Abstract

BACKGROUND:

COVID-19 affected numerous industries and the mining industry has not been immune to the adverse impacts caused by the pandemic.

OBJECTIVE:

This study examines the importance of the mining industry and its benefits to the economy of the producing countries. The paper also gives an insight into the pre-COVID global and Turkish mining industries and investigates the impact of the pandemic on the global and Turkish mining sectors. Furthermore, the study suggests numerous measures that should be adopted in mines to limit the spread of COVID-19 and conduct mining operations safely and efficiently.

METHODS:

An extensive literature review was conducted and relevant papers on the importance and benefits of the mining industry, the Turkish and global mining industry, and the impact of COVID-19 on the Turkish and global mining industry were studied.

RESULTS:

The COVID-19 crisis has deeply affected metal and mineral production and the economic sectors that depend on the mining industry for supplies. The most significant impacts caused by the COVID-19 pandemic on the global mining industry consist of the drastic decline in demand and production and the decrease in the prices of several commodities. As with any complex global situation, the mining industries of some countries were affected more than others by the COVID-19 crisis. The Turkish mining industry was to some extent affected by the COVID-19 crisis, but it quickly recovered.

CONCLUSIONS:

An efficient planning of operations and adopting effective measures and precautions enable limiting the spread of COVID-19 in quarries and mines.

Introduction

COVID-19 has induced the most severe health crisis in this century [1]. Nonetheless, the pandemic does not only illustrate a health matter [2, 3]. COVID-19 has adversely impacted numerous sectors such as national and global economies, financial and social structures, education, politics, and human security [3–5]. The social distancing and lockdown strategies adopted by numerous governments all over the world to limit the spread of the virus negatively affected the global economy [6]. These measures have led to an economic crisis considered to be the worst since the Second World War [1]. The collapse of the global economy caused by COVID-19 has been faster and more severe than the 2008 global financial crisis and even the 1929 Great Depression [3, 7]. The World Bank predicts that this pandemic will likely lead to increasing world poverty for the first time since 1988 [8].

COVID-19 has caused a pronounced disruption of the global supply chains caused by the decrease in consumption and rupture of production [6, 9]. Studies conducted on the impact of the pandemic on the global economy reported that COVID-19 induced a crash of the stock markets, a decrease in the Gross Domestic Product (GPD), the suspension of credit markets, increased bankruptcies, an amplification of unemployment rates [3] and massive capital outflows from emerging markets [9].

Even though most governments allowed mining companies to remain active during the COVID-19 outbreak with limited restrictions [10], the mining industry has not been immune to the adverse impacts caused by the pandemic [9, 11]. The COVID-19 crisis has deeply affected metal and mineral production and the economic sectors that depend on the mining industry for supplies [10]. Experts studying the aftermath of the crisis predict that the mining sector will experience short, medium, and long-term consequences [12] especially in resource-rich countries where the mining industry plays a crucial role in poverty reduction, inclusive growth, and social development [9].

This paper highlights the importance of the mining industry and its benefits to the economy of the producing countries, gives an insight on the global and Turkish mining industries pre-COVID, and investigates the impact of the pandemic on the global and Turkish mining sectors. Furthermore, the study suggests numerous measures that should be adopted in quarries and mines to limit the spread of COVID-19 and conduct mining operations efficiently and safely.

Importance of the mining industry and its benefits to the economy

Throughout the course of history, mining made tremendous contributions to the social and economic prosperity of numerous civilizations. In fact, several cultural eras were named after various minerals or by their derivatives: the Stone Age (prior to 4000 B.C.E.), the Bronze Age (4000 to 5000 B.C.E.), the Iron Age (1500 B.C.E. to 1780 C.E.), the Steel Age (1780 to 1945) and the Nuclear Age (1945 to the present) [13, 14].

Today, we still depend on mining activities in the same way our prehistoric ancestors did [15] as raw materials are the indispensable foundation of every aspect of our modern life and will remain so in the future [16]. Mining products are extensively used in construction and civil engineering projects, electricity generation, vehicle manufacture and fuel, machinery, technological products such as cell phones, computers, satellites, and other electronics, medicines, beauty products, dentistry, fertilizers and food production, energy production and transmission and renewable energy technology [17–19].

The mining sector operates on every continent except Antarctica [20]. The increasingly growing population, urbanization, and income growth are the main factors behind the need for more mined products as more buildings, cars, and consumer products are constantly needed [19]. Therefore, countries’ socio-economic development depends on the existence and production of energy and natural resources [14, 21, 22].

The mining sector is pivotal to the world’s economy [23]. Together with providing the necessary raw materials for numerous industries, it creates thousands of jobs, generates dividends and tax revenues, and directly contributes to the economic prosperity of the producing countries [16–18]. Furthermore, the mining industry produces a trained workforce and small businesses that can serve communities, yields foreign exchange, and account for a significant portion of GDP [18]. The industry also enables the development of regional areas, the prevention of migration, and increasing the value-added and the employment rate of the producing country [14, 24–26].

According to Dorin et al. [27], most of the countries with low or middle national income significantly benefit from the mining sector which substantially contributes to the exports share and accounts for up to 90% of the foreign direct investment (FDI), 10% of the national income and 2% of the total employment. The International Council on Mining and Metals (ICMM) states that no less than 70 countries are extremely dependent on the mining industry and most low-income countries need it to simply survive [19].

An insight on the global mining industry pre-COVID-19

The mining industry is essential to the operating countries and generates important profits for the producing companies. According to Garside [23], the total revenue of the top 40 mining companies between 2005 and 2020 reached 656 billion USD. Table 1 highlights the evolution of the global production of mineral raw materials (bauxite not included) between 2000 and 2019. The global production of mineral raw materials kept increasing between 2000 and 2019 and went from 11,290 million t in 2000 to 17,913 million t in 2019. The most recent statistics on the global mineral data were presented in ‘’World Mining Data 2021”, a report prepared by the International Organizing Committee for the World Mining Congresses. This report gathers details on the global mineral production in 2019. In 2019, 1,587,909,229 t of iron and ferro-alloys, 466,008,328 t of non-ferrous metals, 31,539 t of precious metals, 797,141,169 t of industrial minerals and 15,435,799,404 t of mineral fuels were produced worldwide. Thus, a total of 18,286,889,669 t of minerals and metals were produced worldwide [28]. China, the United States, Russia, Australia, India, Indonesia, Saudi Arabia, Canada, Brazil, and Iran were the top 10 mineral-producing countries in 2019. In fact, China, the biggest mining country in 2019, is the World’s leading country in the production of many commodities such as gold and rare earth [23].

Global production of mineral raw materials (not including bauxite) between 2000 and 2019 [28]

Global production of mineral raw materials (not including bauxite) between 2000 and 2019 [28]

Turkey produces and trades 60 of the 90 mineral materials produced worldwide and is marked by the absence of only 13 types of the missing 30 minerals. In terms of the world reserves, Turkey holds 2.5% of the global industrial materials reserve; 40% of the natural stone reserve, 20% of the bentonite reserve, 1% of the coal reserve, 0.4% of the metallic mineral reserve, and 72% of the global Boron reserve [14, 30]. In fact, Turkey holds 4 billion m3 of exploitable marble, 2,8 billion m3 of exploitable travertine, and 1 billion m3 of granite reserves. A total of 650 different color and texture types of marble can be found in this country [31]. The diversity of mineral deposits in Turkey is explained by the complexity of its geological context.

The mining sector plays a strategic role in the Turkish economy and accounts for 1 to 3% of the total export value of the country. Turkey’s advantages for companies in the mining sector are not limited to its high-quality labor pool, but also include relatively low logistics and drilling costs, proximity to major markets, advantageous government incentives, and competitive taxes [31]. In 2019, Turkey ranked 22nd among the mining countries worldwide and produced a total of 138,921,175 t of minerals and metals distributed as follows: 10,408,20 t of iron and ferro-alloys, 373,495 t of non-ferrous metals, 281 t of precious metals, 35,515,449 t of industrial minerals and 93,368,200 t of mineral fuels. In 2019, Turkey produced 87,280,000 t of lignite, 8,828,800 t of iron, 2,013,000 of steam coal, 6,961,015 t of salt, 1,528,700 t of chromium, 2,255,480 t of bauxite, 39,000 kg of gold and 242,000 kg of silver. According to MAPEG [32], during the same year, Turkey produced 97,371,718 t of energy raw materials, 13,775,717 t of natural stones, 422,754,000 t of cement, and construction raw materials, 34,125,509 t of metals, and 75,730,803 t of industrial raw materials (Table 2). The total value of the produced minerals and metals in Turkey in 2019 reached 25,486 million USD distributed as follows: 15,345 million USD of iron, 1,120 million USD of ferro-alloys, 1,872 million USD of non-ferrous metals, 3,436 million USD of precious metals, 3,635 million USD of industrial minerals and 3,635 million USD of mineral fuels [28].

Mineral production of Turkey between 2015 and 2019 [32]

Mineral production of Turkey between 2015 and 2019 [32]

The mineral sector in Turkey is marked by its substantial contribution to the economy of the country and its high employment rate. Table 3 emphasizes the evolution of the number of workers and mining companies operating in both the public and private mining sectors in Turkey between 2015 and 2019. Table 4 highlights the contribution of the mining industry to the Turkish national economy between 2015 and 2018.

Number of workers and mining companies operating in the mining sector in Turkey between 2015 and 2019 [32]

Contribution of the mining industry to the national economy of Turkey between 2014 and 2018 [32]

Several containment and mitigation measures were implemented by governments all over the globe to limit the spread of COVID-19 [33]. These measures included social-distancing, cluster and entire lockdowns, extensive travel bans, mass quarantines, cancellations of major events and conferences, prohibitions of mass gatherings, and shutdowns of cities and other areas [34, 35]. The adopted measures considerably affected the global economy [36]. The mining industry was impacted by the COVID-19 crisis as the Chinese demand for raw materials declined especially at the beginning of the pandemic leaving investors uncertain about the future of the industry [37]. Nevertheless, as with any complex global situation, not every mining company nor every country was impacted to a large extent [23].

Galas et al. [5] identified feasibility studies’ projects and projects conducted to develop new mines and extract residual resources before the closure decision as to the most affected states by the COVID-19 pandemic in the mining industry. The authors emphasized that the effect of the pandemic on the exploration and discovery stages of the mining process is medium.

In an article published by Azevedo et al. [38], the authors predicted the trajectory of the mining industry back to the next normal based on analyzing 6 major crises marked by their significant impact on the industry. These crises consist of the second oil shock (1981–1987), The Soviet Union collapse (1991–1998), Asia crises (1997-1998), the Dot-com bubble (2001–2003), the financial crisis of 2008-2009, and the commodity price crisis of 2015-2016. The authors predict that similarly to the studied shock waves, the impact of the COVID-19 outbreak on the mining industry will follow 4 main phases as detailed below:

The authors stress that in the context of the COVID-19 crisis, the mining industry is currently under the effect of phases 2 and 3.

The most significant impact caused by the COVID-19 pandemic on the global mining industry consists of the drastic decline in demand since industrial production and construction activities were disrupted for variant periods in most countries [12]. The decrease in demand consequently led to a decrease in production and a fall in the prices of numerous commodities such as aluminum, copper, zinc, nickel, and iron ore [9, 39]. For instance, the global production of iron ore was also affected by the crisis as it dropped by 3% to 2,2 billion tons in 2020 mainly because of the decline of the output of two of the main contributors to the production of iron: Brazil and India [40]. Swart [39] explains this low production by the anticipated low near-term demand for these minerals and metals. Jowitt [10] emphasizes that the witnessed increase in metal stocks and decline in metal prices will adversely affect the mining industry at least in the short term.

Energy commodities were exempt from national lockdowns [9] because of their primary role in supplying numerous industries and economical activities. However, energy commodities such as coal were not immune to the price shock that affected the mining industry. For instance, coal prices drastically decreased due to the low demand in its consuming countries in Europe and Asia as the COVID-19 pandemic caused lower demand for coal by power plants that generate electricity and for industrial uses [41].

Following this price shock and low demand phase, starting mid-2020, the prices of most minerals and metals started to recover as they slowly regained their pre-pandemic prices. For instance, in a study that evaluated the impact of COVID-19 on the mining industry in Ghana, Mali, South Africa, and Zambia, main producers of gold, copper, iron ore, manganese, platinum, bauxite, and diamonds in the African continent, Ahadjie et al. [41] stated that in the studied countries, iron ore regained its pre-pandemic price by May 2020 and that the prices of most of the base metals recovered by the fourth quarter of 2020. The paper also analyzed the price changes of precious metals and emphasized that silver and platinum regained their pre-pandemic prices within only one month.

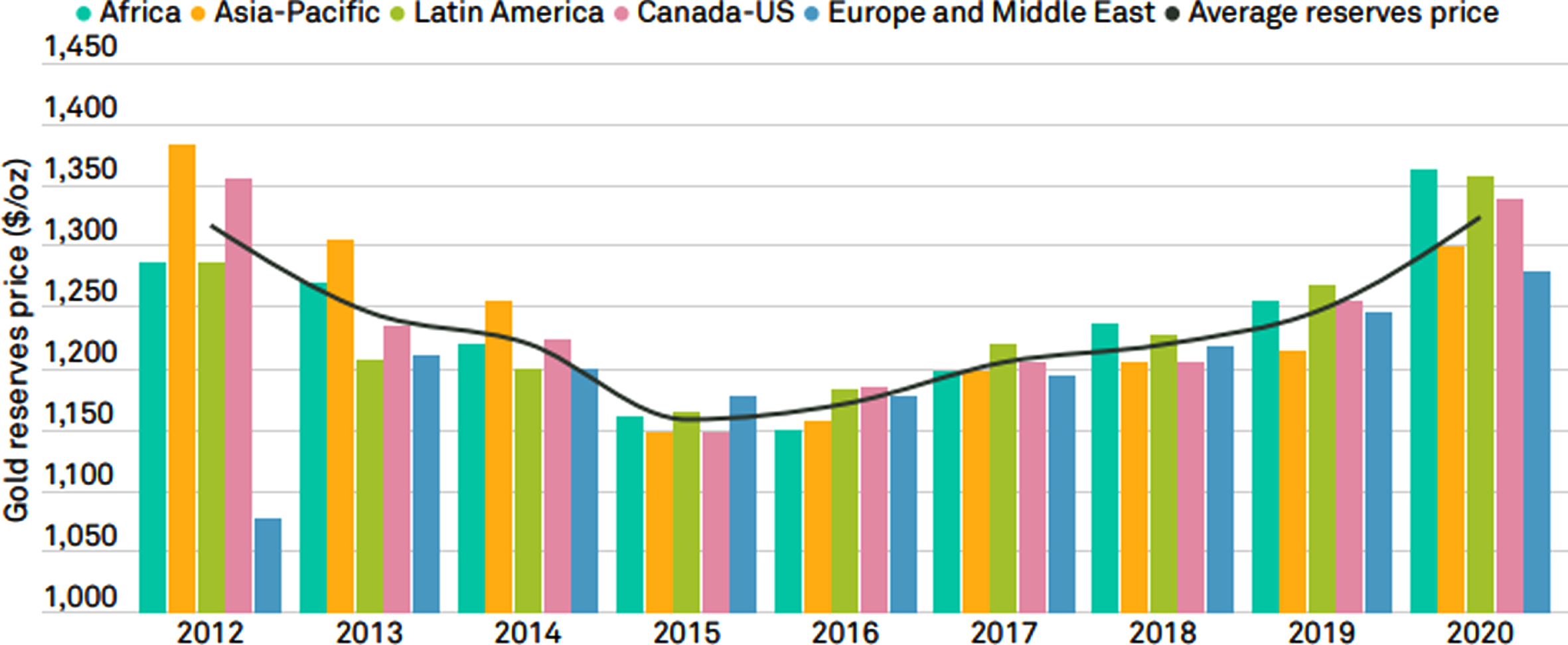

Contrary to the previously mentioned commodities, the demand for gold and consequently its price substantially increased during the COVID-19 pandemic [41]. In fact, this precious metal is a haven and an asset of investment during crisis periods [9, 41] as it benefits from high uncertainty levels [39]. Figure 1 highlights the evolution of the average prices for gold reserves by region between 2012 and 2020. Nonetheless, the increase in gold prices has caused the expansion of Artisanal and Small-Scale (ASM) gold mining operations in numerous countries which caused the environmental deterioration of multiple sites [12].

Average prices for gold reserves by region between 2012 and 2020 [42].

Besides affecting the prices of commodities and disrupting the supply chain, the COVID-19 crisis had other implications on the mining industry. Ramdoo [9] emphasized that the pandemic induced the disruption of the economic activities in local communities which depend on mining companies operating in the region leading to decreased local suppliers’ earnings and increased high bankruptcy risks for Small and Medium Enterprises (SMEs) unable to face the instabilities of the market. Laing [12] highlighted that the price shock and low demand induced the collapses in the shares of numerous large mining multinationals. The paper also accentuated that the implications of the COVID-19 pandemic on the industry may cover laying off workers, mothballing existing mine-sites, reducing corporate social responsibility activities, decreasing investment in new operations, technology, and exploration, and renegotiating taxation and royalty agreements with the host country governments. The COVID-19 crisis did not only affect large mining multinationals. Artisanal and Small-scale Mining (ASM) which employ over 44 million people across the globe suffered was also impacted by the crisis [33].

The mining sectors of numerous countries were deeply affected by the COVID-19 crisis. For instance, in Indonesia, mining activities substantially decreased because of the pandemic which led to a growth decrease to just 0.4 % in the first quarter of 2020 [43]. Compared to 2019, mining and coal revenues decreased by 35% and generated 2,3 billion USD as of August 2020. In an attempt to minimize the impact of the pandemic on the mining industry, numerous new policies and measures were implemented by the Indonesian government. These measures include exempting mining companies from certain fees and taxes, investment incentives, and revisions of the state budget [44]. In Germany, despite restoring the disrupted supply chains and adapting the production to the circumstances of the pandemic during the course of 2020, the fourth quarter of the year was marked by declines in turnover that reached more than 30% [16]. Despite being declared a critical industry and exempting it from shutting down during lockdowns, the mining industry of the United States was still affected by the pandemic. The production of aluminum, iron ore, steel, titanium, barite, and industrial sand and gravel substantially decreased due to the decline in demand by manufacturers [45]. South Africa, one of the most important producers of platinum, chrome, gold, diamond, and palladium, was deeply affected by the strict lockdown measures adopted by the country to limit the spread of the Coronavirus. In April 2020, the total mining output of the country fell by more than 47% compared to 2019. In addition, logistical problems made exporting the produced minerals and metals a hard and expensive task [46]. In Canada, the global low demand for fuel and the drop in natural gas prices induced a reduction in the Canadian mining output [47]. In China, as of August 2020, the mining industry generated a turnover that reached 309 billion € which is 10,9 % less than the turnover of 2019. The profit of the Chinese mining industry added up to 30 billion € decreasing by 38.1% compared to 2019 [16].

The human and economic loss induced by the COVID-19 pandemic was greater in developing countries. The crisis generated an immediate and amplified impact on the poorest and most vulnerable regions [33]. The impact of the pandemic on the mining industry is more severe in resource-rich but economically struggling countries where citizens have to physically work to earn their living [48]. In Mozambique, mining was one of the most heavily affected sectors by the COVID-19 crisis. In 2020, the domestic and foreign impact of the pandemic on the GPD of the country reached 1.5 % while its effect on employment accounted for 1.8 % [49]. According to a study conducted by Lastunen et al. [50], in 2020, compared to the pre-COVID data, the GPD shock in the mining industry reached –22.6 % in Ghana, –20.9 % in Mozambique, +2.9 % in Tanzania, +5.5 % in Zambia, and –14.2 % in Uganda. In Ghana, Mali, South Africa, and Zambia, the pandemic disrupted the mobilization of labor which caused a decrease in the employment rates [41]. In India, where the mining industry is substantially crucial for economically marginalized people, workers have returned to their home base [51] following the cease of mining operations because of the pandemic which left them without a source of income [11]. West Africa, on the other hand, was well equipped to continue mining operations during the COVID-19 pandemic as the recent epidemics endured by the country such as Ebola enabled it to implement the necessary measures to face such alarming events [52].

The mining industries of other countries such as Sri Lanka and Australia were not affected by the pandemic to a great extent. In Sri Lanka, mining was one of the least affected sectors by COVID-19. Deyshappriya [53] highlights that in the worst-case scenario, the reduction in this sector will reach –0.08% in Sri Lanka and –0.65% in South Asia. The Australian government defined the mining industry as an ‘essential industry’ which enabled mining companies to remain active during lockdowns. As a result, the Australian mining industry has survived the crisis caused by the COVID-19 crisis without major losses and even benefited from the increase in gold prices. However, the global decrease in energy needs and the political tension between Australia and China adversely affected the Australian coal production industry [16].

It is hard to predict with certainty the long-term effects of the COVID-19 crisis on the mining industry, especially since the pandemic is still ongoing. In this context, Jowitt [10] states that either a persistent supply-chain disruption or a slower demand growth is likely to occur over the course of the next few years. Galas et al. [5] affirms that the disruption in the production of minerals and metals will adversely affect the future security of supplies of raw materials.

Other scholars, on the other hand, are optimistic about the future of the industry. Statistics by PricewaterhouseCoopers [54] highlight that the mining industry emerged from the COVID-19 pandemic economic crisis without major losses and emphasize that 2020 was an outstanding year for the mining sector as in comparison to 2019, net profit and cash on hand increased respectively by 15% and 40% and market capitalization increased by nearly two-thirds. Ferguson [55] underlines that in the upcoming years the mining sector will benefit from the need for raw materials essential to the global energy transition efforts. Laing [12] highlights that no sharp decline occurred in the global money supply and affirms that mining operations can quickly recover from the effects of the pandemic as the productive capacity remains intact (contrarily to economic crises that follow wars). Jowitt [10] states that the COVID-19 crisis may be followed by a significantly high number of new investment projects in infrastructure, capital, transportation equipment, and consumer durables, which would increase the demand for metals and thus lead to higher prices.

Numerous measures were implemented by the Turkish government to limit the spread of COVID-19 since announcing the first case in Turkey on March 11, 2020. The adopted measures included travel restrictions, curfews, lockdowns, banning mass gathering events, and closing schools and universities [56]. To inform the public about the necessary precautions to limit the spread of the disease and raise awareness about COVID-19, the ‘’Emergency Operation Center” and ‘’Coronavirus Scientific Board” were established in January 2020. Despite being exempt from lockdowns and curfews, the Turkish mining industry was to some extent affected by the COVID-19 crisis. Natural stones’ production slightly decreased from 7,141 thousand t in 2019 to 6,468 thousand t in 2020. Minerals’ production, on the other hand, witnessed an increase from 20,004 thousand t in 2019 to 21,412 thousand t in 2020 (Table 5). The Turkish mining industry quickly recovered from the impacts of the pandemic in 2021 (December not included) as production of natural stones increased again in 2021 to reach 7,201 thousand t in 2021 generating 1928 t million FOB USD. Mineral’s production substantially increased in 2021 (December not included) compared to 2020 and reached 25,083 thousand t generating 4,470 million FOB USD (Table 5).

Production and value of natural stones and minerals of Turkey between 2016 and 2021 [63]

Production and value of natural stones and minerals of Turkey between 2016 and 2021 [63]

Every mine consists of a production area and numerous complexes such as entrances, administrative buildings, offices, laboratories, kitchen, dining halls, dormitories, changing rooms, washrooms, maintenance and repair facilities, parking lots for machinery and equipment, stock areas, and showrooms. The number and distribution of the employees in the workplace are determined based on the intensity of the required tasks. Efficient planning of operations in mining companies enables reducing non-essential interactions between workers and minimizing the amount of time spent in collective areas. Effective measures should be adopted by mining companies to limit the spread of COVID-19 in the workplace. The recommended measures listed below enable limiting the spread of COVID-19 in mines.

COVID-19 safety sign [57].

Planning, resources, and management systems Education and communication Worker health surveillance, self-monitoring, and contact tracing Hygiene and cleaning Site access and work organization Travel and mobility Accommodation

To reduce the risk of the spreading COVID-19, a group of people should be appointed to implement the checklist in every mine. Using the checklist, the team will be able to identify shortcomings and suggest new measures to improve COVID-19 safety measures at the workplace. Furthermore, workplaces should be regularly monitored to ensure the implementation and application of COVID-19 protocols. In fact, a linear and inverse relationship was found between the incidence of COVID-19 in workplaces and the level of inspection of the COVID-19 prevention measures [62].

The COVID-19 pandemic, which started in Wuhan China, affected 224 countries and caused the death of more than 5 million people all over the globe (as of January 4th, 2022). Coronavirus disease is not only a health crisis as it negatively affected numerous industries and generated the biggest global economic crisis since the Second World War.

The mining industry has not been immune to the adverse impacts caused by the pandemic. The COVID-19 crisis has deeply affected metal and mineral production and the economic sectors that depend on the mining industry for supplies. The most significant impacts caused by the COVID-19 pandemic on the global mining industry consist of the drastic decline in demand and production which led to a decrease in the prices of several commodities such as aluminum, copper, zinc, nickel, iron ore, and coal. Starting mid-2020, prices of most minerals and metals started to recover as they slowly regained their pre-pandemic prices. Prices of Gold, on the other hand, substantially increased during the pandemic as it is considered a haven during crisis periods.

As with any complex global situation, the mining industries of some countries were affected more than others by the COVID-19 crisis. While resource-rich but economically struggling countries such as Ghana, Mozambique, Uganda. Ghana, Mali, South Africa, Zambia, and India suffered the most from the impacts of the pandemic, the mining sectors of other countries such as Sri Lanka and Australia were not affected by the disease.

The Turkish mining industry was to some extent affected by the COVID-19 crisis. Natural stones’ production slightly decreased in 2020 because of the pandemic. However, the industry quickly recovered and natural stones’ production increased again in 2021.

Efficient planning of operations and adopting effective measures and precautions enable limiting the spread of COVID-19 in mines. The recommended measures include: Using safety signs, banners, floor labels, and informative posters in gathering places Encouraging workers to get vaccinated, Installing hand disinfection stations, Conducting meeting and training courses online, Implementing strict measures in dining halls, dormitories, changing rooms and washrooms, Shift organization, Seating arrangements in worker transport vehicles, Regular screening and health check-ups, Regular disinfection procedures, and Regular training courses.

Ethical approval

Not applicable.

Informed consent

Not applicable.

Conflict of interest

The authors declare that they have no conflict of interest.

Funding

The authors report no funding.

Footnotes

Acknowledgments

The authors have no acknowledgments.