Abstract

Background

The sustainability of the National Health Insurance (NHI) program heavily relies on the premium of its member. The negligence of a large number of members at pay the premium lead to the failure of the Social Security Agency for Health (SSAH) to deliver its services. This study aims at analyzing important factors that influence the sustainability of premium payment of NHI's self-enrolled members in the Jakarta Greater Area.

Design and methods

This study performed an econometric analysis from the panel and the same respondent's data in 2015 and 2017. The population of the study was NHI's self-enrolled members who lived in the City of Jakarta, Bogor, Depok, Tangerang, Bekasi, (Jakarta Greater Area) and it represents the urban area of Indonesia. The ordinal logistic regression model was used to determine the type of sustainability NHI premium payment.

Results

The survey shows that around 28.3% of self-enrolled members do not pay the NHI insurance premium regularly. Applying ordered logit this study statistically confirms that age of household head, income per month, never experience economic hardship, 1st/2nd class registration, and benefits of SSAH are positively correlated with compliance rate to pay NHI insurance premium. Whereas tobacco consumption, health-seeking behavior, and the 2016 increase of premium are negatively correlated with regular premium payment.

Conclusions

This study calls for policy intervention to improve compliance of premium payment such as i) massive promotion of insurance literacy and benefits of insurance through a health professional, internet, and government officer; ii) expanding auto-debit and installment premium payment; iii) incentive for paying premium regularly and not smoking; and iv) improving access and quality of health services.

Introduction

The implementation of Law No. 40/2004 concerning the National Social Security System (SJSN) and Law No. 24 of 2011 concerning the Social Security Agency (SSA/BPJS) through the implementation of the National Health Insurance (NHI) / Jaminan Kesehatan Nasional program is an important step to achieve Universal Health Coverage (UHC) in Indonesia. The strategy is implemented by dividing the two types of participants, namely i) the recipients of Premium Assistance (PBI) i and ii) the non-PBI group which consist of wage-recipient (formal) workers (PPU), non-workers, and self-enrolled members / Pekerja Bukan Penerima Upah (PBPU). The contributory option of NHI premium payments from each participant is a challenge to ensure the sustainability of NHI program. PPU participants pay the premium from salary percentage deductions, while PBPU participants pay the premium on a self-enrolled based on hospital inpatient classes.

Significance for public health

The innovation of National Health Insurance (NHI) organized by the Social Security Agency for Health (SSAH) is an essential step for the Indonesian government in its goal of achieving Universal Health Coverage (UHC). The existence of the NHI can improve access and quality of health services for the community. The community gets access to the comprehensive health service guarantees, starting from improving health (promotive), preventing illness (preventive), treating diseases (curative), and restoring health (rehabilitative). Therefore, it is important to regularly pay NHI premium, especially for the self-enrolled member/informal sector workers (Pekerja Bukan Penerima Upah) for the continuation of the NHI program which become a global problem, especially in developing countries where the majority of the population is working in the informal sector.

The recipients of premium assistance (PBI) are the NHI participant who consists of the poor and disadvantaged people and their premium are paid by the Government of Indonesia.

Most PBPU participants are from the informal sector workers. They are non-wage recipients, meaning they are expected to register for membership voluntarily and make regular premium payments. Indonesia has a high number of informal sector workers at 53.6%, varying types of activities, and the scale of workers. 1 By a large number of informal sectors, Indonesia faces the consequence of the “missing middle problem” which considers the sustainability premium payment for self-employed members. In the informal sector, they relatively get a lower income, irregular, not recorded in the taxation, and spread in uncertain areas. To date, the number of NHI self-enrolled members are 30,248,656 in 2019, 2 , a significant increase from only 2 million members in 2014. 3

In this paper, we define the sustainability of premium payment as regular payment of NHI participants every month or in advance, early in the beginning (before the 10th of every month). As stated previously, it is a global issue especially in developing countries where the majority of the population is in the informal sector such as Ghana, Kenya, Cambodia, and the Philippines.4-7 The magnitude of the claims ratio of this group declined at the end of 2014, but still showed a high claim ratio of 584%. 8 The irregularity of self-employed members/PBPU premium payments by 28% on a national scale. 9 Based on the 2014 NHI monitoring, the selfenrolled member's premium collection has stalled. 10 Data shows that they do not routinely pay the premium of 34.73% in the Jakarta Greater Area [Social Security Agency for Health (SSAH), September 2017]. However, it makes SSAH's finances sustainable affected. The central government subsidized Rp 25.3 trillion (2017) and Rp 25.5 trillion (2018) for PBI members due to a lack of overall premium to SSAH. 11 After the increasing premium in January 2020, the subsidy approximately increased from Rp54.7 trillion in 2021 to 56.9 trillion in 2024. 12 Besides, 19% of respondents in Jakarta Greater Area found to be an adverse selection who registered to SSAH when they are already sick and also experienced premium payment discontinuation. Jakarta Greater Area with 27 million population was chosen as a research location (Figure 1) based on the justification with the consideration of a large number of self-employed members counted 3.6 million (April 2015), the readiness of the health service side, the most significant urban characteristics in Indonesia, access to information, and the completeness of the premium payment channel. To determine the influence of the premium payment, we need to observe dynamic changes in the self-enrolled member's behavior. During the time 2015-2017, there were policy changes at SSAH such as the 2016 increase of premium rate which can be assessed to the impact of premium payment.

Research area (Jakarta Greater Area).

This study aims to analyze the sustainability of premium payments behavior during the year 2015-2017, for the self-enrolled SSAH members in Jakarta Greater Area. The specific research question of this study is about the descriptive characteristics of the PBPU participants after the increase of NHI premium, several reasons of the respondents willing to sustain in paying the NHI premium, and factors that associated with the sustainability of NHI premium payment.

Design and methods

This study used a primary data survey which was collected from the same household in June 2015 and February 2017. The data was re-taken in 2017 due to the premium increase policy in April 2016 which make PBPU participants have to pay more premium in 2017. 8 The data were collected using structured interviews using a questionnaire. The population of the study was NHI's self-enrolled members who lived in Jakarta, Bogor, Depok, Tangerang, and Bekasi (Jakarta Greater Area). This area was selected for the sample location because it represents the urban condition of Indonesia. The data survey used a multistage random sampling method to represent the location of Greater Area Jakarta. There were six sub-districts chosen in this study using stratified random sampling: 4 sub-districts from Jakarta and 2 sub-districts from Bogor, Depok, Tangerang, and Bekasi. A total of 20 households were chosen in every sub-district using a random sampling method. According to Lwanga and Lemeshow and Rea and Parker's formula, with a 95% confidence interval, the minimum sample size of this survey is 385 respondents.13,14 Other study from Jakarta (Indonesia) used multistage random sampling and it has 102 respondents which represented the condition of this province. 15 The study obtained 404 respondents as a sample in 2015. Meanwhile, in 2017, there were 86 attritions (17.6%) in the sample due to resettlement (62%), respondents refused to be interviewed (9.2%), moving to SSAH non-PBPU categories, PPU or PBI (17.3%), members passed away (2.3%), and invalid data (9.2%). The attrition potentially reduced the sample size. The total sample successfully collected in 2017 was 318 respondents.

The dependent variable of this study is the sustainability of NHI premium payment. Sustainability refers to the regularly or routine of NHI premium payment by the informal sector workers. 9 We define the sustainability of premium payment or “routine” contributions as regular payment of NHI participants every month or in advance, early in the beginning (before the 10th every month), and “not routine” as the opposition. The sustainability variable is categorized ordinally based on the level of routine in paying the premium of NHI which consists of the first category, not routine in 2015 and 2017 as the category of non-compliance in paying the premium; second, routine in 2015 but not routine in 2017 as the category for decreasing the level of compliance; third, not routine in 2015 but routine in 2017 as the category of increasing awareness to pay the NHI premium; fourth, routine in 2015 and 2017 as the group that consistently continues to pay NHI premium.

Independent variables of this study were constructed from the theory of demand for health insurance and it were categorized into household characteristics, predisposing, and enabling factors. 16 This theory is also part of PRECEDE–PROCEED model to apply the factors affecting health behavior. 17

Predisposing factors consist of hospital class membership, health seeking behavior, SSAH registration motive, and knowledge of the SSAH office and service center. While enabling factors to consist of the registration process of SSAH, transportation cost to the health services, and the benefit of NHI.

A multivariate analysis was conducted by the econometric approach using the ordinal logistic regression model. The equation model was presented as follows:

where Y is the sustainability of NHI premium payment, HHC is household characteristics, Predis is the vector of predisposing variables, Enabling is the vector of enabling variables, Reinforce is the vector of reinforcing variables, delta VAR is the vector from 2015 and 2017 changing variables, i is the household observation and e is the error term.

Ordinal variables should be preferentially analyzed by using an ordinal logistic regression model. The ordered logit model is useful for understanding the relative effects of different household characteristics (predictors) on being of the routine of regular payment of NHI. 18 It allows us to ascertain which factors play an important role in enabling individuals who do not regularly pay premiums to change attitudes become routinely pay JKN premiums. Besides, the ordered logit model allows us to interpret the effects of predictors on the underlying ordered scale from not routine to routine in paying the premium and on being sometimes routine and sometimes not routine. If the ordinal model does not meet the parallel regression assumption, the multinomial one is the alternative way.

The result of ordinal logistic regression was showed coefficient beta and odds ratio with confidence interval. After the regression, the marginal effect was performed to measure the constant change from each category of sustainability premium. Post estimation of ordinal logistic regression was continued to parallel regression assumption by using proportional odds test as the goodness of fit and sensitivity analysis of the model. A proportional odds test was also used to assume the categorical coefficient relationship was the same between the lowest and the highest categories. All of the data analysis was done by using Stata version 14.

Results

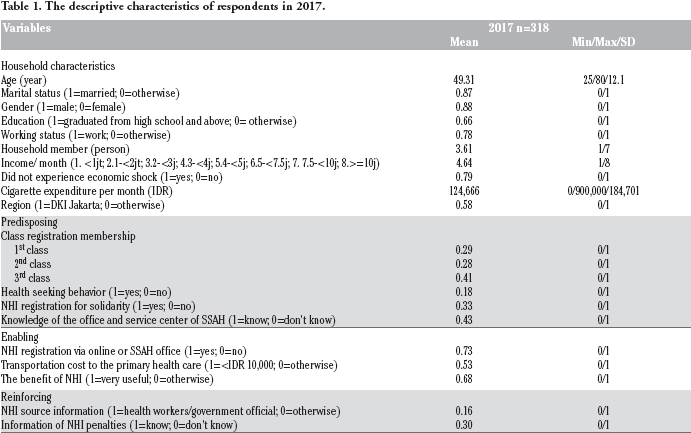

Table 1 shows the characteristics of the respondents of survey data in 2017. The completed comparisons between two surveys in 2015 and 2017 are shown in the appendix (Table 1). More than 60% of respondents have graduated from high school and above in 2015 and 2017. The majority of the respondents (49%) had income in the range of 3-4 million rupiahs in 2017. The amount of respondent's income in 2017 is not much different from the survey in 2015. The majority of respondents registered in the 3rd class registration membership (39%) in 2015 and it increased to 41% in 2017.

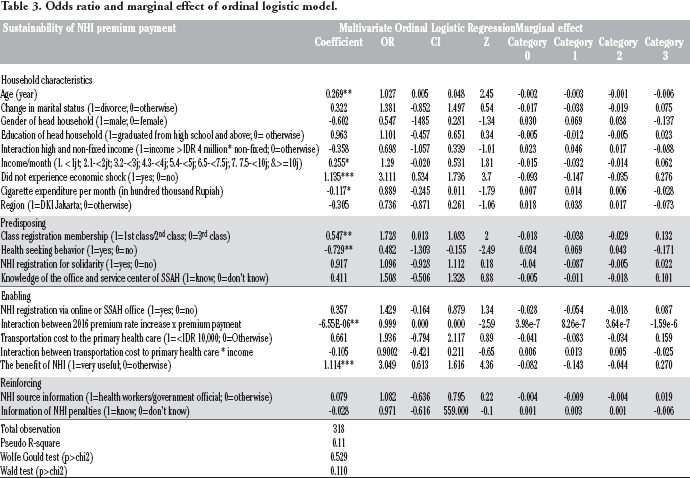

In 2017, more than 40% of respondents knew the office and service center of SSAH (Table 1). Thirty-three percent of respondents signed up for NHI for solidarity. However, more than 50% of respondents are still paying the transportation cost to the primary health care by themselves. As depicted in Table 2, there were 90 respondents (9.7%) who reported as “not routine” in paying the premium of NHI during 2015-2017 and 184 respondents (57.9%) as “routine” premium payment of NHI during 2015-2017. While respondents who were not routine in NHI premium payment in 2015 and become routine in 2017 were 13.8%. Figure 2 shows several reasons of PBPU members did not regularly pay the premium of NHI. Respondents who were more routine in NHI premium payment did not experience economic shock than not routine respondents. Based on the class registration membership, the routine respondents were more registered in 1st or 2nd class than 3rd class. Routine respondents have less transportation cost to the primary health care than not routine category. Besides, respondents who were routine in premium payment were more aware of the benefit of NHI than not routine members. Households from category routine in 2015 and 2017 were 60% participated in the 1st class and 2nd class membership. They have the highest monthly income level compared to the other categories. Households from categories 2 and 3 have the lowest shock economic at 9% and 15% compared to categories 0 and 1 both at 39%. The more result of descriptive statistics of the data in 2015 and 2017 based on respondents’ characteristics in 2017 are shown in the Appendix. Nearly half of respondents (41.51%) of 318 choose the 3rd class membership in the SSAH PBPU in 2015 and it increased to 46.23% in 2017. However, over the studied years, 39 respondents were moving from 1st class to 2nd class or 3rd class, and 2nd class or to 3rd class membership. The result of the assumption test before the ordinal logistic analysis showed the correlation matrix from the regression model was r<0.8 which indicated that there was no multicollinearity problem in the model. Besides, the proportional odds test by using Wolfe and Gould's showed 0.529 and 0.110. It means that the proportional odds assumptions of outcome variables are met. Table 3 shows the estimation result of ordinal logit regression. Age of household head, income per month, never experience economic hardship, 1st/2nd class registration, and benefits of SSAH are positively correlated with compliance levels to pay NHI premium. Whereas tobacco consumption, health-seeking behavior, and the 2016 increase of premium rate are negatively correlated with regular premium payment. The result of the proportional odds model shows that the highest odds of routine pay the NHI premium was never experienced economic hardship (OR=3.11, p<0.01). It means that the respondents who never experience economic hardship increased the probability 3.11 times to routine pay the NHI premium. On contrary, the lowest odds were tobacco consumption (OR=0.89, p<0.1). The respondents who consume cigarettes per month decreased the probability 0.89 times to routine pay NHI premium. At a 10% significance level, the greater monthly family income increased the sustainability of NHI premium payment of self-employed members (OR=1.29, p<0.1). Estimation results showed that the increasing income per month tends to contribute 1.29 times of routine in NHI premium payment. In predisposing group, class registration membership and health-seeking behavior have the largest positive and negative coefficient regression at 0.547 and -0.729 respectively. It means that SSAH PBPU who choose 1st/2nd class registration increased the possibility to become routine in paying the premium. However, they are getting less routine in paying the premium based on health-seeking behavior results. In the enabling group, the effect of premium increased in April 2016 required SSAH PBPU to pay more premium in 2017. Based on the result of interacting with the burden of premium payment, it will be able to reduce the continuity of routine in 2015 and routine in 2017 at p<0.01. According to the marginal effect for different routine levels, by the increase in age of household head and the premium rate, the probability of compliance rate to pay NHI premium is placed at a lower level. However, the benefit of NHI which the respondents think was very useful placed the probability of compliance rate to pay NHI premium at the highest level.

The reasons for the sustainability premium payment based on respondents’ characteristics in 2017.

The descriptive characteristics of respondents in 2017.

SD, standard deviation (shown only for continuous variables); NHI, National Health Insurance; SSAH, Social Security Agency for Health.

Cross tabulation of sustainability of NHI premium payment.

Odds ratio and marginal effect of ordinal logistic model.

Category 0, respondent's payment not routine 2015-not routine 2017; Category 1, respondent's payment routine 2015-not routine 2017; Category 2, respondent's payment not routine 2015-routine 2017; Category 3, respondent's payment routine 2015-routine 2017. NHI, National Health Insurance; SSAH, Social Security Agency for Health; CI, confidence interval; *p<0.10, **p<0.05, ***p<0.01;

Discussion

This study found several important factors related to the sustainability of premium payment to self-employed members/ PBPU. Whereas the issues of premium sustainability payment for informal sectors in social insurance schemes or community-based schemes have also happened in developing countries such as in Ghana, Burkina Faso, Kenya, Cambodia, and The Philippines.4,5,6,7,19,20

Characteristics of respondents and sustainability payment

Between 2015-2017, there are policy changes due to premium payment. First, as of September 2016, the premium payment must be done within a family comprehensively using one virtual account, not individually. Second, as of April 2016, the premium fee rate for PBPU members was increased. Other administrative sanctions such as difficulties in processing driving license, land certificate, passport, or car registration license also proposed to be applied for those who not paying the premium. Participants’ income patterns in 2017 tend to be uncertain. Only 56.92% of respondents had a steady income in 2017. Also, 22% of respondents reported experiencing problems such as job loss (9%), death and severe sickness of household head (8%), business failure, and crop failure (5.6%). In 2017, there were also 90 respondents (28.3%) who paid irregular premiums. Uncertain income (52.22%) and high premium fees (34.44%) are the main reasons for irregular premiums. Channel payment for paying the premium for respondents in the Jakarta Greater Urban Area is not a problem. This study also found that forgetfulness was the reason that selfenrolled members did not pay SSAH premium. Besides, other studies also found the same thing.9,21,22

The data shows respondents’ characteristics are mostly graduated from Senior High Schools or Universities. They registered in NHI to avoid the illness incidence in the future as Feldstein 23 says risk averter will buy insurance due to avoiding the future risk. Other motives to join NHI are respondents willing to accept healthcare services in prompt time, reducing healthcare expenditure, and holding health as the main principle in life.

Concerning the premium payment regularity, there are four related demographic factors, namely: i) age, ii) economic shock, iii) monthly income, and iv) cigarette expenditure per month. The age variable indicates that the higher the age, the more it has a higher chance of paying the regular premium on an ongoing basis during the period 2015 to 2017. This result is related to a higher age risk with the number of pain phases experienced by selfenrolled members. In another study, age is a factor that people consider before getting a health insurance card and payment of the premium. 21,24 Apart from age, respondents with higher monthly income have a chance to pay regular premium continuously from 2015 to 2017. In line with this finding, flexibility in premium payment mechanisms as applied in other countries such as periodic payment preferences or considering a specified period.5,6,25-28

Respondents without economic shock such as experiencing job loss, death, and severe sickness of household head, business failure, and crop failure between 2015-2017 indicate a higher chance of paying premium regularly on an ongoing basis during the period 2015 to 2017. Spending money on cigarettes per month is related to a decrease in the possibility of sustaining routine premium payments from 2015 to 2017. This issue is ironic because self-enrolled members can spend revenue to be allocated for cigarette purchases, but not to pay the premium regularly. SSAH may implement the incentive or disincentive mechanism to encounter smokers who prefer to consume cigarettes rather than paying a premium regularly. Another intervention carried out by the government to reduce cigarette consumption is to increase the tax on cigarettes. As of January 1, 2020, the government will raise cigarette excise tax by 23% and set a minimum selling price to reach an average of 35%. The increase in cigarette excise will have an impact on the rise of cigarette prices, which is supported by most people, and the impact will reduce the smoking prevalence. Research conducted by the Center for Social Security Studies Universitas Indonesia (forthcoming) shows that 88% of people, including smokers support the increase in cigarette excise duty. 29

Predisposing factors related to sustainability payment

Predisposing factors related to the regularity of premium payment include the class of registration variable and the health-seeking behavior variable. PBPU 1st class or 2nd class has a 12.9% higher chance of sustaining premium payment from 2015 until 2017 than 3rd class. The government should provide subsidies for selfemployed members who choose 3rd class to increase the chance of sustaining premium payment. The availability of subsidies and the sustainability of premium payment might be able to reduce the NHI deficit condition. While respondents who specifically seek treatment have a 17.4% lower chance of paying premium routinely. This data indicates a lack of mutual understanding and regularity in the payment of social health insurance premium. Knowledge about insurance has a vital role in expanding the participation of the informal sector. 30 Respondents who reported reasons for joining were to seek treatment, the majority were in 3rd class membership (69.39%). The Philippines is one of the developing countries with the most extended history of the social health insurance system. Individual Paying Program (IPP) is the program for informal sectors which is facing the same problem of small participation and premium from members because participants only pay for insurance when they need to utilize health facilities. Dartanto et al. found that 19% of Jakarta Greater Area respondents registered NHI when they were sick and did not routinely pay the premium. 9 Some policies have been implemented by SSAH related to the prevention of registration when sick, namely the application of waiting time 14 days after registration (waiting period). After that process, they will have a new card in which they can start using. In addition to that, they have what is called service fines, which require participants to pay their dues if they only contribute money to take advantage of the card.

Another study shows a lack of insurance literacy results in a drop-out of health insurance premium payment in Nouna, Burkina Faso. 21 Dartanto et al. also shows the same result which knowledge about SSAH and National Health Insurance Program (JKN) comprehensively increase the probability to pay premium regularly by 5%. 9

The enabling factors related to premium payment regularity

This research also shows the influence of enabling factors to the sustainability payment, namely: i) Premium rate increase, and ii) SSAH or NHI benefit. Changes in the SSAH premium fees rate applied since April 2016 have been the factor in the sustainability of PBPU premium payment. The increased premium rate is considered burdensome and the amount of real premium per family paid from 2015 to 2017 reduces the likelihood of regularly paying the routine premium during this period. Therefore, determining the amount of premium must be a serious concern because it affects the premium payment sustainability. The considerable rates of premium in Ghana are the main reason why some participants quit the health insurance schemes. 31 IDI study shows that premium rate increase should be enforced to another group of members such as formal group (salary recipient workers). 32 An accounting calculation found that the significantly raising premium rate was not linearly applicable to all membership groups. The results of the ordinal logit regression show that a significant increase in the premium rate will discourage participants to pay the premium sustainably. Irregular income among PBPU makes it difficult to pay the number of premiums, thus it eventually discourages them to pay. The calculation of premium proportion to members’ incomes in the data shows that the proportion of the premium paid by PBPU participants compared to their incomes has reached 5%. The 5% proportion is equivalent to the burden given to SSAH participants among wage-recipient-workers (PPU). This proportion is considered high with the respondent's average income per month of Rp 4,227,987 (USD 283.5) or below the provincial minimum wage.

The benefits of NHI membership are felt to be significantly related to the behavior of premium payments. This study found that the respondents have a high satisfaction level with the primary healthcare services (general practitioners, Puskesmas/government clinic, and private clinic) and the secondary healthcare services (hospital). PBPU participants who considered NHI membership to be very beneficial increased the possibility of paying premium regularly by 9.5%. Satisfaction or dissatisfaction with health facilities in the utilization of health insurance can affect the premium payment regularity.21,22,33 If a customer is satisfied then it becomes the success indicator thus encourages repurchasing (a loyal behavior) which in this BPJS context is sustainability payment.34,35

Regarding the health facilities utilization, this study found that there were respondents who used private funds to seek treatments even though they had a SSAH card. The case mentioned above is caused by either poor quality of medical and non-medical services or a distant and inaccessible health facility. The issues above can be addressed by improving the SSAH overall quality in terms of medical and non-medical aspects. One of the means is by expanding the health facility partners to overcome the inaccessibility issues and improving the administration system such as queue booking. The strength of this study is to provide the community's obedience and disobedient overview in paying the NHI premium so that the policymakers know how to determine the factors to intervene to improve the premium payment sustainability for selfenrolled members or informal sector workers. However, the limitation of this study is the attrition is found on the follow-up data in 2017 with some various causes. However, the characteristics in both analysis years appear to be similar although there is a reduction for the sample attrition in 2017. The model obtained from regression will be the estimation model only for urban areas to improve the policies and regulations related to the premium payment behavior of self-enrolled members. The next analysis, especially in the rural area, can be conducted to improve the policy recommendation for the policymakers in Indonesia.

Conclusions and recommendation

This study concluded that the main reason for the selfemployed to join NHI was to get a certain health medication and to get a certain coverage for health expenditure when they were sick. NHI participants from the informal sector who regularly and irregularly pay the premium were 71.7% and 28.3% respectively from 2015 to 2017. Age, monthly income, economic shock experience, and cigarette expenditure were associated with the continuity of NHI premium payment. BPJS Kesehatan (SSAH) should maintain the participation of self-employed members who have the nonfixed income to facilitate installments of premium payment. The government should provide subsidies for self-employed members who choose 3rd class. Based on the research findings, this study divides the proposed policy proposals into three parts, namely short-term, medium-term and long-term policies. There are five short-term policy variations proposed in this study.

First, the suspending payment because forgetting about the payment due date can be solved with an auto-debit system from the bank saving. OJK emphasizes that financial inclusion should continuously grow in expanding public access to the formal financial sector. 36 Cooperation with digital start-ups and online stores just like in super apps is also possible. NHI premium can also be derived by automatically charging the electronic money balances from workers in the informal sector.

Second, one way to maintain PBPU membership in the system to make payments regularly is by facilitating participants with irregular/ fixed incomes using the installment system. In December 2017, the SSAH introduced new payment methods namely “Installment Program”. ii These two new methods help those who particularly have arrears to easily fulfill their payment due.

The Installment Program is a premium collection program for PBPU participants who are carried out by NHI cadres in Indonesia. In addition, NHI cadres also help provide information about NHI to PBPU participants.

Third, raising awareness on the concept of mutual-help/gotong royong helps each other to pay the premium. Socialization material can be in the form of a storyline that promotes human values. Promotion strategies arouse public sympathy with personal stories. The results of the Dartanto survey show that using campaigns that highlight personal bitter stories arouse people's awareness better compared to using a general picture of difficulties. 37

Fourth, expanding the network and improving the health services quality. It is necessary to expand the partnership network to health facilities in Jakarta's Greater Area (Jabodetabek) in collaboration with BPJS to provide easy access to participants. Furthermore, the quality of services, both in medical and non-medical aspects remains a concern. The importance of health care satisfaction was a strong factor that influenced the sustainability of NHI premium payment.

Fifth, cooperation with other strategic partners such as health workers (doctors, midwives, nurses) and government officials. Stakeholders and community leaders can act as informers to provide counseling and education related to the importance of maintaining the premium payment regularity, including disseminating the latest information on the service fines.

The proposed medium-term policies for PBPU include multisector policies involving the government and people's representatives by extending the concept of cooperation and the government's commitment to taxation. The concept of cooperation in question is extending the maximum number of deductions from formal workers’ wages which currently represents the total base salary. This is different from the amount of take-home pay (which is overall income).

Besides, the concept of sin taxes applied in other countries such as the Philippines (tax on gambling and liquor) should be taken into consideration. So, the excise tax on cigarettes in Indonesia can contribute to financing public needs.

The proposed long-term policies for PBPU members include formalizing the types of work owned by PBPUs. As happened in South Korea, the formalization lasted for twelve years following the dynamic macroeconomic conditions in the country. In Indonesia, the informal sector accounts for a significant proportion thus becomes the present challenge for the central government. Going forward, policies to formalize the informal sectors will be crucial. Various policies are needed to incentivize businesses to formalize.

Footnotes

All authors declare no conflict of interest. None of the authors benefited from any direct or indirect funding from the tobacco industry or any other company.

Acknowledgments

We thank to Universitas Indonesia Research Grant 2021 (Community Fund) International Publication Assistance Scheme (PPI) Q2 (PPI Q2) No. NKB-617/UN2.RST/HKP.05.00/2021 which provided a fund for publishing this article. All authors also express their sincere gratitude to all contributors to this study.