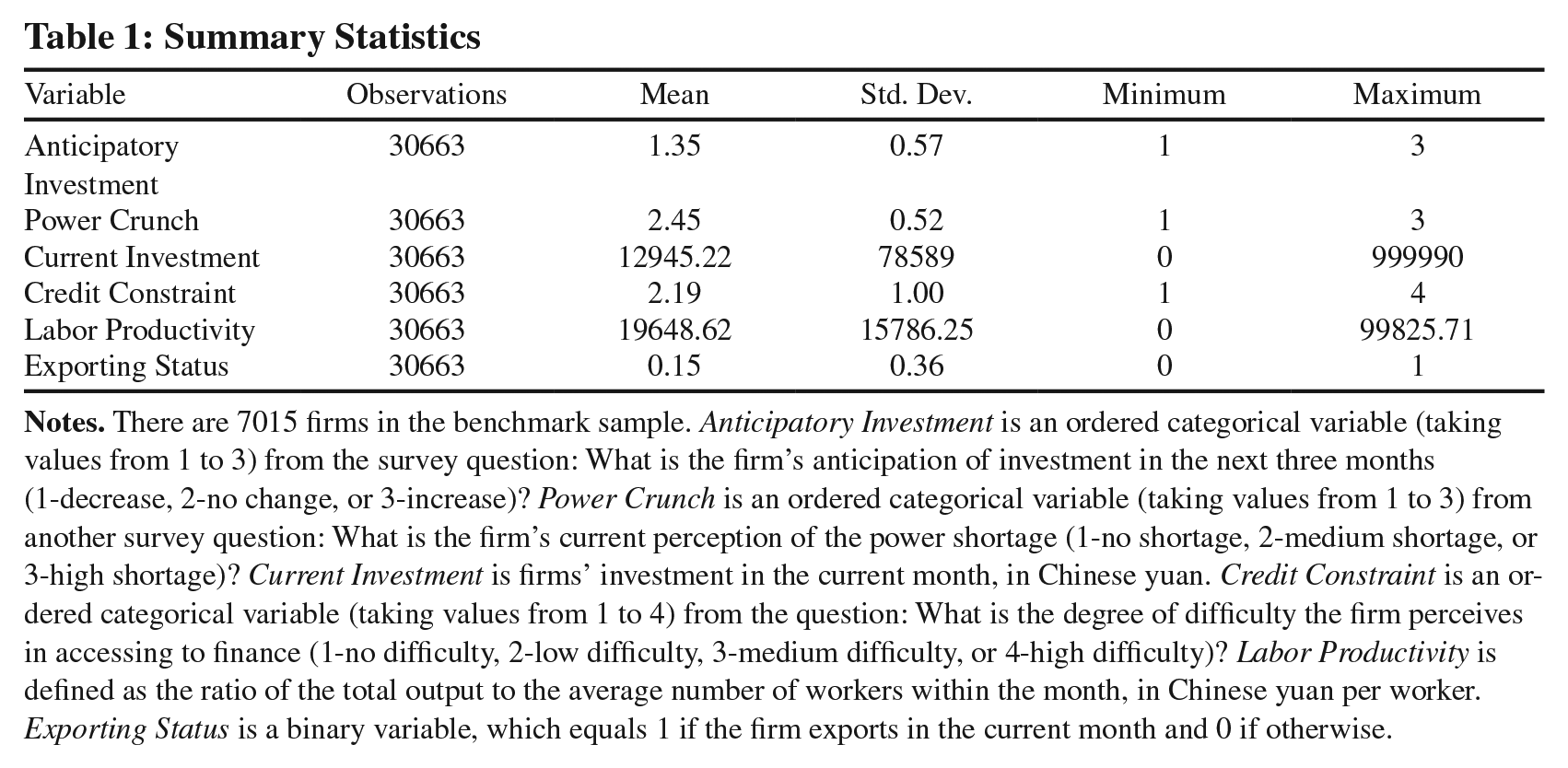

Our sample contains over 30,000 firm/industry/month observations, covering nearly all industries within the manufacturing sector and all prefecture cities of Zhejiang Province for the period of August 2015-August 2016. Table 1 presents summary statistics for the variables of our study. Anticipatory investment equals to 1.35 on average with a standard deviation of 0.57, showing a significant degree of dispersion in the data. The power crunch is less but still fairly dispersed, with a mean of 2.45 and standard deviation of 0.52 . Other control variables demonstrate even higher degrees of dispersion. Noticeably, the monthly investment is small for SMEs in our data, less than 13,000 yuan (or roughly 2,000 US dollars). This result again highlights that our focus on small and medium-sized enterprises, rather than large firms, is valuable. The share of firms that engage in exporting on monthly basis is not small, however, around 15%, reflecting the high degree of trade openness in China’s eastern coastal areas.

Summary Statistics

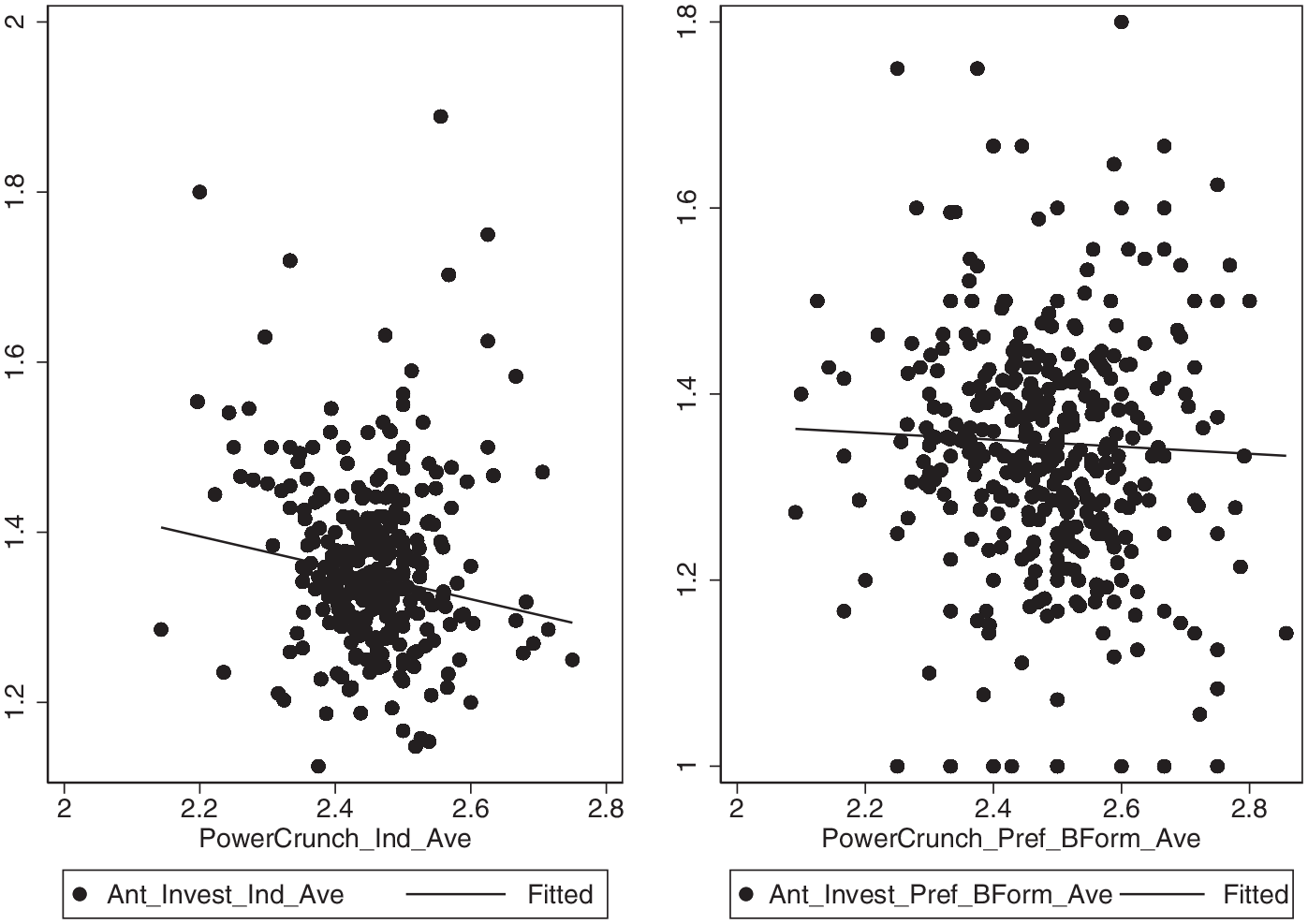

In Figure 1 we plot the correlation between firms’ anticipatory investment and the perception of a current power crunch. The left panel exhibits the correlation using industry-level averages, while the right panel displays the correlation with averages taken at the prefecture city and form of business (e.g., limited liability companies and corporations) level. The industry-level correlation is significantly negative, suggesting that a higher perceived power shortage suppresses firms’ willingness to invest in the short-run future. Although the correlation is less clear at the city and business form level, it still points to a negative relationship between the two variables. 11

Anticipatory Investment and Perceived Power Crunch

3. Empirical Analysis

Our research aim is to investigate the impacts of power crunch on firms’ anticipatory investment by leveraging the microeconomic survey data from the SMEDS. In doing so, we establish the following empirical model to regress anticipatory investment on firms’ perceived power crunch:

where AntInvest is firm i’s anticipatory investment in the next three months and PowerCrunch is firm

3.1 Baseline Regression Results

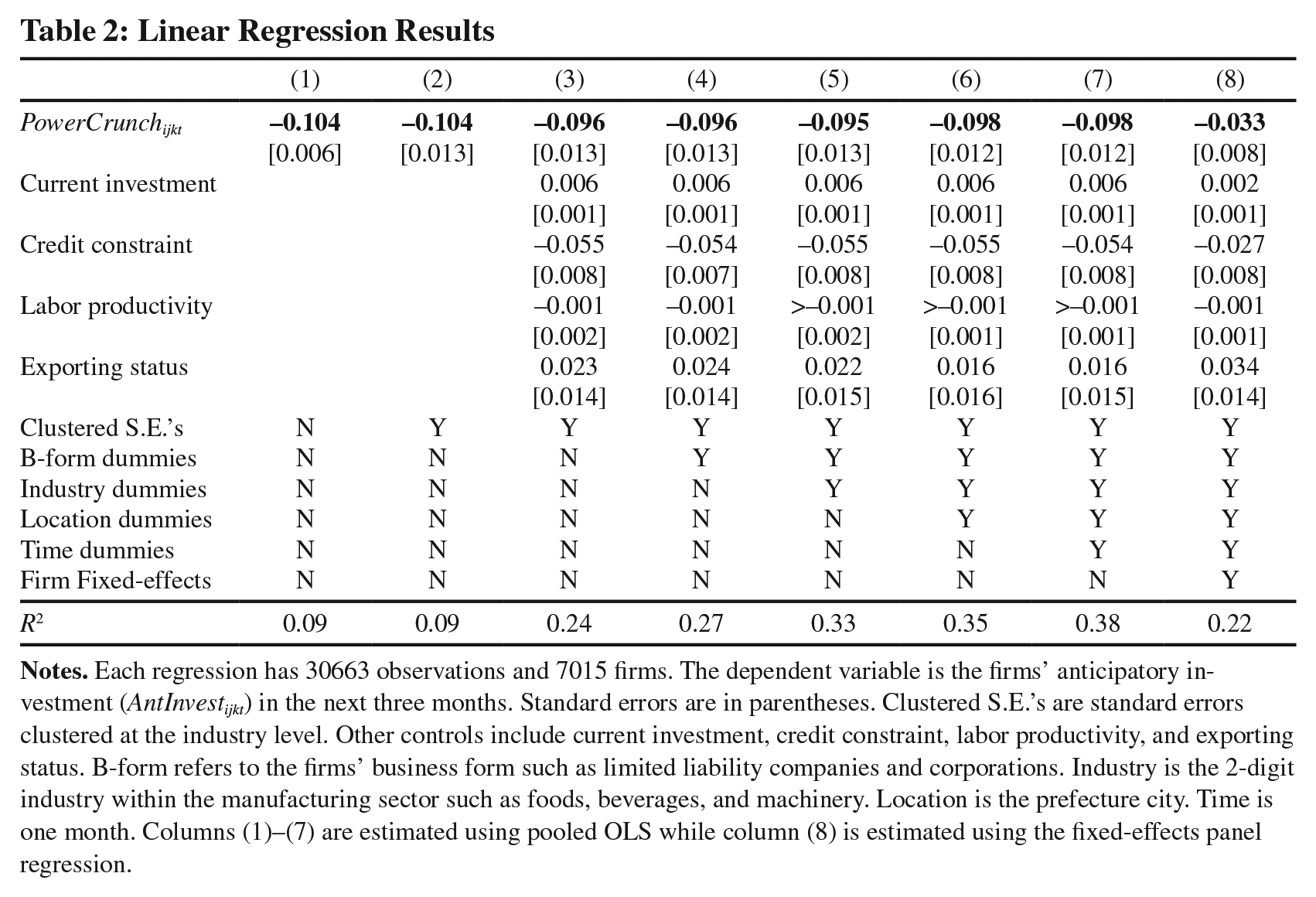

Table 2 shows the estimation results from the linear regression models. Using pooled OLS, column (1) shows a statistically significant (at the 1% level) negative relationship between firms’ anticipatory investment in the next three months and the current perception of the power crunch. Although the economic meaning of the estimated coefficient is hard to interpret as both the dependent and independent variables of interest are ordered categorical variables, a rough calculation reveals a non-negligible negative impact with the effect of the power crunch at around 7.7% of the average value of anticipatory investment. 12 The dynamic effect seems smaller than the magnitude of electricity rationing on firms’ current investment, such as that estimated in Abeberese (2020). 13 However, our study provides new empirical evidence for the persistence of the negative impacts of unreliable infrastructure provision. We show at least that the negative effect lingers over a couple of months after a current electricity shortage. Moreover, we show in Section 4 that the negative impact is actually very sizable in a binary setting.

Linear Regression Results

In column (2), we obtain the same level of statistical significance when we cluster the standard errors at the industry level. The economic and statistical significance remains largely unchanged in column (3), where we add other control variables such as current investment, credit constraint, labor productivity, and export participation to further isolate out the impacts of power crunch on firms’ anticipatory investment. 14 This situation is also true when we gradually control for the fixed effects of business forms, industries, locations, and months from columns (4) to (7). Finally, in column (8), we employ the fixed-effect panel regression to account for firm-level unobserved heterogeneity. It yields an estimate about a third of the pooled OLS estimate, suggesting that firm-level unobserved heterogeneity introduces an upward bias for the impact of the power crunch on firms’ anticipatory investment. Still, in column (8), the negative impact of power crunch is statistically significant at the 1% level.

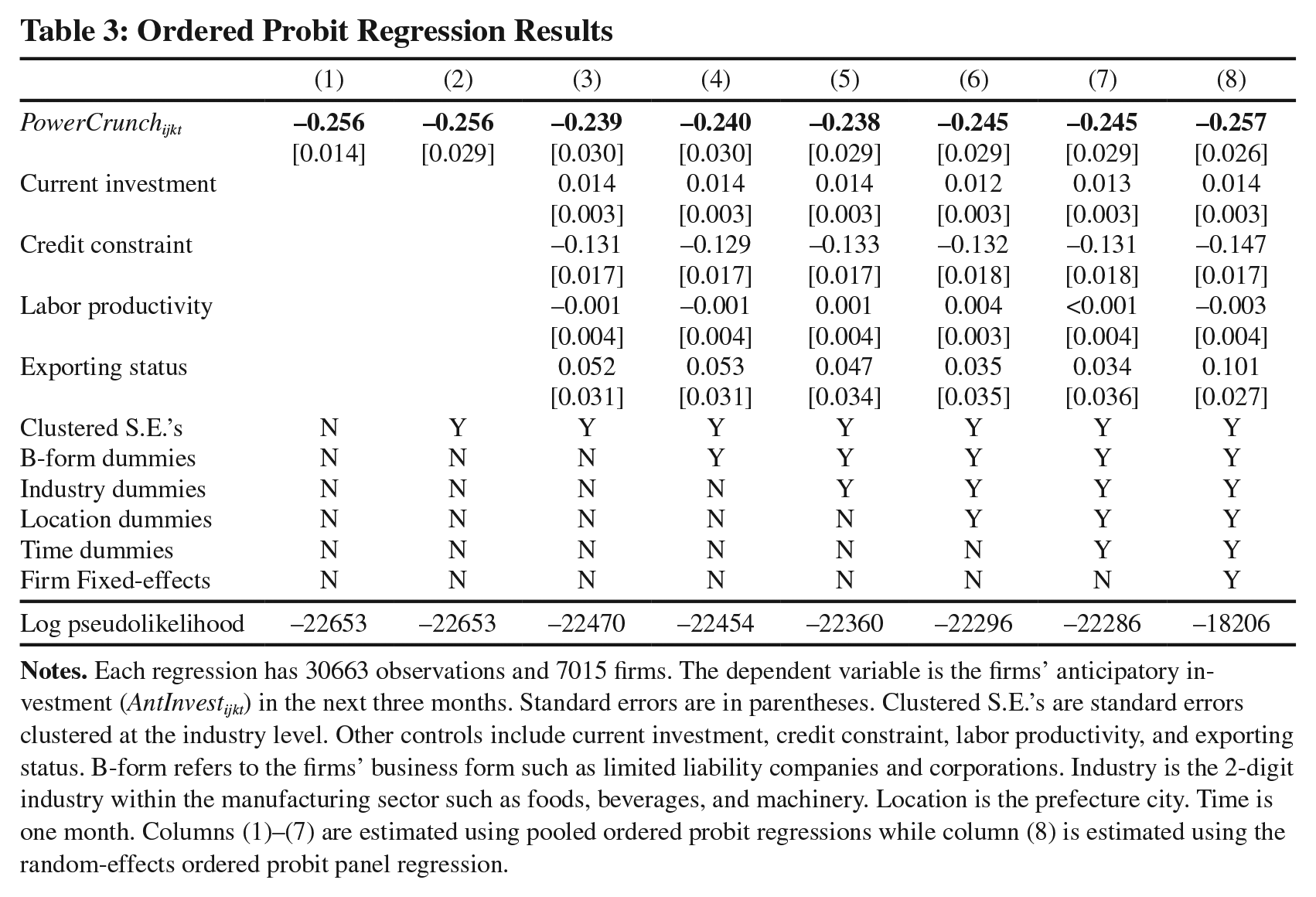

Table 3 presents results that re-estimate Equation 1 using ordered probit regressions. Similar to what we observed in Table 2, there is a statistically negative and economically non-negligible association between anticipatory investment and a current power crunch. The negative impacts of a current electricity shortage on firms’ anticipatory investment are robust in various specifications, including the panel-data random-effects ordered probit model. We are cautious to claim the effects estimated in this study are causal. However, when we implement IV regressions to mitigate the concern of endogeneity for a perceived power crunch using its industry-location average multiplying with a metric of weather condition, we obtain slightly larger but still statistically significant results. 15 We defer more discussions about the endogeneity issue to Section 4.

Ordered Probit Regression Results

3.2 Heterogeneous Results across Industries

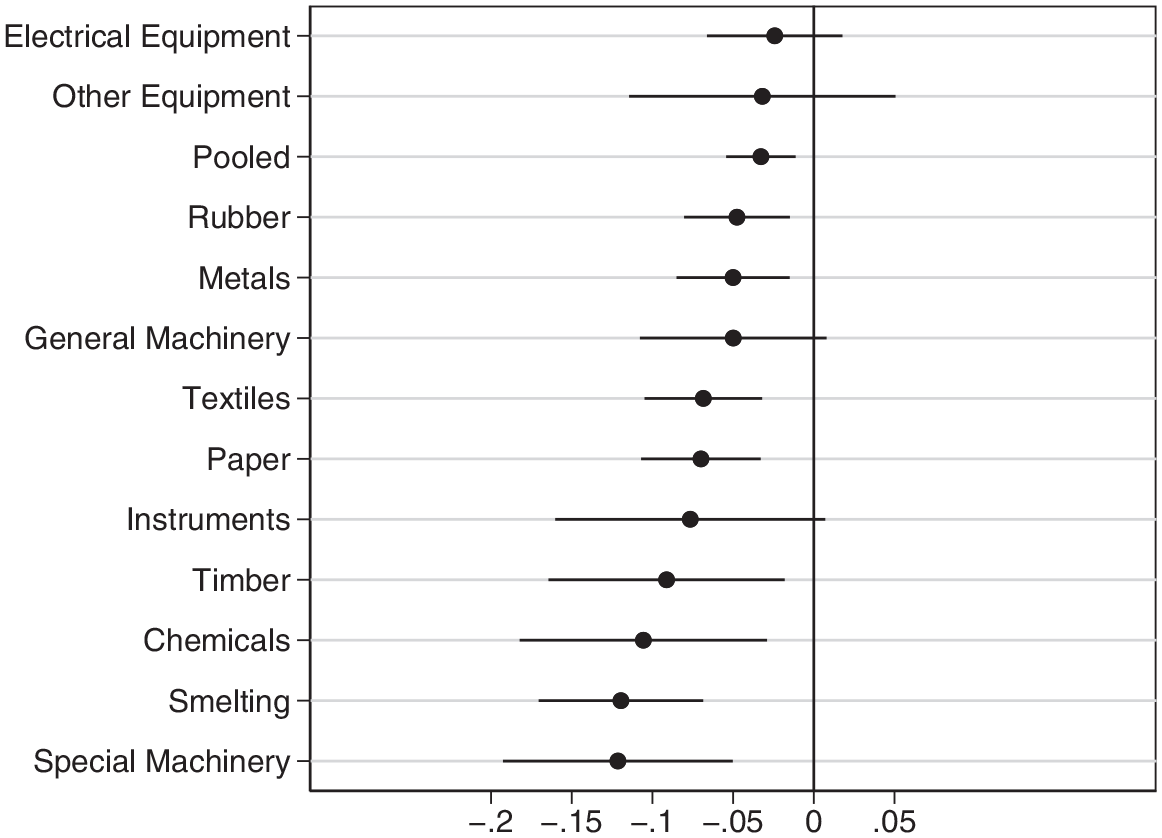

Next, we conduct heterogeneity analysis at the industry level. In total, we have 12 industries with a reliable sample size (with more than 500 observations per industry) within the manufacturing sector. 16 We estimate the impact of firms’ perceived power crunch on anticipatory investment using the panel-data regression specification as in column (8) of Table 2. The estimated coefficients by industry along with the estimate from the pooled case (i.e., column (8) of Table 2) are plotted in Figure 2. It shows that the pooled case masks a great deal of heterogeneity at the industry level. On the one hand, except for electrical equipment and other equipment, the majority of industries exhibit a larger negative impact than the pooled case. On the other hand, the pattern across industries suggests that industries that are electricity intensive or dependent on continuous electricity supply (in other words, electricity dependent), such as chemicals and smelting that cannot be stopped or started in a short time frame, take much larger hits from the negative shock to the power supply.

Estimated Coefficients by Industry

Our industry-level heterogeneous analysis not only shows that there exist differential impacts of power crunch on anticipatory investment across industries, but also implies that the effects of power crunch may work through the lens of firms’ dependence on electricity. Motivated by the latter point, we explore the mechanisms through which the power crunch affects firms’ desire to invest in the future in more depth below. Largely depending on the availability of micro data in our survey, we investigate two competing stories: the channel of electricity dependence versus the channel of capacity utilization.

3.3 Mechanisms: Electricity Dependence vs. Capacity Utilization

We consider two potential mechanisms through which power crunch may pose negative impacts on firms’ anticipatory investment. The first one is the channel of electricity dependence, directly motivated by the observation we obtain from Figure 2. The electricity dependence story relies on the reasoning that firms with a higher degree of dependence on electricity in production is more vulnerable to power shortage, and hence more reluctant to expand investment when they perceive power crunch. Using variables from the SMEDS dataset, we define electricity dependence—ElecDependence ijk -as the ratio of firms’ electricity consumption to total output, in the same spirit of the widely used energy intensity. A higher value of ElecDependence ijkt means that the manufacturing firm is more dependent on electricity in producing goods.

The second mechanism is the channel of capacity utilization. The capacity channel refers to the story that power crunch frees up production capacity and leads to more idle capital stock, and hence reduces firms’ incentive to increase investment in the future. If the capacity story is true, we expect firms with more unused capacity (i.e., lower capacity utilization) to respond more negatively to power crunch. Extant studies on firms’ optimal investment behavior also identify capital utilization as a relevant factor shaping investment behaviors (see, for example, Aminu et al., 2018). In our SMEDS dataset, we have a firm-level recording of capital utilization rate. We define unused production capacity-UnusedCap jjk -as one minus capital utilization rate. The assumption behind the definition of unused production capacity is that a higher rate of capacity utilization is accompanied with a higher rate of capital utilization, which is generally the truth in the manufacturing sector.

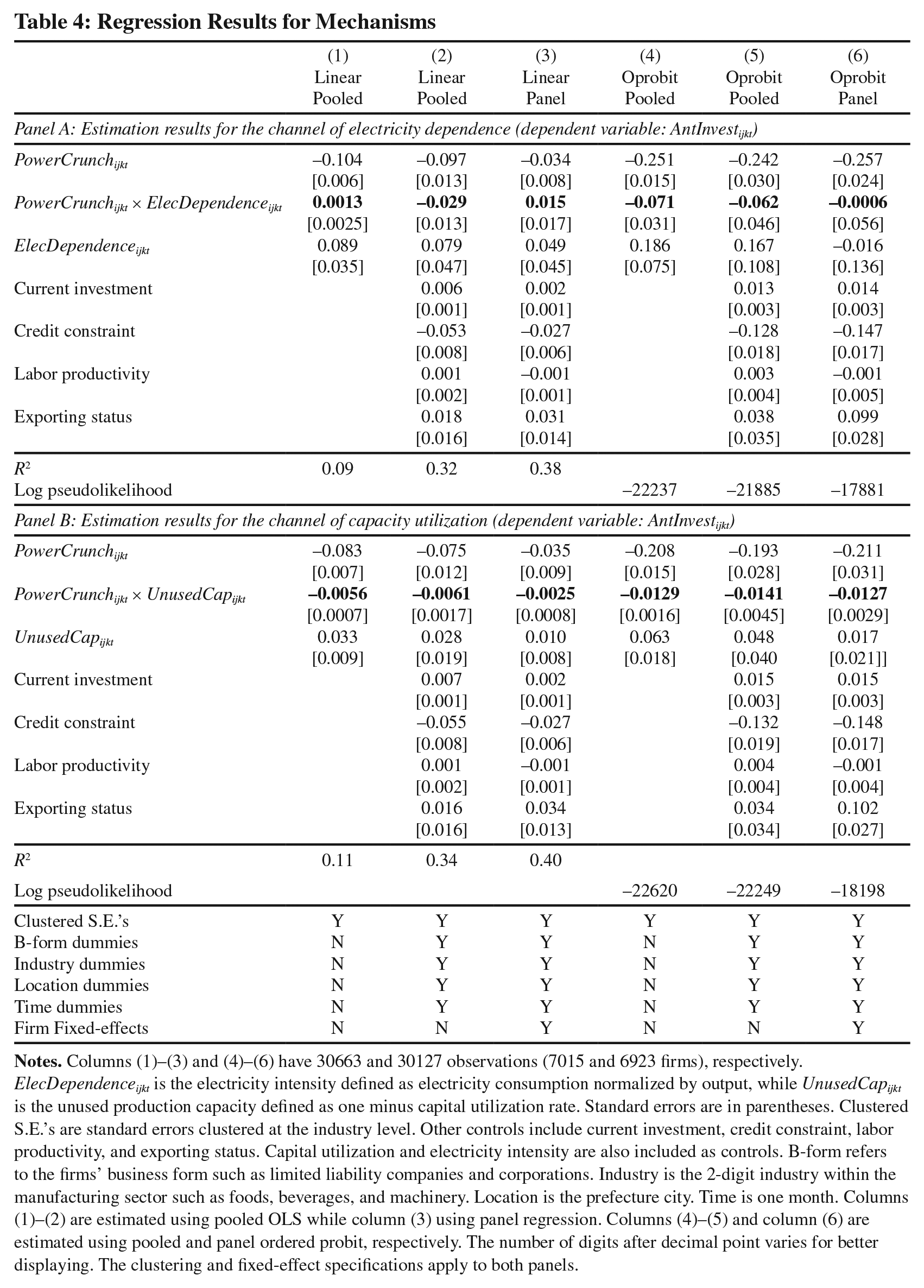

Table 4 shows the results for the two potential mechanisms.

17

Columns (1)-(3) are estimated using linear model. We fail to find supporting evidence for the first channel—electricity dependence-as panel A reveals that the interacted term (

Regression Results for Mechanisms

ElecDependence ijkt is the electricity intensity defined as electricity consumption normalized by output, while UnusedCap ijkt is the unused production capacity defined as one minus capital utilization rate. Standard errors are in parentheses. Clustered S.E.’s are standard errors clustered at the industry level. Other controls include current investment, credit constraint, labor productivity, and exporting status. Capital utilization and electricity intensity are also included as controls. B-form refers to the firms’ business form such as limited liability companies and corporations. Industry is the 2-digit industry within the manufacturing sector such as foods, beverages, and machinery. Location is the prefecture city. Time is one month. Columns (1)-(2) are estimated using pooled OLS while column (3) using panel regression. Columns (4)-(5) and column (6) are estimated using pooled and panel ordered probit, respectively. The number of digits after decimal point varies for better displaying. The clustering and fixed-effect specifications apply to both panels.

Although we find no evidence to support the intuitive observation we get from Figure 2 through the broad electricity dependence channel, it may work through more specific channels we are unable to test using the SMEDS dataset. A promising one may be the channel of electricity reliability. Firms in the chemicals and smelting industries may not just require a large amount of electricity, but also require a reliable supply of electricity without interruptions as the discontinuation of the chemical or physical processes can pose large economic losses and even compromise safety. For example, the chemical process industry requires constant and high quantity electricity supply due to their continuous production process (Riese et al., 2014). Unfortunately, the SMEDS data have no variables to characterize firm-level dependence of electricity reliability, making it impossible to test the specific channel directly. Nevertheless, our survey data help us rule out the broad channel of electricity dependence and supports the channel of capacity utilization. Future work may be done to explore more specific channels such as the electricity reliability when better micro dataset is available. 18

4. Additional Analyses

In this section, we conduct a host of additional analyses: (i) to address the endogeneity concern; (ii) to deal with the economic interpretation of estimated coefficients; and (iii) to highlight the importance of studying SMEs, relative to big firms. We show that our baseline regression results fare well in the exercises to deal with the endogeneity concern, and our baseline estimates bear high economic significance with a large reduction in the likelihood of investing in the next three months for firms that perceive power crunch in the current month. Moreover, we provide evidence for the importance of studying SMEs by showing that smaller firm size leads to disproportionately larger damage caused by the power crunch.

4.1 The Endogeneity of Power Crunch

Our main explanatory variable-power crunch-tends to be endogenous due to reasons such as unobserved confounding factors. For example, a persistent positive shock to the nontradable sector (e.g., construction) of the local economy may drive up firms’ investment in the future but also raises firms’ perception of power crunch as it induces more competition in the demand for power. However, a persisting negative shock to the local oil supply may raise firms’ perception of power crunch but suppress firms’ anticipatory investment. To address endogeneity concerns like those, we construct an instrumental variable for power crunch.

The instrumental variable we adopt is a product of two components: industry-location average of power crunch and month-location weather condition. Specially, the weather condition is the span of extreme temperature at the county level and monthly frequency. We compute the extreme temperature span as the difference between extreme high temperature and extreme low temperature for a given month and county. The monthly extreme high temperature and low temperature are the averages over 1981-2010 for a given month and county. The temperature data comes from the China Meteorological Data Service Centre. 19 For Zhejiang Province, we have access to the data from 1981 to 2010. 20

The relevance of our instrumental variable comes from an economic story of the demand side. Conceptually, a larger span of extreme temperature induces higher demand for electricity from the households as they need to run their A/C more to get heat in the cold weather and cooling in the hot weather. 21 All else being equal, this implies that firms face more competition from the households in demanding for electricity. Since the Chinese government weighs social stability more against economic growth (Berkowitz et al., 2017), the local governments are more likely to put a ration on the supply of power to firms than to households. As a result, firms are more likely to perceive power crunch during a period of time with a larger span of local extreme temperature. This establishes the economic relevance of the instrumental variable.

It is worth mentioning that the current power shortage crisis in China’s Sichuan Province provides a perfect example for what we have theorized above. On August 14th, 2022, on behalf of the provincial government, the Sichuan Provincial Economic and Information Department released an official emergency notice that orders firms to cut power usage and even suspend operation in favor of electricity use by households. 22 Similar emergency notices have been administered during the energy crisis in September and October of 2021 when skyrocketing coal prices in China induced a nationwide power crunch.

Notice that our economic story is essentially the same as the one elaborated in Fisher-Vanden et al. (2015), where they employ cooling and heating degree days (above and below

To increase the variation of our instrumental variable, we add the second component by multiplying the month-location extreme temperature span with the industry-location average of power crunch observed in our data. The rationale for employing the average at the industry and location level to instrument for firm-level survey responses is that the industry-location average characterizes features at the more aggregate level and arguably exogenous for individual firms, and these features are relevant for a given firm because it belongs to that specific location and industry (Reinikka and Svensson, 2006; Fisman and Svensson, 2007; Chen et al., 2010).

23

Hence, the final form of our instrumental variable is the product of industry-location average of power crunch and month-location extreme weather span. We denote the instrument as Temp_IV

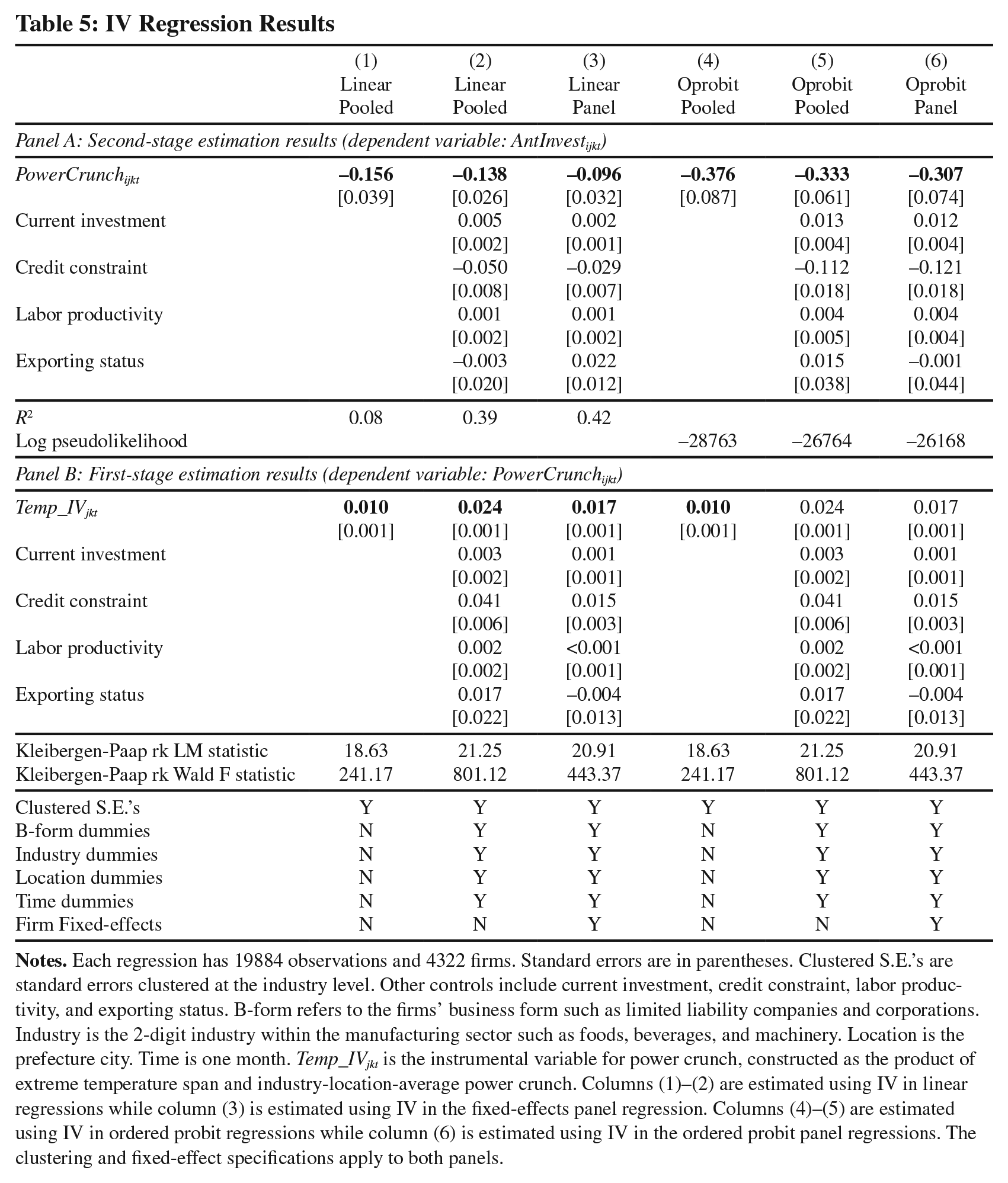

Table 5 presents the regression results using the instrumental variable constructed above. Columns (1)-(3) are estimated using linear models, while columns (4)-(6) using ordered probit models. 25 Two quick takeaways from Table 5. First, the first-stage estimation results show that our instrumental variable is positively correlated with power crunch, in a statistically significant way. It confirms our conjecture that a larger span of extreme temperature drives up the demand competition for electricity between households and firms, and thus makes firm perceive or subject to a higher degree of power crunch. The Kleibergen-Paap rk Wald F statistic is high and suggests that we do not suffer from weak instrument concern in any significant way.

IV Regression Results

Second, the second-stage results essentially resonate with what we find in Table 2 and Table 3 where the instrumental variable is not used. It shows clearly that the power crunch has a negative impact on firms’ anticipatory investment. Although the IV estimates produce a slightly inflated magnitude, the results are very consistent with our baseline cases. The slight larger magnitude of IV estimate may reflect that the omitted confounding factors such as a persistent positive shock to the local nontradable sector tends to generate a positive correlation between power crunch and firms’ desire to invest in the near future. Therefore, when the bias is corrected in the IV estimation, the negative impact of power crunch on firms’ anticipatory investment is even larger.

4.2 The Economic Significance of Power Crunch

We next conduct further analysis to provide more information on the economic significance of our baseline estimates in Table 2 and Table 3. Specifically, we transform categorical variables into binary variables to obtain better economic interpretations for the estimated coefficients. Before we get into the details about the transformation, we want to caution the readers that we prefer using original categorical variables in the baseline regressions for two reasons. First, the original categorical variables are more reliable as it directly comes from the survey questions without any manipulation, which is a more accurate reflection of firms’ perception and anticipation. Second, as we discuss in a footnote below, there are multiple ways to define binary variables out of the categorical variables and it is difficult to determine which way is better. Nevertheless, we still want to provide some direct evidence about the economic significance of the power crunch for firms’ anticipatory investment, and this motivates us to do the further analysis in this subsection.

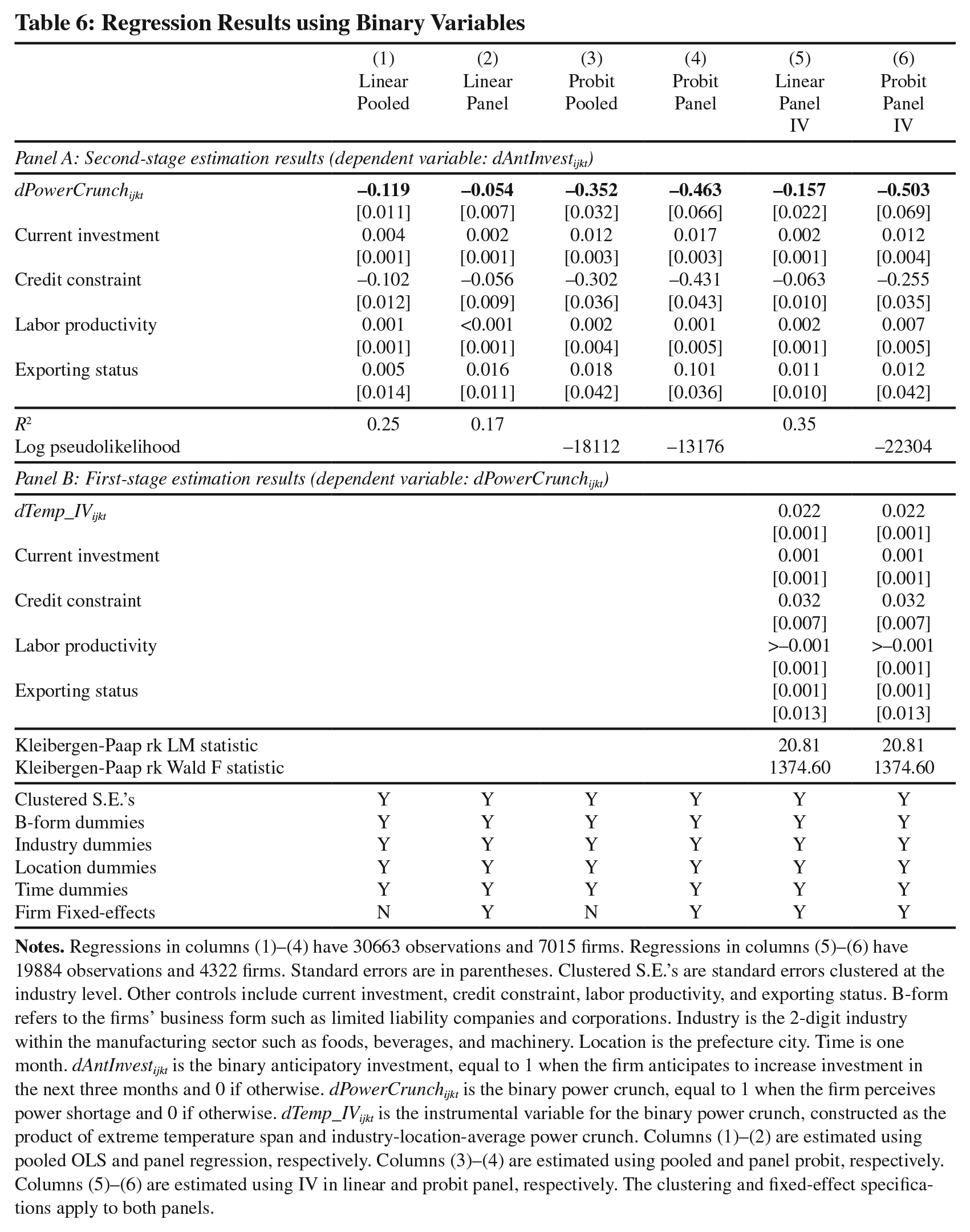

We transform three categorical variables into binary ones. They are anticipatory investment, power crunch, and credit constraint. For anticipatory investment, we re-define it as a binary variable-dAntInvest

ijkt

-that equals to 1 if the firm expects to increase investment in the next three months and 0 if otherwise. For power crunch, re-define it as a binary variable-dPowerCrunc

The estimation results using binary variables are presented in Table 6. Columns (1)-(2) are estimated using linear probability models, and suggest that firms are 5% to 12% less likely to increase investment in the next three month if they perceive power crunch. The IV estimation of the linear probability model in column (5) further confirms the result, and it produces a larger negative impacts as the reduction in likelihood of increasing future investment rises to 16%. The first-stage result in column (5) confirms again the strong relevance of our instrumental variable. By contrast, columns (3)-(4) are estimated using probit models to better fit the binary dependent variables. The nonlinear probit models generate even larger negative coefficients, ranging from 35% to 46% depending on the specifications. When we combine the instrumental variable with the probit model in column (6), we obtain a reduction in probability to increase future investment as large as 50%. Overall, Table 6 reassures us about what we learn from the baseline Table 2 and Table 3: when a firm perceives power crunch, it cuts anticipatory investment in a way that is both statistically and economically significant.

Regression Results using Binary Variables

The large negative impact of power crunch on firms’ anticipatory investment that we reveal using the microeconomic survey data on SMEs may be attributable to three reasons. One explanation for the sizable negative impact hinges on the horizon we have in the SMEDS data. Recall that our micro dataset is at the monthly frequency, and the anticipatory investment is investment in the next three months (i.e., the next quarter). The short-run feature tends to make firms’ decision very volatile, and hence generating highly responsive results. For firms, investment is not urgent and thus can be postponed, which is reflected as a sharp reduction in the short run. If the horizon is year or even longer, firms may have more time to adjust its investment in a smooth way and we may observe less sizable impacts. Alternatively, we can think of the results in the spirits of impulse responses. It is reasonable to have temporary large effects in the near future, but in the long run, the responses fade as firms’ investment decisions move back to the steady state. This also helps to reconcile our sizable impacts in the binary setting with the magnitudes documented by Abeberese (2020) for current investment using less frequent data.

Second, since our data are for SMEs, their small size may contribute to the large negative response of future investment to power crunch. On the one hand, small size creates more flexibility for SMEs to adjust investment decisions as they tend to be lighter in fixed assets. On the other hand, small size makes SMEs less capable to afford profit losses as they may lack the hedging product portfolios that large firms generally have. Hence, the response of SMEs may be more substantial than that of large firms when they face a negative shock to power supply. Also recall that the investment is irreversible (Bernanke, 1983), which reduces the possibility to recover damages caused by power crunch and further inhibits SMEs’ incentives to invest more in the future if they perceive power crunch.

The third explanation for the large negative impact may relate to the political economy of local government officials in China. Due to its specific institutional arrangements, local government officials in China have strong incentives to sacrifice firms’ economic performance for social reasons such as prioritizing the electricity needs of households to keep society stability (Kato and Long, 2006). However, when making such decisions, local governments are more likely to sacrifice firms of smaller size as big firms contribute substantially more to local fiscal revenues and on average hire more workers per firm. The stability of big firms also bears strong symbolic meaning, and hence big firms have disproportionately large weights in the decision process of local officials. When SMEs expect that local governments may be more likely to sacrifice them during the period of power crunch, naturally, they are less likely to invest in the future as the stake of not being able to reap the benefits of investment due to disruptions caused by power crunch is high.

Regression Results using Binary Variables

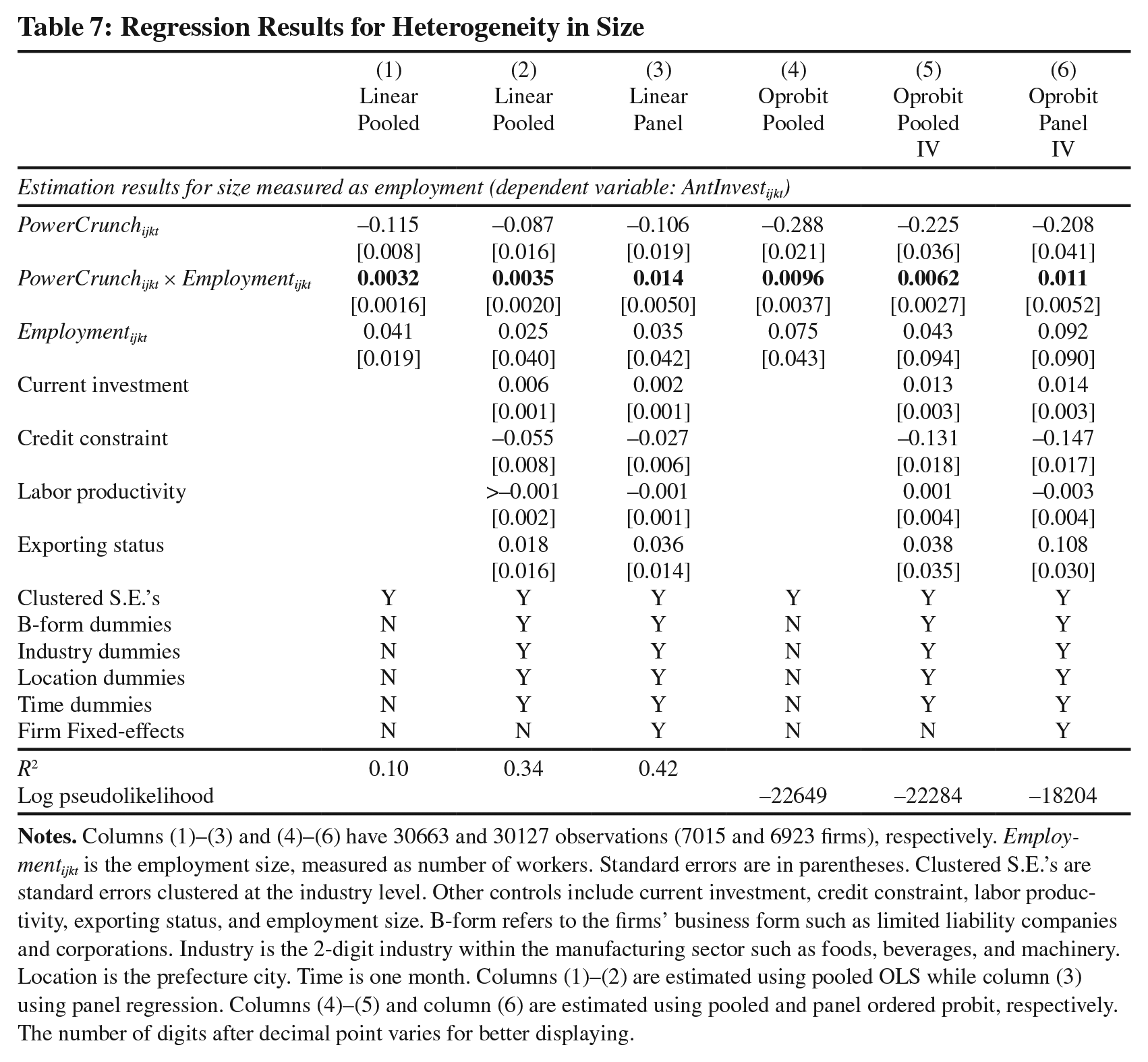

4.3 The Importance of Studying SMEs

Motivated by the fact that SMEs suffer a sizable negative impact of power crunch on future investment, we further highlight the importance of caring about SMEs, relative to big firms, by exploring whether size matters. In doing so, we conduct a new dimension of heterogeneity analysis for our baseline results using firm size.

Table 7 presents the estimation results for heterogeneity in size. For the reason of maximum data availability, we measure size as employment (denoted as Employment

Regression Results for Heterogeneity in Size

The buffering effect created by firm size clearly highlights the importance of caring about SMEs, especially tiny firms, in the period of power crunch. The magnitude of the negative impacts of power crunch on firms’ anticipatory investment increases with a reduction in firm size. It implies that SMEs and particularly tiny firms suffer disproportionately more damage in future investment when they perceive a power crunch. Uncovering this disproportionately larger cost for SMEs is just the first step, more importantly, it strongly calls for more attention and resources directed to help SMEs survive during the difficult time of electricity supply, relative to big firms. Although the microdata we have does not allow us to compare the negative impacts suffered by SMEs and big firms directly, our heterogeneity analysis with respect to firm size still argues profoundly that firm size matters as a smaller size comes with a larger damage. The finding hence further supports our focus on SMEs, and suggests that local government policies should lean more towards SMEs. The caring for SMEs is getting even more imperative as China (and arguably many other economies) has been witnessing more and more frequent power crunches arising from geopolitical risks and extreme weather conditions in the most recent years.

5. Concluding Remarks

Power crunch, a typical energy challenge in the developing word, re-emerges in the developed world due to extreme weather conditions, cyberattacks, and the commitment to energy transition. While there are many studies on these issues in the literature, little is focused on small and medium-sized firms that are the backbone of the labor market in most of the world’s economies. Moreover, much of the extant studies have focused on the impacts on contemporaneous variables such as current investment. In this study, using microeconomic survey data for Chinese manufacturing SMEs, we contribute to the literature by examining the persistence of impacts on investment due to power crunch through the lens of firms’ willingness to invest (or in our terminology, anticipatory investment).

The results show that there is a significant negative relationship between a power crunch and SMEs’ anticipatory investment in the short-run future. The negative impact of the power crunch appears to be more pronounced among industries that are electricity dependent. Our findings seem to indicate that the negative shock to electricity provision has a persistent impact on firms’ investment decisions, at least for SMEs over the span of a couple of months and the impacts are heterogeneous across industries. Further explorations of the underlying mechanisms show that the negative effect is more likely to work through the channel of capacity utilization rather than that of electricity dependence. However, a caveat we want to make is that our empirical work cannot fully rule out the possibility of more specific channels of electricity dependence such as the dependence on electricity reliability. What we truly rule out using our data is the electricity intensity aspect of the dependence on electricity. In other words, we rule out the quantity component but not the quality (in terms of continuous and uninterrupted supply) component of electricity dependence. We leave it for future work that may have access to better survey data with direct measures related to electricity reliability.

Our baseline results slightly underestimate the magnitude of the negative impacts of power crunch on firms’ anticipatory investment when compared with those from the IV estimations that address the potential endogeneity of perceived power crunch. We also provide further evidence for interpreting economic significance of the power crunch by transforming categorical variables into binary ones. We find that SMEs in our sample are up to 50% less likely to increase investment in the next three months if they perceive power crunch. This is an important piece of cost information that policymakers can factor in when designing their energy transition plans that may affect electricity reliability. Furthermore, we find that the anticipatory investment by firms of smaller size are more vulnerable to power crunch as they suffer disproportionately more than their larger counterparts.

Our results suggest that given the climate change and the energy transition, governments need to initiate policies to mitigate the persistent negative impacts on investment originated from an increasing likelihood of power crunch. Technology solutions that can stabilize the power system, such as energy storage and smart grids, could be deployed earlier in recognizing this extra cost revealed in this paper. Moreover, the impacts are industry specific, suggesting that tailored measures to improve the reliability of the electricity supply at the industry level would be more effective than across-the-board measures. Demand response that promotes voluntary reduction of electricity use during peak demand is highly desirable to mitigate the severity of power crunch.

The policy should also protect the confidence of SMEs. Typically, local government tends to prioritize large firms due to their scale of economic outputs and size of employment. However, large firms can better manage power crunch than SMEs because they can use revenues from other regions or other business units to support those affected by power crunch. In contrast, SMEs do not have other branches to hedge, and thus financial loss could threaten their survival. Therefore, policies should project SMEs even more than large firms. Our results also bear strong implications that the mainstream media and policy makers need to investigate and care more about the fate of SMEs, not just large firms, during periodic energy crises.

The financial sector can play a significant role in mitigating the negative impacts of power crunch on SMEs’ by promoting sustainable energy practices and reducing their dependence on the grid (May and Neuhoff, 2021). Financial institutions can offer financing options to help SMEs reduce their energy consumption and dependence on the grid. This can include financing for energy audits, retrofits, and upgrades, which can help SMEs reduce their energy usage and costs. Financial institutions can also help SMEs reduce their dependence on the grid through investing in renewable energies, micro-grids and energy storage systems.

Given the positive externalities of SMEs on the labor markets and local economies, governments can play a role in boosting SMEs’ confidence when they perceive power shortages. Governments and financial institutions can work together to provide financing and technical support to SMEs, helping them to overcome the barriers to accessing sustainable financing and energy-efficient technologies.

Moving forward, the study can be enriched with survey data for a longer period of impact and covering more recent years when power crunch resurfaces as a major economic concern (which is an innocuous limitation of our sample), in other countries or with the consideration of more industry-specific factors such as electricity reliability requirements at the firm or industry level. Those results can provide further guidance for setting energy transition action plans in other countries and/ or improve the policy making in China.

Supplemental Material

sj-docx-1-enj-10.5547_01956574.45.3.dche – Supplemental material for The Power Crunch and Firms’ Anticipatory Investment: Evidence from Manufacturing SMEs in China

Supplemental material, sj-docx-1-enj-10.5547_01956574.45.3.dche for The Power Crunch and Firms’ Anticipatory Investment: Evidence from Manufacturing SMEs in China by Dong Cheng and Xunpeng Shi in The Energy Journal

Footnotes

Appendix

This appendix includes the following three items.

Acknowledgements

We thank two anonymous referees for insightful comments that greatly improve the quality of the paper. Shi acknowledges research support from National Natural Science Foundation of China (No. 72174056). The authors thank Qiyue (Mary) Zhang for excellent research assistance. All errors are our own.

1.

2.

Anticipatory investment refers to the amount of capital firms are willing to invest in the future.

3.

Notice that we use the three terms, investment expectation, willingness to invest, and anticipatory investment interchangeably in this study for the convenience of elaborations.

4.

6.

We want to note that the use of a sample covering 2015-2016 when power crunch was not as severe as 2021-2022 does not harm our main findings as the results we find are already very statistically and economically significant, which should be even more significant in a more challenging period of time, especially for SMEs. In fact, China has been facing a constant threat of power crunch in the past decades for a couple of reasons. We provide two well-recognized reasons here. First, the Chinese economy relies heavily on investment, leaving a plenty of room for imbalance between power supply and demand as the macroeconomy fluctuates. Investment turns out to be one of the most volatile macroeconomic variables, and demand for energy by new investment projects in good economic times can easily drive a big wedge between inflexible supply and flexible demand, and therefore results in power shortages. Second, China’s power supply mainly comes from coal, coupled with a regulated power price (which is generally lower than market-determining prices), generating a disincentive for coalfired power plants when the cost of coal rises during surging demand and hence the profit margin is squeezed or even negative.

7.

In this study, we employ firms’ perceived power crunch rather than firms’ reported incidence of power outages such as that in ![]() for two reasons. First, the reported or realized incidence of power outages is not available in our microeconomic data that we leverage to study the behavior of firms’ anticipatory investment under power shortages. Second, the reported incidence of power outages may significantly underestimate the threat of power shortage and therefore its impacts on firm investment. Since investment can be costly and is generally irreversible, firms are highly likely to react to any signs of power crunch before a power outage actually occurs.

for two reasons. First, the reported or realized incidence of power outages is not available in our microeconomic data that we leverage to study the behavior of firms’ anticipatory investment under power shortages. Second, the reported incidence of power outages may significantly underestimate the threat of power shortage and therefore its impacts on firm investment. Since investment can be costly and is generally irreversible, firms are highly likely to react to any signs of power crunch before a power outage actually occurs.

8.

A leading example is the conglomerate Alibaba, which started in 2003 as a tiny internet firm with only 18 employees in Hangzhou, the capital city of Zhejiang Province.

9.

According to the more recent data from the World Bank, in 2021, Zhangjiang’s GDP is close to the world’s 16th largest economy, Indonesia. Moreover, its 65 million population is larger than Tanzania, the world’s 22 largest country in terms of population.

10.

See Aw et al. (2008) and ![]() , among many others, for additional theoretical discussions about the relationship among these variables and firms’ investment dynamics.

, among many others, for additional theoretical discussions about the relationship among these variables and firms’ investment dynamics.

11.

The relevance of power in firms’ investment and production decisions has been widely discussed in the literature. See, for example, Aminu (2018, ![]() ).

).

12.

Note ![]() , i.e.,

, i.e.,

13.

For comparison, we also conduct regressions for current investment, and find significant negative impacts of power crunch on current investment, which are in line with the extant literature (e.g., Abeberese, 2020). The results for current investment are presented in Table A.1 of the ![]() . The significant negative impacts of power crunch on both current and anticipatory investment clearly demonstrate the persistence of the negative investment effect of power crunches.

. The significant negative impacts of power crunch on both current and anticipatory investment clearly demonstrate the persistence of the negative investment effect of power crunches.

14.

We include firms’ current investment to account for the inertia of investment decisions. One may be concerned about the endogeneity of this independent variable. Excluding it from the set of control variables or instrumenting it with one-month lagged investment (which also reduces the number of observations) does not significantly change our estimation results.

15.

The selection of instrumental variables is based on the common practice in empirical studies of development economics. See, for instance, Reinikka and Svensson (2006) and Fisman and Svensson (2007) for the industry-location component and ![]() for the weather component

for the weather component

16.

Notice that we have 30 industries within the manufacturing sector in our data, and 18 out of these 30 industries have observations less than 500 observations. The 18 manufacturing industries that are excluded in the heterogeneity analysis at the industry level are food, beverage, tobacco, feed, sewing, furniture, printing, cultural-educational-sports, crafts-arts, powersteam-water, petroleum, coking-gas-coal, medical, chemical fiber, plastic, construction materials, other nonmetal minerals, and other manufacturing.

17.

To further reduce the endogeneity concern of the heterogeneity that is defined at the firm level, we also re-define the two dimensions of heterogeneity (i.e., electricity dependence and capital utilization) at the industry level and re-run all regressions in ![]() . These additional results for the mechanisms are presented in Table A.2 of the Appendix. Our main findings in Table 4 survive this robustness check.

. These additional results for the mechanisms are presented in Table A.2 of the Appendix. Our main findings in Table 4 survive this robustness check.

18.

Notice that, due to data unavailability, we are unable to explore the role of generator ownership. During periods of power shortage, firms may fare better if they have invested in self-generation, and firms may also be more likely to buy generators. See, e.g., Alby et al. (2013) and Reinikka and Svensson (2002) for supporting evidence, and ![]() for no evidence. Although we cannot say much about self-generation, our focus on SMEs may mitigate the concern as SMEs are less likely to own generators, relative to big firms.

for no evidence. Although we cannot say much about self-generation, our focus on SMEs may mitigate the concern as SMEs are less likely to own generators, relative to big firms.

20.

The fact that the time period of weather data (January 1981-December 2010) is earlier than our survey data (August 2015-August 2016) strengthens the exogeneity of our instrumental variable as it excludes the possibility that contemporaneous economic activities may affect weather condition.

21.

22.

23.

We conduct a battery of robustness checks for the selection of IV. Specifically, we consider two alternative instrumental variables, where the first one only relies on the exogenous extreme temperature span, and the second one is the product of extreme temperature span and initial-month (i.e., August 2015) industry-location average of power crunch. To further increase the credibility of the exclusion restriction in our benchmark IV, we also exclude industries that are sensitive to extreme weather conditions (i.e., food manufacturing, beverage manufacturing, tobacco processing, and feed processing). The additional results for IV regressions can be found in Table A.3 of the ![]() . Our mains results remain unchanged in those robustness checks.

. Our mains results remain unchanged in those robustness checks.

24.

There are two caveats about the instrumental variable that we construct in this study. First, we need the assumption that the electricity supply is fairly fixed to make the story of demand side work well. This is not a crazy assumption because our time span is a month, a relatively high frequency and short period of time, and thus the adjustment of supply is quite limited. Second, we implicitly assume that households are equipped with housing appliances such as A/C to deal with extreme whether. This is a reasonable assumption because Zhejiang Province is one of the richest provinces in China. Its GDP per capita was 11,878 US dollars in 2014 (Zhejiang Province Bureau of Statistics, 2015), much higher than China’s overall GDP per capita that was 7,679 US dollars in 2014 (National Bureau of Statistics of China, 2015).

25.

Notice that the number of observations drops from 30,663 to 19,884 because only a subset of counties in Zhejiang Province have extreme temperature data compiled by the China Meteorological Data Service Centre.

26.

We also conduct a robustness check by re-defining anticipatory investment in another way. To be specific, we let dAntInves

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.