Abstract

Due to the complexity of the real world, randomness and uncertainty are ubiquitous and interconnected in the real world. In order to measure the research objects that contain both randomness and uncertainty in practical problems, and extend the entropy theory of uncertain random variables, this paper introduces the arc entropy of uncertain random variables and the arc entropy of their functions. On this basis, the mathematical properties of arc entropy and two key formulas for calculating arc entropy are also studied and derived. Finally, two types of the mean variance entropy model with the risk and diversification are established, and the corresponding applications to rare book selection for the rare book market are also introduced.

Introduction

Entropy is a measurable tool used to characterize the difficulties in the realization of predictions as well as the uncertainties in models, and it is closely related to environments where uncertainty and randomness coexist. In order to measure the difficulty of predicting the realization of indeterminacy, Shannon [26] first proposed the concept of entropy, which is named Shannon entropy. Since then, Shannon entropy has been widely carried out by several scholars, and various types of entropy have been investigated. For instance, the relative entropy of random variables was studied by Kullback and Leibler [9] to characterize the differences between two random variables, the quadratic entropy of random variables was presented by Vaida [29] to describe the degree of predicting the realization of a random variable, and the slope entropy was proposed by Li et al. [10] and was applied in underwater acoustic signal processing. In addition, the entropy theory of fuzzy variable was also investigated by Biswas et al. [3] and Pandey et al. [23].

In order to model non-deterministic phenomena in practice and reasonably deal with the belief degree non-deterministic phenomena, uncertainty theory was established by Liu [13] in 2007 and then perfected by Liu [14] in 2009. For the purpose of illustrating the existence of uncertainty in practice, a large number of scholars have carried out many empirical studies such as epidemic spread (Chen et al. [6], Jia and Chen [8], Lio and Liu [12]), grain yield (Liu [18]), natural gas price (Mehrdoust et al. [22]), stock price (Liu and Liu [17]), currency exchange rate (Ye and Liu [30]), electric circuit (Liu [16]), China’s population (Liu [19]), fishery industry (Chen and Liu [4]) and so on. Up to now, uncertainty theory has become a branch of mathematics under the researches of many scholars, has been widely used in industry, engineering, finance and other fields.

However, the real data not only contains uncertainty, but also contains randomness. For the sake of modeling complex systems that contain both uncertainty and randomness, chance theory was proposed by Liu [20], and then the basic concepts such as expected value, variance and entropy of uncertain random variable were also investigated by Liu [20]. Following that, the entropy of uncertain random variable has been studied by many scholars and has been widely applied to various areas. For instance, Sheng et al. [24] proposed the concept of relative entropy of uncertain random variable. Shi et al. [25] presented the sine entropy of uncertain random variable. Liang et al. [11] introduced the entropy with two parameters. Tan and Yu [27] proposed the arc entropy. Ahmadzade et al. [1] presented a partial triangular entropy of uncertain random variable and employed it to mean-variance selection in the financial market. Chen et al. [5] presented an elliptic entropy via elliptic function and established a mean-entropy model. Tan and Yu [28] investigated the hyperbolic entropy. As a flexible devise to measures indeterminacy, the partial tsallis entropy was introduced by He et al. [7] and was invoked to optimize portfolio selection problem in finance. Up to now, the entropy theory of uncertain random variable has made great achievements in real applications. It is well known that uncertainty and randomness coexist in the rare book market as well as the financial market. Therefore, it is very necessary to study the entropy theory of uncertain random variables. However, the existing logarithmic entropy proposed for handling uncertain random variables fails to measure the degrees of uncertainty with respect to some uncertain variable, which is a special kind of uncertain random variables. As an effective supplement for the entropy theory of uncertain random variables, the arc entropy of uncertain random variables will be studied and three mathematical models of arc entropy to portfolio selection of the rare book market will be also introduced in this paper.

This paper is divided into the following five major parts. Section 2 introduces the arc entropy of uncertain random variable and Section 3 studies the mean-entropy model with its application to the rare book portfolio selection. After that, two types of mean-variance-entropy model are investigated in Section 4. Finally, a concise conclusion is given in Section 5.

Arc entropy

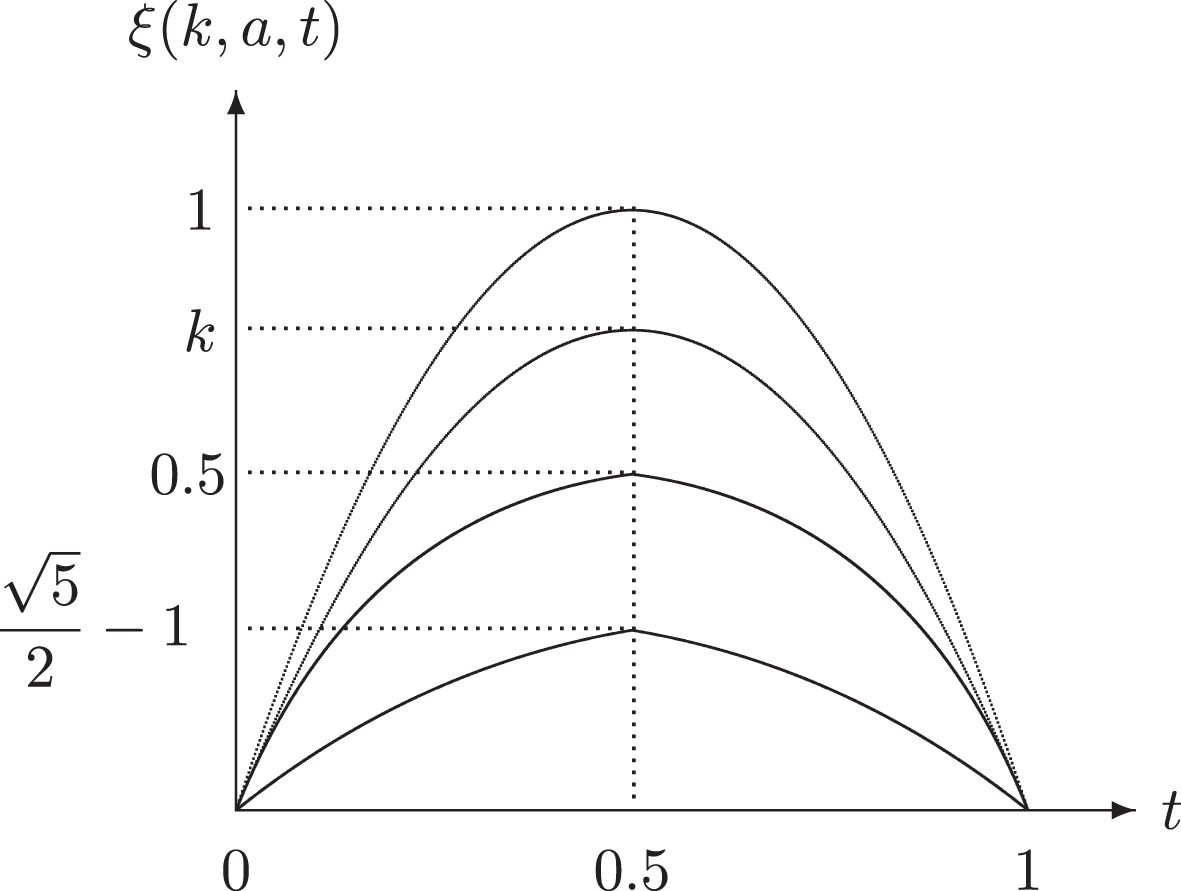

For the sake of charactering the degree of difficulty in the realization of prediction of uncertain random variable, we will introduce the concept of arc entropy in this section, and then we will investigate some properties of the arc entropy. Besides, the arc entropy of the function of uncertain random variables will be studied, and some examples of arc entropy will be also presented.

Arc entropy of uncertain random variable

In fact, the function

Next we will discuss two types of generalized arc entropy.

Note that

In order to discuss the arc entropy in more general cases, this subsection will derive the arc entropy of the function of uncertain random variables.

This section will apply arc entropy to the rare book trading problem in the rare book market. In the complex and collectible rare book market, old rare books and new rare books always coexist. For ancient rare books, we treat historical data as random variables, and then probability theory can be used to estimate the return on investment of a rare book trade. The lack of historical price data for new rare books requires uncertainty theory to deal with financial returns. In order to maximize financial returns and avoid risks in the rare book market, it is necessary to establish a mean entropy model for the rare book market, where the financial return is the expected value and the risk is the entropy.

In order to use this optimized mathematical model to describe the portfolio selection problem in the rare book market, we first introduce some basic symbols as shown in Table ly1.

Suppose there are n kinds of rare book to choose for investors in the rare book market. In order to solve the maximizing financial return of investment with the minimizing risk, the mean-entropy model via arc entropy to solve uncertain random portfolio selection of rare books is proposed as

Some basic symbols of mean-entropy model

Some basic symbols of mean-entropy model

Uncertainty distributions of 6 rare books

Next, the investor chooses 6 rare books for investment portfolio. Since the distribution of random returns is normal, while the distribution of uncertain returns is linear, the optimal combination of rare books can be further simplified to the following form,

Proportion of portfolio on rare books

It can be seen from the Table 3 that when the maximum entropy reaches 0.18, all rare books are selected. It is clear that the optimal choice for rare book 4 increases as the risk level λ increases. When the risk level reaches 0.4, rare book 4 can obtain a higher optimal return.

Uncertainty distributions of 5 rare books

Proportion of portfolio on rare books

Then the mean entropy model can be expressed as

By solving the above optimization problem, we obtain the solutions as showed in Table 5.

Table 5 shows that all rare books are selected when risk level achieves λ = 0.5. As risk level goes up and the financial returns are rising, investments will be concentrated in rare book 5. It is clear that the maximum optimal revenue is 7 with risk level λ = 1.3. To further discuss the application of arc entropy, uncertain returns can also be expressed as various uncertainty distributions such as linear, zigzag, normal and so on.

Uncertainty random distributions of 4 rare books

The investment proportion of 5 rare books

According to Table 6, the optimal solutions can be obtained as showed in Table 7. When the risk level λ = 0.3, all rare books should be invested with different proportions of portfolio selection. However, bookss 1, 3, and 4 account for a very small proportion. It is clear that the proportion of book 3 has increased faster, while the proportion of other books has decreased faster. As the risk level λ increases, the investment will focus on rare book 3. Meanwhile, the expected value is 26.0000.

This section will introduce two types of mean-variance-entropy model via arc entropy for the rare book market to solve the optimization selection problem with returns of rare books, which was proposed by Ahmadzade et al. [2] in 2020. In this section, two mean-variance-entropy models for the rare book market will be proposed to solve the problem of maximizing investment return and diversification of books with control risk.

The mean variance entropy model for programming problem

The expected return of rare book selection of uncertain random variables is

Uncertainty distributions of 3 rare books

Uncertainty distributions of 3 rare books

Obviously, uncertain variables τ

i

, i = 1, 2, 3 and random variable η

i

, i = 1, 2, 3 are independent. Based on Table 61, we can transform the rare book selection into objective programming as follows,

Proportion of portfolio on rare books

According to Table 9, we can easily see that the target value increases with the increase of γ and the increase of λ respectively, which means that the return on investment increases with the increase of control risk and fixed multiplicity increases. Likewise, investment returns also increase with increased diversification and fixed control risk, respectively. This means that a diversified portfolio in the rare book market is necessary. Without loss of generality, in order to maximize investment returns, investors are more willing to hold a diversified portfolio of assets while minimizing investment risks to reflect the attitude of investors.

Portfolio proportion and multi-objective in model

In this section, we will present the following mean-variance-entropy model via arc entropy to solve the multi-objective problem of the rare book portfolio selection.

By solving the optimization selection problem with Table 61, we obtain the optimal proportions of 3 rare books as shown in Table 10.

According to Table 10, it is clear that the expected value is increasing with the variance value decreasing and arc entropy value increasing. Meanwhile, the portfolio proportion of rare book 1 is decreasing with portfolio proportion of rare book 2 decreasing and book 3 increasing, which is showed in Fig. 2.

Convergence curve.

A key argument of this paper is that uncertainty and randomness coexist in the rare book market. In order to model such a rare book market, this paper introduced the numerical properties and principles of arc entropy, and introduced three mathematical models of arc entropy into portfolio selection in the rare book market. First, this paper proposed the concept of arc entropy through the uncertainty distribution, and studied two types of arc entropy as important complements to entropy. Then some mathematical properties of arc entropy were introduced, and the calculation formula of arc entropy was also deduced. Secondly, the mean entropy portfolio selection model was established to solve the rare book selection problem. Third, two mean-variance-entropy models were also introduced, and portfolio optimization with uncertain random returns was proposed to the rare book market. The results of the study showed that the three-arc entropy mathematical model is very effective for investors. Furthermore, the application in future research had broad potential. Finally, the future research can combine real data to analyze the proposed method.

Appendix A Preliminaries

In this section, we will review some basic definitions and theorems in uncertainty theory and chance theory.

Uncertainty theory

Axiom 1: (Normality Axiom) M {Γ} =1.

Axiom 2: (Duality Axiom) M {Λ} + M {Λ

c

} =1,

Axiom 3: (Subadditivity Axiom) For any countable sequence {Λ

i

}, we always have

Chance theory

Chance theory was proposed by Liu [20] as a mathematical tool for modeling complex systems.

Then the expected value of ξ was defined by Liu [21] as